taylor woodrow blue/slate/media/regions... · 5 while improving value for shareholders % return on...

TRANSCRIPT

Taylor Woodrow International Operations

9 November 2005

Delivering shareholder value

Los Arqueros, Marbella, Spain

2

Agenda

• Introduction Iain Napier

• European Operations Ed Hinchliffe

• Tour of Los Arqueros Javier Ballester

• North American Operations John Peshkin

• Wrap up Iain Napier

3

Successfully completed the transition to a focused homebuilder

0

100

200

300

400

500Group Operating Profit

Housing

Other

2000 2004

UK

North America

Other Housing

£m

We have retained the skills in property and construction necessary for success in today’s homebuilding market

4

A period of tremendous change

• Three acquisitions• Bryant (2001), Journey (2002), Wilson Connolly (2003)

• Restructured and refocused the North America business• Single management team

• Increase in homebuilding

• Profit growth driven by market selection, capital investment andfocus on ROCE

• Built UK housing to a scale operation• 3 restructurings in 3 years

• 3 head offices and 17 regional offices closed

• Significantly rationalised the product range

• Reduced headcount by 550

5

While improving value for shareholders

Return on Equity *%

0

50

100

150

200

250

300

350

2000 2004

Equity shareholders’ funds per share

pence

0

5

10

15

20

25

30

2000 2004

* Pre goodwill and exceptionals, but after tax

6

Strategy to grow Shareholder Value

• Grow profits through the cycle

• Presence in different markets gives us alternative growth channels

• Invest where we see the best opportunities

• Cost management initiatives

• Maintain a balanced business portfolio

• Geography, product type, price point

• Improve capital management

• Disposal of non-core assets

• Improving capital turns through geographical diversity and efficiency

7

Group HousingBalanced Business Portfolio

3 year average ROACE Portfolio Strategy

2005 H1 % Capital

EmployedInvestment

trend

UK 22% Grow through improved operational performance, capital efficiency and targeted investment

76%

22%

2%

North America

29% Grow through investment in selected markets

Spain 54% Grow through investment in selected markets

Community Developments

The Green Building, Manchester

Stamford Brook, AltrinchamSandringham Gardens, Stockport

The Paddocks, Widnes Kentmere Place, Altrincham

Community Developments

Cypress at Pacific Ridge, Newport Coast

Carmela in La Quinta, La Quinta

Cliffhaven, Corona Carrigan Lane at the Colonies, Upland

Ventana at Dos Lagos (Corona)

10

Group Housing Making good progress on strategy

Grown profit from operations and margins*

• Profit from operations up 0.6% to £195.4 million

• Operating Margin up 0.8 ppts to 16.8%

Provided a base for future profit growth

• Invested £358 million in the land bank

• Landbank up 17% to 74,567 plots

• Order book up 9% at £1.59 billlion

* Pre-exceptional items and before joint ventures’ interest and tax

Taylor Woodrow European Operations

9 November 2005

Delivering shareholder value

12

Agenda

• History of Taylor Woodrow in Europe

• Spanish market

• Strategy in Spain

• Regional overview• Strategy

• Land position

• Current and future developments

• Summary and Questions

13

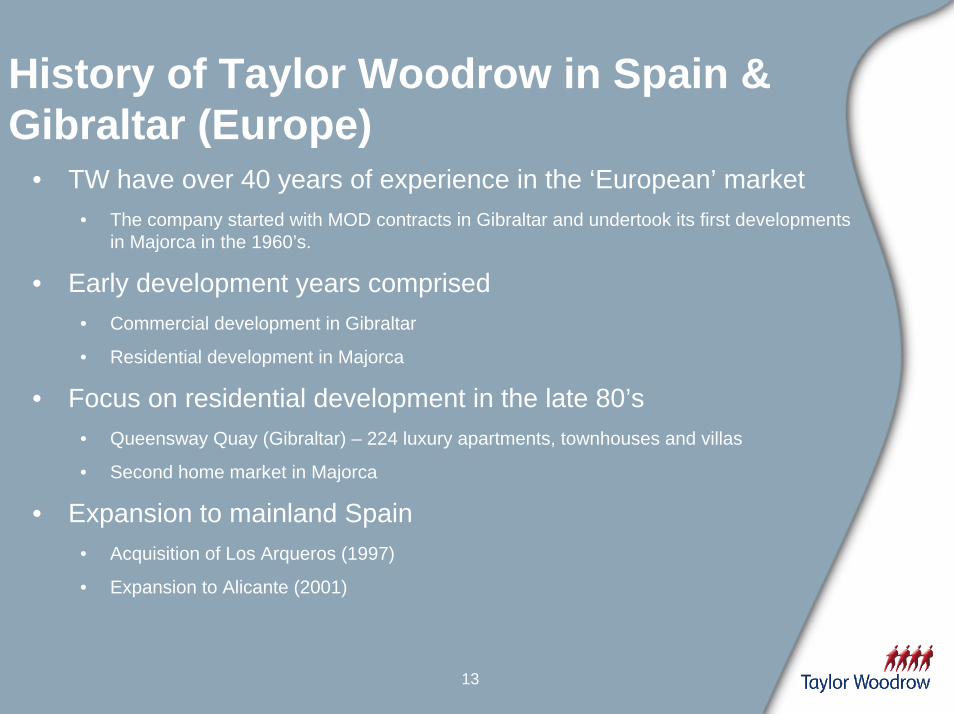

History of Taylor Woodrow in Spain & Gibraltar (Europe)

• TW have over 40 years of experience in the ‘European’ market• The company started with MOD contracts in Gibraltar and undertook its first developments

in Majorca in the 1960’s.

