summer report on cloud computing

DESCRIPTION

summer report on cloud computingTRANSCRIPT

Summer Internship Project Report SIMSREE, Mumbai

1

Brand awareness of CtrlS & Analysis of Market Potential for Cloud Products Summer Internship Project Report

By

Mr. Onkar Jayant Sovani

Roll No. P12038 PGDBM 2012-14

SIMSREE, Mumbai.

Under the guidance of

Mr. Anil Kamaria

AVP, Sales

Ctrls Datacenters Ltd. Mumbai.

IN PARTIAL FULFILMENT OF THE REQUIREMENT OF

POST GRADUATE DIPLOMA IN BUSINESS MANAGEMENT CONDUCTED BY

SYDENHAM INSTITUTE OF MANAGEMENT STUDIES, RESEARCH AND ENTREPRENEURSHIP EDUCATION. MUMBAI.

Summer Internship Project Report SIMSREE, Mumbai

2

Acknowledgement

Amongst the panorama of people who provided me inspiring guidance and encouragement, I

take this opportunity to convey my thanks to those who have given their indebted assistance

and encouragement for completing this project.

Firstly, I would like to express my sincere thanks and gratitude to SIMSREE, Mumbai and

CtrlS Datacenters Ltd. for offering a unique platform to gain exposure of the vibrant and

rapidly growing sector of datacenters and IT infrastructure outsourcing through summer

internship project.

I especially thank my guide Mr Anil Kamaria, AVP Sales, CtrlS Datacenters Ltd. for his

kind support and guidance throughout the tenure of this project.

Also, I would like to express my profound gratitude to Mr Sunil Kumar, Vice President,

Sales and all the people in the Mumbai office of CtrlS Datacenters Ltd. for their constant

support and help in accomplishing the objectives of the project.

Last, but not the least, I thank my friends and colleagues for their efforts and creativity which

has helped in giving final shape and structure to the project.

I hope that I have been successful in my endeavour. Discrepancies, mistakes, if any, are

solely mine.

Mr. Onkar Sovani

Roll No. P12038

PGDBM 2012-14

SIMSREE, Mumbai.

Summer Internship Project Report SIMSREE, Mumbai

3

Executive Summary

CtrlS is India’s leading provider of Datacenter solutions with 2 Tier-IV Datacenters currently

operational in Navi Mumbai and Hyderabad. CtrlS has many firsts to its credit including

India’s first Tier-IV Datacenter, besides DR and Cloud solutions that have redefined the way

IT services are consumed by client organizations.

In a short span, CtrlS has already been recognized by leading industry bodies like

NASSCOM, CII, FICCI etc., for the pioneering work in creating IT infrastructure.

The project is titled: ‘Brand Awareness of CtrlS & Analysis of Market Potential for

Cloud Products’. The objective was to understand CtrlS cloud products and solutions, to

identify the target prospects for these solutions, to create a deep profile of target companies,

followed by creating a survey, and carry out the survey/research and analysis, and finally

make product recommendations on the basis of research and analysis, organize meetings with

the clients for CtrlS sales team and participate in solution selling to the customers.

The project also included attending IT summits, multiple visits to CtrlS Datacenter facility

located at Navi Mumbai. And also, understanding and promoting product lines of Limelight

Networks, Inc. and Global Outlook which are partner companies of CtrlS Datacenter Ltd.

Summer Internship Project Report SIMSREE, Mumbai

4

Summer Internship Evaluation

This is to certify that Mr. Onkar Jayant Sovani has successfully completed his Summer

Internship Program at CtrlS Datacenters Pvt. Ltd.

Evaluation Details:

Name of Student: Onkar Jayant Sovani

Institute: Sydenham Institute of Management Studies, Research &

Entrepreneurship Education (SIMSREE), Mumbai.

Reporting Manager: Mr. Anil Kamaria

Duration: 18th

April 2013 to 18th

June 2013

Project: Seeding the Cloud

Project Description: Brand Awareness of CtrlS & Analysis of Market Potential for Cloud

Products

Project Evaluation: 45 /50

Name of Corporate Mentor

Mr. Anil Kamaria

AVP Sales,

CtrlS Datacenters Ltd. Mumbai

Summer Internship Project Report SIMSREE, Mumbai

5

Table of Contents

Acknowledgement 2

Executive Summary 3

Certificate of Marks 4

Table of contents 5

Industry overview 6

competitor analysis 9

company introduction 11

Prodcut / Service Portfolio 12

SWOT: CtrlS Datacenters Ltd. 13

Literature Review 14

Project Outline & Delieverables 23

Learning opportunities 31

Conclusion 33

Recommendations 34

Way ahead: Future Outlook at the industry 35

Self-assessment of the Internship 37

References 38

Appendices 39

Summer Internship Project Report SIMSREE, Mumbai

6

Industry Overview

India has always had a strong outsourcing sector but when it comes to data centers power

provision and other risks have held it back. But this has not stopped the industry from

thinking big in terms of datacenter build

India - A future-proofed market

India is preparing for a rising need for data center space

The evidence for India’s growing demand for data centers lies in the handbags and pockets of

a growing majority of India’s massive population. In 2000, according to IT services provider

Mahindra Satyam’s Sudhir Nair, SVP and global head of infrastructure management services,

the market for telephonic penetration in India was less than 35 to 38 million people. In 2010,

this stood at 90 million.

To get an idea of market penetration, in 2012 India had a population of 1.22 billion – 50% of

these were aged between 0 and 25.

Gartner expects India will have seen a mobile subscriber base of more than 696 million

connections by the end of 2012, which places its penetration rate at just over half the

population, and the analyst firm expects 72% mobile penetration by 2016. The World Bank

says more than 30 billion applications were downloaded in India in 2011 alone. All this data

has to live somewhere and ‘where’ really is the answer to why India is seeing its data center

footprint rise.

India’s move towards digitization is not too different from those moves seen in the other

BRIC markets. But according to Datacenter Dynamics Industry Census for 2012, India’s data

center market is not moving as fast as China’s or Brazil’s. The reason, according to Nair, is

that India’s market has been prepared for rising amounts of data for some time. He says that

operators have been building out larger-than-needed facilities with higher-than-needed Tier

ratings to meet the predicted rise in demand for colocation and hosting services – and this is

where this market differs.

Building big

India became home to South Asia’s first Tier IV data center in July 2012, when local

provider GPX Global Systems received accreditation from the Uptime Institute for its 4,000

sq.m facility in Mumbai. It has four dedicated utility power feeds from two diverse

substations.

In March 2012, Tata Communications said it now serves 19% of India’s colocation market

with its 350,000 sq ft footprint, comprising ten Tier III facilities servicing more than 700

customers. And in February 2012, Tulip Telecom opened the world’s third-largest data center

in Bengaluru, called Tulip Data City. The Tier IV facility, built for managed services and

colocation, can house as many as 12,000 racks with 100MW of power.

Summer Internship Project Report SIMSREE, Mumbai

7

Filling empty space

Many of the colocation providers in India that boast large, highly Tier-rated facilities have

data centers that, at present, are only about 55% or 60% full, by net occupancy rates. These

companies are mostly into large real estate, as opposed to the other players in the India

market such as the telcos, which have to provide a combination of colo and commodity-based

managed hosting, and the global services providers such as IBM, HP and Mahindra Satyam.

This ‘intermediate’ rating circumvents problems that come with poor access to power coming

in from the grid. In most states, there is no private provider of power, and that means we

cannot get Tier IV, which requires two feeds. Such data centers will qualify for Tier IV but

don’t have that additional power to operate with.

Power and other problems

Power – or lack of reliable sources of it – has long been considered a major challenge for

companies operating in India. Hurleypalmerflatt and Cushman & Wakefield, in their data

center Risk Index for 2012, ranked India second to Brazil in terms of high-risk data center

locations. “Power security remains a significant risk stemming from the lack of diversity of

energy imports and increasing reliance on imported oil,” they say. India was also found to

have a high energy cost – with a ranking of 21 on the index (whereas China, for example,

came in with a ranking of 9, with 30 being the highest level of risk for the global locations).

The rise of services

But not everyone needs a Tier III or IV data center in India, and more and more companies

are in need of data center space. The introduction of compliance laws here have raised the bar

for IT and the need for disaster recovery is growing, as a result, there are a lot of Tier II

companies looking at service providers or co-lo facilities, and this is where aggressive growth

can be observed. There are also a lot of banks and insurance companies having to push the

envelope in terms of increasing capacity because of the need to have automated centers and

the introduction of new banking laws.

The DCD Intelligence Industry Census data collected in 2012 shows that investment in

India’s data center market was expected to reach US$4.4bn in 2012; up from $4.1bn in 2011

(China investment for 2012 was expected to be $8.7bn and Brazil’s $5.5bn). In India, this

represents 1.21m sq. m of data center space being built – up from 0.76m sq. m in 2011 and a

power demand of 1.04 GW in 2012.

In its own forecasts, Gartner valued the colocation and hosting market in India at US$609.1m

in 2012 and by 2016 says it will be worth $1.3bn. “Gartner inquiries indicate a general

increase in interest by the investor community around data centers in India. Gartner analysts

believe there will be increased outsourcing of data center requirements in the forecast period

because of the big data center users, such as banks and the government,” Gartner says.

