tax planning using private corporations. 25 2017... · using private corporations. september 25,...

TRANSCRIPT

USING PRIVATE CORPORATIONS.

September 25, 2017

TAX PLANNING

Canadian Tax Foundation

Outline

• Policy context

• Historical context: current rules

• Consultations: approaches put forward for discussion

• Key questions for discussion

2Department of Finance – September 2017

Increasing Incentives for Tax Planning Using

a Private Corporation

The growing gap between corporate and personal income

tax rates since 2000 has increased rewards associated with

tax planning in a private corporation…

… Over this period, a growing share of

high-income self-employed individuals have

chosen to incorporate

Department of Finance - July 2017 3

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

55%

2000 2002 2004 2006 2008 2010 2012 2014 2016

Federal-Provincial Tax Rates

Combined Federal-Provincial

Small Business Rate: 14.4% (2017)

Combined Federal-Provincial

General Corporate Income Tax Rate: 26.7% (2017)

Top Combined Federal-Provincial Personal Income Tax

Rate: 51.6% (2017)

37.2

percentage

point gap

(2017)

0%

1%

2%

3%

4%

5%

6%

7%

8%

2001 2003 2005 2007 2009 2011 2013

Ta

xa

ble

Active

In

co

me

/ G

DP

Trend in Taxable-Active-Income-to-GDP Ratio, by Type of Business

Canadian Controlled Private Corporations (CCPCs)

Public Corporations and Private Corporations other than CCPCs

Individuals with Self-employment Income

Integration

• Low corporate tax rates on business income are intended to provide

a tax advantage as long as income is retained for active business

reinvestments.

• Income that is paid out of a corporation as a dividend is generally

meant to be subject to the same amount of tax as income received

directly by the individual.

Corporate taxes on earnings + Personal taxes on dividends = Personal

taxes on income earned directly

• Integration issue: incentive to hold savings financed by retained

earnings within corporations to save taxes

• This issue was recognized in 1972

4Department of Finance - July 2017

Historical context: Current rules

• Current system introduced in 1972

• Refundable taxes on investment income ensure integration when

business owner uses after-tax income to finance a passive portfolio

within a corporation

• In 1972, the introduction of Part V tax ensured integration when

using retained earnings to finance a passive portfolio

• Part V tax repealed on the basis that:

• It was seen as complex

• This added complexity was believed not necessary

I believe that these small corporations which enjoy the benefit of the lower rate of tax will, in fact, use these savings to expand their businesses, to improve their technology and to create more jobs for Canadians

5Department of Finance - July 2017

Consultations

• Government is seeking input on best manner to eliminate deferral

advantages going forward

• Paper lays out two broad approaches:

• Reintroduction of Part V tax, with adjustments

• Introduction of a deferred taxation model

- A deferred taxation model could take various forms, two of which are described in the paper:

• Apportionment approach

• Elective approach

6Department of Finance - July 2017

Reintroduction of Part V Tax

• Imposition of an upfront tax when retained earnings are used to

acquire passive investments

• This additional tax would bridge the gap with top PIT rate

- For example, a business eligible for the small business deduction would pay a 35% additional tax at the time of acquisition of portfolio assets

• Tax refundable if later on assets are used to reinvest in the business

• Need to keep track of income streams in order to apply the appropriate amount of tax when investment assets are purchased

• Passive investment income would continue to be taxed as per

current rules

7Department of Finance - July 2017

Deferred Taxation Model: Apportionment Approach

• Need to track source of financing for passive investments in order to

estimate deferral

• Affects businesses at the moment of dividend payout:

• Affects tax outcomes at the moment a dividend is paid out, rather than when an investment asset is acquired

- But in effect, same overall outcome as Part V tax

• Those saving to reinvest in their business not materially affected

• Precision in tax outcomes, tailored to various business situations

8Department of Finance - July 2017

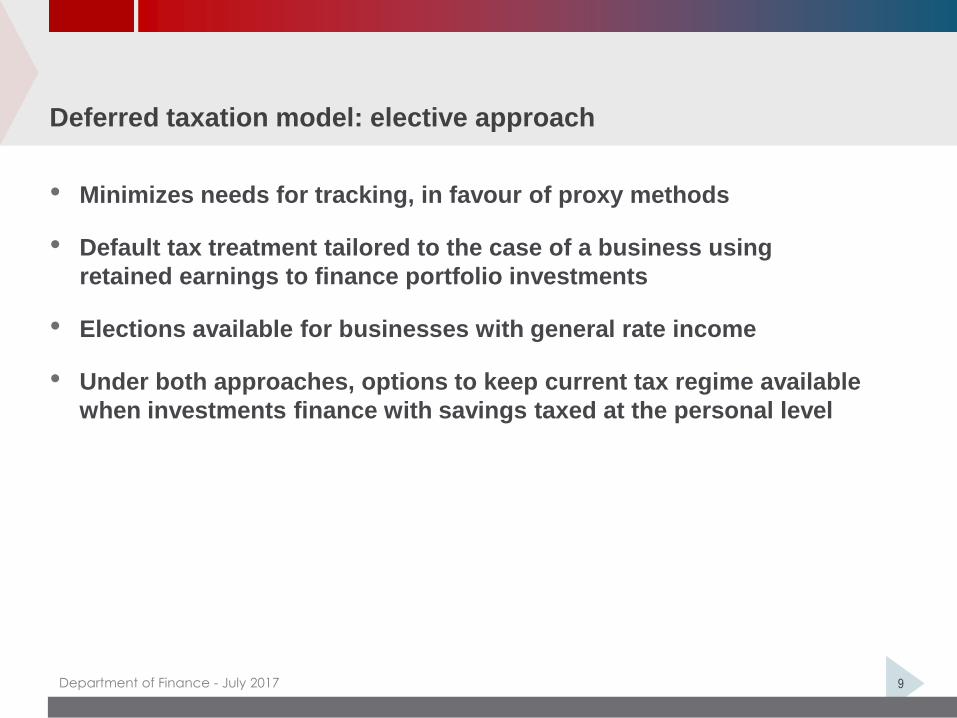

Deferred taxation model: elective approach

• Minimizes needs for tracking, in favour of proxy methods

• Default tax treatment tailored to the case of a business using

retained earnings to finance portfolio investments

• Elections available for businesses with general rate income

• Under both approaches, options to keep current tax regime available

when investments finance with savings taxed at the personal level

9Department of Finance - July 2017

Key questions for discussion

• Government is seeking feedback, in particular:

• What is the best approach to tackle the issue?

• How to minimize complexity, while achieving policy objectives?

• Capital dividend account: what is the appropriate scope of the new tax regime with respect to capital gains?

• Transition issues

10Department of Finance - July 2017

Disclaimer:

This material is for educational purposes only and is not intended to be

advice on any particular matter. No one should act on the basis of any

matter contained in these materials without considering appropriate

professional advice. The presenters expressly disclaim all liability in

respect of anything done or omitted to be done wholly or partly in

reliance upon the contents of these materials.

Tax Planning Using Private Corporations -

July 18, 2017:

Analysis and Discussion with FinanceOttawa, ON

Ted Cook, Director – Tax Legislation Division Department of Finance (Canada)

Income Sprinkling and Conversion of Dividends into Capital Gains

2 2017 Taxation of Private Corporation Policy Conference

INCOME SPRINKLING

3 2017 Taxation of Private Corporation Policy Conference

Overview

● Tax-planning arrangements under which income that would otherwise have been taxed as income of a high-income individual in the absence of the “income sprinkling” arrangement is instead taxed as income of a lower-income individual, typically a family member of the high-income individual

● The intended effect of the arrangement is to have the income subject to a lower or nil effective rate of income tax by accessing otherwise unused tax attributes of the lower-income individual

● Tax benefits from income sprinkling increase with: The difference in tax rates between the transferor and the transferee

The amount of income that can be sprinkled

The number of individuals who can receive the sprinkled income

Income Sprinkling

4 2017 Taxation of Private Corporation Policy Conference

Example

● In base scenario, net earnings are taxable at full PIT rates in the hands of the self-employed individual

● In the scenario where the individual incorporates, the after-CIT profits are paid out as dividends to the owners of the CCPC, including the individual’s spouse and adult child

● Taxes are reduced because the spouse and adult child do not pay federal tax on the dividend income

Income Sprinkling

CCPC

Owner Owner Spouse Child

Federal CIT (10.5%) n/a $23,000 n/a n/a n/a

Provincial CIT (4.5%) n/a $10,000 n/a n/a n/a

Federal PIT $49,000 n/a $11,000 $200 $200

Provincial PIT (ON) $30,000 n/a $9,000 $500 $500

Total tax $79,000

Average tax rate 36%

$54,000

25%

Net self-employment earnings of $220,000

Net profits of $220,000

Post-CIT $187K dividend allocated60%/20%/20% among Owner, Spouse and Child

Base Scenario:Self-employed Incorporated

$112,000 $37,000 $37,000

5 2017 Taxation of Private Corporation Policy Conference

Dividends by Age

Income Sprinkling

0

100

200

300

400

500

600

700

800

900

1,000

0 2 4 6 810

12

14

16

18

20

22

24

26

28

30

32

34

36

38

40

42

44

46

48

50

52

54

56

58

60

62

64

66

68

70

72

74

76

78

80

82

84

86

88

90

92

94

96

98

10

0

No

n-e

lig

ible

div

ide

nd

s ($

mil

lio

n)

Age

2006

2010

2014

6 2017 Taxation of Private Corporation Policy Conference

Issue

● The use of a private corporation in particular facilitates income sprinkling

arrangements

● Income sprinkling raises a number of tax policy concerns

High income individuals able to control income and to whom it is paid can obtain

tax benefits not available to those who do not control income

Erodes tax base

Income Sprinkling

7 2017 Taxation of Private Corporation Policy Conference

Existing Rules

● Existing rules that constrain income sprinkling Longstanding rule restricts the deduction of expenses (including salary) if amount not reasonable

Attribution rules apply to gift arrangements to redirect income back to the high-income individual

Tax on split income (TOSI) introduced in 1999

● Existing rules not fully effective in constraining sprinkling with adults Attribution rules apply to spouses, but tax planning can circumvent the rules

Limited rules to address arrangements involving other adults (such as children)

