tax audit changes and issues patna sept 2014

TRANSCRIPT

TAX AUDIT- CHANGES & ISSUES

ASHOK SETH, LucknowB. Sc, FCA, DISA (ICA)

Introduction

TAR finalized before 25th July 2014 Revision ?

New TAR applicable for earlier years also if audit not complete\ return not filed.

Extension of date to obtain & file TAR Strategy to file returns Before- 34 clauses + 2 annexures After- 41 clauses = NIL annexures13th Sept 2014 Patna CA Ashok Seth, Lucknow 2

General Issues

Communication with Previous Auditor Management Representation Letter

(e.g. 14A, Demands Created, Audits done)

Applicability of Accounting Standards General Purpose Financial Statements AS 1 (Accounting Policies), 2, 5, 16, 22

etc.. Materiality

CA Ashok Seth, Lucknow 313th Sept 2014 Patna

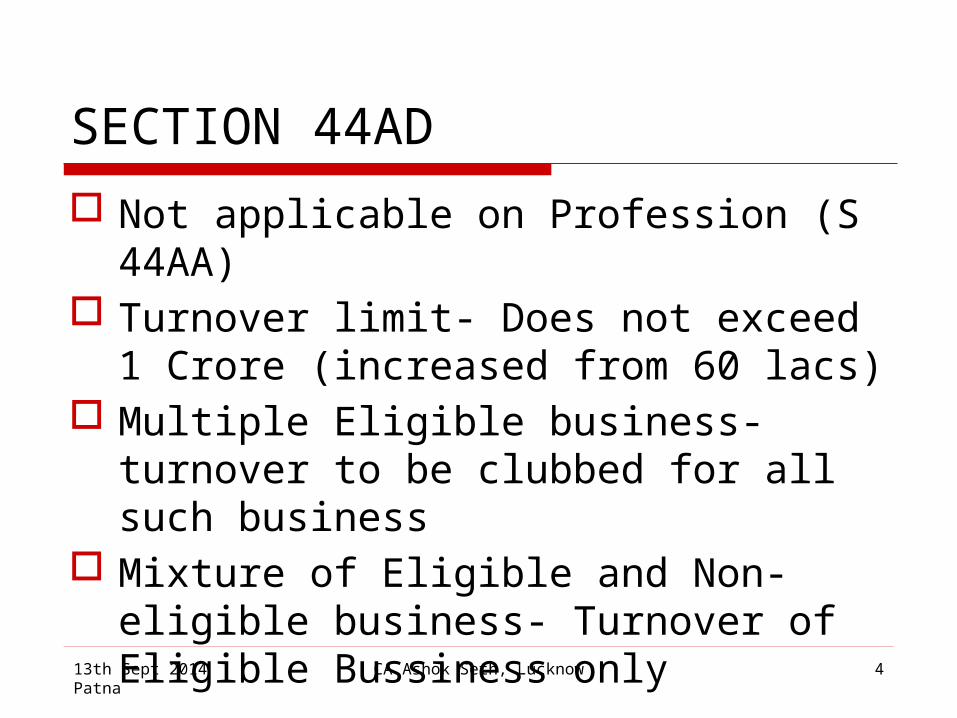

SECTION 44AD

Not applicable on Profession (S 44AA) Turnover limit- Does not exceed 1

Crore (increased from 60 lacs) Multiple Eligible business- turnover to

be clubbed for all such business Mixture of Eligible and Non-eligible

business- Turnover of Eligible Bussiness only

13th Sept 2014 Patna CA Ashok Seth, Lucknow 4

Applicability of 44AB

44AD(5) – Applicability of 44AB if profits of eligible business lower than 8% AND his income exceeds maximum amount not chargeable to tax

13th Sept 2014 Patna CA Ashok Seth, Lucknow 5

SECTION 44AD (Contd.)

The 8% income has to be income under profits and gain from business head

Income assessable under the head other sources or other heads of income other than PGBP (e.g. FDR interest, Rent etc.) not to be considered- Allied Construction 291 ITR (AT) 16 (Del)

13th Sept 2014 Patna CA Ashok Seth, Lucknow 6

SECTION 44AD (Contd.)

