tax issues in asset purchase transactions · capital gains treatment $750,000 capital gains...

TRANSCRIPT

Tax Issues in Asset Purchase Transactions

Catherine A. Brayley

OverviewAssets vs. Shares – How to decide?What’s the big deal about allocation clauses?Where are the forms?How can they pay tax if they’re not getting any money?Let’s reduce the purchase price with consulting agreements!Now that all this money is in the company …

2

Who is Selling?

ASSETS

Canco

Individual

Share Sale

Asset Sale

3

Assets vs. Shares … How to Decide?

4

Purchase and Sale of Assets

Purchaser IssuesSelection of assets and liabilitiesTax basis = Purchase price allocated to asset

Future deductions

Vendor IssuesIncome

Recapture / Terminal LossReserves

5

Purchase and Sale of Shares

Purchaser IssuesInherit tax and other liabilitiesInherit tax cost of assets

Limited opportunity to set up cost base

Vendor IssuesOne level of taxCapital gains treatment$750,000 capital gains exemption

6

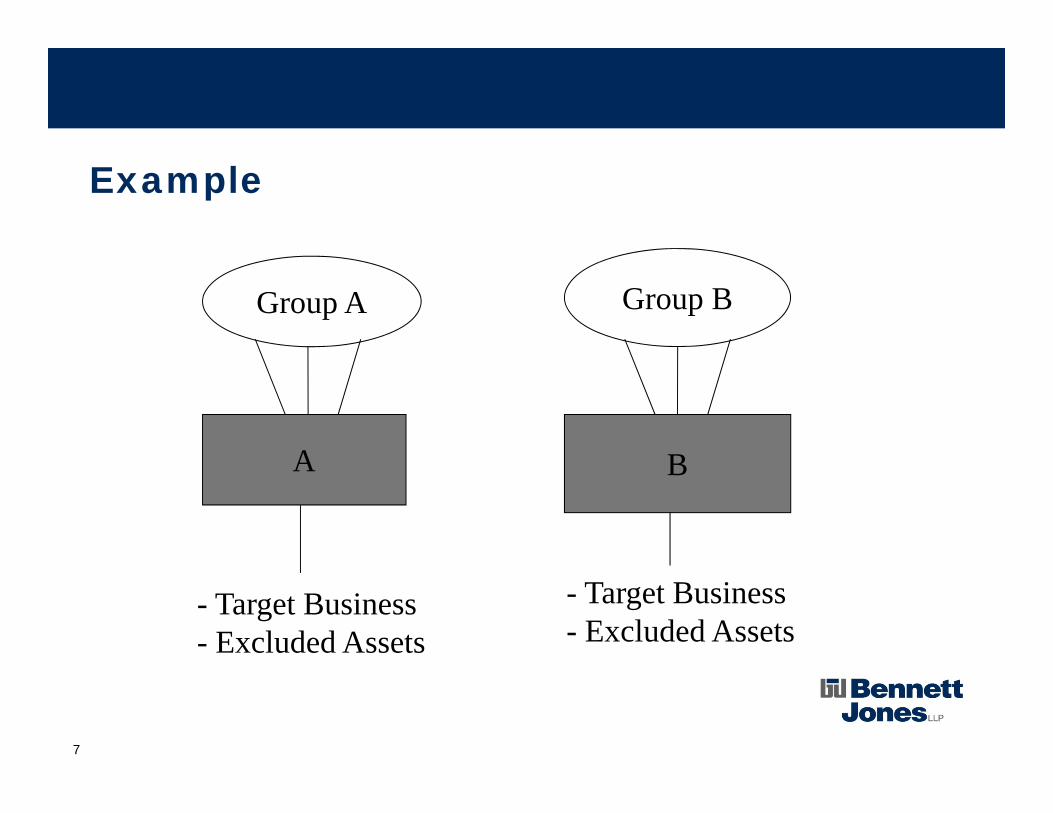

Example

Group B

A B

Group A

- Target Business- Excluded Assets

- Target Business- Excluded Assets

7

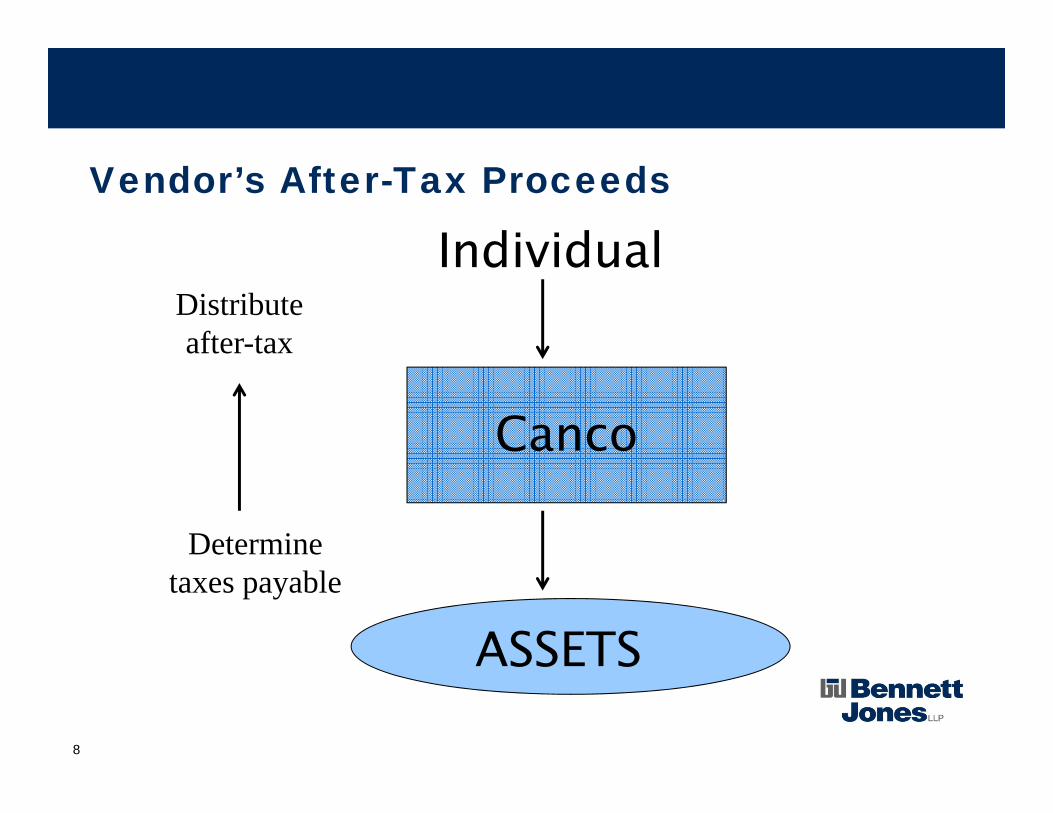

Vendor’s After-Tax Proceeds

Distribute after-tax

Determine taxes payable

ASSETS

Canco

Individual

8

Tax Factors Influencing StructureTax Status of

TargetShareholders of TargetPurchaser

Tax RatesVendorPurchaserShareholders of Target

9

Tax Factors Influencing StructureIncome Generated from Sale of Assets

Ordinary IncomePropertyBusiness

Capital gains (or capital gains equivalent)

Tax CostACB of Target shares to shareholders of TargetAssets of Target that are subject of sale

10

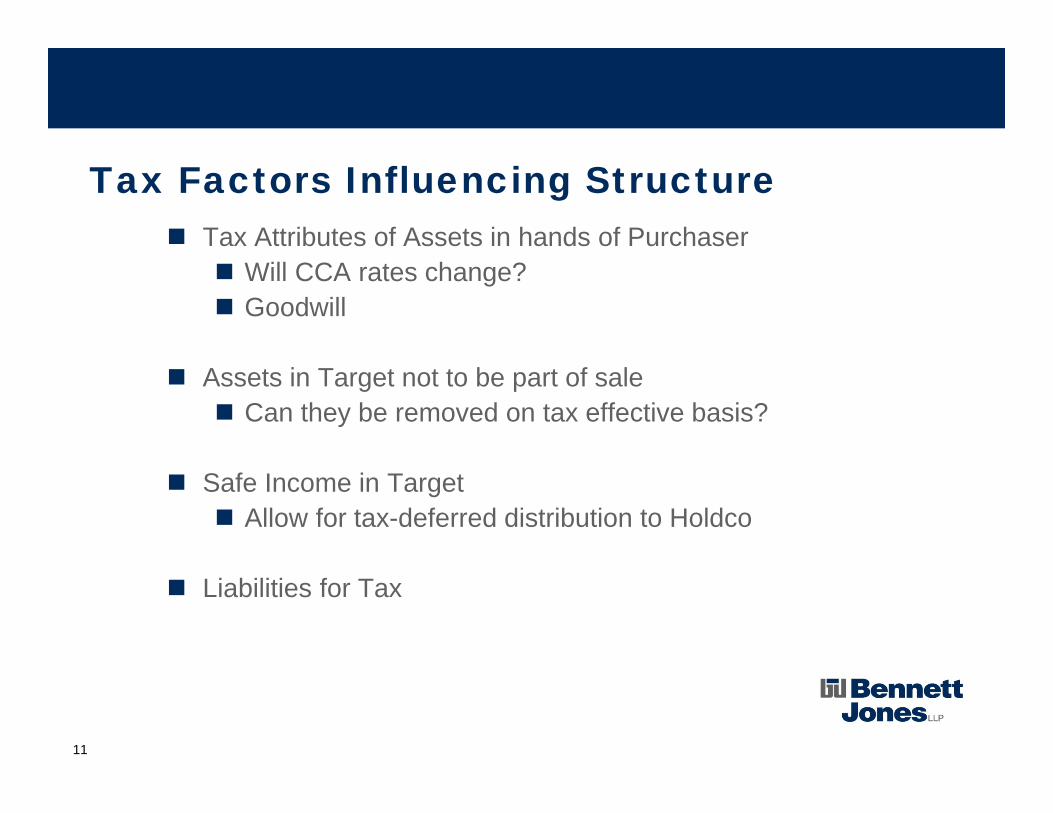

Tax Factors Influencing StructureTax Attributes of Assets in hands of Purchaser

Will CCA rates change?Goodwill

Assets in Target not to be part of saleCan they be removed on tax effective basis?

