sustaining critical sectors of the u.s. defense industrial

TRANSCRIPT

Sustaining Critical Sectors of the U.S. Defense Industrial Base

Barry D. Watts toDD Harrison

C e n t e r f o r s t r a t e g i C a n D B u D g e t a r y a s s e s s m e n t s

Center for Strategic and Budgetary Assessments 1667 K street, nW, suite 900Washington, DC 20006 tel. 202-331-7990 • fax 202-331-8019www.CsBaonline.org

SUSTAINING CRITICAL SECTORS OF THE U.S. DEFENSE INDUSTRIAL BASE

Barry D. Watts and Todd Harrison

2011

© 2011 Center for Strategic and Budgetary Assessments. All rights reserved.

About the Center for Strategic and Budgetary Assessments

The Center for Strategic and Budgetary Assessments (CSBA) is an independent, nonpartisan policy research institute established to promote innovative thinking and debate about national security strategy and investment options. CSBA’s goal is to enable policymakers to make informed decisions on matters of strategy, security policy and resource allocation.

CSBA provides timely, impartial and insightful analyses to senior decision mak-ers in the executive and legislative branches, as well as to the media and the broader national security community. CSBA encourages thoughtful participation in the de-velopment of national security strategy and policy, and in the allocation of scarce human and capital resources. CSBA’s analysis and outreach focus on key questions related to existing and emerging threats to U.S. national security. Meeting these challenges will require transforming the national security establishment, and we are devoted to helping achieve this end.

About the Authors

Prior to joining CSBA in 2002, Barry Watts headed the Office of Program Analysis and Evaluation at the Defense Department (2001–2002). Following retirement from the Air Force in 1986, Mr. Watts was with the Northrop Grumman Analysis Center, which he directed from 1997 to 2001. During his Air Force ca-reer, Mr. Watts flew a combat tour in Vietnam in F-4s, taught logic and philosophy at the US Air Force Academy, served two tours in the Office of Net Assessment, and headed the Red Team in the Air Staff’s Project Checkmate.

Mr. Watts has written on a wide variety of military topics, in-cluding CSBA monographs on the Revolution in Military Affairs (2011); Regaining Strategic Competence (2008 with Andrew Krepinevich); The Case for Long-Range Strike (2008); The Past and Future of the Defense Industrial Base (2008); US Combat Training, Operational Art, and Strategic Competence: Problems and Opportunities (2008); Six Decades of Guided Munitions and Battle Networks (2007); US Fighter Modernization (2007 with Steve Kosiak); Long-Range Strike: Imperatives, Urgency and Options (2005); and The Military Use of Space: A Diagnostic Assessment (2001).

He holds a Bachelor of Science in mathematics from the U.S. Air Force Academy and an Master of Arts in philosophy from the University of Pittsburgh.

Todd Harrison is the Senior Fellow for Defense Budget Studies at the Center for Strategic and Budgetary Assessments.

Mr. Harrison joined CSBA in 2009 from Booz Allen Hamilton, where he supported clients across the Department of Defense, assessing challenges to modernization initiatives and evaluating the performance of acquisition programs. He previously worked in the aerospace industry developing advanced space systems and technologies and served as a Captain in the U.S. Air Force Reserves. Mr. Harrison combines his budgetary, programmatic and engineering experience with a strong background in sys-tems analysis to lead the budget program for CSBA.

Since joining CSBA, Mr. Harrison has authored a number of publications, including The New Guns and Butter Debate, annu-al analysis of the FY 2010, FY 2011, and FY 2012 defense budget request, and Impact of the Wars in Iraq and Afghanistan on the US Military’s Plans, Programs, and Budgets. He is a graduate of the Massachusetts Institute of Technology with both a Bachelor of Science and Master of Science in Aeronautics and Astronautics.

Acknowledgments

The authors would like to thank the CSBA staff for their assistance with this report. Special thanks go to John Speed Meyers for his many contributions and research support; Charlotte Brock, Julie Lascar, and Eric Lindsey for their editorial and production sup-port; and Cutting Edge for their design. The analysis and find-ings presented here are solely the responsibility of the Center for Strategic and Budgetary Assessments and the authors.

