survey of external data possibilities for commercial insurance

TRANSCRIPT

Survey of External Data Possibilities for Commercial Insurance

2013 CAS Ratemaking and Product Management Seminar

Robert J. Walling, III

March 12, 2013 5:15pm PT

About the Presenter – Rob Walling

B.S. Secondary Math Education – Miami University 1987 Fellow of Casualty Actuarial Society (FCAS)

Committee Chair of Ratemaking, ERM and New Fellows

Principal, Pinnacle Actuarial Resources, Inc. Areas of Focus – Captives &Alternative Markets, Regulatory, Commercial Lines Ratemaking and g y gLoss Reserving, Expert Witness, Legislative Cost

Wife, Anne, and three kids, , Graduate of Miami University Lifelong Cincinnati Reds fan

2

Lifelong Cincinnati Reds fan

Topics for Discussion

Internal Data Competitive Benchmarking Alternatives to Credit/Business Characteristics Property Commercial Auto Professional Liability

3

Internal DataInternal Data

Internal Data

Rating Underwriting

Multiline information (auto, WC, umbrella, broadening

Cancellation Reinstatement

d

endorsements, etc.) Affiliations/Associations

Endorsements

Agency Marketing

Claims Application Information

Billi Pl Marketing Loss Prevention

Billing Plan Payment history

5

Loss Control/Loss Prevention Opportunities

Loss Control Surveys Social Media/Customer Satisfaction

Loss Control Survey as Scorecard Input

7

Improvement in Loss Control Survey Score Leads to Better than Expected Lossesp

25,000,000 0.30

GLM Actual vs Expected ‐WC

10%

6%

20,000,000

0.10

0.20

4%

‐4%

0%

‐13% 10,000,000

15,000,000

‐0.10

0.00

Expo

sures

Log o

f Multip

lier

‐17% ‐15%

5,000,000

‐0.30

‐0.20

‐‐0.40

mChange_in_RCA_2

Exposures Relativity Approx 95% Confidence Interval

Type 3: = 0.42%

Improvement in Loss Control Survey Score Leads to Superior Large Loss Experiencep g p

27%20 000 000

25,000,000

0.30

0.40

11% 11% 15,000,000

20,000,000

0.10

0.20

eslier

‐1%0%

10,000,000 0.00 Ex

posure

Log o

f Multip

‐15%‐18%

5,000,000

‐0.20

‐0.10

‐26%

‐‐0.30

Ch i C 2mChange_in_RCA_2

Exposures Likelihood

Competitive BenchmarkingCompetitive Benchmarking

Commercial Auto Scorecard Example

11

Commercial Auto Example ‐ Hartford

NOTICETHELIFT!

