taxing cyberspace : economic application and cross-country policy analysis

TRANSCRIPT

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 1/84

TAXIN G CYBERSPACE : ECO N O M IC A PPLICATIO N AN D

CR O SS-CO U N TRY PO LICY AN ALYSIS

BY: FAR U Q SYED H ASA N

An Honours essay submitted to Carleton Universityin fulfillment of the requirements for the courseECON 4908 as credit to!ards the de"ree of #achelor

of Arts !ith Honours in Economics and $a!%

D epartm ent ! E"nm #"$Car%etn U n#&er$#t'

O tta( a) O ntar#

Apr#% *t+) ,.

- 1 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 2/84

TAB LE O F CO N TEN TSTAB LE O F CO N TEN TS////////////////////////////////////////,0 1 IN TRO D U CTIO N///////////////////////////////////////2

, - CO M M O D ITY TAX TH EO RY//////////////////////////////3

,/0 - H ( Ta4#n5 E! !e"t$ M ar6et$/////////////////////////3,/, 1 Pr#n"#p%e$ ! Ta4at#n/////////////////////////////3

,/,/0 E! !#"#en"'////////////////////////////////////////// 0 ,/,/, E78#t'////////////////////////////////////////////// 02 ,/,/2 S#m p%#"#t'////////////////////////////////////////// 09 ,/,/ N e8tra%#t'////////////////////////////////////////// 0;

//////////////////////////////03,/2 1 CO N SU M PTIO N TAXATIO N /////////////////////////////////////// 03,/2/0 1 Term #n%5'

//////,,/ 1 N ATIO N AL SALES TAX <S/ <ALU E AD D ED TAX =<AT> ////////////////////////////////////////////////,,//0 1 <AT ///////////////////////////,,//, 1 N ATIO N AL SA LES TAX =N ST>

////////////////////////////////////////,0,//2 1 N ST < S/ <AT 2 1 TAX AN D E-CO M M ERCE///////////////////////////////,2/0 1 E-"m m er"e <$/ Br#"6-An?-M rtar//////////////////,2/, 1 @ +at U n#78e Ta4at#n I$$8e$ A r#$e////////////////,;2/2 1 M a#% O r?er H #$tr'///////////////////////////////222/2/0 S#%a$ M a$n C/ &/ @ a$+#n5tn State Ta4 Cm m #$$#n/// 22 2/2/, N at#na% Be%%a$ H e$$) In"/ &$/ D epartm ent ! Re&en8eState D epartm ent ! I%%#n#$ ////////////////////////////// 2 2/2/2 Q 8#%% Crp/ &/ N rt+ D a6ta 033,////////////////// 29

2/ 1 Pr an? Ant#-E-"m m er"e Ta4 Ar58m ent$////////////2*

1 Attem pt$ at P%#"' ///////////////////////////////2/0 1 O ECD /////////////////////////////////////////////2/, 1 O t+er E! !rt$////////////////////////////////////;

. 1 Ca$e St8?#e$ //////////////////////////////////////*./0 1 EU ///////////////////////////////////////////////*./, 1 IN D IA////////////////////////////////////////////.2./2 1 Un#te? State$////////////////////////////////////.3./ 1 A8$tra%#a////////////////////////////////////////9;

9 1 Cn"%8$#n /////////////////////////////////////////;

; 1 B#%#5rap+' //////////////////////////////////////;2

* 1 APPEN D IX///////////////////////////////////////////;3

- 2 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 3/84

0 1 IN TRO D U CTIO N

&he internet connects 'eo'le from around the !orld !ithin

instances to one another diminishes borders and allo!s

for transfer of data at s'eeds that are "ettin" fasterevery year% (ue to its !ides'read reach ease of access

and universality of a''eal many firms have o'ted to )set

u' cam'* on the internet and sell "oods and services

online% &his ty'e of activity has been anointed the name E+

business and the value of these "oods and services is E+

commerce ,short for Electronic Commerce-.% /n this

valuation only 'riced items are included ,information

available for free is ecluded-%

Even thou"h E+commerce has eisted for over thirty years

it has maintained e'onential "ro!th over the last .0 years

alone and there are 'resently an estimated 190 million

'eo'le on the internet in 2004 !orld!ide as com'ared to 34

illion in the year .9952 ,6ee &able 2 in A''endi-%

E+commerce in the United 6tates currently re'resents about

3 'ercent of total retail sales !hich is e'ected to

increase to 8 'ercent by 2008% Of the 71%5 million U%6%

households online this year orrester re'orted that 5.

'ercent sho''ed online%3

E+commerce 'resently re'resents . to 2 of total retail

sales in the EU: total business+to+consumer E+commerce !as

e'ected to increase from ;.0 billion to ;10 billion in

1 esenbour" &homas $% <easurin" Electronic #usiness= >a"e 4% U%6#ureau of Census Au"ust 200. 2 Ca'tain >hili''e <?no!led"e ana"ement Overvie!= @HO November 200. 3 (ne!s%com E+commerce ta bill #efore house 6e'tember 2003 +htt'B!!!%nacsonline%comNAC6Dovernment@ashin"tone'ortArchivesnd0929032%htm

- 3 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 4/84

2003% An estimated 54 of Euro'ean /nternet users !ill sho'

online in 2007%4 esearch sho!s that .5 of the total

'o'ulations in the accession countries !ere usin" the

/nternet by the end of 2003%5

&he U%6% (e'artment of Commerce estimated an overall of

F.077 #illion value of e+business activity in the year

200. G6ee &able . in A''endi% rom the table !e can see

that overall #usiness to Consumer ,#2C- transactions are

lar"er than #usiness to #usiness ,#2#- transactions%

Ho!ever E+commerce #2C are less than .0 of E+commerce #2#

transactions and this sho!s the "reater reliance and

!illin"ness of business to embrace this technolo"y%

&here have been many re'orts that have "rossly over

estimated the losses of ta revenue due to the use of E+

commerce and this has led to much concern !orld!ide% &he

U%6% (e'artment of Commerce estimates re'orted totals of

#2# and #2C sales combined for the years 2000 and 200. as

F14%. #illion and F88%7 #illion res'ectively%7 &hat is a 20

increase in a one year s'an% uture estimates of the value

of E+commerce sales only hi"hli"ht further the im'ortance

of creatin" effective ta 'olicy% &his in 'art !ould be due

to the different accounts of !hat E+commerce com'rises and

also inflated 'roIections of e'ected E+commerce activity%

Althou"h the taation of ,inter-nationally traded "oods is

not somethin" ne! for le"islators the lacJ of definition

and "uidelines about taation has inhibited further

4 Euro'ean Commission 6tudy on (irective 2. November 20035 Aqute esearch ay 2003%

6 Kohnson >eter A% <A Current Calculation of Uncollected 6ales &aesisin" from /nternet Dro!th= >a"e 5 (irect arJetin" Association arch 2003

- 4 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 5/84

le"islation% /t can be ar"ued that the issue of E+commerce

taation requires a miture of 'olitical and economic

rationales for le"islation the effects of !hich may decide

for today and tomorro! ho! E+commerce is conducted

!orld!ide%

&able . GA''endi sho!s the 'ercenta"es of the 'o'ulation

in the res'ective countries that are usin" the internet

and the 'ercenta"e of the 'o'ulation that is actually

maJin" online 'urchases as !ell% @ith ece'tion of /taly

and rance most Euro'ean countries in the database ,such

as the Netherlands (enmarJ and inland- all have very

hi"h internet usa"e rates% A''roimately 20 of the

'o'ulation in each of those countries carries out 'urchases

online% Also note that even thou"h Canada*s 'ercenta"e of

internet users is hi"her than that of the United 6tates

the 'ercenta"e of online consumers in the U%6% is about 1

hi"her than that in Canada% &his could be in 'art because

Canadians have the re'utation to be more risJ averse

o''osed to Americans1 or that there are not enou"h dot-

com ’s tar"etin" the Canadian marJet% Another reason could

'ossibly be the differences in the avera"e a"e of internet

users in the res'ective countries: children may constitute

a lar"er 'ercenta"e of the users in Canada as o''osed to

the U%6% #ear in mind that these statistics are

re'resentative of a 'ercenta"e only and not re'resentative

of the volume of e'enditure ,consum'tion-%8

7 orin %A% and 6uareL % MisJ Aversion evisitedM Kournal ofinance6e'tember .20.+.2.7 .9838 &he 'o'ulation of 6!eden is estimated at 9 million ,2004- ,C/A @orldact#ooJ @ebsite- Canada 32%5 illion (enmarJ and inland 5%4illion each U6A 293 illion U? 70 illion Australia .9 illion/taly 58 illion rance 70 illion and eico at .04%5 illion% 6o

