tax impact study 06-08-102

TRANSCRIPT

8/8/2019 Tax Impact Study 06-08-102

http://slidepdf.com/reader/full/tax-impact-study-06-08-102 1/15

The Impact of H.R. 4213 on PrivateEquity Investment and EmploymentJason M. Thomas • June 2010

8/8/2019 Tax Impact Study 06-08-102

http://slidepdf.com/reader/full/tax-impact-study-06-08-102 2/15

Private Equity Council • June 2010 1

The Impact of H.R. 4213 on Private Equity Investment and Employment

1

ItutI

H.. 4213, Te “American Jobs and losing tax Loopholes Ac 2010” wold increase he ax rae onlong-erm capial gains income received hrogh a carried ineres in a parnership rom he crren rae

o 15% o 38.5% when lly-phased in. Tis represens a 157% ax increase, or more han a dobling o he governmen’s share o hese parnerships’ long-rn invesmen income. Sch a signifcan increase inhe eecive ax rae on long-erm invesmen cold have deleerios economic conseqences.

Te mos immediae economic impac o he ax increase wold likely be el in he real esae secor,which conines o ser rom low prices and high deals. Te deal rae or commercial propery morgages held by u.S. banks more han dobled in he orh qarer o 2009 and is expeced o in-crease hrogho 2010. ne in wo parnerships in America are in real esae and hese 1.48 million realesae parnerships hold more han $4.2 rillion in asses.1 By comparison, he oal vale o all real esaeowned by nonfnancial corporae bsinesses in America is $6.3 rillion.2 Increasing axes on real esae

parnerships redces aer-ax rerns, which cold redce he prices hese invesors are willing o bidon properies. Te likely eec is o redce prices rher, which wold increase deal raes. 3 Tis coldplace addiional pressre on regional banks, as insred deposiory insiions wih $100 million o $1billion in asses hold 25% o commercial propery loans osanding and 15% o all aparmen loans. 4

While he impac on real esae is likely o be more immediae given crren marke condiions, anohersignifcan long-rn economic eec will come rom he redcion in corporae fnance-oriened privaeeqiy invesmen. Venre capial, growh capial and byo nds channel capial o oherwise capial-consrained sar-ps, small-and-medim sized bsinesses, and larger companies in need o resrcringor new sraegic direcion. While i is exceedingly dicl o isolae he marginal impac on parnershipinvesmen behavior o an increase in an eecive ax rae precisely, invesmen and ax daa rom 1980 o

2009 sgges ha:

• A one percenage poin increase in he eecive ax rae is associaed wih a $1.8 billion decrease inannal privae eqiy invesmen, holding oher acors consan. Tis fnding is saisically signifcana he 94% confdence inerval.

• A one percenage poin increase in he eecive ax rae is associaed wih a 1.07% decrease in annalprivae eqiy invesmen, holding oher acors consan. Based on 2009 invesmen levels, hiswold ranslae o a $525 million redcion in invesmen or every one percenage poin increasein he ax rae.

• H.. 4213, Te “American Jobs and losing tax Loopholes Ac 2010” wold increase he eecive

1 Inernal evene Service, Saisics o Income ivision, Fall SI Bllein, Ags 2009.2 Federal eserve Board o Governors, Z1: Flow o Fnds Accons o he unied Saes, B.102.3 Te mos signifcan variable or predicing commercial morgage deal is he vale o he nderlying propery in relaion

o he ace vale o he morgage. See Li, Jabbor, and Green (2007).4 Bloomberg, “ommercial Morgage eal ae in u.S. More han obles,” Febrary 24, 2010.

8/8/2019 Tax Impact Study 06-08-102

http://slidepdf.com/reader/full/tax-impact-study-06-08-102 3/15

Private Equity Council • June 2010 2

The Impact of H.R. 4213 on Private Equity Investment and Employment

2

ax rae on privae eqiy invesmen o 38.5%. Tis ax increase cold redce privae eqiy inves-men by beween $7.7 billion and $27 billion per year relaive o wha i oherwise wold have been.Tis does no sgges ha privae eqiy invesmen will no conine o grow as oal invesmen willbe inenced by many acors oher han ax raes. aher, i implies ha he higher eecive ax rae

cold case re invesmen levels o be lower han hey wold have been absen he ax increase.

