survey of electricity (and gas) trends and drivers in asia · survey of electricity (and gas)...

TRANSCRIPT

Survey of electricity (and gas) trends and drivers in Asia 10th International Chlor-Alkali & Vinyls Conference 2016, Bangkok, Thailand

Xinmin Hu ([email protected])

2-3 March 2016

The Lantau Group Confidential and Proprietary

Who we are

Decisions Support Analysis

Asset Valuation

Strategy and Advanced Analytics

Competition, Markets, Regulation, Policy

Disputes

Market Analysis

Electricity and Gas Sector Focus

The TLG team has

experience throughout

the Asia Pacific region

Office/Presence

Senior Advisors

Offerings:

• Strategic, commercial, and regulatory support

• Ability to connect the dots between fuel markets and power

• Analysis-based recommendations

• Highly relevant international experience

• Accessible experts focussed on the region

Specialist economic consulting firm to the energy sector based in Asia

1

The Lantau Group Confidential and Proprietary

0

5

10

15

20

25

US

¢/k

Wh

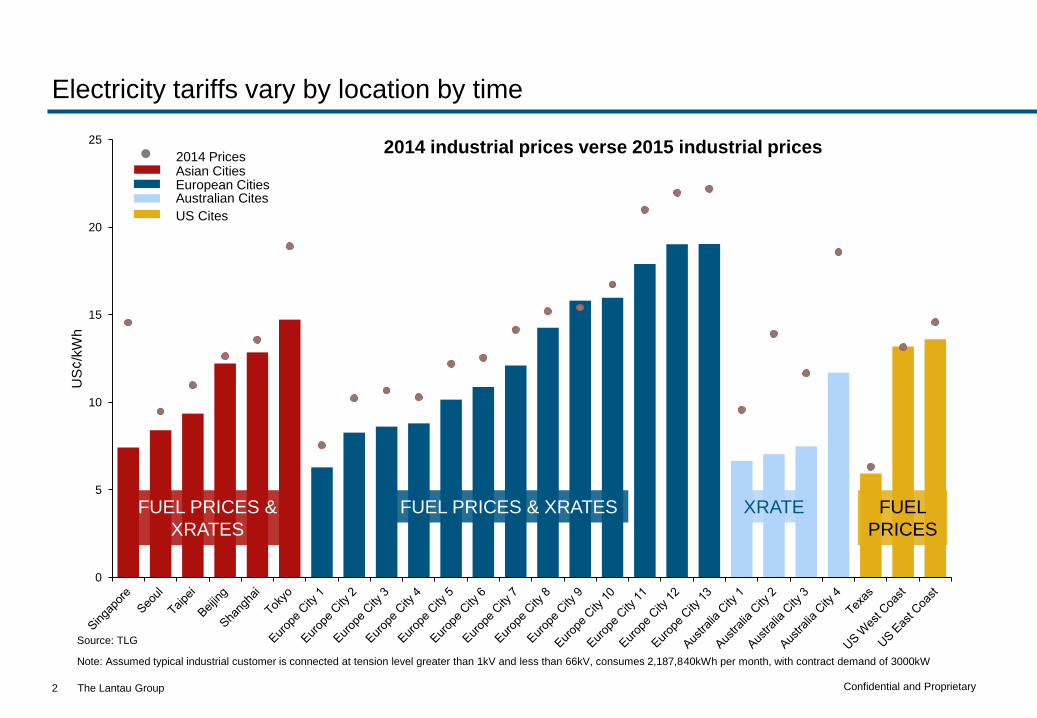

2014 Prices Asian Cities European Cities Australian Cites

US Cites

2014 industrial prices verse 2015 industrial prices

Source: TLG

FUEL

PRICES

FUEL PRICES & XRATES FUEL PRICES &

XRATES

XRATE

Note: Assumed typical industrial customer is connected at tension level greater than 1kV and less than 66kV, consumes 2,187,840kWh per month, with contract demand of 3000kW

