supply chain disruption and innovation · supply chain disruption and ... • costs to make changes...

TRANSCRIPT

Supply chain disruption and innovation!

Professor John Manners-Bell, Chief Executive, Ti Insight!!October 2017!

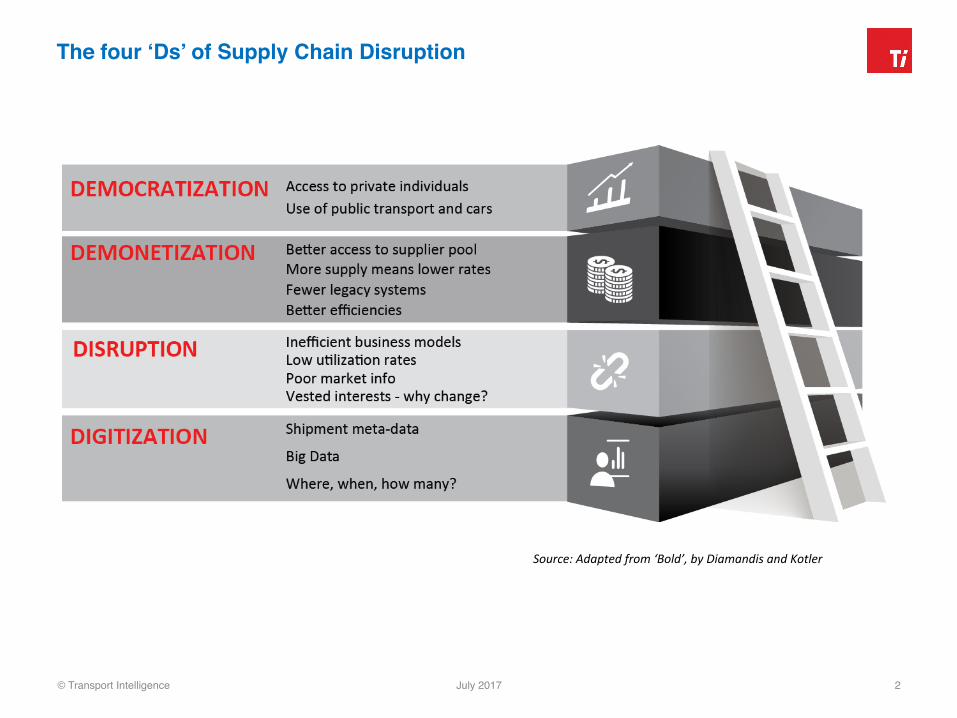

The four ‘Ds’ of Supply Chain Disruption!

© Transport Intelligence! July 2017! 2!

Source:Adaptedfrom‘Bold’,byDiamandisandKotler

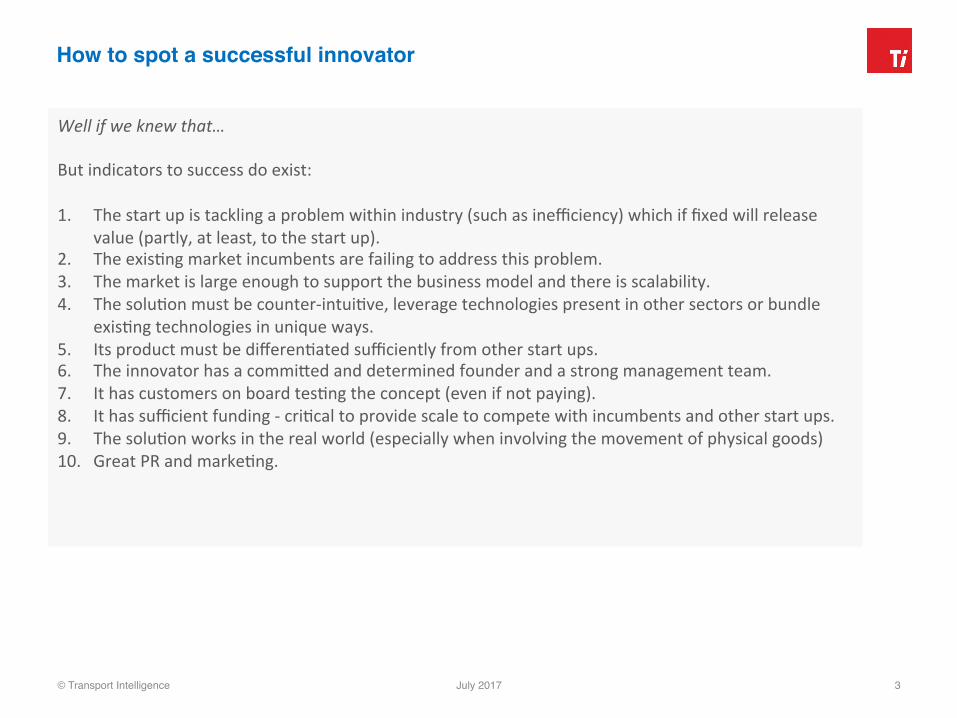

How to spot a successful innovator!

© Transport Intelligence! July 2017! 3!

Wellifweknewthat…Butindicatorstosuccessdoexist:1. Thestartupistacklingaproblemwithinindustry(suchasinefficiency)whichiffixedwillrelease

value(partly,atleast,tothestartup).2. TheexisDngmarketincumbentsarefailingtoaddressthisproblem.3. Themarketislargeenoughtosupportthebusinessmodelandthereisscalability.4. ThesoluDonmustbecounter-intuiDve,leveragetechnologiespresentinothersectorsorbundle

exisDngtechnologiesinuniqueways.5. ItsproductmustbedifferenDatedsufficientlyfromotherstartups.6. TheinnovatorhasacommiMedanddeterminedfounderandastrongmanagementteam.7. IthascustomersonboardtesDngtheconcept(evenifnotpaying).8. Ithassufficientfunding-criDcaltoprovidescaletocompetewithincumbentsandotherstartups.9. ThesoluDonworksintherealworld(especiallywheninvolvingthemovementofphysicalgoods)10. GreatPRandmarkeDng.

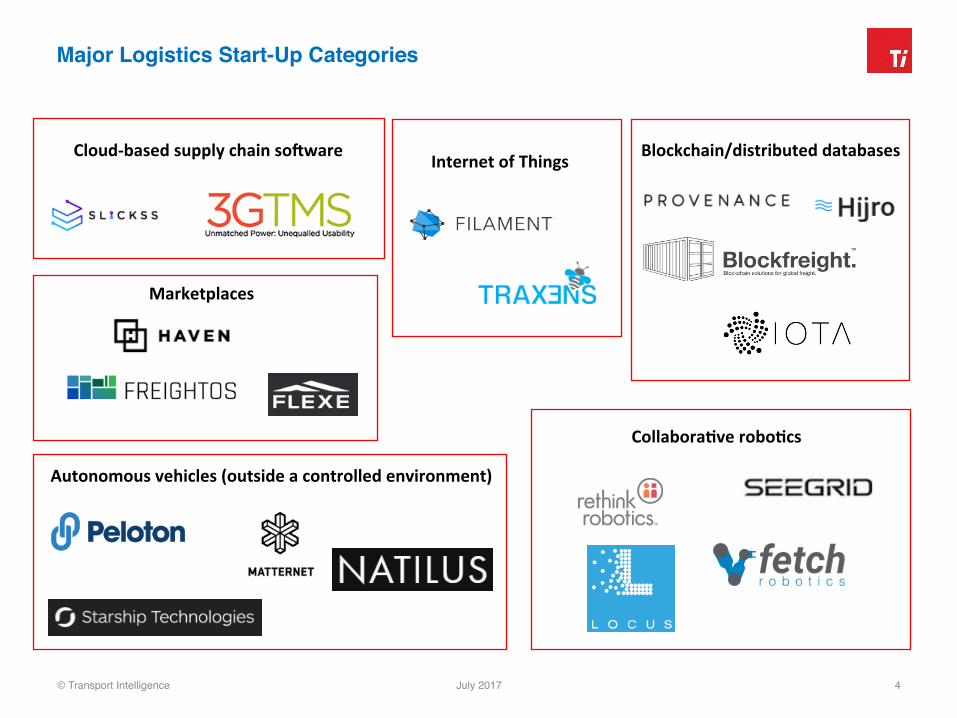

Major Logistics Start-Up Categories!

