tale of two spains

TRANSCRIPT

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 1/70

Spain 2010

What are the markets waiting for?

Marisa Mazo, CFAHead of Strategy & Research

[email protected], 2010

Ahorro Corporación Financiera, S.V., S.A. See important disclosure on the last two pages of this document Ahorro Corporación Financiera, S.V., S.A. See important disclosure on the last two pages of this document

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 2/70

June, 2010

Index

Spain: The recession continues

Spain, at a glance.

Worst is over ut...

Main problems (and challenges) of the Spanish economy.

External sector: restoring competitiveness a must.

mp oymen .: wa ng or a our mar e re orm.

Budget deficit: additional measures in the pipeline?

Suffering from public debt.

.

The financial sector.

Annex.

Ahorro Corporación Financiera, S.V., S.A. 2

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 3/70

June, 2010

Spain (I): Recession continues in 2010.

Spanish GDP may decline by –0.9% in 2010e, after the –3.6% drop in 2009. Positive rates are expected 2011eonwards. However,

’

The new problems:

Unemployment rate: 20.8% by 2011e. Bud et deficit: –9.8% in 2010e.

The everlasting weaknesses:

Current account deficit: how to reduce it to under –4.0%?

Excessive reliance on the residential construction sector: despite the crisis, still c. 6.0% of GDP in 2010e.

Restoring competitiveness: “THE” challenge Are politicians willing to implement structural reforms?

Short-term reforms:

Reduce companies’ overall taxation

Labour reform

Medium-term reforms:

Energy sector.

Distribution of competences among the different public administrations.

Ahorro Corporación Financiera, S.V., S.A. 3

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 4/70

June, 2010

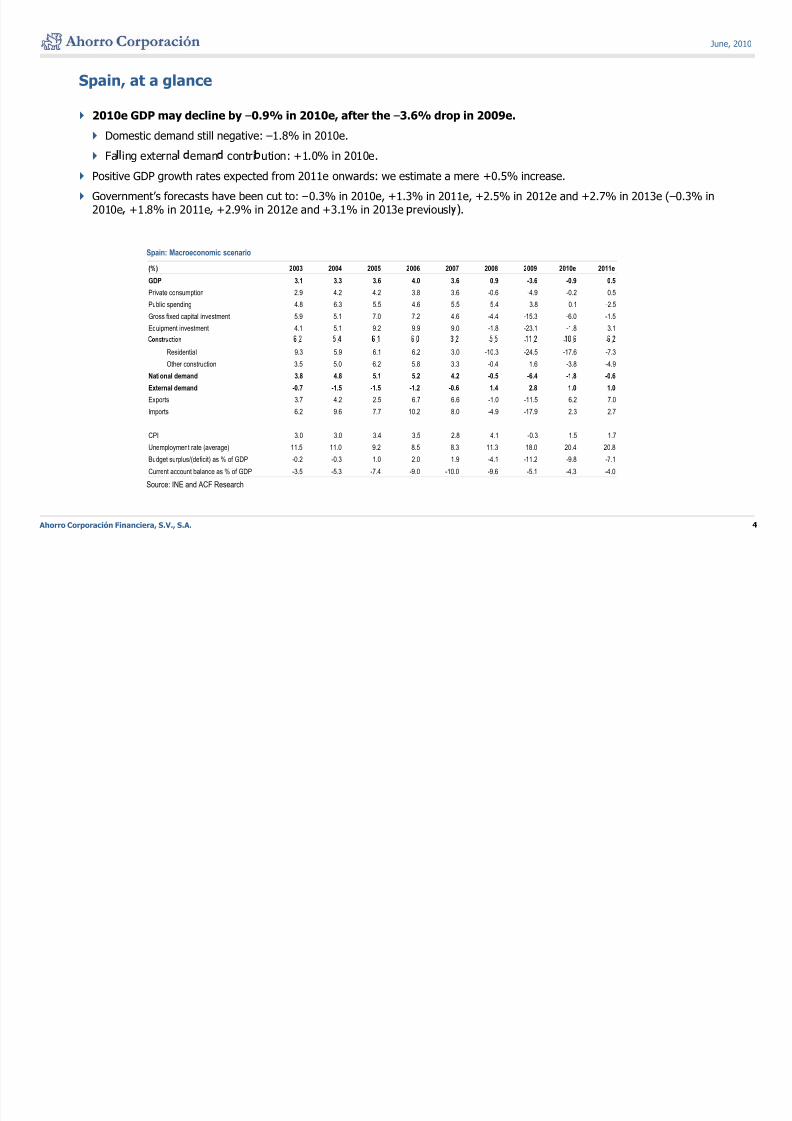

Spain, at a glance

2010e GDP may decline by –0.9% in 2010e, after the –3.6% drop in 2009e.

Domestic demand still negative: –1.8% in 2010e.

Fa ing externa eman contri ution: +1.0% in 2010e.

Positive GDP growth rates expected from 2011e onwards: we estimate a mere +0.5% increase.

Government’s forecasts have been cut to: –0.3% in 2010e, +1.3% in 2011e, +2.5% in 2012e and +2.7% in 2013e (–0.3% in2010e +1.8% in 2011e +2.9% in 2012e and +3.1% in 2013e reviousl .

Spain: Macroeconomic scenario

(%) 2003 2004 2005 2006 2007 2008 2009 2010e 2011e

GDP 3.1 3.3 3.6 4.0 3.6 0.9 -3.6 -0.9 0.5

Private consumption 2.9 4.2 4.2 3.8 3.6 -0.6 -4.9 -0.2 0.5Public spending 4.8 6.3 5.5 4.6 5.5 5.4 3.8 0.1 -2.5

Gross fixed capital investment 5.9 5.1 7.0 7.2 4.6 -4.4 -15.3 -6.0 -1.5

Equipment investment 4.1 5.1 9.2 9.9 9.0 -1.8 -23.1 -1.8 3.1

- - - -. . . . . . . . .

Residential 9.3 5.9 6.1 6.2 3.0 -10.3 -24.5 -17.6 -7.3

Other construction 3.5 5.0 6.2 5.8 3.3 -0.4 1.6 -3.8 -4.9

National demand 3.8 4.8 5.1 5.2 4.2 -0.5 -6.4 -1.8 -0.6

External demand -0.7 -1.5 -1.5 -1.2 -0.6 1.4 2.8 1.0 1.0Exports 3.7 4.2 2.5 6.7 6.6 -1.0 -11.5 6.2 7.0

Imports 6.2 9.6 7.7 10.2 8.0 -4.9 -17.9 2.3 2.7

CPI 3.0 3.0 3.4 3.5 2.8 4.1 -0.3 1.5 1.7

Unemployment rate (average) 11.5 11.0 9.2 8.5 8.3 11.3 18.0 20.4 20.8

Budget surplus/(deficit) as % of GDP -0.2 -0.3 1.0 2.0 1.9 -4.1 -11.2 -9.8 -7.1

Ahorro Corporación Financiera, S.V., S.A. 4

Source: INE and ACF Research

Current account balance as % of GDP -3.5 -5.3 -7.4 -9.0 -10.0 -9.6 -5.1 -4.3 -4.0

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 5/70

June, 2010

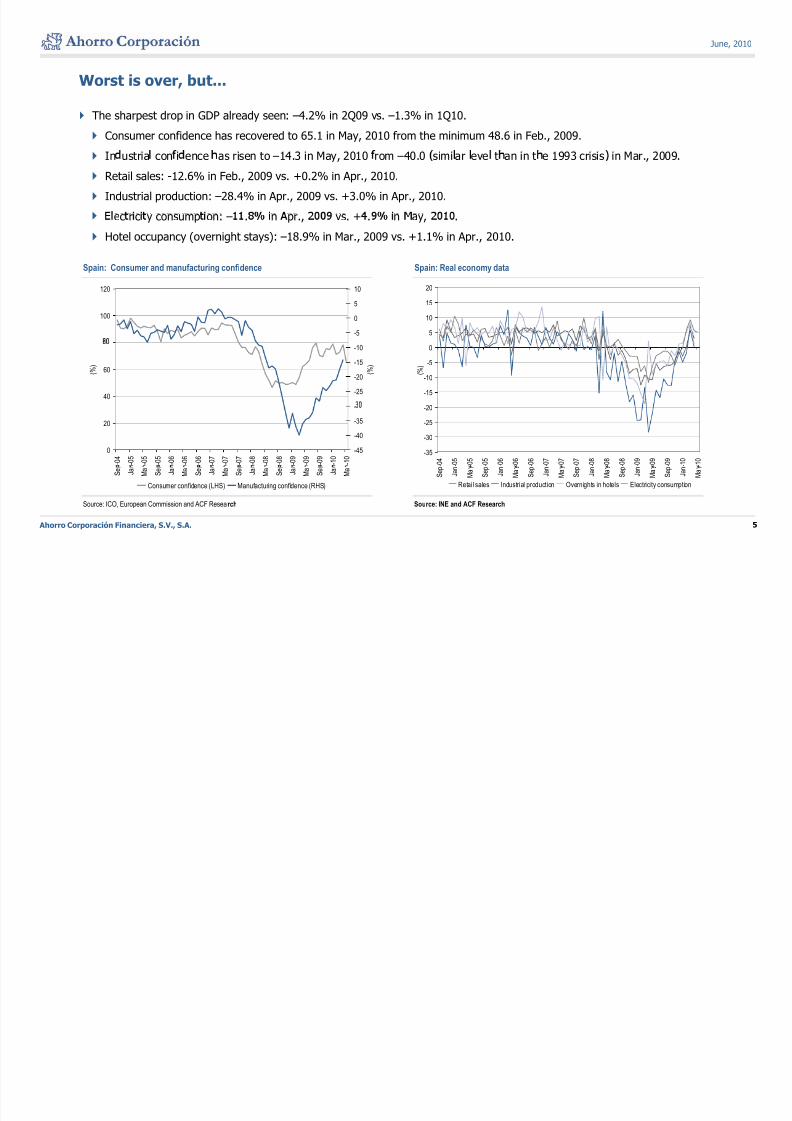

Worst is over, but...

The sharpest drop in GDP already seen: –4.2% in 2Q09 vs. –1.3% in 1Q10.

Consumer confidence has recovered to 65.1 in May, 2010 from the minimum 48.6 in Feb., 2009.

In ustria con i ence as risen to –14.3 in May, 2010 rom –40.0 simi ar eve t an in t e 1993 crisis in Mar., 2009.

Retail sales: -12.6% in Feb., 2009 vs. +0.2% in Apr., 2010.

Industrial production: –28.4% in Apr., 2009 vs. +3.0% in Apr., 2010.

ec r c y consump on: – . n pr., vs. + . n ay, .

Hotel occupancy (overnight stays): –18.9% in Mar., 2009 vs. +1.1% in Apr., 2010.

Spain: Consumer and manufacturing confidence Spain: Real economy data

100

120

-5

0

5

10

5

10

15

20

40

60 ( % )

-25

-20

-15

-10

( % )

-15

-10

-5

0

( % )

0

20

- 0 4

- 0 5

y - 0

5 - 0

5 - 0

6

y - 0

6 - 0

6 - 0

7

y - 0

7 - 0

7 - 0

8

y - 0

8 - 0

8 - 0

9

y - 0

9 - 0

9 - 1

0

y - 1

0-45

-40

-35

-

-35

-30

-25

-20

- 0 4

- 0 5

- 0 5

- 0 5

- 0 6

- 0 6

- 0 6

- 0 7

- 0 7

- 0 7

- 0 8

- 0 8

- 0 8

- 0 9

- 0 9

- 0 9

- 1 0

- 1 0

Ahorro Corporación Financiera, S.V., S.A. 5

Source: ICO, European Commission and ACF Research Source: INE and ACF Research

S e

J a

M a

S e

J a

M a

S e

J a

M a

S e

J a

M a

S e

J a

M a

S e

J a

M a

Consumer confidence (LHS) Manufacturing confidence (RHS)

S e p

J a n

M a

S e p

J a n

M a

S e p

J a n

M a

S e p

J a n

M a

S e p

J a n

M a

S e p

J a n

M a

Retail sales Industrial production Overnights in hotels Electricity consumption

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 6/70

June, 2010

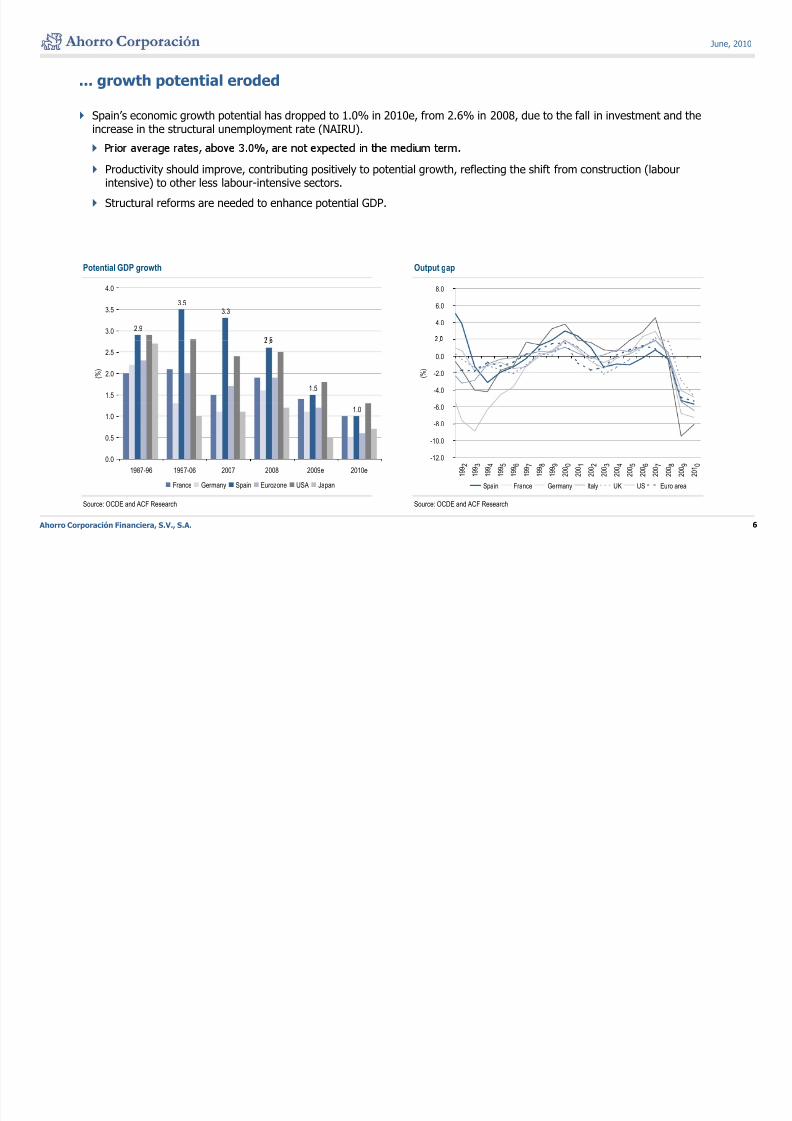

... growth potential eroded

Spain’s economic growth potential has dropped to 1.0% in 2010e, from 2.6% in 2008, due to the fall in investment and theincrease in the structural unemployment rate (NAIRU).

Productivity should improve, contributing positively to potential growth, reflecting the shift from construction (labourintensive) to other less labour-intensive sectors.

Structural reforms are needed to enhance potential GDP.

Potential GDP growth Output gap

4.0

6.0

8.0

2.9

3.53.3

3.0

3.5

4.0

-4.0

-2.0

0.0

.

( % )

.

1.51.5

2.0

2.5

( % )

-12.0

-10.0

-8.0

-6.0

2 3 4 5 6 7 8 9 0 1 2 3 4 5 6 7 8 9 0

1.0

0.0

0.5

1.0

Ahorro Corporación Financiera, S.V., S.A. 6

Source: OCDE and ACF Research Source: OCDE and ACF Research

1 9 9

1 9 9

1 9 9

1 9 9

1 9 9

1 9 9

1 9 9

1 9 9

2 0 0

2 0 0

2 0 0

2 0 0

2 0 0

2 0 0

2 0 0

2 0 0

2 0 0

2 0 0

2 0 1

Spain France Germany Italy UK US Euro area

1987-96 1997-06 2007 2008 2009e 2010e

France Germany Spain Eurozone USA Japan

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 7/70

June, 2010

Main problems (and challenges) in 2010e onwards.

The main threats that the Spanish economy was facing in 2007 are now our main problems:

The high current account deficit and, consequently, massive external financing needs.

A t oug iminis ing, it may sti represent some 3.0%-4.0% o GDP, me ium term.

Net external investment position already accounts for –91% of GDP.

Key challenge: restore the competitiveness of Spanish companies.

xcess ve epen ence on e res en a cons ruc on sec or.

In spite of the crisis, the sector still represents c. 6.0% of GDP in 2010e.

Key challenge: the stabilisation of the sector at a sustainable “cruising speed”.

- .

0.27Mn jobs to be destroyed in 2010e, totalling, c. 2.0Mn since 2008. Unemployment rate may reach 20.8% in 2011e.

The dual economy: the employed (fixed contracts) and the unemployed (temporary labour contracts).

Ke challen e: reform of the labour market.

Budget deficit: from a 2.3% surplus in 2007 to a -9.8% deficit in 2010e (-11.2% in 2009).

Public debt would represent 66% of GDP in 2010e vs. 36% in 2007. Risk of ratings downgrades.

Key challenge: looking for sustainability.

Are politicians willing to implement structural reforms?

Ahorro Corporación Financiera, S.V., S.A. 7

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 8/70

June, 2010

Spanish medium-term challenges

Restoring competitiveness to reduce external leverage is the main challenge that the Spanish economy is facing:

We lack the devaluation option.

Feasi e measures:

Short term: reduce the corporate tax or the employer social security contribution and control labour costs.

Medium term: structural changes (energy, service sector, R&D, education).

40

45Empoyer social security contribution

VAT

(%)

10

12

14

US JapanEUM Germany

(%)

Taxes: International comparisonUnit labour costs: International comparison

15

20

25

30

Corporate tax rate

0

2

4

6

8Spain

0

5

10

m a n y

u s t r i a

l g i u m

S p a i n

i n l a n d

r a n c e

r e e c e

r l a n d s

n g a r y

r e l a n d

I t a l y

o l a n d

r t u g a l

U K

e d e n

-6

-4

-2

1 9 8 1

1 9 8 2

1 9 8 3

1 9 8 4

1 9 8 5

1 9 8 6

1 9 8 7

1 9 8 8

1 9 8 9

1 9 9 0

1 9 9 1

1 9 9 2

1 9 9 3

1 9 9 4

1 9 9 5

1 9 9 6

1 9 9 7

1 9 9 8

1 9 9 9

2 0 0 0

2 0 0 1

2 0 0 2

2 0 0 3

2 0 0 4

2 0 0 5

2 0 0 6

2 0 0 7

2 0 0 8

Ahorro Corporación Financiera, S.V., S.A. 8

G e B

N e t h e

H u I

P S

Source: Eurostat and ACF ResearchSource: Eurostat, and ACF Research

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 9/70

June, 2010

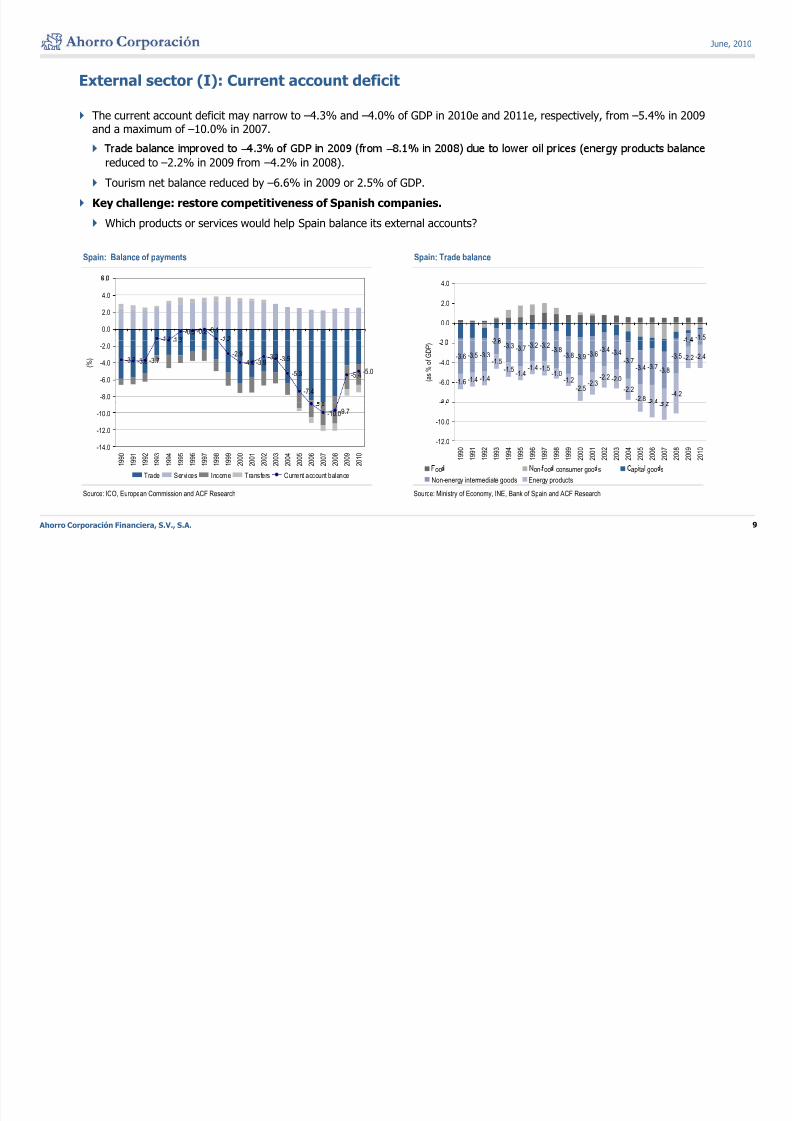

External sector (I): Current account deficit

The current account deficit may narrow to –4.3% and –4.0% of GDP in 2010e and 2011e, respectively, from –5.4% in 2009and a maximum of –10.0% in 2007.

– – reduced to –2.2% in 2009 from –4.2% in 2008).

Tourism net balance reduced by –6.6% in 2009 or 2.5% of GDP.

Key challenge: restore competitiveness of Spanish companies.

Which products or services would help Spain balance its external accounts?

Spain: Balance of payments Spain: Trade balance

-1.1 -

-0.3 -0.2 -0.1

-1 2

0.0

2.0

4.0

.

- -1.5

0.0

2.0

4.0

-3.7 -3.8 -3.7

. - . .

-2.9

-4.0 -3.9-3.3 -3.5

-5.3

-7.4

-5.4-5.0

-8.0

-6.0

-4.0

-2.0

( % ) -3.6 -3.5 -3.3

- .-3.3 -3.7 -3.2 -3.2

-3.8-3.8 -3.9 -3.6

-3.4 -3.4-3.7

-3.4 -3.7-3.8

-3.5

- .

-1.6 -1.4 -1.4

-1.5-1.5

-1.4-1.4 -1.5

-1.0-1.2

-2.5

-2.3-2.2 -2.0

-2.2-2.8 -3.4

-4.2

-2.2 -2.4

-8 0

-6.0

-4.0

- .

( a s

% o

f G D P )

- .

-10.0-9.7

-14.0

-12.0

-10.0

1 9 9 0

1 9 9 1

1 9 9 2

1 9 9 3

1 9 9 4

1 9 9 5

1 9 9 6

1 9 9 7

1 9 9 8

1 9 9 9

2 0 0 0

2 0 0 1

2 0 0 2

2 0 0 3

2 0 0 4

2 0 0 5

2 0 0 6

2 0 0 7

2 0 0 8

2 0 0 9

2 0 1 0

. - .

-12.0

-10.0

.

1 9 9 0

1 9 9 1

1 9 9 2

1 9 9 3

1 9 9 4

1 9 9 5

1 9 9 6

1 9 9 7

1 9 9 8

1 9 9 9

2 0 0 0

2 0 0 1

2 0 0 2

2 0 0 3

2 0 0 4

2 0 0 5

2 0 0 6

2 0 0 7

2 0 0 8

2 0 0 9

2 0 1 0

Ahorro Corporación Financiera, S.V., S.A. 9

Source: ICO, European Commission and ACF Research Source: Ministry of Economy, INE, Bank of Spain and ACF Research

Trade Services Income Transfers Current account balanceoo on- oo consumer goo s ap ta goo s

Non-energy intermediate goods Energy products

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 10/70

June, 2010

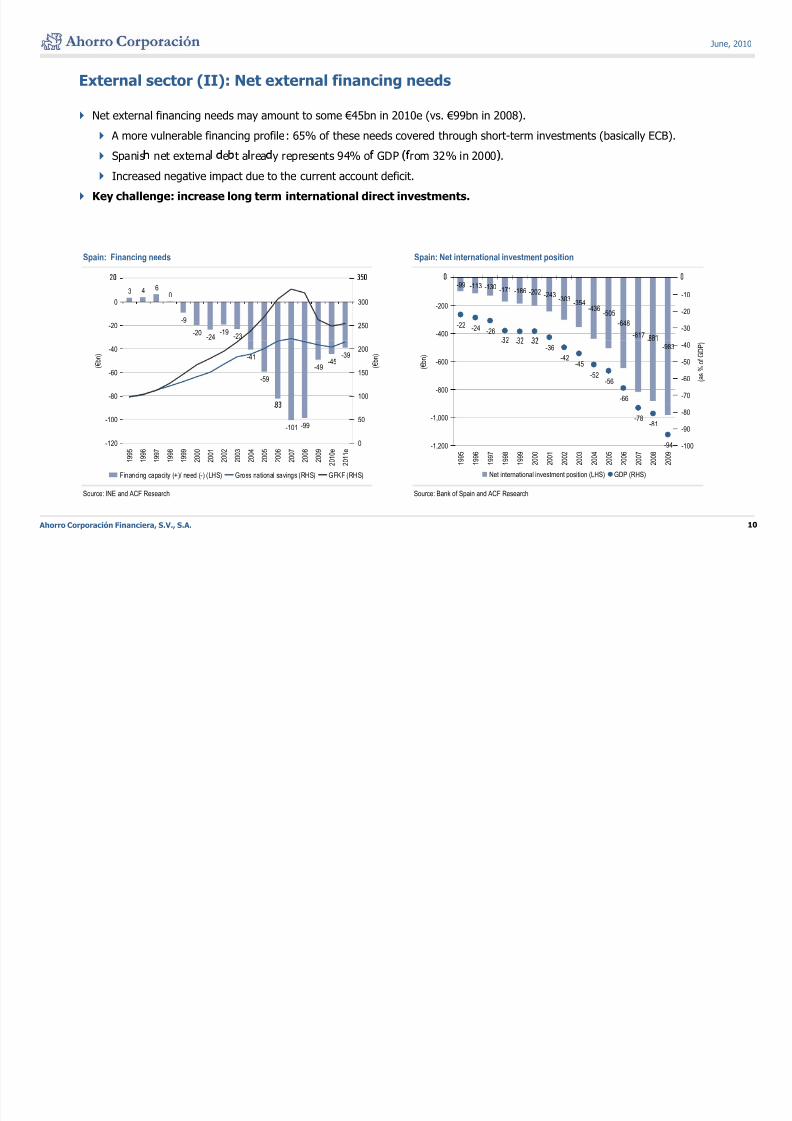

External sector (II): Net external financing needs

Net external financing needs may amount to some €45bn in 2010e (vs. €99bn in 2008).

A more vulnerable financing profile: 65% of these needs covered through short-term investments (basically ECB).

Spanis net externa e t a rea y represents 94% o GDP rom 32% in 2000 .

Increased negative impact due to the current account deficit.

Key challenge: increase long term international direct investments.

