study perfect your score score guide - s3. · pdf filethe amount added to the cost of...

TRANSCRIPT

Name Perfect YourScore Score

Identifying Accounting Terms 19 Pts.Analyzing Accounting Concepts and Practices 27 Pts.

Analyzing Transactions Recorded in Special Journals 24 Pts.Total 70 Pts.

StudyGuide

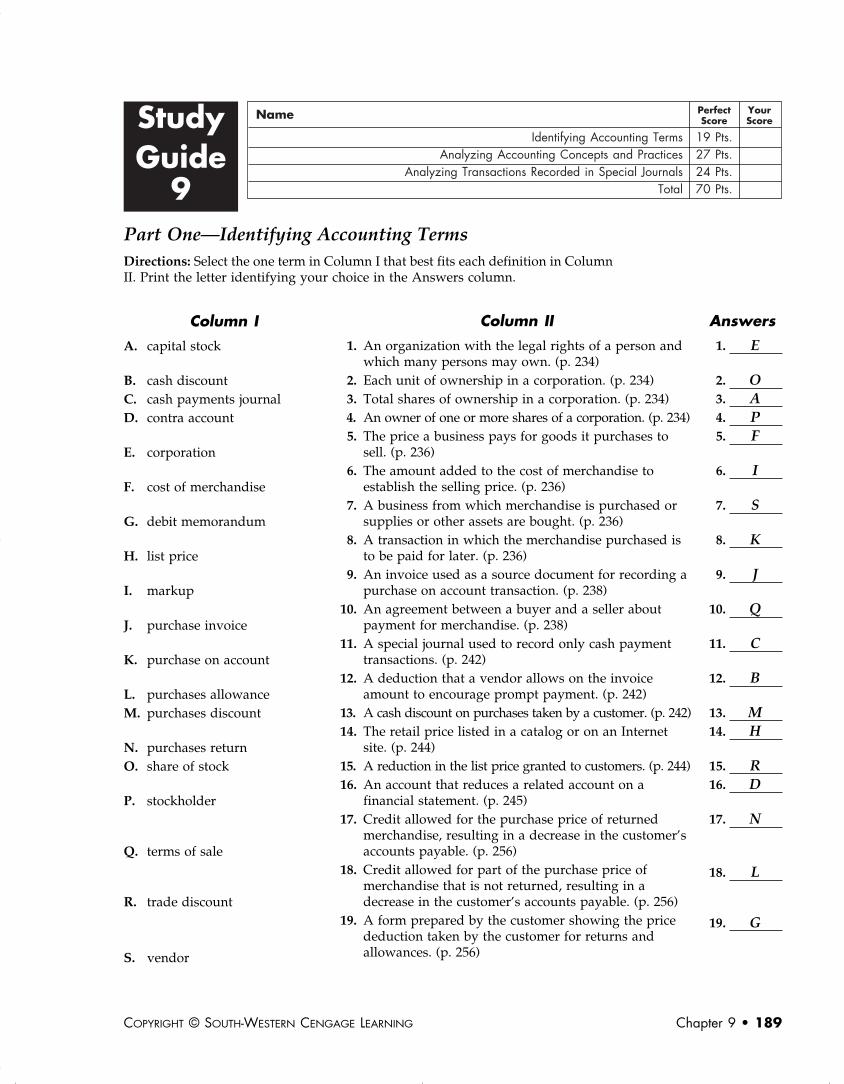

9Part One—Identifying Accounting TermsDirections: Select the one term in Column I that best fits each definition in ColumnII. Print the letter identifying your choice in the Answers column.

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING Chapter 9 • 189

Answers

1. E

2. O3. A4. P5. F

6. I

7. S

8. K

9. J

10. Q

11. C

12. B

13. M14. H

15. R16. D

17. N

18. L

19. G

Column I

A. capital stock

B. cash discountC. cash payments journalD. contra account

E. corporation

F. cost of merchandise

G. debit memorandum

H. list price

I. markup

J. purchase invoice

K. purchase on account

L. purchases allowanceM. purchases discount

N. purchases returnO. share of stock

P. stockholder

Q. terms of sale

R. trade discount

S. vendor

Column II

1. An organization with the legal rights of a person andwhich many persons may own. (p. 234)

2. Each unit of ownership in a corporation. (p. 234)3. Total shares of ownership in a corporation. (p. 234)4. An owner of one or more shares of a corporation. (p. 234)5. The price a business pays for goods it purchases to

