taxes—firearms and ammu- - gpo · 669 bureau of alcohol, tobacco and firearms, treasury pt. 53...

TRANSCRIPT

669

Bureau of Alcohol, Tobacco and Firearms, Treasury Pt. 53

§ 47.62 False statements or conceal-ment of facts.

Any person who willfully, in a reg-istration or permit application, makesany untrue statement of a materialfact or fails to state a material fact re-quired to be stated therein or nec-essary to make the statements thereinnot misleading, shall upon convictionbe fined not more than $1,000,000, or im-prisoned not more than 10 years, orboth.

[T.D. ATF–8, 39 FR 3251, Jan. 25, 1974, asamended by T.D. ATF–215, 50 FR 42162, Oct.18, 1985; T.D. ATF–287, 54 FR 13681, Apr. 5,1989]

§ 47.63 Seizure and forfeiture.

Whoever knowingly imports into theUnited States contrary to law any arti-cle on the U.S. Munitions Import List;or receives, conceals, buys, sells, or inany manner facilitates its transpor-tation, concealment, or sale after im-portation, knowing the same to havebeen imported contrary to law, shall befined not more than $10,000 or impris-oned not more than 5 years, or both;and the merchandise so imported, orthe value thereof shall be forfeited tothe United States.

(18 U.S.C. 545)

[T.D. ATF–8, 39 FR 3251, Jan. 25, 1974, asamended by T.D. ATF–215, 50 FR 42162, Oct.18, 1985]

PART 53—MANUFACTURERS EXCISETAXES—FIREARMS AND AMMU-NITION

Subpart A—Introduction

Sec.53.1 Introduction.53.2 Attachment of tax.53.3 Exemption certificates.

Subpart B—Definitions

53.11 Meaning of terms.

Subpart C—Administrative andMiscellaneous Provisions

53.21 Forms prescribed.53.22 Employer identification number.53.23 Alternate methods or procedures.53.24 Records.

Subparts D–F [Reserved]

Subpart G—Tax Rates

53.61 Imposition and rates of tax.53.62 Exemptions.53.63 Other tax-free sales.

Subparts H–I [Reserved]

Subpart J—Special Provisions Applicableto Manufacturers Taxes

53.91 Charges to be included in sale price.53.92 Exclusions from sale price.53.93 Other items relating to tax on sale

price.53.94 Constructive sale price; scope and ap-

plication.53.95 Constructive sale price; basic rules.53.96 Constructive sale price; special rule

for arm’s length sales.53.97 Constructive sale price; affiliated cor-

porations.53.98 Computation of tax on leases and in-

stallment sales.53.99 Sales of installment accounts.53.100 Exclusion of local advertising charges

from sale price.53.101 Limitation on aggregate of exclusions

and price readjustments.53.102 No exclusion or readjustment for

other advertising charges or reimburse-ments.

53.103 Lease considered as sale.53.104 Limitation on amount of tax applica-

ble to certain leases.

USE BY MANUFACTURER OR IMPORTERCONSIDERED SALE

53.111 Tax on use by manufacturer, pro-ducer, or importer.

53.112 Business or personal use of articles.53.113 Events subsequent to taxable use of

article.53.114 Use in further manufacture.53.115 Computation of tax.

APPLICATION OF TAX IN CASE OF SALES BYOTHER THAN MANUFACTURER OR IMPORTER

53.121 Sales of taxable articles by a personother than the manufacturer, producer,or importer.

Subpart K—Exemptions, Registration, Etc.

53.131 Tax-free sales; general rule.53.132 Tax-free sale of articles to be used

for, or resold for, further manufacture.53.133 Tax-free sale of articles for export, or

for resale by the purchaser to a secondpurchaser for export.

53.134 Tax-free sale of articles for use by thepurchaser as supplies for vessels or air-craft.

VerDate 26<APR>99 10:09 Apr 28, 1999 Jkt 183099 PO 00000 Frm 00665 Fmt 8010 Sfmt 8010 Y:\SGML\183099T.XXX pfrm02 PsN: 183099T

670

27 CFR Ch. I (4–1–99 Edition)§ 53.1

53.135 Tax-free sale of articles to State andlocal governments for their exclusiveuse.

53.136 Tax-free sales of articles to nonprofiteducational organizations.

53.137–53.139 [Reserved]53.140 Registration.53.141 Exceptions to the requirement for

registration.53.142 Denial, revocation or suspension of

registration.53.143 Special rules relating to further man-

ufacture.

Subpart L—Refunds and Other Administra-tive Provisions of Special Applicationto Manufacturers Taxes

53.151 Returns.53.152 Final returns.53.153 Time for filing returns.53.154 Manner of filing returns.53.155 Extension of time for filing returns.53.156 Extension of time for paying tax

shown on return.53.157 Deposit requirement for deposits

made for calendar quarters prior to July1, 1995.

53.158 Payment of tax by electronic fundtransfer.

53.159 Deposit requirement for depositsmade for calendar quarters beginning onor after July 1, 1995.

53.161 Authority to make credits or refunds.53.162 Abatements.53.163–53.170 [Reserved]53.171 Claims for credit or refund of over-

payments of manufacturers taxes.53.172 Credit or refund of manufacturers tax

under chapter 32.53.173 Price readjustments causing overpay-

ments of manufacturers tax.53.174 Determination of price readjust-

ments.53.175 Readjustment for local advertising

charges.53.176 Supporting evidence required in case

of price readjustments.53.177 Certain exportations, uses, sales, or

resales causing overpayments of tax.53.178 Exportations, uses, sales, and resales

included.53.179 Supporting evidence required in case

of manufacturers tax involving expor-tations, uses, sales, or resales.

53.180 Tax-paid articles used for furthermanufacture and causing overpaymentsof tax.

53.181 Further manufacture included.53.182 Supporting evidence required in case

of tax-paid articles used for further man-ufacture.

53.183 Return of installment accounts caus-ing overpayments of tax.

53.184 Refund to exporter or shipper.53.185 Credit on returns.

53.186 Accounting procedures for like arti-cles.

53.187 OMB control numbers.

AUTHORITY: 26 U.S.C. 4181, 4182, 4216–4219,4221–4223, 4225, 6001, 6011, 6020, 6021, 6061, 6071,6081, 6091, 6101–6104, 6109, 6151, 6155, 6161, 6301–6303, 6311, 6402, 6404, 6416, 7502.

SOURCE: T.D. ATF–308, 56 FR 303, Jan. 3,1991, unless otherwise noted.

Subpart A—Introduction

§ 53.1 Introduction.

The regulations in this part (part 53,subchapter C, chapter I, title 27, Codeof Federal Regulations) are designated‘‘Manufacturers Excise Taxes—Fire-arms and Ammunition.’’ The regula-tions relate to the tax on the sale offirearms and ammunition imposed bysection 4181 of the Internal RevenueCode of 1986, and to certain related ad-ministrative provisions of chapter 32,subchapter F, of the Code. Chapter 32,subchapter D of the Code imposes taxeson the sale or use by the manufacturer,producer, or importer of certain rec-reational equipment specified in thatchapter. References in the regulationsin this part to the ‘‘Internal RevenueCode’’ or the ‘‘Code’’ are references tothe Internal Revenue Code of 1986(United States Code of 1986), as amend-ed, unless otherwise indicated. Ref-erences to a section or other provisionof law are references to a section orother provision of the Internal RevenueCode of 1986, as amended, unless other-wise indicated.

§ 53.2 Attachment of tax.

(a) For purposes of this part, themanufacturers excise tax generally at-taches when the title to the articlesold passes from the manufacturer to apurchaser.

(b) When title passes is dependentupon the intention of the parties asgathered from the contract of sale andthe attendant circumstances. In theabsence of expressed intention, thelegal rules of presumption followed inthe jurisdiction where the sale is madegovern in determining when titlepasses.

(c) In the case of a sale on credit, thetax attaches whether or not the pur-chase price is actually collected.

VerDate 26<APR>99 10:09 Apr 28, 1999 Jkt 183099 PO 00000 Frm 00666 Fmt 8010 Sfmt 8010 Y:\SGML\183099T.XXX pfrm02 PsN: 183099T

671

Bureau of Alcohol, Tobacco and Firearms, Treasury § 53.11

(d) Where a consignor (such as a man-ufacturer) consigns articles to a con-signee (such as a dealer), retainingownership in them until they are dis-posed of by the consignee, title doesnot pass, and the tax does not attachuntil sale by the consignee. Where therelationship between a manufacturerand a dealer is that of principal andagent, title does not pass, and the taxdoes not attach, until sale by the deal-er.

(e) In the case of a lease, an install-ment sale, a conditional sale, or a chat-tel mortgage arrangement or similararrangement creating a security inter-est, a proportionate part of the tax at-taches to each payment. See section4217 and §§ 53.103 and 53.104 for a limita-tion on the amount of tax payable onlease payments.

(f) In the case of use by the manufac-turer, the tax attaches at the time theuse begins.

§ 53.3 Exemption certificates.Several sections of the regulations in

this part, relating to sales exempt frommanufacturers excise tax, require themanufacturer to obtain an exemptioncertificate from the purchaser to sub-stantiate the exempt character of thesale. Any form of exemption certificatewill be acceptable if it includes all theinformation required to be contained insuch a certificate by the pertinent sec-tions of the regulations in this part.These certificates are available aspreprinted documents which may be or-dered from the Bureau’s DistributionCenter (see § 53.21 for the address of theDistribution Center). The preprintedcertificates may be reproduced as need-ed.