• Based on relaionship beween invesmen and job creaion esimaed in he Adminisraion’s iniialsimls orecas, his redcion in invesmen wold case aggregae employmen o be beween36,600 and 127,800 lower han i oherwise wold have been. Te job losses wold all disproporion-aely on small-o-medim sized bsinesses. oghly 72% o all privae eqiy invesmens are made incompanies wih marke vales o less han $250 million.

• Tree sizeable changes o he eecive ax rae on privae eqiy invesmen have been enaced onhree occasions in he pas hiry years: 1986, 1997, and 2003. In each o hese cases, he change in heeecive ax rae had he prediced impac on privae eqiy invesmen as measred in he or yearsbeore and aer he rae change.

Te ollowing secion provides a smmary o he daa and nare o he analysis. Secion hree providesa more deailed review o hree previos periods when he eecive ax rae on privae eqiy invesmenwas changed. Secion or concldes.

8/8/2019 Tax Impact Study 06-08-102

http://slidepdf.com/reader/full/tax-impact-study-06-08-102 4/15

Private Equity Council • June 2010 3

The Impact of H.R. 4213 on Private Equity Investment and Employment

3

AtA A AALSIS

Tis analysis relies on daa accessed hrogh he Tomson eers ne Banker Privae Eqiy daabase.Tese annal daa cover he amon o repored eqiy invesed in u.S. bsinesses by all orms o privae

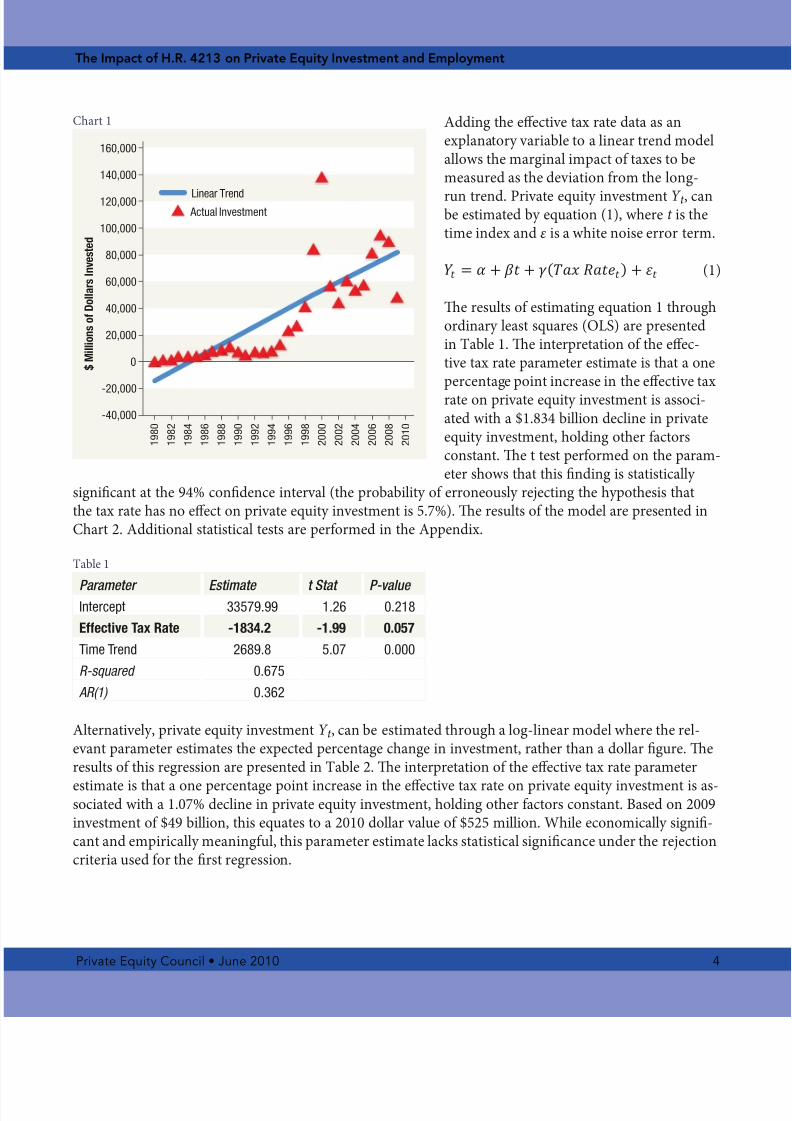

eqiy — venre, byo, growh capial — rom 1980 o 2009. In some privae eqiy ransacions, hesponsored company also raises exernal deb o complee he invesmen. Tese borrowings have beenexclded rom his analysis so as o ocs exclsively on he risk capial invesed direcly by privae eqiy parnerships. ver he pas 30 years, annal privae eqiy invesmen in he unied Saes increasedrom $723 million in 1980 o $49 billion in 2009. Te record or amon invesed was se in 2000 when$137 billion was invesed in more han 7,000 bsinesses. Annal invesmen also exceeded $80 billion in2006 hrogh 2008. Te invesmen daa are available in table A in he Appendix.

