t35 algo survey

DESCRIPTION

While algorithms remain firmly embedded in buy-side strategies, The TRADE’s 6th annual Algorithmic Trading Survey suggests innovation is being stifled in the post-crisis environment.TRANSCRIPT

n the trade n issue 35 n jan-mar 2013 n www.thetradenews.com 79

The 2013 Algorithmic Trading Survey

Recognising excellence in the delivery of algorithmic trading solutions

Featuringn Market review n Broker roll of honour n Market feedback

Based on 1,100 buy-side evaluations

Market review

Illustration: iStockphoto

n The 2013 Algorithmic Trading Survey

Is the electronic trading industry maturing? The

results of The TRADE’s 2013 Algorithmic Trading Survey suggest that algo-rithms are taking their place as ‘another way of getting trades done’ rather than a ticket to the new frontier. Use of individual brokers, it seems, is driven as much by overall ‘research’ expertise as by differentiation in algorith-mic trading capabilities. In one sense, this harks back to the original selling point of algorithms a decade ago as a way of automating cer-tain trader responsibilities to free up resources to

concentrate on other more complex activities.

To be fair, however, the latest survey period includ-ed some ‘challenging’ moments – two fluffed IPOs, and a very, very fat finger incident – and as many sources of regulatory, business and macro-eco-nomic uncertainty as you care to mention. Traders may therefore have been inclined to step back from the bleeding edge. For many, algos did their job in the last 12 months if they effectively cleared the noise and gave buy-side traders the space to focus on the more complex trades. We will see in 2014 if

Volumes and provider numbers stabilise, as algorithms deliver value for money

While algorithms remain firmly embedded in buy-side strategies, The TRADE’s 6th annual Algorithmic Trading Survey suggests innovation is being stifled in the post-crisis environment.

80 n the trade n issue 35 n jan-mar 2013 n www.thetradenews.com

Algo market reaches maturity

the trends discussed below are confirmed. Early signs are that volumes will be higher and volatility lower ahead of next year’s survey, but no one should be think-ing just yet about breaking out the Cava.

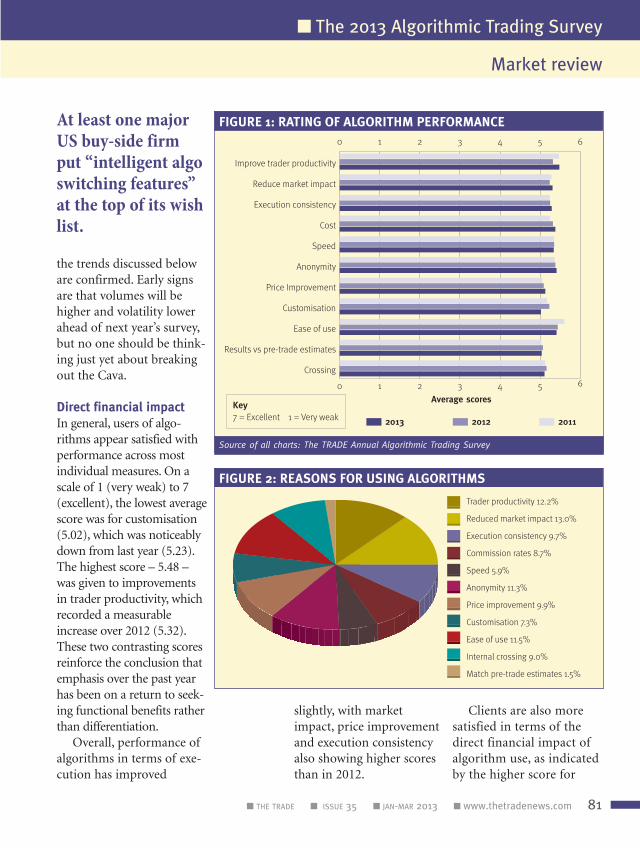

Direct financial impactIn general, users of algo-rithms appear satisfied with performance across most individual measures. On a scale of 1 (very weak) to 7 (excellent), the lowest average score was for customisation (5.02), which was noticeably down from last year (5.23). The highest score – 5.48 – was given to improvements in trader productivity, which recorded a measurable increase over 2012 (5.32). These two contrasting scores reinforce the conclusion that emphasis over the past year has been on a return to seek-ing functional benefits rather than differentiation.

Overall, performance of algorithms in terms of exe-cution has improved

slightly, with market impact, price improvement and execution consistency also showing higher scores than in 2012.

