taxation one complete

TRANSCRIPT

8/12/2019 Taxation One Complete

http://slidepdf.com/reader/full/taxation-one-complete 1/90

+amdg

Taxation One: Outline with Codals

Mickey Ingles2A (2C) Ateneo Law 2012Atty. Montero (Updated: December 14, 2011 – Mickey)

1

Course OutlineTax I

A. In GeneralTaxable Income

The essential difference between capital and income is that capital is a fund; and

income is a flow. Capital is wealth, while income is the service of wealth. Property is a tree, income is the fruit. Labor is a tree, income is the fruit. Capital is a

tree, income the fruit.

Income means profits or gains. (Madrigal v Rafferty)

Income may be defined as the amount of money coming to a person or corporationwithin a specified time, whether as payment for services, interest or profit frominvestment.

o A mere advance in the value of property of a person or a corporation in nosense constitutes the ‘income’ specified in the law. Such advance constitutes

and can be treated merely as an increase in capital. (Fisher v Trinidad)

Cash dividends is taxed as income because it has been realized/received, while stock

dividends is not taxed as income because it is merely inchoate as it is a mereanticipation of income (it becomes income once you sell it).

o

One is an actual receipt of profits; the other is a receipt of a representation ofthe increased value of the assets of a corporation. (Fisher v Trinidad)

When dealing with money or property, the questions you should ask are:

o Is this capital or is this income? o Has it been realized/received or is it merely inchoate?

B. General Principles

SEC. 23. General Principles of Income Taxation in the Philippines. - Except when otherwise provided in this Code:

(A) A citizen of the Philippines residing therein is taxable on all income derived from sources within and without thePhilippines;(B) A nonresident citizen is taxable only on income derived from sources within the Philippines;(C) An individual citizen of the Philippines who is working and deriving income from abroad as an overseas contract

worker is taxable only on income derived from sources within the Philippines: Provided, That a seaman who is acitizen of the Philippines and who receives compensation for services rendered abroad as a member of thecomplement of a vessel engaged exclusively in international trade shall be treated as an overseas contract worker;(D) An alien individual, whether a resident or not of the Philippines, is taxable only on income derived from sourceswithin the Philippines;(E) A domestic corporation is taxable on all income derived from sources within and without the Philippines; and(F) A foreign corporation, whether engaged or not in trade or business in the Philippines, is taxable only on incomederived from sources within the Philippines.

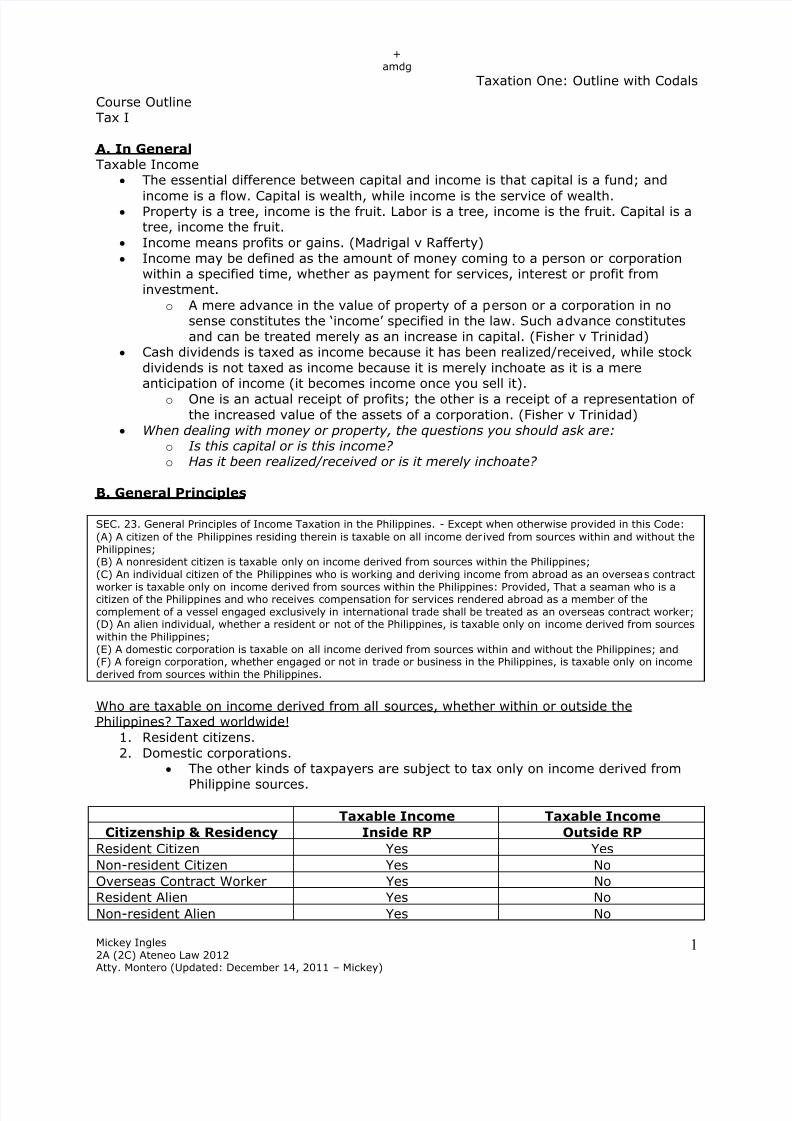

Who are taxable on income derived from all sources, whether within or outside thePhilippines? Taxed worldwide!

1. Resident citizens.

2. Domestic corporations.

The other kinds of taxpayers are subject to tax only on income derived from

Philippine sources.

Taxable Income Taxable Income

Citizenship & Residency Inside RP Outside RP

Resident Citizen Yes Yes

Non-resident Citizen Yes No

Overseas Contract Worker Yes No

Resident Alien Yes No

Non-resident Alien Yes No

8/12/2019 Taxation One Complete

http://slidepdf.com/reader/full/taxation-one-complete 2/90

+amdg

Taxation One: Outline with Codals

Mickey Ingles2A (2C) Ateneo Law 2012Atty. Montero (Updated: December 14, 2011 – Mickey)

2

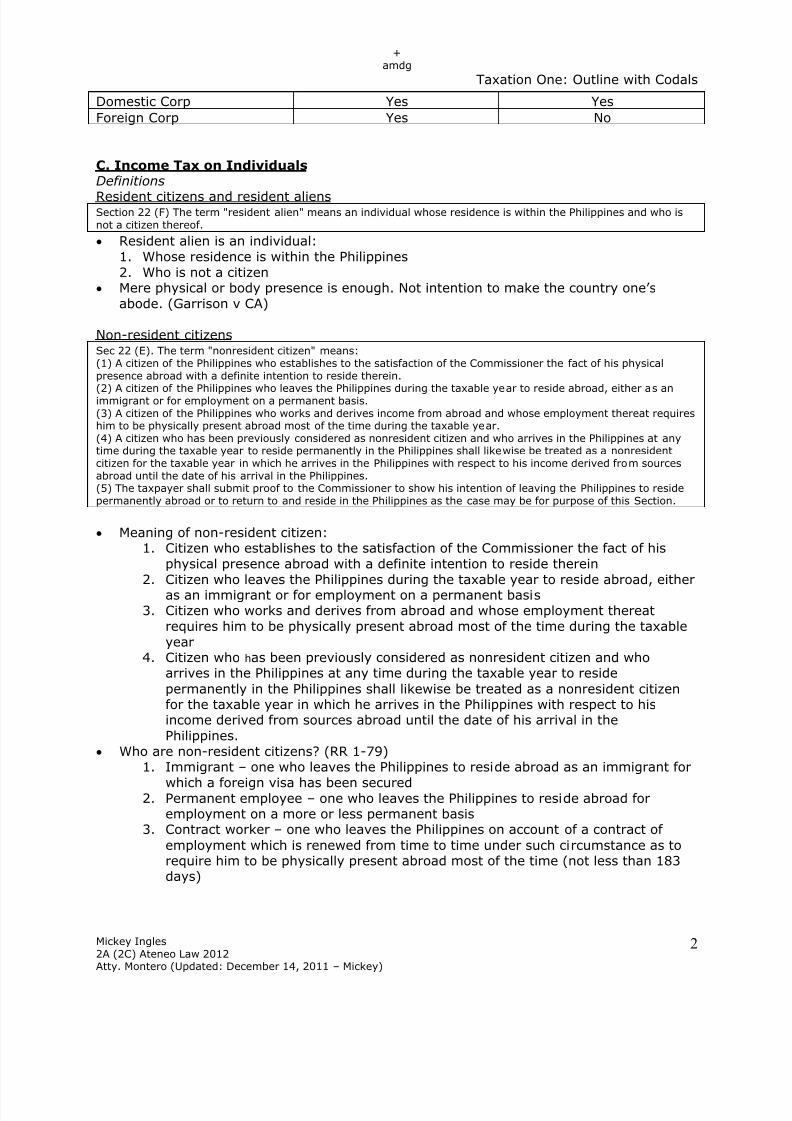

Domestic Corp Yes Yes

Foreign Corp Yes No

C. Income Tax on IndividualsDefinitions

Resident citizens and resident aliensSection 22 (F) The term "resident alien" means an individual whose residence is within the Philippines and who isnot a citizen thereof.

Resident alien is an individual:

1. Whose residence is within the Philippines

2. Who is not a citizen

Mere physical or body presence is enough. Not intention to make the country one’s

abode. (Garrison v CA)

Non-resident citizensSec 22 (E). The term "nonresident citizen" means:(1) A citizen of the Philippines who establishes to the satisfaction of the Commissioner the fact of his physicalpresence abroad with a definite intention to reside therein.

(2) A citizen of the Philippines who leaves the Philippines during the taxable year to reside abroad, either as animmigrant or for employment on a permanent basis.(3) A citizen of the Philippines who works and derives income from abroad and whose employment thereat requireshim to be physically present abroad most of the time during the taxable year.(4) A citizen who has been previously considered as nonresident citizen and who arrives in the Philippines at anytime during the taxable year to reside permanently in the Philippines shall likewise be treated as a nonresidentcitizen for the taxable year in which he arrives in the Philippines with respect to his income derived from sourcesabroad until the date of his arrival in the Philippines.(5) The taxpayer shall submit proof to the Commissioner to show his intention of leaving the Philippines to residepermanently abroad or to return to and reside in the Philippines as the case may be for purpose of this Section.

Meaning of non-resident citizen:1. Citizen who establishes to the satisfaction of the Commissioner the fact of his

physical presence abroad with a definite intention to reside therein

2. Citizen who leaves the Philippines during the taxable year to reside abroad, eitheras an immigrant or for employment on a permanent basis

3. Citizen who works and derives from abroad and whose employment thereat

requires him to be physically present abroad most of the time during the taxable

year4. Citizen who has been previously considered as nonresident citizen and who

arrives in the Philippines at any time during the taxable year to reside

permanently in the Philippines shall likewise be treated as a nonresident citizenfor the taxable year in which he arrives in the Philippines with respect to hisincome derived from sources abroad until the date of his arrival in the

Philippines.