- 5 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 6/84

E+commerce also includes the sale and 'urchase of di"itiLed

"oods ,such as e+booJs e+re'orts- and for services to be

'rovided online% @e shall not be looJin" at either of these

issues% /n this 'a'er / !ill s'ecifically focus on taation

'olicies ado'ted by different countries to!ards the sale of

physical"oods 'urchased over the internet the relevant

economic 'rinci'les that a''ly to this situation and some

of the issues and conflicts of o'inion that surround

internet ta 'olicy%

(ue to the softnature of electronic commerce some uniqueissues arise in formin" ta 'olicy for it that do not eist

in traditional commerce% A select fe! of these issues

include findin" !here Iurisdiction lies in a cross+border

transaction !here Iurisdiction lies !hen there may be

multi'le servers9 involved in 'rocessin" a sin"le

transaction !hen the actual transaction is concluded G!hen

the user clicJs or !hen the "ood is delivered% &here is

also the issue of use taes to be discussed further later

on%

/n order for a firm to be liable for income ta it has to

be 'roven that it has a >ermanent Establishment or >E in

that Iurisdiction% One of the more central questions in E+

commerce !ould be !hether a server can constitute as a >E

or not% /n order for a firm to be liable to remit sales

taes the same 'roof of >E has to be 'rovided% &his

'ermanent establishment is "iven the technical name Nexus%

althou"h there is dee' s'read in the 'o'ulations this is notre'resentative of 'urchasin" activity volume%9 6ervers refers to online com'uters that host an a''lication or !ebsite%

- 6 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 7/84

Kohnson ,2003- ar"ues that an earlier study conducted at

the University of &ennessee "rossly over estimates the

losses in collectable taes% He ar"ues that because of a

faulty understandin" of the dynamics of E+commerce the

!idely held notion that these losses are lar"e and "ro!in"

is incorrect% He further ar"ues that since the maIority of

E+commerce activity is re'resented by #2# transactions and

states currently hold the authority to request an audit of

a firm that is believed to be evadin" taes the 'ro'osed

notion that a detailed definition of neus is not enou"h to

remedy the ta losses% /n other !ords he ar"ues that even

if a detailed definition of neus !as established and

follo!ed by all the nations in the !orld the 'roblem is

much bi""er than Iust the notion of neus% &he need for a

consistent frame!orJ is 'aramount because states have the

choice to formulate ta 'olicy as they see fittin" their

o!n needs% &his may ultimately lead to too many differin"

re"ulations that merchants !ould have to constantly be made

a!are of%

&he 'ur'ose of this study is to find reasons for the

discre'ancies bet!een !hat is considered the o'timal 'olicy

solution in economic theory and the actual 'olicies

im'lemented% After a thorou"h eamination of the

information "athered it !as found that des'ite maIor

attem'ts at international solidarity fe! nations have

succeeded in creatin" collaborative efforts% ost have

decided to maJe decisions in their best interest or

im'lement 'olicy that is in line !ith their already

eistin" 'olicy% /n reality there still remains much !orJ

to be done !ith re"ard to the 'rinci'les that "overn

internet taation and in the harmoniLation of ta 'olicy%

- 7 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 8/84

&raditional retailers that have the resources to do so are

movin" from )bricJ+and+mortar* com'anies and transformin"

into )bricJ+and+clicJ* enter'rises%.0 6o it !ould a''ear

that the internet is here to stay% /n any case the subIect

is !orthy of study% @e can not avoid these issues%

6ection 2 of this 'a'er outlines commodity ta theory and

the 'rinci'les of commodity taation% 6ection 3 eamines

the differences bet!een E+commerce and traditional trade

the unique taation issues that arise in the case of E+

commerce and !hether E+commerce should be taed or not%

6ection 4 looJs at some of the attem'ts at creatin" sound

'olicy by "rou's such as the OEC(% /n 6ection 5 the 'a'er

outlines the s'ecific 'olicies set forth by the Euro'ean

Union /ndia United 6tates and Australia% /t is the

'ur'ose of this section to sho! ho! 'olicies have evolved

and ho! they !ere formulated% $astly 6ection 7 !ill

include my concludin" remarJs follo!ed by an a''endi and

biblio"ra'hy%

10 C6C and 6UN /CO66&E6 <NE& #U6/NE66 6O$U&/ON #/ND6 &HE O&UNE

.500 /N&O &HE NE& ECONO= 200.

- 8 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 9/84

, 1 CO M M O D ITY TAX TH EO RY

,/0 H ( Ta4#n5 E! !e"t$ M ar6et$

&aes are Jno!n to distort economic activity% &aes are

also used to correct distortions in the marJet'lace as

!ell% /n either case the end result is different from

economic activity !ithout restrictions%

Commodity taation has three roles B i- revenue collection

ii- inter'ersonal distribution iii- resource allocation..%

&he loss in the value of economic activity caused by taes

is Jno!n as deadw eight loss% /n the case s'ecific to

consumers it is referred to as excess burden or the added

cost to ta'ayers and society of raisin" revenue throu"h

taes%.2 &he four most !idely acce'ted 'rinci'les of "oods

taation areB efficiency equity sim'licity and

neutrality% &hou"h each of these 'rinci'les is correct

!ithin its o!n realm they often conflict !ith one another

and non+economic obIectives may also alter the course of

ta 'olicy%

,/, Pr#n"#p%e$ ! Ta4at#n

&he four 'rinci'les listed are !idely Jno!n as Adam 6mith*s

<our canons of &aation=.3%

.. Coady (avid and (reLe Kean <Commodity &aation and 6ocial @elfare

B &he Deneralised amsey ule= /nternational &a and >ublic inanceol 9 /ssue 3 ay 2002.2 AuerbachAlan K% M&aation and Economic EfficiencyM University of

California #erJeley 200. >a"e 4.3 6mith Adam <An /nquiry into the Nature and Causes of the @ealth of

Nations /ndiana'olisB $iberty Classics= olume // .98. ''% 825 +828%

- 9 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 10/84

,/,/0 E! !#"#en"'

Efficiency refers to minimiLin" the overall ne"ative

effects of taation s'ecifically the dead!ei"ht losses of

taation% Accordin" to o'timal ta theory if the "oal is

to collect a "iven amount of revenue as efficiently as

'ossible ta rates should be set so that the com'ensated

demand for each commodity is reduced in the same

'ro'ortion% @hen the demand for each "ood de'ends only on

its o!n 'rice this is equivalent to the rule that ta

rates be inversely related to com'ensated 'rice

elasticities of demand%.4 &hus efficiency does not require

the equal taation of all "oods% Doods !ith inelastic

demands should be taed hi"her than "ood !ith elastic

demands and so on%

&aes are also often levied for reasons of holdin" 'eo'le

accountable for the social and 'rivate cost of their

activities% 6moJin" is an eam'le as such% 6moJers im'ose

hi"her costs on 'ublic health care systems and thus their

activities are taed at a hi"her rate in order to

incor'orate that eternality%

.4 osen (ahlby 6mith #oone M>ublic inance in CanadaM >a"e 429

2nd Canadian Ed% cDra!+Hill yerson 2003

- 10 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 11/84

PP Stax

SS

New

C.S. P1P1

Tax

Revenue

D.W.L.

P0 P0

P2

D1New

P.S .

D D0

Q Q

Q1 Q0 Q0 Q1

Consider the above dia"ram !here there are t!o "oods A and

# that are substitutes% @e start off at > 0 P 0 in both

marJets% /f !e !ere no! to im'ose only a ta on marJet A

the su''ly in that marJet is reduced causin" the 'rice to

rise to > . and the quantity su''lied is reduced to P . in

marJet A% &rian"le abc sho!s the total dead!ei"ht loss of

im'osin" the ta% > . is the 'rice 'aid by the customer and

>2 is the amount received by the 'roducer%

#y a''lyin" this ta on "ood A it is no! more attractive

for consumers to 'urchase "ood # because there is no taon it and its 'rice is relatively lo!er% &his causes the