© Transport Intelligence! July 2017! 4!

Cloud-basedsupplychainso2ware

Marketplaces

Blockchain/distributeddatabasesInternetofThings

Autonomousvehicles(outsideacontrolledenvironment)

CollaboraCveroboCcs

European road freight marketplaces!

© Transport Intelligence! July 2017! 5!

• ThebigproblemwithEuropeanroadfreightmarketplacesisthatthereisliMletodifferenDateonefromoneanother.

• TradiDonal‘freightexchanges’havematchedloadsandsparecapacityformanyyears–theonlydifferencewiththelatestgeneraDonofmarketplacesisthattheseservicesmakeuseofsmartphones.

• Inordertobesuccessful,thesebusinessesneedtomaintainbothaneffecDveserviceandalargesupplyofdrivers.

• However,ascompeDDoncommodiDsesthebasicload-matchingservicetheyprovide,shippersrisklowqualityserviceandcarriersrisklowpay–itbecomesaracetotheboMombasedonprice.

• Thesuccessfulcompaniesbuildingonthemarketplaceideawillbemobile-enabledservicebusinesses,notjustatechnologicallayer.

• NetworkeffectsarecriDcaltosuccess.Theseoccurwhenaservicebecomesmorevaluabletoitsusersasmorepeopleadoptit,creaDngbarrierstoentryforrivals,andbarrierstoexitforusers.

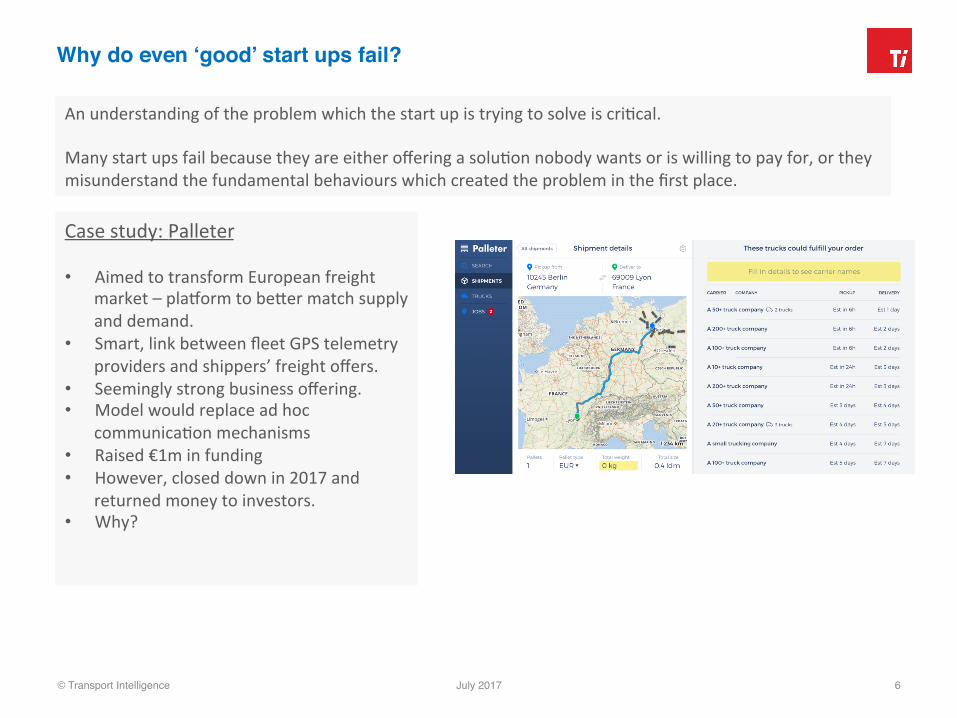

Why do even ‘good’ start ups fail?!

© Transport Intelligence! July 2017! 6!

Casestudy:Palleter• AimedtotransformEuropeanfreight

market–pla^ormtobeMermatchsupplyanddemand.

• Smart,linkbetweenfleetGPStelemetryprovidersandshippers’freightoffers.

• Seeminglystrongbusinessoffering.• Modelwouldreplaceadhoc

communicaDonmechanisms• Raised€1minfunding• However,closeddownin2017and

returnedmoneytoinvestors.• Why?

AnunderstandingoftheproblemwhichthestartupistryingtosolveiscriDcal.ManystartupsfailbecausetheyareeitherofferingasoluDonnobodywantsoriswillingtopayfor,ortheymisunderstandthefundamentalbehaviourswhichcreatedtheprobleminthefirstplace.

Palleter: lessons for other innovators!

© Transport Intelligence! July 2017! 7!

Despitethe‘neat’soluDonaddressingamajorindustryproblematamacrolevel,operaDonalandtechnologicalproblemswerenotaddressed.Technology

• CompanieswereunwillingtospendmoneyandDmeondataextracDonfromtheirexisDngsystems• ITdepartmentswerefocusedonkeepingexisDngsystemsrunning,notonnewiniDaDves.• NobodywillingtogambleonreplacinglegacysystemswithnewoperaDonspla^orms.• ComplexityofdatasharingbetweensupplypartnersunderesDmated.

OperaDonal• Muchofthevauntedsparecapacityontruckswas,inreality,notaccessible.• Companieswereunwillingtore-routetrucksevenshortdistances• Pla^ormrequiredcooperaDonofexisDngplayersandculturalshig

EventhoughaproblemhadbeenidenDfied,Palleter’ssoluDononlyovercamesomeofthechallenges.ItssoluDondidnotfactorintruecostofitsusersandopposiDontochangeatgrassrootslevel.

‘Start up’ value ratio!

© Transport Intelligence! July 2017! 8!

Doestheloadmatchingpla^ormoffercompellingvalueforbothsuppliersandshippers?

StartUpValue=Perceivedbenefits/TotalcostPerceivedbenefits=Valueofincreasedloadsforsuppliers,lowerratesforshippersTotalcost=chargeforusingservice(negligible,inPalleter’sesDmaDon)BUTPalleterunder-esDmatedtangibleandintangiblecostsforsuppliers(andhenceshippers)Totalcostshouldhaveincluded:• coststomakechangestosuppliers’andshippers’technologysystemsaswellasmanagementDme• intangiblecostssuchaschangingoperaDngpracDces(andunwillingnesstoadoptnewoperaDng

models)• Dmetakentore-routetrucks

Theresultwas:• notenoughuserstocreatecompeDDvemarket• higherpricesonPalleterthanonopenmarket• incumbents(suchasDSV)wereactuallymorepricecompeDDveforlessefficienttransport.

