syllabus for ccfa qualifying exams - iicfaglobal.com · syllabus for ccfa qualifying exams ... 2.1...

TRANSCRIPT

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 0

INTERNATIONAL INSTITUTE OF CERTIFIED

FORENSIC ACCOUNTANTS, INC. IICFA, USA

Syllabus for CCFA

Qualifying Exams

A Member of the International Federation of Forensic Accountants & Auditors (IFFAA)

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 1

A PUBLICATION OF THE INTERNATIONAL INSTITUTE OF CERTIFIED FORENSIC

ACCOUNTANTS, INC., USA

Copyright © International Institute of Certified Forensic Accountants, IICFA, USA, 2014

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording or otherwise without prior Permission from the Institute of Chartered Certified Forensic Accountants. INTERNATIONAL INSTITUTE OF CERTIFIED FORENSIC ACCOUNTANTS, INC USA

Registered Office Address: 16192 Coastal Highway, Lewes, DE 19958, Sussex

USA

Administrative Office: LBV 73 Community 17 Lashibi, Tema Ghana

Tel: +233(0)303931477

Mobile: +233(0)244709741

+233 (0) 504422455

[email protected] www.iicfaglobal.com

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 2

Table of Contents Introduction .............................................................................................................................................................. 3

Features of the Professional Examination Scheme.............................................................................................. 6

Objectives and Expected Performance Outcome of Each Level........................................................................ 7

The Chartered Certified Forensic Accountant, CCFA ........................................................................................ 8

PROFESSIONAL LEVEL 1 ..................................................................................................................................... 9

1.1 Principles of Forensic Accounting ............................................................................................................ 9

1.2 Principles of Fraud Examination ............................................................................................................ 14

1.3 Principles of Taxation ............................................................................................................................... 19

1.4 Financial Accounting Foundation .......................................................................................................... 23

1.5 Business Management Studies ................................................................................................................ 29

PROFESSIONAL LEVEL 2 ................................................................................................................................... 34

2.1 Forensic Criminology and Legal Studies ..................................................................................................... 34

2.2 Corporate Fraud and Internal Control ......................................................................................................... 38

2.3 Financial Statement and Institution Fraud................................................................................................... 43

2.4 Financial Reporting ......................................................................................................................................... 47

2.5 Forensic Investigation Techniques ................................................................................................................ 52

PROFESSIONAL LEVEL 3 ................................................................................................................................... 59

3.1 Management Accounting and Cost Control ................................................................................................ 59

3.2 Computer Forensics and Cyber Crime ......................................................................................................... 64

3.3 Financial Management Strategy .................................................................................................................... 69

3.4 Financial Crime Law ................................................................................................................................. 75

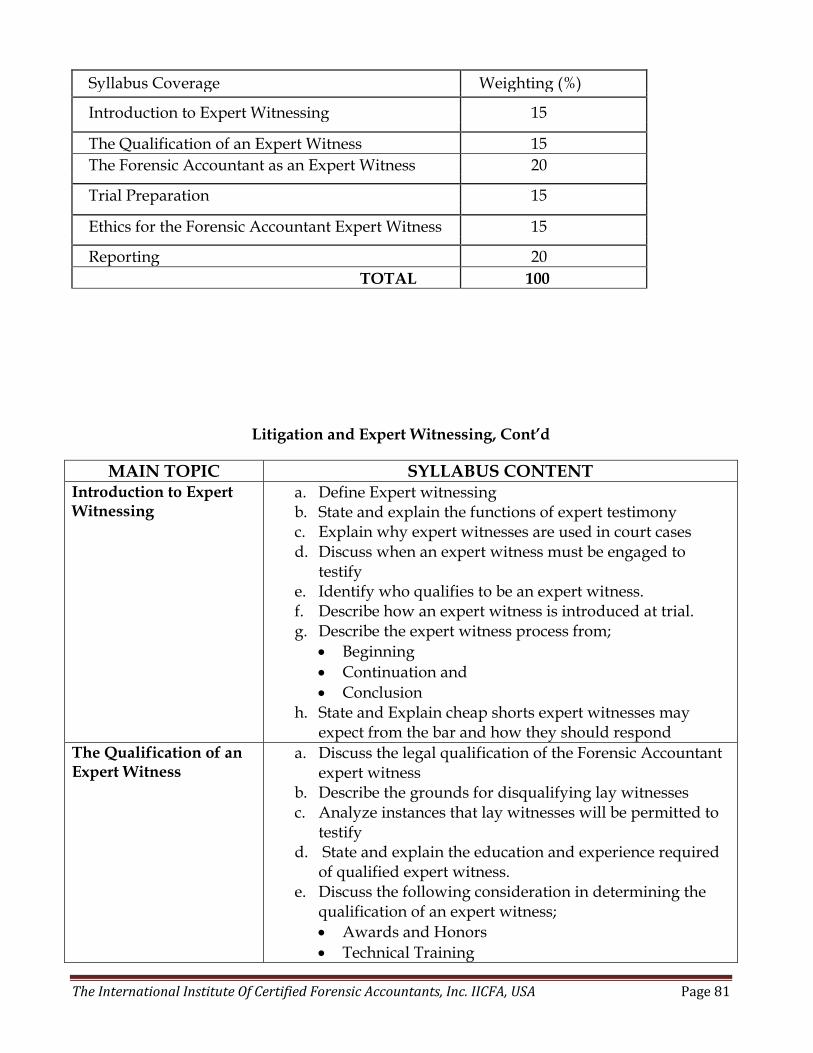

3.5 Litigation and Expert Witnessing ........................................................................................................... 80

PROFESSIONAL LEVEL 4 ................................................................................................................................... 84

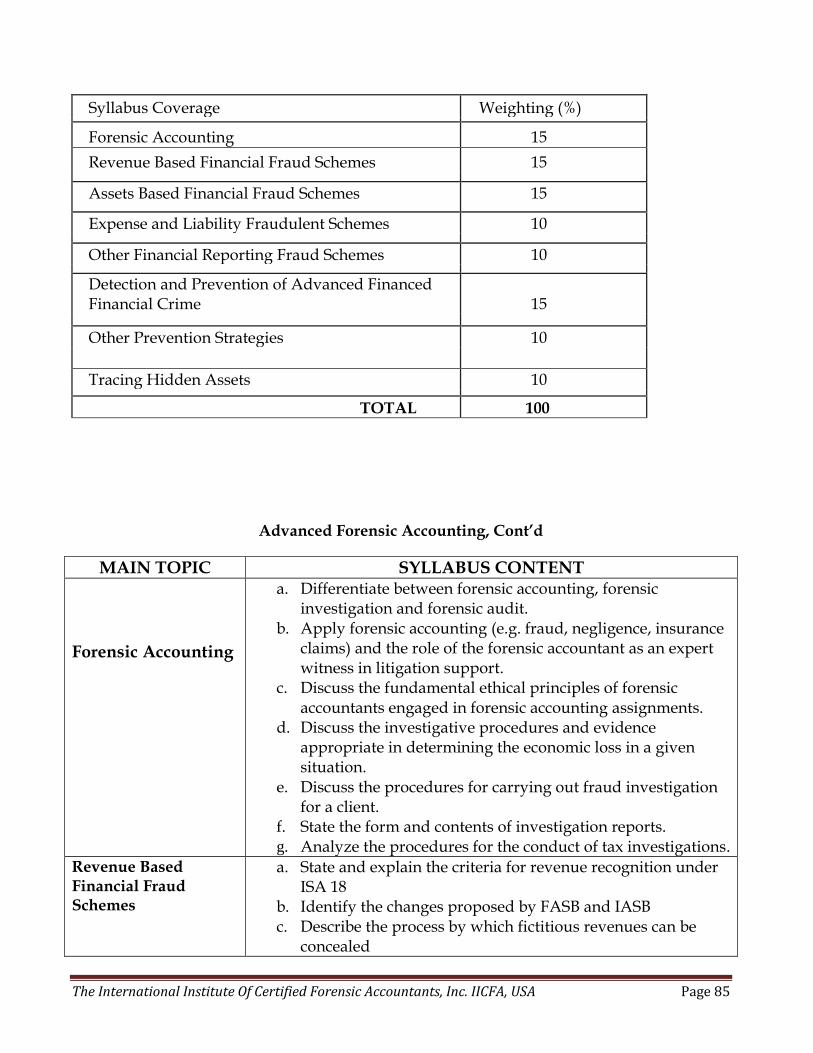

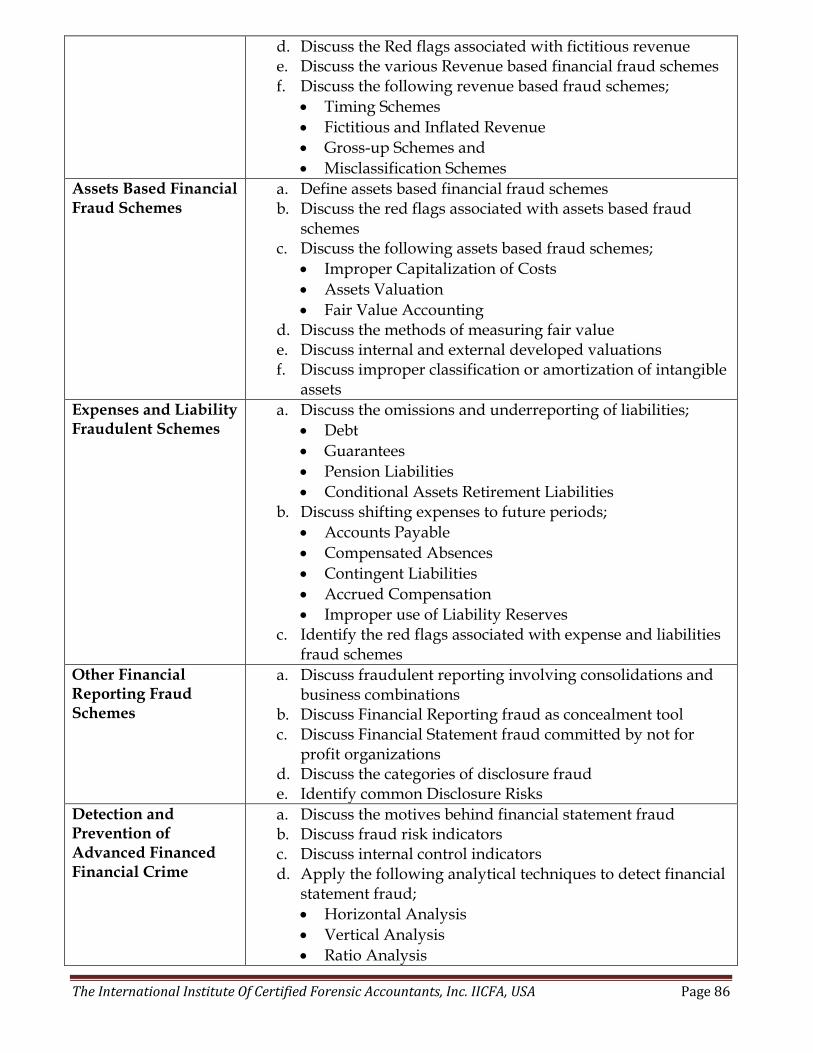

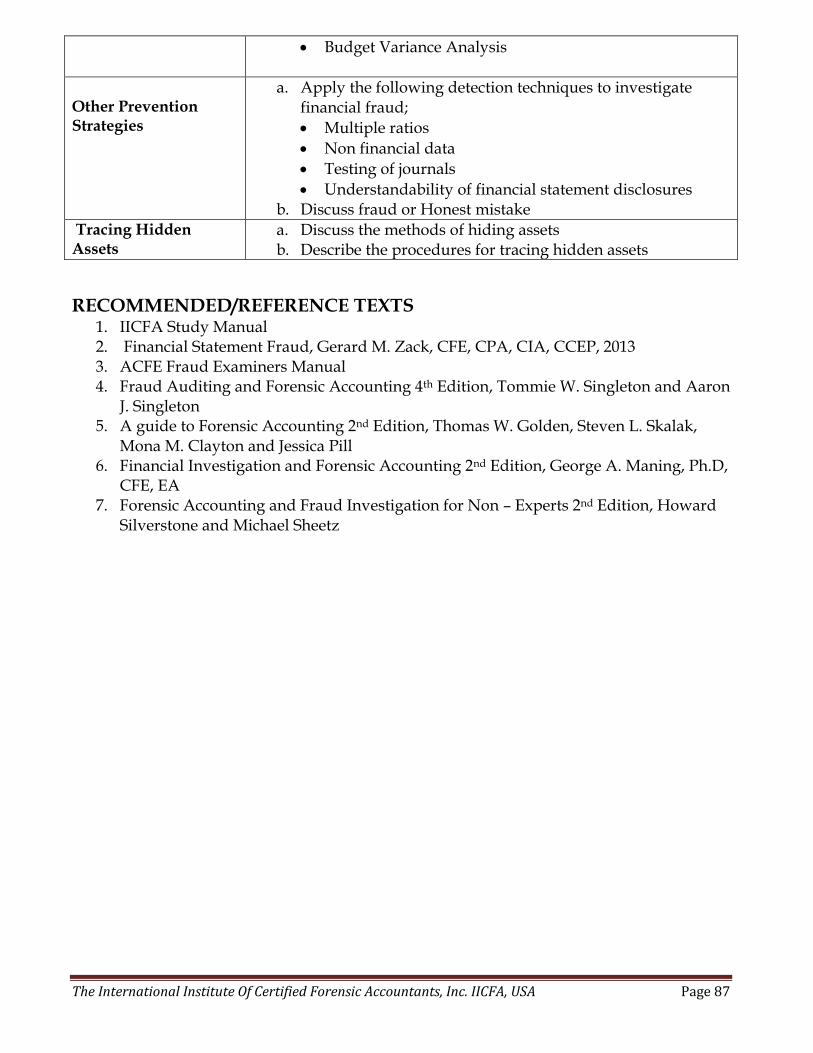

4.1 Advanced Forensic Accounting .................................................................................................................... 84

