tax & estate planning for snowbirds - cifps · pdf filetax & estate planning for...

TRANSCRIPT

Tax & Estate Planning for Snowbirds

Amin Mawani Schulich School of Business York University

Taxes do influence behaviour

Windowless CastlesNarrow frontagesSIN & gasoline taxesRRSP contributions

Taxes Matter

How much dependency deduction and child credit do you get for a kid born on December 31st?– “Taxes and the Timing of Births” by

Dickert-Conlin and Chandra. Journal of Political Economy, 1999.

Taxes and the Timing of Births

12/31• Holiday effects• High income vs. low income

Taxes and the Timing of…Death?

Estate tax rates have varied across the past century– “Dying to Save Taxes: Evidence from

Estate-Tax Returns on the Death Elasticity”by Slemrod and Kopczuk. Review of Economics and Statistics May 2003.

Dying to Save Taxes

High tax Low tax

Low tax High tax

Changing Estate & Gift Tax Rates

Year Max Estate Max Gift Tax Rate Tax Rate

2008 45% 45%2009 45% 45%2010 0% 35%2011 55% 55%

And Changing thresholds

Year Estate Transfer Lifetime Gift Exempt Amount Exempt Amount

2008 $2 million $1 million2009 $3.5 million $1 million2010 tax repealed $1 million2011 $1 million $1 million

Outline: US Income Tax Issues

– US residency requirements for taxation– Substantial Presence Test (SPT)– Exemption from Substantial Presence Test – Earning US Rental Income – Individual Taxpayer Identification Number

(ITIN)

US Estate Planning

Increasingly important to your clients– Strengthening Canadian $– Declining US house prices– More Canadians purchasing recreational

property in the U.S.– Need to be aware of U.S. estate tax

exposure before directly investing in US real estate

Basis of US Taxation

US residents (for tax purposes) & citizens taxed on their worldwide income by the US– Double tax relief with Foreign Tax Credits (FTC)

Nonresident aliens taxed only on US source income– Passive income subject to withholding tax on

gross income– Capital gains not taxed except for Capital Gains

on US real property interests

Required to File US Personal Tax Return if:

US CitizenGreen card HolderTrigger Substantial Presence test (SPT)– Spend lots of time (e.g., 4 months) in the

U.S. every year

Substantial Presence Test (SPT)

Substantial Presence Test (SPT)triggered in 2008 if

Spend > 31 days in the US in 2008 and# of days spent in US in 2008

+ 1/3 # of days spent in US in 2007+ 1/6 # of days spent in US in 2006≥ 183 days

Spending 4 months (≈ 122 days) in the US each year for 3 consecutive years triggers SPT ⇒ making the snowbird a resident alien in the US for tax purposes

⇒ requiring reporting of worldwide income to IRS

Counting the # of days in the US

Canadians may soon be subject to an automated entry / exit system at the Canadian–US border that automatically tracks the exact # of days spent in US– Canadians currently exempt from using

this system

Nonresident alien

If the total # of days in the US over the immediate past 3 years ≤ 182, the snowbird is deemed to be a nonresident alien for US income tax purposesDays spent in US while seeking medical treatment for condition arising in the US are counted as non-US days for SPT

Escaping SPT

Filing IRS Form 8840 – “Closer Connection Exception Statement for Aliens” – by June 15th of the year following the SPT triggerClaiming exemption under the Canada-US Tax Treaty Closer Connection Exception is easier

Shorter visit to the US every 3rd year

IRS Form 8840 needs to be filed annually if you meet the SPTIf in one of the 3 years you are not in the US long enough to achieve a 3-year average of > 122 days, then the SPT count effectively starts over again

⇒ Filing requirement for Form 8840 may end up being deferred for a few years

Closer Connection Exception

Claim that you have a closer connection to Canada than to the US, and therefore deserve to be treated as a non-resident for tax purposes (in IRS Form 8840)Claim determined by (1) location of family home; (2) family; (3) personal belonging; (4) social, political, cultural & religious ties; (5) business activities

Escaping SPT via the Tax Treaty

A snowbird could be considered resident of both Canada and the US for tax purposesCanada-US Income Tax Convention allows choice under Article IV(2) based on: (1) location of permanent home; (2) centre of vital interests (where are economic and personal relations closer?); (3) habitual abode; (4) citizenship; and (5) competent authority