[T.D. ATF–380, 61 FR 37005, July 16, 1996]

Subpart B—Definitions

§ 53.11 Meaning of terms.When used in this part and in forms

prescribed under this part, where nototherwise distinctly expressed or mani-festly incompatible with the intentthereof, terms shall have the meaningsascribed in this section. Words in theplural form shall include the singular,and vice versa, and words importingthe masculine gender shall include the

feminine. The terms ‘‘includes’’ and‘‘including’’ do not exclude otherthings not enumerated which are in thesame general class or are otherwisewithin the scope thereof.

ATF officer. An officer or employee ofthe Bureau of Alcohol, Tobacco andFirearms (ATF) authorized to performany function relating to the adminis-tration or enforcement of this part.

Calendar quarter. A period of 3 cal-endar months ending on March 31, June30, September 30, or December 31.

Calendar year. The period which be-gins January 1 and ends on the fol-lowing December 31.

Chapter 32. For purposes of this partchapter 32 means section 4181, chapter32, of the Internal Revenue Code of1986, as amended.

Code. Internal Revenue Code of 1986,as amended.

Director. The Director, Bureau of Al-cohol, Tobacco and Firearms, the De-partment of the Treasury, Washington,DC 20226.

Electronic fund transfer (EFT). Anytransfer of funds effected by a tax-payer’s financial institution, either di-rectly or through a correspondentbanking relationship, via the FederalReserve Communications System(FRCS) or Fedwire to the Treasury Ac-count at the Federal Reserve Bank.

Exportation. The severance of an arti-cle from the mass of things belongingwithin the United States with the in-tention of uniting it with the mass ofthings belonging within some foreigncountry or within a possession of theUnited States.

Exporter. The person named as ship-per or consignor in the export bill oflading.

Financial institution. A bank or otherfinancial institution, whether or not amember of the Federal Reserve Sys-tem, which has access to the FederalReserve Communications Systems(FRCS) or Fedwire. The ‘‘FRCS’’ or‘‘Fedwire’’ is a communications net-work that allows Federal Reserve Sys-tem member financial institutions toeffect a transfer of funds for their cus-tomers (or other financial institutions)to the Treasury Account at the FederalReserve Bank.

VerDate 26<APR>99 10:09 Apr 28, 1999 Jkt 183099 PO 00000 Frm 00667 Fmt 8010 Sfmt 8010 Y:\SGML\183099T.XXX pfrm02 PsN: 183099T

672

27 CFR Ch. I (4–1–99 Edition)§ 53.11

Firearms. Any portable weapons, suchas rifles, carbines, machine guns, shot-guns, or fowling pieces, from which ashot, bullet, or other projectile may bedischarged by an explosive.

Importer. Any person who brings ataxable article into the United Statesfrom a source outside the UnitedStates, or who withdraws such an arti-cle from a customs bonded warehousefor sale or use in the United States. Ifthe nominal importer of a taxable arti-cle is not its beneficial owner (for ex-ample, the nominal importer is a cus-toms broker engaged by the beneficialowner), the beneficial owner is the‘‘importer’’ of the article for purposesof chapter 32 of the Code and is liablefor tax on his sale or use of the articlein the United States. See section 4219of the Code and 27 CFR 53.121 for thecircumstances under which sales bypersons other than the manufactureror importer are subject to the manu-facturers excise tax.

Knockdown condition. A taxable arti-cle that is unassembled but completeas to all component parts.

Manufacturer. Includes any personwho produces a taxable article fromscrap, salvage, or junk material, orfrom new or raw material, by proc-essing, manipulating, or changing theform of an article or by combining orassembling two or more articles. Theterm also includes a ‘‘producer’’ and an‘‘importer.’’ Under certain cir-cumstances, as where a person manu-factures or produces a taxable articlefor another person who furnishes mate-rials under an agreement whereby theperson who furnished the materials re-tains title thereto and to the finishedarticle, the person for whom the tax-able article is manufactured or pro-duced, and not the person who actuallymanufactures or produces it, will beconsidered the manufacturer.

A manufacturer who sells a taxablearticle in a knockdown condition is lia-ble for the tax as a manufacturer.Whether the person who buys suchcomponent parts or accessories and as-sembles a taxable article from themwill be liable for tax as a manufacturerof a taxable article will depend on therelative amount of labor, material, andoverhead required to assemble thecompleted article and on whether the

article is assembled for business or per-sonal use.

Person. An individual, trust, estate,partnership, association, company, orcorporation. When used in connectionwith penalties, seizures, and forfeit-ures, the term includes an officer oremployee of a partnership, who as anofficer, employee or member, is under aduty to perform the act in respect ofwhich the violation occurs.

Pistols. Small projectile firearmswhich have a short one-hand stock orbutt at an angle to the line of bore anda short barrel or barrels, and which aredesigned, made, and intended to beaimed and fired from one hand. Theterm does not include gadget devices,guns altered or converted to resemblepistols, or small portable guns erro-neously referred to as pistols, as, forexample, Nazi belt buckle pistols, glovepistols, or one-hand stock guns firingfixed shotgun or fixed rifle ammuni-tion.

Possession of the United States. In-cludes Guam, the Midway Islands, Pal-myra, the Panama Canal Zone, theCommonwealth of Puerto Rico, Amer-ican Samoa, the Virgin Islands, andWake Island.

Purchaser. Includes a lessee where thelessor is also the manufacturer of thearticle.

Region. A Bureau of Alcohol, Tobaccoand Firearms Region.

Regional director (compliance). Theprincipal ATF regional official respon-sible for administering regulations inthis part.

Revolvers. Small projectile firearmsof the pistol type, having a breech-loading chambered cylinder so ar-ranged that the cocking of the hammeror movement of the trigger rotates itand brings the next cartridge in linewith the barrel for firing.

Sale. An agreement whereby the sell-er transfers the property (that is, thetitle or the substantial incidents ofownership in goods) to the buyer for aconsideration called the price, whichmay consist of money, services, orother things.

Secretary. The Secretary of the Treas-ury or his delegate.

Shells and cartridges. Include any arti-cle consisting of a projectile, explosive,

VerDate 26<APR>99 10:09 Apr 28, 1999 Jkt 183099 PO 00000 Frm 00668 Fmt 8010 Sfmt 8010 Y:\SGML\183099T.XXX pfrm02 PsN: 183099T

673

Bureau of Alcohol, Tobacco and Firearms, Treasury § 53.22

and container that is designed, assem-bled, and ready for use without furthermanufacture in firearms, pistols or re-volvers. A person who reloads usedshell or cartridge casings is a manufac-turer of shells or cartridges within themeaning of section 4181 if such reloadedshells or cartridges are sold by the re-loader. However, the reloader is not amanufacturer of shells or cartridges if,in return for a fee and expenses, he re-loads casings of shells or cartridgessubmitted by a customer and returnsthe reloaded shells or cartridges withthe identical casings provided by thecustomer to that customer. Under suchcircumstances, the customer would bethe manufacturer of the shells or car-tridges and may be liable for tax on thesale of articles. See section 4218 of theCode and § 53.112.

Taxable article. Any article taxableunder section 4181 of the Code.

Treasury Account. The Department ofTreasury’s General Account at theFederal Reserve Bank of New York.

Vendor. Includes a lessor where thelessor is also the manufacturer of thearticle.

[T.D. ATF–308, 56 FR 303, Jan. 3, 1991, asamended by T.D. ATF–312, 56 FR 31083, July9, 1991; T.D. ATF–330, 57 FR 40325, Sept. 3,1992; T.D. ATF–365, 60 FR 33670, June 28, 1995;T.D. ATF–404, 63 FR 52603, Oct. 1, 1998]

Subpart C—Administrative andMiscellaneous Provisions

§ 53.21 Forms prescribed.

(a) The Director is authorized to pre-scribe all forms required by this part.All of the information called for ineach form shall be furnished as indi-cated by the headings on the form andthe instructions on or pertaining to theform. In addition, information calledfor in each form shall be furnished asrequired by this part.

(b) Requests for forms should bemailed to the ATF Distribution Center,7943 Angus Court, Springfield, Virginia22153.

(c) Signature authorization. An indi-vidual’s signature on a return, state-ment, or other document made by orfor a corporation or a partnership shallbe prima facie evidence that the indi-

vidual is authorized to sign the return,statement, or other document.

[T.D. ATF–308, 56 FR 303, Jan. 3, 1991. Redes-ignated in part by T.D. ATF–365, 60 FR 33670,June 28, 1995, as amended by T.D. 372, 61 FR20724, May 8, 1996]

§ 53.22 Employer identification num-ber.

(a) Requirement of application. (1) Ex-cept for one-time or occasional filers,every person who makes a sale or useof an article with respect to which atax is imposed by section 4181 of theCode, and who has not earlier been as-signed an employer identification num-ber or has not applied for one, shallmake an application on Form SS–4 foran employer identification number.The application and any supple-mentary statement accompanying itshall be prepared in accordance withthe applicable form, instructions, andregulations and shall set forth fullyand clearly the data therein called for.Form SS–4 may be obtained from anyinternal revenue district office, inter-nal revenue service center or ATF re-gional office. The application shall befiled with the internal revenue officerdesignated in the instructions applica-ble to Form SS–4. The application shallbe signed by:

(i) The individual if the person is anindividual;

(ii) The president, vice-president, orother principal officer, if the person isa corporation;

(iii) A responsible and duly author-ized member or officer having knowl-edge of its affairs, if the person is apartnership or other unincorporatedorganization; or

(iv) The fiduciary, if the person is atrust or estate.