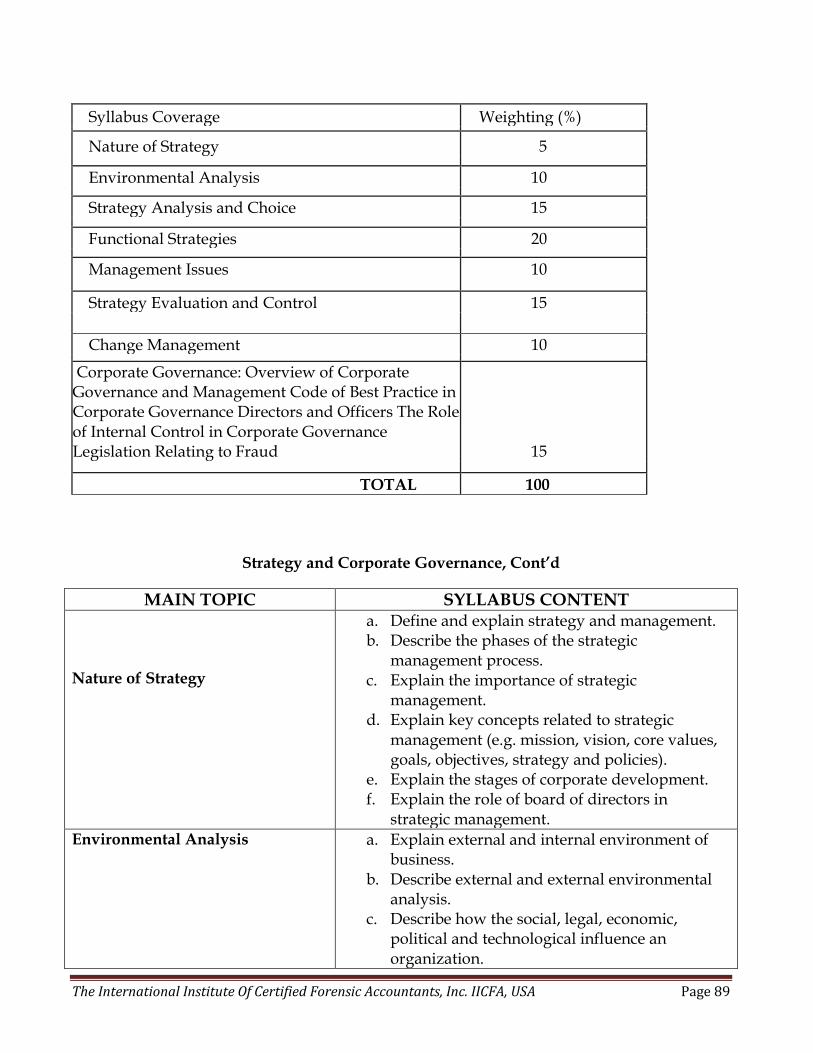

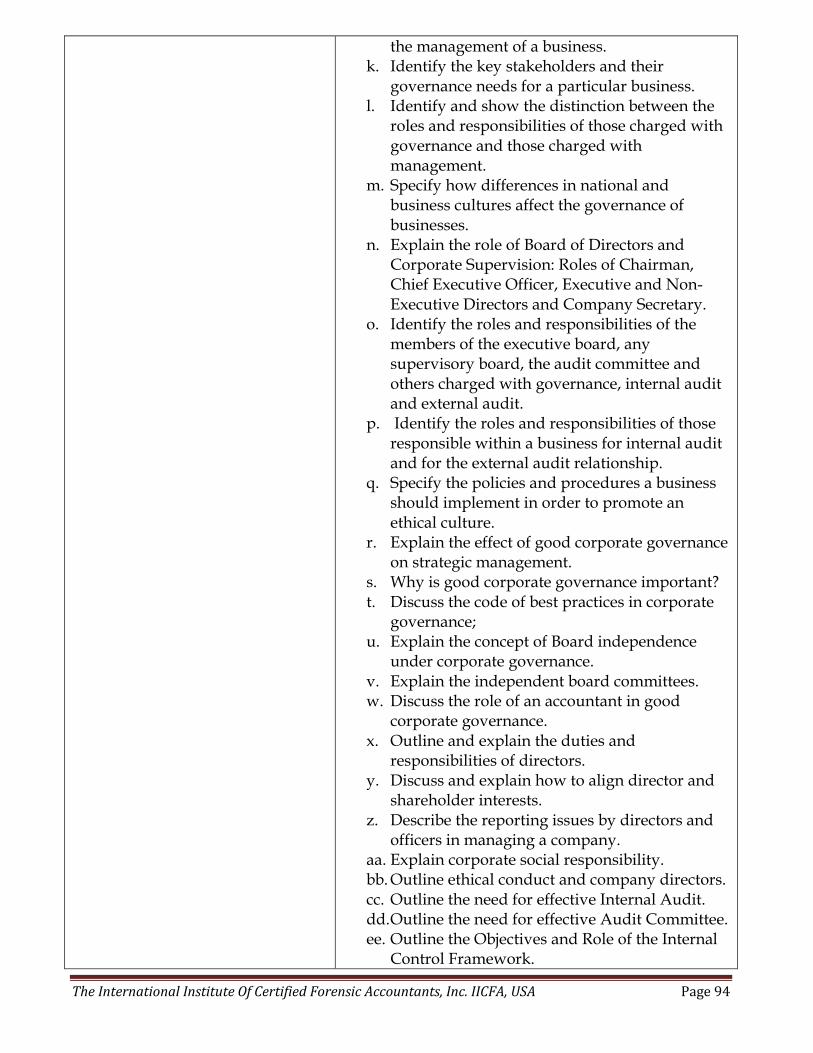

4.2 Strategy and Corporate Governance............................................................................................................. 88

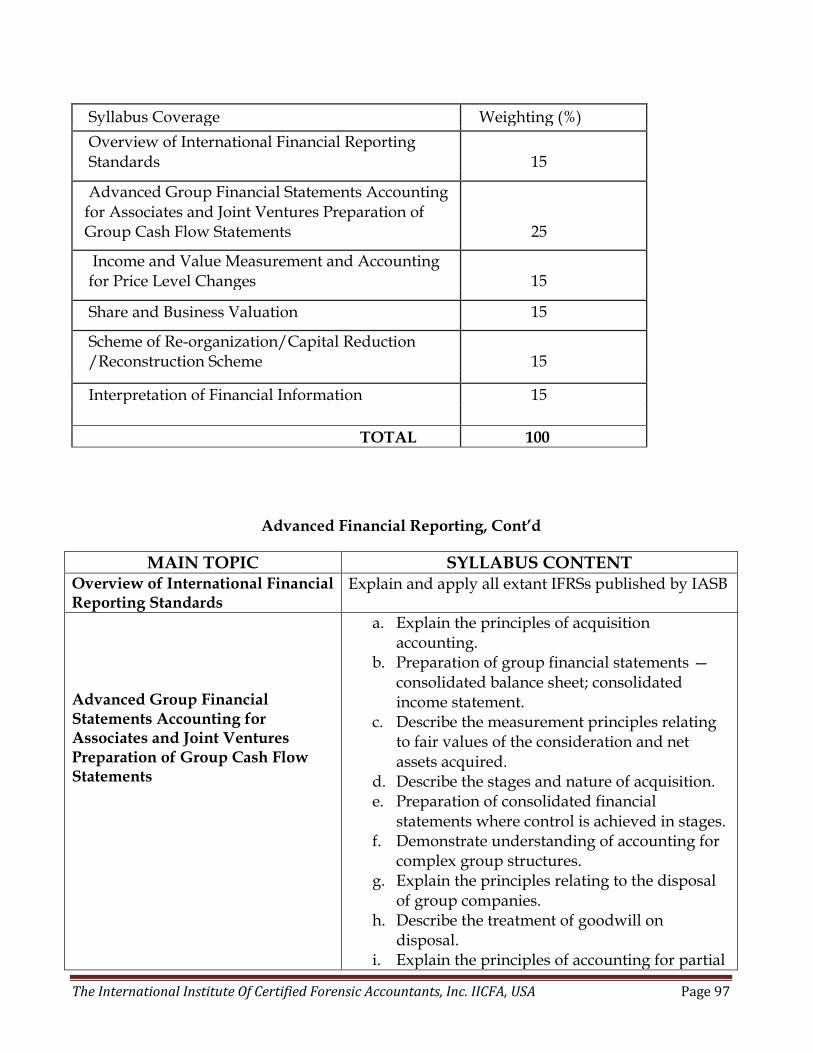

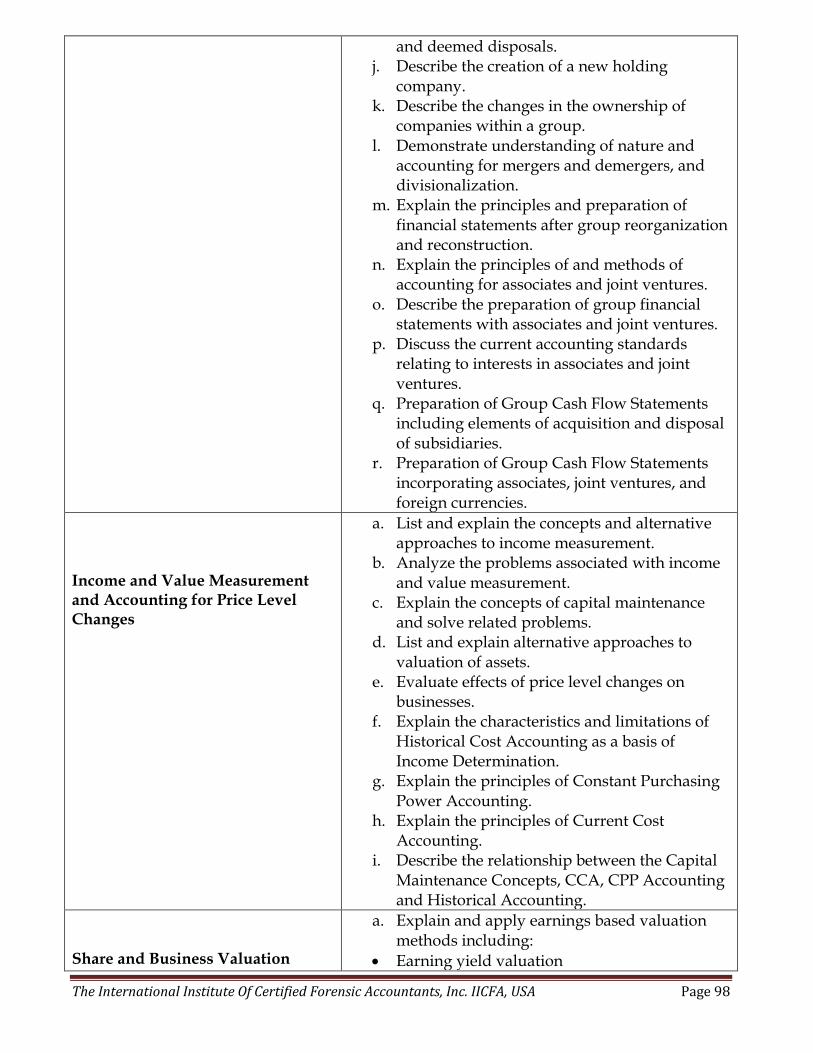

4.3 Advanced Financial Reporting ...................................................................................................................... 96

4.4 Assurance and Professional Practice .......................................................................................................... 101

4.5 Compliance, Ethics and Public Governance .............................................................................................. 110

Entry Requirement .............................................................................................................................................. 114

Exemption Policy ................................................................................................................................................. 114

Capstone Path to CCFA Certification ............................................................................................................... 114

CCFA Exams Period ............................................................................................................................................ 115

Alliances ................................................................................................................................................................ 115

The Chartered Doctorate (Ch.D,) ...................................................................................................................... 115

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 3

Introduction

The International Institute of Certified Forensic Accountants, Inc. IICFA - USA formerly

(Association of Chartered Certified Forensic Accountants, ACCFA) is an international

organization for Forensic Accounting Professionals globally. The IICFA is incorporated in

the USA under the State laws of Delaware.