Safe Income in TargetAllow for tax-deferred distribution to Holdco

Liabilities for Tax

11

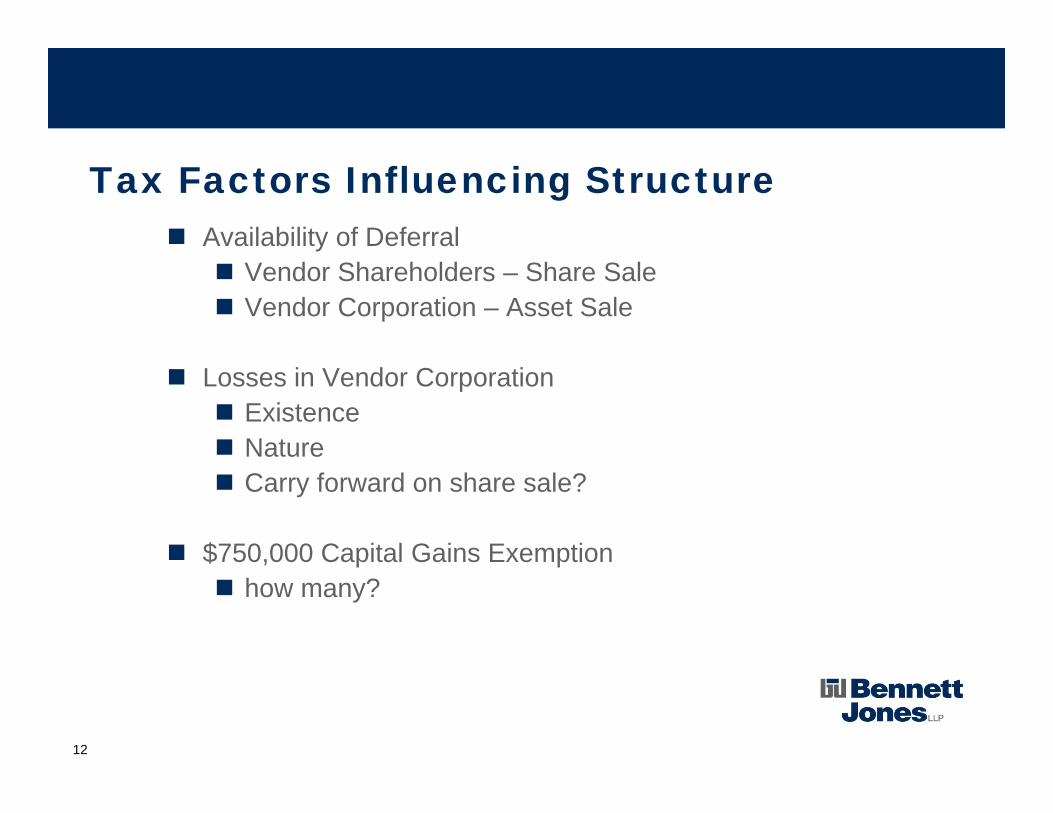

Tax Factors Influencing StructureAvailability of Deferral

Vendor Shareholders – Share SaleVendor Corporation – Asset Sale

Losses in Vendor CorporationExistenceNatureCarry forward on share sale?

$750,000 Capital Gains Exemptionhow many?

12

Due DiligenceFinancial Statements

Consolidated versus entity basisWhat are you given?

Balance SheetIncome StatementStatement of Changes in Financial PositionNotes

Complete picture?Source of tax information – T2Minute book

13

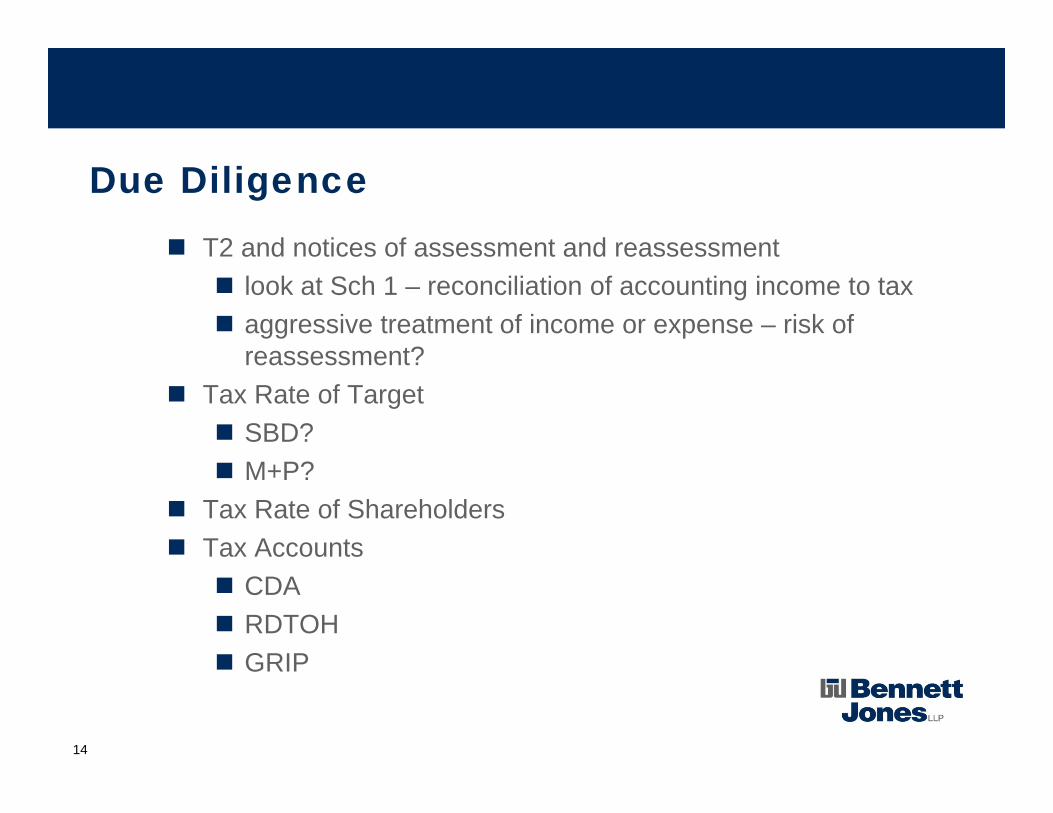

Due DiligenceT2 and notices of assessment and reassessment

look at Sch 1 – reconciliation of accounting income to taxaggressive treatment of income or expense – risk of reassessment?

Tax Rate of TargetSBD?M+P?