Jurisprudence has limited the effective scope of some of the rules: 1998 Neumann decision (Supreme Court of Canada)

● Some structures have been identified that seek to circumvent the TOSI rules applicable to minors

Income Sprinkling

8 2017 Taxation of Private Corporation Policy Conference

LCGE Multiplication

● The Lifetime Capital Gains Exemption (LCGE) provides an exemption in computing

taxable income in respect of capital gains realized by individuals on the disposition

of qualified farm or fishing property (QFFP) and qualified small business

corporation shares (QSBCS)

● By having family members (or a family trust) as shareholders of the QSBC, the

LCGE limit of each family member can be accessed on a disposition of the QSBCS

● This raises a concern the individuals may be able to claim the LCGE even though

they may not have invested in, or otherwise contributed to, the business value

reflected in the capital gains from the disposition of the QSBCS

Income Sprinkling

9 2017 Taxation of Private Corporation Policy Conference

Policy Response

Proposals to address income sprinkling

● Expand TOSI rules to Canadian resident individuals, whether minor or adult, who receive ‘split income’

● Refine ‘split income’ definition Include new categories of amounts, such as corporate debt

Income received by an individual over 17 from a corporation will only be split income if a related individual (a ‘connected individual’) has a certain measure of influence over the corporation

● Introduce a reasonableness test to determine whether split income received by an individual over 17 will be subject to the TOSI The test is more stringent for individuals between 18 and 24

Income Sprinkling

10 2017 Taxation of Private Corporation Policy Conference

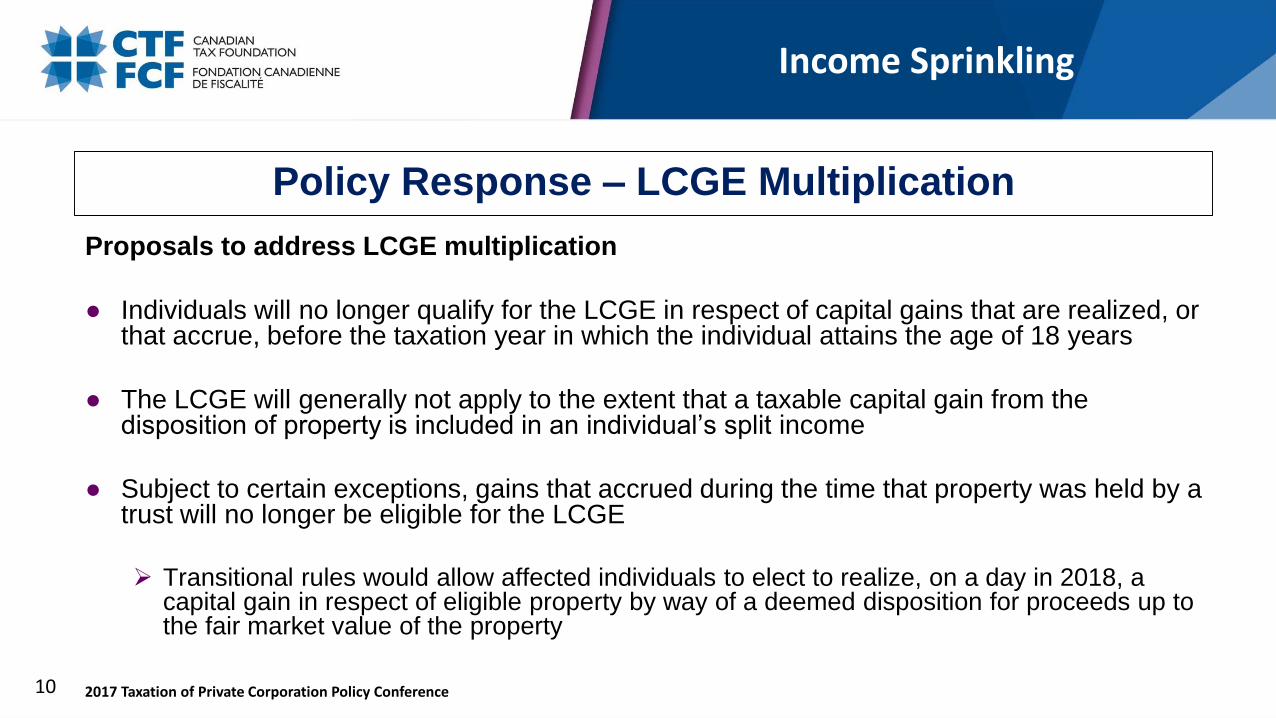

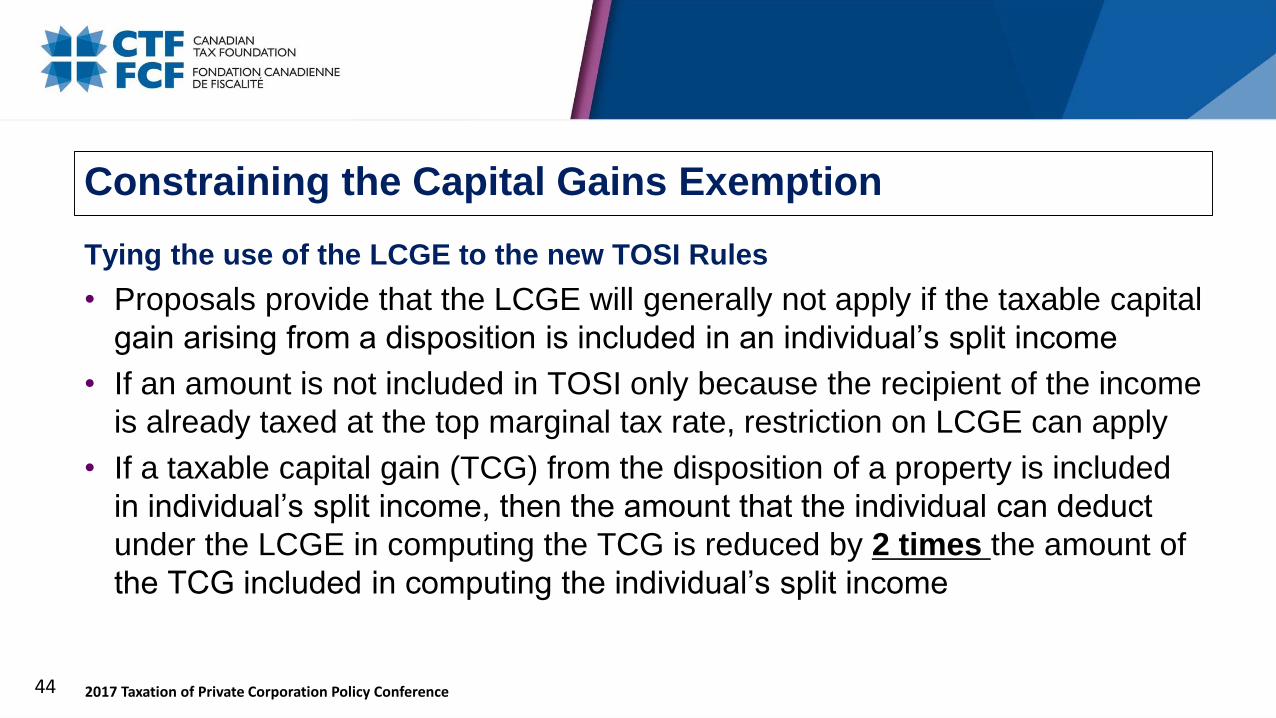

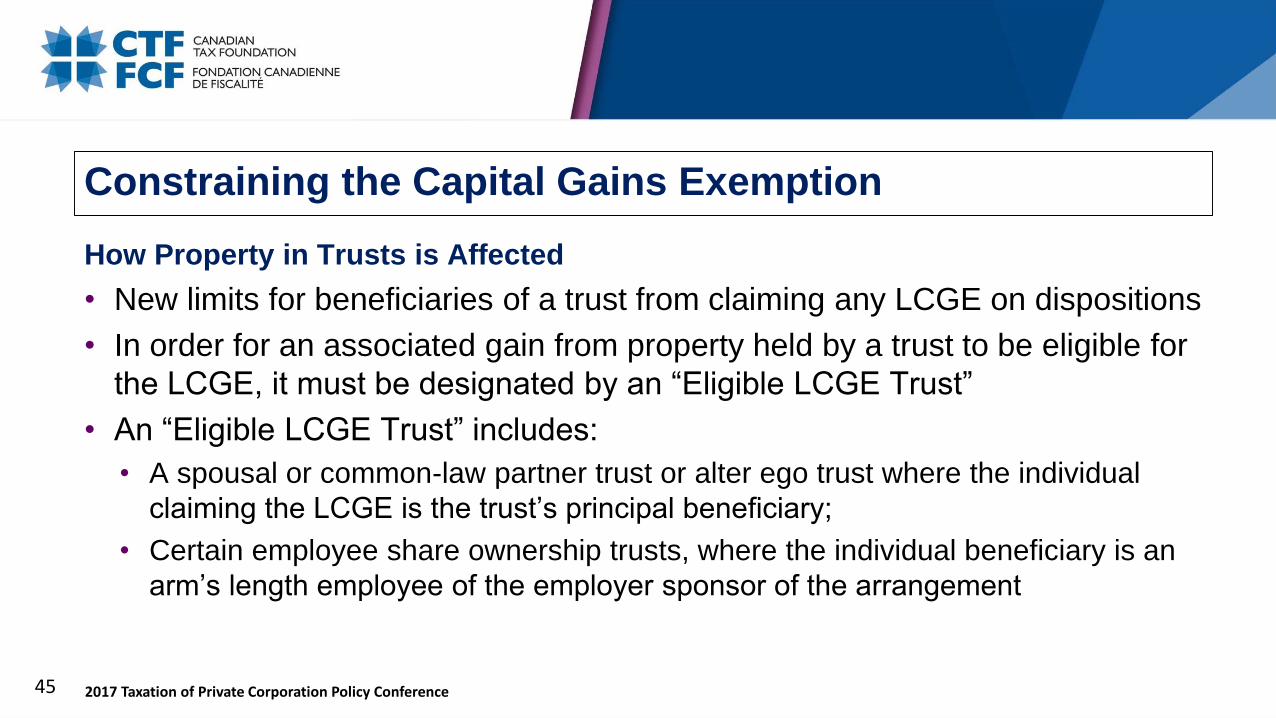

Policy Response – LCGE Multiplication

Proposals to address LCGE multiplication

● Individuals will no longer qualify for the LCGE in respect of capital gains that are realized, or that accrue, before the taxation year in which the individual attains the age of 18 years