The IICFA awards the CCFA and the CGFA Credentials to only individuals who have

passed the rigorous qualifying examinations held by the Institute.

The Chartered Certified Forensic Accountant, CCFA is the Flagship Credential of the IICFA

and the Certified General Forensic Accountant, CGFA is designed for Forensic Accounting

Generals. The IICFA credentials are the global standard for Forensic Accounting Education,

Certification and Accreditation globally.

IICFA is also a pioneer member of the International Federation of Forensic Accountants and

Auditors, IFFAA

Mission

IICFA’s mission is to promote Forensic Accounting Education, Certification and Training

Globally.

Vision

The vision of IICFA, USA is to be a reference point in forensic accounting certification

globally.

Objectives;

To enhance the quality of the principles and practice of the Forensic Accounting

Profession Globally.

To undertake research and education to promote the advancement of knowledge of

the theory and practice of Forensic Accounting

To hold and administer professional examinations and award certificates, diplomas

and prizes.

To collaborate with other professional bodies and educational institutions with a view

to promoting the principles and practice of the quality of Forensic Accounting

nationally and internationally.

To maintain a high standard of professionalism, probity and credibility among

members of the Institute

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 4

Board of Governors, BoG

The IICFA, USA is governed by the Board of Governors, BoG which takes strategic decision

towards the future growth of the Institute. The Board of Governors, BoG consists of the

President, the Chairman, and the Vice Chairman respectively and is assisted by the Board of

Regents, BoR and the Global Council of Regional Directors, GCRD.

Board of Regents, BoR

The Board of Regents comprises experts and experienced Chartered Certified Forensic

Accountants, CCFA’s who provides expert advise on various topical forensic accounting

issues and mentor newly qualified CCFA’s. The Regents are appointed by members of the

Institute every two years.

Leadership

The leadership of the IICFA, USA is made up of various committees steering the affairs of

the Institute. Every committee member must be a CCFA in good standing. The following are

the committees;

Global Council of Regional Directors, GCRD

The Global Council of Regional Directors has the responsibility to oversee the overall

governance and professional development of IICFA, USA Regional Directors and their

corresponding chapters. It is the mission of this council to implement strategic planning as it

relates to the guidance, governance, and enrichment of IICFA, USA and its chapters in

support of the organization’s strategic goals.

Education and Research Committee, ECR

The responsibilities of the Education and Research Committee, ERC are to undertake

research and education to promote the advancement of knowledge of the theory and practice

of the Forensic Accounting through publications, training, exams and collaboration with

other professional bodies and academic institutions.

Ethics and Professional Standards Committee, EPSC

The responsibilities of the Ethics and Professional Standards Committee, EPSC are to ensure

the maintenance and enforcement of the code of conducts, ethics and professional standards

of the Institute and also to ensure complaints and disciplinary actions are resolved among

members.

Finance Committee, FC

The Finance Committee is responsible for reviewing and providing guidance for the

organization's financial matters. Specifically, the committee assures internal controls,

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 5

independent audit, and financial analysis for the organization. The Finance Committee is

responsible for oversight of external communications related to IICFA, USA’s finances,

requiring prior approval from IICFA, USA’s Board of Governors.

Membership

FCCFA – The FCCFA means Fellow of Chartered Certified Forensic Accountant awarded to

only those CCFA’s who have contributed extraordinarily towards the progress and growth

of the Institute. CCFA’s with 5 years progressive post qualification experience can apply for

fellowship status. The FCCFA is the highest level of membership in the Institute.

CCFA – The CCFA’s are those members who have written and passed the qualifying exams

of the Institute

Students Membership – Students Membership is open to all students studying the CCFA

exams.

Corporate Membership – These are Practicing Chartered Certified Forensic Accounting

Firms and other Corporate/Academic Institutions that support the objectives of the Institute.

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 6

Features of the Professional Examination Scheme

The Professional Examination Scheme of the Institute comprises the following and is subject

to review from time to time in order to meet the rapid changes in both theory and practice in

the global Forensic Accounting Fraternity.

Four (4) Level, five (5) papers each of 20 papers in total

Clearly defined and obtainable learning outcome from each part. This will enable

partly qualified candidates to be placed in industry and on other programs

respectively.

A more intellectual, easy to fit and implement, graduate conversion and exemption

scheme to enable higher grade candidate entrants thus, degree and diploma holders to

gain sufficient Forensic Accounting competence and double up their eventual

professional Forensic Accounting Qualification.

All Students have ten (10) years from the date of registration within which to

complete all the examination of the Institute of Chartered Certified Forensic

Accountant. After the ten (10) years period any students who has not completed the

examinations of the Institute will not be eligible to take further examinations of the

Institute.

More emphasis on Business strategy, reporting, analysis, investigation and

communication thereby making candidates to appreciate the overall realities of the

business environment making the strategic decision makers and to use advisory skills

more effectively.

Increased emphasis on business forensic investigation advisory skills at the final

level 4.

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 7

Objectives and Expected Performance Outcome of Each Level

Each of the Four (4) levels of the examination scheme has a wide objective and expected

performance outcome as indicated below. Within each subject at any level, the syllabus

coverage as well as the detailed, but specific objectives and learning outcome stated. The

broad objective and the learning outcomes of the Four (4) levels are as follows;

LEVEL 1

Five (5) foundation papers

Provision of basic principles and knowledge required to understand forensic

accounting, fraud Examination and the business environment.

LEVEL 2

Five (5) technical core papers

Test of technical competence and expertise required of global forensic accountant

Acquisition of background knowledge and skills necessary for effective performance

at middle management level.

LEVEL 3

Five (5) core papers

Emphasis on business cases, strategy and advisory skills

LEVEL 4

Five (5) core papers

Emphasis on business cases, strategy and advisory skills

Results and Interpretation

The pass mark is 50%. The results will be published as ‘Pass’ or ‘Fail’. A candidate who fails

a paper has the option to rewrite that paper in subsequent examination until his/her

candidature expires

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 8

The Chartered Certified Forensic Accountant, CCFA

The Chartered Certified Forensic Accountant, CCFA credential is the global standard in

forensic accounting certification awarded by the INTERNATIONAL INSTITUTE OF

CERTIFIED FORENSIC ACCOUNTANTS, IICFA, USA. To be awarded with the CCFA

designation one must pass all four (4) levels of the CCFA qualifying exams and obtain two

years post qualification or professional experience with a reputable forensic accounting firm.

All qualified students must undergo a three day practical forensic accounting workshop

before graduation and admission into membership. The CCFA is the global certification for

truly qualified forensic accountants. The CCFA seeks to add value to the clients or employers

who engages the services of CCFA’s. CCFA’s are saving government and corporations

millions of dollars every day through the dint of the CCFA’s skills and competence. CCFA’s

does this through transparency and integrity.

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 9

PROFESSIONAL LEVEL 1

1.1 Principles of Forensic Accounting

1. OBJECTIVES AND LEARNING OUTCOME

At the end of the course candidates should be able to;

Define and explain basic Forensic Accounting Concepts

Understand the fundamental principles and objectives of Forensic Accounting

Examine a fact related to economic damages, business valuation or other

investigations

Understand the basic concept of red flags, such as accounting anomalous, analytical

anomalous and behavioral patterns among others.

Explain the essential skills set required for the Forensic Accounting profession

Outline the Major component of Assets Misappropriation Schemes

Define skimming and describe the most common skimming schemes

Identify major users of forensic accounting information and their specific needs

Define Fraudulent Disbursement and explain its major component

Explain the Methods of Making Illegal Payments in Corruption Schemes

Explain Payroll Schemes, Lapping, Bid – Rigging, Cheque Tampering and Corruption

Identify the education and qualification forensic accountants must possess in order for

them to be admitted as expert witnesses in any court of competent jurisdiction.

Explain the Recommendations made by the Treadway Commission to curb

Fraudulent Financial Reporting

Examine the responsibilities of signing officers under the Sarbanes-Oxley Act

2. EXAMINATION STRUCTURE

The examination will be a three-hour paper of seven (7) questions. Candidates will be required to answer any five (5) questions. 3. SYLLABUS WEIGHTING GRID

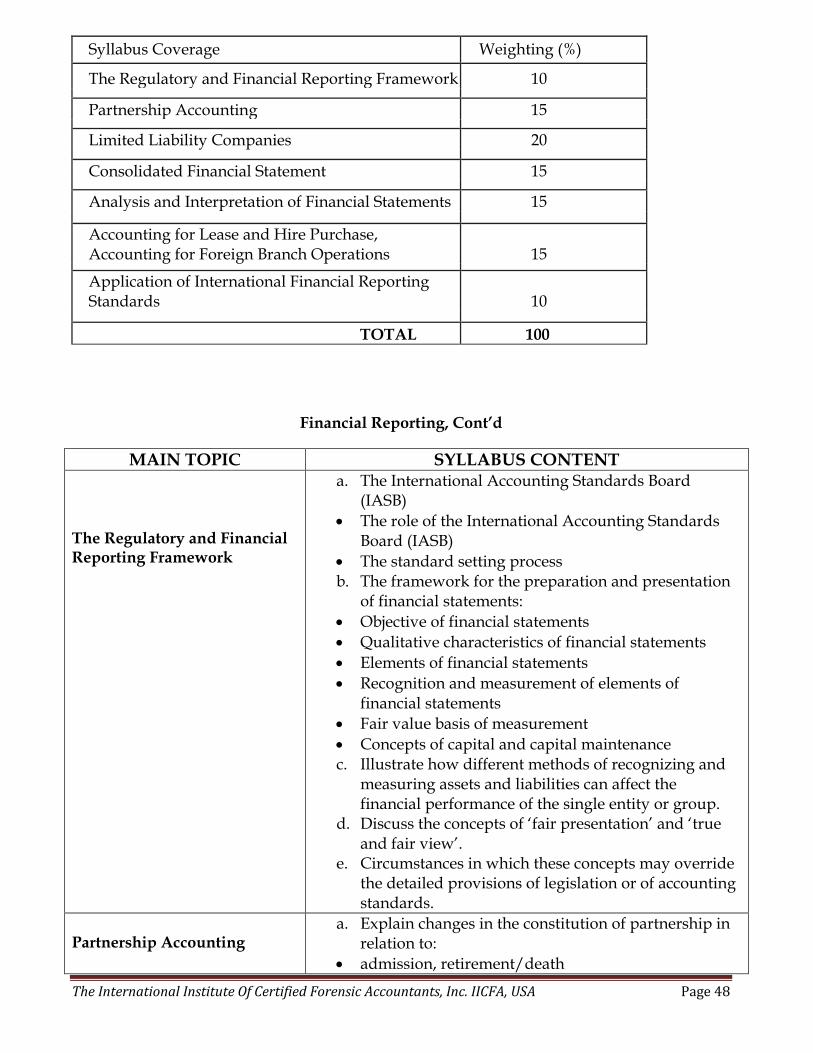

This grid shows the relative weightings of topics within this subject and should guide the relative study time spent on each. The marks available in the assessment will equate to the weightings below. However, there might be slight variations in some instances as they serve as a guide only.

