swinburne's 2012 ias/ifrs in vietnam survey

DESCRIPTION

Swinburne's 2012 IAS/IFRS in Vietnam survey is to evaluate the support given to the convergence process of Vietnamese Accounting Standards (VAS) with International Accounting Standards (IAS) and International Financial Reporting Standards (IFRS) in Vietnam.The target participants are auditors, financial statement preparers/users, accounting academics, financial analysts and business executives who havegeneral knowledge about VAS, IAS/IFRS and the accounting practices in Vietnam. The findings of the survey are for a doctoral thesis and relatedpublications of the author, Ms Duc Hong Thi Phan, PhD student of Swinburne University, Melbourne, Australia. The survey is administered using the mixed methods, including mailing to over 5,000 CFO, Auditors, Academic in Vietnam wide. The same survey is also administered online at link http://opinio.online.swin.edu.au/s?s=12114 and promoted via social media networks i.e LinkedIn, Facebook, Twitter. The author, Ms Duc Hong Thi Phan, holds the full copyrights of this survey, both hardcopy and online versions and their results. The author is willing to share the aggregated analysed survey findings for research purposes. If you would like to have access to these reports please write to the author at [email protected]TRANSCRIPT

Faculty of Business

and Enterprises

Cnr William and

Wakefield Street Hawthorn

Mail H25

PO Box 218 Hawthorn

Victoria 3122 Australia

Telephone +61 3 9214 8000

Facsimile +61 3 9819 5454

http://www.swin.edu.au

© Copyright 2012 Duc Hong Thi Phan

SURVEY BOOKLET

Swinburne’s 2012 IAS/IFRS Convergence in Vietnam

Instruction

���� The survey is to evaluate the support given to the convergence process of

Vietnamese Accounting Standards (VAS) with International Accounting Standards

(IAS) and International Financial Reporting Standards (IFRS) in Vietnam.

���� The target participants are auditors, financial statement preparers/users,

accounting academics, financial analysts and business executives who have

general knowledge about VAS, IAS/IFRS and the accounting practices in

Vietnam. The findings of the survey are for a doctoral thesis and related

publications of the researcher.

���� Your participation is voluntary and that you are free to withdraw from the project at

any time without explanation. It takes approximately 20 to 30 minutes to complete

the survey. Your anonymity is preserved and you will not be identified in any

publications.

���� There are no right or wrong answers. All we are interested in. is your perception

related to IAS/IFRS implementation.

���� Place (X) in an appropriate square or fill in the provided space if required.

���� Please ensure that you answer ALL questions. Missing question(s) might result in

the whole questionnaire being invalid.

This survey has been approved by or on behalf of Swinburne’s Human Research

Ethics Committee. If you have any questions regarding this project, please contact:

Ms Duc Hong Thi Phan, Student Researcher, Email: [email protected]

Dr Nicholas Mroczkowski, Coordinating Supervisor, Email: [email protected]

Dr Meropy Barut, Associate Supervisor, Email: [email protected]

Please return the completed questionnaire using the enclosed envelope. No stamp is required

Faculty of Business

and Enterprises

Cnr William and

Wakefield Street Hawthorn

Mail H25

PO Box 218 Hawthorn

Victoria 3122 Australia

Telephone +61 3 9214 8000

Facsimile +61 3 9819 5454

http://www.swin.edu.au

Survey: Swinburne’s 2012 IAS/IFRS Convergence in Vietnam Page 1

© Copyright 2012 Duc Hong Thi Phan

Letter of Introduction

Friday, 06/04/2012

Dear sir/madam,

I am currently a PhD student at Swinburne University of Technology, Australia.

I am conducting research which examines the extent of the convergence

progress of Vietnamese Accounting Standards (VAS) with International

Accounting Standards and International Financial Reporting Standards

(IAS/IFRS) in Vietnam. The findings of the survey will be used for my PhD

thesis and for related publications. I would like to invite you to participate in

this research project. Participation is completely voluntary.