Who are non-resident citizens? (RR 1-79)1. Immigrant – one who leaves the Philippines to reside abroad as an immigrant for

which a foreign visa has been secured2. Permanent employee – one who leaves the Philippines to reside abroad for

employment on a more or less permanent basis3. Contract worker – one who leaves the Philippines on account of a contract of

employment which is renewed from time to time under such circumstance as torequire him to be physically present abroad most of the time (not less than 183days)

8/12/2019 Taxation One Complete

http://slidepdf.com/reader/full/taxation-one-complete 3/90

+amdg

Taxation One: Outline with Codals

Mickey Ingles2A (2C) Ateneo Law 2012Atty. Montero (Updated: December 14, 2011 – Mickey)

3

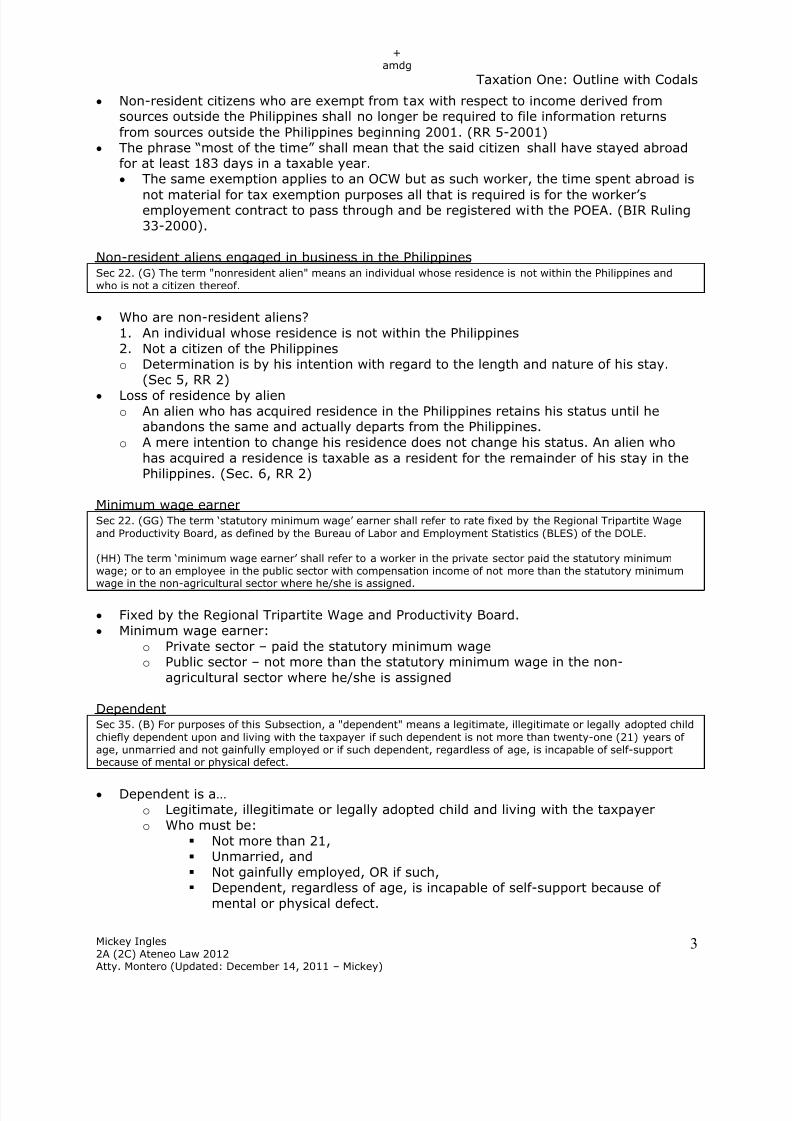

Non-resident citizens who are exempt from tax with respect to income derived fromsources outside the Philippines shall no longer be required to file information returns

from sources outside the Philippines beginning 2001. (RR 5-2001)

The phrase “most of the time” shall mean that the said citizen shall have stayed abroadfor at least 183 days in a taxable year.

The same exemption applies to an OCW but as such worker, the time spent abroad is

not material for tax exemption purposes all that is required is for the worker’semployement contract to pass through and be registered with the POEA. (BIR Ruling33-2000).

Non-resident aliens engaged in business in the PhilippinesSec 22. (G) The term "nonresident alien" means an individual whose residence is not within the Philippines andwho is not a citizen thereof.

Who are non-resident aliens?

1. An individual whose residence is not within the Philippines

2. Not a citizen of the Philippineso Determination is by his intention with regard to the length and nature of his stay.

(Sec 5, RR 2)

Loss of residence by alieno An alien who has acquired residence in the Philippines retains his status until he

abandons the same and actually departs from the Philippines.

o A mere intention to change his residence does not change his status. An alien who

has acquired a residence is taxable as a resident for the remainder of his stay in thePhilippines. (Sec. 6, RR 2)

Minimum wage earnerSec 22. (GG) The term ‘statutory minimum wage’ earner shall refer to rate fixed by the Regional Tripartite Wage

and Productivity Board, as defined by the Bureau of Labor and Employment Statistics (BLES) of the DOLE.

(HH) The term ‘minimum wage earner’ shall refer to a worker in the private sector paid the statutory minimumwage; or to an employee in the public sector with compensation income of not more than the statutory minimumwage in the non-agricultural sector where he/she is assigned.

Fixed by the Regional Tripartite Wage and Productivity Board.

Minimum wage earner:

o Private sector – paid the statutory minimum wageo Public sector – not more than the statutory minimum wage in the non-

agricultural sector where he/she is assigned

DependentSec 35. (B) For purposes of this Subsection, a "dependent" means a legitimate, illegitimate or legally adopted child

chiefly dependent upon and living with the taxpayer if such dependent is not more than twenty-one (21) years ofage, unmarried and not gainfully employed or if such dependent, regardless of age, is incapable of self-supportbecause of mental or physical defect.

Dependent is a…

o Legitimate, illegitimate or legally adopted child and living with the taxpayer

o Who must be:

Not more than 21,

Unmarried, and

Not gainfully employed, OR if such, Dependent, regardless of age, is incapable of self-support because of

mental or physical defect.

8/12/2019 Taxation One Complete

http://slidepdf.com/reader/full/taxation-one-complete 4/90

+amdg

Taxation One: Outline with Codals

Mickey Ingles2A (2C) Ateneo Law 2012Atty. Montero (Updated: December 14, 2011 – Mickey)

4

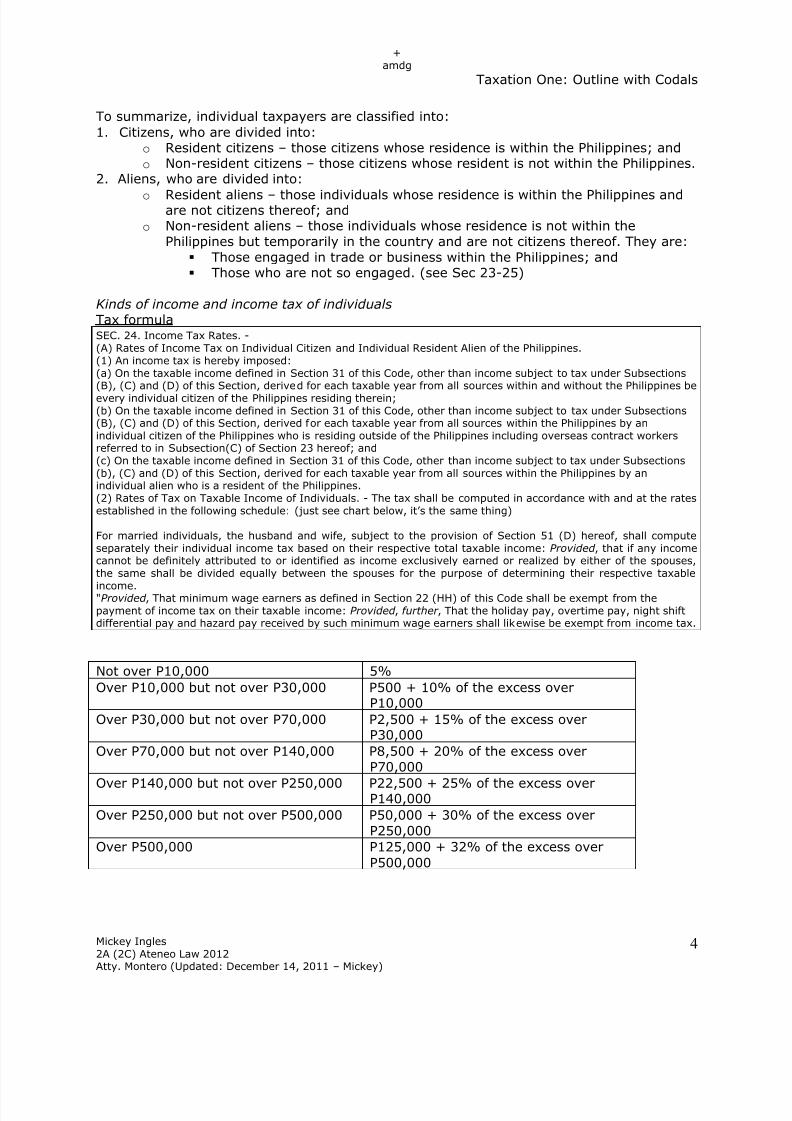

To summarize, individual taxpayers are classified into:

1. Citizens, who are divided into:o Resident citizens – those citizens whose residence is within the Philippines; and

o Non-resident citizens – those citizens whose resident is not within the Philippines.2. Aliens, who are divided into:

o

Resident aliens – those individuals whose residence is within the Philippines andare not citizens thereof; and

o Non-resident aliens – those individuals whose residence is not within the

Philippines but temporarily in the country and are not citizens thereof. They are:

Those engaged in trade or business within the Philippines; and

Those who are not so engaged. (see Sec 23-25)

Kinds of income and income tax of individualsTax formulaSEC. 24. Income Tax Rates. -(A) Rates of Income Tax on Individual Citizen and Individual Resident Alien of the Philippines.(1) An income tax is hereby imposed:(a) On the taxable income defined in Section 31 of this Code, other than income subject to tax under Subsections(B), (C) and (D) of this Section, derived for each taxable year from all sources within and without the Philippines beevery individual citizen of the Philippines residing therein;(b) On the taxable income defined in Section 31 of this Code, other than income subject to tax under Subsections(B), (C) and (D) of this Section, derived for each taxable year from all sources within the Philippines by anindividual citizen of the Philippines who is residing outside of the Philippines including overseas contract workersreferred to in Subsection(C) of Section 23 hereof; and(c) On the taxable income defined in Section 31 of this Code, other than income subject to tax under Subsections(b), (C) and (D) of this Section, derived for each taxable year from all sources within the Philippines by anindividual alien who is a resident of the Philippines.(2) Rates of Tax on Taxable Income of Individuals. - The tax shall be computed in accordance with and at the ratesestablished in the following schedule: (just see chart below, it’s the same thing)

For married individuals, the husband and wife, subject to the provision of Section 51 (D) hereof, shall computeseparately their individual income tax based on their respective total taxable income: Provided , that if any incomecannot be definitely attributed to or identified as income exclusively earned or realized by either of the spouses,the same shall be divided equally between the spouses for the purpose of determining their respective taxable

income."Provided , That minimum wage earners as defined in Section 22 (HH) of this Code shall be exempt from thepayment of income tax on their taxable income: Provided , further , That the holiday pay, overtime pay, night shiftdifferential pay and hazard pay received by such minimum wage earners shall likewise be exempt from income tax.