Spain: Financing needs Spain: Net international investment position

3 4

6

0

-9

-20-24

-19-23

-20

0

250

300

-99 -113 -130 -171-186 -202 -243 -303

-354-436

-505

-648

-817-

-22 -24 -26-400

-200

-30

-20

-10

-41

-59

-49-45

-39

-80

-60

-40

( € b n

)

100

150

200

( € b n

)

-983- - -

-36

-42-45

-52-56

-66-800

-600 ( € b n )

-70

-60

-50

-40

( a s %

o f G D P )

-

-101 -99

-120

-100

1 9 9 5

1 9 9 6

1 9 9 7

1 9 9 8

1 9 9 9

2 0 0 0

2 0 0 1

2 0 0 2

2 0 0 3

2 0 0 4

2 0 0 5

2 0 0 6

2 0 0 7

2 0 0 8

2 0 0 9

2 0 1 0 e

2 0 1 1 e

0

50 -78-81

-94-1,200

-1,000

1 9 9 5

1 9 9 6

1 9 9 7

1 9 9 8

1 9 9 9

2 0 0 0

2 0 0 1

2 0 0 2

2 0 0 3

2 0 0 4

2 0 0 5

2 0 0 6

2 0 0 7

2 0 0 8

2 0 0 9

-100

-90

-80

Ahorro Corporación Financiera, S.V., S.A. 10

Source: INE and ACF Research Source: Bank of Spain and ACF Research

Financing capacity (+)/ need (-) (LHS) Gross national savings (RHS) GFKF (RHS) Net international investment position (LHS) GDP (RHS)

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 11/70

June, 2010

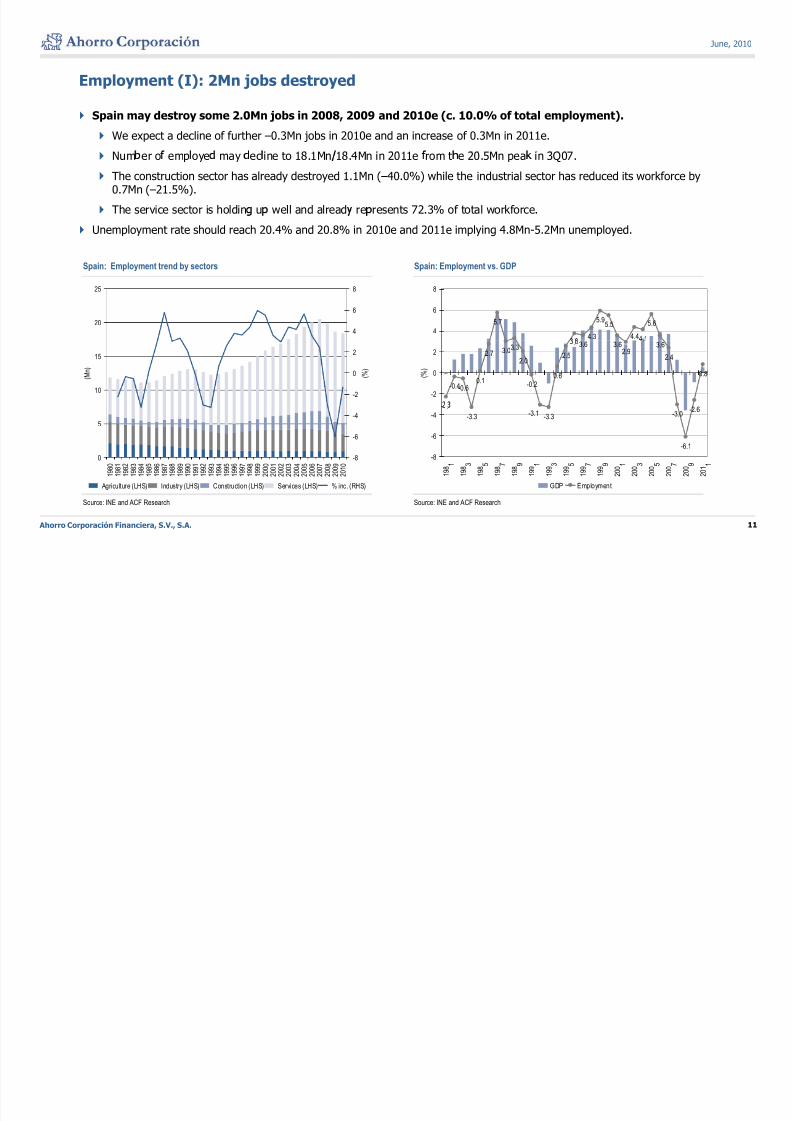

Employment (I): 2Mn jobs destroyed

Spain may destroy some 2.0Mn jobs in 2008, 2009 and 2010e (c. 10.0% of total employment).

We expect a decline of further –0.3Mn jobs in 2010e and an increase of 0.3Mn in 2011e.

Num er o emp oye may ec ine to 18.1Mn 18.4Mn in 2011e rom t e 20.5Mn pea in 3Q07.

The construction sector has already destroyed 1.1Mn (–40.0%) while the industrial sector has reduced its workforce by0.7Mn (–21.5%).

The service sector is holdin u well and alread re resents 72.3% of total workforce.

Unemployment rate should reach 20.4% and 20.8% in 2010e and 2011e implying 4.8Mn-5.2Mn unemployed.

Spain: Employment trend by sectors Spain: Employment vs. GDP

5.7

4.3

5.95.5

4.44.1

5.64

6

8

20

25

4

6

8

-0.4-0.60.1

2.7 3.03.3

2.0

-0.20.6

2.5

. 3.6 3.62.9

.3.6

2.4

0.8

-2

0

2

( % )

10

15

( M n

)

-2

0

2

( % )

- .

-3.3 -3.3 -3.0

-6.1

-2.6-3.1

-8

-6

-4

1 3 5 7 9 1 3 5 7 9 1 3 5 7 9 10

5

0 1 2 3 4 5 6 7 8 9 0 1 2 3 4 5 6 7 8 9 0 1 2 3 4 5 6 7 8 9 0-8

-6

-4

Ahorro Corporación Financiera, S.V., S.A. 11

Source: INE and ACF Research Source: INE and ACF Research

1 9 8

1 9 8

1 9 8

1 9 8

1 9 8

1 9 9

1 9 9

1 9 9

1 9 9

1 9 9

2 0 0

2 0 0

2 0 0

2 0 0

2 0 0

2 0 1

GDP Employment

1 9 8

1 9 8

1 9 8

1 9 8

1 9 8

1 9 8

1 9 8

1 9 8

1 9 8

1 9 8

1 9 9

1 9 9

1 9 9

1 9 9

1 9 9

1 9 9

1 9 9

1 9 9

1 9 9

1 9 9

2 0 0

2 0 0

2 0 0

2 0 0

2 0 0

2 0 0

2 0 0

2 0 0

2 0 0

2 0 0

2 0 1

Agriculture (LHS) Industry (LHS) Construction (LHS) Services (LHS) % inc. (RHS)

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 12/70

June, 2010

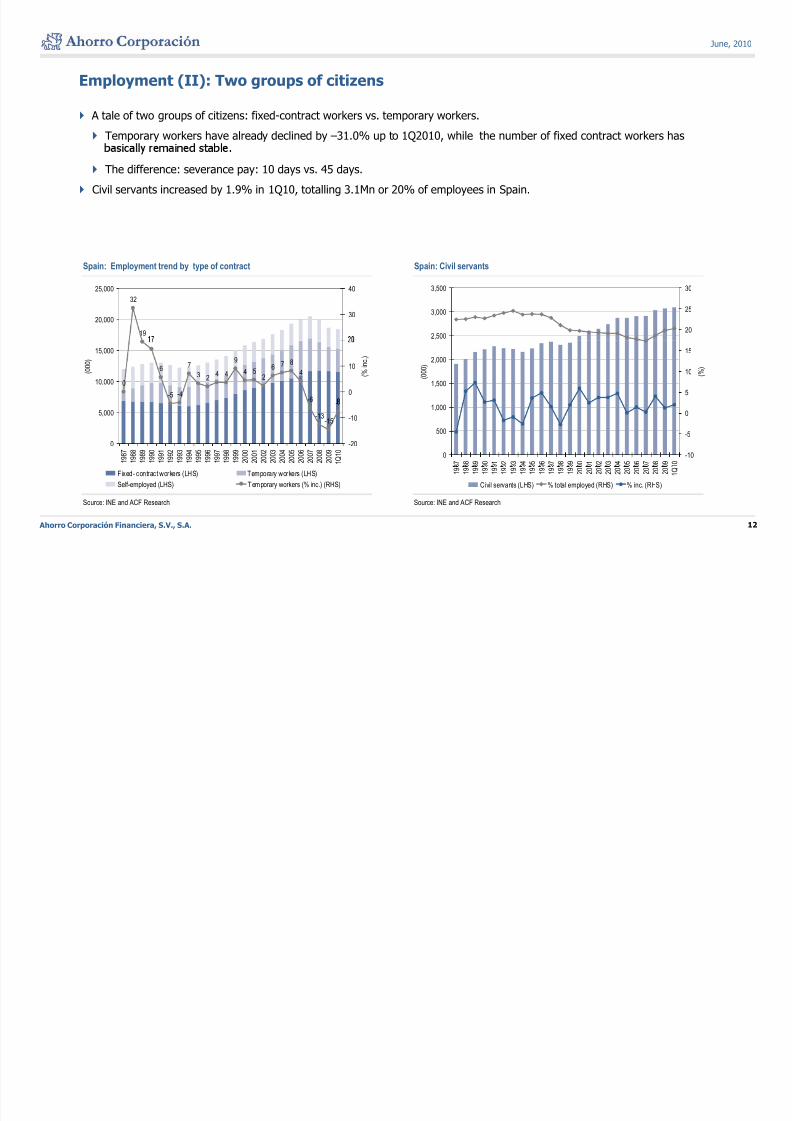

Employment (II): Two groups of citizens

A tale of two groups of citizens: fixed-contract workers vs. temporary workers.

Temporary workers have already declined by –31.0% up to 1Q2010, while the number of fixed contract workers has

The difference: severance pay: 10 days vs. 45 days.

Civil servants increased by 1.9% in 1Q10, totalling 3.1Mn or 20% of employees in Spain.

Spain: Employment trend by type of contract Spain: Civil servants

32

19

20,000

25,000

30

40

2,500

3,000

3,500

20

25

30

0

6

-5 -4

7

3 24 4

9

4 52

6 7 8

4

-6 -

10,000

15,000

( 0 0 0 )

0

10 ( %

i n c . )

1,500

2,000

( 0 0 0 )

5

10

15

( % )

-13-15

0

5,000

1 9 8 7

1 9 8 8

1 9 8 9

1 9 9 0

1 9 9 1

1 9 9 2

1 9 9 3

1 9 9 4

1 9 9 5

1 9 9 6

1 9 9 7

1 9 9 8

1 9 9 9

2 0 0 0

2 0 0 1

2 0 0 2

2 0 0 3

2 0 0 4

2 0 0 5

2 0 0 6

2 0 0 7

2 0 0 8

2 0 0 9

1 Q 1 0

-20

-10

0

500

1,000

8 7

8 8

8 9

9 0

9 1

9 2

9 3

9 4

9 5

9 6

9 7

9 8

9 9

0 0

0 1

0 2

0 3

0 4

0 5

0 6

0 7

0 8

0 9

1 0

-10

-5

0

Ahorro Corporación Financiera, S.V., S.A. 12

Source: INE and ACF Research Source: INE and ACF Research

Fixed- contract workers (LHS) Temporary workers (LHS)

Self-employed (LHS) Temporary workers (% inc.) (RHS)

1 9

1 9

1 9

1 9

1 9

1 9

1 9

1 9

1 9

1 9

1 9

1 9

1 9

2 0

2 0

2 0

2 0

2 0

2 0

2 0

2 0

2 0

2 0

1 Q

Civil servants (LHS) % total employed (RHS) % inc. (RHS)

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 13/70

June, 2010

Employment (III): The long awaited labour market reform

Trade unions and national business association(CEOE) to reach an agreement before the deadline date: June, 11th

(deadline pushed back twice).

Consensus is highly unlikely mainly because of differences on severance payment

Government draft to be approved by Royal-Decree next June, 16th (according to the press):

Severance a ment to be reduced from 45 to 20 da s if com anies have economic roblems currentl onl a lied tocompanies in the red).

The contract to promote employment , with just 33 days of severance payment, to be applied to all new contracts.

Penalize overuse of temporary contracts (limit short contracts to maximum 2 years).

Increase severance payment for subcontracts.

Promote part-time contracts (German model).

Set up a severance payment fund (Austrian model) which would pay 8 of the 33 days of severance pay for long-termcontracts.

If the Government approves this draft without consensus, trade unions will go on strike next June, 28th.

In our view, there are important elements that are not in this “ informal” proposal:

Collective agreements.

Social security costs: amongst the highest in Europe.

Linkage of salary increases to productivity instead of CPI.

Ahorro Corporación Financiera, S.V., S.A. 13

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 14/70

June, 2010

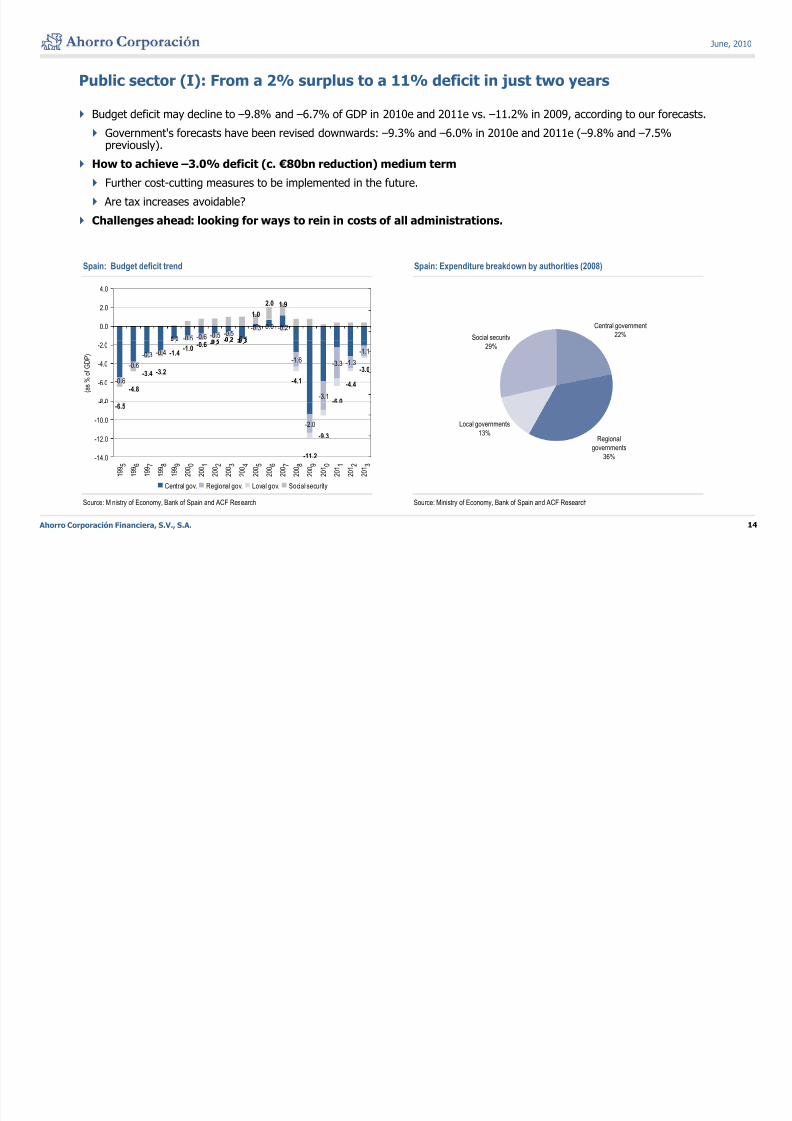

Public sector (I): From a 2% surplus to a 11% deficit in just two years

Budget deficit may decline to –9.8% and –6.7% of GDP in 2010e and 2011e vs. –11.2% in 2009, according to our forecasts.

Government's forecasts have been revised downwards: –9.3% and –6.0% in 2010e and 2011e (–9.8% and –7.5%previously).

How to achieve –3.0% deficit (c. €80bn reduction) medium term

Further cost-cutting measures to be implemented in the future.

Are tax increases avoidable?

Challenges ahead: looking for ways to rein in costs of all administrations.

Spain: Budget deficit trend Spain: Expenditure breakdown by authorities (2008)

Central government

22%Social security- -0.5 -0.6 -0.5 -0.5-0.1

-0.3 0.0 -0.2

-

1.0

2.0 1.9

0.0

2.0

4.0

29%

-0.6

-0.6

-0.3 -0.4

. .

-1.6

-3.1

-3.3 -1.3

-1.1

-4.8

-3.4 -3.2

-1.4-1.0

-0.6 - . - . - .

-4.1

-6.0

-4.4

-3.0

-8.0

-6.0

-4.0

-2.0

( a s

% o

f G D P )

Regional

governments

36%

Local governments

13%-2.0

-6.5

-11.2

-9.3

-14.0

-12.0

-10.0

.

5 6 7 8 9 0 1 2 3 4 5 6 7 8 9 0 1 2 3

Ahorro Corporación Financiera, S.V., S.A. 14

Source: Ministry of Economy, Bank of Spain and ACF Research Source: Ministry of Economy, Bank of Spain and ACF Research

1 9 9

1 9 9

1 9 9

1 9 9

1 9 9

2 0 0

2 0 0

2 0 0

2 0 0

2 0 0

2 0 0

2 0 0

2 0 0

2 0 0

2 0 0

2 0 1

2 0 1

2 0 1

2 0 1

Central gov. Regional gov. Loval gov. Social security

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 15/70

June, 2010

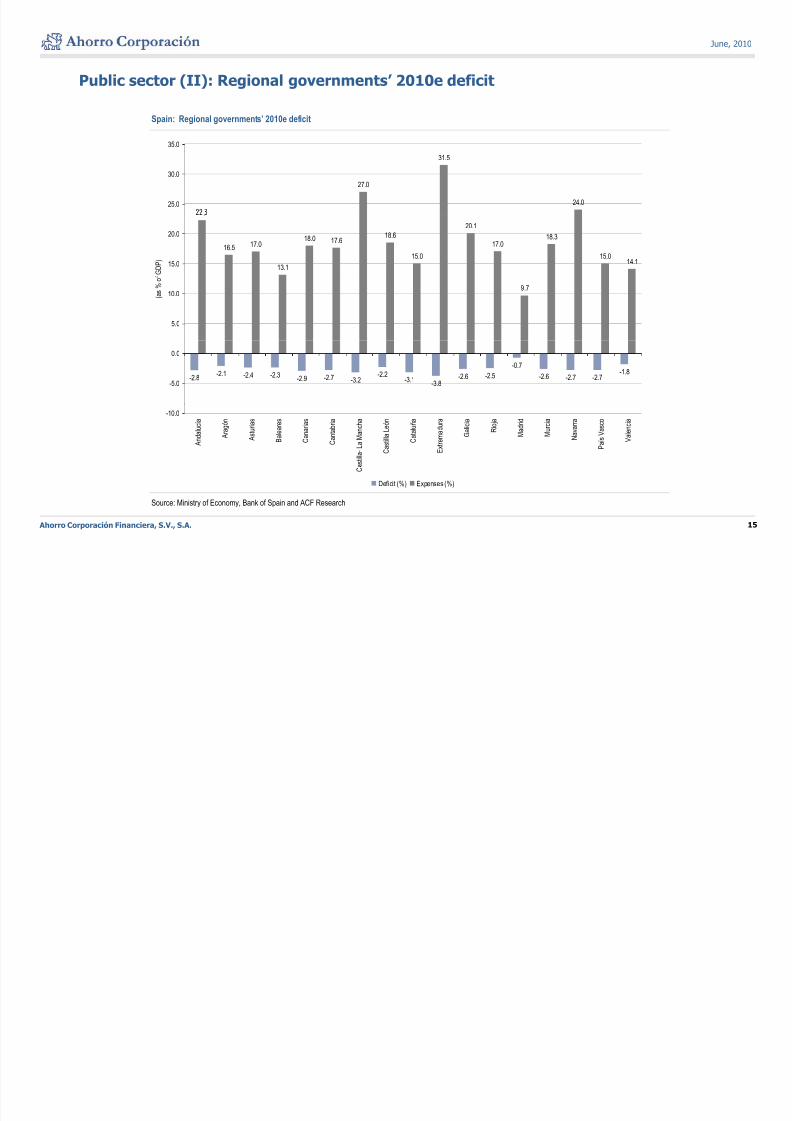

Public sector (II): Regional governments’ 2010e deficit

Spain: Regional governments’ 2010e deficit

35.0

27.0

31.5

24.025.0

30.0

.

16.5 17.0

13.1

18.0 17.618.6

15.0

20.1

17.018.3

15.014.115.0

20.0

f G D P )

9.7

5.0

10.0 ( a

s %

o

-2.8-2.1 -2.4 -2.3

-2.9 -2.7 -3.2-2.2

-3.1-3.8

-2.6 -2.5

-0.7

-2.6 -2.7 -2.7-1.8

-5.0

0.0

-10.0

A n

d a

l u c

í a

A r a g

ó n

A s

t u r i a s

B a

l e a r e s

C a n a r i a s

C a n

t a b r i a

a s

t i l l a -

L a

M a n c

h a

C a s

t i l l a L e

ó n

C a

t a l u ñ a

E x

t r e m a

d u r a

G a

l i c i a

R i o j a

M a

d r i d

M u r c

i a

N a v a r r a

P a

í s V a s c o

V a

l e n c

i a

Ahorro Corporación Financiera, S.V., S.A. 15

Source: Ministry of Economy, Bank of Spain and ACF Research

C

Deficit (%) Expenses (%)

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 16/70

June, 2010

Public sector (III): Government stimulus packages

Total stimulus packages implemented since 2008 amount to some €47.5bn (4.3% of GDP).

Revenues measures:€28.5bn, including personal income tax reduction and wealth tax elimination.

Expenses measures: €19.0Mn, inc u ing oca governments civi wor s, strategic sectors an t e car in ustry.

The Sustainable Economy Law (to be approved):

Aim: to improve the economy, competitiveness and environment.e orms o superv sory con ro organ sms , , mprovemen o nanc a regu a on, re uce ureaucracy,

reduction of the payment periods of the public administrations.

Specific measures:

Tax measures related to real-estate market: elimination of the deduction on acquisition of first home in 2011.

Financial instruments: €20.0bn co-financed (ICO and financial institutions). The March 2010 government proposal (March, 2010):

VAT reduction and tax deductions for home remodelling.

Loans and credit: promoting direct financing to SMEs (ICO) and speeding up the payment deadline for Public Administration’s to 30d and to 60d for large companies.

Increasing competitiveness: simplify administrative processes, international expansion of SMEs, R&D, define energy

policy for 2020, promote off-season tourism.

Giving a boost to industrial policy: increasing the industrial sector’s weight from 15.5% to 18% of GDP, definingthe new strategic sectors (automotive, aerospace, IT and Agri-food).

Reigning in budget deficit: cut personnel expenditure (-4%) and a plan to “streamline” government (cut pay for top-

Ahorro Corporación Financiera, S.V., S.A. 16

Easy financing for SMEs and families: speeding up consolidation of the financial system and use of FROBprogramme.

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 17/70

June, 2010

Public sector (IV): The “PLAN” (May, 2010)

Goal: reduction of the budget deficit by additional €16bn in 2010 and 2011 on top the €15bn already announced in January.

Measures an estimate savings:

Average reduction in civil servants’ pay of 5% in 2010 and freezing in 2011: €3,169Mn and €2,472Mn, respectively.

Reduction in infrastructure investments: €2,125Mn in 2010 and €2,125Mn in 2011.ens on paymen s reez ng n : , n.

Elimination of transitory early retirement system: €250Mn in 2010 and €150Mn in 2011.

Elimination of the childbirth allowance of €2,500: €1,250Mn in 2011.

, .

Foreign aid cuts: €300Mn in 2010 and €500Mn in 2011.

End to retroactive payments for new applicants for dependency allowances: €300Mn in 2011.

Re ional and local overnments will make an additional savin of €1 200Mn 2010-11 .

Breakdown of total savings: €6.7bn in 2010e and €10.0bn in 2011e (or 0.6% of GDP and 1.0% of GDP).

Impact on Spanish GDP: –0.5% in 2011e:

Private consumption to be eroded by –0.2%.

Non-residential construction investment reduced by –0.2%

Public expenditure to be reduced by an additional –0.1%.