conTenTs

vii executive summary

1 chapter 1. Introduction

3 chapter 2. Metrics and scope

5 chapter 3. The emergence of a Permanent Defense Industry

13 chapter 4. Differences beteen Defense Acquisition and a Free Market

19 chapter 5. efficiency Then and now

27 chapter 6. suggestions on Improving efficiency

37 chapter 7. DoD’s Approach To Managing the U.s. Defense Industry

41 chapter 8. Three Acquisition cases

51 chapter 9. sustaining the Vital sectors of the Defense Industrial Base

59 chapter 10. Industrial Mobilization and Attrition

65 Appendix 1. cost-per-Pound for Tactical Aircraft

67 Appendix 2. selected U.s. Force Levels versus U.s. Defense spending, 1986 to 2009

69 Appendix3.Table1withCosts/UnitinConstantFY2011Dollars

71 Appendix4.TheTopTwentyDefenseFirmsWorldwidein2008

75 Appendix5.Top-TierU.S.DefenseIndustryConsolidation,1993to2007

77 Appendix6.The1986DescriptionofDefenseAcquisitionbythePresident’sBlueRibbonCommissiononDefenseManagement

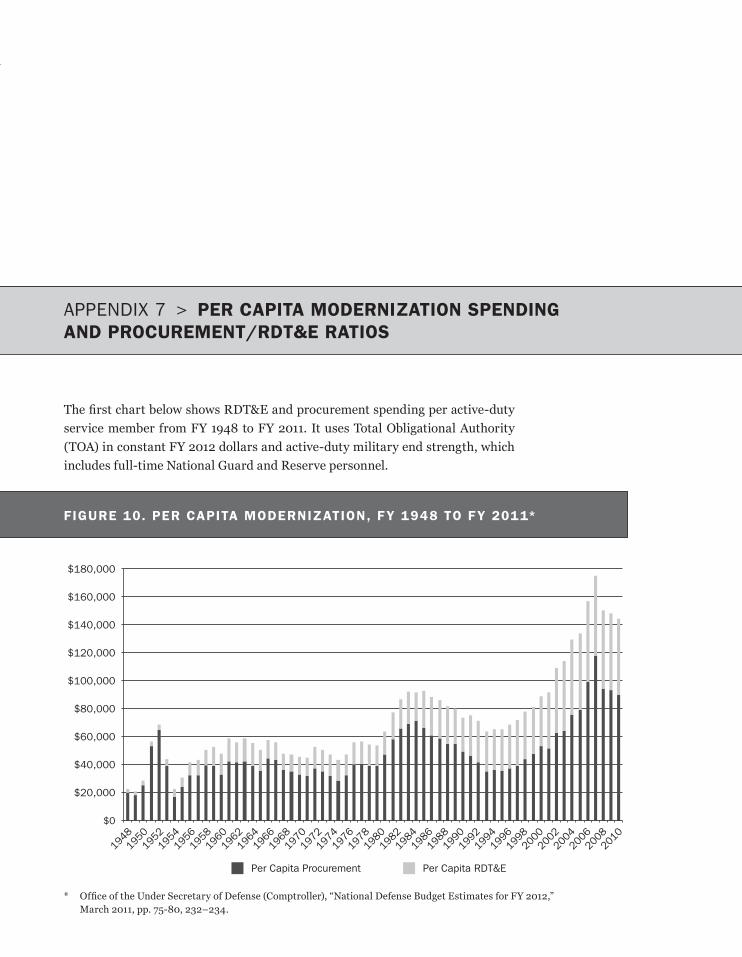

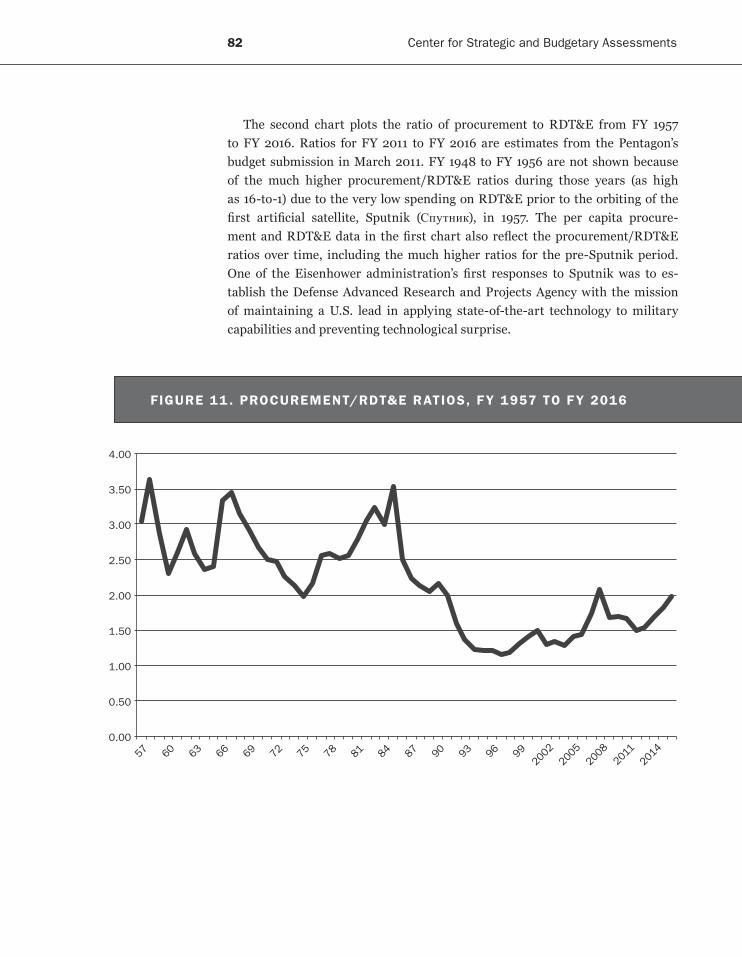

81 Appendix7.PerCapitaModernizationSpendingandProcurement/RDT&ERatios

FIgURES

6 Figure1.Ford’sWillowRunBomberPlantduringWorldWarII10 Figure2.U.S.MonthlyAverageMunitionsProductionbyQuarter,

July1,1940toJuly31,194520 Figure3.UnitCostTrendsinTacticalAircraftandTanks28 Figure4.DoD’sRequirements,Acquisition,andExecutionSystems60 Figure5.TheEmergenceofU.S.-SovietNuclearParity66 Figure6.Cost-per-PoundofSelectedFighterandAttackAircraft68 Figure7.SelectedU.S.ForceLevelsVersusU.S.DefenseSpending73 Figure8.ChineseJ-2075 Figure9.Top-TierU.S.DefenseIndustryConsolidation,1993to200781 Figure10.PerCapitaModernization,FY1948toFY201182 Figure11.Procurement/RDT&ERatios,FY1957toFY2016

TABLES

22 Table1.Cost-ChangeRatiosforTwenty2010MDAPs(NormalizedforInflationandQuantity)

24 Table2.Cost-ChangeRatiosforEighteen1950sAirForcePrograms38 Table3.TopAmericanPrimeDefenseContractorsin200970 Table4.CostChangeRatiosforTwenty2010MDAPS

(InConstantFY2011Dollars)

72 Table5.TheTopTwentyDefenseFirmsWorldwidein2008

ExECUTIvE SUmmARy

From 1812 to World War II, government arsenals produced almost all of the ord-nance for the U.S. Army and a good share of the ordnance and ships for the U.S. Navy. Once the December 1941 Japanese attack on Pearl Harbor had brought the United States into the conflict, however, it soon became apparent that gov-ernment arsenals could not meet the war’s demands for massive quantities of military equipment. To meet this demand, the bulk of U.S. weapons production shifted to private, for-profit companies.

Following World War II, the onset of the Cold War, American leaders’ determi-nation to create an international system centered on U.S. power, and the Korean War combined to create, for the first time in the nation’s history, a permanent defense industrial base. Today as in the 1950s, the U.S. defense industry is com-prised of for-profit companies that develop and produce the weapons used by the U.S. military Services and many allied nations. Despite this system’s recurring problems containing costs and delivering weapons on schedule, it is difficult to disagree with Norman Augustine’s judgment that the modern U.S. defense indus-try helped to win the Cold War and has produced weapons that are the envy of the world’s military forces. Looking to the future, there is every reason to think that the United States’ defense industrial base will continue to be a source of strategic advantage in the decades ahead—if it is adequately maintained.

This monograph focuses on two main questions concerning what is most ac-curately described as the “military-industrial-Congressional” complex. First, does it function like a normal free market in which the forces of supply and de-mand—Adam Smith’s invisible hand—can be relied upon to allocate resources efficiently, encourage innovation, and exhibit the kind of price sensitivity evident in commercial markets such as consumer electronics? Second, what has been the Department of Defense’s approach to sustaining a strong, technologically vibrant and financially successful domestic defense industry?

x center for strategic and Budgetary Assessments

The short answer to the first question is that the U.S. defense industry is a highly regulated sector of the U.S. economy in which the government is both the sole customer—even if it speaks with many discordant voices—and the regula-tor. Fundamental decisions about what weapons to develop, the relative priority to be given to cost, schedule and performance, and the funding to be allocated annually to various weapons programs are the result of complex, often politi-calized, interactions between the military Services and their war-fighting com-munities, the Joint Chiefs of Staff, the Office of the Secretary of Defense, the White House, and Congress. It is, therefore, a serious misunderstanding of the realities of weapons acquisition in the United States to think that the U.S. de-fense industry operates like a normal free market. A classic free market involves many small buyers and many small suppliers, and competition among buyers and suppliers drives prices toward stable, economically efficient equilibrium levels. None of these features resemble the way in which the U.S. defense industrial base functions. Consequently, incremental regulatory and statutory adjustments to defense acquisition based on the presumption that the defense industry operates like a normal free market are not only unlikely to improve efficiency, but have often made things worse.

These conclusions are not new. In a seminal 1962 economic analysis of the weapons acquisition process, Merton Peck and Frederic Scherer reached similar conclusions. In their view, one of the foremost reasons for the non-market struc-ture of the defense industrial base was the much greater uncertainty confronting weapon acquisitions compared to commercial product developments in the rest of the U.S. economy. Indeed, they went a step further, arguing against the very possibility of defense acquisition functioning like a free market. Almost two de-cades later, Jacques Gansler’s 1980 analysis of the defense industry portrayed the continuing belief that the industry functions like a free market as a myth, adding that it was one widely perpetuated by the Defense Department, Congress, and the defense industry itself. Nevertheless, as evidenced by current senior officials in the Defense Department and recent Congressional legislation, this myth contin-ues to be widely accepted in both the Pentagon and Congress.

Much of the reason for the persistence of belief in the free-market character of the military-industrial-Congressional complex stems from the understandable frustration over the continuing inability of the requirements, acquisition and budget execution systems to control cost and schedule. The B-2 bomber, of which only twenty-one were eventually procured, ended up with a unit cost over $2 billion. Currently, unit acquisition cost growth in the F-35 Joint Strike Fighter program is over 50 percent (using constant dollars), the schedule has slipped considerably for all three variants, and the end of these problems is not yet in sight. Such examples inevitably lend credence to the impression that cost over-runs, schedule slippage and performance shortfalls in major defense acquisition programs are growing steadily worse.

Sustaining Critical Sectors of the U.S. Defense Industrial Base xi

Surprisingly, this impression, like the conviction that the defense industry operates like a free market, also appears to be something of a myth. Based on a RAND analysis of a number of Air Force acquisition programs during the 1950s, cost overruns were, on average, greater then than they are today and schedule slippage was not appreciably worse. Nevertheless, it is natural to suppose that just as competition and innovation have steadily driven down the costs of com-puting and commercial electronics since the 1960s, market forces can also im-prove the efficiency of defense acquisition. Indeed, a recurring recommendation has been that “major improvements” could be made in defense acquisition “by emulating the model of the most successful industrial companies.”1

Without question, there is a great deal of inefficiency, if not waste, in the U.S. defense industry (although outright fraud has been, and remains, rare). The im-pulse to try to achieve greater efficiency is, therefore, understandable, and this paper advances some modest suggestions for improvement. However, these sug-gestions are offered in the context of the regrettable conclusion that the U.S. de-fense industry does not now, and is unlikely ever to, function like a free market. It is natural for American policy makers to hope that Adam Smith’s invisible hand will improve defense acquisition. Unfortunately, while one can see why this hope has endured, the underlying assumption that the U.S. defense industry functions like a free market is simply false.

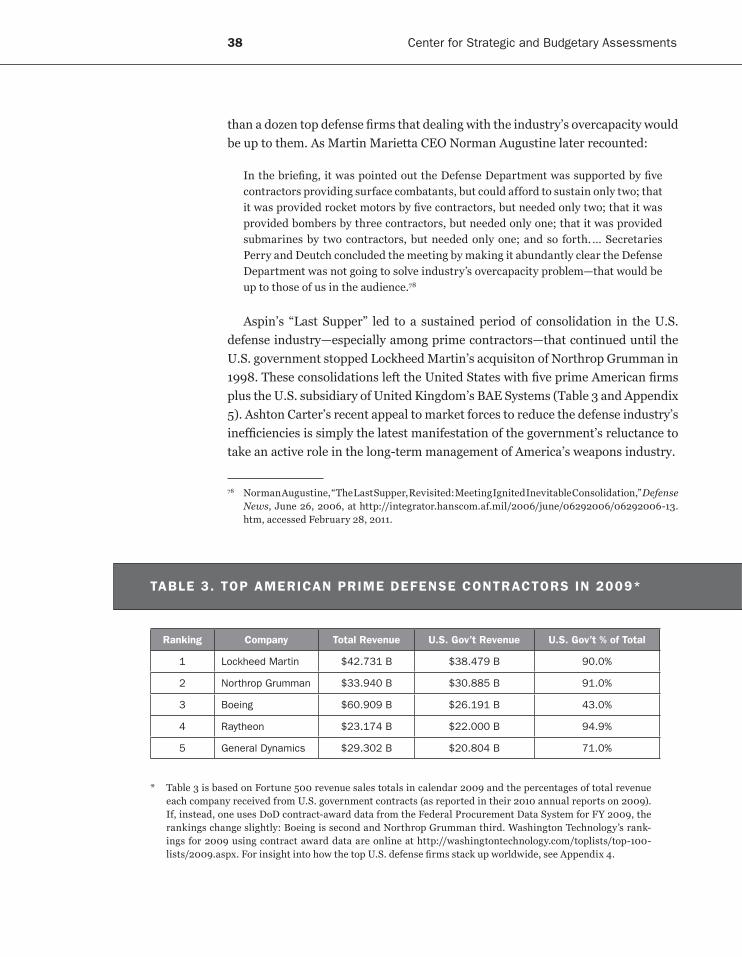

Equally important to recognize, though, is that the issue of the defense in-dustry’s efficiency is separate from that of whether the U.S. government ought to have a long-term strategy for sustaining the vital elements of the nation’s defense industrial base. Since the emergence of a standing military-industrial-Congressional complex in the 1950s, the U.S. government has shown little in-clination to develop—much less to pursue over any period of time—a coherent, long-term strategy for maintaining a healthy domestic defense industry. Instead, the Pentagon and the rest of the federal government have generally taken a laissez-faire, hands-off approach. There is no better illustration of this than the 1993 dinner at which Secretary of Defense Les Aspin, Deputy Secretary William Perry, and Under Secretary for Acquisition and Technology John Deutch ex-plained to the chief executive officers of more than a dozen top U.S. defense firms that the problem of the defense industry’s substantial overcapacity precipitated by the Cold War’s end would be left up to them to solve.