Clients are also more satisfied in terms of the direct financial impact of algorithm use, as indicated by the higher score for

Market review

n The 2013 Algorithmic Trading Survey

0 1 2 3 4 5 6

0 1 2 3 4 5 6

Crossing

Results vs pre-trade estimates

Ease of use

Customisation

Price Improvement

Anonymity

Speed

Cost

Execution consistency

Reduce market impact

Improve trader productivity

Average scoresKey7 = Excellent 1 = Very weak 2013 2012 2011

Figure 1: rating oF algorithm perFormance

Source of all charts: The TRADE Annual Algorithmic Trading Survey

Match pre-trade estimates 1.5%

Internal crossing 9.0%

Ease of use 11.5%

Customisation 7.3%

Price improvement 9.9%

Anonymity 11.3%

Speed 5.9%

Commission rates 8.7%

Execution consistency 9.7%

Reduced market impact 13.0%

Trader productivity 12.2%

Figure 2: reasons For using algorithms

At least one major US buy-side firm put “intelligent algo switching features” at the top of its wish list.

n the trade n issue 35 n jan-mar 2013 n www.thetradenews.com 81

82 n the trade n issue 35 n jan-mar 2013 n www.thetradenews.com

Market review

n The 2013 Algorithmic Trading Survey

refinement, some providers have taken their foot off the gas to a certain degree. Anecdotal evidence suggests a fairly healthy level of dia-logue between buy-side desks and their algorithm providers in parallel with the growth of execution services, but this is not feeding through into per-formance ratings.

Anonymity has also received slightly higher scores this year, up from 5.38 to 5.41. At least one buy-side trader with multiple provid-ers cited anonymity as some-thing his firm was seeking to a greater degree from all of its providers.

Scores for anonymity have been rising gradually but steadily in recent years, while those for crossing have been going down – from 5.16 last year to 5.11 in the latest survey. This could reflect ongoing con-cerns about the ‘darkness’ of dark pools. Said one UK fund manager: “We’re look-ing for better feedback on trading counterparties within the electronic space, particularly concerning entrants to their dark pools.” Another urged greater transparency into order routing decisions. Greater pressure on trading desks to explain execution choices to clients and

both trader productivity already observed and lower costs.

Customisation on the other hand would normally be regarded as one area for providers to invest to win business. The lower scores awarded to this and to ease of use suggest that in terms of innovation and invest-ment in algorithmic

0

1

2

3

4

5

6

7

8

Notanswered

More than$50 billion

$10-50billion

$1-10billion

$0.5-1billion

$0.25-0.5billion

Up to $0.25billion

Num

ber

of a

lgor

ithm

pro

vide

rs

Assets under management

2013 2012 2011

Figure 3: average number oF proviDers useD by aum More than half of respondents used algorithms for 30% or more of value traded for the second year in a row

0

10

20

30

40

50

>12*8-12*5-73-41-2

% o

f re

spon

dent

s

Number of providers

2013 2012 2011

Figure 4: number oF proviDers useD

* In 2011, respondents could only specify a maximum of ‘five or more’ algo providers

Market review

n The 2013 Algorithmic Trading Survey

n the trade n issue 35 n jan-mar 2013 n www.thetradenews.com 83

Market review

n The 2013 Algorithmic Trading Survey

Market review

n The 2013 Algorithmic Trading Survey

Last year the top three reasons for using algo-rithms were reduced market impact (13.6%), ease of use (12.1%) and trader produc-tivity (11.1%). In this year’s survey, the same three rea-sons again appeared at the top though in a different order. The desire to reduce market impact was down from 13.6% to 13%; trader productivity was up from 11.1% to 12.2%, while ease of use was down from 12.1% to 11.5%. The big-gest change was in the rela-tive importance of price improvement as a reason to deploy algorithms, up from 7.8% last year to 9.9% in 2013. Anonymity increased in recognition, so to speak, but not in ranking, remain-ing the fourth most impor-tant reason for using algo-rithms, rising from 10.8% to 11.3%.

Figures 3 and 4 show some noticeable changes over the past 12 months in the number of providers used, measured both by assets under management and by percentage of respondents. Last year, for all but the smallest manag-ers with less than US$0.25 billion under management, the trend was to increase the number of algorithm pro-viders. In the latest survey,

clients. Scores are consist-ent, but hardly exciting. Respondents trying to grind out a return in a tough trading environment appear more focused on tangible outcomes such as price improvement and productivity.

boards is a well-established trend and one that is unlikely to relent until alpha generation recovers.

grinding out resultsPre-trade cost estimation and speed are apparently of decreasing importance to

0 10 20 30 40 50 60 70 80

0 10 20 30 40 50 60 70 80

VWAP

TWAP

Other

Implementation shortfall(single stock)

Implementation shortfall(basket)

Dark liquidity seeking

Participation

% of respondents

2013

2012

2011

Figure 6: types oF algorithms useD

% o

f re

spon

dent

s

% of value traded using algorithms

0

10

20

30

40

50

Notanswered

40%and over

30-40%20-30%10-20%5-10%0-5%

2013 2012 2011

Figure 5: algorithm usage by value traDeD

84 n the trade n issue 35 n jan-mar 2013 n www.thetradenews.com

Market review

n The 2013 Algorithmic Trading Survey

volume), which were the second most popular cate-gory last year, used by 65.7% of respondents, have seen a similar decline in use over the same period (68.5% to 56.3%) to the point that VWAP – depend-able old VWAP – just by staying more or less where it is, is now in second place at 58.9%.

