syngene international ltd. (syngene). nse code · pdf fileanand rathi research time horizon...

TRANSCRIPT

Anand Rathi Research

Time Horizon – 12 Months

December 2, 2015

Source: Company Reports, Anand Rathi Research, Ace Equity

V

A

L

U

E

P

I

C

k

Analyst: Ridhi [email protected]

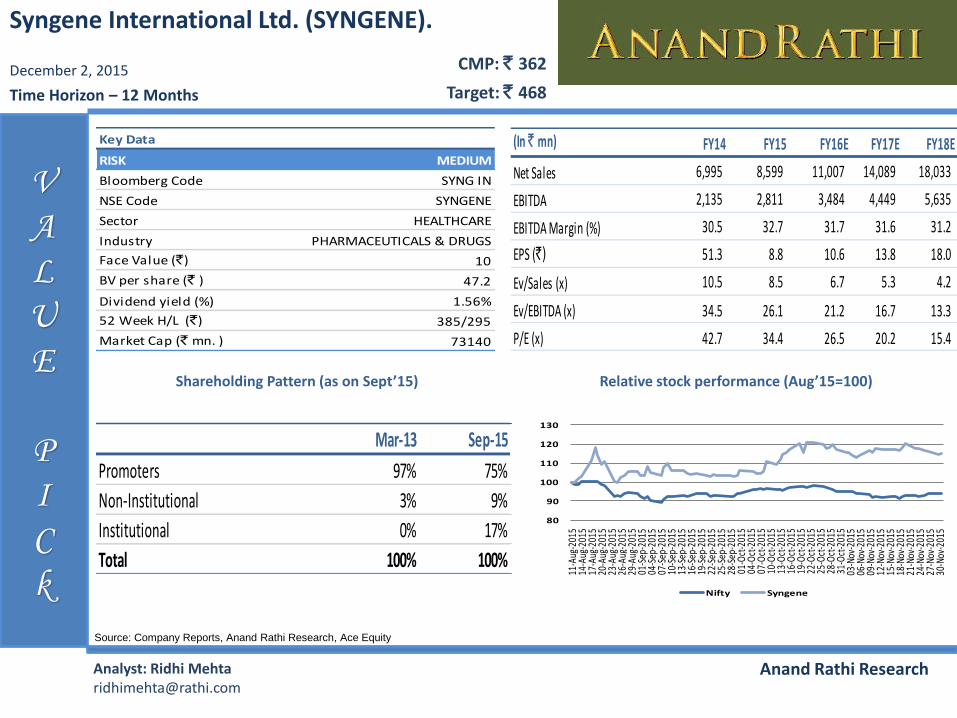

Relative stock performance (Aug’15=100)

CMP: ` 362

Target: ̀ 468

Shareholding Pattern (as on Sept’15)

Syngene International Ltd. (SYNGENE).

Mar-13 Sep-15

Promoters 97% 75%

Non-Institutional 3% 9%

Institutional 0% 17%

Total 100% 100%

RISK MEDIUM

Bloomberg Code SYNG IN

NSE Code SYNGENE

Sector HEALTHCARE

Industry PHARMACEUTICALS & DRUGS

Face Value (`) 10

BV per share (` ) 47.2

Dividend yield (%) 1.56%

52 Week H/L (`) 385/295

Market Cap (` mn. ) 73140

Key Data (In ` mn) FY14 FY15 FY16E FY17E FY18E

Net Sales 6,995 8,599 11,007 14,089 18,033

EBITDA 2,135 2,811 3,484 4,449 5,635

EBITDA Margin (%) 30.5 32.7 31.7 31.6 31.2

EPS (`) 51.3 8.8 10.6 13.8 18.0

Ev/Sales (x) 10.5 8.5 6.7 5.3 4.2

Ev/EBITDA (x) 34.5 26.1 21.2 16.7 13.3

P/E (x) 42.7 34.4 26.5 20.2 15.4

80

90

100

110

120

130

11-A

ug-2

015

14-A

ug-2

015

17-A

ug-2

015

20-A

ug-2

015

23-A

ug-2

015

26-A

ug-2

015

29-A

ug-2

015

01-S

ep-2

015

04-S

ep-2

015

07-S

ep-2

015

10-S

ep-2

015

13-S

ep-2

015

16-S

ep-2

015

19-S

ep-2

015

22-S

ep-2

015

25-S

ep-2

015

28-S

ep-2

015

01-O

ct-2

015

04-O

ct-2

015

07-O

ct-2

015

10-O

ct-2

015

13-O

ct-2

015

16-O

ct-2

015

19-O

ct-2

015

22-O

ct-2

015

25-O

ct-2

015

28-O

ct-2

015

31-O

ct-2

015

03-N

ov-2

015

06-N

ov-2

015

09-N

ov-2

015

12-N

ov-2

015

15-N

ov-2

015

18-N

ov-2

015

21-N

ov-2

015

24-N

ov-2

015

27-N

ov-2

015

30-N

ov-2

015

Nifty Syngene

2 Anand Rathi Research

Syngene International Ltd. (SYNGENE).

Established in 1994 as India’s first Contract Research Organization, Syngene today has evolved as an integrated end –to-end

discovery & development service provider for novel molecular entities (NMEs) across the range of industrial sectors. It

amalgamated Clinigene International Limited (subsidiary), which provides clinical research and clinical trial services, into Syngene

The company enjoys multiyear, multi disciplinary partnership with some of the most respected research focused companies like

Bristol-Myers Squibb Co., Abbott laboratories (Singapore) Pte. Ltd. and Baxter International Inc., among others.

The company has also entered into 3 long-term contracts with two existing clients for commercial manufacturing of their novel

small molecules and also extended long term, dedicated centre contract with Bristol Myers Squibb till 2020

Syngene has world-class R&D and manufacturing infrastructure spread over 900,000 sq.ft. It has also initiated operations at new

state of the art Stability Centre and completed expansion of Manufacturing facilities in Bengaluru, India. This manufacturing

facilities are audited successfully by US FDA, EMA, AAALAC and major life sciences partners. Recently, company has successfully

cleared 2 US FDA audit of facilities with no 483s or observations in the last 6 months.

Additionally, Syngene has set an investment target of US$ 200mn over FY16 to FY18 for (1) Brownfield expansion in its small

molecule manufacturing facility, (2) setting up a new biologic manufacturing facility, (3) expanding its research laboratory in

Bengaluru and for a Greenfield manufacturing unit in the Mangalore SEZ that would be ready in three years.

On financial front, the company has shown exponential growth on all fronts. We believe revenues for Syngene to grow at a CAGR

of 45% between FY15 and FY18 and post healthy EBITDA as well as net profit margins. The scrip trades at P/E of 20.2x FY18E EPS

and we believe the valuations are justifiable based on no listed peer and superior financials. We are initiating our coverage on

Syngene International ltd. with “BUY” recommendation and target price of `468 per share.

SYNGENE INSIGHT

Source: Company Reports, Anand Rathi Research, Ace Equity

3 Anand Rathi Research

Syngene International Ltd. (SYNGENE).

