summer internship project report

TRANSCRIPT

1

Chapter 1 - Introduction

1.1 Company Profile

Krishna Maruti Limited

KML entered the auto interior manufacturing business with a single product (seating system

for Maruti 800 CC Car) in year 1994.

The company manufactures 8 different products with over 100 different models.

India's First Total Auto Interior Group of Companies manufacturing all the requirements of

auto interiors including Seating Systems, Rear View Mirrors, Head Rest Assemblies, Arm

Rest Assemblies, Seat Trims (Covers), Injection Moulded Door Trims, Roof liners &

Moulded Carpets.

Figure 1.1.1

The company reached all this in short spans of time because they firmly practice the ' 6 - F'

principle throughout the organisation:

Focused: Focus towards customer delight, engineering infrastructure, cost

consciousness and continuous improvements through '5 - S', 'Kaizens', Quality Circle

Meetings and Suggestion Meetings.

Fast: Fast system & technological up - gradation and implementation.

Flexible: Flexible towards customer requirements.

Friendly: Creating friendly environment among customer, employees & vendors.

Firm: Firmly adhering to laid down policies & procedures &

2

Fun: Achieving the targets in stipulated time.

In order to be a leader in its field, a strong centralized R & D Centre (first of its kind in

country) was established with an investment of $ 1.5 Million. This centre is the best in the

country and is recognized by the Department of Scientific & Industrial Research, Ministry of

Science & Technology, and Govt. of India. This centre is capable of not only testing as per

International Standards but can also issue Test Certificates to other Seat manufacturers. This

test centre can also perform test for non - Automotive components for Endurance &

Repeatability.

Vision of the Company

Our Vision, Our Goals, Our Focus, Our Dreams, all these are very clear to us, that we have

to be a WORLD CLASS COMPANY and this, we must achieve.

To achieve this, Quality, Cost, Delivery& Development are the key factors and all of us I am

sure, recognize this.

To achieve anything, what is also very important is Discipline, Time Management, Systems

and Procedures and above all respect for individuals.

To recognize the respect for the individual, we need to get the FEAR, DOUBT &

INSECURITY out of everybody’s system as we all need to Learn and ultimately develop.

The need of the hour for success is to use every brain in the organization, as everybody has to

have something to contribute in terms of value addition.

Products

Seating Systems

KML started its operations with only 1 model and a production capability of 40 sets/day.

Today we manufacture 16 different models. Krishna Maruti Limited has a production

capacity of 400,000 Seating Systems/ annum.

Presently Krishna Maruti Limited produces 16 different Variants of seating systems of

following

3

Models: BALENO, ESTEEM, WAGON R, ZEN, OMNI, MARUTI 800cc & ALTO.

Krishna Maruti Limited has capabilities to Manufacture Seating Systems as an OE to

potential customers for their range of products.

Rear View Mirrors

Company produces a range of Outside & inside Rear View Mirror Assemblies for Maruti

Udyog Limited and Honda Siel Cars India Limited.

With 35% OE market share, Every Fifth Indian Car has Rear View Mirror Assembly

manufactured by Krishna Toyo Limited.

The range can easily be extended to suit the requirements of other Auto Manufacturers.

Head and Arm Rests

Krishna Pads Limited uses NC Controlled Puromat High - Pressure Foaming Machine for its

foaming application for producing Head Rest & Arm Rest Assemblies for all models of

Maruti's Car.

Seat Trims

Krishna Trims Limited is catering Krishna Maruti Limited's total requirement of trims. KPL

provides these items for the following cars:

Standard 800

Omni Van HR

Zen

Esteem

Wagon R

Baleno

Auditorium Seat

Krishna Quinette is a 50:50 Joint Venture Company of Krishna Maruti Limited with Quinette

Gallay of France.

Quinette Gallay is the World Leader in the field of Auditorium Seats with over 70% of its

4

total production servicing the Export Business. Quinette Gallay has presence in all the 6

Continents and installations in over 50 Countries.

Krishna Quinette produces special seating system for auditorium applications. The company

started its Commercial Operations since July 2003.

Injection Moulded Door Trims

This division manufacturer:

Door Trims

Roof Headliners

Carpets

For producing Injection Moulded Door Trims, we have Toshiba's (Japan) 1300 Tonne

Machines and for the Assembling of various plastic parts together, we use Branson's (USA)

Ultrasonic Welding Process.

For our Roof liners, we have Meyer's (Germany) Lamination Machine & Thermoforming

Machine. We are the only Indian Company to use Twin Head Robotic Water - Jet Cutting

Machine from ABB - IR Sweden.

The company is all set to use its specialty in Injection Moulding for producing components

for White Good Industry.

Roof Liners

The division was setup in July 2000 & the machines for lamination & thermo foaming was

commission in December 2000. The commercial production started in Feb 2001.This plant

can manufacture 2,00,000 Roof Headliners of various models per year.

For Lamination of Substrates, Fully Automatic & Continuous Lamination Machine from

Meyer - Germany is used. The Machine is capable of laminating up to five different materials

together in a single operation. For moulding the Laminated Substrates into the required

shape, the Thermoforming Press is used. This Press is High Capacity Single Acting

Hydraulic Machine with advance controllers governing accurate controls over required

parameters for consistent results.

5

The Twin Head Water Jet Cutting Machine from ABB IR - Sweden is the only machine of its

kind in India. This highly sophisticated machine is not only capable of cutting materials in an

very environmentally friendly & energy efficient way. The use of such an advance system

ensures very high degree of Accuracy, Precision & Repeatability.

Raw Materials Used in Production

At Krishna the basic raw materials used are:

Polyurethane raw materials to produce moulded cushion pads -Polygons &

Isocyanides.

CRCA sheet metal components.

Tubular lengths of various sizes.

Water soluble black paints & pre-treatment chemical.

PVC fabrics.

Laminated polyester & cotton fabrics.

Wire Spring

Polypropylene for injection moulded components.

Hardware items.

Various industrial consumables like mig wire, adhesives, safety items, spot welding

electrodes etc.

Seat adjuster mechanism assemblies.

Seat recliner mechanism assemblies.

Rear seat lock assemblies.

Automotive fabric.

Treads.

Substrate for roof head liner (rigid foam).

Mirror sheets.

Felt for moulded carpet.

Needles punch fabric for moulded carpet.

CRCE sheet.

Non - woven fabric.

Fasteners for various sizes.

6

1.2 Purpose of Study

Financial analysis of a company is conducted to judge the financial soundness and profits of

the company. It helps in evaluating the current position of the firm in terms of finances

available and suggesting the areas of improvement in it. The Research is to be conducted on

current years and last year’s financial reports which would help in analysing the company’s

current financial position and compare it with previous year’s financial position. A SWOT

analysis of company would also be conducted which would help in knowing the strengths,

weakness, opportunities and threats in context to the company. The research would also

provide an insight to the company’s management about the company’s financial position and

accordingly through the results obtained they can formulate and implement policies which

would help them to improve the financial position of the company if required.

1.3 Context of Study

Finance is an important part of any organization as major decisions in an organization are

taken with the amount of finances available with the company. Proper management of

finances helps the firms to grow and avoids undesired position for the firm to be in like

bankruptcy. Financial analysis of a company is conducted so as to be aware of the current

financial position of the company and the current resources available with the company with

its ability to meet the expenses of the company. It also suggests the areas in which

improvements and savings can be made. The financial analysis of a company provides the

management with the insight to know the position of finances of a company. With the help of

many ratios calculated and comparative analysis done the current financial position of the

company can be interpreted.

1.4 Significance of the Study

Research study would be conducted in an in depth way which would provide the management

a clear cut picture of the organization financial position which would help them to come up

with some different policies regarding handling finances of the company. The research study

would also help the teachers in evaluating the student’s understanding and interpretation of

the financial position of the company through usage of different methods and techniques for

arriving at a particular figure.

7

1.5 Theoretical Framework

In the research study various ratios would be calculated of the year 2011 and 2010 with the

help of company’s balance sheet and comparison of these ratios would be done to check

whether the company has become financially strong or not. The ratios would be calculated in

Microsoft excel and would be interpreted with the help of suitable charts. Subsequently in the

excel sheet comparative and common size balance sheet and income statement would be

created and they would be interpreted with the help of charts. Through this procedure we

would get to know that the firm was better in the financial year ending 2010 or in the

financial year ending 2011.

8

Chapter 2 – Review of Literature

2.1 Review of Literature

Upadhyay1 (2001) said that financial analysis should be adopted to appraise the financial

performance of the companies. Financial analysis basically included calculation of various

ratios which are also beneficial for the investor as he/she gets to know about the financial

position of the company. The limitations faced were that the companies on which the

financial analysis was performed had different method of calculations.