Electricity tariffs vary by location by time

2

The Lantau Group Confidential and Proprietary

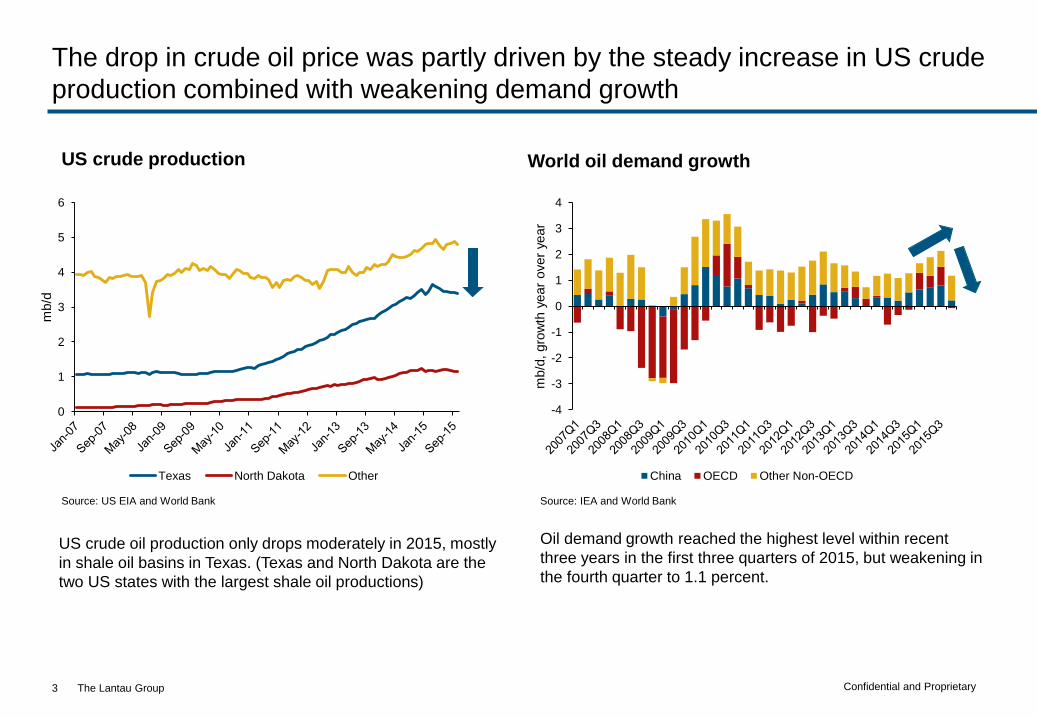

The drop in crude oil price was partly driven by the steady increase in US crude

production combined with weakening demand growth

3

Source: US EIA and World Bank

US crude production World oil demand growth

Source: IEA and World Bank

-4

-3

-2

-1

0

1

2

3

4

mb/d

, gro

wth

year

over

year

China OECD Other Non-OECD

0

1

2

3

4

5

6

mb/d

Texas North Dakota Other

US crude oil production only drops moderately in 2015, mostly

in shale oil basins in Texas. (Texas and North Dakota are the

two US states with the largest shale oil productions)

Oil demand growth reached the highest level within recent

three years in the first three quarters of 2015, but weakening in

the fourth quarter to 1.1 percent.

The Lantau Group Confidential and Proprietary

Forward price curves are still converging, but to a lower long-term level –

though the range is wide

4

Brent forward curve

Source: ICE

Dated Brent

($/barrel)

2013 (historical) 109

2014 (historical) 99

2015 (historical) 53

2016 (forecast) 32

2017 (forecast) 38

2018 (forecast) 42

2019 (forecast) 45

2020 (forecast) 47

0

20

40

60

80

100

120

140

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 2024

End 2009

USD/barrel

June 2014

End 2008

Sept 2014

October 2014

Feb 2015

June 2015

15 Jan 2016

End 2009

USD/barrel

June 2014

End 2008

Sept 2014

October 2014

Feb 2015

Dec 2015

Spot Brent

50 to 75

80 to 100 June ‘14 to Feb ‘15

June ‘15 to Jan ‘16

?

