tax deducted at source presented by: sowmya “pay as you earn”

TRANSCRIPT

TAX DEDUCTED AT SOURCE

Presented By: Sowmya

“PAY AS YOU EARN”

Why – Tax Deducted At Source ?

What is Tax Deducted At Source ?

TDS

Relevant Sections

Sec 192 – Salary Sec 193 – Interest on Securities Sec 194 – Dividends Sec 194A – Interest other than Interest on Securities Sec 194B – Winnings from Lotteries, Crosswords,

Puzzles etc. Sec 194BB– Winnings from Horse race

Sec 194C – Payment to Resident Contractors Sec 194D – Insurance commission Sec 194E – Payment to Non Resident Sportsmen

or Sports Association Sec 194EE – Payments in respect of Deposit under

National Savings Scheme Sec 194G – Commission on sale of Lottery Tickets

Relevant Sections

Sec 194H – Commission and Brokerage Sec 194I – Rent Sec 194J – Fees for Professional or Technical

Services Sec 194K – Income in respect of units Sec 194LA –Payment of Compensation on

acquisition of certain immovable

property

Relevant Sections

Section 194 LB ( w.e.f 01.06.2011 )

Income by way of Interest from

INFRASTRUCTURE DEBT FUND

Insertion 2011

Person responsible to deduct tax- Employer Tax to be deducted at rate applicable to

individuals. Inclusion of income from other heads Payment of tax on Non Monetary Perquisites. Salary from more than one employer. Adjustment of amount deducted U/s192.

Sec 192 – Salary

Case Law: CIT Vs Venron Expat Services INC. (2010)

The assesse failed to deduct tax monthly, however deducted towards the end of FY.

Sec 192 – Salary

Judgment: Permits adjustment of excess or deficit. No Interest U/s 201(1A).

Sec 193 - Interest on Securities

Person responsible to deduct tax – Central or state govt.Local authority.Company or corporation established by govt.

Rate of tax - 10%.

Exemptions:• Debentures (Resident Individuals)

Paid by Account Payee Cheque of amount not exceeding Rs 2,500

List of interest payments- No TDS required Interest on Listed Securities Payment to New Pension Trust National Defence Bonds National Defence Loan National Development Bond 7-year NSC Gold Bonds LIC, GIC or any of its subsidiaries

Sec 193 - Interest on Securities

Sec 194 – Dividends

Person Liable to deduct tax is the principal officer.

Rate of tax - 10%. Applicable only if dividend is paid u/s 2(22)(e).