I would be grateful if you could spend 20 to 30 minutes of your time at your

convenience to answer the questionnaire. I have sent you two questionnaire

booklets in both English and Vietnamese languages. Please choose to answer

the questionnaire in the language that you feel most comfortable. Please

assist me to achieve the maximum response rate by passing on the other

booklet to your colleague or manager. I set my goal of 1,000 returned

questionnaires to achieve the statistical results which best represent the

perceptions of Vietnamese accounting/auditing professionals about IAS/IFRS.

Please return the completed questionnaire in the enclosed reply paid envelope

or email to [email protected]. Alternatively, you may prefer to

complete the questionnaire online (both English & Vietnamese) at the link

http://opinio.online.swin.edu.au/s?s=12114.

By completing the questionnaire you will assist in contributing to knowledge

regarding the potential advantages, and disadvantages of IAS/IFRS; the

challenges of the IAS/IFRS implementation process; the potential influence

factors on the acceptance of IAS/IFRS in Vietnam; and what best approaches

for the future evolution of Vietnamese accounting standards are available in

light of the current global movement towards IAS/IFRS. I believe that the

findings of the project will assist the Vietnamese Accounting Standard Setters

in making favourable decisions affecting accounting practice, which will in turn

support social and economic development in Vietnam.

Your response to this questionnaire will be kept absolutely confidential.

Subsequent reports based on this research will only present aggregate data in

statistical form without identifying individual responses. All responses will be

coded and the originals destroyed. No identifiable information will be used and

all data will be grouped for analysis.

Faculty of Business

and Enterprises

Cnr William and

Wakefield Street Hawthorn

Mail H25

PO Box 218 Hawthorn

Victoria 3122 Australia

Telephone +61 3 9214 8000

Facsimile +61 3 9819 5454

http://www.swin.edu.au

Survey: Swinburne’s 2012 IAS/IFRS Convergence in Vietnam Page 2

© Copyright 2012 Duc Hong Thi Phan

This project has been approved by Swinburne’s Human Research Ethics

Committee (SUHREC) in line with the National Statement on Ethical Conduct

in Research Involving Humans. If you have any complaints or concerns about

the conduct of this project, please call (+61) 3 9214 5223 or write to.

The Chair of Human Research Ethics Committee

Swinburne University of Technology

PO Box 218, Hawthorn Vic 3122, Australia

Email: [email protected]

Thank you very much for your time and valued contribution. Should you

require any further information about this invitation please do not hesitate to

contact me at [email protected].

Yours sincerely

Duc Hong Thi Phan (Ms)