The Lantau Group Confidential and Proprietary

Lower prices are leading to delays in new gas development projects

5

2015 2016

3.6 Mtpa PNG T1

3.6 Mtpa PNG T2

5 Mtpa Australia Gorgon T1

5 Mtpa Gorgon T2

5 Mtpa GorgonT3

4.25 Mtpa Australia (Curtis) T1

2017

4.25 Mtpa Curtis T2

7.8 Mtpa Australia Gladstone T1,2

2.1 Mtpa Indonesia Donggi-Senoro

4.5 Mtpa Australia APLNG T1

2014

= coal seam gas projects

9 Mtpa Sabine Pass LNG

train 1 and 2 from US

9 Mtpa Sabine Pass LNG

train 3 and 4

2018

Originally planned commission date

Current low LNG prices pushed back new LNG projects

The Lantau Group Confidential and Proprietary

0

50

100

150

200

Most tariff reductions linked to fuel markets

Newcastle coal price FOB, USD per metric ton

0

50

100

150 Brent crude oil price, USD per barrel

Source: World Bank

Down>60%

Down>70%

The Lantau Group Confidential and Proprietary

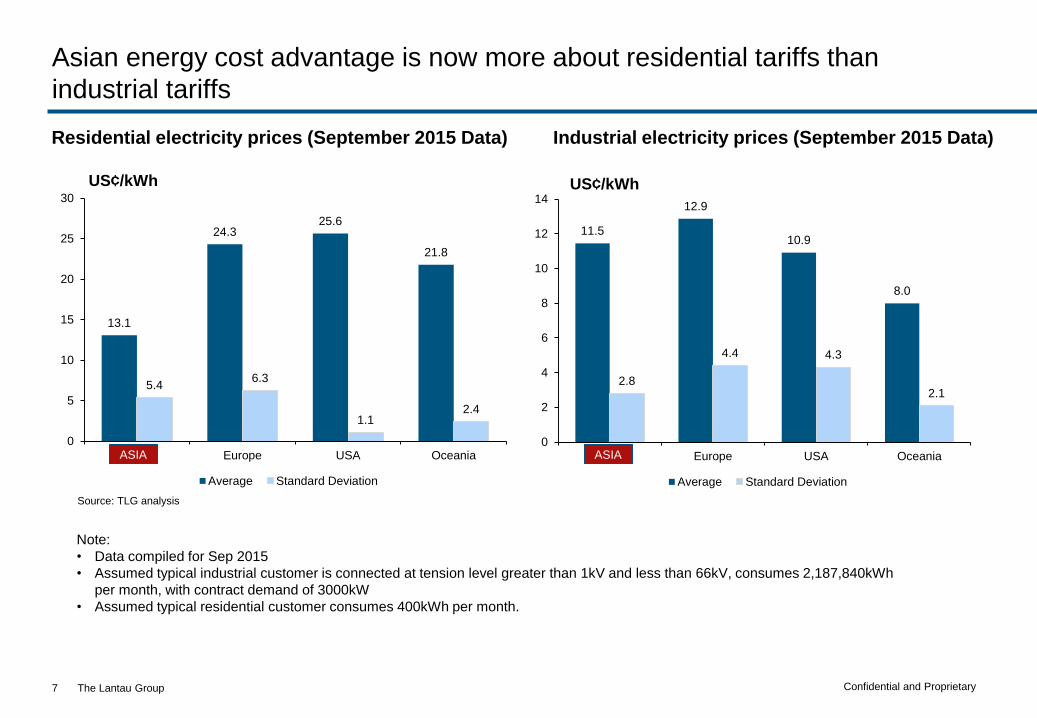

13.1

24.3 25.6

21.8

5.4 6.3

1.1 2.4

0

5

10

15

20

25

30

Aisa Europe USA Oceania

Average Standard Deviation

11.5

12.9

10.9

8.0

2.8

4.4 4.3

2.1

0

2

4

6

8

10

12

14

Aisa Europe USA Oceania

Average Standard Deviation

Asian energy cost advantage is now more about residential tariffs than

industrial tariffs

Note:

• Data compiled for Sep 2015

• Assumed typical industrial customer is connected at tension level greater than 1kV and less than 66kV, consumes 2,187,840kWh

per month, with contract demand of 3000kW

• Assumed typical residential customer consumes 400kWh per month.