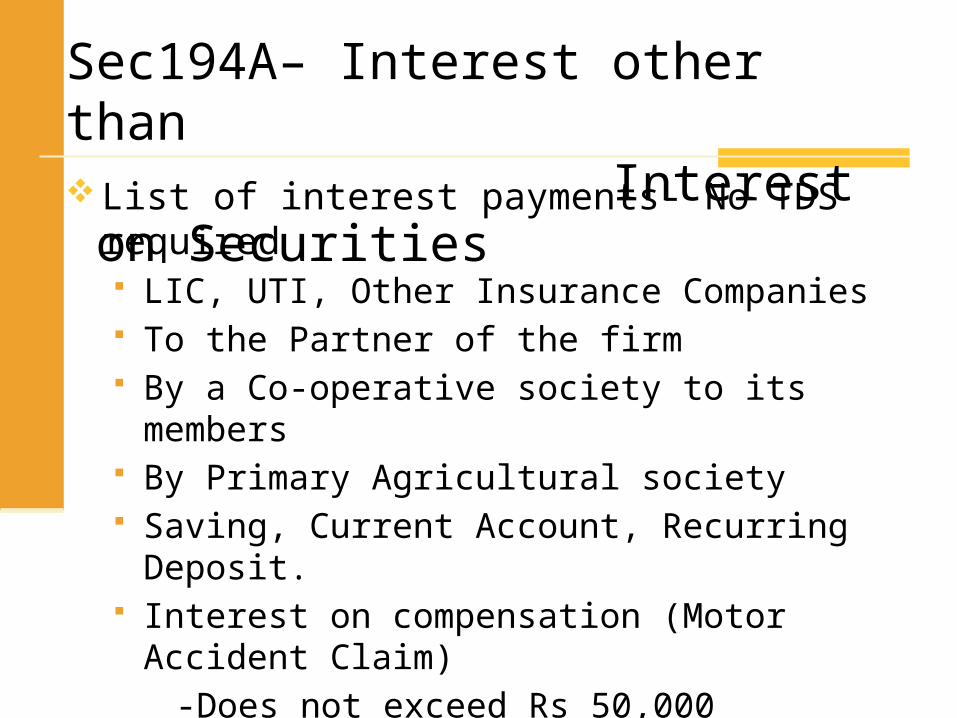

Sec194A– Interest other than Interest on Securities Rate of tax – 10% Exemption Limit –

Interest by Banking company - Rs 10,000

Others - Rs 5,000 Credit or Payment, whichever is earlier.

Sec194A– Interest other than Interest on SecuritiesList of interest payments- No TDS required

LIC, UTI, Other Insurance Companies To the Partner of the firm By a Co-operative society to its members By Primary Agricultural society Saving, Current Account, Recurring Deposit. Interest on compensation (Motor Accident Claim)

-Does not exceed Rs 50,000 Interest on Zero Coupon Bond.

Sec 194B- Winnings from Lotteries, Crosswords, Puzzles etc. Deductor – Any person paying the sum by way

of winning Rate of tax – 30% At the time of payment Exemption limit –

Upto 30.06.10 - Rs 5,000

From 01.07.10 - Rs 10,000

H. Anraj Vs Government of TamilnaduEssential elements that constitute lottery.

A prize or some advantage in the nature of prize, Distribution thereof by chance and Consideration paid or promised for purchasing

the chance.

Sec 194B- Winnings from Lotteries, Crosswords, Puzzles etc.

Case Law: ACIT Vs Director of State Lotteries, Assam.

Income accruing to an agent/trader in respect of prizes on unsold/unclaimed lottery tickets in his possession.

Judgment: Income From Business, not winning from

lottery. Hence not subject to TDS.

Sec 194B- Winnings from Lotteries, Crosswords, Puzzles etc.

Sec 194BB– Winnings from Horse race Deductor – Licensed by the govt. or licensed

bookmaker Rate of tax – 30% At the time of payment Exemption limit –

Upto 30.06.10 - Rs 2,500

From 01.07.10 - Rs 5,000

Case Law:Royal Calcutta Turf ClubLimit u/s 194BB is applicable for each payment or entire winning for the FY?

Judgment:Limit should be applied to each payment and not the entire winnings.

