tax incentives for farm businesses - university of...

TRANSCRIPT

Tax Incentives

For Farm Businesses

Parman R. Green UM Extension Ag Business Mgmt. Specialist

111 N. Mason

Carrollton, MO 64633

(660) 542-1792

[email protected] http://agebb.missouri.edu/agtax/index.htm

2

Business – Tax Strategies

Section 179 - “expense capital expenditures”

First-year Bonus Depreciation - “economic stimulus”

Domestic Production Deduction - “must pay wages”

Long-term Capital Gains - “can’t beat free”

Medical Expenses - “hire your spouse”

Home Office - “a business should have an office”

Travel - “make it a business trip”

Education - “put your child to work”

3

Business of Farming - Not Schedule F Instructions

File Schedule C (Form 1040) instead of

Schedule F if :

(a) Your principal source of income is from

providing agricultural services such as

soil preparation, veterinary, farm labor,

horticultural, or management for a fee

or on a contract basis,

or

(b) you are engaged in the business of

breeding, raising, and caring for dogs,

cats, or other pet animals.

4

Hobby or Business? factors IRS will look for:

business-like

time and effort

depend on the revenue

circumstances beyond the taxpayer’s control (losses)

operation changed over time

knowledge

profit in similar activities

appreciation of the assets

5

Presumption of “For Profit”

General Rule:

Report profit at least 3 of last 5 tax years

Breeding, Training, Showing, or Racing Horses:

Report profit at least 2 of last 7 tax years

6

Section 179

Maximum Section 179 is indexed:

$500,000 for 2011

$139,000 for 2012

Limits amount for SUVs (between 6,000 to 14,000 lbs)

$25,000

7

Section 179

2011:

Section 179 limited for investments over $1,000,000

$1 for every $1 over $1,000,000

2012:

Section 179 limited for investments over $560,000

$1 for every $1 over $560,000

First-year Bonus Depreciation

Percentage: 50% for 2012 (100% for 2011)

Qualifying Property:

MACRS property with recovery period of 20 years

or less

Acquired during 2012

Original use commences with taxpayer

Dollar Limit: None

8

9

Domestic Production Deduction

Provides for a deduction to help offset the

repeal of the Extra-Territorial Income

Exclusion

Deduction is 9 percent for 2012

10

Domestic Production Deduction

Acronyms to Know

DPAD - Domestic Production Activities Deduction

DPGR - Domestic Production Gross Receipts

MPGE – Manufactured, Produced, Grown, Extracted

(qualifying domestic activities)

QPAI - Qualified Production Activities Income

QPAI = DPGR - COGS - Expenses

11

Domestic Production Deduction

Limited to lesser of :

9% Qualified Production Activities Income (QPAI)

9% of Taxable Income (entity) or AGI (individuals)

50% of W-2 Wages

12

Domestic Production Deduction

QPAI :

For most farmers the QPAI will be the sum of

their Schedule F net income and the gain

from the sale of raised breeding, dairy, or

draft livestock reported on Form 4797.

13

Domestic Production Deduction

Excluded Income:

Sales of purchased draft, breeding, or dairy livestock

Sales of land, machinery, or equipment

Patronage dividend if coop allocates DPAD

Contract animal production (animals not owned by taxpayer)*

Custom hire income*

Direct Payments (CCC)*

Transportation activities*

* 5% Safe Harbor Rule

14

Domestic Production Deduction

Wages paid do not include:

Wage paid in commodities

Wages paid to your child under age 18

Compensation paid in non-taxable fringe benefits

15

Long-Term Capital Gains Tax

Federal rates: generally, 15% or 0%

Exceptions:

Gain on collectibles 28%

Unrecaptured Section 1250 gain 25%

16

Long-Term Capital Gains Tax

15% or 0% ?

15% - if the regular tax rate that would apply is

greater than 15%

0% - if the regular tax rate that would apply is

15% or less

17

Medical Expenses - Business

Requirements:

Employ your spouse

Establish health reimbursement plan (Sec. 105 Plan)

Advantages:

Deductible as Sch F business expense

Avoids any Sch A itemized deduction limitation

Reduces self-employment taxes

18

Health Savings Account

(HSA)

Tax Benefit:

Tax deduction for contribution

Tax-free earnings

Tax-free withdrawals for qualified medical

expenses

19

Who Can Have an HSA

Any adult if they:

Have coverage under a “high deductible health plan” (HDHP)

Have no other first-dollar medical coverage

Do not participate in FSA or HRA that reimburses expenses before deductible amount of HSA is reached

Limited-purpose FSA or HRA

can pay for “other health coverage”, except L-T care

20

High Deductible Health Plans 2012

Does not cover first-dollar expenses

Deductible must be at least:

$1,200 – self-only coverage

$2,400 – family coverage

Annual out-of-pocket expenses cannot exceed:

$ 6,050 – self-only coverage

$12,100 – family coverage

21

High Deductible Health Plan

Example - George

Self-only coverage

$2,000 deductible (DED)

$6,050 out of pocket (OOP)

22

High Deductible Health Plan

Example - George

Hospitalized for seven days:

$15,000 total cost

- 2,000 deductible (HSA or OOP)

= 13,000

- 1,950 15% co-pay (OOP)

= $11,050 paid by HDHP

George has now paid $3,950 of his annual $6,050

maximum out-of-pocket expenses.

23

Who Can Have an HSA

Any adult if they:

Are not enrolled in Medicare

Cannot be claimed as dependent on

someone else’s tax return

24

Health Savings Account

No earned income requirement

No maximum income limitation

No required distribution at age 70½

25

HSA Contributions - 2009

Up to the amount of your HDHP deductible, but

not more than:

$3,100 – self-only coverage

$6,250 – family coverage

Age 55 or older “catch-up” -- $1,000

Thus, maximum for a couple both 55 or older is

$8,250.

26

HSA Contributions

Can be made up to April 15th of following

year

Account holder gets deduction for

contributions to their HSA, even if someone

else makes the contribution

27

Home Business Office

Must be used “Exclusively and Regularly”

As the “Principal Place of Business

Place to meet or deal with clients or customers

28

Principal Place of Business

Must meet both:

Used exclusively & regularly for administrative or

management activities

Have no other fixed location where you conduct

substantial administrative or management activities

29

Home Business Office Deduction

The following office expenses are limited if

business expenses are greater than business

gross income

Utilities

Insurance

Depreciation

30

Travel and Meals

100% Deductible

Air, rail, auto

Lodging

Telephone

Dry cleaning

Tipping for any of the above

50% Deductible

Meals while traveling

31

Travel

Outside United States:

Entirely for business – deduct all your expenses

Primarily for business – allocation between business

and personal activities

On Cruise Ships:

Deductible if:

Bonda fide business-related program on board

Majority of days are spent in program attendance

Ship is registered in the U.S.

Ship stops only at U.S. ports (or possessions)

Trip costs are less than $2,000

32

Education Costs - Child

“Put them to work”

If farmer – gift them last year’s raised grain

Be aware of “kiddie tax”

Gift them appreciated stock

Be aware of “kiddie tax”

33

Resources - Online

Farmer’s Tax Guide – IRS Publication 225 http://www.irs.gov/pub/irs-pdf/p225.pdf

Ag Tax Tidbits http://agebb.missouri.edu/agtax/

34

Entertainment

Directly-Related Test:

Main purpose was the active conduct of business

You did engage in business

More than general expectation of getting income or some specific business benefit

Associated Test:

Associated with active conduct of business

Entertainment was directly before or after substantial business discussion

Deduction generally only 50%

35

Wages Paid In-Kind

Fundamental Principles:

Payment not in form readily converted to cash

Employee must exercise dominion and control

over the payment

36

IRS Guidelines – Wages Paid In-Kind

Commodity Identified

Documentation of Transfer

Not Intended to be Substitute for Cash

Employee - Negotiates Sale

Employee - Risk of Gain or Loss

Time Interval Between Receipt and Sale

Employee – Bears Cost of Ownership

37

Observations –– In-Kind Wages

are considered compensation for purposes of

IRA contributions.

are not considered “wages” for the earnings test

in retirement.