Source: TLG analysis

Industrial electricity prices (September 2015 Data) Residential electricity prices (September 2015 Data)

US¢/kWh US¢/kWh

ASIA ASIA

7

The Lantau Group Confidential and Proprietary

China

8

The Lantau Group Confidential and Proprietary

Key factors affecting power cost in China

9

Reduction and control of coal

use in key cities

Gas/coal price/demand growth drops

More stringent environmental control costs

Promotion of Renewable

energy

Increasing transmission costs due to UHV builds

Upwards factors:

• Emissions control and

national ETS

• Renewable share

• Reduction of coal use

• UHV and grid expansion

Downwards factors:

• Fall of fuel prices

• Fall of project cost of

wind and solar

• Slowing growth of

demand

Opportunities from

market reform:

• Direct contracting

• Retail market opening

• Power plant dispatch

policies

The Lantau Group Confidential and Proprietary

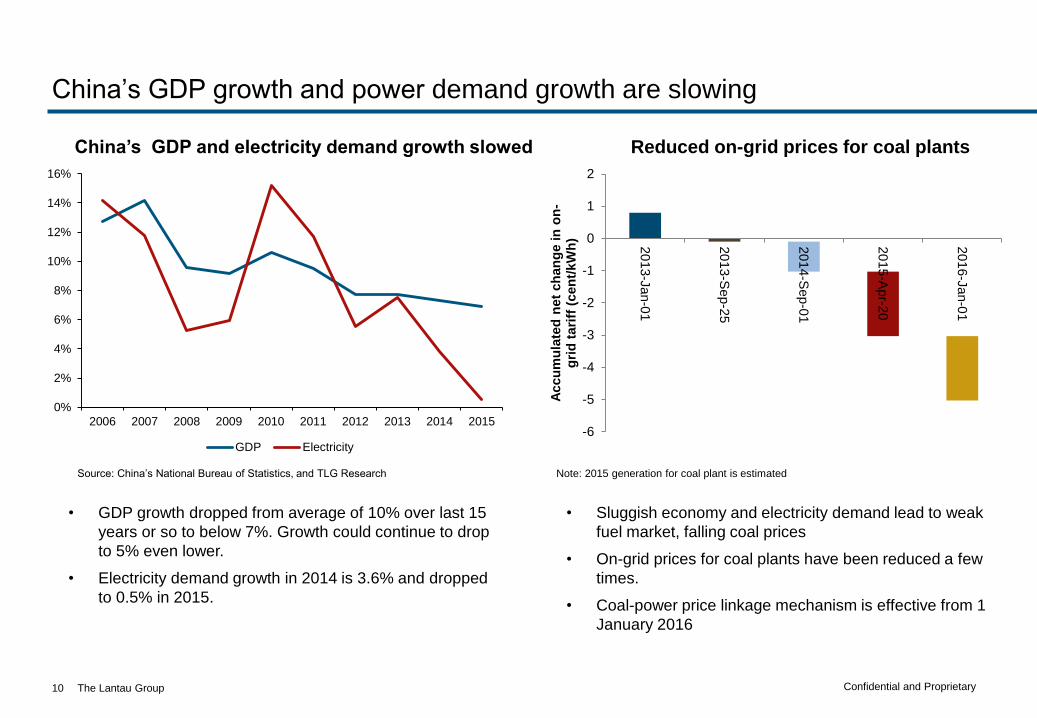

China’s GDP growth and power demand growth are slowing

10

0%

2%

4%

6%

8%

10%

12%

14%

16%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

GDP Electricity

China’s GDP and electricity demand growth slowed

Source: China’s National Bureau of Statistics, and TLG Research

• GDP growth dropped from average of 10% over last 15

years or so to below 7%. Growth could continue to drop

to 5% even lower.