12

Trucking Example – Great West

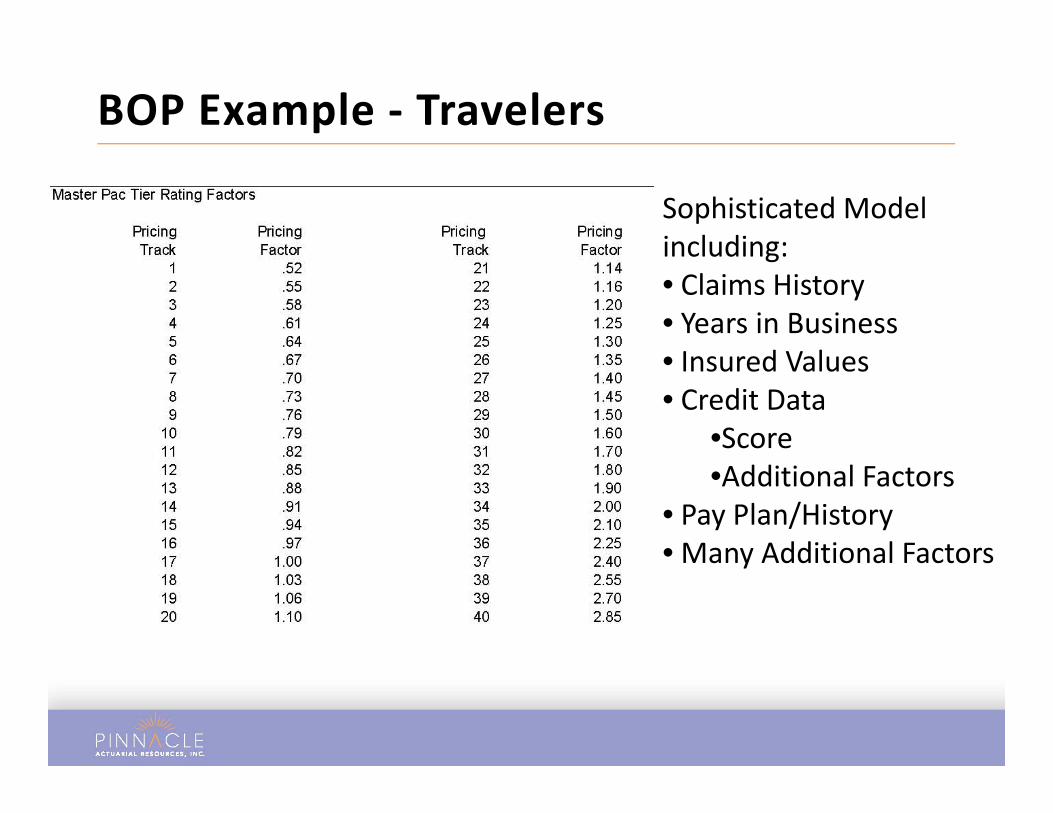

BOP Example ‐ Travelers

Sophisticated Model including:including:• Claims History• Years in BusinessI d V l• Insured Values