Prather2 (1999) mentioned that application of ratio analysis technique to personal financial

statements offers insight into the strengths and weaknesses of a family financial situation.

Ratios are calculated in assessing the general or specific financial position of a person. The

limitations faced in this article basically were that the household people generally don’t

reveal their original data in terms of expenses and incomes which they have for a financial

year.

Martikainen3 (1998) stated the core areas of research were considered to be financial ratios. It

is observed that it is typical of financial ratio analysis research that there are several

unexpectedly distinct lines with research traditions of their own. A common feature of all the

areas of financial ratio analysis research seems to be that while significant regularities can be

observed, they are not necessarily stable across the different ratios, industries, and time

periods. This leaves much space for the development of theoretical basis and for further

empirical research.

Fujii4 (2001) said that the financial system plays a fundamental role in the economic system

in facilitating the transfer of resources, liquidity and price information. Banks and financial

markets are two basic structures that consist of financial system and they are distinct in the

way they perform the financial functions. The analysis to be done with banks and financial

markets has to be done in a consolidated framework which would also provide a direction for

future research.

9

Altman5

(1998) mentioned the usage of traditional ratio analysis and discriminant analysis

used for prediction of corporate bankruptcy. Several types of models and calculations were

performed for the prediction purpose. The concluding remarks given in the article were that

traditional ratio analysis alone can predict the bankruptcy but if used jointly with discriminant

analysis it can be helpful in predicting the company’s bankruptcy. The limitation from the

above study was that the firms which were examined were all publicly held manufacturing

corporations for which comprehensive financial data were obtainable including market price

quotations.

Bravo6 (2006) mentioned in his research article that analysis is based on the existence of a

relationship of individual ratio. The article also used the data envelopment analysis

methodology for improving the efficiency in measurement.

Krivonozhko7 (2011) stated in this article the comparison of data analysis with data

envelopment analysis approach. It is shown that using ratio analysis implies that a one

multidimensional space is projected onto other subspaces many times. As a result, significant

distortion of the performance assessment of units takes place. The theoretical results are

validated by computational experiments on the data taken from financial accounts of Russian

banks.

Edmister8 (2009) wanted to study and test a number of methods of analysing financial ratios

to predict small business failure. Although not all of the methods and ratios are predictors of

failure, many ratio variables are found which do predict failure of Small Business. Using

step-wise multiple discriminant analysis on the simple correlation of the entering variable

with the included variables, a function of independent ratio variables, which is highly

accurate in classifying borrowers in the test sample, is developed. Methods of analysis found

useful are classification of a borrower's ratio into quartiles relative to other borrowers in the

sample, observation of an up- or down-trend for a three-year period this leads the author to

qualify his conclusion above with the provision that at least three consecutive financial

statements be available for analysis of a small business.

10

Singh9 (2002) mentioned in his article that financial ratios have always been a valuable tool

for lodging industry managers. Ratios allow the user to summarise and analyse related data to

provide meaningful information for making decisions. The purpose of the present study is to

identify commonly used ratios in the lodging industry and discover their importance level for

lodging financial executives. Operating and Profitability ratios clearly stand out as the most

important ratios for lodging managers. The study makes a contribution by educating

managers about the range of ratios and their relative importance.

Athanassopoulos10

(1994) mentioned in his article that the use of ratio analysis in itself is

insufficient for assessing performance, and that more advanced tools like data envelopment

analysis should be used to complement ratio analysis. Data envelopment analysis is used in

the paper to address a series of issues concerning the measurement of corporate performance,

which includes an assessment of sales' efficiency, the effects of economies of scale,

benchmarking of a firm's performance and the association between industry groups and

performance. The paper uses data drawn from the grocery industry in the UK.

Mr. Choi11

(1983) stated that financial ratios, which may be appropriate measures of financial

risk and return, are often misused when applied to foreign companies. This is due to

differences in international accounting principles. A more serious problem, however, is that

even when ratios are based on U.S. GAAP, they are misinterpreted because the U.S. investor

does not understand a particular foreign environment that influences all financial ratios in that

environment.

Salo12

(2010) stated that determination of ranking intervals, which indicate the best and worst

efficiency rankings that a DMU can attain relative to other DMUs and dominance relations,

which show what other DMUs a given DMU dominates in pairwise efficiency comparisons.

Unlike conventional efficiency scores, these results are insensitive to outlier DMUs. They

also show how the DMUs' efficiency ratios relate to each other for all feasible weights, rather

than for those weights only for which the data envelopment analysis (DEA) efficiency score

of some DMU is maximized.

11

Ahrendsen13

(2012) mentioned that the research is to evaluate the financial performance

measures calculated and reported by the Economic Resource Service (ERS) from ARMS

data. The evaluation includes the calculation method and the underlying assumptions used in

obtaining the reported values. The financial measures calculated and reported are compared

with those recommended by the Farm Financial Standards Council (FFSC). The values

reported by ERS are duplicated and alternative methods for calculating the financial

performance measures are considered. The values obtained from the various calculation

methods are compared and contrasted.

Royer14

(1991) stated that using the comparative ratio analysis through nonparametric

statistical methods provides no evidence to support the hypothesis that U.S. farmer

cooperatives generally are financially weaker than other firms. Although some cooperative

groups had lower current ratios than industry standards, most of these groups consisted of

marketing associations for which differences may be explained largely by the unique business

relationships between the associations. Comparisons of debt/equity ratios indicate that, except

for regional grain and farm supply associations, cooperatives generally are less leveraged

than other firms.

de15

(2011) stated that to reduce the number of financial ratios and to find out the categories

of financial ratios on the basis of empirical evidence, factor Analysis technique is being used

successfully by different researches during the last three decades. In this study Factor

Analysis has been applied over audited financial data of selected cement companies of India

for a period of 10 years. Initially 44 financial ratios grouped in 7 categories are selected for

the study. Before conducting Factor Analysis, variables having low inter-correlation with the

other variables are excluded.

Hsieh16

(2001) mentioned that ratio analysis is an excellent way of looking into a firm’s

financial status. In a multi-criteria decision-making framework, poor quality of criteria

selection, i.e. financial ratios, will consequently undermine the quality of evaluation. As each

sector of the industry is intrinsically unique, the set of critical ratios for different sectors will

certainly vary. The approach for finding useful financial ratios will not distinguish itself with

respect to the concerned sector rather than the purpose of analysis. The proposed approach

incorporates the concept of multi-criteria decision making and the entropy method. The

approach is demonstrated in a case study in which major property development firms in

Taiwan are evaluated.

12

Mr.Hsu17

(2010) stated that in today’s information technology world, real time financial data

is readily available via many financial websites, such as MSN Money, Google Finance etc.

The incorporation of computer technology in finance classes has become more popular than

ever in this information technology environment. Based on his experience as a finance

professor, he has summarized that his teaching note to demonstrate an alternative tool in

performing financial ratio analysis. The class assignment presented is designed to help

students learn how to assess the company’s overall operations and current financial standing

via an on-line database available in MSN Money website. It can be used in any corporate

finance class. He collected student feedback on the assignment, and the vast majority of the

survey participants perceived the assignment as a very good learning experience. The only

limitation is that online updating of the websites should be done on a regular basis.

13

Chapter 3 – Research Methods and Procedures

3.1 Research Objective

The primary objective of my project would be to provide a thorough analysis of two financial

years i.e. 2009 – 2010 and 2010 – 2011. This will be mainly accomplished by employing a

detailed ratio analysis on the financial data available for two years. In addition to this

comparative balance sheet would also be analysed which would help in better comparison of

the financial position of the company for two years. The report will also focus on the non –

financial aspect using a strategic planning tool known as SWOT analysis which focuses on

strength, weakness, opportunities and threats for the comp any. The main aims and objectives

of the report can be summarized as follows –

To analyse the strength, weakness, opportunities and threats which have resulted from

the adopted strategy and their impact on the company as a whole.

To analyse the Cash Position, liquidity, profitability and solvency position of the firm.

To perform a comparative balance sheet analyses, this would provide a better

understanding of the financial position of the firm.

To analyse the overall efficiency of the firm through calculation of ratios.

3.2 Research Design

The research design which has been used in my study is descriptive design as the current

information has been obtained through the current source of information i.e. annual reports of

the company and comparison design which basically includes comparison two financial years

of Krishna Maruti ltd.

14

3.3 Research Questions

These research conducted would be help us to answer the questions for which the research is

being conducted.