● The LCGE will generally not apply to the extent that a taxable capital gain from the disposition of property is included in an individual’s split income

● Subject to certain exceptions, gains that accrued during the time that property was held by a trust will no longer be eligible for the LCGE

Transitional rules would allow affected individuals to elect to realize, on a day in 2018, a capital gain in respect of eligible property by way of a deemed disposition for proceeds up to the fair market value of the property

Income Sprinkling

11 2017 Taxation of Private Corporation Policy Conference

CONVERSION OF DIVIDENDS INTO CAPITAL GAINS

12 2017 Taxation of Private Corporation Policy Conference

Overview

● Dividends are taxed at a higher rate than capital gains, which are only one-half taxable

● Individual shareholders can reduce their income taxes by converting corporate income (e.g., amounts that would otherwise be paid out as dividends) into capital gains

● The federal and provincial tax savings in 2016 associated with converting dividends into lower-taxed capital gains is approximately $17,500 per $100,000 of conversions of ineligible dividends (at the average/highest

provincial tax rate for ineligible dividends paid from corporate earnings taxed at the small business rate)

$11,100 per $100,000 of eligible dividends (at the average/highest provincial tax rate for eligible dividends paid from corporate earnings taxed at the 15% general rate)

Conversion of Dividends

13 2017 Taxation of Private Corporation Policy Conference

Section 84.1 – Dividend Treatment (applicable)

● Section 84.1 addresses individual tax avoidance that can arise when an individual sells shares of a Canadian corporation to another corporation related to the individual (e.g., owned by individual, spouse, siblings, children/grandchildren)

● Such share sales could, absent section 84.1, be used to convert dividends in the hands of the individual into lower-taxed capital gains, including gains eligible for the Lifetime Capital Gains Exemption (LCGE) This is because the related corporation could pay the individual with the proceeds of a

dividend from the Canadian corporation, which the related corporation can receive tax-free because the inter-corporate dividend deduction is available

● To prevent this result, the proceeds from the share sale are treated as a taxable dividend and not as a capital gain if section 84.1 applies

Conversion of Dividends

14 2017 Taxation of Private Corporation Policy Conference

Section 84.1 – Capital Gains (inapplicable)

● Section 84.1 does not apply on a sale of shares by individuals to their

children, to any other related individual, or any arm’s length person

Individuals can claim capital gains treatment – including the LCGE, where

available – on a direct sale of shares to their children

It is not necessary for section 84.1 to apply in this case because the individual

purchaser would face dividend taxation if they attempt to withdraw earnings of

the corporation

Conversion of Dividends

15 2017 Taxation of Private Corporation Policy Conference

Avoidance of Section 84.1 (cont’d)

● The conversion of dividends into lower-taxed capital gains ineligible for the

LCGE benefits owners of both large and small private corporations

● Section 84.1 applies only to sales by individuals to corporations and can be

avoided

Conversion of Dividends

16 2017 Taxation of Private Corporation Policy Conference

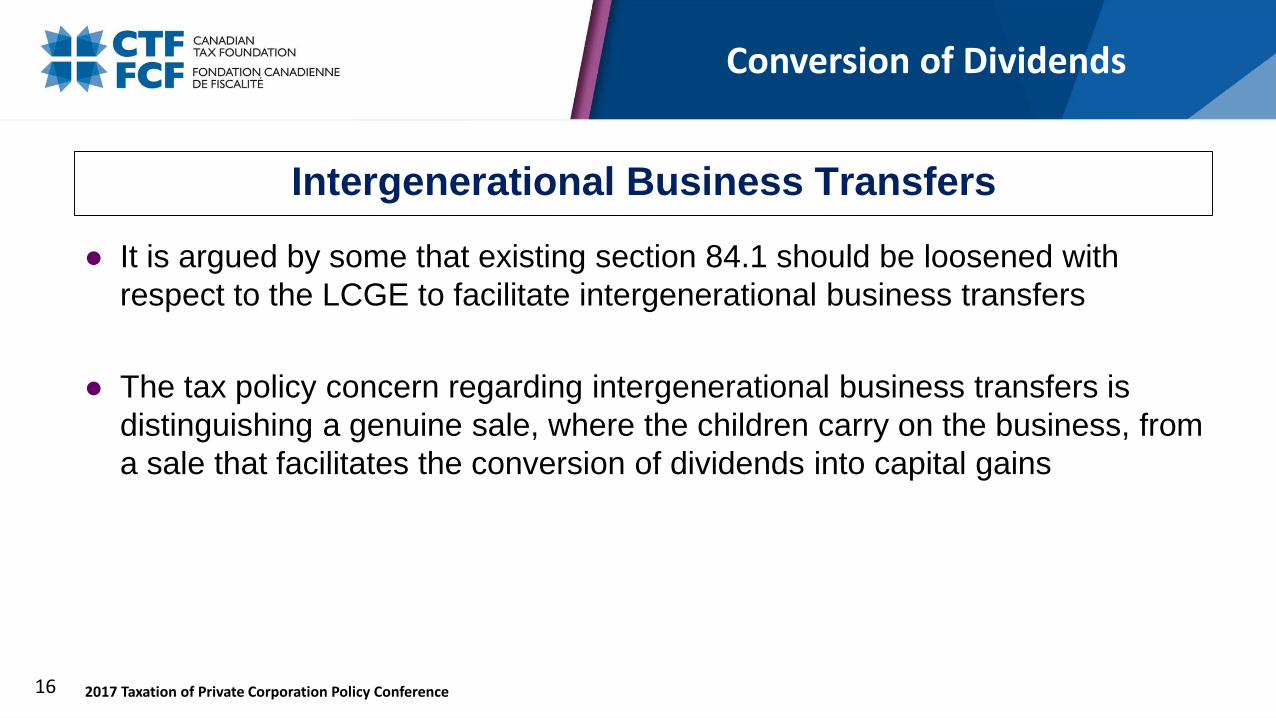

Intergenerational Business Transfers

● It is argued by some that existing section 84.1 should be loosened with

respect to the LCGE to facilitate intergenerational business transfers

● The tax policy concern regarding intergenerational business transfers is

distinguishing a genuine sale, where the children carry on the business, from

a sale that facilitates the conversion of dividends into capital gains

Conversion of Dividends

17 2017 Taxation of Private Corporation Policy Conference

Policy Response

● Proposed amendment to section 84.1 to address “multi-step” planning

● Proposed introduction of a supporting anti-avoidance rule to address other

transactions that could be used to convert dividends into capital gains

● Comments sought regarding whether, and how, it would be possible to

better accommodate genuine intergenerational business transfers while still

protecting against potential abuses

Conversion of Dividends

Disclaimer:

This material is for educational purposes only and is not intended to be

advice on any particular matter. No one should act on the basis of any

matter contained in these materials without considering appropriate

professional advice. The presenters expressly disclaim all liability in respect

of anything done or omitted to be done wholly or partly in reliance upon the

contents of these materials.

Tax Planning Using Private Corporations -

July 18, 2017:

Analysis and Discussion with FinanceOttawa, ON

Speaker name: David G. Duff Affiliation: Allard School of Law, University of British Columbia

Passive Income: Historical and Legislative Context and Comments

2 2017 Taxation of Private Corporation Policy Conference

Background to Proposals

● long-term reductions in corporate rates (general and small business) and

recent increases in personal rates – incentive to earn and retain income in a

corporation (both for business and non-business purposes)

● lower tax on capital gains than dividends with LCGE and 50% inclusion rate

– incentive for surplus stripping

● individual unit and progressive rates – incentive for income-splitting and

multiplication of LCGE, facilitated by SCC decision in Neuman (1998),

limited scope of TOSI in section 120.4, and provincial regulatory changes

Passive Income: Historical and Legislative Context and Comments

3 2017 Taxation of Private Corporation Policy Conference

Is there a problem?

● 50% growth in CCPCs from 2001 to 2014

● substantial increase in ABI of CCPCs as a share of GDP and decrease in

self-employment income as a share of GDP

● revenue losses, efficiency/neutrality concerns, and implications for tax

fairness (horizontal and vertical equity)

● are all these tax benefits necessary to encourage small businesses?

Passive Income: Historical and Legislative Context and Comments

4 2017 Taxation of Private Corporation Policy Conference

Possible Structural Reforms

● reduce personal rates, increase corporate rates, adopt a single corporate rate,

and/or adopt a dual rate income tax with higher and progressive rates on labour

income and a lower flat rate on capital income

● repeal LCGE and increase capital gains inclusion rate to restore symmetry between

effective tax rate on capital gains and dividends

● flatten rates and/or adopt a spousal or familial unit either generally or for specific

tax benefits like the LCGE

Passive Income: Historical and Legislative Context and Comments

5 2017 Taxation of Private Corporation Policy Conference

Alternatives to Structural Reforms

● rules denying low corporate rates (and LCGE) to specific categories of taxpayers,

to income other than active business income (passive income), and/or to income

used to acquire assets not used in an active business (passive investments)

● anti-avoidance rules to prevent surplus stripping

● attribution and other rules (like the TOSI) to regulate income-splitting and

multiplication of LCGE

Passive Income: Historical and Legislative Context and Comments

6 2017 Taxation of Private Corporation Policy Conference

Rules Excluding Specific Kinds of Taxpayers

● personal services businesses (incorporated employees) excluded from SBD after

November 12, 1981

● > 5 FTE exception (arm’s length until 1984)

● additional 5% federal tax applicable after 2015 (so 33%)

● non-qualifying businesses (professional practices of accountants, dentists, lawyers,

doctors, veterinarians, chiropractors and certain services businesses) excluded

from SBD from 1979 to 1984

● Quebec approach limits SBD to primary and manufacturing businesses or

businesses with a minimum number of employees (at least 5,500 hours)

Passive Income: Historical and Legislative Context and Comments

7 2017 Taxation of Private Corporation Policy Conference

Higher Rates on Passive Income

● portfolio dividends received by private or subject corporations – refundable Part IV

tax (similar to effective tax rate on non-eligible dividends)