• Credit Data•Score•Additional Factors

• Pay Plan/History• Many Additional FactorsMany Additional Factors

BOP Scorecard ‐ Farmers

Underwriting Scorecard ‐ Farmers

Underwriting Scorecard ‐ Farmers

Alternatives to Credit/Business Characteristics

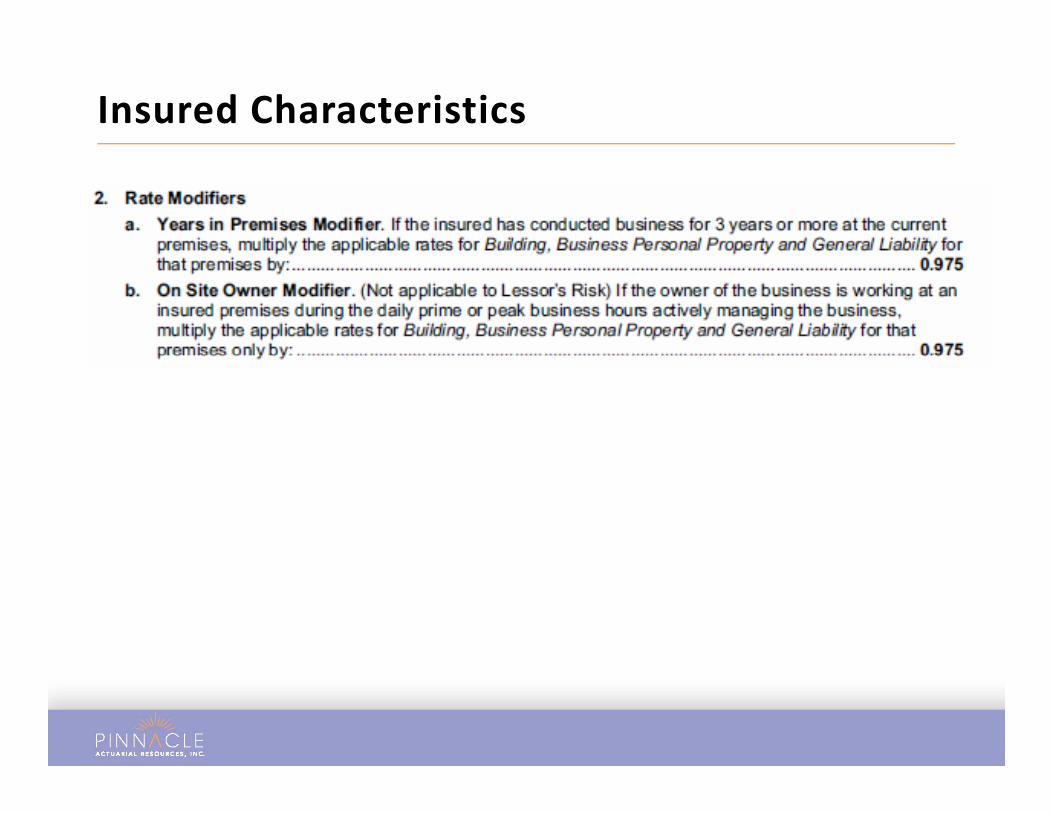

Insured Characteristics

Years in Business vs. Year on Risk (Tenure)l Prior Claims

Collateral Policies/Endorsements Years at Current Premises On‐Site Owner vs AbsenteeOn Site Owner vs. Absentee Payment History (NSF, Cancelation Notice, Reinstatement)Reinstatement) Type of Company (S‐Corp, C Corp, LLC, Sole

i )Proprietor, etc.)