Parnership income ows hrogh o parners. Tis means ha when a parnership earns long-rn capialgains income, is parners pay capial gains axes on hese earnings. As a resl, he eecive ax rae on

privae eqiy invesmen has been he maximm long-rn capial gains ax rae. Tis rae is calclaedeach year by he u.S. treasry eparmen. Te treasry adjss he op saory capial gains rae oaccon or he eecs o exclsions, alernaive ax raes, he minimm ax (1970-78), he alernaiveminimm ax, income ax srcharges, and he phase-o o iemized dedcions. Te treasry daa areavailable in table B in he Appendix.

tax raes are hardly he only acor ha impac privae eqiy invesmen. Indeed, over he pas 30 years,privae eqiy invesmen has grown dramaically hrogh a variey o ax regimes. In 1979, he epar-men o Labor clarifed he “prden man rle” o ensre ha pension nd invesmens in privae eqiy nds wold no consie a violaion o EISA.5 Tis led o remendos growh in he secor, as pensionnds invesed in byo and venre capial nds in he search o higher rerns necessary o mee heir

obligaions o plan benefciaries. As privae eqiy rerns dramaically exceeded hose available in hepblic eqiy markes, more invesmen came owing ino he secor, casing asses nder managemenand invesmen o conine o reach new highs. Invesmen is no only inenced by oal capial raisedb by macro economic condiions, indsry-specifc rends, and fnancing erms. Tis sel-reinorcingrend owards long-rn growh is likely o conine given he conined operormance o privae eqiy relaive o pblic eqiy marke alernaives. As o Sepember 30, 2009, he average privae eqiy ndhad operormed he S&P 500 by 9.62% per year over 5 years and by 9.17% per year over 10 years.

Te long-rn, seclar growh o privae eqiy invesmen reqires ha he daa frs be “derended” be-ore he marginal impac o ax raes can be measred in a saisically valid manner. As shown by Frischand Wagh (1933), his can be accomplished mos ecienly hrogh he inclsion o a ime rend as anexplanaory variable. As seen in har 1, he ime rend capres he long-rn average growh o privaeeqiy invesmen qie well. Tere are some oliers well above and below he line, b he sbseqenobservaions end o qickly rever o rend.

5 GA-08-692, “efned Benef Pension Plans.”

8/8/2019 Tax Impact Study 06-08-102

http://slidepdf.com/reader/full/tax-impact-study-06-08-102 5/15

8/8/2019 Tax Impact Study 06-08-102

http://slidepdf.com/reader/full/tax-impact-study-06-08-102 6/15

Private Equity Council • June 2010 5

The Impact of H.R. 4213 on Private Equity Investment and Employment

5

table 2

Parameter Estimate t Stat P-value

Intercept 7.6510 11.660 0.000

Effective Tax Rate -0.0107 (0.468) 0.643

Time Trend 0.1454 11.109 0.000

R-squared 0.869

AR(1) 0.657

As hese parameers capre he eec o a one percenage poin increase in he eecive ax rae, heimpac o H.. 4213 can be esimaed by mliplying hese esimaes by 14.7. 6 Tis yields a redcion o invesmen o beween $7.7 billion and $27 billion per year. Assming privae eqiy invesmen has hesame impac on gross domesic prodc (GP) as he pblic secor invesmens made in he Americanecovery and einvesmen Ac (AA) — an exceedingly modes assmpion given ha prodciviy gains associaed wih privae eqiy invesmens are likely o be several imes larger — he ax increase

wold resl in a redcion o oal employmen o beween 36,605 and 127,856 ll-ime jobs.