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 10

SYLLABUS COVERAGE WEIGHTING %

Overview of Forensic Accounting 20

Accounting Information System and Fraud Schemes 20

The Legal Role and Qualification of Forensic Accountants 20

Gathering, Obtaining and Evaluating non – financial Evidence in Forensic Accounting 20

Auditors’ and Management Responsibilities 20

TOTAL 100

Principles of Forensic Accounting, Cont’d

MAIN TOPIC SYLLABUS CONTENT

Overview of Forensic Accounting

a. Define Forensic Accounting and Explain how the forensic accounting profession came into being

b. Narrate the history of the Fraud and the Anti-fraud Profession

c. Differentiate between the following;

Fraud Auditing and Forensic Accounting

Financial Auditors, Forensic Accountants and Fraud Auditors

Corporate Fraud and Occupational Fraud

Economic Extortion and Conflict of interest d. State and Explain the principles of fraud Audit e. Describe the skills set, knowledge and abilities required of

Forensic Accountants f. Identify the Similarities between Financial Auditors,

Forensic Accountants and Fraud Auditors g. Identify the types of organizations that will require the

services of Forensic Accountants h. State and Explain the essential skills set required for the

Forensic Accounting profession i. Define the following categories of external fraud;

Securities Fraud

Insurance Fraud

Credit Card and Cheque Fraud

Tax Fraud

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 11

Consumer Fraud and

Money Laundering

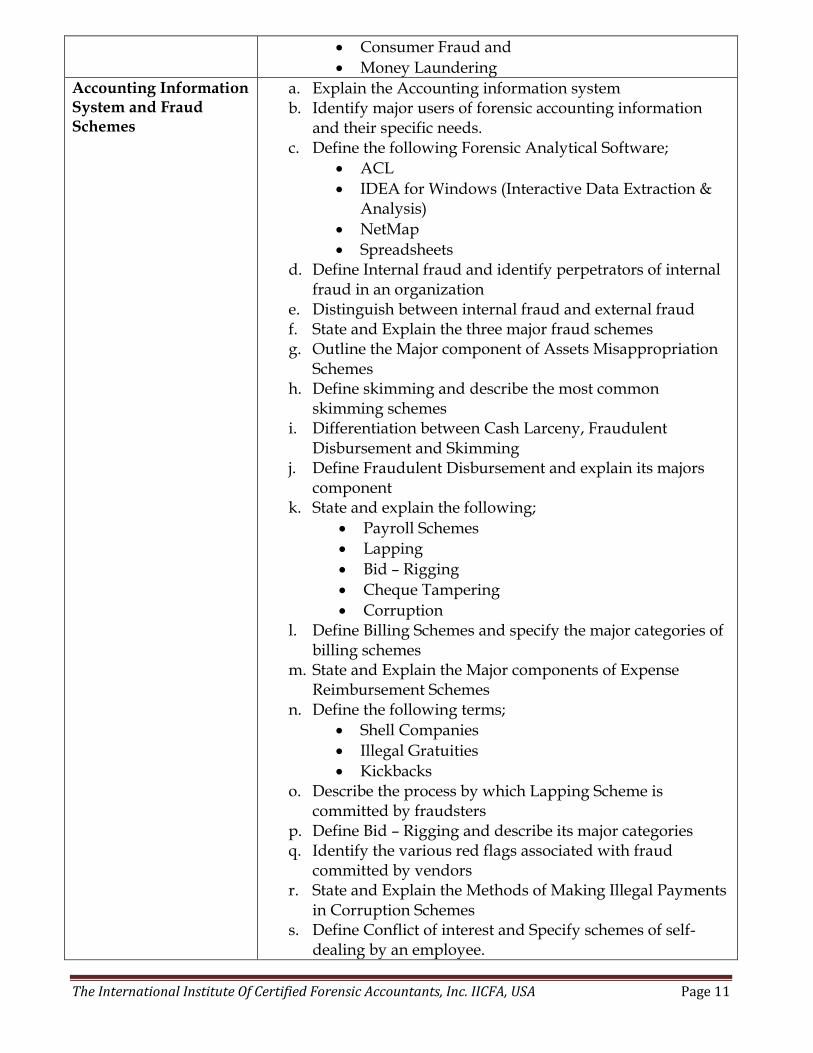

Accounting Information System and Fraud Schemes

a. Explain the Accounting information system b. Identify major users of forensic accounting information

and their specific needs. c. Define the following Forensic Analytical Software;

ACL

IDEA for Windows (Interactive Data Extraction & Analysis)

NetMap

Spreadsheets d. Define Internal fraud and identify perpetrators of internal

fraud in an organization e. Distinguish between internal fraud and external fraud f. State and Explain the three major fraud schemes g. Outline the Major component of Assets Misappropriation

Schemes h. Define skimming and describe the most common

skimming schemes i. Differentiation between Cash Larceny, Fraudulent

Disbursement and Skimming j. Define Fraudulent Disbursement and explain its majors

component k. State and explain the following;

Payroll Schemes

Lapping

Bid – Rigging

Cheque Tampering

Corruption l. Define Billing Schemes and specify the major categories of

billing schemes m. State and Explain the Major components of Expense

Reimbursement Schemes n. Define the following terms;

Shell Companies

Illegal Gratuities

Kickbacks o. Describe the process by which Lapping Scheme is

committed by fraudsters p. Define Bid – Rigging and describe its major categories q. Identify the various red flags associated with fraud

committed by vendors r. State and Explain the Methods of Making Illegal Payments

in Corruption Schemes s. Define Conflict of interest and Specify schemes of self-

dealing by an employee.

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 12

t. Explain Fixed Assets Schemes and describe how an organization suffers from such a scheme.

u. Identify major red flags associated with assets misappropriation

The Legal Role and Qualification of Forensic Accountants

a. State Explain the role that Forensic Accountants play in the legal system

b. Identify the education and qualification forensic accountants must possess in order for them to be admitted as expert witnesses in any court of competent jurisdiction.

Gathering, Obtaining, and Evaluating Non-Financial Evidence

a. Define evidence and identify the basic forms of evidence b. Evaluate Burden of Proof in civil litigation and criminal

litigation c. Differentiate between circumstantial evidence and direct

evidence d. State and Explain the factors of relevant evidence e. Discuss the Exclusionary Rule to evidence f. Explain the following;

Authentication

Chain of Custody

Digital Evidence

Hearsay

Impeachment g. Distinguish between Hearsay and Impeachment h. Describe Attorney – Client Privilege i. Explain the following attorney-client privilege protection;

Confidentiality

Professional Service

Integrity

Conflict of Interest

Due diligence

Auditors’ and Management Responsibilities

a. State and Explain management responsibilities for the quality, integrity, reliability and internal control of the financial reporting process and in accordance with GAAP and IFRS

b. Define organizational ethics c. Examine the responsibilities of signing officers under the

Sarbanes-Oxley Act d. Discuss the independent of an Audit Committee e. Identify the main responsibilities of External Auditors f. State and explain the roles internal auditors play in

preventing internal fraud. g. State and the major institutions that formed the Treadway

Commission h. Explain the following Recommendations made by the

Treadway Commission to curb Fraudulent Financial

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 13

Reporting;

Mandatory Independent Audit Committee

Written Charter

Resources and Authority

Informed, Vigilant and Effective Audit Committee

RECOMMENDED/REFERENCE TEXTS

1. IICFA Study Manual 2. Fraud Auditing and Forensic Accounting 4th Edition, Tommie W. Singleton and Aaron

J. Singleton 3. A guide to Forensic Accounting 2nd Edition, Thomas W. Golden, Steven L. Skalak,

Mona M. Clayton and Jessica Pill 4. Financial Investigation and Forensic Accounting 2nd Edition, George A. Maning, Ph.D,

CFE, EA 5. Forensic Accounting and Fraud Investigation for Non – Experts 2nd Edition, Howard

Silverstone and Michael Sheetz.

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 14

1.2 Principles of Fraud Examination

1. OBJECTIVES AND LEARNING OUTCOME

At the end of the course candidates should be able to;

Understand basic fraud examination concepts

Understand the various causes of fraud red flags

Perform Fraud Risk Assessment

Profile a fraudster and demonstrate sound knowledge in fraud examination

Understand the Fraud Tree

Apply knowledge of the Fraud Trial Angle to profile fraudsters

Understand the qualified skills and competences of Fraud Examiners

Appreciate the qualities of a Fraud Examiner

Understand the most common types of fraud businesses face in the current

environment and the prevention and detection methods

Explain effective anti-fraud detection control mechanisms

Explain fraud prevention strategies in an organization

Explain the Benefits of Fraud Risk Assessment to an Organization

Design a sample fraud risk assessment framework

Explain the classical approaches to fraud prevention control program

Describe the steps in developing a Fraud Risk Management Program

Describe the Fraud Theory Approach to Fraud Examination

Discuss the Fraud Examination Methodology

Explain the Steps in a Fraud Examination

Write a Sample Fraud Examination Report

2. EXAMINATION STRUCTURE

The examination will be a three-hour paper of seven (7) questions. Candidates will be required to answer any five (5) questions.

3. SYLLABUS WEIGHTING GRID

This grid shows the relative weightings of topics within this subject and should guide the relative study time spent on each. The marks available in the assessment will equate to the weightings below. However, there might be slight variations in some instances as they serve as a guide only.

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 15

SYLLABUS COVERAGE WEIGHTING %

Introduction 10

Fraud Schemes 10

Fraud Detection 20

Fraud Prevention 20

Fraud Risk Assessment 20

Fraud Risk Management 10

Fraud Examination 10

TOTAL 100

Principles of Fraud Examination, Cont’d

MAIN TOPIC SYLLABUS CONTENT Introduction a. Define Fraud and distinguish between Corporate Fraud

and Management Fraud b. State and explain the similarities between the following;

Fraud

Theft

Embezzlement c. Define the Fraud Triangle and Identify its major

components d. State and explain the major reasons why people commit

fraud e. Examine the profile of a fraudster and identify who is

likely to commit fraud in an economy f. State and Explain the reasons why employees commit

fraud g. Define Fraud Taxonomy h. State and Explain the following Fraud Taxonomies

Consumer and Investor Frauds

Criminal and Civil Fraud

Fraud for and Against the Organization

Internal and External Fraud

Management and Non-Management Fraud i. Identify the types of frauds committed by the following;

Creditors

Customers

Stakeholders

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 16

Competitors

Company/Employers

Bankers

Insurance Carriers

Government Agencies j. Define Fraud tree and identify its major components

Fraud Schemes a. Define Fraud Schemes b. State and Explain the Various Red flags associated with

the following fraud schemes;

Fraudulent Financial Statement

Assets Misappropriation

Bribery and Corruption c. Explain the Characteristics of the following Fraud

Schemes;

Assets Misappropriation – Cash Receipts

Assets Misappropriation – Fraudulent Disbursement

Assets Misappropriation – Inventory and Other Assets

Financial Statement Fraud

Financial Institution Fraud

Bribery and Corruption

Consumer Fraud

Cheque and Credit Card Fraud

Health Care Fraud

Insurance Fraud

Public Sector Fraud

Internet/Computer Fraud

Securities Fraud, etc

Fraud Detection a. Define Fraud Detection b. State and explain effective anti-fraud detection control

mechanisms c. State and Explain how the following fraud schemes can

be detected;

Financial Statement Fraud Schemes

Assets Misappropriation Schemes

Corruption Schemes d. Describe how the following can be used to detect

fraudulent activities in an organization;

Horizontal and Vertical Analysis of financial reports

Ratio Analysis

Surprise Audits

Data Mining

Fraud Prevention a. Define Fraud Prevention b. State and explain fraud prevention strategies in an

organization c. Explain the axiom ‘Perception of Detection’

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 17

d. Explain the following methods of increasing perception of detection;

Surveillance

Prosecution

Anonymous tips

Catch me if you can

Enforcement of ethics and fraud policies

Surprise Audits e. Explain the following classical approaches to fraud

prevention control program;

Detective Approach

Preventive Approach

Investigative Approach

Directive Approach

Observation Approach

Insurance Approach f. Explain the Following other approaches to Fraud

Prevention;

Regular Audits

Background checks

Internal Controls

Invigilation

Fraud Risk Assessment a. Define Fraud Risk Assessment b. Distinguish between residual and inherent fraud risk c. Identify the Major Fraud Risk Factors d. State and Explain the Benefits of Fraud Risk Assessment

to an Organization e. State and explain the qualities of a good fraud risk

assessment program. f. State and Explain the Consideration for Developing an

effective Fraud Risk Assessment g. Explain the following objectives for the preparation of

fraud risk assessment;

Assembling the right team to lead and conduct the fraud risk assessment

Determining the best techniques to use in conducting the fraud risk assessment

Obtaining the Sponsor’s agreement on the work to be performed

Educating the organization and openly promote the process

h. Design a sample fraud risk assessment framework i. Discuss the following Approaches to residual fraud risks

response;

Avoid the risk

Transfer the risk

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 18

Mitigate the Risk

Assume the Risk j. State and Explain the factors to consider when reporting

the assessment results k. State and explain the fraud risk assessment

tools/modules

Fraud Risk Management a. Define Fraud Risk Management b. Describe the Fraud Risk Management Framework c. State and explain the objectives of Fraud Risk

Management Program d. Describe the steps in developing a Fraud Risk

Management Program e. Identify the Major component of a Fraud Risk

Management Program f. Examine the integration of anti-fraud initiatives into risk

management

Fraud Examination a. Define Fraud Examination b. State and Explain the Major distinctions between fraud

examination, forensic accounting and financial statement audit

c. Explain the following axioms of fraud examination;

Fraud Is Hidden

Reverse Proof

Existence of Fraud

Predication d. Describe the Fraud Theory Approach to Fraud

Examination e. Explain the following Fraud Theory Approach

procedures;

Analyzing available data

Creating a Hypothesis

Testing the Hypothesis

Refining and amending the Hypothesis f. Discuss the Fraud Examination Methodology g. State and Explain the Steps in a Fraud Examination h. Write a sample Fraud Examination Report

RECOMMENDED/REFERENCE TEXTS 1. ACCFA Study Manual 2. Principles of Fraud Examination, Dr. Joseph T. Wells 3. Corporate Fraud Handbook, Prevention and Detection, Dr. Joseph T. Wells 4. Introduction to Fraud Examination, ACFE 5. Fraud Auditing and Forensic Accounting 4th Edition, Tommie W. Singleton and Aaron

J. Singleton 6. ACFE Fraud Examiners Manual

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 19

1.3 Principles of Taxation

4. OBJECTIVES AND LEARNING OUTCOME

At the end of the course candidate should be able to;

Understand tax administration in respect of Internal Revenue Service (IRS), Value Added Tax Service (VATS) and Customs, Excise & Preventive Service (CEPS), Revenue Agencies Governing Board (RAGB).