Not applicable on Profession (S 44AA) Turnover limit- Does not exceed 1

Crore (increased from 60 lacs) Multiple Eligible business- turnover to

be clubbed for all such business Mixture of Eligible and Non-eligible

business- Turnover of Eligible Bussiness only

13th Sept 2014 Patna CA Ashok Seth, Lucknow 7

Decision MatrixIncome from Eligible Bussiness

Total Income Applicability of 44AD

Applicability of 44AB &

44AA> 8% of turnover

Exceeds Exemption

Limited

Yes No

= 8% of turnover

Exceeds Exemption

Limited

Yes No

< 8% of turnover

Exceeds Exemption

Limited

No Yes

< 8% of turnover

Less than Exemption

Limited

No No

13th Sept 2014 Patna CA Ashok Seth, Lucknow 8

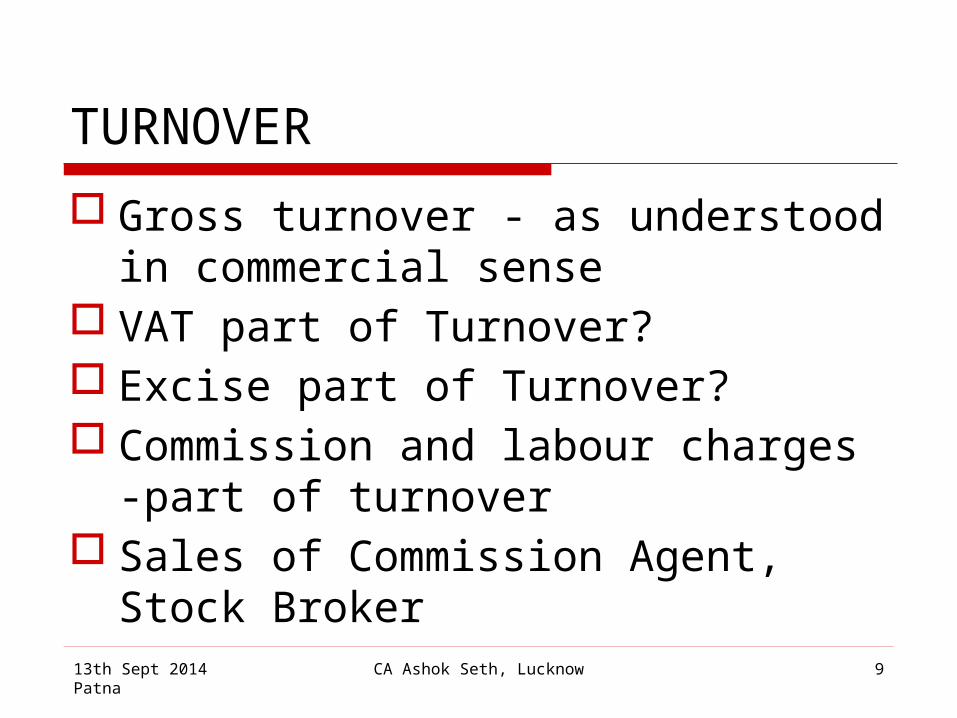

TURNOVER

Gross turnover - as understood in commercial sense

VAT part of Turnover? Excise part of Turnover? Commission and labour charges -

part of turnover Sales of Commission Agent, Stock

Broker13th Sept 2014 Patna CA Ashok Seth, Lucknow 9

Turnover in Speculative Bussiness and Derivatives

In case of a day trader/speculator, & derivatives transactions in Security and Commodity Markets: - Sum total of differences, whether

positive or negative (Para 5.11(a) to (c) of ICAI Guidance Note) and also premium on sale of options unsettled transactions at year end

13th Sept 2014 Patna CA Ashok Seth, Lucknow 10

Example of TurnoverType Shares Profits (a) Loss (b)

