tav airports ppp applications and investments … \\nlon14p20505a\gis$\verticals\transport and...

TRANSCRIPT

““ PP

P a

pp

licati

on

s a

nd

In

vestm

en

ts a

t A

irp

ort

sP

PP

ap

plicati

on

s a

nd

In

vestm

en

ts a

t A

irp

ort

s””

Tu

nis

, T

un

is,

Dece

mb

er

Dece

mb

er

2007

2007

Halu

k B

ilgi

Halu

k B

ilgi

PD

G, T

AV

Tunis

ie S

.A.

PD

G, T

AV

Tunis

ie S

.A.

TAV AIRPORTS

TAV AIRPORTS

1

\\nlo

n14

p205

05a

\GIS

$\V

ert

icals

\Tra

nsp

ort

and

Logis

tics (

TP

T)\

Clie

nts

2\T

AV

\IP

O 2

00

6\O

the

r\R

oad

sho

w\T

AV

Roadsh

ow

pre

se

nta

tion

FIN

AL v

9 (

No

Scrip

t).p

pt

/1

CO

NT

EN

TC

ON

TE

NT

�Aviation Industry

�Growth in Aviation Business

�The Player in the Market

�Valuation of an Airport as aBusiness

�TAV Airports as a succesful example for a company born through PPP

�IPO of TAV

�Example for a different type of PPP “TUNISIA”

2

\\nlo

n14

p205

05a

\GIS

$\V

ert

icals

\Tra

nsp

ort

and

Logis

tics (

TP

T)\

Clie

nts

2\T

AV

\IP

O 2

00

6\O

the

r\R

oad

sho

w\T

AV

Roadsh

ow

pre

se

nta

tion

FIN

AL v

9 (

No

Scrip

t).p

pt

/2

Aviation Industry

Aviation Industry

TODAY

�18.300 commercial aircraft

�4.2 billion passengers

�2000 commercial airports

�93 Airports represent the %

64

of the passengers in the world

BY

YEAR 2020

�35.000 commercial aircraft

�9 billion passengers

�~$300 billion investm

ent is needed

for Airport constructions, expansions

Solution

: Public Private Partnerships (PPPs)

Problem

: Inadequate Airport Infrastructure -

3

\\nlo

n14

p205

05a

\GIS

$\V

ert

icals

\Tra

nsp

ort

and

Logis

tics (

TP

T)\

Clie

nts

2\T

AV

\IP

O 2

00

6\O

the

r\R

oad

sho

w\T

AV

Roadsh

ow

pre

se

nta

tion

FIN

AL v

9 (

No

Scrip

t).p

pt

/3

AIR

PO

RT

S ...

AIR

PO

RT

S ...

Airports,

are the m

elting pots of

globalization where

travellers m

ultibusinesses

products and goods m

eet in

one place...

Airport operators have to

bring dynamic life to airports

which will help you to

become chosen by airlines

and passengers..

Airports are no longer sim

ply

infrastructure providers,they

are m

ulti-businesses,

facing commercial

disiplines,focusing on new

investm

ents and sustainable

growth...

4

\\nlo

n14

p205

05a

\GIS

$\V

ert

icals

\Tra

nsp

ort

and

Logis

tics (

TP

T)\

Clie

nts

2\T

AV

\IP

O 2

00

6\O

the

r\R

oad

sho

w\T

AV

Roadsh

ow

pre

se

nta

tion

FIN

AL v

9 (

No

Scrip

t).p

pt

/4

PP

Ps a

nd

Ke

y S

ucce

ss F

acto

rsP

PP

s a

nd

Ke

y S

ucce

ss F

acto

rs

�B

.O.T

. (B

uild

Op

era

te T

ran

sfe

r)

�B

.T.O

. (B

uild

Tra

nsfe

r O

pera

te)

�B

.O.O

. (B

uild

Op

era

te O

wn

)