Summer Internship Project Report SIMSREE, Mumbai

8

“The increased focus on data center efficiency, reliability and cost optimization in India has

led to a few interesting changes. Enterprises with a large captive data center presence may not

necessarily exercise this in a big way,” Gartner says. “But the midmarket and government-

owned enterprises are increasingly investing in hosting or managed services, primarily to

ensure that they can focus on their core business and get a highly skilled data center partner

fulfilling their infrastructure growth plans.”

The value add

Mahindra Satyam, which is the ICT arm of the US$15.9bn Mahindra Group of companies,

delivers hosting services, with 25,000 to 28,000 sq. ft. of raised floor internally, which is

rated Tier III – this caters for its own internal use and Tier 1 customers, like those in the

automotive industry.

Such facilities, have been built to cater for services over the next ten years. Companies are

expected to move towards cloud or Software-as-a-Service models in future, and in these

situations compliance will become critical. Such customers will also be interested in green

credentials, including Power Usage Effectiveness (PUE) (although PUE has not been adopted

widely in the India market).

The cost of real estate in India is also rising. It is already up to the tune of ten times what it

was years back, and this is all pushing up the cost to a level where colo could become a more

attractive offering. India will benefit is with the services it can place on top of its offerings.

Skills are still cheap here – in the range of $20 to $25 an hour, where in another market that

could be in the range of $60 to $75.

While much of India’s growth, according to those working in the market, seems to be coming

from local demand, such attractive figures in a maturing market could put India on the map

for outsourcing – this time with data center services. And, unlike other emerging market

players, when it comes to technology this is a scenario that seems to be part of the national

identity of the nation’s tech industry. Knowledge workforce is growing rapidly, and there is

an all-round understanding that this sector needs to be cutting edge, which is forcing people

to look at India differently. But India needs to maintain compliance and standards, and really

find ways to add to the services the industry can offer.

Summer Internship Project Report SIMSREE, Mumbai

9

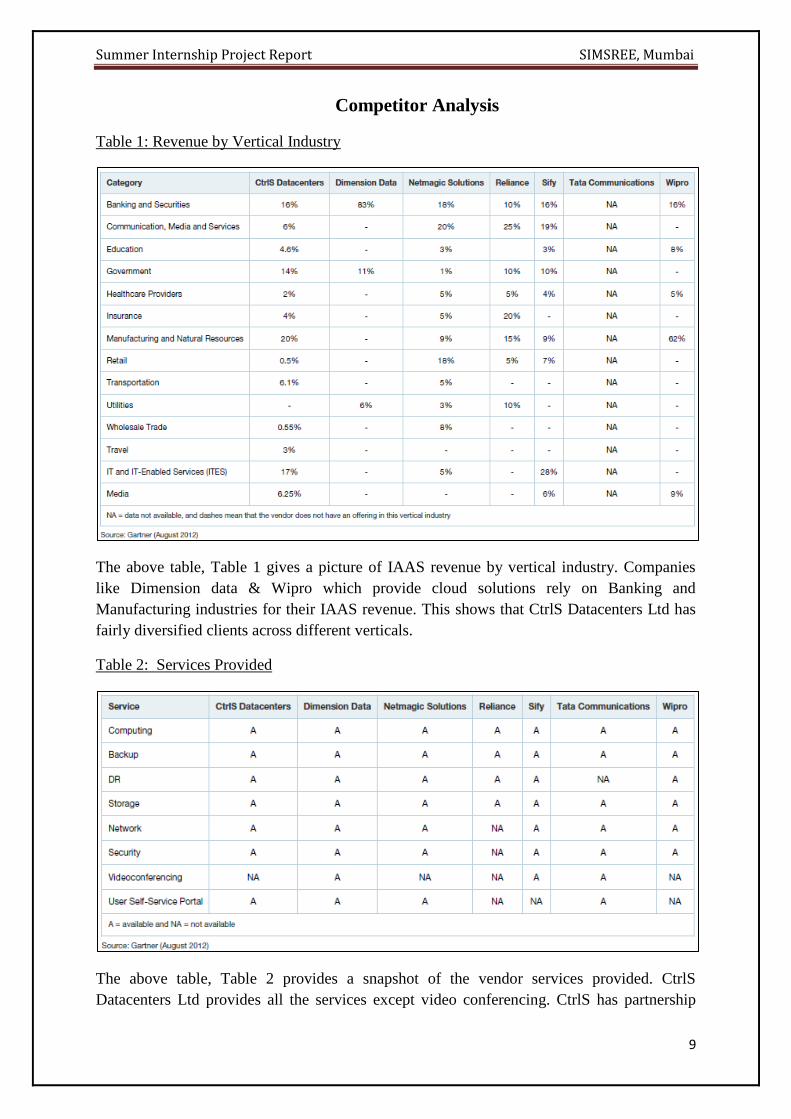

Competitor Analysis

Table 1: Revenue by Vertical Industry

The above table, Table 1 gives a picture of IAAS revenue by vertical industry. Companies

like Dimension data & Wipro which provide cloud solutions rely on Banking and

Manufacturing industries for their IAAS revenue. This shows that CtrlS Datacenters Ltd has

fairly diversified clients across different verticals.

Table 2: Services Provided

The above table, Table 2 provides a snapshot of the vendor services provided. CtrlS

Datacenters Ltd provides all the services except video conferencing. CtrlS has partnership

Summer Internship Project Report SIMSREE, Mumbai

10

with Limelight Networks and Global Outlook for selling CDN (Content Delivery Network) &

Mailing services respectively.

Table 3: Datacenter Capacity : India - 2011

Above table shows the datacenter capacity of major Indian players in 2011.

Table 4: Comparison of various parameters of major Indian Datacenter players

Players in Thousand Sq.Ft

TULIP 1000

RELIANCE 650

TATA COMMUNICATIONS 575

CtrlS 370

AIRTEL 250

SIFI 200

NET MAGIC 200

India Datacenters Capacity 2011

Parameter \ Player Tulip Telecom Reliance IDC Tata

Communicat

ion

CtrlS Bharati

Airtel

Sify NetMagic

BuiltUp Area (Sq.Ft.) 1000000 650000 575000 370000 250000 200000 200000

No. of DataCenters 5 9 9 3 6 4 7

Locations Mumbai 2,

Bnagalore 2,

Delhi 1

Mumbai 4,

Bangalore 3,

Chennai 1,

Hyderabad 1

Mumbai 3,

Pune,

New Delhi,

Hyderabad,

Kolkata,

Bangalore,

Chennai

Mumbai 1

Hyderabad 1,

Delhi 1

Mumbai,

Pune, Noida,

Bangalore,

Delhi,

Chennai

Mumbai 2,

Chennai,

Bangalore

Mumbai 4,

Chennai, Delhi,

Bangalore

Service Portfolio Colocation,

MNS,

EDC,

VAS,

Prof Services

Colocation,

MNS,

EDC,

VAS,

Prof Services

Colocation,

EDC,

VAS

Colocation,

MNS,

EDC,

VAS,

DR

Colocation,

EDC,

VAS

Colocation,

MNS,

EDC,

VAS

Colocation,

VAS

Vertical Focus Government,

BFSI,

Manufacturing,

Telecom,

IT/ITES

BFSI,

Manufacturing,

Media,

Entertainment

IT/ITES

BFSI,

IT/ITES

BFSI,

Manufacturing,

Telecom,

Media,

Health/Pharma,

Aviation

BFSI,

Telecom,

Media,

Content

Providers

Government

, ITES

BFSI,

ITES

Manufacturing

Summer Internship Project Report SIMSREE, Mumbai

11

Company Overview: CtrlS Datacenters Ltd.

CtrlS is India’s leading provider of Datacenter solutions with 2 Tier-IV datacenters currently

operational in Navi Mumbai and Hyderabad. CtrlS has many firsts to its credit including

India’s first Tier-IV datacenter, besides DR and Cloud solutions that have redefined the way

IT services are consumed by client organizations.

In a short span, CtrlS has already been recognized by leading industry bodies like

NASSCOM, CII, FICCI etc., for the pioneering work in creating IT infrastructure.

CtrlS is a young organization, but more importantly, it is an entrepreneurial and resourceful

organization, ever ready to soar higher with new ideas and new ways of doing business.

There is a consistent effort to think new and think different. The rigidity of doing business

with plug and play products is not for us. We believe that every problem presents a potential

opportunity to invent a new way of working.

Headquartered in Hyderabad, CtrlS Datacenters Pvt Ltd was founded in 2008 by the Rs. 750

Crore (US $1.4 billion approximately) (EV) Pioneer Group, which is primarily involved in IT

– services, consulting and infrastructure. The Group has been growing at more than 100

percent compound annual growth rate of over the past 15 years.

CtrlS has Datacenters in Hyderabad and Mumbai with an upcoming facility in Delhi. The

company has developed the capabilities to provide platform level services which include

Datacenter infrastructure, storage, backup, hardware, OS layers, and network and security

layers. It offers a host of outsourced business solutions and services such as Disaster

Recovery on demand, Managed services, Private cloud-on-demand to enable clients to make

the paradigm shift from the captive Datacenter model to the outsourced one.

The CtrlS Datacenter is Tier IV certified and provides 99.995% uptime guarantee, less than

22 minutes of downtime in a year and N+N redundancy. With 1.42 PUE, it is the most power

efficient Datacenter in India. Dual power sources and an additional captive power plant

ensure uninterrupted power and cooling systems. It also provides high bandwidth availability

and a choice from India’s leading TELCOs.