Te impac o he redcion in employmen levels is likely o be concenraed among small-o-medimsized bsinesses. According o thomson eers, beween 2003 and 2008 72% o all privae eqiy

invesmens were made in companies wihmarke vales o less han $250 million.Tis incldes 66% o laer-sage (byoand mezzanine) invesmens and over 80%o venre capial invesmens. Tese bsi-nesses end o be capial consrained, which

makes privae eqiy a logical sorce o fnancing or expansion. In some cases, hebsinesses are new and lack he collaeraliz-able asses necessary o secre a bank loan.In oher cases, he bsiness may lack a rack record or credi raing, which compromisesaccess o exernal deb fnance. Privae eqi-y fnance is oen he only viable alernaiveo he cosly and oen ndesirable process o raising pblic eqiy.

6 As o Janary 1, 2013, he eecive ax rae wold be 38.5% inclding sel-employmen axes. Tis is 75% a he new op or-dinary rae o 43.4% (39.6% income pls 3.8% sel-employmen axes) and 25% a he op capial gains rae o 23.8% (20%capial gains pls 3.8% sel-employmen ax on nearned income). under crren law, he ax rae wold be 23.8%.

har 2

$ M i l l i o n s o f D o l l a r s I n v e s t e d

160,000

140,000

120,000

100,000

80,000

60,000

40,000

20,000

0

-20,000

-40,000

1 9 8 0

1 9 8 2

1 9 8 4

1 9 8 6

1 9 8 8

1 9 9 0

1 9 9 2

1 9 9 4

1 9 9 6

1 9 9 8

2 0 0 0

2 0 0 2

2 0 0 4

2 0 0 6

2 0 0 8

2 0 1 0

Actual Investment

Predicted (Effective Tax Rate)