The basic questions included in my research design are –

1. In which year Krishna Maruti ltd. is performing better through the calculation of the

ratios?

2. In which year Krishna Maruti ltd. Have a better liquidity ratio?

3. In which year the Cash Position ratio of Krishna Maruti ltd. is better?

4. Are the expenses of the company under control?

3.4 Instruments Used

The main instruments used in my research study without which the research couldn’t have

been conducted are the respective company’s annual reports. These reports are the core

aspect of the respective study as many figures calculated in excel are done through them only

and the comparisons done is been through them only.

3.5 Techniques Used

Ratio Analysis

Ratio analysis is one of the main accounting techniques of financial analysis to evaluate the

financial position and performance of a company. It involves comparison and calculation of a

number of profitability, liquidity, efficiency and gearing ratios which in turn paint a thorough

picture of company’s performance over a period of time.

Ratio analysis helps in the following ways –

It helps in simplification of the financial statements of the business and also helps in

providing a complete picture of various changes in the financial condition of a

business.

It helps the management in making investment decisions by seeing at the various ratios

calculated.

The ratios calculated also helps in intercompany comparison.

15

Limitations of Ratio Analysis

Different Companies may adopt different accounting policies which are like different

methods of depreciation and which in turn lead to different figures.

The figures in company’s annual report is likely to be of several months out of date

and may not provide current and best indication of performance.

Careful interpretation of ratios calculated is very important so as to proper decisions

by the management can be taken; wrong interpretation of ratio analysis can make the

business suffer.

SWOT Analysis

A SWOT analysis is carried out in this Research Report as the main business technique used

to analyse internal and external factors which have an impact on the company. It carries out

an assessment of a company’s strengths and weaknesses. It also evaluates the opportunities

and threats that may arise in the future for the company. This involves an analysis of external

factors such as the economic environment and the industry.

Limitations of SWOT Analysis

One major shortcoming with the SWOT analysis is that although it emphasises the

importance of the four elements associated with the organisational and environmental

analysis, it does focus on how the company can identify the elements for their own company.

For example, what if a strength identified by the company is not truly strength? While a

company might believe its customer service is strong, they may be unaware of problems with

employees or the capabilities of other companies to provide a higher level of customer

service

16

Chapter 4 – Data Analysis and Interpretation

4.1 SWOT Analysis of Krishna Maruti ltd.

Strengths

Joint Venture

Krishna Maruti ltd. is a group which is in joint venture with Maruti Suzuki ltd. and it supplies

them the interior of their cars, so Krishna group has a fixed client and therefore the sales

expenditure of company is less in terms of searching of clients.

Stronger Brand Image

In this type of industry Krishna Maruti ltd. holds a very strong brand image as it also

manufactures seats for cinema hall like PVR movie halls. The reason for having a strong

brand image is because of its joint venture with Maruti Suzuki ltd. which has the maximum

number of Cars selling in India, so other car manufacturers company in India automatically

give them contracts of manufacturing car seating systems for their cars.

Weakness

Decline in Sales

The main client of Krishna Maruti ltd. is Maruti Suzuki ltd. so whenever there is a strike at

the plant of Maruti Suzuki ltd. the sales income of Krishna Maruti ltd. is heavily affected,

thus which leads to a high decline in the profits of the company too.

Shortage of Absolute Cash

The amount of absolute cash available with Krishna Maruti ltd. is quite less which is a

weakness for the company because to meet its daily expenses the company has to avail short

term loans or working capital loans, which in turns increases the interest expenses of the

company.

Opportunities

New Products

As Maruti Suzuki ltd. launches new product in the market like Ertiga, Krishna Maruti ltd.

also has to manufactures new product which increases the sales of the company and hence

also the profit margin of the company.

17

Threats

Risk of Losing Customer

Due to many companies now entering in this type of industry, competition is seeping through

this industry and the company has to work harder to maintain the customer base with them.

SWOT ANALYSIS IN A NUTSHELL

Figure 4.1.1

Strenghts • Joint Venture

• Stronger Brand Image

Weakness • Decline in Sales

• Shortage of Absolute Cash

Opportunities • New Products

Threats • Risk of Losing Customer

18

4.2 Data Analysis and Interpretation

Table of Ratios

Table No. 4.2.1

Type of Ratios Year Ending 2010 Year Ending 2011 Absolute Cash Ratio 0.08 0.05

Cash Position to Total Assets

Ratio

3.85 2.35

Interval Measure 5.75 3.29

Current Ratio 1.08 1.24

Quick Ratio 0.46 0.56

Debt – Equity Ratio 1.47 0.98

Proprietary Ratio 0.2 0.28

Total Liabilities to Net worth

Ratio

1.71 1.46

Gross Profit Ratio 13.1 14.75

Net Profit Ratio 1.78 1.85

Operating Profit Ratio 3.65 2.07

Return on Assets 0.045 0.058

Return on Capital Employed 0.17 0.12

Raw Material Expenses 86.2 85.4

Production Expenses 2.57 3.13

Administrative and Selling

Expenses

2.33 2.74

Assets Turnover Ratio 2.55 3.13

Fixed Assets Turnover Ratio 6.07 8.12

Working Capital Turnover

Ratio

60.54 29.91

Inventory Turnover Ratio for

Finished goods

29.26 32.83

Inventory Turnover Ratio for

Raw Materials

54.25 64.08

Inventory Holding

Period(Finished Goods)

12.47 11.11

Inventory Holding

Period(Raw Materials)

6.72 5.69

Fixed Charge Coverage Ratio 4.96 4.24

Overall Profitability Ratio 17.84 11.55

19

0

0.02

0.04

0.06

0.08

20102011

2010

2011

Ratio Analysis of Krishna Maruti ltd. for the year 2009 – 2010 & 2010 – 2011

Cash Position Ratios

Absolute Cash Ratio

It is basically the company’s ratio of current cash and cash equivalents to meet its current

liabilities. Ideal Ratio or the benchmark ratio in this case varies from industries to industries.

It basically helps to look into the figures of cash and readily convertible cash to the extent

which can meet the company’s current liabilities.

Figure 4.2.1

From the above Figure 4.2.1 the absolute cash ratio for the company in the year 2010 is 0.08

and for year 2011 is 0.05 so we can interpret that the ratio has decreased in year 2011 from

the previous year of 2010, which means the readily available cash with the company has also

decreased, but on other hand the good thing is that the current liabilities of the company for

the year 2011 has also decreased.

20

0

1

2

3

4

20102011

2010

2011

Cash Position to Total Assets Ratio

Cash position to total assets ratio indicates the proportion of liquid cash in the total assets of

the entity. This helps the company to analyse the liquid cash which is at present with the

company i.e. ready cash available.

Figure 4.2.2

From the Above figure 4.2.2 the cash position to total assets ratio in the year 2010 is 3.85 and

2011 is 2.35, so the ratio for the company has declined in the year 2011 as in comparison to

year 2010 not because that the amount of total assets increased in 2011 but due to sale of the

marketable investments of the company in the year 2011 so the amount of cash reservoir

decreased thus it also lead to decline in the cash position to total assets ratio.

21

0

1

2

3

4

5

6

20102011

2010

2011

Interval Measure

Interval Measure ratio helps to determine the number of days in which the company can

measure its expenses with the amount of cash liquidity available. The cash position which

should be maintained by the company should neither too low or neither too high. A high ratio

would indicate that the business is having idle cash and a too low ratio could land the

company into trouble as it might not be able to cover up its day to day expenses.

Figure 4.2.3

From the Above figure 4.2.3 the interval measure ratio in the year 2010 is 5.75 and 2011 is

3.29, which means that ratio was on a higher side in 2010 and the company had a good

amount of cash liquidity available to meet its day to day expenses, but for the next year the

liabilities also decreased, so the amount in liquid cash was also decreased and used for other

purpose. Company is doing optimum utilization of its funds.

22

1

1.05

1.1

1.15

1.2

1.25

20102011

2010

2011

Liquidity Ratios

Current Ratio

This ratio is basically calculated to give an idea of the company’s ability to pay its short term

liabilities with the use of short term assets. Higher the ratio means more ability of the

company to pay its liabilities. A ratio under 1 would mean that the company would be unable

to pay its current liabilities if they become due at that point of time. The Benchmark ratio for

current ratio is generally 2:1. A much higher ratio would indicate that the company is not able

to manage its current assets properly and fuller utilization of the assets is not taking place.