BOP Insured Characteristics Example

Years in Business

Years in Business + Prior Claims

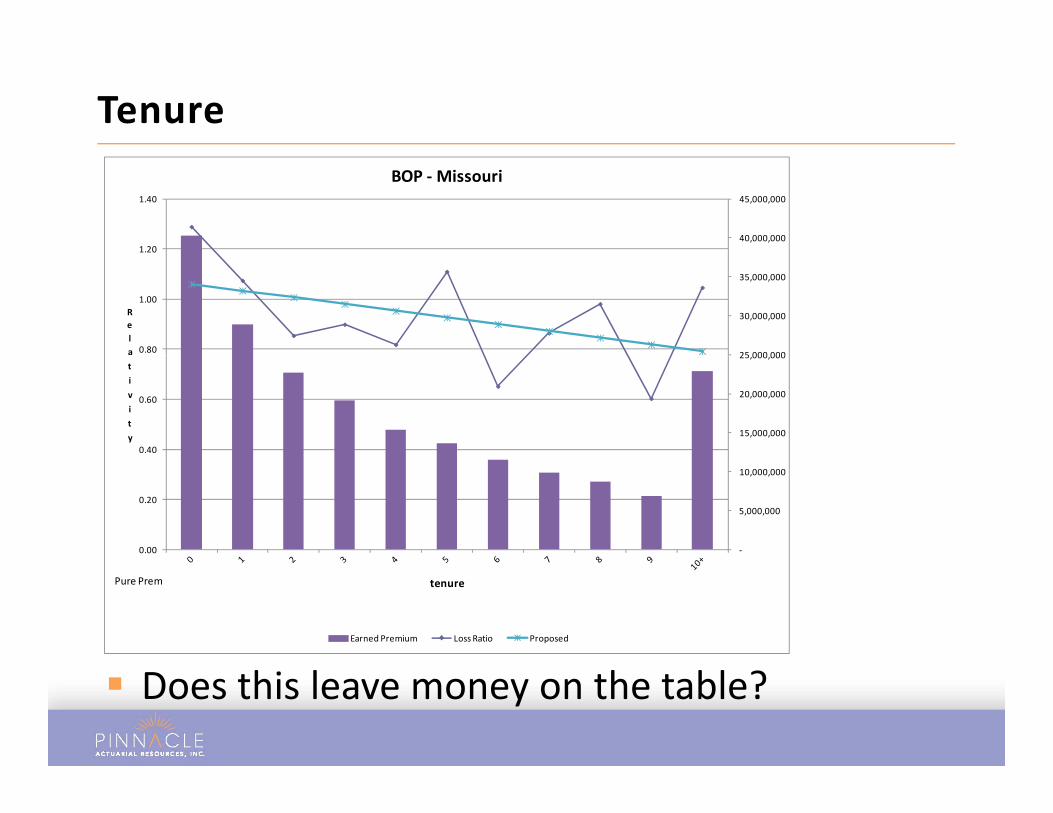

Tenure

40,000,000

45,000,000

1.20

1.40

BOP ‐Missouri

25 000 000

30,000,000

35,000,000

0.80

1.00Rela

15,000,000

20,000,000

25,000,000

0.40

0.60

tivity

‐

5,000,000

10,000,000

0.00

0.20

tenure

Earned Premium Loss Ratio Proposed

Pure Prem

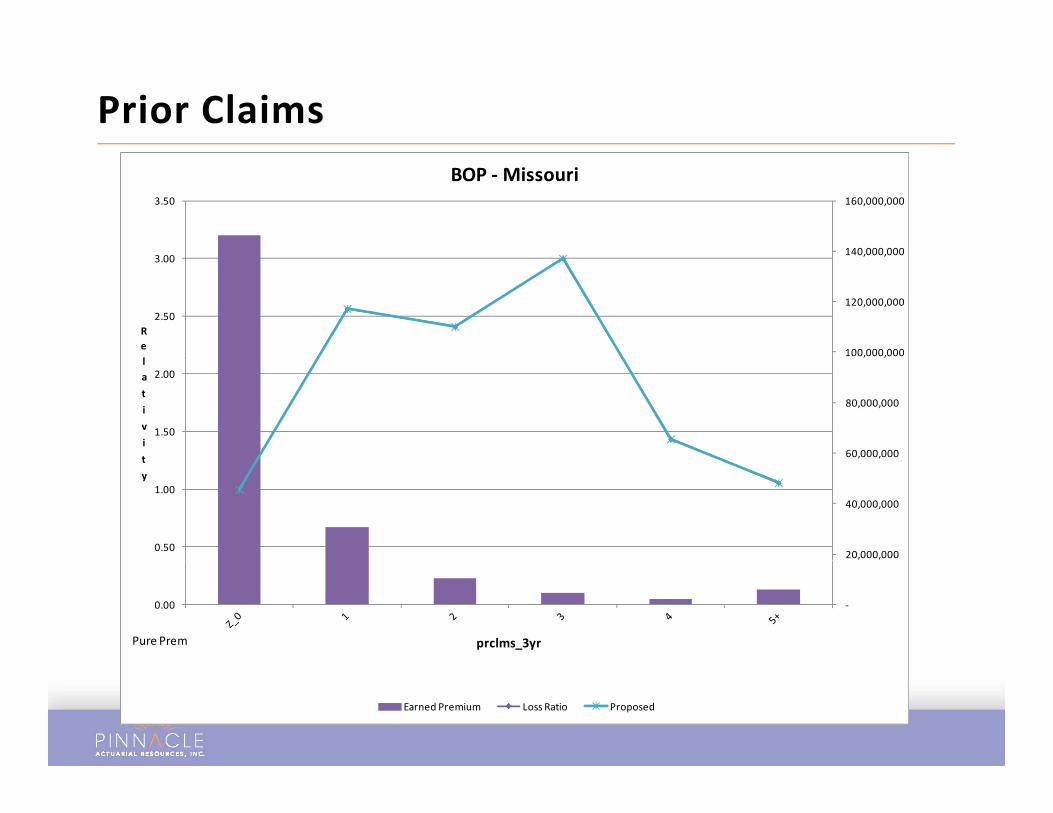

Does this leave money on the table?

Prior Claims

140 000 000

160,000,000 3.50

BOP ‐Missouri

100,000,000

120,000,000

140,000,000

2.50

3.00

Re

60,000,000

80,000,000

100,000,000

1.50

2.00lativit

20,000,000

40,000,000

, ,

0.50

1.00

ty

‐0.00

prclms_3yrPure Prem

Earned Premium Loss Ratio Proposed

Prior Claims

3 0

3.5

2.5

3.0

1.5

2.0

1.0

0.0

0.5

None 1 Sm 1 Lg 2 Sm 1 Sm, 1 Lg 2 Lg 3 Sm 2 Sm, 1 Lg 1 Sm, 2 Lg 3 Lgg , g g , g , g g

