target corporation financial valuation

TRANSCRIPT

/Users/dianacolgrove/Desktop/50.png

TARGET

Financial Valuation

Overview

Background

Comparables

Pro Formas

Sensitivity Analysis

Conclusion & Recommendation

Background

Started as Dayton Dry Goods: 1902First Target store 1962“Tar-Zhay”Target.direct366,000 Worldwide Team Members

Massive Data Breach

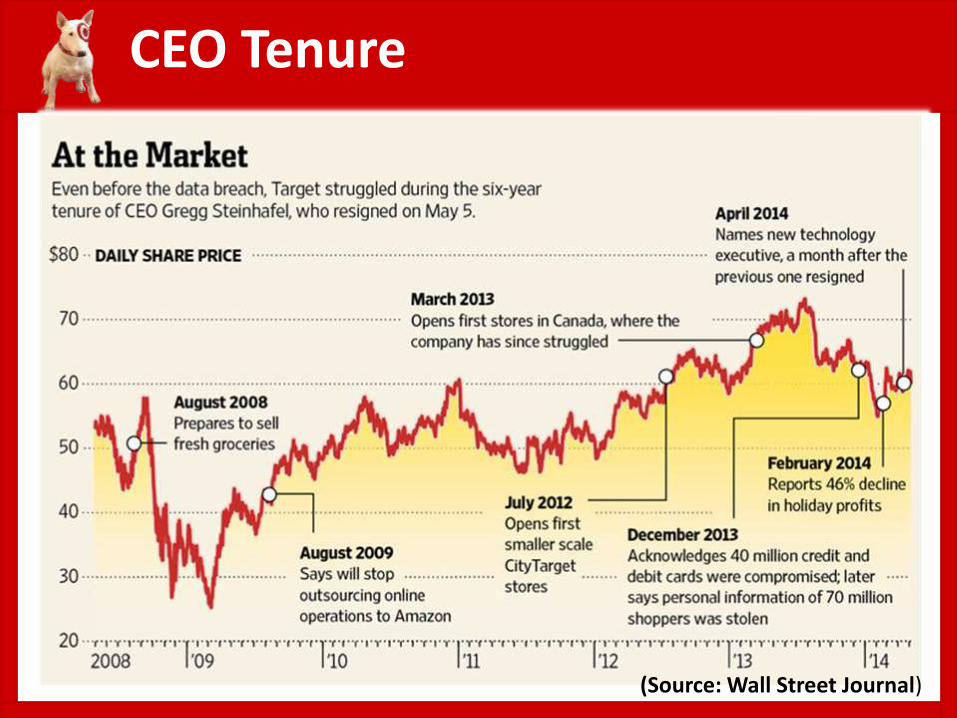

CEO Tenure

(Source: Wall Street Journal)

Comparables

Market Cap P/E P/S EPS

Net Income

Share Price

Target (TGT) 37.44B 19.26 0.51 4.52 1.14B $62.79

Walmart (WMT) 255.75B 16.1 0.53 4.88 15.88B $79.20

Amazon (AMZN) 134.48B 488.68 1.7 0.64 300.00M $292.24

Dollar General

(DG) 17.80B 17.9 1.1 3.17 1.03B $56.75

Industry 28.54M 17.3 0.06 3.17 6.36B $50.29

Comparables

$0.00

$50.00

$100.00

$150.00

$200.00

$250.00

$300.00

$350.00

$400.00

2010 2011 2012 2013Target $55.77 $48.53 $57.35 $62.79

Walmart $54.07 $59.76 $68.23 $78.69

Amazon $180.00 $173.10 $250.87 $398.79

Dollar General $30.67 $41.14 $44.01 $60.32

Share Prices 2010-2013

2010 2011 2012 2013

TGT 3.3 4 4.28 4.52

WMT 3.71 4.47 4.54 5.02

AMZN 1.37 2.53 -0.09 0.59

DG 1.04 1.82 2.22 2.85

EPS

Comparables

AMZN

DG

TGT

(Source: EDGAR Online)