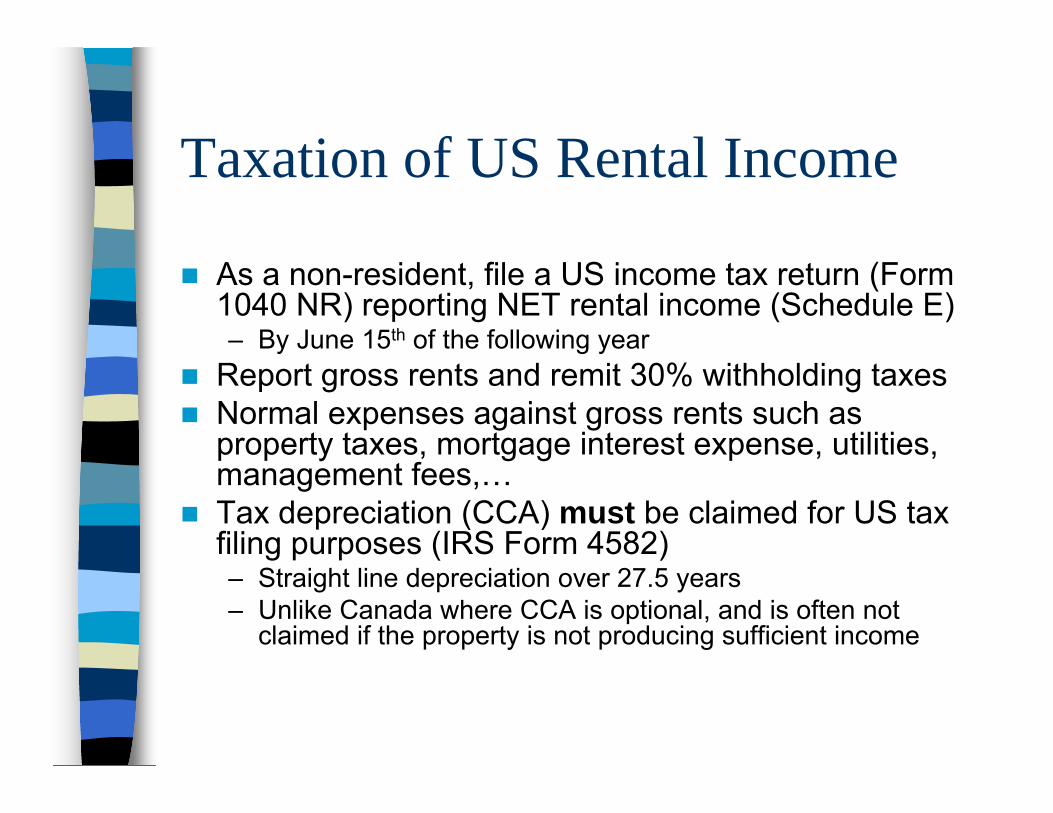

Taxation of US Rental Income

As a non-resident, file a US income tax return (Form 1040 NR) reporting NET rental income (Schedule E)– By June 15th of the following year

Report gross rents and remit 30% withholding taxesNormal expenses against gross rents such as property taxes, mortgage interest expense, utilities, management fees,…Tax depreciation (CCA) must be claimed for US tax filing purposes (IRS Form 4582)– Straight line depreciation over 27.5 years – Unlike Canada where CCA is optional, and is often not