• Early development years comprised• Commercial development in Gibraltar

• Residential development in Majorca

• Focus on residential development in the late 80’s• Queensway Quay (Gibraltar) – 224 luxury apartments, townhouses and villas

• Second home market in Majorca

• Expansion to mainland Spain• Acquisition of Los Arqueros (1997)

• Expansion to Alicante (2001)

14

Where we operate today

Alicante

Malaga

Baleares

Gibraltar

10 active sites

4 active sites

4 active sites

4 active sites

15

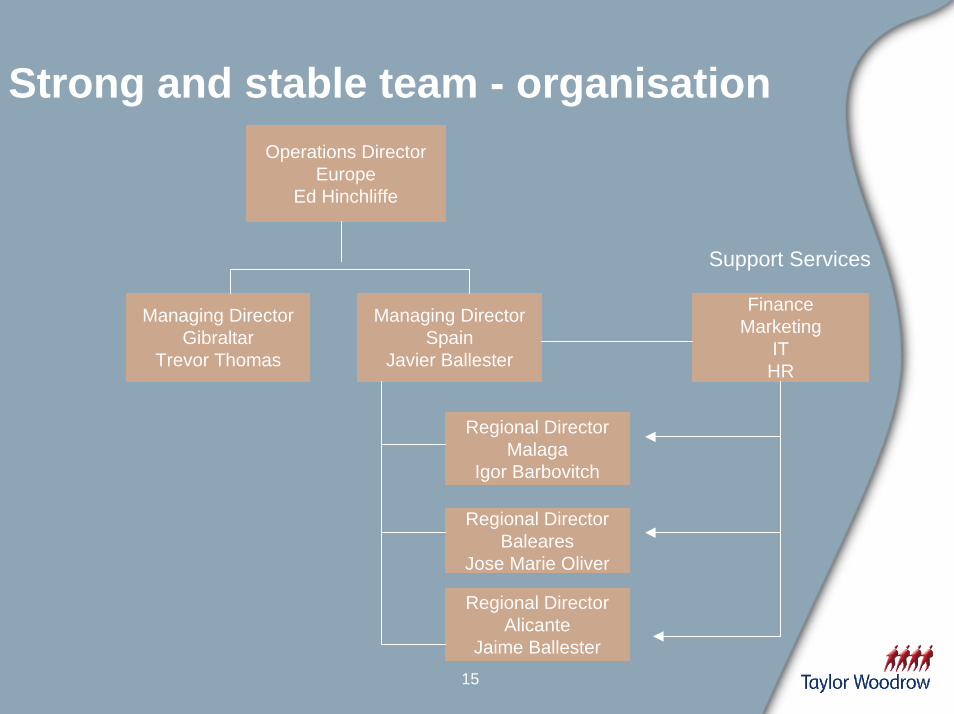

Strong and stable team - organisationOperations Director

EuropeEd Hinchliffe

Support Services

Managing DirectorGibraltar

Trevor Thomas

Managing DirectorSpain

Javier Ballester

FinanceMarketing

ITHR

Regional DirectorAlicante

Jaime Ballester

Regional DirectorBaleares

Jose Marie Oliver

Regional DirectorMalaga

Igor Barbovitch

16

We have three major categories of customer

• Second home buyers• Mainly British, focused on ‘traditional’ holiday locations

• Seeking a ‘Mediterranean’ lifestyle, preferably with investment capital uplift

• Low cost airlines ease accessibility and determine location

• First home buyers• Mainly Spanish

• Limited to urban developments in Majorca (Manacor, Palma) and Malaga

• Investors• High net worth individuals (tax exiles in Gibraltar)

• Buy to let investors

17

A record of success

£m 2000 01 02 03 04 CAGR%

ASP (£’000s) 109 127 154 186 178 13.0

Completions 253 326 306 345 415 13.2

76.5

20.1

26.3

43.1

52.1

28.7

34.7

4.7

18.6

12.4

Turnover 27.9 42.0 48.3 65.9

Operating Profit 6.1 8.7 11.6 20.3

Operating Margin (%) 21.9 20.7 24.0 30.8

Capital Employed 21.8 25.5 27.7 34.0

ROACE (%) 32.7 36.8 43.6 65.7

Spain

Javier Ballester

19

Spanish Market

• 740,000 new units in Spain in 2004

• 330,000 Mediterranean coastline units in 2004

• Inventory of 2nd home market units estimated at 3.5 m

• 40% owned by foreigners

Source: Richard Ellis CB

20

Spanish second home market is forecast to grow steadily

Source – Grupo i 2005

0

20

40

60

80

100

120

140

160

2005 2006 2007 2008 2009 2010

ForeignNational

‘000annual completions

• Foreign investment in Spanish homes has grown to >€6bn per year

21

British buyers have been fuelling demand

Source: AFI

UK36%

Germany23%

France6%

Holland3%

Italy2%

Other30%

Market for second homes owned by foreigners in 2003

22

Spain and Gibraltar – preferred areas for second homes

Balearics

Foreign/Spanish

Costa del Sol (1/1)*Costa Blanca (2/2)Costa Calida (3/3)Balearics (4/8)Costa Azahar (5/4)Costa Luz (6/5)Canaries (7/10)Costa Dorada (8/7)Costa Brava (9/6)Costa Verde (10/9)