Student Researcher

Survey: Swinburne’s 2012 IAS/IFRS Convergence in Vietnam

Survey: Swinburne’s 2012 IAS/IFRS Convergence in Vietnam Page 3

© Copyright 2012 Duc Hong Thi Phan

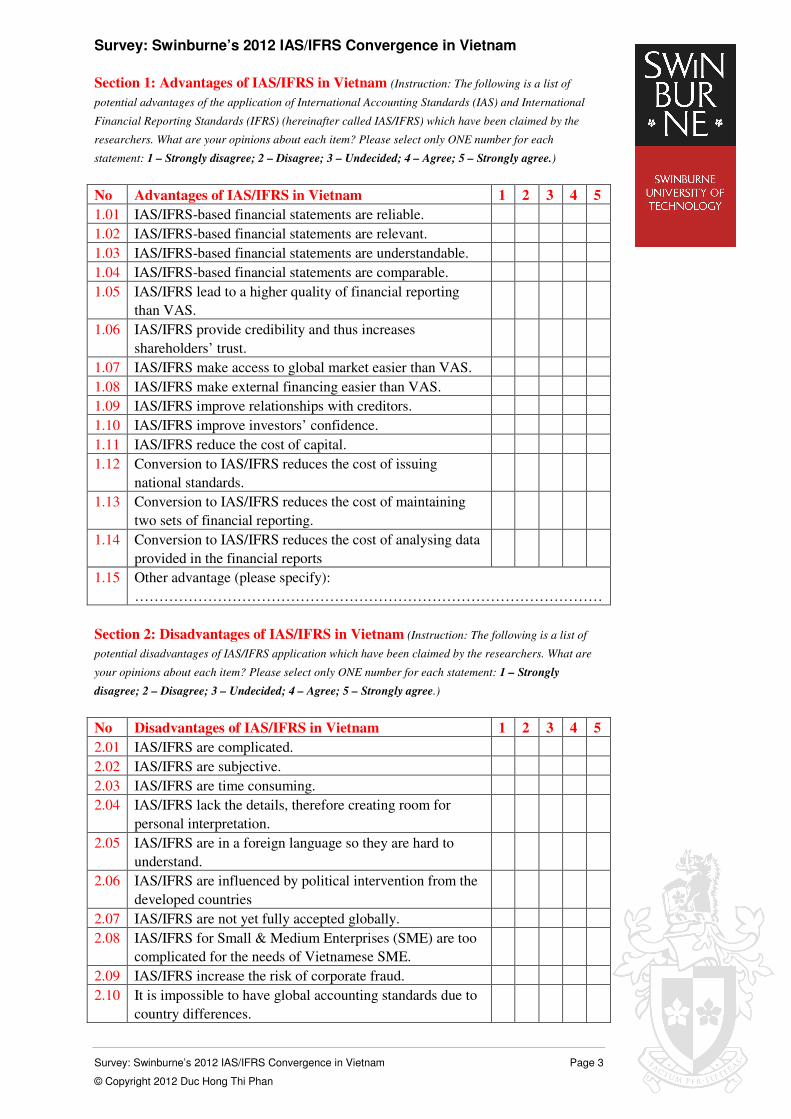

Section 1: Advantages of IAS/IFRS in Vietnam (Instruction: The following is a list of

potential advantages of the application of International Accounting Standards (IAS) and International

Financial Reporting Standards (IFRS) (hereinafter called IAS/IFRS) which have been claimed by the

researchers. What are your opinions about each item? Please select only ONE number for each

statement: 1 – Strongly disagree; 2 – Disagree; 3 – Undecided; 4 – Agree; 5 – Strongly agree.)

No Advantages of IAS/IFRS in Vietnam 1 2 3 4 5

1.01 IAS/IFRS-based financial statements are reliable.

1.02 IAS/IFRS-based financial statements are relevant.

1.03 IAS/IFRS-based financial statements are understandable.

1.04 IAS/IFRS-based financial statements are comparable.

1.05 IAS/IFRS lead to a higher quality of financial reporting

than VAS.

1.06 IAS/IFRS provide credibility and thus increases

shareholders’ trust.

1.07 IAS/IFRS make access to global market easier than VAS.

1.08 IAS/IFRS make external financing easier than VAS.

1.09 IAS/IFRS improve relationships with creditors.

1.10 IAS/IFRS improve investors’ confidence.

1.11 IAS/IFRS reduce the cost of capital.

1.12 Conversion to IAS/IFRS reduces the cost of issuing

national standards.

1.13 Conversion to IAS/IFRS reduces the cost of maintaining

two sets of financial reporting.

1.14 Conversion to IAS/IFRS reduces the cost of analysing data

provided in the financial reports

1.15 Other advantage (please specify):

……………………………………………………………………………………

Section 2: Disadvantages of IAS/IFRS in Vietnam (Instruction: The following is a list of

potential disadvantages of IAS/IFRS application which have been claimed by the researchers. What are

your opinions about each item? Please select only ONE number for each statement: 1 – Strongly

disagree; 2 – Disagree; 3 – Undecided; 4 – Agree; 5 – Strongly agree.)

No Disadvantages of IAS/IFRS in Vietnam 1 2 3 4 5

2.01 IAS/IFRS are complicated.

2.02 IAS/IFRS are subjective.

2.03 IAS/IFRS are time consuming.

2.04 IAS/IFRS lack the details, therefore creating room for

personal interpretation.

2.05 IAS/IFRS are in a foreign language so they are hard to

understand.