The reduction in number of survey respondents citing use of dark liquidity seeking algorithms is at odds with rising levels of dark pool executions reported in major markets and anecdo-tal evidence on the value many buy-side desks ascribe to their ability to access off-exchange liquidity. However, the last 12 months have also been characterised by the kind of volatility that forced traders back onto lit venues. Moreover, traders may be expressing a preference for exploring the dark pools of brokers with a track record in a particular name – as demonstrated by reliable indications of interest – rather than using an algo to go from venue to venue potentially leaving a trail for predators to follow. n

to come, at least one major US buy-side firm with multiple providers put “intelligent algo switching features” at the top of its wish list.

Algorithm usage overall remains high. The percent-age of respondents using algorithms for 40% or more of value traded is in the mid-forties, if slightly below last year’s total, while those using algorithms for 30-40% of value traded have risen in number (see Figure 5). As such, more than half of respondents used algorithms for 30% or more of their value traded for the second year in a row.

no room at the top?The annual hit parade of individual algorithm types offers few surprises in this year’s survey though relative trends have been confirmed. Dark-liquidity-seeking algo-rithms – top of the charts last year – remain popular though the percentage of respondents using them has declined over the past two years by well over 10 per-centage points from 75.2% to 62.5%. Participation algorithms (percentage of

those at the two ends of the spectrum have reversed their previous trends. This is most noticeable at the top end, where for buy-side firms with US$50 billion under management, the average number of provid-ers has dropped below six.

consolidating businessIn percentage terms, the biggest drop has been in the number of firms using five to seven providers, down from 24.5% to 20.5%, while more firms are using eight to twelve providers than in 2012. The percentage of respondents using between one and four providers remains similar, however: 59% in 2012 and 59.3% in 2013.

This is no doubt a reflec-tion of market conditions: lower overall equity trading volumes and relatively poor performance by active asset managers in 2012, com-pared to exchange-traded funds, index trackers and other passive, lower-cost investment strategies. Lower trading volumes mean less commission to spend, which should logically translate into the buy-side consolidating business among fewer brokers/algo-rithm providers. Perhaps a sign of client requirements

Dark-liquidity-seeking algorithms – top of the charts last year – remain popular

88 n the trade n issue 35 n jan-mar 2013 n www.thetradenews.com

Broker Roll of Honour

n The 2013 Algorithmic Trading Survey

Illustration: iStockphoto

Functional capabilities

The 2013 broker Roll of Honour

PRICE IMPROVEMENT

ROLL OF HONOURCitiSanford C BernsteinUBS

ONES TO WATCHInstinetJefferies

This category saw a number of changes from a year ago. UBS retained its Roll of Honour position but was joined this year by Sanford C Bernstein and Citi. The Roll of Honour names were all well ahead of the average score for the question across the survey of 5.13. The average score was slightly improved from the 2012 result of 5.09 but was nonetheless well

Survey respondents were asked to provide a rating for each algorithm provider

on a numerical scale from 1.0 (very weak) to 7.0 (excellent), covering 11 functional

criteria. In general 5.0 is the ‘default’ score of respondents. In total more than

1100 individual evaluations were submitted covering over 30 providers. These

evaluations were used to compile the provider Roll of Honour. Each evaluation

was weighted according to three characteristics of each respondent; the value of

assets under management; the proportion of business done using algorithms;

and the number of different providers being used. In this way the evaluations of

the largest and broadest users of algorithms were weighted at up to three times

the weight of the smallest and least experienced respondent.

In arriving at the overall Roll of Honour the scores received in respect of each of

the 11 functional capabilities were further weighted according to the importance

attached to them by respondents to the Survey. The aim is to ensure that in

assessing service provision the greatest impact results from the scores received

from the most sophisticated users in the areas they regard as most important.

Finally it should be noted that responses provided by affiliated entities are

ignored and a few other responses were also excluded where the respondent

could not be properly verified.

The 11 functional capabilities are grouped into three categories: those that impact

on actual execution performance; those that affect direct and indirect costs of

trading; and capabilities that are of a qualitative and more subjective nature.