claimed if the property is not producing sufficient income

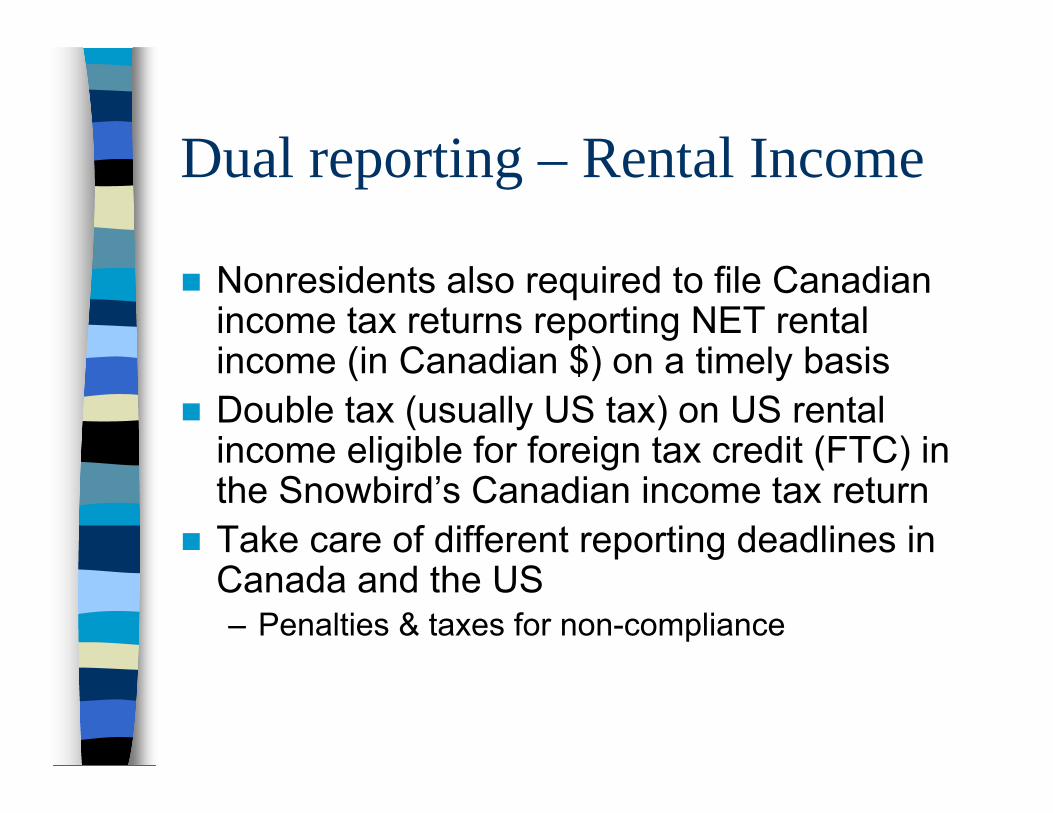

Dual reporting – Rental Income

Nonresidents also required to file Canadian income tax returns reporting NET rental income (in Canadian $) on a timely basisDouble tax (usually US tax) on US rental income eligible for foreign tax credit (FTC) in the Snowbird’s Canadian income tax returnTake care of different reporting deadlines in Canada and the US– Penalties & taxes for non-compliance

Tax Compliance Issues - ITIN

Non-resident aliens need a US Individual Taxpayer Identification Number (ITIN) for tax reporting (Not the same as U.S. SIN)ITIN obtained by IRS Form W-7 & necessary for– escaping SPT (IRS Form 8840) – reporting US rental income (IRS Form 1040NR) – reporting US capital gains on sale of real property– for recovering withholding taxes (Form 1040NR)

Outline: US Estate Planning

What assets are subject to estate tax?Timing & Base of estate taxUnderstand the threshold exemptionsHow the estate tax is computed?How the estate tax credit is computed?Estate Planning Strategies

Assets subject to US Estate Taxes

Real estate in the USShares of US corporations; US T-billsMutual fundsGold, jewelry, artAnnuity contracts payable by US corpCanadian pooled funds investing in US securities

Assets not subject to estate taxes

Cash in US banks not used in businessCash in Canadian branch of US banksLife insurance proceeds of a non-resident alienUS government bonds > one yearCanadian mutual funds in US $ that invest directly in US securities

Timing & Base of Estate Tax

Upon transfer of a deceased person’s US taxable estate

Base = gross fair market value of assets located (or deemed to be located) in US and owned at the time of an individual’s death

Estate tax credits & exemptions

US residents & citizens entitled to a unified credit of $780,800 (in 2008), which exempts $2 million of property from estate taxesUS$3.5 million exempted by 2009Unlimited amount exempted by 2010US$1 million exempted by 2011