Understand the general objectives of tax and to calculate personal income tax, capital gains tax, gift tax corporation tax and VAT in straightforward scenarios.

Understand the fundamental concepts and principles of the tax system and the relevance of taxation to personal and business activities.

Explain the general objectives of tax, the influences upon the tax system and the different types of tax.

Explain the issues arising in the course of performing tax work and identify the obligations of imposing taxes on the taxpayer and the implications for taxpayers of non-compliance.

Calculate the amounts of income tax owed by or owed to individuals.

Calculate the capital gains tax payable by individuals and the chargeable gains subject to corporation tax.

Calculate the corporation tax liabilities of companies.

Calculate the amount of VAT owed by or owed to businesses.

Explain the various taxes collected by CEPS, e.g. Import duties, Import VAT and NHIL.

Apply the tax principles and laws in the work environment.

Determine tax liabilities of taxpayers in the various tax systems.

5. EXAMINATION STRUCTURE The examination will be a three-hour paper of five compulsory questions.

6. SYLLABUS WEIGHTING GRID This grid shows the relative weightings of topics within this subject and should guide the relative study time spent on each. The marks available in the assessment will equate to the weightings below. However, there might be slight variations in some instances as they serve as a guide only.

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 20

SYLLABUS COVERAGE WEIGHTING %

Tax Administration 20

Indirect Taxes 20

Direct Taxes 40

Double Taxation 5

Capital Gains Tax 10

Gift Tax 5

TOTAL 100

Principles of Taxation (Cont’d)

MAIN TOPIC SYLLABUS CONTENT

Tax Administration

a. Narrate how and when taxation was introduced. b. Differentiate between direct and indirect taxes. c. Examine the advantages and disadvantages of each system. d. Explain the role of taxation in the national economy. e. Describe the attributes of a good tax system. f. Explain the statutory powers and functions of the Commissioners of IRS, CEPS and VAT Service to ensure compliance with tax rules. g. Assess whether the powers of the Commissioners are adequate to enable them perform efficiently and effectively. h. Explain the rights and obligations of the tax payer. i. State the dates for filing of returns by the various categories of taxpayers and penalties for noncompliance. j. State and explain the various forms used by different taxpayers for filing returns. k. State the penalties imposed by the Commissioners and the courts. l. Explain the difference between tax avoidance and tax evasion. m. Define pecuniary penalties. n. State the penalties imposed under the various tax laws.

a. Differentiate between Customs and Excise duties b. State and explain the different taxes collected by Customs, Excise and Preventive Service (CEPS).

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 21

Indirect Taxes

c. Explain the concept of Value Added Tax. d. Identify when a business could or should register for VAT and state the time limits. e. Determine the tax point for a supply of goods or services. f. Differentiate between taxable supply (standard rated), exempt supply, relief supply and zero-rated supply.

Direct Taxes

a. Define the concepts of income and income tax. b. Enumerate and explain the various sources of income. c. Explain the concept of employment and examine the assessment of employment income. d. Examine the advantages and disadvantages of PAYE system. e. Define basic salary. f. State and explain other benefits in cash and kind associated with employment. g. Describe the determination of benefits in kind. h. Explain the meaning of tax relief and examine the various types of tax relief. i. Explain the types of income that are exempt from tax in the hands of the employee and state the rationale behind such exemptions. j. Distinguish between trade, business, profession and vocation. k. State the deductions that are allowed in determining income assessable to tax. l. State and explain deductions that are not allowed in determining assessable income. m. Explain the conditions and rationale for granting capital allowance. n. Define qualifying expenditure and explain the types of qualifying expenditure. o. Explain the methods for calculating capital allowance. p. Define unearned income, give some relevant examples and explain the mode of assessment of an unearned income. q. Differentiate between tax holidays and tax exemptions. r. Explain the rationale for granting tax holidays and tax exemptions. s. Identify the types of businesses that enjoy tax holidays and tax exemptions. t. Explain the procedures for determining assessable income, chargeable income and tax liabilities and compute actual tax liabilities. u. Explain the mode of assessment of individuals, partnerships and companies. v. Explain withholding tax, state the various types of withholding tax and examine the necessity for having withholding taxes. w. Examine the effectiveness of withholding taxes administration.

Double Taxation

a. Explain double taxation and state the need for having double taxation avoidance agreements. b. Identify the countries that have double taxation agreements with your country and explain the nature of the arrangement.

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 22

c. Define and calculate tax credit relief.

Capital Gains Tax

a. Identify chargeable assets under the capital gains tax. b. Define and explain realization. c. Define consideration received and cost base. d. Explain transactions which are exempt from capital gains tax. e. Compute capital gains. f. Explain the procedures for filing of returns and payment of capital gains and sanctions.

Gift Tax

a. Define taxable gifts. b. Determination of the value of a gift. c. State the transactions that are exempt under the Gift Tax and explain the rationale for granting the exemptions. d. Compute gift tax. e. Describe the procedure for filing and payment of gift tax and state the sanctions.

RECOMMENDED/REFERENCE TEXTS 1. IICFA Study Manual 2. Taxation for Business Decision Makers, Shirley Dennis-Escoffier and Karin Fortin, Wiley 3. Akakpo, V.K.A. Principles, Concepts and Practice of Taxation. 4. Dua Agyeman, E. Income Tax, Gift Tax and Capital Gains Tax, EDA Publications.

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 23

1.4 Financial Accounting Foundation

1. OBJECTIVES AND LEARNING OUTCOME

This paper is designed to enable candidates acquire and appreciate fundamental accounting

knowledge in businesses. At the end of the course, candidates should be able to;

Demonstrate sound knowledge and understanding of accounting principles, concepts

and their application in the preparation of financial statements

To ensure that students have a sound understanding of the techniques of double entry

accounting and can apply its principles in recording transactions, adjusting financial

records and preparing non-complex financial statements.

Able to identify and correct omissions and errors in accounting records and financial

statements.

Able to specify the components of financial statements and prepare and present non-

complex accounts for sole traders, partnerships and limited companies.

Specify why an entity maintains financial records and prepares financial statements.

Identify the sources of information for the preparation of accounting records and

financial statements.

Record and account for transactions and events resulting in income, expenses, assets,

liabilities and equity in accordance with the appropriate basis of accounting and the

laws, regulations and accounting standards applicable to the financial statements.

Prepare a trial balance from accounting records and identify the uses of the trial

balance.

Prepare accounts and financial statements from incomplete records.

Understand the different bases of preparing financial statements.

Apply some international financial reporting standards.

Define the qualitative characteristics of financial information and the fundamental

bases of accounting

2. FORM OF EXAMINATION

The examination will be a three-hour paper consisting of five compulsory questions. (All the

five questions must be answered.)

3. SYLLABUS WEIGHTING GRID

This grid shows the relative weightings of topics within this subject and should guide the

relative study time spent on each. The marks available in the assessment will equate to the

weightings below.

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 24

However, there might be slight variations in some instances as they serve as a guide only.

SYLLABUS COVERAGE WEIGHTING (%)

Conceptual Framework of Accounting, Maintaining

Financial Records Principles of Double Entry &

Books of Prime Entry 20

Adjustments to Accounting Records and Financial

Statements Accounting for non-current

Assets (tangibles and intangibles) 15

Preparation of Financial Statements including

Cash Flow 20

Preparation of Financial Statements for

Non-profit Making Organizations, Preparation of

Financial Statements from Incomplete Records 20

Accounting for specialized transactions 15

Introduction to financial statements analysis 10

TOTAL 100

Financial Accounting Foundation (Cont’d)

MAIN TOPIC SYLLABUS CONTENT

1.1 Conceptual Framework of Accounting

a. Define and explain the scope of accounting, financial accounting, book-keeping, cost and management accounting, and their similarities and differences. b. Explain the needs of external and internal users of accounting information. c. Describe forms of Business Entity: and explain the meaning of ‘entity.’ d. Explain the categories of business organizations. (i) Sole Proprietorships: Their characteristics, benefits and limitations. (ii) Partnerships: Their characteristics, benefits and limitations. (iii) Limited Liability Companies: Their characteristics,

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 25

benefits and limitations e. Explain the differences between Partnerships and limited liability companies. f. Explain the purpose of financial statements by 1AS 1. g. Explain the accounting assumptions and concepts. h. Outline the components of financial statements. i. Identify the main users of financial information and their information needs. j. Identify and explain accounting concepts and conventions. k. Outline the qualitative characteristics of financial statements. l. Outline the elements of financial statements and the basis of their recognition and their measurements. m. Explain Accounting Standards: their purpose, standards setting process, IASB membership.

1.2 Maintaining Financial Records

a. Specify why an entity maintains financial records and prepares financial statements. b. Identify the sources of information for the preparation of accounting records and financial statements. c. Record and account for transactions and events resulting in income, expenses, assets, liabilities and equity in accordance with the appropriate basis of accounting and the laws, regulations and accounting standards applicable to the financial statements. d. Record and account for changes in the ownership structure and ownership interests in an entity.

1.3 Principles of Double Entry and Books of Prime Entry 1.3 Principles of Double Entry and Books of Prime Entry. Cont’d

a. Understand and apply the accounting equation. b. Identify the elements of financial statements:

Types, definitions, relationships and distinctions.

The nature of transactions. c. Outline the contents and purpose of different types of business documentation, including: quotation, sales order, purchase order, goods received note; goods dispatched note, invoice, statement, credit note, debit note, remittance advice, receipt. d. Identify the main types of ledger accounts and books of prime entry (cash books, the sales day book and the sales ledger, the purchases day book and the purchases ledger) and understand their nature and function. e. Understand and illustrate the uses of journals and the posting of journal entries into ledger accounts. f. Identify the main types of business transactions e.g. sales, purchases, payments, receipts. g. Identify correct journals from given narrative. h. Illustrate how to balance and close a ledger account.

2.1 Adjustment to Accounting Records and Financial Statements

a. Identify and explain the types of errors that can affect trial balance and its effects on financial statements. (i) Explain how these can be corrected. (ii) Explain the purpose of suspense accounts.

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 26

(iii) Explain the uses of journals to correct errors in draft financial statements. b. Explain the accounting for the following in financial statements; (i) Stocks/inventories. (ii) Tangible non-current assets. (iii) Fixed Assets and Depreciation. (iv) Intangible non-current assets and amortization. (v) Accruals and prepayments. (vi) Debtors/receivables and trade creditors/payables. (vii) Provisions and contingencies. (viii) Returns inwards and outwards. (ix) Discount received and discount allowed. (x) Capital and revenue expenditures. xii. Bad debts, provisions for doubtful debts, provisions for discounts on debtors. c. Prepare Bank Reconciliation Statement.

2.2 Accounting for Non-Current Assets

a. Describe the accounting treatment for property, plant and equipment in accordance with IAS 16. b. Explain the methods and policies of depreciation (limited to straight line, reducing balance and revaluation methods). c. Explain the reasons for depreciation and accounting for provision for depreciation. d. Account for disposal of property, plant and equipment using ledger accounts. e. Account for recognition of Intangible assets in accordance with IAS 38. f. Explain the differences between depreciation and amortization.

2.3 Preparation of Financial Statement of a Partnership Firm

a. Prepare and present income statement and balance sheet of a sole trader: i Manufacturing Account ii Trading Account iii Profit and Loss Account iv Balance Sheet

3.1 Preparation of Financial Statement of a Sole Trader

a. Describe the procedure for forming a partnership. b. Prepare final accounts of partnership:

Trading, profit and loss account

Profit and loss appropriation account

Partners’ capital and current accounts

Balance sheet c. Explain the procedure for admission of a partner. d. Explain the methods of valuing goodwill. e. Explain revaluation in relation to an admission of a new partner, change in the profit sharing ratio, or a retirement/death.

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 27

f. Prepare partnership accounts for an admission, change in the profit sharing ratio, or a retirement. g. Prepare accounts for simple dissolution (excluding piecemeal realization).

3.2 Preparation of Financial Statements of a Company

a. Distinguish between. - Ordinary Share and Preference Share. - Authorized Capital and Stated Capital. - Income Surplus and Capital Surplus. b. Describe the nature and types of debentures. c. Explain the nature and purpose of final accounts of a limited liability company. d. Draft company final accounts for internal use. e. Define cash flow and explain cash flow statement. f. Describe the usefulness of cash flow statement. g. Prepare a simple cash flow statement in accordance with IAS 7.

4.1 Preparation of Financial Statements for Not-for-Profit Organizations

a. Identify the type of entity that is a non-profit making organization. b. Identify the purpose of such organizations. c. Outline the differences between income statement for non-profit making organization and income statement for a profit making business. d. Prepare receipts and payments account, income statement and a balance sheet for a non-profit making organization.