Creating a defensible freight exchange!

© Transport Intelligence! July 2017! 9!

• TruckerPathofferscrowd-sourcedguidancetotruckdrivers;thisincludesthenearesttruckstop,weighstaDons,hotels,dieselfuelandfreightshipments.

• Freightshipmentsaremanagedthroughamarketplacesystemforregionalorlong-haulbusiness,wherebrokerssubmitshipmentsalongwithdeadlines,desDnaDonsandotherrequirements,withparkingandnavigaDoninformaDontolong-haultruckersintheUS.

• ThecompanyiniDallylaunchedasafreeinformaDonserviceapp,beforesubsequentlyaddingthefreightmarketplace.Assuch,thebusinesshadculDvatedacommunityofusers,andhasbuiltoutitsmarketplaceasanaddiDonalservicewithinawiderecosystem.

• Furthermore,TruckerPathhasbeensuccessfulinaddingapaymentsservice‘InstaPay’.Thisnon-recoursefactoringarrangementpayscarriersimmediately,issuingaone-Dmeflatratewithnohiddenfees,andaddressesamajorpainpointamongstcarrierswhoogenwait30-60daysbeforereceivingpayment.

• Intotal,TruckerPathclaimstoserve550,000longhaultruckersintheUS,outofatotalofroughly1.6m.Thecompany’smarketplacebusiness,‘Truckloads’,servessubstanDallyless(around100,000with3mmonthlyloadposDngs),butbygainingtracDonamongstthepopulaDonoflong-hauldriversintheUS,thecompanyhasestablishedadefensibleposiDon.

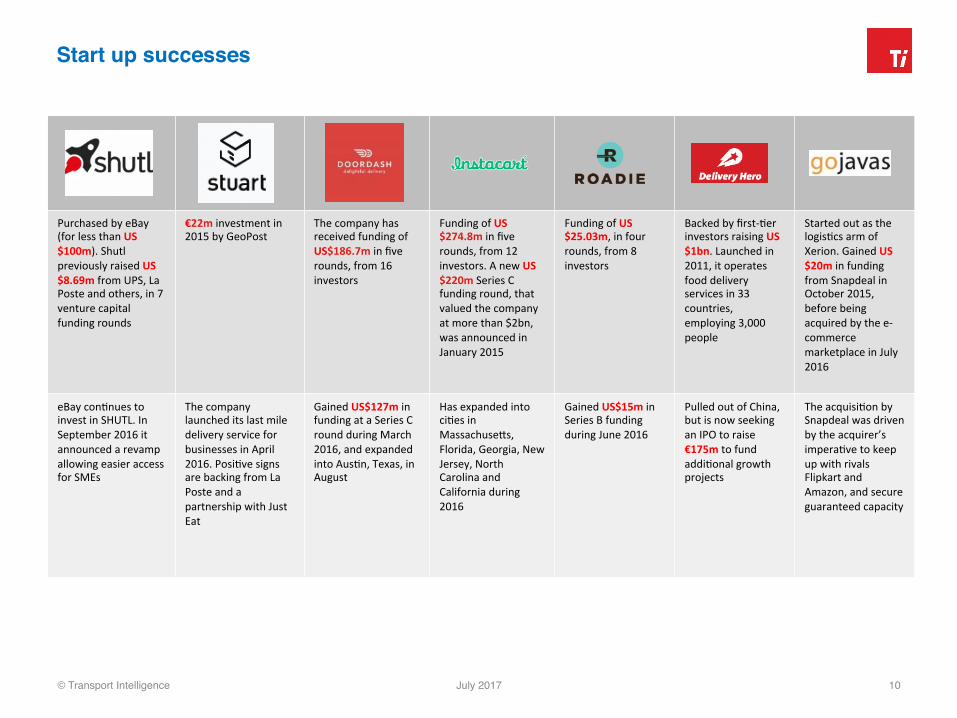

Start up successes!

© Transport Intelligence! July 2017! 10!

PurchasedbyeBay(forlessthanUS$100m).ShutlpreviouslyraisedUS$8.69mfromUPS,LaPosteandothers,in7venturecapitalfundingrounds

€22minvestmentin2015byGeoPost

ThecompanyhasreceivedfundingofUS$186.7minfiverounds,from16investors

FundingofUS$274.8minfiverounds,from12investors.AnewUS$220mSeriesCfundinground,thatvaluedthecompanyatmorethan$2bn,wasannouncedinJanuary2015

FundingofUS$25.03m,infourrounds,from8investors

Backedbyfirst-DerinvestorsraisingUS$1bn.Launchedin2011,itoperatesfooddeliveryservicesin33countries,employing3,000people

StartedoutasthelogisDcsarmofXerion.GainedUS$20minfundingfromSnapdealinOctober2015,beforebeingacquiredbythee-commercemarketplaceinJuly2016

eBayconDnuestoinvestinSHUTL.InSeptember2016itannouncedarevampallowingeasieraccessforSMEs

ThecompanylauncheditslastmiledeliveryserviceforbusinessesinApril2016.PosiDvesignsarebackingfromLaPosteandapartnershipwithJustEat

GainedUS$127minfundingataSeriesCroundduringMarch2016,andexpandedintoAusDn,Texas,inAugust

HasexpandedintociDesinMassachuseMs,Florida,Georgia,NewJersey,NorthCarolinaandCaliforniaduring2016

GainedUS$15minSeriesBfundingduringJune2016

PulledoutofChina,butisnowseekinganIPOtoraise€175mtofundaddiDonalgrowthprojects

TheacquisiDonbySnapdealwasdrivenbytheacquirer’simperaDvetokeepupwithrivalsFlipkartandAmazon,andsecureguaranteedcapacity

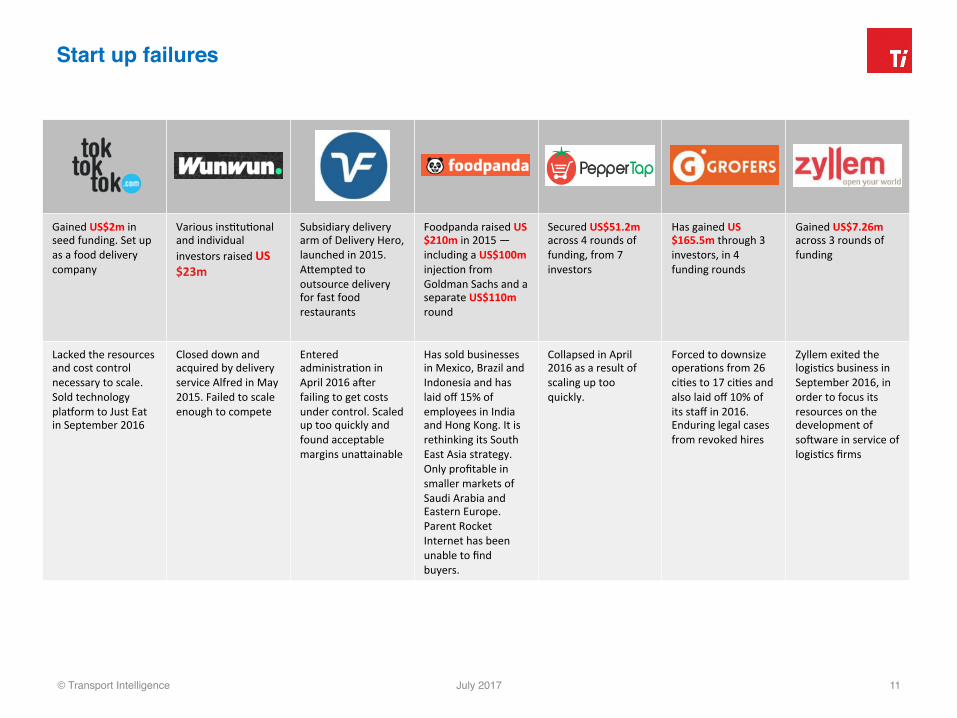

Start up failures!

