taxation of extractive industries in east and central … industries in east and central africa are...

TRANSCRIPT

Taxation of extractive industries in East and Central Africa Are these in harmony?

Page 2

Moderator Panel

Max Mangoro Silke Mattern Albena Todorova

Partner EY Zimbabwe

Partner EY Tanzania

Partner EY Mozambique

Nelson Mwila

Tax Principal EY Zambia

Panel

Africa Tax Conference™ 2015

Page 3

► Mining industry is unique and not easily comparable with other generic economic sectors

► Resources are owned by the state but mostly extracted by private sector ► High risk as there is no guarantee of discovery or mine profitability ► Development is capital intensive with long lead times ► Mineral prices and exchange rates are highly volatile ► Mining can be long lived

Africa Tax Conference™ 2015

Mining sector The facts

Page 4

► Countries must compete for highly mobile international exploration and development investment capital.

► Explorers are attracted by potential prospects. ► Mine developers are attracted by profitability:

► Mining companies by stability (political, social and fiscal)

Africa Tax Conference™ 2015

A competitive world

Page 5

► A competitive and attractive mining fiscal regime is key for investment and mining recovery

► This has been the case for many countries that have witnessed mining sector growth over the past two decades

► According to the United Nations (UN) survey of mining companies (2005), 60% of the top 10 decision criteria a prospective mining investor considers before undertaking a mining project (investment) are tax related

Africa Tax Conference™ 2015

The need for a competitive and stable fiscal regime

Page 6

Top 10 Factors considered by investors

Top 10 factors considered by investors Related to tax?

1. Geological potential for target mineral No

2. Profitability of potential operations Yes

3. Security of tenure and permitting No

4. Ability to repatriate profits Yes

5. Ability to predetermine tax liability Yes

6. Stability of tax regime Yes

7. Consistency of minerals policies Yes

8. Realistic foreign exchange controls No

9. Stability of exploration terms and conditions Yes

10. Ability to predetermine environmental obligations No

Africa Tax Conference™ 2015

Page 7

► At the first ATRN (African Tax Administration Forum) International tax workshop held at Victoria Falls in September 2013, the International Monetary Fund (IMF); African Regional Technical Assistance Centre (Afritac) East representatives said that governments’ shares of mining income should be: ► 40% to 60% in mining ► 65% to 85% in petroleum

► And that shares below this range should be cause for concern and regret: ► In 2013, Zimbabwe miners contributed 13% to fiscus, which was 17% of mining

income. (source Reserve Bank of Zimbabwe (RBZ), Communications Zone (COMZ)

Africa Tax Conference™ 2015

Natural resources taxation

Page 8

Discussion

Africa Tax Conference™ 2015

Page 9

The extractive industry tax life cycle

The extractive industry as a whole has a life cycle that is subject to different taxes.

Exploration Development and production Close down

Africa Tax Conference™ 2015

Page 10

Incentives and challenges

Africa Tax Conference™ 2015

Page 11

Multiple taxes and tax rates

Rate (%)

Tax head Tanzania Zambia Zimbabwe Mozambique

Royalties 3, 5, 15 6 and 9 1 to 15 1.5 to 8

Corporate tax 30 30 15 and 25 32

Withholding tax 5, 10, 15 20 0 &15

VAT 18 16 15

Customs duty 0-25 0 to 20 0 to 60

Capital gains tax 30 1, 5, 20

PAYE 0 to 30 0 to 35 0 to 50

Windfall taxes - Yes APT ( sml) -

MRTT 10

MRRT 20

Africa Tax Conference™ 2015

Page 12

► In the past five years, many countries in the region have adopted low and stable mining royalty regimes.

► This has enabled countries such as Mozambique, Zambia, Democratic Republic of Congo (DRC) and Tanzania more than double their Foreign Direct Investment (FDI) in the mining sector.

► Zimbabwe has been different, as rates changed five times, with for gold and platinum going up by more than 100% and 200% respectively.

Africa Tax Conference™ 2015

Need for fiscal stability Example: royalty

2009 Mid 2010 2010 2011 2012 2013

Platinum 3 3.50 4 5 10 10

Gold 3 3.50 4 4.50 7 7

Page 13

► Capital expenditure incurred exclusively for mining operations is deductible at a rate of 100%/150% (in year cost incurred)

► There are fiscal stability clauses in mineral development agreements (MDAs) ► There is ring fencing per mining concession ► 3 (MDAs) or 5% witholding tax (WHT) for local service suppliers

Africa Tax Conference™ 2015

Tanzania mining tax incentives

Page 14

► MDAs are not always upheld by revenue authority ► MDAs have no real fiscal stability in newer agreements ► Agreed royalty rates (gold) were renegotiated ► VAT refund claims ► Fuel levy ► Significant administrative burden of reporting ► Capital gains tax (CGT) on indirect share transfers