An employer identification numberwill be assigned to the person in duecourse upon the basis of informationreported on the application requiredunder this section.

(2) Time for filing Form SS–4. The ap-plication for an employer identifica-tion number shall be filed no later thanthe seventh day after the date of thefirst sale or use of an article with re-spect to which a tax is imposed bychapter 32 of the Code. However, theapplication should be filed far enoughin advance of the first required use of

VerDate 26<APR>99 10:09 Apr 28, 1999 Jkt 183099 PO 00000 Frm 00669 Fmt 8010 Sfmt 8010 Y:\SGML\183099T.XXX pfrm02 PsN: 183099T

674

27 CFR Ch. I (4–1–99 Edition)§ 53.23

such number to permit issuance of thenumber in time for compliance withsuch requirement.

(3) One-time or occasional filers. A per-son who files a return under the provi-sions of section 53.151(a)(5) is not re-quired to make application for an em-ployer identification number. Suchpersons may use their social securitynumber on any return, statement orother document submitted to ATF bythat person in lieu of an employer iden-tification number.

(b) Use of employer identification num-ber. The employer identification num-ber assigned to a person liable for a taximposed by chapter 32 of the Code shallbe shown on any return, statement, orother document submitted to ATF bythe person.

[T.D. ATF–308, 56 FR 303, Jan. 3, 1991, asamended by T.D. ATF–365, 60 FR 33670, June28, 1995]

§ 53.23 Alternate methods or proce-dures.

(a) A taxpayer, on specific approvalby the Director as provided in this sec-tion, may use an alternate method orprocedure in lieu of a method or proce-dure specifically prescribed in thispart. The Director may approve an al-ternate method or procedure, subjectto stated conditions, when—

(1) Good cause has been shown for theuse of the alternate method or proce-dure;

(2) The alternate method or proce-dure is within the purpose of, and con-sistent with the effect intended by, thespecifically prescribed method or pro-cedure, and affords equivalent securityto the revenue; and

(3) The alternate method or proce-dure will not be contrary to any provi-sion of law and will not result in an in-crease in cost to the Government orhinder the effective administration ofthis part. No alternate method or pro-cedure relating to the assessment, pay-ment, or collection of tax shall be au-thorized under this paragraph.

(b) Where the taxpayer desires to em-ploy an alternate method or procedure,a written application to do so shall besubmitted to the regional director fortransmittal to the Director. The appli-cation shall specifically describe theproposed alternate method or proce-

dure and shall set forth the reasonstherefor. Alternate methods or proce-dures shall not be employed until theapplication has been approved by theDirector. The taxpayer shall, duringthe period of authorization of an alter-nate method or procedure, comply withthe terms of the approved application.Authorization for any alternate meth-od or procedure may be withdrawnwhenever, in the judgment of the Di-rector, the revenue is jeopardized orthe effective administration of thispart is hindered by the continuation ofsuch authorization.[T.D. ATF–365, 60 FR 33670, June 28,1995]

§ 53.24 Records.(a) In general—(1) Form of records. The

records required by the regulations inthis part shall be kept accurately, butno particular form is required for keep-ing the records. Such forms and sys-tems of accounting shall be used as willenable an ATF officer to ascertainwhether liability for tax is incurredand, if so, the amount thereof.

(2) [Reserved](b) Copies of returns, schedules, and

statements. Every person who is re-quired, by the regulations in this partor by instructions applicable to anyform prescribed thereunder, to keepany copy of any return, schedule,statement, or other document, shallkeep such copy as a part of the records.

(c) Records of claimants. Any personwho, pursuant to the regulations inthis part, claims a refund, credit, orabatement, shall keep a complete anddetailed record with respect to the tax,interest, addition to the tax, additionalamount, or assessable penalty to whichthe claim relates. Such record shall in-clude any records required of theclaimant by paragraph (b) of this sec-tion and subpart L of this part.

(d) Place and period for keepingrecords. (1) All records required by thispart shall be prepared and kept by theperson required to keep them, at one ormore convenient and safe locations ac-cessible to ATF officers, and shall atall times be immediately available forinspection by such officers.

(2) Except as otherwise provided inthis subparagraph, every person re-quired by the regulations in this part

VerDate 26<APR>99 10:09 Apr 28, 1999 Jkt 183099 PO 00000 Frm 00670 Fmt 8010 Sfmt 8010 Y:\SGML\183099T.XXX pfrm02 PsN: 183099T

675

Bureau of Alcohol, Tobacco and Firearms, Treasury § 53.61

to keep records in respect of a tax shallmaintain such records for at leastthree years after the due date of suchtax for the return period to which therecords relate, or the date such tax ispaid, whichever is later. The records ofclaimants required by paragraph (c) ofthis section shall be maintained for aperiod of at least three years after thedate the claim is filed.

(e) Reproduction of original records. (1)General books of account, such as cashbooks, journals, voucher registers,ledgers, etc., shall be maintained andpreserved in their original form. How-ever, reproductions of supportingrecords of details, such as invoices,vouchers, production reports, salesrecords, certificates, proofs of expor-tation, etc., may be kept in lieu of theoriginal records. Any process may beused which accurately and timely re-produces the original record, and whichforms a durable medium for reproduc-ing and preserving the original record.

(2) Copies of records treated as originalrecords. Whenever records are repro-duced under this section, the repro-duced records shall be preserved in con-veniently accessible files, and provi-sions shall be made for examining,viewing, and using the reproducedrecords the same as if they were theoriginal record. Such reproducedrecords shall be treated and consideredfor all purposes as though they werethe original record. All provisions oflaw and regulations applicable to theoriginal record are applicable to the re-produced record.

[T.D. ATF–365, 60 FR 33670, June 28, 1995]

Subparts D–F [Reserved]

Subpart G—Tax Rates

§ 53.61 Imposition and rates of tax.(a) Imposition of tax. Section 4181 of

the Code imposes a tax on the sale ofthe following articles by the manufac-turer, producer, or importer thereof:

(1) Pistols;(2) Revolvers;(3) Firearms (other than pistols and

revolvers); and(4) Shells and cartridges.(b) Parts or accessories—(1) In general.

No tax is imposed by section 4181 of the

Code on the sale of parts or accessoriesof firearms, pistols, revolvers, shells,and cartridges when sold separately orwhen sold with a complete firearm foruse as spare parts or accessories. Thetax does attach, however, to sales ofcompleted firearms, pistols, revolvers,shells, and cartridges, and to sale ofsuch articles that, although in knock-down condition, are complete as to allcomponent parts.

(2) Component parts. Component partsare items that would ordinarily be at-tached to a firearm during use and, inthe ordinary course of trade, are pack-aged with the firearm at the time ofsale by the manufacturer or importer.All component parts for firearms areincludible in the price for which the ar-ticle is sold.

(3) Nontaxable parts. Parts sold withfirearms that duplicate componentparts that are not includible in theprice for which the article is sold.

(4) Nontaxable accessories. Items thatare not designed to be attached to afirearm during use or that are not, inthe ordinary course of trade, providedwith the firearm at the time of the saleby the manufacturer or importer arenot includible in the price for whichthe article is sold.

(5) Examples—(i) In general. The fol-lowing examples are provided as guide-lines and are not meant to be all inclu-sive.

(ii) Component parts. Component partsinclude items such as a frame or re-ceiver, breech mechanism, triggermechanism, barrel, buttstock,forestock, handguard, grips, buttplate,fore end cap, trigger guard, sight or setof sights (iron or optical), sight mountor set of sight mounts, a choke, a flashhider, a muzzle brake, a magazine, aset of sling swivels, and/or an attach-able ramrod for muzzle loading fire-arms when provided by the manufac-turer or importer for use with the fire-arm in the ordinary course of commer-cial trade. Component parts also in-clude any part provided with the fire-arm that would affect the tax status ofthe firearm, such as an attachableshoulder stock.

(iii) Nontaxable parts. Nontaxableparts include items such as extra bar-rels, extra sights, optical sights andmounts (in addition to iron sights),

VerDate 26<APR>99 10:09 Apr 28, 1999 Jkt 183099 PO 00000 Frm 00671 Fmt 8010 Sfmt 8010 Y:\SGML\183099T.XXX pfrm02 PsN: 183099T

676

27 CFR Ch. I (4–1–99 Edition)§ 53.62

spare magazines, spare cylinders, extrachoke tubes, and spare pins.

(iv) Nontaxable accessories. Non-taxable accessories include items suchas cleaning equipment, slings, slip onrecoil pads (in addition to standardbuttplate), tools, gun cases for storageor transportation, separate items suchas knives, belt buckles, or medallions.Nontaxable accessories also include op-tional items purchased by the cus-tomer at the time of retail sale that donot change the tax classification of thefirearm, such as telescopic sights andmounts, recoil pads, slings, sling swiv-els, chokes, and flash hiders/muzzlebrakes of a type not provided by themanufacturer or importer of the fire-arm in the ordinary course of commer-cial trade.