It is also the only one of its kind in India to provide 8-zone security, scalability for up to 10

years, guaranteeing the highest availability and least energy consumption. Armed with top-

of-the-line features and the very best of infrastructure and technology, it offers clients an

array of benefits which can drive a saving of up to 40 percent on total cost of ownership.

The facility sets the benchmark in the data centre space with 8-zone security, making it the

most secure data centre in India. It has ISO-20000-1, ISO-27001 and BS 25999 certifications.

Summer Internship Project Report SIMSREE, Mumbai

12

Product / Service portfolio: CtrlS Datacenters Ltd.

1. Public Cloud

1a. Virtual Private Server

1b. Real

1c. Enterprise

2. Content Delivery Network

3. High Availability VPS

4. Dedicated Hosting

5. Mail & Messaging

6. Mailing Solutions

6a. Zimbra

6b. Qmail

6c. Hosted Exchange

7. Online Backup

8. Online Storage

9. Colocation Services

10. Firewall & Security

11. Managed Services

12. Disaster Recovery (DR)

13. Business Continuity Plan (BCP)

14. Standard Servers

15. Cloud Testing

Summer Internship Project Report SIMSREE, Mumbai

13

SWOT analysis: CtrlS Datacenters Ltd.

Strengths

Asia’s largest Tier-IV datacentre

only service provider to position itself as a DR-as-a-service provider

Datacenter & Cloud offerings are the core offerings of company

3X faster than international

Branded and brand new hardware

30-day money back guarantee

24 x forever customer support

Quick and easy provisioning

transparent pricing structure

Weaknesses

Brand Value

Geographical presence

Marketing Focus

Opportunities

Huge market for DR & BCP adoption as CtrlS is the only provider of DR-as-a-

service

Cloud users and providers cited “analytics” and “automation” as a service they’d

like to have

Large untapped market in India

Strong adoption opportunities in Government sector

Threats

Customers currently have varied perceptions about the company

Aggressive market offerings by big players like Reliance & Tata

Summer Internship Project Report SIMSREE, Mumbai

14

Literature Review

Datacenter

A data centre is a dedicated space where companies can keep and operate most of the ICT

infrastructure that supports their business. This would be the servers and storage equipment

that run application software and process and store data and content. For some companies this

might be a simple cage or rack of equipment, for others it could be a room housing a few or

many cabinets, depending on the scale of their operation.

The space will typically have a raised floor with cabling ducts running underneath to feed

power to the cabinets and carry the cables that connect the cabinets together.

The environment is controlled in terms of areas such as temperature & humidity, both to

ensure the performance and the operational integrity of the systems within. Facilities will

generally include power supplies, backup power, chillers, cabling, fire and water detection

systems and security controls.

Data centres can be in-house, located in a company’s own facility, or outsourced with

equipment being collocated at a third-party site. Outsourcing does not necessarily mean

relinquishing control of your equipment – it can be as simple as finding the right place to

house that equipment.

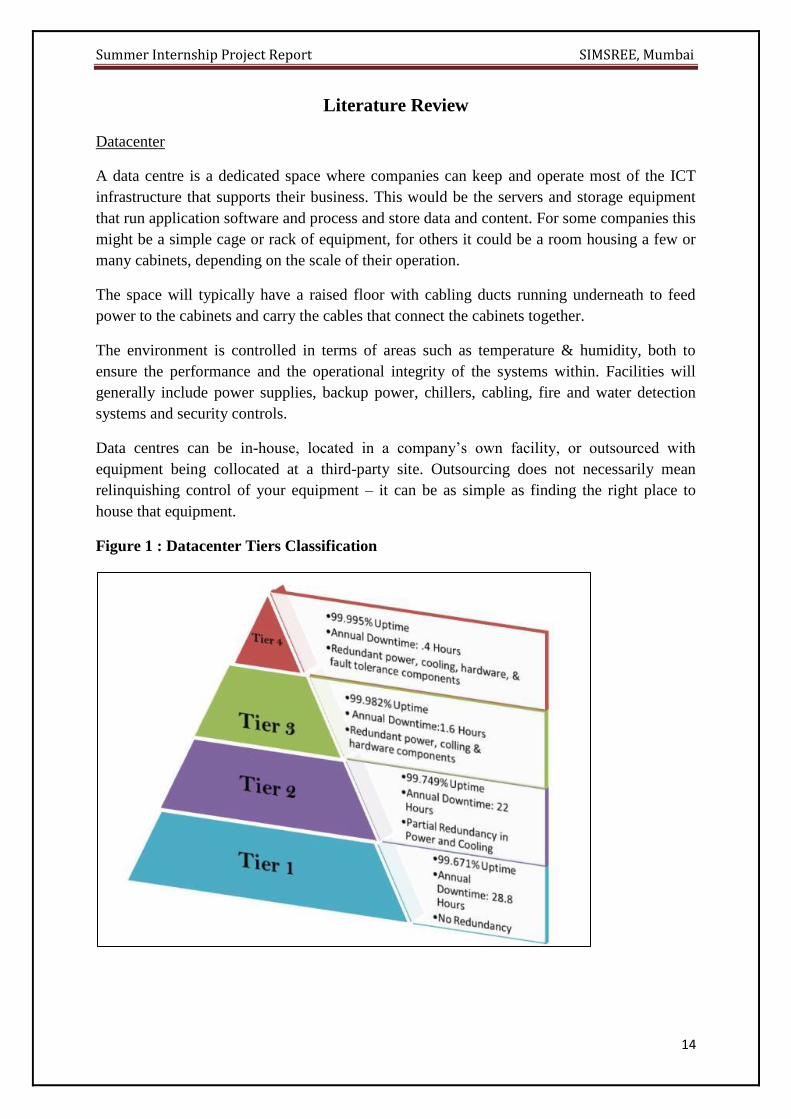

Figure 1 : Datacenter Tiers Classification

Summer Internship Project Report SIMSREE, Mumbai

15

The Telecommunications Industry Association is a trade association accredited by ANSI

(American National Standards Institute). In 2005 it published ANSI/TIA-942,

Telecommunications Infrastructure Standard for Data Centers, which defined four levels

(called tiers) of data centers in a thorough, quantifiable manner. Above figure, Figure 1

explains various datacenter tiers. The simplest is a Tier 1 data center, which is basically a

server room, following basic guidelines for the installation of computer systems. The most

stringent level is a Tier 4 data center, which is designed to host mission critical computer

systems, with fully redundant subsystems and compartmentalized security zones controlled

by biometric access controls methods. Another consideration is the placement of the data

center in a subterranean context, for data security as well as environmental considerations

such as cooling requirements.

Data center infrastructure: In-house hosting versus outsourcing

When it comes to IT infrastructure, an in-house data center is among the big ticket CAPEX

items for most Indian CIOs. This is why many businesses prefer to have a better OPEX-

CAPEX equation by taking the data center outsourcing route. Today, Indian organizations are

definitely looking at IT infrastructure outsourcing as an alternative, with co-located hosting

prices dropping on a consistent basis.

This trend is substantiated by analyst firm Gartner Inc., which observes that despite the

economic slowdown infrastructure outsourcing (including IT) will witness bullish growth in

FY '09-'10. The call between in-house data center infrastructure and opting for co-located

data center services involves more than just accounting jugglery.

Data center outsourcing and India.org

In India, organizations are sceptical when it comes to putting their entire IT infrastructure

under another entity's control. Business critical applications continue to be hosted and

managed internally in most large and medium Indian businesses, more so in the case of

financial services companies such as banking and insurance firms that store highly sensitive

personal data. However, the trend of outsourcing non-critical applications to third-party

service providers is on the rise.

Outsourced data center infrastructure services are adopted largely by organizations that have

realized that IT is an enabler and not its core function. If this describes your company, does it

make sense to outsource?

When it comes to in-house infrastructure, there are challenges like regulatory compliance

requirements, data center design and levels of built-in redundancy. Also, how does one

foresee the business requirements five years down the line? One does not think of these

factors upfront. That is where the third-party players come into picture, as the data center is

their core focus.

Summer Internship Project Report SIMSREE, Mumbai

16

Requirement analysis

The data center function to be outsourced (entire vs. partial) is a strategic step that has to take

into account many factors. Organization should evaluate its data before considering

outsourcing. Confidentiality of the data plays a major role when taking this decision.

When an organization decides to opt for a mix of in-house and outsourced data center

infrastructure, benchmarking is a good start. This will help it identify loopholes to be

remedied by involving third-party experts.

Smart companies have to realize the levels up to which they want to build and buy. Things

which are strategic in nature on which organizations have good control should be done in

house. Outsourcing should be considered for things that they do not specialize in.

Data center infrastructure provider selection

Evaluating a vendor can be a troublesome task. Service provider's capability, infrastructure,

facility and security mechanisms, credibility in the market and cost factor are the crucial

points to look at. Site visits are critical to understand the service provider's capabilities.

Comprehensive reference checks with the service provider's existing clients come next on the

evaluation checklist. Security, transparency and trust issues come into the picture when an

organization puts its data in the hands of a third party. The service aspect is yet another key

issue. This is where service level agreements (SLA) play an important role in bridging this

trust. The SLA should have sufficient safeguards in place to protect your organization's

interests. However, the validity of an SLA in the Indian context is still disputable.