Sec 194BB– Winnings from Horse race

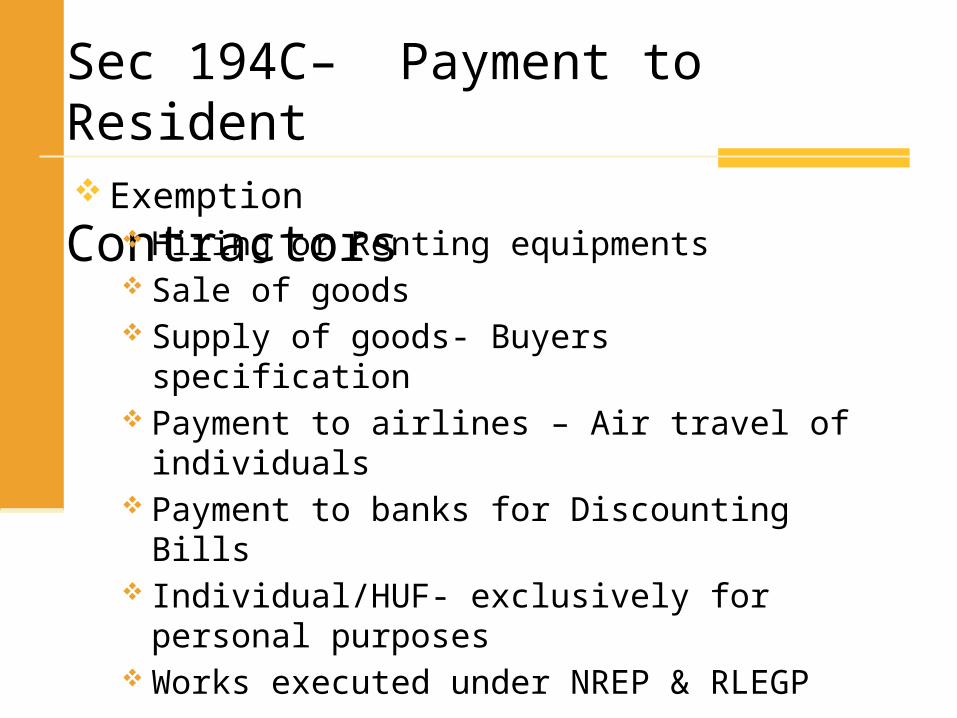

Sec 194C– Payment to Resident

Contractors Rate of Tax –

Individuals and HUFs - 1%

Others - 2%

Exemption Limit-

Upto 30.06.10- Rs 20,000/50,000

From 01.07.10- Rs 30,000/75,000

Sec 194C– Payment to Resident

Contractors Exemption Hiring or Renting equipments Sale of goods Supply of goods- Buyers specification Payment to airlines – Air travel of individuals Payment to banks for Discounting Bills Individual/HUF- exclusively for personal

purposes Works executed under NREP & RLEGP

Case law: Mukta Arts Vs ACIT (2010)

Assessee was engaged in Film Financing and made certain payments by way of advances to another party for production of film.

Judgment: Assessee was not acting as contractor nor the

other party a contractee

Assessee was not required to deduct tax.

Sec 194C– Payment to Resident Contractors

Sec 194D – Insurance commission

Person responsible to deduct tax- Insurance companies.

Rate of tax – 10% Credit or Payment, whichever is earlier. Exemption limit –

Upto 30.06.10 - Rs 5,000

From 01.07.10 - Rs 20,000

Sec 194E– Payment to Non Resident Sportsmen or Sports Association

Rate of tax – 10%+SC + EC 2% + SHEC 1% Credit or Payment, whichever is earlier. No Provision For deduction of Tax at lower rate. Category of payee – Income to NR by way of

Participation in India in any game (excl card or gambling)

Advertisement Contribution of article relating to any game or sport.

Sec 194EE– Payments in respect of Deposit under NSS

Rate of Tax-20%At time of paymentExemption Limit- Rs 2,500No Provision For deduction of Tax at lower

rate.No TDS if payment to legal heir.

Sec 194G – Commission on sale of Lottery Tickets Rate of tax – 10% Exemptions –

Payment not exceeding Rs 1,000.

Payment to New Pension Trust. Category of payee

Any person stocking, purchasing or selling lottery tickets

Case Law:MS hameed Vs director of State Lotteries (2001)Discount given to an agent on bulk purchase of lottery ticket from state Govt.