(c) Rates of tax. Tax is imposed on thesale of the articles specified in section4181 of the Code at the rates indicatedbelow.

Percent

(1) Pistols ............................................................... 10(2) Revolvers ......................................................... 10(3) Firearms (other than pistols and revolvers) ..... 11(4) Shells and cartridges ....................................... 11

(d) Computation of tax. The tax iscomputed by applying to the price forwhich the article is sold the applicablerate. For definition of the term ‘‘price’’see section 4216 of the Code and theregulations contained in subpart J ofthis part.

(e) Liability for tax. The tax imposedby section 4181 of the Code is payableby the manufacturer, producer, or im-porter making the sale.

[T.D. ATF–308, 56 FR 303, Jan. 3, 1991, asamended by T.D. ATF–404, 63 FR 52603, Oct.1, 1998]

§ 53.62 Exemptions.(a) Firearms subject to the National

Firearms Act. Section 4182(a) providesthat the tax imposed by section 4181 ofthe Code shall not attach to the sale ofany firearms on which the tax imposedby section 5811 of the Code (relating totax on the transfer of machine guns,short-barreled firearms, and otherweapons) has been paid. Any manufac-turer, producer, or importer claimingsuch an exemption from the tax im-posed by section 4181 of the Code mustmaintain such records and be prepared

to produce such evidence as will estab-lish the right to the exemption.

(b) Sales to Defense Department or toU.S. Coast Guard—(1) Military depart-ment. Section 4182(b) of the Code pro-vides that the tax imposed by section4181 of the Code shall not attach to thesale of firearms, pistols, revolvers,shells, or cartridges that are purchasedwith funds appropriated for a militarydepartment of the United States. Forthis purpose, the term ‘‘military de-partment’’ means the Department ofthe Army, the Department of the Navy,and Department of the Air Force. In-cluded in the Department of the Navyare naval aviation and the MarineCorps.

(2) Coast Guard. Section 655, title 14,U.S.C., provides that no tax on the saleor transfer of firearms, pistols, revolv-ers, shells, or cartridges may be im-posed on such articles when boughtwith funds appropriated for the UnitedStates Coast Guard.

(3) Supporting evidence. Any manufac-turer, producer, or importer claimingan exemption from the tax imposed bysection 4181 of the Code by reason ofsection 4182(b) and section 655, title 14of the Code must maintain suchrecords and be prepared to producesuch evidence as will establish theright to the exemption. Generally,clearly identified orders or contracts ofa military department signed by an au-thorized officer of the military depart-ment will be sufficient to establish theright to the exemption. In the absenceof such orders or contracts, a state-ment, signed by an authorized officerof a military department or the CoastGuard, that the prescribed articleswere purchased with funds appro-priated for that military department orthe Coast Guard will constitute satis-factory evidence of the right to an ex-emption.

[T.D. ATF–308, 56 FR 303, Jan. 3, 1991, asamended by T.D. ATF–344, 58 FR 40354, July28, 1993]

§ 53.63 Other tax-free sales.

For provisions relating to tax-freesales of firearms and ammunition see:

(a) Section 4221 and 27 CFR 53.131,‘‘Tax-free sales; general rule’’.

VerDate 26<APR>99 10:09 Apr 28, 1999 Jkt 183099 PO 00000 Frm 00672 Fmt 8010 Sfmt 8010 Y:\SGML\183099T.XXX pfrm02 PsN: 183099T

677

Bureau of Alcohol, Tobacco and Firearms, Treasury § 53.91

(b) Section 4223 and 27 CFR 53.132,‘‘Tax-free sale of articles to be used for,or resold for, further manufacture’’.

(c) Section 4222 and 27 CFR 53.140,‘‘Registration’’.

Subparts H–I [Reserved]

Subpart J—Special Provisions Ap-plicable to ManufacturersTaxes

§ 53.91 Charges to be included in saleprice.

(a) In general. The ‘‘price’’ for whichan article is sold includes the totalconsideration paid for the article,whether that consideration is in theform of money, services, or otherthings. However, for purposes of thetaxes imposed under chapter 32 of theCode, certain collateral charges madein connection with the sale of a taxablearticle must be included in the taxablesale price, whereas others may be ex-cluded. Any charge which is requiredby a manufacturer, producer, or im-porter to be paid as a condition of itssale of a taxable article and which isnot attributable to an expense fallingwithin one of the exclusions providedin section 4216 of the Code or the regu-lations thereunder is includable in thetaxable sale price. It is immaterial forthis purpose that the charge may bepaid to a person other than the manu-facturer, producer, or importer, or thatit may be separately billed to the pur-chaser as a charge earmarked for ex-penses incurred or to be incurred in hisbehalf, such as charges for demonstra-tion or display of the article, for salespromotion programs, or otherwise.With respect to the rules relating toexclusion of charges for local adver-tising of a manufacturer’s products, seesection 4216(e) of the Code and § 53.100.In the case of sales on credit, a car-rying, finance, or service charge is ex-cludable from the sale price if it is rea-sonably related to the costs of carryingthe deferred portion of the sale price(such as interest on the deferred por-tion of the sale price, expenses of book-keeping necessary to keep the recordsof such sales, and expenses of cor-respondence and other communicationin connection with collection).

(b) Tools and dies. Separate chargesfor tools and dies used in the manufac-ture or production of a taxable articleare to be included, in whole or in part,in the sale price on which the tax isbased. It is immaterial whether thecharges for such items are billed in alump sum or are amortized or allocatedto each of the taxable articles. If, atthe termination of a contract to manu-facture taxable articles, the tools anddies used in production pass to the pur-chaser, only the amount of deprecia-tion of the tools and dies incurred inproduction, computed on a ‘‘productionoutput’’ basis, should be included inthe sale price. If the purchaser fur-nishes the tools and dies, the amountof the cost thereof, to the extent thatsuch cost has been depreciated in theproduction of the taxable articles(computed on a ‘‘production output’’basis), shall be included in determiningthe sale price of the articles for pur-poses of computing the tax.

(c) Charges for warranty. A charge fora warranty of an article which themanufacturer, producer, or importerrequires the purchaser to pay in orderto obtain the article shall be includedin the sale price of the article on whichthe tax is computed. On the otherhand, a charge for a warranty of a tax-able article paid at the purchaser’s op-tion shall not be included in the saleprice for purposes of computing taxthereon.

(d) Charges for coverings, containers,and packing. Any charge by the manu-facturer, producer, or importer for cov-erings and containers of whatever na-ture used to pack an article for ship-ment shall be included as part of thesale price for the purpose of computingthe tax, whether or not the charges areidentified as such on the invoice or arebilled separately. Even though there isan agreement that the manufacturer,producer, or importer will repay all ora portion of the charge for the cov-erings or containers upon the returnthereof, the full charge neverthelessshall be included in the sale price. It isimmaterial whether the charge madeat the time of sale is more or less thanthe actual value of the covering or con-tainer. See § 53.173(b)(4) for provisionsrelating to the claiming of a credit or

VerDate 26<APR>99 10:09 Apr 28, 1999 Jkt 183099 PO 00000 Frm 00673 Fmt 8010 Sfmt 8010 Y:\SGML\183099T.XXX pfrm02 PsN: 183099T

678

27 CFR Ch. I (4–1–99 Edition)§ 53.92

refund in the case of a price readjust-ment due to the return or repossessionof a covering or container. Packingcharges are to be included in the saleprice whether the charges cover normalpacking or special packing services,such as for extra protection of the arti-cle or for odd-lot quantities. This ruleshall apply whether the packing serv-ices are initiated by the manufacturer,producer, or importer or are furnishedat the request of the purchaser andwhether the packing is performed bythe manufacturer, producer, or im-porter or by another person at his re-quest. If the purchaser supplies pack-ing materials, the fair market value ofsuch materials must be included in thetax base when computing tax liabilityon the sale of the article.

(e) Taxable and nontaxable articles soldas a unit. Where a taxable article and anontaxable article are sold by the man-ufacturer as a unit, the tax attaches tothat portion of the manufacturer’s saleprice of the unit which is properly allo-cable to the taxable article. Normally,the taxable portion of such a unit maybe determined by applying to the man-ufacturer’s sale price of the unit theratio which the manufacturer’s sepa-rate sale price of the taxable articlebears to the sum of the sale prices ofboth the taxable and nontaxable arti-cles, if such articles are sold separatelyby the manufacturer. Where the arti-cles (or either one of them) are not soldseparately by the manufacturer and donot have established sale prices, thetaxable portion is to be determinedfrom a comparison of the actual costsof the articles to the manufacturer.Thus, if the cost of the taxable articlerepresents four-fifths of the total costof the complete unit, the tax applies tofour-fifths of the price charged by themanufacturer for the unit.

[T.D. ATF–308, 56 FR 303, Jan. 3, 1991, asamended by T.D. ATF–312, 56 FR 31083, July9, 1991]

§ 53.92 Exclusions from sale price.(a) Tax—(1) Tax not part of taxable sale

price. The tax imposed by chapter 32 ofthe Code on the sale of an article is notpart of the taxable sale price of the ar-ticle. Thus, if a manufacturer com-putes the tax on a sale price which isdetermined without regard to the tax,

and it charges the proper tax as a sepa-rate item, the amount of tax socharged does not become a part of thetaxable sale price and no tax is due onthe tax so charged. Where no separatecharge is made as tax, it will be pre-sumed that the price charged to thepurchaser for the article includes theproper tax, and the proper percentageof such price will be allocated to thetax.