Ahorro Corporación Financiera, S.V., S.A. 17

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 18/70

June, 2010

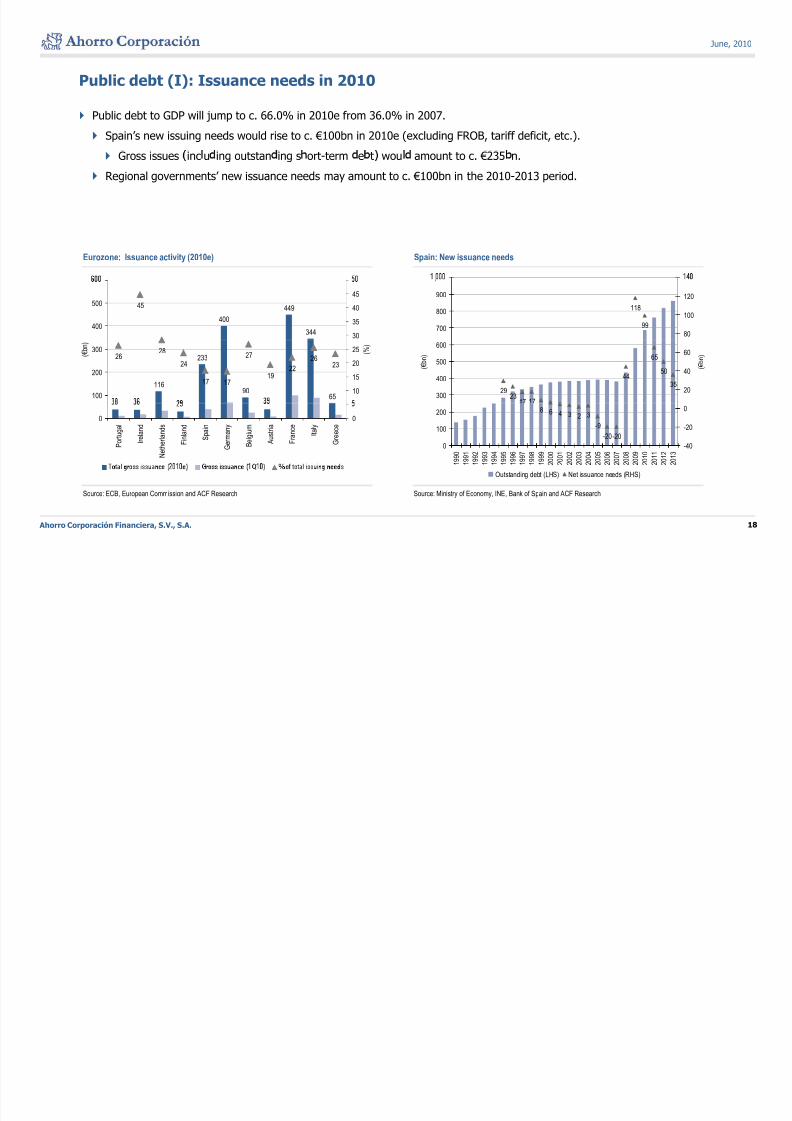

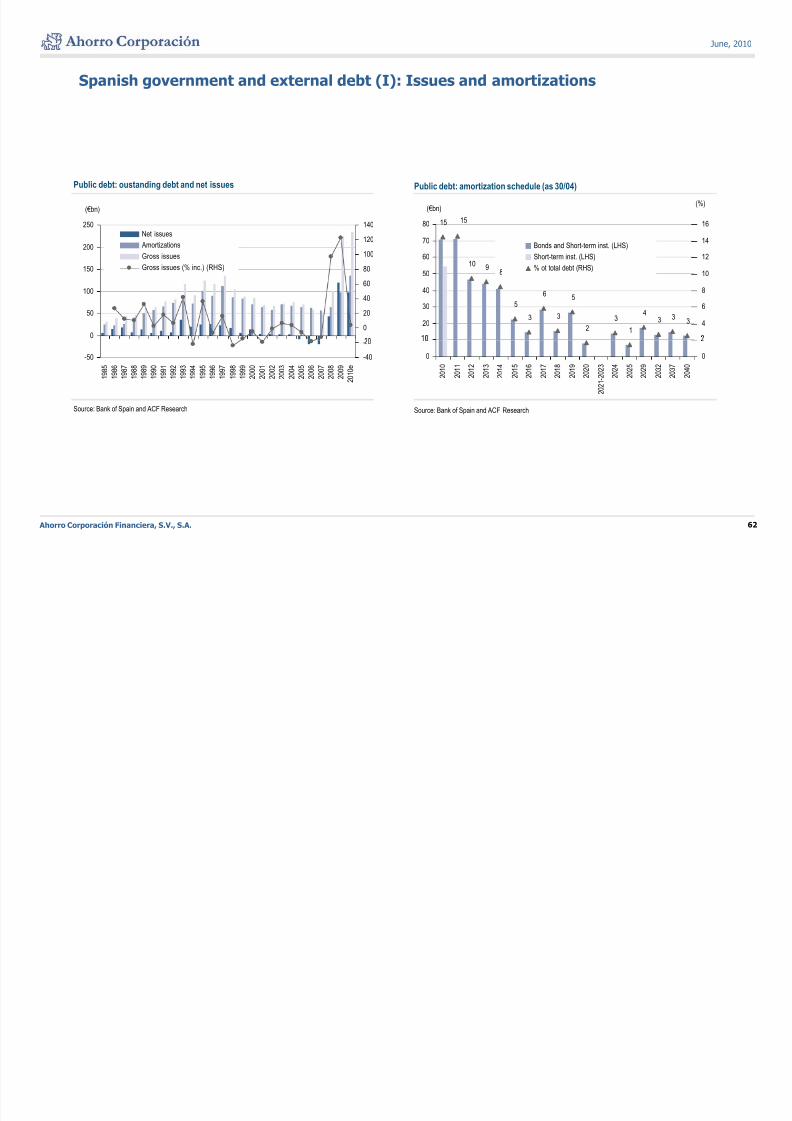

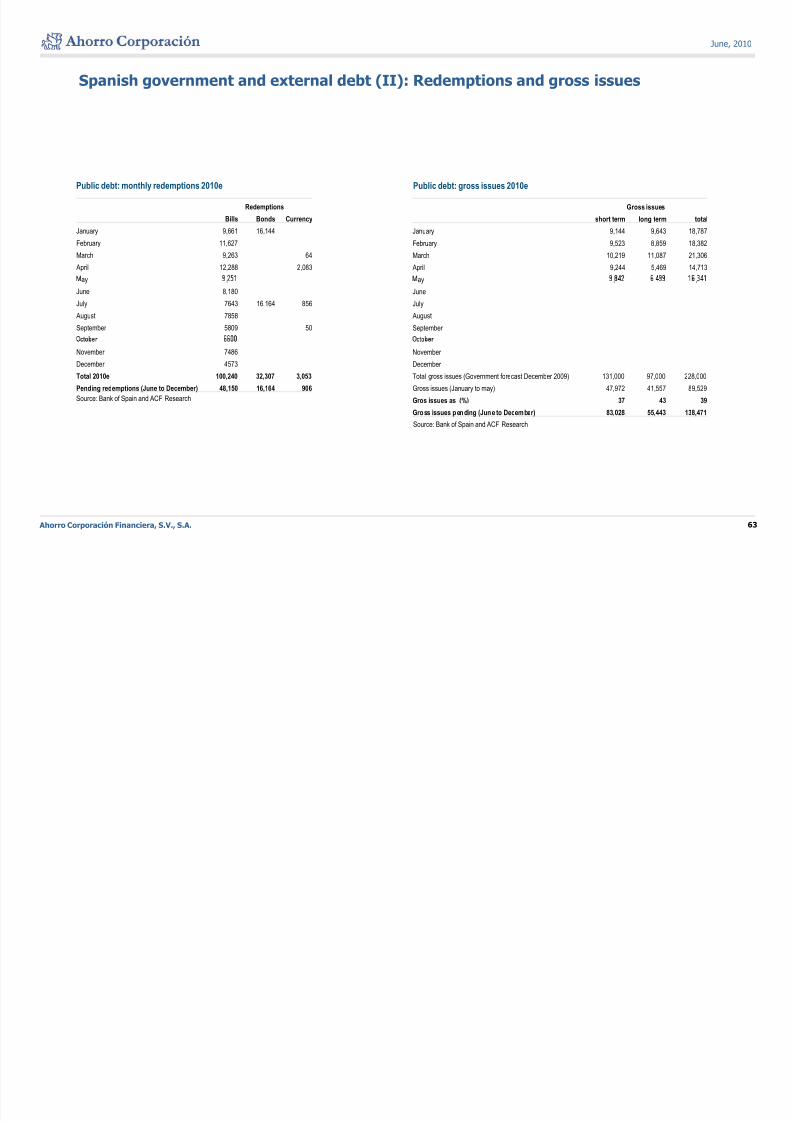

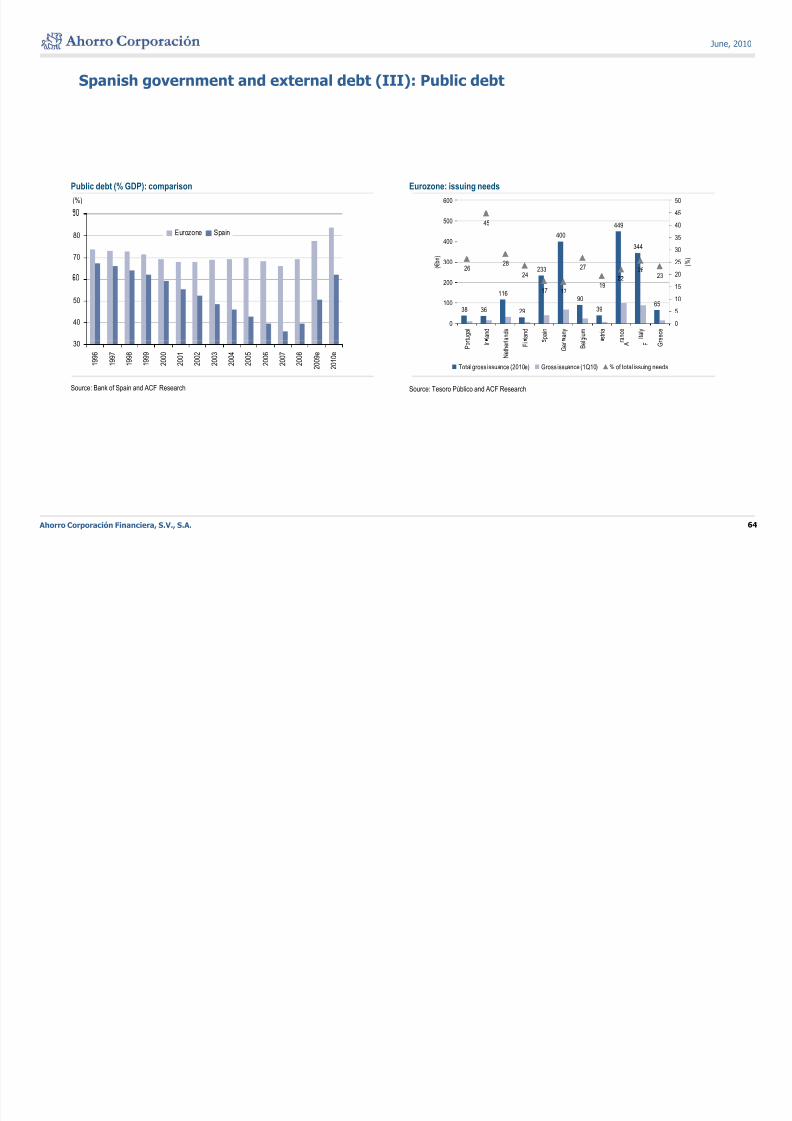

Public debt (I): Issuance needs in 2010

Public debt to GDP will jump to c. 66.0% in 2010e from 36.0% in 2007.

Spain’s new issuing needs would rise to c. €100bn in 2010e (excluding FROB, tariff deficit, etc.).

Gross issues inc u ing outstan ing s ort-term e t wou amount to c. €235 n.

Regional governments’ new issuance needs may amount to c. €100bn in the 2010-2013 period.

Eurozone: Issuance activity (2010e) Spain: New issuance needs

118

99700

800

900

,

80

100

120

400

449

344

45

400

500

30

35

4045

29 2317 17

44

65

50

35

300

400

500

600

( € b n

)

20

40

60

( € b n

)

116

233

90 65

2628

24

17 17

27

1922

2623

100

200

300 ( € b n )

10

15

20

25 ( % )

8 6 4 3 2 3

-9

-20-20

0

100

200

1 9 9 0

1 9 9 1

1 9 9 2

1 9 9 3

1 9 9 4

1 9 9 5

1 9 9 6

1 9 9 7

1 9 9 8

1 9 9 9

2 0 0 0

2 0 0 1

2 0 0 2

2 0 0 3

2 0 0 4

2 0 0 5

2 0 0 6

2 0 0 7

2 0 0 8

2 0 0 9

2 0 1 0

2 0 1 1

2 0 1 2

2 0 1 3

-40

-20

0

0

P o r t u g a l

I r e l a n d

N e t h e r l a n d s

F i n l a n d

S p a i n

G e r m a n y

B e l g i u m

A u s t r i a

F r a n c e

I t a l y

G r e e c e

0

Ahorro Corporación Financiera, S.V., S.A. 18

Source: ECB, European Commission and ACF Research Source: Ministry of Economy, INE, Bank of Spain and ACF Research

Outstanding debt (LHS) Net issuance needs (RHS)

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 19/70

June, 2010

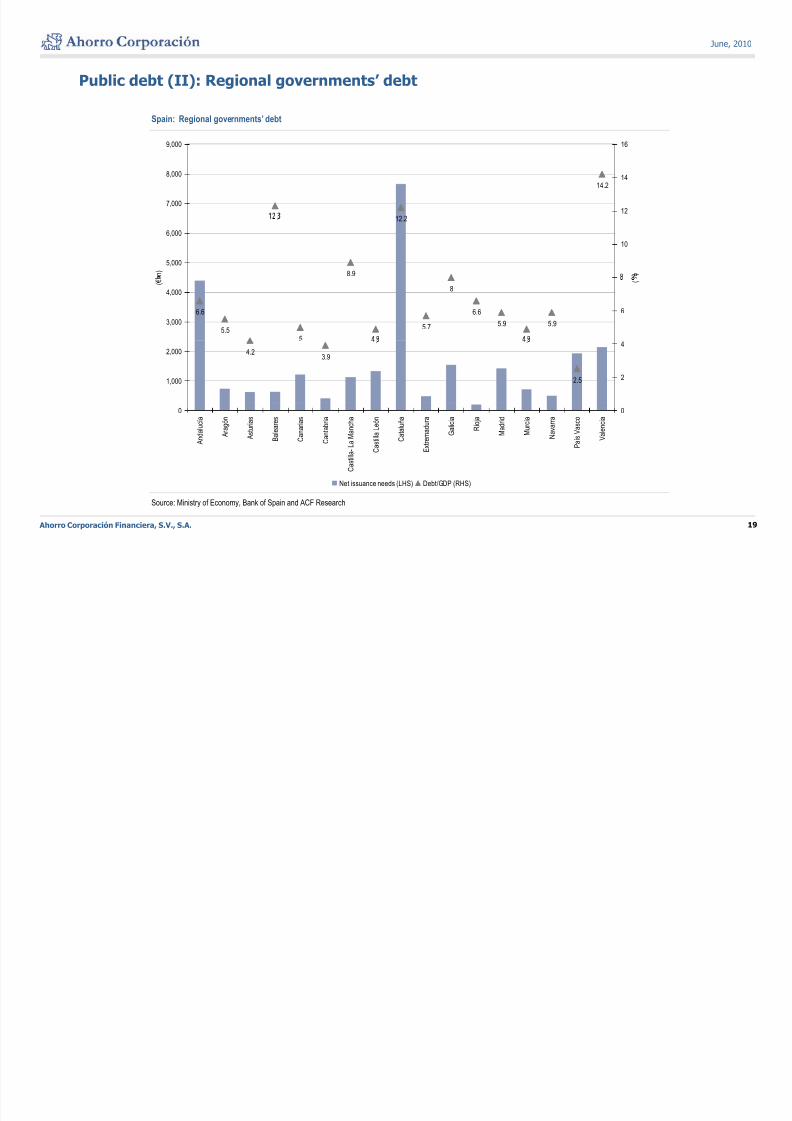

Public debt (II): Regional governments’ debt

Spain: Regional governments’ debt

9,000 16

14.2

7,000

8,000

12

14

.

8.9

12.2

5,000

6,000

n )

10

)

6.6

5.55

5.7

8

6.6

5.9 5.93,000

4,000

( €

6

(

4.23.9

. .

2.51,000

2,000

2

4

0

A n d a l u c í a

A r a g ó n

A s t u r i a s

B a l e a r e s

C a n a r i a s

C a n t a b r i a

a s t i l l a -

L a M a n c h a

C a s t i l l a L e ó n

C a t a l u ñ a

E x t r e m a d u r a

G a l i c i a

R i o j a

M a d r i d

M u r c i a

N a v a r r a

P a í s V a s c o

V a l e n c i a

0

Ahorro Corporación Financiera, S.V., S.A. 19

Source: Ministry of Economy, Bank of Spain and ACF Research

C

Net issuance needs (LHS) Debt/GDP (RHS)

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 20/70

June, 2010

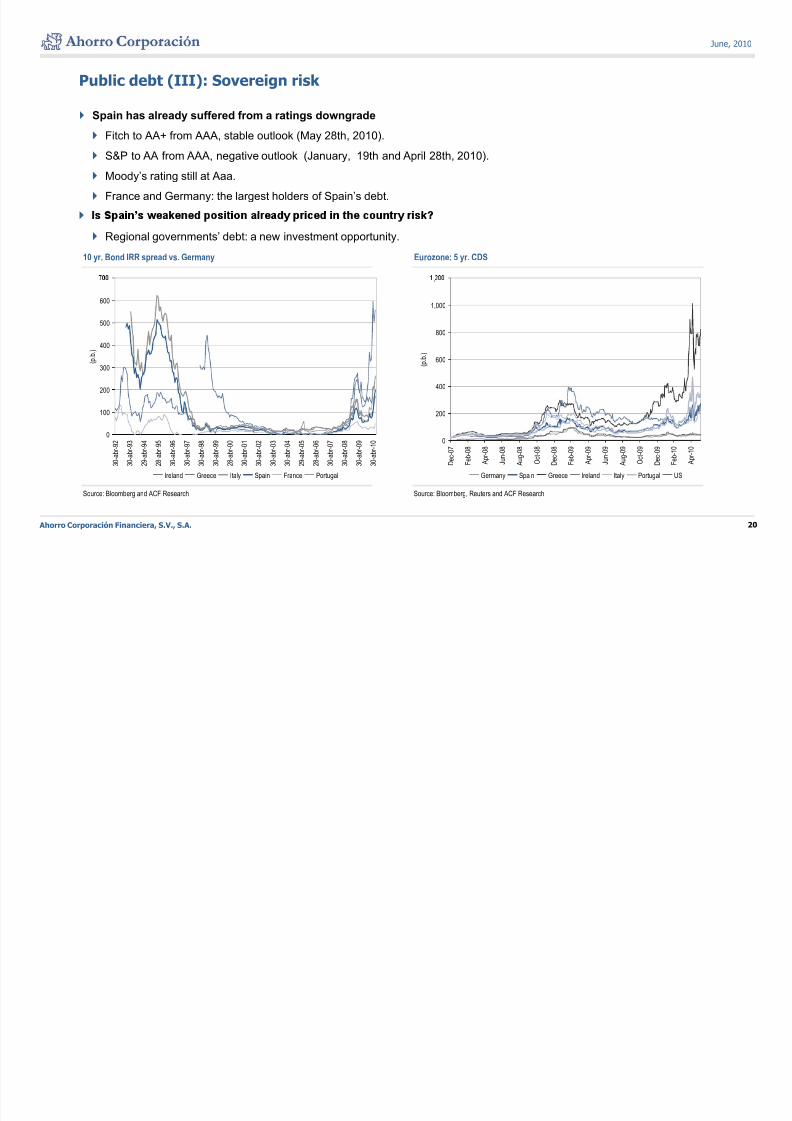

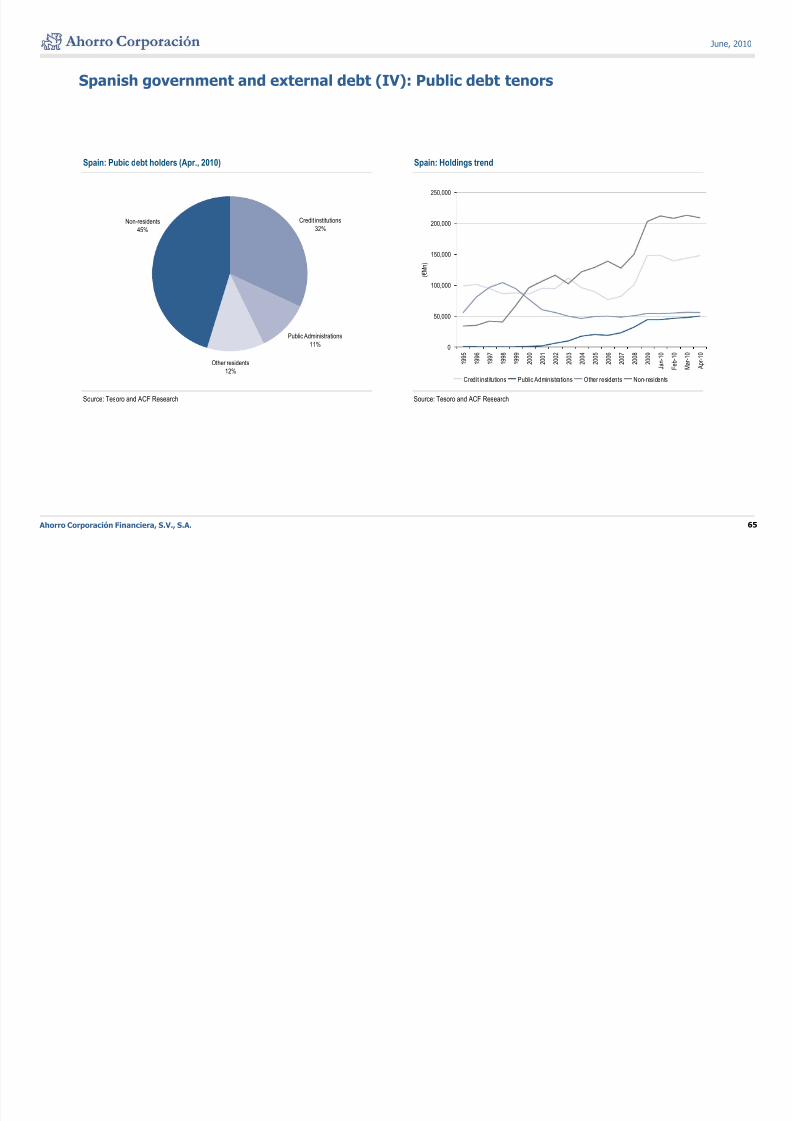

Public debt (III): Sovereign risk

Spain has already suffered from a ratings downgrade

Fitch to AA+ from AAA, stable outlook (May 28th, 2010).

S&P to AA from AAA, negative outlook (January, 19th and April 28th, 2010).

Moody’s rating still at Aaa.

France and Germany: the largest holders of Spain’s debt.

Regional governments’ debt: a new investment opportunity.

10 yr. Bond IRR spread vs. Germany Eurozone: 5 yr. CDS

500

600

800

1,000

,

200

300

400

( p . b . )

400

600 ( p

. b . )

0

100

3 0

- a b r - 9

2

3 0

- a b r - 9

3

2 9

- a b r - 9

4

2 8

- a b r - 9

5

3 0

- a b r - 9

6

3 0

- a b r - 9

7

3 0

- a b r - 9

8

3 0

- a b r - 9

9

2 8

- a b r - 0

0

3 0

- a b r - 0

1

3 0

- a b r - 0

2

3 0

- a b r - 0

3

3 0

- a b r - 0

4

2 9

- a b r - 0

5

2 8

- a b r - 0

6

3 0

- a b r - 0

7

3 0

- a b r - 0

8

3 0

- a b r - 0

9

3 0

- a b r - 1

0 0

200

D e c - 0

7

F e

b - 0

8

A p r - 0

8

J u n - 0

8

A u g - 0

8

O c

t - 0 8

D e c - 0

8

F e

b - 0

9

A p r - 0

9

J u n - 0

9

A u g - 0

9

O c

t - 0 9

D e c - 0

9

F e

b - 1

0

A p r - 1

0

Ahorro Corporación Financiera, S.V., S.A. 20

Source: Bloomberg and ACF Research Source: Bloomberg, Reuters and ACF Research

Ireland Greece Italy Spain France Portugal Germany Spain Greece Ireland Italy Portugal US

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 21/70

June, 2010

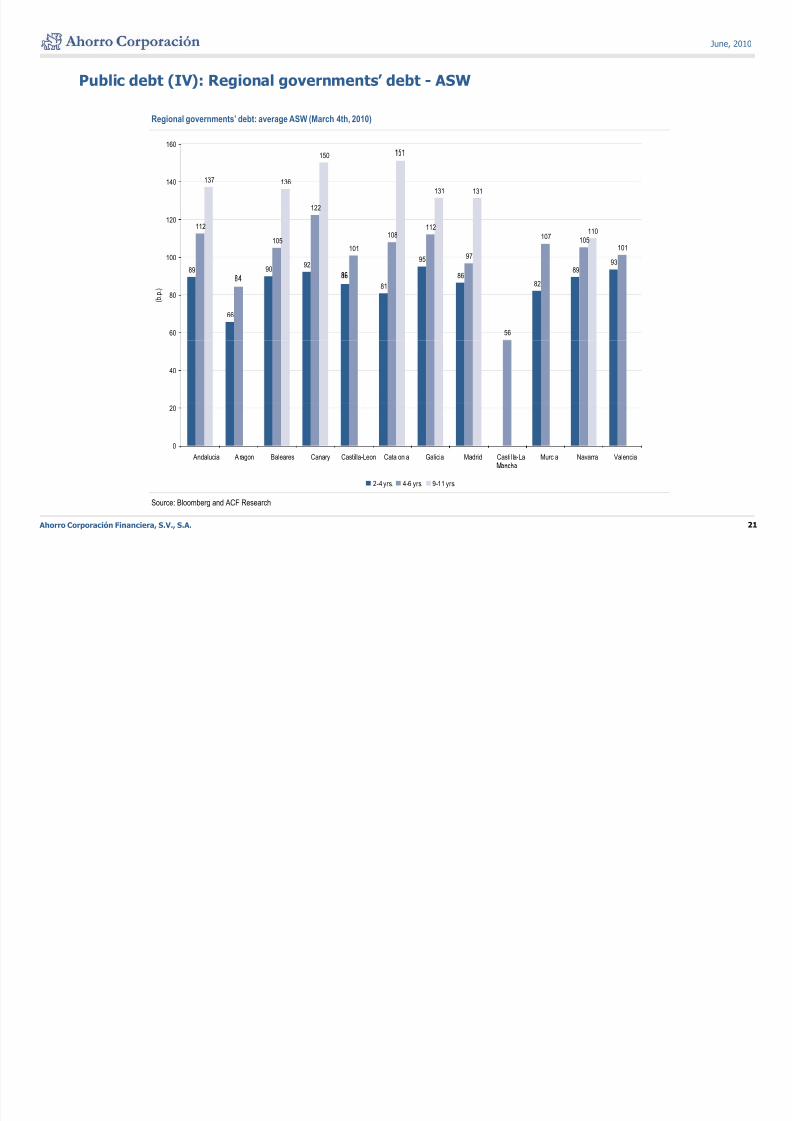

Public debt (IV): Regional governments’ debt - ASW

Regional governments’ debt: average ASW (March 4th, 2010)

160

122

137 136

150

131 131

140

89 9092

95

8689

93

112

105101

108112

97

107105

101

110

100

120

66

81 82

5660

80 ( b . p . )

40

0

20

Andalucia Aragon Baleares Canary Castilla-Leon Catalonia Galicia Madrid Castil la-La Murcia Navarra Valencia

Ahorro Corporación Financiera, S.V., S.A. 21

Source: Bloomberg and ACF Research

2-4 yrs. 4-6 yrs. 9-11 yrs.

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 22/70

June, 2010

Real estate sector (I): Has it touched bottom?

We estimate a –17.6% drop in investment in residential construction in 2010e and –7.3% in 2011e (–24.5% in 2009).

Housing starts: c. 150,000 in 2009e and 2010e. (–57% vs. 2008 and –80% vs. peak housing starts)

Finis e ouses may reac ow in 2011e or 2012e.

Investment in residential construction may represent c. 6.0% of GDP in 2011e from maximum of 9.0% in 2006.

Still above lows of the early nineties.ey c a enge: re uce epen ence on e res en a cons ruc on sec or.

Spanish GDP: Investment in construction Spain: Housing starts

14 14 13 1312 12 12

1315

161614

14 1413

12 1213

1314

1516

16 17

1818 18

1615 15

14

16

18

600,000

700,000

800,000

,

60

80

100

6

8

10

12

( a s

% o

f G D P )

300,000

400,000

500,000

( u n

i t s )

-20

0

20

40

( % )

6 6 6 5 5 4 4 5 5 5 5 5 4 4 4 4 5 5 5 5 6 7 7 8 8 7 7 6

0

2

4

1 9 8 0

1 9 8 2

1 9 8 4

1 9 8 6

1 9 8 8

1 9 9 0

1 9 9 2

1 9 9 4

1 9 9 6

1 9 9 8

2 0 0 0

2 0 0 2

2 0 0 4

2 0 0 6

2 0 0 8

2 0 1 0 e

0

100,000

200,000

1 9 7 1

1 9 7 4

1 9 7 7

1 9 8 0

1 9 8 3

1 9 8 6

1 9 8 9

1 9 9 2

1 9 9 5

1 9 9 8

2 0 0 1

2 0 0 4

2 0 0 7

2 0 1 0

-80

-60

-40

Ahorro Corporación Financiera, S.V., S.A. 22

Source: INE and ACF Research Source: INE and ACF Research

Investment in construction of which housing Housing starts (LHS) % inc. (LHS)

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 23/70

June, 2010

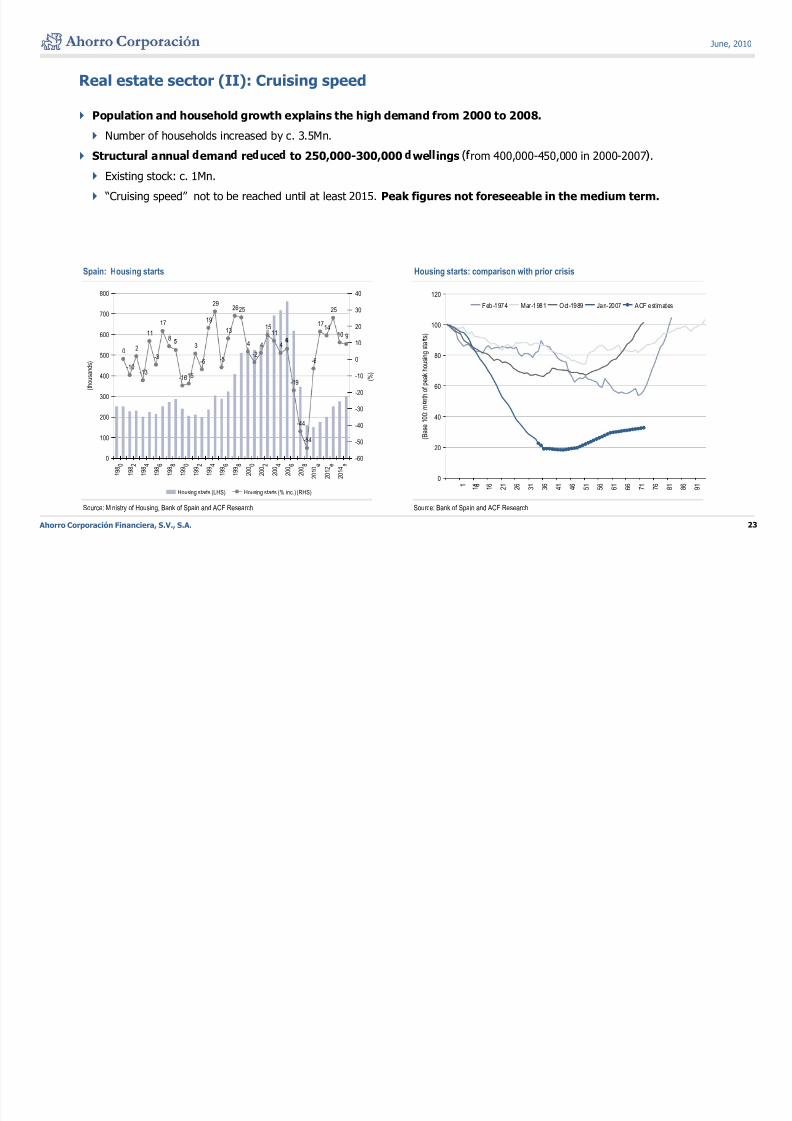

Real estate sector (II): Cruising speed

Population and household growth explains the high demand from 2000 to 2008.

Number of households increased by c. 3.5Mn.

Structura annua eman re uce to 250,000-300,000 we ings rom 400,000-450,000 in 2000-2007 .

Existing stock: c. 1Mn.

“Cruising speed” not to be reached until at least 2015. Peak figures not foreseeable in the medium term.