�L

on

g T

erm

Co

ncessio

ns

�T

rad

e S

ale

s

�C

learl

y d

efi

ned

sco

pes

�C

lear

defi

nit

ion

of

the R

eve

nu

e S

tream

s

�C

lear

defi

nit

ion

of

Co

st

Cen

ters

�A

gre

ed

Cap

ex

(C

ap

ital

Exp

en

dit

ure

) b

ased

on

th

e c

on

cep

t(d

esig

n)

�P

red

efi

ned

leg

al

fram

ewo

rk

�F

air

defi

nit

ion

of

“term

inati

on

cla

uses”

�D

isp

ute

Cla

use

5

\\nlo

n14

p205

05a

\GIS

$\V

ert

icals

\Tra

nsp

ort

and

Logis

tics (

TP

T)\

Clie

nts

2\T

AV

\IP

O 2

00

6\O

the

r\R

oad

sho

w\T

AV

Roadsh

ow

pre

se

nta

tion

FIN

AL v

9 (

No

Scrip

t).p

pt

/5

Valu

ati

on

Para

mete

rsV

alu

ati

on

Para

mete

rs

Re

ven

ues

1)

Aero

nau

tical R

even

ues

•P

ax F

ee

•L

an

din

g F

ee

•P

ark

ing

Fe

e

•L

igh

tin

g F

ee

•P

BB

Fe

e

•C

he

ck i

n C

UT

E F

ee

•S

ecu

rity

Fe

e ...

. E

tc

•2)

No

n a

ero

nau

tical

Reven

ues (C

om

merc

ial)

•D

uty

Fre

e R

eve

nu

es

•F

&B

Re

ve

nu

es

•C

ar-

Park

Re

ve

nu

es

•A

dvert

isem

en

t

•A

rea a

llo

ca

tio

n r

even

ue..

..etc

.

Op

ex

Th

e O

PE

X in

air

po

rts is

main

ly s

ala

ries o

f em

plo

yees,

main

ten

an

ce

exp

en

dit

ure

s, ele

ctr

icit

y an

d w

ate

r co

nsu

mp

tio

n

Cap

ex

CA

PE

X i

s t

he a

mo

un

t o

f in

vestm

en

t n

eed

ed

to

b

uild

a n

ew t

erm

inal o

r a

run

wa

y o

r exp

an

d a

te

rmin

al;

or

for

refu

rbis

hm

en

t.

6

LO

DO

CS

1 -

#172

131v14

/6

Valu

ati

on

: L

ucra

tive M

ult

iple

s

Sourc

e:

Blo

om

berg

, IB

ES

Conse

nsus E

stim

ate

s

Da

te A

nn

ou

nc

ed

Ta

rge

tA

cq

uir

or

Sta

ke

(%)

EV

(€)

EV

/EB

ITD

A

(X)

Oct-

06

Lo

ndo

n C

ity A

irp

ort

AIG

10

01

.110

na

Ju

n-0

6B

AA

Fe

rro

via

l1

00

14

.79

01

3,8

De

c-0

5B

ud

ape

st A

irpo

rtB

AA

75

1.8

53

39

,3

De

c-0

5C

op

enh

age

n A

irp

ort

Ma

cq

ua

rie

89

2.6

14

13

,4

Ma

r.0

5H

och

tief

Air

po

rtC

DC

-Ha

stin

gs

50

12

59

,8

Fe

b-0

5C

op

enh

age

n A

irp

ort

Ma

cq

ua

rie

11

16

79

,6

No

v-0

4B

IAC

Ma

cq

ua

rie

70

73

59

,8

No

v-0

4T

BI

Ae

na

10

09

17

12

,6

Oct-

04

Lo

ndo

n L

uto

n A

irp

ort

TB

I2

91

16

15

,3

Ma

y.0

3B

elfast

City

Airp

ort

Fe

rro

via

l1

00

49

19

,6

Ju

l-0

2R

om

e A

irp

ort

M

acq

ua

rie

45

1.0

67

14

,5

Co

mp

an

yC

ou

ntr

yEV/07E EBITDA(X)