sell. (p. 236)6. The amount added to the cost of merchandise to

establish the selling price. (p. 236)7. A business from which merchandise is purchased or

supplies or other assets are bought. (p. 236)8. A transaction in which the merchandise purchased is

to be paid for later. (p. 236)9. An invoice used as a source document for recording a

purchase on account transaction. (p. 238)10. An agreement between a buyer and a seller about

payment for merchandise. (p. 238)11. A special journal used to record only cash payment

transactions. (p. 242)12. A deduction that a vendor allows on the invoice

amount to encourage prompt payment. (p. 242)13. A cash discount on purchases taken by a customer. (p. 242)14. The retail price listed in a catalog or on an Internet

site. (p. 244)15. A reduction in the list price granted to customers. (p. 244)16. An account that reduces a related account on a

financial statement. (p. 245)17. Credit allowed for the purchase price of returned

merchandise, resulting in a decrease in the customer’saccounts payable. (p. 256)

18. Credit allowed for part of the purchase price ofmerchandise that is not returned, resulting in adecrease in the customer’s accounts payable. (p. 256)

19. A form prepared by the customer showing the pricededuction taken by the customer for returns andallowances. (p. 256)

b-te_09-study-189-192.qxd 10/29/07 5:27 PM Page 189 SECOND REVISED

190 • Working Papers TE CENTURY 21 ACCOUNTING, 9TH EDITION

Part Two—Analyzing Accounting Concepts and PracticesDirections: Place a T for True or an F for False in the Answers column to show whether each of thefollowing statements is true or false.

Answers

1. T2. F3. T

4. T

5. T6. T

7. T8. F

9. F

10. T

11. F12. T13. T

14. T15. F

16. F17. T

18. F19. T20. T

21. F22. F23. T

24. T25. T

26. F27. T

1. Unlike a proprietorship, a corporation exists independent of its owners. (p. 234)2. A corporation can incur liabilities but cannot own property. (p. 234)3. As in proprietorships, information in a corporation's accounting system is kept separate

from the personal records of the owners, and this accounting concept application is called aBusiness Entity. (p. 234)

4. The selling price of merchandise must be greater than the cost of merchandise for abusiness to make a profit. (p. 236)

5. The cost account Purchases is used only to record the value of merchandise purchased. (p. 236)6. When purchases are recorded at their cost, including any related shipping costs and taxes,

the Historical Cost accounting concept is being applied. (p. 236)7. Recording entries in a journal with special amount columns saves time. (p. 237)8. All purchase transactions, including purchases made on account and purchases made for

cash, are recorded in the purchases journal. (p. 237)9. The source document for recording a purchase on account transaction is a memorandum

describing the merchandise purchased. (p. 238)10. By listing the quantity, the description, the price of each item, and the total amount

purchased, the Objective Evidence concept is applied. (p. 238)11. A purchase invoice usually lists only the total cost of the merchandise. (p. 238)12. A purchase on account transaction increases the amount owed to a vendor. (p. 239)13. A cash payments journal includes a special amount column for the cash account and the

accounts payable account. (p. 242)14. The source document for most cash payments is the check issued. (p. 242)15. When supplies are purchased for use in the business, the amount is recorded in the

purchases account. (p. 243)16. A special journal entry is made to show the amount of a trade discount. (p. 244)17. The terms of sale 2/15, n/30 mean that 2% of the invoice amount may be deducted if paid

within 15 days of the invoice date or the total invoice amount must be paid within 30 days.(p. 245)

18. Purchase discounts are recorded in the general journal. (p. 245)19. The contra account Purchases Discount has a normal credit balance. (p. 245)20. The custodian prepares a petty cash report when the petty cash fund is to be replenished.

(p. 248)21. The petty cash account Cash Short and Over is a permanent account. (p. 249)22. A journal is proved and ruled only at the end of a fiscal period. (p. 250)23. To begin a new journal page, the totals from the previous journal page are carried forward

to the next journal page. (p. 251)24. Buying supplies on account is recorded in the general journal. (p. 254)25. When supplies are purchased on account, the Store Supplies account balance increases and

the Accounts Payable account balance increases. (p. 255)26. The source document for a purchases return is a check. (p. 256)27. The normal account balance of Purchases Returns and Allowances is a credit. (p. 257)

b-te_09-study-189-192.qxd 10/29/07 5:27 PM Page 190 SECOND REVISED

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING Chapter 9 • 191

Name Date Class

Part Three—Analyzing Transactions Recorded inSpecial JournalsDirections: In Answers Column l, print the abbreviation for the journal inwhich each transaction is to be recorded. In Answers Columns 2 and 3, printthe letters identifying the accounts to be debited and credited for eachtransaction.