Figure 4.2.4

From the Above figure the current ratio in the year 2010 is 1.08 and 2011 is 1.24, which

means that the ratio in the year 2010 is closer to 1 and it is not a good sign for the company

because if the liabilities become due at that point, company would face problem in paying

them back but in the next financial year i.e. 2011 this ratio increased to 1.24 which means

that the company has improved its position to meet the current liabilities if they occur at that

point of time. The optimum ratio that should be maintained by the company is 2:1 as it shows

that adequate funds are with the company for meeting its current liabilities.

23

0

0.1

0.2

0.3

0.4

0.5

0.6

20102011

2010

2011

Quick Ratio

Quick Ratio is calculated to check the firm’s ability to meets its current liabilities with most

of its liquid assets. It basically takes into consideration the most liquid assets available with

the company and includes stock, bonds but it removes inventory from the liquid assets as

some companies have problem in converting their inventories instantly into cash. The

benchmark ratio in this is generally 1:1.

Figure 4.2.5

From the Above figure 4.2.5 the quick ratio for the company in the year 2010 is 0.46 and

2011 is 0.56, which means that the ratio for Krishna Maruti ltd. has increased from its

preceding year 2010 due to increase in the amount of the cash available with the company

basically. This is good sign for the company, more the ratio close to 1 it is better for the

company. The company in the year 2011 is in a more good position in terms of finances to

pay off its liabilities with its most liquid assets.

24

0

0.5

1

1.5

20102011

2010

2011

Capital Structure Ratios

Debt – Equity Ratio

Debt – Equity Ratio basically means the proportion of outside debt and equity in firm’s

capital. An optimum debt – equity capital structure is preferred by any organization because

excess of outside funds can increase the interest amount which has to be paid. Debt – Equity

majorly depends upon the industry in which the company is operating.

Figure 4.2.6

From the above figure 4.2.6 the debt - equity ratio for the company in the year 2010 is 1.47

and 2011 is 0.98, which means that the Debt – Equity ratio was on a higher side in 2010

because of higher proportion of debt in 2010 so more interest is being paid, but in 2011 there

was a subsequent fall in the debt – equity ratio which is due to repayment of loans which in

turns also lowers the total interest amount of loans and enhances the liquidity of the firm.

25

0

0.05

0.1

0.15

0.2

0.25

0.3

20102011

2010

2011

Proprietary ratio

It is the Proportion of shareholder’s funds to the total assets of the company. A higher ratio

basically indicates that the firm has sufficient amount of equity to support the functioning of

the business. The calculation of this ratio helps the creditors in evaluating the company. A

higher proprietary ratio indicates that the company has enough funds to pay to its creditors

and whereas a low ratio indicates less funds for repayment to creditors.

Figure 4.2.7

From the above figure 4.2.7 the proprietary ratio for the company in the year 2010 is 0.2 and

2011 is 0.28, which means that the proprietary ratio has marginally increased in 2011 from

2010 so it signifies that the company’s amount of equity has increased for supporting the

functioning of the business. It also indicates that the amount of funds the company has to pay

its creditors has also increased and repayment of these funds can be done faster.

26

1.3

1.4

1.5

1.6

1.7

1.8

20102011

2010

2011

Total Liabilities to Net Worth Ratio

It is calculated to depict the extent to which the net worth of the business can set of the

liabilities. A ratio greater than 1 indicates that the creditors have a greater risk in the business

than the owners as it shows the amount of liabilities in the business is higher.

Figure 4.2.8

From the above figure 4.2.8 the total liabilities to net worth ratio for the company in the year

2010 is 1.71 and 2011 is 1.46, which means that the ratio is a bit higher than 1 which is the

desirable ratio, but in fact in the year 2011 this ratio has been bought down to be more closer

than 1. Ratio being less than 1 is not a good sign for the company.

27

12

12.5

13

13.5

14

14.5

15

20102011

2010

2011

Profitability Ratio

Gross Profit Ratio

This ratio basically shows how efficiently a business is using its materials and labours in the

production process. It is the difference between Sales revenue and cost of making a product

before deducting taxes, interests. Higher the gross profit ratio it is much better.

Figure 4.2.9

From the above figure 4.2.9 the gross profit ratio for the company in the year 2010 is 13.1

and 2011 is 14.75, which means that the Gross Profit ratio has increased in 2011 and is a

good sign for the company as it reflects that efficient utilisation of raw materials and

production process is being taken place in the business and overall productivity of the

company is being enhanced.

28

1.74

1.76

1.78

1.8

1.82

1.84

1.86

20102011

2010

2011

Net Profit Ratio

The net profit percentage is the ratio of after-tax profits to net sales. It reveals the remaining

profit after all costs of production and administrations have been deducted from sales,

and income taxes recognized. Higher the net profit means higher is the earning of the

business.

Figure 4.2.10

From the above figure 4.2.10 the net profit ratio for the company in the year 2010 is 1.78 and

2011 is 1.85, which means that the net profits of the firm has shown an increase in the year

2011 from the preceding year 2010 and is a good sign for the business which is majorly due

to less payment of amount in deferred taxes in the year 2011 in comparison to the year 2010.

The lesser payment has eventually lead to an increase in the net profits of the company.

29

0

1

2

3

4

20102011

2010

2011

Operating Profit Ratio

The operating profit margin ratio indicates how much profit a company makes after paying

for variable costs of production such as wages, raw materials, etc. It is expressed as a

percentage of sales and shows the efficiency of a company controlling the costs and expenses

associated with business operations. Higher the operating profit ratio means the company is

more efficient in controlling the expenses.

Figure 4.2.11

From the above figure 4.2.11 the operating profit ratio for the company in the year 2010 is

3.65 and 2011 is 2.07, which clearly indicates that the ratio has declined in year 2011 from its

preceding year 2010 due to reason being increase in administrative and selling expenses i.e.

Repair and Maintenance, Conveyance and miscellaneous expenses (major amount increased

in these expenses) and cost of goods sold also showed an increase in the year 2011.

30

0

0.01

0.02

0.03

0.04

0.05

0.06

20102011

2010

2011

Return on Assets

It gives an idea about how efficient management is at using its assets to generate earnings.

Higher return on assets basically tells us that the company is earning large amount of money

on less investments. Main objective of Return on assets is to make large profits at lesser

investments.

Figure 4.2.12

From the above figure 4.2.12 the return on assets ratio for the company in the year 2010 is

0.045 and 2011 is 0.058, which means that the return on assets have increased in the year

2011 from the preceding year 2010, which is a good sign for the company as it shows that

assets are being properly managed in the company. With a higher return in the year 2011 it is

clearly indicating that the assets are being well managed by the management and producing

more results than its preceding year.

31

0

0.05

0.1

0.15

0.2

20102011

2010

2011

Return on Capital Employed

Capital employed is basically defined as the difference of total assets – total liabilities. It is

defined as the return which is provided to shareholders on the investment they have done.

Higher return means capital employed is being used more efficiently.

Figure 4.2.13

From the above figure 4.2.13 the return on capital employed ratio for the company in the year

2010 is 0.17 and 2011 is 0.12, which indicates that the return on the capital employed is

constant and is more or less the same for the two years i.e. 2010 and 2011. The return on

capital employed is not that high because not much of capital is employed by the company

from the outside sources.

32

85

85.2

85.4

85.6

85.8

86

86.2

20102011

2010

2011

Expenses Ratios

Direct Expenses Ratio –

Raw Materials Expenses

The calculation of this ratio basically helps us to know the increase/decrease in the

consumption of the raw materials in percentage form in respect to sales which lead to

increase in the expenses in the firm.

Figure 4.2.14

From the above figure 4.2.14 the raw material expenses ratio for the company in the year

2010 is 86.2 and 2011 is 85.4, which indicates that the raw materials expenses of the

company have decreased in the year 2011 in comparison to the year 2010. The raw materials

consumed in year 2011 is more than 2010 but the proportion of sales increase is also more

than 2010, which shows that the raw materials are being used in the company more

efficiently in 2011.

33

0

0.5

1

1.5

2

2.5

3

3.5

20102011

2010

2011

Production Expenses

By calculation of this ratio the analyst gets to know the increase/decrease in the production

expenses of the company in respect to the sales of the company.

Figure 4.2.15

From the above figure 4.2.15 the production expenses ratio for the company in the year 2010

is 2.57 and 2011 is 3.13, which indicates that the production expenses ratio have risen in the

year 2011 from 2010 because of a significant increase in all of the production expenses of the

company in comparison to the increase in the sales of the company, which in turn led has led

to an increase in the ratio of production expenses in respect to the sales of the company.

34

2.1

2.2

2.3

2.4

2.5

2.6

2.7

2.8

20102011

2010

2011

In - Direct Expenses Ratio –

Administrative and Selling Expenses Ratio

These are the expenses incurred by the company which are not related to the production

process of the company and hence are indirect expenses. These expenses incurred indirectly

leads to sales in a company.