Global Pharma R&D Trends…..

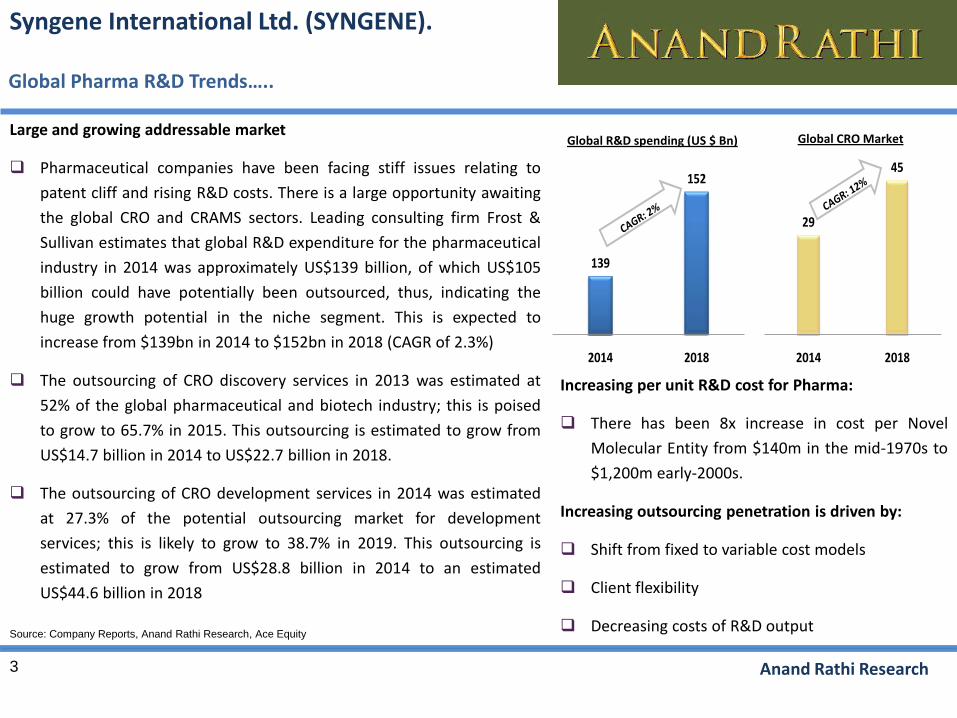

Large and growing addressable market

Pharmaceutical companies have been facing stiff issues relating to

patent cliff and rising R&D costs. There is a large opportunity awaiting

the global CRO and CRAMS sectors. Leading consulting firm Frost &

Sullivan estimates that global R&D expenditure for the pharmaceutical

industry in 2014 was approximately US$139 billion, of which US$105

billion could have potentially been outsourced, thus, indicating the

huge growth potential in the niche segment. This is expected to

increase from $139bn in 2014 to $152bn in 2018 (CAGR of 2.3%)

The outsourcing of CRO discovery services in 2013 was estimated at

52% of the global pharmaceutical and biotech industry; this is poised

to grow to 65.7% in 2015. This outsourcing is estimated to grow from

US$14.7 billion in 2014 to US$22.7 billion in 2018.

The outsourcing of CRO development services in 2014 was estimated

at 27.3% of the potential outsourcing market for development

services; this is likely to grow to 38.7% in 2019. This outsourcing is

estimated to grow from US$28.8 billion in 2014 to an estimated

US$44.6 billion in 2018

139

152

2014 2018

29

45

2014 2018

Global R&D spending (US $ Bn) Global CRO Market

Increasing per unit R&D cost for Pharma:

There has been 8x increase in cost per Novel

Molecular Entity from $140m in the mid-1970s to

$1,200m early-2000s.

Increasing outsourcing penetration is driven by:

Shift from fixed to variable cost models

Client flexibility

Decreasing costs of R&D outputSource: Company Reports, Anand Rathi Research, Ace Equity

4 Anand Rathi Research

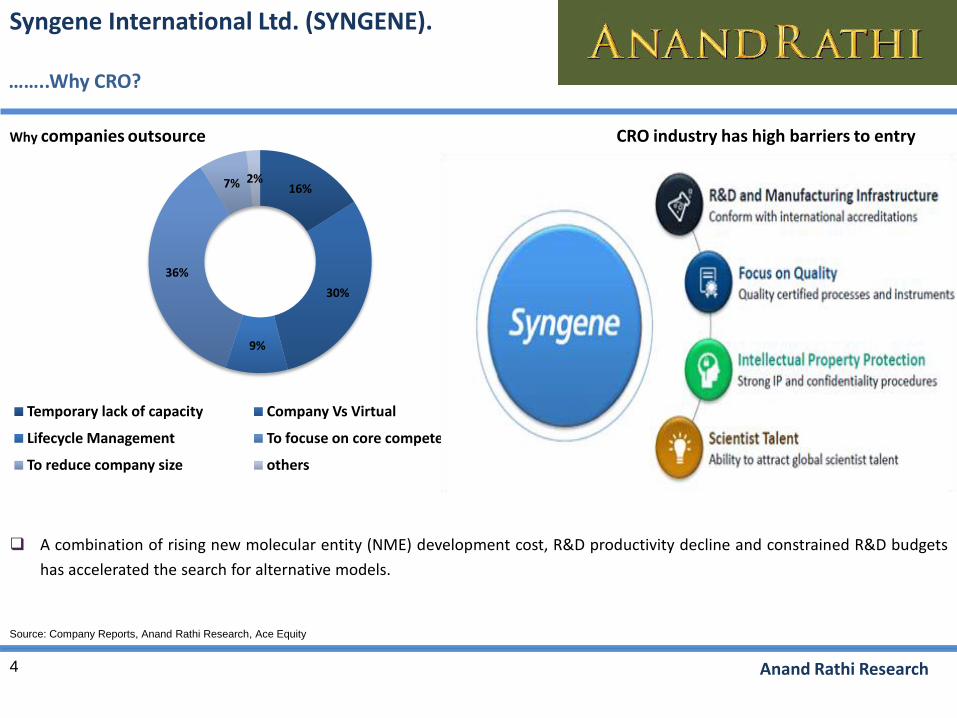

16%

30%

9%

36%

7% 2%

Temporary lack of capacity Company Vs Virtual

Lifecycle Management To focuse on core competences

To reduce company size others

Why companies outsource

Syngene International Ltd. (SYNGENE).

……..Why CRO?

CRO industry has high barriers to entry

A combination of rising new molecular entity (NME) development cost, R&D productivity decline and constrained R&D budgets

has accelerated the search for alternative models.

Source: Company Reports, Anand Rathi Research, Ace Equity

5 Anand Rathi Research

Dedicated centers

Integrated Services

Dedicated Infrastructure customized

for client’s requirements

Long term, FTE based contracts

Currently 3 in place: BBRC, ANRD

and BGRC

Syngene International Ltd. (SYNGENE).