38

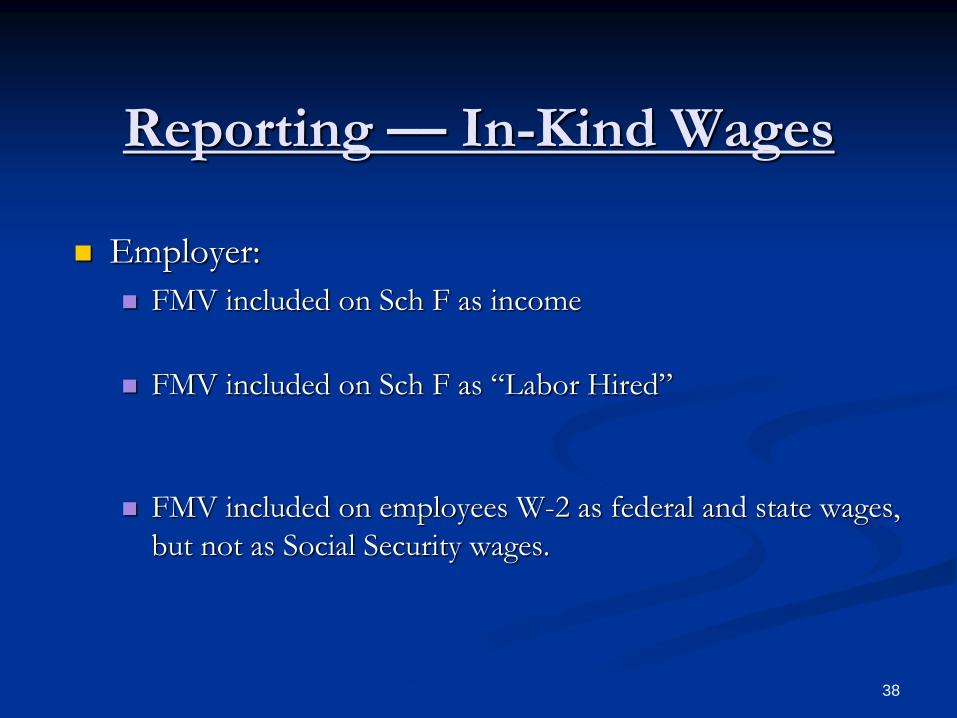

Reporting –– In-Kind Wages

Employer:

FMV included on Sch F as income

FMV included on Sch F as “Labor Hired”

FMV included on employees W-2 as federal and state wages,

but not as Social Security wages.

39

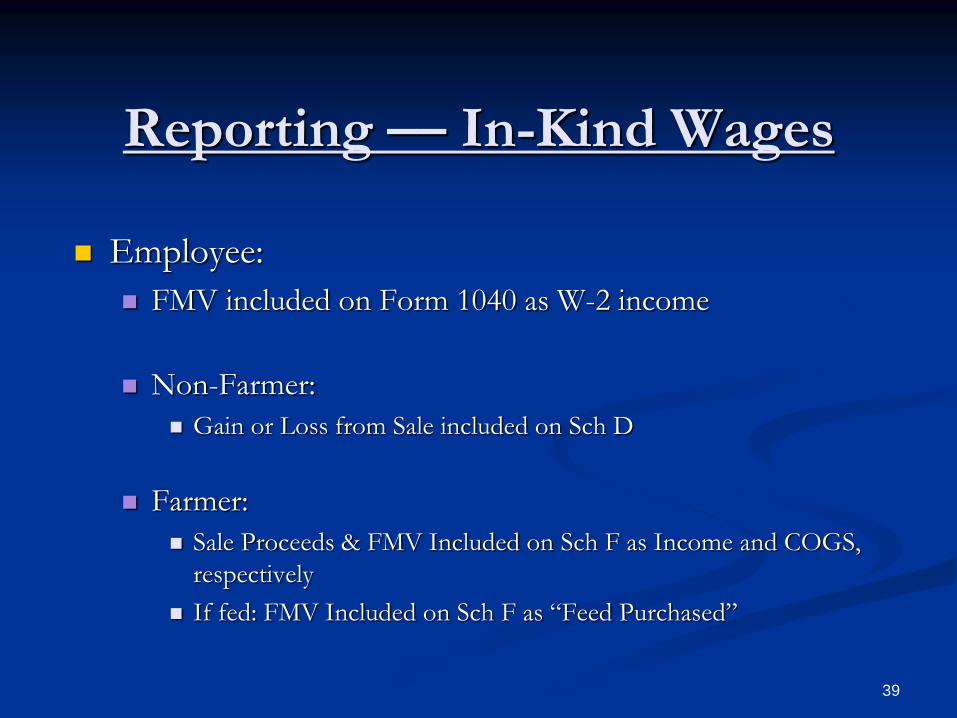

Reporting –– In-Kind Wages

Employee:

FMV included on Form 1040 as W-2 income

Non-Farmer:

Gain or Loss from Sale included on Sch D

Farmer:

Sale Proceeds & FMV Included on Sch F as Income and COGS,

respectively

If fed: FMV Included on Sch F as “Feed Purchased”

40

Wages – FICA Paid by Employer

Employees share of FICA taxes :

counts as wages subject to income tax

not counted as wages subject to Social Security

& Medicare taxes

41

Wages – FICA Paid by Employer

Example : Employer pays employee’s share of FICA taxes on wages of $10,000. W-2 Box 1 Wages, tips, etc. $10,765

$10,000 x 1.0765

Pub. 225 – Social Security & Medicare Taxes

W-2 Box 3 Soc. Security Wages $10,000

W-2 Box 5 Medicare Wages $10,000 (this example assumes the employee withholding is 7.65%)