MEASURINg FUNCTIONAL CAPAbILITIES

1 Roll of Honour recipients are listed in alphabetical order throughout the survey.

Broker Roll of Honour

n The 2013 Algorithmic Trading Survey

n the trade n issue 35 n jan-mar 2013 n www.thetradenews.com 89

EXECUTION CONSISTENCY

ROLL OF HONOURCredit SuisseSanford C BernsteinUBS

ONES TO WATCHFidelityWeeden

To the extent that clients are using algorithms as a way to enhance trader productivity and keep costs down, consistency of execution results, measured against standard benchmarks, is often more important than actually achieving gains through trading. This aspect has been diminishing in importance to clients in the last two years. In terms of total mentions by respondents it accounted for 9.7% this year, compared with 10.7% in 2012, ranking now behind price improvement for the first time in the history of the survey.

regard this as the single most important area in terms of evaluating overall provider performance. In 2013 the proportion of mentions was 13.0% down slightly from 13.6% in 2012, but more important than all other questions.

Because of its importance, it is perhaps to be expected that the overall score across the survey at 5.31 should closely parallel the survey average of 5.30. In fact scores were better in 2013 than 2012, when this question achieved a score of 5.24 overall. Indeed the score in 2013 is at the best ever level. The breakdown of scores is also quite consistent with just over 40% of scores at the 6.0 or 7.0 level, implying above average perception. In this category, the Roll of Honour winners included none of the 2012 names, though Credit Suisse came close to repeating and Liquidnet were identified in 2012 as ‘one to watch’.

below the average survey score across all questions of 5.30. While providers have made some progress in improving clients’ views about their ability to deliver better execution performance, it is clear from the scoring that many clients remain somewhat sceptical.

This is one area to which clients attach growing importance. If providers are genuinely contributing to achievement of better prices then the success of algorithms is assured and their benefit quite clear. It is therefore not surprising that this area achieved a level of 9.9% of respondents mentioning it as a key criterion in their assessment of providers, up from 7.8% in 2012. The growing importance and continued relative concern about capabilities suggests that customers do want to see further demonstrable progress in this area.

REDUCINg MARKET IMPACT

ROLL OF HONOURITGLiquidnetUBS

ONES TO WATCHCredit SuisseRBC Capital

Reducing market impact is especially important to large long-only managers seeking to create or unwind large positions with the lowest level of information leakage possible. Algorithmic trading, with its sophisticated child order creation processes, is designed to help achieve this objective. It is therefore not surprising that clients

Broker Roll of Honour

n The 2013 Algorithmic Trading Survey

90 n the trade n issue 35 n jan-mar 2013 n www.thetradenews.com

survey and ranks as a key criterion in the increased use of algorithms by clients. It is especially critical when dealing room expenses and staffing levels are under pressure because of reduced asset and trading levels. In terms of relevance to clients, it obtained 12.2% of total mentions up from 11.1% in 2012.

Somewhat unusually, the names that appear in the Roll of Honour in 2013 are different from 2012. This would suggest that some new names are perhaps having a greater positive impact on productivity as well as some more traditional names having made greater strides in the last 12 months. It should also be noted that in many cases the Roll of Honour names in 2012 continued to score well, but not well enough to repeat their mention from a year ago. As a result of the strong showing, 46% of all responses achieved a score better than the 5.0 ‘default’ level. The number of scores in the unsatisfactory (3.0 or less) categories was lower than for any other question.

COST AND COMMISSIONS

ROLL OF HONOURBank of America Merrill LynchBarclaysBloomberg Tradebook

ONES TO WATCHITGKnight Capital

For a growing number of clients, allocations to algorithmic trading are seen as part of the overall broker commission allocation and algorithms are a way to reduce average commission costs. For these

IMPROVINg TRADER PRODUCTIVITY

ROLL OF HONOURDeutsche BankInstinetMorgan Stanley

ONES TO WATCHJefferiesSanford C Bernstein

Having suffered a quite significant decline in 2012, scores for improving trader productivity bounced back sharply in 2013. With an average score of 5.48, the question achieved the best scores among the 11 questions and was also well ahead of the overall survey average of 5.30. Compared with 5.32 in 2012, the perceptions appear to be materially improved. This is significant because this area is the second-most important in the

Consistency is an area in which scores have belied the strong belief that it is a natural attribute of algorithmic trading. However in 2013 scores moved slightly ahead for the second year in a row. The average across all responses was 5.29 which is virtually identical with the 5.30 across all questions. It is also up from 5.25 in 2012. In terms of the Roll of Honour winners this year, UBS repeated its placing from 2012. Credit Suisse has always performed well in this area, but was not in the 2012 Roll of Honour, while Sanford C Bernstein scored well in 2012 without featuring in the rankings and has improved in terms of response levels and scores in 2013. For the second year in a row Fidelity scored very well in this category but failed to obtain sufficient responses to be included in the Roll of Honour.