Development Services

Preclinical studies, Stability,

formulation, CMC and Clinical

supplies, Clinical development

etc.

Largely FFS based services

(both short and long term)

High renewal rates in

Manufacturing services

Verticals Overview

Discovery Services

Discovery Chemistry, Discovery

Biology and in-vivo services

Multi-client infrastructure

Largely FTE based engagements,

typically renewed annually

High renewal rates

Source: Company Reports, Anand Rathi Research, Ace Equity

6 Anand Rathi Research

Syngene International Ltd. (SYNGENE).

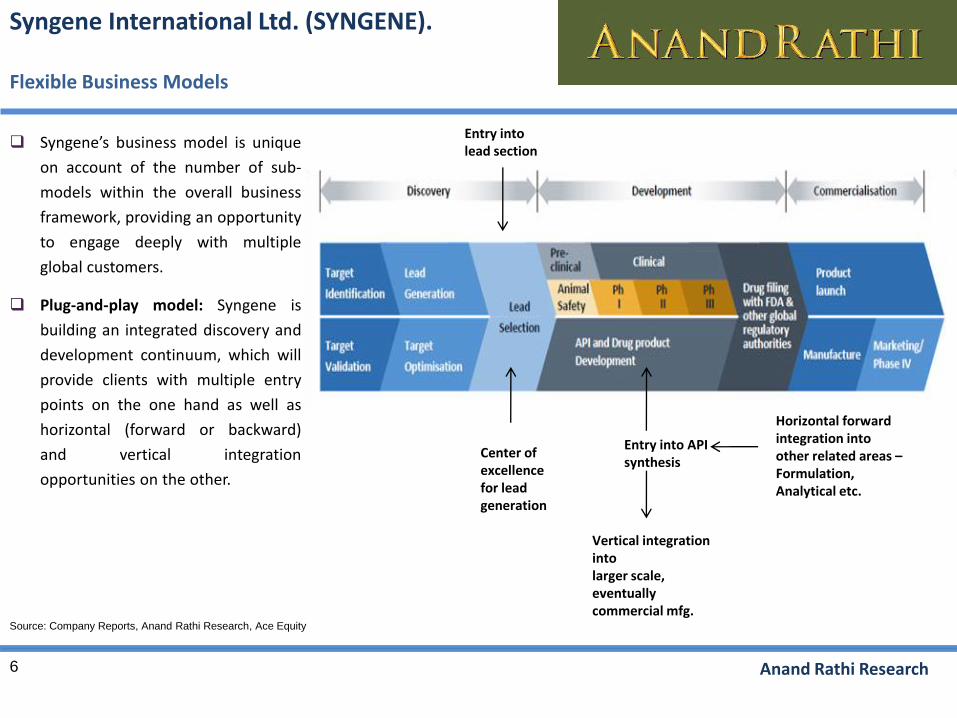

Flexible Business Models

Syngene’s business model is unique

on account of the number of sub-

models within the overall business

framework, providing an opportunity

to engage deeply with multiple

global customers.

Plug-and-play model: Syngene is

building an integrated discovery and

development continuum, which will

provide clients with multiple entry

points on the one hand as well as

horizontal (forward or backward)

and vertical integration

opportunities on the other.

Center of excellence for lead generation

Entry into API synthesis

Vertical integration intolarger scale, eventuallycommercial mfg.

Horizontal forwardintegration intoother related areas –Formulation, Analytical etc.

Entry into lead section

Source: Company Reports, Anand Rathi Research, Ace Equity

7 Anand Rathi Research

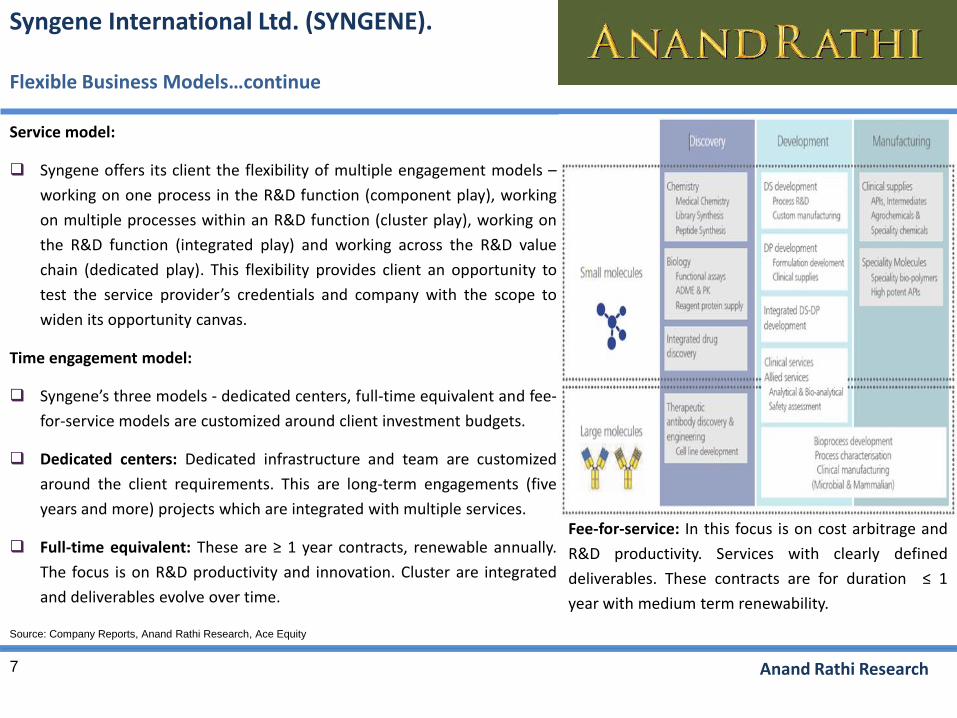

Service model:

Syngene offers its client the flexibility of multiple engagement models –

working on one process in the R&D function (component play), working

on multiple processes within an R&D function (cluster play), working on

the R&D function (integrated play) and working across the R&D value

chain (dedicated play). This flexibility provides client an opportunity to

test the service provider’s credentials and company with the scope to

widen its opportunity canvas.

Time engagement model:

Syngene’s three models - dedicated centers, full-time equivalent and fee-

for-service models are customized around client investment budgets.

Dedicated centers: Dedicated infrastructure and team are customized

around the client requirements. This are long-term engagements (five

years and more) projects which are integrated with multiple services.

Full-time equivalent: These are ≥ 1 year contracts, renewable annually.

The focus is on R&D productivity and innovation. Cluster are integrated

and deliverables evolve over time.

Syngene International Ltd. (SYNGENE).

Fee-for-service: In this focus is on cost arbitrage and

R&D productivity. Services with clearly defined

deliverables. These contracts are for duration ≤ 1

year with medium term renewability.

Source: Company Reports, Anand Rathi Research, Ace Equity

Flexible Business Models…continue

8 Anand Rathi Research

Syngene International Ltd. (SYNGENE).