Travelers VA New Selected

Multiple Policy Discounts

Insured Characteristics

PropertyProperty

Property Characteristics

Building Ageld l ll ll Building Type – Sole Occupant, Mall, Strip Mall

Central Alarm Validation of Total Insured Values Inspection Data – (Real Estate and Prior Claims)Inspection Data (Real Estate and Prior Claims) Hazard Zones (Flood, Brush Fire, Coast/Wind, Sink Holes Earthquake)Sink Holes, Earthquake)

Commercial AutoCommercial Auto

VINs, MVRs and Prior Claims

VIN Decoding Well established New products related to trailers, equipment modifications, etc.

MVRsSeveral vendors Several vendors

Key question – Ordering Protocols – Who? How often? Prior Claims

Commercial C.L.U.E. gaining traction

31

Federal Motor Carrier Safety Administration‐Safety Measurement System Replaces SAFER Scores companies in several categories

Unsafe Driving (Speeding, reckless, lane changes) Fatigued Driving/Hours of Service

Driver Fitness/Training Driver Fitness/Training Controlled Substances/Alcohol Vehicle Maintenance Cargo‐Related (Spills, HazMat) Crash Experience

32

SMS Basic Information

33

SMS Basic Information

34

SMS Scoring

35

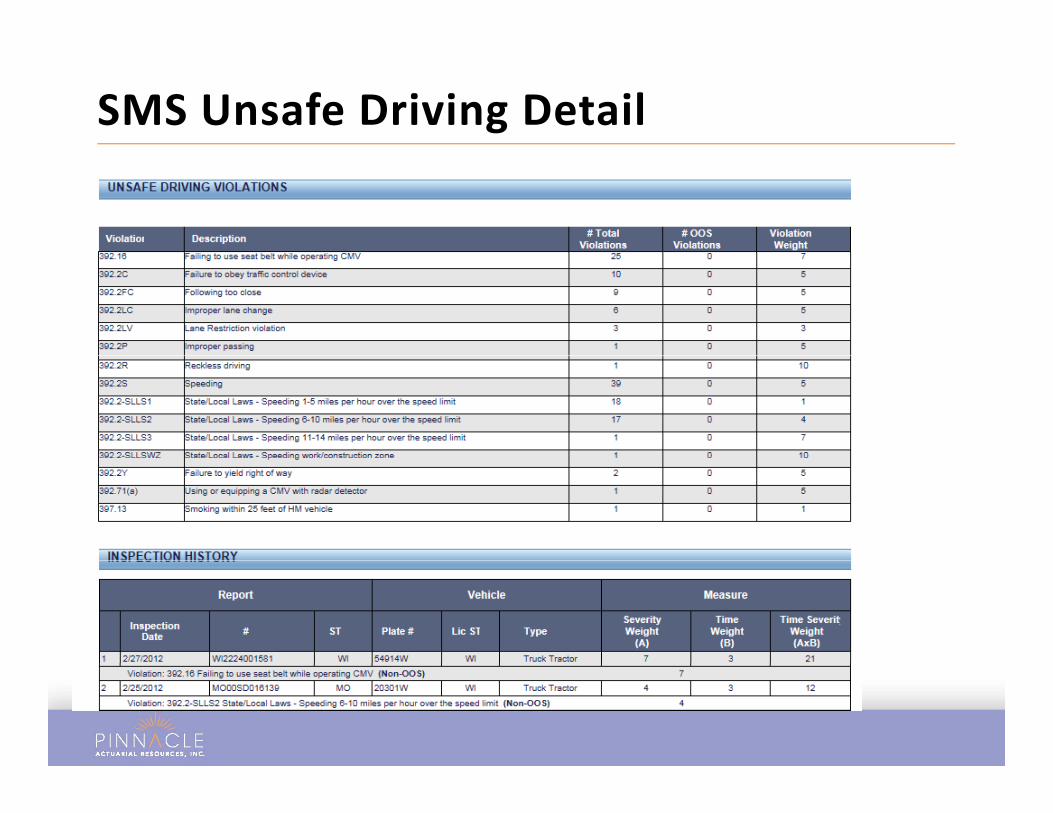

SMS Unsafe Driving Detail

SMS Unsafe Driving Detail

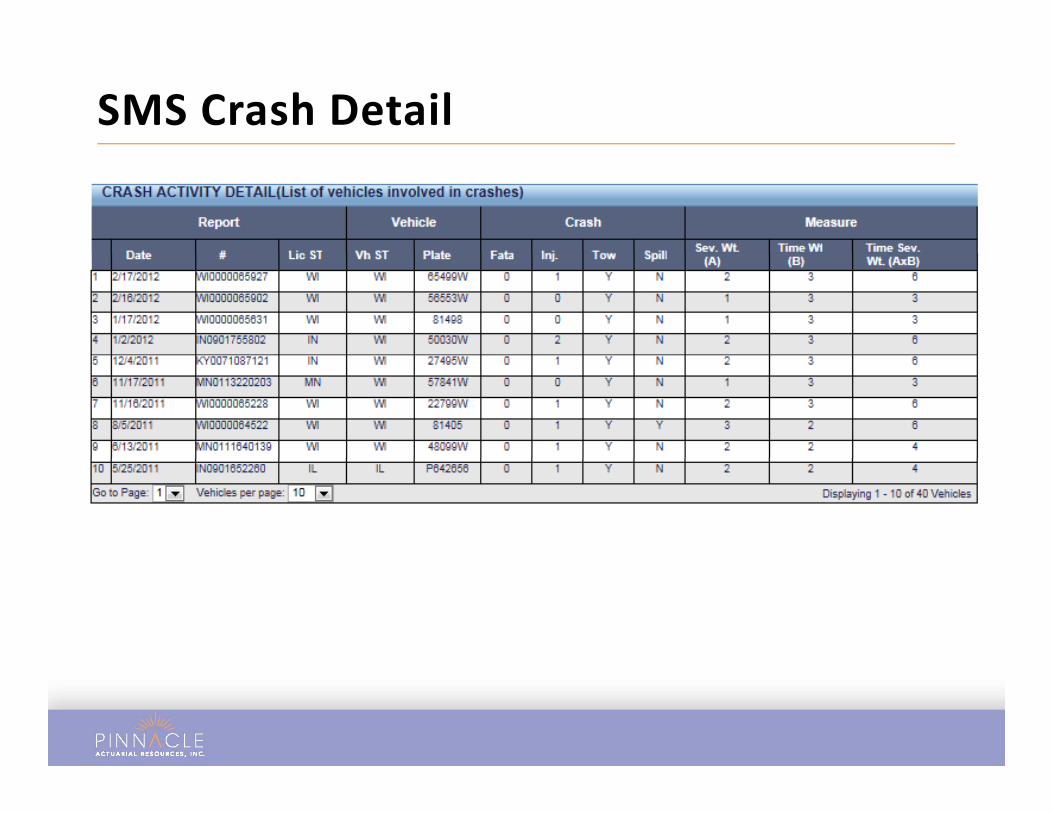

SMS Crash Detail

SMS Crash Detail

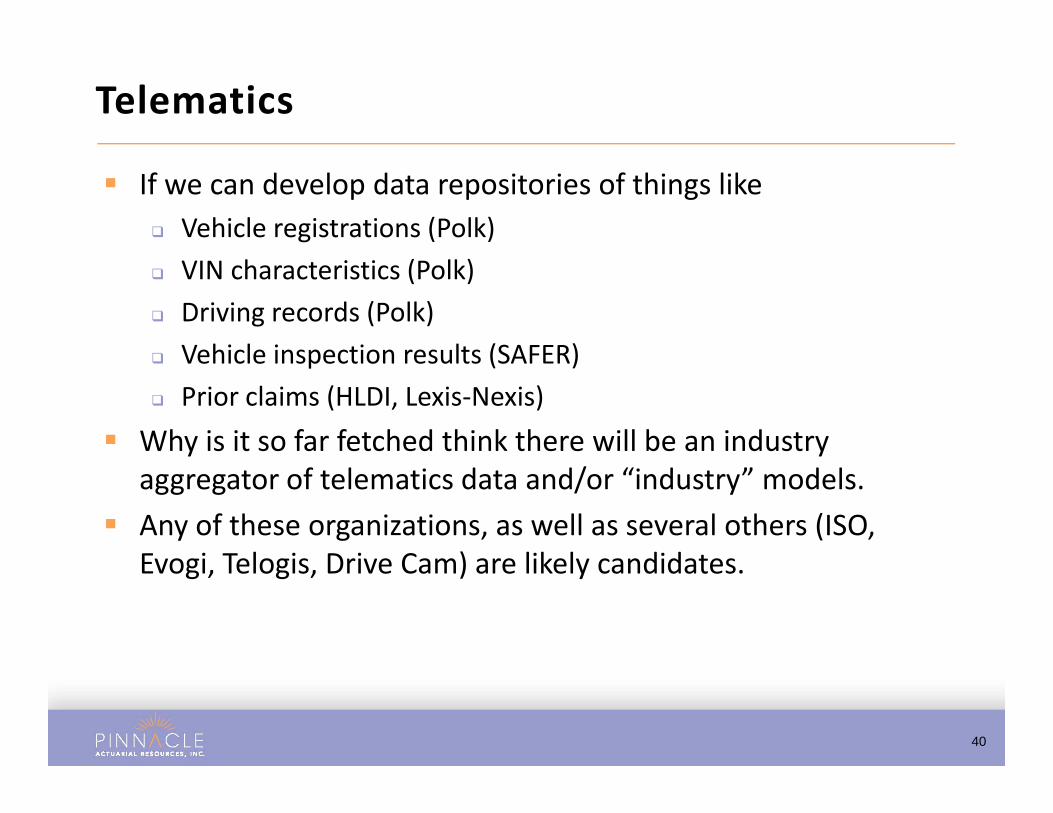

Telematics

If we can develop data repositories of things like Vehicle registrations (Polk) VIN characteristics (Polk) Driving records (Polk) Vehicle inspection results (SAFER) Vehicle inspection results (SAFER) Prior claims (HLDI, Lexis‐Nexis)

Why is it so far fetched think there will be an industry aggregator of telematics data and/or “industry” models.

Any of these organizations, as well as several others (ISO, Evogi Telogis Drive Cam) are likely candidatesEvogi, Telogis, Drive Cam) are likely candidates.

40

Professional LiabilityProfessional Liability

Hospital Professional Data

Centers for Medicare & Medicaid Services (CMS) Hospital Quality Initiative(CMS) Hospital Quality Initiative Captures information on over 4,000 Medicare‐