Broker Roll of Honour

n The 2013 Algorithmic Trading Survey

n the trade n issue 35 n jan-mar 2013 n www.thetradenews.com 91

Bank of America Merrill Lynch achieved Roll of Honour status for the second year in a row, joined this year by Citi and Goldman Sachs. Deutsche Bank scored well and nearly repeated its Roll of Honour position of 2012. Scores for ConvergEx were particularly strong but across a rather limited number of responses. Hence their inclusion as ‘one to watch’. Ease of use is the third most important area of evaluation for clients. It gained 11.3% of all mentions across the Survey. This was however down slightly on 2012. It may also be that once different bank capabilities are installed and familiar to staff, ease of use becomes less important than their actual performance.

CROSSINg

ROLL OF HONOURCitiCredit SuisseITG

ONES TO WATCHBank of America Merrill LynchLiquidnet

The proliferation of broker dark pools coupled with concerns about ‘toxic’ flow has resulted in brokers and clients alike being more sensitive to how crossing is perceived and how risks can be reduced without eliminating the possibilities to lower costs through use of crossing. Smart order routers are becoming smarter and may become even more transparent as regulators become further engaged with the developments of trading generally. In 2013, crossing became less important to clients (9.0% of mentions compared with 10.4% a

EASE OF USE

ROLL OF HONOURBank of America Merrill LynchCitiGoldman Sachs

ONES TO WATCHConvergExDeutsche Bank

Scores for ease of use were the second highest in the whole survey, despite the fact that for the second year in a row scores actually declined. It may be that the use of more providers simply makes trading with all of them somewhat more complicated. However, for clients looking for a simple productivity enhancing tool, complexity – whether in terms of number and variety of algorithms or the parameters that can be set – may be in danger of becoming too much of a good thing. Even so around 45% of responses scored a 6.0 or 7.0 on this question, so many clients clearly remain well satisfied.

clients, the level of commission payable is an important component. However there are also many other costs and savings associated with the use of algorithmic trading beyond simply commission levels. These include the costs of connectivity and systems integration, where relevant, as well as the ability to handle more trading with lower costs.

In this context it is interesting to note that both Bloomberg Tradebook and ITG offer trading services as well as algorithmic trading capabilities themselves. Their bundled approach clearly appeals to clients in terms of cost. The importance of this factor grew again in 2013, gaining 8.7% of total mentions. However that remains well behind factors associated with trading outcomes. Scores also improved for the second year in succession. The average of 5.38 was among the best in the survey. This suggests that all parties have a realistic view of why algorithms are being used and the fact that the arrangement is seen as being mutually beneficial.

92 n the trade n issue 35 n jan-mar 2013 n www.thetradenews.com

Broker Roll of Honour

n The 2013 Algorithmic Trading Survey

year earlier). This reversed a steadily upward trend in interest and engagement with crossing.

The best scores were recorded by some of the names who have historically been involved in trying to maximise opportunities without involving too much high-frequency trading volume. Liquidnet by virtue of its business model has always been focused on this aspect of service and seems to be gaining ever more recognition in Europe particularly. ITG repeated its Roll of Honour ranking from 2012 and Credit Suisse has scored well in this area for a number of years. However the average score remains among the less convincing in the survey and was down to 5.11 in 2013, from 5.16 in 2012. Along with price improvement it received the lowest percentage of ‘excellent’ (7.0) scores at a little over 6%.

ANONYMITY

ROLL OF HONOURBloomberg TradebookJ.P. MorganLiquidnet

ONES TO WATCHJefferiesRBC Capital

Anonymity is intrinsically linked to crossing and reducing market impact in the minds of customers. Crossing should help preserve anonymity and one result of preserving anonymity should be lower slippage costs. The importance of anonymity has been increasingly recognised within the survey as well as being stressed by advocates of algorithmic trading, smart order routing and crossing. In 2013 11.3% of mentions of critical criteria were for anonymity, up from 10.8% in 2012. While scores for crossing and reducing market impact have changed little in the last two years, scores for anonymity have continued to improve. In 2013, they reached 5.41, which was the equal second best of all scores.

The banks in the Roll of Honour have all changed in the last year. RBC Capital was again in the ‘ones to watch’ segment, achieving good scores but insufficient responses to merit a better position. Liquidnet, as with crossing, has sought to focus very carefully on preserving anonymity and clients are increasingly appreciative of its approach. This is an area where the range of score, even across the major banks is wider than in many

areas. It is also an area where one ‘mistake’ will be costly in terms of perceptions which may well endure for a long time after the event has passed.

SPEED

ROLL OF HONOURCredit SuisseMorgan StanleyUBS

ONES TO WATCHBarclaysHSBC

Low latency was and remains important to a particular class of high-volume trading house, whether a proprietary trading desk or a hedge fund. As algorithmic trading has expanded to include all major buy-side firms the relative importance of this area has decreased. It is also very difficult to measure and complete understanding of its impact requires a very granular level of analysis of a high volume of data. Most clients do not have the ability, interest or resources to undertake the effort entailed. Perhaps it is not surprising therefore that this question received only 5.9% of mentions in terms of being important – better only than pre-trade analysis.