* Figures in brackets indicate preference for foreign buyers/Spanish buyers

Airports served by low cost airlines

Del Sol

Calida

Blanca

Aza

har

Dorada

Brava

Verde

De la Luz

23

Competition

• Competitors• Very fragmented in mainland Spain

• Companies are becoming more professional

• Joint ventures with financial institutions

• Poor marketing, high dependence on estate agencies

• TWE competitive position• Sole British plc developer in Spain

• TW brand very strong in Majorca

• Strong British market

• UK sales operation

24

Taylor Woodrow Espana selling structure

Potential market

Brand awareness

Enquire info

Sending info

Reserve

Site visit

British citizens looking for a house in Spain.

Advertising in UK media.

UK marketing operations

UK marketing operations.

Sponsored inspection visits.

14 developments on Spanish coast .

25

Build on successful UK marketing operations • Develop a new more attractive and efficient TW Espana web site

• Focus media investment on proven success

• Create estate agent selling network incorporating two new sales people to manage two key UK regions

• Establish relationship with non real estate partners to improve prospect strike rate

• Working with two third parties on a trial basis

• UK Telesales team focus on increasing inspection visits

26

TWE strategy summary

• Focus on British second home market in three core regions: Baleares, Malaga and Alicante

• Grow organically in areas of strength

• Concentrate on acquiring new sites below 200 units utilising deferred payment terms.

• Average selling prices about €300,000.

• Product mix of apartments and townhouses.

• Build on the success of UK marketing operations• Manage risk by:

• Geographic diversity• Developing sales and marketing to Spanish second home purchasers• Spanish first home developments where land opportunities present themselves• Examine opportunities in the new growth areas

27

Balearics

Alicante

Malaga

Palma

Ibiza

Mahon (Minorca)

Gibraltar

Tarragona

28

Balearics

• 2004 unit completion was 125 from 10 sites (61.6% of FC’s were second homes)

• Reinforce leadership in the second home market by growing the business in Majorca

• Continue with local market (2-3 sites at any one time) in Palma

• Expand to Tarragona (Montbrio site) in mainland Spain

• Explore land opportunities on Menorca and Ibiza

29

Balearics

Las Brisas phase I

• 44 terraced villas

• Priced from €290,000 to €380,000.

30

Balearics

Cala Llonga

• 58 apartments

• Priced from €235,000 to €315,000

31

Alicante

Alicante

Murcia

Malaga

Palma

Gibraltar

Castellon

Almeria

32

Alicante

• 2004 unit completions was 44 from 1 site (100% of FC’s were second homes)

• Concentrate operations in Alicante and Murcia in the first instance

• Consider expansion to Almería and Castellon

• Explore limited opportunity in the first home market in Alicantewhere land opportunities arise