Africa Tax Conference™ 2015

Challenges in Tanzanian mining regime

Page 15

► Customs duties exemption: ► Customs duties exemption on the importation of class K goods, as well as other tools

and machinery listed in the legislation, to be applied in the mining operations ► VAT

► Exemption from VAT on services related to drilling, exploration and construction of infrastructure within the mining activity in the research and exploration phase

Africa Tax Conference™ 2015

Mozambique incentives to mining sector

Page 16

► New legislation with no regulations as yet ► Developing industry knowledge by tax authorities ► Tax authority systems not yet adapted to new legislation requirements (ring

fencing) ► VAT burden and refund challenges ► Taxation on group restructuring and transfer of mining rights

Africa Tax Conference™ 2015

Mozambique tax challenges

Page 17

► No dividend withholding tax by a company carrying on mining operations ► Losses are carried forward for a period not exceeding 10 years; however,

losses to be set off in a charge year is limited to 50% of the income from the mining operation

► There are rebates on specific imported materials and consumables

Africa Tax Conference™ 2015

Zambia tax incentives

Page 18

► 2015 experienced two mining tax regimes, namely: ► 0% corporation income tax rate from 1 January to 30 June 2015 ► 8% royalty for underground mining and 20% for open cast mining

► From 1 July 2015, this regime was reversed as follows: ► 30% corporation income tax rate was reinstated ► 6% royalty for underground mining and 9% for open cast mining

► Unpredictable copper prices

Africa Tax Conference™ 2015

Challenges from the Zambia mining tax regime

Page 19

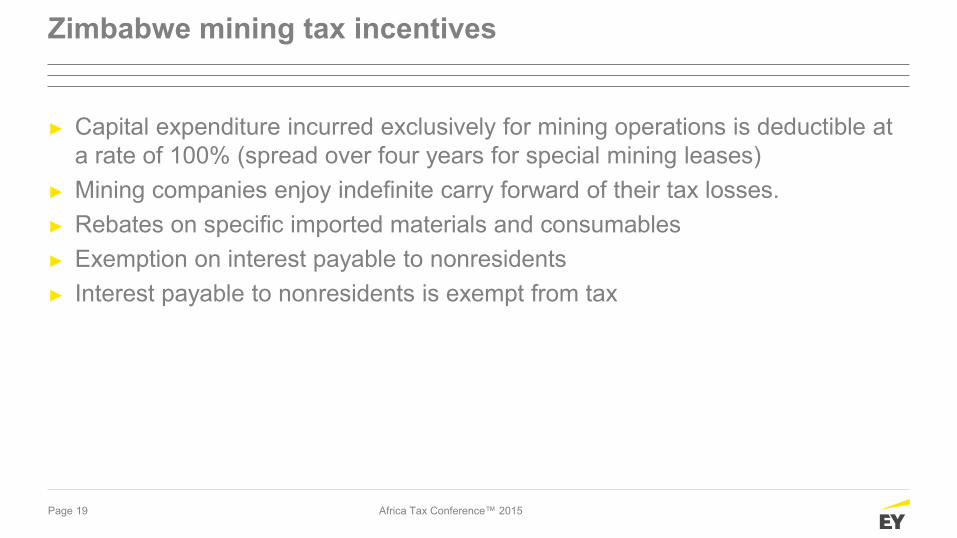

► Capital expenditure incurred exclusively for mining operations is deductible at a rate of 100% (spread over four years for special mining leases)

► Mining companies enjoy indefinite carry forward of their tax losses. ► Rebates on specific imported materials and consumables ► Exemption on interest payable to nonresidents ► Interest payable to nonresidents is exempt from tax

Africa Tax Conference™ 2015

Zimbabwe mining tax incentives

Page 20

► High and unpredictable royalty tax burden ► Non - tax deductibility of royalty ► Apparent lack of coordination between government departments and agencies

when levying charges and fees to mining companies ► High Environment Management Agency’s charges ► High - ground and related mining fees and charges ► Non - uniformity of rural district charges

Africa Tax Conference™ 2015

Challenges from the Zimbabwe mining tax regime

Page 21

► Resource nationalism has taken the following forms: ► Mandated beneficiation ► State ownership or participation ► Taxes or royalties and windfall profits taxes ► Mining reform ► Import/export restriction ► Transparency ► Retreating resource nationalism: returning focus to investment attraction