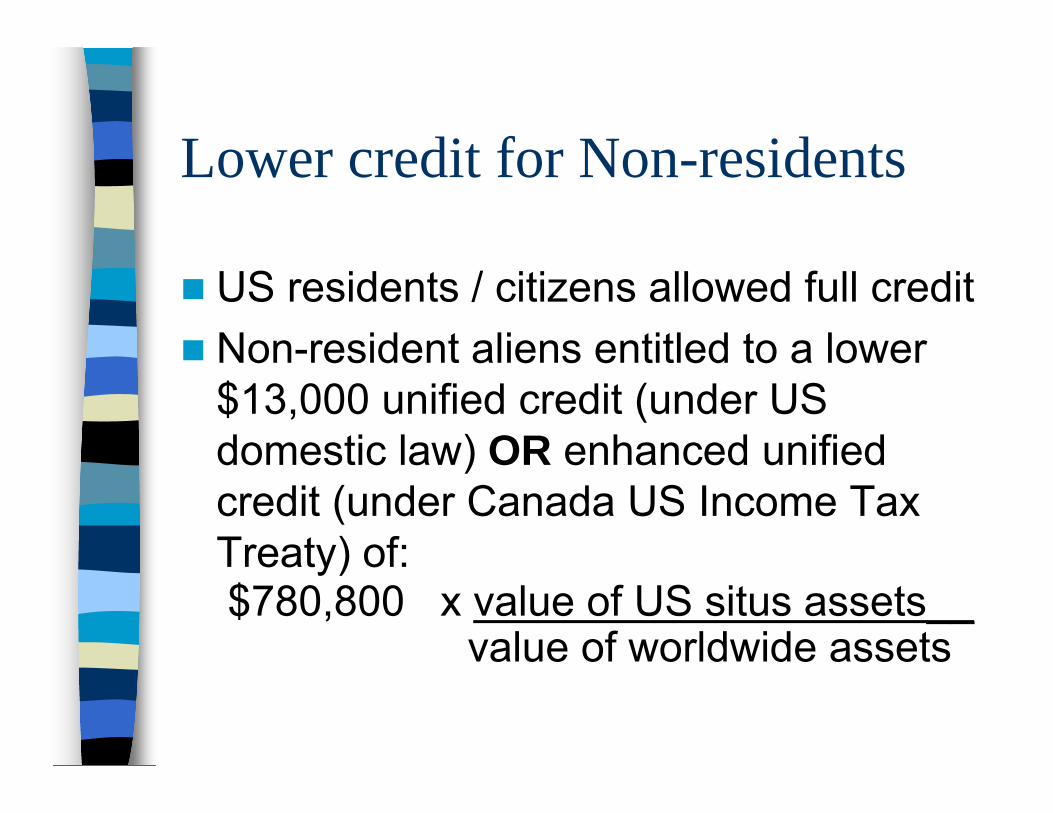

Lower credit for Non-residents

US residents / citizens allowed full creditNon-resident aliens entitled to a lower $13,000 unified credit (under US domestic law) OR enhanced unified credit (under Canada US Income Tax Treaty) of:$780,800 x value of US situs assets__

value of worldwide assets

Estate tax rate schedule - 2008

taxable estate then plus of excess> ≤ tax =(A) (B) over (C)

100,000 150,000 23,800 30% 100,000150,000 250,000 38,800 32% 150,000250,000 500,000 70,800 34% 250,000500,000 750,000 155,800 37% 500,000750,000 1,000,000 248,300 39% 750,0001,000,000 1,250,000 345,800 41% 1,000,0001,250,000 1,500,000 448,300 43% 1,250,0001,500,000 and over 555,800 45% 1,500,000