Tax Rate of ShareholdersTax Accounts

CDARDTOHGRIP

14

Due Diligence

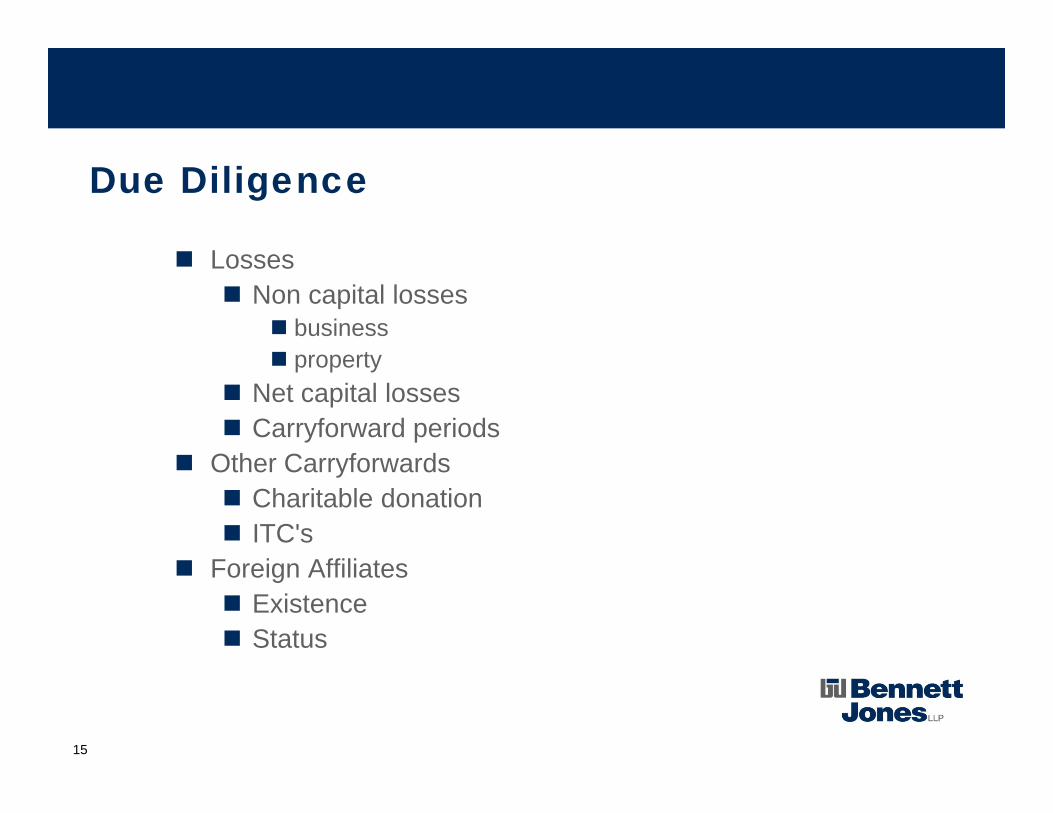

LossesNon capital losses

businessproperty

Net capital lossesCarryforward periods

Other CarryforwardsCharitable donationITC's

Foreign AffiliatesExistenceStatus

15

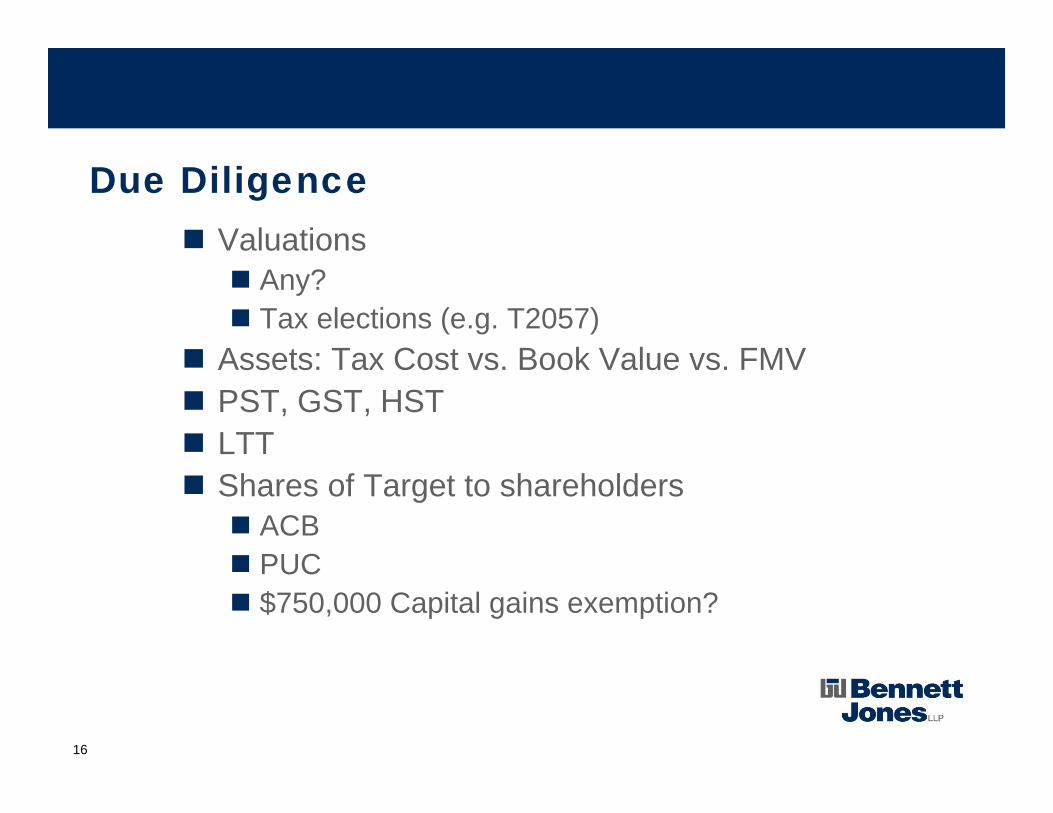

Due DiligenceValuations

Any?Tax elections (e.g. T2057)

Assets: Tax Cost vs. Book Value vs. FMVPST, GST, HSTLTTShares of Target to shareholders

ACBPUC$750,000 Capital gains exemption?

16

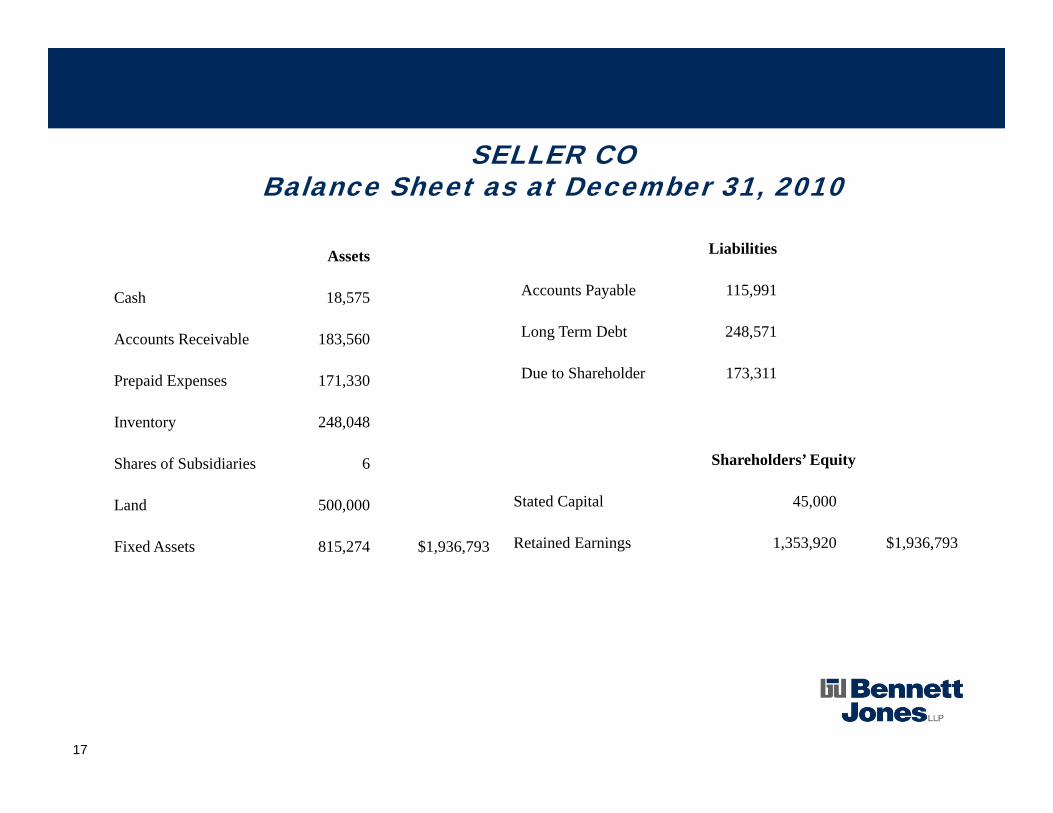

SELLER COBalance Sheet as at December 31, 2010

Assets

Cash 18,575

Accounts Receivable 183,560

Prepaid Expenses 171,330

Inventory 248,048

Shares of Subsidiaries 6

Land 500,000

Fixed Assets 815,274 $1,936,793

Liabilities

Accounts Payable 115,991

Long Term Debt 248,571

Due to Shareholder 173,311

Shareholders’ Equity

Stated Capital 45,000

Retained Earnings 1,353,920 $1,936,793

17

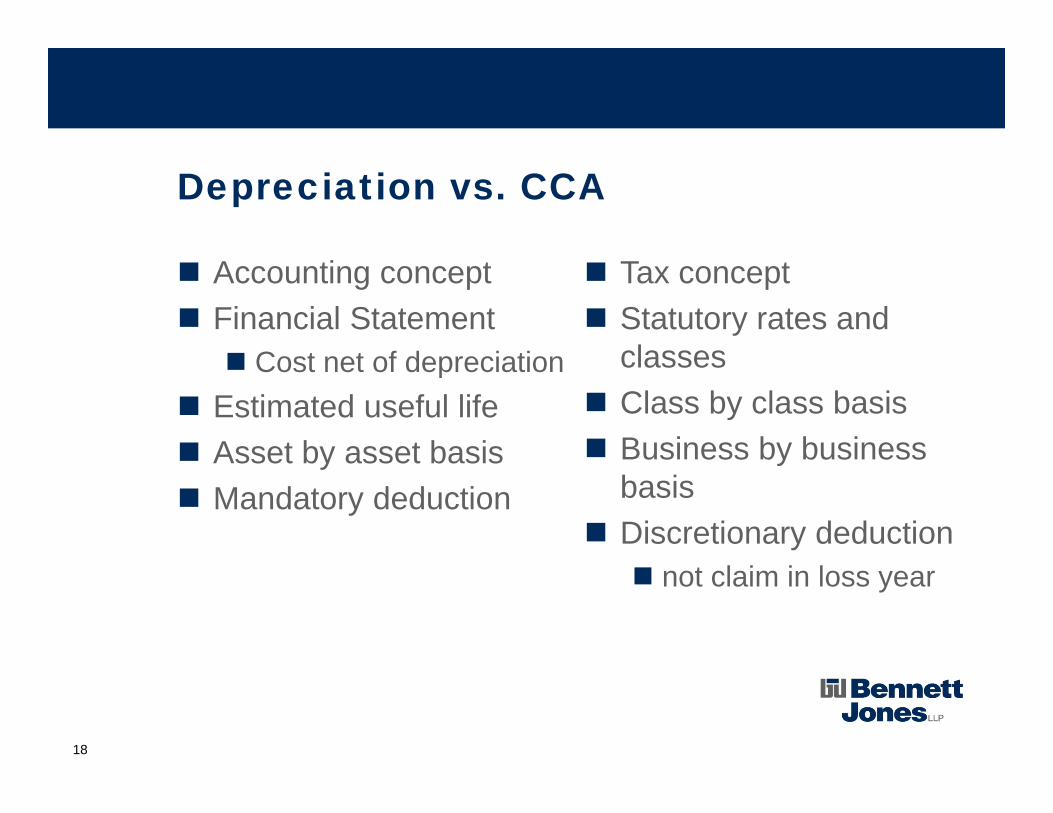

Depreciation vs. CCA

Accounting concept Financial Statement

Cost net of depreciationEstimated useful lifeAsset by asset basisMandatory deduction

Tax conceptStatutory rates and classesClass by class basisBusiness by business basisDiscretionary deduction

not claim in loss year

18

T2S(8) – Capital Cost Allowance

19

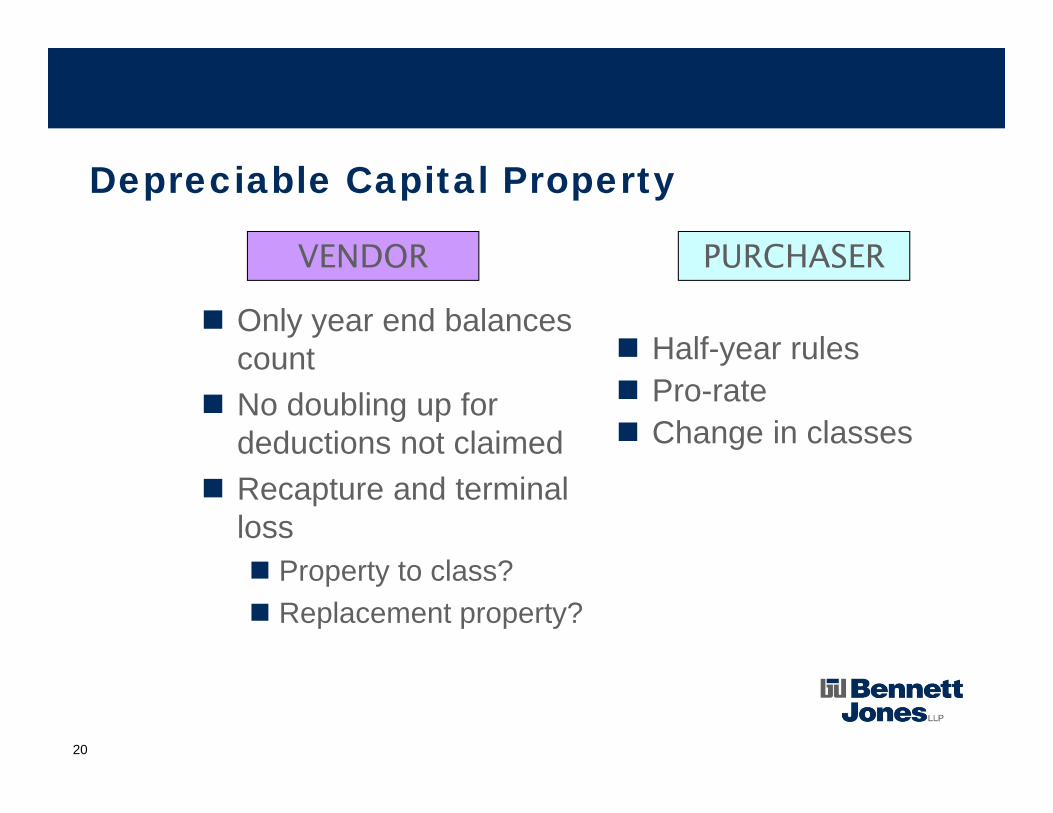

Depreciable Capital Property

Only year end balances countNo doubling up for deductions not claimedRecapture and terminal loss

Property to class?Replacement property?