(2) Computation of tax. If an articlesubject to tax at the rate of 10 percentis sold for $100 and an additional itemof $10 is billed as tax, $100 is the tax-able selling price and $10 is the amountof tax due thereon. However, if the ar-ticle is sold for $100 with no separatebilling or indication of the amount ofthe tax, it will be presumed that thetax is included in the $100, and a com-putation will be necessary to deter-mine what portion of the total amountrepresents the sale price of the articleand what portion represents the tax.The computation is as follows:

Taxablesale price =

sale price includ-ing tax

100 + rate of tax

Thus, if the tax rate is 10 percent andthe sale price including tax is $100, thetaxable sale price is $90.91 (that is, $100divided by (100+10)), and the tax is 10percent of $90.91, or $9.09.

(b) Transportation, delivery, insurance,or installation charges—(1) Charges in-curred pursuant to sale. Charges fortransportation, delivery, insurance, in-stallation, and other expenses actuallyincurred in connection with the deliv-ery of an article to a purchaser pursu-ant to a bona fide sale shall be ex-cluded from the sale price in com-puting the tax. Such charges includeall items of transportation, delivery,insurance, installation, and similar ex-pense incurred after shipment to a cus-tomer begins, in response to the cus-tomer’s order, pursuant to a bona fidesale. However, costs of such nature in-curred by a manufacturer, producer, orimporter in transporting, in the nor-mal course of business and for its ben-efit and convenience, articles from afactory or port of entry to a warehouse

VerDate 26<APR>99 10:09 Apr 28, 1999 Jkt 183099 PO 00000 Frm 00674 Fmt 8010 Sfmt 8010 Y:\SGML\183099T.XXX pfrm02 PsN: 183099T

679

Bureau of Alcohol, Tobacco and Firearms, Treasury § 53.92

or other facility (regardless of the loca-tion of such warehouse or facility) arenot considered as being incurred inconnection with the delivery of an arti-cle to a purchaser pursuant to a bonafide sale, and charges therefor cannotbe excluded from the sale price in com-puting tax liability. Similarly, an al-lowance granted by a manufacturer asreimbursement for expenses incurredby the purchaser in shipping used arti-cles to the manufacturer for creditagainst the purchase price of taxablearticles shall not be excluded from thesale price when computing tax due onthe sale of the taxable articles. In anyevent, no charge may be excluded fromthe sale price unless the conditions setforth in paragraph (b)(2) of this sectionare complied with. Said conditions areprescribed under the authority grantedthe Secretary in section 4216(a) of theCode.

(2) Only actual expenses to be excluded.Where a separate charge is made fortransportation or other expenses in-curred in connection with the deliveryof an article to the purchaser pursuantto a bona fide sale, there shall be ex-cluded in arriving at the sale price sub-ject to tax only that portion of thecharge which represents the actual ex-penses incurred for the transportationor other excludable expenses. Where aseparate charge is less than the actualexpense, the difference is presumed tobe included in the billed price. Suchdifference, together with the separatecharge, shall be excluded in arriving atthe sale price on which the tax is com-puted. Similarly, where no separatecharge is made but the manufacturer,producer, or importer incurs an ex-pense of the type to which this para-graph has application, the amount ofsuch expense actually incurred shall beexcluded from the sale price on whichthe tax is computed. Where transpor-tation expense is incurred in conjunc-tion with a shipment composed of bothtaxable and nontaxable articles, onlythe portion of the expense allocable tothe taxable articles shall be exclud-able. In general, unless the taxpayerestablishes to the satisfaction of theregional director that another methodreasonably apportions such freight ex-pense between taxable and nontaxablearticles, such expense should be appor-

tioned on the basis of the relativeweights (or, if available, the relativepublished tariff rates) applicable to thetaxable and nontaxable articles. Whereit is not feasible to apportion such ex-pense on the basis of relative weightsor tariff rates, the expense shall be ap-portioned on another reasonable basis;for example, in the case of a shipmentincluding both taxable and nontaxablearticles which are subject to the sametariff rate, it may be appropriate to ap-portion the transportation expense onthe basis of the relative sale prices. Acharge for insurance in connectionwith the delivery of an article to a pur-chaser is considered to represent an ex-pense actually incurred only to the ex-tent that an amount equivalent to suchcharge is paid or payable by the manu-facturer to a person authorized to as-sume such insurance risk.

(3) Transportation, delivery, or installa-tion services performed by manufacturer.For purposes of computing the taxablesale price of articles, it is immaterialwhether the transportation, delivery,or other services of the type to whichthis paragraph has application are per-formed by a common carrier or inde-pendent agency for or on behalf of themanufacturer, producer, or importer,or are performed by the manufacturer,producer, or importer with the use ofits own vehicles or other facilities.Thus, where a manufacturer, producer,or importer performs the transpor-tation, delivery, or other services withits equipment, tools, employees, etc.,the cost of such services allocable tothe sale of the taxable article shall beexcluded. In determining whether anexpense is an excludable transportationor delivery expense, only those ex-penses incurred by reason of the factthat the purchaser accepts delivery atsome point other than the manufactur-er’s place of business shall be consid-ered excludable transportation or de-livery expenses. All expenses incurredin placing an article packed, ready forshipment on the loading dock at themanufacturer’s factory are not exclud-able transportation or delivery ex-penses. An allowance granted by themanufacturer, producer, or importer tothe purchaser for transportation, deliv-ery, or other expenses incurred or to be

VerDate 26<APR>99 10:09 Apr 28, 1999 Jkt 183099 PO 00000 Frm 00675 Fmt 8010 Sfmt 8010 Y:\SGML\183099T.XXX pfrm02 PsN: 183099T

680

27 CFR Ch. I (4–1–99 Edition)§ 53.93

incurred by the purchaser in connec-tion with the sale shall be excluded incomputing the taxable sale price, ifcharges for similar expenses would beexcludable if incurred by the manufac-turer.

(4) Records in support of exclusion.Every manufacturer, producer, or im-porter making sales of taxable articlesshall keep records which will disclosethe amount of transportation, delivery,insurance, installation or other ex-pense actually incurred by it in con-nection with the delivery of a taxablearticle to a purchaser pursuant to abona fide sale.

(c) Other charges. A charge or expensenot within the scope of paragraph (a)or (b) of this section, whether or notseparately stated, may not be excludedin computing the taxable sale price un-less it can be shown by adequaterecords that the charge or expense isnot properly included as a manufac-turing or selling expense or is in noway incidental to placing the article incondition packed ready for shipment.Commissions to manufacturers’ agents,or allowances, payments, or adjust-ments made to, and for the benefit of,persons other than the purchaser maynot be excluded or deducted, under anycondition, in computing the sale priceupon which the tax is computed.

§ 53.93 Other items relating to tax onsale price.

(a) Exchanges. If, in connection withthe sale of an article subject to a taximposed under chapter 32 of the Codeon the price for which sold, a manufac-turer receives from its vendee anotherarticle in exchange, the tax on themanufacturer’s sale shall be computedon the basis of the amount allowed forthe article received from the vendee,plus any additional amount chargedthe vendee.

(b) Replacements under warranty. If anarticle, subject to a tax imposed underchapter 32 of the Code on the price forwhich sold, is returned to the manufac-turer by reason of the failure of the ar-ticle under a warranty as to its qualityor service, and a new article is given bythe manufacturer, free, or at a reducedprice, the tax on the new article shallbe computed on the actual amount, ifany, to be paid to the manufacturer for

the new article. See § 53.174(b) for thecircumstances under which the allow-ance made by the manufacturer, pro-ducer, or importer upon the return ofthe first article constitutes a price re-adjustment of the sale price of the firstarticle and the extent, if any, to whicha credit may be allowed, or refundmade, of the tax paid by the manufac-turer, producer, or importer on the saleof the first article.

(c) Readjustments in sale price. Read-justment in sale price (such as allow-able discounts, rebates, bonuses, etc.)cannot be anticipated. The tax must bebased upon the original price unlessthe readjustments have actually beenmade prior to the close of the periodfor which the tax upon the sale is re-turned. However, if the price uponwhich the tax was computed is subse-quently readjusted, credit may betaken against the tax due on a subse-quent return or a claim for refund filedas provided by section 6416(b)(1) of theCode and §§ 53.174–53.176.

[T.D. ATF–308, 56 FR 303, Jan. 3, 1991, asamended by T.D. ATF–344, 58 FR 40354, July28, 1993]

§ 53.94 Constructive sale price; scopeand application.

(a) In general. Section 4216(b) of theCode pertains to those taxes imposedunder chapter 32 of the Code that arebased on the price for which an articleis sold, and contains the provisions forconstructing a tax base other than theactual sale price of the article, undercertain defined conditions.

(b) Specific applications. (1) Section4216(b)(1) of the Code applies to:

(i) Arm’s-length sales at retail or onconsignment, other than those sales atretail and to retailers to which section4216(b)(2) of the Code and § 53.96 apply;and

(ii) Sales otherwise than at arm’slength, and at less than fair marketprice.

(2) Section 4216(b)(2) of the Code ap-plies generally to arm’s-length sales ofan article at retail or to retailers, orboth, where the manufacturer also sellsthe same article to wholesale distribu-tors.