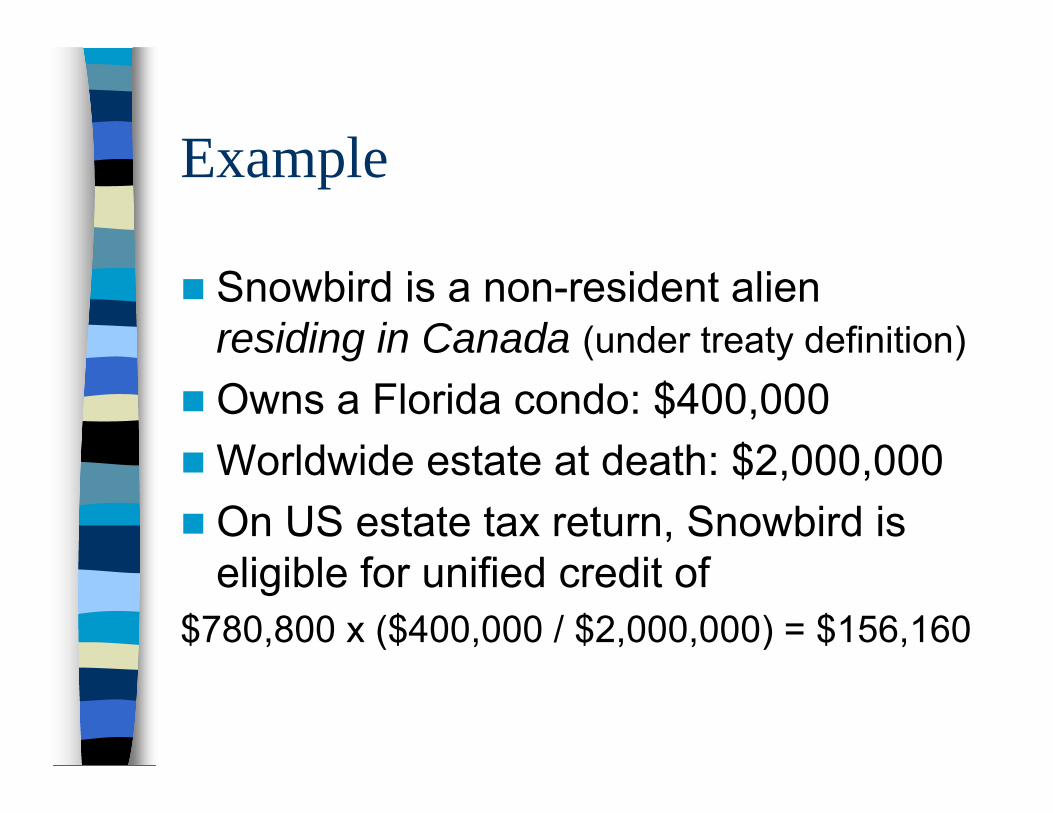

Example

Snowbird is a non-resident alien residing in Canada (under treaty definition)Owns a Florida condo: $400,000Worldwide estate at death: $2,000,000On US estate tax return, Snowbird is eligible for unified credit of

$780,800 x ($400,000 / $2,000,000) = $156,160

Example - continued

Gross estate tax on condo with fair market value of $400,000 at time of death = $121,800 (from rate schedule)$121,800=$70,800 + 34%(400,000–250,000)Unified tax credit > Gross estate tax, OR $156,160 > $121,800∴ Snowbird will not pay any estate tax

Canadian residency emphasized

Numerical example applies to Canadian residents (as determined under the Tax Treaty residency rules)If Snowbird had died while being a non-resident of Canada (for income tax purposes), she would be limited to the $13,000 unified creditNon-residents of Canada do not qualify for the enhanced unified credit under the Treaty

Additional credits against US estate taxes

Marital credit – if snowbird transfers US property at death to Canadian spouseFeature of the Canada – US Tax TreatyEffectively doubles the available creditNeed to make an election on estate tax return (IRS Form 706-NA)Unlimited marital deduction for gifts & bequests made to US citizen spouses

Canadian Foreign Tax Credit (FTC)

Canada allows a tax credit for US estate taxes paidCredit limited to related Canadian tax on the capital gains from property in the same yearUS estate tax based on gross valueWhile Canadian tax based on capital gainsIf value of property is large relative to accrued gain, then FTC offers only limited reliefU.S. & Canadian tax need to be triggered in same year for FTC to be applied