Spain: Housing starts Housing starts: comparison with prior crisis

100

120

t s )

Feb-1974 Mar-1981 Oct-1989 Jan-2007 ACF est imates

11

17

8

19

29

13

2625

1511

1714

25

10 9600

700

800

20

30

40

60

80

n t h

o f p e a k h o u s i n g s t a

0

-10

2

-13

-3

-16

3

-6 -5

4

-2

4 4

-19

-6

-15

300

400

500

( t h o u s a n d s )

-20

-10

0

10

( % )

20

40

( B a s e 1 0 0 : m

-44

-54

0

100

200

0 2 4 6 8 0 2 4 6 8 0 2 4 6 8 e e e

-60

-50

-40

-30

Ahorro Corporación Financiera, S.V., S.A. 23

Source: Ministry of Housing, Bank of Spain and ACF Research Source: Bank of Spain and ACF Research

0 1 6

1 1

1 6

2 1

2 6

3 1

3 6

4 1

4 6

5 1

5 6

6 1

6 6

7 1

7 6

8 1

8 6

9 1

1 9 8

1 9 8

1 9 8

1 9 8

1 9 8

1 9 9

1 9 9

1 9 9

1 9 9

1 9 9

2 0 0

2 0 0

2 0 0

2 0 0

2 0 0

2 0 1 0

2 0 1 2

2 0 1 4

Housing starts (LHS) Housing starts (% inc.) (RHS)

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 24/70

June, 2010

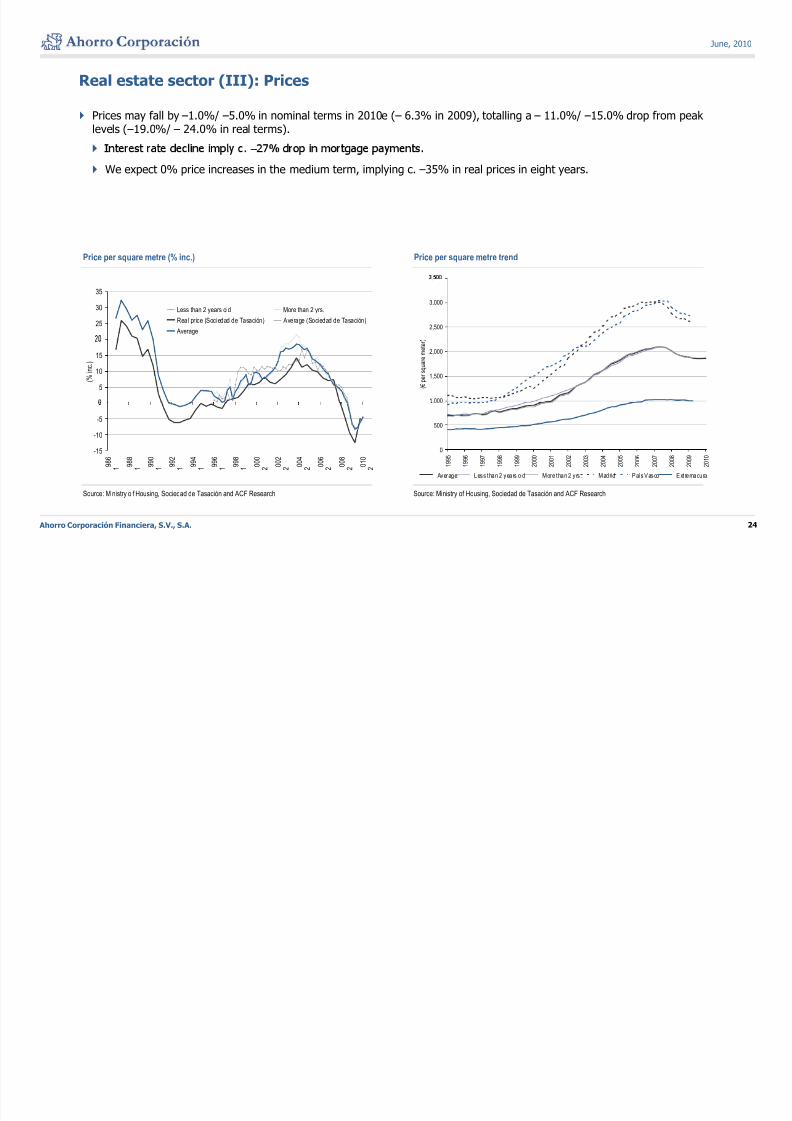

Real estate sector (III): Prices

Prices may fall by –1.0%/ –5.0% in nominal terms in 2010e (– 6.3% in 2009), totalling a – 11.0%/ –15.0% drop from peak levels (–19.0%/ – 24.0% in real terms).

–

We expect 0% price increases in the medium term, implying c. –35% in real prices in eight years.

Price per square metre (% inc.) Price per square metre trend

25

30

35

Less than 2 years old More than 2 yrs.

Real price (Sociedad de Tasación) Average (Sociedad de Tasación)

Average2,500

3,000

,

)

5

10

15

( % i n

c . )

1,000

1,500

2,000

( € p e r s q u a r e m e t e r

-15

-10

-5

9 8 6

9 8 8

9 9 0

9 9 2

9 9 4

9 9 6

9 9 8

0 0 0

0 0 2

0 0 4

0 0 6

0 0 8

0 1 0

0

500

1 9 9 5

1 9 9 6

1 9 9 7

1 9 9 8

1 9 9 9

2 0 0 0

2 0 0 1

2 0 0 2

2 0 0 3

2 0 0 4

2 0 0 5

2 0 0 6

2 0 0 7

2 0 0 8

2 0 0 9

2 0 1 0

Ahorro Corporación Financiera, S.V., S.A. 24

Source: Ministry o f Housing, Sociedad de Tasación and ACF Research Source: Ministry of Housing, Sociedad de Tasación and ACF Research

1 1 1 1 1 1 1 2 2 2 2 2 2

Average Less than 2 years o ld More than 2 y rs . Madrid País Vasco Ext remadura

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 25/70

June, 2010

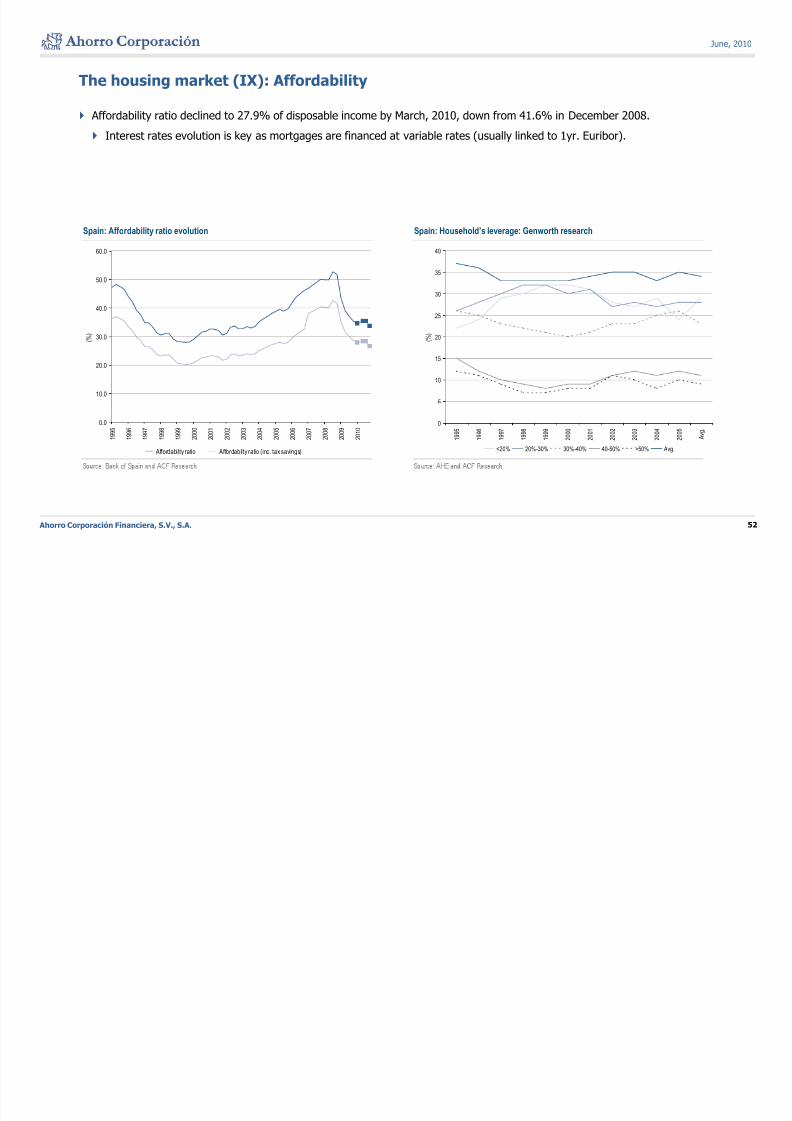

Real estate sector (IV): Why prices have not fallen much

Average payment declined by –27.3% in 2009.

We expected payments to be stable in 2010e but they may increase by c. 17.0% in 2011e due to higher interest rates.

A or a i ity ratio roppe to 27.9% in 1Q10 rom 34.1% in 1Q09 an a maximum o 42.5% in 3Q08.

We expect this level to hold steady in the coming years.

Higher interest rates impact to be offset by increasing family income and flat property prices.ax sav ngs o e e m na e as o or ren a s g er an , : c. . p.p. mpac

Annual mortgage payments Affordablity ratio

-

-9

-5 -5

-1410,000

12,000

-10

0

50.0

60.0

-40 -39

-29

-23-25 -26

-19

-24

-27.3

6,000

8,000

( € )

-30

-20

( % ) 30.0

40.0

( % )

-50 -50 -50 -49

-44

0

2,000

4,000

-60

-50

-40

0.0

10.0

.

Ahorro Corporación Financiera, S.V., S.A. 25

Source: AHE, Bank of Spain ACF Research Source: AHE, Bank of Spain ACF Research

1 9 9 0

1 9 9 1

1 9 9 2

1 9 9 3

1 9 9

1 9 9 5

1 9 9 6

1 9 9 7

1 9 9 8

1 9 9 9

2 0 0 0

2 0 0 1

2 0 0 2

2 0 0 3

2 0 0

2 0 0 5

2 0 0 6

2 0 0 7

2 0 0 8

2 0 0 9 e

2 0 1 0 e

2 0 1 1 e

2 0 1 2 e

Initial payment 2009e payment 2011e payment Payment reduction (%) (RHS)

1 9 9 5

1 9 9 6

1 9 9 7

1 9 9 8

1 9 9 9

2 0 0 0

2 0 0 1

2 0 0 2

2 0 0 3

2 0 0 4

2 0 0 5

2 0 0 6

2 0 0 7

2 0 0 8

2 0 0 9

2 0 1 0

Affordabilty ratio Affordabilty ratio (inc. tax savings)

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 26/70

June, 2010

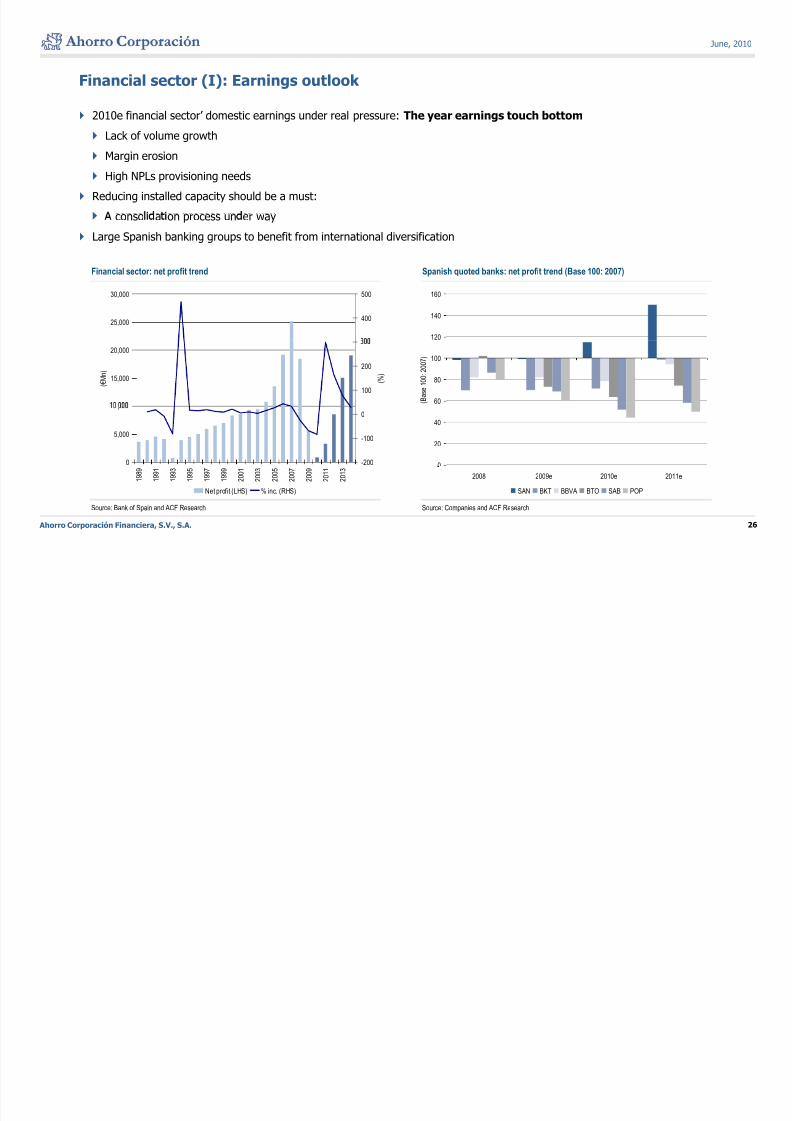

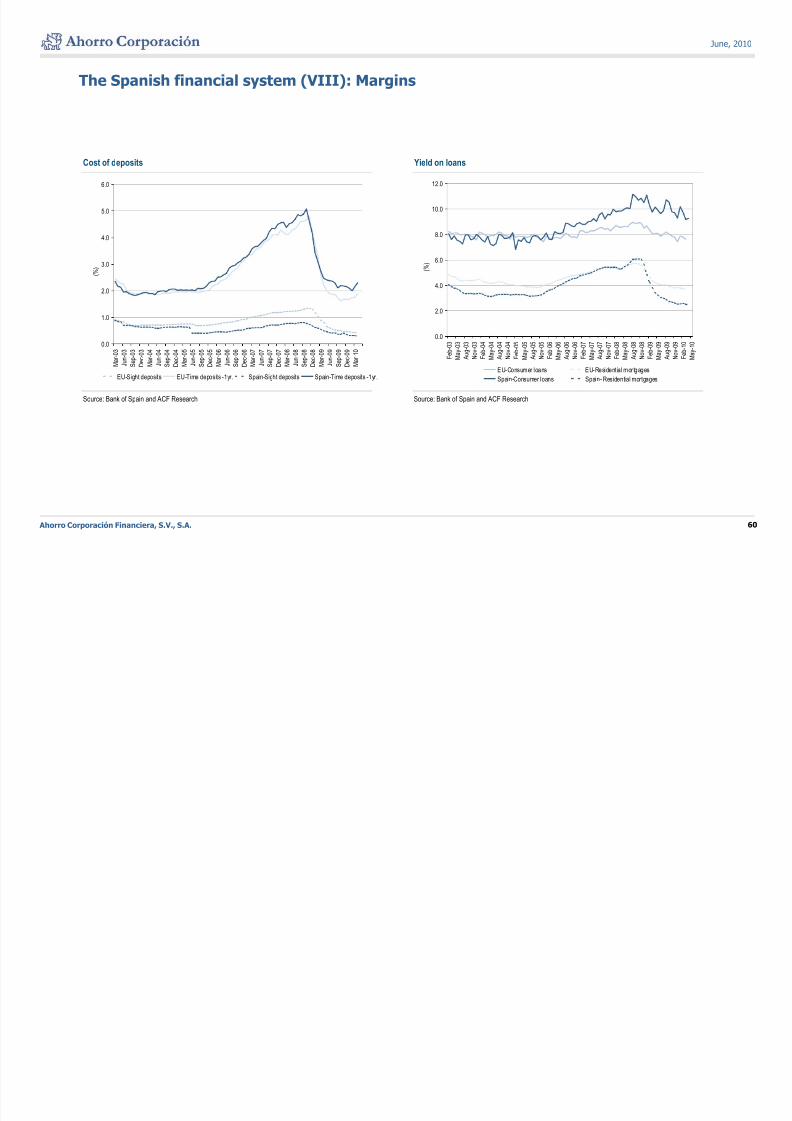

Financial sector (I): Earnings outlook

2010e financial sector’ domestic earnings under real pressure: The year earnings touch bottom

Lack of volume growth

Margin erosion

High NPLs provisioning needs

Reducing installed capacity should be a must:

conso a on process un er way

Large Spanish banking groups to benefit from international diversification

Financial sector: net profit trend Spanish quoted banks: net profit trend (Base 100: 2007)

25,000

30,000

400

500

120

140

160

15,000

20,000

( € M n )

100

200

( % )

60

80

100

( B a

s e 1 0 0 : 2 0 0 7 )

0

5,000

,

-200

-100

0

0

20

40

Ahorro Corporación Financiera, S.V., S.A. 26

Source: Bank of Spain and ACF Research Source: Companies and ACF Research

1 9 8 9

1 9 9 1

1 9 9 3

1 9 9 5

1 9 9 7

1 9 9 9

2 0 0 1

2 0 0 3

2 0 0 5

2 0 0 7

2 0 0 9

2 0 1 1

2 0 1 3

Net profit (LHS) % inc. (RHS)

2008 2009e 2010e 2011e

SAN BKT BBVA BTO SAB POP

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 27/70

June, 2010

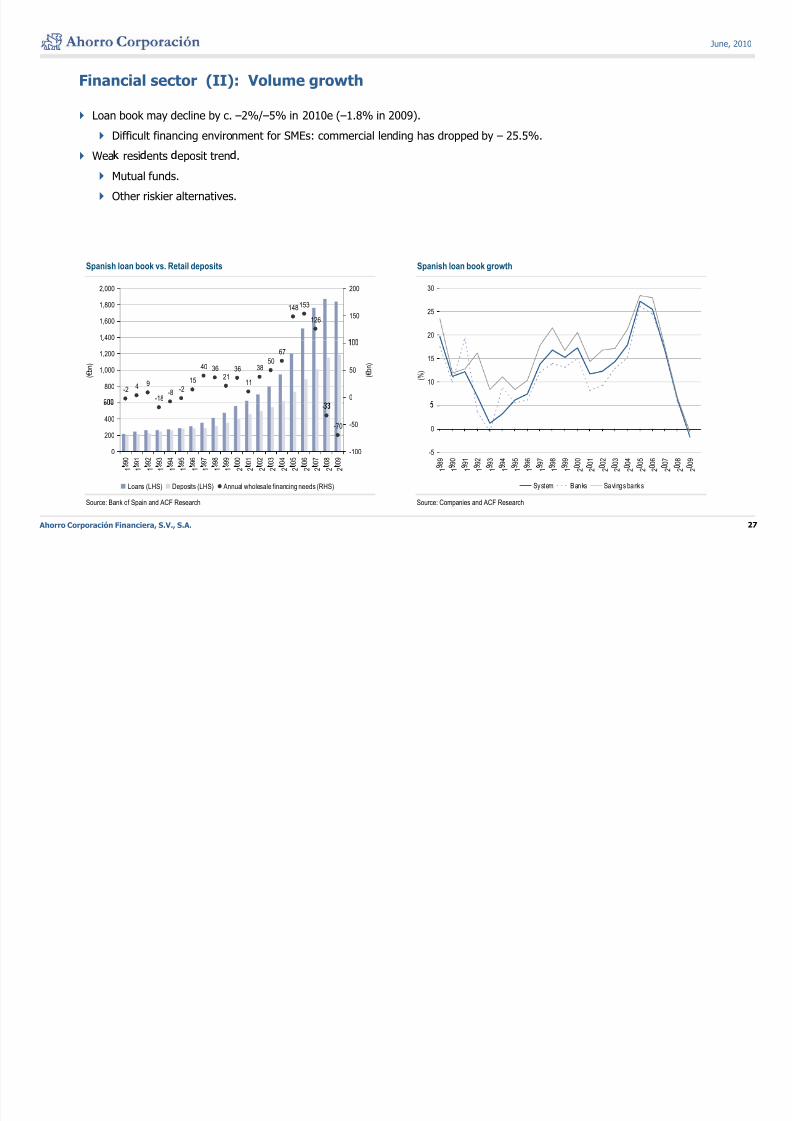

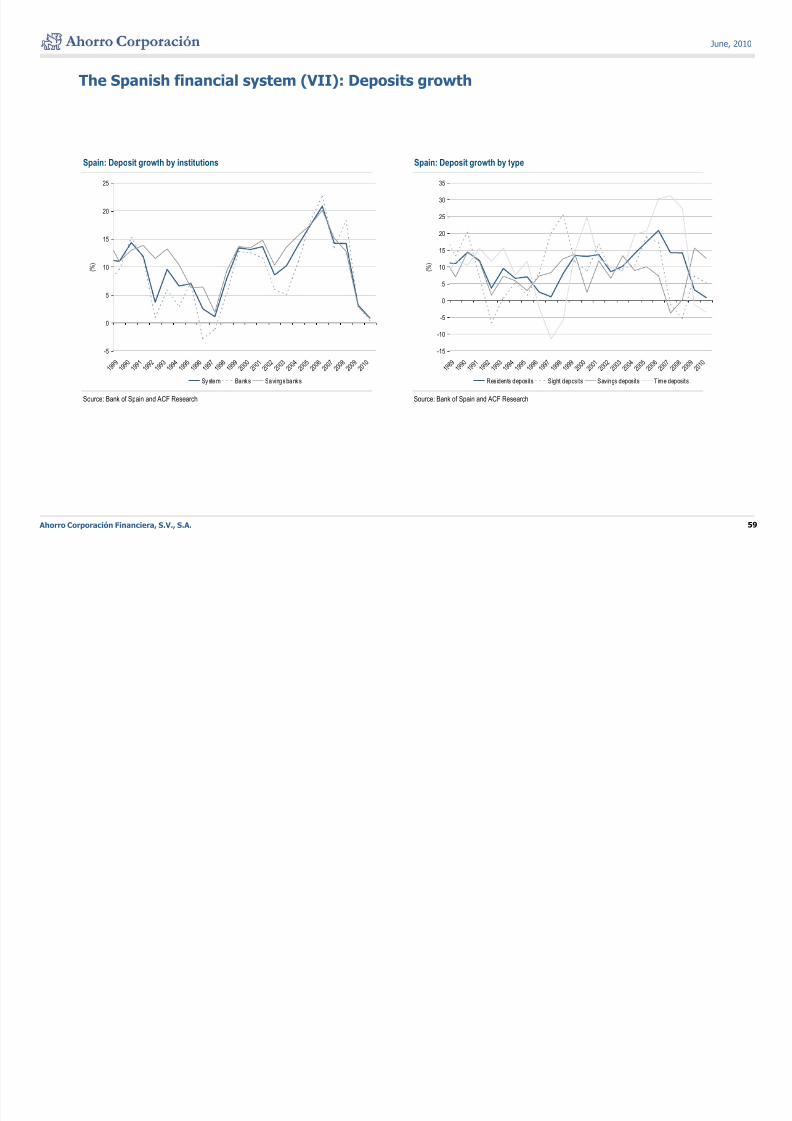

Financial sector (II): Volume growth

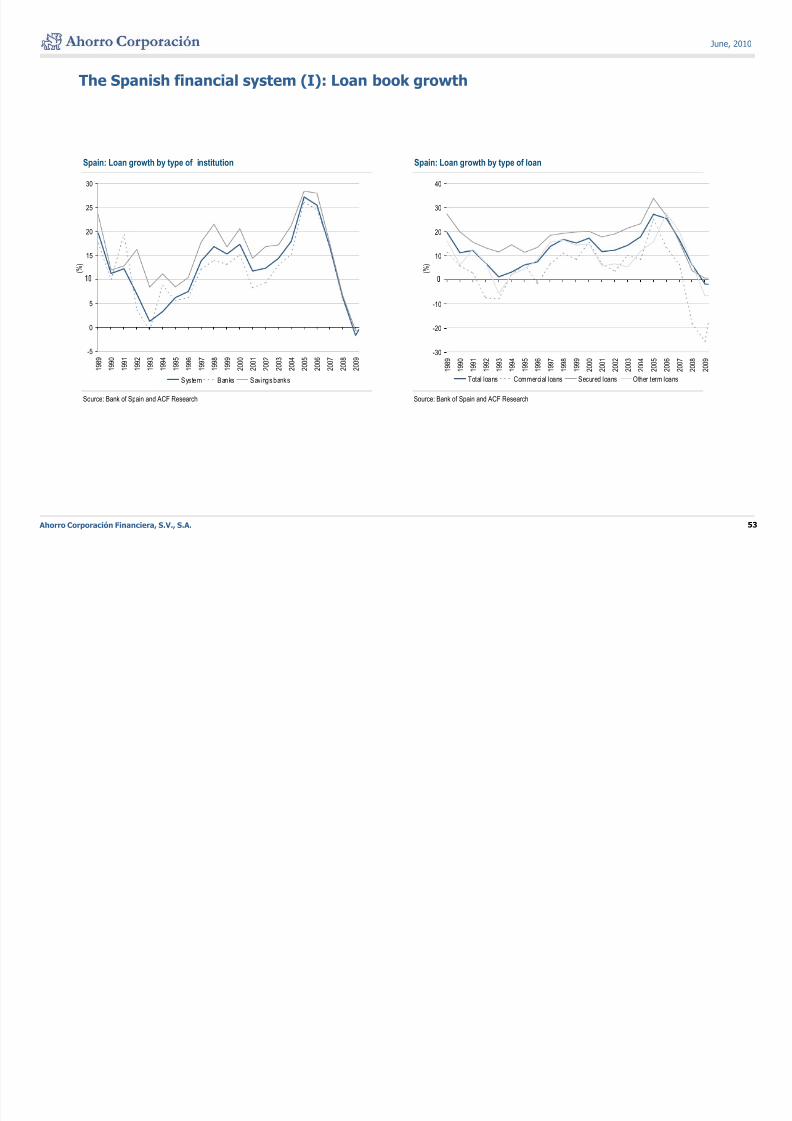

Loan book may decline by c. –2%/–5% in 2010e (–1.8% in 2009).

Difficult financing environment for SMEs: commercial lending has dropped by – 25.5%.

Wea resi ents eposit tren .

Mutual funds.

Other riskier alternatives.