Half-year rulesPro-rateChange in classes

VENDOR PURCHASER

20

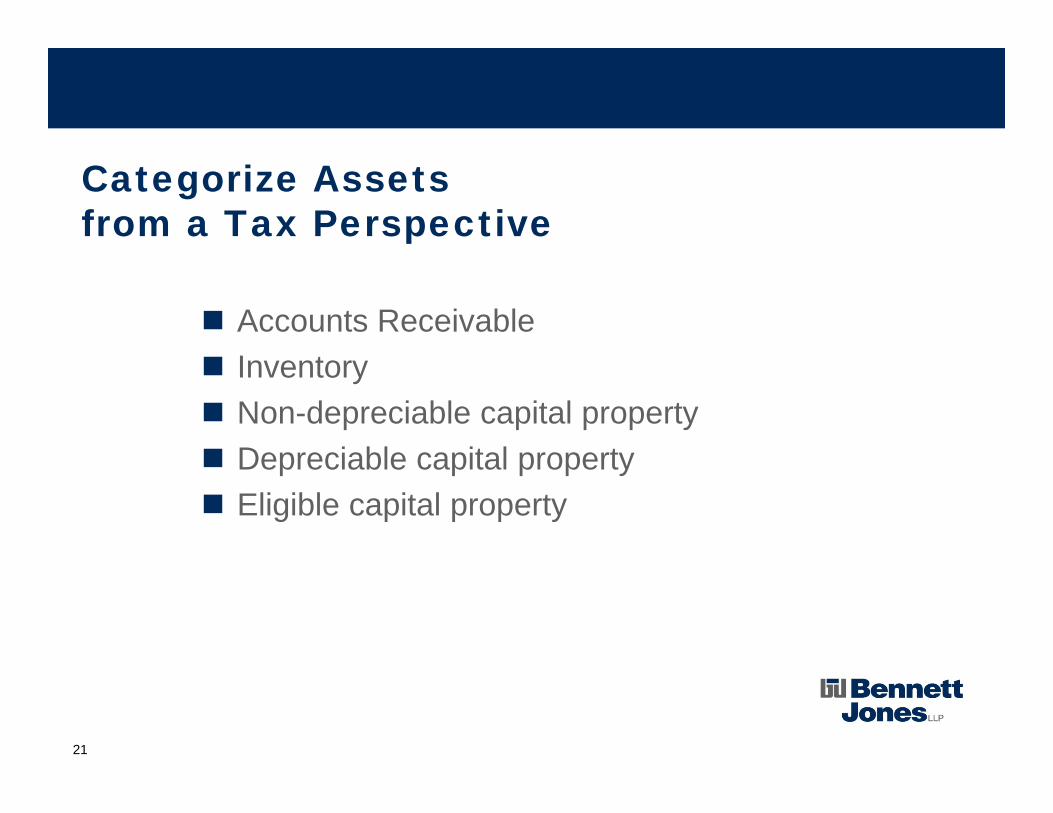

Categorize Assets from a Tax Perspective

Accounts ReceivableInventoryNon-depreciable capital propertyDepreciable capital propertyEligible capital property

21

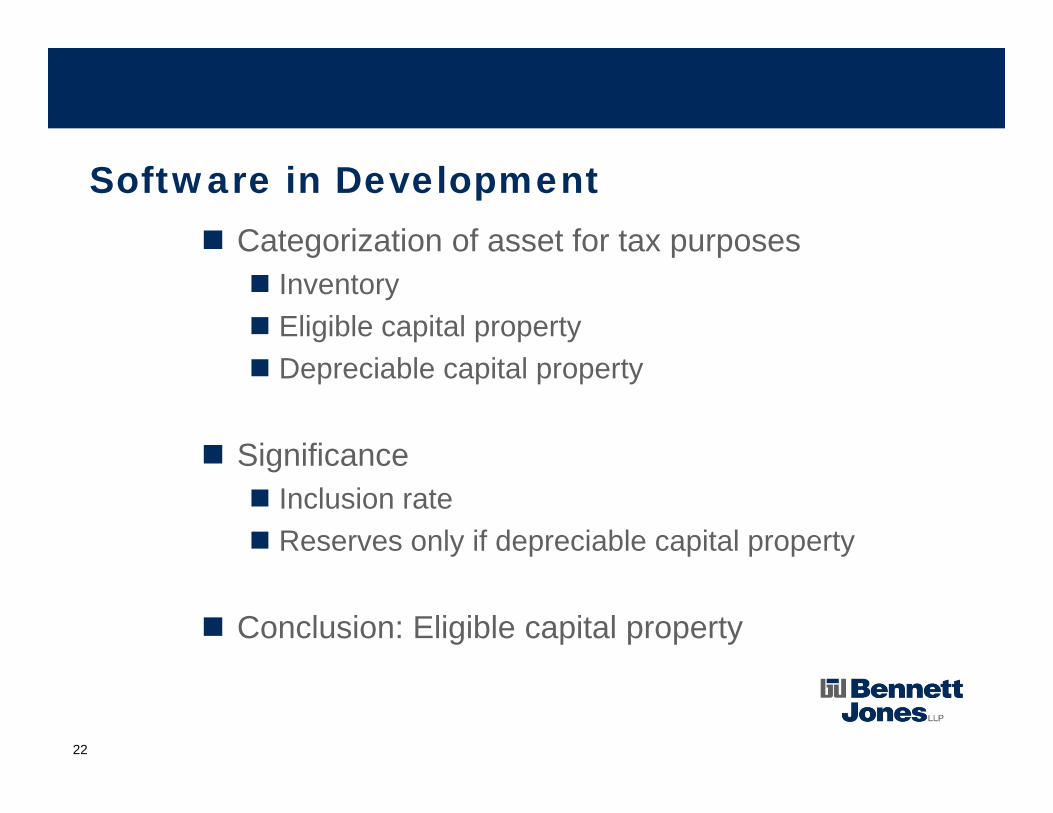

Software in DevelopmentCategorization of asset for tax purposes

InventoryEligible capital propertyDepreciable capital property

SignificanceInclusion rateReserves only if depreciable capital property

Conclusion: Eligible capital property

22

What’s the big deal about allocation clauses?

23

Allocation of Purchase Price

Mutual

Vendor’s interest and Purchaser’s interest mutually exclusive

Trade-offs?

24

TENSION!!!!

Non-depreciable capital propertyDepreciable capital property

Little or no recaptureEligible capital propertyDepreciable capital propertyInventory

InventoryDepreciable capital property – high rate CCAEligible capital propertyDepreciable capital property – low rate CCACapital property

Vendor’s Preference

Purchaser’s Preference

25

Acceptance by CRAOpposing InterestsCRA generally acceptsS.68

Not reasonable in circumstancesNo evidence of hard bargaining in negotiationsSham, subterfugeProperty and Services

AgreementDetailed allocation

ScheduleProcess to determine

Covenant to file consistently

26

Where are the Forms?

27

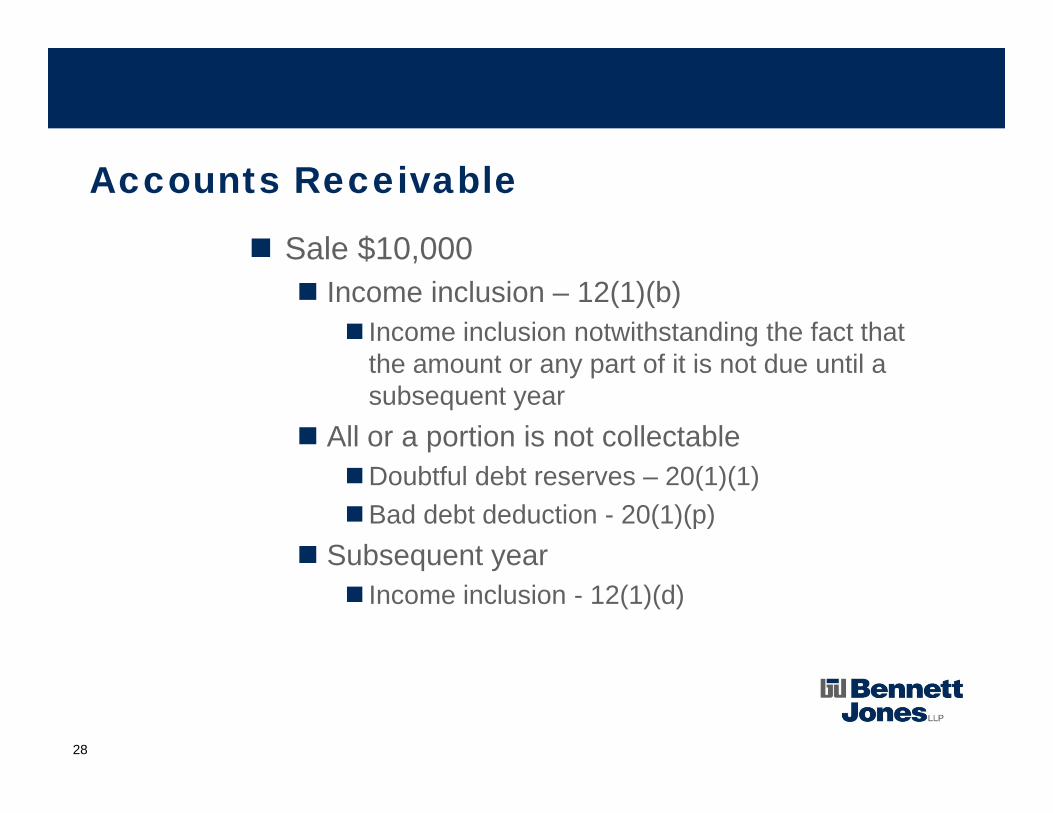

Accounts Receivable

Sale $10,000Income inclusion – 12(1)(b)