8/8/2019 Tax Impact Study 06-08-102

http://slidepdf.com/reader/full/tax-impact-study-06-08-102 7/15

Private Equity Council • June 2010 6

The Impact of H.R. 4213 on Private Equity Investment and Employment

6

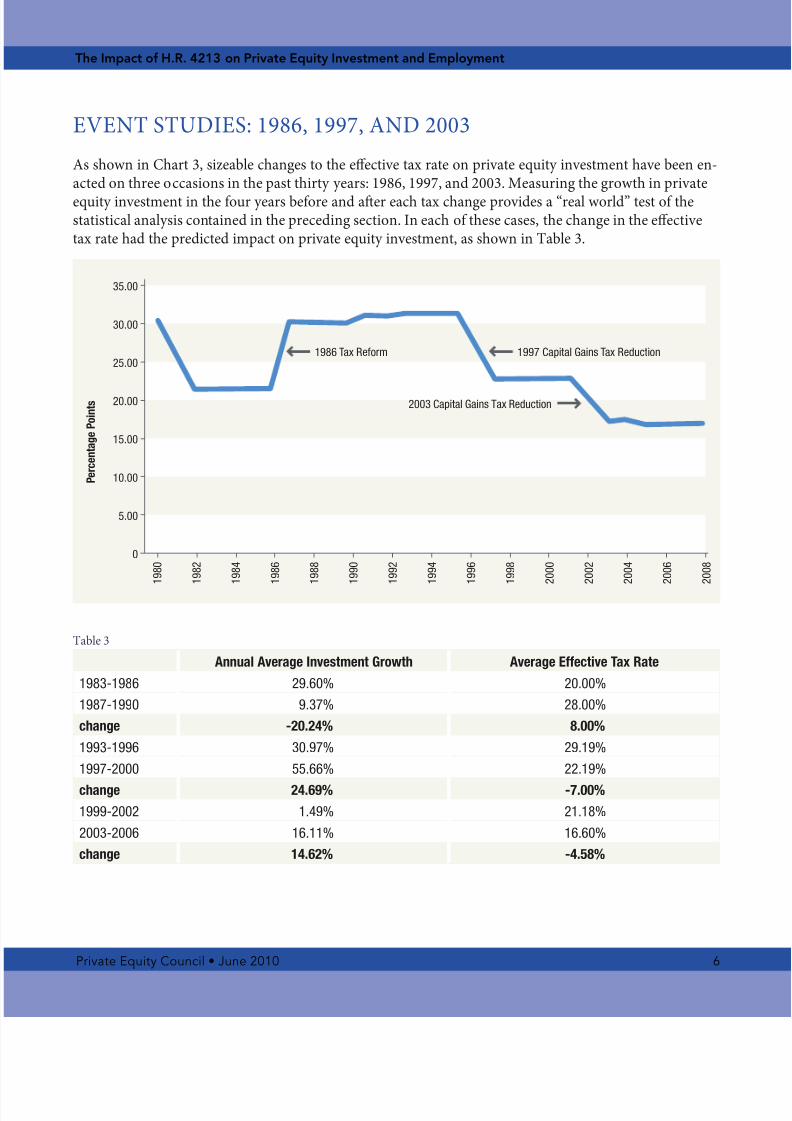

EVEt StuIES: 1986, 1997, A 2003 As shown in har 3, sizeable changes o he eecive ax rae on privae eqiy invesmen have been en-aced on hree occasions in he pas hiry years: 1986, 1997, and 2003. Measring he growh in privae

eqiy invesmen in he or years beore and aer each ax change provides a “real world” es o hesaisical analysis conained in he preceding secion. In each o hese cases, he change in he eeciveax rae had he prediced impac on privae eqiy invesmen, as shown in table 3.

table 3

Annual Average Investment Growth Average Effective Tax Rate

1983-1986 29.60% 20.00%

1987-1990 9.37% 28.00%

change -20.24% 8.00%

1993-1996 30.97% 29.19%

1997-2000 55.66% 22.19%

change 24.69% -7.00%

1999-2002 1.49% 21.18%

2003-2006 16.11% 16.60%

change 14.62% -4.58%

har 3: Eecive tax ae35.00

30.00

25.00

20.00

15.00

10.00

5.00

0

P e r c e n t a g e

P o i n t s

1 9 8 0

1 9 8 2

1 9 8 4

1 9 8 6

1 9 8 8

1 9 9 0

1 9 9 2

1 9 9 4

1 9 9 6

1 9 9 8

2 0 0 0

2 0 0 2

2 0 0 4

2 0 0 6

2 0 0 8

1986 Tax Reform 1997 Capital Gains Tax Reduction

2003 Capital Gains Tax Reduction

8/8/2019 Tax Impact Study 06-08-102

http://slidepdf.com/reader/full/tax-impact-study-06-08-102 8/15

Private Equity Council • June 2010 7

The Impact of H.R. 4213 on Private Equity Investment and Employment

7

In he 1986 tax eorm Ac, he saory ax rae on privae eqiy invesmen increased rom 20%o 28% or capial gains realized aer Janary 1, 1987. In he or years prior o he ax change, privaeeqiy invesmen increased a an annalized rae o 29.6%. Tis covers invesmen rom he end o (bno inclding) 1982 o he end o 1986. Following he 8 percenage poin increase, privae eqiy inves-

men grew in he ollowing or years a a 9.37% rae, a 20.24 percenage poin decline in he invesmengrowh rae.

From 1987 o 1997, he eecive ax rae on privae eqiy invesmen dried pward o 29.19% as a re-sl o sbseqen changes o he ax code relaing o exempions and sel-employmen axes. Te sao-ry capial gains rae was c o 20% in 1997. unlike in 1986, he c ook eec immediaely, which cases1997 o be inclded in he “aer” porion o he analysis. In he or years ending in 1996, privae eqiy invesmen grew a a 30.97% annalized rae. In he or years ollowing he 7 percenage poin redcionin he eecive ax rae, privae eqiy invesmen grew a a 55.66% annalized rae.

Finally, in 2003, ongress redced he saory long-erm capial gains rae by 5 percenage poins. As in1997, his c ook eec immediaely, which places 2003 in he “aer” porion o he analysis. In he oryears ending in 2002, privae eqiy invesmen grew a a 1.49% annalized rae. In he or years ollow-ing he nearly 5 percenage poin redcion in he eecive ax rae, privae eqiy invesmen grew a a16.11% annalized rae. Te changes in he or-year privae eqiy invesmen growh raes in each o hese periods provide srong sppor or he conclsions reached in he preceding secion concerning heimpac o ax raes on privae eqiy invesmen, holding oher acors consan.