Future RIL 500.00

Future Tata 200.00

Future Infosys 800.00

Total 1,300.00 200.00

GROSS TURNOVER WILL BE (a + b) 1,500.00

13th Sept 2014 Patna CA Ashok Seth, Lucknow 11

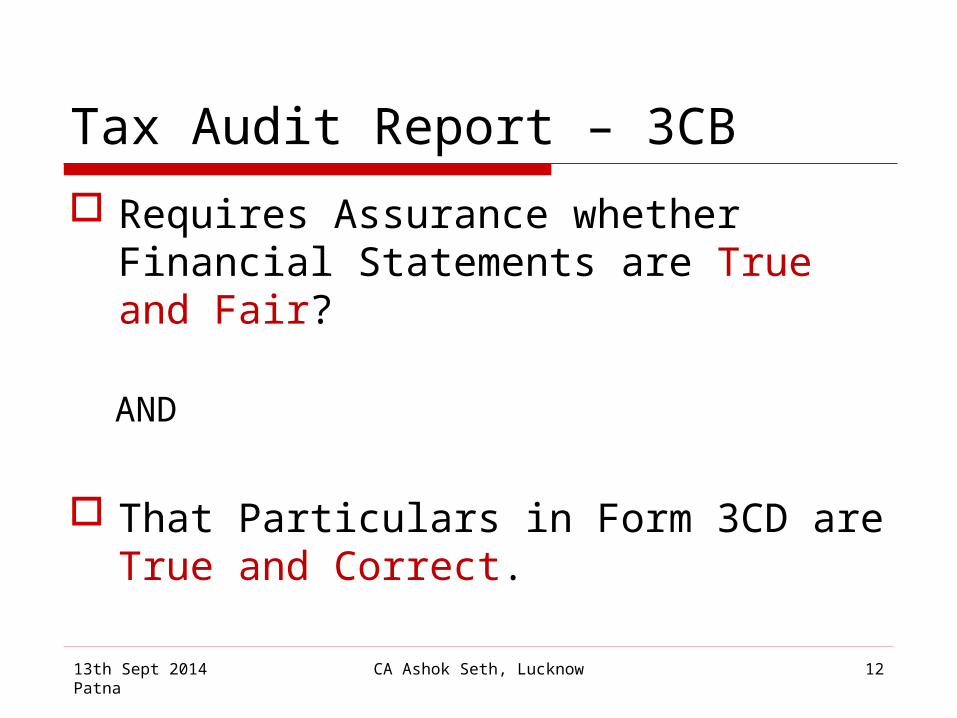

Tax Audit Report – 3CB

Requires Assurance whether Financial Statements are True and Fair?

AND

That Particulars in Form 3CD are True and Correct.

13th Sept 2014 Patna CA Ashok Seth, Lucknow 12

True and Fair- 3CB

To include disclaimer as per Para 19 of SA 700 (AAS 28) relating to preparation of accounts by the assessee and the scope of audit.

Membership No of signatory and FRN no of firm should be given. Stamp of auditor (In hard copy only)

13th Sept 2014 Patna CA Ashok Seth, Lucknow 13

Changes in 3CA

Para-1(a) The audited profit and loss account for the period beginning from_____ to ending on _______

Para-3 In our opinion ……………and according to examination of books of account including other relevant documents and explanations given ______ subject to the following observations/qualifications, if any:

13th Sept 2014 Patna CA Ashok Seth, Lucknow 14

Changes in 3CB

Para-1- The audited profit and loss account for the period beginning from_____ to ending on _______

Para-2- books of account maintained at the head office at _______ and __(number)_ branches.

Para-3(a)- We report the following observations /comments/ discrepancies/ inconsistencies, if any:

13th Sept 2014 Patna CA Ashok Seth, Lucknow 15

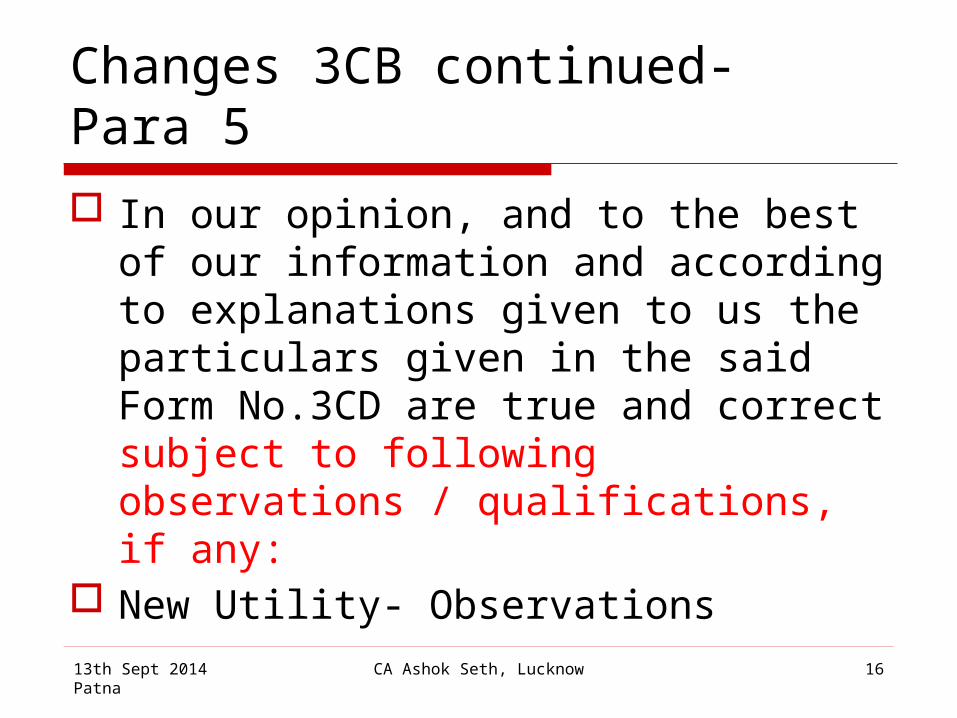

Changes 3CB continued- Para 5

In our opinion, and to the best of our information and according to explanations given to us the particulars given in the said Form No.3CD are true and correct subject to following observations / qualifications, if any:

New Utility- Observations

13th Sept 2014 Patna CA Ashok Seth, Lucknow 16

Changes in 3CD

Clause 4- Whether the assessee is liable to pay indirect tax like excise duty, service tax, sales tax, customs duty, etc. (Para 17.6 Page of GN 2014)- report for all Branches if separate

If applicable but not registered appropriate disclosure.

Registration taken but not liable ?13th Sept 2014 Patna CA Ashok Seth, Lucknow 17

Clause 6 & 8

Previous Year from______ to ______ Relevant clause of section 44AB under which

the audit has been conducted- More than one ?

13th Sept 2014 Patna CA Ashok Seth, Lucknow 18

a) Sale > 1 Crore Sub Clause (a)

b) Profession > 25 Lacs Sub Clause (b)

c) 44AE Truck plying, 44BB, 44BBB

Sub Clause (C)

d) 44AD NP < 8% Sub Clause (d)

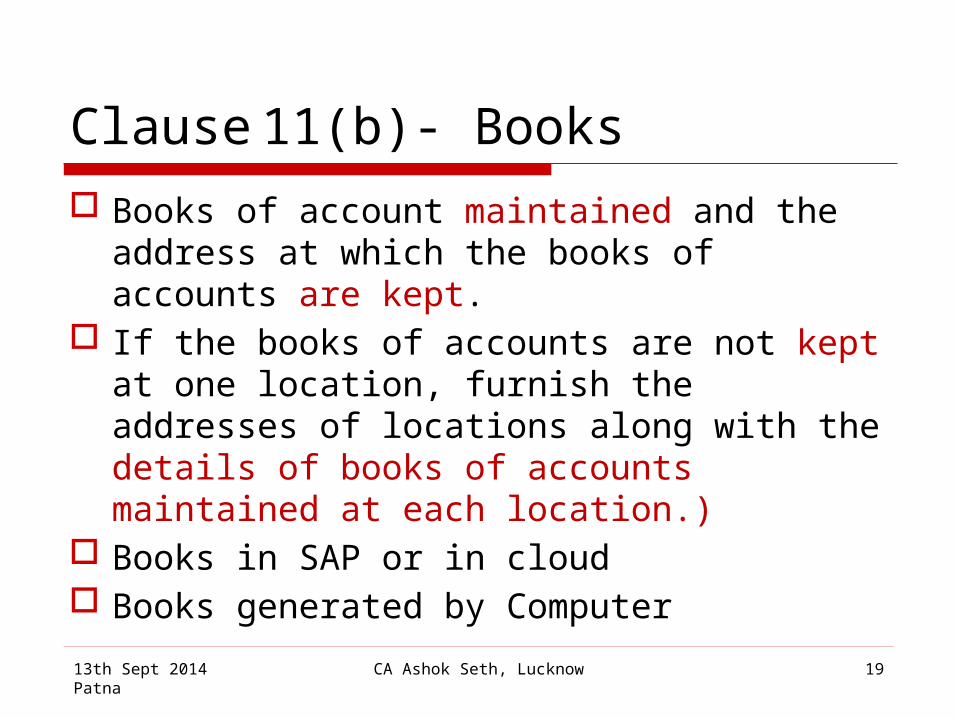

Clause 11(b)- Books

Books of account maintained and the address at which the books of accounts are kept.

If the books of accounts are not kept at one location, furnish the addresses of locations along with the details of books of accounts maintained at each location.)

Books in SAP or in cloud Books generated by Computer

13th Sept 2014 Patna CA Ashok Seth, Lucknow 19

CLASUE 11(C)

List of books of account and nature of (not list) relevant documents examined

Documents- Sec 2(22AA)- includes electronic records.