Income inclusion notwithstanding the fact that the amount or any part of it is not due until a subsequent year

All or a portion is not collectableDoubtful debt reserves – 20(1)(1)Bad debt deduction - 20(1)(p)

Subsequent yearIncome inclusion - 12(1)(d)

28

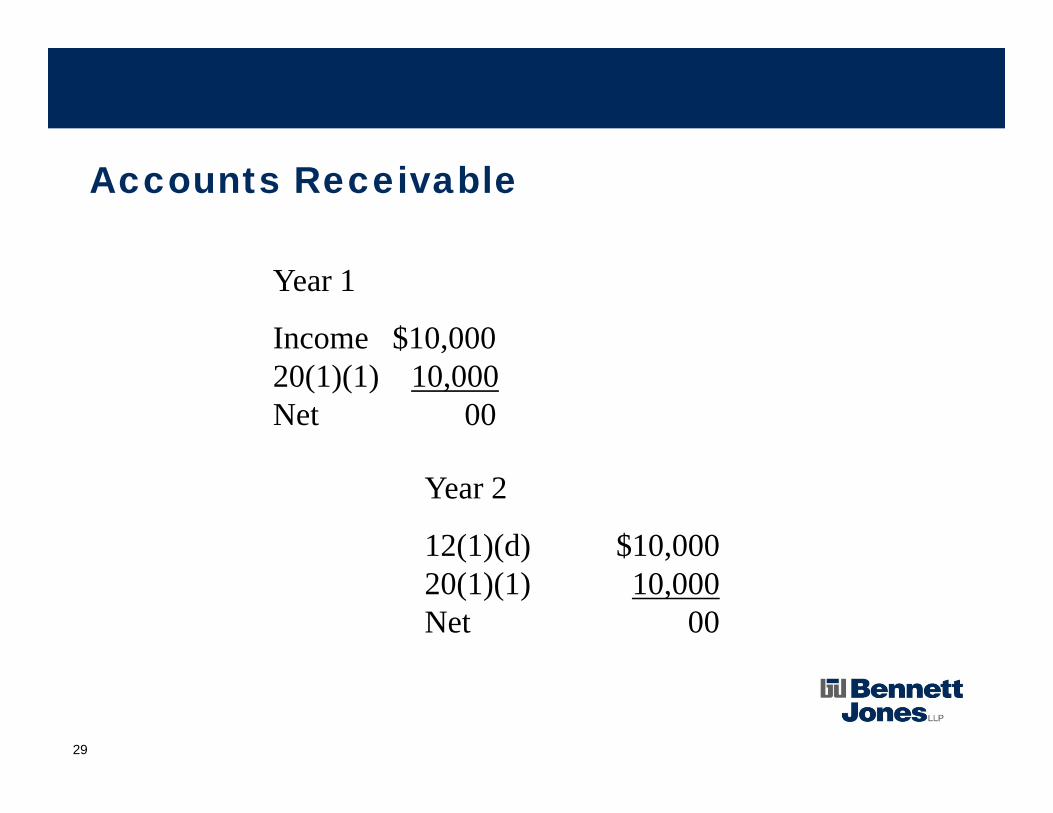

Accounts Receivable

Year 1

Income $10,00020(1)(1) 10,000Net 00

Year 2

12(1)(d) $10,00020(1)(1) 10,000Net 00

29

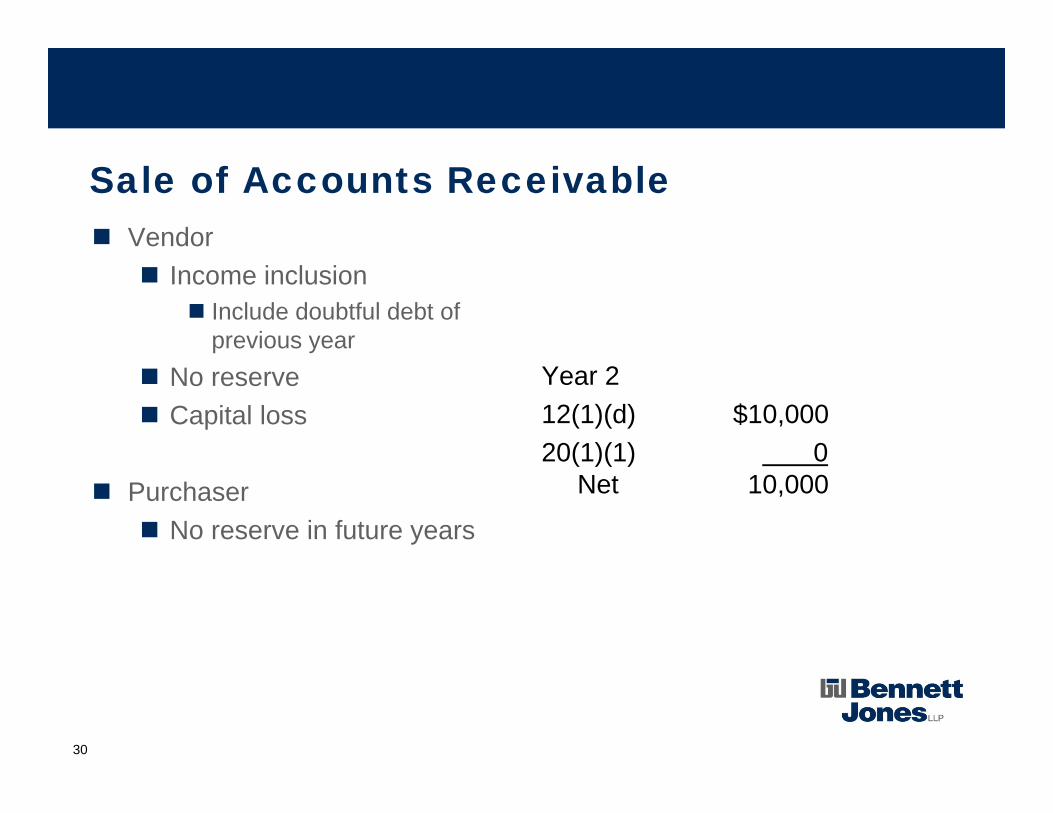

Sale of Accounts ReceivableVendor

Income inclusionInclude doubtful debt of previous year

No reserveCapital loss

PurchaserNo reserve in future years

Year 212(1)(d) $10,00020(1)(1) 0

Net 10,000

30

Accounts Receivable Solution

Section 22 ElectionJoint

ConditionsVendor carries on businessPurchaser proposes to carry on businessAll or substantially all of assets of business