demand for Dood # to increase from ( 0 to ( .% Holdin" all

other thin"s constant this causes the 'rice of Dood # to

increase and quantity su''lied also increases% &hus

overall 'rice and quantity increases in the marJet for

- 11 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 12/84

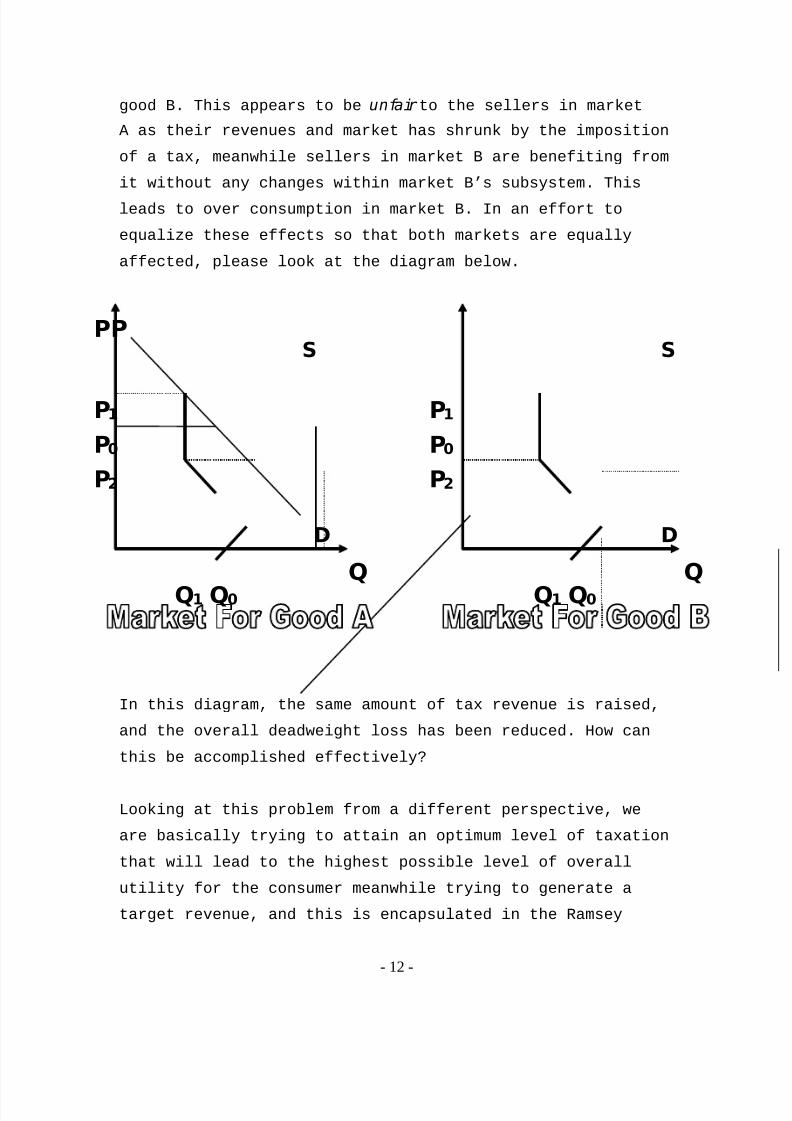

"ood #% &his a''ears to be unfairto the sellers in marJet

A as their revenues and marJet has shrunJ by the im'osition

of a ta mean!hile sellers in marJet # are benefitin" from

it !ithout any chan"es !ithin marJet #*s subsystem% &his

leads to over consum'tion in marJet #% /n an effort to

equaliLe these effects so that both marJets are equally

affected 'lease looJ at the dia"ram belo!%

PPS S

P1 P1

P0 P0

P2 P2

D D

Q Q

Q1 Q0 Q1 Q0

/n this dia"ram the same amount of ta revenue is raised

and the overall dead!ei"ht loss has been reduced% Ho! can

this be accom'lished effectivelyQ

$ooJin" at this 'roblem from a different 'ers'ective !e

are basically tryin" to attain an o'timum level of taation

that !ill lead to the hi"hest 'ossible level of overall

utility for the consumer mean!hile tryin" to "enerate a

tar"et revenue and this is enca'sulated in the amsey

- 12 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 13/84

ule% Coady and (reLe ,2002- tell us that the inde of

relative discoura"ement should be the same for all

unconstrained taes%

&he above illustration can be etended from t!o industries

to t!o countries as !ell% Consider the 'ossibility that one

country is tain" a "ood mean!hile the other is not or

conversely !here a non+resident of a country is not taed

on 'urchases% &his could lead to a lot of cross+border

'urchasin" to avoid taation% ,&his in turn leads to a ta

base erosion of both the countries if there is no non+

resident taation in the host country as !ell%-

urthermore this affects local merchants because their

revenues are declinin" as 'ersons continue to 'urchase from

abroad and avoid taes% 6inn ,.990- su""ests that in order

to avoid this sur"e in cross+border 'urchasin" there must

be a harmoniLation of ta rates es'ecially in free trade

re"ions%.5 6ince technolo"y allo!s us to maJe 'urchases from

abroad this is an im'ortant issue% &he 'roblem is ho! to

harmoniLe Q

,/,/, E78#t'

Equity is a 'rinci'le of taation that refers to the burden

of taation fallin" on individuals !ho <are obli"ed to

contribute in 'ro'ortion to their res'ective interests in

the estate=.7% urthermore Drove ,.914- tells us that <the

subIects of every state ou"ht to contribute to the su''ort

of the "overnment as nearly as 'ossible in 'ro'ortion to

their res'ective abilities= ,ability+to+'ay 'rinci'le-%

.5 6inn H%@ <&a HarmoniLation and ta com'etition in Euro'e%=

Euro'ean Economic evie! 34 489+504 .990.7 Droves Harold <&a >hiloso'hers= >a"e .. &he University of

@isconsin >ress .914

- 13 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 14/84

&his has been inter'reted ,(o!ner 200.- to mean that ta

burden on an individual should corres'ond to the benefits

they receive% &his is !hat is Jno!n as the benefit

'rinci'le 'ut forth by Adam 6mith and later com'ounded u'on

by ills.1% Another a''lication of the same 'rinci'le brin"s

us to the sacrifice 'rinci'le of taation that tells us

that each individual should )sacrifice* an equivalent

'ortion relative to their income in the form of taes%

&he limitation to this 'rinci'le is that taes are levied

based entirely on the level of income one attains% /f !e

!ere to further study this 'rinci'le the fla! !ould be

evident almost immediately% or instance !e have t!o

individuals !ith the same income same a"e and !orJ in the

same industry% Ho!ever one of them has no children

mean!hile the other one does% Unfairly one individual may

be carryin" more burden relative to dis'osable income than

the other% Ho! does this relate to someone else !ho is

maJin" more than either of the t!o and lives in the same

areaQ

&here are t!o forms of equity that try and Iustify these

t!o differences both of !hich serve to 'rovide ethical

considerations into the levyin" of taes% &hey are

HoriLontal and ertical Equity% HoriLontal Equity refers to

the notion that <'eo'le in equal 'ositions Gshould be

treated equally=.8

% &his measure of equal 'ositions is

"enerally measured by some inde of !ealth or income% osen

.1 Neill Kon % M&he benefit and sacrifice 'rinci'les of taationB A

synthesisM 6ocial Choice R @elfare 2000 ol% .1 /ssue . '..1.8 osen Harvey 6 MAN A>>OACH &O &HE 6&U( O /NCOE U&/$/& AN(

HO/SON&A$ EPU/&M Puarterly Kournal of Economics ay18 ol% 92/ssue 2 '301

- 14 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 15/84

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 16/84

,/,/2 S#m p%#"#t'

&aes should be levied and collected in a manner that is

convenient and easy to understand for the ta'ayer%.9

Com'licated ta rules maJe it difficult for 'ersons to

understand and com'ly !ith them and it also maJes

monitorin" and enforcement more difficult for "overnments%

A delicate balance must be Je't bet!een Jee'in" 'olicy

sim'le and Jee'in" it Iust% As the tain" authority tries

to incor'orate more and more variables to try and encom'ass

all the 'ossible set of situations its maJes the system

more difficult and com'licated for even a learned 'erson to

understand% Ho!ever !e must succumb to the fact that

Iustice for all is not 'ossible for "enerally a''lied ta

rules% /t !ill suffice to try and achieve a "eneral notion

of Iustice%20

&hese set of rules must be available !ith ease to the

ta'ayer and must be easily understandable as !ell% &here

must be a system that su''orts the queries of these

individuals and that 'rocesses these ta claims as they

a''ear% Availability of ta rules is essential to

com'liance !ith them% &hus !ith the evolution of the

internet amon"st other thin"s ta authorities have

benefited "reatly from this technolo"y by even "oin" so far

as creatin" online ta filin" systems Gsuch as Australia

and Canada alon" !ith maJin" ta 'olicy more available to

the 'ublic%

.9 /&E> <&a >rinci'les B #uildin" blocJs of a sound ta system= >a"e

. 200420 Denerally a''lied rules can not encom'ass the total array of 'ossible

situations%

- 16 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 17/84

,/,/ N e8tra%#t'