There are a number of reasons why this hands-off approach to managing the U.S. defense industry has persisted through the first decade of the twenty-first century. One, of course, is the government’s understandable reluctance to pick winners and losers—despite the fact that every acquisition decision government

1 President’s Blue Ribbon Commission on Defense Management, A Quest for Excellence: Final Report to the President, June 1986, p. 52. David Packard, a co-founder of Hewlett Packard, chaired this commission.

xii center for strategic and Budgetary Assessments

officials make does so by influencing the shape, structure, and composition of the industry. Another reason for the U.S. government’s laissez-faire approach is the belief that the defense industry will always be there, ready and able to produce whatever weapons the military Services require. Unfortunately, this belief ap-pears increasingly questionable. U.S. defense firms are, after all, for-profit en-terprises. They have shareholders or owners who expect them to make money. As such they have no economic incentive to continue funding out of their own pockets design capabilities for military-unique product lines in which they have little hope of even having a near-time opportunity to compete for a new program, much less of winning one.

The foreseeable erosion of design capabilities for military-unique products means, at a minimum, that as new starts for major weapons systems grow fewer and further between, the U.S. government’s options will increasingly narrow to one or two prime contractors, as has already happened with tactical fighters and reconnaissance satellites. It is not unrealistic to foresee a day in which the U.S. defense industry no longer possesses the design or production capabilities for certain weapons systems. Indeed, this has already happened to the United Kingdom in the case of nuclear attack submarines. The Royal Navy set out in 1997 to develop a new class of nuclear attack submarines, but discovered some five to six years into the program that neither the contractor, BAE Systems, nor any other British firm had the requisite design and production skills to produce the Astute-class submarines. The British were able to turn to General Dynamics Electric Boat in the United States for the missing expertise. But if the Pentagon one day found itself in the same situation with a major weapons system, to whom would it turn?

The current situation regarding sustainment of the U.S. defense industrial base is, therefore, clear. The United States has not pursued an overall strategy for preserving its domestic defense infrastructure since this industry emerged in the 1950s as a permanent sector of the U.S. economy. Gansler’s observation in 1982 that the United States is the only nation in the world that does not treat its defense industry as a valuable national resource remains true today. However, in light of the fiscal austerity likely to constrain U.S. spending on national security in the years immediately ahead and the growing complexities and dangers in the nation’s security environment, a long-term strategy seems imperative if the vital sectors of the defense industry are to be preserved. The simple truth is that for-profit U.S. defense companies are not at all likely to preserve the capabilities the military Services will need in areas where they have no defense business. If the vital sectors of the defense industrial base are to be maintained, the U.S. govern-ment will need to develop and implement a strategy of some sort.

A plausible guiding policy for sustaining the U.S. defense industrial base as a national asset and enduring source of advantage can be stated as follows:

Sustaining Critical Sectors of the U.S. Defense Industrial Base xiii

The United States’ defense industrial base strategy should ensure the preserva-tion of those few sectors that are currently critical to American national security, adding over time any emerging sectors that become critical, and ruthlessly under-funding or jettisoning any sectors that cease to be critical.

In other words, the overarching policy would be the adaptive sustainment of those elements of the defense industrial base that are truly important to retain.

The foremost point to be made about this broad policy is that of the perhaps two or three dozen sectors into which the defense industrial base can be logi-cally segmented, the number of strategically critical sectors cannot exceed five to seven. Good strategy is always about choice—in this case favoring the genuinely vital sectors of the defense industry while, more importantly, neglecting or ig-noring the rest. An industrial-base “strategy” that seeks to preserve every sector deemed desirable by any of the war-fighting communities across the four military Services, the prime defense contractors, or their Congressional allies is not in fact a strategy and will not succeed. Indeed, even within the truly critical sectors, not every design or production capability will merit preservation. The sine qua non of the proposed guiding policy, then, is the imperative to make hard choices. Which five (or six, or seven) sectors of the U.S. defense industrial base are truly critical to national security, and which elements within those sectors are themselves im-portant enough to justify preservation? This is the essential question that must be answered to underpin the development and implementation of a coherent, long-term strategy to preserve the vital core of the U.S. defense industry.

Reaching consensus on a meaningful answer to this question is a formida-ble challenge even within the Department of Defense, much less between the Pentagon and Congress. But even if consensus were to be achieved, there would remain other strategic questions about the defense industrial base. Once the Soviet Union achieved rough strategic-nuclear parity with the United States around 1970, the need to continue paying for surge or mobilization capacity that would be lost in a nuclear exchange came to been seen as an avoidable drain on defense resources. This perception was reinforced by the extremely modest attrition that U.S. forces experienced in the 1991 Persian Gulf War and subse-quent episodes of high-intensity combat operations (Afghanistan in 2001–2002 and Iraq in 2003). One further question, then, is whether surge or mobilization might be needed against an opponent with the size, strategic depth, and stay-ing power of China. Whatever the answer, the U.S. defense budget is entering another period of austerity, reinforced by the global financial crisis and the un-checked growth of U.S. government debt. While there may be little agreement on how much modernization funding (research and development plus procurement) the Pentagon will need annually to sustain its domestic industrial base, no strat-egy for preserving the American defense industry is likely to succeed unless it is adequately funded.

“We must be the great arsenal of democracy.”

— Franklin D. Roosevelt, December 29, 19402

“The U.S. defense industry helped to win the Cold War.”

— Norman Augstine, 19973

“The fundamental starting point is the understanding that we in DOD do not make our weapons systems. They come from our defense industry. And these weapons systems are, second only to our superb men and women in uniform, what makes our military power unrivaled and what provides the buttress of national and interna-tional securtity. A strong, technologically vibrant and financially successful defense industry is therefore in the national interest.”

— Ashton Carter, February 9, 20114

What is the fundamental economic character of the permanent defense indus-try that emerged in the United States during the 1950s? What was it about this industry that provoked President Dwight Eisenhower, in his January 1961 fare-well address, to warn against the acquisition of unwarranted influence by the

2 Franklin Delano Roosevelt, fireside radio chat on national security, delivered December 29, 1940, at http://www.americanrhetoric.com/speeches/fdrarsenalofdemocracy.html, accessed February 8, 2011. This website includes an audio mp3 of Roosevelt’s speech. The phrase “arsenal of democ-racy” originated with the American playwright Robert Sherwood and was suggested to Roosevelt by Harry Hopkins.

3 Norman R. Augustine, “Reshaping an Industry: Lockheed Martin’s Survival Story,” Harvard Business Review, May–June 1997, p. 83.

4 Ashton B. Carter, “The Defense Industry Enters a New Era,” prepared remarks at the Cowen Investment Conference, New York, NY, February 9, 2011, p. 2.

cHAPTeR 1 > INTRODUCTION

2 center for strategic and Budgetary Assessments

military-industrial complex?5 Does the government-industry weapons acquisi-tion process function anything remotely like a classic free market? How efficient or inefficient has defense acquisition been over time, and how do the complex relations between the Office of the Secretary of Defense (OSD) in the Department of Defense (DoD), the military Services, Congress, and private weapons contrac-tors affect metrics such as cost and schedule? Since the 1950s, has the U.S. gov-ernment ever attempted any systematic, long-term management of the country’s defense industrial base as a source of long-term strategic advantage and, if not, what hard choices would be required to develop and implement a strategy aimed at sustaining the defense industry’s critical capabilities?

These are the questions that this paper addresses. They highlight the first-order issues that must be confronted if one is to think productively about what is most accurately labeled the “military-industrial-Congressional complex.”6

Nevertheless, these issues—especially the non-market structure of the U.S. de-fense industry—are also widely ignored in public and policy debates over the per-ceived inefficiency, waste, and corruption of the U.S. weapons acquisition process.

5 Dwight Eisenhower, “Farewell Radio and Television Address to the American People,” January 17, 1961, at http://www.eisenhower.archives.gov/all_about_ike/Speeches/Farewell_Address.pdf, accessed January 24, 2011. In 1959, Eisenhower had decried what he termed a “munitions lobby” in response to full-page ads for competing products by defense firms. Merton J. Peck and Frederic M. Scherer, The Weapons Acquisition Process: An Economic Analysis (Boston, MA: Harvard University, 1962), p. 242.

6 Eisenhower’s farewell address used the term “military-industrial complex.” However, in 1993 then Brigadier General Andrew J. Goodpaster, who served as staff secretary and defense liaison officer to Eisenhower from 1954 to 1961, told Davis that the president had elected to strike the word “Congressional” just minutes before he spoke (Thomas J. Davis, “The Military Industrial Congressional Complex,” email to Barry Watts, February 25, 2011).