EV/08E EBITDA(X)

EV/09E EBITDA(X)

AD

PF

ran

ce1

3,5

12

,21

1,2

Fra

po

rtG

erm

an

y8

,68

,27

,8

Vie

nna

Au

str

ia1

0,2

9,6

8,9

TA

VT

AV

(*)

(*)

Tu

rkey

Tu

rkey

8,2

8,2

6,4

6,4

5,6

5,6

Zu

rich

Sw

itze

rla

nd

9,9

9,3

8,9

Ae

ro D

el S

ure

ste

(A

SU

R)

Me

xico

9,6

8,2

7,3

Ae

ro D

el P

aci

fico

(G

AP

)M

exi

co

13

,21

1,5

10

,4

Ae

ro D

el C

en

tra

l N

ort

e (

OM

A)

Me

xico

13

10

,79

,4

Air

po

rts o

f T

ha

ilan

dT

ha

iland

10

87

Be

ijin

g C

ap

. In

t’l

Ch

ina

32

,12

4,5

21

,9

Ha

inan

Me

ilan

Airp

ort

Ch

ina

8,4

6,9

5,3

GM

RIn

dia

52

,52

8,5

16

,1

Me

dia

n1

0,2

9,6

8,9

Sourc

e:

Com

pan

y re

po

rts, P

ressre

lea

ses

Min

imu

m9,6

Maxim

um

39,3

Med

ian

13,6

Mean

15,8

7

LO

DO

CS

1 -

#172

131v14

/7

Co

nce

ssio

n O

verv

iew

Co

nce

ssio

n O

verv

iew

Sourc

e:

Com

pan

y da

ta,

Note

s:

(1)

As o

f 30

Ju

ne

200

7

Typ

e /

exp

ire

Sco

pe

Co

ncessio

n

fee

200

6P

ax (

mp

pa)

Fee/p

ax

Inte

rn’l

Fee/p

ax

do

mesti

cA

irp

ort

Lease

(2021)

Intl

+ d

om

$165m

/yr

21.2

US

$15

€3

Ista

nb

ul

Ata

turk

BO

T(2

023)

Intl

+ d

om

-4.5

5€15

€3

An

kara

E

sen

bo

ga

BO

T(2

015)

Intl

-1.4

5€15

-Iz

mir

A

Men

dere

s

BO

T(2

027)

Intl

+ d

om

-0.6

US

$22

(+ 2

% p

.a.)

US

$6

Tb

ilis

i

Vo

lum

e

gu

ara

nte

e

No

0.6

m D

om

.0.7

5 In

t’l fo

r 2007 +

5%

p

.a.

1.0

m In

t’l fo

r 2006 +

3%

p

.a.

No

TA

V s

tak

e

100%

100%

100%

60%

BO

T+

co

ncessio

n(2

047)

Intl

+ d

om

11-2

6%

of

rev

en

ues

fro

m

2010 t

o 2

047

4.2

€8.2

5 in

2008

€9 in

2009

€8.2

5 in

2008

€9 in

2009

Mo

nasti

r&

En

fid

ha

No

100%

BO

T(2

027)

Intl

+ d

om

--

US

$12

US

$7

Batu

mi

No

60%

8

LO

DO

CS

1 -

#172

131v14

/8

TA

V A

irp

ort

s O

verv

iew

TA

V A

irp

ort

s O

verv

iew

O&

M, IT

an

d S

ecu

rity

�T

AV

O&

M (

10

0%

):

�C

om

merc

ial a

rea

allo

catio

ns

�C

IP / V

IP

�T

AV

IT

(9

6%

):

�A

irport

IT

serv

ices

�T

AV

Se

cu

rity

(6

7%

):

�S

ecurity

serv

ice

pro

vider

in

Ista

nbul,

Ankara

and Izm

ir

Air

po

rts

Du

ty F

ree

Fo

od

an

d

Be

vera

ge

Gro

un

d

Ha

nd

lin

gO

the

r

Tu

rke

y

�Is

tan

bul A

tatü

rk A

irp

ort

(1

00

%)

�A

nka

ra E

sen

bo

ğa

Air

po

rt

(10

0%

)

�Iz

mir

Ad

na

n M

en

de

res

Air

po

rt (

Intl.