&a neutrality refers to the effects that chan"es in

taation have on "overnment income% /f a ta chan"e has no

net chan"e on the "overnment*s ta revenues then the ta

is said to be revenue+neutral% /f the same amount of ta is

'aid by a consumer for eam'le before and after the

chan"e the ta is said to be incidence+neutral%

&he Jey conce't here is that of indifference% /f ta

neutrality is a''lied to a 'urchaser*s decision then the

taes 'laced on the different avenues of 'urchasin" the

"ood should not be discriminate a"ainst any of them% &he

'urchaser should be indifferent to buyin" under either

system% /f the conce't !ere to be a''lied to ca'ital

investment decisions s'ecifically in the case of ca'ital

im'ort or e'ort then the ta system should maJe the

decision maJer indifferent to investin" ca'ital

domestically or abroad% 6imilarly this conce't can be

a''lied to many other thin"s such as national neutrality

,'urchasin" decisions based on different ta Iurisdictions

!ithin a country-%

Ho!ever !e Jno! the above case not to be true% &here are

thousands of ta Iurisdictions !ithin North America alone%

ather than com'etin" !ith one another for businesses and

adIust ta rates !ithin their Iurisdictions a ta similar

to the sales ta has been introduced on remote 'urchases%

&his is one attem't to "et around the 'roblem of com'etin"

ta rates% Ho!ever the 'roblem s'ecific to the U%6% is

that of com'liance Gdiscussed in further detail in 2%4 and

5%3%

- 17 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 18/84

A sales ta is a 'ro'ortional ta because everyone 'ays the

same rate re"ardless of income and also the more you

consume the more you 'ay in taes: it*s relative to ho!

much you consume ,s'end-% A use ta is a sales ta im'osed

on out+of+state vendors for sellin" "oods !ithin their

Iurisdiction% A use ta is a''lied at the same rate as the

state*s sales ta%

- 18 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 19/84

,/2 1 CO N SU M PTIO N TAXATIO N

,/2/0 1 Term #n%5'

/n "eneral there are t!o different methods of taationB

direct and indirect% &hese are t!o methods of taation used

in 'ractice% &he "eneral distinction made bet!een them is

that direct taes are on income and 'ro'erty and are

usually 'aid )directly*% /ndirect taes are 'laced on

activities and not 'aid directly% Eam'les of direct taes

are income taes 'ro'erty taes inheritance taes and

social security char"es% Eam'les of indirect taes include

retail taes ecise taes tariffs and value added taes%

&hese "enerally tend to be re"ressive ,as the value of the

'urchase increases the 'ercenta"e 'aid on them decreases-

and are often criticiLed as 'lacin" a hi"her burden the

'oor% Historically indirect taes have remained under

federal Iurisdiction and 'rovinces have been ecluded from

im'osin" them% /nitially servin" as the main source of

revenue for the "overnment ,fur and tobacco e'orts e%

Canada- they no! re'resent a smaller 'ercenta"e of federal

revenues%2.

A use ta is a ty'e of sales ta ,indirect ta- that is

'laced on remote 'urchases to reduce local ta base

erosion% A use ta is a means of su''lementin" lost revenue

from sales taes% &hus sales taes are taes a''lied to

sales ori"inatin" !ithin a Iurisdiction and a use ta is

'laced on sales of remote ori"in% >lease note the

difference bet!een the t!o as they !ill not be used

interchan"eably hence forth%

21 osen ,2003- et al% >%7

- 19 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 20/84

,/ 1 N ATIO N AL SALES TAX <S/ <ALU E AD D ED TAX =<AT>

#elo! !e shall taJe a looJ at the characteristics of A&

ta systems and N6& ta systems% @e shall com'are them as

!ell% &he 'ur'ose of this section is to hi"hli"ht ho! the

ty'e of ta system under !hich a firm o'erates affects the

'rices that it faces and char"es its accountin" methods

and the amount of taes it 'ays%

,//0 1 <AT

alue added taes a''ly to the value added to a "ood or

service contributed by a firm throu"h the use of its

factors of 'roduction% &hus if a firm buys lumber from a

lumber com'any and 'roduces tables from the lumber the

lumber car'enter !ould 'ay A& on the value added of

convertin" the trees into useable lumber and the furniture

maJer !ould 'ay A& on the value added of turnin" lumber

into tables% A firm !ould 'ay A& by subtractin" the A&

'aid on its in'uts from the A& 'aid on its sales% &here

are three ty'es of A&B i- Consum'tion+ty'e A& ii- income

A& and iii- Dross >roduct A&%22 &he consum'tion+ty'e A&

is the only one used in develo'ed countries% /n Canada the

D6& is liJe a A& because it taes final 'urchases as !ell%

,//, 1 N ATIO N AL SA LES TAX =N ST>

National sales taes are collected by vendors on behalf of

the "overnment at the final 'oint of sale and not at every

stage of production.&he ta rate a''lied is usually a

fied rate% (e'endin" on the ty'e of 'roduct bein" sold

the rate may vary% /n "eneral ho!ever 'roducts are cou'led

22 #icJley Kames % <A alue+Added &a Contrasted @ith National 6ales

&a= Con"ressional esearch 6ervice &he $ibrary of Con"ressDovernment and inance (ivision 6e'tember 2004

- 20 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 21/84

to"ether in broad "rou's and each !ithin its cate"ory has

the same ta a''lied% #icJley ,2004- tells us that ideally

the 'rice of the "oods equals the sum of the value added at

all sta"es of 'roduction and thus a A& or N6& a''lied at

the same rate !ould yield the same ta base and equal

revenue% He lays out for us the follo!in" differences that

maJe one system 'referable over the other%

,//2 1 N ST < S/ <AT

A?m #n#$trat#&e "$t$

A N6& system does not require firms to collect ta

information and 'ay taes if no final sales have been made

althou"h a A& system does% /f a firm is usin" a credit

method of collection under A& it is required to Jee' all

invoices that may be subIect to an audit% &his maJes the

A& system more e'ensive to maintain%

En!r"em ent

Under a A& system firms have an incentive to double+checJ

their re'orts to ensure accuracy for t!o reasons% &hey

!ould firstly double+checJ to maJe sure that they are

remittin" the ri"ht amounts and secondly there is a

"reater chance of them "ettin" cau"ht if the re'orts are

falsified because the "overnment may cross+checJ the

results !ith the re'orts of their su''liers% &hey may

ho!ever be able to collude to"ether to falsify both

re'orts but the N6& has neither a cross+checJin" nor a

self+checJin" mechanism at all% &herefore !e may e'ect

hi"her com'liance rates !ith A& and better enforcement%

D 8%e Ta4at#n ! G ?$ an? Ser&#"e$

(ouble taation occurs !hen in'uts or "oods are taed

multi'le times as one seller sells them to the net% /n a

A& system this may be avoided because in'uts are ta

- 21 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 22/84

deductible% Under a N6& system firms !ould have to 'rovide

eclusion certificates to su''liers before maJin" the

'urchase% Eclusion certificates are state issued

certificates to manufacturers to avoid double taation%

Also 'revious attem'ts at avoidin" double taation at the

state level have failed thus maJin" it more cumbersome and

inefficient to avoid double taation under a N6& system

o''osed to a A& system%

M a4#m 8m Ta4 Rate

/t may be said that due to increased levels of enforcement

Gand "ettin" cau"ht and voluntary com'liance by merchants

the incentive to evade taation is reduced under a A&

system% &hus #icJley ,2003- tells us that the ta rate for

a A& may be raised to a level hi"her than a N6& before a

ta evasion issue arises% On the other hand hi"her

com'liance rates mean hi"her 'robability of "atherin" taes

that !ould other!ise not be re'orted so ta rates could be

lo!ered to raise the same amount of revenue because more

'eo'le are com'liant% Equally so they may be raised to

"enerate more revenue%

T#m e R e78#re? t Im p%em ent

&he A& system !ould taJe more time to im'lement than a N6&

system sim'ly because the A& a''lies to many more firms

and 'ersons must be tau"ht the ne! ta rules% Also the A&

is more com'licated than the N6&%

<#$##%#t'