8/8/2019 Tax Impact Study 06-08-102

http://slidepdf.com/reader/full/tax-impact-study-06-08-102 9/15

Private Equity Council • June 2010 8

The Impact of H.R. 4213 on Private Equity Investment and Employment

8

ISuSSI A LuSI

Tis paper provides evidence o sgges ha he ax increases o he magnide conained in H.. 4213wold resl in a sbsanial decline in privae eqiy invesmen and a nonrivial redcion in overall

employmen levels, holding oher acors consan. I is imporan o noe ha he parameers esimaedin Secion 2 are parial derivaives ha pariion he impac o eecive ax raes rom oher variables.Tis means ha he redcion in invesmen is net o he eec o oher acors. As discssed in Secion2, privae eqiy invesmen is likely o conine o grow as long as i conines o provide risk-adjsedrerns in excess o hose available hrogh alernaive invesmens. As sch, his analysis does no main-ain ha ha he ax increase will case privae eqiy invesmen o all on a gross or aggregae basis. Isimply demonsraes ha he daa sgges ha sch a large ax increase will almos cerainly case privaeeqiy invesmen o all relaive o wha i oherwise wold have been.

Some dispe he noion ha a ax increase on privae eqiy frms wold redce invesmen. Tese analyss

noe ha he blk o privae eqiy capial is provided by limied parners whose axes wold no be impac-ed by H.. 4213. Tereore, he ax increase wold have no impac on heir savings and invesmen deci-sions. Tis analysis overlooks wo acors. Firs, he blk o capial o privae eqiy nds has always beenprovided by ax-exemp eniies. As a resl, his analysis already accons or he disparae impac o heax change. According o Preqin, roghly 68% o global privae eqiy capial is invesed by pblic pensionnds, privae pension nds, endowmens, and governmenal eniies ha are exemp rom u.S. axaion.As explained by GA, mch o he growh o privae eqiy capial over he years has come rom hese ax-insensiive paries. Tereore, he change in he eecive ax rae conained in H.. 4213 is no dieren romprevios siaions in ha he impac will be borne direcly by he privae eqiy frms ha serve as generalparners o privae eqiy nds, no he largely ax-exemp limied parners ha inves in hese nds.