Despite the uncertainty prevalent on the infrastructure provider's service-level fronts, CAPEX

savings have been a big draw for all the Indian organizations opting for data center

outsourcing. Adding to this is the reduction in management complexity and skilled manpower

costs.

As a trend, data center infrastructure outsourcing is growing in India since available expertise

and resources for in-house data centers cannot always be found. However, outsourcing is

definitely not set to wipe out the in-house models.

Cloud computing

Cloud computing is a general term for anything that involves delivering hosted services over

the Internet. These services are broadly divided into three categories: Infrastructure-as-a-

Service (IaaS), Platform-as-a-Service (PaaS) and Software-as-a-Service (SaaS). The name

cloud computing was inspired by the cloud symbol that's often used to represent the Internet

in flowcharts and diagrams.

Summer Internship Project Report SIMSREE, Mumbai

17

Figure 2: Cloud services

A cloud service has three distinct characteristics that differentiate it from traditional hosting.

Figure 2 explains various kinds of cloud services. It is sold on demand, typically by the

minute or the hour; it is elastic -- a user can have as much or as little of a service as they want

at any given time; and the service is fully managed by the provider (the consumer needs

nothing but a personal computer and Internet access). Significant innovations in virtualization

and distributed computing, as well as improved access to high-speed Internet and a weak

economy, have accelerated interest in cloud computing.

Table 5: Comparison of Public & Private Cloud

Parameters Public cloud Private cloud

Single sign-on Impossible Possible

Scaling up Easy while within defined limits Laborious but no limits

Customization Impossible Possible

Initial cost Typically zero Typically high

Running cost Predictable Unpredictable

Privacy No (Host has access to the data) Yes

Public Cloud

A public cloud is one based on the standard cloud computing model, in which a service

provider makes resources, such as applications and storage, available to the general public

over the Internet. Public cloud services may be free or offered on a pay-per-usage model.

Table 5 gives a comparison between Public & Private Cloud.

The main benefits of using a public cloud service are:

Summer Internship Project Report SIMSREE, Mumbai

18

• Easy and inexpensive set-up because hardware, application and bandwidth costs are

covered by the provider.

• Scalability to meet needs.

• No wasted resources because you pay for what you use.

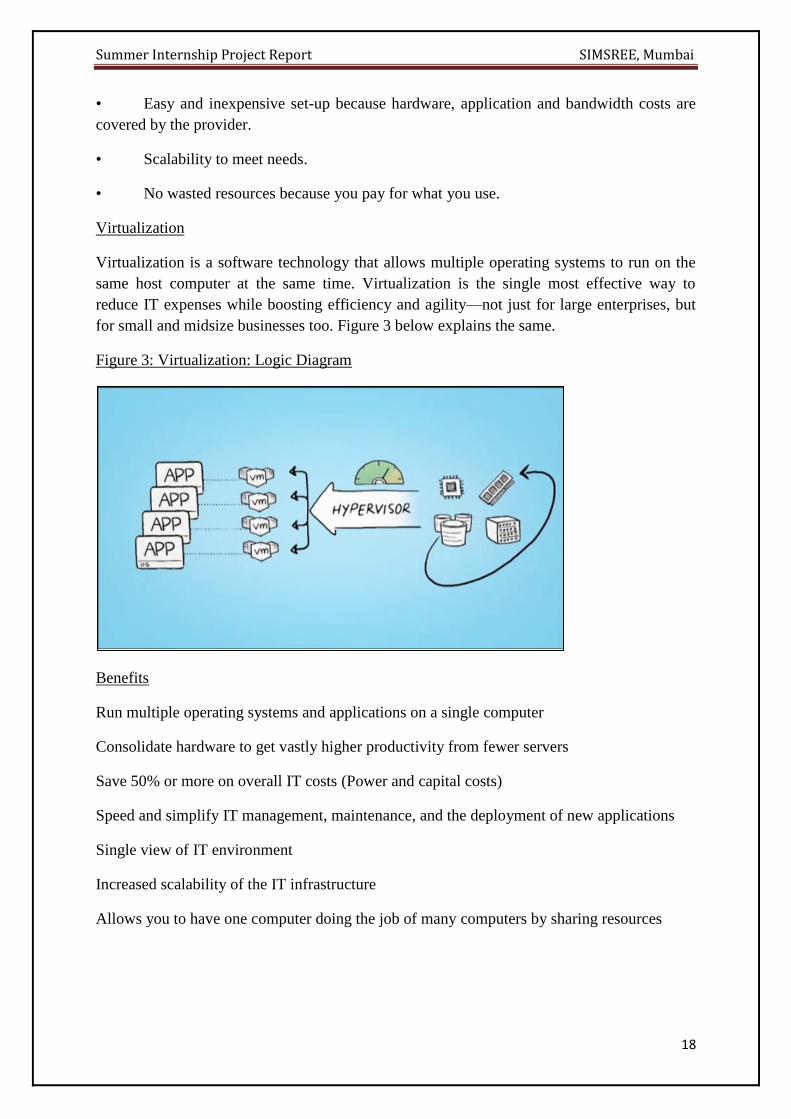

Virtualization

Virtualization is a software technology that allows multiple operating systems to run on the

same host computer at the same time. Virtualization is the single most effective way to

reduce IT expenses while boosting efficiency and agility—not just for large enterprises, but

for small and midsize businesses too. Figure 3 below explains the same.

Figure 3: Virtualization: Logic Diagram

Benefits

Run multiple operating systems and applications on a single computer

Consolidate hardware to get vastly higher productivity from fewer servers

Save 50% or more on overall IT costs (Power and capital costs)

Speed and simplify IT management, maintenance, and the deployment of new applications

Single view of IT environment

Increased scalability of the IT infrastructure

Allows you to have one computer doing the job of many computers by sharing resources

Summer Internship Project Report SIMSREE, Mumbai

19

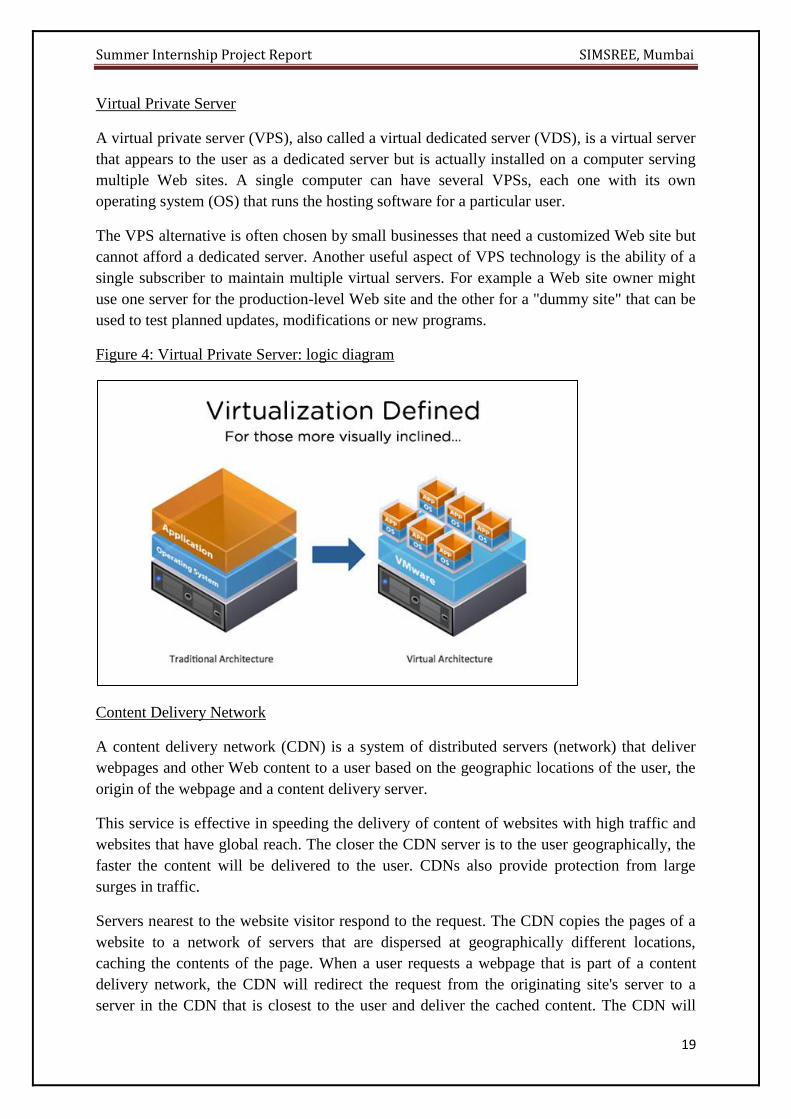

Virtual Private Server

A virtual private server (VPS), also called a virtual dedicated server (VDS), is a virtual server

that appears to the user as a dedicated server but is actually installed on a computer serving

multiple Web sites. A single computer can have several VPSs, each one with its own

operating system (OS) that runs the hosting software for a particular user.

The VPS alternative is often chosen by small businesses that need a customized Web site but

cannot afford a dedicated server. Another useful aspect of VPS technology is the ability of a

single subscriber to maintain multiple virtual servers. For example a Web site owner might

use one server for the production-level Web site and the other for a "dummy site" that can be

used to test planned updates, modifications or new programs.