● investment income of a CCPC – not eligible for SBD, additional tax under section

123.3, partly refunded (but not fully integrated)

● includes income from property, income from a specified investment business [> 5 FTE

exception], and net taxable capital gains

● excludes income from property incident or pertaining to an active business or used or

held principally for the purpose of gaining or producing income from an active business

● cases generally recognize reasonable reserves for business purposes but not passive

investments for later investment in active business

Passive Income: Historical and Legislative Context and Comments

8 2017 Taxation of Private Corporation Policy Conference

Higher Rates on Income Used to Acquire Passive Investments

● refundable tax on ineligible investments – enacted in 1972 and retroactively

repealed in 1973

not “actively” considered by the Government “at the present time” due to liquidity

issues

● alternative approach: deferred taxation with no dividend refund for tax on

investment income, and tax on dividends (including dividends from the non-

taxable portion of capital gains) based on the source of the capital used to

acquire passive investments (apportionment or elective methods)

consultation on “any aspect” of possible rule to tax corporate passive income

Passive Income: Historical and Legislative Context and Comments

9 2017 Taxation of Private Corporation Policy Conference

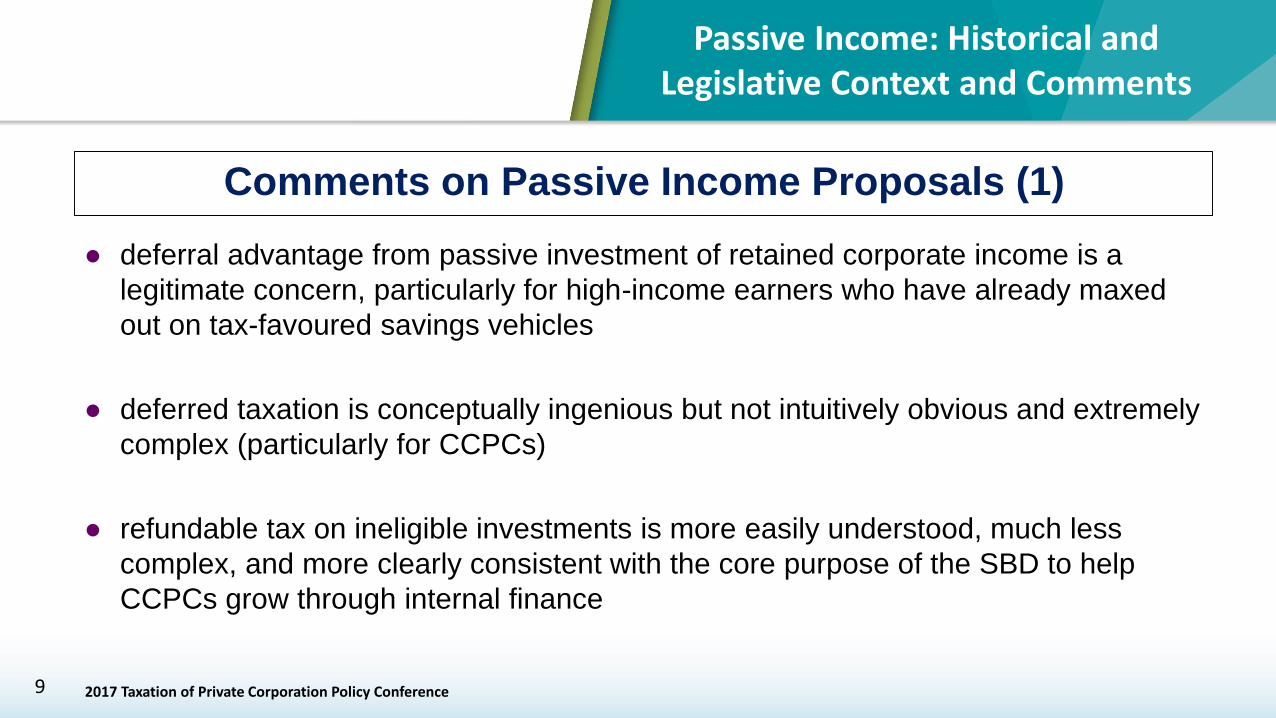

Comments on Passive Income Proposals (1)

● deferral advantage from passive investment of retained corporate income is a

legitimate concern, particularly for high-income earners who have already maxed

out on tax-favoured savings vehicles

● deferred taxation is conceptually ingenious but not intuitively obvious and extremely

complex (particularly for CCPCs)

● refundable tax on ineligible investments is more easily understood, much less

complex, and more clearly consistent with the core purpose of the SBD to help

CCPCs grow through internal finance

Passive Income: Historical and Legislative Context and Comments

10 2017 Taxation of Private Corporation Policy Conference

Comments on Passive Income Proposals (2)

● tax on ineligible investments puts pressure on distinction between passive

investments for business purposes and passive investments for personal

wealth accumulation

passive investment to finance later expansion?

passive investment to finance parental leave?

passive investment with mixed purposes (retirement and business

emergencies)?

● consider combining a tax on ineligible investments with safe harbours or a

threshold, which might also help address liquidity issues

Passive Income: Historical and Legislative Context and Comments

Disclaimer:

This material is for educational purposes only and is not intended to be

advice on any particular matter. No one should act on the basis of any

matter contained in these materials without considering appropriate

professional advice. The presenters expressly disclaim all liability in

respect of anything done or omitted to be done wholly or partly in

reliance upon the contents of these materials.

Tax Planning Using Private Corporations -

July 18, 2017:

Analysis and Discussion with FinanceOttawa, ON

Speaker name: Kevin Milligan Affiliation: Vancouver School of EconomicsUniversity of British Columbia

Integration and the Taxation of Passive Income: An Economic Perspective

2 2017 Taxation of Private Corporation Policy Conference

Carter Commission V.4, p. 84

“The system would neither encourage nor

discourage the retention of earnings by

corporations.”

Integration and Passive Income: An Economic Perspective

3 2017 Taxation of Private Corporation Policy Conference

Roadmap

• Why integration?

• Do proposals improve integration?

• How much will the changes affect businesses?

• Caveats on Implementation.

Integration and Passive Income: An Economic Perspective

4 2017 Taxation of Private Corporation Policy Conference

What is Integration?

● Tax at individual level should reflect tax paid at corporate level.

● Or, all paths for a $ from “profit to pocket” should bear same tax.

● Also, no financial gain from readjusting location of savings.

“The system would neither encourage nor discourage the retention of earnings

by corporations.”

Integration and Passive Income: An Economic Perspective

5 2017 Taxation of Private Corporation Policy Conference

Why Integration?

● Neutrality: Target is for people to make same decisions under taxation as

they would without taxation.

This is a free-market goal: business decisions based on the business merits.

This is the literal definition of economic efficiency for taxation.

Integration and Passive Income: An Economic Perspective

6 2017 Taxation of Private Corporation Policy Conference

Why Integration?

● Neutrality: Target is for people to make same decisions under taxation as

they would without taxation.

This is a free-market goal: business decisions based on the business merits.

● Retirement savings? Maternity leaves? ‘Buffer’ savings? Saving for

investment?

These are all fine, but inside/outside firm should be a business decision.

Integration and Passive Income: An Economic Perspective

7 2017 Taxation of Private Corporation Policy Conference

Why Integration?

● Neutrality: Target is for people to make same decisions under taxation as

they would without taxation.

This is a free-market goal: business decisions based on the business merits.

● Retirement savings? Maternity leaves? ‘Buffer’ savings? Saving for

investment?

These are all fine, but inside/outside firm should be a business decision.

● Reminder: the reason we have SBD is to facilitate investment.

Not as a place to tax-advantage savings for those with large portfolios.

Integration and Passive Income: An Economic Perspective

8 2017 Taxation of Private Corporation Policy Conference

Ways Current Integration Falls Short

● It’s notional: still get DTC when firm pays no tax.

Can do direct passthrough of tax bills, e.g. Taiwan; ‘franking’ in Australia

● Fed-Prov: one national gross-up rate for whole country.

● Tax-exempts like pension funds / RRSPs can’t claim DTC.

● Capital gains rate is currently too low compared to dividends/wages.

● Firms claiming SBD have ‘head-start’ deferral advantage for saving.

Integration and Passive Income: An Economic Perspective

9 2017 Taxation of Private Corporation Policy Conference

Does Proposal Improve Integration?

● Focus on high bracket: why?

Flat rate on passive income calibrated for high-bracket investors.

High-bracket investors more likely to have substantial passive portfolios.

● Low-mid bracket investors

Currently disadvantaged for passive saving in CCPC. This shortcoming not

addressed.

More likely to have open RRSP/TFSA room for long-term savings.

Integration and Passive Income: An Economic Perspective

10 2017 Taxation of Private Corporation Policy Conference

Does Proposal Improve Integration?

● Current system is over-integrated: favours retained earnings inside firm.

Current tax of passive income inside/outside firm is comparable…but…

But savings inside the firm get a ‘head start’ from light taxation of SBD.

● Proposed correction: remove RDTOH.

Increases tax on passive income to compensate for ‘head start’.

For a high-bracket Ontario investor, effective rate on passive income is 73%.

Excessive? Need higher rate to balance big ‘head start’ to achieve integration.

Integration and Passive Income: An Economic Perspective

11 2017 Taxation of Private Corporation Policy Conference

Does Proposal Improve Integration?

Evidence #1: Try to replicate Finance Table 7

Integration and Passive Income: An Economic Perspective

STATUS QUO

STATUS

QUO PROPOSAL

INDIVIDUAL INSIDE CCPC

INSIDE

CCPC

ITEM RATE SAVINGS SAVINGS SAVINGS

Start with $100 of pre-corp tax active businss income 100.00 100.00 100.00

Federal SBD tax rate 10.50% 10.50 10.50 10.50

Ontario SBD tax rate 4.50% 4.50 4.50 4.50

Starting Principal 46.50 85.00 85.00

Interest at 3% 3.00% 27.29 27.29

Special tax on passive income 50.17% 13.69 13.69

RDTOH account 30.67% 8.37

Federal personal tax 33.00%

ONT personal Tax 20.53% 7.00

Portfolio value at end of 10 years 53.41 98.60 98.60

Refund of pre-paid tax RDTOH 8.37

Amount available for distribution as dividend 106.97 98.60

Taxable personal income after grossup 17.00% 125.15 115.36

Federal personal tax 33.00% 41.30 38.07

ONT personal tax 20.53% 25.69 23.68

Dividend tax credit, federal 10.52% 13.17 12.14

Dividend tax credit, ONT 4.30% 5.38 4.96

After-Tax Net Worth after 10 years 53.41 58.52 53.94

12 2017 Taxation of Private Corporation Policy Conference

Does Proposal Improve Integration?