Figure 4.2.16

From the above figure 4.2.16 the administrative and selling expenses ratio for the company in

the year 2010 is 2.33 and 2011 is 2.74, which means that expenses have also increased in a

larger proportion to the sales of the company, which has led to an increase in the ratio also.

Major Changes in administrative and sales expenses are seen in Travelling and Conveyance

Expenses, Repair and Maintenance Expenses and Selling and Distribution Expenses.

35

0

0.5

1

1.5

2

2.5

3

3.5

20102011

2010

2011

Turnover Ratios

Assets Turnover Ratio

This ratio basically measures a firm’s efficiency at using its assets in generating sales or

revenue. Higher the ratio is better for the company. Companies with low profit margin have

high assets turnover ratio and whereas companies with high profit margin have low assets

turnover ratio.

Figure 4.2.17

From the above figure 4.2.17 the assets turnover ratio for the company in the year 2010 is

2.55 and 2011 is 3.13, which indicates that the assets turnover ratio has increased from the

previous year because of the increase in the net sales and not much increase/decrease in the

assets side. The increase in the sales of the company has mainly lead to the increase in this

ratio overall.

36

0

2

4

6

8

10

20102011

2010

2011

Fixed Assets Turnover Ratio

It is defined as the company’s ability to generate net sales from the fixed assets investments

specifically property, plant and equipment. A higher fixed assets turnover reflects that the

company is being effective in using the investments in fixed assets to generate revenues.

Figure 4.2.18

From the above figure 4.2.18 the fixed assets turnover ratio for the company in the year 2010

is 6.07 and 2011 is 8.12, which indicates that the ratio has shown an increase in the year 2011

from the preceding year 2010 which is a good sign for the company representing efficiency

and effectiveness in usage of fixed assets investments. The higher ratio means that the

company is using the assets in an efficient manner.

37

0

10

20

30

40

50

60

70

20102011

2010

2011

Working Capital Turnover Ratio

This ratio is calculated to derive the depletion of working capital in order to get sales for the

business. Working capital is Current Assets - Current Liabilities. In general sense higher the

working capital turnover ratio is better because it then reflects that the company is generating

a higher amount of sales as compared to the money used to fund the sales. The working

capital also varies from industries to industries, some have a high working capital

requirement and some have a low requirement.

Figure 4.2.19

From the above figure 4.2.19 the working capital turnover ratio for the company in the year

2010 is 60.54 and 2011 is 29.91, which basically indicates that the working capital was more

efficiently used in 2010 to fund the sales, but in the year 2011 the amount invested in

working capital didn’t yield that much increased sales of the company, so there is a decline in

the ratio.

38

203040

20102011

2010 2011

InventoryTurnover(Finished

Goods)29.26 32.83

2010 2011

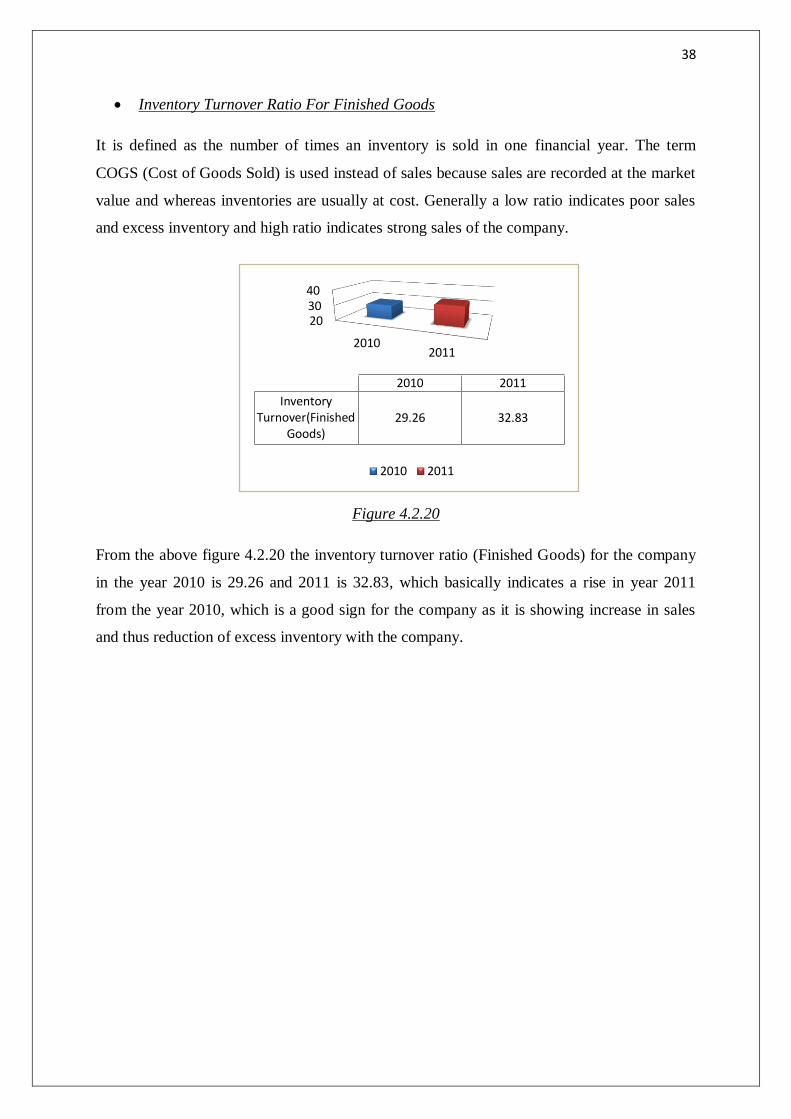

Inventory Turnover Ratio For Finished Goods

It is defined as the number of times an inventory is sold in one financial year. The term

COGS (Cost of Goods Sold) is used instead of sales because sales are recorded at the market

value and whereas inventories are usually at cost. Generally a low ratio indicates poor sales

and excess inventory and high ratio indicates strong sales of the company.

Figure 4.2.20

From the above figure 4.2.20 the inventory turnover ratio (Finished Goods) for the company

in the year 2010 is 29.26 and 2011 is 32.83, which basically indicates a rise in year 2011

from the year 2010, which is a good sign for the company as it is showing increase in sales

and thus reduction of excess inventory with the company.

39

45

50

55

60

65

20102011

2010

2011

Inventory Turnover Ratio For Raw Materials

This ratio is calculated so as to know the rate at which raw materials are being converted into

finished goods in a business. Higher side of this ratio reflects that more goods are being

produced which is leading to more sales and no excess of raw materials stock with the

company, but lower side of this ratio reflects excess stock of raw materials is lying idle with

the business. A company should try to analyse the market trends of demand of the goods and

should produce accordingly so as to minimize wastages of lying of excess stock of raw

materials.

Figure 4.2.21

From the above figure 4.2.21 the inventory turnover ratio (Raw Materials) for the company in

the year 2010 is 54.25 and 2011 is 64.08, which indicates an increase in the ratio from the

preceding year 2010, due to that the raw materials are being utilised more efficiently and

there is lying less of excess inventory of raw materials with the company. It is a good sign for

the company and the company should try and maintain this level.

40

10

10.5

11

11.5

12

12.5

20102011

2010

2011

Inventory Holding Period (Finished Goods)

This term basically means the number of days the finished goods inventory is being in

company’s warehouses. The company incurs various costs on holding of these finished

goods. A higher side of this ratio indicates that the company is holding the finished goods

stocks for a long time and it increases the company’s overall expenditure. A company

generally prefers lower inventory holding periods.

Figure 4.2.22

From the above figure 4.2.22 the inventory holding period (Finished Goods) for the company

in the year 2010 is 12.47 and 2011 is 11.11, which shows that the inventory holding period

for finished goods have decreased for the company, due to the sales of the company which

are increasing and the company is also able to lower its inventory holding costs.

41

5

5.5

6

6.5

7

20102011

2010

2011

Inventory Holding Period (Raw Materials)

It means the time when the raw materials are purchased and the time they are used in

production of the final goods. The time between purchasing of raw materials and using them

in production process is inventory holding period. A company always prefers that its raw

materials don’t remain idle and their purchases don’t go waste due to obsoleteness or by

getting spoiled.

Figure 4.2.23

From above figure 4.2.23 the inventory holding period (Raw Material) for the company in the

year 2010 is 6.72 and 2011 is 5.69, which indicates that the inventory holding period has

decreased in 2011 from 2010, and it’s a good sign for the company indicating lesser raw

materials getting spoiled and more utilization of raw materials in the company.