31

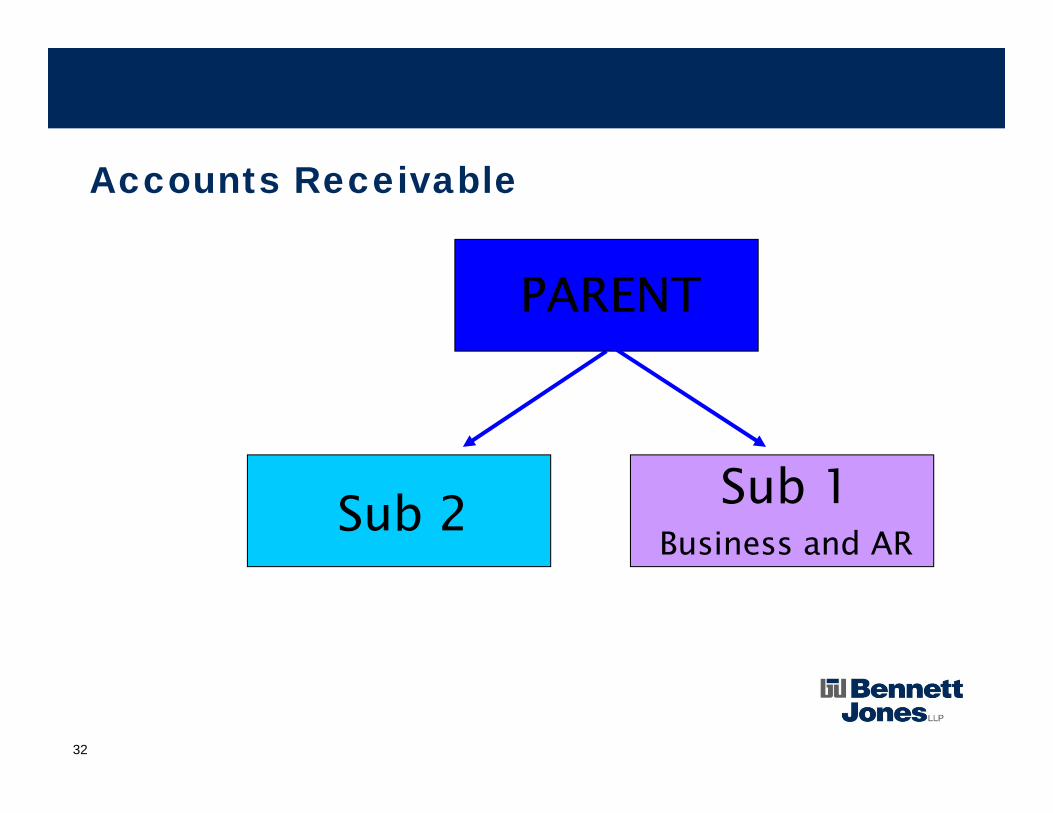

Accounts Receivable

PARENT

Sub 2 Sub 1Business and AR

32

Accounts Receivable

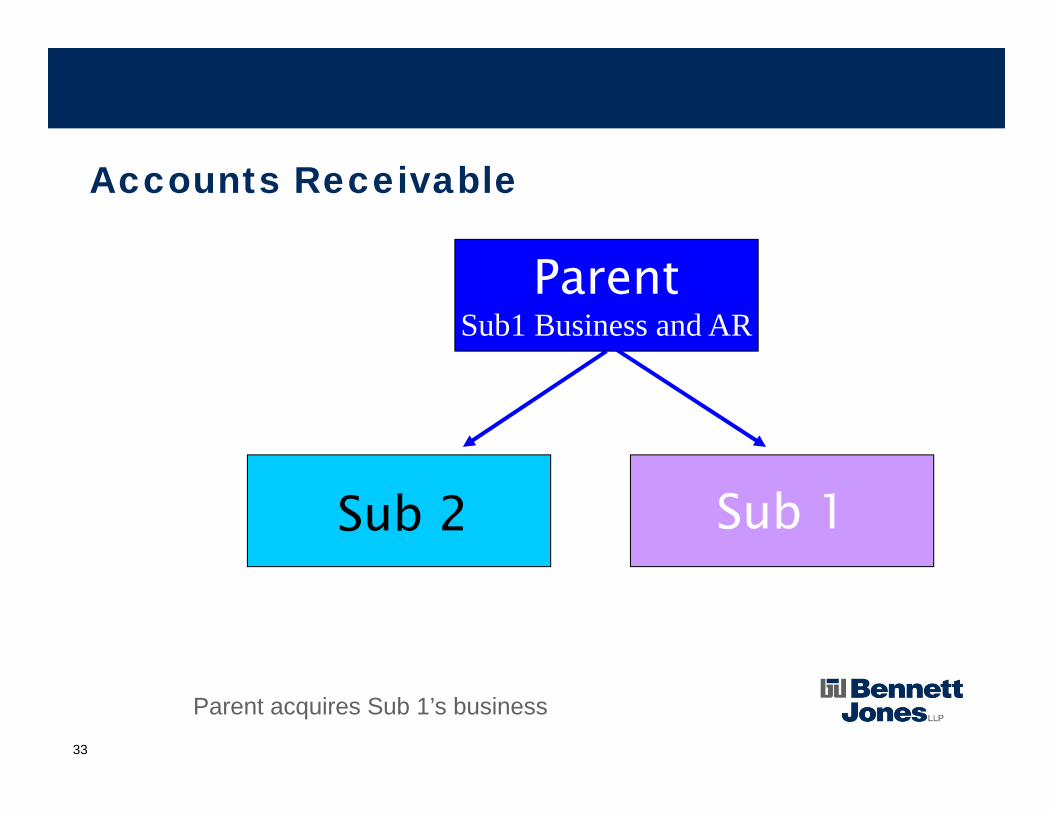

Sub 1

ParentSub1 Business and AR

Sub 2

Parent acquires Sub 1’s business33

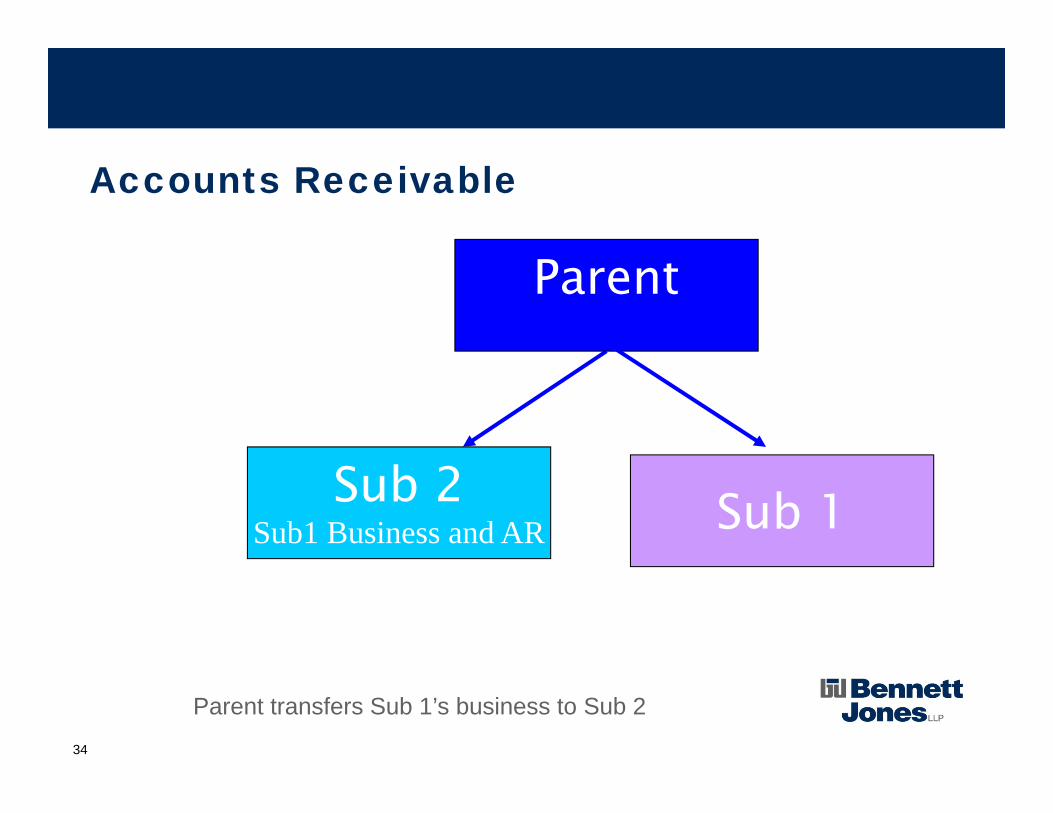

Accounts Receivable

Sub 2Sub1 Business and AR Sub 1

Parent

Parent transfers Sub 1’s business to Sub 234

Accounts Receivable, cont’d

ConditionsVendor carries on the businessPurchaser (Parent) proposes to carry on the businessSection 22 election not available

35

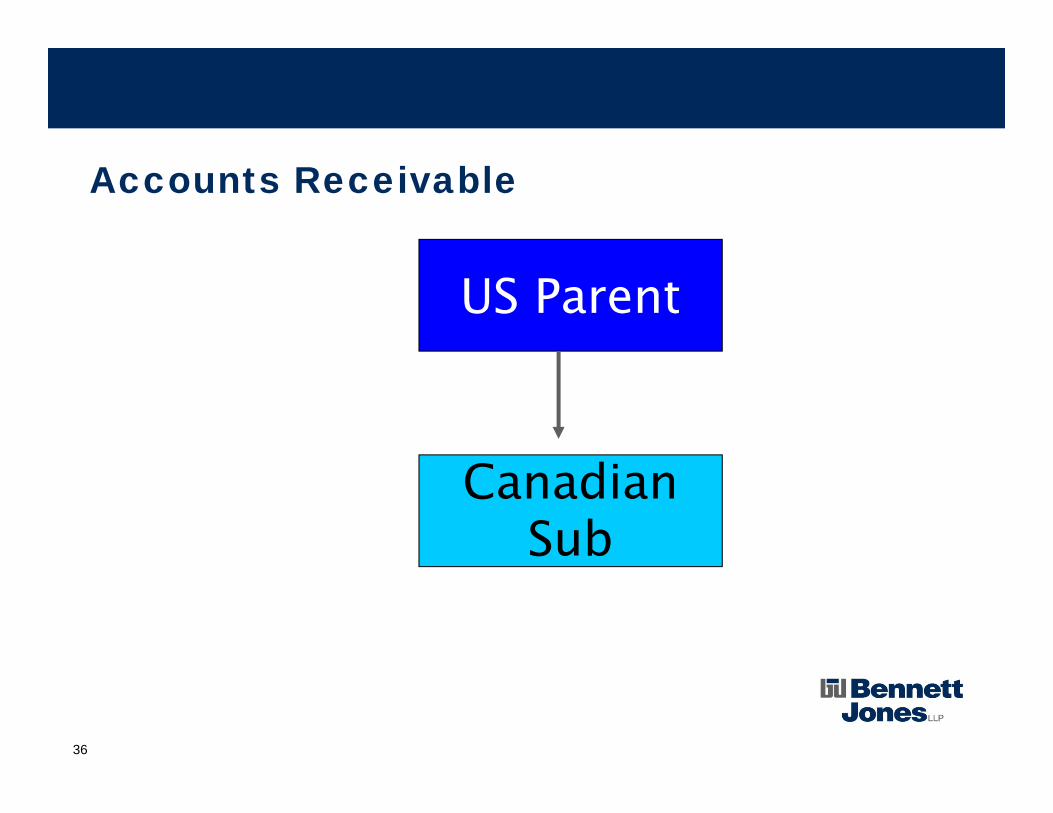

Accounts Receivable

US Parent

Canadian Sub

36

Accounts Receivable

US Parent

Canadian Sub

Canadian Vendor

Machinery and Equipment

Inventory and AR

37

Accounts Receivable, cont’d

ConditionsAll or substantially all of the assets of the vendor

Section 22 election not available

38

Accounts Receivable, cont’d

All accounts receivable of business?

Transportation CompanyTrucking business, courier businessSelling trucking business

Separate business

Who bears risk if election not available?

39

How can they pay tax if they’re not getting any money?

40

Deferrals

ReservesAmount due after end of yearDemand note?

StrategyTerm of promissory noteAmount of down payment

41

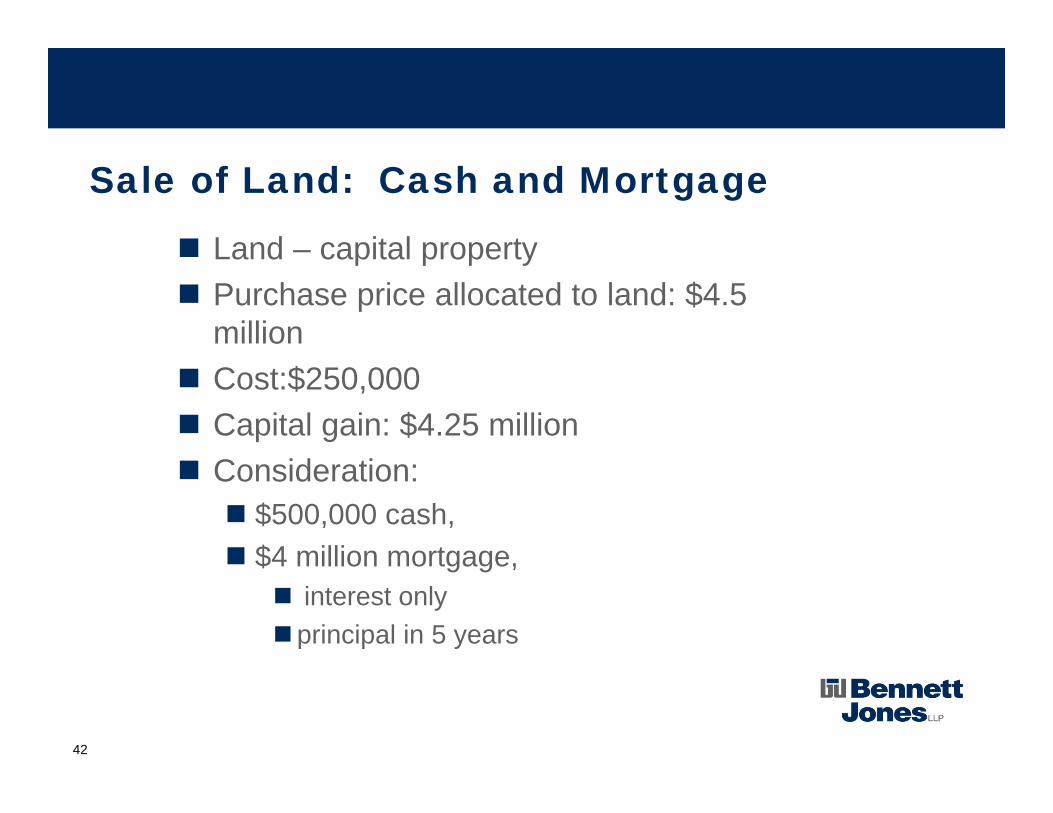

Sale of Land: Cash and Mortgage

Land – capital propertyPurchase price allocated to land: $4.5 millionCost:$250,000Capital gain: $4.25 millionConsideration:

$500,000 cash, $4 million mortgage,

interest onlyprincipal in 5 years

42

Tax in Year of Sale

Proceeds 4,500,000Less: ACB 250,000Capital Gain 4,250,000

Taxable capital gain 2,125,000

Tax (48.7%)** 1,034,875

** a portion of tax is refundable on payment of dividends

43

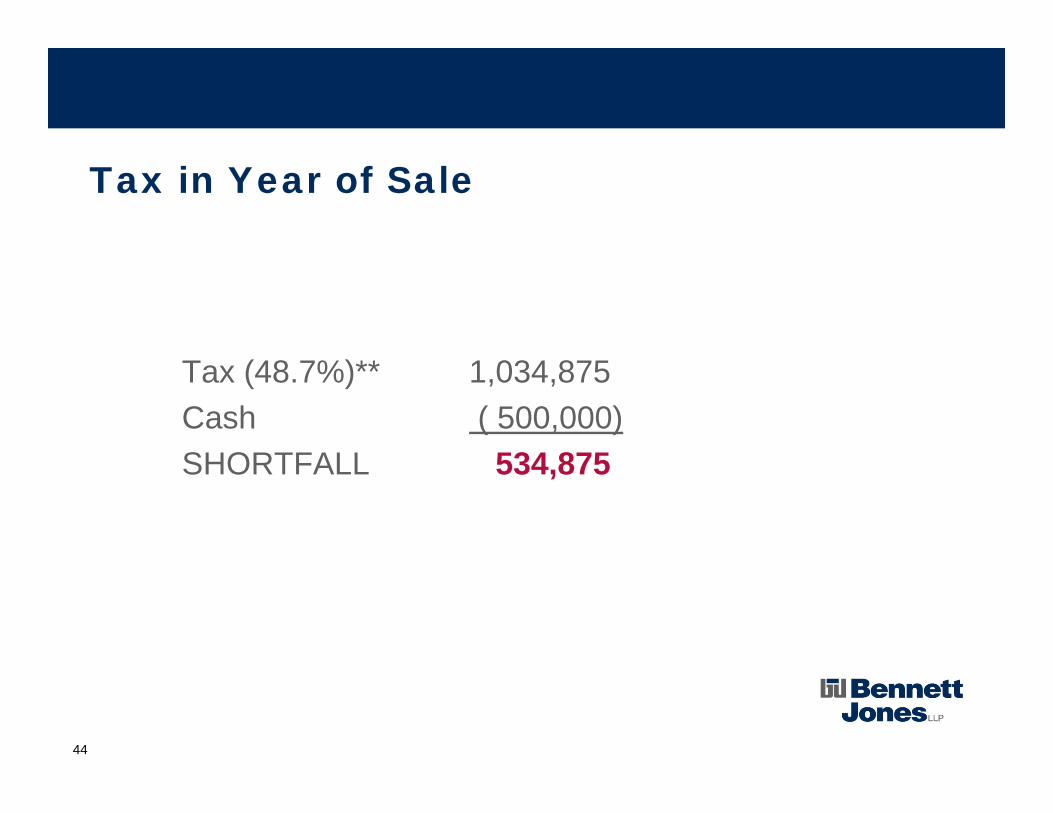

Tax in Year of Sale

Tax (48.7%)** 1,034,875Cash ( 500,000)SHORTFALL 534,875

44

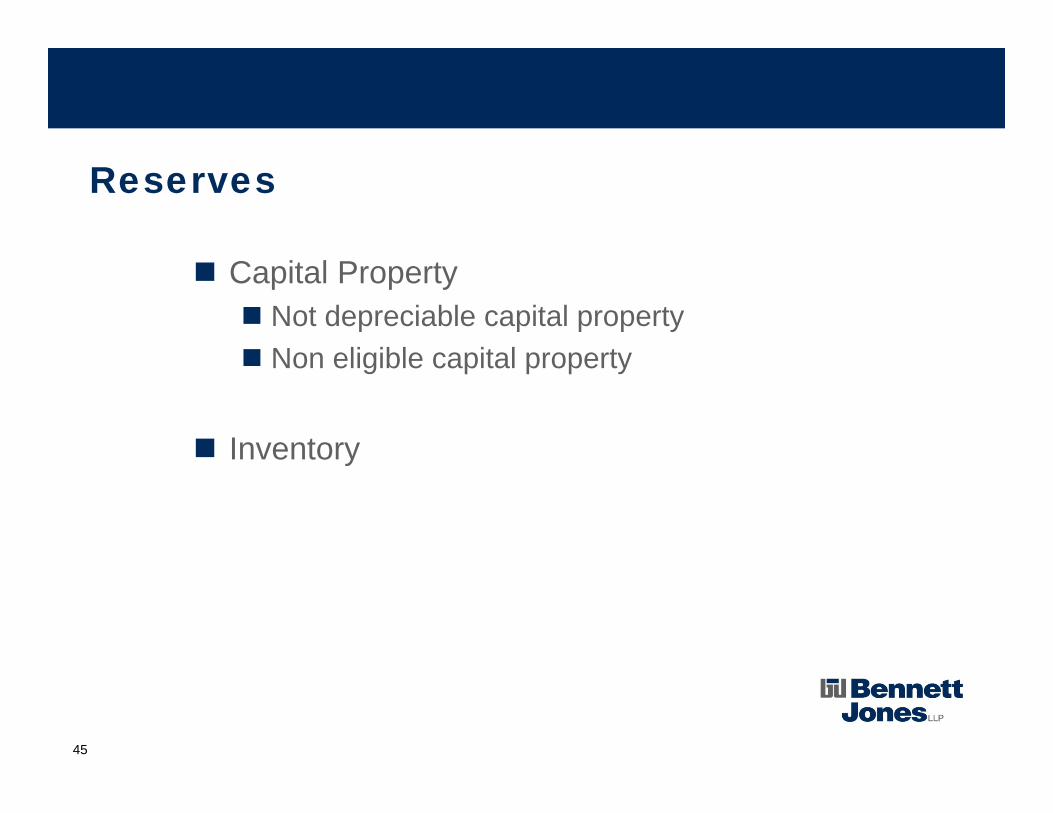

Reserves

Capital PropertyNot depreciable capital propertyNon eligible capital property

Inventory

45

Tax in Year of Sale Proceeds 4,500,000Less: ACB 250,000Capital Gain 4,250,000Reserve 3,400,000Gain 850,000