Evidence #2: Observation

● If system is currently properly integrated, there should be no advantage to

retaining earnings.

● We observe financial planners advising clients to save in CCPC for tax

savings.

http://lmgtfy.com/?q=doctors+canada+incorporation+deferral+advantage

● If system were today properly integrated, all that advice would be wrong…

Integration and Passive Income: An Economic Perspective

13 2017 Taxation of Private Corporation Policy Conference

How much will proposals matter?

● We need to keep the scale of the change in mind.

● Imagine $100,000 in passive portfolio; 5% interest.

RDTOH is 30.67%, or $1,534.

But this is taxed as non-eligible dividend at 45.30% (Ont, high bracket)

So, RDTOH is worth $838 if paid immediately.

This is <1% of principal, but knocks down rate of return.

After 10 years, could affect terminal value of portfolio by 8-15%.

Integration and Passive Income: An Economic Perspective

14 2017 Taxation of Private Corporation Policy Conference

How much will proposals matter?

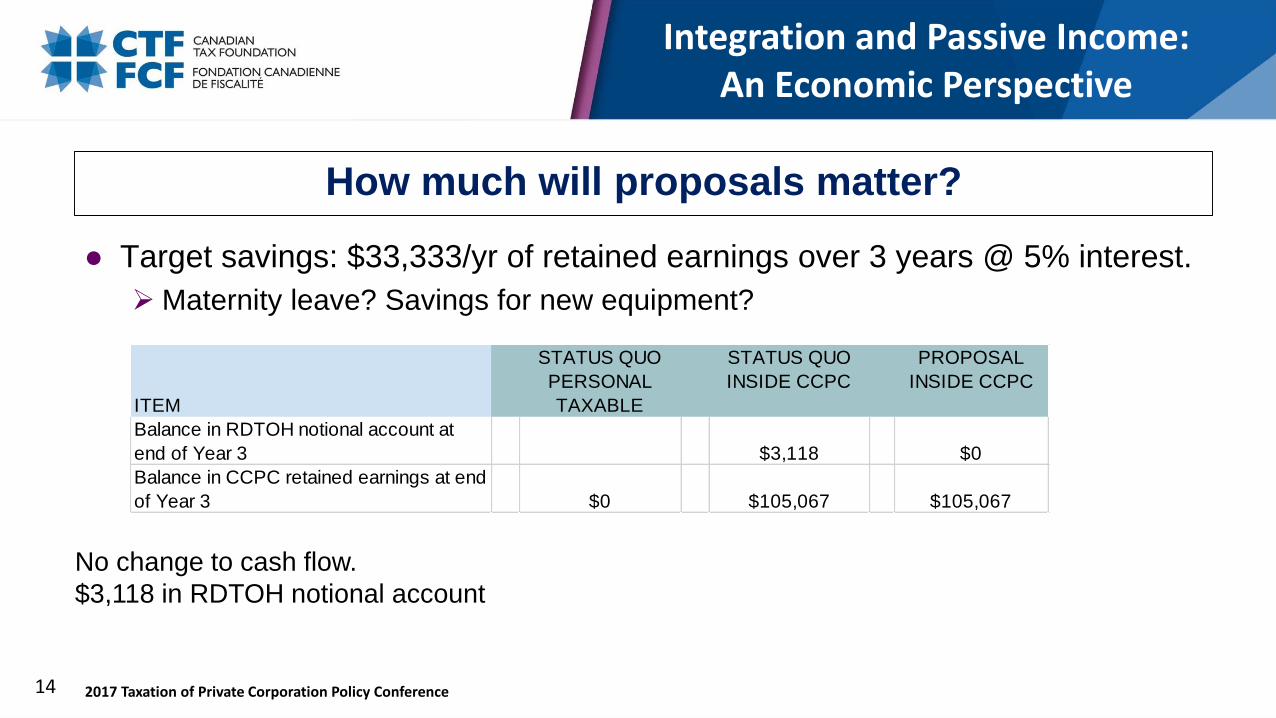

● Target savings: $33,333/yr of retained earnings over 3 years @ 5% interest.

Maternity leave? Savings for new equipment?

Integration and Passive Income: An Economic Perspective

STATUS QUO STATUS QUO PROPOSAL

PERSONAL INSIDE CCPC INSIDE CCPC

ITEM TAXABLE

Balance in RDTOH notional account at

end of Year 3 $3,118 $0

Balance in CCPC retained earnings at end

of Year 3 $0 $105,067 $105,067

No change to cash flow.

$3,118 in RDTOH notional account

15 2017 Taxation of Private Corporation Policy Conference

How much will proposals matter?

● Terminal value of these savings once personal tax is paid.

Integration and Passive Income: An Economic Perspective

PERSONAL INSIDE CCPC INSIDE CCPC

ITEM TAXABLE

Balance in RDTOH notional account at

end of Year 3 $3,118 $0

Balance in CCPC retained earnings at end

of Year 3 $0 $105,067 $105,067

Balance on personal account at end of

Year 3 $58,370 $59,189 $57,483

Status quo: CCPC beats personal by $819.

Proposal: Personal beats CCPC by $887.

16 2017 Taxation of Private Corporation Policy Conference

Carter Commission V.4, p. 84

“The system would neither encourage nor

discourage the retention of earnings by

corporations.”

Integration and Passive Income: An Economic Perspective

17 2017 Taxation of Private Corporation Policy Conference

Caveats on Implementation

● Lots of important challenges await…

Transition: how the grandfathering will work.

Intercompany shareholdings; investments.

We will hear more today!

● This is serious: Need to weigh the costs and benefits of proposals.

Finance’s response: are there non-messy fixes?

Integration and Passive Income: An Economic Perspective

18 2017 Taxation of Private Corporation Policy Conference

Final thought

● This package is clearly a ‘patch’ on a messy system.

● Should we wait for Carter 2.0 before acting?

If we can’t have it all, should we do anything?

● I argue: no

We can all play “fantasy tax reform”….

We must also ask: does this improve on status quo?

Integration and Passive Income: An Economic Perspective

Disclaimer:

This material is for educational purposes only and is not intended to be

advice on any particular matter. No one should act on the basis of any

matter contained in these materials without considering appropriate

professional advice. The presenters expressly disclaim all liability in respect

of anything done or omitted to be done wholly or partly in reliance upon the

contents of these materials.

Tax Planning Using Private Corporations -

July 18, 2017:

Analysis and Discussion with FinanceOttawa, ON

Jack MintzThe School of Pubiic PolicyUniversity of Calgary

Tax Planning Using Private Corporations: Passive Income

2 2017 Taxation of Private Corporation Policy Conference

● Economic role of passive assets:

Retained earnings held in passive assets provides liquidity.

Provides equity finance for investment – investment has been shown to be

higher if firms have cash flow.

Internal resources enable better firms to separate themselves from poor quality

firms to raise equity and debt finance.

Passive assets improve credit risk.

Passive asset provides savings within the corporation for investors when

withdrawn (this is the focus of the July 18th proposals).

Passive Income Rules

3 2017 Taxation of Private Corporation Policy Conference

Benefits of July 18th Passive Income Rules

● Intent is to improve integration of corporate and personal taxes by clawing

back deferral if active business income is invested in passive assets.

● Reduces (but does not achieve fully) neutrality between savings held inside

and outside the CCPCs by investors.

● Reduces the incentive to create CCPCs rather than sole proprietorships or

partnerships (no particular evidence provided on the size of the distortion –

U.S. studies (e.g. Austin Goolsbie suggest not large).

● Raises more revenue for government to lock-in high personal income tax

rates levied in 2015. About $23 billion of passive income is roughly 16% of

active business income (total industry passive income is 10% of operating

income).

Passive Income Rules

4 2017 Taxation of Private Corporation Policy Conference

Distortions/Complexity created by Passive Income Rules

1. Given limitations on full refundability of losses – self-employed losses can

be generally used against other personal income while losses trapped in a

company – rules lead to higher taxes on corporate risky investment.

2. Limits deferral with passive assets – creates a bias towards deferral

achieved through real assets, which could lead to sub-marginal

investments.

3. Indifference works for investors at the top rate – tax neutrality does not

approximate for CCPC owners with marginal tax rates below the top rate.

4. Passive assets for business purposes, as opposed to savings, would need

some sort of brightline test but difficult to properly do (eg. private equity

investments by venture capitalists).

Passive Income Rules

5 2017 Taxation of Private Corporation Policy Conference

Distortions/Complexity created by Passive Income Rules

5. Tax on passive income already results in a significant loss in real principal

with non-tax sheltered assets. (Bond paying 3 percent with 2 percent

inflation and 50% tax rate as real return of -0.5%).

6. Private companies becoming public or non-CCPC could avoid passive

income rules – leads to a new distortion with respect to ownership.

7. Rules are exceedingly complex especially with allocation method.

8. Few countries follow Canadian rules – potential loss in tax competitiveness

especially relative to the United States.

Passive Income Rules

6 2017 Taxation of Private Corporation Policy Conference

Canada’s Tax on Small Business not Competitive

Passive Income Rules

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

$1M $2M $3M $4M $5M $6M $7M $8M $9M $10M $11M $12M $13M $14M $15M $16M $38M $39M $40M

Marg

inal E

ffecti

ve T

ax R

ate

Size of Capital (CAD$ Million)

Canada Small Business Entrepreneur USA Entrepreneur (S Corporation) USA Entrepreneur (Small Business)

7 2017 Taxation of Private Corporation Policy Conference

A Better Approach

● To reduce distortions and complexity as well as encourage growth:

Consider an election to pass income of corporation to owner (egU.S. sub-chapter S

corporations)

Removes the distinction between passive and active business income.

Reduces distinction between self-employed income and private corporate income.

Treats losses similarly to self-employed income and therefore risk.