Figure 4: Virtual Private Server: logic diagram

Content Delivery Network

A content delivery network (CDN) is a system of distributed servers (network) that deliver

webpages and other Web content to a user based on the geographic locations of the user, the

origin of the webpage and a content delivery server.

This service is effective in speeding the delivery of content of websites with high traffic and

websites that have global reach. The closer the CDN server is to the user geographically, the

faster the content will be delivered to the user. CDNs also provide protection from large

surges in traffic.

Servers nearest to the website visitor respond to the request. The CDN copies the pages of a

website to a network of servers that are dispersed at geographically different locations,

caching the contents of the page. When a user requests a webpage that is part of a content

delivery network, the CDN will redirect the request from the originating site's server to a

server in the CDN that is closest to the user and deliver the cached content. The CDN will

Summer Internship Project Report SIMSREE, Mumbai

20

also communicate with the originating server to deliver any content that has not been

previously cached.

Dedicated Hosting

Dedicated hosting is simply a server located in a data center somewhere in which you have

complete control over and hence is “dedicated” only to you.

Dedicated hosting is “A dedicated hosting service, dedicated server, or managed hosting

service is a type of Internet hosting in which the client leases an entire server not shared with

anyone. This is more flexible than shared hosting, as organizations have full control over the

server(s), including choice of operating system, hardware, etc. Server administration can

usually be provided by the hosting company as an add-on service. In some cases a dedicated

server can offer less overhead and a larger return on investment. Dedicated servers are most

often housed in data centers, similar to colocation facilities, providing redundant power

sources and HVAC systems. In contrast to colocation, the server hardware is owned by the

provider and in some cases they will provide support for your operating system or

applications.”

Hosted Exchange

Hosting is an approach to application deployment where the servers are housed in a secure

data center which meets stringent requirements of physical security and environmental

controls. All hardware and software is owned, maintained, updated and backed-up by a third-

party hosting provider, freeing the end user from having to spend tens of thousands of dollars

on purchasing hardware and software for the office, constantly monitoring data availability,

With a hosted Exchange solution, there’s no need to install a new application in your office

or attempt to integrate this new system into the company’s existing infrastructure. A hosted

approach also eliminates the up-front expense of having to buy expensive hardware and

software, the need to hire additional personnel to maintain and upgrade the servers or train an

existing IT staff on the new technology. The hosting provider is responsible for keeping the

system up-to-date and often offers at least a 99.9 percent uptime guarantee to ensure that its

clients have access to critical data around-the-clock. And ensuring software updates are

installed. Businesses then “rent” the services that benefit their needs, paying for only what

they use.

Colocation Services

A server, usually a Web server, that is located at a dedicated facility designed with resources

which include a secured cage or cabinet, regulated power, dedicated Internet connection,

security and support.

These co-location facilities offer the customer a secure place to physically house their

hardware and equipment as opposed to locating it in their offices or warehouse where the

potential for fire, theft or vandalism is much greater.

Summer Internship Project Report SIMSREE, Mumbai

21

Most co-location facilities offer high-security, including cameras, fire detection and

extinguishing devices, multiple connection feeds, filtered power, backup power generators

and other items to ensure high-availability which is mandatory for all Web-based, virtual

businesses.

Firewall & Security

The word firewall originally referred literally to a wall, which was constructed to halt the

spread of a fire. In the world of computer firewall protection, a firewall refers to a network

device which blocks certain kinds of network traffic, forming a barrier between a trusted and

an untrusted network. It is analogous to a physical firewall in the sense that firewall security

attempts to block the spread of computer attacks.

Disaster Recovery (DR)

Every business needs a strong disaster recovery plan. Like any difficult topic, disaster

recovery is something that nobody wants to think about, but everyone needs to plan for.

Disaster recovery is the ability to continue work after any number of catastrophic problems,

ranging from a computer virus or hacker attack to a natural disaster such as flood, fire, or

earthquake. Having a disaster recovery plan in place takes a little time and effort, but the

peace of mind it brings and the ability to continue work after the unthinkable are well worth

it.

Disaster recovery must take into account how a business is run and the different elements are

required to keep the business going. These needs vary from business to business, and a good

disaster recovery plan should be designed for the individual business's needs. Using a generic

disaster recovery strategy is better than nothing, but it may stress elements that are less

important to your business, or worse, leave out critical aspects.

Business Continuity Plan (BCP)

The creation of a strategy through the recognition of threats and risks facing a company, with

an eye to ensure that personnel and assets are protected and able to function in the event of a

disaster. Business continuity planning (BCP) involves defining potential risks, determining

how those risks will affect operations, implementing safeguards and procedures designed to

mitigate those risks, testing those procedures to ensure that they work, and periodically

reviewing the process to make sure that it is up to date.

Summer Internship Project Report SIMSREE, Mumbai

22

Benefits of Cloud Approach

Figure 5: Benefits of Cloud Approach

Services that offer Cloud storage can provide businesses with the storage space that they

simply wouldn’t otherwise have access to. As storage is provided using a vast remote server,

businesses can pay a relatively small amount of money (compared to the relevant cost of

physical hardware) to receive a phenomenal amount of storage space.

As more and more companies rely on the Cloud, this means that the need for a contingency

plan in the case of file loss can be completely eradicated. Recovery times are quick and

relatively simple should anything go wrong, as all information and data is backed up onto the

servers. This is great in the event of files being accidentally removed, or worse, stolen.

A huge benefit to businesses is the ability for multiple staff to access, edit and share folders

and files that they are currently working on. This means that collaboration between teams of

people can be greatly improved, and no time is wasted on uploading and emailing files

individually. This end result for businesses – efficiency.

Cloud resources are easily scalable – they can be altered to suit growing needs, which is

perfect for companies who are unsure of their growth curve.

On the topic of efficiency, it’s also worth noting that using Cloud as your storage solution

will use at least 30% less energy than by using regular servers based on-site.

The Cloud has also rapidly become more and more accessible via smartphones and tablets –

meaning that your documents are truly available anytime and anywhere. For people who

work on the move, or do a lot of travelling, this can be a lifeline for effectively managing

time away from the office.

Summer Internship Project Report SIMSREE, Mumbai

23

Project Outline & Deliverable details

Title: Seeding the cloud

Description: Brand awareness of CtrlS & Analysis of Market Potential for Cloud Products

Deliverables:

Under this project I was supposed to undertake the following tasks:

1. Understand CtrlS Cloud products and solutions

Initially for around 5 days, I was given training about the Company, its business

model, various products and services offered by company. Also, sufficient reading

material was given for studying the details on the above points. I also visited the

datacentre located at Mahape, Near Ghansoli, Navi Mumbai. This visit was designed

to make interns understand the infrastructure details of an actual datacentre which will

be crucial while understanding client requirements and how those can be

accommodated.

We also attended 2 conferences based on the agenda of Datacentres and Cloud

products. This also helped us understand global outlook and recent trends for this

industry.

Also, this phase included comparing the product and service portfolio offered by

company with its competitors. Analysing their strong footholds, core competencies,

target market either geography wise or product wise.

2. Identify the target prospects for these solutions

After getting sufficient hold on the knowledge about the products and services offered

by the CtrlS, I worked on understanding generic requirements by various types of

companies with respect to IT infrastructure.

For Ex. Companies having heavy data uploaded on their websites will need CDN

(Content Delivery Network) solutions.

Corporate offices will prefer mailing solutions.

IT / ITES companies need BCP (Business continuity plan) solutions

3. Create a survey to be administered to the client database

For getting above information, it was required to have a standard procedure to follow

and a standard set of questions to be asked to the companies. Hence we prepared

questionnaires which helped in keeping consistency in the survey which was to be

carried out. This questionnaire was reviewed and confirmed by our mentor.

Summer Internship Project Report SIMSREE, Mumbai

24

4. Carry out the survey/research and analysis

Using the questionnaire, survey was carried out to get the required information which

would help creating a deep profile of the prospective clients. Various ways to conduct

this survey was taking appointments and visiting the companies, cold calls, telephonic

conversations, Email communications and social media. We also met few clients

during the conferences which we attended.

5. Create a deep profile of target companies

In this deliverable, I worked on forming a detailed profile of selected companies. This

included company’s business area, size, nature of office work, their current IT needs

and IT solutions which they are using. This all information was supposed to be

entered into n CRM tool (kind of a database) used by company.

6. On the basis of the research and analysis, make product recommendations

In this phase, I discussed about the profiles of the companies studied with the

solutions team (led by solution architect) to understand which of the solutions offered

by CtrlS can serve the requirements of the companies. Based on this analysis and

discussions, I recommended relevant products and services to the companies which

were approached earlier for survey purpose.

7. Organize meetings with the clients for CtrlS sales team

Based on the responses given by companies, I pursued to get any possibility to get

prospective business from the approached companies. This included following up

with company representatives, discussing with them regarding any doubts about their

requirements or the solutions provided by CtrlS. And, on conviction, if they are

interested to have a meeting with CtrlS solution sales team, then I also organized

those meetings either at client location or at CtrlS office.

Method of Study

Market research

According to the American Marketing Association:

"Market research is the systematic gathering, recording and analysing of data about problems

relating to the marketing of goods and services."