There are obviously some differences in scores, but clients generally appear well satisfied. The average score was 5.34 in 2013, virtually unchanged again from the 5.35 seen in 2011 and 2012. It is slightly better than the survey average of 5.30 across all questions. The Roll of Honour names include Morgan Stanley repeating its success

Broker Roll of Honour

n The 2013 Algorithmic Trading Survey

n the trade n issue 35 n jan-mar 2013 n www.thetradenews.com 93

Broker Roll of Honour

n The 2013 Algorithmic Trading Survey

CONSISTENCY WITH PRE-TRADE ESTIMATES

ROLL OF HONOUR Credit SuisseITGInstinet

ONES TO WATCH Bank of America Merrill LynchCiti

By far the least important question in the survey, the ability of providers to accurately predict execution costs is seen by clients as unproven at best, and potentially misleading at worst. Part of the problem seems to be that the process does not lend itself to easy, simple or consistent analysis which leads to a measure of client confusion. Recently a number of providers have sought to counter this through provision of sophisticated execution consulting services as well as real-time cost analysis. It will be interesting to see if this has an effect on perceptions in the next few years. However so far the activity earns poor scores, the average was 5.04 the second worst of all 11 questions and little changed from the 5.07 of 2012 or the 5.03 of 2011.

The question scored the highest percentage of respondents giving it a 5.0 ‘default’ score. It would appear that its low average reflects disinterest rather than disaffection with performance. That it attracted only 1.54% of mentions of important factors would support the conclusion that clients do not care enough to have strong feelings as regards performance of vendors. ITG and Instinet both repeated Roll of Honour positions from 2012 while Citi and BAML also scored relatively well. n

of 2012 together with the two biggest banks in terms of response numbers, UBS and Credit Suisse. HSBC scored well but their number of responses was not sufficient to merit a stronger position.

CUSTOMISATION

ROLL OF HONOUR Bank of America Merrill LynchSociété GénéraleUBS

ONES TO WATCHFidelityITG

Customisation is the area that showed the sharpest decline in scores in the entire survey. The average score in 2013 was only 5.02, barely above the ‘default’ score and well below the 5.30 average across all 11 questions. The score was well down on the 5.23 seen in 2012. It attracted by far the largest number of scores at 3.0 and below; more than twice that of the next worst question. It would seem

that as the business has matured and in an environment of tight resources, the willingness of providers to offer an ever-increasing array of custom services has declined. This is only to be expected in the circumstances. Nonetheless, providers would do well to take note that clients have already noticed and are likely to become more disillusioned if the situation continues, especially if market structures themselves are changing.

None of the 2012 Roll of Honour names repeated their performance this year, though ITG again scored well. Fidelity scores were exceptionally good in this area, but the number of responses is insufficient to merit Roll of Honour status. It is also worth noting that customisation is among the least important features for many clients, generating only 7.3% of mentions. It may be that clients have seen the writing on the wall and are adjusting expectations accordingly. However providers would be unwise to rely on that situation continuing.

Broker Roll of Honour

n The 2013 Algorithmic Trading Survey

94 n the trade n issue 35 n jan-mar 2013 n www.thetradenews.com

how each provider ranks against one another. The science is not perfect – sometimes clients use different brokers in different markets or for different trade types. Nonetheless it offers an important context within which to analyse raw scores.

Not surprisingly the names on the list are much more consistent from one year to the next. Providers may not always manage all their clients well all of the time, but they will work very hard to maintain a positive perception among these ‘opinion leading’ clients. They will also face more consistent and broad competition for business from this group.

The average scores from these customers continued to be generally lower than in the survey as a whole. Even so, the average scores achieved by the Roll of Honour names were comfortably ahead of the average across the survey as a whole; adequate testimony to their commitment and effectiveness. n

and also scored well marking it out as up and coming.

As noted above, client responses are weighted based around different factors. Leading clients are not defined by size of assets or trading volumes alone; experience and expertise with algorithmic trading is also a critical part of the assessment. In addition, their priorities are often different from smaller and less sophisticated clients and so the weighting attached to each question in looking at overall performance must be taken into account. Finally it is possible to look at ‘head to head’ analysis where various respondents all use a number of common providers. This allows us to look at

LEADINg CLIENTS

ROLL OF HONOURGoldman SachsMorgan StanleyUBS

ONES TO WATCHCredit SuisseSanford C Bernstein

In 2013, Morgan Stanley followed through on its ‘one to watch’ position in 2012 by appearing in the Roll of Honour. It just displaced Credit Suisse which nonetheless performed well again with this group. Sanford C Bernstein achieved a good level of penetration with this client group

Overall performance

As well as considering the functional capabilities of algorithm providers, the

survey also assessed overall performance as measured across all capabilities.