© Transport Intelligence! July 2017! 11!

GainedUS$2minseedfunding.Setupasafooddeliverycompany

VariousinsDtuDonalandindividualinvestorsraisedUS$23m

SubsidiarydeliveryarmofDeliveryHero,launchedin2015.AMemptedtooutsourcedeliveryforfastfoodrestaurants

FoodpandaraisedUS$210min2015—includingaUS$100minjecDonfromGoldmanSachsandaseparateUS$110mround

SecuredUS$51.2macross4roundsoffunding,from7investors

HasgainedUS$165.5mthrough3investors,in4fundingrounds

GainedUS$7.26macross3roundsoffunding

Lackedtheresourcesandcostcontrolnecessarytoscale.Soldtechnologypla^ormtoJustEatinSeptember2016

CloseddownandacquiredbydeliveryserviceAlfredinMay2015.Failedtoscaleenoughtocompete

EnteredadministraDoninApril2016agerfailingtogetcostsundercontrol.ScaleduptooquicklyandfoundacceptablemarginsunaMainable

HassoldbusinessesinMexico,BrazilandIndonesiaandhaslaidoff15%ofemployeesinIndiaandHongKong.ItisrethinkingitsSouthEastAsiastrategy.OnlyprofitableinsmallermarketsofSaudiArabiaandEasternEurope.ParentRocketInternethasbeenunabletofindbuyers.

CollapsedinApril2016asaresultofscalinguptooquickly.

ForcedtodownsizeoperaDonsfrom26ciDesto17ciDesandalsolaidoff10%ofitsstaffin2016.Enduringlegalcasesfromrevokedhires

ZyllemexitedthelogisDcsbusinessinSeptember2016,inordertofocusitsresourcesonthedevelopmentofsogwareinserviceoflogisDcsfirms

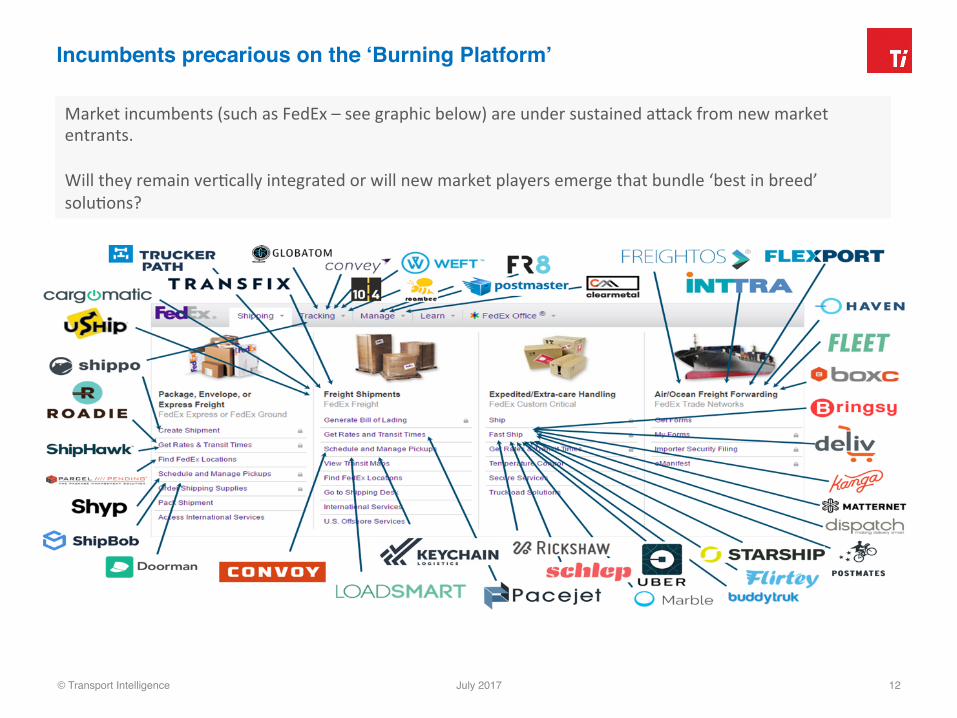

Incumbents precarious on the ‘Burning Platform’!

© Transport Intelligence! July 2017! 12!

Marketincumbents(suchasFedEx–seegraphicbelow)areundersustainedaMackfromnewmarketentrants.WilltheyremainverDcallyintegratedorwillnewmarketplayersemergethatbundle‘bestinbreed’soluDons?

!

© Transport Intelligence! July 2017! 13!

• Foundedin2013byCEORyanPetersen• VCfundingof$94minlastfouryears(spentonR&D,recruitmentandtraining)• 4officesinUS;2inAsiaand1inEurope• 280employees• Planstocreate25crossdockfaciliDesformergeintransitservices• CEOexpectstobeTop20NVOCContranspacificlanesbyendof2017

FlexportisparttradiDonalforwarderandparttechnologycompany.Itrealisesthatforwardingisnotacommodity,butatthesameDmecanusetechnologytoimprovedecision-makingthroughincreasedvisibility.‘…forwardingfirst,codingsecond’SuiteofdigiDzedservicesinclude:• Palletlevelvisibility• Compliance• Truckingcompanypla^orm• Purchaseordermanagement

• SMEsalargeproporDonofFlexport’scustomersusingself-serviceinterface• ManycustomerssellingonAmazonorfast-growinge-commercecompanies• China-USabigmarket• PredictabilityfundamentaltoFlexport’srelaDonswithairandoceancarriers• Aimstobe‘premiumprovider’

E-Commerce Challenges and Opportunities!