The key words are:

• Systematic - using a clear, organised method or system

Summer Internship Project Report SIMSREE, Mumbai

25

• Gathering - knowing what data you are seeking, and collecting it

• Recording - keeping clear, organised records of what you discover

• Analysing - collating and interpreting data in order to draw out relevant trends and

conclusions that can be used as a basis for a strategy

• Problems relating to marketing - obstacles that are preventing the growth of the

business.

The first step was to gather secondary information. Secondary information is often called

'desk research' and is frequently the starting point for any research. This has already been

collected by someone else, often for another purpose. It often represents therefore, one of the

cheapest and easiest sources of information.

The data gathered in this way often helps to define and clarify problems within the context of

the research objectives. Following on from that, an organisation can look to generate the

more closely focused primary data it requires.

Data Collection Methods

1. Surveys

With concise and straightforward questionnaires, you can analyse a sample group that

represents your target market. The larger the sample, the more reliable your results will be.

In-person surveys are one-on-one interviews typically they allow to present people

with samples of products, packaging, or advertising and gather immediate feedback.

In-person interviews include unstructured, open-ended questions. In-person surveys

can generate response rates of more than 90 percent, but they are costly. With the time

and labour involved, the tab for an in-person survey can run as high as some

investment per interview.

Telephone surveys are less expensive than in-person surveys, but costlier than mail.

However, due to consumer resistance to relentless telemarketing, convincing people

to participate in phone surveys has grown increasingly difficult. Telephone surveys

generally yield response rates of 50 to 60 percent.

Mail surveys are a relatively inexpensive way to reach a broad audience. They're

much cheaper than in-person and phone surveys, but they only generate response rates

of 3 percent to 15 percent. Despite the low return, mail surveys remain a cost-

effective choice for small businesses.

2. Market Potential Analysis

The market potential analysis determines whether and to what extent a market for your

service or product exists. Therefore, it researches the number of potentially saleable units and

potential customers, and in addition, the price range for your products and services accepted

by the target group.

Summer Internship Project Report SIMSREE, Mumbai

26

The market potential analysis clarifies whether the market is receptive to your product or

service, or whether competitors have already exhausted the market potential.

The market potential analysis determines

If your product or service will appeal to consumers of the target market -

marketability,

How many consumers would buy your product or service at what price - potential

analysis

And what market volume you can count on - market position.

Market potential analysis - Market position - Marketability - Market volume

3. Desk Research

Desk research (secondary research), in contrast to primary research, means to gather

information from existing data. This can be data that has already been collected for other

purposes and is reused.

Secondary information is required in addition to research-economic terms as, on one hand,

not all data can be collected by you. On the other hand, the incorporation of secondary data

and / or a comparison of secondary and primary data supplement a study in a meaningful

way.

Methodology Used

We had datacentre tours at CtrlS Datacenters, Navi Mumbai. This helped us in understanding

product line and solutions offered by the company,

Colocation - server colocation, rack colocation

Public Cloud & Hosting - Cloud VPS, private cloud, Unmanaged Dedicated,

Managed Dedicated, MyCloud, hosted exchange, hosted linux

IT Infrastructure - storage on demand, online backup, DR on demand, High

Availability Solution, Cage-Raised Floor, Virtualization Server

We learned the target prospects of these products, created a list of companies which could be

targeted. We also had knowledge transfer session with partner companies Limelight

Networks and Global Outlook for CDN services and mailing services respectively. We did a

survey on these companies with which I could understand their requirements. The surveys

were done face-to-face, through telephonic interview and mail surveys. Based on the analysis

of survey result, we made product recommendations. Figure 4 shows the steps followed for

study in brief.

Summer Internship Project Report SIMSREE, Mumbai

27

Figure 6: Methodology Used

Data Collection & Analysis

Note: Refer Questionnaire 1 for data collection attached in appendices of report.

Sample Data recorded: 110 responses

Figure 7: Industry wise comparison

Above figure, Figure 7 shows various industries targeted by us during our project.

Knowledge Building

• Understanding CtrlS Products & Services

• Identifying & Profiling target customers

Data Collection

• Questionnaire Preparation

• Information gathering

• Visit to customer site

• Face to face interview

Business Creation

• Compilation of data to arrive at value proposition

• Lead generation

Summer Internship Project Report SIMSREE, Mumbai

28

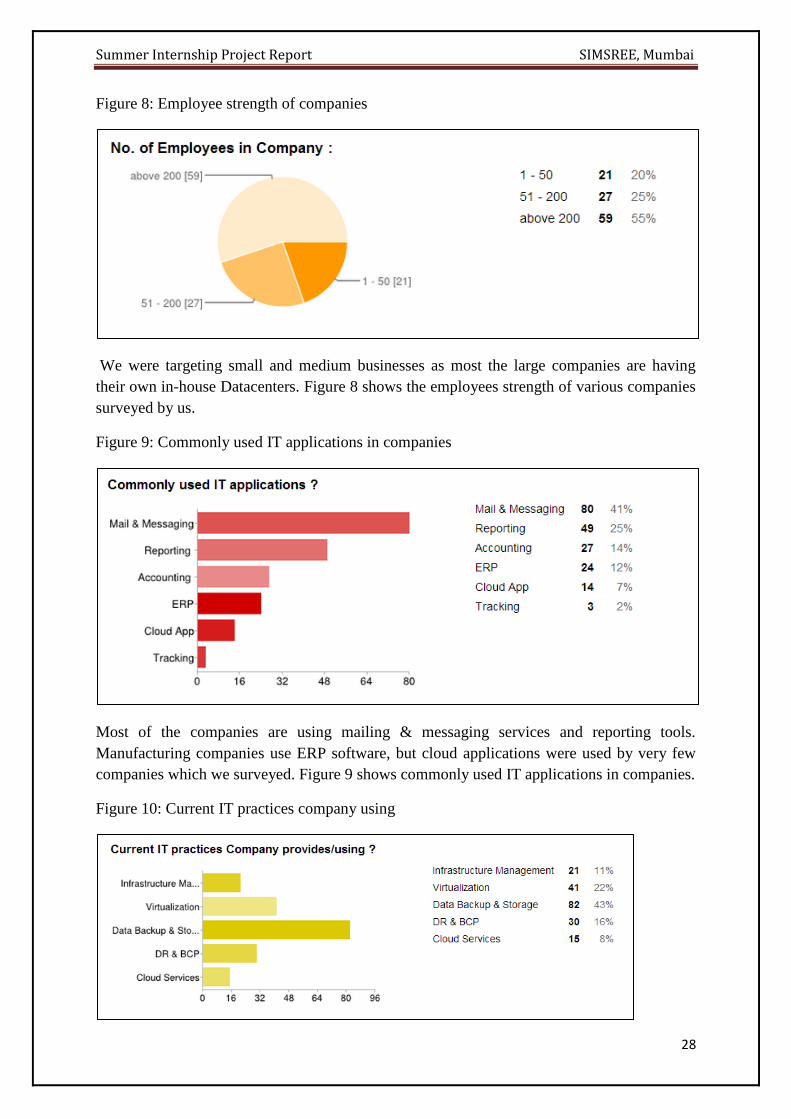

Figure 8: Employee strength of companies

We were targeting small and medium businesses as most the large companies are having

their own in-house Datacenters. Figure 8 shows the employees strength of various companies

surveyed by us.

Figure 9: Commonly used IT applications in companies

Most of the companies are using mailing & messaging services and reporting tools.

Manufacturing companies use ERP software, but cloud applications were used by very few

companies which we surveyed. Figure 9 shows commonly used IT applications in companies.

Figure 10: Current IT practices company using

Summer Internship Project Report SIMSREE, Mumbai

29

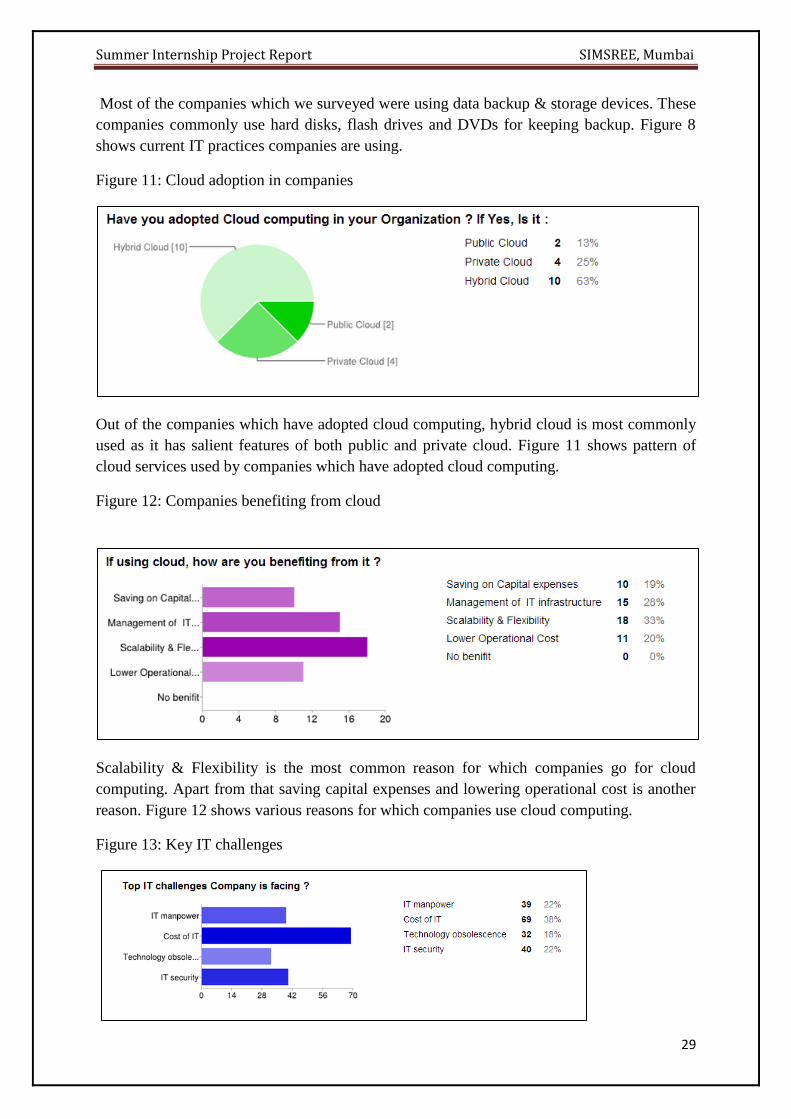

Most of the companies which we surveyed were using data backup & storage devices. These

companies commonly use hard disks, flash drives and DVDs for keeping backup. Figure 8

shows current IT practices companies are using.