2.06 IAS/IFRS are influenced by political intervention from the

developed countries

2.07 IAS/IFRS are not yet fully accepted globally.

2.08 IAS/IFRS for Small & Medium Enterprises (SME) are too

complicated for the needs of Vietnamese SME.

2.09 IAS/IFRS increase the risk of corporate fraud.

2.10 It is impossible to have global accounting standards due to

country differences.

Survey: Swinburne’s 2012 IAS/IFRS Convergence in Vietnam Page 4

© Copyright 2012 Duc Hong Thi Phan

No Disadvantages of IAS/IFRS in Vietnam 1 2 3 4 5

2.11 Countries like Vietnam do not need IAS/IFRS.

2.12 Countries like Vietnam do not have any voice in the

IAS/IFRS setting process.

2.13 National pride is compromised when national standards

give way to IFRS.

2.14 Costs of conversion from VAS to IAS/IFRS will outweigh

its benefits.

2.15 Other disadvantage (please specify):

……………………………………………………………………………………

Section 3: Challenges of IAS/IFRS implementation in Vietnam (Instruction: The

following is a list of potential challenges of IAS/IFRS implementation which have been claimed by the

Researchers. What are your opinions about each item? Please select only ONE number for each

statement: 1 – Strongly disagree; 2 – Disagree; 3 – Undecided; 4 – Agree; 5 – Strongly agree.)

No Challenges of IAS/IFRS implementation in Vietnam 1 2 3 4 5

3.01 Updating information technology systems

3.02 Updating accounting processes

3.03 Updating auditing processes

3.04 Managing public perception of changes in financial

statements

3.05 Managing transition workload while maintaining day-to-

day activities

3.06 Educating non-financial staff/management

3.07 Educating financial staff/management

3.08 Insufficient guidance on first-time application of IFRS

3.09 Lack of timely IAS/IFRS translation into the Vietnamese

language

3.10 Limited coverage of IAS/IFRS in the current university

curriculum

3.11 Other challenge (please specify):

……………………………………………………………………………………

3.12 If given a choice, would your company consider adopting IAS/IFRS? Please

explain why:

……………………………………………………………………………………

Section 4: Readiness of IAS/IFRS conversion in Vietnam (Instruction: When responding

to these statements, focus on your knowledge and experience about IAS/IFRS. Where does your company

stand in terms of preparedness for the adoption of each of the IAS/IFRS standards? Please select only

ONE number for each statement: 1 – Nothing done to date; 2 – Have done some planning; 3 – Have

completed an impact assessment; 4 – Have moved beyond an impact assessment; 5 –Ready for

conversion to IAS/IFRS; NA – Not applicable to your company.)

No Readiness of IAS/IFRS conversion in Vietnam 1 2 3 4 5 NA

4.01 First time Adoption of IFRS (IFRS 1)

4.02 Share-based Payment (IFRS 2)

4.03 Business Combinations (IFRS 3)

4.04 Insurance Contracts (IFRS 4)

4.05 Non-current Assets Held for Sale and Discontinued

Operations (IFRS 5)

Survey: Swinburne’s 2012 IAS/IFRS Convergence in Vietnam Page 5

© Copyright 2012 Duc Hong Thi Phan

No Readiness of IAS/IFRS conversion in Vietnam 1 2 3 4 5 NA

4.06 Exploration for and Evaluation of Mineral Resources

(IFRS 6)

4.07 Financial Instruments (IFRS 7, IFRS9, IAS32, IAS39)

4.08 Operating Segments (IFRS 8)

4.09 Consolidated Financial Statements (IFRS 10, IAS27)

4.10 Joint Arrangements (IFRS 11)

4.11 Disclosure of Interests in Other Entities (IFRS 12)

4.12 Fair Value Measurement (IFRS 13)

4.13 Presentation of Financial Statements (IAS 1)

4.14 Inventories (IAS 2)

4.15 Cash Flow Statements (IAS 7)

4.16 Accounting Policies, Changes in Accounting

Estimates and Errors (IAS 8)