PJ—Purchases journal; GJ—General journal; CPJ—Cash payments journal

Account Titles

A. AccountsPayable

B. Cash

C. Cash Short andOver

D. MiscellaneousExpense

E. Petty Cash

F. Purchases

G. PurchasesDiscount

H. PurchasesReturns andAllowances

I. Rent Expense

J. Supplies

K. Tri-CountySuppliers

L. Wixom Sports

M. YukonOutfitters

Transactions

1–2–3. Purchased merchandise on account from WixomSports. (p. 239)

4–5–6. Paid cash for rent. (p. 243)

7–8–9. Purchased merchandise for cash. (p. 244)

10–11–12. Paid cash on account to Wixom Sports, lesspurchases discount. (p. 245)

13–14–15. Paid cash on account to Tri-County Suppliers. (p. 246)

16–17–18. Paid cash to replenish the petty cash fund:supplies, miscellaneous, cash over. (p. 249)

19–20–21. Bought supplies on account from Yukon Outfitters.(p. 255)

22–23–24. Returned merchandise to Tri-County Suppliers. (p. 257)

Answers

Journal Debit Credit

1. PJ 2. F 3. A, L

4. CPJ 5. I 6. B

7. CPJ 8. F 9. B

10. CPJ 11. A, L 12. B, G

13. CPJ 14. A, K 15. B

16. CPJ 17. D, J 18. B, C

19. GJ 20. J 21. A, M

22. GJ 23. A, K 24. H

b-te_09-study-189-192.qxd 10/29/07 5:27 PM Page 191 SECOND REVISED

192 • Working Papers TE CENTURY 21 ACCOUNTING, 9TH EDITION

Skimming and Careful ReadingWe must learn to use different techniques as we read. Sometimes we need to skim material very quickly,touching only the high points. At other times we need to read slowly and carefully, concentrating on everyword.

SkimmingSkimming helps you gain a general understanding of what is contained in material without slow and carefulreading. You may wish to skim a magazine article to determine if it contains information you want to readcarefully later.

You can use skimming to preview an assignment before you read for details. You should first read the ti-tle and the introduction quickly. You should then read the main headings and glance through the para-graphs. By skimming first, you will know what is included before you become involved in the details.

If you own the book, you may wish to use a highlighter sparingly as you skim. This will help call your attention to certain parts of a selection later. If you highlight too much, it will be of little help to you.

You can also use skimming to review material that you have studied previously. Before an exam, forexample, you may want to read quickly through the material to be sure that you have not forgotten anyimportant points.

Careful ReadingMany times you will be responsible for every detail in a reading assignment. You may have to remembernames, dates, and facts that are of great importance. Before you read for details, you should skim thematerial first to gain an overview. Then you should read it slowly and carefully.

As you read carefully, you should ask yourself what is included in each paragraph. If you can summarizeeach paragraph as you read, you will have a good understanding. Then you should determine if you can remember names, dates, and other details. If you cannot, you should read the material again, concentratingon the details while keeping the overall picture in mind.

ConclusionSkimming and careful reading are techniques that will be extremely useful to you in the future. You shouldknow which technique to use and be sure to use it properly. Skimming will give you an overall view of thematerial. Careful reading will ensure that you know the details.