0%

10%

20%

30%

40%

50%

60%

2008 2009 2010 2011 2012 2013 2014 2015 2016 2019

JohnLewisOnlineSalesas%ofTotal

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

JohnLewisOnlineSalesY-o-Y-BlackFridayWeek

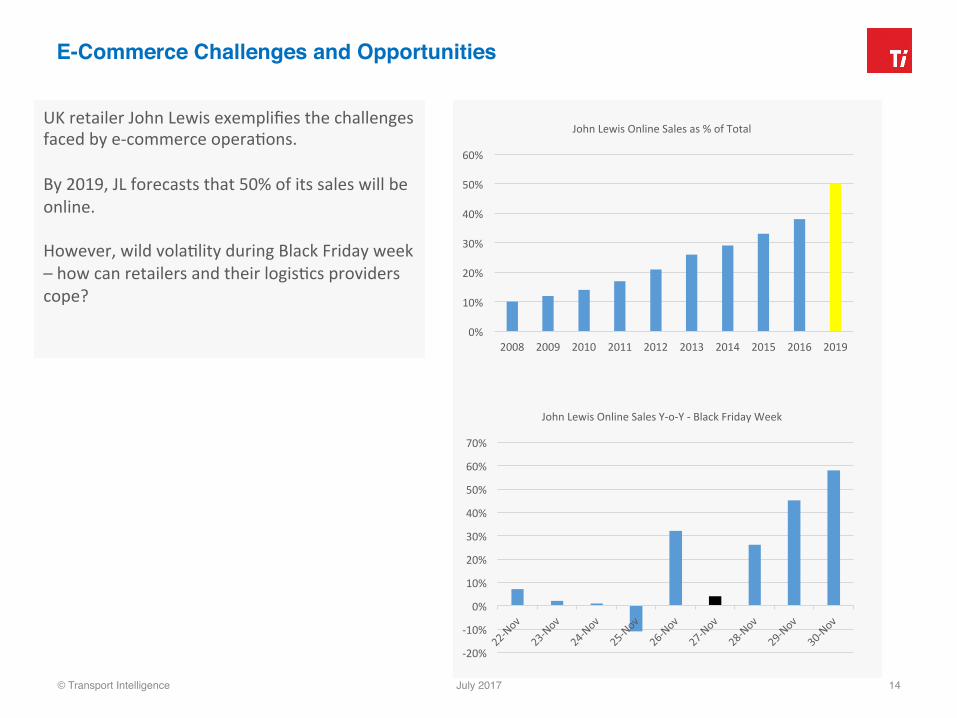

UKretailerJohnLewisexemplifiesthechallengesfacedbye-commerceoperaDons.By2019,JLforecaststhat50%ofitssaleswillbeonline.However,wildvolaDlityduringBlackFridayweek–howcanretailersandtheirlogisDcsproviderscope?

© Transport Intelligence! July 2017! 14!

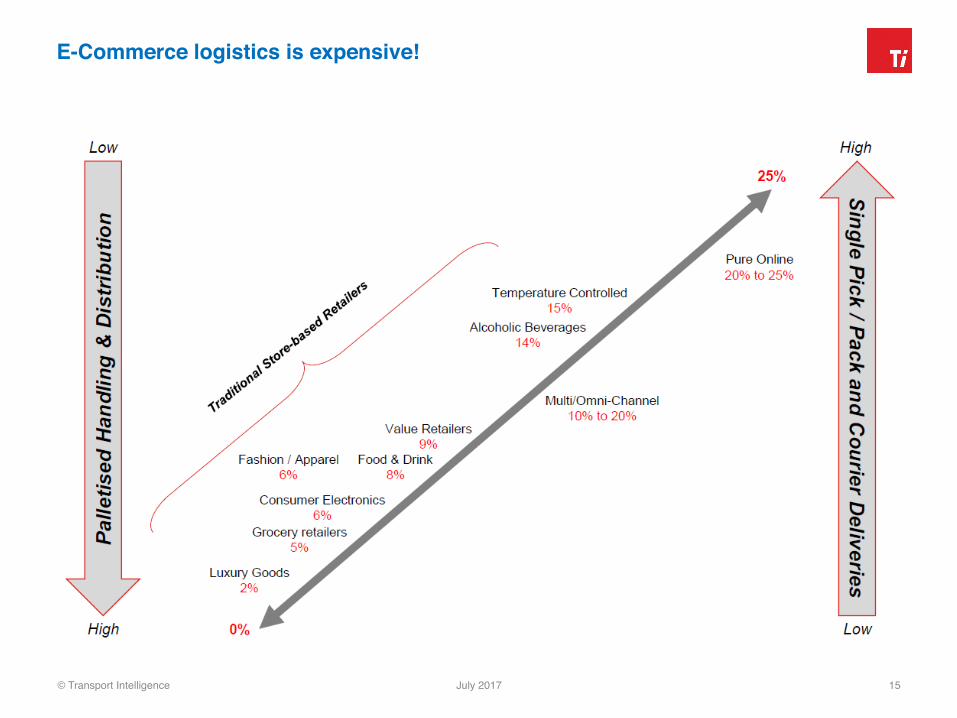

E-Commerce logistics is expensive!!

© Transport Intelligence! July 2017! 15!

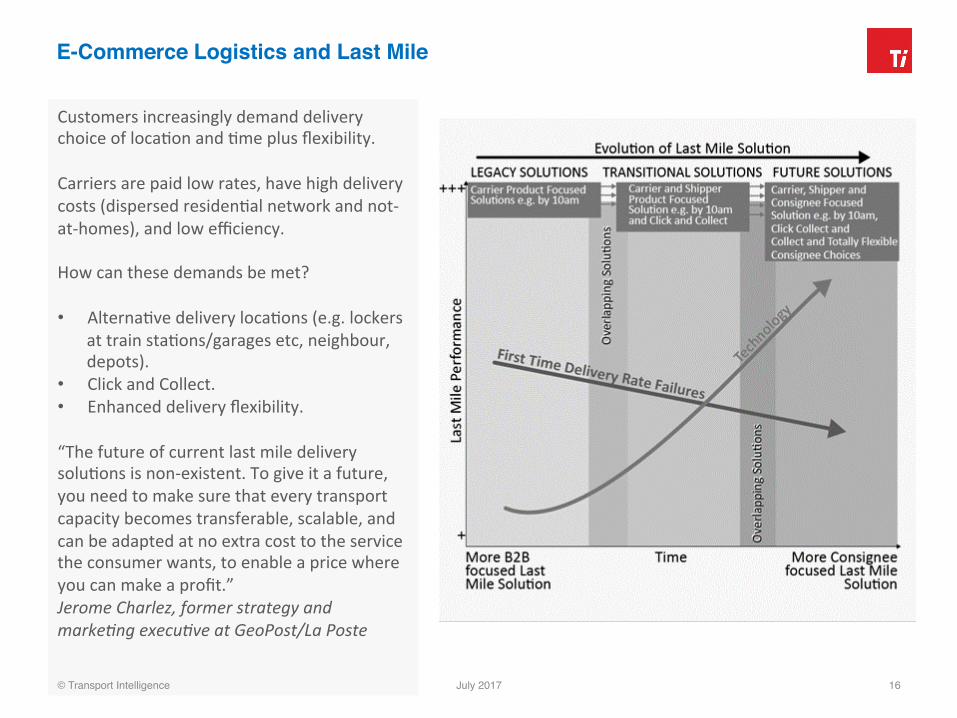

E-Commerce Logistics and Last Mile!

CustomersincreasinglydemanddeliverychoiceoflocaDonandDmeplusflexibility.Carriersarepaidlowrates,havehighdeliverycosts(dispersedresidenDalnetworkandnot-at-homes),andlowefficiency.Howcanthesedemandsbemet?• AlternaDvedeliverylocaDons(e.g.lockers

attrainstaDons/garagesetc,neighbour,depots).