f d h lcertified hospitals

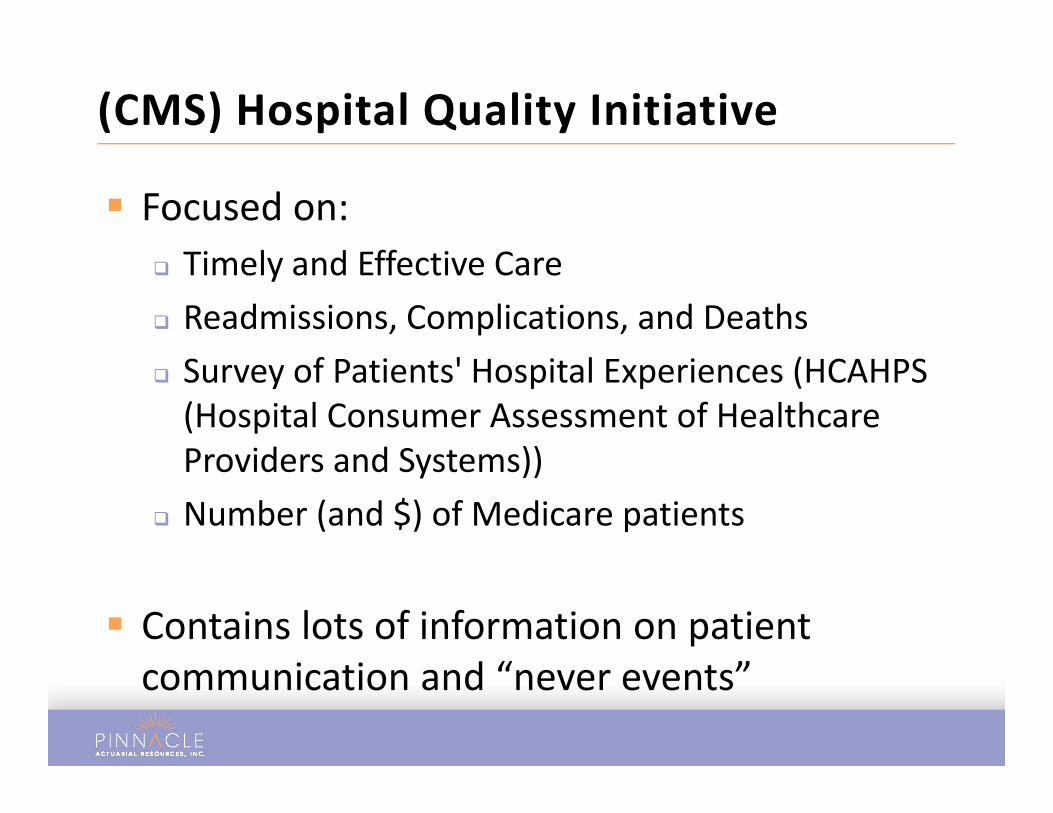

(CMS) Hospital Quality Initiative

Focused on:Ti l d Eff i C Timely and Effective Care

Readmissions, Complications, and Deaths Survey of Patients' Hospital Experiences (HCAHPS (Hospital Consumer Assessment of Healthcare Providers and Systems))Providers and Systems))

Number (and $) of Medicare patients

Contains lots of information on patient i i d “ ”communication and “never events”

Patients not given information about what to do during their recovery at home.

32%45,000

50,000

0.30

0.40

Medical ‐ 0_150k Model 3 Frequency

26%

35,000

40,000

0.10

0.20

‐5%

0%

20,000

25,000

30,000

‐0.20

‐0.10

0.00

Expo

sures

Log o

f Multip

lier

‐35%‐39%

5,000

10,000

15,000

‐0.50

‐0.40

‐0.30

‐‐0.60

H_COMP_6_N_P_rng Type 3: = <.0001

Exposures Frequency Approx 95% Confidence Interval

yp

Blood Incompatibility Claims

60,000

0 80

0.90

Medical ‐ 0_150k Model 3 Frequency

76%

40,000

50,000

0.60

0.70

0.80

33%

30,000

0.40

0.50

Expo

sures

Log o

f Multip

lier

10,000

20,000

0.10

0.20

0.30

0% ‐0.00

HAC_3_rng Type 3: = <.0001

Exposures Frequency Approx 95% Confidence Interval

yp

Pneumonia Death Rate

45,000

50,000 0.20

Medical ‐ 0_150k Model 3 Frequency

30 000

35,000

40,000

0.10

0.15

‐1%0%

4% 4% 4%

20,000

25,000

30,000

0.00

0.05

Expo

sures

Log o

f Multip

lier

‐9%

5,000

10,000

15,000

‐0.10

‐0.05

‐‐0.15

pneumonia_death_rate_rng Type 3: = <.0001

Exposures Frequency Approx 95% Confidence Interval

Patients Receiving “Right Antibiotic”

45,000

50,000 0.30

Medical ‐ 0_150k Model 3 Frequency

14%

35,000

40,000

0.10

0.20

16%

0%

20,000

25,000

30,000

‐0.10

0.00

Expo

sures

Log o

f Multip

lier

‐16%

‐20%

5,000

10,000

15,000

‐0.30

‐0.20

‐‐0.40

OP_7_rng Type 3: = <.0001

Exposures Frequency Approx 95% Confidence Interval