4.2 Preparation of Financial Statements from Incomplete Records

Prepare Income statement and balance sheet of an entity from incomplete records.

5. Accounting for Specialized Transactions; Joint Venture; Investments; Royalties; Branch

a. Explain joint venture. b. Distinguish between joint venture and partnership. c. Explain how to make entries in the accounts of a joint venture. d. Explain investments accounts, and how they are used. e. Record transactions in investment accounts. f. Explain royalties, minimum rent and short workings. g. Record royalties in the books of the lessee and lessor (including sub-royalties or leases). h. Prepare departmental and branch accounts (excluding foreign branches).

6. Introduction to Financial Statement Analysis

a. Calculate basic financial ratios from given income statement and/or balance sheet: - Profitability Ratios - Liquidity (Short term solvency) Ratios - Gearing/Leverage Ratios - Activity/Efficiency Ratios - Investment Ratios b. Explain the meaning and uses of the above ratios. c. Outline the limitations of financial ratios as tool for performance measurement.

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 28

LIST OF RECOMMENDED TEXT 1. IICFA Study Manual 2. Financial Accounting Fundamental, by ICAG 3. Introduction to Accounting and Finance, 2nd Edition by Geoff Black 4. Wood F. Business Accounting 1: Financial Times. 5. Millichamp, R. A. (1992) Foundation Accounting; DPP.

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 29

1.5 Business Management Studies

1. OBJECTIVES AND LEARNING OUTCOMES

At the end of course candidates should be able to;

Explain the objectives of business and the functions of management;

Explain the major concepts, theories and techniques in the field of general management;

Apply the concepts, theories and techniques in analyzing and providing solutions to business problems;

Describe the various functional areas of an organization and how they relate to one another;

Describe the environment within which businesses operate;

Appraise the impact of economic, social, political, legal, technological and global changes in the environment on management decisions.

2. FORM OF EXAMINATION The examination will be a three-hour paper of seven (7) questions. Candidates will be required to answer any five (5) questions. 3. SYLLABUS WEIGHTING GRID This grid shows the relative weightings of topics within this subject and should guide the relative study time spent on each. The marks available in the assessment will equate to the weightings below. However, there might be slight variations in some instances as they serve as a guide only.

Syllabus Coverage Weighting (%)

Introduction to Management Studies 10

Planning and Decision Making 15

Organizing, Motivation, Leadership, Controlling 30

Communication Groups and Team Work 15

Human Resource Management 10

Marketing Management 10

Operations Management 10

TOTAL 100

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 30

Business Management Studies Cont’d

MAIN TOPIC SYLLABUS CONTENT

Introduction to Management Studies

a. Explain the objectives of business organizations. b. Explain the four (4) functions of management and state the other major elements in the management process. c. Explain the roles of management. d. Explain the types of skills needed by managers. e. Describe how managerial jobs differ according to the levels and areas of responsibility. f. Explain the evolution of management theories. g. Explain how socio-cultural, legal, economic, political and technological and global changes influence businesses. h. Explain the concept of stakeholders and distinguish between primary and secondary stakeholders. i. Explain the nature of the power and interests of stakeholders. j. Explain the social responsibility of businesses.

Planning and Decision Making

a. Define and differentiate between the following key terminologies:

Planning

Forecasting

Objective setting

Policies

Programmes

Schedules

Procedures

Budgeting b. State and describe types of plans. c. Categorize the types of planning at the different levels of management. d. Explain the planning process. e. Explain the steps in the decision making process. f. Appraise alternative solutions and select appropriate solution(s) to organizational problems. g. Evaluate and apply skills necessary for effective decision making as regards the entire spectrum of management and organization.

Organizing

a. Describe the elements that make up organizational structure and its related units. b. Develop organizational charts and explain their importance. c. Describe the main approaches to job design. d. Explain the major methods of vertical co-ordination, including formalization, span of management, centralization vs. decentralization, delegation, line and staff positions. e. Analyze delegation, authority, responsibility and accountability and their impact on motivation and organizational culture. f. Explain, analyze and evaluate the concept of coordination as an integral part of management.

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 31

g. Distinguish between types and conditions for business and organizational integration. h. Identify and state the characteristics and relationships associated with planning, organizing, leading and controlling in organizations. i. Appraise the role and importance of co-ordination.

Leadership

a. Define leadership. b. Explain the major sources of a leader’s power. c. Explain the following leadership theories:

Traits theory

Behavioral theory

Contingency theory

Managerial grid

Tannenbaum and Schmidt leadership continuum

Fieldler’s contingency theory

Situational leadership

Path-goal theory.

Contemporary theories d. Explain the various leadership styles

Motivation

a. Explain the theories of motivation. b. Describe the role of behavioral aspect of motivation. c. Evaluate the limitations to motivation theories. d. Describe how teamwork and consultative management are used as motivational tools. e. Outline the linkage between motivation and output.

Controlling

a. Explain the nature and importance of organizational control. b. Describe the control process. c. Discuss the different organizational control process. d. Explain the different control methods.

Communication

a. Explain the meaning and role of communication in modern organizations. b. Explain the main forms of communication. c. Describe the communication process. d. Distinguish between organizational communication channels and explain their role in managing effectively. e. Discuss the roles of negotiation in the management process both within an organization and with external bodies. f. Identify and describe barriers to communication.

Groups and Teamwork

a. Define and analyze the concept of management groups, inter or intra-group relations and how motivation influences group/managerial behavior. b. Analyze and evaluate the concept of team approach in directing organizational activities. c. Explain how groups are formed within organizations and how this affects performance. d. Explain the nature, functions and purposes of social groups in

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 32

organizations. e. Explain inter-personal and inter-group relations and distinguish between them. f. Define and analyze the concept of organizational culture and business etiquette in organizations.

Human Resource Management

a. Explain the role of the human resource management function and its relationship to other parts of the organization. b. Describe the recruitment process. c. Distinguish between training and development and show their relationship. d. Explain the meaning and effects and/or application of job evaluation, staff appraisal, performance measurement and evaluation; promotion and demotion. e. Explain the disciplinary procedure in human resource management. f. Explain compensation systems and the significance of indirect compensation. g. Explain the concept of organizational health and safety and its benefits. h. Distinguish between duties of employers and employees responsibilities.

Marketing Management

a. Explain the marketing concept. b. Outline the strategic roles of marketing in organizations. c. Explain the main elements of a marketing plan and importance. d. Explain segmentation and targeting of markets and positioning of products within markets. e. Explain the elements of the marketing mix and their application. f. Describe the role of technology in modern marketing. g. Explain the differences and similarities in the marketing of products and services. h. Design and implement a pricing strategy. i. Explain customer care strategies as a means of achieving competitive advantage and their relationship with total quality management.

Operations Management

a .Explain the following types of production process:

Job production

Batch production

Mass/continuous/flow production

Explain and compare the following methods of plant layout:

Process layout

Product layout

Fixed-position layout. c. Discuss the role of operations management in organizations. d. Explain the concept of quality and total quality management. e. Explain how the quality of products and services can be assessed, measured and improved.

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 33

RECOMMENDED/REFERENCE TEXTS 1. IICFA Study Manual 2. Appleby P. O. Modern Business Administration, Pitman. 3. Boachie-Mensah, F. O. Essentials of Management, Woeli Publishing Services. 4. Cole, G. A. Management: Theory and Practice. DP Publications. 5. Marfo-Yiadom, E. Principles of Management, Woeli, Publishing Services.

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 34

PROFESSIONAL LEVEL 2

2.1 Forensic Criminology and Legal Studies

1. OBJECTIVES AND LEARNING OUTCOMES

At the end of course candidates should be able to;

Outline a brief history of Forensic Criminology

Understand Forensic Criminology and the various theory approaches to criminal behavior

Discuss Classical Criminology and identify its major components

Discuss Psychological, Social Structure, Social Process, Social Control and Differential

Reinforcement Theories and identify and explain their major components

Discuss Edwin H. Sutherland’s Principles of Criminology

Explain the Law relating to Search and Seizure

Describe the Charging Process in Criminal Litigation Cases

Describe the Trial Process

Outline the causes of crime associated with government, corporations and individuals

Demonstrate adequate knowledge of the criminal and civil justice systems

Identify the various individual rights and obligations under the civil and criminal justice systems

Understand white collar crime and the effects of white collar crime on the economy

Explain evidence and explain the various forms of evidence.

Explain the contributing factors of Economic Crime

Define Digital Evidence and Identify its major forms

Explain the rules regarding circumstantial evidence

Distinguish between Substantive and Procedural Law

2. FORM OF EXAMINATION The examination will be a three-hour paper of five (5) questions. Candidates will be required to answer all five (5) questions. 3. SYLLABUS WEIGHTING GRID This grid shows the relative weightings of topics within this subject and should guide the relative study time spent on each. The marks available in the assessment will equate to the weightings below.

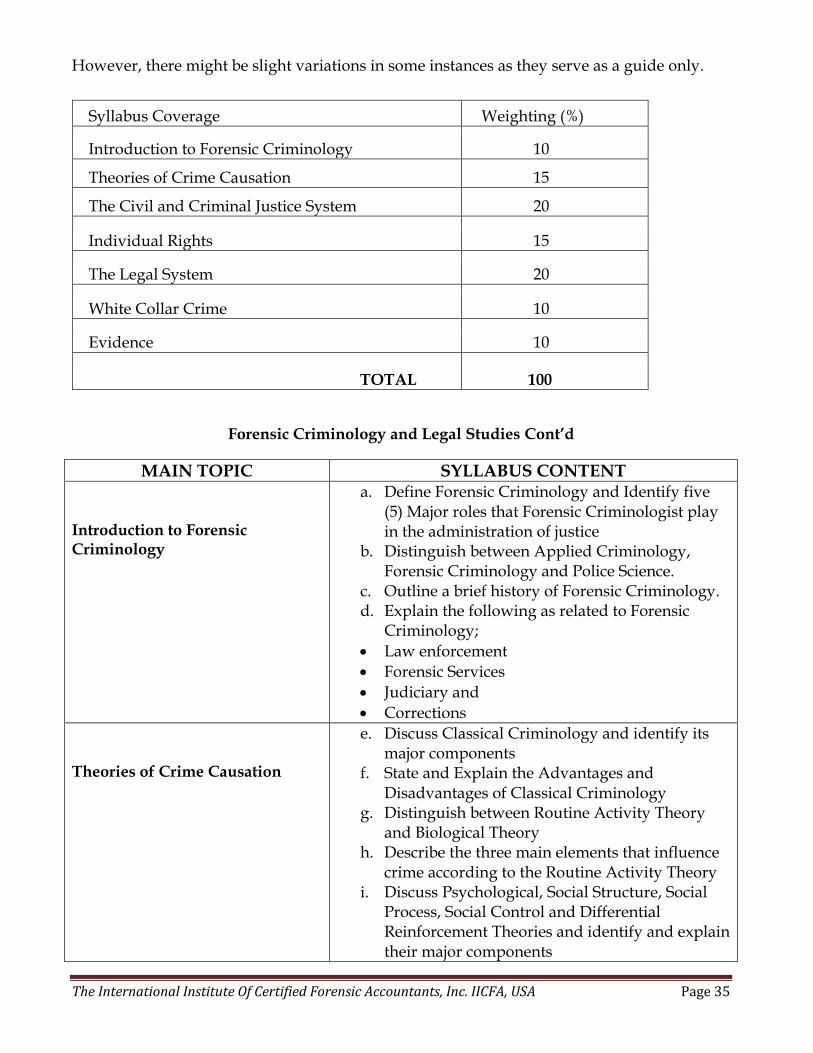

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 35

However, there might be slight variations in some instances as they serve as a guide only.