(3) Section 4216(b)(3) of the Code pro-vides a formula for determining a con-structive sale price for sales of taxable

VerDate 26<APR>99 10:09 Apr 28, 1999 Jkt 183099 PO 00000 Frm 00676 Fmt 8010 Sfmt 8010 Y:\SGML\183099T.XXX pfrm02 PsN: 183099T

681

Bureau of Alcohol, Tobacco and Firearms, Treasury § 53.95

articles between members of an affili-ated group of corporations (as ‘‘affili-ated group’’ is defined in section 1504(a)of the Code) in those instances wherethe purchasing corporation regularlyresells to retailers but does not regu-larly resell to wholesale distributors,and except for situations where section4216(b)(4) of the Code applies.

(4) Section 4216(b)(4) of the Code pro-vides a special method for computing aconstructive sale price for sales of tax-able articles between affiliated cor-porations where the purchasing cor-poration sells only to retailers, and thenormal method of selling within the in-dustry is for manufacturers to sell towholesale distributors.

(c) Definitions. For purposes of sec-tion 4216(b) of the Code and §§ 53.94–53.97and unless otherwise indicated:

(1) Sale at retail. A ‘‘sale at retail,’’ ora ‘‘retail sale’’, is a sale of an article toa purchaser who intends to use or leasethe article rather than resell it. Thefact that articles are sold in wholesalelots, or at wholesale prices, will notchange the character of such sales as‘‘sales at retail’’ if the purchaser is notengaged in the business of resellingsuch articles, and acquires them forthe purpose of using them rather thanreselling them.

(2) Retail dealers. A ‘‘retail dealer’’, or‘‘retailer’’, is a person engaged in thebusiness of selling articles at retail.

(3) Wholesale distributor. The term‘‘wholesale distributor’’ means a per-son engaged in the business of sellingarticles to persons engaged in the busi-ness of reselling such articles.

§ 53.95 Constructive sale price; basicrules.

(a) In general. Section 4216(b)(1) of theCode sets forth the conditions that re-quire the Secretary to construct a saleprice on which to compute a tax im-posed under chapter 32 of the Code onthe price for which an article is sold.The section requires a constructivesale price to be established where ataxable article is:

(1) Sold at retail;(2) Sold while on consignment; or,(3) Sold otherwise than through an

arm’s-length transaction at less thanfair market price.

(b) Sales at retail. Section 4216(b)(1)(A)of the Code relates to the determina-tion of a constructive sale price forsales of taxable articles sold at arm’s-length and at retail. In the case of suchsales, the constructive sale price is thehighest price for which such articlesare sold to wholesale distributors, inthe ordinary course of trade, by manu-facturers or producers thereof, as de-termined by the Secretary. If the con-structive sale price is less than the ac-tual sale price, the constructive saleprice shall be used as the tax base. Ifthe constructive sale price is not lessthan the actual sale price, the actualsale price shall be considered as notless than fair market, and shall be usedas the tax base. In determining thehighest price for which articles are soldby manufacturers to wholesale dis-tributors, there must be taken intoconsideration the normal industrypractices with respect to inclusionsand exclusions under section 4216(a) ofthe Code. However, once a constructivesale price has been determined by theSecretary, no further adjustment ofsuch price shall be made. The provi-sions of section 4216(b)(1)(A) of theCode and this paragraph shall notapply in those instances where the pro-visions of section 4216(b)(2) of the Codeand § 53.96 apply.

(c) Sales on consignment. As in thecase of sales at retail, the constructivesale price for sales on consignmentshall be the price for which such arti-cles are sold, in the ordinary course fortrade, by manufacturers or producersthereof, as determined by the Sec-retary. For purposes of section4216(b)(1)(B) of the Code and this para-graph, an article is considered to besold on consignment if it is sold whileit is on consignment to a person whichhas the right to sell, and does sell, sucharticle in its own name, but never re-ceives title to the article from themanufacturer. Ordinarily, the con-structive sale price of an article soldon consignment is the net price re-ceived by the manufacturer from theconsignee. The provisions of section4216(b)(1)(B) of the Code and this para-graph shall not apply if the provisionsof section 4216(b)(2) of the Code and§ 53.96 apply.

VerDate 26<APR>99 10:09 Apr 28, 1999 Jkt 183099 PO 00000 Frm 00677 Fmt 8010 Sfmt 8010 Y:\SGML\183099T.XXX pfrm02 PsN: 183099T

682

27 CFR Ch. I (4–1–99 Edition)§ 53.96

(d) Sales not at arm’s-length. For pur-poses of section 4216(b)(1)(C) of theCode and this paragraph, a sale is con-sidered to be made under cir-cumstances otherwise than at ‘‘arm’s-length’’ if:

(1) One of the parties is controlled (inlaw or in fact) by the other, or there iscommon control, whether or not suchcontrol is actually exercised to influ-ence the sale price, or

(2) The sale is made pursuant to spe-cial arrangements between a manufac-turer and a purchaser.In case of an article sold otherwisethan at arm’s-length, and at less thanfair market price, the constructive saleprice shall be the price for which sucharticles are sold, in the ordinary courseof trade, by manufacturers or pro-ducers thereof, as determined by theSecretary. Once such a constructivesale price has been determined, no fur-ther adjustment of such price shall bemade. See sections 4216(b) (3) and (4) ofthe Code, and § 53.97, for specific meth-ods for determining constructive saleprices for intercompany sales undercertain defined conditions.

§ 53.96 Constructive sale price; specialrule for arm’s-length sales.

(a) In general. Section 4216(b)(2) of theCode provides a special rule underwhich a manufacturer shall determinea constructive sale price for this sale oftaxable articles at retail, and to retaildealers, under certain conditions. Therule is applicable where:

(1) The manufacturer regularly sellssuch articles at retail, or to retailers,or both, as the case may be,

(2) The manufacturer also regularlysells such articles to one or morewholesale distributors in arm’s-lengthtransactions, and the manufacturer es-tablishes that its prices in such casesare determined without regard to anybenefit to be derived under section4216(b)(2) of the Code, and

(3) The transactions are arm’s-lengthtransactions.

(4) A manufacturer meeting the fore-going requirements shall base its taxliability for sales at retail and sales toretailers on the lower of its actual saleprice or the highest price for which itsells the same articles under the sameconditions to wholesale distributors.

(b) Definitions. For purposes of sec-tion 4216(b)(2) of the Code and this sec-tion:

(1) Actual sale price. ‘‘Actual saleprice’’ means the actual selling pricefor an article determined in the samemanner as sale price is determined fora taxable sale. Accordingly, such pricemust reflect the inclusions and exclu-sions set forth in section 4216(a) of theCode, and any price adjustments de-scribed in section 6416(b)(1) of the Code.

(2) Highest price to wholesale distribu-tors. The ‘‘highest price’’ chargedwholesale distributors for an article bya manufacturer, producer, or importerthereof, is the highest price at whichthe manufacturer, producer, or im-porter sells the article to wholesaledistributors, determined without re-gard to quantity. Such price shall bedetermined in the same manner as saleprice is determined for a taxable salewith respect to the inclusions and ex-clusions under section 4216(a) of theCode; however, since the price is to bea ‘‘highest’’ price, no further adjust-ment may be made for price readjust-ments under section 6416(b)(1) of theCode.

(3) Regular sales. An article is consid-ered to be sold ‘‘regularly’’ at retail orto retailers if sales are made at retailor to retailers periodically andrecurringly as a regular part of theseller’s business. If a seller makes onlyisolated or casual sales of an article atretail or to retailers, it is not consid-ered to be selling ‘‘regularly’’ at retailor to retailers. Similarly, a manufac-turer is considered to be making reg-ular sales of an article to one or moredistributors if it sells the article to atleast one distributor periodically andrecurringly as a regular part of itsbusiness.

(4) Normal method of sales in industry.In the absence of a showing to the Di-rector of a more appropriate manner ofdetermining the normal method ofsales within an industry which is prac-tical in application, the normal meth-od of sales within an industry shall beregarded as not being at retail or to re-tailers, or both, if the industry dollarvolume of sales which are at retail orto retailers, or both, is less than halfthe total industry dollar volume ofsales at all levels of distribution by

VerDate 26<APR>99 10:09 Apr 28, 1999 Jkt 183099 PO 00000 Frm 00678 Fmt 8010 Sfmt 8010 Y:\SGML\183099T.XXX pfrm02 PsN: 183099T

683

Bureau of Alcohol, Tobacco and Firearms, Treasury § 53.97

manufacturers, producers, or import-ers, including sales to other manufac-turers, producers, or importers.

[T.D. ATF–308, 56 FR 303, Jan. 3, 1991, asamended by T.D. ATF–312, 56 FR 31083, July9, 1991]

§ 53.97 Constructive sale price; affili-ated corporations.

(a) In general. Sections 4216(b) (3) and(4) of the Code establish procedures fordetermining a constructive sale priceunder section 4216(b)(1)(C) of the Codefor sales between corporations that aremembers of the same ‘‘affiliatedgroup’’, as that term is defined in sec-tion 1504(a) of the Code.