Would eliminate benefit (if any left) of small business deduction. IIntroduce

investment and employment tax credits instead to encourage investment.

Given small business deduction is of little value with integration, move to single

corporate income tax rate and dividend tax credit. Equalize capital gains and dividend

tax rates.

Passive Income Rules

Disclaimer:

This material is for educational purposes only and is not intended to be

advice on any particular matter. No one should act on the basis of any

matter contained in these materials without considering appropriate

professional advice. The presenters expressly disclaim all liability in respect

of anything done or omitted to be done wholly or partly in reliance upon the

contents of these materials.

Tax Planning Using Private Corporations -

July 18, 2017:

Analysis and Discussion with FinanceOttawa, ON

Bruce BallCPA Canada,Alex LaurinC.D. Howe Institute,Jeffrey Trossman Blake, Cassels & Graydon LLP

Taxation of Investment Income

Disclaimer:

This material is for educational purposes only and is not intended to be

advice on any particular matter. No one should act on the basis of any

matter contained in these materials without considering appropriate

professional advice. The presenters expressly disclaim all liability in respect

of anything done or omitted to be done wholly or partly in reliance upon the

contents of these materials.

Tax Planning Using Private Corporations -

July 18, 2017:

Analysis and Discussion with FinanceOttawa, ON

Assessing the Policy Objectives of the Finance Proposals

3 2017 Taxation of Private Corporation Policy Conference

What is the policy objective for passive income proposal?

● To eliminate tax incentives for CCPC owners to retain “active” earnings, if

the goal is to hold “passive” investments for future personal consumption

● To eliminate a perceived “unfair” tax advantage to CCPC owners compared

to other investors

● Incentive to retain earnings fostered by low small-business income tax rate

leaving greater investment potential

● Tax “inequity” derived from partial relief of CCPC taxes on passive

investment income

Assessing the Policy Objectives

4 2017 Taxation of Private Corporation Policy Conference

Three Key Observations

1. Measured against a consumption-based tax system with progressive

rates, the current CCPC tax regime has many unobjectionable features

2. General-rate earnings (retained for future personal consumption) enjoy no

significant tax advantages, and produce a suboptimal outcome when

measured against a consumption tax baseline; small-business-rate

earnings enjoy a tax outcome pretty much on par with personal retirement

savings.

3. The proposed regime would not level the playing field: it would leave small

business owners with significantly less tax-assisted retirement saving

opportunities than available to some others.

Assessing the Policy Objectives

5 2017 Taxation of Private Corporation Policy Conference

Features of PIT Regime

● Personal Investment Income

Under comprehensive income base, both the initial capital and the investment

income are taxed. Cascading of taxes on saving encourages consumption in the

present, and distorts investment choices (housing)

Under consumption tax base, tax cascading is avoided: retirement plans, TFSA,

other registered accounts

Real-world tax systems are hybrids

Canada’s PIT operates largely on a consumption tax basis (less than 20% of

investment income accumulations are subject to tax)

Assessing the Policy Objectives

6 2017 Taxation of Private Corporation Policy Conference

Features of CCPC Regime

● CCPC Income Regime

Income spent on “active” business consumption attracts no immediate tax

Retained income used for passive investments gets partial relief

Income distributed for personal consumption attracts personal taxes

PIT/CIT integration mechanism = no double taxation

Under perfect integration, business income used for personal consumption

would be taxed on a near consumption basis

Passive investment income sourced from earnings subject to the general CIT

rate is under-integrated = higher effective tax burden on income distributed for

personal consumption

Assessing the Policy Objectives

7 2017 Taxation of Private Corporation Policy Conference

Tax Illustrations: Is the Current CPCC Regime Equitable?

Net Wealth Available for Personal Consumption after Ten Years, 2017

$100,000 Initial Gross Investment, Provincial Average, 3% Rate of Return

Assessing the Policy Objectives

Regime

Interest Dividends Capital Gains

Wealth ($) Gap Wealth ($) Gap Wealth ($) Gap

Salary IncomeTaxable Account 56,632 - 59,177 - 61,476 -

RRSP/TFSA 65,763 +16% 65,763 +11% 65,763 +7%

Current Regime:

CCPC Income

Small Bus. Rate 60,838 +7% 66,522 +12% 69,988 +14%

General Rate 56,204 -1% 60,933 +3% 63,825 +4%

Proposed Regime:

CCPC Income

Small Bus. Rate 56,068 -1% 58,324 -1% 60,937 -1%

General Rate 52,227 -8% 55,193 -7% 56,284 -8%

8 2017 Taxation of Private Corporation Policy Conference

Unequal Tax-Assisted Retirement Wealth Opportunities

Maximum Tax-Assisted Career Accumulations of Retirement Wealth

$150,000 Salary at Retirement

Assessing the Policy Objectives

Source: Pierlot and Siddiqi (2011). Actuarial valuations under standard assumptions assuming 35-year career.

9 2017 Taxation of Private Corporation Policy Conference

Leveling the Playing Field

● The proposed CCPC regime – in effect restricting business owners to

personal RRSP room to tax-effectively save for retirement – would not level

the field

● The proposed regime – if enacted – should be accompanied by a reform of

the tax-assisted retirement savings system that would equalize possibilities

● SB owners are at greater risk of insufficient RRSP room because of:

potential bankruptcy, fluctuating income, early withdrawals to fund business

● Annual income-based limits on retirement savings should be abandoned

and replaced with a uniform lifetime accumulation limit set to replicate

maximum DB accumulations

Assessing the Policy Objectives

Disclaimer:

This material is for educational purposes only and is not intended to be

advice on any particular matter. No one should act on the basis of any

matter contained in these materials without considering appropriate

professional advice. The presenters expressly disclaim all liability in respect

of anything done or omitted to be done wholly or partly in reliance upon the

contents of these materials.

Tax Planning Using Private Corporations -

July 18, 2017:

Analysis and Discussion with FinanceOttawa, ON

Implementation and Technical Issues with the Finance Proposals

11 2017 Taxation of Private Corporation Policy Conference

Outline of Proposal

Proposal would be to make refundable taxes non-refundable in certain

circumstances, as a way of promoting perceived horizontal equity between

business owners and employees

• Premise that business owners and employees are similarly situated is open to

serious debate – but that is not the purpose of this part of the discussion

• Refundable tax rates assume business owner is in top rate bracket

• not true for many small business owners, who would face significant tax increase

• this design flaw would need to be fixed

• Overall approach would result in dramatically different tax treatment of “active

income” (“AI”) and “passive income” (“PI”)

Policy Conference

12 2017 Taxation of Private Corporation Policy Conference

Outline of Proposal

• Existing distinctions in domestic rules (between AI and PI) for CCPCs serve a

much narrower purpose – stakes are much higher in proposed regime

• New system would introduce a new policy – effectively taxing the rate “gap” as if

it had been immediately distributed

• This is achieved indirectly by making currently refundable taxes non-refundable;

overall effect is to (theoretically) put owner in same position as if “gap” had been

distributed and taxed immediately; therefore, effect is to tax corporation’s capital

• New concepts needed

Policy Conference

13 2017 Taxation of Private Corporation Policy Conference

“Active” vs. “Passive” Income – Core Definition

Distinguishing AI from PI – Basic definition of PI

• Should income from property presumptively be classified as PI?

− If so, why?

− Income from property can include economically productive activities

• Leasing/licensing of property – real/personal/intangible property –

different rules?

− Early stage software development – is that income from property?

Policy Conference

14 2017 Taxation of Private Corporation Policy Conference

“Active” vs. “Passive” Income – Core Definition

• Is a >5 employees test appropriate?

− If so, why?

− Current “specified investment business” definition serves a narrower purpose; stakes

now much higher

− Core service providers may not be employees

− Consider equivalence rules as in old Part XI ($250K rule)

− Rules should address provision of services by employees of affiliates and

partnership structures, as in definition of “investment business” in 95(1); paragraph

(b) of “specified investment business” is unduly narrow

• This is complicated!

Policy Conference

15 2017 Taxation of Private Corporation Policy Conference

“Active” vs. “Passive” Income – “Excess” Passive Assets

Distinguishing AI from PI – Rules to delineate “excess” passive assets

• Rules should recognize business realities which may require seemingly

excess passive assets to be retained in corporation for good business

reasons having nothing to do with tax deferral

− Prudent cash management to plan for contingencies generally

− Retention of cash for possible identified extraordinary expenses

− Maintaining credit standing opposite bank or other creditors

Policy Conference

16 2017 Taxation of Private Corporation Policy Conference

“Active” vs. “Passive” Income – “Excess” Passive Assets

− Retention of cash for future acquisitions that can reasonably be

anticipated

− Retention of cash for possible future capital investment that can

reasonably be anticipated in machinery & equipment, real estate,

intangible property, R&D, etc.

− Concept needed to define what is meant by “excess” passive assets

Policy Conference

17 2017 Taxation of Private Corporation Policy Conference

“Active” vs. “Passive” Income – “Excess” Passive Assets

• Policy alternatives include a qualitative test or a bright-line test

− Qualitative test - what is “reasonable in the circumstances” – disputes likely

− Bright-line test could look to specific dollar thresholds and/or specific time

horizons (e.g., 36-month rule in FIE proposals – paragraph (d) of “qualifying

entity” definition in proposed subsection 94.1(1), Bill C-10, passed by House

of Commons Oct. 29/07)

− Trade-off among objectives of fairness, workability, likelihood of disputes

− This is complicated!

Policy Conference

18 2017 Taxation of Private Corporation Policy Conference

“Active” vs. “Passive” Income – Inter-affiliate Payments

Active business income should not become “passive” just

because it is paid from one corporation to another

• For example, one company in the group may lease real or personal

property or lend money to the main operating company

• 129(6) adopts the principle that character does not change in limited

circumstances, and for the limited purpose for which it now applies

Policy Conference

19 2017 Taxation of Private Corporation Policy Conference

“Active” vs. “Passive” Income – Inter-affiliate Payments

−129(6) requires payor and payee to be “associated” corporations

for active business income to retain its character when paid

within the group

“associated” concept pertains to the SBD, so not appropriate for

this much larger purpose

Alternatives

“affiliated”

“non-arm’s length”

Minimum 10% votes/value test, as in 95(2)(a)(ii)

Policy Conference

20 2017 Taxation of Private Corporation Policy Conference

“Active” vs. “Passive” Income – Inter-affiliate Payments

consider other factors in designing inter-affiliate payments rule

apportionment of expenses and losses

payments involving partnerships

Policy Conference

21 2017 Taxation of Private Corporation Policy Conference

“Active” vs. “Passive” Income – Inter-corporate Dividends

• For dividends, the “connected” test in Part IV determines whether

dividend is a “portfolio” dividend subject to 38-1/3% refundable tax

− In determining whether Part IV tax is non-refundable, is this the right

test?