What basic measures or metrics should be used to assess such core concerns as the relative efficiency of weapons acquisition and the U.S. defense industrial base? In 1959, two RAND analysts advanced four criteria for judging the success of military acquisition programs:

1. Costs (development and production);

2. Time of Availability (initial operational availability);

3. System Performance (in the sense of all the qualities that contribute to the effectiveness of a military system within its intended domain); and

4. Utility (the broader military value of the weapon system over and above whether it meets its specific performance goals).7

The first three criteria are relatively quantifiable. The Defense Department regularly publishes Selected Acquisition Reports (SARs) that have baseline and current costs for major defense acquisition programs (MDAPs).8 In the case of a troubled program such as the F-35 Joint Strike Fighter (JSF), the draft SAR published in March 2010 contains extensive cost data, descriptions of unclassi-fied performance objectives, and the schedule of projected annual procurement

7 A. W. Marshall and W. H. Meckling, “Predictability of the Costs, Time, and Success of Development,” RAND P-1821, revised December 11, 1959, p. 4.

8 SARs from June 2010 back to 1973 can be accessed at http://www.acq.osd.mil/ara/am/sar/. Currently an MDAP is a program designated as such by the Under Secretary of Defense for Acquisition, Technology, and Logistics (USD(AT&L)), or estimated by the USD(AT&L) to require an eventual total expenditure for Research, Development, Test and Evaluation (RDT&E) of more than $365 million in Fiscal Year (FY) 2000 constant dollars or, for procurement, of more than $2.19 billion in FY 2000 constant dollars.

cHAPTeR 2 > mETRICS AND SCOpE

4 center for strategic and Budgetary Assessments

quantities through 2035.9 The fourth criterion, overall utility, is more qualitative. A weapon system could completely meet or exceed its detailed performance goals when fielded but still be obsolesced by external developments. The rapid emer-gence during the 1950s of thermonuclear warheads small and light enough to be delivered over intercontinental distances by ballistic missiles led to the early retirement of air-breathing nuclear cruise missiles such as the Navy’s SSM-N-8 Regulus and the Air Force’s SM-62 Snark.10 Soviet intercontinental ballistic mis-siles (ICBMs) also eroded the utility of the F-102 and F-106 interceptors for de-fending the United States against a Soviet nuclear attack irrespective of their ability to intercept Long-Range Aviation’s nuclear bombers.

By and large, the U.S. government “customer” has generally emphasized per-formance or schedule—and sometimes both—over cost. The Corona program to develop a reconnaissance satellite provided dramatically better strategic recon-naissance deep inside the Soviet Union than manned aircraft could, and became extremely urgent after Francis Gary Power’s U-2 was shot down by S-75 Dvina surface-to-air missiles near Degtyarsk on May 1, 1960. Similarly, during the 1950s the perceived imperative to keep up with the Soviets in strategic-nuclear forces gave overriding urgency to early U.S. ICBM programs such as Atlas and Titan.11 In most cases, though, U.S. acquisition programs have given first priority to performance with cost in third place. The B-2 and F-22 illustrate programs in which performance was accorded first priority, schedule second, and cost third.

The Defense Department procures many things besides advanced weapon systems. However, everyday items such as jet fuel, office computer equipment, and food for military dining facilities are rarely the focus of acquisition debates. Thus, like Merton Peck and Frederic Scherer’s classic 1962 economic analysis of the U.S. weapons acquisition process, this paper concentrates on the “conception, development, and production of technically advanced weapons” for the ultimate use of the U.S. military and its close allies.12

9 Defense Acquisition Management Information Retrieval (DAMIR), “Selected Acquisition Report (DRAFT SAR): F-35, As of December 31, 2009,” RCS DD-AT&L(Q&A)823-198, March 26, 2010, pp. 10–12, 14–16, 26–27. The earliest DAMIR document on the JSF program is dated 1996.

10 Marshall and Meckling, “Predictability of the Costs, Time, and Success of Development,” p. 5.11 In 1955 President Eisenhower designed the U.S. ICBM project “a research and development

program of the highest priority above all others”—Neil Sheehan, A Fiery Peace in a Cold War: Bernard Schriever and the Ultimate Weapon (New York: Random House, 2009), p. 299.

12 Peck and Scherer, The Weapons Acquisition Process, p. 3. With the exception of Chapter 9’s attempt to model cost, time, and quality relationships in the absence of technical and bureau-cratic uncertainties, this massive study by the research division of Harvard’s Graduate School of Business Administration remains worthy of study even today.

From the War of 1812 until World War II, government arsenals produced almost all of the ordnance for the U.S. Army and a good share of the ordnance and ships for the U.S. Navy.13 However, the arsenals and shipyards the government main-tained in peacetime usually lacked the capacity to meet the increased demands of wartime. Under the arsenal system, private firms generally took up the slack during conflicts such as the American Civil War and then downsized or returned to commercial business after the fighting ceased. This “feast-or-famine” pattern persisted until World War II.

From 1942 to 1945, the “bulk” of U.S. weapons production “in all fields shift-ed to private firms.”14 Roosevelt’s “Arsenal of Democracy” was largely built on the United States’ existing industrial base. The wartime distribution of defense contracts “more or less followed the existing pattern of manufacturing and the major industrial states—Michigan, Pennsylvania, Ohio, and Indiana—ranked high in prime contract awards.”15 Wartime aircraft production illustrates both the shift to private firms and the role played by automobile manufacturers. After the Japanese attack on Pearl Harbor brought the United States into the war, the rapid growth of demand for aircraft exceeded the American aircraft indus-try’s production capacity. In 1940, the United States produced less than 2,900 bombers and fighters; in 1944, the total was nearly 74,000 (35,003 bombers and 38,873 fighters).16 As a result, automobile companies—primarily Ford, General Motors, and Fisher Body—filled the capacity gap by building or converting plants

13 Peck and Scherer, The Weapons Acquisition Process, p. 98. 14 Peck and Scherer, The Weapons Acquisition Process, p. 99. 15 Peck and Scherer, The Weapons Acquisition Process, p. 112. 16 Alan L. Gropman, Mobilizing U.S. Industry in World War II (Washington, DC: National Defense

University, August 1996), McNair Paper 50, p. 96. From 1940 through 1945, the United States produced 98,431 bombers and 100,708 fighters (ibid.).

cHAPTeR 3 > THE EmERGENCE OF A pERmANENT DEFENSE INDUSTRy

6 center for strategic and Budgetary Assessments

to produce entire planes, major aircraft subassemblies, tanks, anti-aircraft guns, etc.17 In the case of heavy bombers, the 3.5-million-square-foot plant Ford built at Willow Run, Michigan, produced 8,685 of the 18,482 B-24s built during World War II.18 After the war, however, the automobile companies largely exited the defense business.

The emergence, for the first time in U.S. history, of a standing U.S. defense industry that existed in peacetime as well as wartime resulted from a confluence of factors. One, of course, was the shift from arsenals to private firms and univer-sities that occurred during World War II. Developments such as radar, proximity fuses, electronic computers, and the atomic bomb were beyond the capabilities of government arsenals. As Irving Stewart, Vannevar Bush’s deputy director at the wartime Office of Scientific Research and Development (OSRD), wrote in 1948:

Previous efforts to bring civilian science into the program of weapon development were based on the theory that the Services would know what they needed and would ask the scientists to aid in its development. Modern science has progressed to the point where the military chieftains were not sufficiently acquainted with its

17 Peck and Scherer, The Weapons Acquisition Process, p. 191. General Motors’ Eastern Aircraft Division produced FM Wildcats (F4Fs) and TBM Avengers (TBF Avengers). By August 1945, Fisher Body had delivered, among other wartime products, 21,000 tanks, major subassemblies for some 10,000 B-25s and B-29s, 422,000 aircraft instruments, 3,400 anti-aircraft guns, 550,000 shells, and thousands of diesel crankcases for submarines.

18 Jenny Nolan, “Willow Run and the Arsenal of Democracy,” The Detroit News, January 28, 1997, at http://apps.detnews.com/apps/history/index.php?id=73, accessed February 7, 2011.