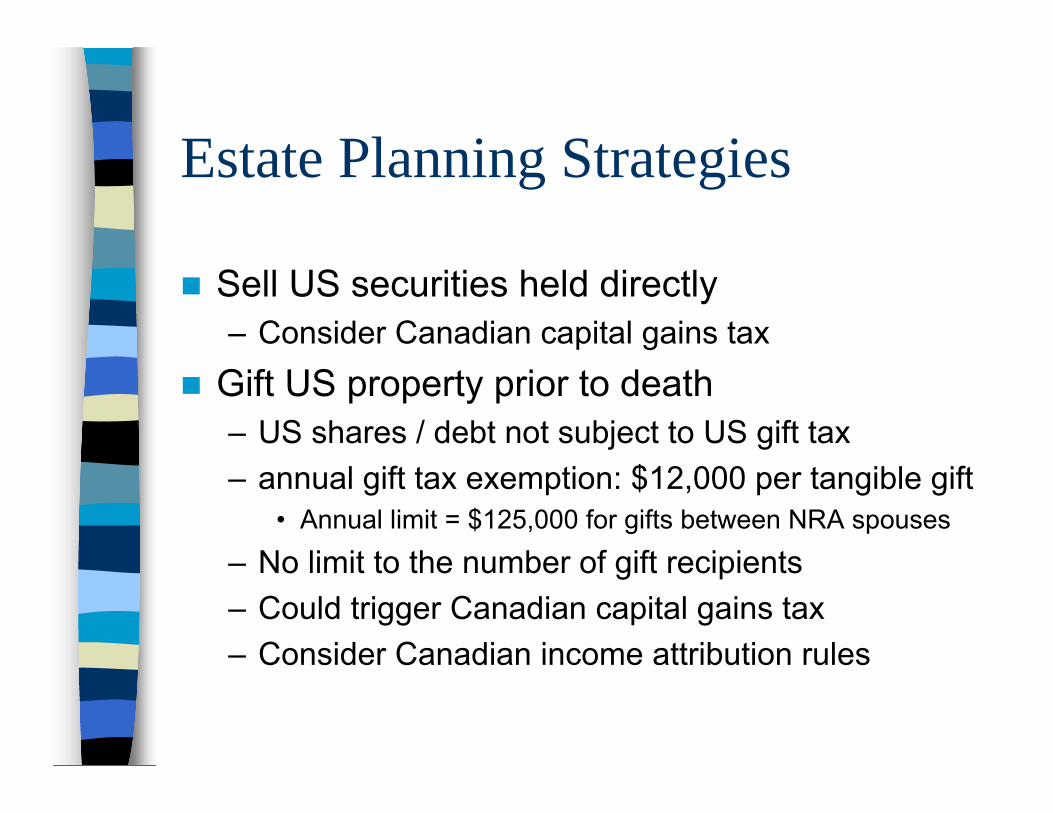

Estate Planning Strategies

Sell US securities held directly– Consider Canadian capital gains tax

Gift US property prior to death– US shares / debt not subject to US gift tax– annual gift tax exemption: $12,000 per tangible gift

• Annual limit = $125,000 for gifts between NRA spouses

– No limit to the number of gift recipients– Could trigger Canadian capital gains tax– Consider Canadian income attribution rules

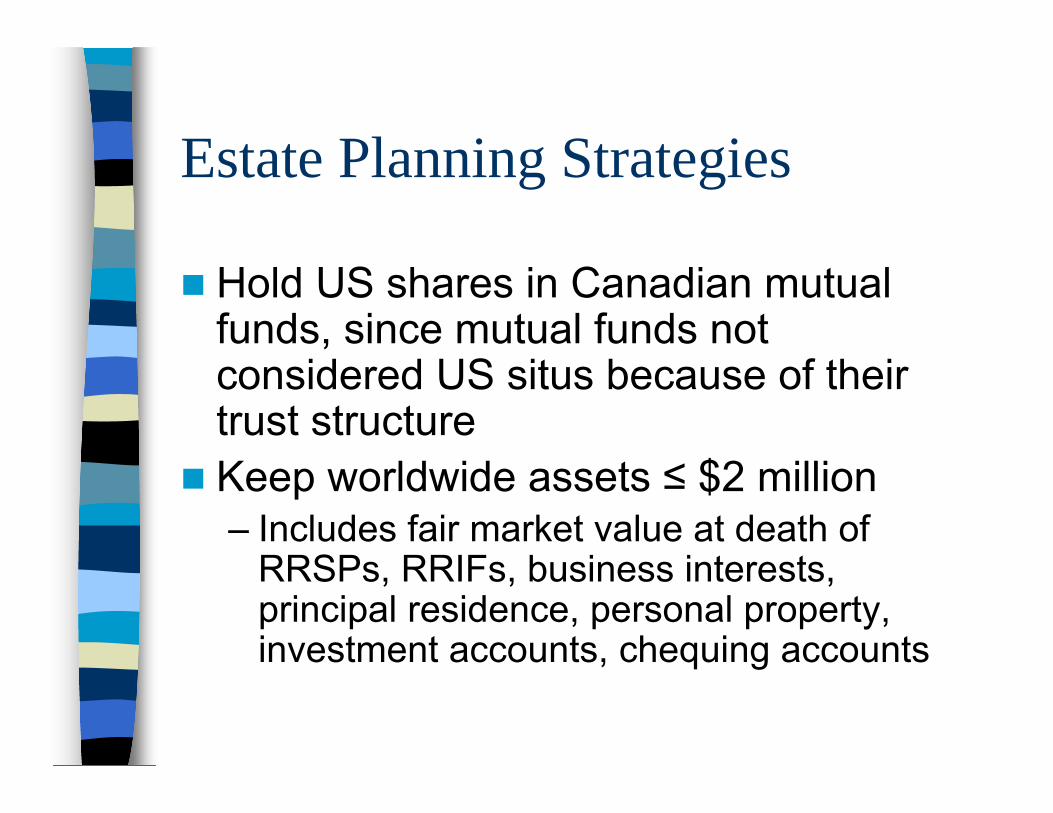

Estate Planning Strategies

Hold US shares in Canadian mutual funds, since mutual funds not considered US situs because of their trust structureKeep worldwide assets ≤ $2 million– Includes fair market value at death of

RRSPs, RRIFs, business interests, principal residence, personal property, investment accounts, chequing accounts