E.g. Bills/Invoices/ Receipts/ Cr or Dr Notes/Statutory Registers/ Agreements/ Correspondence/ Third party confirmations etc.

13th Sept 2014 Patna CA Ashok Seth, Lucknow 20

Clause 13

13(a) Method of accounting employed-In Utility Cash or Mercantile

13(d)- Details of deviation, if any, in the method of accounting employed from accounting standards prescribed under section 145 and the effect thereof on the profit or loss

Method of accounting Vs. Accounting Policy

13th Sept 2014 Patna CA Ashok Seth, Lucknow 21

Clause 17

Where any land or building or both is transferred during the previous year for a consideration less than value adopted or assessed or assessable by any authority of a State Government referred to in section 43CA or 50C

Un-Registered Documents In Individual- Capital assets forming \

not forming part of accounts ?13th Sept 2014 Patna CA Ashok Seth, Lucknow 22

Clause 17 Issues: -

When and whether transfer takes place- Auditors duty on difference of opinion

Land and Building forming part of block- where block is still positive sec 50 not applicable- Auditors Stand?

13th Sept 2014 Patna CA Ashok Seth, Lucknow 23

Reporting Clause 17

Detail of Property

Consideration received or accrued

Value adopted or assessed orassessable

13th Sept 2014 Patna CA Ashok Seth, Lucknow 24

Clause 20(b)

Details of contributions received from employees for various funds as referred to in section 36(1)(va) (Sec 2(24)(x)) Col: - Nature of fund Sum Received from employees Due date Actual amount Paid Actual Date of payment

13th Sept 2014 Patna CA Ashok Seth, Lucknow 25

Clause 21

In some clauses “amounts debited to P&L Account being” (sub clause (a)) Expenditure incurred at clubs being cost

of services and facilities used. Penalty or fine for violation of law

(b) Inadmissible u/s 40(a) On Payments to NR under sub clause(i) under sub clause(ia)

13th Sept 2014 Patna CA Ashok Seth, Lucknow 26

Clause 21(d) Sec 40A(3)

Disallowance Clause 21(d)(A) Deemed Income Clause 21(d)(B) On the basis of the examination of

books of account and other relevant documents/evidence

Certificate dispensed with

13th Sept 2014 Patna CA Ashok Seth, Lucknow 27

Clause 24

Amounts deemed to be profits and gains under

section 32AC- Special deduction for New Machinery > 100 Crore

33AB (Tea Development) 33ABA (Site Restoration Fund) 33AC (Reserve for Shipping business)

13th Sept 2014 Patna CA Ashok Seth, Lucknow 28

Clause 28 (Page 188 of GN 2014)

Whether during the previous year the assessee has received any property, being share of a company not being a company in which the public are substantially interested, without consideration or for inadequate consideration as referred to in section 56(2)(viia), if yes, please furnish the details of the same

13th Sept 2014 Patna CA Ashok Seth, Lucknow 29

Clause 28 Contd.

Section 56(2)(viia)- Applicable to Firms and Companies

Valuation to be done as per 11UA (Rule 11U provides Definitions)

Controversy on right issue, Bonus Shares, allotment of shares by company

Details required in utility no format in form 3CD

13th Sept 2014 Patna CA Ashok Seth, Lucknow 30

Clause 28- Details

Name of the person from whom shares received

PAN if available Name of the Co whose shares Recd CIN No of Shares Consideration paid Fair Market value of shares

13th Sept 2014 Patna CA Ashok Seth, Lucknow 31

Clause 29 (Applicable to Cos)

Whether during the previous year the assessee received any consideration for issue of shares which exceeds the fair market value of the shares as referred to in section 56(2)(viib), if yes, please furnish the details of the same