StudySkills

b-te_09-study-189-192.qxd 10/29/07 5:27 PM Page 192 SECOND REVISED

Name Date Class

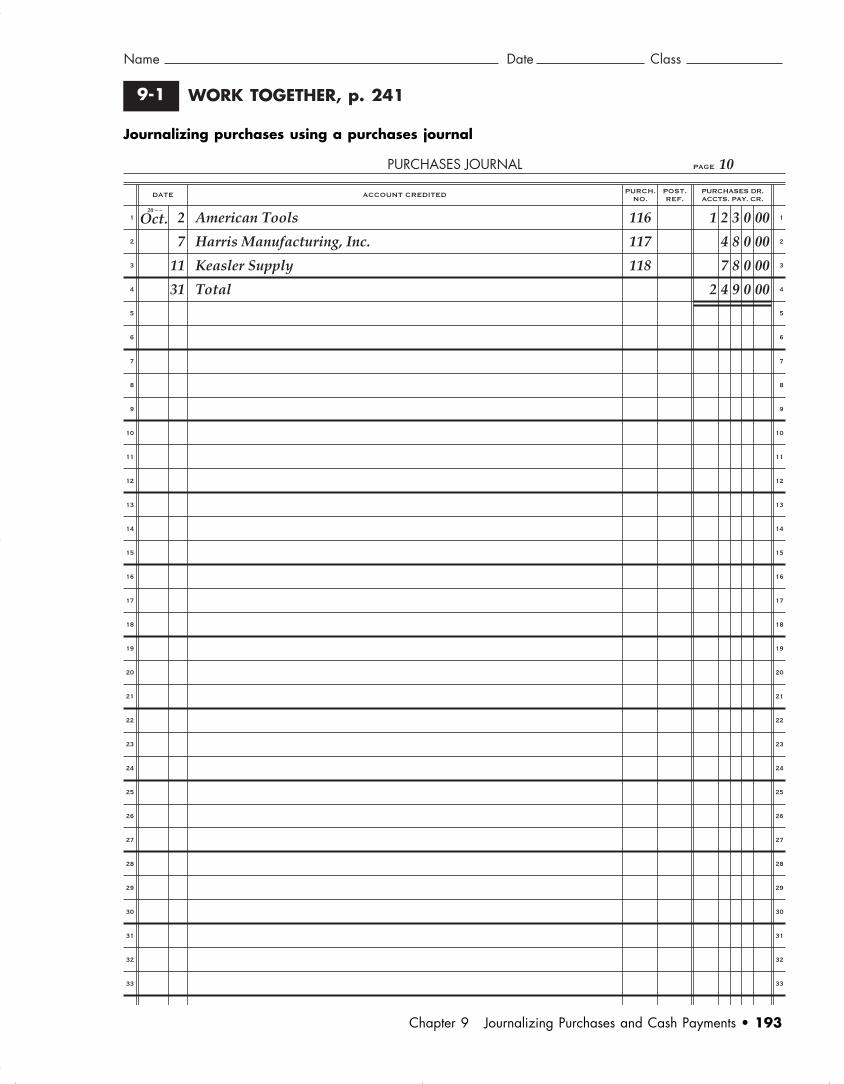

WORK TOGETHER, p. 2419-1

Journalizing purchases using a purchases journal

Chapter 9 Journalizing Purchases and Cash Payments • 193

PURCHASES JOURNAL PAGE 10

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

DATE ACCOUNT CREDITED PURCHASES DR.ACCTS. PAY. CR.

Oct.20 – –

2

7

11

31

American Tools

Harris Manufacturing, Inc.

Keasler Supply

Total

PURCH.NO.

POST.REF.

1 2 3 0 00

4 8 0 00

7 8 0 00

2 4 9 0 00

116

117

118

BTE_Ch09-193-220.qxd 10/29/07 7:02 PM Page 193 SECOND REVISED

ON YOUR OWN, p. 2419-1

Journalizing purchases using a purchases journal

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING194 • Working Papers TE

PURCHASES JOURNAL PAGE 11

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

DATE ACCOUNT CREDITED PURCHASES DR.ACCTS. PAY. CR.

Nov.20 – –

4

9

18

30

Ulman Supply, Inc.

Else Silver Co.

Pratt Paints

Total

PURCH.NO.

POST.REF.

6 7 0 00

2 3 4 5 00

1 1 5 0 00

4 1 6 5 00

149

150

151

BTE_Ch09-193-220.qxd 10/29/07 7:02 PM Page 194 SECOND REVISED

Name Date Class

WORK TOGETHER, p. 2479-2

Chapter 9 Journalizing Purchases and Cash Payments • 195

Journ

aliz

ing c

ash

paym

ents

usi

ng a

cash

paym

ents

journ

al

CA

SH P

AYM

ENTS

JOU

RNA

LP

AG

E10

12

34

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

DA

TE

AC

CO

UN

T T

ITL

E

PU

RC

HA

SE

SD

ISC

OU

NT

CR

ED

IT

CA

SH

CR

ED

IT

Oct

.20

– –

1 7 11 17 19

Uti

liti

es E

xpen

se

Supp

lies

—O

ffic

e

Pur

chas

es

Wes

t Su

pply

Qui

ll F

ores

t P

rodu

cts

CK

.N

O.