This analysis took account of both un-weighted and weighted scores based on

the different levels of importance attached to the various aspects of service

covered in the survey.

MEASURINg OVERALL PERFORMANCE

Market feedback

n The 2013 Algorithmic Trading Survey

98 n the trade n issue 35 n jan-mar 2013 n www.thetradenews.com

Algos under the microscope

Illustration: iStockphoto

Macro-economic uncer-tainties, dominated by

the euro-zone debt and at times the fate of the euro itself fuelled another year of high volatility, low volumes and high correlation where stocks tended to move together in response to mar-ket conditions and events. As a result, the returns to be had by stock market inves-tors in 2012 were distinctly beta in nature.

Some institutional inves-tors chose to withdraw from the equity markets and invest in other more predictable asset classes while others found that tried and tested trading models and strategies could no longer be relied upon to deliver the expected levels of return.

As Brian Gallagher, head of electronic trading in Europe at Morgan Stanley, observes, “A lot of institu-tional investors, particularly

the bigger mutual funds and long-only asset manag-ers, were either underweight Europe or the turnover in their portfolio was heavily reduced, which impacted liquidity and made trading conditions more difficult because of the absence of longer-term flow.”

It is not surprising that dark liquidity-seeking algo-rithms remained the most commonly-used strategy in The TRADE’s Algorithmic Trading Survey in 2013 and scores for anonym-ity rose emphasising the importance of having effec-tive signalling risk controls when accessing dark liquid-ity in a low-volume market where there is a greater risk of information leakage.

The experience of Paul Collins, head of EMEA equity trading at global asset manager Franklin Templeton, tallies with these results. “Overall, our

As trading volumes dipped in 2012, institutional trading desks squeezed more value out of their algorithms by increasing scrutiny of execution performance data.

Market feedback

n The 2013 Algorithmic Trading Survey

n the trade n issue 35 n jan-mar 2013 n www.thetradenews.com 99

algorithmic trading volumes are increasing and the trend was for more dark liquidity-seeking algorithms with built-in signalling risk func-tionality. As market dynamics shift and change, we look to shift and change with them.”

Deep-rooted knowledgeWhile in the early days of 2013 markets appear less volatile as strong investment inflows stabilise values, there are a wide range of challeng-es and uncertainties facing buy-side firms. An inexhaus-tive list might include the impact on liquidity of finan-cial transaction taxes already in force in several European countries including France and now Italy; the outcome of the MiFID review, espe-cially in the areas of high-frequency trading, creation of a consolidated tape and access to dark liquidity; and the control issues arising from market infrastructure and systems failures rang-ing from the 2010 US flash crash to last August’s Knight Capital market making sys-tems glitch.

These make having a deep-rooted knowledge of electronic trading offerings and market and systemic risk essential to obtaining the best trading outcomes for end-investors.

“In the past, to some degree, the emphasis was on just using algorithmic tools. Now it has become much more of a conscious, educat-ed decision process to work out where it is best to use them and where it is not and how to optimise that process. The target is not to execute a specified percentage of your flow but to execute optimally which may result in a speci-fied percentage of your flow being executed electronically. It really does feel that the knowledge and education on the buy-side has come on dramatically over the last couple of years,” says Owain Self, global head of algorith-mic trading at UBS.

For Brian Schwieger, head of EMEA algorith-mic execution at Bank of America Merrill Lynch, the key buy-side drivers in 2012 into 2013 are liquidity and service. It follows that these should be core sell-side per-formance differentiators.

“Overall algorithm usage patterns remained pretty stable into the end of 2012 and beginning of 2013. Most top-tier provid-ers now offer intelligent algorithms with effective anti-gaming logic which recognise market conditions and adapt trading strate-gies accordingly. These have

helped alleviate a lot of the buy-side’s concerns over market impact in less-liquid stocks and markets,” he says.

Some buy-side traders are putting their market

n “A lot of institutional investors were either

underweight Europe or portfolio turnover was heavily reduced, which impacted liquidity.”Brian Gallagher, head of electronic trading, Europe, Morgan Stanley

100 n the trade n issue 35 n jan-mar 2013 n www.thetradenews.com

Market feedback

n The 2013 Algorithmic Trading Survey

His colleague, Richard Gray, head of algo servicing group and trading, EMEA, Liquidnet, shares this view, noting “a lot of algorithmic controls and parameters are very detailed and to begin with most of them were not utilised. Now buy-side

clients are digging deeper under the covers and want to know what you can offer them and what controls you can help them with.”

The experience of some institutional investors points to increased scrutiny of broker performance, a more stringent policing of data flows from brokers and pro-active involvement in execu-tion processes to ensure buy-side traders have access to information they can use to analyse performance and make meaningful choices on where to send order flow. The continuing post-MiFID evolution of venues can pose a challenge and make this an onerous task with the impetus on good quality information from brokers.