Growth Rate & Tax Rate

From To Growth Rate Tax Rate

2013 2014 2.12 % 36.48 %

2014 2015 2.42 % 36.48 %

2015 2016 2.72 % 36.48 %

2016 2017 3.02 % 36.48%

2017 2018 3.32 % 36.48%

Long-Term Growth 3.60 %

WACC

Risk-free Interest Rate 3.54 %

Market Return 10.00 %

Market Risk Premium 6.46 %

Beta 0.9

Cost of Equity 9.35 %

Equity 38.83B

Debt 13.78B

Cost of Debt 4.69 %

Tax Rate 36.48 %

WACC 7.68 %

Income Statement 2013

Income Statement ($000s) Year: 2013 % Sales

Total Sales (Sale + Credit Sale) 73,301,000 100%

COGS (Except Depreciation and Amortization) (53,160,000) 72.52%

Gross Profit 20,141,000.00 27.48%

Sale, Marketing and Administrative (14,984,000) 20.44%EBITDA

5,157,000 7.04%

Depreciation (2,223,000) 3.03%EBIT

2,934,000 4.00%

Interest Expense (net) (1,126,000) 1.54%

Pretax Income 1,808,000 2.47%

Income Tax (659,558.40) 0.90%

Net Income 1,148,442 1.57%

Balance Sheet 2013

Balance Sheet ($000s) Year:2013 % Sales

Assets

Cash and Equivalents 695,000 0.95%

Accounts Receivable - 0.00%

Inventories 8,766,000 11.96%

Other CA2,112,000 2.88%

Total Current Assets 11,573,000 15.79%

Prop, Plant & Equip 31,378,000 42.81%

Other LT Assets 1,602,000 2.19%

Total Assets 44,553,000 60.78%

Liabilities & Stockholders' Equity

Accounts Payable 11,617,000 15.85%

Other ST or LT Liabilities 2,923,000 3.99%

Debt 13,782,000 18.80%

Total Liabilities 28,322,000 38.64%

Stockholders' Equity 16,231,000 22.14%

Total Liabilities & Equity 44,553,000 60.78%

Plug

Year 2013 2014 2015 2016 2017 2018

Total Assets 44,553,000 45,497,524 46,598,564 47,866,045 49,311,599 50,948,744

Total Liab. & Shares before Plug 45,592,670 46,610,798 47,792,136 49,147,361 50,688,998