PO

ST

.R

EF

.

GE

NE

RA

L

DE

BIT

CR

ED

IT

85

00

52

00

32

000

68

40

85

00

52

00

32

000

33

51

60

43

80

00

5

AC

CO

UN

TS

PA

YA

BL

ED

EB

IT

34

20

00

43

80

00

321

322

323

324

325

BTE_Ch09-193-220.qxd 10/29/07 7:02 PM Page 195 SECOND REVISED

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING196 • Working Papers TE

ON YOUR OWN, p. 2479-2

Journ

aliz

ing c

ash

paym

ents

usi

ng a

cash

paym

ents

journ

al

CA

SH P

AYM

ENTS

JOU

RNA

LP

AG

E11

12

34

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

DA

TE

AC

CO

UN

T T

ITL

E

PU

RC

HA

SE

SD

ISC

OU

NT

CR

ED

IT

CA

SH

CR

ED

IT

Nov

.20

– –

2 6 9 12 14

Uti

liti

es E

xpen

se

Supp

lies

—O

ffic

e

Pur

chas

es

Rac

ing

Imag

es

SPL

Ren

ovat

ions

CK

.N

O.

PO

ST

.R

EF

.

GE

NE

RA

L

DE

BIT

CR

ED

IT

24

800

14

200

20

40

00

84

60

24

800

14

200

20

40

00

41

45

40

25

73

00

5

AC

CO

UN

TS

PA

YA

BL

ED

EB

IT

42

30

00

25

73

00

432

433

434

435

436

BTE_Ch09-193-220.qxd 10/29/07 7:02 PM Page 196 SECOND REVISED

WORK TOGETHER, p. 253

Name Date Class

9-3

Performing other cash payments journal operations

Chapter 9 Journalizing Purchases and Cash Payments • 197

CASH PAYMENTS JOURNAL PAGE

1 2 3 4

DATE ACCOUNT TITLE PURCHASESDISCOUNT

CREDIT

CASHCREDIT

CK.NO.

POST.REF.

GENERAL

DEBIT CREDIT

5

ACCOUNTSPAYABLE

DEBIT

5

23

24

25

23

24

25

27

27

27

Supplies

Ace Manufacturing

Carried Forward

2 3 4 30

18 4 8 6 85 4 5 8 56

3 79

2 5 1 34

2 3 4 30

1 8 5 81

34 2 6 0 45

1 8 9 60

16 4 8 3 50

534

535

✔

CASH PAYMENTS JOURNAL PAGE 61 2 3 4

1

2

3

4

5

6

1

2

3

4

5

6

DATE ACCOUNT TITLE PURCHASESDISCOUNT

CREDIT

CASHCREDIT

Mar.20 – –

27

31

31

Brought Forward

Supplies—Office

Supplies—Store

Miscellaneous Expense

Cash Short and Over

Totals

CK.NO.

POST.REF.

GENERAL

DEBIT CREDIT

18 4 8 6 85

4 5 23

6 6 18

4 9 25

18 6 4 7 51

4 5 8 56

1 25

4 5 9 81

2 5 1 34

2 5 1 34

34 2 6 0 45

1 5 9 41

34 4 1 9 86

5

ACCOUNTSPAYABLE

DEBIT

16 4 8 3 50

16 4 8 3 50

536✔

PETTY CASH REPORT

Fund TotalPayments:

Less: Total paymentsEquals: Recorded amount on handLess: Actual amount on handEquals: Cash short (over)

Explanation ReconciliationReplenishAmount

Amount to Replenish

Date: Custodian:

Supplies—OfficeSupplies—StoreMiscellaneous

March 31,20-- Kevin Tomlinson

45.2366.1849.25

160.66 39.34 40.59 (1.25)

160.66

(1.25) 159.41

200.00

Debit CreditColumn Title Column Totals Column Totals

General Debit . . . . . . . . . . . . . . . . . . . . $18,647.51General Credit . . . . . . . . . . . . . . . . . . . $ 459.81Accounts Payable Debit . . . . . . . . . . . . 16,483.50Purchases Discount Credit . . . . . . . . . . 251.34Cash Credit . . . . . . . . . . . . . . . . . . . . . 34,419.86Totals . . . . . . . . . . . . . . . . . . . . . . . . . . $35,131.01 $35,131.01

BTE_Ch09-193-220.qxd 10/29/07 7:02 PM Page 197 SECOND REVISED

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING198 • Working Papers TE

ON YOUR OWN, p. 2539-3

Performing other cash payments journal operations

CASH PAYMENTS JOURNAL PAGE

1 2 3 4

DATE ACCOUNT TITLE PURCHASESDISCOUNT

CREDIT

CASHCREDIT

CK.NO.