Not over P10,000 5%

Over P10,000 but not over P30,000 P500 + 10% of the excess overP10,000

Over P30,000 but not over P70,000 P2,500 + 15% of the excess overP30,000

Over P70,000 but not over P140,000 P8,500 + 20% of the excess over

P70,000

Over P140,000 but not over P250,000 P22,500 + 25% of the excess overP140,000

Over P250,000 but not over P500,000 P50,000 + 30% of the excess over

P250,000

Over P500,000 P125,000 + 32% of the excess over

P500,000

8/12/2019 Taxation One Complete

http://slidepdf.com/reader/full/taxation-one-complete 5/90

+amdg

Taxation One: Outline with Codals

Mickey Ingles2A (2C) Ateneo Law 2012Atty. Montero (Updated: December 14, 2011 – Mickey)

5

Gross IncomeLess: Deductions

Taxable IncomeTax RateTax Due

Know the tax base and the tax rate!

Only resident citizens and domestic corporations are taxed on income derived from

abroad. Worldwide taxable!

The tax is imposed upon taxable compensation or employment income, businessincome, and income derived from the practice of professions derived by citizens andresident aliens.

Married individuals shall compute separately their individual income tax based on theirrespective total taxable income.

o If any income cannot be definitely attributed to, or identified as incomeexclusively earned or realized by either of the spouses, the same shall be divided

equally between them for the purpose of determining their respective taxableincome.

Minimum wage earners are exempt from the payment of income tax on their taxableincome. Holiday pay, overtime pay, night shift differential pay, and hazard pay receivedby them are likewise exempt from income tax.

A non-resident alien individual engaged in trade or business in the Philippines is subjectto the income tax in the same manner as an individual citizen and a resident alien on

taxable income received from sources within the Philippines.

For non-resident aliens not so engaged, the tax is

o 25% of the entire or gross income received from sources within the Philippinesand

o 15% of the gross income received as compensation, salaries, and other

emoluments by reason of his employment by: regional or area headquarters and regional operating headquarters of

multinational corporations; offshore banking units established by a foreign corporation in the

Philippines; or by foreign petroleum service contractor or subcontractors operating in the

Philippines. (Sec 25 (A-E))

Final income tax – interests, royalties, awards, dividends, capital gains on sale of shares,

realtySec 24. (B) Rate of Tax on Certain Passive Income.(1) Interests, Royalties, Prizes, and Other Winnings. - A final tax at the rate of twenty percent (20%) is herebyimposed upon the amount of interest from any currency bank deposit and yield or any other monetary benefit fromdeposit substitutes and from trust funds and similar arrangements; royalties, except on books, as well as otherliterary works and musical compositions, which shall be imposed a final tax of ten percent (10%); prizes (exceptprizes amounting to Ten thousand pesos (P10,000) or less which shall be subject to tax under Subsection (A) of

Section 24; and other winnings (except Philippine Charity Sweepstakes and Lotto winnings), derived from sourceswithin the Philippines: Provided, however, That interest income received by an individual taxpayer (except a

nonresident individual) from a depository bank under the expanded foreign currency deposit system shall besubject to a final income tax at the rate of seven and one-half percent (7 1/2%) of such interest income: Provided,further, That interest income from long-term deposit or investment in the form of savings, common or individualtrust funds, deposit substitutes, investment management accounts and other investments evidenced by certificatesin such form prescribed by the Bangko Sentral ng Pilipinas (BSP) shall be exempt from the tax imposed under thisSubsection: Provided, finally, That should the holder of the certificate pre-terminate the deposit or investmentbefore the fifth (5th) year, a final tax shall be imposed on the entire income and shall be deducted and withheld bythe depository bank from the proceeds of the long-term deposit or investment certificate based on the remainingmaturity thereof:

8/12/2019 Taxation One Complete

http://slidepdf.com/reader/full/taxation-one-complete 6/90

+amdg

Taxation One: Outline with Codals

Mickey Ingles2A (2C) Ateneo Law 2012Atty. Montero (Updated: December 14, 2011 – Mickey)

6

Four (4) years to less than five (5) years - 5%;Three (3) years to less than (4) years - 12%; and

Less than three (3) years - 20%

(2) Cash and/or Property Dividends - A final tax at the following rates shall be imposed upon the cash and/orproperty dividends actually or constructively received by an individual from a domestic corporation or from a jointstock company, insurance or mutual fund companies and regional operating headquarters of multinationalcompanies, or on the share of an individual in the distributable net income after tax of a partnership (except ageneral professional partnership) of which he is a partner, or on the share of an individual in the net income aftertax of an association, a joint account, or a joint venture or consortium taxable as a corporation of which he is amember or co-venturer:

Six percent (6%) beginning January 1, 1998;Eight percent (8%) beginning January 1, 1999; and

Ten percent (10% beginning January 1, 2000.

Provided, however, That the tax on dividends shall apply only on income earned on or after January 1, 1998.Income forming part of retained earnings as of December 31, 1997 shall not, even if declared or distributed on orafter January 1, 1998, be subject to this tax.

(C) Capital Gains from Sale of Shares of Stock not Traded in the Stock Exchange. - The provisions of Section 39(B)notwithstanding, a final tax at the rates prescribed below is hereby imposed upon the net capital gains realized

during the taxable year from the sale, barter, exchange or other disposition of shares of stock in a domesticcorporation, except shares sold, or disposed of through the stock exchange.Not over P100,000……………………………........ 5%

On any amount in excess of P100,000………… 10%

(D) Capital Gains from Sale of Real Property. -(1) In General. - The provisions of Section 39(B) notwithstanding, a final tax of six percent (6%) based on thegross selling price or current fair market value as determined in accordance with Section 6(E) of this Code,whichever is higher, is hereby imposed upon capital gains presumed to have been realized from the sale,exchange, or other disposition of real property located in the Philippines, classified as capital assets, includingpacto de retro sales and other forms of conditional sales, by individuals, including estates and trusts: Provided,That the tax liability, if any, on gains from sales or other dispositions of real property to the government or any ofits political subdivisions or agencies or to government-owned or controlled corporations shall be determined eitherunder Section 24 (A) or under this Subsection, at the option of the taxpayer.(2) Exception. - The provisions of paragraph (1) of this Subsection to the contrary notwithstanding, capital gainspresumed to have been realized from the sale or disposition of their principal residence by natural persons, the

proceeds of which is fully utilized in acquiring or constructing a new principal residence within eighteen (18)calendar months from the date of sale or disposition, shall be exempt from the capital gains tax imposed under thisSubsection: Provided, That the historical cost or adjusted basis of the real property sold or disposed shall becarried over to the new principal residence built or acquired: Provided, further, That the Commissioner shall havebeen duly notified by the taxpayer within thirty (30) days from the date of sale or disposition through a prescribedreturn of his intention to avail of the tax exemption herein mentioned: Provided, still further, That the said taxexemption can only be availed of once every ten (10) years: Provided, finally, that if there is no full utilization ofthe proceeds of sale or disposition, the portion of the gain presumed to have been realized from the sale ordisposition shall be subject to capital gains tax. For this purpose, the gross selling price or fair market value at thetime of sale, whichever is higher, shall be multiplied by a fraction which the unutilized amount bears to the grossselling price in order to determine the taxable portion and the tax prescribed under paragraph (1) of thisSubsection shall be imposed thereon.

Sec 22 (Y) The term "deposit substitutes" shall mean an alternative from of obtaining funds from the public (theterm 'public' means borrowing from twenty (20) or more individual or corporate lenders at any one time) other

than deposits, through the issuance, endorsement, or acceptance of debt instruments for the borrowers ownaccount, for the purpose of relending or purchasing of receivables and other obligations, or financing their ownneeds or the needs of their agent or dealer. These instruments may include, but need not be limited to bankers'acceptances, promissory notes, repurchase agreements, including reverse repurchase agreements entered into byand between the Bangko Sentral ng Pilipinas (BSP) and any authorized agent bank, certificates of assignment orparticipation and similar instruments with recourse: Provided, however, That debt instruments issued for interbankcall loans with maturity of not more than five (5) days to cover deficiency in reserves against deposit liabilities,including those between or among banks and quasi-banks, shall not be considered as deposit substitute debtinstruments.

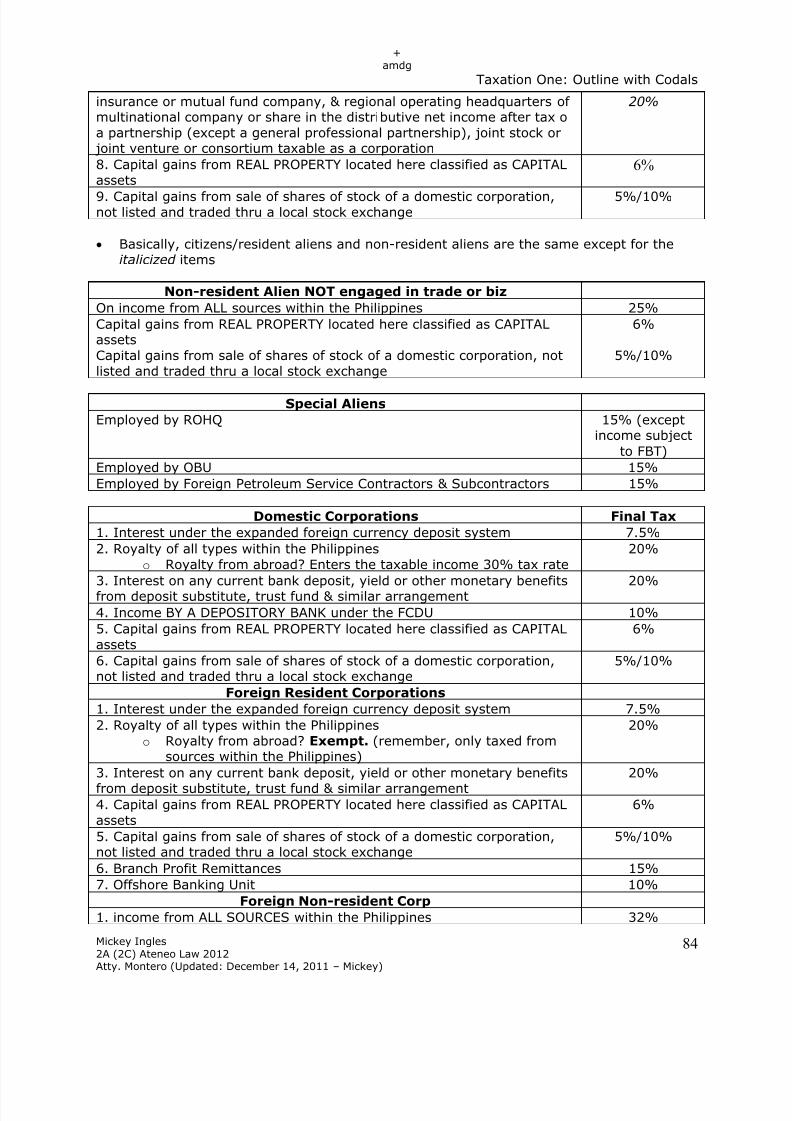

Tax Rate on Certain Passive Income on Citizens and Resident Final Tax

8/12/2019 Taxation One Complete

http://slidepdf.com/reader/full/taxation-one-complete 7/90

+amdg

Taxation One: Outline with Codals

Mickey Ingles2A (2C) Ateneo Law 2012Atty. Montero (Updated: December 14, 2011 – Mickey)