Spanish loan book vs. Retail deposits Spanish loan book growth

20

25

30

148153

126

1,400

1,600

1,800

2,000

150

200

10

15

( % )

-2 4 9

-18 -8

-215

40 3621

36

11

3850

67

800

1,000

1,200

( € b n )

0

50 ( € b n )

-5

0

8 9

9 0

9 1

9 2

9 3

9 4

9 5

9 6

9 7

9 8

9 9

0 0

0 1

0 2

0 3

0 4

0 5

0 6

0 7

0 8

0 9

-

-70

0

200

400

9 9 0

9 9 1

9 9 2

9 9 3

9 9 4

9 9 5

9 9 6

9 9 7

9 9 8

9 9 9

0 0 0

0 0 1

0 0 2

0 0 3

0 0 4

0 0 5

0 0 6

0 0 7

0 0 8

0 0 9

-100

-50

Ahorro Corporación Financiera, S.V., S.A. 27

Source: Bank of Spain and ACF Research Source: Companies and ACF Research

1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2 2 2

System Banks Savings banks

1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2 2 2

Loans (LHS) Deposits (LHS) Annual wholesale financing needs (RHS)

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 28/70

June, 2010

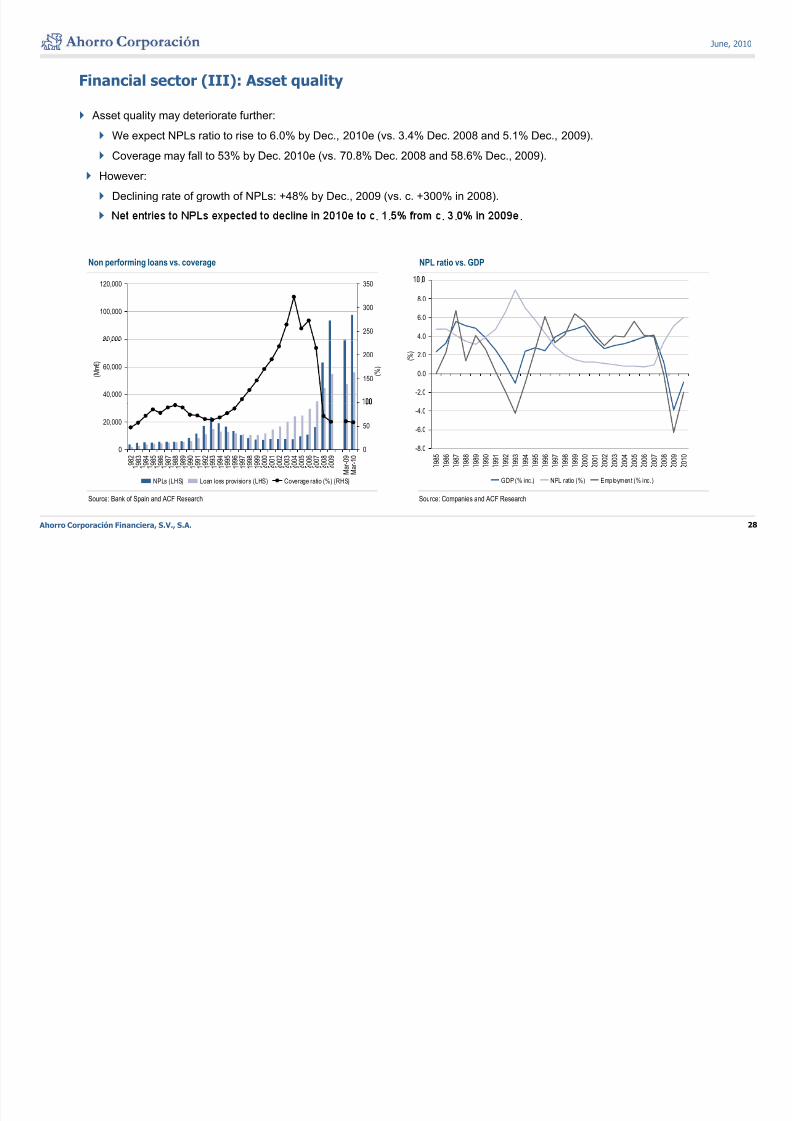

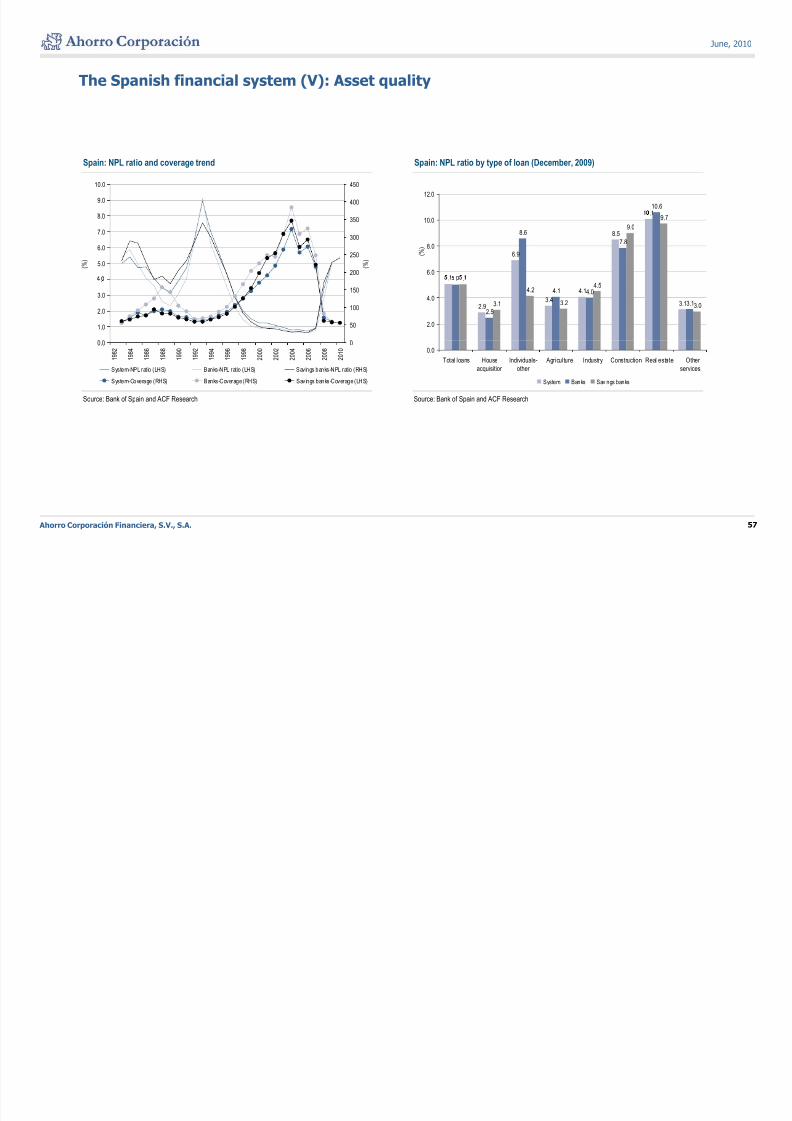

Financial sector (III): Asset quality

Asset quality may deteriorate further:

We expect NPLs ratio to rise to 6.0% by Dec., 2010e (vs. 3.4% Dec. 2008 and 5.1% Dec., 2009).

Coverage may fall to 53% by Dec. 2010e (vs. 70.8% Dec. 2008 and 58.6% Dec., 2009).

However:

Declining rate of growth of NPLs: +48% by Dec., 2009 (vs. c. +300% in 2008).

. . . . .

Non performing loans vs. coverage NPL ratio vs. GDP

4.0

6.0

8.0

.

80 000

100,000

120,000

250

300

350

-2.0

0.0

2.0 ( % )

40,000

60,000

,

( M n € )

150

200

( % )

-8.0

-6.0

-4.0

1 9 8 5

1 9 8 6

1 9 8 7

1 9 8 8

1 9 8 9

1 9 9 0

1 9 9 1

1 9 9 2

1 9 9 3

1 9 9 4

1 9 9 5

1 9 9 6

1 9 9 7

1 9 9 8

1 9 9 9

2 0 0 0

2 0 0 1

2 0 0 2

2 0 0 3

2 0 0 4

2 0 0 5

2 0 0 6

2 0 0 7

2 0 0 8

2 0 0 9

2 0 1 0

0

20,000

9 8 2

9 8 3

9 8 4

9 8 5

9 8 6

9 8 7

9 8 8

9 8 9

9 9 0

9 9 1

9 9 2

9 9 3

9 9 4

9 9 5

9 9 6

9 9 7

9 9 8

9 9 9

0 0 0

0 0 1

0 0 2

0 0 3

0 0 4

0 0 5

0 0 6

0 0 7

0 0 8

0 0 9

r - 0 9

r - 1 0

0

50

Ahorro Corporación Financiera, S.V., S.A. 28

Source: Bank of Spain and ACF Research Source: Companies and ACF Research

GDP (% inc.) NPL ratio (%) Employment (% inc.)

1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 M a

M a

NPLs (LHS) Loan loss provisions (LHS) Coverage ratio (%) (RHS)

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 29/70

June, 2010

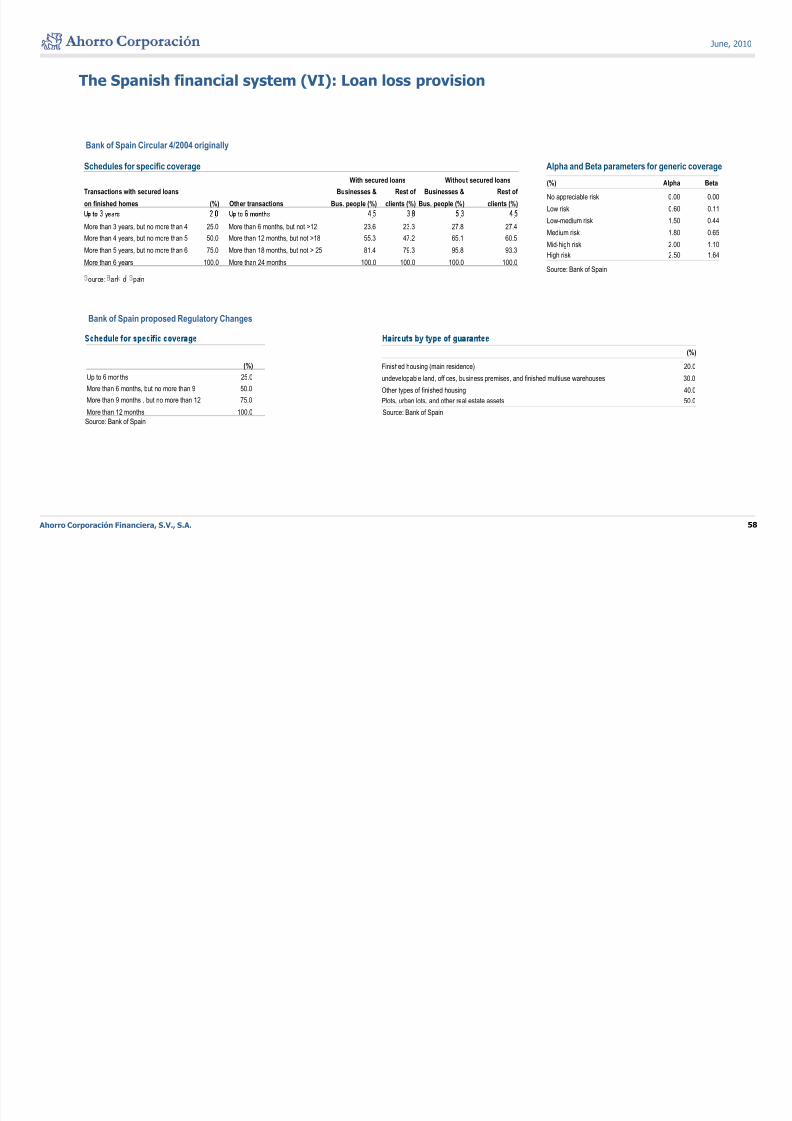

Financial sector (IV): The solvency issue

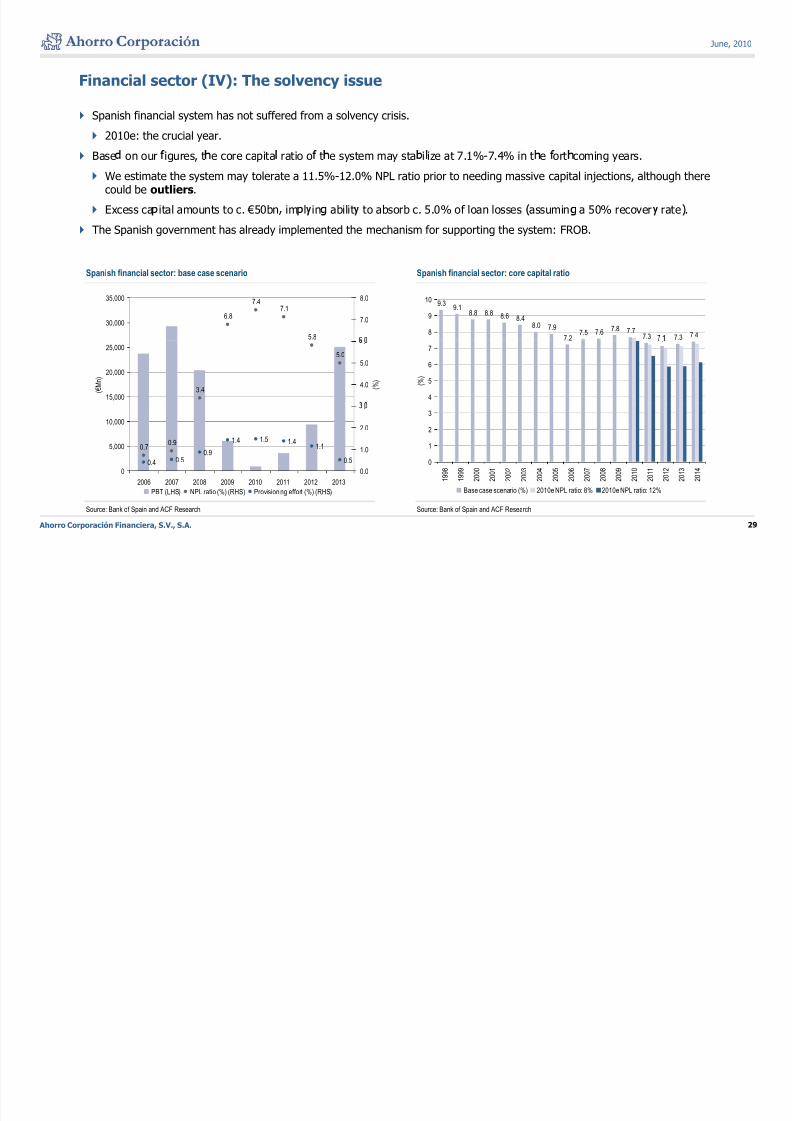

Spanish financial system has not suffered from a solvency crisis.

2010e: the crucial year.

Base on our igures, t e core capita ratio o t e system may sta i ize at 7.1%-7.4% in t e ort coming years.

We estimate the system may tolerate a 11.5%-12.0% NPL ratio prior to needing massive capital injections, although therecould be outliers.

Excess ca ital amounts to c. €50bn im l in abilit to absorb c. 5.0% of loan losses assumin a 50% recover rate .

The Spanish government has already implemented the mechanism for supporting the system: FROB.

Spanish financial sector: base case scenario Spanish financial sector: core capital ratio

6.8

7.47.1

5.8

30,000

35,000

7.0

8.0 9.39.1

8.8 8.8 8.6 8.48.0 7.9

7.27.5 7.6 7.8 7.7

7.3 7.3 7.48

9

10

3.4

5.0

15,000

20,000

25,000

( € M n )

4.0

5.0

.

( % )

.

4

5

6

7

( % )

0.70.9

0.4 0.50.9

1.4 1.5 1.41.1

0.5

5,000

10,000

1.0

2.0

.

0

1

2

3

Ahorro Corporación Financiera, S.V., S.A. 29

Source: Bank of Spain and ACF Research Source: Bank of Spain and ACF Research

0

2006 2007 2008 2009 2010 2011 2012 2013

0.0

PBT (LHS) NPL ratio (%) (RHS) Provisioning effort (%) (RHS)

1 9 9 8

1 9 9 9

2 0 0 0

2 0 0 1

2 0 0 2

2 0 0 3

2 0 0 4

2 0 0 5

2 0 0 6

2 0 0 7

2 0 0 8

2 0 0 9

2 0 1 0

2 0 1 1

2 0 1 2

2 0 1 3

2 0 1 4

Base case scenario (%) 2010e NPL ratio: 8% 2010e NPL ratio: 12%

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 30/70

June, 2010

Financial sector (V): FROB

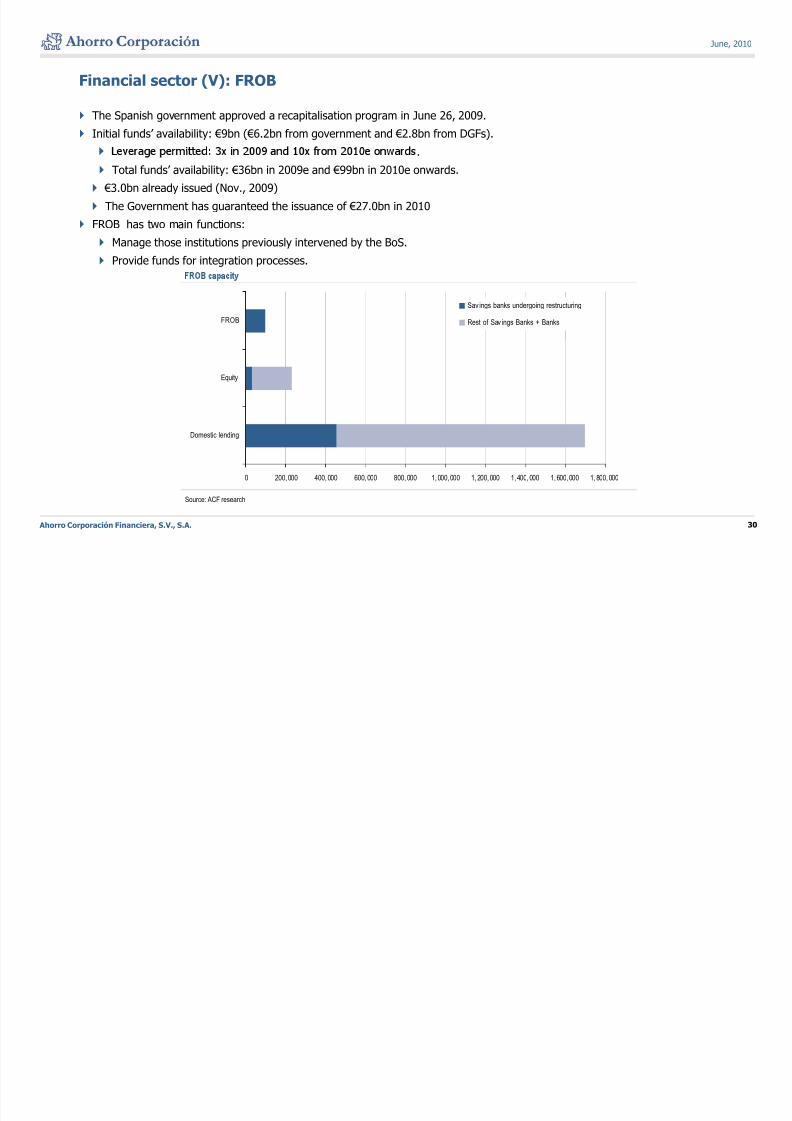

The Spanish government approved a recapitalisation program in June 26, 2009.

Initial funds’ availability: €9bn (€6.2bn from government and €2.8bn from DGFs).

.

Total funds’ availability: €36bn in 2009e and €99bn in 2010e onwards.

€3.0bn already issued (Nov., 2009)

The Government has guaranteed the issuance of €27.0bn in 2010

FROB has two main functions:

Manage those institutions previously intervened by the BoS.

Provide funds for integration processes.

FROB

Sav ings banks undergoing restructuring

Rest of Sav ings Banks + Banks

Equity

Domestic lending

Ahorro Corporación Financiera, S.V., S.A. 30

0 200,000 400,000 600,000 800,000 1,000,000 1,200,000 1,400,000 1,600,000 1,800,000

Source: ACF research

J 2010

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 31/70

June, 2010

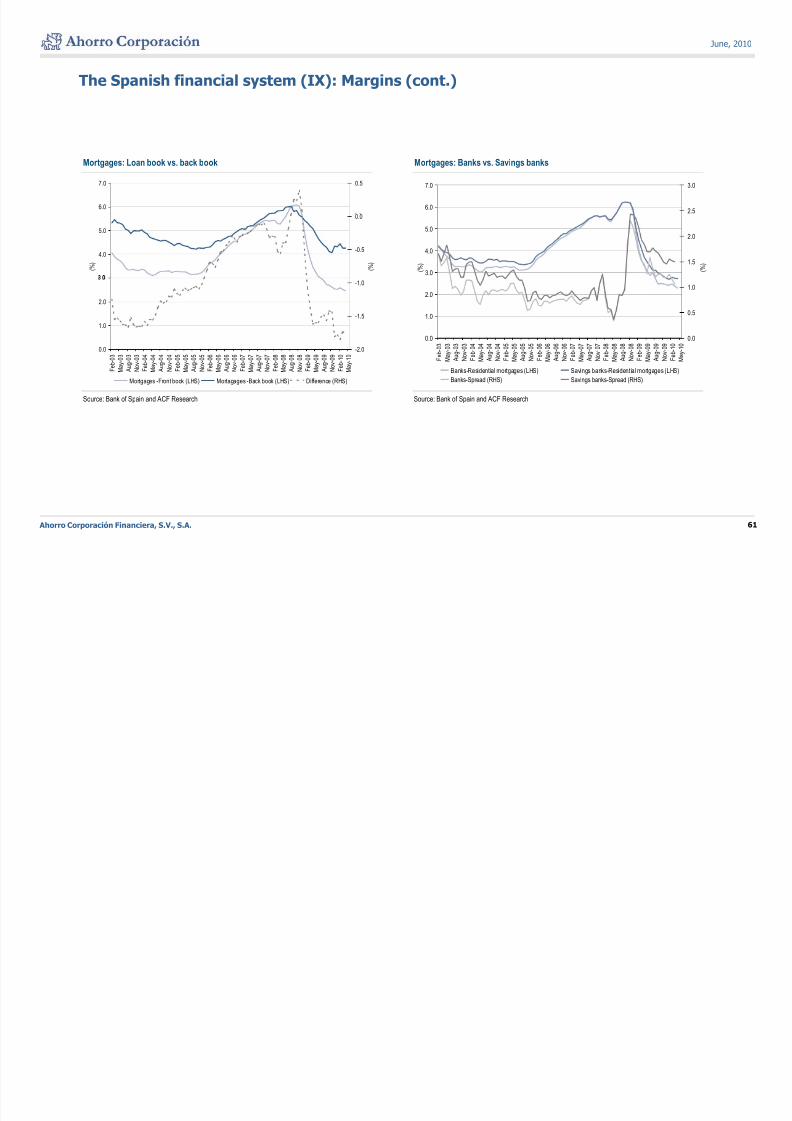

Financial sector (VI): Consolidation process

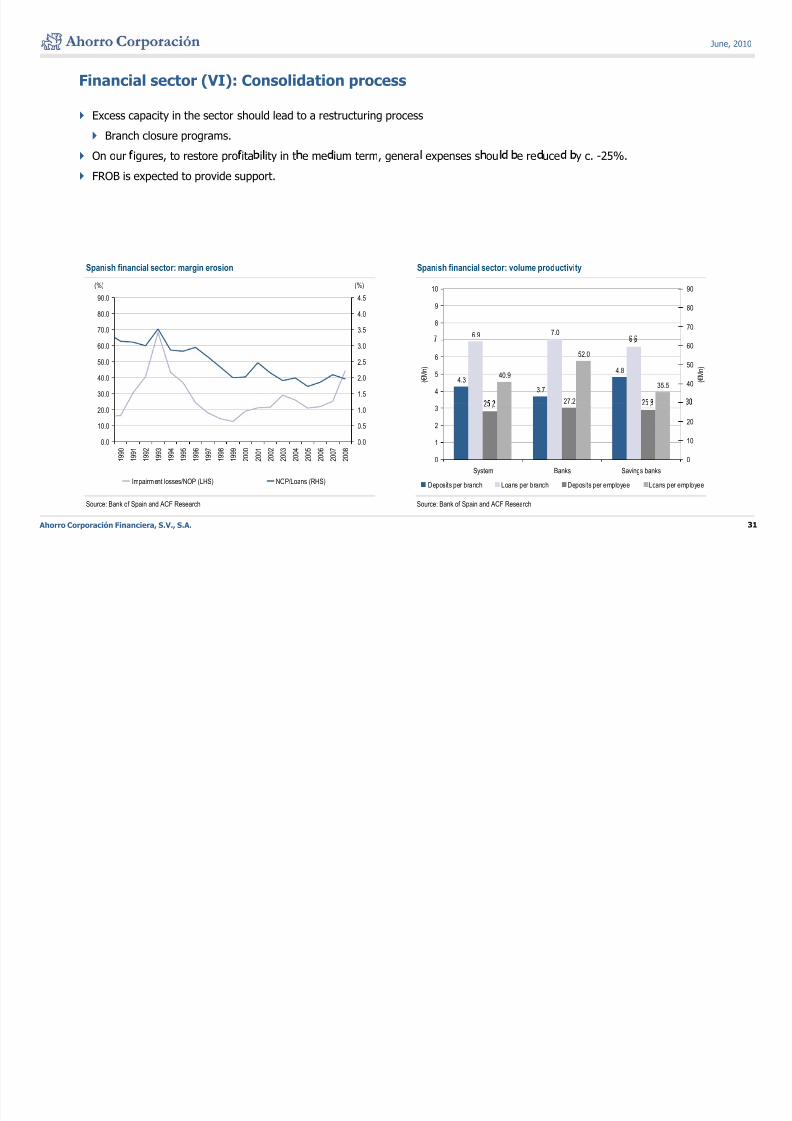

Excess capacity in the sector should lead to a restructuring process

Branch closure programs.

On our igures, to restore pro ita i ity in t e me ium term, genera expenses s ou e re uce y c. -25%.

FROB is expected to provide support.

Spanish financial sector: margin erosion Spanish financial sector: volume productivity

6.9 7.0

8

9

10

70

80

90

70.0

80.0

90.0

(%)

3.5

4.0

4.5

(%)

4.3

3.7

4.8

.

27.2

40.9

52.0

35.54

5

6

( € M n )

40

50

60

( € M n )

30.0

40.0

50.0

60.0

1.5

2.0

2.5

3.0

. .

0

1

2

3

0

10

20

0.0

10.0

20.0

1 9 9 0

1 9 9 1

1 9 9 2

1 9 9 3

1 9 9 4

1 9 9 5

1 9 9 6

1 9 9 7

1 9 9 8

1 9 9 9

2 0 0 0

2 0 0 1

2 0 0 2

2 0 0 3

2 0 0 4

2 0 0 5

2 0 0 6

2 0 0 7

2 0 0 8

0.0

0.5

1.0

Ahorro Corporación Financiera, S.V., S.A. 31

Source: Bank of Spain and ACF Research Source: Bank of Spain and ACF Research

System Banks Savings banks

Deposits per branch Loans per branch Deposits per employee Loans per employeeImpairment losses/NOP (LHS) NOP/Loans (RHS)

J ne 2010

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 32/70

June, 2010

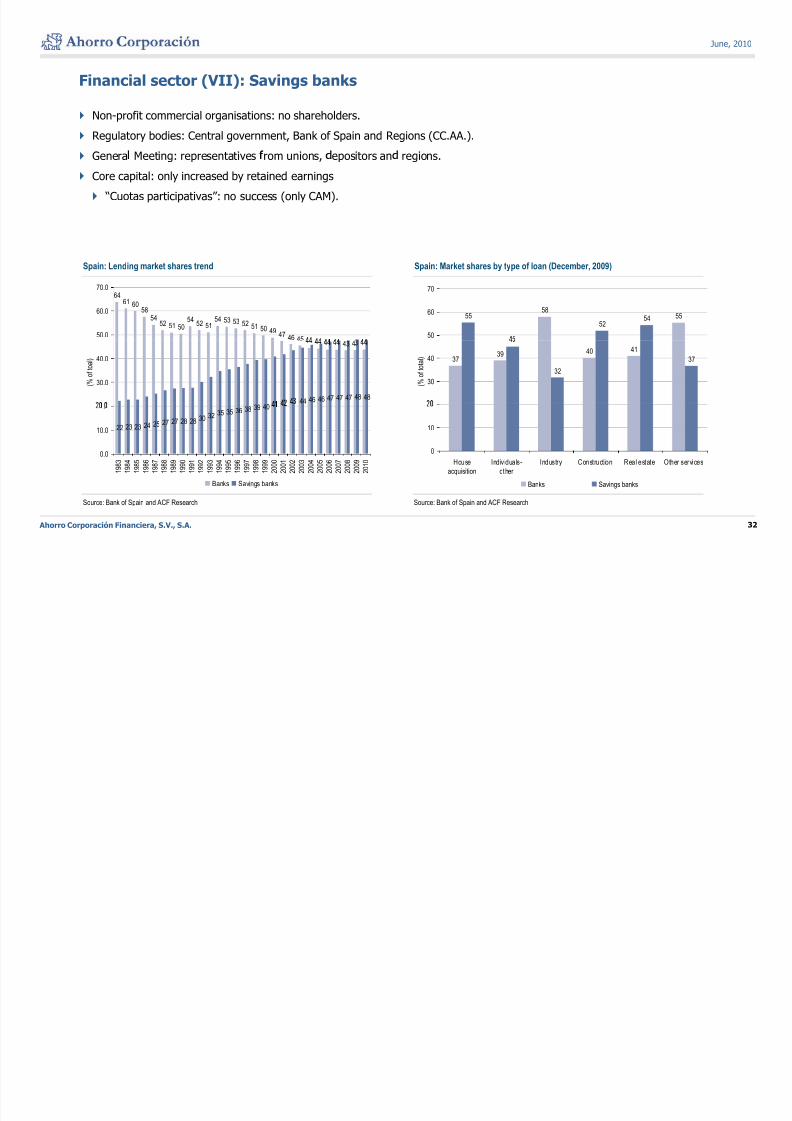

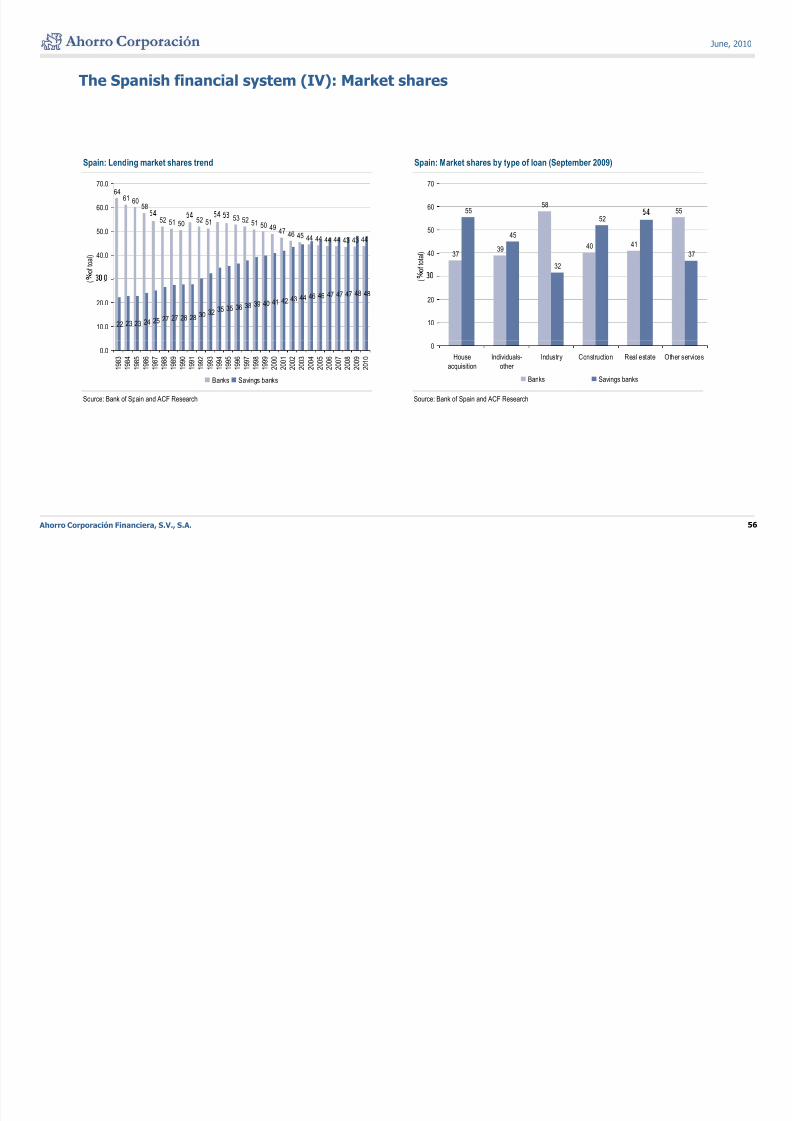

Financial sector (VII): Savings banks

Non-profit commercial organisations: no shareholders.