• Electricity demand growth in 2014 is 3.6% and dropped

to 0.5% in 2015.

• Sluggish economy and electricity demand lead to weak

fuel market, falling coal prices

• On-grid prices for coal plants have been reduced a few

times.

• Coal-power price linkage mechanism is effective from 1

January 2016

Note: 2015 generation for coal plant is estimated

Reduced on-grid prices for coal plants

-6

-5

-4

-3

-2

-1

0

1

2

20

13-J

an-0

1

20

13-S

ep-2

5

20

14-S

ep-0

1

20

15-A

pr-2

0

20

16-J

an-0

1

Accu

mu

late

d n

et

ch

an

ge in

on

-g

rid

tari

ff (

cen

t/kW

h)

The Lantau Group Confidential and Proprietary

Environmental problems remain serious and more renewable energy targeted

11

Curtailment of wind and solar generation from

2013-2015

Source: NEA publications

National Climate Center

Days of

smog

Smoggy days of 74 cities in 2013

While the regions in the East, South and Central are perplexed by air quality problems, clean power generation of wind and solar in the west and north is being curtailed.

Transmission to link the regions is needed.

The Lantau Group Confidential and Proprietary

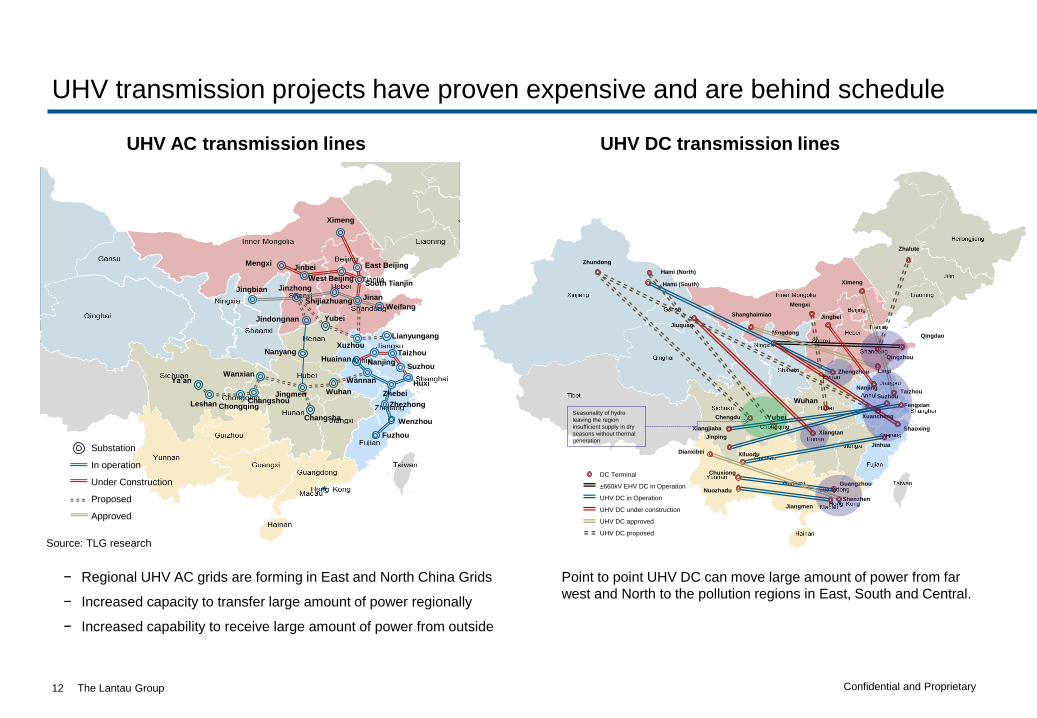

UHV transmission projects have proven expensive and are behind schedule

12

Ximeng

Mengxi

West BeijingSouth Tianjin

Weifang

JinanShijiazhuang

JinzhongJingbian

Jindongnan Yubei

Xuzhou

Nanjing

Taizhou

Suzhou

Huxi

Zhebei

Wannan

Huainan

Wuhan

Changsha

Nanyang

Substation

In operation

Under Construction

Proposed

Approved

Zhezhong

Ya’an

Leshan ChongqingChangshou

Wanxian

Fuzhou

Wenzhou

Jingmen

Jinbei East Beijing

Lianyungang

Source: TLG research

DC Terminal

±660kV EHV DC in Operation

UHV DC in Operation

UHV DC under construction

UHV DC approved

UHV DC proposed

Jinping

Nuozhadu

Jiangmen

Hami (South)

Taizhou

Ningdong

Shaoxing

Mengxi

Xiluodu

Jinhua

Ximeng

Wuhan

Zhengzhou

Xiangjiaba

Qingdao

Jiuquan

Xiangtan

Zhalute

Shanghaimiao

Fengxian

Qingzhou

Linyi

Suzhou

Shenzhen

Dianxibei

Chuxiong

Guangzhou

Zhundong

XuanchengChengdu Yubei

Hami (North)

Seasonality of hydro

leaving the region

insufficient supply in dry

seasons without thermal

generation

Jingbei

Nanjing

UHV AC transmission lines UHV DC transmission lines

− Regional UHV AC grids are forming in East and North China Grids

− Increased capacity to transfer large amount of power regionally

− Increased capability to receive large amount of power from outside

Point to point UHV DC can move large amount of power from far

west and North to the pollution regions in East, South and Central.