7

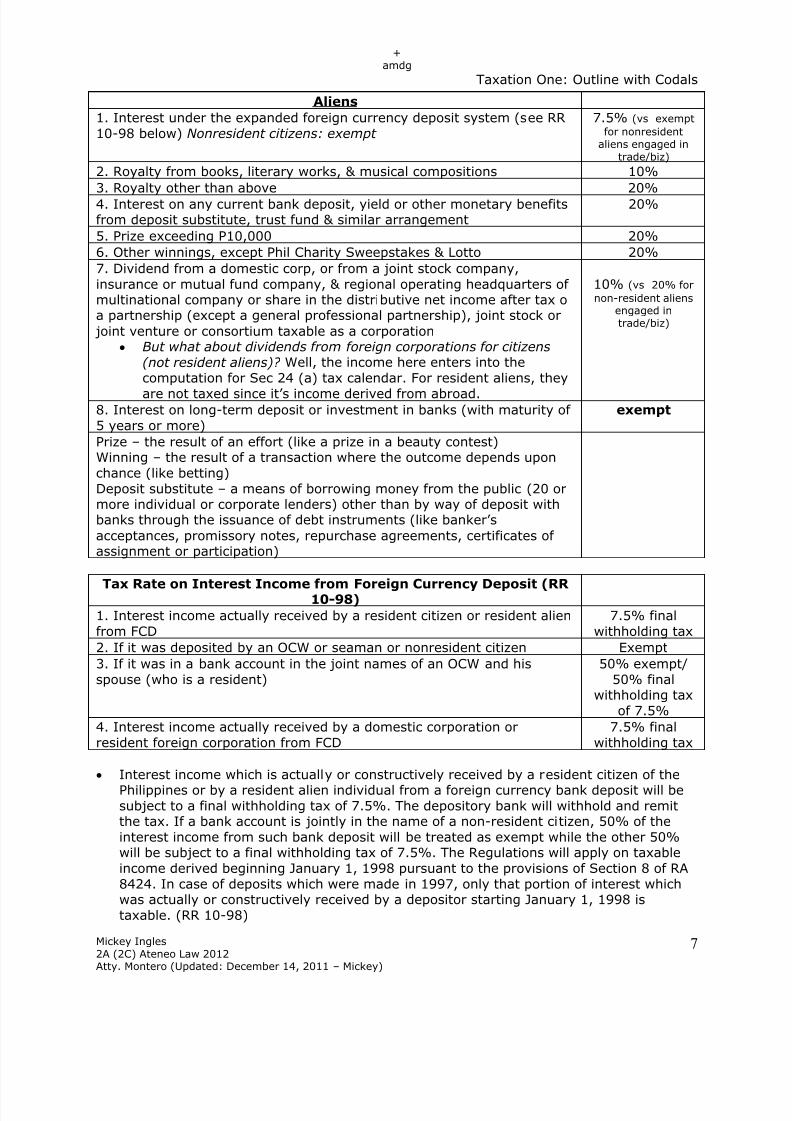

Aliens

1. Interest under the expanded foreign currency deposit system (see RR

10-98 below) Nonresident citizens: exempt

7.5% (vs exempt

for nonresidentaliens engaged in

trade/biz) 2. Royalty from books, literary works, & musical compositions 10%

3. Royalty other than above 20%

4. Interest on any current bank deposit, yield or other monetary benefitsfrom deposit substitute, trust fund & similar arrangement

20%

5. Prize exceeding P10,000 20%

6. Other winnings, except Phil Charity Sweepstakes & Lotto 20%

7. Dividend from a domestic corp, or from a joint stock company,

insurance or mutual fund company, & regional operating headquarters ofmultinational company or share in the distributive net income after tax oa partnership (except a general professional partnership), joint stock or

joint venture or consortium taxable as a corporation

But what about dividends from foreign corporations for citizens

(not resident aliens)? Well, the income here enters into the

computation for Sec 24 (a) tax calendar. For resident aliens, they

are not taxed since it’s income derived from abroad.

10% (vs 20% for

non-resident aliensengaged intrade/biz)

8. Interest on long-term deposit or investment in banks (with maturity of

5 years or more)

exempt

Prize – the result of an effort (like a prize in a beauty contest)Winning – the result of a transaction where the outcome depends upon

chance (like betting)

Deposit substitute – a means of borrowing money from the public (20 ormore individual or corporate lenders) other than by way of deposit withbanks through the issuance of debt instruments (like banker’s

acceptances, promissory notes, repurchase agreements, certificates ofassignment or participation)

Tax Rate on Interest Income from Foreign Currency Deposit (RR10-98)

1. Interest income actually received by a resident citizen or resident alien

from FCD

7.5% final

withholding tax

2. If it was deposited by an OCW or seaman or nonresident citizen Exempt

3. If it was in a bank account in the joint names of an OCW and his

spouse (who is a resident)

50% exempt/

50% finalwithholding tax

of 7.5%

4. Interest income actually received by a domestic corporation or

resident foreign corporation from FCD

7.5% final

withholding tax

Interest income which is actually or constructively received by a resident citizen of the

Philippines or by a resident alien individual from a foreign currency bank deposit will besubject to a final withholding tax of 7.5%. The depository bank will withhold and remitthe tax. If a bank account is jointly in the name of a non-resident citizen, 50% of the

interest income from such bank deposit will be treated as exempt while the other 50%will be subject to a final withholding tax of 7.5%. The Regulations will apply on taxable

income derived beginning January 1, 1998 pursuant to the provisions of Section 8 of RA

8424. In case of deposits which were made in 1997, only that portion of interest whichwas actually or constructively received by a depositor starting January 1, 1998 is

taxable. (RR 10-98)

8/12/2019 Taxation One Complete

http://slidepdf.com/reader/full/taxation-one-complete 8/90

+amdg

Taxation One: Outline with Codals

Mickey Ingles2A (2C) Ateneo Law 2012Atty. Montero (Updated: December 14, 2011 – Mickey)

8

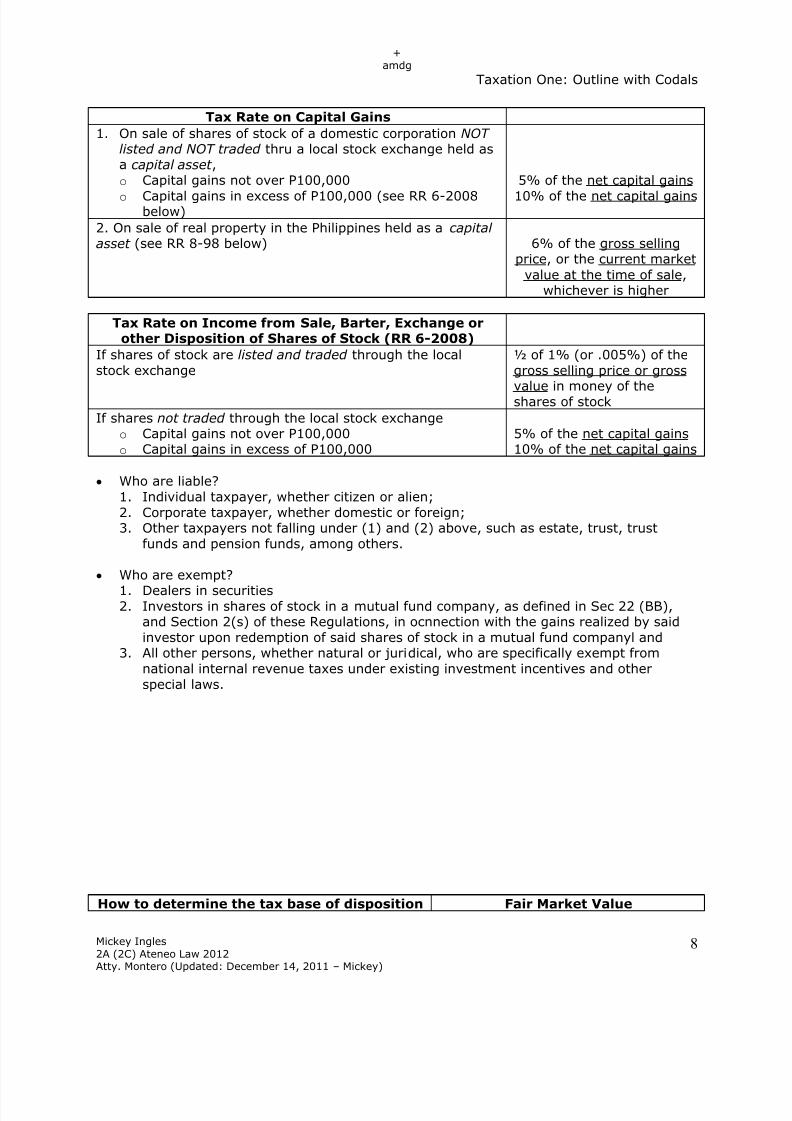

Tax Rate on Capital Gains

1. On sale of shares of stock of a domestic corporation NOTlisted and NOT traded thru a local stock exchange held asa capital asset ,

o Capital gains not over P100,000

o

Capital gains in excess of P100,000 (see RR 6-2008below)

5% of the net capital gains

10% of the net capital gains

2. On sale of real property in the Philippines held as a capital

asset (see RR 8-98 below) 6% of the gross sellingprice, or the current market

value at the time of sale,whichever is higher

Tax Rate on Income from Sale, Barter, Exchange orother Disposition of Shares of Stock (RR 6-2008)

If shares of stock are listed and traded through the local

stock exchange

½ of 1% (or .005%) of the

gross selling price or gross

value in money of theshares of stock

If shares not traded through the local stock exchangeo Capital gains not over P100,000

o Capital gains in excess of P100,0005% of the net capital gains10% of the net capital gains

Who are liable?