Regulatory bodies: Central government, Bank of Spain and Regions (CC.AA.).

Genera Meeting: representatives rom unions, epositors an regions.

Core capital: only increased by retained earnings

“Cuotas participativas”: no success (only CAM).

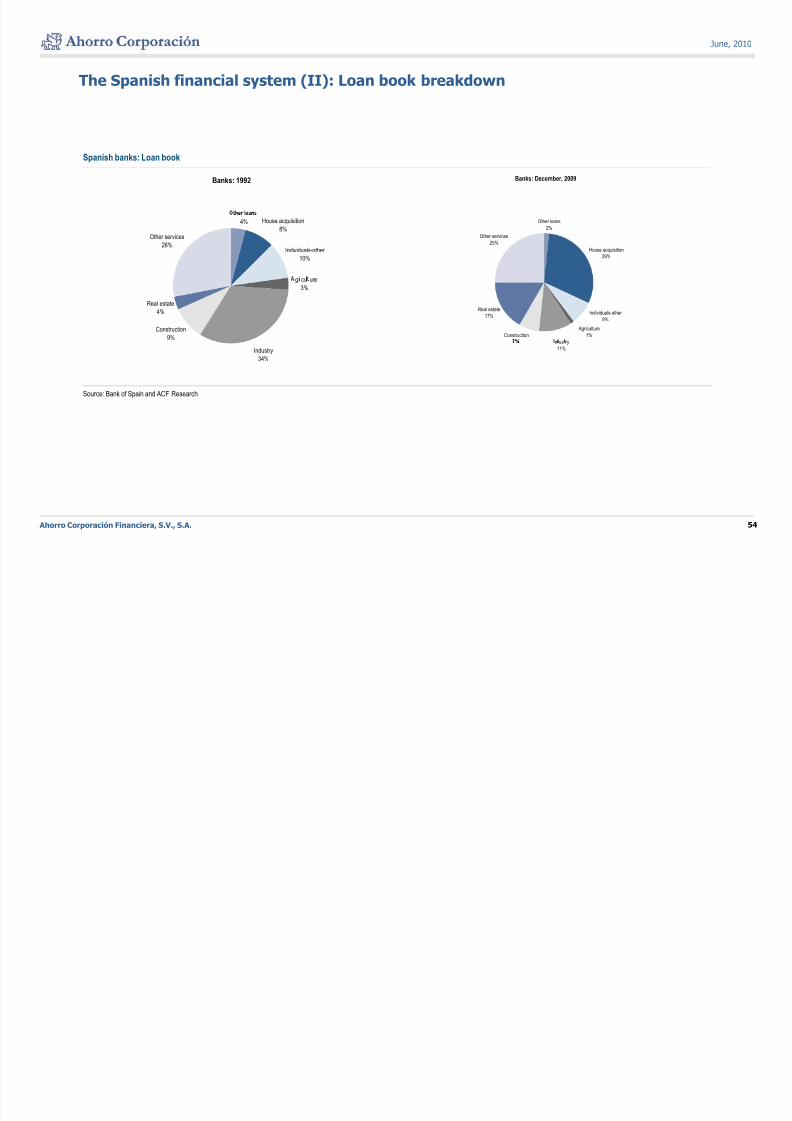

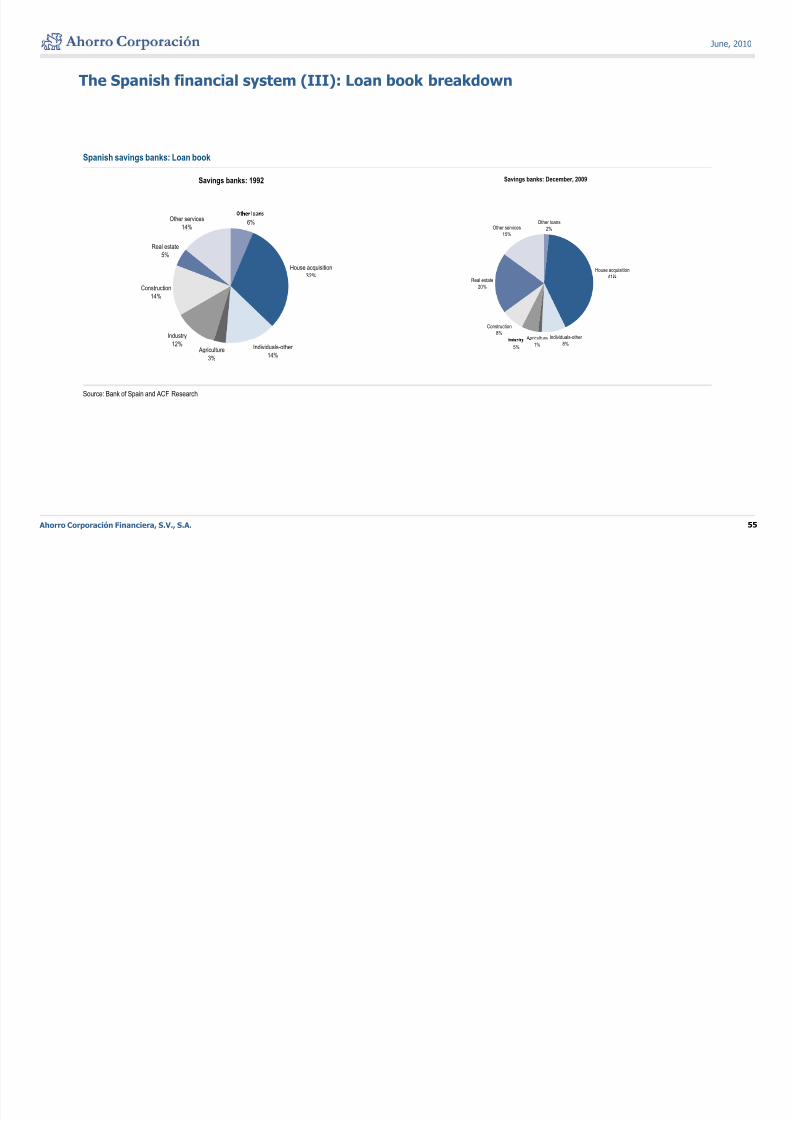

Spain: Lending market shares trend Spain: Market shares by type of loan (December, 2009)

6461 60

5854

52 51 5054

52 5154 53 53 52 51 50 49

47 46 4550.0

60.0

70.0

585555

5254

50

60

70

43 4

44 46 46 47 47 47 48 48

30.0

40.0

( % o

f t o a l ) 37

39 40 41

32

37

30

40

( % o

f t o t a l )

22 23 23 24 25 27 27 28 28 30 32 35 35 36 38 39 40

0.0

10.0

.

8 3

8 4

8 5

8 6

8 7

8 8

8 9

9 0

9 1

9 2

9 3

9 4

9 5

9 6

9 7

9 8

9 9

0 0

0 1

0 2

0 3

0 4

0 5

0 6

0 7

0 8

0 9

1 0

0

10

House Individuals- Industry Construction Real estate Other services

Ahorro Corporación Financiera, S.V., S.A. 32

Source: Bank of Spain and ACF Research Source: Bank of Spain and ACF Research

1 9

1 9

1 9

1 9

1 9

1 9

1 9

1 9

1 9

1 9

1 9

1 9

1 9

1 9

1 9

1 9

1 9

2 0

2 0

2 0

2 0

2 0

2 0

2 0

2 0

2 0

2 0

2 0

Banks Savings banks

acquisition other

Banks Savings banks

June 2010

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 33/70

June, 2010

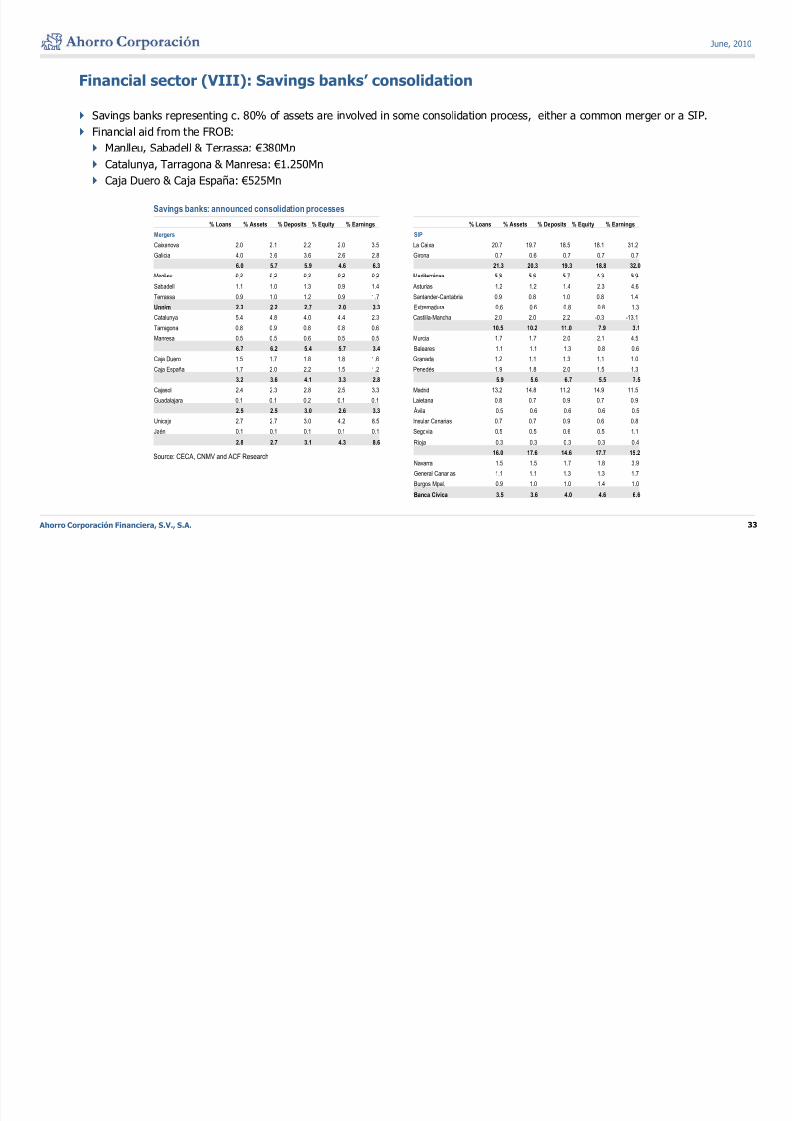

Financial sector (VIII): Savings banks’ consolidation

Savings banks representing c. 80% of assets are involved in some consolidation process, either a common merger or a SIP.

Financial aid from the FROB:

Manlleu Sabadell & Terrassa: €380Mn

Catalunya, Tarragona & Manresa: €1.250Mn

Caja Duero & Caja España: €525Mn

Savings banks: announced consolidation processes

% Loans % Assets % Deposits % Equity % Earnings % Loans % Assets % Deposits % Equity % Earnings

Mergers SIP

Caixanova 2.0 2.1 2.2 2.0 3.5 La Caixa 20.7 19.7 18.5 18.1 31.2

Galicia 4.0 3.6 3.6 2.6 2.8 Girona 0.7 0.6 0.7 0.7 0.7

6.0 5.7 5.9 4.6 6.3 21.3 20.3 19.3 18.8 32.0

Manlleu 0.3 0.2 0.3 0.2 0.2 Mediterráneo 5.8 5.6 5.7 4.3 8.9. . . . . . . . . .

Sabadell 1.1 1.0 1.3 0.9 1.4 Asturias 1.2 1.2 1.4 2.3 4.6

Terrassa 0.9 1.0 1.2 0.9 1.7 Santander-Cantabria 0.9 0.8 1.0 0.8 1.4Unnim 2.3 2.2 2.7 2.0 3.3 Extremadura 0.6 0.6 0.8 0.8 1.3

Catalunya 5.4 4.8 4.0 4.4 2.3 Castilla-Mancha 2.0 2.0 2.2 -0.3 -13.1

Tarragona 0.8 0.9 0.8 0.8 0.6 10.5 10.2 11.0 7.9 3.1

Manresa 0.5 0.5 0.6 0.5 0.5 Murcia 1.7 1.7 2.0 2.1 4.5

6.7 6.2 5.4 5.7 3.4 Baleares 1.1 1.1 1.3 0.8 0.6

Caja Duero 1.5 1.7 1.8 1.8 1.6 Granada 1.2 1.1 1.3 1.1 1.0

Caja España 1.7 2.0 2.2 1.5 1.2 Penedés 1.9 1.8 2.0 1.5 1.3

3.2 3.6 4.1 3.3 2.8 5.9 5.6 6.7 5.5 7.5

Cajasol 2.4 2.3 2.8 2.5 3.3 Madrid 13.2 14.8 11.2 14.9 11.5

Guadalajara 0.1 0.1 0.2 0.1 0.1 Laietana 0.8 0.7 0.9 0.7 0.92.5 2.5 3.0 2.6 3.3 Ávila 0.5 0.6 0.6 0.6 0.5

Unicaja 2.7 2.7 3.0 4.2 8.5 Insular Canarias 0.7 0.7 0.9 0.6 0.8

Jaén 0.1 0.1 0.1 0.1 0.1 Segovia 0.5 0.5 0.6 0.5 1.1

2.8 2.7 3.1 4.3 8.6 Rioja 0.3 0.3 0.3 0.3 0.4

16.0 17.6 14.6 17.7 15.2

Navarra 1.5 1.5 1.7 1.8 3.9Source: CECA, CNMV and ACF Research

Ahorro Corporación Financiera, S.V., S.A. 33

General Canarias 1.1 1.1 1.3 1.3 1.7

Burgos Mpal. 0.9 1.0 1.0 1.4 1.0

Banca Cívica 3.5 3.6 4.0 4.6 6.6

June 2010

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 34/70

June, 2010

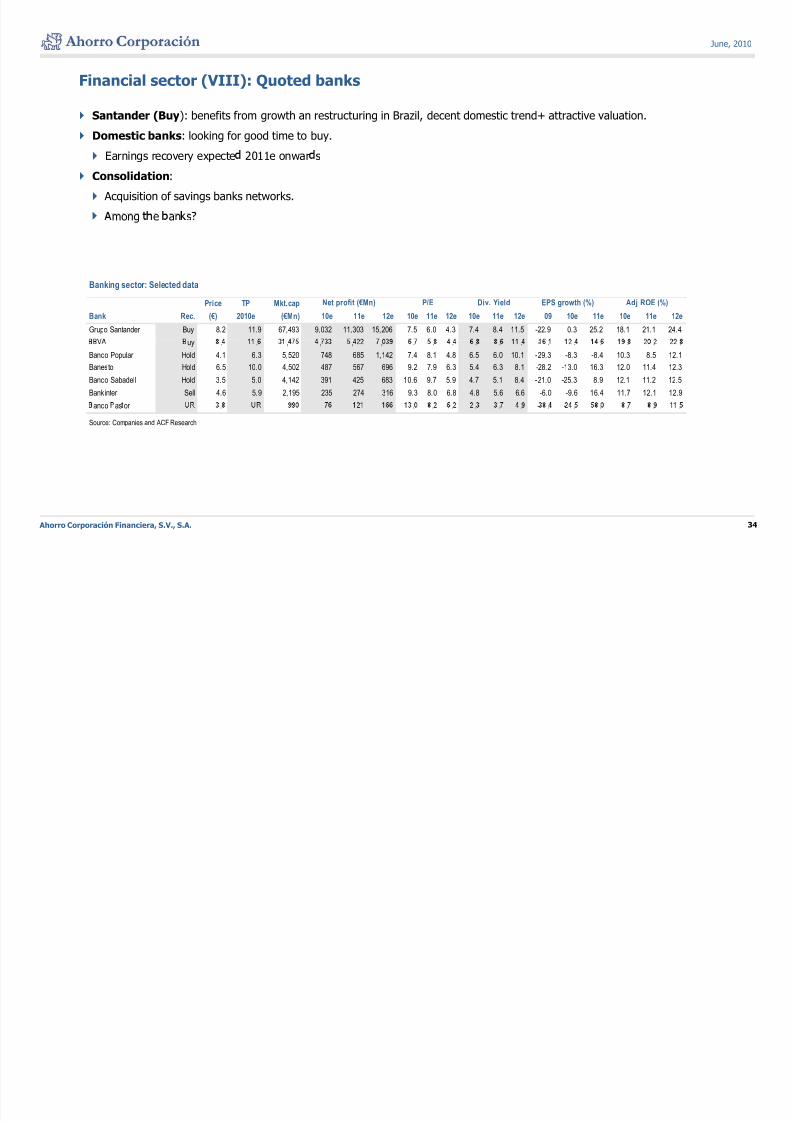

Financial sector (VIII): Quoted banks

Santander (Buy): benefits from growth an restructuring in Brazil, decent domestic trend+ attractive valuation.

Domestic banks: looking for good time to buy.

Earnings recovery expecte 2011e onwar s

Consolidation:

Acquisition of savings banks networks.

mong e an s

Banking sector: Selected data

Price TP Mkt.cap

Bank Rec. (€) 2010e (€Mn) 10e 11e 12e 10e 11e 12e 10e 11e 12e 09 10e 11e 10e 11e 12e

Grupo Santander Buy 8.2 11.9 67,493 9,032 11,303 15,206 7.5 6.0 4.3 7.4 8.4 11.5 -22.9 0.3 25.2 18.1 21.1 24.4

Net profit (€Mn) Adj ROE (%)EPS growth (%)P/E Div. Yield

uy . . , , , , . . . . . . - . . . . . .

Banco Popular Hold 4.1 6.3 5,520 748 685 1,142 7.4 8.1 4.8 6.5 6.0 10.1 -29.3 -8.3 -8.4 10.3 8.5 12.1

Banesto Hold 6.5 10.0 4,502 487 567 696 9.2 7.9 6.3 5.4 6.3 8.1 -28.2 -13.0 16.3 12.0 11.4 12.3

Banco Sabadell Hold 3.5 5.0 4,142 391 425 683 10.6 9.7 5.9 4.7 5.1 8.4 -21.0 -25.3 8.9 12.1 11.2 12.5

Bankinter Sell 4.6 5.9 2,195 235 274 316 9.3 8.0 6.8 4.8 5.6 6.6 -6.0 -9.6 16.4 11.7 12.1 12.9

Source: Companies and ACF Research

anco as or . . . . . . . - . - . . . . .

Ahorro Corporación Financiera, S.V., S.A. 34

June, 2010

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 35/70

June, 2010

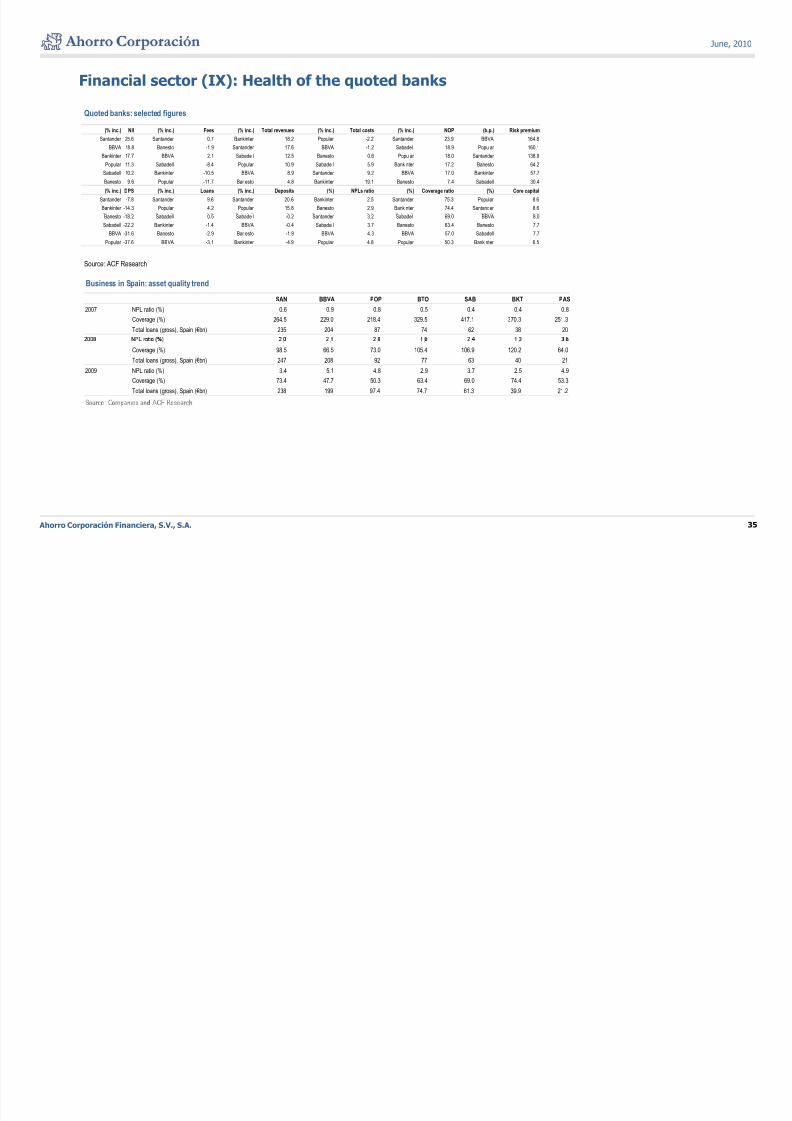

Financial sector (IX): Health of the quoted banks

Quoted banks: selected figures

(% inc.) NII (% inc.) Fees (% inc.) Total revenues (% inc.) Total costs (% inc.) NOP (b.p.) Risk premium

Santander 25.6 Santander 0.7 Bankinter 18.2 Popular -2.2 Santander 23.9 BBVA 164.8

BBVA 18.8 Banesto -1.9 Santander 17.6 BBVA -1.2 Sabadell 18.9 Popular 160.1

Bankinter 17.7 BBVA -2.1 Sabadell 12.5 Banesto 0.6 Popular 18.0 Santander 138.9

Popular 11.3 Sabadell -8.4 Popular 10.9 Sabadell 5.9 Bankinter 17.2 Banesto 64.2

Sabadell 10.2 Bankinter -10.5 BBVA 8.9 Santander 9.2 BBVA 17.0 Bankinter 57.7

Banesto 9.6 Popular -11.7 Banesto 4.8 Bankinter 19.1 Banesto 7.4 Sabadell 30.4

(% inc.) DPS (% inc.) Loans (% inc.) Deposits (%) NPLs ratio (%) Coverage ratio (%) Core capital

Santander -7.8 Santander 9.6 Santander 20.6 Bankinter 2.5 Santander 75.3 Popular 8.6

Bankinter -14.3 Popular 4.2 Popular 15.8 Banesto 2.9 Bankinter 74.4 Santander 8.6

Source: ACF Research

Banesto -18.2 Sabadell 0.5 Sabadell -0.2 Santander 3.2 Sabadell 69.0 BBVA 8.0

Sabadell -22.2 Bankinter -1.4 BBVA -0.4 Sabadell 3.7 Banesto 63.4 Banesto 7.7

BBVA -31.6 Banesto -2.9 Banesto -1.9 BBVA 4.3 BBVA 57.0 Sabadell 7.7

Popular -37.6 BBVA -3.1 Bankinter -4.9 Popular 4.8 Popular 50.3 Bankinter 6.5

Business in Spain: asset quality trend

SAN BBVA POP BTO SAB BKT PAS2007 NPL ratio (%) 0.6 0.9 0.8 0.5 0.4 0.4 0.8

Coverage (%) 264.5 229.0 218.4 329.5 417.1 370.3 251.3

Total loans (gross), Spain (€bn) 235 204 87 74 62 38 20

. . . . . . .

Coverage (%) 98.5 66.5 73.0 105.4 106.9 120.2 64.0

Total loans (gross), Spain (€bn) 247 208 92 77 63 40 21

2009 NPL ratio (%) 3.4 5.1 4.8 2.9 3.7 2.5 4.9

Coverage (%) 73.4 47.7 50.3 63.4 69.0 74.4 53.3

Total loans (gross), Spain (€bn) 238 199 97.4 74.7 61.3 39.9 21.2

Ahorro Corporación Financiera, S.V., S.A. 35

June, 2010

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 36/70

,

Ahorro Corporación Financiera, S.V., S.A. 36

June, 2010

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 37/70

Annex

Annex 1. Population and employment

Annex 2. Housing mar et in Spain

Annex 3. Spanish financial system

Annex 4. Spanish Government and external debt

Ahorro Corporación Financiera, S.V., S.A. 37

June, 2010

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 38/70

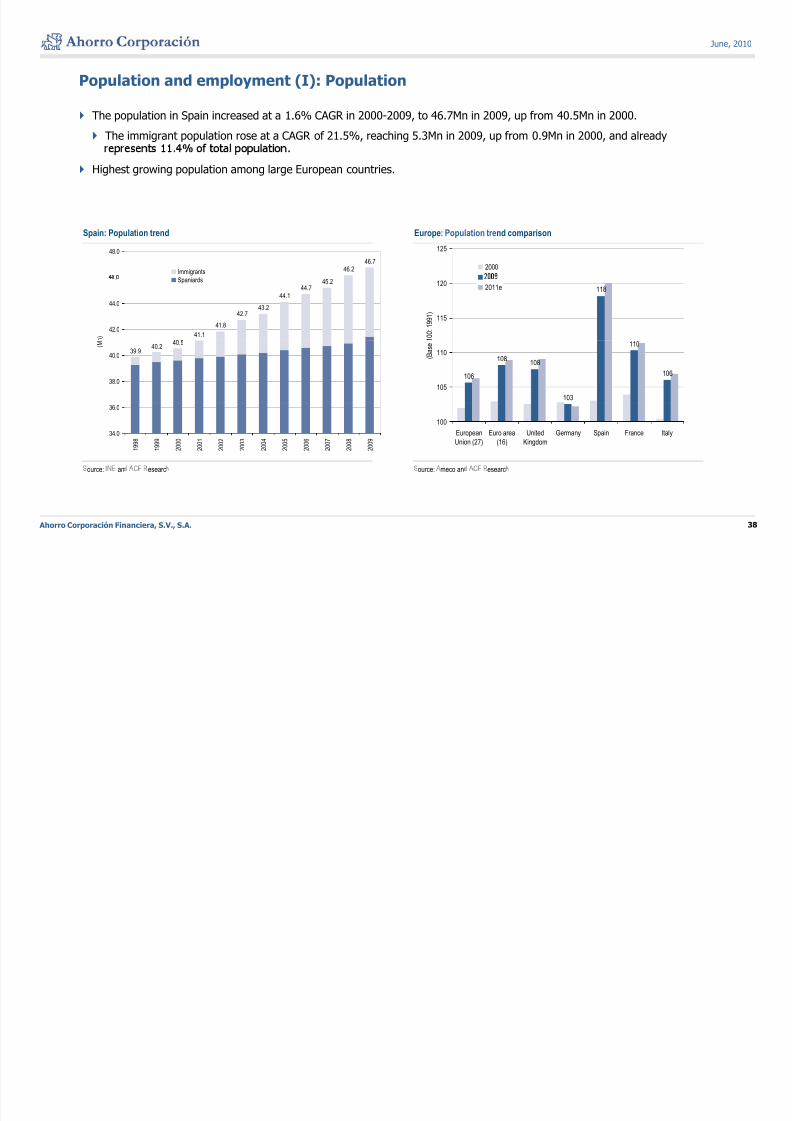

Population and employment (I): Population

The population in Spain increased at a 1.6% CAGR in 2000-2009, to 46.7Mn in 2009, up from 40.5Mn in 2000.