42

3.8

4

4.2

4.4

4.6

4.8

5

20102011

2010

2011

Some Other Ratios

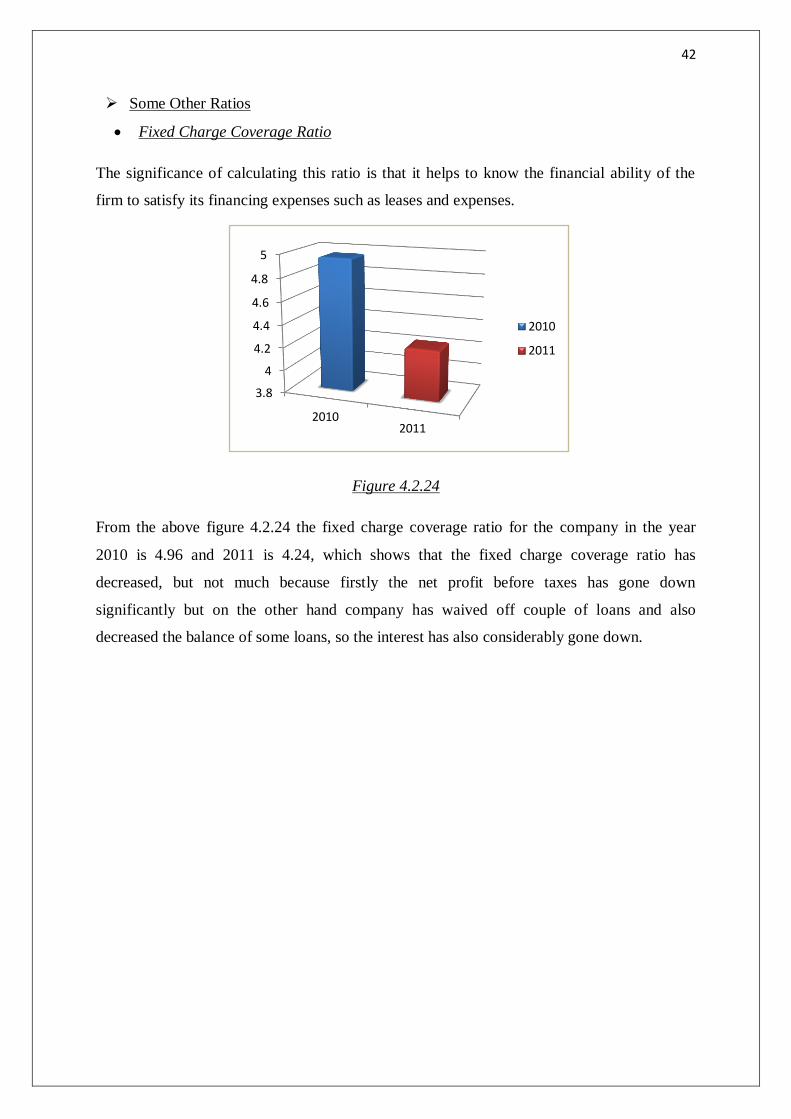

Fixed Charge Coverage Ratio

The significance of calculating this ratio is that it helps to know the financial ability of the

firm to satisfy its financing expenses such as leases and expenses.

Figure 4.2.24

From the above figure 4.2.24 the fixed charge coverage ratio for the company in the year

2010 is 4.96 and 2011 is 4.24, which shows that the fixed charge coverage ratio has

decreased, but not much because firstly the net profit before taxes has gone down

significantly but on the other hand company has waived off couple of loans and also

decreased the balance of some loans, so the interest has also considerably gone down.

43

0

5

10

15

20

20102011

2010

2011

Over All Profitability Ratio

This ratio helps is deriving the overall profit that the business has been able to generate in the

financial year. It helps the comparison of the profit with the previous year or with some other

company.

Figure 4.2.25

From the above figure 4.2.25 the overall profitability ratio for the company in the year 2010

is 17.84 and 2011 is 11.55 and indicates that the ratio has decreased in the year 2011 from the

preceding year 2010, even though the net sales increased in the year 2011 but the amount of

expenditure was greater in 2011 so the operating before decreased and thus the profitability

of the business also went down. There was an increase in material and manufacturing

expenses, salaries and benefits and administrative and selling expenses. Expenditure should

be controlled in order to increase the operating profits.

44

4.3 Analysis of Comparative Balance Sheet of Krishna Maruti ltd.

As at As at Absolute Percentage 31.03.2011 (Rs. 31.03.2010 (Rs. Increase(Decrease) Increase(Decrease)

Particulars In Lacs) In Lacs) 2010-2011 2010-2011

A. Sources of Funds:

Shareholders’ Funds

Share Capital 424.10 424.10 0.00 0.00 Reserves and Surplus 8334.79 6543.15 1791.64 21.50

8758.89 6967.25 1791.64 20.46

Loan Funds

Secured Loans 8583.17 9998.97 -1415.80 -16.50 Unsecured Loans 0.00 300.00 -300.00 0.00

8583.17 10298.97 -1715.80 -19.99 Deferred Tax

Liability 514.47 544.65 -30.18 -5.87

TOTAL 17856.53 17810.87 45.66 0.26

B. Applications of Funds:

Fixed Assets

Gross Block 27031.18 27614.61 -583.43 -2.16 Less: Depreciation 15123.88 13310.44 1813.44 11.99

Net Block 11907.30 14304.17 -2396.87 -20.13 Capital work in

Progress 1858.88 1104.22 754.66 40.60

13766.18 15408.38 -1642.20 -11.93

Investments 341.99 967.32 -625.33 -182.85

Current Assets, Loans and Advances

Inventories 2620.30 2402.33 217.97 8.32 Sundry Debtors 7312.21 6169.52 1142.69 15.63 Cash and Bank

Balances 385.80 349.85 35.95 9.32 Loans and Advances 6440.38 8658.98 -2218.60 -34.45

16758.69 17580.69 -822.00 -4.90

Less: Current Liabilities and

Provisions

Current Liabilities &

Provisions 13010.32 16145.51 -3135.19 -24.10

Net Current Assets 3748.37 1435.18 2313.19 61.71

TOTAL 17856.54 17810.87 45.67 0.26

45

1. Share Capital

As from our Analysis, there has been neither increase nor decrease in the issuance of the

shares, therefore no issuance of shares have taken place.

2. Reserve and Surplus

From our Analysis, the amount of reserve and surplus increased in the year 2011 from the

preceding year 2010 because of the increase in the amount of profit and loss a/c. It is a good

sign for the company as it indicates that firm is making a good profit and has more of its own

funds which are being added to reserve and surplus account.

Absolute Increase/Decrease

(2010 – 2011)

0.00

Percentage Increase/Decrease

(2010 – 2011)

0.00%

Absolute Increase

(2010 – 2011)

1791.64

Percentage Increase

(2010 – 2011)

20.46%

46

3. Shareholder’s Funds

The shareholder’s funds have increased in the year 2011 due to increase in the amount of

reserve and surplus of the company.

4. Secured Loans

As from our analysis, the amount of secured loans has decreased in the year 2011 from the

preceding year 2010 because of repayment of loans done by the company like BCS –

CITIBANK Loan was finished by the company and repayment of term loans.

Absolute Increase

(2010 – 2011)

1791.64

Percentage Increase

(2010 – 2011)

20.46%

Absolute Decrease

(2010 – 2011)

-1415.80

Percentage Decrease

(2010 – 2011)

-16.50%

47

5. Unsecured Loans

From the analysis, the amount of unsecured loans has been finished in the year 2011 from its

preceding year 2010 in which some amount was available. This is a good step by the

company as it leads to lower interest amount payments.

6. Loan Funds

As from our analysis conducted, the loan’s figure of the company has gone down quite

drastically and it’s a good sign for the company. The percentage change in the figure of the

loan’s funds is also significant.

Absolute Decrease

(2010 – 2011)

-300.00

Percentage Decrease

(2010 – 2011)

0.00%

Absolute Decrease

(2010 – 2011)

-1715.80

Percentage Decrease

(2010 – 2011)

-19.99%

48

7. Deferred Tax Liability

As from the analysis done, the amount of Deferred Tax liability has decreased in the year

2011 from the preceding year 2010. It is a good sign for the company as the tax liability has

been decreased in the financial year 2011.

8. Fixed Assets

From the Analysis done, the amount of fixed assets in 2011 is less than preceding year 2010

reason being sale of fixed assets being done. Major Sales that took are of plant and machinery

present in the company. Little additions have been made in the company in terms of fixed

assets.