4.17 Events After the Balance Sheet Date (IAS 10)

4.18 Construction Contracts (IAS 11)

4.19 Income Taxes (IAS 12)

4.20 Property, Plant and Equipment (IAS 16)

4.21 Leases (IAS 17)

4.22 Revenue (IAS 18)

4.23 Employee Benefits (IAS 19)

4.24 Accounting for Government Grants, Disclosure of

Government Assistance (IAS 20)

4.25 The Effects of Changes in Foreign Exchange Rates

(IAS 21)

4.26 Borrowing Costs (IAS 23)

4.27 Related Party Disclosures (IAS 24)

4.28 Accounting and Reporting by Retirement Benefit

Plans (IAS 26)

4.29 Investments in Associates (IAS 28)

4.30 Financial Reporting in Hyperinflationary Economies

(IAS 29)

4.31 Interests in Joint Ventures (IAS 31)

4.32 Earnings Per Share (IAS 33)

4.33 Interim Financial Reporting (IAS 34)

4.34 Impairment of Assets (IAS 36)

4.35 Provisions, Contingent Liabilities and Contingent

Assets (IAS 37)

4.36 Intangible Assets (IAS 38)

4.37 Investment Property (IAS 40)

4.38 Agriculture (IAS 41)

Q4: What timeline would be required for preparation for full conversion to IAS/IFRS?

Timeline 1 year 2 years 3 years 4 years 5 years Over 5 years

Section 5: Choices of IAS/IFRS implementation in Vietnam (Instruction: The following

is a list of potential choices of IAS/IFRS application in Vietnam. What approach do you believe would

suit Vietnam context? Please indicate your choice for each statement listed below. Please select only

ONE number for each statement: 1 – Strongly disagree; 2 – Disagree; 3 – Undecided; 4 – Agree; 5 –

Strongly agree.)

Survey: Swinburne’s 2012 IAS/IFRS Convergence in Vietnam Page 6

© Copyright 2012 Duc Hong Thi Phan

No Choices of IAS/IFRS implementation in Vietnam 1 2 3 4 5

Adoption or Convergence

5.01 Full adoption approach, i.e. replace entirely VAS by

IAS/IFRS and provide supplementary information only for

national issues not addressed in IAS/IFRS (big bang

approach).

5.02 Convergence approach, i.e. introduce IAS/IFRS standard

by standard and eventually have Vietnamese accounting

system comparable to IAS/IFRS (staggered approach).

5.03 Adaptation approach, i.e. amend and adjust IAS/IFRS to

suit the Vietnamese context.

5.04 No change approach, i.e. continue with the current VAS,

no change is required.

5.05 Other approach (please specify):

……………………………………………………………………………………

Voluntary or Mandatory

5.06 Allow the voluntary use of IAS/IFRS for all reporting

entities

5.07 Allow the voluntary use of IAS/IFRS only for publicly

listed entities

5.08 Allow the voluntary use of IAS/IFRS only for foreign

invested entities

5.09 Allow the voluntary use of IAS/IFRS only for financial

institutions

5.10 Require the mandatory use of IAS/IFRS for all reporting

entities

5.11 Require the mandatory use of IAS/IFRS only for publicly

listed entities

5.12 Require the mandatory use of IAS/IFRS only for foreign

invested entities

5.13 Require the mandatory use of IAS/IFRS only for financial

institutions

5.14 Do not allow IAS/IFRS at all.

5.15 Other approach (please specify):

……………………………………………………………………………………

Q5: What timeline would be required for preparation for the above choice of

IAS/IFRS implementation in Vietnam?

Timeline 1 year 2 years 3 years 4 years 5 years Over 5 years

Section 6: Factors influence on the acceptance of IAS/IFRS in Vietnam (Instruction:

The following is a list of factors which have been claimed by the researchers to influence the acceptance

of IAS/IFRS in a developing country like Vietnam. What are your opinions about each factor? Please

select only ONE number for each statement: 1 – Strongly disagree; 2 – Disagree; 3 – Undecided; 4 –

Agree; 5 – Strongly agree.)