The immigrant population rose at a CAGR of 21.5%, reaching 5.3Mn in 2009, up from 0.9Mn in 2000, and already

Highest growing population among large European countries.

Spain: Population trend Europe: Population trend comparison

125

200046.246.7

48.0

Immigrants

118

115

120

1 0 0 : 1 9 9 1 )

2011e

41.1

41.8

42.743.2

44.144.7

45.2

42.0

44.0

.

n )

Spaniards

106

108108

103

110

106

105

110 ( B a s e

39.940.2

40.5

38.0

40.0

( M

100

European

Union (27)

Euro area

(16)

United

Kingdom

Germany Spain France Italy34.0

36.0

1 9 9 8

1 9 9 9

2 0 0 0

2 0 0 1

2 0 0 2

2 0 0 3

2 0 0 4

2 0 0 5

2 0 0 6

2 0 0 7

2 0 0 8

2 0 0 9

Ahorro Corporación Financiera, S.V., S.A. 38

ource: an esearc ource: meco an esearc

June, 2010

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 39/70

Population and employment (II): Population estimates

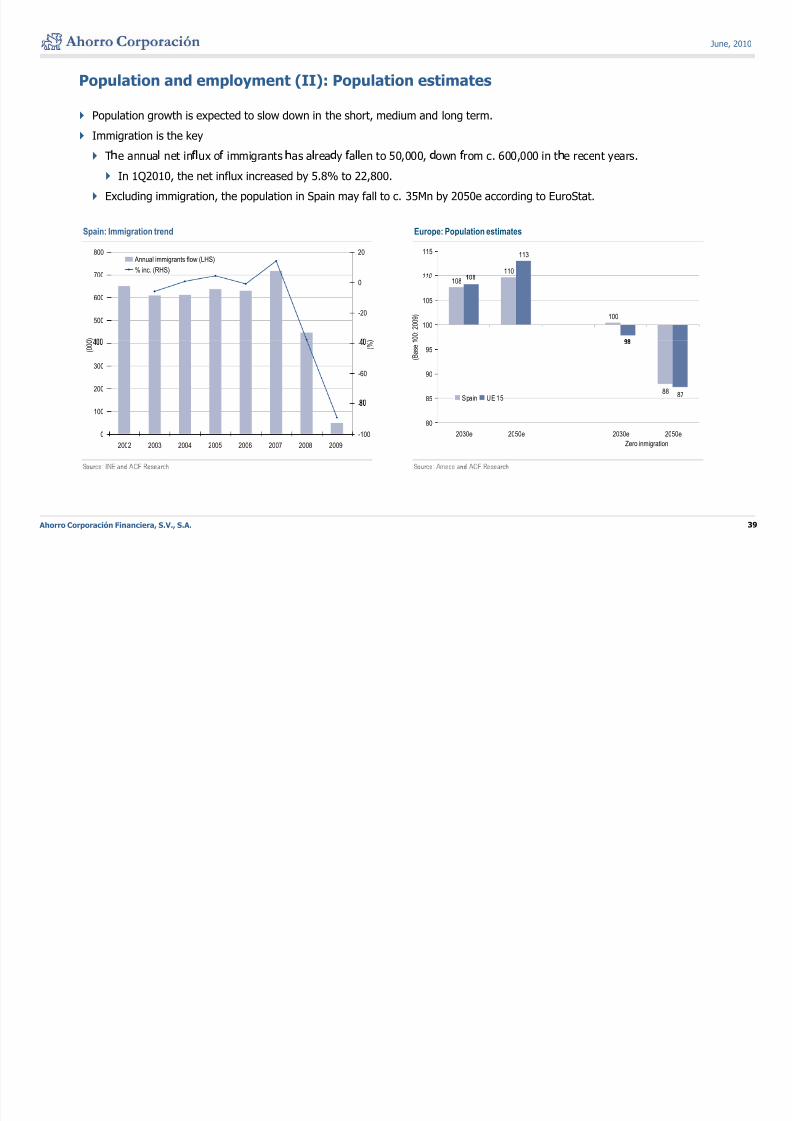

Population growth is expected to slow down in the short, medium and long term.

Immigration is the key

T e annua net in ux o immigrants as a rea y a en to 50,000, own rom c. 600,000 in t e recent years.

In 1Q2010, the net influx increased by 5.8% to 22,800.

Excluding immigration, the population in Spain may fall to c. 35Mn by 2050e according to EuroStat.

Spain: Immigration trend Europe: Population estimates

110

113

110

115

700

800 20 Annual immigrants flow (LHS)

% inc. (RHS)

108

100

100

105

0 0 :

2 0 0 9 )

500

600

)

-20

0

88 8785

90

95 ( B a s e

1

Spain UE 15

200

300

( 0 0 0

-60

- ( % )

80

2030e 2050e 2030e 2050e

Zero inmigration

0

100

2002 2003 2004 2005 2006 2007 2008 2009

-100

-

Ahorro Corporación Financiera, S.V., S.A. 39

June, 2010

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 40/70

Population and employment (III): Active population

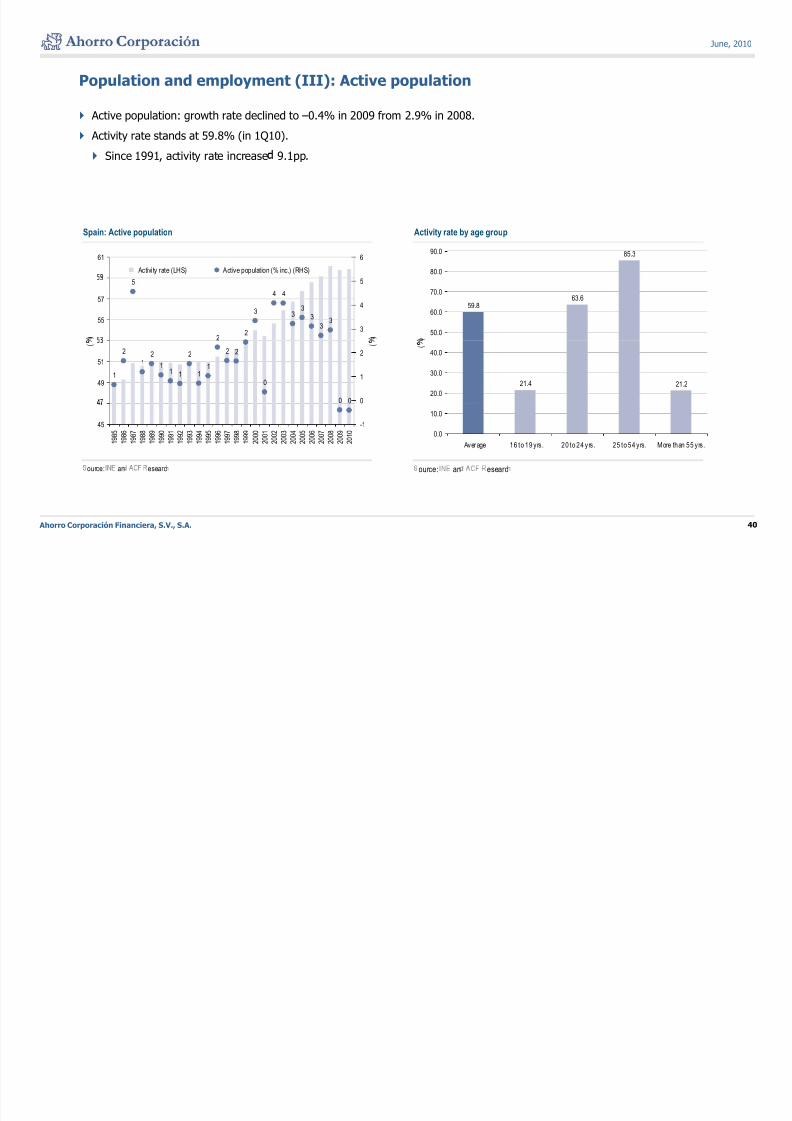

Active population: growth rate declined to –0.4% in 2009 from 2.9% in 2008.

Activity rate stands at 59.8% (in 1Q10).

Since 1991, activity rate increase 9.1pp.

Spain: Active population Activity rate by age group

61 6

Activity rate (LHS) Active population (% inc.) (RHS)

85.3

80.0

90.0

5

22

3

4 4

33

3

3355

57

)

3

4

5

)

59.8 63.6

50.0

60.0

70.0

)

1

2

12

11 1

2

11

2 2

0

0 0

49

51

(

0

1

2

(

21.4 21.2

20.0

30.0

40.0 (

45

1 9 8 5

1 9 8 6

1 9 8 7

1 9 8 8

1 9 8 9

1 9 9 0

1 9 9 1

1 9 9 2

1 9 9 3

1 9 9 4

1 9 9 5

1 9 9 6

1 9 9 7

1 9 9 8

1 9 9 9

2 0 0 0

2 0 0 1

2 0 0 2

2 0 0 3

2 0 0 4

2 0 0 5

2 0 0 6

2 0 0 7

2 0 0 8

2 0 0 9

2 0 1 0

-1

0.0

10.0

Average 16 to 19 yrs. 20 to 24 yrs. 25 to 54 yrs. More than 55 yrs.

Ahorro Corporación Financiera, S.V., S.A. 40

ource: an esearc ource: an esearc

June, 2010

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 41/70

Population and employment (IV): Employment

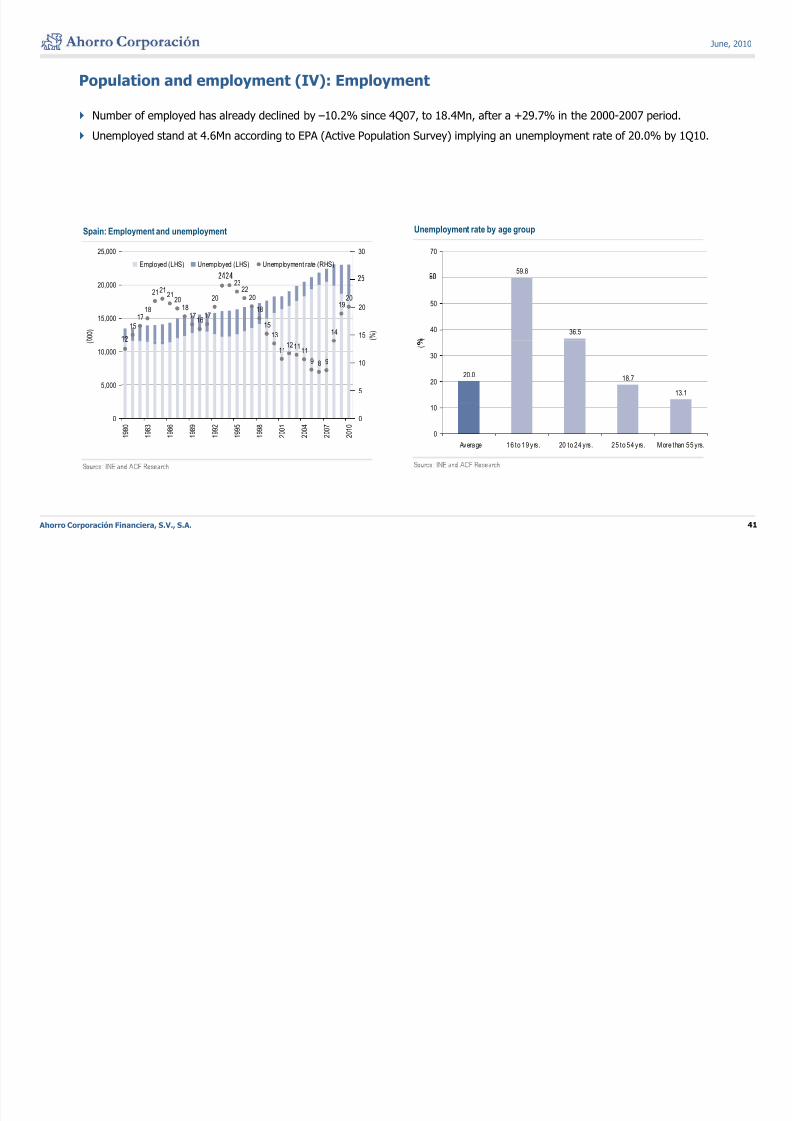

Number of employed has already declined by –10.2% since 4Q07, to 18.4Mn, after a +29.7% in the 2000-2007 period.

Unemployed stand at 4.6Mn according to EPA (Active Population Survey) implying an unemployment rate of 20.0% by 1Q10.

Spain: Employment and unemployment Unemployment rate by age group

25,000 30

Employed (LHS) Unemployed (LHS) Unemployment rate (RHS)59.8

70

15

1718

212121

201817

1617

20

2322

20

18

15

13 14

1920

15,000

20,000

0 0 0 )

15

20

( % ) 36.540

50

)

111211

11

9 8 9

5,000

10,000

(

5

10

20.0 18.7

13.1

20

30

(

0

1 9 8 0

1 9 8 3

1 9 8 6

1 9 8 9

1 9 9 2

1 9 9 5

1 9 9 8

2 0 0 1

2 0 0 4

2 0 0 7

2 0 1 0

0

0

10

Average 16 to 19 yrs. 20 to 24 yrs. 25 to 54 yrs. More than 55 yrs.

Ahorro Corporación Financiera, S.V., S.A. 41

June, 2010

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 42/70

Population and employment (V): Employment (cont.)

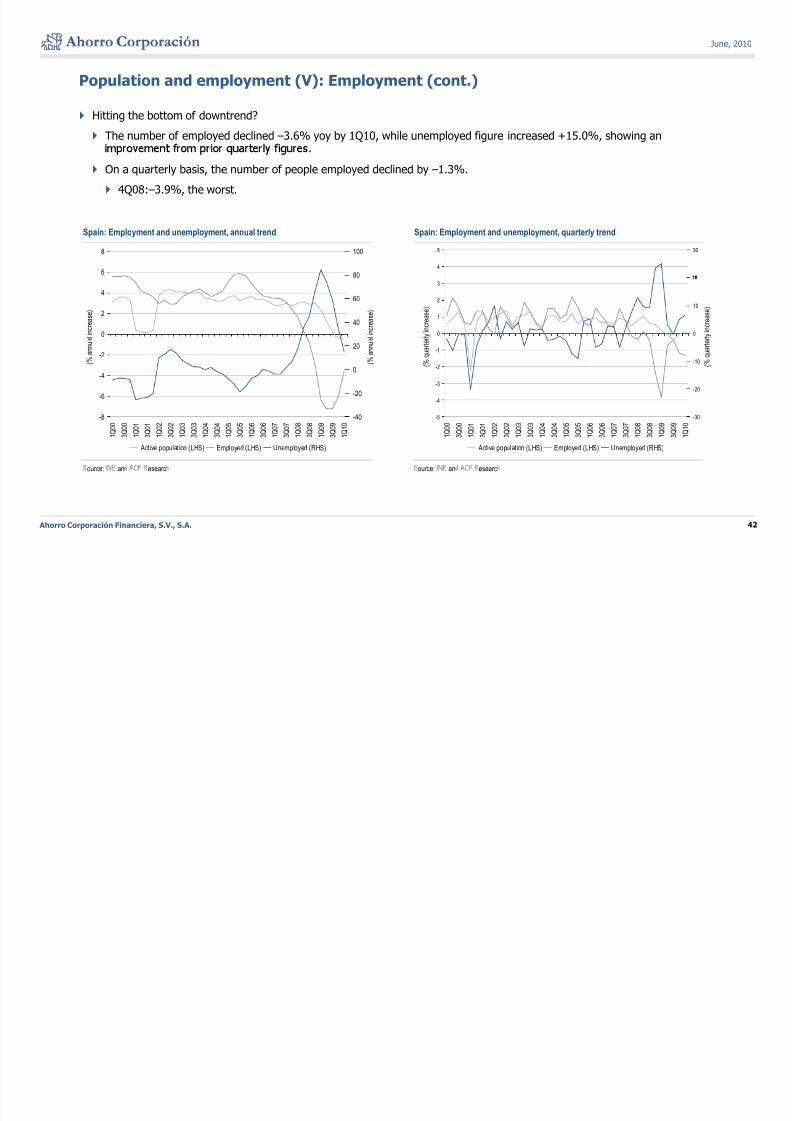

Hitting the bottom of downtrend?

The number of employed declined –3.6% yoy by 1Q10, while unemployed figure increased +15.0%, showing an

On a quarterly basis, the number of people employed declined by –1.3%.

4Q08:–3.9%, the worst.

Spain: Employment and unemployment, annual trend Spain: Employment and unemployment, quarterly trend

6

8

80

100

4

5 30

0

2

4

a l i n c r e a s e )

40

60

a l i n c r e a s e )

0

1

2

3

r l y i n c r e a s e )

0

10

r l y i n c r e a s e )

-6

-4

-2 ( %

a n n u

-20

0

20

( % a

n n u

-4

-3

-2

-1

( % q

u a r t e

-20

-10 ( %

q u a r t e

-8

1 Q 0 0

3 Q 0 0

1 Q 0 1

3 Q 0 1

1 Q 0 2

3 Q 0 2

1 Q 0 3

3 Q 0 3

1 Q 0 4

3 Q 0 4

1 Q 0 5

3 Q 0 5

1 Q 0 6

3 Q 0 6

1 Q 0 7

3 Q 0 7

1 Q 0 8

3 Q 0 8

1 Q 0 9

3 Q 0 9

1 Q 1 0

-40

Active population (LHS) Employed (LHS) Unemployed (RHS)

-5

1 Q 0 0

3 Q 0 0

1 Q 0 1

3 Q 0 1

1 Q 0 2

3 Q 0 2

1 Q 0 3

3 Q 0 3

1 Q 0 4

3 Q 0 4

1 Q 0 5

3 Q 0 5

1 Q 0 6

3 Q 0 6

1 Q 0 7

3 Q 0 7

1 Q 0 8

3 Q 0 8

1 Q 0 9

3 Q 0 9

1 Q 1 0

-30

Active population (LHS) Employed (LHS) Unemployed (RHS)

Ahorro Corporación Financiera, S.V., S.A. 42

ource: an esearc ource: an esearc

June, 2010

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 43/70

Population and employment (VI): Unemployment rate

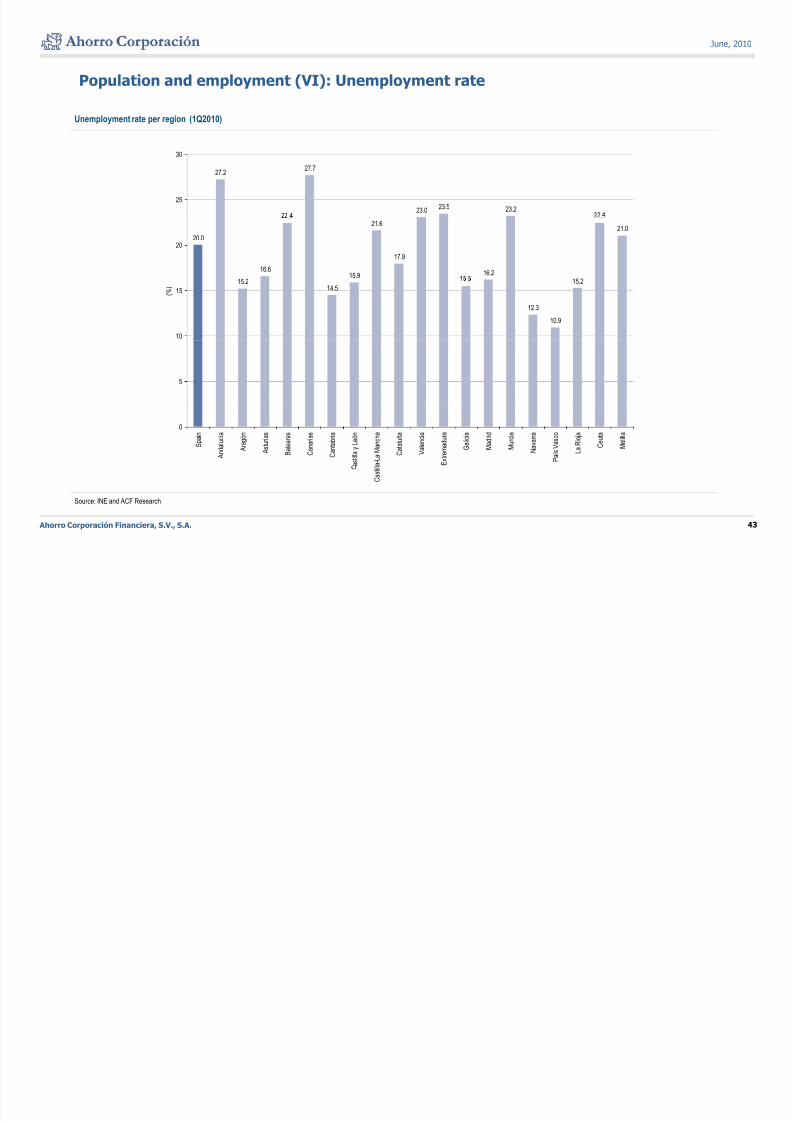

Unemployment rate per region (1Q2010)

27.227.7

23.0 23.5 23.2

25

30

20.0

16.6

.

15.9

21.6

17.9

16.2

.

21.0

20

15.214.5

.

12.3

10.9

15.2

10

15 ( % )

5

0

S p a i n

A n d a l u c í a

A r a g ó n

A s t u r i a s

B a l e a r e s

C a n a r i a s

C a n t a b r i a

a s t i l l a y L e ó n

l a - L a M a n c h a

C a t a l u ñ a

V a l e n c i a

E x t r e m a d u r a

G a l i c i a

M a d r i d

M u r c i a

N a v a r r a

P a í s V a s c o

L a R i o j a

C e u t a

M e l i l l a

Ahorro Corporación Financiera, S.V., S.A. 43

Source: INE and ACF Research

C a s t i l

June, 2010

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 44/70

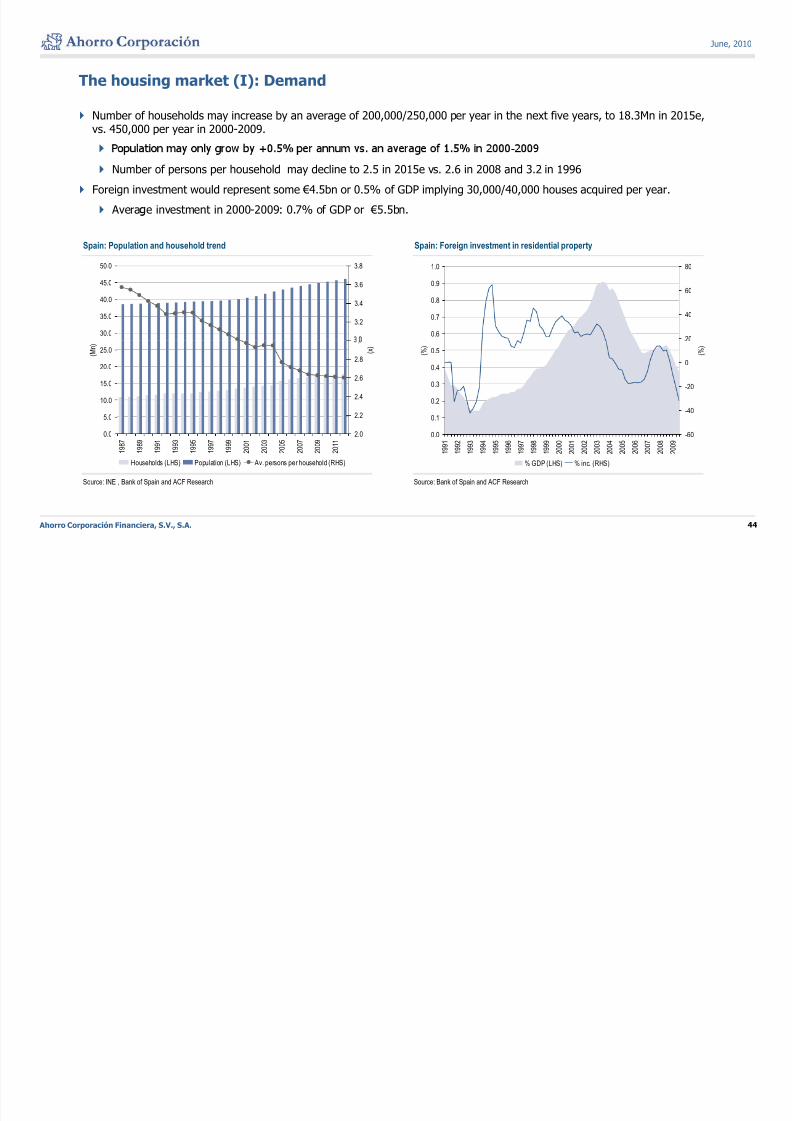

The housing market (I): Demand

Number of households may increase by an average of 200,000/250,000 per year in the next five years, to 18.3Mn in 2015e,vs. 450,000 per year in 2000-2009.

-

Number of persons per household may decline to 2.5 in 2015e vs. 2.6 in 2008 and 3.2 in 1996

Foreign investment would represent some €4.5bn or 0.5% of GDP implying 30,000/40,000 houses acquired per year.

Avera e investment in 2000-2009: 0.7% of GDP or €5.5bn.

Spain: Population and household trend Spain: Foreign investment in residential property

50.0 3.8 1.0 80

30.0

35.0

40.0

45.0

3.2

3.4

3.6

0.6

0.7

0.8

0.9

20

40

60

10.0

15.0

20.0

25.0 ( M n )

2.4

2.6

2.8

.

( x )

0.2

0.3

0.4

0.5 ( % )

-20

0

( % )

0.0

5.0

1 9 8 7

1 9 8 9

1 9 9 1

1 9 9 3

1 9 9 5

1 9 9 7

1 9 9 9

2 0 0 1

2 0 0 3

2 0 0 5

2 0 0 7

2 0 0 9

2 0 1 1

2.0

2.2

Households (LHS) Population (LHS) Av. persons per household (RHS)

0.0

0.1

1 9 9 1

1 9 9 2

1 9 9 3

1 9 9 4

1 9 9 5

1 9 9 6

1 9 9 7

1 9 9 8

1 9 9 9

2 0 0 0

2 0 0 1

2 0 0 2

2 0 0 3

2 0 0 4

2 0 0 5

2 0 0 6

2 0 0 7

2 0 0 8

2 0 0 9

-60

-40

% GDP (LHS) % inc. (RHS)

Ahorro Corporación Financiera, S.V., S.A. 44

Source: INE , Bank of Spain and ACF Research Source: Bank of Spain and ACF Research

June, 2010

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 45/70

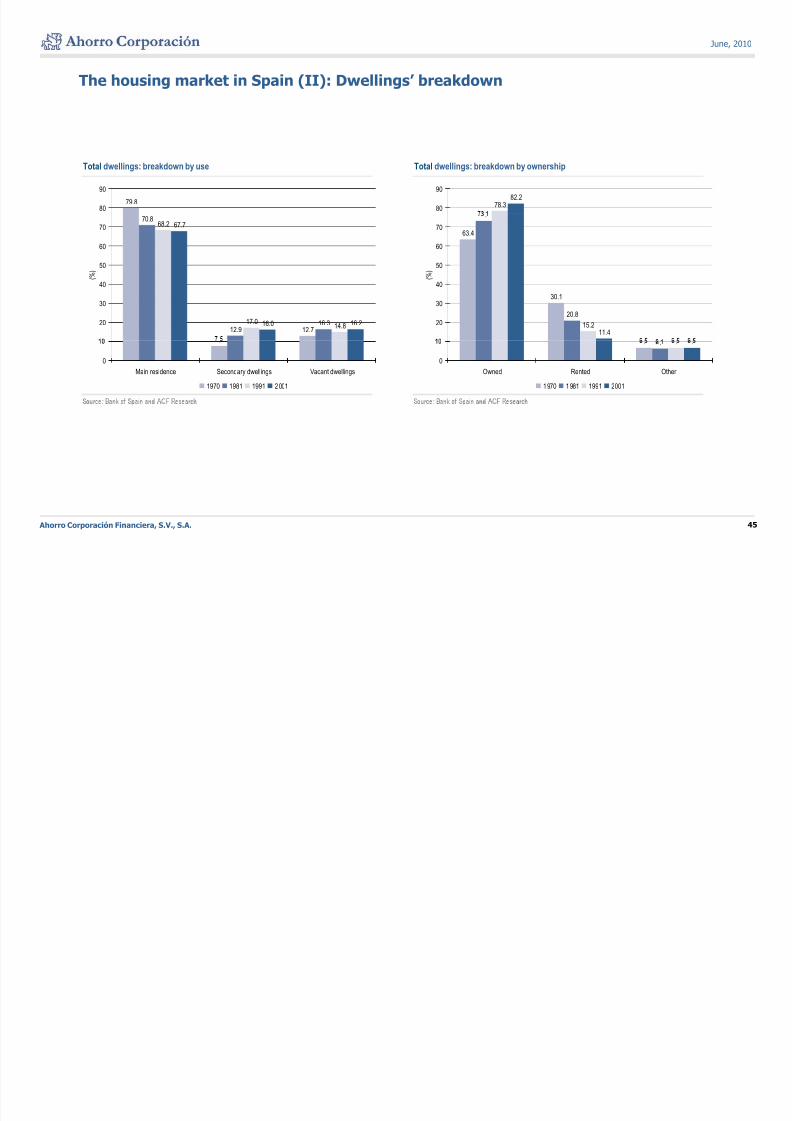

The housing market in Spain (II): Dwellings’ breakdown

Total dwellings: breakdown by use Total dwellings: breakdown by ownership

78.3

82.2

80

90

79.880

90

63.4

.