33

Alicante

Lagos Alenda

• Golf course

• 152 apartments

• Priced from €152,500

34

Malaga

Alicante

Malaga

Palma

GibraltarCadiz

Huelva

35

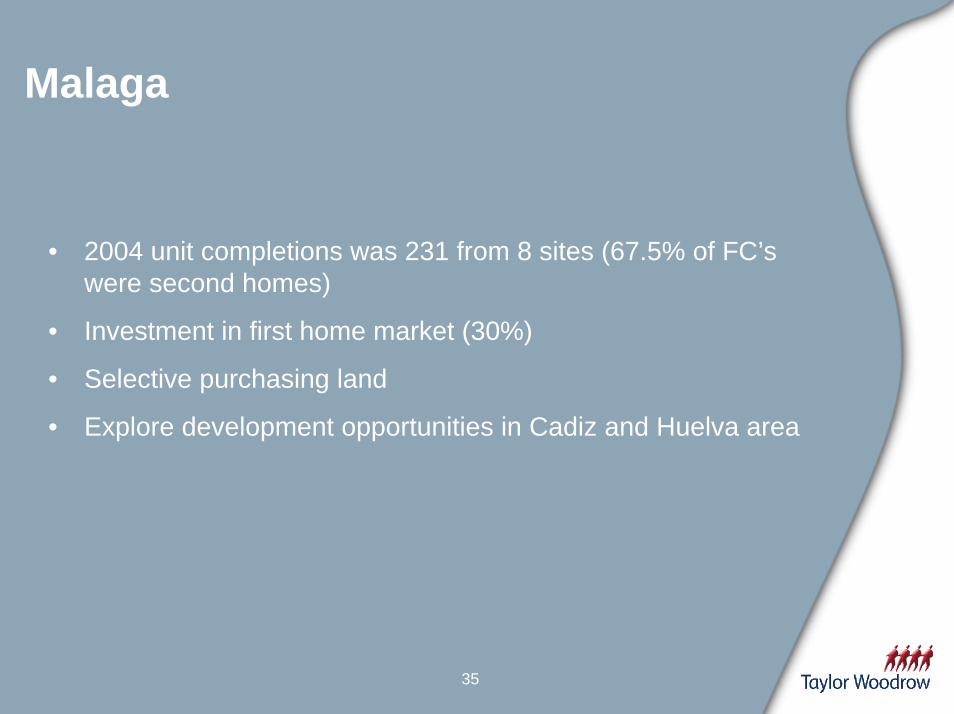

Malaga

• 2004 unit completions was 231 from 8 sites (67.5% of FC’s were second homes)

• Investment in first home market (30%)

• Selective purchasing land

• Explore development opportunities in Cadiz and Huelva area

36

Malaga

Los Eucaliptos

• 90 apartments

• Priced from €230,000 to €410,000

37

Malaga

Almendros II

• 20 townhouses

• Priced from €460,000

Gibraltar

Ed Hinchliffe

39

Gibraltar

• The Gibraltar market

• Premium/foreign

• Local X

• The premium market is very buoyant• High net worth investors

• Finance and betting industry

• Young local aspirational professionals

• Future traders

• Investors

40

Why are they buying?

• Attractive tax residency scheme for qualifying individuals

• No capital gains tax/no inheritance tax

• Lower buy-in cost than other low tax jurisdictions

• Sterling currency

• UK law and administration

• Excellent long term rental investment

• Mediterranean climate

• Land linked to Spain

41

Gibraltar

• Focus on premium end of the market

• Limit exposure to one or two major projects at any time

• Exploit our reputation as the leading premium developer on the Rock with local land owners and government

• Sell off-plan well in advance of build start• 25% non-refundable deposits

42

Gibraltar

• 25 apartments& penthouses

• priced from£345k to £865k

43

Gibraltar

• 81 apartments andpenthouses

• Priced from £305k to£1.5m

Summary & Questions

45

Summary

• Markets remain strong

• Experienced and capable team of managers with a track record of delivery

• We know and understand our core markets and will continue to focus on the second home opportunity for UK customers

• Robust plans in place to grow our business

Taylor Woodrow North American Operations

9 November 2005

Delivering shareholder value

47

Agenda

• Introduction John Peshkin

• California / Arizona Mike Forsum

• Florida Doug Schwartz

• Texas John Peshkin

• Ontario Brian Johnston

• Outlook & Questions

48

History of Taylor Woodrow in North America

• Long homebuilding history• Canada since 1953

• Florida since 1973

• Texas since 1978

• California since 1978

• Acquired Phoenix operations (Journey Homes) in 2002

49

Active in some of the strongestNorth American markets

Land bank 4,117

Land bank 9,316

Land bank 10,444

Land bank 10,565

Land bank 3,631

Data as at 30 June 2005 (owned and controlled lots)

50

Strong and stable team

John PeshkinNA CEO

Mike ForsumCalifornia / Arizona

Doug SchwartzFlorida

Brian JohnstonCanada

Tim TowellTexas

Support Services• Finance• IT• HR• Commercial

51

Strategy and objectives

• Manage a balanced portfolio through the business cycle• Products• Price points • Geographies

• Operate efficiently, at scale, in markets with strong sustainable growth prospects

• Job growth• Favourable demographics

• Expand in existing markets first; opportunistically evaluate other markets

• Maintain top quartile returns on capital and profit growth

52

Regional Operations

• Arizona • Develop premiere master-planned communities for homebuilding

• Mitigate risks by pre-selling parcels to other builders

• California • Continue to capitalise on prestigious brand and associated premium whilst

maintaining middle-market position

• Canada• Maximise value associated with Monarch respected brand through blend of land

development and high-rise to complement centralised Toronto homebuilding core business

• Florida/Texas• Continue successful land development projects while increasing scale

homebuilding operations in core markets

53

US Housing starts expected to moderate to sustainable levels

Thousands of annual starts

0

200

400

600

800

1000

1200

1400

1600

1800

2000

19861987

19881989

19901991

19921993

19941995

19961997

19981999

20002001

20022003

2004

Total Multi-Family

Total Single-Family

Source: NAHB, U.S. Census Bureau

• Strong growth in starts 2002 through to 2005

• 2005 expected to be 2.0m starts

• NAHB forecasts 5% decrease in 2006 & 2007 (1.8m starts)

54

Long-term housing demand supports projected starts

Note: Historical supply figures represent completions, forecasts use starts.