No Factors influence on the acceptance of IAS/IFRS in

Vietnam

1 2 3 4 5

External pressures from multinational lending agencies

and donors

6.01 World Bank (WB)

Survey: Swinburne’s 2012 IAS/IFRS Convergence in Vietnam Page 7

© Copyright 2012 Duc Hong Thi Phan

No Factors influence on the acceptance of IAS/IFRS in

Vietnam

1 2 3 4 5

6.02 Asian Development Bank (ADB)

6.03 International Monetary Fund (IMF)

6.04 International Finance Corporation (IFC)

6.05 World Trade Organisation (WTO)

6.06 Japanese Official Development Assistance (ODA) fund

6.07 Korean Official Development Assistance (ODA) fund

External pressures from International Professional

Bodies

6.08 International Federation of Accountants (IFAC)

6.09 The Association of Chartered Certified Accountants

(ACCA)

6.10 The Society of Certified Practising Accountants of

Australia (CPA Australia)

6.11 Asean Federation of Accountants (AFA)

6.12 Asian-Oceanian Standard-Setters Group (AOSSG)

6.13 International Accounting Standards Board (IASB)

Internal pressures from associations/organisations in

Vietnam

6.14 Vietnam Association of Certified Public Accountants

(VACPA)

6.15 Vietnam Accounting & Auditing Association (VAA)

6.16 International accountancy firms (i.e. Big Four audit firms)

6.17 Academic of large accounting universities

6.18 Industry Leading Enterprises

6.19 Multinational Corporations

6.20 Key trading partner countries

Other factors

6.21 Needs to attract more foreign direct investment

6.22 Needs to raise finance in international capital market

6.23 Needs to enhance the development of national stock

exchange market

6.24 Needs to enhance national reputation as being in

compliance with international rules

6.25 Lobby from the leading publicly listed companies

6.26 Lobby from the leading foreign companies

6.27 Requirements of financial institutions and major creditors

6.28 Requirements of state regulatory authorities

6.29 Following Asian countries which successfully adopted or

converged to IAS/IFRS

6.30 Following the trend of over 120 countries which permit or

require IAS/IFRS

6.31 Other factor (please specify)

……………………………………………………………………………………

Q6. In your opinion, what top three factors have most significant influence? Please

provide the factor numbers (e.g. 6.xx)

_____________________________________________________________________

Survey: Swinburne’s 2012 IAS/IFRS Convergence in Vietnam Page 8

© Copyright 2012 Duc Hong Thi Phan

Section 7: Recommendation to Vietnamese Accounting Standards Committee –

VASC (It is optional. However, the aggregate findings of the study will be forwarded to the Vietnamese

Accounting Standards Committee. So please do not hesitate, be direct and honest.)

Q7.1 What top three accounting issues/standards should be viewed as priority in the

path to converge VAS towards IAS/IFRS? i. _____________________________________________________________________

ii. _____________________________________________________________________

iii. _____________________________________________________________________

Q7.2 Do you have any other recommendation to VASC? (give details if any)

_____________________________________________________________________

_____________________________________________________________________

_____________________________________________________________________

Section 8: Background of the respondent (Thank you. I would now like to finish off with some

questions about your organisation and yourself for statistical purposes.)

8.1 Your Gender Male Female

8.2 Your Age Under 21 21-30 31-40 41-50 51-60 Over 60

8.3 Your Highest High school Vocational Diploma Bachelor Master Doctorate

Academic Qualification

8.4 Main language Vietnamese English Other, please specify:…………………………………………………………………

of highest qualification

8.5 Member of None VACPA VAA ACCA CPA Other (specify)

professional bodies (select as many as appropriate)

Australia …………….......

8.6 IFRS training Self-study VACPA VAA ACCA CPA Australia Other (specify)

…………….......