Multiple Layers of Growth

Customer Engagement

Expanding/Extendingexisting clients:

1. High service integration

2. Dedicated center model

Engage New Clients:

1. Tailored service offerings

2. Dedicated personnel

Forward Integration

Moving CRO to CRAMSwith commercialmanufacturing :

1. “Follow the molecule”by expanding intocommercialization

Capability

Capability Additions:

1. New capabilities acrossmultiple domains includingthe allied sectors

2. Stability, analytical &bio-analytical services, viraltesting

New platforms:

siRNA, DC.

Capacity

Capacity Expansion:

1. Consistent Expansion

2. FTE services, manufacturing, formulation, biologics, stability

Source: Company Reports, Anand Rathi Research, Ace Equity

9 Anand Rathi Research

Syngene International Ltd. (SYNGENE).

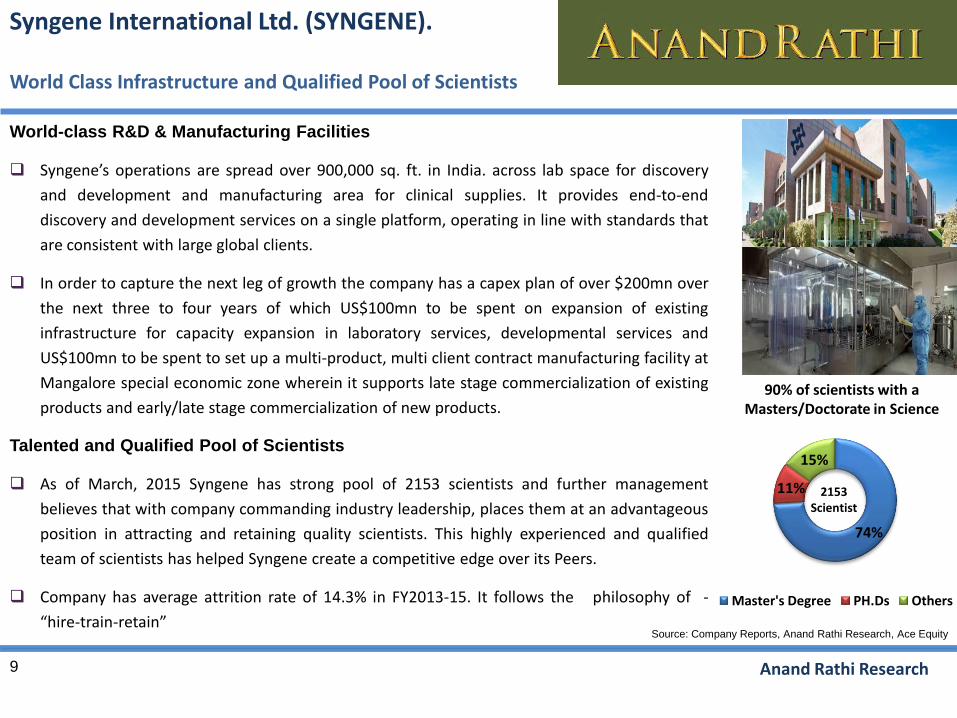

World-class R&D & Manufacturing Facilities

Syngene’s operations are spread over 900,000 sq. ft. in India. across lab space for discovery

and development and manufacturing area for clinical supplies. It provides end-to-end

discovery and development services on a single platform, operating in line with standards that

are consistent with large global clients.

In order to capture the next leg of growth the company has a capex plan of over $200mn over

the next three to four years of which US$100mn to be spent on expansion of existing

infrastructure for capacity expansion in laboratory services, developmental services and

US$100mn to be spent to set up a multi-product, multi client contract manufacturing facility at

Mangalore special economic zone wherein it supports late stage commercialization of existing

products and early/late stage commercialization of new products.

Talented and Qualified Pool of Scientists

As of March, 2015 Syngene has strong pool of 2153 scientists and further management

believes that with company commanding industry leadership, places them at an advantageous

position in attracting and retaining quality scientists. This highly experienced and qualified

team of scientists has helped Syngene create a competitive edge over its Peers.

Company has average attrition rate of 14.3% in FY2013-15. It follows the philosophy of -

“hire-train-retain”

World Class Infrastructure and Qualified Pool of Scientists

74%

11%

15%

Master's Degree PH.Ds Others

2153 Scientist

90% of scientists with a Masters/Doctorate in Science

Source: Company Reports, Anand Rathi Research, Ace Equity

10 Anand Rathi Research

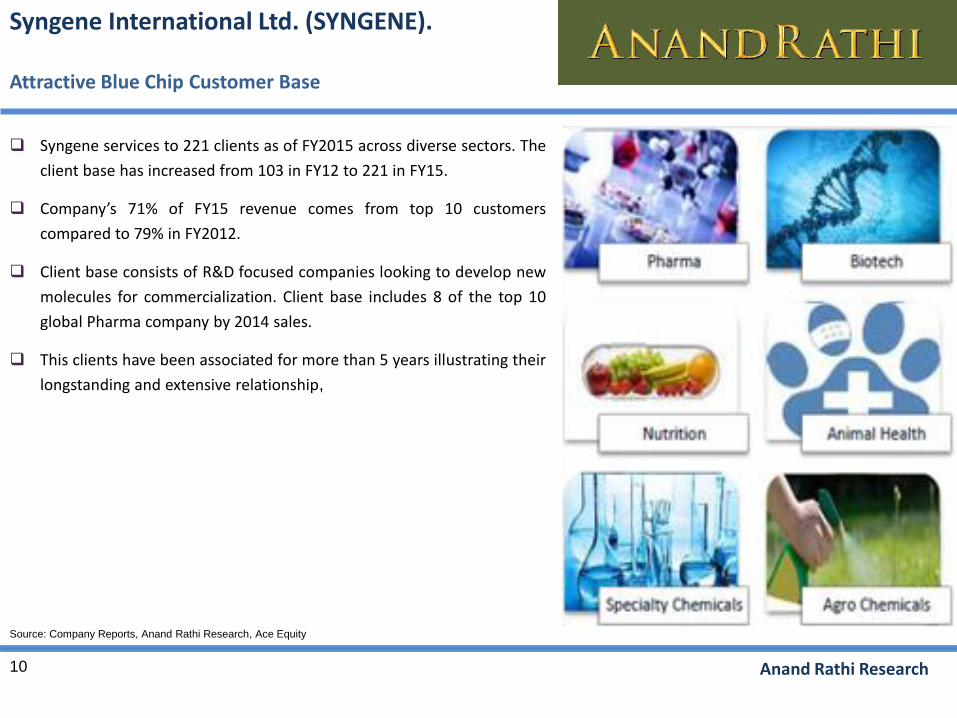

Syngene services to 221 clients as of FY2015 across diverse sectors. The

client base has increased from 103 in FY12 to 221 in FY15.

Company’s 71% of FY15 revenue comes from top 10 customers

compared to 79% in FY2012.

Client base consists of R&D focused companies looking to develop new

molecules for commercialization. Client base includes 8 of the top 10

global Pharma company by 2014 sales.