Te

rmin

al)

(1

00

%)

Ge

org

ia

�T

bili

si I

nte

rna

tiona

l A

irp

ort

an

d B

atu

mi

Air

po

rt(6

0%

)

Tu

nis

ia

�M

on

astir

and

En

fidha

A

irp

ort

s(1

00

%)

AT

Ü(5

0%

)

�Larg

est duty

fre

e

opera

tor

in T

urk

ey

�P

art

ner

with

Un

ifre

e –

leadin

g G

erm

an tra

vel

reta

iler

(Tra

vel V

alu

e)

BT

A (

67

%)

�44 o

utle

ts w

ith a

tota

l seatin

g c

apacity

of

4,5

00 in

Ista

nbul

�O

pera

tes Ista

nbul

Airport

Hote

l

�B

akery

& p

astr

y fa

cto

ry

serv

ing S

tarb

ucks in

T

urk

ey

Hav

aş

(100%

)

�T

raff

ic, ra

mp a

nd c

arg

o

handlin

g

�M

ajo

rgro

undhandle

r in

T

urk

ey

with

a c

.51%

share

�O

pera

tes in

11

airport

s

in T

urk

ey

inclu

din

g

Ista

nbul,

Ankara

, Iz

mir

and A

nta

lya

““ Co

nn

ecti

vit

y i

s P

rod

ucti

vit

yC

on

necti

vit

y i

s P

rod

ucti

vit

y””