Source: NAHB, U.S. Census Bureau, Manufactured Housing Institute, and Smith Barney

2004-2013

Low Mid High1,300 1,500 1,650400 400 400185 185 185

1,885 2,085 2,235Low Mid High

1,350 1,500 1,600335 360 400

1,685 1,860 2,000

In thousands

Total StartsMulti-FamilySingle-Family

Sources of Supply:= Net Annual Housing Demand

+ Change in Vacancies+ Demolitions

Ann. Chg. In HouseholdsAnnual Sources of Demand:

1,4781,4641,524285441507

1,1931,0231,017

1,7671,6951,799306275136235104290

1,2261,3161,373’94-’03’84-’93’74-’83

55

Monthly housing payments to remain affordable

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

11%

12%

1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Mortgage Rate

30 yr. Fixed rate

1 yr. ARM

Source: Various

• 30-year fixed rates currently around 6.2%; 1 year ARM around 5.4%

• NAHB forecast for 2006 increases 30-year to 6.5%; 1 year ARM to 5.7%

• 2005 House price growth ranged between 5% - 20% in TW markets

• NAHB forecasts 2006 national price growth of 3% -5%

• Expect TW marketsto trend to thislevel

56

Strategy to achieve objectives in a “normal” market

• Maximise forward sales • September 30th : Sold well into Q2 2006

• Aim to be 50% pre sold by end of year

• Position bulk of homes in middle-market

• Keep a disciplined portfolio approach

• Increase operational efficiencies

• Maintain a conservative approach to land acquisitions• Fewer larger long-term land acquisitions

• All land bought has planning in place

57

Balanced portfolio will deliver objectives

18%

31%

18%

29%

Texas, 4%

36%

14%

26%

20%

Texas, 4%

Revenue Splits H1 2005 Home completions H1 2005

58

Product mix will deliver objectives

0%

20%

40%

60%

80%

100%

Price Point Type of Business

70-75%

10-15%

10-15%

Low-rise

High-rise

Land development

Entry-level

Move-up

Luxury

40-50%

40-50%

10-15%

59

Achieving growth objectives

Growth

Increase capitalin strong markets

Exploit niches

Open satellitesAcquire into new markets

e.g. Beach-front condos

e.g. Journey e.g. San Diego Division,

Southern California

e.g. Florida, Arizona, California

60

2004 Performance

Average home selling price (US$k) 374 339 10.3

Home completions 3,635 2,786 30.5

Lot completions 2,323 2,940 (21.0)

Turnover (US$m) 1,581 1,108 39.4

Operating profit (US$m) * 233.5 146.4 54.9

Operating margin (%)* 14.8 13.3 11.3

ROACE (%) * 37.7 26.1 11.6

2004 2003 %

* Pre goodwill amortisation

61

Average home selling price (US$k) 399.2 357.6 11.6

Home completions 1,668 1,500 11.2

Lot completions 1,017 1,492 (31.8)