Figure 11: Cloud adoption in companies

Out of the companies which have adopted cloud computing, hybrid cloud is most commonly

used as it has salient features of both public and private cloud. Figure 11 shows pattern of

cloud services used by companies which have adopted cloud computing.

Figure 12: Companies benefiting from cloud

Scalability & Flexibility is the most common reason for which companies go for cloud

computing. Apart from that saving capital expenses and lowering operational cost is another

reason. Figure 12 shows various reasons for which companies use cloud computing.

Figure 13: Key IT challenges

Summer Internship Project Report SIMSREE, Mumbai

30

Most of the companies have cost of IT has their pain point. Apart from that technology

getting obsolete is another major problem. Figure 13 depicts major IT challenges faced by

companies surveyed.

Figure 14: companies IT investment in future

Most of the companies specially manufacturing firms don’t have a specific budget allocated

for IT spending.

Summer Internship Project Report SIMSREE, Mumbai

31

Learning opportunities

Gartner IT Infrastructure Operations & Data Center Summit

Agenda of Summit: Accelerate Growth, Drive Transformation, Achieve Operational

Excellence

As the nexus of IT forces such as cloud computing, mobility, social media and big data start

being relevant in India, IT professionals are not only evaluating alternate ways of procuring

and managing IT services but new ways to drive business growth. Infrastructure &

Operations (I&O) professionals have the responsibility to inspire their businesses by being

agile, reliable, efficient and highly collaborative by striking a balance between the traditional

and the futuristic approaches of managing technology with an eye on containing the cost of

IT.

This second edition of IT Infrastructure Operations and Data Centre Summit in India euiped

IT and I&O leaders with the capability of making smart infrastructure investments which can

help to achieve operational excellence without ignoring need to optimize the cost structure.

Frameworks on the understanding the business value of cloud, mobility and big data coupled

with best practices of deploying virtualization, emerging infrastructure technologies and their

ability to deliver promising return on investment, was presented in this 2 day Summit.

The Gartner IT Infrastructure Operations & Data Center Summit offered a breadth and depth

of knowledge that uniquely met the requirements of data center professionals across

disciplines. Through prescriptive, practical advice — complemented by strategic

recommendations — the 3-track agenda addressed today's not-to-be ignored trends,

technologies and imperatives including:

Cloud Computing

Virtualization

IT Operations

Mobility

Modernization

Servers and Operating Systems

Disaster Recovery and Business Continuity

Storage

CtrlS was silver sponsor for the event.

Global High on Cloud Summit

About the Summit:

Anyone who follows technology trends has undoubtedly heard the term “cloud service”

thrown around a few gazillion times over the past few years. Cloud Computing has emerged

as a big surprise when people were struggling to get rid of the troubles involved with

traditional web hosting and computing solutions for their business ventures.

Summer Internship Project Report SIMSREE, Mumbai

32

Cloud Computing anywhere across the globe describes delivery of hosted services through

the internet. People are shifting their business applications from traditional software models

to the mighty cloud. You can hardly predict what would be our future if cloud computing

wouldn’t be there to manoeuvre establishments safely towards profitable positions.

The Information Technology market in BRIC is to grow at a CAGR of 14.1% over the period

2011-2015. One of the key factors contributing to this markets growth is the increasing IT

spending in BRIC. The IT market in BRIC market has also been witnessing increasing IT

spending by banking sector.

Through The Global High on Cloud Summit the issues, concerns, latest trends, new

technology and upcoming innovations on the Cloud platform were addressed and it provided

an open forum and opportunity to everyone in the industry to come together and share their

ideas & updates and provide a global outlook.

Key Topics:

Trends & Challenges – Cloud as a technology, current market trends & practices for

implementation.

Regulatory & Compliance major concern on Cloud! – Cloud computing seems simple in

concept, and indeed, simplicity of operation, deployment and licensing are its most appealing

assets.

Monitoring Cloud – Performance stats on the application, Unified ontology of Cloud

Computing, Cloud Scalability, Controls & compliance.

Big Data Cloud Computing – Big Data is a relatively new phenomenon. As with any new

adoption, the adoption of big data depends on the tangible benefits it provides to Business.

Mobile Cloud Computing – The analysis of the impact of mobile computing on the various

services, Mobile cloud computing gives new company chances for mobile network providers.

Security in Cloud – Applications and services based on cloud computing are dramatically

emerging. However, in order to enjoy the wide utilization of cloud computing through

wired/wireless networking, providing sufficient assurance of information security such as

confidentiality, authentication, non-repudiation, and integrity is the critical factor.

CtrlS was official green cloud partner

Summer Internship Project Report SIMSREE, Mumbai

33

Conclusion

The cloud has the potential to become the preferred mechanism for software delivery,

bringing more choices to organisations when selecting an application provider, and resulting

in fewer reasons to maintain their own applications on-premise. As such, cloud adoption will

increase dramatically; and when moving to the cloud, businesses will need to think carefully

about how they will ensure that cloud providers can meet promised service-level agreements

(SLAs).

We are also going to see a higher rate of adoption of mobile devices (smartphones and

tablets) within the workforce in 2013. These shifts should inspire enterprises to analyse and

plan for what kind of internal applications they will need in order to enable and mobilise

around cloud within the business.

CtrlS is the only company in India whose primary focus is on Datacenter business whereas,

other providers like Netmagic, Sify, Reliance, Tulip etc., considers Datacenter services as

part of their business. This clearly says that CtrlS is the only company in country which takes

Datacenter business seriously and should leverage on this advantage.

Despite being the hottest buzzword around, cloud adoption has been rather slow-moving,

accounting for a tiny 1.4% of the total IT spends of enterprises in India. Industry concerns

about cost are not deep enough to impact this number alone. The truth is, security in the cloud

is a real concern, and with an expected spike from USD 400 million to USD 4.5 billion by

2015, it is a good time to put to rest some of the biggest concerns Enterprises might have in

this regard.

Summer Internship Project Report SIMSREE, Mumbai

34

Recommendations

After analysing complete data following key areas company need to focus on:

1. As most of the companies are already practicing Mailing, Reporting & Accounting IT

services, company have to aggressively promote the Cloud Services offerings.

2. About 50% of companies we surveyed are having Data backup & Storage facility so

these companies should be approached for other services like DR, Cloud and Virtualization.

3. Around 48% of the companies we surveyed were having data backup & storage

facilities. The companies usually keep backup in CDs, DVDs, flash drives and hard drives.

These traditional devices don’t last for more than 5 years. These companies should be

targeted for pay per use Data backup & storage solutions.

4. 40% of the companies were having insufficient budget allocated for IT spending,

these companies should be advised on Opex models offered by CtrlS Datacenters Ltd.

5. Most of the companies use cloud solutions for scalability and flexibility. Most

companies find security features on cloud as real concern.

6. Small or midsize businesses (SMBs) are the most likely to adopt public IaaS/utility

hosting. CtrlS should consider preconfigured solutions for the SMB segment.

7. In the long term, SLA adherence and service provider quality and support will

determine total service costs, and the level of agility and elasticity end users can plan for in

their infrastructures. CtrlS should ensure that they strictly follow the agreed-on SLAs.

Summer Internship Project Report SIMSREE, Mumbai

35

Way ahead: Future Outlook at the industry

India Data Center market is expected to see significant growth in the next five years as there

has been increased adoption by Indian companies of the third party data center services and

the government has also increased its cloud computing initiatives where it is directly setting

up data centers and also using the services of the third party data center service providers.

Reliance Communications has announced the multiple orders bagged from Central and State

Government of India as the company has signed long term contract with The Department of

Post, Municipal Corporation of Greater Mumbai (BMC), Madhya Pradesh Border Checkpost

Development Company Limited along with Karnataka DISCOM and Chattisgarh DISCOM.

McKinsey has estimated that the third party outsourced data centre market in India is

expected to grow at a CAGR of 32% to Rs 5,500 crore by the year 2017 with verticals such

as banking and financial services, media and entertainment service, manufacturing,

international telecom providers and retail accounting for 70% of this growth. TechNavio's

analysts forecast the Data Center Equipment market in India to grow at a CAGR of 10.4%

over the period 2011-2015.