A A& is less visible to consumers as they !ould believe

that at least 'art of the A& !ould fall on 'roducers at

different sta"es of 'roduction: this is not so% Almost the

entire burden of both A& and N6& falls u'on the consumer%

Consum'tion taes !hether 'laced on consumers or

manufacturers are described as bein" 'aid by the consumer

- 22 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 23/84

because it is believed that consumers are less fleible

than 'roducers% >roducers can also 'lace the entire ta

burden on to the consumer by raisin" 'rices equivalent to

the ta they are to remit% 6ince the N6& is 'aid u'front by

the customer at the retail level they may feel that the

burden is u'on them more so% A& le"islators also have the

o'tion to choose !hether the amount of ta levied should be

'rinted on the recei't mean!hile under N6& the amount of

ta 'aid has to be e'licitly !ritten on the recei't% $ess

visibility may maJe consumers feel more comfortable about

consumin"%

- 23 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 24/84

2 1 TAX AN D E-CO M M ERCE

2/0 1 E-"m m er"e <$/ Br#"6-An?-M rtar

/t is useful to thinJ of E+commerce in terms of three

com'onentsB su''ortin" infrastructure electronic business

'rocesses and electronic commerce transactions%23 &he

su''ortin" infrastructure consists of electronic com'onents

that are used to carry out core business functions% Also

it 'rovides su''ort for the com'anies* eistence on the

internet itself% &his includes any hard!are and soft!are

used as !ell as all human ca'ital invested in the secure

o'eration of the enter'rise% /n essence the su''ortin"

infrastructure is the bacJbone of the system%

E+commerce business 'rocesses are the same as those of

traditional business ece't that these 'rocesses are

carried out usin" com'uters over a net!orJ24% E+commerce

transactions are concluded usin" any method of 'ayment made

to an online merchant for services'roducts furnished% Note

here ho!ever that 'ayment does not need to be made online:

traditional methods of 'ayments may be used to maJe

'ayments% ethods of 'ayments include the credit card

method of 'ayment and some "eneric methods of 'ayment

desi"ned s'ecifically for use on the internet such as

>ay'al% Ho!ever in order for a transaction to be

23 esenbour" &homas $% <easurin" Electronic #usinessB (efinitions

Underlyin" Conce'ts and easurement >lans= Economic >ro"rams #ureau

of the Census T htt'B!!!%census%"ove'cd!!!ebusines%htm $ast

ie!ed 6uccessfully on (ec 3rd 2004%

24 A net!orJ is 2 or more com'uters connected to"ether for the 'ur'oses

of communication%

- 24 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 25/84

considered a 'art of E+commerce revenue the agreem ent to

purchase m ust be m ade online%25

&hus if the internet is used to "ather information

re"ardin" the 'urchase of a "oodservice and then 'ayment

is made in 'erson then this is not considered E+commerce

revenue% /n this s'ecific case E+commerce has hel'ed to

facilitate sales not bear them%

&he most basic advanta"e that E+commerce has over

traditional business is that of convenience% &his

convenience allo!s consumers to access information from

their choice of location% &his convenience also translates

into the convenience of business mobility and the ability

to u'date and access information quicJly% &his does not

mean that businesses can chan"e their location 'er se as

their central G'hysical location has the same 'ro'erties

attached to it as those of a conventional merchant%

Ho!ever they may choose and move their servers !ith

relative ease to 'ossibly avoid taation% E+commerce allo!s

for real-tim e monitorin" of inventories and adIustments of

'rices% Althou"h the lar"er of the traditional retailers do

have means of real+time monitorin" they do not enIoy the

ability to adIust 'rices in real+time27% E+commerce allo!s

savin"s on valuable )menu* costs%

25 esenbour" &homas $% <easurin" Electronic #usinessB (efinitions

Underlyin" Conce'ts and easurement >lans= Economic >ro"rams #ureau

of the Census T htt'B!!!%census%"ove'cd!!!ebusines%htm $ast

ie!ed 6uccessfully on (ec 3rd 2004%

27 eal time refers to the ability to have immediate a''lication of

modifications% eal time means there are no ,si"nificant- delays andis equivalent to sayin" the chan"es are bein" made )$ive*%

- 25 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 26/84

Core strate"ic decisions are technolo"y based in E+

commerce !hereas in traditional businesses technolo"ical

decisions are usually not 'art of business strate"y% &his

reliance on electronic media to carry out core functions of

the business can also lead to 'roblems !hereby the com'any

!ould have to "o offline ,<close sho'=- tem'orarily until

the 'roblem is solved%21 Equally so an advanta"e of bein"

an e+business is that there are no hours of o'eration i%e%

the sho' is al!ays o'en%

&he "eneral means of communicatin" !ith 'otential customers

is electronic% &here is often no human interaction in #2C

transactions% Consumers are allo!ed to bro!se and sho'

around as much as they liJe !ithout the 'ressure of

sales'ersons and ultimately the 'urchase decision is

entirely u' to them%

An eam'le of E+commerce that most 'eo'le are familiar !ith

is AmaLon%com% AmaLon ,for short- is one of the "iants of

the E+commerce industry% /t acts as a !holesaler for

smaller firms located 'redominantly !ithin North America

but it has also established itself in the U? Ka'an

rance and Dermany% /ts main 'resence is online only !ith

a cor'orate headquarters in 6eattle @A%28 &he !ebsite

offers a variety of 'roducts ran"in" from electronic

consumer "oods booJs baby 'roducts to Jitchen R "arden

'roducts% AmaLon "rossed F3%93 billion in 2002 alone29

%

any online merchants chose to follo! the AmaLon model of

21 Eam'les may include 'o!er outa"es hard!are or soft!are failure or

malicious attacJs from unJno!n sources% 28 / !as in contact !ith AmaLon Customer service this information !as

obtained via email AmaLon%com Customer 6ervice29

6alJever Ale% <Ho! AmaLon O'ens U' and Cleans U'= #usiness @eeJa"aLine Kune 2003

- 26 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 27/84

conductin" business ,a sin"le 'oint of sale for many

merchants- s'ecific to their o!n marJets%

As in the traditional retailin" case !ord of mouth is a

maIor contributor to future sales% Customer o'inions are

o'en to anybody in the !orld on the internet as o''osed to

a certain locale thus 'ertainin" to either 'ositive or

ne"ative ri''le effects ar"uably more si"nificant than

those in the traditional case% &he "lobal a''lication of E+

commerce allo!s for an indefinite amount of com'etitors% As

ne! com'etitors arrive into the marJet'lace on a daily

basis the end result is a very fierce com'etitive

environment%

2/, @ +at U n#78e Ta4at#n I$$8e$ Ar#$e

(ue to its infancy as a form of business there is a lacJ

of industry standards for E+commerce as o''osed to

traditional businesses% A number of issues arise because of

the nature of E+commerce itself% &he analysis outlined

belo! identifies unique issues s'ecific to E+commerce that

set it aside from traditional trade issues% Annette Nellen

has collected a meanin"ful list of issues related

s'ecifically to E+commerce discussed belo!%30

# 8r#$?#"t#n #$$8e$ 1

Eistin" ta systems de'end on the 'hysical location of

businesses to determine !hat Iurisdiction they fall under%

/n order to 'rove this obli"ation it must be 'roven that a

firm has a >ermanent Establishment ,>E- or Neus 'resent in

30 Nellen Annette% <E+commerce B &o &a or Not to &a Q &hat is the

Puestion V Or is it Q= >a"e .4 6an Kose 6tate University 200.

- 27 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 28/84

the controlled area% A >E may be "enerally defined as any

location that facilitates <the carryin" on of the business

of the enter'rise throu"h this fied 'lace of business=%3.

E+commerce allo!s firms to have very little 'hysical

'resence in an area if they so !ish% &his lacJ of 'hysical

'resence is attributable to the mobility of the E+commerce

business model% @hen a firm falls under the tain"

Iurisdiction of a state it must collect use and sales

taes on behalf of that state as !ell as remit other taes

that it !ould normally be required to% $ocation factors

usually raise ta issues at the state local and

international level%32 &he question then arisesB because

'ersons are consumin" "oods !ithin the boundaries of a

country u'on !hom does that country im'ose use taes the

seller or the buyerQ An ar"ument can be made for either

case G6ee 6ection 3%4% &his is a central issue in the E+

commerce ta riddle because ta authorities can not 'roceed

!ithout Jno!led"e of !here the ta burden lies% A tem'orary

solution used by the U%6% to solve this issue has been to

im'ose a ta moratorium on E+commerce businesses until a

frame!orJ can be established%

An im'ortant element of this question 'osed is that one can

easily assume that both the seller and the buyer are in the

same Iurisdiction% Com'leities arise !hen sales are made

by manufacturers to consumers in a different Iurisdiction%

3. OEC( Committee on iscal Affairs MC$A//CA&/ON ON &HE A>>$/CA&/ON O

&HE>EANEN& E6&A#$/6HEN& (E/N/&/ON /N E+COECEBCHANDE6 &O &HECOEN&A ON &HE O(E$&AW CONEN&/ON ON A&/C$E 5M OEC( (ecember200032 Nellen Annette% <E+commerce B &o &a or Not to &a Q &hat is the

Puestion V Or is it Q= >a"e .3 6an Kose 6tate University 200.