− Anomalies in the “connected” test

186(2) has been interpreted as a “count-the-shares” rather than “count-

the-votes” test; corporations can be related without being connected

Unusual to require “more than 10%” rather than “10% or more”

Policy Conference

22 2017 Taxation of Private Corporation Policy Conference

“Active” vs. “Passive” Income – Inter-corporate Dividends

− From a policy perspective, is the “connected” test really the correct test to

distinguish AI from PI?

Consider whether dividend received from non-arm’s length (but not

“connected”) corporation should be subject to permanent Part IV tax

What about dividend from arm’s length, active corporation in which investor

has (say) a 9% interest? – Part IV tax applies, but is it appropriate for that tax

to be permanent?

Discussion raises more fundamental question of what is meant by

“reinvestment in the business”

Should rules create a tax incentive for investing in affiliated, rather than

unaffiliated active businesses? Why?

There should be a coherent basis for making the distinction

Policy Conference

23 2017 Taxation of Private Corporation Policy Conference

“Active” vs. “Passive” Income – Capital Gains

• Capital gain could arise from disposition of asset used to earn AI (“active asset”)

or PI (“passive asset”)

• Proposals would change the integration rules by denying CDA as a way to tax

the rate “gap”

− Should distinguish capital gains from dispositions of passive vs. active asset

− Capital gain from disposing of active asset is, in effect, a way of realizing the value

built up in the active business

Policy Conference

24 2017 Taxation of Private Corporation Policy Conference

“Active” vs. “Passive” Income – Capital Gains

● Appreciation may be the result of any number of factors:

- creation or enhancement of goodwill,

- development of trade names or brands,

- discovery of a technological breakthrough,

- valuable supply or distribution agreements,

- appreciating land values,

- luck, and

- an innumerable list of other factors.

Policy Conference

25 2017 Taxation of Private Corporation Policy Conference

“Active” vs. “Passive” Income – Capital Gains

● If and when the corporation disposes of a tangible or intangible asset used

in the business, the resulting gain does not conceptually resemble a passive

return

● Gain represents current realization of expected future cash flows

● It follows that there is a fundamental distinction between capital gains

realized from disposition of an asset used in an active business and other

capital gains (for example, from disposing of a publicly traded portfolio

investment)

Policy Conference

26 2017 Taxation of Private Corporation Policy Conference

“Active” vs. “Passive” Income – Capital Gains

● This distinction is recognized in the foreign affiliate rules

● These rules are a good starting point for designing a new system

● These rules draw a distinction between property used in carrying on an

active business (“excluded property”) and other property

● Taxable capital gains from dispositions of excluded property are excluded

from the definition of “foreign accrual property income” (“FAPI)

Policy Conference

27 2017 Taxation of Private Corporation Policy Conference

“Active” vs. “Passive” Income – Capital Gains

● Excluded property definition takes account of the possibility that the

disposing affiliate may dispose of an active business by selling shares of a

lower tier subsidiary

● Shares of a foreign affiliate that derive “all or substantially all” of their value

from property used in an active business are thus defined as excluded

property

● Determination of “excluded property” status of shares can be complicated in

practice

Policy Conference

28 2017 Taxation of Private Corporation Policy Conference

“Active” vs. “Passive” Income – Capital Gains

● While foreign affiliate system was designed to achieve different legislative

objectives, it provides a good starting point

● Taxable capital gain derived from a disposition of an asset used in an active

business should be regarded as AI, and the accompanying non-taxable

portion should be added to CDA

● Treatment of such gains as passive income seems conceptually flawed

Policy Conference

29 2017 Taxation of Private Corporation Policy Conference

“Active” vs. “Passive” Income – Capital Gains

● Rules needed to treat shares of certain corporations as excluded property

under the new regime

● 10% test similar to foreign affiliate definition makes some sense

● If private corporation realizes gain from disposing of shares of a foreign

affiliate that meet the current “excluded property” definition, taxable portion

of that gain ought to be classified as AI under the new regime and not

treated as PI

Policy Conference

30 2017 Taxation of Private Corporation Policy Conference

“Active” vs. “Passive” Income – Capital Gains

• Gains from dispositions of goodwill, trademarks and other intangibles used in a

business:

− Gain on sale would have been regarded as business income prior to recent changes

to replace ECE regime with Class 14.1

− Should those changes affect AI/PI distinction?

Policy Conference

31 2017 Taxation of Private Corporation Policy Conference

Classification of Losses

• If loss is realized, need to determine whether “active” or “passive”

− Similar to distinction between “active” losses and FAPLs in foreign affiliate rules

− Rules will be needed to track “surplus” accounts

Policy Conference

32 2017 Taxation of Private Corporation Policy Conference

Source of Capital

Income derived from capital not sourced from “lightly taxed” income is

not intended to be subject to new regime

• Premise of consultation paper is that a system is needed to distinguish:

− Capital derived from “lightly” taxed business income (income on which “should” be

subject to non-refundable corporate taxes),

from

− Capital derived from other sources (income on which should still be eligible for

refundable treatment)

Policy Conference

33 2017 Taxation of Private Corporation Policy Conference

Source of Capital

• Non-refundable corporate tax should not apply to:

− Investment income derived from capital contributed by shareholder in non-rollover

transaction

No rate “gap” – asset came in from after-tax dollars of shareholder

− Investment income derived from capital acquired by corporation through issuance of

debt/equity/other securities in non-rollover transaction (e.g., borrowing, share

offering)

No rate “gap” – asset came in from after-tax dollars of investor

− Investment income derived from capital acquired by corporation from a foreign

source dividend, interest or other payment

No rate “gap” – asset came in from foreign source

Policy Conference

34 2017 Taxation of Private Corporation Policy Conference

Source of Capital

• Need to create and track several “surplus” or similar accounts to give effect to

these principles

• Need special rules for rollovers, amalgamations, wind-ups, divisive

reorganizations

• Revisit active/passive distinction in FIE proposals and FAPI rules

• Developing coherent rules is complicated!

Policy Conference

35 2017 Taxation of Private Corporation Policy Conference

Transition

Government states that new rules will apply only “going forward”

●How to achieve this without byzantine transitional rules?

●Non-refundable taxes amount to a tax on the “capital” represented by the

rate “gap”

− Apparent ~73% “all-in” tax on investment income is designed to tax the rate “gap” as

if it had been immediately distributed

− Unless and until it is distributed, this is capital of the corporation

− elimination of refundability will erase a potential future corporate asset (the refund)

as the new system comes into effect

Policy Conference

36 2017 Taxation of Private Corporation Policy Conference

Transition

• To make changes truly prospective:

− Income derived from capital accumulated before new regime takes effect (and

income derived from that income) should not be subject to non-refundable taxes

− That capital was accumulated in a regime in which “high” taxes on private

corporations’ investment income were temporary/refundable

− Will require a determination of aggregate passive assets on “coming-into-force” date,

and tracking of “surplus” account, ordering rules, etc.

Policy Conference

37 2017 Taxation of Private Corporation Policy Conference

Scope of Application

CCPCs vs. foreign-controlled corporations

• premise of proposed regime is a Canadian resident individual owner- not true

for foreign controlled corporation

• special 10-2/3% tax already applies only to CCPCs in recognition of this basic

difference

• competitiveness issue

• would have to deal with branch tax if proposed to extend new regime to foreign-

controlled corporations

Policy Conference

38 2017 Taxation of Private Corporation Policy Conference

Reality of Under-integrated System

• If all benefits of deferral are to be eliminated, the under-integrated system

leaves those considering a new business with a heavy cost to get limited

liability, unless they plan to reinvest substantially all profits “in the business” in

perpetuity, rather than earmarking a portion of profit for future consumption at

some point

• Elective check-the-box system could help

• Fine-tune rules to mitigate under-integration, don’t just assume under-

integration away

Policy Conference

Disclaimer:

This material is for educational purposes only and is not intended to be

advice on any particular matter. No one should act on the basis of any

matter contained in these materials without considering appropriate

professional advice. The presenters expressly disclaim all liability in respect

of anything done or omitted to be done wholly or partly in reliance upon the

contents of these materials.

Tax Planning Using Private Corporations -

July 18, 2017:

Analysis and Discussion with FinanceOttawa, ON

Possible Alternatives to Finance Proposals

40 2017 Taxation of Private Corporation Policy Conference

Other Possible Alternatives

● “Check the Box” Flow Through

● Impose a Refundable Tax on Ineligible Investments?

● Repeal or Replace the Small Business Deduction?

● Increase the corporate refundable tax rate?

● Comprehensive Tax Review?

Policy Conference

41 2017 Taxation of Private Corporation Policy Conference

Check the Box Flow Through

● Integration and debate around use of tax deferral is less relevant if

shareholders can be taxed on income as a flow through

● Can set corporate and personal rates without same concern around

integration if there is a “safe harbour” for private corporation owners to pay

single level of tax at personal rate if they so choose

● A lower tax rate could be applied on business income to provide an incentive

similar to SBD (similar rule under consideration in US?)

● Seems like an approach worth study if starting a brand new tax system

● Significant transitional issues?

Policy Conference

42 2017 Taxation of Private Corporation Policy Conference

Impose a Refundable Tax on Ineligible Investments?

● Was referred in the consultation paper but dismissed

● Makes the most theoretical sense for what Finance is trying to do?

• The best way to prevent the accumulation of investment income on the tax

deferral is to prevent you from investing it in the first place?

• Works best if:

− One single source of income where after-tax use is a concern

− One good use of assets and one bad

• Would create need for complicated rules in concept and application, and would

have adverse business implications such as waiting for tax refunds when

passive assets are repurposed for business use

Policy Conference

43 2017 Taxation of Private Corporation Policy Conference

Repeal or Replace The Small Business Deduction?