Absolute Decrease

(2010 – 2011)

-30.18

Percentage Decrease

(2010 – 2011)

-5.87%

Absolute Decrease

(2010 – 2011)

-583.43

Percentage Decrease

(2010 – 2011)

-2.16%

49

9. Depreciation

The amount of depreciation being higher because of rate of depreciation for plant and

machinery is high and it has increased in the financial years.

10. Net Block

The amount of net block would be less in 2011 as compared to 2010 because of the decrease

in the amount of fixed assets and increase in the amount of depreciation for the year ending

2011, the amount of net block is less than from the year 2010.

Absolute Increase

(2010 – 2011)

1813.44

Percentage Decrease

(2010 – 2011)

11.99%

Absolute Decrease

(2010 – 2011)

-2396.87

Percentage Decrease

(2010 – 2011)

-20.13%

50

11. Capital Work in Progress

From the analysis done, the working capital has increased in the business as from the annual

report we could also rectify that the amount has increased in the working capital for the year

2011 from the preceding year 2010.

12. Applications of Funds

The total funds of the company have decreased in the year 2011 from the preceding year

2010, Reason being higher rate of depreciation of the assets.

Absolute Increase

(2010 – 2011)

754.66

Percentage Increase

(2010 – 2011)

40.60%

Absolute Decrease

(2010 – 2011)

-1642.20

Percentage Decrease

(2010 – 2011)

-11.93%

51

13. Investments

The amount of investments for the company has decreased in the year 2011 from the year

2010, reason being sale of many current investments done by the company.

14. Inventories

From the analysis done, the amount of inventories has increased for the company in the year

2011 from the preceding year 2010, reason being increased sales of the company in the year

2011 so it leads to increasing the work in progress and goods in transit inventories.

Absolute Decrease

(2010 – 2011)

-625.33

Percentage Decrease

(2010 – 2011)

-182.25%

Absolute Increase

(2010 – 2011)

217.97

Percentage Increase

(2010 – 2011)

8.32%

52

15. Sundry Debtors

The amount of sundry debtors have risen in 2011 from the preceding year 2010, reason being

amount in debt outstanding for more than 6 months has increased and amount of others debt

has also increased.

16. Cash and Bank Balances

From the analysis conducted, the amount in cash and bank balances have increased in the

year 2011 from the preceding year 2010, reason being increase in the cheques in hand of the

company, increase of balance in current accounts and increase of interest accrued on fixed

deposits.

Absolute Increase

(2010 – 2011)

1142.69

Percentage Increase

(2010 – 2011)

15.63%

Absolute Increase

(2010 – 2011)

35.95

Percentage Increase

(2010 – 2011)

9.32%

53

17. Loans and Advances

The amount of loans and advances that the company has provided has decreased in the year

2011 from the previous year 2010 because of decrease in advance recoverable in cash or

kind, reduction in advance tax amount and reduction of balance in amount with central excise

authorities.

18. Current Assets

The amounts of current assets have decreased in the year 2011 from a marginal amount due

to decrease in amount of loans and advances which the company has provided to the other

parties and other sections of the current assets have increased.

Absolute Decrease

(2010 – 2011)

-2218.60

Percentage Increase

(2010 – 2011)

-34.45%

Absolute Decrease

(2010 – 2011)

-882.80

Percentage Increase

(2010 – 2011)

-4.90%

54

19. Current Liabilities and Provisions

As from the analysis conducted, the amount of current liabilities and provisions because of

amount due from micro and small enterprises, provision for gratuity amount and mark to

market forward contract have decreased.

20. Net Current Assets

As from the analysis conducted, the net current assets of the company have increased for the

year 2011 more in comparison to the year 2010. A good percentage increase can also be seen

which a good sign for the company’s growth.

Absolute Decrease

(2010 – 2011)

-3135.39

Percentage Increase

(2010 – 2011)

-24.10%

Absolute Increase

(2010 – 2011)

2313.19

Percentage Increase

(2010 – 2011)

61.71%

55

Chapter 5 - Conclusion

Summary of Findings

The Research conducted let to a number of findings which are of importance and are

summarised below in the following points:

The company currently has a low balance in readily cash available which means that if

daily expense emerges of a higher amount the company might have problem in

fulfilling it from the current resources available and might have to seek for some

external borrowing.

The debt – equity ratio has also decreased due to repayment of many long term loans

done be the company in the year ending 2010 which reflected less of debt in the year

2011.

The total liabilities of the company are still higher in comparison to the net worth of

the business.

Both the gross profit and net profit ratio of the company has increased which basically

reflects that proper use of production facilities by the company and proper payment of

taxes by the company.

The operating ratio has decreased which means that the expense of the company has

increased mainly administrative and selling expenses.

The expenses incurred in production process have been effectively handled by the

company as the ratio calculated and result derived is remarkable but on the other hand

the indirect expenses of the company has increased

The work capital ratio of the company has shown a much decline in the year 2011

which is not a good sign for the company.

The inventory being produced has increased for the company due to increase in sales

and effective use of raw materials is being taken place also which is seen through the

calculation of the ratios.

An Increase in the reserve and surplus of the company can be seen in the current year

ending 2011.

Company has sold many of its investments in the year ending 2011.

An increase in the debtors of the company can be seen due increased sales which

increase the debtor’s amount also.

56

Discussion of Research Question

1. The overall financial performance of Krishna Maruti ltd. is seen better in the year

ending 2011 due to repayment of loans and increase in the sales of the company in

comparison to the year ending 2010 but the amount of expenses in the year ending

2011 has also increased for Krishna Maruti ltd. which should be controlled by the

company in a proper manner.

2. The liquidity ratio can be seen better in the year 2011 for Krishna Maruti ltd. as due to

reduction in the liabilities of the company and increase in the income from the cash

generated from increased sales both the ratios i.e. current and quick ratio has shown a

rise from their previous year and are closer to the benchmark ratios.

3. The cash position for the company has shown a decline which is not a good sign for

the company because for supporting the cash needed the company has also took a step

and have sold off their investments but instead the company should try and maintain

sufficient cash for supporting their day to day activities.

4. Yes the expenses of the company which are directly related to the production of the

goods are under control and the ones which are not related to the production of goods

and are indirect expenses are not under controlled and have increased in the year

ending 2011.

Recommendations

The recommendations which I would like to provide from my side to the management is

that –

The company should able to maintain adequate amount of cash with them so that

the company can carry out its day to day activities without any hindrances.

The company should also try control its indirect expenses which are on a rise

mainly due to rise in the administrative expenses.

The company should also try and bring out its liabilities so that it is much closer to

the total net worth of the business and not greater than it.

57

Limitations

The limitations which I incurred in the research study are as follows –

The balance sheet audited for the company in the year 2010 was done by some

other firm in comparison to the balance sheet audited for the company in the year

2011, which basically leads to different calculations for amounts like depreciation

calculated and some variation can be seen in the ratios calculated.

58

References

1. Upadhyay, K.P (2001) , Nepalese Business Studies

2. Prather, Carol G (1999), Ratio analysis technique applied to personal Financial

Statements.