50

60

70

% )

70.868.2 67.7

50

60

70

% )

30.1

20.8

15.211.4

20

30

40 (

12.712.916.317.0

14.816.0 16.220

30

40 (

. . . .

0

Owned Rented Other

1970 1981 1991 2001

.

0

Main residence Secondary dwellings Vacant dwellings

1970 1981 1991 2001

Ahorro Corporación Financiera, S.V., S.A. 45

June, 2010

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 46/70

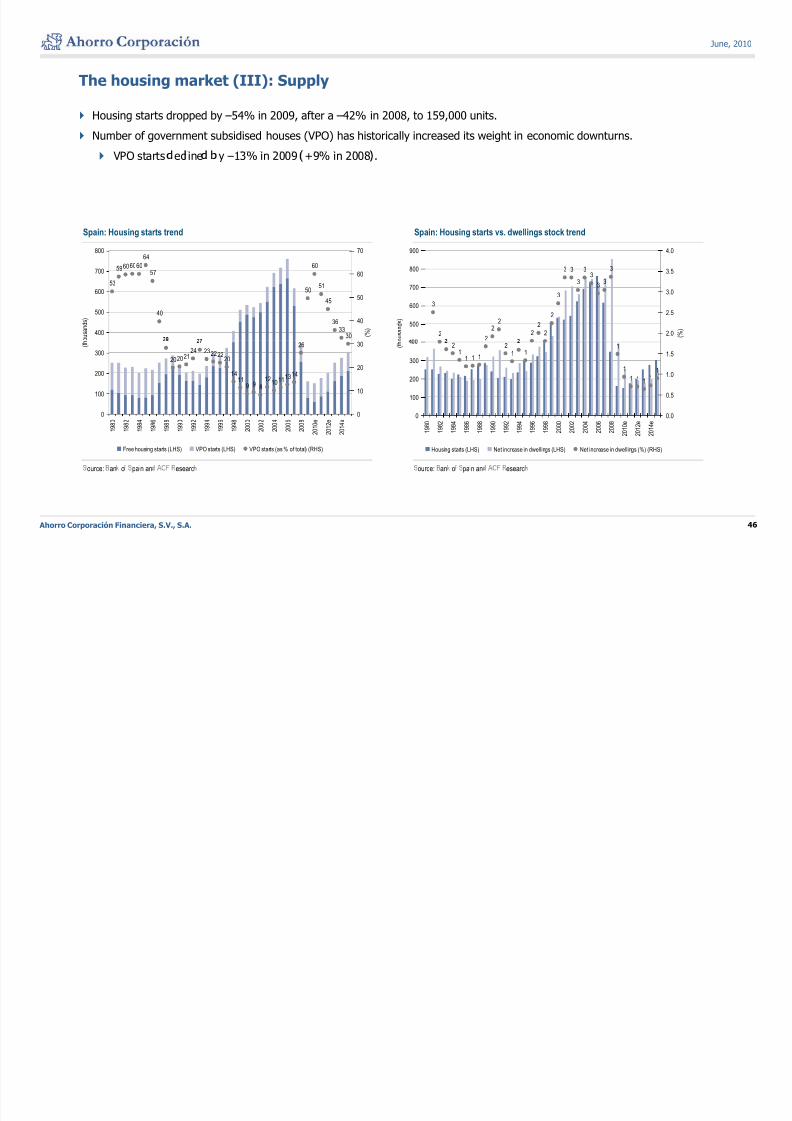

The housing market (III): Supply

Housing starts dropped by –54% in 2009, after a –42% in 2008, to 159,000 units.

Number of government subsidised houses (VPO) has historically increased its weight in economic downturns.

VPO starts ec ine y –13% in 2009 +9% in 2008 .

Spain: Housing starts trend Spain: Housing starts vs. dwellings stock trend

59606060

64

5760

700

800

60

70

3 3 33

3800

900

3.5

4.0

53

40

5051

45

3633

30400

500

600

o u s a n d s )

40

50

( % )

3

22

22

2

2

2

3

33

3

2500

600

700

o u s a n d s )

2.0

2.5

3.0

( % )

20202124 232222

20

1411

9 9 8

1210111314

26

100

200

300

( t h

10

20

30 21

1 1 1

21 1

1

1

1 1 11

1

100

200

300

( t h

0.5

1.0

1.5

0

1 9 8 0

1 9 8 2

1 9 8 4

1 9 8 6

1 9 8 8

1 9 9 0

1 9 9 2

1 9 9 4

1 9 9 6

1 9 9 8

2 0 0 0

2 0 0 2

2 0 0 4

2 0 0 6

2 0 0 8

2 0 1 0 e

2 0 1 2 e

2 0 1 4 e

0

Free housing starts (LHS) VPO starts (LHS) VPO starts (as % of total) (RHS)

0

1 9 8 0

1 9 8 2

1 9 8 4

1 9 8 6

1 9 8 8

1 9 9 0

1 9 9 2

1 9 9 4

1 9 9 6

1 9 9 8

2 0 0 0

2 0 0 2

2 0 0 4

2 0 0 6

2 0 0 8

2 0 1 0 e

2 0 1 2 e

2 0 1 4 e

0.0

Housing starts (LHS) Net increase in dwellings (LHS) Net increase in dwellings (%) (RHS)

Ahorro Corporación Financiera, S.V., S.A. 46

ource: an o pa n an esearc ource: an o pa n an esearc

June, 2010

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 47/70

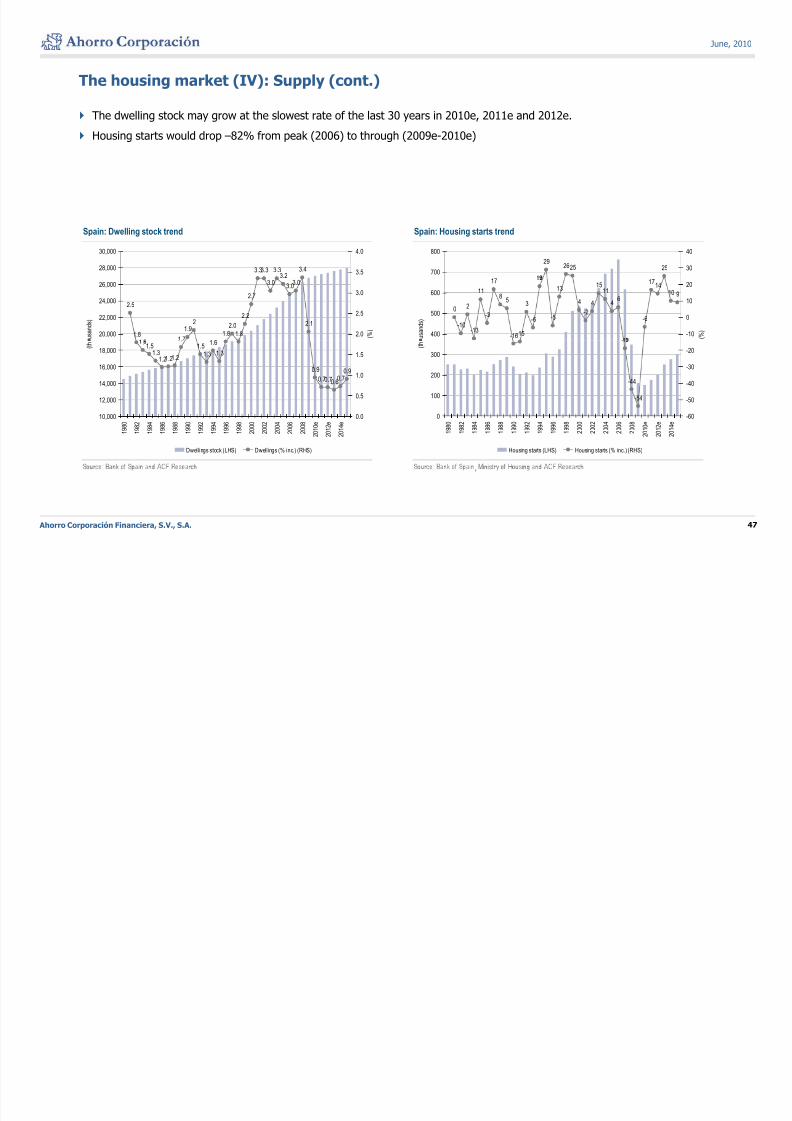

The housing market (IV): Supply (cont.)

The dwelling stock may grow at the slowest rate of the last 30 years in 2010e, 2011e and 2012e.

Housing starts would drop –82% from peak (2006) to through (2009e-2010e)

Spain: Dwelling stock trend Spain: Housing starts trend

3.33.3 3.33.2

3.428,000

30,000

3.5

4.0

292625 25

700

800

30

40

2.5

1.81.7

1.91.8

2.0

1.8

2.2

2.7

3.03.0

3.0

2.12

20,000

22,000

24,000

26,000

u s a n d s )

2.0

2.5

3.0

( % )

0

-10

2

-13

11

-3

17

8

5

-16

3

-6 -5

13

4-2

4

1511

46

-

-6

1714

10 9

-15400

500

600

u s a n d s )

-10

0

10

20

( % )

.1.5

1.31.21.21.2

.1.5

1.3

1.6

1.3

0.9

0.70.70.60.7

0.9

12,000

14,000

16,000

18,000 ( t h

0.5

1.0

1.5

-

-44

-54

100

200

300

( t h

-50

-40

-30

-20

10,000

1 9 8 0

1 9 8 2

1 9 8 4

1 9 8 6

1 9 8 8

1 9 9 0

1 9 9 2

1 9 9 4

1 9 9 6

1 9 9 8

2 0 0 0

2 0 0 2

2 0 0 4

2 0 0 6

2 0 0 8

2 0 1 0 e

2 0 1 2 e

2 0 1 4 e

0.0

Dwellings stock (LHS) Dwellings (% inc.) (RHS)

0

1 9 8 0

1 9 8 2

1 9 8 4

1 9 8 6

1 9 8 8

1 9 9 0

1 9 9 2

1 9 9 4

1 9 9 6

1 9 9 8

2 0 0 0

2 0 0 2

2 0 0 4

2 0 0 6

2 0 0 8

2 0 1 0 e

2 0 1 2 e

2 0 1 4 e

-60

Housing starts (LHS) Housing starts (% inc.) (RHS)

Ahorro Corporación Financiera, S.V., S.A. 47

,

June, 2010

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 48/70

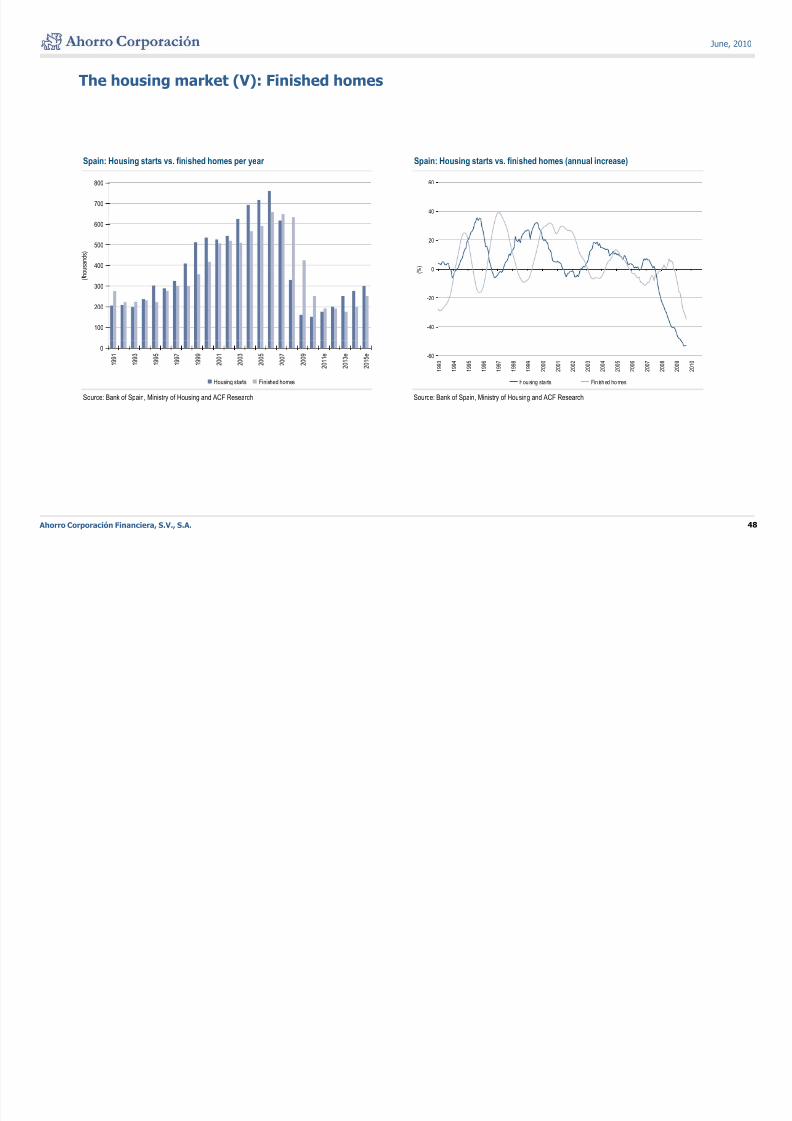

The housing market (V): Finished homes

Spain: Housing starts vs. finished homes per year Spain: Housing starts vs. finished homes (annual increase)

700

800

40

60

400

500

600

h o u s a n d s )

0

20

( % )

100

200

300

(

-40

-20

Source: Bank of Spain, Ministry of Housing and ACF Research Source: Bank of Spain, Ministry of Housing and ACF Research

0

1 9 9 1

1 9 9 3

1 9 9 5

1 9 9 7

1 9 9 9

2 0 0 1

2 0 0 3

2 0 0 5

2 0 0 7

2 0 0 9

2 0 1 1 e

2 0 1 3 e

2 0 1 5 e

Housing starts Finished homes

-60

1 9 9 3

1 9 9 4

1 9 9 5

1 9 9 6

1 9 9 7

1 9 9 8

1 9 9 9

2 0 0 0

2 0 0 1

2 0 0 2

2 0 0 3

2 0 0 4

2 0 0 5

2 0 0 6

2 0 0 7

2 0 0 8

2 0 0 9

2 0 1 0

Hou sing sta rts Fin ish ed ho mes

Ahorro Corporación Financiera, S.V., S.A. 48

June, 2010

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 49/70

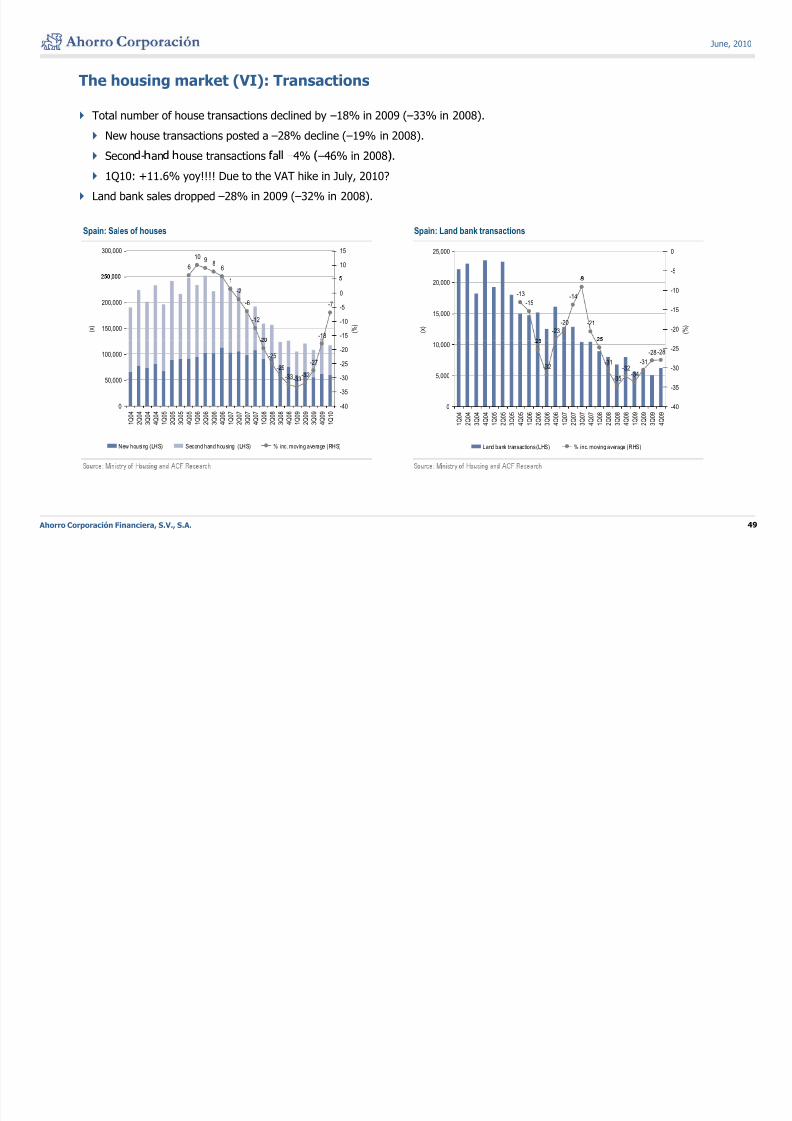

The housing market (VI): Transactions

Total number of house transactions declined by –18% in 2009 (–33% in 2008).

New house transactions posted a –28% decline (–19% in 2008).

Secon - an ouse transactions a –4% –46% in 2008 .

1Q10: +11.6% yoy!!!! Due to the VAT hike in July, 2010?

Land bank sales dropped –28% in 2009 (–32% in 2008).

Spain: Sales of houses Spain: Land bank transactions

6

10 98

6

300,000

10

15 25,000

-5

0

1

-2

-6

-12

--18

-7

150,000

200,000

,

( x )

-15

-10

-5

0

( % )

-13

-15

-23

-20

-14

-

-21

-

15,000

20,000

( x )

-20

-15

-10

( % )

-

-25

-29

-33-33-32

-27

50,000

100,000

-35

-30

-25

-20

-

-32-31

-35

-32-34

-31

-28 -28

5,000

10,000

-35

-30

-25

0

1 Q 0 4

2 Q 0 4

3 Q 0 4

4 Q 0 4

1 Q 0 5

2 Q 0 5

3 Q 0 5

4 Q 0 5

1 Q 0 6

2 Q 0 6

3 Q 0 6

4 Q 0 6

1 Q 0 7

2 Q 0 7

3 Q 0 7

4 Q 0 7

1 Q 0 8

2 Q 0 8

3 Q 0 8

4 Q 0 8

1 Q 0 9

2 Q 0 9

3 Q 0 9

4 Q 0 9

1 Q 1 0

-40

New housing (LHS) Second hand housing (LHS) % inc. moving average (RHS)

0

1 Q 0 4

2 Q 0 4

3 Q 0 4

4 Q 0 4

1 Q 0 5

2 Q 0 5

3 Q 0 5

4 Q 0 5

1 Q 0 6

2 Q 0 6

3 Q 0 6

4 Q 0 6

1 Q 0 7

2 Q 0 7

3 Q 0 7

4 Q 0 7

1 Q 0 8

2 Q 0 8

3 Q 0 8

4 Q 0 8

1 Q 0 9

2 Q 0 9

3 Q 0 9

4 Q 0 9

-40

Land bank transactions (LHS) % inc. moving average (RHS)

Ahorro Corporación Financiera, S.V., S.A. 49

June, 2010

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 50/70

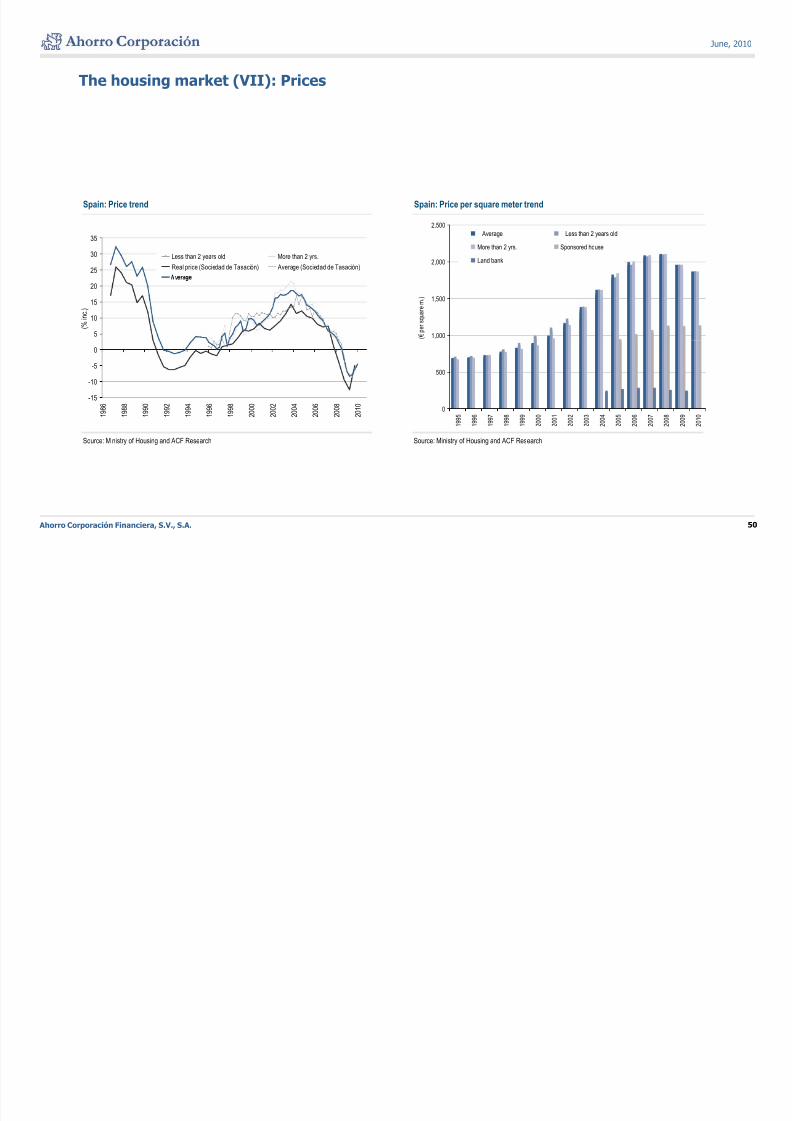

The housing market (VII): Prices

Spain: Price trend Spain: Price per square meter trend

25

30

35

Less than 2 years old More than 2 yrs.

Real price (Sociedad de Tasación) Average (Sociedad de Tasación)2,000

2,500

Average Less than 2 years old

More than 2 yrs. Sponsored house

Land bank

5

10

15

20

( % i n

c . )

1,000

1,500

( € p e r s q u a r e m

. )

-15

-10

-5

0

500

Source: Ministry of Housing and ACF Research Source: Ministry of Housing and ACF Research

1 9 8 6

1 9 8 8

1 9 9 0

1 9 9 2

1 9 9 4

1 9 9 6

1 9 9 8

2 0 0 0

2 0 0 2

2 0 0 4

2 0 0 6

2 0 0 8

2 0 1 0

0

1 9 9 5

1 9 9 6

1 9 9 7

1 9 9 8

1 9 9 9

2 0 0 0

2 0 0 1

2 0 0 2

2 0 0 3

2 0 0 4

2 0 0 5

2 0 0 6

2 0 0 7

2 0 0 8

2 0 0 9

2 0 1 0

Ahorro Corporación Financiera, S.V., S.A. 50

June, 2010

8/9/2019 Tale of Two Spains

http://slidepdf.com/reader/full/tale-of-two-spains 51/70

The housing market (VIII): Prices (cont.)

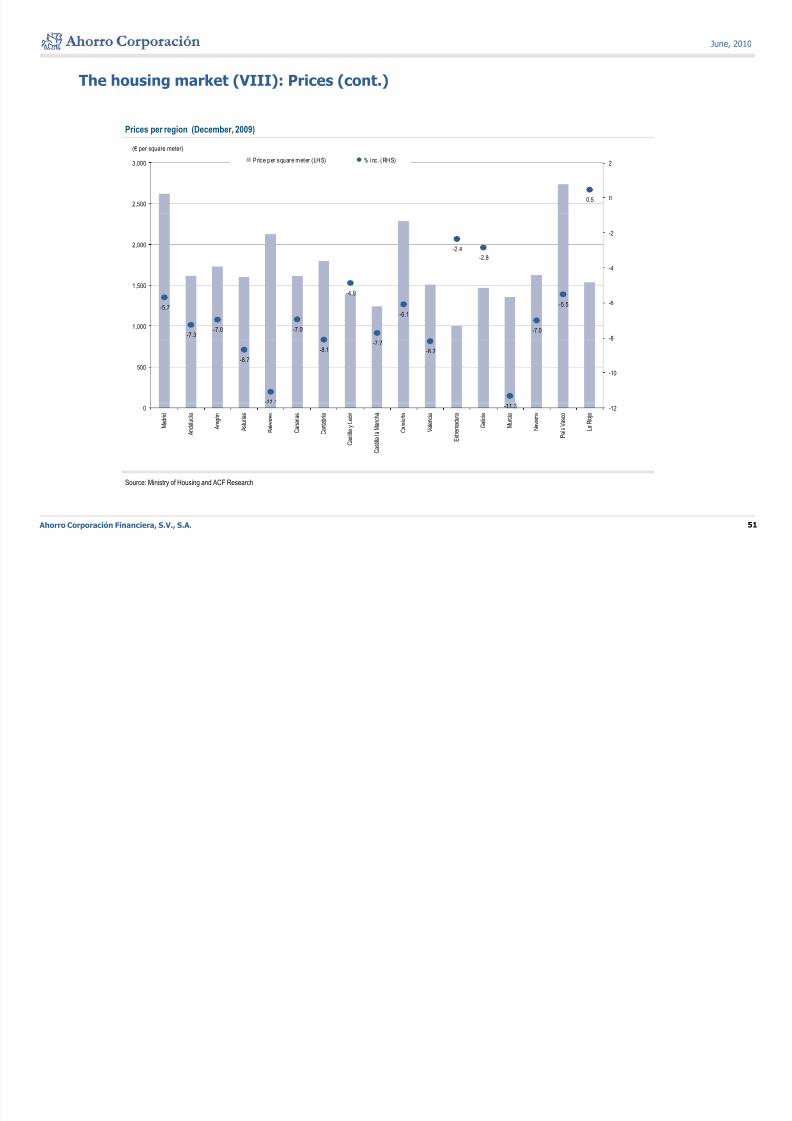

Prices per region (December, 2009)

(€ per square meter)

0.5

2,500

3,000

0

2Price per square meter (LHS) % inc . (RHS)

-2.4

-2.8

2,000

-4

-2

-5.7

-7.3-7.0 -7.0

-4.9

-6.1

-7.0

-5.5

1,000

1,500

-8

-6

-8.7