FIGURE 1 . FORD’S WILLOW RUN BOmBER pLANT DURING WORLD WAR I I

source: U.s. Army signal corps

Sustaining Critical Sectors of the U.S. Defense Industrial Base 7

possibilities to know for what they might ask with a reasonable expectation that it could be developed. The times called for a reversal of the situation, namely letting men who knew the latest advances in science become more familiar with the needs of the military in order that they might tell the military what was possible in sci-ence so that together they might assess what should be done. It was this conception which Bush and his colleagues sold to President Roosevelt and to which General Marshall and Admiral Stark gave their blessing …19

The atomic bomb readily illustrates Stewart’s point. “World War II,” Vannevar Bush later observed, “was the first war in human history to be affected decisively by weapons unknown at the outbreak of hostilities.”20

These lessons, which argued powerfully against returning to an arsenal sys-tem, were further reinforced by episodes such as the dismal performance of the Newport Torpedo Station’s Mark-14 torpedo. The Newport facility developed the Mark-14 during the 1930s, and the Mark-14 was the principal torpedo used by U.S. submarines during World War II. However, early in the war operational ex-perience in the Pacific began to reveal major deficiencies in the weapon. Tests conducted by operational submarines based in Australia in mid-1942 confirmed what many submarine skippers had begun to suspect: the Mark-14 ran an aver-age of 11 feet deeper than its set depth.21 By April 1943, further tests and combat experience revealed that the Mark-14’s magnetic-influence exploder was defective and, by mid-1943, it became clear that the Mark-14’s contact exploder was also prone to failure when the impact angle approached 90 degrees, a perfect shot.22 Due to an unfortunate confluence of personalities and bureaucratic inertia, it took twenty-one months to isolate and correct all of the Mark-14’s defects—less time than it took the OSRD to develop and field the first acoustic homing torpedo, the Mark-24, from scratch.23 Part of the reason it took so long to correct the Mark-14’s defects was that each problem masked the remaining ones. Nevertheless, long

19 Irvin Stewart, Organizing Scientific Research for War: The Administrative History (Boston, MA: Little, Brown, 1948), p. 6. OSRD was created formally by Executive Order 8807 on June 28, 1941. It largely superseded the earlier National Research Defense Committee, which had been established under Vannevar Bush in July 1940 “to coordinate, supervise, and conduct scientific research on the problems underlying the development, production, and use of mechanisms and devices of warfare” in the United States. OSRD was given almost unlimited access to funding and resources, and Bush reported only to President Roosevelt. It was discontinued in December 1947.

20 Vannevar Bush in Stewart, Organizing Scientific Research for War, p. ix. 21 Clay Blair, Jr., Silent Victory: The U.S. Submarine War against Japan (New York: Bantam Books,

1975), pp. 160, 274–278, 292; also, Frederick J. Milford, “U.S. Navy Torpedoes,” Pt. 2, “The Great Torpedo Scandal, 1941–43,” The Submarine Review, October 1996, pp. 83–87.

22 Blair, Silent Victory, pp. 412–415, 437–438; also, Milford, Pt. 2, “The Great Torpedo Scandal, 1941–43,” pp. 87–90.

23 Blair, Silent Victory, pp. 20, 140–141, 206, 216, 225–227, 280–281, 348, 367, 401–404, 413–415. Bell Lab designed the Mark-24 and Western Electric produced it. The development began in December 1941 and the torpedo was deployed operationally in March 1943 (A. C. Dickieson, “Early ‘Smart Bombs’ at Bell Labs,” reprinted from Vintage Electrics, Vol. 3, No. 1, at http://www.smecc.org/early_’smart_bombs’_at_bell_labs.htm, accessed February 8, 2011).

8 center for strategic and Budgetary Assessments

after operational units began experiencing problems with the weapon on combat patrols, the Navy’s Newport Torpedo Station resisted realistic testing.24 “The scan-dal was not that there were problems in what was then a relatively new weapon, but rather the refusal by the ordnance establishment [ashore] to verify the prob-lems quickly and make appropriate alterations.”25 As Clay Blair documented in 1975, each of the Mark-14’s major defects was largely “discovered and fixed in the field—always over the stubborn opposition of the [Navy’s] Bureau of Ordnance.”26

While the Mark-14 torpedo scandal was small potatoes compared to decid-ing whether an operational atomic bomb could be fielded, both issues reflected the growing intrusion of science into the weapon acquisition process during the Second World War. A striking feature of American wartime experience “was the extent to which scientists, temporarily in government service, acted as the promoters for new weapons, made the important development decisions, and participated in their administration.”27 The success of operations research in ap-plying mathematics and scientific methods to military problems led the newly independent U.S. Air Force to establish the nation’s first “think tank,” the RAND Corporation, in 1948.28 Over the next decade, virtually all the “basic ideas and philosophies about nuclear weapons and their use” were generated by RAND’s civilian strategists.29 Thus, the wartime collaboration between the military, in-dustry, and scientists not only continued after 1945 but also reinforced the shift from arsenals to private defense firms. By 1958, arsenals carrying out activities comparable to those of private defense contractors were estimated to account for less than 10 percent of the resources devoted to new weaponry.30

Three main externalities encouraged the development of a permanent defense industrial base centered on for-profit defense companies. First and foremost was the onset of the Cold War, whose central feature was the U.S.-Soviet competition in nuclear arms. A second catalyst was the determination of U.S. post-war lead-ers—including President Harry Truman, George Kennan, Dean Acheson, George Marshall and Paul Nitze—to “create an international system with American

24 Milford, Pt. 2, “The Great Torpedo Scandal, 1941–43,” p. 82.25 Milford, Pt. 2, “The Great Torpedo Scandal, 1941–43,” p. 83.26 Blair, Silent Victory, p. 439; Milford, Pt. 2, “The Great Torpedo Scandal, 1941–43,” p. 92. 27 Peck and Scherer, The Weapons Acquisition Process, p. 177.28 General H. H. “Hap” Arnold, who commanded the Army Air Forces during World War II, directed

the creation of Project RAND, which later became the RAND Corporation. His reasons were best captured in a postwar report he wrote to Henry Stimson: “During this war the Army, Army Air Forces, and the Navy have made unprecedented use of scientific and industrial resources. The conclusion is inescapable that we have not yet established the balance necessary to insure the con-tinuance of teamwork among the military, other government agencies, industry, and the universi-ties. Scientific planning must be years in advance of the actual research and development work.” (“The Origins of RAND,” at http://www.rand.org/about/history.html, accessed March 9, 2011).

29 Bernard Brodie, “The Development of Nuclear Strategy,” International Security, Spring 1978, p. 67. 30 Peck and Scherer, The Weapons Acquisition Process, p. 98.

Sustaining Critical Sectors of the U.S. Defense Industrial Base 9

power at its center” in order to minimize the possibility of major power conflicts as destructive as the two world wars had been.31 And, third, the North Korean dictator Kim Il-sung’s invasion of South Korea in June 1950 precipitated a rapid increase in military spending.

There were, of course, other factors that served to foster both the creation of a permanent defense industrial base and the eclipse of government arsenals. One was the “rise of missiles and electronics and the decline of ordnance, ships, and, to a more limited extent, aircraft”; these developments constituted a dramatic change in the weapons business, and witnessed the migration of defense produc-tion from the pre-World War II industrial states to California, Texas, Washington and rejuvenated defense firms in the New England states.32 California, for ex-ample, went from 8.7 percent of defense contracts in 1945 to 24 percent in 1959–1960.33 The other important post-World War II trend was the declining role of large-quantity production.34 During World War II the United States produced nearly 35,000 heavy bombers (12,731 B-17s, 18,482 B-24s, and 3,970 B-29s). Subsequently, the Air Force procured 2,032 B-47s during the early 1950s, 744 B-52s during the late 1950s and early 1960s, 100 B-1Bs during the 1980s, and 21 B-2s during 1994–2000.35 This decline in production quantities went hand in hand with an increasing emphasis on advanced-technology weaponry, quality, and state-of-the-art performance.

There was, then, a confluence of trends and forces that reshaped the composi-tion and structure of defense acquisition in the United States after World War II. The shift from arsenals to private defense contractors has proved permanent. Quality has become ascendant over quantity, and a peacetime defense industry has become a permanent feature of the U.S. economy, continuing even after the collapse of the Soviet Union.

Largely forgotten in current discussions of the U.S. defense industry is the is-sue of mobilization for protracted conflict. President Roosevelt’s pre-1942 efforts to mobilize the U.S. economy were resisted by Congress and uncoordinated. As a result, one of the lessons that the U.S. government drew from World War II was the need for a permanent, rationalized mobilization apparatus. Toward this end, in December 1950 President Harry Truman established the Office of Defense

31 Robert Kagan, “The Price of Power,” The Weekly Standard, January 24, 2011, at http://www.weeklystandard.com/articles/price-power_533696.html?nopager=1, accessed February 8, 2011.

32 Peck and Scherer, The Weapons Acquisition Process, pp. 110, 112. For insight into firms such as Hughes and TRW that were at the forefront of the growth in defense electronics and missiles in the Los Angeles basin, see Thomas C. Reed, At the Abyss: An Insider’s History of the Cold War (New York: Ballantine, 2004), pp. 61–68, 125.

33 Peck and Scherer, The Weapons Acquisition Process, p. 111. 34 Peck and Scherer, The Weapons Acquisition Process, p. 161. 35 The same trend toward smaller and smaller quantities are evident in fighter aircraft, surface naval

combatants, nuclear submarines and other major weapon systems.

Quality has become

ascendant over

quantity, and a

peacetime defense

industry has become

a permanent feature

of the U.S. economy,

continuing even

after the collapse of

the Soviet Union.

10 center for strategic and Budgetary Assessments

Mobilization or ODM (which became the Office of Civil and Defense Mobilization in 1958). Truman appointed General Electric’s president Charles E. Wilson as ODM’s first director.36 In this position Wilson was a member of the Executive Office of the President, and the nineteen mobilization agencies eventually created within ODM had the authority to control every aspect of the U.S. economy. During the Korean conflict Wilson became so powerful that he was referred to as “co-president.” After the ceasefire in Korea, though, ODM’s role in the U.S. economy became less intrusive. Most of ODM’s production, wage and price controls were relaxed by the fall of 1953. While ODM was initially powerful under Wilson, the organization eventually fell victim to the nuclear competition between the United States and Soviet Union. As the Soviets began to field intercontinental missiles

36 After leaving ODM, Wilson served as Eisenhower’s defense secretary from 1953 to 1957.

FIGURE 2. U.S. mONTHLy AvERAGE mUNITIONS pRODUCTION By QUARTER, JULy 1 , 1940 TO JULy 31 , 1945

Aircraft

Guns and Fire Control

Ammunition

Combat and Motor Vehicles

Communication and Electronic Equipment

Other Equipmentand Supplies

Ships

Bill

ions

of S

tand

ard

Mun

ition

s D

olla

rs

Aircraft23.9%

Guns and Fire Control

5.8%

Ammunition10.6%

Combat and Motor Vehicles

11.6%

6

4

2

03Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q

1940 1941 1942 1943 1944 1945

Comm. and Elect. Equip.