Rule 11U and 11UA applicable No format in form but details required

in Utility

13th Sept 2014 Patna CA Ashok Seth, Lucknow 32

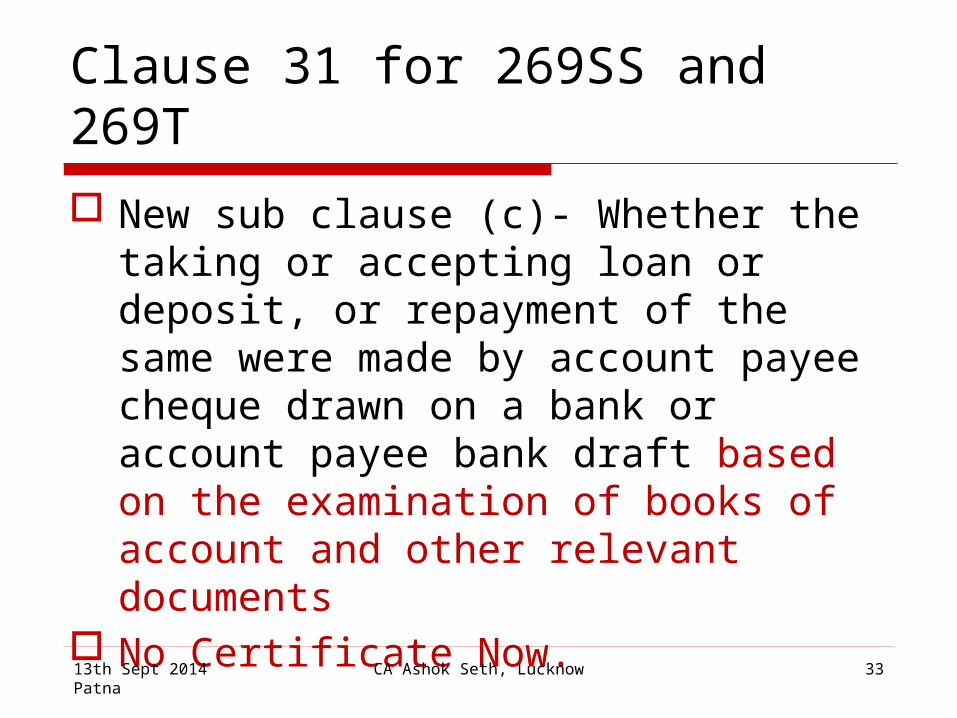

Clause 31 for 269SS and 269T

New sub clause (c)- Whether the taking or accepting loan or deposit, or repayment of the same were made by account payee cheque drawn on a bank or account payee bank draft based on the examination of books of account and other relevant documents

No Certificate Now.13th Sept 2014 Patna CA Ashok Seth, Lucknow 33

Clause 32(c), (d) & (e)

Whether the assessee has incurred any speculation loss referred to in section 73 or 73A (Specified business sec 35AD) during the previous year, If yes, please furnish the details of the same. (Page 204 of GN)

In the case of company whether the company is deemed to be carrying on speculation business if yes furnish details

13th Sept 2014 Patna CA Ashok Seth, Lucknow 34

Clause 33- Deductions admissible

Chapter III (section 10A Free trade zones and 10AA Special economic zones) newly included for deduction

Amounts admissible as per the provision of the Act, and fulfils the conditions, if any, specified under the relevant provisions of Act, or Rules, or any other guidelines, circular, etc., issued in this behalf

13th Sept 2014 Patna CA Ashok Seth, Lucknow 35

Clause 34 for TDS & TCS

If assessee required to deduct TDS\TCS- required to furnish details as per chart

Whether TDS returns filed in time

13th Sept 2014 Patna CA Ashok Seth, Lucknow 36

TDS \ TCS- Detail Chart Col-4 Total amount of the nature Col-5 Amount on which Tax was liable to be

deducted Col-6 Total amount on which TDs deducted

at specified rates Col-7 Tax deducted Col-8 Total amount on which TDS at less than

specified rate Col-9 TDS on Col 8 amounts Col-10 TDS not deposited13th Sept 2014 Patna CA Ashok Seth, Lucknow 37

34(b)- Return filling

If returns not filed in time then the following also to be certified: -

Whether the statement of Tax deducted or collected contains information about all transactions which are required to be reported

13th Sept 2014 Patna CA Ashok Seth, Lucknow 38

Clause 34(C)

Whether liable to pay interest u/s 201(1A) or 206C(7)- If yes furnish details of payments.-

Diff in computation of month by Traces and assessee.