Judgment:Such Discount is not a commission and not liable for TDS

Sec 194G – Commission on sale of Lottery Tickets

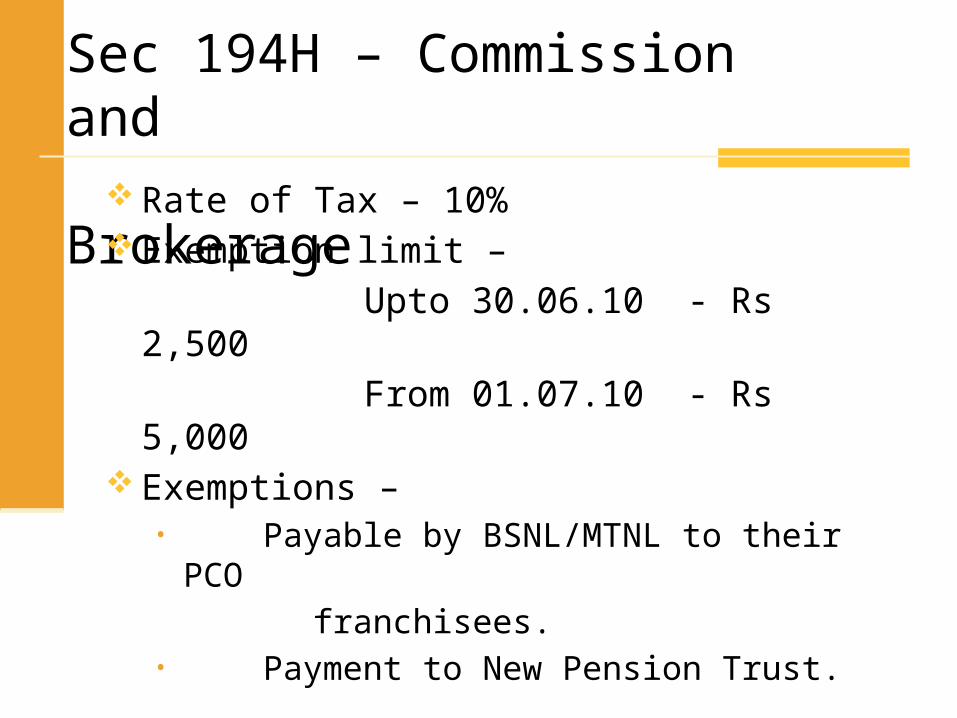

Sec 194H – Commission and Brokerage

Rate of Tax – 10% Exemption limit –

Upto 30.06.10 - Rs 2,500

From 01.07.10 - Rs 5,000 Exemptions –

• Payable by BSNL/MTNL to their PCO

franchisees.• Payment to New Pension Trust.

Case Law: Vodafone Essar Cellular Limited vs ACIT.Sale of sim card and recharge coupons at discounted price to distributors

Judgment:Such Discount given is a commission, hence liable for TDS

Sec 194H – Commission and Brokerage

Sec 194I – Rent

Rate of Tax –

Land/building/ furniture/Fittings – 10%

Machinery/Plant/Equipment – 2% Exemption limit –

Upto 30.06.10 - Rs 1,20,000

From 01.07.10 - Rs 1,80,000 Exemptions –

• If Payee is govt or local authority.• Payment to New Pension Trust

Case Law:CIT Vs Asiana Airlines (2009)Landing and Parking charges collected. Is it liable for TDS u/s 194I ?

Judgment:Landing and Parking charges is “Deemed” to be rent and liable for TDS

Sec 194I – Rent

Circulars and Cases U/S 194I

If a person has taken particular space on rent and sub-lets it.

Hotel Accomodation taken on regular basis.Building is let-out along with furniture/ fittings.Payment made for warehousing charges.Payment made to landlord in nature of

advance rent or non-refundable deposit.

Sec 194J – Fees for Professional or Technical Services

Rate of Tax – 10% Exemption Limit-

Upto 30.06.10- Rs 20,000

From 01.07.10- Rs 30,000 Exemptions –

Payment by individual/HUF Exclusively for their

personal purposes Payment to New Pension Trust.

Category of payee – Professional service or Technical service or Royalty or payments received U/s 28(1)(va)

Case Law:CIT Vs Bharthi cellular ltd Interconnection/port charges paid

Judgment:Fees for technical service includes only service rendered by human not robots/machines

Sec 194J – Fees for Professional or Technical Services

Illustrative cases of TDS u/s 194J

Advertising agency makes payment to models.

Payment made to Recruitment agency.Payment made by a company to share

registrar.Maintenance contract involving Technical

services.Service of professional cameraman.

Sec 194K – Income in respect of units Not relevant now as income from units is

exempt w.e.f. Assessment year 04-05

Sec 194LA–Compensation on acquisition of immovable property

Rate of Tax- 10%

Exemption Limit- Rs1,00,000

Exemption: Payment to New Pension Trust

Case Law:State of Kerala Vs MariammaDate of Deduction in case of delayed payment in compensation

Judgment:Deduction to be made on the date of payment even though the acquisition may have been made much before.