Plug (95,103) (12,234) 73,909 164,238 259,746

After 45,497,567 46,598,564 47,866,045 49,311,599 50,948,744

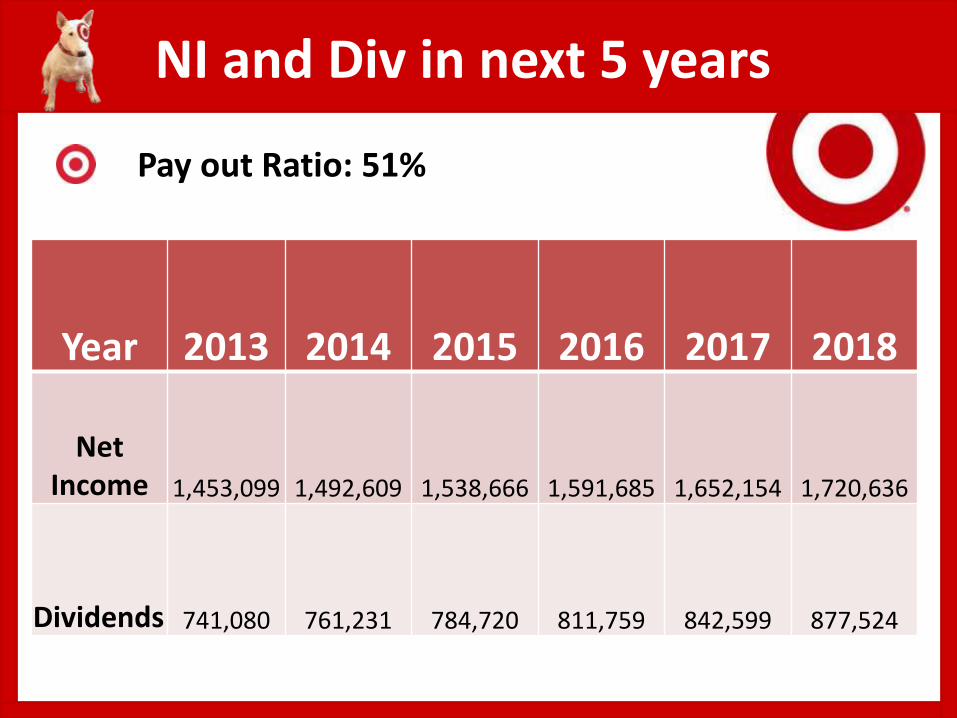

NI and Div in next 5 years

Year 2013 2014 2015 2016 2017 2018

Net Income 1,453,099 1,492,609 1,538,666 1,591,685 1,652,154 1,720,636

Dividends 741,080 761,231 784,720 811,759 842,599 877,524

Pay out Ratio: 51%

FCF & Intrinsic ValueTimeline 0 1 2 3 4 5 6

Year 2013 2014 2015 2016 2017 2018 2019

FCFs 4,901,428 5,123,078 5,367,645 5,637,514 5,935,376 6,149,049

PV of all FCFs $ 125,536,743 Time 0 Cash $ 695,000Time 0 Debt $ 13,782,000Intrinsic Market Cap $ 112,449,743 BilShares Outstanding $ 633,170 Mil Intrinsic Price/Share $ 177.60