5.7%

Other Equipmentand Supplies

20.5%

Ships21.9%

source: Wartime Production Achievements and the Reconversion Outlook (Washington, Dc: War Production Board, 1945), p. 105”

Sustaining Critical Sectors of the U.S. Defense Industrial Base 11

able to deliver megaton-class thermonuclear warheads throughout the United States, interest in traditional defense mobilization faded in the belief that after a nuclear exchange there would be little industrial capacity left to mobilize. ODM was consolidated into the Federal Civil Defense Administration in 1958, and in July 1961 the Office of Civil and Defense Mobilization ceased to exist. Thus, the 1950s not only witnessed the emergence of a standing defense industrial base but a gradual decline in attention to industrial mobilization.

In 1980, Jacques Gansler portrayed the widespread presumption that market forces—Adam Smith’s invisible hand37—could be relied upon to produce eco-nomic efficiency and strategic responsiveness in the U.S. defense industry as a dangerous myth. Early in The Defense Industry, he highlighted some thirty ways in which the structure of defense acquisition in the United States diverged from a free market involving many small buyers and sellers, with buyer choices be-ing based on price and prices being set by the efficient interplay of supply and demand.38 By contrast, the combination of a single buyer (the U.S. government), a few very large prime contractors in each segment of the industry, and a small number of extremely expensive weapons programs constituted a structure for doing business that was altogether different from a classic free market.39

In considering the conduct and performance of the defense industry it is critically important that one recognize the great degree of regulation present, in spite of the fact that defense is not normally listed as a regulated industry. This regulation is unique in kind, in that the regulator is also the buyer. With so much involvement on the part of the buyer in the operation of the supplier, there can be no free market at work. Yet the Department of Defense, the defense industry, and Congress continue to perpetuate the myth that a free market is in operation, and count on the invisible hand of this market to produce economic efficiency.40

37 Adam Smith first used the term “invisible hand” to suggest that market forces lead the rich to contribute to the wealth of all by pursuing their own narrow self interests in his 1759 The Theory of Moral Sentiments—Adam Smith, D. D. Raphael and A. L. Macfie (eds.) The Theory of Moral Sentiments (Indianapolis, IN: Liberty Fund, 1984), Part IV, Chapter I, pp. 184–185. Smith again invoked the invisible hand to make the same point in his 1776 The Wealth of Nations (see Book 4, Chapter II).

38 Jacques S. Gansler, The Defense Industry (Cambridge, MA, & London: MIT Press, 1980), pp. 30–31.39 Gansler, The Defense Industry, p. 69. 40 Gansler, The Defense Industry, p. 92.

cHAPTeR 4 > DIFFERENCES BETEEN DEFENSE ACQUISITION AND A FREE mARkET

14 center for strategic and Budgetary Assessments

The dominant characteristic of the U.S. defense industry was, therefore, “the lack of competition for most of the dollars involved.”41 True, prior to source selection, there was fierce rivalry between prime contractors to win the initial development contracts for new weapon systems. But once source selection had been made,

the remainder of the program—product development, which may last over ten years, and then long-term production and product support—is normally conducted in a sole-source environment, where the contractor is essentially in a monopoly position and the government is dependent upon that producer for military equipment that it badly wants and for which it will usually pay whatever is asked.42

Gansler therefore concluded that “well over 90 percent of the defense contract dollars were not awarded on the basis of price competition or in the presence of any incentives that would drive down costs.”43 Furthermore, he observed, most government policies, DoD acquisition regulations, and Congressional statutes aimed at improving acquisition were predicated on the presumption that it is a free market and, as a result, “have not had the desired effects.”44 Recurring acquisition reform efforts had either maintained the non-free-market structure that emerged in the 1950s or had actually made things worse.

Gansler, of course, was not the first to notice the fundamentally non-market character of the U.S. defense industrial base. In 1962, this insight was a ma-jor finding of Merton Peck and Frederic Scherer’s The Weapons Acquisition Process.45 They concluded that the uncertainties and risks embedded in the weapons acquisition process not only made it unique, but vitiated the use of free-market concepts such as “competition,” “price,” “buyer,” and “seller” in thinking about how the U.S. defense industry functioned:

Payments to contractors are on the basis of cost incurred, yet competitive prices are an essential feature of a market system. In weapons acquisition the buyer exercises control over sellers through the auditing of costs and other activities that involve the government in the internal management of its contractors. Yet another essential element of a market system is that the buyers exert their control only by distributing their patronage among competing sellers. Similarly, while in a market system the

41 Gansler, The Defense Industry, p. 92. 42 Gansler, The Defense Industry, p. 93. 43 Gansler, The Defense Industry, p. 93. 44 Gansler, The Defense Industry, p. 96. For empirical analysis of the burden statues and regula-

tions impose on DoD program offices, see Jeffrey A. Drezner, et al., Measuring the Statutory and Regulatory Constraints on DoD Acquisition: An Empirical Analysis (Santa Monica, CA: RAND, MG569, 2007). Surprisingly, this research found that compliance activities constituted less than 5 percent of the total staff time available and had few adverse consequences (ibid, pp. 56–57).

45 Because a great deal of the basic source material was classified, Assistant Secretary of Defense (Installations and Logistics) Perkins McGuire and his successor, Thomas Morris, provided the staff for this study with clearance and “need to know” in return for submitting all written material to the OSD security office for clearance (Peck and Scherer, The Weapons Acquisition Process, p. xi).

Sustaining Critical Sectors of the U.S. Defense Industrial Base 15

initiative for product decisions rests upon sellers, [yet in defense] the government rather than its contractors decides what weapons are to be created through its pro-gram decisions. Program decisions are in turn implemented by … scores of optimi-zation decisions … , some made by government agencies, some shared between the government and its contractors, and still others made by contractors. At this more detailed level the decision-making roles of government and contractors become en-twined in a manner foreign to a market system’s rigid distinction between buyers and sellers. Thus weapons acquisition is characterized by a form of economic organization quite different from the market system found elsewhere in the U.S. economy.46

Here one of the most striking differences between the defense industry and the rest of the U.S. economy was that the U.S. government is ultimately a single buyer even if, in practice, it speaks with “many different and discordant” voices.47

Peck and Scherer went even further than simply pointing out the funda-mentally non-market character of the permanent defense industrial base that emerged in the 1950s. They offered four reasons for what they termed the “re-grettable” conclusion that a market system in its entirety could never exist for weapon acquisition: (1) individual weapons projects require such large expendi-ture of private financing that their development is virtually impossible by private firms48; (2) the development of advanced weapons involves far larger technical, bureaucratic and funding uncertainties than do commercial products; (3) a free market could not determine the product characteristics desired by government buyers of advanced weaponry; and (4) price competition in advanced weapons is not like that in a free market.49 Suffice it to say that Peck and Scherer’s con-clusions about the unique, non-market character of defense acquisition were certainty true in the early 1960s, and Gansler’s analysis confirmed that they remained true into the 1980s.

How much has the fundamental character of the U.S. defense industry moved in the direction of functioning like a normal free market since the Cold War ended? One looks in vain for evidence that there has been discernible movement in this direction. In April 2009, none other than Secretary of Defense Robert Gates ob-served that the “perennial procurement and contracting cycle—going back many

46 Peck and Scherer, The Weapons Acquisition Process, p. 582.47 Peck and Scherer, The Weapons Acquisition Process, p. 76. Gansler, too, emphasized that DoD is

a single buyer for weapons, whereas there are many buyers, large and small, for most commercial products (Gansler, The Defense Industry, p. 30).

48 During the late 1950s, Northrop used its own funds to develop the F-5 as a low-cost, lightweight fighter that could be sold to less-developed nations under the Military Assistance Program. Over 2,200 F-5s were eventually built and hundreds remain in service today. Later, Northrop invested some $1.2 billion of its own money to develop the F-20, but the Reagan administration’s decision to sell F-16s overseas doomed the F-20, of which only three were built. The F-5, therefore, is the last supersonic jet fighter that an aerospace firm was able to develop on its own dime and success-fully market.

49 Peck and Scherer, The Weapons Acquisition Process, pp. 57–60.

16 center for strategic and Budgetary Assessments

decades—of adding layer upon layer of cost and complexity onto fewer and fewer platforms that take longer and longer to build must come to an end.”50 The follow-ing month, President Barack Obama made much the same observation when he signed the “Weapon System Acquisition Reform Act of 2009.” In the president’s view, the act represented “an important next step” toward reforming a defense procurement process in which “taxpayers are charged too much for weapons sys-tems that too often arrive late.”51 Moreover, the persistence of substantial cost growth in many current acquisition programs (see Table 1 in the next section) supports the judgment that, despite repeated numerous attempts at reform, the U.S. defense industry still does not operate like a classic free market. Again, a sine qua non of free markets is price sensitivity based on supply and demand, competi-tion, and innovation, characteristics not present in defense acquisition.