Taxable capital gain 425,000

Tax (48.7%)** 206,975

Cash Remaining = $293,025

** a portion of tax is refundable on payment of dividends

46

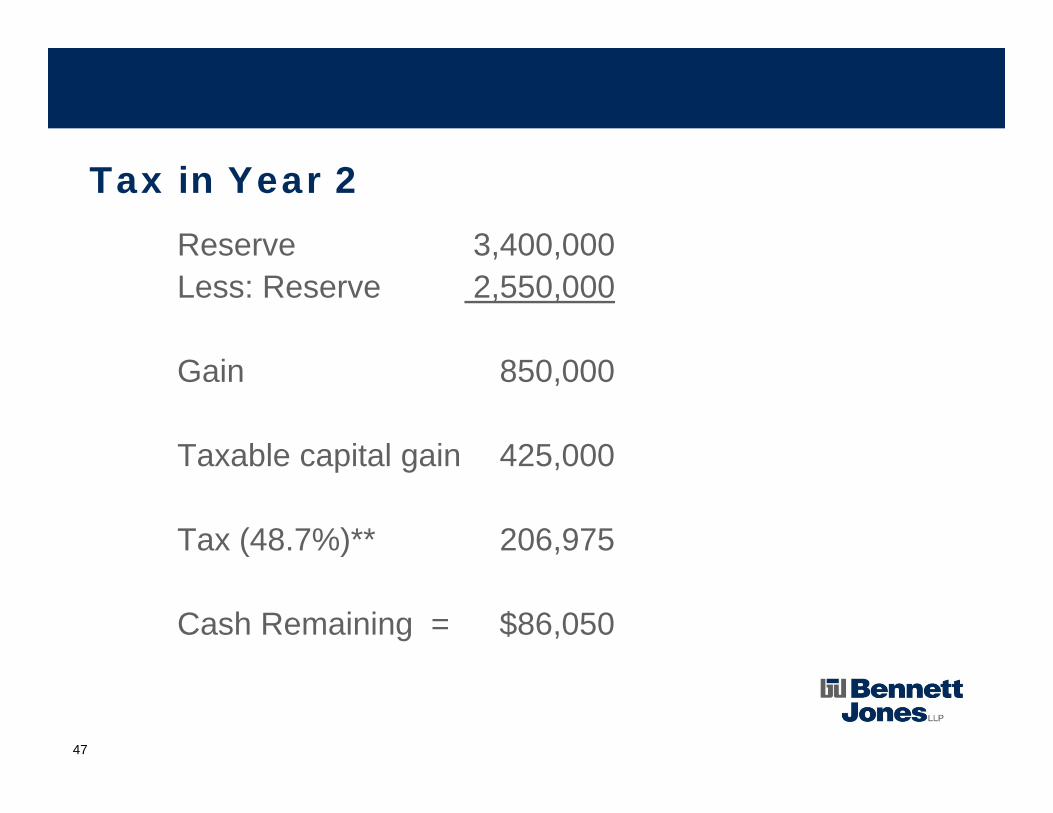

Tax in Year 2 Reserve 3,400,000Less: Reserve 2,550,000

Gain 850,000

Taxable capital gain 425,000

Tax (48.7%)** 206,975

Cash Remaining = $86,050

47

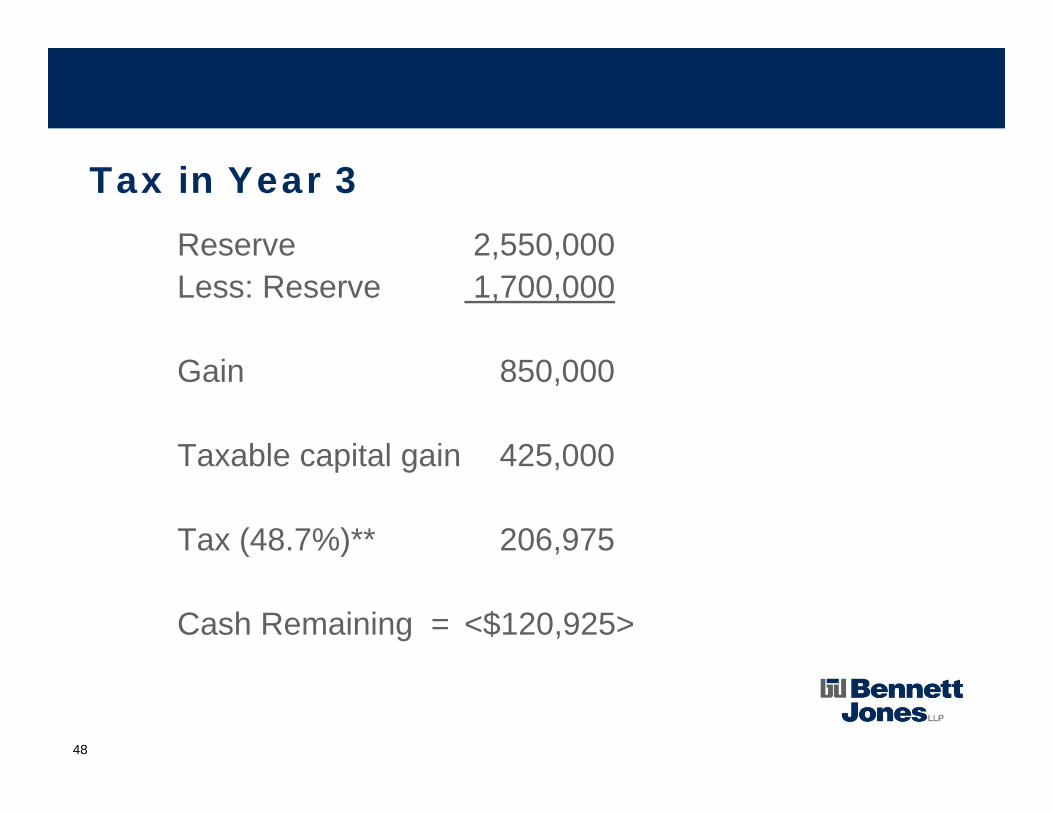

Tax in Year 3 Reserve 2,550,000Less: Reserve 1,700,000

Gain 850,000

Taxable capital gain 425,000

Tax (48.7%)** 206,975

Cash Remaining = <$120,925>

48

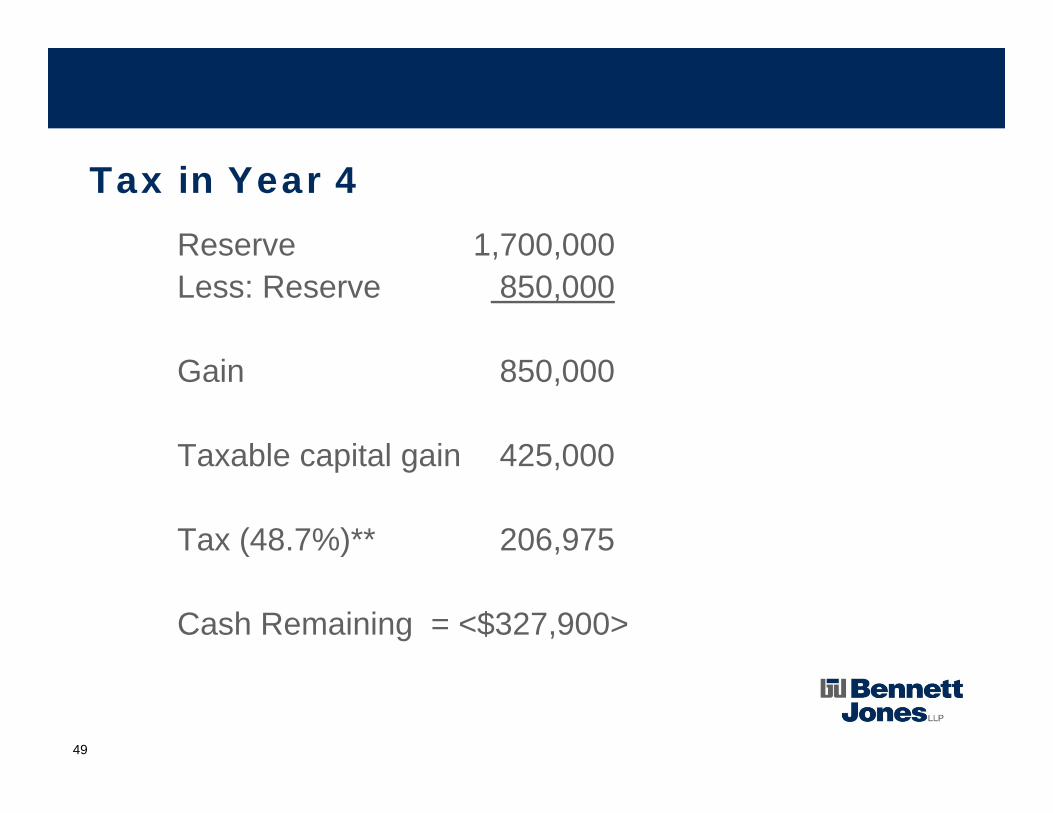

Tax in Year 4 Reserve 1,700,000Less: Reserve 850,000

Gain 850,000

Taxable capital gain 425,000

Tax (48.7%)** 206,975

Cash Remaining = <$327,900>

49

Tax in Year 5 Reserve 850,000Less: Reserve 000

Gain 850,000

Taxable capital gain 425,000

Tax (48.7%)** 206,975

Cash Remaining = 4,172,100

50

Let’s Reduce the Purchase Price with Consulting Payments!

51

Consulting AgreementPurchase deduct payments provided reasonable

services provided, etc.

Income inclusion at full ratesDeferralEarned income for RRSP

52

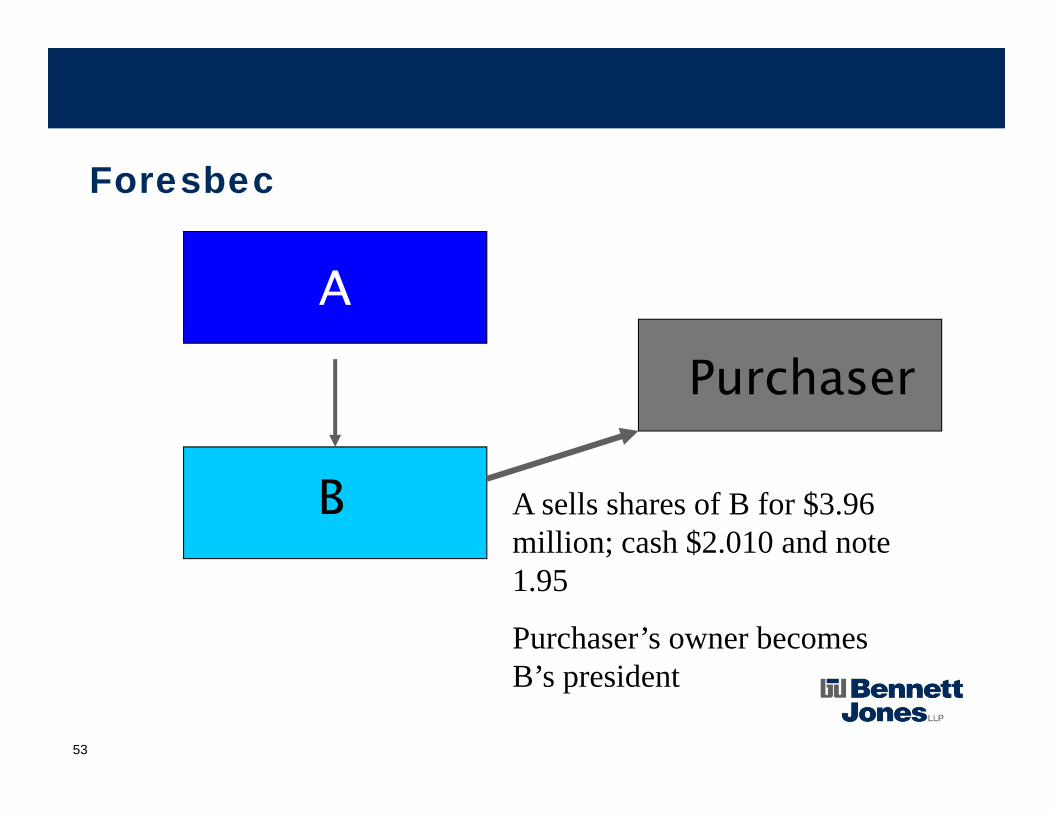

Foresbec

A

B

Purchaser

A sells shares of B for $3.96 million; cash $2.010 and note 1.95

Purchaser’s owner becomes B’s president

53

ForesbecMajor disagreement between Purchaser’s shareholder and A’s presidentPurchaser’s shares in B acquired by A: price was equal to cash of $1,750,000 unpaid purchase price and waiver of other amountsContract provided that B would enter into contract for services with Purchaser’s President for $150,000 to be paid over 3 years

Signed by A, B, not PurchaserB deducted payment

54

Foresbec

TCC, FCADeduction in computing income denied

guarantee of paymentenable to purchase sharesno services

Ss.15(1) benefit since B paid part of purchase price for purchase of shares by AStatute-barred years openPenalties

55

Let’s reduce the purchase price

Separate agreementsConsiderationReasonablePigs get fat, hogs get slaughtered

56

Now that all this money is in the company ….

57

Distribution of After-Tax Proceeds

Repayment of shareholder loans

Return of paid-up capital

Capital dividend

Taxable dividend

58

Thank you

59