The Lantau Group Confidential and Proprietary

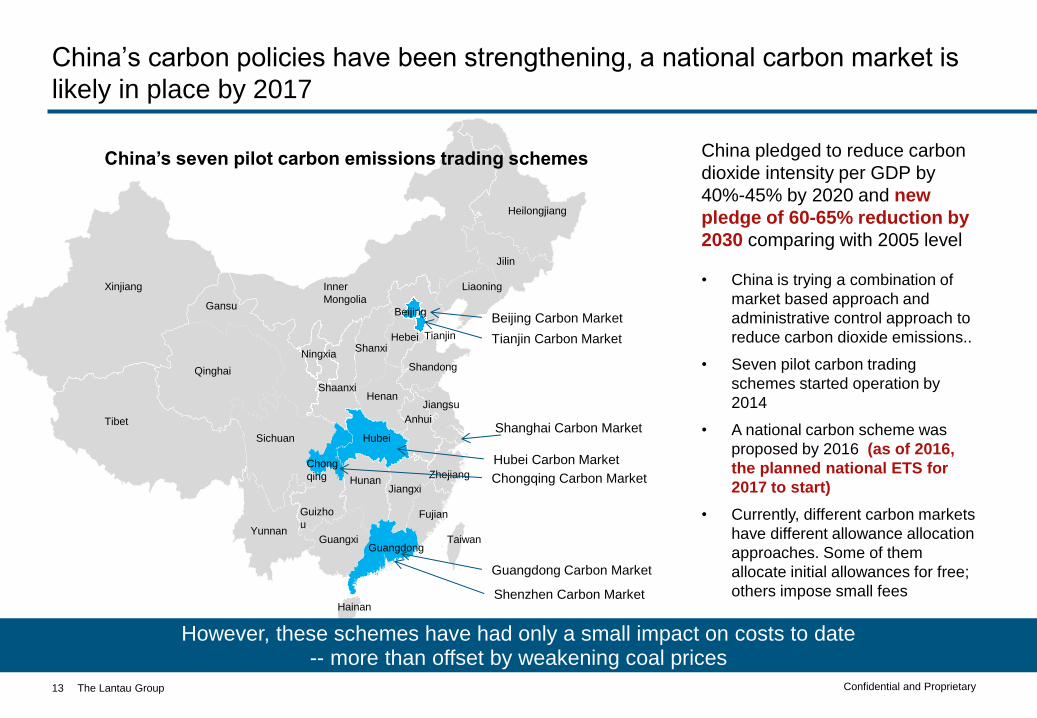

China’s carbon policies have been strengthening, a national carbon market is

likely in place by 2017

13

Xinjiang

Tibet

Qinghai

Gansu

Inner

Mongolia

Ningxia

Sichuan

Yunnan

Guizho

u

Chong

qing

Guangdong

Fujian

Taiwan

Jiangxi

Guangxi

Hunan

Hubei

Henan

Anhui

Jiangsu

Shandong

Liaoning

Jilin

Heilongjiang

Shanxi

Shaanxi

Hebei

Beijing

Zhejiang

Hainan

Beijing Carbon Market

Tianjin Carbon Market

Guangdong Carbon Market

Shenzhen Carbon Market

Shanghai Carbon Market

Chongqing Carbon Market

Hubei Carbon Market

China pledged to reduce carbon

dioxide intensity per GDP by

40%-45% by 2020 and new

pledge of 60-65% reduction by

2030 comparing with 2005 level

• China is trying a combination of

market based approach and

administrative control approach to

reduce carbon dioxide emissions..

• Seven pilot carbon trading

schemes started operation by

2014

• A national carbon scheme was

proposed by 2016 (as of 2016,

the planned national ETS for

2017 to start)

• Currently, different carbon markets

have different allowance allocation

approaches. Some of them

allocate initial allowances for free;

others impose small fees

However, these schemes have had only a small impact on costs to date -- more than offset by weakening coal prices