Nevertheless, the myth about the free-market character of the U.S. defense industry persists. To cite a recent example, in February 2011 Ashton Carter, the Pentagon’s Under Secretary for Acquisition, Technology, and Logistics, an-nounced at an investment conference that Secretary of Defense Robert Gates’ ef-ficiency initiative would, in the main, “rely on normal market forces to make the most efficient adjustments to the defense industrial base.”52 Nor was Carter alone in continuing to subscribe to this view of how the defense industry functions. Title II, Section 202, of the “Weapon System Acquisition Reform Act of 2009” requires the Secretary of Defense to include in the acquisition strategy for each MDAP “measures to ensure competition, or the option of competition, at both the prime contract level and the subcontract level … throughout the life-cycle of such a pro-gram as a means to improve contractor performance.”53 Here again the underlying premise is that just as free-market competition has contained costs and improved performance in computers, consumer electronics, and other commercial sectors, free-market competition can also achieve efficiencies in the defense industry.

The obvious way to achieve such competition would be, as Section 202 of the 2009 reform act suggests, to retain more than one supplier at the prime and sub-contractor levels well past source selection. But in the case of congressional efforts

50 Robert M. Gates, “Defense Budget Recommendation Statement,” April 6, 2009, at http://www.defenselink.mil/speeches/speech.aspx?speechid=1341, accessed February 13, 2011.

51 President Barack Obama, “Remarks by the President at signing of the Weapons Systems Acquisition Reform Act,” The White House, May 22, 2009, at http://www.whitehouse.gov/search/site/weapons%20systems%20acquisition%20form%20act%20of%202009, accessed February 13, 2011.

52 Ashton Carter, “The Defense Industry Enters a New Era,” remarks at Cowen Investment Conference, New York, NY, February 9, 2011.

53 The “Weapons Systems Acquisition Reform Act of 2009,” Public Law 111-23, is available at http://www.gpo.gov/fdsys/pkg/PLAW-111publ23/pdf/PLAW-111publ23.pdf. For a summary of recent Congressional efforts to reform defense acquisition, see Moshe Schwartz, “Defense Acquisitions: How DOD Acquires Weapon Systems and Recent Efforts to Reform the Process,” Congressional Research Service RL34026, April 23, 2010.

In fact, the

U.S. defense

industry … does

not operate like

a classic free

market.

Sustaining Critical Sectors of the U.S. Defense Industrial Base 17

to develop an alternative engine for the F-35, Secretary Gates has adamantly re-sisted doing so. As he explained to Representative John Larson in May 2010,

DOD’s independent Cost Analysis and Program Evaluation (CAPE) estimates that an additional $2.9 billion would be required to take an alternate engine, the F136, to competitive procurement in FY17. While the $2.9 billion cost is real and certain, the benefits of a second engine are not. CAPE has concluded that a second engine might provide savings if both engine vendors respond to competitive pressures and drive prices lower and the second engine supplier matches the F135’s vendor prices for the duration of the competition. Some international partners are almost certain to only buy the F136 engine made by the General Electric (GE) and Rolls Royce team, and the Navy has stated they will only buy one engine to avoid having to maintain two different engines aboard a ship. While DOD favors competition where possible, in this case there would not be a true competition between the engine vendors, with accompanying reductions in cost. Therefore, it is DOD’s strong judgment that these real costs outweigh the theoretical benefit.54

Presumably the added expense of second production lines for major items such as the JSF, the Trident II submarine-launched ballistic missile (SLBM), the Space-Based Infrared Systems (SIBRS) satellites, or Global Hawk RQ-4 unmanned aerial reconnaissance vehicles would be far more expensive than the alternative F136 engine for which Congress has provided $1.3 billion in unrequested addi-tional funding. Even if separate sources were preserved throughout production, the small quantities the government procures these days would probably not al-low either competitor to get far enough down its learning curve to yield savings greater than the costs of funding a second source. In fact, if the competition were to be staged as a multi-round split buy (with, say, 60 percent going to the winner and 40 percent to the loser each round), then the cost advantage obtained by the winner of the first round by being able to progress further down the learning curve could make it impossible for the loser of the first round to win any subse-quent rounds. Consequently, as the Pentagon moves into an era of fiscal austerity, it is difficult to envision Section 2o2 of the 2009 acquisition reform act being implemented successfully, especially at the prime level. If not, then there appears to be scant hope that defense acquisition will move perceptibly in the direction of functioning like a true free market anytime soon.

54 Robert M. Gates, letter to John B. Larson, May 25, 2010, p. 1. This letter is available at http://f135engine.blogspot.com/2010/05/letter-from-defense-secretary-robert.html. In the case of the F-16, however, the Air Force funded the development and testing of a second engine. In the first four years of the resulting competition, results based on comparing actual costs to the program’s baseline estimate included: nearly 30 percent cumulative savings for acquisition costs; roughly 16 percent cumulative savings for operations and support costs; and total savings of about 21 percent in overall life cycle costs” (Michael Sullivan, “Defense Acquisitions: Analysis of Costs for the Joint Strike Fighter Engine Program,” statement before the Subcommittees on Air and Land Forces, and Seapower and Expeditionary Forces, House Armed Services Committee, March 22, 2007, GAO-07-656T, p. 12).

In fact, if the

competition were

to be staged as a

multi-round split

buy, then the cost

advantage obtained

by the winner of the

first round by being

able to progress

further down the

learning curve could

make it impossible

for the loser of the

first round to win

any subsequent

rounds.

For decades, a constant criticism of the U.S. defense industry has been that the ac-quisition system has been unable to control either program or unit costs.55 Figure 3’s left-hand plot shows unit-cost trends from 1940 to 1980 for both tactical air-craft and tanks using a logarithmic scale on the vertical axis. These trends, which have certainly persisted into the 2000s for tactical aircraft, reflect the persistent inclination of Service and OSD customers to accord first priority in weapons pro-grams to state-of-the-art performance. True, early-as-possible availability has also occasionally been accorded top priority in major weapons programs; a recent example is the Mine Resistant Ambush Protected (MRAP) vehicle program. In most cases, however, cost has tended to end up in last place, even when initially given first billing. In the early days of both the JSF and the Evolved Expendable Launch Vehicle (EELV) programs, controlling costs was a major, if not overriding, priority. But even in the case of EELV, cost control gave way to performance in the sense of insisting on the availability of two reliable launch vehicles.

The most important consequence of the acquisition system’s inability to con-trol costs has been to limit the quantities of advanced weapons systems that the Defense Department has been able to buy. Especially in areas such as U.S. naval combatants and Air Force combat aircraft, inventory levels have steadily gone down since the mid-1990s (see Appendix 2). Perhaps the most striking illustra-tion can be seen in the case of all-aspect, low-observable (LO) combat aircraft. Ignoring the JSF, the Pentagon has started four major programs to field “stealthy” combat aircraft: the F-117, the B-2, the Advanced Tactical Aircraft (A-12), and the Advanced Tactical Fighter (F-22). Only three of these planes entered operational service: the now-retired F-117, the B-2 and the F-22. The Navy’s A-12, conceived

55 See, for example, John Lehman. “Wasteful Spending Is a Clear and Present Danger,” The Wall Street Journal, July 18, 2009, at http://online.wsj.com/article/SB124787043032160493.html, ac-cessed February 12, 2011.

cHAPTeR 5 > EFFICIENCy THEN AND NOW

20 center for strategic and Budgetary Assessments

to replace its aging A-6, was cancelled by defense secretary Richard Cheney in January 1991.56 Granted, all four of these “stealth” programs were begun before the Cold War ended. So the quantities initially envisioned were undoubtedly influenced by American perceptions of the Soviet threat. Still, at the outset the Services planned to field 20 F-117s and no less than 132 B-2s, 858 ATAs for the Navy and Marine Corps (with possibly another 400 for the Air Force), and 750

56 Litigation over the A-12’s cancellation between the government and the contractors continued into 2011. Initially General Dynamics and McDonnell Douglas (now Boeing) challenged the termina-tion on the grounds that the Air Force did not share knowledge about stealth technology from the F-117 and B-2 programs. A federal claims court ruled that because of the withheld information the contractors did not default and ordered the Pentagon to pay them $1.2 billion in expenses. A fed-eral appeals court then overturned this decision and ordered a new trial, at which DoD prevailed and asked the contractors to return $1.35 billion it had paid them for work never accepted plus interest. On March 23, 2011, the U.S. Supreme Court vacated the appeals court ruling and sent the case back to the federal circuit (Marcus Weisgerber, “Supreme Court Overturns A-12 Ruling against Contractors,” Defense News, May 23, 2011).

* The left-hand chart is an early version of the basis of Augustine’s lighthearted “law” that by 2054 the entire defense budget will purchase just one aircraft (norman R. Augustine, “Land Warfare,” Ieee Transactions on Aerospace and electronic systems, Vol. Aes-22, no. 5, september 1986, p. 510, Figure 46). The right-hand chart updates Augustine’s original for tactical aircraft using sources such as Air Force fact sheets and constant FY 1998 dollars. currently Augustine says that the ongoing growth in aircraft unit prices is “right on target” to fulfill his original prediction (“Defence spending in a Time of Austerity,” The Economist, August 28, 2010, p. 21).