As Liquidnet’s Gray observes, “In the past it was more about whether you were engaging with dark liquidity. But the debate has moved on to not just where you go but how you interact with that particular venue to optimise your execution outcomes. Different dark pools offer very different value to different market participants.”

Brokers are increas-ingly expected to complete questionnaires from their buy-side clients which are used to compare

knowledge and experience into consolidating their broker lists and demanding greater levels of information around the execution pro-cess to meet the challenges of accessing and interacting with the right type of liquid-ity and measuring perfor-mance. “We now have better knowledge and understand-ing of what happens to our order flow when it becomes part of the algorithmic trad-ing process and our level of scrutiny has increased. We are asking brokers for a lot more targeted data and information around the exe-cution process,” says Franklin Templeton’s Collins.

Aligning expectationsBrokers have noticed a sea change in buy-side understanding and engage-ment and, in an increas-ingly competitive environ-ment, are keen to respond positively.

“Focus has moved from algorithmic functionality to the trading expectations and execution outcomes individual clients are seek-ing to achieve, and how we can help to secure these in challenging market condi-tions,” says Per Lovén, head of EMEA product and strategy for block trading platform firm Liquidnet.

n “The debate has moved on to how you interact

with a particular venue to optimise your execution outcomes.”Richard Gray, head of algo servicing group and trading, EMEA, Liquidnet

Market feedback

n The 2013 Algorithmic Trading Survey

n the trade n issue 35 n jan-mar 2013 n www.thetradenews.com 101

in broker relationships. Puhakka sees greater buy-side awareness of the impact on their order flow of inherent broker prefer-ences on routing logic and encourages them to con-sider alternatives that give buy-side traders more con-trol over this aspect of the trading process.

“Buy-side firms are seeking further clarity and transparency when using sell-side tools; do they really give the buy-side access to multiple sources of liquid-ity or to liquidity that suits

Market feedback

n The 2013 Algorithmic Trading Survey

them more. It is at this point where you may need addi-tional transparency as you are asking more relevant questions,” says Collins.

Simo Puhakka, former head of trading of Helskini-based buy-side firm Pohjola Asset Management and now CEO of Pohjola Asset Management Execution Services (PAMES), which develops and markets smart order routing and algorithmic execution ser-vices to buy-side firms, is a long-standing champion of increased transparency

execution experience and performance.

“Over the last year, we have seen the majority of clients doing much more analysis around what their order flow is like and what they need to achieve objec-tive-wise. This has changed how the buy-side is inter-acting with the electronic desk. They will restrict the venues they access, look to the venues with more func-tionality that can improve execution and use algo-rithms with a continued focus on anti-gaming and liquidity selection tactics,” observes UBS’s Self.

Toward transparencyReliance on brokers for the information used to scrutinise performance has led some heads of trad-ing to focus on increasing transparency in broker relationships.

“Increasing transparency is an ongoing key consid-eration. The more transpar-ent the electronic trading arena becomes, the more confidence we have in the efficiency of the products we use and venues and access we have. It is an evolution-ary process: you start using algorithmic trading tools, you understand them better and you start to scrutinise

n “The more transparent the electronic trading arena becomes, the more confidence we have

in the efficiency of the products we use.”Paul Collins, head of equity trading, EMEA, Franklin Templeton

Market feedback

n The 2013 Algorithmic Trading Survey

102 n the trade n issue 35 n jan-mar 2013 n www.thetradenews.com

macro level, using algo-rithms at their desk instead of outsourcing execution to broker cash desks. Control over the underlying liquid-ity has been seen as the missing link. Now there is a tendency to get control over the routing logic as well,” said PAMES’ Puhakka.

Encouraging competitionThe buy-side tested the boundaries of its influ-ence in 2012 and saw some brokers (generally those in the top-tier with deep pockets) responding and adapting their services and offerings. Attention on both sides was focused on get-ting the best out of existing products and on higher levels of service to the buy-side in terms of informa-tion. Franklin Templeton’s Collins sums up his buy-side expectations for the coming year: “I see the overall use of algorithmic trading increasing and becoming more concen-trated amongst brokers and providers who share a dynamic view of the world. However we have an obliga-tion to encourage competi-tion and efficiency by polic-ing and analysing execution and overall performance, while being aware of the available alternatives.” n

broker preferences? Using broker smart order routing logic to access particular venues is fine provided that you are aware of the poten-tially higher opportunity costs you will have by doing so,” he said.

Some buy-side firms are taking this further and moving towards a more self-directed trading approach. “In recent years the buy-side has taken more control over the trading decisions at the

n “Clients have a continued focus on anti-gaming and

liquidity selection tactics.”Owain Self, global head of algorithmic trading, UBS