Stock Price $ 59.13

% Higher 200%

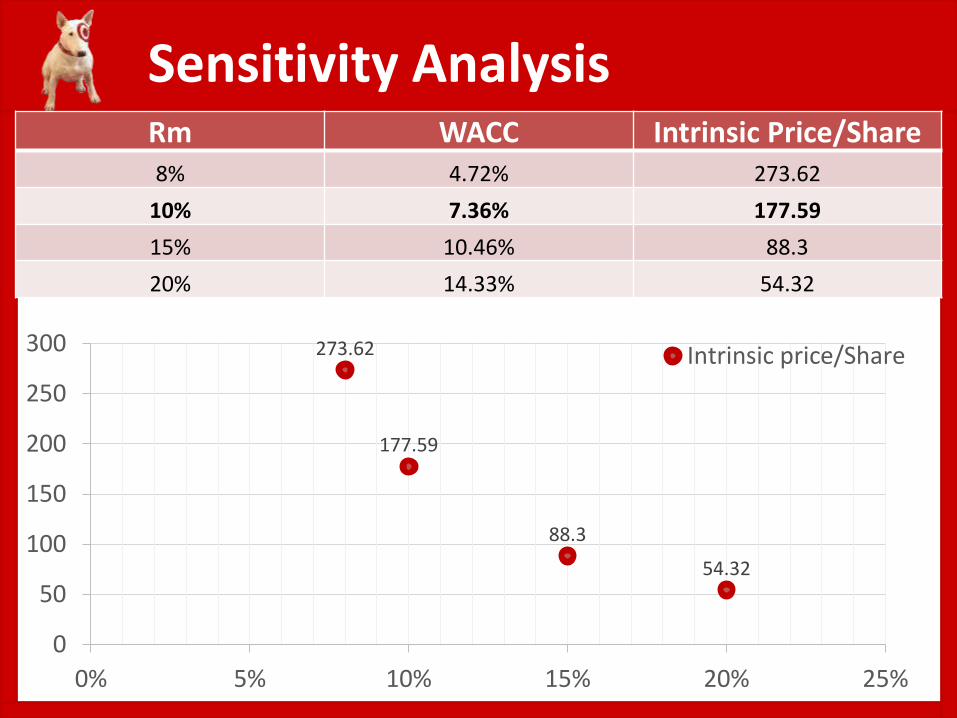

Sensitivity Analysis

273.62

177.59

88.3

54.32

0

50

100

150

200

250

300

0% 5% 10% 15% 20% 25%

Intrinsic price/Share

Rm WACC Intrinsic Price/Share8% 4.72% 273.62

10% 7.36% 177.59

15% 10.46% 88.3

20% 14.33% 54.32

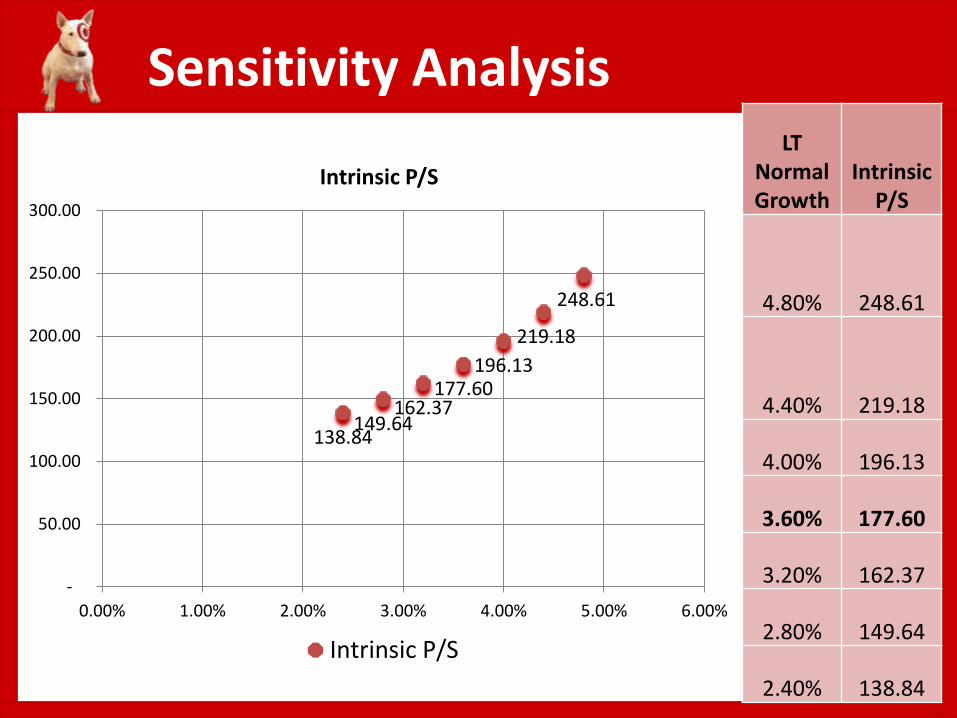

Sensitivity AnalysisLT

Normal Growth

Intrinsic P/S

4.80% 248.61

4.40% 219.18

4.00% 196.13

3.60% 177.60

3.20% 162.37

2.80% 149.64

2.40% 138.84

248.61

219.18

196.13177.60

162.37149.64

138.84

-

50.00

100.00

150.00

200.00

250.00

300.00

0.00% 1.00% 2.00% 3.00% 4.00% 5.00% 6.00%

Intrinsic P/S

Intrinsic P/S

Sensitivity Analysis

Beta WACCIntrinsic

Price/Share1.1 8.64% 139.901.0 8.16% 156.780.9 7.68% 177.600.8 7.21% 203.920.7 8.06% 238.27

273.62

177.59

88.3054.32

0.00

50.00

100.00

150.00

200.00

250.00

300.00

0% 5% 10% 15% 20% 25%

Intrinsic Price/Share

Intrinsic price/Share

Sensitivity Analysis

Years30-year Treasury

yield WACCIntrinsic

Price/Share2000 6.23% 7.88% 168.372010 4.69% 7.77% 173.542014 3.54% 7.68% 177.6

Undervalued

Focus on Online Market

Expand Global Business

Conclusion & Recommendations

Questions?