8.7 Years of Less than 1-5 years 6-10 years 11-15 years 16-20 years Over 20 years

working experience 1 year

8.8 Years of living None 1 year 2 years 3 years 4 years Over 4 years

overseas

8.9 Self-assessment Not at all Very poor Poor Average Good Excellent

about IAS/IFRS knowledge (out of 10)

(0 point) (1-2 points) (3-4 points) (5-6 points) (7-8 points) (9-10 points)

8.10 Level of IAS/ Not required Very basic Basic Average Good Excellent

IFRS knowledge required at work (out of 10)

(0 point) (1-2 points) (3-4 points) (5-6 points) (7-8 points) (9-10 points)

8.11 Frequency of Never Few times Few times Few times Few times Daily

IAS/ IFRS use at work per year per quarter per month per week

8.12 What role best Financial Financial Auditor Lecturer Researcher Other (specify)

describes you when answering this survey?

report preparer

report user ……………………

8.13 Your current Junior Senior Team Manager Head of the Other (specify)

position leader organisation ………………..

Survey: Swinburne’s 2012 IAS/IFRS Convergence in Vietnam Page 9

© Copyright 2012 Duc Hong Thi Phan

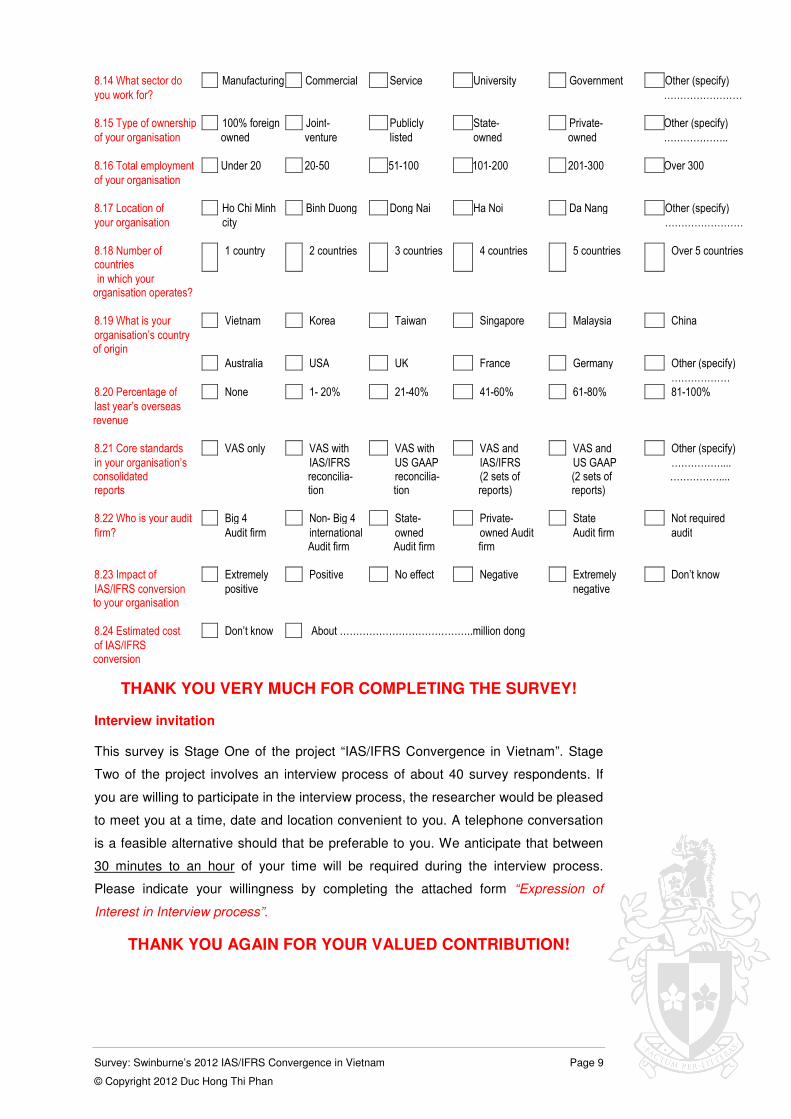

8.14 What sector do Manufacturing Commercial Service University Government Other (specify)

you work for? ……………………

8.15 Type of ownership 100% foreign Joint- Publicly State- Private- Other (specify)

of your organisation owned venture listed owned owned ………………..