This clients have been associated for more than 5 years illustrating their

longstanding and extensive relationship,

Syngene International Ltd. (SYNGENE).

Source: Company Reports, Anand Rathi Research, Ace Equity

Attractive Blue Chip Customer Base

11 Anand Rathi Research

Though Syngene follows unique business model, its closest

comparable peer is Wuxi Pharmatech & GVK bioscience

Wuxi Pharmatech (Global Player): The company is a leading global

contract R&D services provider serving the pharmaceutical, biotech,

and medical device industries. It provides a broad and integrated

portfolio of laboratory and manufacturing services throughout the

R&D process. Wuxi Phramatech is listed both on US & Chinese stock

exchange. Client base includes Pfizer, Merck, AstraZeneca, Novartis,

Genentech, Millennium, etc.

GVK Bioscience (Indian Player): GVK Biosciences (GVK BIO) is

one of Asia’s leading Discovery Research and Development

organizations. GVK BIO provides a broad spectrum of services, across

the R&D and manufacturing value chain with a focus on speed and

quality. GVK BIO capabilities include integrated programs, discovery

services, Clinical development, Contract manufacturing, formulation

& informatics. The company is not publicly listed

Syngene International Ltd. (SYNGENE).

Competitive Analysis

Particulars FY15 FY14 CY14

INR (Mn) Syngene GVK Bio WuXi

Sales 8,599 4,186 41,150

Sales Growth (%) 23.0 33.0 17.0

EBITDA 2,811 1,324 9,159

EBITDAM (%) 34.1 31.6 22.0

PAT 1,750 960 6,847

PATM (%) 20.4 23.0 17.0

ROCE (%) 23.3 21.7 26.7

No. of Scientist 2,153 2,000 6,000

12 Anand Rathi Research

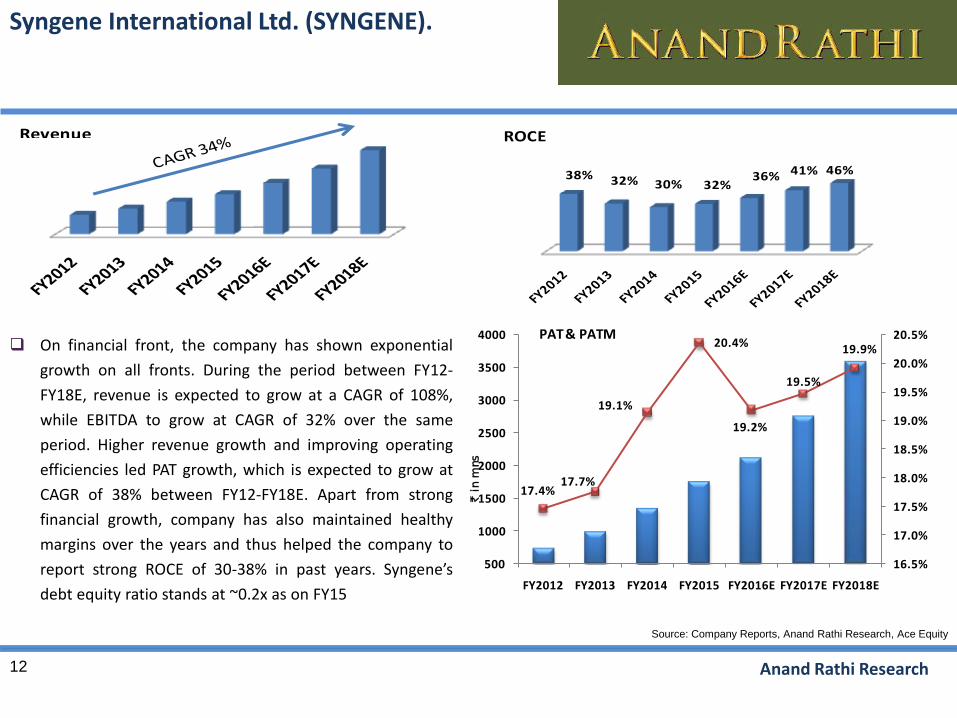

On financial front, the company has shown exponential

growth on all fronts. During the period between FY12-

FY18E, revenue is expected to grow at a CAGR of 108%,

while EBITDA to grow at CAGR of 32% over the same

period. Higher revenue growth and improving operating

efficiencies led PAT growth, which is expected to grow at

CAGR of 38% between FY12-FY18E. Apart from strong

financial growth, company has also maintained healthy

margins over the years and thus helped the company to

report strong ROCE of 30-38% in past years. Syngene’s

debt equity ratio stands at ~0.2x as on FY15

Syngene International Ltd. (SYNGENE).

Source: Company Reports, Anand Rathi Research, Ace Equity

Revenue

38% 32% 30% 32%36% 41% 46%

ROCE

17.4%17.7%

19.1%

20.4%

19.2%

19.5%

19.9%

16.5%

17.0%

17.5%

18.0%

18.5%

19.0%

19.5%

20.0%

20.5%

500

1000

1500

2000

2500

3000

3500

4000

FY2012 FY2013 FY2014 FY2015 FY2016E FY2017E FY2018E

PAT & PATM

` in m

ns

13 Anand Rathi Research

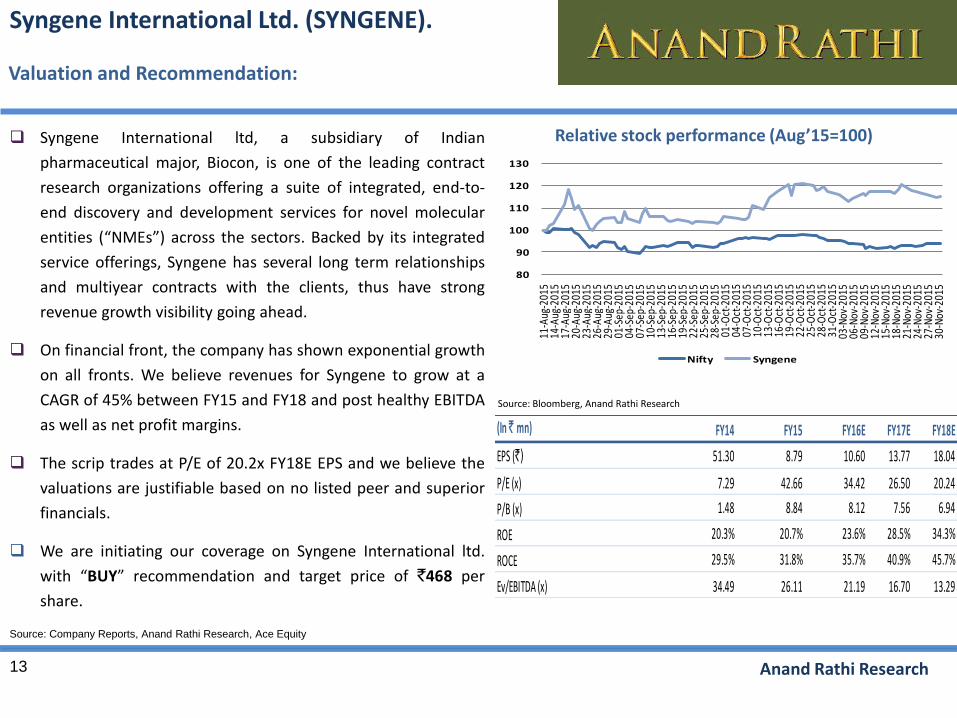

Syngene International ltd, a subsidiary of Indian

pharmaceutical major, Biocon, is one of the leading contract

research organizations offering a suite of integrated, end-to-

end discovery and development services for novel molecular

entities (“NMEs”) across the sectors. Backed by its integrated

service offerings, Syngene has several long term relationships

and multiyear contracts with the clients, thus have strong

revenue growth visibility going ahead.