Africa Tax Conference™ 2015

Resource nationalism update

Page 22

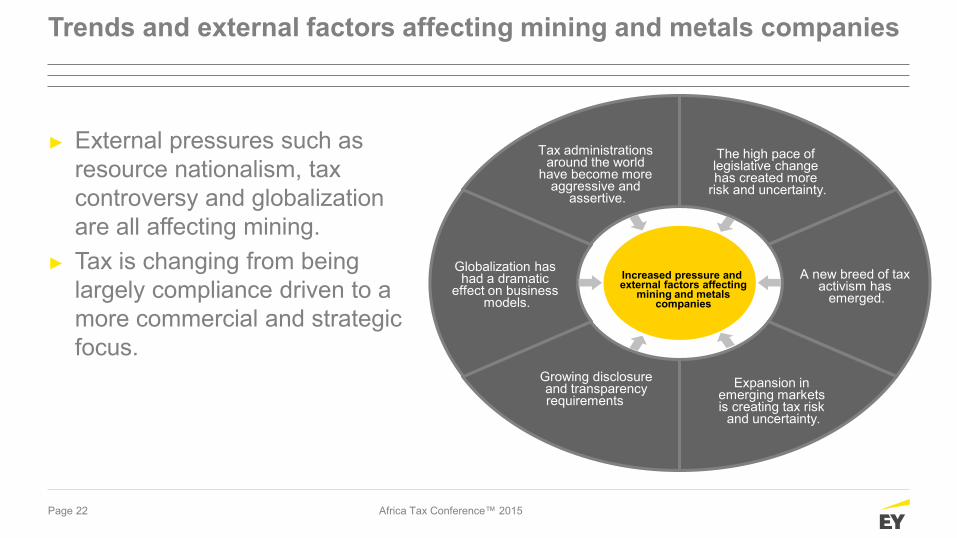

► External pressures such as resource nationalism, tax controversy and globalization are all affecting mining.

► Tax is changing from being largely compliance driven to a more commercial and strategic focus.

Africa Tax Conference™ 2015

Trends and external factors affecting mining and metals companies

The high pace of legislative change has created more

risk and uncertainty.

Growing disclosure and transparency requirements

Expansion in emerging markets is creating tax risk

and uncertainty.

A new breed of tax activism has

emerged.

Globalization has had a dramatic

effect on business models.

Tax administrations around the world

have become more aggressive and

assertive.

Increased pressure and external factors affecting

mining and metals companies

Page 23 Africa Tax Conference 2015

The pendulum of risk has swung

► Economic uncertainty ► Volatile markets ► Massive capital outlays

► Squeezed margins ► Suboptimal returns ► Impairments

► Weaker prices ► Cost inflation ► Cost overruns

► More conservative approach to risk, including tax risk, by mining and metals companies

► Would you describe the focus on tax planning and reporting as aggressive, assertive, conservative or passive?

Page 24

Presentations to the board include:

Greater engagement with the board

Africa Tax Conference™ 2015

Tax exposures Effective tax rate

Interaction with tax authorities’ audits, claims and disputes

Transactions

Changes in tax interpretations or

laws in jurisdictions

where they have operations

Tax provisions

Page 25

Main challenges facing the tax function

Africa Tax Conference™ 2015

What are the main challenges facing tax functions?

Page 26

“increases — the more you have the me they want.” — Survey respondent

► The world’s tax administrations are joining forces at a startling speed, and concepts and processes are being shared.

► 72% of tax directors at mining and metals companies report a substantial increase in controversy with authorities.

Question: if controversy has increased, what areas have tax authorities considered or reviewed?

Africa Tax Conference™ 2015

Growing wave of mining tax controversy

Page 27

► KPI’s for senior tax personnel are aligned to business strategy, with a focus on the importance of risk mitigation and increasing cash flow.

Question: what are the key performance indicators for tax function personnel within organizations?

Africa Tax Conference™ 2015

What are companies focusing on: set KPIs

Effective tax rate / minimizing tax burden

Timely compliance

Risk mitigation

72%

25%

28%

38%

43%

5%

Page 28

Question: what are the top considerations in tax planning?

Africa Tax Conference™ 2015

Aligning the tax agenda with the business agenda

Page 29

Conclusions

Africa Tax Conference™ 2015

Page 30

► Most of the tax heads in the Southern African Development Community countries are similar; the major differences are on the rates of the taxes

► Royalties are the most common form of taxation ► Tax administrations collaborate with other tax administrations with developed

skills ► Transfer pricing and tax avoidance are the flavors of the moment ► Countries have the same transparency requirements; for example, Tanzania,

Zambia and Mozambique, who are already Extractive Industries Transparency Initiative (EITI) compliant

► Countries that have adopted low and stable mining royalty regimes have attracted more FDI

Africa Tax Conference™ 2015

Conclusions

EY | Assurance | Tax | Transactions | Advisory About EY EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities. EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com. © 2015 EYGM Limited. All Rights Reserved. EYG no. DL1426 This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice. ey.com