Syllabus Coverage Weighting (%)

Introduction to Forensic Criminology 10

Theories of Crime Causation 15

The Civil and Criminal Justice System 20

Individual Rights 15

The Legal System 20

White Collar Crime 10

Evidence 10

TOTAL 100

Forensic Criminology and Legal Studies Cont’d

MAIN TOPIC SYLLABUS CONTENT Introduction to Forensic Criminology

a. Define Forensic Criminology and Identify five (5) Major roles that Forensic Criminologist play in the administration of justice

b. Distinguish between Applied Criminology, Forensic Criminology and Police Science.

c. Outline a brief history of Forensic Criminology. d. Explain the following as related to Forensic

Criminology;

Law enforcement

Forensic Services

Judiciary and

Corrections

Theories of Crime Causation

e. Discuss Classical Criminology and identify its major components

f. State and Explain the Advantages and Disadvantages of Classical Criminology

g. Distinguish between Routine Activity Theory and Biological Theory

h. Describe the three main elements that influence crime according to the Routine Activity Theory

i. Discuss Psychological, Social Structure, Social Process, Social Control and Differential Reinforcement Theories and identify and explain their major components

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 36

j. Discuss Edwin H. Sutherland’s Principles of Criminology

The Civil and Criminal Justice System

a. Differentiate between the following;

Pleadings

Discovery

Trial and

Verdict b. Describe the procedures for Civil Litigation

Cases c. Explain the following privileges as may be

determined by a judge;

Litigation Privilege

Attorney-Client Privilege

Settlement Negotiations d. Distinguish between Adversary and Non-

Adversary Evidence e. Explain the final decision/ruling in a Civil

Litigation Case f. Explain the following Remedies in a Civil

Litigation Case;

Declaratory Remedies

Equitable Remedies and

Injunction g. Describe the Charging Process in Criminal

Litigation Cases h. Distinguish between information and indictment i. Describe the Trial Process j. Identify and describe the major parties in trial

process k. Distinguish between Common and Civil law

systems and describe how trial is conducted and verdict is reached.

l. Explain the following;

Sentencing

Appeal and

Punishment

Individual Rights

a. State and Explain the Rights and Obligations under Civil and Criminal Law

b. State and Explain the Law relating to Search and Seizure

c. State and Explain the following torts (Civil Wrongs) a CCFA must avoid;

Defamation

Invasion of Privacy

False imprisonment

Malicious Prosecution

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 37

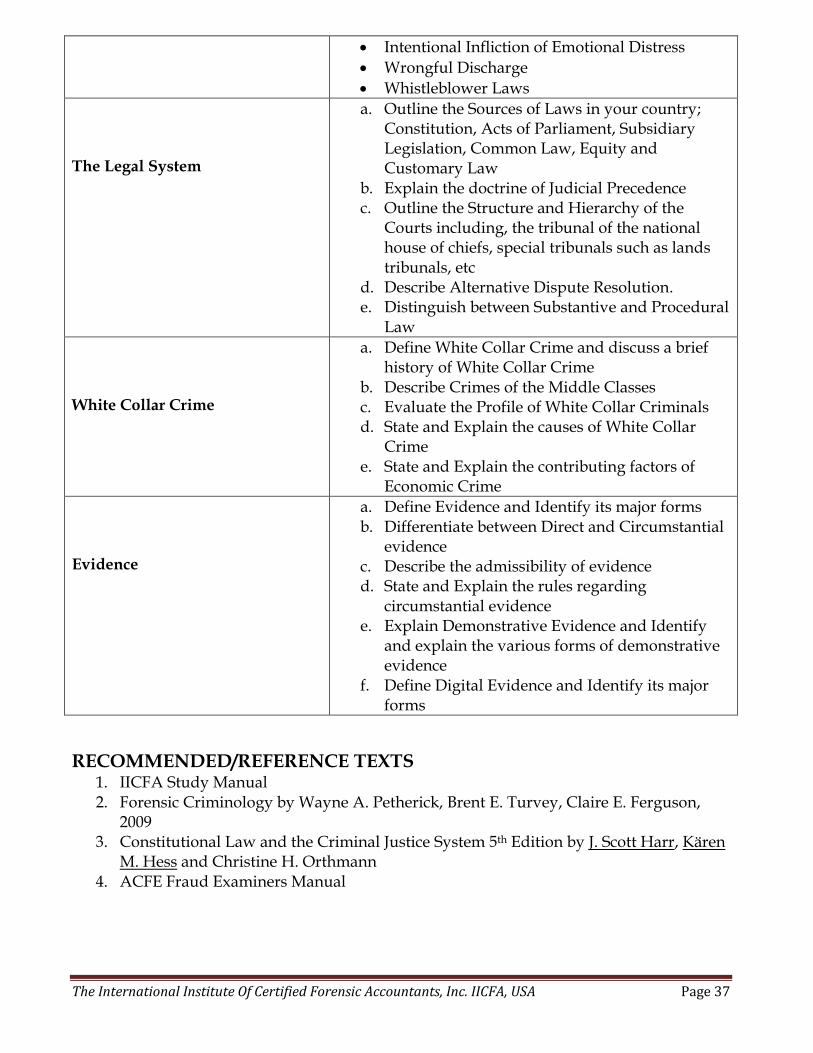

Intentional Infliction of Emotional Distress

Wrongful Discharge

Whistleblower Laws

The Legal System

a. Outline the Sources of Laws in your country; Constitution, Acts of Parliament, Subsidiary Legislation, Common Law, Equity and Customary Law

b. Explain the doctrine of Judicial Precedence c. Outline the Structure and Hierarchy of the

Courts including, the tribunal of the national house of chiefs, special tribunals such as lands tribunals, etc

d. Describe Alternative Dispute Resolution. e. Distinguish between Substantive and Procedural

Law

White Collar Crime

a. Define White Collar Crime and discuss a brief history of White Collar Crime

b. Describe Crimes of the Middle Classes c. Evaluate the Profile of White Collar Criminals d. State and Explain the causes of White Collar

Crime e. State and Explain the contributing factors of

Economic Crime Evidence

a. Define Evidence and Identify its major forms b. Differentiate between Direct and Circumstantial

evidence c. Describe the admissibility of evidence d. State and Explain the rules regarding

circumstantial evidence e. Explain Demonstrative Evidence and Identify

and explain the various forms of demonstrative evidence

f. Define Digital Evidence and Identify its major forms

RECOMMENDED/REFERENCE TEXTS 1. IICFA Study Manual 2. Forensic Criminology by Wayne A. Petherick, Brent E. Turvey, Claire E. Ferguson,

2009 3. Constitutional Law and the Criminal Justice System 5th Edition by J. Scott Harr, Kären

M. Hess and Christine H. Orthmann 4. ACFE Fraud Examiners Manual

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 38

2.2 Corporate Fraud and Internal Control

1. OBJECTIVES AND LEARNING OUTCOMES

At the end of course candidates should be able to;

Understand the types of crimes perpetuated by and against an organization and the social and economic effect of organizational crime on the image of the organization.

Explain how organizations can control Organizational Crime

Distinguish between Competitive Intelligence and Espionage and Identify their sub-

categories

Explain the various forms of corporate spying

Explain the various means through which an Organization loses information

Explain Open Source Information and Identify the Intelligence Pyramid.

Outline the favorite targets of intelligence

Identify the warning signs of infiltration

Describe the process of investigating information theft and outline the prevention

strategies for information theft.

Measure the cost of Occupational Fraud

Outline the causes of Occupational Fraud and Abuse and explain the fraud triangle.

Explain the techniques for collecting and evaluating audit evidence;

Explain and apply basic auditing concepts like internal controls, sampling, compliance test, substantive test, weakness test, etc to detect and prevent fraud.

Identify the fundamental principles of effective control systems

Explain the types and limitations of internal control.

Show how specified internal controls mitigate risk and state their limitations

Examine the merits and demerits of outsourcing of internal audit function.

Conduct test of controls and transactions 2. FORM OF EXAMINATION The examination will be a three-hour paper of five (5) questions. Candidates will be required to answer all five (5) questions. 3. SYLLABUS WEIGHTING GRID This grid shows the relative weightings of topics within this subject and should guide the relative study time spent on each. The marks available in the assessment will equate to the weightings below. However, there might be slight variations in some instances as they serve as a guide only.

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 39

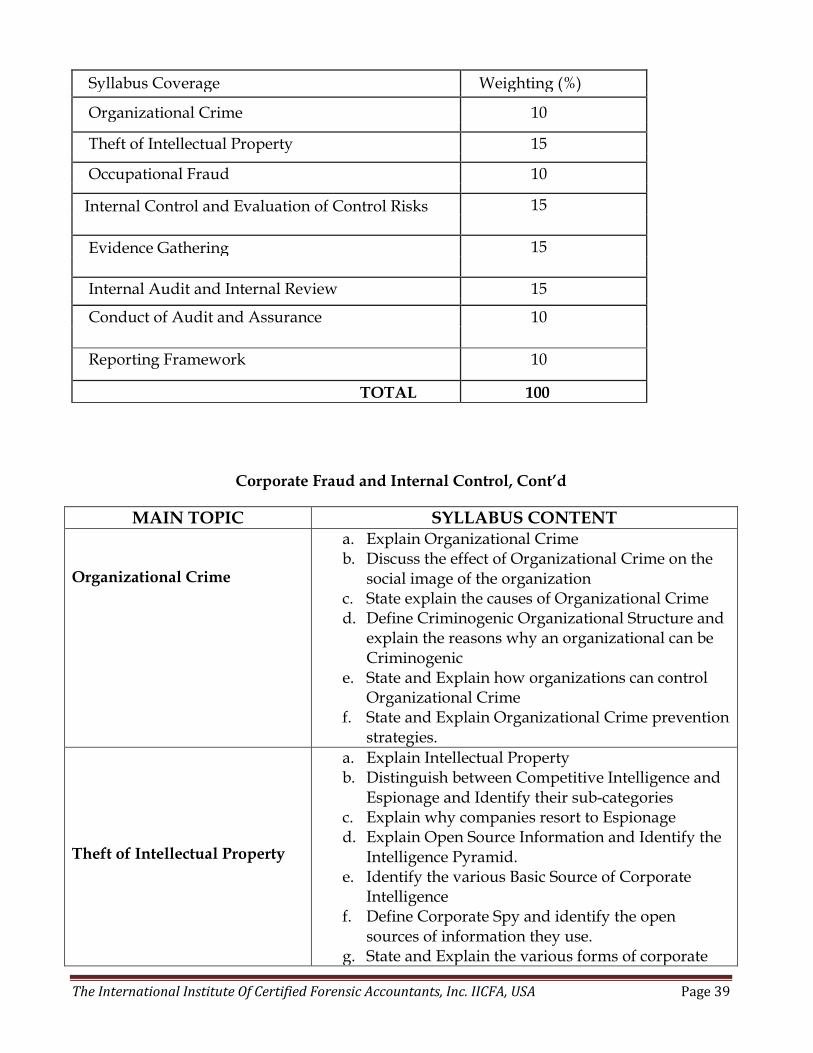

Syllabus Coverage Weighting (%)

Organizational Crime 10

Theft of Intellectual Property 15

Occupational Fraud 10

Internal Control and Evaluation of Control Risks 15

Evidence Gathering 15

Internal Audit and Internal Review 15

Conduct of Audit and Assurance 10

Reporting Framework 10

TOTAL 100

Corporate Fraud and Internal Control, Cont’d

MAIN TOPIC SYLLABUS CONTENT Organizational Crime

a. Explain Organizational Crime b. Discuss the effect of Organizational Crime on the

social image of the organization c. State explain the causes of Organizational Crime d. Define Criminogenic Organizational Structure and

explain the reasons why an organizational can be Criminogenic

e. State and Explain how organizations can control Organizational Crime

f. State and Explain Organizational Crime prevention strategies.

Theft of Intellectual Property

a. Explain Intellectual Property b. Distinguish between Competitive Intelligence and

Espionage and Identify their sub-categories c. Explain why companies resort to Espionage d. Explain Open Source Information and Identify the

Intelligence Pyramid. e. Identify the various Basic Source of Corporate

Intelligence f. Define Corporate Spy and identify the open

sources of information they use. g. State and Explain the various forms of corporate

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 40

spying h. State and explain the places spies snoop. i. Outline the favorite targets of intelligence j. State and explain the various means through which

an Organization loses information k. Identify the warning signs of infiltration l. Describe the process of investigating information

theft and outline the prevention strategies for information theft.