On financial front, the company has shown exponential growth

on all fronts. We believe revenues for Syngene to grow at a

CAGR of 45% between FY15 and FY18 and post healthy EBITDA

as well as net profit margins.

The scrip trades at P/E of 20.2x FY18E EPS and we believe the

valuations are justifiable based on no listed peer and superior

financials.

We are initiating our coverage on Syngene International ltd.

with “BUY” recommendation and target price of `468 per

share.

Relative stock performance (Aug’15=100)

Valuation and Recommendation:

Source: Bloomberg, Anand Rathi Research

Syngene International Ltd. (SYNGENE).

Source: Company Reports, Anand Rathi Research, Ace Equity

(In ` mn) FY14 FY15 FY16E FY17E FY18E

EPS (`) 51.30 8.79 10.60 13.77 18.04

P/E (x) 7.29 42.66 34.42 26.50 20.24

P/B (x) 1.48 8.84 8.12 7.56 6.94

ROE 20.3% 20.7% 23.6% 28.5% 34.3%

ROCE 29.5% 31.8% 35.7% 40.9% 45.7%

Ev/EBITDA (x) 34.49 26.11 21.19 16.70 13.29

80

90

100

110

120

130

11-A

ug-2

015

14-A

ug-2

015

17-A

ug-2

015

20-A

ug-2

015

23-A

ug-2

015

26-A

ug-2

015

29-A

ug-2

015

01-S

ep-2

015

04-S

ep-2

015

07-S

ep-2

015

10-S

ep-2

015

13-S

ep-2

015

16-S

ep-2

015

19-S

ep-2

015

22-S

ep-2

015

25-S

ep-2

015

28-S

ep-2

015

01-O

ct-2

015

04-O

ct-2

015

07-O

ct-2

015

10-O

ct-2

015

13-O

ct-2

015

16-O

ct-2

015

19-O

ct-2

015

22-O

ct-2

015

25-O

ct-2

015

28-O

ct-2

015

31-O

ct-2

015

03-N

ov-2

015

06-N

ov-2

015

09-N

ov-2

015

12-N

ov-2

015

15-N

ov-2

015

18-N

ov-2

015

21-N

ov-2

015

24-N

ov-2

015

27-N

ov-2

015

30-N

ov-2

015

Nifty Syngene

14 Anand Rathi Research

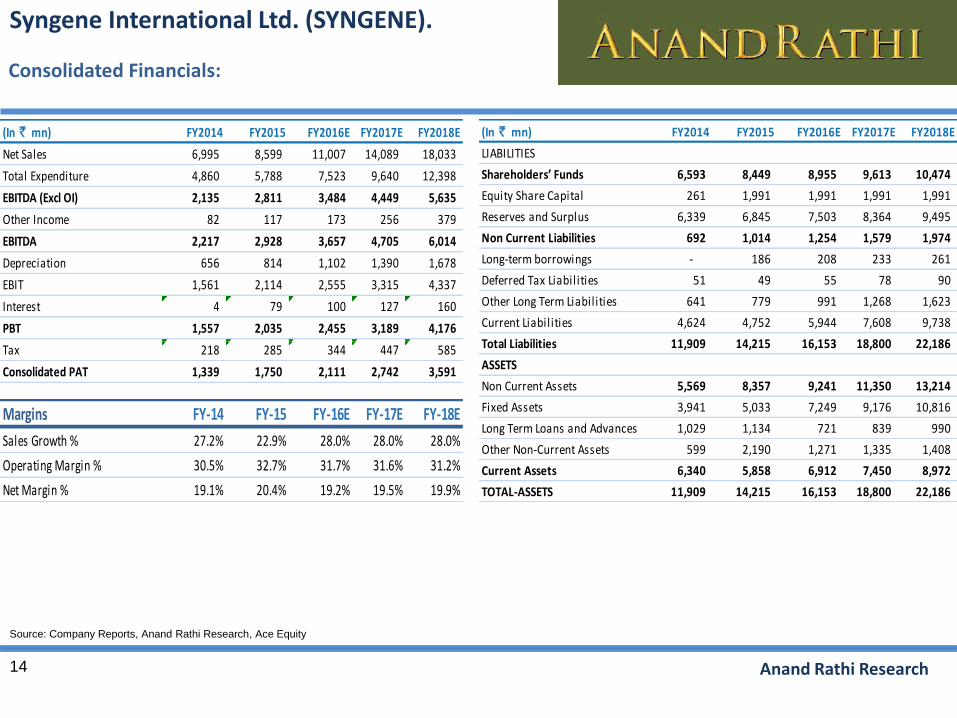

Consolidated Financials:

Syngene International Ltd. (SYNGENE).

Source: Company Reports, Anand Rathi Research, Ace Equity

(In ` mn) FY2014 FY2015 FY2016E FY2017E FY2018E

Net Sales 6,995 8,599 11,007 14,089 18,033

Total Expenditure 4,860 5,788 7,523 9,640 12,398

EBITDA (Excl OI) 2,135 2,811 3,484 4,449 5,635

Other Income 82 117 173 256 379

EBITDA 2,217 2,928 3,657 4,705 6,014

Depreciation 656 814 1,102 1,390 1,678

EBIT 1,561 2,114 2,555 3,315 4,337

Interest 4 79 100 127 160

PBT 1,557 2,035 2,455 3,189 4,176

Tax 218 285 344 447 585

Consolidated PAT 1,339 1,750 2,111 2,742 3,591

Margins FY-14 FY-15 FY-16E FY-17E FY-18E

Sales Growth % 27.2% 22.9% 28.0% 28.0% 28.0%

Operating Margin % 30.5% 32.7% 31.7% 31.6% 31.2%

Net Margin % 19.1% 20.4% 19.2% 19.5% 19.9%

(In ` mn) FY2014 FY2015 FY2016E FY2017E FY2018E

LIABILITIES

Shareholders’ Funds 6,593 8,449 8,955 9,613 10,474

Equity Share Capital 261 1,991 1,991 1,991 1,991

Reserves and Surplus 6,339 6,845 7,503 8,364 9,495

Non Current Liabilities 692 1,014 1,254 1,579 1,974

Long-term borrowings - 186 208 233 261

Deferred Tax Liabilities 51 49 55 78 90

Other Long Term Liabilities 641 779 991 1,268 1,623

Current Liabilities 4,624 4,752 5,944 7,608 9,738

Total Liabilities 11,909 14,215 16,153 18,800 22,186

ASSETS

Non Current Assets 5,569 8,357 9,241 11,350 13,214

Fixed Assets 3,941 5,033 7,249 9,176 10,816

Long Term Loans and Advances 1,029 1,134 721 839 990

Other Non-Current Assets 599 2,190 1,271 1,335 1,408

Current Assets 6,340 5,858 6,912 7,450 8,972

TOTAL-ASSETS 11,909 14,215 16,153 18,800 22,186

15 Anand Rathi Research

Forex fluctuation

Amount of global R&D spend outsourcing to India,

Client Concentration,

Execution efficacy, Quality & regulatory

Key Risks:

Syngene International Ltd. (SYNGENE).