- 28 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 29/84

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 30/84

this to ha''en there must be 'roof of a >ermanent

Establishment ,>E- or Neus% &he definition of source in

traditional ta theory is <the 'lace !here !ealth is

'roduced that is the community of economic life !hich

maJes 'ossible the yield of the acquisition of the !ealth%

&his yield or acquisition is due ho!ever not only to a

'articular thin" but to the human relations !hich may hel'

in creatin" them=34% &hus by havin" a 'hysical 'resence or

a sellin" a"ent !ithin a Iurisdiction that state then has

the ri"ht to ta any "ood 'roduced !ithin its borders

re"ardless of !here it is sold% &he main advanta"e of the

source+based 'rinci'le is !ith reference to income: it

avoids double taation% @hen a''lied to cross+border

commerce businesses !ould other!ise be required to maJe

'ayments to ta authorities other than their o!n de'endin"

on the definition of >E established by that state%

ii- Nature of the 'roducts

Althou"h this is outside the sco'e of this 'a'er it is

still an im'ortant as'ect of the issues surroundin" E+

commerce ta 'olicy% any forms of di"itiLed "oods may be

sold and offered on the internet such as music documents

ne!s'a'ers and customiLed information% &here is also a

'roblem of >E considerations and ho! to Iustly a''ly taes

to these 'roducts% /n a destination+based system there are

no 'hysical controls ,such as customs- to im'ose use taes

on the 'roducts before users can obtain the "oods and in a

source+based system it is difficult to establish !here

eactly the contract of a"reement tooJ 'lace% G&here is a

'lethora of information available on the ta im'lications

34 orst (avid $% <&he Continuin" itality of 6ource+#ased &aation in

the Electronic A"e= &a Notes /nternational .991

- 30 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 31/84

of each of these scenarios%35 A "reater 'roblem ho!ever is

that of monitorin" this activity% Ho! is it 'ossible for

authorities to Jno! that a di"ital 'roduct has echan"ed

handsQ 6o far a strict division bet!een tan"ible and

intan"ible "oods traded online eists% &hou"h hard to

conceive a semi+tan"ible 'roduct it may ha''en in the

future%

iii- Ne! ty'es of Assets

any of the assets that are critical to identification of

an e+business are intan"ible in nature such as the domain

name ,!!!%!eb'a"e%com- the !eb+'a"es that lie !ithin the

!ebsite and the soft!are used ,or develo'ed s'ecifically-

for use and o'eration of the business% Evaluation is a

'roblem of these intan"ible "oods for ta and accountin"

'ur'oses% or eam'le ho! !ould one determine accrued

amortiLation on domain name re"istryQ &hus these ne! ty'es

of 'ro'erty have accountin" and ta im'lications%

iv- aJin" o'timal use of the internet may challen"e old

rules

Nellen "ives a 'erfect eam'le of a non+'rofit or"aniLation

that sets u' a donation service on its !ebsite%

&raditionally one is required to maintain a recei't of

'hilanthro'ic activity for ta deduction 'ur'oses% &he

'roblem here althou"h not so com'le ,the or"aniLation can

mail a recei't to the individual- may become com'le in

other circumstances% An eam'le mi"ht be a !ebsite that

35 6ee or Eam'le oster >e''er R 6hefelman >$$C M>ro'osed Ne! $a!sB

Chan"in" the ules of Contract ormationM % #ro!ns!ord and D% Ho!ells<@hen 6urfers 6tart to 6ho'B /nternet Commerce and Contract $a!=#radley K% reeman <Electronic Contracts under Canadian $a! A>ractical Duide= Hill v% Date!ay 2000 /nc udder v% icrosoft Cor'%

- 31 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 32/84

'ays individuals for visitin" !ebsites of businesses that

advertise !ith them% (oes the state have a ri"ht to ta

that income "enerated under the su'ervision of a firm that

does not eist !ithin its borders Q

v- Other /ssues

Electronic means of communication and the electronic front

that e+businesses o'erate on allo! the scatterin" of their

!orJforce over the "lobe% /ncome re'ortin" may become an

issue under such circumstances% &here is also the issue of

!hat !ill suffice as 'roof for transactions conducted over

the internet ,di"ital si"natures et cetera-%

&he E+commerce ta issue is surrounded by the idea of

source+destination ta accountability% &his business model

is very similar in nature to another case in recent

history% &he net section dra!s similarities bet!een E+

commerce and the ail Catalo"ue industry to identify the

Jinds of taation that are useful% 6ince similar issues

!ere raised !hen the ail Catalo"ue industry first emer"ed

it may serve as a "uide for ta 'olicy on the internet%

- 32 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 33/84

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 34/84

!ere not a''licable to the la!s of @ashin"ton state since

they did not o'erate in that Iurisdiction%

&he U%6% 6u'reme Court u'held the ta statin" that it !as

not a ta on interstate commerce but rather a use ta%31

&hus this case 'rovided basis for other states to start

'lacin" use ta on remote sales% #y the .970*s all states

!ith sales taes had 'assed some form of use ta%38

/t !as found that des'ite not havin" an established

'resence !ithin a state a vendor is liable to 'ay use ta%

&he case of Nelson v% ont"omery @ard ,.94.- established

that if a firm has a 'hysical 'resence in a state then it

has to remit all taes a''licable in that state% &his

includes the 'resence of seller*s em'loyees inde'endent

contractors stocJ of "oods ,!arehouses- re'resentatives

or a"ents taJin" orders for an out+of+state seller%39 &his

relationshi' established the required Nexus to ta a

com'any% @e can almost immediately see ho! this relates to

the remote sale ta dilemma re"ardin" E+commerce to be

discussed later%

2/2/, N at#na% Be%%a$ H e$$) In"/ &$/ D epartm ent ! Re&en8e

State D epartm ent ! I%%#n#$

National #ellas Hess !as a mail order com'any based in

?ansas City issouri% All orders 'laced !ere 'laced

31 6ilas ason Co% v% &a Commission of 6tate of @ashin"ton 302 U%6%

.87 58 6%Ct% 233 ,.931-38 $undy ?athleen >% M&he &aation of E+commerceB &he /na''licability

of >hysical >resence Necessitates an Economic >resence 6tandardM &heichmond Kournal of $a! and &echnolo"y olume /// /ssue 2all 200.39 artie Charles @% </ssues in Use &a AdministrationB /ncreasin" the

Com'liance ate= in Collectin" &aes in the Cybera"e .999%

- 34 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 35/84

throu"h the mailin" system% &his firm had no established

neus in the 6tate of /llinois%

/n .971 the 6tate of /llinois obtained a Iud"ment a"ainst

#ella Hess to collect use ta on "oods sold !ithin

/llinois% &he Court cited that it has never held that a

6tate may im'ose the duty of use ta collection and 'ayment

u'on a seller !hose only connection !ith customers in the

6tate is by common carrier or the United 6tates mail%40

&en years later in National Deo"ra'hic 6ociety v%

California 6tate #oard of EqualiLation ,.911- National

Deo"ra'hic !as required to remit use ta because they had

t!o in+state offices mainly there for advertisin"

'ur'oses%4. &his !as enou"h to establish a Neus !ithin the

state and thus 'ermitted the state to collect use taes%

/n .985 after a t!o year study the Advisory Commission on

/nter"overnmental elations ,AC/- su""ested that Con"ress

ado't federal le"islation to require out+of+state vendors

to collect sales and use taes and remit them to the 'ro'er

authorities%42 AC/ at the time estimated that F2%2 #illion

in use taes !ould be collected if this system !ere

administered 'ro'erly% Ho!ever >om' ,.99.- tells us that

that this effort !as fruitless% urthermore he mentions

that businesses attem'ted to utiliLe the mail catalo"ue

industry to order office su''lies and the liJe to avoid

sales taes% &his is a 'rime eam'le of tax avoidance and

40 Duerriero ichael K% <@hatXs Net%%%or Neus /n 6tate And $ocal

&a= etro'olitan Cor'orate Counsel ma"aLine 6e't 2003

4. NA&/ONA$ DEODA>H/C v% CA$% EPUA$/SA&/ON #(% 430 U%6% 55. ,.911- 430

U%6% 55.42 AC/ <6tate and $ocal &aation of Out+Of+6tate ail Order 6ales=

A'ril .987

- 35 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 36/84

this is one of the central issues surroundin" the E+

commerce ta 'roblem% Net !e eamine the case of the Puill

Cor'oration%

2/2/2 Q 8#%% Crp/ &/ N rt+ D a6ta 033,

Puill Cor'oration !as a mail order com'any that had offices

and !arehouses in /llinois Deor"ia and California% &heir

main 'roduct !as office su''lies sold throu"h flyers and

catalo"s% Puill had no em'loyees or infrastructure set u'

in North (aJota and !as bein" sued for use ta% A maIor

'art of this case !as determinin" !hether ta 'olicy !as

im'edin" interstate commerce !hich in effect !ould be a

violation of the U%6% Constitutions* Commerce Clause%43 @hen

the case made its !ay to court the court declined to

follo! the #ellas Hess 'recedent based on B <the tremendous

social economic commercial and le"al innovations= of the

'ast quarter+century have rendered its holdin"