Tianjin

China’s seven pilot carbon emissions trading schemes

The Lantau Group Confidential and Proprietary

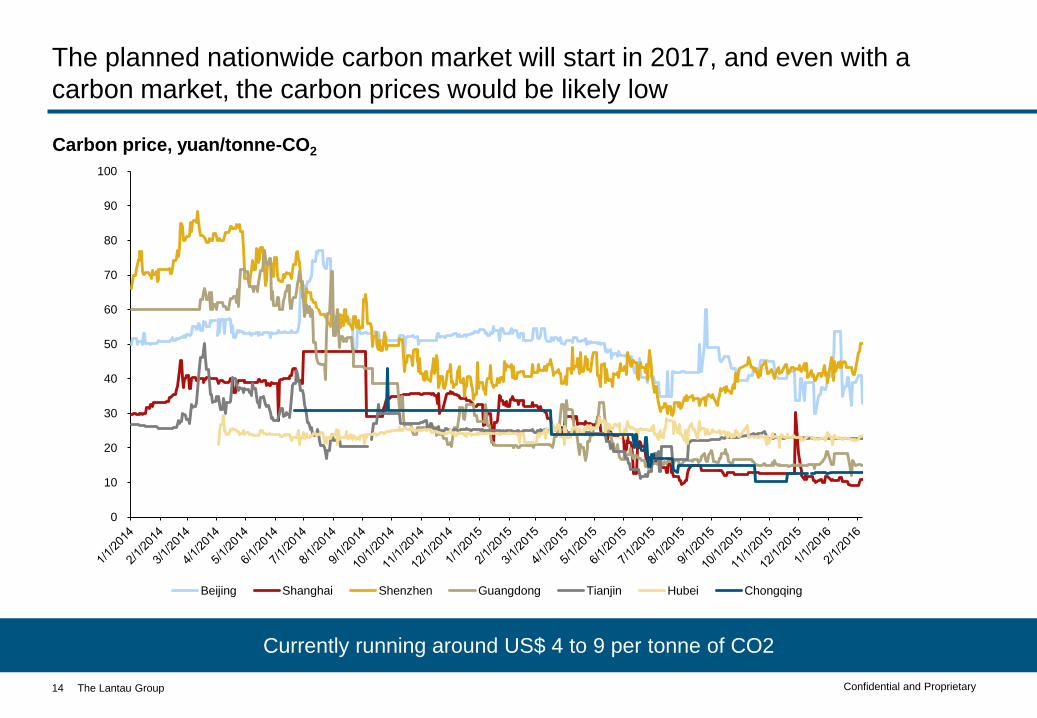

The planned nationwide carbon market will start in 2017, and even with a

carbon market, the carbon prices would be likely low

14

Currently running around US$ 4 to 9 per tonne of CO2

Carbon price, yuan/tonne-CO2

0

10

20

30

40

50

60

70

80

90

100

Beijing Shanghai Shenzhen Guangdong Tianjin Hubei Chongqing

The Lantau Group Confidential and Proprietary

China is reforming its energy and power industry, opportunities exist but…

15

Market reform implementation remains unclear

Network separation and separate transmission and distribution pricing

• Bilateral contracting between end users and generators is becoming possible;

• Changing regulation of transmission pricing already led to lower tariffs in Shenzhen, the pilot reform

Retail market opening

• Competition aimed to improve the efficiency of retailers

• Should increase choices of end-users and potentially lower prices

Reforming generation dispatch

• Increasing competition in the generation sector

• Supply cost reduction overall

The Lantau Group Confidential and Proprietary

Summary

• Dramatically weaker energy cost environment due to fuel market and macro factors

• Some delays to new gas and oil projects seen, some efforts to firm prices, and an upward

sloping oil forward curve

– But forecast is still well below levels projected even a year ago

• Asian electricity prices driven largely by fuel prices, fuel mix, and environmental concern

• Each market affected differently based on its fuel mix, reliance on imported fuels, and supply /

demand balance

16

The Lantau Group Confidential and Proprietary

Contact

Mike Thomas [email protected]

Xinmin Hu [email protected]

By phone +852 2521 5501 (office)

By mail 4602-4606 Tower 1, Metroplaza

223 Hing Fong Road,