Turnover (US$m) 823.7 656.2 25.5

Operating profit (US$m) * 137.7 98.1 40.0

Operating margin (%)* 16.7 14.9 12.0

ROACE (%) * 36.7 30.0 22.3

H12005

2005 H1 Performance

H12004 %

* Pre goodwill amortisation

62

Consistent growth in Operating Profit

$77.6$100.7

$150.7

$233.5

$98.1

$137.7

$0

$40

$80

$120

$160

$200

$240

2001 2002 2003 2004 2004 H1 2005 H1

US$m

+30%

+50%

+55%

+40%

* Pre goodwill amortisation and exceptional items

63

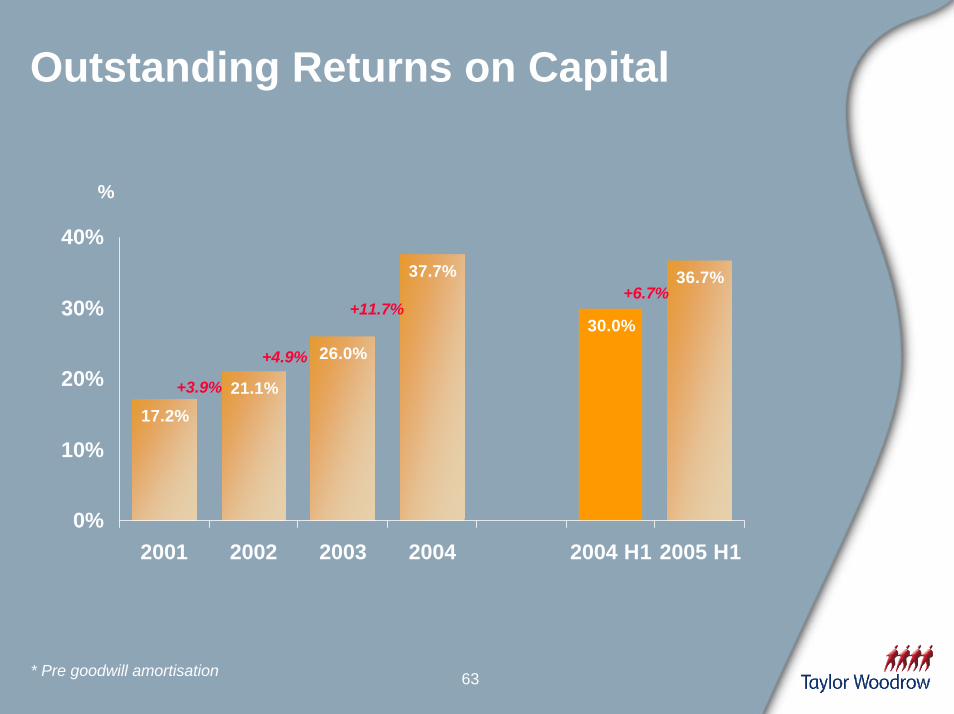

Outstanding Returns on Capital

17.2%21.1%

26.0%

37.7%

30.0%

36.7%

0%

10%

20%

30%

40%

2001 2002 2003 2004 2004 H1 2005 H1

%

+3.9%

+4.9%

+11.7%+6.7%

* Pre goodwill amortisation

California

Mike Forsum

65

Market and macro trends

Job GrowthAug 2005

vs Aug 2004

Pop’n Growth2000-2030

Housing Permits2004

House Price Inflation2004

California 1.5% 37% 207,000 20%+

• Californian housing market has been very strong in recent years

• Annual population growth of 250,000 households; continued undersupply of around 50,000 new homes per year

• Other US builders now commenting of softness at luxury price levels in South California but TW product continues to sell well

Source: Department of Labor, Census data, NAHB

66

California land bank and completions

706

2379 2450

4117

241

497

697

273307

0

500

1000

1500

2000

2500

3000

3500

4000

4500

2002 2003 2004 2005 H1

Land bank

0

100

200

300

400

500

600

700

Home Completions

Land bankFY home completionsHY home completions

As at H1 2005; a 3.5 year land bank based on last 12 months home and lot completions

67

California average selling prices

1064

786 776 797

0

200

400

600

800

1000

1200

2002 2003 2004 2005 H1

$k

68

Strategy

• Southern California• Maintain presence in luxury market

• Continue to capitalise in middle-market

• Expansion into Palm Springs

• Northern California• Concentration on San Jose infill market

• Building scale operations through 2005 onwards

69

Southern California

Cypress, Irvine

• From $2.5 million

• Luxury market

70

Northern California

Hawthorn Place, San Jose

• From $700,000

• Move-up

Arizona

Mike Forsum

72

Market and macro trends

Job GrowthAug 2005

vs Aug 2004

Pop’n Growth2000-2030

Housing Permits2004

House Price Inflation2004

Arizona 4.1% 109% 65,000 20%+

• Phoenix housing market has been running at record levels (volumeand price appreciation) in recent years

• Growth in permits in latter part of 2005 have slowed

• Price increases are starting to moderate

Source: Department of Labor, Census data, NAHB

73

Arizona land bank and completions

3649

5947

7119

9316

689

841

211

509

375

2000

4000

6000

8000

10000

2002 2003 2004 2005 H1

Land bank

100

200

300

400

500

600

700

800

900

Home Completions

Land bankFY home completionsHY home completions

As at H1 2005; a 6.6 year land bank based on last 12 months home and lot completions

74

Arizona average selling prices

120132

183

206

0

50

100

150

200

250

2002 2003 2004 2005 H1

$k

75

Strategy

• Active in entry and move-up markets

• Acquire master-planned communities• Complete planning whilst land under option

• Retain best lots for home building

• Sell remaining lots to other builders

76

Arizona

Thompson Ranch, Phoenix

• From $120,000

• Entry-level market

77

Arizona

Shamrock Estates, Phoenix

• From $300,000

• Move-up market

Florida

Doug Schwartz

79

Market and macro trends

Job GrowthAug 2005

vs Aug 2004

Pop’n Growth2000-2030

Housing Permits2004

House Price Inflation2004

Florida 3.4% 80% 256,000 20%+

• Low-rise market has continued in 2005 to be very strong underwrittenby strong demographics; high-rise beachfront condo market started to soften in second half of 2005

• Still a strong seasonal market (Jan-April main selling months)

• Strong deposit structure and good order book

Source: Department of Labor, Census data, NAHB

80

Florida land bank and completions

3405

5213

7632

10586

384

505

305297

202

0

2000

4000

6000

8000

10000

12000

2002 2003 2004 2005 H1

Land bank

0

100

200

300

400

500

600

Home Completions

Land bankFY home completionsHY home completions

As at H1 2005; a 12.1 year land bank based on last 12 months home and lot completions