Occupational Fraud

a. Define Occupational Fraud and Identify the reasons why employees commit fraud

b. Discuss the Fraud Triangle c. Define Employee theft and explain the causes of

employee theft d. Measure the cost of Occupational Fraud e. State and explain the techniques of preventing

occupational fraud Internal Control and Evaluation of Control Risks

a. State the reasons for organizations having effective systems of control.

b. Identify the fundamental principles of effective control systems.

c. Identify the main areas of a business that need effective control systems.

d. Identify the components of internal control in both manual and IT environments, including:

the overall control environment and Control Procedures

preventive, detective and corrective controls

internal audit as a control factor e. Define and classify different types of internal

control, with particular emphasis upon those which impact upon the quality of financial information.

f. Show how specified internal controls mitigate risk and state their limitations.

g. Identify internal controls for an organization in a given scenario.

h. Identify internal control weaknesses in a given scenario.

i. Identify, for a specified organization, the sources of information which will enable a sufficient record to be made of accounting or other systems and internal controls.

j. Define internal control. k. State and explain the types and limitations of

internal control. l. Explain the following in relation to internal control:

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 41

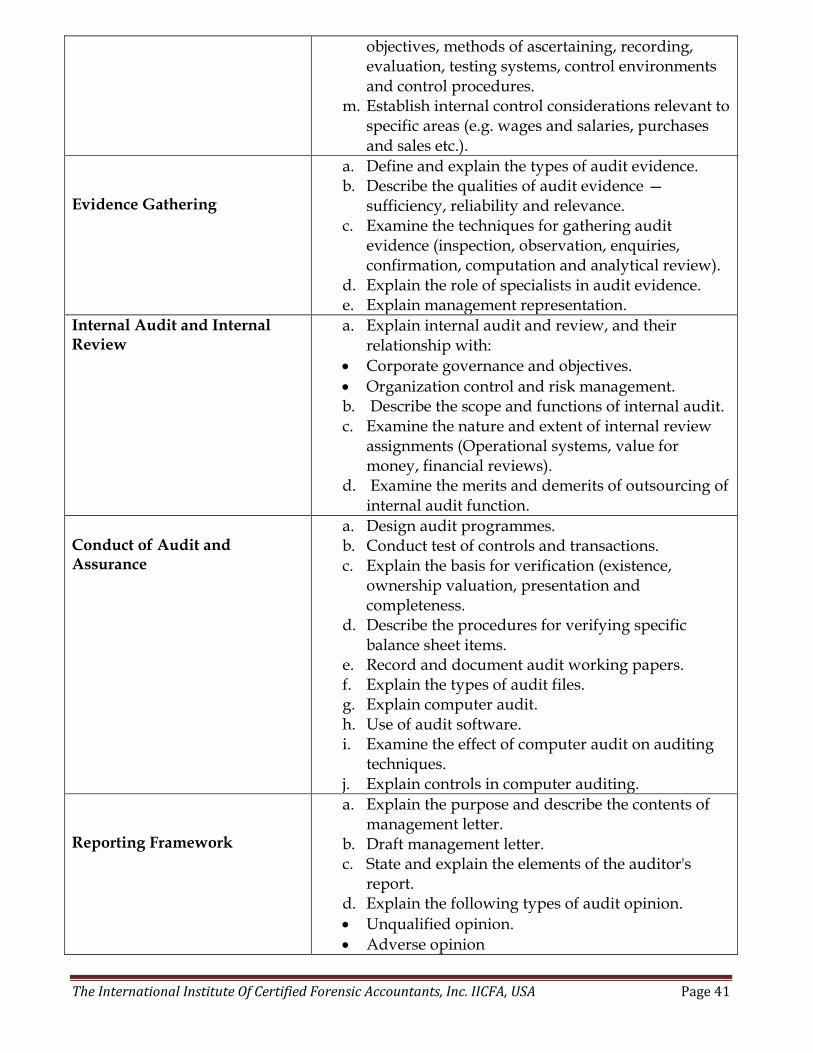

objectives, methods of ascertaining, recording, evaluation, testing systems, control environments and control procedures.

m. Establish internal control considerations relevant to specific areas (e.g. wages and salaries, purchases and sales etc.).

Evidence Gathering

a. Define and explain the types of audit evidence. b. Describe the qualities of audit evidence —

sufficiency, reliability and relevance. c. Examine the techniques for gathering audit

evidence (inspection, observation, enquiries, confirmation, computation and analytical review).

d. Explain the role of specialists in audit evidence. e. Explain management representation.

Internal Audit and Internal Review

a. Explain internal audit and review, and their relationship with:

Corporate governance and objectives.

Organization control and risk management. b. Describe the scope and functions of internal audit. c. Examine the nature and extent of internal review

assignments (Operational systems, value for money, financial reviews).

d. Examine the merits and demerits of outsourcing of internal audit function.

Conduct of Audit and Assurance

a. Design audit programmes. b. Conduct test of controls and transactions. c. Explain the basis for verification (existence,

ownership valuation, presentation and completeness.

d. Describe the procedures for verifying specific balance sheet items.

e. Record and document audit working papers. f. Explain the types of audit files. g. Explain computer audit. h. Use of audit software. i. Examine the effect of computer audit on auditing

techniques. j. Explain controls in computer auditing.

Reporting Framework

a. Explain the purpose and describe the contents of management letter.

b. Draft management letter. c. State and explain the elements of the auditor's

report. d. Explain the following types of audit opinion.

Unqualified opinion.

Adverse opinion

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 42

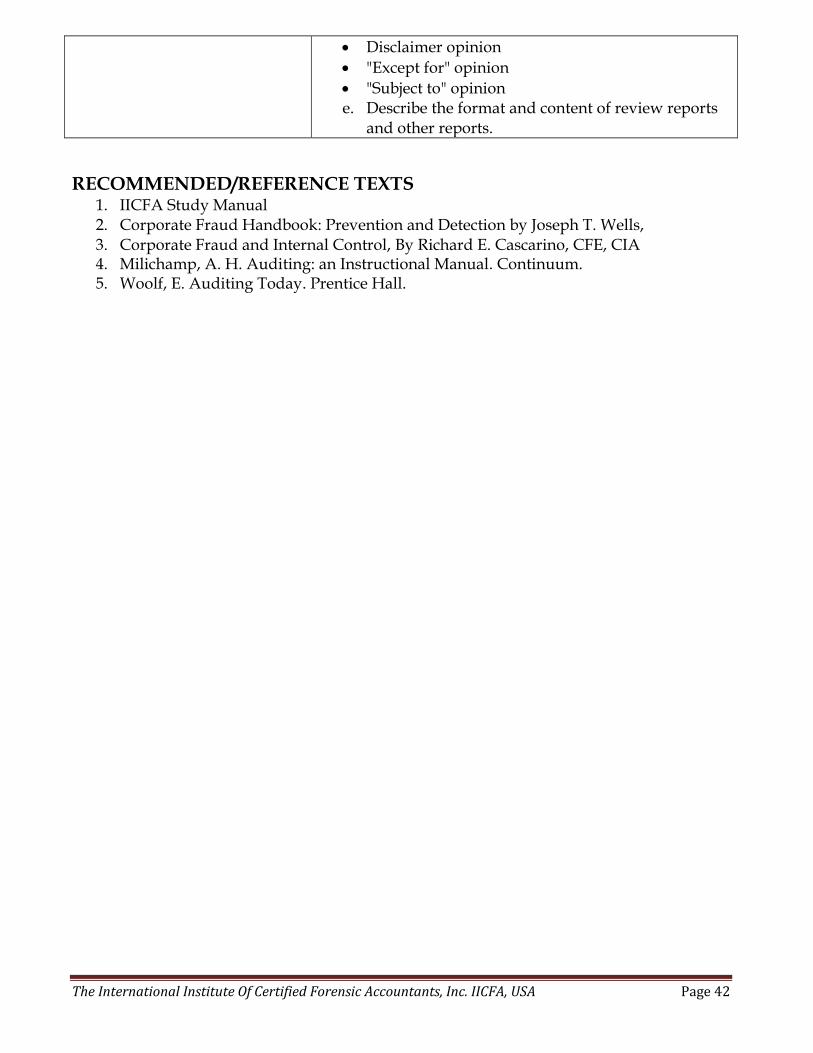

Disclaimer opinion

"Except for" opinion

"Subject to" opinion e. Describe the format and content of review reports

and other reports.

RECOMMENDED/REFERENCE TEXTS 1. IICFA Study Manual 2. Corporate Fraud Handbook: Prevention and Detection by Joseph T. Wells, 3. Corporate Fraud and Internal Control, By Richard E. Cascarino, CFE, CIA 4. Milichamp, A. H. Auditing: an Instructional Manual. Continuum. 5. Woolf, E. Auditing Today. Prentice Hall.

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 43

2.3 Financial Statement and Institution Fraud

1. OBJECTIVES AND LEARNING OUTCOMES

At the end of course candidates should be able to;

Outline the reasons and red flags associated with financial statement fraud

Understand Financial Statement Fraud Schemes

Apply Financial Statement Analysis to detect and prevent fraud

Explain Securities fraud and identify the red flags associated with Ponzi Schemes

Identify the various vehicles and methods of money laundering

Outline the objectives and responsibilities of the Basel Committee on Banking Supervision

Understand Embezzlement Schemes and identify the red flags of various schemes of embezzlement

Understand credit card fraud and identify the red flags associated with credit card fraud.

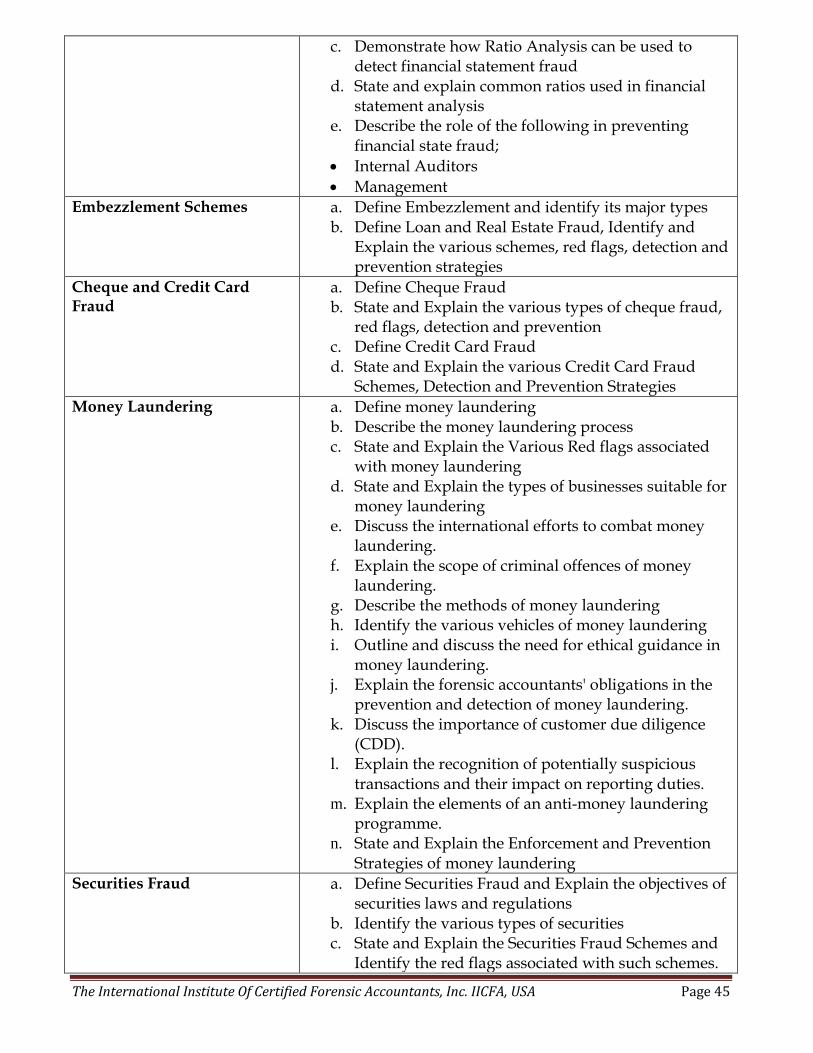

Demonstrate how Ratio Analysis can be used to detect financial statement fraud

Explain the Various Red flags associated with money laundering

Explain the types of businesses suitable for money laundering

Explain the recognition of potentially suspicious transactions and their impact on reporting duties

Define Global Liquidity Standards and Calculate various liquidity ratios

Explain the principles of developing Risk Management 2. FORM OF EXAMINATION The examination will be a three-hour paper of five (5) questions. Candidates will be required to answer all five (5) questions. 3. SYLLABUS WEIGHTING GRID This grid shows the relative weightings of topics within this subject and should guide the relative study time spent on each. The marks available in the assessment will equate to the weightings below. However, there might be slight variations in some instances as they serve as a guide only.

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 44

Syllabus Coverage Weighting (%)

Introduction to Financial Statement Fraud 5

Financial Statement Fraud - Schemes 10

Financial Statement Fraud – Red flags 10

Financial Statement Analysis and Prevention 10

Embezzlement Schemes 10

Cheque and Credit Card Fraud 15

Money Laundering 20

Securities Fraud 10

The Basel Committee on Banking Supervision 10

TOTAL 100

Financial Statement and Institution Fraud, Cont’d

MAIN TOPIC SYLLABUS CONTENT Introduction to Financial Statement Fraud

a. Define Financial Statement Fraud b. Outline the Causes of Financial Statement Fraud c. Account for the trends in Financial Statement Fraud

Financial Statement Fraud Schemes

a. State and Explain the major financial statement fraud schemes;

Overstated Assets or Revenue

Understated Liabilities or Expenses b. Explain the following classification of financial

statement fraud schemes

Fictitious Revenue

Timing Differences

Improper Assets Valuation

Concealed Liabilities and Expense

Improper Disclosures c. Define Channel Stuffing

Financial Statement Fraud Red flags

a. Identify the Various Red flags associated with the following classes of financial statement fraud;

Fictitious Revenue

Timing Differences

Improper Assets Valuation

Concealed Liabilities and Expense

Improper Disclosures

Financial Statement Analysis and Prevention

a. Define Financial Statement Analysis b. Distinguish between horizontal and Vertical

Analysis of Financial Statement.

The International Institute Of Certified Forensic Accountants, Inc. IICFA, USA Page 45

c. Demonstrate how Ratio Analysis can be used to detect financial statement fraud