Kwai Fong, Hong Kong

Online www.lantaugroup.com

Rigour

Value

Insight

Energy Power Utilities

17

Thank You

The Lantau Group Confidential and Proprietary

Fuel prices affect each Asian country differently – reflecting differences in fuel mix

and energy policy and regulation

18

Source: Various government sources

Generation fuel mix across countries

in 2013 and 2014 China

Coal generation share

was squeezed down by

hydro and other

renewables. More

renewable generation

means more levies on

end-users to pay

renewable generation. On

average, tariff increased in

2014 from 2013

Japan

More gas generation to

replace expensive oil

power generation, reducing

overall supply cost,

offsetting the replacement

cost of cheaper nuclear

generation. Tariff on

average reduced slightly in

2014 from 2013.

Australia

Lower hydro availability

was compensated by more

gas and renewable

generation, which are more

expensive. Tariffs

increased in 2014 from

2013, even gas price in

2014 was cheaper than in

2013.

Singapore

Expensive oil generation

was squeezed to 0.9%

from 5% by cheaper gas

generation. Tariff

decreased in 2014 from

2013

Australia (NSW) China Japan Singapore

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2013 2014 2013 2014 2013 2014 2013 2014

Coal Gas Oil Nuclear Hydro Other renewables Others

Local

Coal

Imported

Gas

Imported

Coal

Imported

Gas & Oil

The Lantau Group Confidential and Proprietary

0

20

40

60

80

100

120

140

160

0

100

200

300

400

500

600

700

800

900

1000

0

2000

4000

6000

8000

10000

12000

14000

16000

0

20

40

60

80

100

120

140

160

180

200

Brent oil price in Asian currencies compared to USD

19

Source: World Bank, Oanda

Down 71%

Brent crude oil price, USD per barrel Brent crude oil price, CNY per barrel

Brent crude oil price, SGD per barrel

Down 69%

Brent crude oil price, JPY per barrel

Down 66% Down 67%