Sec 194LA–Compensation on acquisition of immovable property

Sec 194LB –Income from Infrastructure Debt Fund

Rate of Tax- 5%Payment to

Non residents other than companyForeign Company

Credit or Payment, whichever is earlier.W.e.f 01.06.2011

Sec 195 – TDS on Non Residents

Payment to Non residents other than companyForeign Company

Payment or Credit – whichever is earlierRate of Tax

Rate as per the Finance ActRate U/s 90Rate U/s 90A

Sec 195 – Verdicts

TDS liability only if income is taxable.Soliciting exhibitors outside India for an event

in India.No TDS on income earned before PE

established in India.Managerial & Consultancy services liable to

TDS. Interest to non resident with no PE in India

liable to TDS.

Sec 195 A – Grossing Up

Income payable net of taxGross IncomeLess: TDSNet Income

Obligation to furnish certificate to the Deductee (Net Income & TDS thereon)

Sec 196 – NO TDS

No TDS in case payment to Govt RBI Corp established by Central Act Mutual Fund U/s 10(23D)

Sec 196 B – Income from Units purchased in Foreign currencyIncome from units

U/s 115 AB LTCG on transfer of such units

Rate of Tax – 10% + SC + EC +SHEC

Sec 196 C – Foreign Currency Bonds / GDR’s

Payment to Non ResidentIncome by way of

Interest/dividend on GDR’s & BondsLTCG on transfer of such bonds

Rate of Tax – 10% + SC + EC +SHEC

Sec 196 D – Income of Foreign Institutional Investors

Income from Securities

Rate of Tax – 20% + SC + EC +SHEC

Sec 197 - No Deduction or Lower RateCertificate for deduction at lower rate

Make application to AO

No deduction or less deduction

No Certificate to be issued if PAN is not provided

Tax Deducted is deemed to be Income Received

TDS deducted & remitted – payment on behalf of the person from whom it was deducted

Service Tax – TDS Where sum is used – Including Service tax Where income is used – Excluding Service tax

Other Issues

TDS to be deposited to the credit of Govt. Tax deducted on behalf of Govt.

Without tax challan – same day With tax challan – on or before 7days

Tax deducted by others Credited or paid in March – on or before 30 April Other case – on or before 7days

Form 15H/15G

Other Issues

Assessee in default Non deduction, non payment , Non payment

of tax U/s 192(1A) Interest U/s 201

Does not deduct tax Fails to remit tax to the Govt. Does not pay tax U/s 192(1A)

Rate of Interest for default DOD – Actual DOD = 1% DOD - Date of actual payment = 1.5%

Other Issues

Important Points

Book entryConsolidated TDS certificate Issue of duplicate TDS certificateNew Pension Trust

Important Points

Failure to furnish PAN Highest of

Rate in Finance Act Rate in force( Fin Act) 20%

Deductor – 194A/194C/194H/194I/194J Any assessee(other than individual/HUF who

are not subject to tax audit U/s 44AB for the preceeding financial year)

E- Filing

Assesses mandatorily required to e-file Govt. Company Assessee subject to tax audit U/s 44AB Deducteess or Collectees for previous FY

quarter is = or > 50

TIN facilitates a PAN holder to view Annual Tax Statement online

Form 26AS contains Details of tax deducted on behalf of the taxpayer

by deductors Details of tax collected on behalf of the taxpayer

by collectors Advance tax/self assessment tax/regular

assessment tax, etc. deposited by the taxpayers (PAN holders)

Details of paid refund received during the financial year

Form 26AS

Responsibility of the receiver of payment.Presumption that buyer of goods will have

taxable income.

Tax Collected at Source

Rate of TCS

Tax Collected at Source

Specified goods Rate

Alcoholic liquor for human consuption 1%

Tendu leaves 5%

Timber obtained 2.5%

Any other forest product 2.5%

Scrap 2%

Parking lot 2%

Toll Plaza 2%

Mining And Quarring 2%

No TCS Buyer should be resident in India. Furnish self declaration in writing. Goods to be utilsed for manufacturing,

processing or producing and not for trading. Submit copy of declaration within 7th of

following month.

Tax Collected at Source

THANK YOU