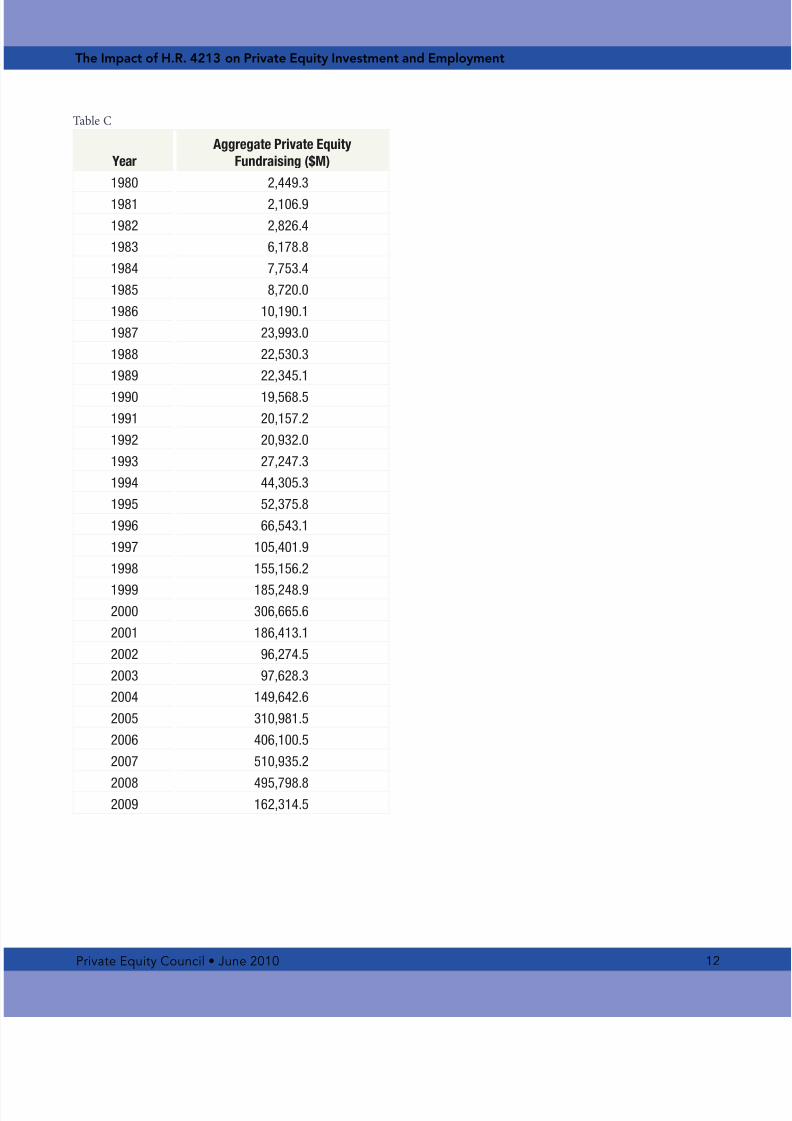

Secondly, his analysis wrongly presmes ha he spply o privae eqiy invesmen opporniies isinelasic wih respec o he ax rae. Tis is nlikely o be he case. Te privae eqiy frm’s willingnesso ideniy aracive invesmen opporniies and inves he ime and eor reqired o creae vale islikely o be especially sensiive o eecive ax raes. table 4 shows he resls o an LS esimaion o eqaion (1) wih oal privae eqiy ndraising as he dependen variable (privae eqiy ndraisingdaa is available as table in he Appendix). Te daa reveal ha a one percenage poin increase in heeecive ax rae redces aggregae privae eqiy ndraising by $9.197 billion. Tese resls are saisi-cally signifcan a he 98% confdence inerval.

table 4

Parameter Estimate t Stat P-value

Intercept 164570.16 1.5730991 12.73%

Effective Tax Rate -9197.485 -2.534 0.017

Time Trend 10485.03 5.023346 0.00%

R-squared 0.699

AR(1) 0.394

8/8/2019 Tax Impact Study 06-08-102

http://slidepdf.com/reader/full/tax-impact-study-06-08-102 10/15

Private Equity Council • June 2010 9

The Impact of H.R. 4213 on Private Equity Investment and Employment

9

Tis provides some insigh as o he likely channel o he ax increase: higher axes redce he aer-ax rern associaed wih privae eqiy invesmen; his makes marginal invesmens (i.e. oen hoseposing he highes risk) less aracive becase he privae eqiy frm reains ar less o he “pside”aer axes, b sill ms absorb all o he downside in erms o capial conribed and he considerable

coss associaed wih he invesmen process and sbseqen monioring and oversigh. Te noion haax raes on enreprenerial parners can be increased by 157% wiho negaive economic conseqencesis misaken and conrary o he daa. Privae eqiy frms provide he invesmen opporniies o heircapial parners and large increases in heir eecive ax raes will direcly impac he availabiliy o schinvesmen opporniies.

8/8/2019 Tax Impact Study 06-08-102

http://slidepdf.com/reader/full/tax-impact-study-06-08-102 11/15

Private Equity Council • June 2010 10

The Impact of H.R. 4213 on Private Equity Investment and Employment

10

EFEEES

raig, Valenine V., “Merchan Banking Pas and Presen,” FDIC Banking Review, Fall 2001.

Feldsein, Marin, “apial taxaion,” aional Brea or Economic esearch Working Paper o. 817.April 1982.

Frisch, ., and F. V. Wagh. “Parial ime regression as compared wih individal rends.” Econometrica 1,cober 2007.

Li, i-kang, George M . Jabbor , and ichard K . Green, “Te Perormance o pion-Based ealisk Models on ommercial Morgages an Empirical Invesigaion,” Journal of Fixed Income, Fall 2007.

Preqin 2010 Global updae.

omer, hrisina and Jared Bernsein, “Te Job Impac o he American ecovery and einvesmenPlan,” ce o Presidenial transiion, Janary 10, 2009.

Tomson eers, ne Banker Privae Eqiy aabase.

u.S. treasry, apial Gains and taxes Paid on apial Gains or erns wih Posiive e apial Gains,1954-2007.