• ClickandCollect.• Enhanceddeliveryflexibility.“ThefutureofcurrentlastmiledeliverysoluDonsisnon-existent.Togiveitafuture,youneedtomakesurethateverytransportcapacitybecomestransferable,scalable,andcanbeadaptedatnoextracosttotheservicetheconsumerwants,toenableapricewhereyoucanmakeaprofit.”JeromeCharlez,formerstrategyandmarkeEngexecuEveatGeoPost/LaPoste

© Transport Intelligence! July 2017! 16!

Last Mile Solutions Case Studies!

© Transport Intelligence! July 2017! 17!

Urbantz• Belgium-basedfirstandlastmiledelivery

cloudsogware• Raisedapproximately€750k• SavingDmebyincreasingdelivery

efficiencyofparcelsrounds• AutomaDcallyorderingdeliveryschedule

andinformingdrivervia• RealDmeend-to-endtracking• Improveefficiency‘byupto50%’–from

140ordersperdayto210(atpeak)• Negligibletrainingrequired• Believedtobedevelopingdynamic

deliveryopDons–geofencingofend-recipients.

‘Stuart’(acquiredbyLaPoste)• DisrupDveon-demanddeliveryappand

pla^ormdesignedforCityLogisDcs.• Foundedin2015inParisandBarcelona.• Backedby€22Mininvestment,Stuartis

buildingoutitsurbanlogisDcspla^ormacrossEurope:London,Brussels,Berlin,Madrid.

• Operatesnetworksofself-employedcouriers.

• Samehourdelivery.• ‘AmazonPrimeNowforlocalstores’• Notjustfood(peaksandtroughsfor

couriers)–deliveryallday.• GeoPostearlyinvestor(22%in2015)but

now100%owner.

Strategy• ProvideSMEcouriercompanieswith

‘corporatequality’TMScapabiliDes.

Strategy• Enableincumbenttotestlastmile

technologiesandbusinessmodelbeforeenteringmarket.

Consolidation in the on-demand delivery sphere!

© Transport Intelligence! July 2017! 18!

• ThecriDcalquesDonforcompaniesprovidingon-demanddeliveryservicesiswhetherornotthereisalargeenoughmarkettosupportthem.

• Inordertomakeaprofit,businesseslikeDeliverooneedtohaveahighfrequencyoforderswithinanoperaDonalarea,andifthisfrequencydropsbelowacertainrate,theuniteconomicsoftheserviceareunworkable.

• Therearetwomaincausesofthis:• Themarketwasneverlargeenoughtosupporttheserviceinthefirstplace• CompeDDonfromrivalserviceprovidershasdilutedmarketshare

• SolongascompeDngstart-upspossessthefundingtoexpandtheirbusiness,thelaMerissuecanbeaddressedbypricingincenDvesforbothcouriersandconsumersinordertobuildeffecDveeconomiesofscale.

• Thisinevitablyresultsinfinanciallosses,forcingstart-upsinacompeDDvemarkettomaketoughchoiceswhenthemoneybeginstorunout.

• ConsolidaDonamongsttheexisDngcompaniesisinevitable,throughM&Aandbankruptcy.Duetothegeographicalnatureofthismarket,itislikelythatcertaincompanieswilldominateincertaincountries;DidiChuxinginChinaversusUberintheUSA,forexample.

Sharing Economy and Crowdshipping!

TransportaDonservicesarehighlyinefficient:29%HGVsrunningempty(FTA).Thankstotheadvancesinmobiletechnologies,independentcontractorscannowbelinkedmoreefficientlywhichinthecaseofUber,couldresultindisintermediaDonoflegacycarriers.Wal-martnowpiloCngtheuseofemployeestoundertakedeliveries

NetworkconnectedmobiledevicesareverypowerfulcommunicaDonandsensorpla^orms.

Theyarethemeanstoengageeverypartyinthechain.AlloftheparDescanbecombinedintoavirtualpartnershiptaskedwithdeliveringtheservicetothecustomer.

TheyhavebeenuDlizedbydisruptorssuchasUbertochallengeregulatedsectorssuchastaxis–butnowalsotransportaDon.

© Transport Intelligence! July 2017! 19!

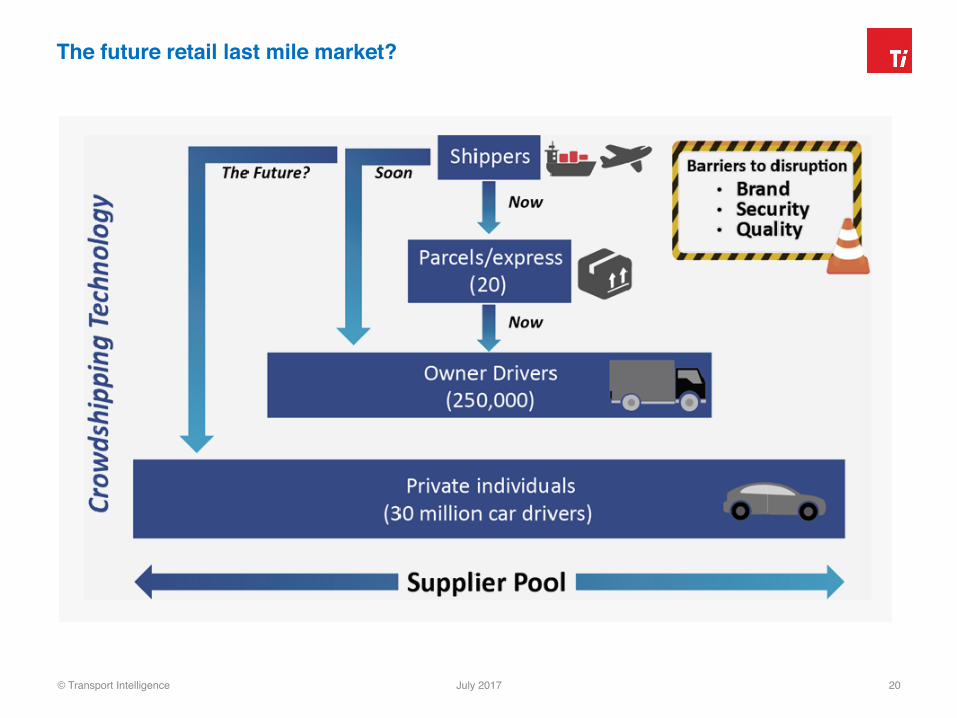

The future retail last mile market?!

© Transport Intelligence! July 2017! 20!