1. Individual taxpayer, whether citizen or alien;

2. Corporate taxpayer, whether domestic or foreign;3. Other taxpayers not falling under (1) and (2) above, such as estate, trust, trust

funds and pension funds, among others.

Who are exempt?

1.

Dealers in securities2. Investors in shares of stock in a mutual fund company, as defined in Sec 22 (BB),

and Section 2(s) of these Regulations, in ocnnection with the gains realized by said

investor upon redemption of said shares of stock in a mutual fund companyl and3. All other persons, whether natural or juridical, who are specifically exempt from

national internal revenue taxes under existing investment incentives and other

special laws.

How to determine the tax base of disposition Fair Market Value

8/12/2019 Taxation One Complete

http://slidepdf.com/reader/full/taxation-one-complete 9/90

+amdg

Taxation One: Outline with Codals

Mickey Ingles2A (2C) Ateneo Law 2012Atty. Montero (Updated: December 14, 2011 – Mickey)

9

of stock (RR 6-2008)

Sales of stock listed and traded through the LSE FMV is the actual selling price

Sales of stock listed but not traded through theLSE

FMV is the closing price on the daywhen the shares were sold, transferred,

etc (if no sale was made on that day inthe LSE, then the closing price on the

day nearest to the date of sale,transfer, or exchange of the said

shares)

Sales of stock not listed and not traded throughthe LSE

FMV is the book value of the shares ofstock as shown in the financial

statements duly certified by an

independent CPA nearest to the date ofsale

Final Tax Rate on Sales, Exchanges, or Transfers or RealProperties Classified as Capital Assets (RR 8-98)

Sale of real property in the Philippines 6% of the gross selling

price, or the currentmarket value at the time

of sale, whichever ishigher

If sale was made to the government or to GOCCs Either 6% of the gross

selling price/currentmarket value or under

the normal income tax

rate, taxpayer’s option

Creditable Withholding Tax on Sales, Exchanges or

Transfers of Real Properties classified as Ordinary Assets(RR 8-98)

1. If the seller is habitually engaged in the real estate businesso Selling price is less than P500,000

o Selling price is P500,000 to P2m

o Selling price is above P2m

1.5%3%

5% of gross selling

price/current marketvalue, whichever is

higher

2. If the seller is not habitually engaged in the real estate

business

7.5% of gross selling

price/current marketvalue, whichever is

higher

3. If the seller is exempt from creditable withholding tax as per

RR 2-98

Exempt

Conditions to be exempt from capital gains tax of 6% on the sale, exchange, ordisposition of a principal residence (RR 13-99)

1. The proceeds from the sale, exchange, or disposition of his principal residence must

be fully utilized in acquiring or construing a new principal residence within 18

months. There must be proof. 2. This can only be availed of ONLY ONCE every 10 years

8/12/2019 Taxation One Complete

http://slidepdf.com/reader/full/taxation-one-complete 10/90

+amdg

Taxation One: Outline with Codals

Mickey Ingles2A (2C) Ateneo Law 2012Atty. Montero (Updated: December 14, 2011 – Mickey)

10

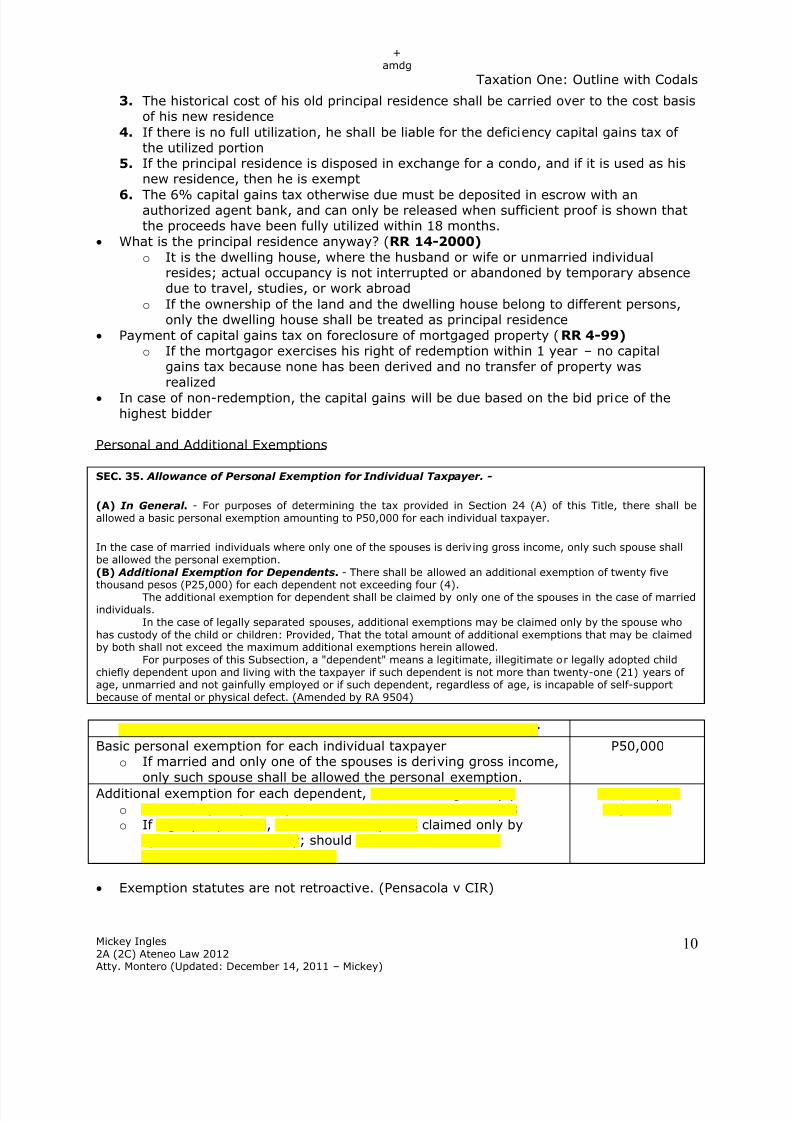

3. The historical cost of his old principal residence shall be carried over to the cost basisof his new residence

4. If there is no full utilization, he shall be liable for the deficiency capital gains tax ofthe utilized portion

5. If the principal residence is disposed in exchange for a condo, and if it is used as hisnew residence, then he is exempt

6.

The 6% capital gains tax otherwise due must be deposited in escrow with anauthorized agent bank, and can only be released when sufficient proof is shown thatthe proceeds have been fully utilized within 18 months.

What is the principal residence anyway? (RR 14-2000)

o It is the dwelling house, where the husband or wife or unmarried individualresides; actual occupancy is not interrupted or abandoned by temporary absencedue to travel, studies, or work abroad

o If the ownership of the land and the dwelling house belong to different persons,only the dwelling house shall be treated as principal residence

Payment of capital gains tax on foreclosure of mortgaged property (RR 4-99) o If the mortgagor exercises his right of redemption within 1 year – no capital

gains tax because none has been derived and no transfer of property wasrealized

In case of non-redemption, the capital gains will be due based on the bid price of thehighest bidder

Personal and Additional Exemptions

SEC. 35. Allowance of Personal Exemption for Individual Taxpayer. -

(A) In General . - For purposes of determining the tax provided in Section 24 (A) of this Title, there shall beallowed a basic personal exemption amounting to P50,000 for each individual taxpayer.

In the case of married individuals where only one of the spouses is deriving gross income, only such spouse shallbe allowed the personal exemption.(B) Additional Exemption for Dependents. - There shall be allowed an additional exemption of twenty five

thousand pesos (P25,000) for each dependent not exceeding four (4).The additional exemption for dependent shall be claimed by only one of the spouses in the case of marriedindividuals.

In the case of legally separated spouses, additional exemptions may be claimed only by the spouse whohas custody of the child or children: Provided, That the total amount of additional exemptions that may be claimedby both shall not exceed the maximum additional exemptions herein allowed.

For purposes of this Subsection, a "dependent" means a legitimate, illegitimate or legally adopted childchiefly dependent upon and living with the taxpayer if such dependent is not more than twenty-one (21) years ofage, unmarried and not gainfully employed or if such dependent, regardless of age, is incapable of self-supportbecause of mental or physical defect. (Amended by RA 9504)

Personal and additional exemption for individual taxpayer

Basic personal exemption for each individual taxpayer

o If married and only one of the spouses is deriving gross income,

only such spouse shall be allowed the personal exemption.

P50,000

Additional exemption for each dependent, not exceeding four (4)

o Claimed by only one spouse in case of married individualso If legally separated, additional exemptions claimed only by

spouse who has custody; should not exceed maximum

additional exemptions allowed

P25,000 per

dependent

Exemption statutes are not retroactive. (Pensacola v CIR)

8/12/2019 Taxation One Complete

http://slidepdf.com/reader/full/taxation-one-complete 11/90

+amdg

Taxation One: Outline with Codals

Mickey Ingles2A (2C) Ateneo Law 2012Atty. Montero (Updated: December 14, 2011 – Mickey)

11

Discounts for senior citizens is now treated as tax deductions, as per RA 9257. Thissucks for the taxpayer because he doesn’t get the “peso for peso” benefit which he

would have gotten if it were considered a tax credit as before. (M.E. Holdings Corp v CIR& CTA)

Senior Citizens are

o Resident citizens

o

At least 60 years old They are not exempt from income taxes unless they are considered

minimum wage earners. (RA 9994, which also took out the previous

P60,000 requirement)

Change of status

Sec 35. (C) Change of Status. - If the taxpayer marries or should have additional dependent(s) as defined above during

the taxable year, the taxpayer may claim the corresponding additional exemption, as the case may be, in full forsuch year.

If the taxpayer dies during the taxable year, his estate may still claim the personal and additionalexemptions for himself and his dependent(s) as if he died at the close of such year.

If the spouse or any of the dependents dies or if any of such dependents marries, becomes twenty-one(21) years old or becomes gainfully employed during the taxable year, the taxpayer may still claim the same

exemptions as if the spouse or any of the dependents died, or as if such dependents married, became twenty-one(21) years old or became gainfully employed at the close of such year.

Personal exemption allowable to nonresident alien individualsSec. 35 (D) Personal Exemption Allowable to Nonresident Alien Individual. - A nonresident alien individualengaged in trade, business or in the exercise of a profession in the Philippines shall be entitled to a personalexemption in the amount equal to the exemptions allowed in the income tax law in the country of which he is asubject - or citizen, to citizens of the Philippines not residing in such country, not to exceed the amount fixed inthis Section as exemption for citizens or resident of the Philippines: Provided, That said nonresident alien shouldfile a true and accurate return of the total income received by him from all sources in the Philippines, as requiredby this Title.