Source: Company Reports, Anand Rathi Research

16 Anand Rathi Research

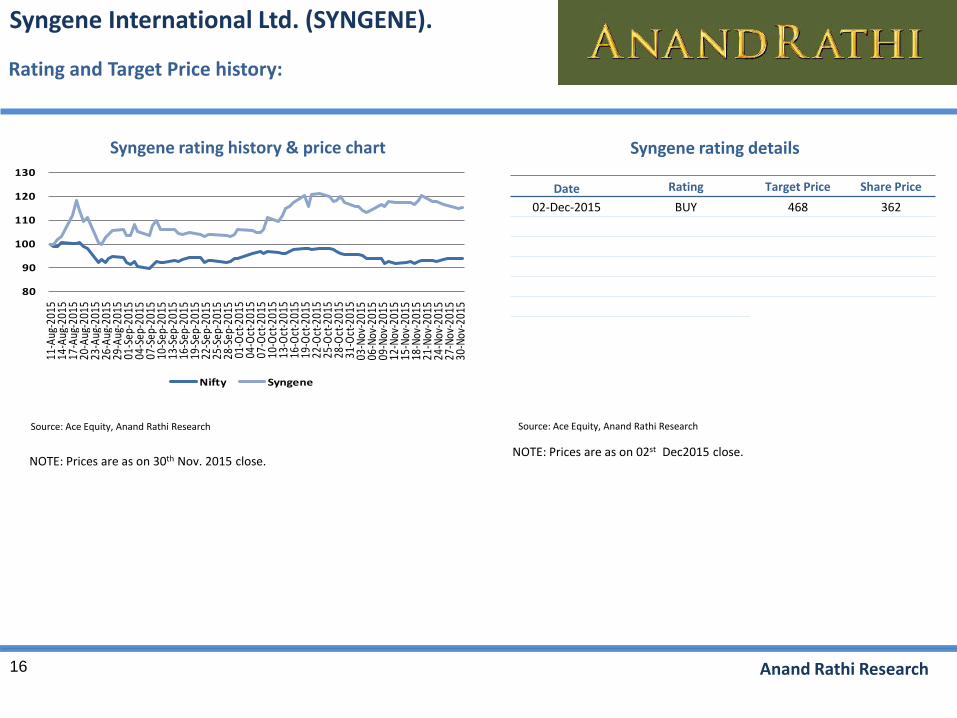

Rating and Target Price history:

Syngene rating detailsSyngene rating history & price chart

Source: Ace Equity, Anand Rathi Research Source: Ace Equity, Anand Rathi Research

NOTE: Prices are as on 30th Nov. 2015 close.

Syngene International Ltd. (SYNGENE).

NOTE: Prices are as on 02st Dec2015 close.

Date Rating Target Price Share Price

02-Dec-2015 BUY 468 362

80

90

100

110

120

130

11-A

ug-2

015

14-A

ug-2

015

17-A

ug-2

015

20-A

ug-2

015

23-A

ug-2

015

26-A

ug-2

015

29-A

ug-2

015

01-S

ep-2

015

04-S

ep-2

015

07-S

ep-2

015

10-S

ep-2

015

13-S

ep-2

015

16-S

ep-2

015

19-S

ep-2

015

22-S

ep-2

015

25-S

ep-2

015

28-S

ep-2

015

01-O

ct-2

015

04-O

ct-2

015

07-O

ct-2

015

10-O

ct-2

015

13-O

ct-2

015

16-O

ct-2

015

19-O

ct-2

015

22-O

ct-2

015

25-O

ct-2

015

28-O

ct-2

015

31-O

ct-2

015

03-N

ov-2

015

06-N

ov-2

015

09-N

ov-2

015

12-N

ov-2

015

15-N

ov-2

015

18-N

ov-2

015

21-N

ov-2

015

24-N

ov-2

015

27-N

ov-2

015

30-N

ov-2

015

Nifty Syngene

17 Anand Rathi Research

Syngene International Ltd. (SYNGENE).

Disclaimer:

Research Disclaimer and Disclosure inter-alia as required under Securities and Exchange Board of India (Research Analysts) Regulations, 2014

Anand Rathi Share and Stock Brokers Ltd. (hereinafter refer as ARSSBL) (Research Entity) is a subsidiary of the Anand Rathi Financial Services Ltd. ARSSBL is a corporate

trading and clearing member of Bombay Stock Exchange Ltd, National Stock Exchange of India Ltd. (NSEIL), Multi Stock Exchange of India Ltd (MCX-SX), United stock

exchange and also depository participant with National Securities Depository Ltd (NSDL) and Central Depository Services Ltd. ARSSBL is engaged into the business of

Stock Broking, Depository Participant, Mutual Fund distributor.

The research analysts, strategists, or research associates principally responsible for the preparation of Anand Rathi Research have received compensation based upon

various factors, including quality of research, investor client feedback, stock picking, competitive factors, firm revenues.

General Disclaimer: - This Research Report (hereinafter called “Report”) is meant solely for use by the recipient and is not for circulation. This Report does not

constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. The

recommendations, if any, made herein are expression of views and/or opinions and should not be deemed or construed to be neither advice for the purpose of

purchase or sale of any security, derivatives or any other security through ARSSBL nor any solicitation or offering of any investment /trading opportunity on behalf of

the issuer(s) of the respective security (ies) referred to herein. These information / opinions / views are not meant to serve as a professional investment guide for the

readers. No action is solicited based upon the information provided herein. Recipients of this Report should rely on information/data arising out of their own

investigations. Readers are advised to seek independent professional advice and arrive at an informed trading/investment decision before executing any trades or

making any investments. This Report has been prepared on the basis of publicly available information, internally developed data and other sources believed by ARSSBL

to be reliable. ARSSBL or its directors, employees, affiliates or representatives do not assume any responsibility for, or warrant the accuracy, completeness, adequacy

and reliability of such information / opinions / views. While due care has been taken to ensure that the disclosures and opinions given are fair and reasonable, none of

the directors, employees, affiliates or representatives of ARSSBL shall be liable for any direct, indirect, special, incidental, consequential, punitive or exemplary

damages, including lost profits arising in any way whatsoever from the information / opinions / views contained in this Report. The price and value of the investments

referred to in this Report and the income from them may go down as well as up, and investors may realize losses on any investments. Past performance is not a guide

for future performance. ARSSBL does not provide tax advice to its clients, and all investors are strongly advised to consult with their tax advisers regarding taxation

aspects of any potential investment.