(b) Sales to which section 4216(b)(3) ofthe Code applies. Section 4216(b)(3) ofthe Code provides a procedure for de-termining a constructive sale priceunder section 4216(b)(1)(C) of the Codein those instances where:

(1) A manufacturer, producer or im-porter regularly sells a taxable articleto a wholesale distributor which is amember of the same affiliated group asthe manufacturer, producers or im-porter, and

(2) The wholesale distributor regu-larly sells such article to one or moreindependent retailers, but does not reg-ularly sell to wholesale distributors.Under such circumstances the con-structive sale price for the article shallbe an amount equal to 90 percent of thelowest price for which the distributorregularly sells the article in arm’s-length transactions to such inde-pendent retailers. Once the construc-tive sale price has been determined, noadjustment shall be made for inclu-sions or exclusions under section4216(a) of the Code or price readjust-ments under section 6416(b)(1) of theCode. If both sections 4216(b)(3) and4216(b)(4) of the Code apply with re-spect to the sale of an article, the con-structive sale price for such articleshall be the lower of the prices com-puted under sections 4216(b)(3) and4216(b)(4).

(c) Sales to which section 4216(b)(4) ofthe Code applies. Section 4216(b)(4) ofthe Code provides a procedure for de-termining a constructive sale priceunder section 4216(b)(1)(C) of the Codein those instance where:

(1) A manufacturer, producer, or im-porter regularly sells (except for tax-free sales) a taxable article only to awholesale distributor which is a mem-ber of the same affiliated group as themanufacturer, producer, or importer,

(2) The distributor regularly sells (ex-cept for tax-free sales) such articleonly to retail dealers, and

(3) The normal method of sales forsuch articles within the industry is tosell such articles in arm’s-length trans-actions to wholesale distributors.

(4) Under section 4216(b)(4) of theCode, the constructive sale price ofsuch article shall be the median priceat which the distributor, at the time ofthe sale by the manufacturer, resellsthe article to retail dealers, reduced bya percentage of such price equal to thepercentage which:

(i) The difference between the medianprice for which comparable articles aresold to wholesale distributors, in theordinary course of trade, by manufac-turers of producers thereof, and themedian price at which such wholesaledistributors in arm’s-length trans-actions sell such comparable articlesto retailers, is of

(ii) The median price at which suchwholesale distributors in arm’s-lengthtransactions sell such comparable arti-cles to retailers.

(iii) For purposes of this paragraph,the ‘‘median price’’ for which an articleis sold at a particular level of distribu-tion is the price midway between thehighest and lowest prices charged vend-ees at the particular level of distribu-tion. Where only one price is chargedat a level of distribution, ‘‘medianprice’’ is equivalent to ‘‘actual price’’.All sale prices referred to in para-graphs (c) and (d) of this section areprices that must reflect the inclusionsand exclusions set forth in section4216(a) of the Code. However, once aconstructive sale price has been deter-mined under these paragraphs, no fur-ther adjustment of such price is al-lowed.

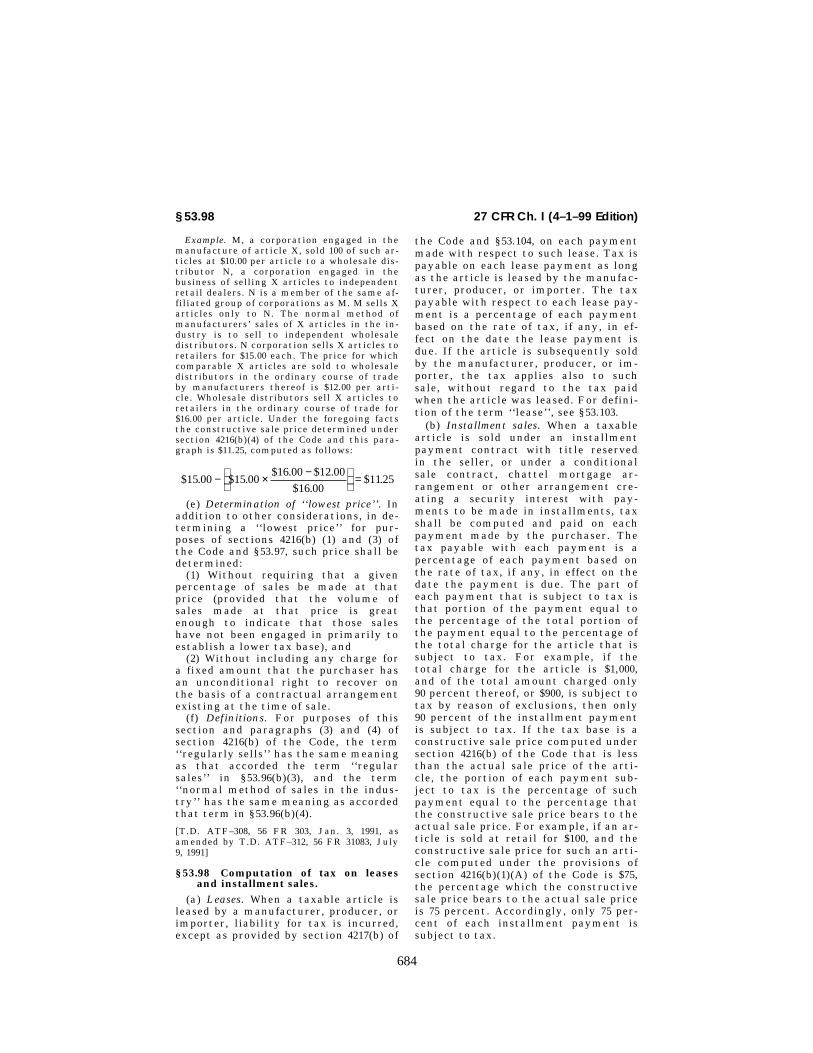

(d) Application of section 4216(b)(4) ofthe Code. The application of section4216(b)(4) of the Code and paragraph (c)of this section may be illustrated bythe following example:

VerDate 26<APR>99 10:09 Apr 28, 1999 Jkt 183099 PO 00000 Frm 00679 Fmt 8010 Sfmt 8010 Y:\SGML\183099T.XXX pfrm02 PsN: 183099T

684

27 CFR Ch. I (4–1–99 Edition)§ 53.98

Example. M, a corporation engaged in themanufacture of article X, sold 100 of such ar-ticles at $10.00 per article to a wholesale dis-tributor N, a corporation engaged in thebusiness of selling X articles to independentretail dealers. N is a member of the same af-filiated group of corporations as M. M sells Xarticles only to N. The normal method ofmanufacturers’ sales of X articles in the in-dustry is to sell to independent wholesaledistributors. N corporation sells X articles toretailers for $15.00 each. The price for whichcomparable X articles are sold to wholesaledistributors in the ordinary course of tradeby manufacturers thereof is $12.00 per arti-cle. Wholesale distributors sell X articles toretailers in the ordinary course of trade for$16.00 per article. Under the foregoing factsthe constructive sale price determined undersection 4216(b)(4) of the Code and this para-graph is $11.25, computed as follows:

$15. $15.$16. $12.

$16.$11.00 00

00 00

0025− × −

=

(e) Determination of ‘‘lowest price’’. Inaddition to other considerations, in de-termining a ‘‘lowest price’’ for pur-poses of sections 4216(b) (1) and (3) ofthe Code and § 53.97, such price shall bedetermined:

(1) Without requiring that a givenpercentage of sales be made at thatprice (provided that the volume ofsales made at that price is greatenough to indicate that those saleshave not been engaged in primarily toestablish a lower tax base), and

(2) Without including any charge fora fixed amount that the purchaser hasan unconditional right to recover onthe basis of a contractual arrangementexisting at the time of sale.

(f) Definitions. For purposes of thissection and paragraphs (3) and (4) ofsection 4216(b) of the Code, the term‘‘regularly sells’’ has the same meaningas that accorded the term ‘‘regularsales’’ in § 53.96(b)(3), and the term‘‘normal method of sales in the indus-try’’ has the same meaning as accordedthat term in § 53.96(b)(4).

[T.D. ATF–308, 56 FR 303, Jan. 3, 1991, asamended by T.D. ATF–312, 56 FR 31083, July9, 1991]

§ 53.98 Computation of tax on leasesand installment sales.

(a) Leases. When a taxable article isleased by a manufacturer, producer, orimporter, liability for tax is incurred,except as provided by section 4217(b) of

the Code and § 53.104, on each paymentmade with respect to such lease. Tax ispayable on each lease payment as longas the article is leased by the manufac-turer, producer, or importer. The taxpayable with respect to each lease pay-ment is a percentage of each paymentbased on the rate of tax, if any, in ef-fect on the date the lease payment isdue. If the article is subsequently soldby the manufacturer, producer, or im-porter, the tax applies also to suchsale, without regard to the tax paidwhen the article was leased. For defini-tion of the term ‘‘lease’’, see § 53.103.

(b) Installment sales. When a taxablearticle is sold under an installmentpayment contract with title reservedin the seller, or under a conditionalsale contract, chattel mortgage ar-rangement or other arrangement cre-ating a security interest with pay-ments to be made in installments, taxshall be computed and paid on eachpayment made by the purchaser. Thetax payable with each payment is apercentage of each payment based onthe rate of tax, if any, in effect on thedate the payment is due. The part ofeach payment that is subject to tax isthat portion of the payment equal tothe percentage of the total portion ofthe payment equal to the percentage ofthe total charge for the article that issubject to tax. For example, if thetotal charge for the article is $1,000,and of the total amount charged only90 percent thereof, or $900, is subject totax by reason of exclusions, then only90 percent of the installment paymentis subject to tax. If the tax base is aconstructive sale price computed undersection 4216(b) of the Code that is lessthan the actual sale price of the arti-cle, the portion of each payment sub-ject to tax is the percentage of suchpayment equal to the percentage thatthe constructive sale price bears to theactual sale price. For example, if an ar-ticle is sold at retail for $100, and theconstructive sale price for such an arti-cle computed under the provisions ofsection 4216(b)(1)(A) of the Code is $75,the percentage which the constructivesale price bears to the actual sale priceis 75 percent. Accordingly, only 75 per-cent of each installment payment issubject to tax.