Should auditor take cognizance of traces notice and their method of calculation

13th Sept 2014 Patna CA Ashok Seth, Lucknow 39

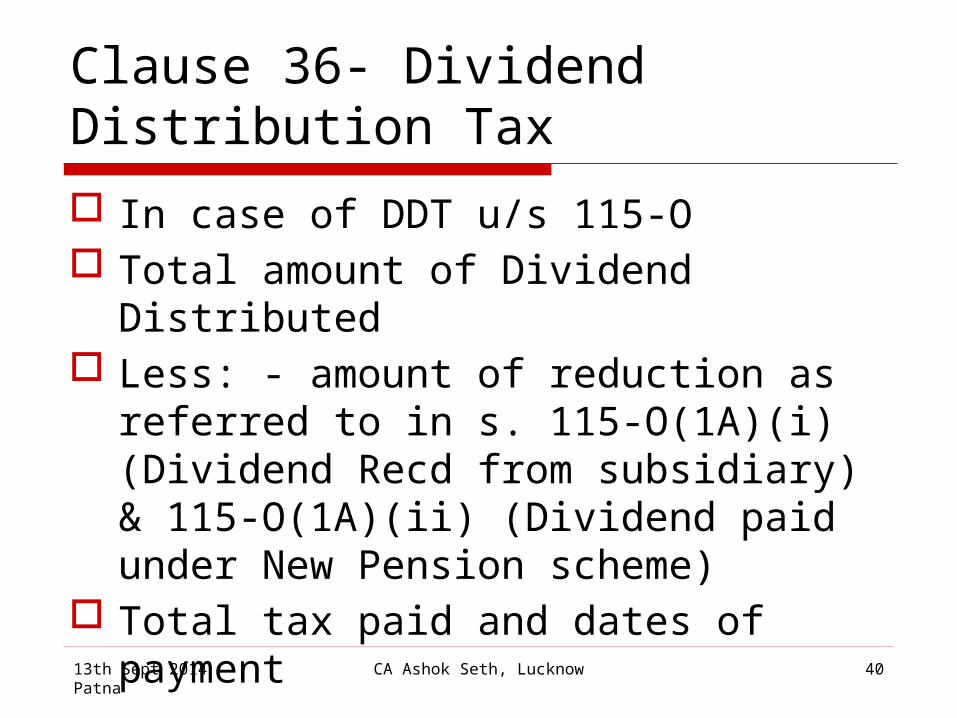

Clause 36- Dividend Distribution Tax

In case of DDT u/s 115-O Total amount of Dividend Distributed Less: - amount of reduction as

referred to in s. 115-O(1A)(i) (Dividend Recd from subsidiary) & 115-O(1A)(ii) (Dividend paid under New Pension scheme)

Total tax paid and dates of payment

13th Sept 2014 Patna CA Ashok Seth, Lucknow 40

Clause 37 to 39

Whether any: - Cost audit was carried out, Audit was conducted under the Central

Excise Act, 1944, Audit was conducted under section 72A

of the Finance Act,1994- Service Tax

13th Sept 2014 Patna CA Ashok Seth, Lucknow 41

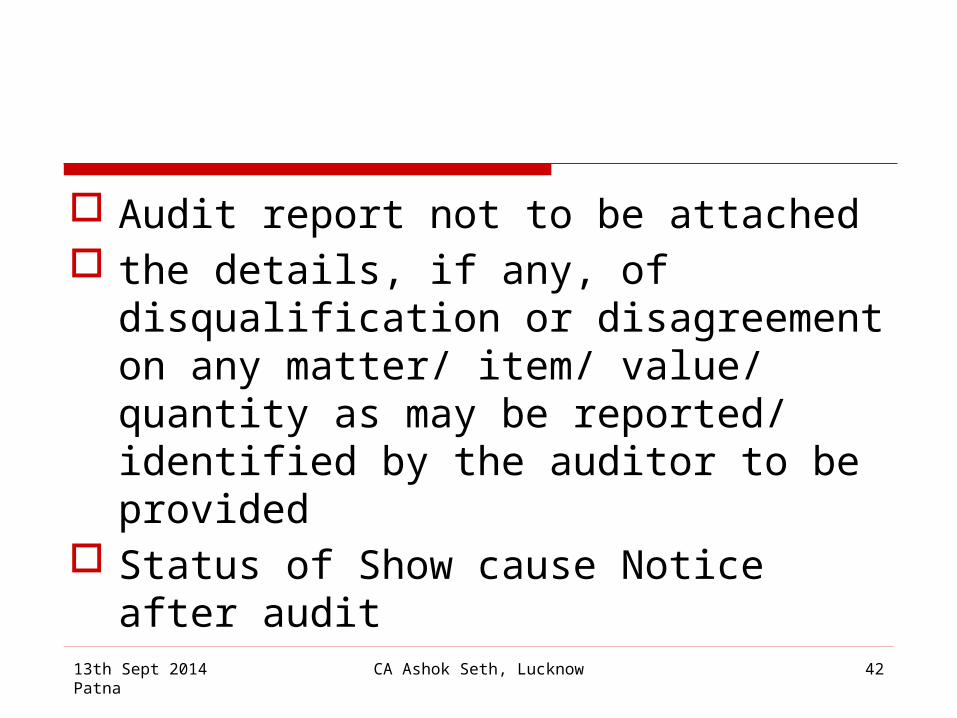

Audit report not to be attached the details, if any, of disqualification

or disagreement on any matter/ item/ value/ quantity as may be reported/ identified by the auditor to be provided

Status of Show cause Notice after audit

13th Sept 2014 Patna CA Ashok Seth, Lucknow 42

Clause 40- Ratios

Now previous year’s figures also to be given.