The Indian IT infrastructure market comprising of servers, storage and networking equipment

will reach US$2.05 billion in 2012, a 10.3% increase over 2011, according to Gartner, Inc.

The IT infrastructure market is expected to reach $3.01 billion by 2016. Revenue growth will

be primarily driven by ongoing data center modernization, as well as new data center build

outs. Servers are the largest segment of the Indian IT infrastructure market, with revenue

forecast to reach $754.5 million in 2012, and grow to $967.2 million in 2016. The external

controller-based storage disk market in India is expected to grow from $439.4 million in end-

user spending to $842 million in 2016. The enterprise network equipment market in India,

which includes enterprise LAN and WAN equipment, is expected to grow from $861 million

in 2012 to $1.2 billion in 2016. Gartner Analysts predict that Indian businesses are looking to

focus on optimizing the IT Infrastructure and strategy by implementing virtualization and

ongoing investment in large captive data centers mixed with the capacity growth initiated by

the data center service providers are the key drivers for growth. Mobility, social media and

cloud computing adoption will have significant influence on the way data centers are

designed, operated and managed their by the data center services providers.

Dimension Data estimates data centre market in India is growing at a CAGR of 22% and will

touch Rs 6,500 crore by 2016. BSNL offers managed co-location, managed hosting and cloud

services through the Internet Data Centers (IDC), which have been built by Dimension Data

for BSNL. This public-private initiative will leverage the strength of BSNL in telecom

infrastructure and vacant buildings and that of Dimension Data in providing data center and

cloud computing," Communications and IT Minister Kapil Sibal said while inaugurating

BSNL IDC services. Dimension Data operates and manages IDC centers, which are located

in Mumbai, Faridabad, Ahmedabad, Jaipur, Ludhiana and Ghaziabad. Each of these is run at

a Tier III level and all make use of vacant space BSNL has at its telephone exchanges.

According to Reji Thomas Cherian, VP, Telecom, Media & Entertainment, Capgemini India,

the Cloud Computing market including PaaS, IaaS and SaaS was worth $400 mn for India

alone. Data center services revenue is projected to touch $2.6bn in 2012. The managed

Summer Internship Project Report SIMSREE, Mumbai

36

security market in India was worth $321 mn in 2011 and is expected to see rapid growth.

Moreover, managed third party data center services generated revenues to the tune of $662

mn in 2011 and this too is on a high growth trajectory.

The majority of respondents would use the "Clouds" in the private sector as a data storage

device ("IaaS" - Infrastructue-as-a-service) use (43%). The potential use of software-as-a-

service service ("SaaS" - use of applications over the Internet) with 5% of mention, however,

is comparatively manageable. The benefits to consumers are also facing an added value for

software companies. Besides saving development cost as may be developed in the future

platform-independent, and a curb software piracy can be expected.

According to survey scalability, agility, and cost were the leading reasons why companies

were moving to the cloud. Companies just don’t want to be burdened by clunky servers that

require expensive time and resources to maintain. Instead, they want to outsource key

services to specialists so they can focus on being nimble and innovative with their products.

According to recent IDC report there will be the huge cloud adoption in future,

Globally, almost two-thirds of enterprises are planning, implementing, or using cloud

computing, and more than 50% of businesses agree that cloud computing is a high

priority.

However, more than three-quarters of businesses have apprehension about the

security, access, or data control of cloud computing.

Summer Internship Project Report SIMSREE, Mumbai

37

Self-assessment of the Internship

The Summer Internship Project was surely one of the best parts in the curriculum of the two

year PGDBM course. It provided me with an exposure of the very vibrant and rapidly

growing industry of Infrastructure outsourcing and datacenters.

Working as a Trainee at CtrlS Datacenters Ltd. also gave me an opportunity to study and

understand the cloud products and their market potential. This would surely increase the

prospects of shaping my career as a IT consultant in future.

Talking about the correlation of the Internship with classroom knowledge, it provided me the

platform to apply my skills and knowledge, to the given work under consideration; for

instance, analysing competitors, SWOT analysis of CtrlS Datacenters, Industry analysis. It

gave me hands on experience to work on some of the project deliverables which were under

consideration.

Thus, having gained insights of a totally new sector the Internship was a very good learning

experience for me.

Summer Internship Project Report SIMSREE, Mumbai

38

References

http://itbizcharts.blogspot.in/2011/11/india-third-party-hosting-data-center.html

http://searchdatacenter.techtarget.in/feature/Data-center-infrastructure-In-house-

hosting-versus-outsourcing

http://pic.dhe.ibm.com/infocenter/tivihelp/v28r1/index.jsp?topic=%2Fcom.ibm.tivoli.t

pm.scenario.doc%2Fvirtual%2Fccom_basics.html

http://www.vmware.com/virtualization/virtualization-basics/how-virtualization-

works.html

http://www.webopedia.com/TERM/C/co_location.html

http://www.gartner.com/technology/summits/apac/data-center-india/about.jsp

http://www.slideshare.net/rajeshdgr8/india-data-center-market-2011

http://www.ctrls.in/downloads/emerging_data_center_trends.pdf

http://www.nasscom.in/mr-p-sridhar-reddy-cmd-ctrls

http://www.theglobalhighoncloudsummit.com/#!about-the-summit/c24fs

http://itbizcharts.blogspot.in/2012/09/india-data-center-market-2012.html

http://www.skopos.de/en/newspress/169-cloud-computing-und-cloud-gaming-die-

zukunft-ist-heiter-bis-wolkig.html

Competitive Landscape: Indian Utility Hosting and Cloud IaaS Providers Published: 2

August 2012 Gartner

Summer Internship Project Report SIMSREE, Mumbai

39

Appendices

Questionnaire 1: Detailed

1. Company Name / Nature of Business:

2. Number of Employees in Company:

5 - 10

10 - 20

above 20

3. How many people work in IT team ?

Up to 2 people

2 - 5

> 5 people

4. How many Computers does your Organization have?

5 - 10

10 - 20

Above 20

5. What is the Installed Servers?

1 - 5

above 5

None

6. What are the most commonly used IT applications?

7. Have you attempted Server virtualization? If yes, what level?

No, we have not attempted server virtualization

above 70%

50% - 70%

30% - 50%

Less than 30%

Summer Internship Project Report SIMSREE, Mumbai

40

8. What are the current IT practices your company provides/using?

Email & Messaging

Data Backup

Network & Security

Infrastructure Management

9. Are you aware of Cloud Computing ?

(.....If your answer is No, go to Question no.14)

Yes

No

10. Have you adopted Cloud computing in your Organization ? If Yes, Is it :

Public Cloud

Private Cloud

Hybrid Cloud

11. If you are currently using the cloud, what are you using it for ?

Online Backup

Product testing

On-Cloud apps

12. If using cloud, how are you benefiting from it ?

Saving on Capital expenses

Management of IT infrastructure

Scalability & Flexibility

Lower Operational Cost

No benefit

13. Are you aware of BYOD (Bring your own device) ?

Yes, I am aware

Yes, I am aware and have implemented in my organization

No

14. Do you have a Disaster Recovery (DR) Plan?

DR helps you in preventing your data from accidents like, Fire/water/earthquakes..

Still in the Planning Stage

Plan to set up DR in next 6 months

Plan to set up DR in next 6 months to 1 year

Plan to set up DR in next 1 to 2 years

No plan as yet for DR

Summer Internship Project Report SIMSREE, Mumbai

41

15. What are the top IT challenges you are facing?

IT manpower

Cost of IT

Technology obsolescence

IT security

Other:

16. How are you tackling these Challenges?

Considering Partially Outsourcing IT requirements

Considering Fully Outsourcing IT requirements

No solution

17. What Financial constraint do you foresee in meeting your IT challenges?

Financing not much of constraint for the right Solution

Setting up IT is a capital intensive

Difficult to calculate and justify ROI

Other:

18. Planned investment in IT in the next:

0 - 6 months

6 - 12 months

After 12 months

19. What is your Annual IT budget?

< Rs. 5 lakhs

Rs. 5 lakhs to Rs. 10 lakhs

Rs. 10 lakhs to Rs. 25 lakhs

> Rs. 25 lakhs

20. Do you have Business Continuity Plan in place? If yes, do you have in-house BCP

team?

Yes

No

21. Your Contact Details: NAME, DESIGNATION, EMAIL ID , CONTACT NO.

Summer Internship Project Report SIMSREE, Mumbai

42

Questionnaire 2:

Company Name

Nature of business

BFSI

IT & ITES

Telecom

Manufacturing

Government

Services

Media

Pharma

Other

No. of Employees in Company :

1 - 50

51 - 200

above 200

Commonly used IT applications ?

Mail & Messaging

Reporting

Accounting

ERP

Cloud App

Tracking

Summer Internship Project Report SIMSREE, Mumbai

43

Current IT practices Company provides/using ?

Infrastructure Management

Virtualization

Data Backup & Storage

DR & BCP

Cloud Services

Have you adopted Cloud computing in your Organization ? If Yes, Is it :

Public Cloud

Private Cloud

Hybrid Cloud

If using cloud, how are you benefiting from it ?

Saving on Capital expenses

Management of IT infrastructure

Scalability & Flexibility

Lower Operational Cost

No benifit

Top IT challenges Company is facing ?

IT manpower

Cost of IT

Technology obsolescence

IT security