FIGURE 3. UNIT COST TRENDS IN TACTICAL AIRCRAFT AND TANkS*

$10$107 7

$10$106 6

$10$105 5

$10$104 4

Ave

rage

Uni

t C

ost

(Mill

ions

The

n-Ye

ar $

) A

vera

ge U

nit

Cos

t (M

illio

ns T

hen-

Year

$)

F-14 F-14

F-15 F-15

1940

1940

1980

1980

Year of IOCYear of IOC

Harrier Harrier F-4J F-4J

A-6 A-6

F-111A F-111A F-111D F-111D

F-4B F-4B F-105 F-105 A-7E A-7E

A-7A A-7A F-104 F-104

F-8E F-8E F-5 F-5

F-106 F-106

A-1E A-1E

F-101 F-101

F-102 F-102

F-100 F-100 F-84 F-84

F-86 F-86

P-51 P-51

P-38 P-38

P-47 P-47

F-4U F-4U

MBT-70 MBT-70 M60A1E2 M60A1E2

M60A1 M60A1

M60 M60

M48A3 M48A3

M48A1 M48A1

M48 M48 M41 M41

M-4

F9F-6 F9F-6

A-4D A-4D

F8F-2 F8F-2

MAIN BATTLE TANKS

MAIN BATTLE TANKS

TACT

ICAL

AIR

CRAF

T

Year of Initial Operational CapabilityYear of Initial Operational Capability

F-14 F-14

F-15A/B F-15A/B

F-15C/D F-15C/D

F/A-18A/B F/A-18A/B

A-10 A-10 F-16A/B F-16A/B

F-16C/D Block 25-32 F-16C/D Block 25-32

Ave

rage

Uni

t C

ost

(Mill

ions

FY

98

$)

Ave

rage

Uni

t C

ost

(Mill

ions

FY

98

$)

F-15E F-15E

F/A-18C/D F/A-18C/D

F/A-18E/F F/A-18E/F

F-22 F-22

$200$200

$100$100

$50 $50

$40 $40

$30 $30

$20 $20

$10$10

F-35 F-35 Estimates Estimates (Dec 2009) (Dec 2009)

1945

1945

1950

1950

1955

1955

1960

1960

1965

1965

1970

1970

1975

1975

1970

1970

1975

1975

1980

1980

1985

1985

1990

1990

1995

1995

2000

2000

2005

2005

2010

2010

2015

2015

Sustaining Critical Sectors of the U.S. Defense Industrial Base 21

Air Force F-22s and 618 carrier variants for a grand total of 2,778 jets. The F-117 alone was procured in greater numbers than originally envisioned. B-2 and F-22 cost growth, successive reductions in planned buys, the A-12’s cancelation and the Navy’s exit from the F-22 program in favor of an improved variant of F/A-18 resulted in only 267 of these aircraft being fielded (59 F-117s, 21 B-2s, and 187 F-22s). What makes these final quantities so distressing is, of course, the large development costs these aircraft required. The B-2 and F-22 developments each cost the U.S. taxpayer over $24 billion (in then-year dollars).57 Reducing the F-22 buy from 750 to 187 added nearly $100 million to the unit acquisition cost of each fighter, and reducing the B-2 buy from 132 to 21 added almost $1 billion to the unit acquisition price of each bomber.58

It is tempting to conclude, in light of post-Cold War production quantities being as truncated as they were in case of the B-2, that the efficiency of DoD’s weapons acquisition process has been growing progressively worse over time. Surprisingly, however, this does not appear to be the case. Based on available data, cost-change ratios and schedule slippage during the 1950s were not dramatically better than they are today.

The right hand columns in Table 1 display cost-change ratios for twenty current MDAPs. The ratios have been normalized to remove the effects of inflation and to account for changes in the quantities to be procured. The base-year original and current program costs used to compute the cost-per-unit ratios for each MDAP are not completely comparable unless the programs being compared have the same base year. For example, the cost/quantity prices for the Air Force’s Advanced Medium Range Air-to-Air Missile (AMRAAM) are in constant FY 1992 dollars, whereas the price for the Guided Multiple Launch Rocket System (GMLRS) is in FY 2003 dollars. (See Appendix 3 for Table 1 with the original and current acqui-sition unit prices in constant FY 2011 dollars.) Note, also, that two cumulative cost-change ratios are shown for the two programs—the F-22 and the V-22—in which re-baselining in 2005 lost visibility into prior changes in program costs and planned buy quantities. The F-22 program, for instance, experienced a cost-change ratio of 2.89—a 189 percent cost overrun per unit—from 1990 to the end of 2004, whereas the re-baselined program has a cost-change ratio of only 1.04—a mere 4 percent increase—since 2005. Thus, the cumulative cost growth per F-22 has been 200 percent.

57 For the B-2’s RDT&E cost in then-year dollars, see Department of the Air Force (DoAF), “Supporting Data for Fiscal Year 1999 Amendment: Research, Development, Test and Evaluation Descriptive Summaries,” Volumes I, II, & III, February 1998, p. 821; for F-22 RDT&E, see DoAF, “Fiscal Year (FY) 2008/2009 Budget Estimates: Research, Development, Test and Evaluation Descriptive Summaries,” Vol. II, February 2007, p. 899.

58 The cancelation of programs such as the Comanche helicopter and the Future Combat Systems suggests that during the 2000s the Army had even more difficulty getting from development to production than the Air Force or Navy. See Marjorie Censer, “Go Big or Go To War with the Weapons You Have,” The Washington Post, May 29, 2011, pp. G1 and G4.

Based on available

data, cost-change

ratios and schedule

slippage during the

1950s were not

dramatically better

than they are today.

22 center for strategic and Budgetary Assessments

TABLE 1 . COST-CHANGE RATIOS FOR TWENTy 2010 mDApS (NORmALIzED FOR INFLATION AND QUANTITy)*

* The primary source for Table 1 is DoD, OUSD(AT&L) ARA/AM, “Selected Acquisition Report (SAR) Summary Tables: As of Date: December 31, 2010,” April 5 2011. However, earlier SARs were used to capture prior cost and quantity changes for two programs that were re-baselined: the F-22 and the V-22. The cost-change ratios in gray boxes were used to compute the average for all twenty programs. If the re-baselining of the F-22 and V-22 is ignored, then the average cost-change ratio for Table 1 is 1.21. Congress requires that cost growth in DoD acquisition programs be reported relative to the original baseline (US Code Title 10, Subtitle A, Part IV, Chapter 144, § 2435, “Baseline Description,” as of February 1, 2010). However, if the acquisition or procurement unit price exceeds the critical cost growth thresholds in § 2433, the baseline can be adjusted or revised. Senator Sam Nunn and Congressman Dave McCurdy first established thresholds for reporting program cost growth to Congress in an amendment to the 1982 Defense Authorization Act. These reporting requirements were made permanent in 1983. Breaches of the cost-growth thresholds in § 2435 are commonly known as “Nunn-McCurdy breaches.”

program (Base year)

Base year $ (millions) per Unit

Cost-Change Ratio

Cumulative Change Ratio

original/Quantity

current/Quantity

F-35 Joint strike Fighter (2002) $61.793 $110.134 1.78

F-22 Advanced Tactical Fighter (1990) $93.009 $268.503 2.893.00

F-22 Raptor (2005) $355.148 $369.490 1.04

AMRAAM (1992) $0.797 $1.000 1.26

Joint Direct Attack Munition (1995) $0.026 $0.022 0.86

global Hawk RQ-4A/B (2000) $69.052 $171.039 2.48

Reaper MQ-9 (2008) $27.497 $28.359 1.03

global Positioning system IIA (2010) $480.100 $527.200 1.10

Advanced eHF (2002) $1,933.567 $1,945.067 1.01

F/A-18e/F super Hornet (2000) $84.814 $83.880 0.99

ssn 774 nuclear Attack submarine (1995) $2,145.120 $2,107.317 0.98

cVn 78 class Aircraft carrier (2000) $9,567.067 $9,142.000 0.96

DDg-51 Aegis Destroyer (1987) $737.117 $802.199 1.09

Trident II sLBM (1983) $31.428 $48.729 1.55

V-22 (1986) $25.27 $69.21 2.742.74

V-22 (2005) $109.717 $109.625 1.00

stryker (2004) $3.949 $3.671 0.93

guided MLRs (2003) $0.070 $0.111 1.59

Longbow Apache (1996) $7.507 $15.027 2.00

UH-60M Black Hawk Upgrade (2005) $13.605 $16.064 1.18

Patriot PAc 3 (2002) $7.838 $7.932 1.01

MQ-1c UAs gray eagle (2010) $378.738 $162.006 0.43

1.40 Average

Sustaining Critical Sectors of the U.S. Defense Industrial Base 23

Two further observations should put the cost-change data in Table 1 in per-spective. First, the choice of programs was somewhat arbitrary. The intent was to include major platforms from all the Services with a sampling of troubled MDAPs in which there had been substantial cost growth. Nevertheless, Table 1 contains several programs—including the F/A-18E/F, the SSN 774 nuclear attack submarine, the Stryker ground combat vehicle, the Joint Direct Attack Munition (JDAM), and, most dramatically, the MQ-1C Gray Eagle unmanned air sys-tem—in which the cost per unit has gone down rather than up. Second, while the overall average program cost-change in Table 1 is an increase of 40 percent, this percentage is greater than the 22 percent cost growth over all of the Pentagon’s 101 MDAPs as of December 31, 2010. The U.S. Army’s average across twenty-four major acquisition programs is only 19 percent, the average for the thirty-six Navy and Marine Corps MDAPs is 15 percent, and the Air Force’s average is 26 percent over thirty-one major programs.