VerDate 26<APR>99 10:09 Apr 28, 1999 Jkt 183099 PO 00000 Frm 00680 Fmt 8010 Sfmt 8010 Y:\SGML\183099T.XXX pfrm02 PsN: 183099T

685

Bureau of Alcohol, Tobacco and Firearms, Treasury § 53.100

(c) Sales on credit. Where articles aresold on credit under conditions otherthan those specified in paragraph (b) ofthis section, the entire tax shall be re-ported and paid with the return cov-ering the period in which the sale ismade, even though the price may notbe paid to the manufacturer, producer,or importer until a later date, or notpaid at all.

§ 53.99 Sales of installment accounts.

(a) In general. Except as provided inparagraph (d) of this section, in case ofa sale or other disposition by a manu-facturer, producer, or importer of aninstallment account of the type speci-fied in section 4216(c) of the Code, thetax shall not apply to subsequent in-stallment payments on such account.Instead, there shall be paid an amountequal to the difference between the taxpreviously paid on such installment ac-count and the total tax computed byapplying:

(1) To each installment due beforethe sale of the installment account, therate of tax applicable at the time pay-ment thereof was due, and

(2) To each installment, the time forpayment of which has not arrived, therate of tax which, under the provisionsof chapter 32 of the Code as in effect onthe date of the sale of the installmentaccount, is (or is to be) in effect on thedate such installment is due. However,see paragraph (b) of this section if thesale is made in a bankruptcy or insol-vency proceeding. The tax due underthis paragraph shall be included in thereturn for the period in which the ac-count is sold.

(b) Sale in bankruptcy or insolvencyproceeding. In the case of a sale of aninstallment account of a manufacturer,producer, or importer pursuant to theorder of, or subject to the approval of,a court of competent jurisdiction in abankruptcy or insolvency proceeding,the amount of tax due shall be com-puted and paid as provided in para-graph (a) of this section but shall notexceed the amount of tax computed bymultiplying:

(1) The proportionate share of theamount for which such accounts aresold which is allocable to each unpaidinstallment payment, by

(2) The rate of tax which, under theprovisions of chapter 32 of the Code asin effect on the date of the sale of theinstallment account, is (or is to be) ineffect on the date such payment is due.

(c) Collection of installment accounts onbehalf of the manufacturer. Where amanufacturer, producer, or importerretains title to an installment accountbut turns it over to another person forcollection on a fee basis, no sale ofsuch account (or other disposition ascontemplated in section 4216(d) of theCode) has been made. The tax shallcontinue to be paid as provided by sec-tion 4216(c) of the Code.

(d) Returned installment accounts.Where an installment account whichhas been sold or otherwise disposed ofis returned to the manufacturer, pro-ducer, or importer who sold it under anagreement under which the accountwas sold, and credit or refund has beenallowed under section 6416(b)(5) of theCode and § 53.183, the manufacturer,producer, or importer shall pay tax asprovided by section 4216(c) of the Codeand § 53.98 on any subsequent paymentsmade on such returned installment ac-count until such time as there shallhave been paid the total tax liabilitywith respect to the account as com-puted under paragraph (a) of this sec-tion.

(e) Limitation. The sum of theamounts payable under this sectionand § 53.98 or an installment accountshall not exceed the total amount oftax which would be payable if such in-stallment account had not been sold orotherwise disposed of (computed as pro-vided in subsection (c)).

§ 53.100 Exclusion of local advertisingcharges from sale price.

(a) In general. Section 4216(e) of theCode deals with the treatment to be ac-corded charges made by a manufac-turer for, and reimbursements by amanufacturer or expenditures in con-nection with the advertising of certainarticles subject to excise tax underchapter 32 of the Code. Section 4216(e)of the Code provides an exclusion(which is in addition to the exclusionsprovided by section 4216(a) of the Codeand § 53.92) in respect of charges forlocal advertising, as defined in para-graph (b) of this section, for purposes

VerDate 26<APR>99 10:09 Apr 28, 1999 Jkt 183099 PO 00000 Frm 00681 Fmt 8010 Sfmt 8010 Y:\SGML\183099T.XXX pfrm02 PsN: 183099T

686

27 CFR Ch. I (4–1–99 Edition)§ 53.100

of determining the price for which anarticle is sold. See paragraph (c) of thissection. The exclusion provided by sec-tion 4216(e) of the Code and paragraph(c) of this section has application onlyif the advertising is broadcast over aradio or television station, appears in anewspaper or magazine, or is displayedby means of an outdoor advertisingsign or poster. Section 4216(e) of theCode also provides an overall limita-tion in respect of the sum of theamount of the exclusions from price ascharges for local advertising and theamount of the readjustments author-ized under section 6416(b)(1) of the Code(relating to credits or refunds for pricereadjustments) in respect of reimburse-ments by a manufacturer of expendi-tures for local advertising. See § 53.101.For provisions prohibiting exclusionfrom price or readjustment of price inrespect of charges for, and reimburse-ments of expenditures for, advertisingother than local advertising, see§ 53.102.

(b) Definition of local advertising—(1)In general. For purposes of the regula-tions under sections 4216(e) and6416(b)(1) of the Code (§§ 53.100–53.102and 53.173–53.176), the term ‘‘local ad-vertising’’ means advertising which re-lates to an article with respect towhich tax is imposed under chapter 32of the Code on the price for which soldand which:

(i) Is initiated or obtained by the pur-chaser or any subsequent vendee,

(ii) Names the article for which theprice is determinable under section 4216and states the location at which sucharticle may be purchased at retail, and

(iii) Is broadcast over a radio stationor television station, appears in anewspaper or magazine, or is displayedby means of an outdoor advertisingsign or poster.

(2) Initiating or obtaining advertising.For purposes of paragraph (b)(1) of thissection, the advertising must be initi-ated or obtained by one or more of thepersons in the chain of distribution ofthe article (wholesale distributor, job-ber, dealer, etc.) who purchased the ar-ticle for resale. For purposes of thissubparagraph, the manufacturer is notconsidered to be one of the persons inthe chain of distribution of the article.In general, advertising of an article is

considered to be initiated or obtainedby one or more persons in the chain ofdistribution of the article if any suchperson:

(i) Takes an active part in the actualplanning and development, or in the ar-rangements or negotiations leading tothe development, of the form and con-tent of the advertising, or

(ii) Contracts for the placement ofthe advertising.The participation by the manufacturerof the article in the planning, develop-ment, or placement of the advertisingis immaterial provided the advertisingis in fact initiated or obtained by oneor more persons in the chain of dis-tribution of the article. Furthermore,it is immaterial whether or not the ad-vertising is subject to the approval ofthe manufacturer of the article. How-ever, if no person in the chain of dis-tribution of the article takes an activepart in the actual planning and devel-opment, or in the arrangements or ne-gotiations leading to the development,of the form and content of the adver-tising, but, rather, all such planning,development, arrangements, and nego-tiations are accomplished by the manu-facturer of the article, then such man-ufacturer is considered to have initi-ated the advertising, and if he also con-tracts for the placement of the adver-tising, such advertising does not qual-ify as ‘‘local advertising’’.

(3) Identification of article and sales lo-cation. To meet the requirements ofparagraph (b)(1) of this section, the ad-vertising must identify the article forwhich the price is determinable undersection 4216 of the Code and give the lo-cation or locations at which the articlemay be purchased at retail. All prod-ucts taxable at the same rate under thesame section of chapter 32 of the Codeshall be considered to be an ‘‘article’’for purposes of the preceding sentence.No specific method or means of identi-fication is prescribed. The identifica-tion of the article may be madethrough the use of the name of themanufacturer or the use of an estab-lished trade-mark, such as a seal, pic-ture, letter or letters, etc., or a com-bination thereof. The advertising mustidentify the particular retail establish-ment or establishments at which thearticle may be purchased at retail but

VerDate 26<APR>99 10:09 Apr 28, 1999 Jkt 183099 PO 00000 Frm 00682 Fmt 8010 Sfmt 8010 Y:\SGML\183099T.XXX pfrm02 PsN: 183099T

687

Bureau of Alcohol, Tobacco and Firearms, Treasury § 53.100

need not specify the location of anysuch establishment in terms of thenumber by which the premises are des-ignated or the name of the street onwhich the retail premises are situated.However, the location of the retailpremises must be described suffi-ciently, as, for example, by referenceto a particular named shopping area orshopping center, to enable customersto find the retail establishment.

(4) Determination of costs of local ad-vertising. Where an advertisement iden-tifies more than one article, and allsuch articles are not taxable, or arenot taxable at the same rate under thesame section of chapter 32 of the Code,a reasonable allocation of the cost ofthe advertisement must be madeamong:

(i) Articles taxable at the same rateunder the same section of the Code,and