81

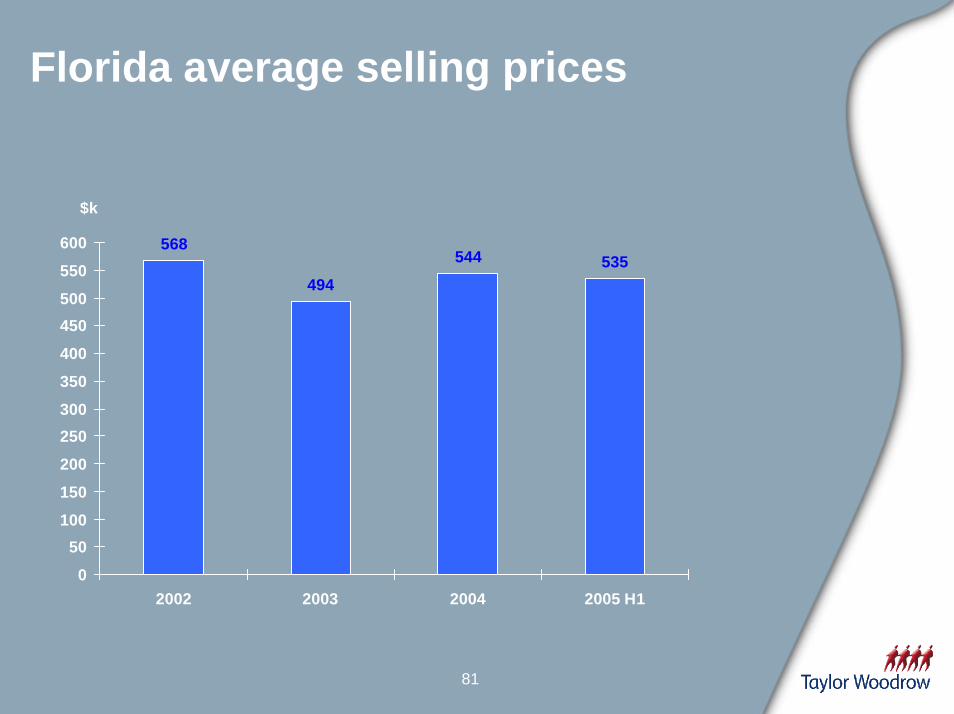

Florida average selling prices

568

494

544 535

0

50100

150

200

250300

350

400

450500

550

600

2002 2003 2004 2005 H1

$k

82

Strategy

• Continue to build scale in three local markets

• Keep bulk of product in affordable middle-market segment

• Balance between master-planned communities, lot positions and high-rise

• For high-rise, generally pre-sell buildings to around 50% before construction start, with material deposit levels

• Supplement core business by opportunistic land development projects outside homebuilding markets

83

Southwest Florida

Lucaya, Fort Myers

• From $260,000

• Second home, retirees

84

Southeast Florida

Mirasol, West Palm Beach

• From $650,000

• Luxury market

85

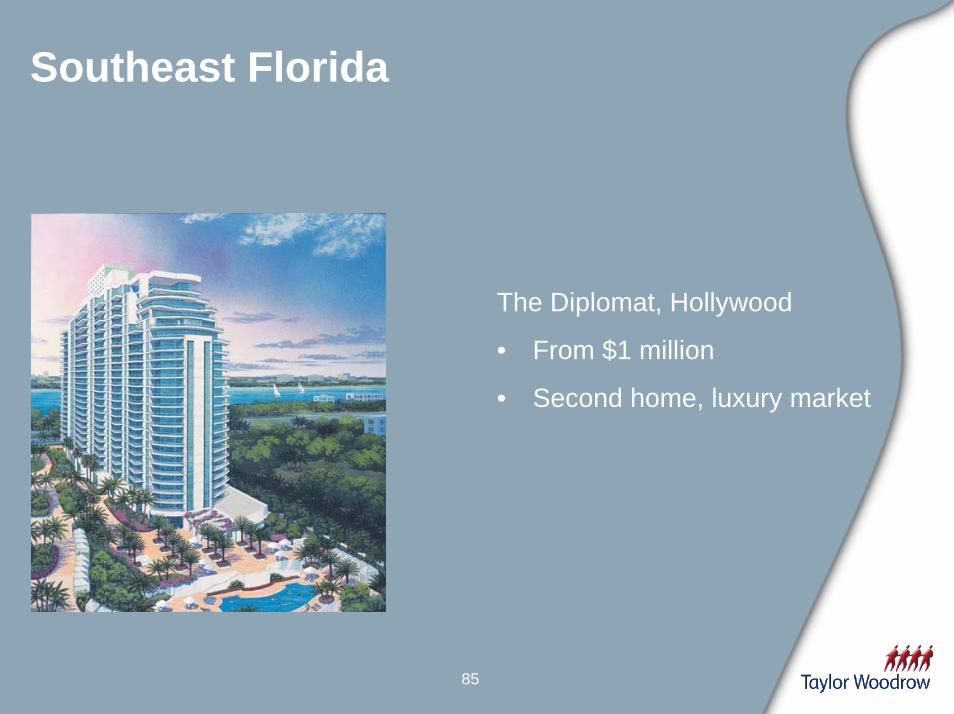

Southeast Florida

The Diplomat, Hollywood

• From $1 million

• Second home, luxury market

86

Central Florida

Waterchase, Tampa

• From $600,000

Texas

John Peshkin

88

Market and macro trends

Job GrowthAug 2005

vs Aug 2004

Pop’n Growth2000-2030

Housing Permits2004

House Price Inflation2004

Texas 1.3% 60% 188,000 3-5%

• Texas markets have not enjoyed the run up in prices as other markets have

• Remain well balanced markets in terms of supply and demand

• Recently experiencing improved demand

Source: Department of Labor, Census data, NAHB

89

Texas land bank and completions

24442329

37683631

94

5952 59

33

1500

2000

2500

3000

3500

4000

2002 2003 2004 2005 H1

Land bank

0

10

20

30

40

50

60

70

80

90

100

Home Completions

Land bankFY home completionsHY home completions

As at H1 2005; a 9.6 year land bank based on last 12 months home and lot completions