9

LO

DO

CS

1 -

#172

131v14

/9

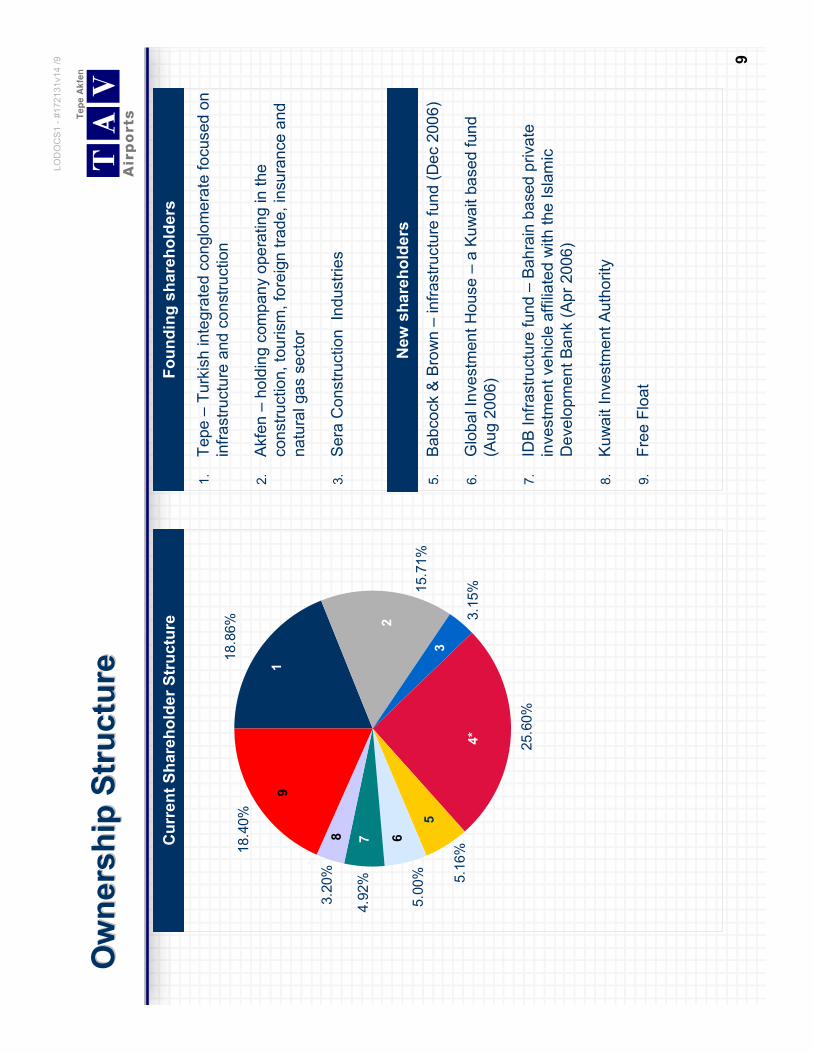

Ow

ners

hip

Str

uctu

reO

wn

ers

hip

Str

uctu

re

Fo

un

din

g s

ha

reh

old

ers

1.

Tepe

–T

urk

ish

inte

gra

ted

con

glo

me

rate

fo

cused

on

infr

astr

uctu

re a

nd

co

nst

ruction

2.

Akfe

n –

ho

ldin

g c

om

pan

y o

pe

ratin

g in

the

con

str

uctio

n,

tou

rism

, fo

reig

n t

rade

, in

sura

nce

and

na

tura

l ga

s s

ecto

r

3.

Se

ra C

on

str

uction

In

du

str

ies

4.

Go

ldm

an

Sa

chs (

De

c 2

006

)

5.

Bab

cock &

Bro

wn

–in

fra

str

uctu

re f

und

(D

ec 2

00

6)

6.

Glo

bal In

vestm

en

t H

ouse

–a

Ku

wa

it b

ased

fund

(A

ug 2

006

)

7.

IDB

Infr

astr

uctu

re f

und –

Ba

hra

in b

ase

d p

riva

te

inve

stm

en

t ve

hic

le a

ffili

ate

d w

ith

the

Isla

mic

D

eve

lopm

en

t B

an

k (

Ap

r 2006

)

8.

Ku

wa

it In

vestm

en

t A

uth

ority

9.

Fre

e F

loa

t

Cu

rre

nt

Sh

are

ho

lde

r S

tru

ctu

re

18.4

0%

3.2

0%

4.9

2%

5.0

0%

15.7

1%

18.8

6%

5.1

6%

3.1

5%

25.6

0%

1

2

3

4*

5

7

9

6N

ew

sh

are

ho

lde

rs

8

10

LO

DO

CS

1 -

#172

131v14

/10

Off

eri

ng

Su

mm

ary

Off

eri

ng

Su

mm

ary

�G

lob

al

Inte

rna

tio

na

l O

ffe

r (6

9%

)�

Ou

tsid

e U

S,

ins

titu

tio

na

l in

ves

tors

un

de

r R

eg

S�

Pu

bli

c o

ffe

r in

Tu

rkey

(31

%)

�T

RY

10

.00

(P

rice

Ran

ge

TR

L 8

.55

–T

RL

10

.30

)

�Is

tan

bu

l S

toc

k E

xc

han

ge

(“I

SE

”)

�10

cit

ies

vis

ite

d i

n E

uro

pe

an

d M

idd

le E

as

t

�11

da

y ro

ad

sh

ow

co

mp

ris

ing

48

on

e-o

n-o

ne

mee

tin

gs

, c

on

fere

nc

e c

all

s w

ith

11

in

ves

tors

a

nd

gro

up

me

eti

ng

s w

ith

54

in

ves

tors

�In

to

tal,

ma

na

ge

me

nt

pre

se

nte

d t

o o

ver

113

in

ves

tors

, m

an

ag

ing

eq

uit

y a

sse

ts w

ort

h

mo

re t

ha

n U

S$1

tri

llio

n

�c

.$5

bil

lio

n w

ort

h o

f b

ids

rec

eiv

ed

, 16

tim

es

ove

rsu

bsc

rib

ed

�In

tern

ati

on

al

de

ma

nd

: c

.$4

bil

lio

n (

18x

ove

rsu

bsc

rib

ed

), d

em

an

d f

rom

149

fo

reig

n

inve

sto

rs�

Do

mes

tic

dem

an

d:

c.$

1 b

illi

on

(1

0x

ove

rsu

bs

cri

be

d),

de

ma

nd

fro

m 1

8,4

28

do

mes

tic

in

ves

tors

Off

er

Siz

e

IPO

Pri

ce

Ro

ad

sh

ow

Rece

pti

on

fro

m

inve

sto

rs

Off

er

Str

uc

ture

Lis

tin

g

�18

.4%

fre

e f

loa

tin

clu

din

g o

ver

all

otm

en

t�

Mix

of

25

% p

rim

ary

an

d 7

5%

sec

on

da

ry s

ha

res

�$3

20m

off

er

wit

h a

MC

ap

of

$1

,740m

11

LO

DO

CS

1 -

#172

131v14

/11

Air

po

rt P

laye

r S

eg

me

nta

tio

nA

irp

ort

Pla

ye

r S

eg

me

nta

tio

nP

laye

rs m

anagin

g/o

wnin

g a

irport

s inte

rnationally

need to h

ave

both

str

ong fin

ancia

l re

sourc

es a

nd

esta

blis

hed c

redib

ility

Air

po

rt O

pera

tor

Seg

men

tati

on

Matr

ixA

irp

ort

Op

era

tor

Seg

men

tati

on

Matr

ix

Hig

h

Lo

w

Esta

blis

hed

C

red

ibil

ity

Hig

hly

Lim

ited

Sig

nif

ican

t P

ote

nti

al

Fin

an

cia

l R

eso

urc

es

Source :Exambela Consulting / UK

Financial Institutions

Goldman Sachs,ABN Amro,

Deutche Bank,etc..

Van-

couver

Changi

Vienna Schiphol

Vinci

Alterra

ADP

Fraport

Macquarie

Airports

Ferrovial

Hoctief

nice

TAV

12

LO

DO

CS

1 -

#172

131v14

/12

TAV ISTANBUL

TAV ISTANBUL

TAV ISTANBUL

TAV ANATOLIA

TAV ANATOLIA

TAV ANATOLIA

TAV IZMIR

TAV IZMIR

TAV IZMIR

TAV GEORGIA,

TBILISI

TAV GEORGIA,

TAV GEORGIA,

TBILISI

TBILISI

BTA FOOD &

BEVARAGE

BTA FOOD &

BTA FOOD &

BEVARAGE

BEVARAGE

HAVAS GROUND

HANDLING

HAVAS GROUND

HAVAS GROUND

HANDLING

HANDLING

TAV SECURITY

TAV SECURITY

TAV SECURITY

TAV IT

TAV IT

TAV IT

TAV O&M

TAV O&M

TAV O&M

ATU DUTY FREE

ATU DUTY FREE

ATU DUTY FREE

TAV AIRPORTS

HOLDING

TAV

TAV AIRPORTS

AIRPORTS

HOLD

HOLDII NG

NG

TAV GEORGIA,

BATUMI

TAV GEORGIA,

TAV GEORGIA,

BATUMI

BATUMI

TAV TUNISIE,

MONASTIR

TAV TUNISIE,

TAV TUNISIE,

MONASTIR

MONASTIR

TAV TUNISIE,

ENFIDHA

TAV TUNISIE,

TAV TUNISIE,

ENFIDHA

ENFIDHA

TAV CONSTRUCTION

TAV

TAV CONSTRUCTION

CONSTRUCTION

TAV CAIRO

TAV CAIRO

TAV CAIRO

TAV QATAR

TAV QATAR

TAV QATAR

TAV ENFIDHA

TAV ENFIDHA

TAV ENFIDHA

TAV BATUMI

TAV BATUMI

TAV BATUMI

TAV DUBAI

TAV DUBAI

TAV DUBAI

“On

e S

top

Sh

op

So

luti

on

s ”