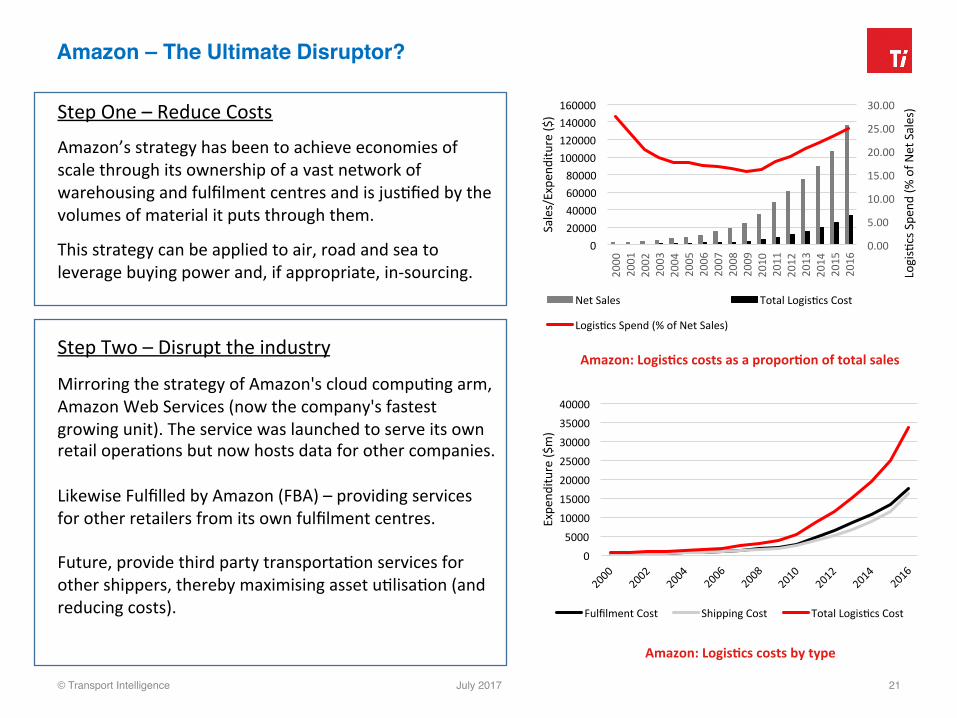

Amazon – The Ultimate Disruptor?!

© Transport Intelligence! July 2017! 21!

StepOne–ReduceCosts

Amazon’sstrategyhasbeentoachieveeconomiesofscalethroughitsownershipofavastnetworkofwarehousingandfulfilmentcentresandisjusDfiedbythevolumesofmaterialitputsthroughthem.

Thisstrategycanbeappliedtoair,roadandseatoleveragebuyingpowerand,ifappropriate,in-sourcing.StepTwo–Disrupttheindustry

MirroringthestrategyofAmazon'scloudcompuDngarm,AmazonWebServices(nowthecompany'sfastestgrowingunit).TheservicewaslaunchedtoserveitsownretailoperaDonsbutnowhostsdataforothercompanies.LikewiseFulfilledbyAmazon(FBA)–providingservicesforotherretailersfromitsownfulfilmentcentres.Future,providethirdpartytransportaDonservicesforothershippers,therebymaximisingassetuDlisaDon(andreducingcosts).

Amazon:LogisCcscostsasaproporConoftotalsales

Amazon:LogisCcscostsbytype

0

5000

10000

15000

20000

25000

30000

35000

40000

Expe

nditu

re($

m)

FulfilmentCost ShippingCost TotalLogisDcsCost

0.00

5.00

10.00

15.00

20.00

25.00

30.00

020000400006000080000

100000120000140000160000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

LogisDcsSpe

nd(%

ofN

etSales)

Sales/Expe

nditu

re($

)

NetSales TotalLogisDcsCost

LogisDcsSpend(%ofNetSales)

Amazon – Logistics strategy!

© Transport Intelligence! July 2017! 22!

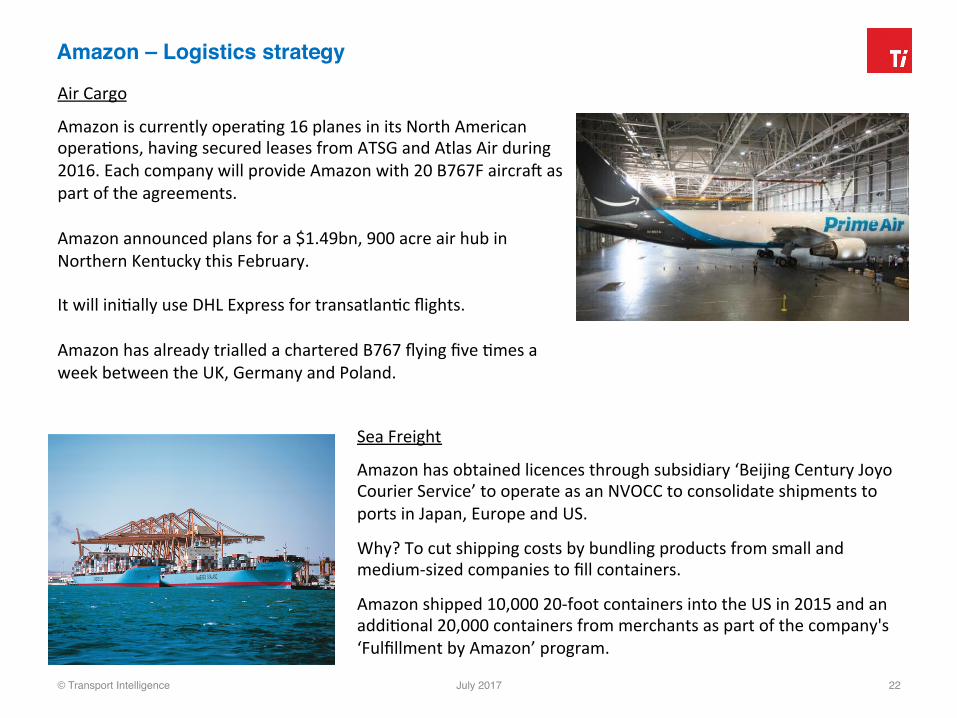

AirCargo

AmazoniscurrentlyoperaDng16planesinitsNorthAmericanoperaDons,havingsecuredleasesfromATSGandAtlasAirduring2016.EachcompanywillprovideAmazonwith20B767Faircragaspartoftheagreements.

Amazonannouncedplansfora$1.49bn,900acreairhubinNorthernKentuckythisFebruary.ItwilliniDallyuseDHLExpressfortransatlanDcflights.AmazonhasalreadytrialledacharteredB767flyingfiveDmesaweekbetweentheUK,GermanyandPoland.

SeaFreight

Amazonhasobtainedlicencesthroughsubsidiary‘BeijingCenturyJoyoCourierService’tooperateasanNVOCCtoconsolidateshipmentstoportsinJapan,EuropeandUS.

Why?Tocutshippingcostsbybundlingproductsfromsmallandmedium-sizedcompaniestofillcontainers.

Amazonshipped10,00020-footcontainersintotheUSin2015andanaddiDonal20,000containersfrommerchantsaspartofthecompany's‘FulfillmentbyAmazon’program.

Amazon – Last Mile!

© Transport Intelligence! July 2017! 23!

StrategytoverDcallyintegratetransportservicesinsomemarketswhereitseespotenDaltodrivedowncosts.Actas4PLinothers.

US• AmazonPrimeFresh(groceries)ownsdeliveryfleets

insomestates• PrimeNowtrucksinselectedciDes• Amazonrestaurants–mealdeliveryservice• AmazonPrimeSame-Day• AmazonFlex–Uber-Cargolikeservice• Ownsandoperatestrailersfortrunkingbetween

AmazonfaciliDes

France• Amazonholds25%ofColisPrivé,ahomedelivery

companywith2,000sub-contractorsandvolumesof35millionparcels.FullacquisiDonblockedoncompeDDongrounds.

UK• Amazonoperatesatleast24deliverydepotsinthe

UK,whichareoperatedbyAmazonLogisDcs–thisdisintermediatestransportoperaDonstouDlisearound45smallandregionalplayers

Germany

• AmazonhasopenedasorDngcentreinMunich,employing130workersasafirststeptocutoutlargerparcelscompanies(DHLandHermes).Alsoestablishingparcellockernetwork.