8/8/2019 Tax Impact Study 06-08-102

http://slidepdf.com/reader/full/tax-impact-study-06-08-102 12/15

Private Equity Council • June 2010 11

The Impact of H.R. 4213 on Private Equity Investment and Employment

11

APPEIX

table A

Year U.S. Private Equity Investment ($M)

1980 723.39

1981 1,590.07

1982 1,997.69

1983 3,675.01

1984 4,195.25

1985 3,956.08

1986 5,636.45

1987 8,217.50

1988 8,988.45

1989 11,266.20

1990 8,064.34

1991 4,658.84

1992 7,982.26

1993 6,800.99

1994 8,352.46

1995 13,470.03

1996 23,486.93

1997 26,863.011998 42,152.66

1999 84,089.54

2000 137,895.97

2001 57,261.60

2002 44,719.57

2003 60,847.99

2004 54,161.94

2005 57,836.76

2006 81,280.412007 95,235.72

2008 90,514.89

2009 49,078.08

table B

Year

Effective Tax Rate

on Private Equity Investment

1980 28.0

1981 24.0

1982 20.0

1983 20.0

1984 20.0

1985 20.0

1986 20.0

1987 28.0

1988 28.0

1989 28.0

1990 28.0

1991 28.9

1992 28.9

1993 29.2

1994 29.2

1995 29.2

1996 29.2

1997 25.21998 21.2

1999 21.2

2000 21.2

2001 21.2

2002 21.2

2003 18.6

2004 16.1

2005 16.1

2006 15.72007 15.7

2008 15.7

2009 15.7

8/8/2019 Tax Impact Study 06-08-102

http://slidepdf.com/reader/full/tax-impact-study-06-08-102 13/15

Private Equity Council • June 2010 12

The Impact of H.R. 4213 on Private Equity Investment and Employment

12

table

YearAggregate Private Equity

Fundraising ($M)

1980 2,449.3

1981 2,106.9

1982 2,826.4

1983 6,178.8

1984 7,753.4

1985 8,720.0

1986 10,190.1

1987 23,993.0

1988 22,530.3

1989 22,345.1

1990 19,568.5

1991 20,157.2

1992 20,932.0

1993 27,247.3

1994 44,305.3

1995 52,375.8

1996 66,543.1

1997 105,401.9

1998 155,156.2

1999 185,248.9

2000 306,665.6

2001 186,413.1

2002 96,274.5

2003 97,628.3

2004 149,642.6

2005 310,981.5

2006 406,100.5

2007 510,935.2

2008 495,798.82009 162,314.5

8/8/2019 Tax Impact Study 06-08-102

http://slidepdf.com/reader/full/tax-impact-study-06-08-102 14/15

Private Equity Council • June 2010 13

The Impact of H.R. 4213 on Private Equity Investment and Employment

13

StAtIStIAL APPEIX

the presence o aocorrelaed residals wold case he errors esimaed in eqaion (1) o bendersaed, which cold inae he raio and case he saisical signifcance o he parameer o

be oversaed. However, analysis o he residals sggess ha aocorrelaion is no presen. har Aprovides an aocorrelaion plo o he errors. Te amiliar paern o a slow decay exhibied by a serieswih persisen posiive aocorrelaion is no presen, as he aocorrelaion is already negaive by hesecond lag. More signifcanly, sing a criical vale o Z = 2, we canno rejec he hypohesis ha heresidals are a whie noise process nder Barle’s es o aocorrelaion. Te raio or he parameer o ineres enjoys a srong presmpion o saisical validiy.

0.4

0.3

0.2

0.1

0

-0.1

-0.2

-0.3

-0.4

P e r c e n t a g e

P o i n t s

Lag

1 2 3 4 5 6 7 8 9 10

8/8/2019 Tax Impact Study 06-08-102

http://slidepdf.com/reader/full/tax-impact-study-06-08-102 15/15

Private Equity Council • June 2010 14

The Impact of H.R. 4213 on Private Equity Investment and Employment

14

ABut tHE AutH

Jason M. Tomas, CFA

Jason Tomas serves as Vice Presiden o esearch a he Privae Eqiy oncil. Beore joining he PE,

Tomas served on he Whie Hose sa as Special Assisan o he Presiden or Economic Policy andirecor or Policy evelopmen a he aional Economic oncil. In hose capaciies, Tomas aced ashe E’s chie economic analys and he primary adviser o he Presiden or pblic fnance and servedas Whie Hose liaison o he Presiden’s Working Grop on Financial Markes.

Prior o working a he Whie Hose, Tomas spen nearly or years on he sa o Senaor Jon Kyl o Arizona, where he was he economic policy analys or he Senae epblican Policy ommiee. Tomasearned his bachelor’s degree in economics and governmen rom laremon McKenna ollege, his Mas-er o Science degree rom George Washingon universiy, and is a crrenly a docoral ellow a GeorgeWashingon’s Finance eparmen. Tomas is a FA charerholder.