Continued…

18 Anand Rathi Research

Syngene International Ltd. (SYNGENE).

Disclaimer:

Contd.

Opinions expressed are our current opinions as of the date appearing on this Research only. We do not undertake to advise you as to any change of our views expressed in this Report. Research Report may differ between ARSSBL’s RAs and/ or ARSSBL’s associate companies on account of differences in research methodology, personal judgment and difference in time horizons for which recommendations are made. User should keep this risk in mind and not hold ARSSBL, its employees and associates responsible for any losses, damages of any type whatsoever.

ARSSBL and its associates or employees may; (a) from time to time, have long or short positions in, and buy or sell the investments in/ security of company (ies) mentioned herein or (b) be engaged in any other transaction involving such investments/ securities of company (ies) discussed herein or act as advisor or lender / borrower to such company (ies) these and other activities of ARSSBL and its associates or employees may not be construed as potential conflict of interest with respect to any recommendation and related information and opinions. Without limiting any of the foregoing, in no event shall ARSSBL and its associates or employees or any third party involved in, or related to computing or compiling the information have any liability for any damages of any kind.

Details of Associates of ARSSBL and Brief History of Disciplinary action by regulatory authorities & its associates are available on our website i. e. www.rathionline.com

Disclaimers in respect of jurisdiction: This report is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or which would subject ARSSBL to any registration or licensing requirement within such jurisdiction(s). No action has been or will be taken by ARSSBL in any jurisdiction (other than India), where any action for such purpose(s) is required. Accordingly, this Report shall not be possessed, circulated and/or distributed in any such country or jurisdiction unless such action is in compliance with all applicable laws and regulations of such country or jurisdiction. ARSSBL requires such recipient to inform himself about and to observe any restrictions at his own expense, without any liability to ARSSBL. Any dispute arising out of this Report shall be subject to the exclusive jurisdiction of the Courts in India.

Copyright: - This report is strictly confidential and is being furnished to you solely for your information. All material presented in this report, unless specifically indicated

otherwise, is under copyright to ARSSBL. None of the material, its content, or any copy of such material or content, may be altered in any way, transmitted, copied or

reproduced (in whole or in part) or redistributed in any form to any other party, without the prior express written permission of ARSSBL. All trademarks, service marks

and logos used in this report are trademarks or service marks or registered trademarks or service marks of ARSSBL or its affiliates, unless specifically mentioned

otherwise.

Contd.

19 Anand Rathi Research

Disclaimer:

Contd.

Statements on ownership and material conflicts of interest, compensation - ARSSBL and Associates

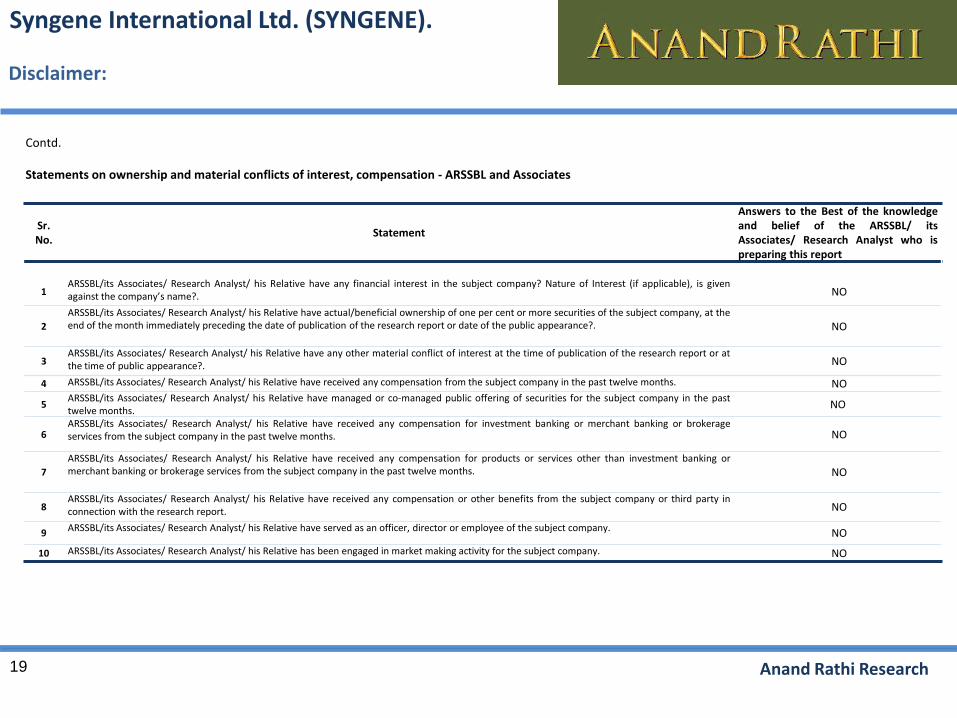

Sr. No.

Statement

Answers to the Best of the knowledgeand belief of the ARSSBL/ itsAssociates/ Research Analyst who ispreparing this report

1ARSSBL/its Associates/ Research Analyst/ his Relative have any financial interest in the subject company? Nature of Interest (if applicable), is givenagainst the company’s name?. NO

2

ARSSBL/its Associates/ Research Analyst/ his Relative have actual/beneficial ownership of one per cent or more securities of the subject company, at theend of the month immediately preceding the date of publication of the research report or date of the public appearance?. NO

3ARSSBL/its Associates/ Research Analyst/ his Relative have any other material conflict of interest at the time of publication of the research report or atthe time of public appearance?. NO

4 ARSSBL/its Associates/ Research Analyst/ his Relative have received any compensation from the subject company in the past twelve months. NO

5ARSSBL/its Associates/ Research Analyst/ his Relative have managed or co-managed public offering of securities for the subject company in the pasttwelve months.

NO

6ARSSBL/its Associates/ Research Analyst/ his Relative have received any compensation for investment banking or merchant banking or brokerageservices from the subject company in the past twelve months. NO

7

ARSSBL/its Associates/ Research Analyst/ his Relative have received any compensation for products or services other than investment banking ormerchant banking or brokerage services from the subject company in the past twelve months. NO

8ARSSBL/its Associates/ Research Analyst/ his Relative have received any compensation or other benefits from the subject company or third party inconnection with the research report. NO

9 ARSSBL/its Associates/ Research Analyst/ his Relative have served as an officer, director or employee of the subject company. NO

10 ARSSBL/its Associates/ Research Analyst/ his Relative has been engaged in market making activity for the subject company. NO

Syngene International Ltd. (SYNGENE).