TAV LIBYA

TAV LIBYA

TAV LIBYA

11.000 EMPLOYEES

TAV AIRPORTS

11.000 EMPLOYEES

11.000 EMPLOYEES

TAV AIRPORTS

TAV AIRPORTS

6.000 EMPLOYESS

TAV CONSTRUCTION

6.000 EMPLOYESS

6.000 EMPLOYESS

TAV CONSTRUCTION

TAV CONSTRUCTION

TA

V T

UN

ISIA

SA

Op

era

tio

n o

f H

ab

ib

Bu

rgib

a

Inte

rna

tio

nal

Air

po

rt

Co

nstr

uc

tio

nan

d

Op

era

tio

n o

f th

e Z

ine

El

Ab

idin

eB

en

Ali

En

fid

ha

Inte

rna

tio

nal

Air

po

rt

Bo

th

co

ncessio

ns

are

fo

r p

eri

od

o

f 40 y

ears

b

eg

inn

ing

fr

om

th

e d

ate

o

f sig

nin

g

Th

e

co

ncessio

n

ag

reem

en

t is

b

ased

on

re

ven

ue

sh

ari

ng

an

d

investm

en

t fo

r th

e b

oth

air

po

rts

14

LO

DO

CS

1 -

#172

131v14

/14

Mis

sio

nT

o C

reate

th

e m

ost

ad

van

ced

air

po

rt in

th

e r

eg

ion

fro

m a

Gre

en

field

are

a t

o in

cre

ase p

assen

ger

nu

mb

ers

an

d s

erv

ice level fo

r air

lin

es, p

assen

gers

an

d e

mp

loye

es

wit

h t

he u

tmo

st

att

en

tio

n t

o t

he

en

vir

on

men

t an

d h

um

an

rig

hts

wh

ile g

en

era

tin

g d

irect

an

d a

dd

ed

valu

e t

o t

he T

un

isia

n E

co

no

my

Vis

ion

To

Gen

era

te t

he b

igg

est

Air

po

rt H

ub

in

th

e r

eg

ion

to

serv

e n

ot

on

ly f

or

Tu

nis

ia b

ut

all A

fric

a a

nd

S

ou

thern

Eu

rop

e b

y co

nn

ecti

ng

all C

on

tin

en

ts t

o E

nfi

dh

a w

ith

th

em

ost

ad

van

ced

avia

tio

n

sta

nd

ard

s a

nd

tech

no

log

y an

d m

ake t

he T

un

isia

on

e o

f th

e b

est

Med

iate

rran

ain

desti

nati

on

fo

r W

orl

dw

ide T

ravele

rs

TU

NIS

IA

15

LO

DO

CS

1 -

#172

131v14

/15

�During the next plan (2007-2011), Tunisia's economy should witness an

annual growth rate of 6%, compared to 4,5% from 2001 to 2006.

�The 2007 Davos W

orld Economic Forum Report ranks Tunisia first in Africa

and second in the Arab W

orld after Dubai , in term

s of tourist and travel

competitiveness.

�The report, which is based on the basis of three m

ain criteria: business

environment, human and natural resources and the quality of political

reform

s undertaken, also writes that Tunisia ranks 34 th in the world

insofar as its travel and tourist competitiveness are concerned.Tunisia

comes ahead of Turkey (52 nd ), Thailand (43 rd ) and Morocco (57 th ).

�Tunisia 's which is also one of the m

ajor destinations in the world when it

comes to health and spa tourism, has recently launched in a significant

upgrading effort of its hotels and services. More than 6 m

illiontourists visit

the country each year, m

aking it one of the top Mediterranean

destinations.

16

LO

DO

CS

1 -

#172

131v14

/16