• InMunich,Amazonnowhas240deliveryvansoperatedbysixsub-contractors.Onlaunch,thisoperaDontookathirdofDHL'svolumesinMunich.

• Amazonisnotonlylookingatmovingitsowngoods.‘Weknowwe’reverygoodatlogisDcs.Whyshouldn’tweturnthatintoaninfrastructureofferthatotherscanuse?’-RoyPerDcucci,Amazon’sEuropeanheadoflogisDcs.

Next steps: Groceries and Fashion supply chains!

© Transport Intelligence! July 2017! 24!

WholefoodsacquisiDon

• AmazonentersbricksandmortargroceryretailingpredominantlyintheUS.

• DeploybothitslogisDcsandtechnologyinfrastructure.

• HelpWholeFoodsdevelop,drivingdowncostsandsalesup.

• PotenDalhomedeliveryand‘PrimeNow’• In-store‘clickandcollect’capabiliDes.• Dronedispatchpoints?• ThespringboardtofurtheracquisiDons–

especiallyintherestofworld?

AmazonPrimeWardrobe

• Pickbetween3-15items.• Tryonforupto7days• Freepickupofreturnedclothes• Keep5ormorefor20%discount• FreeserviceforPrimemembers• Onlinefashionfastgrowingmarket–17%of

allonlinespend.• ImplicaDonsforreverselogisDcs–increasein

costs.AmazonFashion

• End-to-endsupplychainapproach• OtheriniDaDves:‘Stylecheck’throughthe

EchoLookdevice(Alexa-enabledcamera)tocreatea‘personallookbook’.

• Amazonfilespatentdesignforon-demandapparelmanufacturingfacility.

Blockchain in Supply Chains!

© Transport Intelligence! July 2017! 25!

• Theblockchainisapermanentdigitalrecord(orledger)oftransacDonsthatisstoredacrossadistributednetworkofcomputers.

• ThewayitoperatesavoidsduplicaDonandisalmostimpossibletomodifyorspoofbyunauthorizedparDes.

• Althoughthereisoneclearmasterrecord,thecomputersinvolvedarenotownedorcontrolledbyanysinglepartyororganisaDon.

• Thedistributednatureoftheblockchainmeansthatitcannotbetamperedwitheasily.

• SupplychainsareessenDallyaseriesofcontractsbetweennumerousparDesengagedinthebuyingofcomponents,productsandservicestomanufacture,verify,transport,storeandselltocustomers.

• EachelementofthesechainsinvolvesnetworksofparDcipantsexchangingdataandinformaDonwithvaryingdegreesofaccuracyandclarity.

Benefitswillinclude:• ImprovecashflowbystreamliningfinancialtransacDons.

• Improvedinventoryvisibilityacrossfragmentednetworks.

• Shipmentvisibility.• AuthenDcityofproductsguaranteedandreducDonofcounterfeiDng.

• AuthenDcaDonofVerifiedGrossMass(VGM)data.

• EthicalimplicaDons–applicaDoninmovementofendangeredspeciesproducts.

Challengesare:

• SheervolumeoftransacDonsslowingdownvalidaDonprocess.

• OvercomingpercepDonoftransparencyandlackofconfidenDality.

Blockchain in Supply Chains!

© Transport Intelligence! July 2017! 26!

• MarineTransportInternaDonal–AforwarderworkingwithblockchaintechnologycompanyTrustMeandpredicDveanalysisexpertBlackSwanData.Thecompanyplanstouseblockchaintoallowcompaniestobuild‘ecosystems’betweensupplychainparDeswithtrustgainedastransacDonsarepubliclyrecorded.ApplyingthetechnologytomanagetheVerifiedGrossMass(VGM)datarequiredbytheIMO’sSOLAStreaty.

• MaerskLine–MaerskhasdevelopedasystemwithIBMusingtheopen-sourcedHyperledgerblockchaintomanageitscargo,providingvisibility.ItalsoaimstoprovidepubliclyviewableinformaDononemptycontainerstoallowshipperstofindextracapacityacrosstheshippingindustry.

• Foxconn–FnConn,asubsidiaryofFoxconn,oneofthelargestelectronicmanufacturersintheworld,hasjoinedupwithmarketplacelendingpla^ormDianrong.Thetwocompaniesaretriallingablockchainsupplychainfinancepla^ormaimedatprovidingfinancetosuppliersviapeer-to-peerlending.

• Everledger–Astart-upbasedintheUK,Everledgerhasbuiltaglobal,digitalledgerthattracksassetsthroughouttheirproductjourneyandisworkingwithSAPAribaonsupplychainapplicaDons.

• Skuchain–SkuchainisdevelopingasoluDontofacilitatelendingbyfinanciersagainsttradeinstrumentssuchaspurchaseordersandinvoices,thuscollateralisingtheloans.ThecompanyalsoprovidesvisibilityonthetransacDonstatesoftheseloans.

• CargoChain–Astart-upwhichoffersaseMlementpla^ormthatprovidesallparDesinashippingtransacDonwithaninterfacetoviewinformaDonassociatedtocargo.DeploysRFIDtoprovidereal-Dmevisibility.

• Yojee-–Astart-upwhichprovidesaparceldeliverymarketplaceusingArDficialIntelligence(AI)andblockchain.Theformerisusedtoassigndeliveryjobstodrivers,whilstthelaMerrecordsthetransacDons.

• TransRisk–Financestart-upthatprovidesfuturescontractstohedgeagainstmovementsinlinehaulfreightrates.ItusesblockchaintorecordtransacDonsonitstradingtool.

About Ti!

All rights reserved. No part of this publication may be reproduced in any material form including photocopying or storing it by electronic means without the written permission of the copyright owner, Transport Intelligence Limited. !

This report is based upon factual information obtained from a number of sources. Whilst every effort is made to ensure that the information is accurate, Transport Intelligence Limited accepts no responsibility for any loss or damage caused by reliance upon the information in this report.!

Ti’s Origin and Development!

Ti is a leading logistics and supply chain market analysis company developed around five pillars of growth:!

• Logistics Briefing!

• Ti Market Research Reports!

• Ti Insight portals!

• Ti Consulting!

• Ti Conferences and Training !

Ti acts as advisors to the World Economic Forum, World Bank, UN and European Commission and have 14 years worth of providing expert analysis to the worlds leading manufacturers, retailers, banks, consultancies, shipping lines and logistics providers.!

What Sets Ti Apart?!

• Globally recognised and trusted brand!

• Global Associate Network provides a multi-country, multi-disciplinary and multi-lingual extension to Ti’s in-house capabilities!

• More than fourteen years of knowledge delivery to global manufacturers, retailers, banks, consultancies, shipping lines and logistics providers!

• Unique web-based intelligence portals!

• Interactive dashboard!

• On-going and comprehensive programmes of primary and secondary research!

Intelligence tailored to your specific sector !Insight drives strategy – if you would like to know more about our global or local logistics insights in your sector please contact: !

!

Global Head Office !T: +44 (0)1666 519 901!

!John Manners-Bell!Chief Executive!!T: +44 (0)1666 519 909!E: [email protected] !

www.ti-insight.com !