<obsoleGte=%44

&hus states are still 'rohibited from demandin" sales

taes from remote sellers in the sale of "oods be they via

mail tele'hone or internet orders%

Puill Cor'% continued to flourish in the years follo!in"

its court 'roceedin"s% /t !ent on to setu' an online

'resence !!!%quillcor'%com and that venture !as also a

success% /n .998 6ta'les Co% 'urchased Puill Cor'% mostly

because of its internet success database marJetin"

abilities and brand equity%45 6ta'les intended to establish

43 6cudder Keffrey A% <E+commerce B Choosin" the A''ro'riate &a

odel= aIor &hemes in Economics 200344 6u'reme Court of the United 6tates 410 N%@% 2d 203 208 ,.99.-

45 &roy iJe <PU/$$ >UCHA6E D/E6 6&A>$E6 E+>E6ENCE= (iscount 6tore

Ne!s ol% 31 /ssue 8 .998

- 36 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 37/84

its online 'resence throu"h the Puill Cor' and thus bou"ht

the com'any%

(ue to the results of the Puill Case a similar ar"ument is

made for not tain" E+commerce% /t may be ar"ued that

because the t!o forms of commerce are so similar in nature

Gout+of+state vendors that the same rules should a''ly to

both% &his ar"ument is 'resented in the net section%

- 37 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 38/84

2/ Pr an? Ant#-E-"m m er"e Ta4 Ar58m ent$

&here have been ar"uments made for and a"ainst the taation

of E+commerce since the issue first 'resented itself% or

some it may seem inconceivable that E+commerce !ould not be

taed and vice versa% &he ar"uments 'resented belo! ar"ue

both sides of the ar"ument and are meant to hi"hli"ht some

of the 'ractical moral and social issues that may arise

!hen decidin" to ta or not%

Pr:E-com m erce is a boom ing industry and has the potential

for great grow th. hus it is im perative that the correct

legal structure !including taxes" be put into place to

accom m odate new aspects of the technology as they em erge.

/t is almost natural for one to assume that because the

scale and sco'e of E+commerce is so !ides'read that the

'ersons involved in e+business are abusin" the current

)loo'holes* in the ta system to abstain from 'ayin" taes%

Ho!ever the truth of the matter is that in 200. a study

estimated that only 5 of the !orld 'o'ulation !as online47

and another estimates that in 2003 this number "re! to .041

of !hich 90 are from industrialiLed countries and nearly

a third are in America% 6o this 'roblem is re"ion s'ecific

the data sho!s and also the marJet for E+commerce is not

quite as lar"e as one mi"ht e'ect%

47 (ennis 6ylvia MKust 5 >ercent Of @orld OnlineM(ecember .. 2000 T

htt'B!!!%com'uteruser%comne!s00.2..ne!s.5%html $ast ie!ed BKuly 29th 200441 6harma (inesh C% M6tudy finds "a's in di"ital divide theoryM October

29 2003 T htt'Bmsn%com%com2.00+..04Y2+5098184%htmlQ'artZmsn $astie!ed B Kuly 29th 2004

- 38 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 39/84

#ruce o and urray48 ar"ue that there is no evidence that

the chan"es in ecess burden and the addition of

administrative and com'liance costs are hi"h enou"h to

!arrant an eem'tion of all E+commerce transactions nor is

there is any evidence that this ecess burden is hi"her

than alternative means of collective revenue%

Cn : E-com m erce is in its infancy# and applying taxes to

this industry could stifle its grow th and prevent future

grow th.A study by Austan Doolsbee and Konathan Sittrain

,.999- estimated the sales ta loss to local and state

"overnments came to a''roimately F2.0 million !hich is

less than 0%25 of overall ta revenues% Ho!ever they

estimate that this !ill rise to a''roimately .0 by the

year 2001%49 &he study si"nifies the tremendous "ro!th

'otential of E+commerce and thus if left untaed the "reat

'otential for ta base erosion% Althou"h at first it may

a''ear that the amount of ta erosion is minute there is

'otential for much "reater losses in the future% &he

ar"ument does not bear merit !hen E+commerce reaches its

more mature sta"es as a technolo"y%

A .998 study by #oston Consultin" "rou' found that the to'

four cate"ories of online sales are Com'uter "oods

inancial services Auctions and &ravel%50 Of these four

travel and financial services are not taable Gno sales

ta thus there is no loss in revenue from this activity%

48 #ruce (onald and o @illiam and urray atthe! M&o &a Or Not

&o &a Q &he Case of Electronic CommerceM Contem'orary Economic>olicy ol% 2. /ssue . '25 Kan200349 DoolsbeeAustan and SittrainKonathan <Evaluatin" the Costs and

#enefits of &ain" /nternet Commerce= ay 20 .999%50 #oston Consultin" Drou' and 6ho'%or" <&he 6tate of Online

etailin"= November .998

- 39 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 40/84

Also included in the auctions fi"ure is consumer+to+

consumer 'urchases such as on e+bay on !hich no sales ta

is due either%

Pr: Not taxing E-com m erce w ill harm $m ain street’

m erchants w ho are sub%ect to sales tax# and this w ould

erode tax bases.&he ar"ument bears merit !ithin itself in

that it !ould be unfairnot to ta E+commerce 'urchases and

subIu"ate traditional retailers to sales ta even thou"h

they may be sellin" the eact same 'roduct ,or service-%

&his may also lead to many conventional businesses to "o

the E+commerce route all the !ay and abandon their 'hysical

'resence in an effort to avoid 'ayin" taes% eferrin" bacJ

to the 'rinci'le of vertical equity not tain" E+commerce

and leavin" main street merchants taed !ould be unfair to

lo!+income families !ho either do not have the facilities

or the education to utiliLe the advanta"es 'osed by E+

commerce%

Cn:&f E-com m erce is taxed then due to the ease of

relocating# e-business firm s w ill locate them selves in tax

havens to avoid paying sales and use taxes. his m ay cause

states to engage in a bidding eff ort to reduce taxes to

accom m odate business presence.&his is a very valid threat

and an etreme eam'le of tax avoidance% @ithin minutes it

is 'ossible to )move* a !ebsite from one country to

another and thus avoid some ty'es of taes% Already there

are many com'anies that offer settin" u' )offshore* !eb+

hostin" services to taJe advanta"e of !hat they call )ta

- 40 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 41/84

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 42/84

'rice for internet access that !ill be taed% &hus anybody

usin" )basic* internet 'acJa"es under the floor 'rices !ill

not be taed for their usa"e% Anythin" over and above that

!ill be considered a luury 'acJa"e and thus taed

accordin"ly% &his is more an ar"ument a"ainst tain"

internet usa"e than internet 'urchases%

Doolsbee ,.999- notes ho! it is im'ortant to Jee' an o'en

frame of mind about this situation% He ar"ues that for

eam'le rou"hly 20 of com'uter 'urchases are made by

consumers directly from manufacturers% One of the maIor

com'uter 'roducers in the U6A is (ell and they have an

available o'tion to 'urchase com'uters online% Kust because

the internet is not available to a consumer that does not

mean that 'urchases can not be made from (ell% &here is

still the available o'tion of usin" the tele'hone%

&herefore the 'oint Doolsbee is tryin" to maJe is that

the 'roblem is much broader than internet vs% traditional

retailers as the non+availability of the internet may not

hinder sales from online merchants and also the non+

availability of the internet does not mean that those same

'urchases !ould be made at merchants on ) ain streetGsame

Iurisdiction%

- 42 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 43/84

1 Attem pt$ at P%#"'

/0 1 O ECD

&he Or"aniLation for Economic Co+o'eration and (evelo'ment

,OEC(- is an or"aniLation that hel's "overnments deal !ith

some of the challen"es of livin" in a "lobal society%

Currently there are 30 member countries that com'rise of

the OEC(% &hese members include Austria Australia

#el"ium Canada 6!itLerland U%? and the United 6tates%

OEC( mainly deals !ith economic social trade and

"overnance issues and to create 'olicies that !orJ%

Currently the 'roblem has been that of !ei"hin" the 'ros

and cons of the ar"uments 'resented above each of !hich

bein" taJen into account !hen creatin" sound 'olicy% 6ince

the 'olicy has to be a''licable to a number of states a

"eneral solution that the OEC( has to !orJ to!ards is that

of ta harmoniLation to avoid ta dis'utes and a system

that is sim'le and fair at the same time%

@ith re"ard to the taation of E+commerce the OEC( has

carried out many studies that are s'ecific to the heart of

the subIect53% 6ince E+commerce is a trans+border method of

carryin" out business activity it has thus been much more

im'ortant to Jee' the international frame!orJ in mind !hen

dealin" !ith any 'olicy issues%

/n October .998 the OEC( inisterial Conference !as held

in Otta!a Canada% &his conference laid the "rounds for the

<OEC( Action >lan or Electronic Commerce=%

53OEC( + <E+commerce &a B A sober vie! of Cybers'ace= (avid Holmes

2002: <A borderless @orldB ealisin" the 'otential of "lobal ElectronicCommerce= OEC( .998 : <&he Economic and 6ocial /m'act of ElectronicCommerce= OEC( .999