90

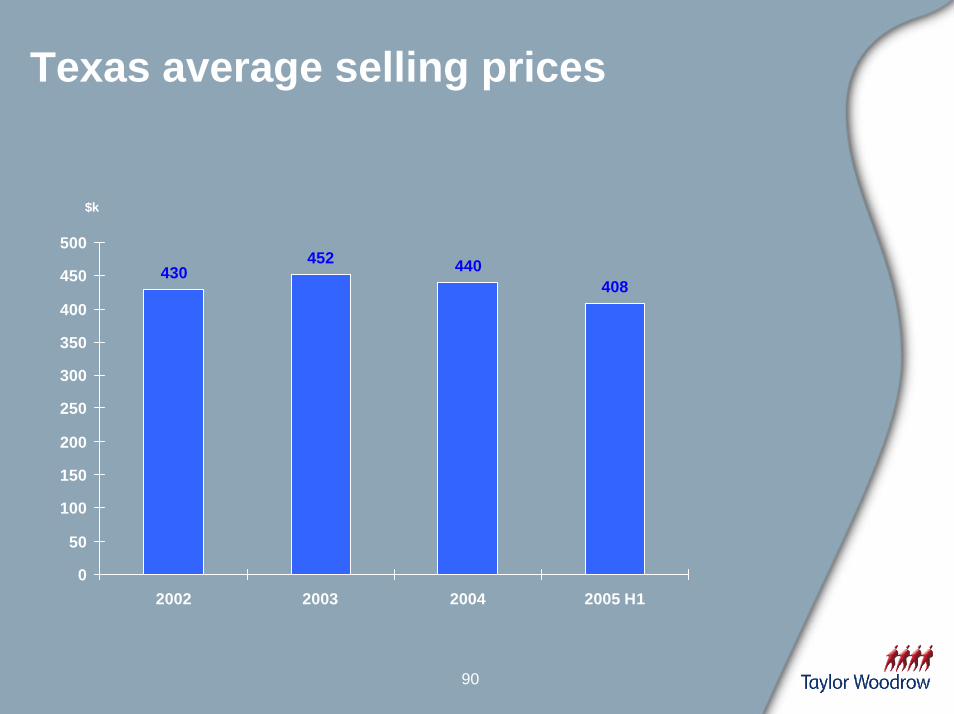

Texas average selling prices

430452 440

408

0

50

100

150

200

250

300

350

400

450

500

2002 2003 2004 2005 H1

$k

91

Strategy

• Leverage existing master-planned communities to build scale homebuilding operations in Austin and Houston

• Continue to migrate downward to middle-market homes

92

Austin

Steiner Ranch, Austin

• From $300,000

• Move-up market

93

Houston

Copper Lakes, Houston

• From $265,000

• Move-up market

Ontario

Brian Johnston

95

Market and macro trends

Job GrowthAug 2005

vs Aug 2004

Pop’n Growth2004-2031

Housing Permits2004

House Price Inflation2004

Ontario 1.4% 33% 85,000 5%

• Low-rise market holding up well in 2005

• Land supply in Greater Toronto tight

• High-rise market very active

Source: Department of Labor, Ontario Ministry of Finance

96

Ontario land bank and completions

5280

98909040

104441498

496

1030

1157

617

0

2000

4000

6000

8000

10000

12000

2002 2003 2004 2005 H1

Land bank

0

200

400

600

800

1000

1200

1400

1600

Home CompletionsLand bankFY home completionsHY home competions

As at H1 2005; a 5.8 year land bank based on last 12 months home and lot completions

97

Ontario average selling prices

168

215233

269

0

50

100

150

200

250

300

2002 2003 2004 2005 H1

$k

98

Strategy

• Low-rise• Centralised operations in Toronto and Ottawa

• Leverage advantages from financial strength

• High-rise• Affordable product in downtown Toronto

• Exploit existing relationships

• Lumpy completions profile

99

Ottawa

Stonebridge, Ottawa

• From $280,000

• Move-up market

100

Toronto

eq1 at Equinox, Toronto

• From $220,000

• Entry level, second home market

Summary & Questions

102

Summary

• Long established business, with experienced local management

• Successful track record

• On track to meet our expectations• Market remains strong

• Land bank well placed for 2006 & beyond• 38,073 units at HY 2005

• 100% of land in place for 2006

• 95% of land in place for 2007

• Strong order book for 2006• Sold well into Q2 2006

• Future growth driven by volume

• Actions in place to achieve top quartile returns and profit growth in a more normal market

Taylor Woodrow International Operations

9 November 2005

Delivering shareholder value

Los Arqueros, Marbella, Spain

104

Summary

• Long established international operations

• Strong, experienced local management

• Track record of delivering profit growth and high returns on capital

• Well positioned for continued success• Excellent land positions

• Proven strategy

105

Update on current trading

• Group trading in line with expectations• Prospects remain good and we continue to benefit from our portfolio strategy

• UK demand slightly stronger than last year• Market is competitive, margin pressures remain

• Overall net reservations up 15% from slightly fewer sites

• North America remains strong• Signs of moderation in certain hotspots

• Record order book gives us confidence for 2005 and 2006

• Hurricane Wilma has caused some interruption to build schedules, but do not at this stage anticipate any material profit impact

106

Questions and Answers