3. Martikainen, Teppo (1998), Journal of Business Economics.

4. Fujii, Mariko (2001), Research Centre for Advanced Economic Engineering.

5. Altman, Edward (1998), Journal of Finance.

6. Bravo, M I Gonzalez (2006), Journal of Operational Research Society.

7. Krivonozhko, V.E (2011), Journal of Management Mathematics.

8. Edmister, Robert O.(2009), Journal of Financial and Quantitative Analysis.

9. Singh, A.J (2002), Journal of Retail and leisure Property.

10. Athanassopoulos, Antreas D. (1994), Journal of Operational Research society.

11. Choi, D.S (1983), Journal of International Business Studies.

12. Salo, Ahti (2010), Journal of Management Sciences.

13. Ahrendsen, Bruce L. (2012), Agricultural Financial Review.

14. Royer, Jeffery S. (1991), Journal of Agricultural Cooperation.

15. De, Anupam (2011), Journal of Business Studies Quarterly.

16. Hsieh, Ting Ya (2001), Logistics Information Management.

17. Hsu, H. Christine (2010), Journal of College Teaching and Learning.

18. Irwin, Techniques of Financial Analysis

19. Gosh, T.P, Accounting and Finance for Managers

59

APPENDIX A – RATIO DEFINITIONS

Cash Position Ratios

Absolute Cash Ratio

Cash Reservoir

Current Liabilities

Cash Position to Total Assets Ratio

Cash Reservoir

*100

Total Assets

Interval Measure

Cash Reservoir

Average Daily Cash Expenses

Liquidity Ratios

Current Ratio

Current Assets

Current Liabilities

Quick Ratio

Quick Assets

Current Liabilities

60

Capital Structure Ratios

Debt – Equity Ratio

Debt

Equity

Proprietary ratio

Proprietary Funds

Total Assets

Total Liabilities to Net Worth Ratio

Total Liabilities

Net Worth

Profitability Ratio

Gross Profit Ratio

Gross Profit

*100

Sales

Net Profit Ratio

Net Profit

*100

Sales

61

Operating Profit Ratio

Operating Profit

*100

Sales

Return to Shareholders

Net Profit after Interest and Tax

Shareholder’s Fund

Return on Assets

Net Income

Total Assets

Return on Capital Employed

EBIT

Capital Employed

Expenses Ratios

Direct Expenses Ratio –

Raw Materials Expenses

Raw Materials Consumed

*100

Sales

62

Production Expenses

Production Expenses

*100

Sales

In - Direct Expenses Ratio –

Administrative and Selling Expenses Ratio

Administrative and Selling Expenses

*100

Sales

Turnover Ratios

Assets Turnover Ratio

Sales

Total Assets

Fixed Assets Turnover Ratio

Sales

Fixed Assets

Working Capital Turnover Ratio

Sales

Working Capital

63

Inventory Turnover Ratio For Finished Goods

Cost of Goods Sold

Average Inventory

Inventory Turnover Ratio For Raw Materials

Raw Materials Consumed

Average Inventory

Inventory Holding Period (Finished Goods)

365

Inventory Turnover Ratio

Inventory Holding Period (Raw Materials)

365

Inventory Turnover Ratio

Some Other Ratios

Fixed Charge Coverage Ratio

Net Profit before Interest and Tax

Interest Charges

64

Over All Profitability Ratio

Operating Profit

*100

Capital Employed

65

APPENDIX B – Excel Calculations

DATA 2010 (Rs. In Lacs) 2011 (Rs. In Lacs)

CASH RESERVOIR 1,317.17 727.79

CURRENT LIABILTIES 16145.51281 13,010.32

TOTAL ASSETS (CP RATIO) 34195.18605 31,033.23

AVERAGE DAILY CASH EXPENSES 255.641687 255.18

CURRENT ASSETS 17580.68846 16,758.69

QUICK ASSETS 7453.02212 7706.83

TOTAL DEBT 10298.97279 8,583.17

TOTAL EQUITY 6967.24825 8,758.89

TOTAL ASSETS 33956.38685 30,866.85

TOTAL LIABILITES 26989.1386 22,107.96

NET SALES 86,926.36 96,736.88

COST OF GOODS SOLD 75471.59592 82,460.06

GROSS PROFIT 11454.76408 14,276.82

NET PROFIT AFTER TAX 1547.52091 1,791.64

OPERATING PROFIT 3179.17119 2,003.46

EBIT 3179.17119 2,003.46

CAPITAL EMPLOYED 17810.87404 17,856.53

RAW MATERIALS CONSUMED 74995.34814 82,614.01

PRODUCTION EXPENSES 2237.03024 3,032.54

ADMINISTRATIVE & SELLING

EXPENSES

2033.88388 2,655.90

FIXED ASSETS 14304.16516 11,907.29

WORKING CAPITAL 1435.17565 3,748.37

AVERAGE INVENTORY 2579.32636 2511.315

AVERAGE INVENTORY(RAW

MATERIALS)

1382.31148 1289.17

INTEREST ON TERM LOAN 640.89055 472.32

TANGIBLE ASSETS 16706.49894 14527.59

66

TYPES OF RATIOS 2010 2011

CASH POSITION RATIOS

Absolute Cash Ratio = Cash Reservoir/Current Liabilities 0.081581181 0.06

Cash Position to Total Assets Ratio = Cash Reservoir/Total

Assets * 100

3.85191646 2.35

Interval Measure(Ability of Cash reservoir to meet Cash

Expenses) = Cash Reservoir/Average Daily Cash Expenses

5.152406932 2.85

LIQUIDITY RATIOS

Current Ratio = Current Assets/Current Liabilities 1.088890063 1.29

Quick Ratio = Quick Assets/Current Liabilities 0.461615695 0.59236283

2

CAPITAL STRUCTURE RATIOS

Debt - Equity Ratio = Debt/Equity 1.478198052 0.98

Proprietary Ratio = Proprietary Funds/Total Assets 0.205182262 0.28376364

9

Total Liabilities to Net Worth Ratio = Total Liabilities/Net

Worth

1.714756604 1.41

PROFITABILTY RATIOS

SHAREHOLDER'S EQUITY 6967.24825 8,758.89

INVESTMENTS 967.31648 341.99

NET WORTH 15739.34081 15,655.66

67

Gross Profit Ratio = Gross Profit/Sales * 100 13.17754946 14.7584044

5

Net Profit Ratio = Net Profit/Sales * 100 1.78026655 1.85207544

4

Operating Profit Ratio = Operating Profit/Sales * 100 3.657315445 2.07104053

8

Return to Shareholders = Net Profit After Interest and

Tax/Shareholder's Fund

0.222113646 0.20455103

3

Return on Assets = Net Income/Total Assets 0.04557378 0.05804414

8

Return on Capital Employed = EBIT/Capital Employed 0.17849608 0.11

EXPENSES RATIOS

Direct Expenses Ratio -

Raw Materials Consumed/Sales*100 86.27457556 85.40

Production Expenses/Sales*100 2.573477412 3.13483337

5

Indirect Expenses Ratio -

Administrative & Selling Expenses/Sales*100 2.339778037 2.74548858

7

TURNOVER RATIOS

Assets Turnover = Sales/Total Assets 2.559941386 3.13400557

6

Fixed Assets Turnover = Sales/Fixed Assets 6.076996387 8.12

68

Working Capital Turnover = Sales/Working Capital 60.5684468 25.8077190

9

Inventory Turnover(For Finished Goods) = Cost of Goods

Sold/Average Inventory

29.26019642 32.8354109

3

Inventory Turnover(For Raw Materials) = Raw Materials

Consumed/Average Inventory(For Raw Materials)

54.25358121 64.0830999

8

Inventory Holding Period(For Finished Goods) =

365/Inventory Turnover Ratio

12.474284 11.1160478

8

Inventory Holding Period(For Raw Materials) =

365/Inventory Turnover Ratio

6.727666485 5.69572945

3

Some Other Ratios

Fixed Charge Coverage Ratios = Net Profit Before Interest

and tax/Interest Charges

4.960552453 4.24174288

6

Over All Profitability Ratio = Operating Profit/Capital

Employed*100

17.84960796 11.2197610

6

69

COMPARATIVE BALANCE SHEET

Particulars As at

31.03.2011

(Rs. In Lacs)

As at

31.03.2010

(Rs. In Lacs)

Absolute

Increase(Decrease

) 2010-2011

Percentage

Increase(Decrease)

2010-2011

A. Sources of

Funds:

Shareholders’

Funds

Share Capital 424.10 424.10 0.00 0.00

Reserves and

Surplus

8334.79 6543.15 1791.64 21.50

8758.89 6967.25 1791.64 20.46

Loan Funds

Secured Loans 8583.17 9998.97 -1415.80 -16.50

Unsecured Loans 0.00 300.00 -300.00 0.00

8583.17 10298.97 -1715.80 -19.99

Deferred Tax

Liability

514.47 544.65 -30.18 -5.87

TOTAL 17856.53 17810.87 45.66 0.26

B. Applications

of Funds:

Fixed Assets

Gross Block 27031.18 27614.61 -583.43 -2.16

Less:

Depreciation

15123.88 13310.44 1813.44 11.99

Net Block 11907.30 14304.17 -2396.87 -20.13

Capital work in

Progress

1858.88 1104.22 754.66 40.60

13766.18 15408.38 -1642.20 -11.93

70

Investments 341.99 967.32 -625.33 -182.85

Current Assets,

Loans and

Advances

Inventories 2620.30 2402.33 217.97 8.32

Sundry Debtors 7312.21 6169.52 1142.69 15.63

Cash and Bank

Balances

385.80 349.85 35.95 9.32

Loans and

Advances

6440.38 8658.98 -2218.60 -34.45

16758.69 17580.69 -822.00 -4.90

Less: Current

Liabilities and

Provisions

Current

Liabilities &

Provisions

13010.32 16145.51 -3135.19 -24.10

Net Current

Assets

3748.37 1435.18 2313.19 61.71

TOTAL 17856.54 17810.87 45.67 0.26