If previous year’s figures regrouped the ratios should be recomputed ?

The details required to be furnished for principal items of goods traded or manufactured or services rendered

13th Sept 2014 Patna CA Ashok Seth, Lucknow 43

Clause 41

Furnish the details of demand raised or refund issued during the previous year under any tax laws other than Income Tax Act, and Wealth tax Act, along with details of proceedings

VAT \ Customs\ Excise \ Service Tax \ State Excise\ Entertainment Tax\ Professional Tax etc. etc. etc.

Management Representation13th Sept 2014 Patna CA Ashok Seth, Lucknow 44

General

If previous years audit was done by other auditor note should be given:-

The Financial statements of the Company as at ______ and for the year then ended were audited by another firm of Chartered Accountants, who vide their report dated _____, expressed an un-modified opinion on those financial statements.

13th Sept 2014 Patna CA Ashok Seth, Lucknow 45

Important Un-changed clauses14(b)- 145(A) variation

145A(ii)- further adjusted to include the amount of any tax, duty, cess or fee actually paid or incurred by the assessee to bring the goods to the place of its location and condition as on the date of its valuation (Page 99 of GN 2014)

Adjustments are profit neutral – CIT v. Indo Nippon Chemicals Co. Ltd. 261 ITR 275 (SC)

13th Sept 2014 Patna CA Ashok Seth, Lucknow 46

Others

Clause 18- Dispute in Depreciation e.g. additional Depreciation issues-

Clause 21(h)- Disallowance under section 14A- Judicial pronouncements

13th Sept 2014 Patna CA Ashok Seth, Lucknow 47

14A (Contd.)

The amount of inadmissible expenses depends upon facts and circumstances of the case.

Rule 8D does not mandate that assessee should necessarily compute the disallowance as per Rule 8D(2)

The Auditor will have to verify the amount of inadmissible expenditure as determined by the assessee.

13th Sept 2014 Patna CA Ashok Seth, Lucknow 48

14A (Contd.)

If in agreement with computation by assessee, report amount with suitable disclosure of material assumptions

If not in agreement, either give Qualified opinion, Adverse opinion, or Disclaimer of opinion – where neither basis nor supporting documents provided

13th Sept 2014 Patna CA Ashok Seth, Lucknow 49

Clause 17A- Interest to MSME

Interest inadmissible u/s 23 of the MSME Development Act, 2006.

Sec 16 of MSME Act the Date from which and rate at which interest is payable.

Sec 22 Provides for additional information in Audited Financial statements. Appropriate qualification

13th Sept 2014 Patna CA Ashok Seth, Lucknow 50

Clause 17A- Interest to MSME (Contd.)

Where auditee neither provided nor paid any interest under MSME act- NIL can be reported in clause 17A.

If interest payable and not provided in financial statements- effect on true and fairness to be seen

13th Sept 2014 Patna CA Ashok Seth, Lucknow 51

Clause 23- 40A(2)(b) Refer Page 158 & 273 of GN 2014

Now: Any other company carrying on business in which the first mentioned company has substantial interest will also be covered – refer – sub section (v)

13th Sept 2014 Patna CA Ashok Seth, Lucknow 52

Miscellaneous

Clause 27(b)- Prior Period expenditure- Refer AS 5

Clause 32- Brought forward loses- appropriate disclosure.

Clause 32(b)- Losses carry over – Section 79 Change of share holding

13th Sept 2014 Patna CA Ashok Seth, Lucknow 53

If you wait for happy moments, you will wait forever.

But if you start believing that you are happy,

you will be happy forever.Good Day!

CA Ashok Seth, Lucknow 5413th Sept 2014 Patna

Please mail your comments to

55CA Ashok Seth, Lucknow13th Sept 2014 Patna

THANK YOU

56

Have a good day

CA Ashok Seth, Lucknow13th Sept 2014 Patna