● Is the Small Business Deduction the Issue?

• Using 10-Year accumulation rationale, is retaining general rate income (GRI) for

investments a significant issue if no income sprinkling/gain planning?

− Practically, any benefit provided from investing the deferral is eaten away by the

under integration on GRI and/or investment income

• Investing cash in a private corporation and earning investment income is also

not an issue (pure investment corporation, conceded in paper)

• Is after-tax SBI the only materially contentious source of investments?

• If so, would it make more sense to focus on the small business deduction?

• Following charts use Finance Table 7 assumptions with actual rates for 2017

Policy Conference

44 2017 Taxation of Private Corporation Policy Conference

10-Year Net Worth Analysis – General Rate Business Income

Policy Conference

Personally Corporation Adv./Disadv.

BC $61,110 $62,015 $905

Alberta 60,706 60,755 49

Saskatchewan 61,043 62,536 1,493

Manitoba 57,495 55,506 -1,989

Ontario 53,370 54,885 1,515

Quebec 53,658 54,575 917

New Brunswick 53,671 56,858 3,187

Nova Scotia 52,757 49,344 -3,413

PEI 56,209 55,069 -1,140

Newfoundland & Labrador 56,302 49,902 -6,400

Assumed Rates Used by Finance 57,535 60,457 2,922

45 2017 Taxation of Private Corporation Policy Conference

10-Year Net Worth Analysis – Income Eligible for the SBD

Policy Conference

Personally Corporation Advantage

BC $61,110 $65,113 $4,003

Alberta 60,706 64,555 3,849

Saskatchewan 61,043 66,485 5,442

Manitoba 57,495 61,025 3,530

Ontario 53,370 58,510 5,140

Quebec 53,658 57,549 3,891

New Brunswick 53,671 58,095 4,424

Nova Scotia 52,757 56,993 4,236

PEI 56,209 59,279 3,070

Newfoundland & Labrador 56,302 60,766 4,464

Assumed Rates Used by Finance 57,535 63,207 5,672

46 2017 Taxation of Private Corporation Policy Conference

10-Year Net Worth Analysis – Observations

● Small business income:

• Provincial numbers fairly consistent – integration on SBI generally works

• “Province of Finance” NW > All provinces other than Saskatchewan

• Average NW advantage is $4,200 – Is this significant on $100,000 of SBI?

● General Rate Income (GRI)

• Keeping GRI in a corporation and paying it out later as a dividend represents a

cost in many provinces, investing the deferral helps reduce the cost

• The integration on investment income is imperfect as well

• Unclear any changes are needed on GRI without more study?

● Results do vary based on the rate of return & type of income

Policy Conference

47 2017 Taxation of Private Corporation Policy Conference

Is the Small Business Deduction an Issue?

● Considerations and questions that could be considered:

• In terms of the growth in the number of private corporations, do we know how

much growth is directly related to reinvesting the value of the SBD in passive

assets?

• If the government deals with income sprinkling and capital gain planning, how

many taxpayers would set up private companies in the future for passive

investment tax planning purposes? Motivation often based on multiple factors?

Policy Conference

48 2017 Taxation of Private Corporation Policy Conference

Is the Small Business Deduction an Issue?

● Considerations and questions that should be considered:

• If the possibility of reinvesting the SBD saving is a concern, would amending,

replacing or just repealing the small business deduction reduce the growth of

private corporations used for passive investment tax planning purposes?

• Redesign the SBD as a more targeted tax expenditure designed to reward

economic growth, positive impact on economy and risk taking (rather than

tracking and dealing with corporations investing it)?

Policy Conference

49 2017 Taxation of Private Corporation Policy Conference

Increase the corporate refundable tax rate?

● This was action government took previously – would more of the same help?

● Issues:

• At the end of the day, the tax is returned when dividends are paid - tax deferral

was effectively invested?

• Not refunded if passive assets invested in business – punitive?

• For the same reasons discussed before, take a good look at the SBD?

Policy Conference

50 2017 Taxation of Private Corporation Policy Conference

Comprehensive Tax Review?

● Passive income proposals suggested in paper would make for a complicated

tax system and seem to assume other aspects of the tax system are

effective and should remain in place (e.g. small business deduction)

● Paper assumes aspects that are theoretically part of the system but are not

working in reality (e.g. integration)

● Ensure key drivers of the tax system make sense before adding more

complication around them?

● A review of other countries indicates what Canada is examining would be

fairly unique – blazing a trail brings risk?

● Are there better ways to deal with the key issues of concern?

Policy Conference

Disclaimer:

This material is for educational purposes only and is not intended to be

advice on any particular matter. No one should act on the basis of any

matter contained in these materials without considering appropriate

professional advice. The presenters expressly disclaim all liability in

respect of anything done or omitted to be done wholly or partly in

reliance upon the contents of these materials.

Tax Planning Using Private Corporations -

July 18, 2017:

Analysis and Discussion with FinanceOttawa, ON

Sandra MahDLA Piper (Canada) LLP

H. Michael DolsonFelesky Flynn LLP

Taxation of Investment Income: Practitioner Perspectives on Proposals and Potential Issues

2 2017 Taxation of Private Corporations Policy Conference

Syllabus

● Policy issues

● Anticipated legislative issues

● Anticipated behavioural response and real-world results

Practitioner Perspectives

3 2017 Taxation of Private Corporations Policy Conference

Policy Issues

● Intergenerational equity issue:

Proposed changes level playing field within some cohorts, not between them

Even intra-cohort levelling may be superficial

Cascading gender equity and racial equity implications

Cascading vertical equity implications

Practitioner Perspectives

4 2017 Taxation of Private Corporations Policy Conference

Policy Issues

● If tax policy objective is to prevent tax-motivated incorporation, entire

package may be a poorly targeted solution

Similar to issues with continued approach to PSB corporations

For many incorporated services businesses, incorporation is payer’s choice

Significant non-neutrality due to payroll taxes and provincial laws

Benefits disproportionately enjoyed by payers:

Consider employees vs. contractors in Calgary 2015-16

Payers advertise purported tax benefits to workers so workers don’t revolt

● Admittedly less of an issue for professionals

● Is this policy negatively affecting how CCPCs will finance their businesses

Practitioner Perspectives

5 2017 Taxation of Private Corporations Policy Conference

Policy Issues

● Foreign solutions to this problem do not seem to have been considered

Some may be better or worse than what is proposed, but should be canvassed

● Example: Netherlands minimum salary regime

Corporation must pay controlling shareholder wages equal to the lesser of:

Greater of (i) €45,000; and (ii) 75% of corporation’s pre-wage taxable income; and

Proven wages of a similarly-skilled worker

75% requirement inapplicable if shareholder generated <90% of profit

If shareholder is underpaid, imputed employment income plus penalty

● Might satisfactorily address passive income and income splitting issues,

while potentially being simpler

Practitioner Perspectives

6 2017 Taxation of Private Corporations Policy Conference

Policy Issues

● Is the small business deduction still viable?

Are the significant recent efforts to preserve integrity worth the effort?

● Is integration still good tax policy?

Proposed regime represents significant departure from integration principle

Apportionment method might achieve integration over long horizon using Milligan’s

assumptions, but that is not what integration has historically been about

Practitioner Perspectives

7 2017 Taxation of Private Corporations Policy Conference

Legislative Issues

● Finance is probably downplaying the complexity of the apportionment

method for passive income

Likely end result will be something similar to a domestic equivalent of the FA

surplus rules, in order to prevent chicanery

Not clear how loans (for shareholder or inter-corporate) would factor in

Not clear how losses will be allocated or tracked

Not clear if assets can change status from passive to active

Not clear how dividends will be paid

Practitioner Perspectives

8 2017 Taxation of Private Corporations Policy Conference

Legislative Issues

● Elective method requires assumptions too simplistic to work in practice

Why is it reasonable to assume that shareholder contributions are not used to

make passive investments?

What if SBD-electing corporation earns $600,000 of income?

What if corporation is unsure whether or not its income qualifies for the SBD?

Real problem for potential PSB corporations or potential SIB corporations

Extreme unfairness if workers are not causing PSB proliferation

● Here, the benefits of simplicity are illusory given the complexity of transition

Practitioner Perspectives

9 2017 Taxation of Private Corporations Policy Conference

Legislative Issues

● Proposed regime will place considerable pressure on both bright-line tests

and common-law tests relating to active vs. passive income

Considerable additional tax wedge between ≤5 full-time employees and >5 full-

time employees for, say, property rental businesses

Likely to encounter Ensite-type litigation surrounding use or risking of income-

producing properties in active business

Incentive for characterizing two potentially separate businesses (e.g. real estate

development and real estate leasing) as a single business

Practitioner Perspectives

10 2017 Taxation of Private Corporations Policy Conference

Legislative Issues

● Will capital gains realized on disposition of business assets/goodwill

continue to generate CDA?

White Paper suggests not, if source of gain is reinvested corporate income

This seems to be an improper result

Practitioner Perspectives

11 2017 Taxation of Private Corporations Policy Conference

Legislative Issues

● “Control” is too high a threshold for an investment in another corporation to

generate a CDA-increasing capital gain

Creates punitive result if two or more arm’s length corporations go into business

More realistic threshold required, along the lines of FA status

● “Exclusively” is an unattainable threshold for subsidiary’s investment in

business assets

More realistic threshold would resemble the QSBC share test

● Other circumstances may exist where capital gains should generate CDA

Practitioner Perspectives

12 2017 Taxation of Private Corporations Policy Conference

Legislative Issues

● Important aspects of proposed regimes lack sufficient detail to provide

meaningful comment:

Is the election one time or for each fiscal year for the Elective Method?

Potential limited use of election - only those corporations that have significant

passive investment or immaterial passive investments

Investment corporation election

Effects of election if made by existing corporation, and timing and types of transfer

that will result in transfer tax

How will grandfathering be accomplished?

Will it phase out over time?

Care will have to be taken to avoid capital lock-in effect

Practitioner Perspectives

13 2017 Taxation of Private Corporations Policy Conference

Legislative Issues

● Extension of regime to non-CCPCs may have unintended negative effects

Private corporations used by non-residents to make investments in Canada

No tax policy reason to be concerned about deferred personal income, Canada

can’t tax that income anyway

Extension of regime without caution would materially increase effective tax rate,