Personal Exemptions allowable to

nonresident alien individuals

If engaged in trade, business or in the exercise ofa profession

Entitled to a personal exemption in theamount equal to the exemptions

allowed in the income tax law of his

country for Filipinos, but it shouldn’texceed the amount fixed here forexemptions

If not engaged in trade, business or in the exerciseof a profession

None, because Sec 25 (B) states thathe will be taxed upon his entireincome.

De Leon states that nonresident aliens are not entitled to additional exemptions fordependents. (P. 135, Fundamentals of Taxation 2009)

Optional Standard DeductionSec. 34 (L) Optional Standard Deduction. - In lieu of the deductions allowed under the preceding Subsections,

an individual subject to tax under Section 24, other than a nonresident alien, may elect a standard deduction in anamount not exceeding forty percent (40%) of his gross sales or gross receipts, as the case may be. In the case ofa corporation subject to tax under section 27(A) and 28(A)(1), it may elect a standard deduction in an amount notexceeding forty percent (40%) of it gross income as defined in Section 32 of this Code. Unless the taxpayersignifies in his return his intention to elect the optional standard deduction, he shall be considered as havingavailed himself of the deductions allowed in the preceding Subsections. Such election when made in the returnshall be irrevocable for the taxable year for which the return is made: Provided, That an individual who is entitledto and claimed for the optional standard shall not be required to submit with his tax return such financial

8/12/2019 Taxation One Complete

http://slidepdf.com/reader/full/taxation-one-complete 12/90

8/12/2019 Taxation One Complete

http://slidepdf.com/reader/full/taxation-one-complete 13/90

+amdg

Taxation One: Outline with Codals

Mickey Ingles2A (2C) Ateneo Law 2012Atty. Montero (Updated: December 14, 2011 – Mickey)

13

taxpayer for himself, including his family, shall be allowed as a deduction from his gross income: Provided, Thatsaid family has a gross income of not more than Two hundred fifty thousand pesos (P250,000) for the taxableyear: Provided, finally , That in the case of married taxpayers, only the spouse claiming the additional exemptionfor dependents shall be entitled to this deduction.

The taxpayer is allowed a deduction of P2,400/family or P200/month for health and/or

hospitalization insurance premiums, provided:o

Said family’s gross income is not more than P250,000 for the taxable year. If married, only the spouse claiming the additional exemption for dependents can avail

of this.

Exclusions and deductions (discussion from De Leon’s book)

Exclusions are incomes that are exempt from the tax. They are not to be included in the

tax return unless information regarding it is specifically called for.o Examples:

Life insurance proceeds paid to beneficiaries upon the death of the

insured. Value of the property acquired by inheritance or donation, because it is

subject to estate or donor’s tax.

Retirement benefits, pensions, etc, received by government officials andemployees from the GSIS and SSS in recognition of their services. So withretirement benefits of private firms, under certain conditions.

Prizes and awards made primarily in recognition of religious, charitable,

scientific, educational, artistic, etc, competitions and tournaments. Christmas bonus, 13th month pay, productivity incentives, and other

benefits received up to a max of P30,000.

Gains from the sale or retirement of bonds or other certificates ofindebtedness with a maturity of more than 5 years.

Deductions are items or amounts which the law allows to be deducted under certain

conditions from the gross income of a taxpayer in order to arrive at the taxable income.

Both reduce actual gross income although exclusions are not included in the income taxreturn.

Some general principals governing deductions include:o The taxpayer seeking a deduction must point to some specific provision of the

statute authorizing the deduction; and

o He must be able to prove that he is entitled to the deduction authorized or

allowed.

They are allowed only where there is a clear provision in the statute for thededuction claimed.

Taxable gross income is affected by exclusions because the latter are omitted from the

former and are not reported on the income tax return but is not affected by deductionsbecause they are subtracted after gross income is determined and are reported on thereturn.

Kinds of deductions:

1. Deductions from compensation income.2. Deductions from business/professional income.

3. Deductions from corporate income.

4. Special deductions5. Deductions allowed by special laws.

Tax on non-resident aliens

Non-resident aliens engaged in business in the PhilippinesSEC. 25. Tax on Nonresident Alien Individual. - (A) Nonresident Alien Engaged in trade or Business Within the Philippines. -

8/12/2019 Taxation One Complete

http://slidepdf.com/reader/full/taxation-one-complete 14/90

+amdg

Taxation One: Outline with Codals

Mickey Ingles2A (2C) Ateneo Law 2012Atty. Montero (Updated: December 14, 2011 – Mickey)

14

• (1) In General . - A nonresident alien individual engaged in trade or business in the Philippines shall be subject to

an income tax in the same manner as an individual citizen and a resident alien individual, on taxableincome received from all sources within the Philippines. A nonresident alien individual who shall come tothe Philippines and stay therein for an aggregate period of more than one hundred eighty (180) daysduring any calendar year shall be deemed a 'nonresident alien doing business in the Philippines'. Section22 (G) of this Code notwithstanding.

• (2) Cash and/or Property Dividends from a Domestic Corporation or Joint Stock Company, or Insurance orMutual Fund Company or Regional Operating Headquarters or Multinational Company, or Share in theDistributable Net Income of a Partnership (Except a General Professional Partnership), Joint Account, JointVenture Taxable as a Corporation or Association., Interests, Royalties, Prizes, and Other Winnings. - Cashand/or property dividends from a domestic corporation, or from a joint stock company, or from aninsurance or mutual fund company or from a regional operating headquarters of multinational company,or the share of a nonresident alien individual in the distributable net income after tax of a partnership(except a general professional partnership) of which he is a partner, or the share of a nonresident alienindividual in the net income after tax of an association, a joint account, or a joint venture taxable as acorporation of which he is a member or a co-venturer; interests; royalties (in any form); and prizes(except prizes amounting to Ten thousand pesos (P10,000) or less which shall be subject to tax underSubsection (B)(1) of Section 24) and other winnings (except Philippine Charity Sweepstakes and Lottowinnings); shall be subject to an income tax of twenty percent (20%) on the total amount thereof:Provided, however, that royalties on books as well as other literary works, and royalties on musicalcompositions shall be subject to a final tax of ten percent (10%) on the total amount thereof: Provided,further , That cinematographic films and similar works shall be subject to the tax provided under Section28 of this Code: Provided, furthermore, That interest income from long-term deposit or investment in the

form of savings, common or individual trust funds, deposit substitutes, investment management accountsand other investments evidenced by certificates in such form prescribed by the Bangko Sentral ng Pilipinas(BSP) shall be exempt from the tax imposed under this Subsection: Provided, finally, that should theholder of the certificate pre-terminate the deposit or investment before the fifth (5 th) year, a final tax shallbe imposed on the entire income and shall be deducted and withheld by the depository bank from theproceeds of the long-term deposit or investment certificate based on the remaining maturity thereof:

Four (4) years to less than five (5) years - 5%;Three (3) years to less than four (4) years - 12%; andLess than three (3) years - 20%.

(3) Capital Gains. - Capital gains realized from sale, barter or exchange of shares of stock in domestic corporationsnot traded through the local stock exchange, and real properties shall be subject to the tax prescribed underSubsections (C) and (D) of Section 24.

A nonresident alien engaged in trade or business in the Philippines is subject to thesame income tax rate as citizens and resident aliens, on taxable income received from

all sources within the Philippines. A nonresident alien who stays in the Philippines for an aggregate period of more than

180 days shall be deemed as nonresident alien doing business in the Philippines.

Tax Rate on Certain Passive Income on Nonresident Aliens

Engaged in Trade, Business or Exercising a Profession

Final Tax

1. Interest under the expanded foreign currency deposit system exempt

2. Royalty from books, literary works, & musical compositions 10%

3. Royalty other than above 20%

4. Interest on any current bank deposit, yield or other monetary benefits

from deposit substitute, trust fund & similar arrangement

20%

5. Prize exceeding P10,000 20%

6. Other winnings, except Phil Charity Sweepstakes & Lotto 20%7. Dividend from a domestic corp, or from a joint stock company,

insurance or mutual fund company, & regional operating headquarters ofmultinational company or share in the distributive net income after tax oa partnership (except a general professional partnership), joint stock or

joint venture or consortium taxable as a corporation

What about dividends from foreign corps? Exempt. Nonresidentaliens are not taxed worldwide.

20% (compare

with citizens andresident aliens)

8. Gross income from cinematographic films & similar works 25%

8/12/2019 Taxation One Complete

http://slidepdf.com/reader/full/taxation-one-complete 15/90

+amdg

Taxation One: Outline with Codals

Mickey Ingles2A (2C) Ateneo Law 2012Atty. Montero (Updated: December 14, 2011 – Mickey)

15

9. Interest on long-term deposit or investment in banks (with maturity of5 years or more)

exempt

Tax Rate on Capital Gains (same with residents, and

nonresident aliens not engaged in business)

2. On sale of shares of stock of a domestic corporation NOT

listed and NOT traded thru a local stock exchange held asa capital asset ,

o Capital gains not over P100,000

o Capital gains in excess of P100,000

5% of the net capital gains

10% of the net capital gains

2. On sale of real property in the Philippines held as a capitalasset 6% of the gross selling

price, or the current marketvalue at the time of sale,

whichever is higher

Non-resident aliens not engaged in business in the PhilippinesSec. 25 (B) Nonresident Alien Individual Not Engaged in Trade or Business Within the Philippines. - There shall be levied, collected and paid for each taxable year upon the entire income received from all sources

within the Philippines by every nonresident alien individual not engaged in trade or business within the Philippinesas interest, cash and/or property dividends, rents, salaries, wages, premiums, annuities, compensation,remuneration, emoluments, or other fixed or determinable annual or periodic or casual gains, profits, and income,and capital gains, a tax equal to twenty-five percent (25%) of such income. Capital gains realized by a nonresidentalien individual not engaged in trade or business in the Philippines from the sale of shares of stock in any domesticcorporation and real property shall be subject to the income tax prescribed under Subsections (C) and (D) ofSection 24.

Nonresident aliens not engaged in business are taxed 25% of their entire income within

the Philippines.

That means they have no deductions!

Their capital gains are the same with nonresident aliens engaged in business (see table

above!)

Special aliensSec. 25 (C) Alien Individual Employed by Regional or Area Headquarters and Regional Operating

Headquarters of Multinational Companies. - There shall be levied, collected and paid for each taxable yearupon the gross income received by every alien individual employed by regional or area headquarters and regionaloperating headquarters established in the Philippines by multinational companies as salaries, wages, annuities,compensation, remuneration and other emoluments, such as honoraria and allowances, from such regional or areaheadquarters and regional operating headquarters, a tax equal to fifteen percent (15%) of such gross income:Provided, however , That the same tax treatment shall apply to Filipinos employed and occupying the same positionas those of aliens employed by these multinational companies. For purposes of this Chapter, the term'multinational company' means a foreign firm or entity engaged in international trade with affiliates or subsidiariesor branch offices in the Asia-Pacific Region and other foreign markets.