- 43 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 44/84

&he action 'lan entails the follo!in" B52

• #uildin" &rust for Users and Consumers &o instill

confidence in di"ital marJet'lace%

• Establishin" "round rules for the di"ital marJet'lace

aJin" 'olicies that !ill ensure 'rotection for all

'arties involved Iust as there are in the 'hysical

marJet'lace%

• Establishin" "rounds for the information

infrastructure for electronic commerce &he "oal

behind this is to establish and maintain com'etition

in the communications industry in order to Jee' costs

'rices do!n and Jee' quality hi"h%

• aimiLin" the benefits of electronic commerce

aimiLin" both social and economic benefits to the

countries involved or"aniLations and consumers and

etend this model to develo'in" countries%

&he difference bet!een this meetin" and those before it isthat s'ecific "uidelines roles and res'onsibilities !ere

e'licated to member countries%

Also identified !ere the follo!in" 'rinci'les that should

a''ly to E+commerce taation la!sB54 neutrality efficiency

certainty sim'licity effectiveness fairness and

fleibility%

An im'ortant 'art of this accord !as that the develo'ment

of the E+commerce sector should be left to the 'rivate

sector to do themselves throu"h the use of ca'ital and

54 OEC( E+commerce >olicy #rief 200.

- 44 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 45/84

utiliLin" ne! technolo"ies as they emer"e% &his avoids

dis'utes over tariff+liJe arran"ements over claims that

"overnment assistance is allo!in" an industry in that

country to flourish%

&he OEC( commissioned a study by a &echnical Advisory Drou'

,&AD- to study the E+commerce ta issue% One of their maIor

"oals !as to identify the amount of different ty'es of

activity and methods of transactions that !ould constitute

E+commerce% &he &AD outlined 28 different 'ossible ty'es of

transactions55 thus 'rovidin" an available taonomy of the

transactions that !ould o'en the door for 're'arin" the

best 'olicy for each of the cate"ories% &he t!o relevant

cate"ories for us are Cate"ory .B <&he sale of tan"ible

"oods over the internet= and Cate"ory 23B <Online

Auctions= G#2C sales of tan"ible "oods only% &he re'ort

cate"oriLes these sales as 'art of business+'rofit Gthus

liable to different ta rules and not as royalties%

/n 200. the Committee of iscal Affairs 'ublished a e'ort

entitled <&aation and Electronic CommerceB /m'lementin"

the Otta!a &aation rame!orJ Conditions=% Alon" !ith

6mith*s 4 canons of taation the CA calls for another

'rinci'le to be included in taation issuesB leibility

&a systems should be fleible and dynamic enou"h to Jee'

'ace !ith commercial and technolo"ical develo'ments%57 &he

CA "o on to define a >ermanent Establishment ,>E- as <a

fied 'lace of business throu"h !hich the business of an

55 &echnical Advisory Drou' on &reaty Characterisation of Electronic

Commerce >aymentsM&AW &EA& CHAAC&E/6A&/ON /66UE6 A/6/ND O E+COECEM ebruary 200. OEC(57 OEC( </m'lementin" &he Otta!a &aation rame!orJ Challen"e=

,#reifin"- Committee of iscal Affairs >a"e . 2000

- 45 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 46/84

enter'rise is !holly or 'artly carried on= !hich is crucial

to the ar"ument of establishin" neus% E'licitly ecluded

from this definition are facilities used solely to store

dis'lay or deliver the "oods%

One of the maIor contributions of this study is the

su""estion that consum'tion taes on cross+border trade

should taJe 'lace in the location !here consum'tion taJes

'lace% Also that an international consensus should be held

for ta on "oods en route to other locations or bein"

!arehoused ,this has to do !ith !hether these 'rocesses add

value to the 'roduct or not-%51

&his a''lies to #usiness+to+

#usiness transactions% or #usiness+to+Consumer

transactions the 'lace of consum'tion is the Iurisdiction

!here the 'urchaser resides and thus that Iurisdiction

!ould im'lement use taes on those 'urchasers !ithin its

borders% &his refers to the destination+based sourcin"

'rinci'le referred to earlier%

/n another re'ort "uidelines !ere laid out on ho! to avoid

multi'le taation of E+commerce activity or conversely

unintentional non+taation58 Gnot tain" "oods that should

be taed% &he re'ort calls for 'artici'ants to !ait

'atiently until allcountries a''ly the destination based

taation 'rinci'le or until consistent rules are com'iled%

&he same recommendation !as made for uniform definition and

verification controls%

51 OEC( </m'lementin" &he Otta!a &aation rame!orJ Challen"e=

,#reifin"- Committee of iscal Affairs 200058 OEC( </m'lementin" &he Otta!a &aation rame!orJ Challen"e=

,#reifin"- Committee of iscal Affairs >a"e 3 2000

- 46 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 47/84

Ho!ever it must be noted that the res'onsibility for

collectin" D6& ,A& in some Iurisdictions- remains !ith the

seller51 ,>a"e 20-% All a''licable taes must be collected

at the time of the transaction as chances of correctin"

this error are minimal in later sta"es% &his is obviously

creates difficulty for the sellers as they must remit

taes to different Iurisdictions around the !orld% or

eam'le if / 'urchased a "ood online from a com'any in

>aJistan they must remit the D6& to the Canadian

Dovernment%

/, 1 O t+er E! !rt$

&here have been other efforts made by "rou's such as

UN/C/&A$ and the @&O% Ho!ever none have been as

com'rehensive as the efforts of the OEC(% &hey do not

'ossess the sim'licity or thorou"hness that the OEC( model

offers% A close second !ould have to be an advisory

committee re'ort those 're'ared by )&he Koint enture &a

>olicy Drou'* in arch 2000% &hey 'ro'osed .. 'ossible

alternatives meant to a''ease different 'arties and

different 'arts of the E+commerce ta riddle G6ee &able 3

A''endi%59

59 Koint enture &a >olicy Drou' <6ummary of A''roaches or A''lyin"

6ales and Use &aes to E+commerce= 6ilicon alley Net!orJ 2000

- 47 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 48/84

. 1 Ca$e St8?#e$

&his section of the 'a'er intends to observe !hat real life

'olicy has been ado'ted by a select "rou' of countries% &he

subIects of this section are the EU United 6tates /ndia

and Australia% Each s'ecific subIect has been chosen due to

either their monumental involvement in the E+commerce ta

issue or because of distinct features of the country that

!ould maJe its E+commerce ta 'olicy more interestin"%

Ultimately these countries are meant to re'resent differin"

!ays of handlin" the same 'roblem and !ill assist in

tryin" to understand !hy sound economic theory is not

al!ays easy to translate into reality%

or each of the countries there is a table in the a''endi

that sho!s 'o'ulation e'ected internet 'enetration

e'ected transactions over /nternet for a "iven date ho!

much of that transaction is #2# and their conce't of a

'ermanent establishment ,>E-%

./0 1 EU

/n 2004 the Euro'ean Union consisted of .5 Countries%

Another .0 accession countries !ere 'ermitted to Ioin in

2004% &he EU commission is more than half a century old

and their "oals include maintainin" the overall "eneral

'ros'erity of the re"ion and free flo! of "oods 'eo'le

and ca'ital !ithin the union% (evelo'in" 'olicy for the

"rou' of nations on emer"in" ne! "rounds is also 'art of

the directive of the commission% &he 'roblem that sets the

EU aside from the others is that the 'olicy that it maJes

has to address the concerns of its members% &hus there is

added 'ressure and com'leity to each issue because of

harmoniLation%

- 48 -

8/18/2019 Taxing Cyberspace : Economic Application and Cross-Country Policy Analysis

http://slidepdf.com/reader/full/taxing-cyberspace-economic-application-and-cross-country-policy-analysis 49/84

AcJno!led"in" the economic 'otential for E+commerce in the

years to come the EU and U6 released a Ioint statement on

Electronic commerce in .991% &he U6 &reasury had first

initially made the statement the EU re'lied and they made

a Ioint statement follo!in" that% Here are some of the

'oints discussed and a"reed u'onB70

• /nternational coo'eration and coordination are

required in order to establish a frame!orJ that !ill

harness the 'o!er of the internet and its uses for

trade%

•

E+commerce !ill be an im'ortant robust en"ine for

"ro!th in the 2.st century%

• E'ansion of "lobal E+commerce !ill be marJet led