8.16 Total employment Under 20 20-50 51-100 101-200 201-300 Over 300

of your organisation

8.17 Location of Ho Chi Minh Binh Duong Dong Nai Ha Noi Da Nang Other (specify)

your organisation city ……………………

8.18 Number of countries

1 country 2 countries 3 countries 4 countries 5 countries Over 5 countries

in which your organisation operates?

8.19 What is your Vietnam Korea Taiwan Singapore Malaysia China

organisation’s country of origin

Australia USA UK France Germany Other (specify)

………………

8.20 Percentage of None 1- 20% 21-40% 41-60% 61-80% 81-100%

last year’s overseas revenue

8.21 Core standards VAS only VAS with VAS with VAS and VAS and Other (specify)

in your organisation’s consolidated reports

IAS/IFRS reconcilia-tion

US GAAP reconcilia-tion

IAS/IFRS (2 sets of reports)

US GAAP (2 sets of reports)

…………….... ……………....

8.22 Who is your audit Big 4 Non- Big 4 State- Private- State Not required

firm? Audit firm international Audit firm

owned Audit firm

owned Audit firm

Audit firm audit

8.23 Impact of Extremely Positive No effect Negative Extremely Don’t know

IAS/IFRS conversion to your organisation

positive negative

8.24 Estimated cost Don’t know About …………………………………..million dong

of IAS/IFRS conversion

THANK YOU VERY MUCH FOR COMPLETING THE SURVEY! Interview invitation

This survey is Stage One of the project “IAS/IFRS Convergence in Vietnam”. Stage

Two of the project involves an interview process of about 40 survey respondents. If

you are willing to participate in the interview process, the researcher would be pleased

to meet you at a time, date and location convenient to you. A telephone conversation

is a feasible alternative should that be preferable to you. We anticipate that between

30 minutes to an hour of your time will be required during the interview process.

Please indicate your willingness by completing the attached form “Expression of

Interest in Interview process”.

THANK YOU AGAIN FOR YOUR VALUED CONTRIBUTION!

Survey: Swinburne’s 2012 IAS/IFRS Convergence in Vietnam

Survey: Swinburne’s 2012 IAS/IFRS Convergence in Vietnam Page 10

© Copyright 2012 Duc Hong Thi Phan

Expression of Interest to participate in an Interview Process

I agree to participate in the interview process involving empirical research on

the convergence process of IAS/IFRS in Vietnam and I am happy to further

explain my answers in the survey.

I also agree that the interview may be recorded by an electronic device on the

condition that no part of the recording is included or made public in any way.

I agree that the research data collected for the study may be published or

provided to other researchers on the condition that anonymity is preserved

and that I or my organisation cannot be identified or otherwise without the prior

express written consent of the participant.

By signing this document, I express my interest in the interview process.

Date:

Signature of Participant: …..…………………………………………………………

Name of Participant: …..……………………………………………………………...

Address: …..…………………………………………………………….....................

Email: …………………………………………………………………………………..

Contact number: …..…………………………………………………………………

Swinburne is an internationally-

recognised provider of quality

education, an institution with a rich

legacy of industry collaborations,

and has a reputation for high-

impact focused research.

Swinburne has been named

amongst the top 3% research-

intensive universities in the world

according to prestigious world

academic ranking lists.

Swinburne University combines

teaching, research and industry

expertise within a supportive real

world learning environment which

produces great professional

outcomes for its graduates.

Swinburne has a reputation for

excellence in applied research in

partnership with industry, business,

government and not-for-profit

organisations.

Swinburne Relevant High Impact Research

Swinburne has been named in

the top 400 in the Times Higher

Education World University

Rankings 2011-2012 and top 450

by the QS World University

Rankings 2011.

QS World University Rankings

2011 also awarded Swinburne 5-

star ratings for graduate

employability, infrastructure and

internationalisation.