(D) Alien Individual Employed by Offshore Banking Units. - There shall be levied, collected and paid for eachtaxable year upon the gross income received by every alien individual employed by offshore banking unitsestablished in the Philippines as salaries, wages, annuities, compensation, remuneration and other emoluments,such as honoraria and allowances, from such off-shore banking units, a tax equal to fifteen percent (15%) of suchgross income: Provided, however, That the same tax treatment shall apply to Filipinos employed and occupying thesame positions as those of aliens employed by these offshore banking units.

(E) Alien Individual Employed by Petroleum Service Contractor and Subcontractor. - An Alien individual who is apermanent resident of a foreign country but who is employed and assigned in the Philippines by a foreign servicecontractor or by a foreign service subcontractor engaged in petroleum operations in the Philippines shall be liableto a tax of fifteen percent (15%) of the salaries, wages, annuities, compensation, remuneration and otheremoluments, such as honoraria and allowances, received from such contractor or subcontractor: Provided,however, That the same tax treatment shall apply to a Filipino employed and occupying the same position as an

8/12/2019 Taxation One Complete

http://slidepdf.com/reader/full/taxation-one-complete 16/90

+amdg

Taxation One: Outline with Codals

Mickey Ingles2A (2C) Ateneo Law 2012Atty. Montero (Updated: December 14, 2011 – Mickey)

16

alien employed by petroleum service contractor and subcontractor.

Any income earned from all other sources within the Philippines by the alien employees referred to underSubsections (C), (D) and (E) hereof shall be subject to the pertinent income tax, as the case may be, imposedunder this Code.

Special Aliens

1. Employed by regional or area headquarters & regionaloperating headquarters established in the Philippines by

multinational;

15% on gross income

2. Employed by offshore banking units 15% on gross income

3. Permanent resident of a foreign country but who is employed

and assigned in the Philippines by a foreign service contractor orby a foreign service subcontractor engaged in petroleumoperations in the Philippines

15%

Provided the same tax shall apply to Filipinos employed and occupying the same positionas these aliens.

These apply only to positions of a highly technical or highly managerial nature. ( Atty.Montero)

All income earned from all other sources within the Philippines by the special alienemployees shall be subject to the pertinent income tax imposed by the Code.

Tips on answering

Thought process in answering problems:

1. Is this income? If not, then it’s not really a income tax problem. 2. Who’s the taxpayer? And what’s the source? Refer to Sec 23!

3. What’s the specific rate? See sec 24-25!

For example, what is the tax rate of on income derived from dividends from foreigncorporations for 1. Citizens 2. Resident aliens and 3. Nonresident aliens engaged in trade or

business?

1.

Citizens

a. Yes, it’s income.

b. The source is outside the Philippines. Are they liable for sources from outsidethe Philippines? Yes! Citizens are taxed worldwide!

c. What’s the specific tax rate? Hmm… since it’s not in any of the charts, but

they still have to be taxed, then the income they derive from dividends fromforeign corporations will be considered in computing the tax rate based on thetax calendar of Sec 24(a)

2. Resident aliens

a. Yes, it’s income. b. The source is outside the Philippines. Are they liable for sources from outside

the Philippines? No! They aren’t taxed worldwide.

3.

Nonresident aliens engaged in trade or businessa. Yes, my dear, it’s income. b. The source is outside the Philippines. Are they liable for source from outside

the Philippines? No! They aren’t taxed worldwide either.

D. Definitions Section 22, Tax Code

Definition of corporations

8/12/2019 Taxation One Complete

http://slidepdf.com/reader/full/taxation-one-complete 17/90

+amdg

Taxation One: Outline with Codals

Mickey Ingles2A (2C) Ateneo Law 2012Atty. Montero (Updated: December 14, 2011 – Mickey)

17

Sec 22 (B) The term "corporation" shall include partnerships, no matter how created or organized, joint-stock

companies, joint accounts (cuentas en participacion), association, or insurance companies, but does not includegeneral professional partnerships and a joint venture or consortium formed for the purpose of undertakingconstruction projects or engaging in petroleum, coal, geothermal and other energy operations pursuant to anoperating consortium agreement under a service contract with the Government. "General professionalpartnerships" are partnerships formed by persons for the sole purpose of exercising their common profession, nopart of the income of which is derived from engaging in any trade or business.

Corporations include:

o Partnerships, no matter how created or organized

o Joint-stock companies

o Joint accounts

o Associations

o Insurance companies

It does not includeo General professional partnerships;

o Joint venture or consortium formed for the purpose of undertaking construction

projects, or engaging in petroleum, coal, geothermal and other energy operationspursuant to an operating or consortium agreement under a service contract withthe government.

Remember your partnership lessons! (AFISCO and Pascual cases) All co-owernships are not deemed unregistered partnerships.(Obillos v CIR)

The moment inheritance shares are used as part of the common assets to be used in

making profits, it is considered part of the taxable income of an unregistered

partnership. (Ona v CIR)

Requisites of a JV:1. Contribution by each party

2. Profits are shared among the parties

3. There is joint right of mutual control over the subject matter4. There is a single business transaction rather than a general or continuous transaction

(BIR Ruling 317-92, in this case, the first agreement of the two parties to construct the

6750 Bldg was not taxable because they had not derived income/profits from it. the

construction of the building was mere return of the capital which they shelled out.However, once the two corporations were placed under one sole management to operate

the business affairs of the two, the JV was taxable separate from the two corporationscomprising it. The distribution by the JV to the two constituent corporations was nottaxable because it was considered intra-corporate dividends.)

E. Income Tax RatesSEC. 27. Rates of Income tax on Domestic Corporations. -

(A) In General. - Except as otherwise provided in this Code, an income tax of thirty-five percent (35%) is herebyimposed upon the taxable income derived during each taxable year from all sources within and without thePhilippines by every corporation, as defined in Section 22(B) of this Code and taxable under this Title as acorporation, organized in, or existing under the laws of the Philippines: Provided, That effective January 1, 2009,the rate of income tax shall be thirty percent (30%).

In the case of corporations adopting the fiscal-year accounting period, the taxable income shall be computedwithout regard to the specific date when specific sales, purchases and other transactions occur. Their income andexpenses for the fiscal year shall be deemed to have been earned and spent equally for each month of the period.The corporate income tax rates shall be applied on the amount computed by multiplying the number of monthscovered by the new rates within the fiscal year by the taxable income of the corporation for the period, divided bytwelve.Provided, further, That the President, upon the recommendation of the Secretary of Finance, may effective January1, 2000, allow corporations the option to be taxed at fifteen percent (15%) of gross income as defined herein, afterthe following conditions have been satisfied:(1) A tax effort ratio of twenty percent (20%) of Gross National Product (GNP);(2) A ratio of forty percent (40%) of income tax collection to total tax revenues;

8/12/2019 Taxation One Complete

http://slidepdf.com/reader/full/taxation-one-complete 18/90

+amdg

Taxation One: Outline with Codals

Mickey Ingles2A (2C) Ateneo Law 2012Atty. Montero (Updated: December 14, 2011 – Mickey)

18

(3) A VAT tax effort of four percent (4%) of GNP; and

(4) A 0.9 percent (0.9%) ratio of the Consolidated Public Sector Financial Position (CPSFP) to GNP.The option to be taxed based on gross income shall be available only to firms whose ratio of cost of sales

to gross sales or receipts from all sources does not exceed fifty-five percent (55%).The election of the gross income tax option by the corporation shall be irrevocable for three (3)

consecutive taxable years during which the corporation is qualified under the scheme.For purposes of this Section, the term 'gross income' derived from business shall be equivalent to gross

sales less sales returns, discounts and allowances and cost of goods sold. "Cost of goods sold" shall include allbusiness expenses directly incurred to produce the merchandise to bring them to their present location and use.

For a trading or merchandising concern, "cost of goods" sold shall include the invoice cost of the goodssold, plus import duties, freight in transporting the goods to the place where the goods are actually sold, includinginsurance while the goods are in transit.

For a manufacturing concern, "cost of goods manufactured and sold" shall include all costs of productionof finished goods, such as raw materials used, direct labor and manufacturing overhead, freight cost, insurancepremiums and other costs incurred to bring the raw materials to the factory or warehouse.

In the case of taxpayers engaged in the sale of service, 'gross income' means gross receipts less salesreturns, allowances and discounts.

Tax rate of Domestic Corporations 30% of taxable income from all sources withinand outside the Philippines, or2% of gross income if MCIT applies, or

15% of gross income if the following conditions

are met:1. tax effort ratio of 20% of GNP

2. ratio of 40% of income tax collection to

total tax revenues3. VAT tax effort of 4% of GNP; and4. .9% ratio of the Consolidated Public Sector

Financial Position (CPSFP) to GNP (this lastone has yet to be implemented)

Option to be taxed based on gross income shall be available only to firms whose ratio of

cost of sales to gross sales or receipts from all sources does not exceed 55%

Election of the gross income tax option by the corporation shall be irrevocable for

3 consecutive taxable years

Domestic corporations are subject to any or some of the following: Capital gains tax

Final tax on passive income

Normal tax

Minimum corporate income tax (MCIT)

Gross income tax (GIT)

Improperly accumulated earnings tax (IAET)

Gross Income Computation

Gross Sales

Less: Sales Returns

Discounts

Allowances

CoGS (all business expenses directly incurred to produce the merchandise and bringthem to their present location or use)

Total Gross Income

CoGS for a Trading or Merchandise Concern

Invoice cost of goods sold

Import duties

Freight in transporting the goods to the place where the goods are actually sold

Insurance while the goods are in transit

8/12/2019 Taxation One Complete

http://slidepdf.com/reader/full/taxation-one-complete 19/90

+amdg

Taxation One: Outline with Codals

Mickey Ingles2A (2C) Ateneo Law 2012Atty. Montero (Updated: December 14, 2011 – Mickey)

19

CoGS for a Manufacturing Concern

All costs of production of finished goods such as raw materials, direct labor & manufacturingoverhead

Freight cost

Insurance premiums

Other costs incurred to bring the raw materials to the factory or warehouse

Gross Income Computation for a Service Concern

Gross Sales

Less: Sales Returns

Discounts

Allowances

Cost of Services (all direct costs & expenses necessarily incurred to provide theservices required by the customers & clients including:

Salaries & employee benefits of personnel, consultants & specialistsdirectly rendering the service

Cost of facilities directly utilized in providing the service such as

depreciation or rental of equipment use & cost of supplies If it’s a bank, interest expense is included

Total Gross income of a service concern

F. Proprietary Educational Institutions and Hospitals

(B) Proprietary Educational Institutions and Hospitals. - Proprietary educational institutions and hospitals which arenonprofit shall pay a tax of ten percent (10%) on their taxable income except those covered by Subsection (D)hereof: Provided, that if the gross income from unrelated trade, business or other activity exceeds fifty percent(50%) of the total gross income derived by such educational institutions or hospitals from all sources, the taxprescribed in Subsection (A) hereof shall be imposed on the entire taxable income. For purposes of this Subsection,the term 'unrelated trade, business or other activity' means any trade, business or other activity, the conduct ofwhich is not substantially related to the exercise or performance by such educational institution or hospital of its

primary purpose or function. A "Proprietary educational institution" is any private school maintained andadministered by private individuals or groups with an issued permit to operate from the Department of Education,Culture and Sports (DECS), or the Commission on Higher Education (CHED), or the Technical Education and SkillsDevelopment Authority (TESDA), as the case may be, in accordance with existing laws and regulations.