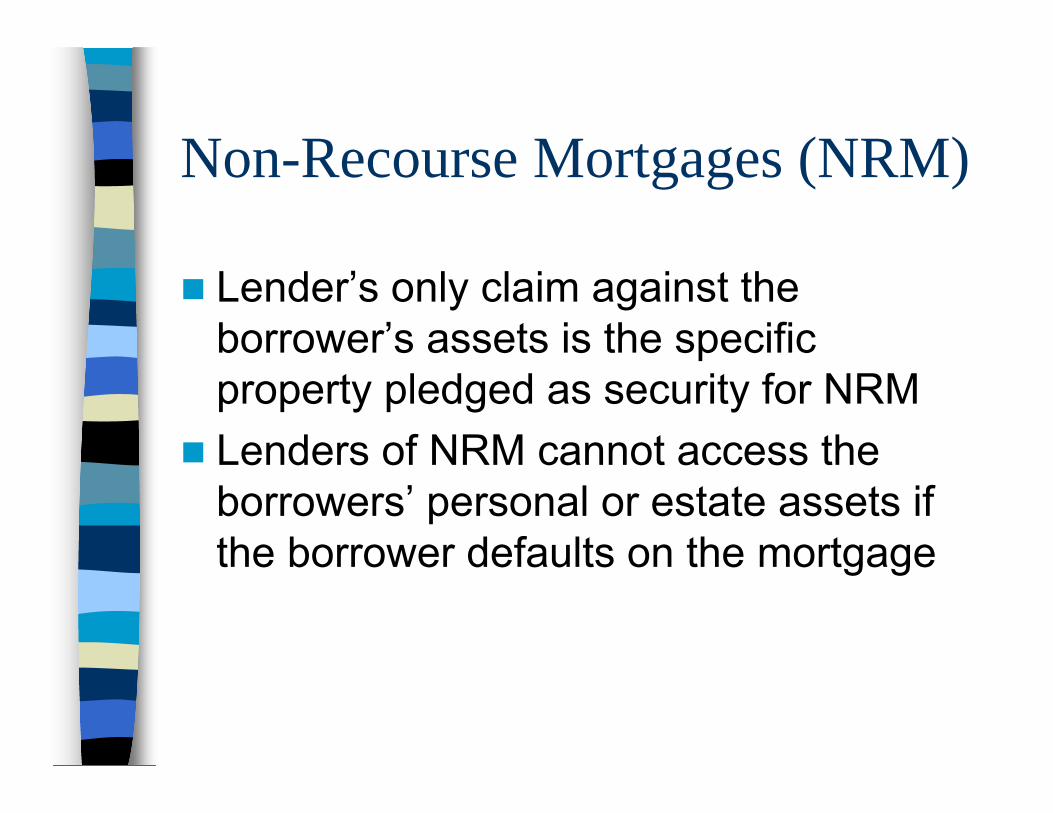

Non-Recourse Mortgages (NRM)

Lender’s only claim against the borrower’s assets is the specific property pledged as security for NRMLenders of NRM cannot access the borrowers’ personal or estate assets if the borrower defaults on the mortgage

Non Recourse Mortgage (NRM)

Unlike a conventional mortgage, a Non Recourse Mortgage (NRM) reduces the net value of the US real estate subject to US estate taxIn contrast, a conventional mortgage reduces net assets subject to US estate taxes by the fraction:

US Assets / Worldwide Assets

NRM ExampleConventional Non Recourse Mortgage Mortgage

Value of US Real Estate $500,000 $500,000

Value of Worldwide Estate $5,000,000 $5,000,000

Mortgage $300,000 $300,000

US Real Estate $500,000 $500,000Less: Mortgage -10%*(300,000) -100% ($300,000)

Estate subject toUS estate taxes $470,000 $200,000

10% = $500,000 / $5,000,000

Conventional vs. NRM

Since US assets = 10% of worldwide assets (=$500,000 / $5,000,000), then only 10% of the conventional mortgage (or $30,000) can be netted from value of US real estate (for estate tax purposes)In the case of a NRM, the entire $300,000 mortgage can be netted from value of US real estate

Refinance US real estate with NRM

Exchange conventional mortgage with Non Recourse Mortgage– Subject to risk tolerance, keep financing

high to reduce value subject to estate taxNRM is tax-deductible (for Canadian tax purposes) if used to purchase income generating investments outside RRSPs – This may ↑ portfolio risk if more equities

Non Recourse Mortgage (NRM)

Appropriate for High Net Worth ClientsBanks will not lend >60% of prop. value Now offered by Canadian BanksAppropriate only for Canadian residents owning real property in the USNeeds to be at arm’s lengthStrategy does not apply to US citizens

Corporate owned real estateNo US estate taxes on the death of the shareholderHowever, CRA assesses a taxable benefit on the shareholder of a single purpose corporation -ITA 15(1) (since 2004)∴ corporate owned real estate not practical