Proprietary educational institution is:o Any private school maintained & administered by private individuals or groups

o With an issued permit to operate from the DECS or CHED or TESDA

Tax rate of proprietary educational

institutions and hospitals

10% on their taxable income (except for passive

income), or30% on their entire taxable income if the gross

income from unrelated trade, business or other

activity exceeds 50% of the total gross income of

the institution Unrelated trade, business or other activity means

o Any trade, business or other activity

o The conduct of which is not substantially related to the exercise or performance

by such its institution of its primary purpose or function.

For non-stock, non-profit educational institutions, all revenues use actually, directly andexclusively for educational purposes are exempt.

o Their exemption refers only to revenues derived from assets used actually,

directly and exclusively for educational purposes.

8/12/2019 Taxation One Complete

http://slidepdf.com/reader/full/taxation-one-complete 20/90

+amdg

Taxation One: Outline with Codals

Mickey Ingles2A (2C) Ateneo Law 2012Atty. Montero (Updated: December 14, 2011 – Mickey)

20

o Income from cafeterias, canteens & bookstores are also exempt if they areowned & operated by the educational institution and are located within the school

premises.o However, they shall be subject to internal revenue taxes on income from trade,

business or other activity, the conduct of which is not related to the exercise orperformance by such educational institutions of their educational purposes or

functions, i. e. rental payment from their building/premises. (RR 76-2003) For non-stock, non-profit corporations who are exempt, they are still liable for taxes on:

o Income derived from any of their real properties (rental payment form their

building premises)

o Any activity conducted from profit regardless of disposition thereof

o Interest income from any bank deposits or yield on deposit substitutes (final taxof 20%)

o If its foreign currency deposit, final tax of 7.5%

o They shall also be withholding agents for their employee’s compensation income

subject to withholding tax (RR 76-2003)

For private educational institutions, they are exempt from VAT, but they must be

accredited with either DECS or CHED.

o However, income derived from trade, business or other activity is still taxable.

o

Their bank deposits and foreign currency deposits are exempt from withholdingtaxes but they must show proof that such income is used to fund proposedprojects for their institution’s improvement.

o They shall also be the withholding agents for their employee’s compensationincome subject to withholding tax.

G. GOCCs

Sec. 27 (C) Government-owned or Controlled-Corporations, Agencies or Instrumentalities. - The

provisions of existing special or general laws to the contrary notwithstanding, all corporations, agencies, orinstrumentalities owned or controlled by the Government, except the Government Service Insurance System(GSIS), the Social Security System (SSS), the Philippine Health Insurance Corporation (PHIC), and the PhilippineCharity Sweepstakes Office (PCSO), shall pay such rate of tax upon their taxable income as are imposed by this

Section upon corporations or associations engaged in s similar business, industry, or activity.

GOCCs are taxed on the same rate upon their taxable income upon corporations orassociations engaged in similar business, industry, or activity.

o Exempt GOCCs:

GSIS

SSS PHIC

PCSO

As per RA 9337, PAGCOR was deleted from the list of exempt GOCCs.

H. Passive Income

Sec. 27 (D) Rates of Tax on Certain Passive Incomes. -

(1) Interest from Deposits and Yield or any other Monetary Benefit from Deposit Substitutes and from Trust Fundsand Similar Arrangements, and Royalties. - A final tax at the rate of twenty percent (20%) is hereby imposed uponthe amount of interest on currency bank deposit and yield or any other monetary benefit from deposit substitutesand from trust funds and similar arrangements received by domestic corporations, and royalties, derived fromsources within the Philippines: Provided, however, That interest income derived by a domestic corporation from adepository bank under the expanded foreign currency deposit system shall be subject to a final income tax at therate of seven and one-half percent (7 1/2%) of such interest income.

8/12/2019 Taxation One Complete

http://slidepdf.com/reader/full/taxation-one-complete 21/90

+amdg

Taxation One: Outline with Codals

Mickey Ingles2A (2C) Ateneo Law 2012Atty. Montero (Updated: December 14, 2011 – Mickey)

21

(2) Capital Gains from the Sale of Shares of Stock Not Traded in the Stock Exchange. - A final tax at the rates

prescribed below shall be imposed on net capital gains realized during the taxable year from the sale, exchange orother disposition of shares of stock in a domestic corporation except shares sold or disposed of through the stockexchange:Not over P100,000………………………..... 5%Amount in excess of P100,000…………….. 10% (3) Tax on Income Derived under the Expanded Foreign Currency Deposit System. - Income derived by a

depository bank under the expanded foreign currency deposit system from foreign currency transactions withnonresidents, offshore banking units in the Philippines, local commercial banks including branches of foreign banksthat may be authorized by the Bangko Sentral ng Pilipinas (BSP) to transact business with foreign currency depositsystem shall be exempt from all taxes, except net income from such transactions as may be specified by theSecretary of Finance, upon recommendation by the Monetary Board to be subject to the regular income taxpayable by banks: Provided, however, That interest income from foreign currency loans granted by such depositorybanks under said expanded system to residents other than offshore banking units in the Philippines or otherdepository banks under the expanded system shall be subject to a final tax at the rate of ten percent (10%).

Any income of nonresidents, whether individuals or corporations, from transactions with depository banks underthe expanded system shall be exempt from income tax

(4) Intercorporate Dividends. - Dividends received by a domestic corporation from another domestic corporationshall not be subject to tax.(5) Capital Gains Realized from the Sale, Exchange or Disposition of Lands and/or Buildings. - A final tax of six

percent (6%) is hereby imposed on the gain presumed to have been realized on the sale, exchange or dispositionof lands and/or buildings which are not actually used in the business of a corporation and are treated as capitalassets, based on the gross selling price of fair market value as determined in accordance with Section 6(E) of thisCode, whichever is higher, of such lands and/or buildings.

Tax Rate on Passive Income of Domestic Corporations Final Tax

1. Interest under the expanded foreign currency deposit system 7.5%

2. Royalty of all types within the Philippines

o Royalty from abroad? Enters the taxable income 30% tax rate

20%

3. Interest on any current bank deposit, yield or other monetary benefits

from deposit substitute, trust fund & similar arrangement

20%

4. Dividend from domestic corporations (inter-corporate dividend) exempt

Tax Rate on Capital Gains (same as individuals)

3. On sale of shares of stock of a domestic corporation NOTlisted and NOT traded thru a local stock exchange held asa capital asset ,

o Capital gains not over P100,000

o Capital gains in excess of P100,000

5% of the net capital gains

10% of the net capital gains

2. On sale of real property in the Philippines held as a capitalasset 6% of the gross selling

price, or the current market

value at the time of sale,whichever is higher

Tax Rate of BANKS on Income Derived under the Expanded FCDSystem

Final Tax

1. Income derived by a depository BANK from foreign currencytransactions with non-residents, OBUs, etc

exempt

2. Interest income from foreign currency loans granted by a bank toresidents other than OBUs

10%

Income of non-residents (individuals or corporations) from transactions with depository

bank under the expanded FCD system are exempt.

8/12/2019 Taxation One Complete

http://slidepdf.com/reader/full/taxation-one-complete 22/90

+amdg

Taxation One: Outline with Codals

Mickey Ingles2A (2C) Ateneo Law 2012Atty. Montero (Updated: December 14, 2011 – Mickey)

22

What are deposit substitutes?(Y) The term "deposit substitutes" shall mean an alternative from of obtaining funds from the public (the term'public' means borrowing from twenty (20) or more individual or corporate lenders at any one time) other thandeposits, through the issuance, endorsement, or acceptance of debt instruments for the borrowers own account,for the purpose of relending or purchasing of receivables and other obligations, or financing their own needs or theneeds of their agent or dealer. These instruments may include, but need not be limited to bankers' acceptances,

promissory notes, repurchase agreements, including reverse repurchase agreements entered into by and betweenthe Bangko Sentral ng Pilipinas (BSP) and any authorized agent bank, certificates of assignment or part icipationand similar instruments with recourse: Provided, however, That debt instruments issued for interbank call loanswith maturity of not more than five (5) days to cover deficiency in reserves against deposit liabilities, includingthose between or among banks and quasi-banks, shall not be considered as deposit substitute debt instruments.

A deposit substitute is a means of borrowing money from the public (20 or moreindividual or corporate lenders) other than by way of deposit with banks through the

issuance of debt instruments.

Sale of shares

Tax Rate on Income from Sale, Barter, Exchange or

other Disposition of Shares of Stock (RR 6-2008)

If shares of stock are listed and traded through the local

stock exchange

½ of 1% (or .005%) of the

gross selling price or grossvalue in money of theshares of stock

If shares not traded through the local stock exchange

o Capital gains not over P100,000

o Capital gains in excess of P100,0005% of the net capital gains10% of the net capital gains

FCDU

Income of non-residents (individuals or corporations) from transactions with depositorybank under the expanded FCD system are exempt.

Intercorporate dividends

Dividends received by a domestic corporation from another domestic corporation shall

not be subject to tax.o Why? Law assumes that the dividends received will be injected to the capital,

which will eventually be taxed when the corporation gets income from the use ofthe capital.

Sale of realty

Final Tax Rate on Sales, Exchanges, or Transfers or RealProperties Classified as Capital Assets (RR 8-98)

Sale of real property in the Philippines 6% of the gross sellingprice, or the current

market value at the time

of sale, whichever is

higherIf sale was made to the government or to GOCCs Either 6% of the gross

selling price/currentmarket value or under

the normal income taxrate, taxpayer’s option

Creditable Withholding Tax on Sales, Exchanges or

Transfers of Real Properties classified as Ordinary Assets

8/12/2019 Taxation One Complete

http://slidepdf.com/reader/full/taxation-one-complete 23/90

+amdg

Taxation One: Outline with Codals

Mickey Ingles2A (2C) Ateneo Law 2012Atty. Montero (Updated: December 14, 2011 – Mickey)

23

(RR 8-98)

1. If the seller is habitually engaged in the real estate business

o Selling price is less than P500,000o Selling price is P500,000 to P2m

o Selling price is above P2m

1.5%3%

5% of gross selling

price/current market

value, whichever ishigher

2. If the seller is not habitually engaged in the real estatebusiness

7.5% of gross sellingprice/current marketvalue, whichever is

higher

3. If the seller is exempt from creditable withholding tax as perRR 2-98

Exempt

If the mortgagor exercises his right of redemption within 1 year, no capital gains tax.

In case of non-redemption, the capital gains will be due based on the bid price of thehighest bidder. (RR 4-99)