Can use Canadian partnership to purchase US property, with the partnership electing to be treated as a corporation for US estate tax purposes (“check-the-box” election)and treated as a partnership for Canadian tax Shareholder benefit issues avoided

Partnership ElectionSnowbird considered to own shares of Canco upon death, & not US real estateDrawback: (long-term) capital gains tax rate on disposition of property is higher for corporations (35%) than for individuals (15%)Drawback eliminated if election delayed until after death and property sold before death, since property deemed to be sold by a partnership (while snowbird alive) Needs complex post-mortem planning to avoid double taxation

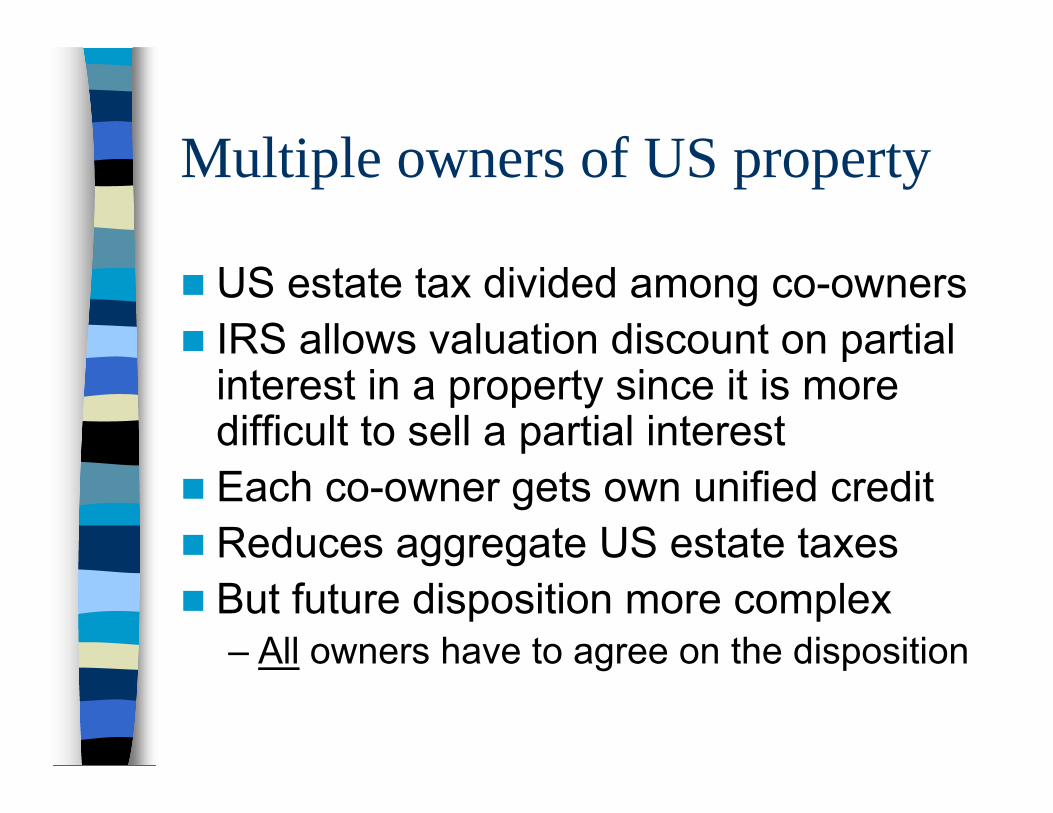

Multiple owners of US property

US estate tax divided among co-ownersIRS allows valuation discount on partial interest in a property since it is more difficult to sell a partial interestEach co-owner gets own unified creditReduces aggregate US estate taxesBut future disposition more complex– All owners have to agree on the disposition

Canadian Personal TrustSnowbird (settlor) can settle the trust with sufficient funds to purchase US propertySpouse / children are named beneficiariesSnowbird is neither beneficiary nor a trustee– Necessary to avoid IRC §2036 on attribution

Snowbird funds annual operating costsLife interest for spouse & capital interest for spouse & children⇒ value of the trust property is not part of the Snowbird’s estateCaveat: 21-year deemed disposition rule

Life insurance to fund US estate taxOften not feasible for elderly snowbirds or those with serious medical conditionsInsurance policy premiums to fund US estate tax liability not deductible for tax purposesInsurance proceeds on life of a non-resident, non-citizen not considered US situs property and therefore not subject to estate taxHowever, insurance proceeds reduce unified credit since insurance proceeds (payable to the estate) included in gross value of deceased’s worldwide estate (“denominator”)

Questions?

Comments?