POST.REF.

GENERAL

DEBIT CREDIT

5

ACCOUNTSPAYABLE

DEBIT

11

23

24

25

23

24

25

28

28

28

Advertising Expense

GRF Manufacturing, Inc.

Carried Forward

1 5 0 0 00

25 6 2 4 85 9 5 8 48

5 0 36

4 9 2 15

1 5 0 0 00

2 4 6 7 64

59 3 1 6 72

2 5 1 8 00

35 1 4 2 50

625

626

✔

CASH PAYMENTS JOURNAL PAGE 121 2 3 4

1

2

3

4

5

6

7

1

2

3

4

5

6

7

DATE ACCOUNT TITLE PURCHASESDISCOUNT

CREDIT

CASHCREDIT

June20 – –

28

30

30

Brought Forward

Supplies—Office

Supplies—Store

Miscellaneous Expense

Repair Expense

Cash Short and Over

Totals

CK.NO.

POST.REF.

GENERAL

DEBIT CREDIT

25 6 2 4 85

5 6 21

4 8 27

3 6 17

8 2 25

0 62

25 8 4 8 37

9 5 8 48

9 5 8 48

4 9 2 15

4 9 2 15

59 3 1 6 72

2 2 3 52

59 5 4 0 24

5

ACCOUNTSPAYABLE

DEBIT

35 1 4 2 50

35 1 4 2 50

627✔

PETTY CASH REPORT

Fund TotalPayments:

Less: Total paymentsEquals: Recorded amount on handLess: Actual amount on handEquals: Cash short (over)

Explanation ReconciliationReplenishAmount

Amount to Replenish

Date: Custodian:

Supplies—OfficeSupplies—StoreMiscellaneousRepairs

June 30,20-- Jerri Harris

56.2148.2736.1782.25

222.90 27.10 26.48 0.62

222.90

0.62 223.52

250.00

Debit CreditColumn Title Column Totals Column Totals

General Debit . . . . . . . . . . . . . . . . . . . . $25,848.37General Credit . . . . . . . . . . . . . . . . . . . $ 958.48Accounts Payable Debit . . . . . . . . . . . . 35,142.50Purchases Discount Credit . . . . . . . . . . 492.15Cash Credit . . . . . . . . . . . . . . . . . . . . . 59,540.24Totals . . . . . . . . . . . . . . . . . . . . . . . . . . $60,990.87 $60,990.87

BTE_Ch09-193-220.qxd 10/29/07 7:02 PM Page 198 SECOND REVISED

Name Date Class

Chapter 9 Journalizing Purchases and Cash Payments • 199

WORK TOGETHER andON YOUR OWN, p. 258

9-4

Journ

aliz

ing o

ther

tra

nsa

ctio

ns

usi

ng a

gen

eral

journ

al

GEN

ERA

L JO

URN

AL

PA

GE

8

DA

TE

AC

CO

UN

T T

ITL

E

DE

BIT

CR

ED

ITD

OC

.N

O.

PO

ST

.R

EF

.

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

Oct

.20

– –

5 7 11

14

Supp

lies

—St

ore

Acc

ount

s P

ayab

le/D

esig

ner

Supp

lies

Acc

ount

s P

ayab

le/H

endr

ix P

rodu

cts

Pur

chas

es R

etur

ns a

nd A

llow

.

Supp

lies

—O

ffic

e

Acc

ount

s P

ayab

le/O

ffic

e E

xpre

ss

Acc

ount

s P

ayab

le/F

retz

Ind

ustr

ies

Pur

chas

es R

etur

ns a

nd A

llow

.

18

000

54

000

24

000

12

39

00

18

000

54

000

24

000

12

39

00

M35

DM

65

M36

DM

66

Wor

k T

oget

her

9-4

On

You

rO

wn

9-4

BTE_Ch09-193-220.qxd 10/29/07 7:02 PM Page 199 SECOND REVISED

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING200 • Working Papers TE

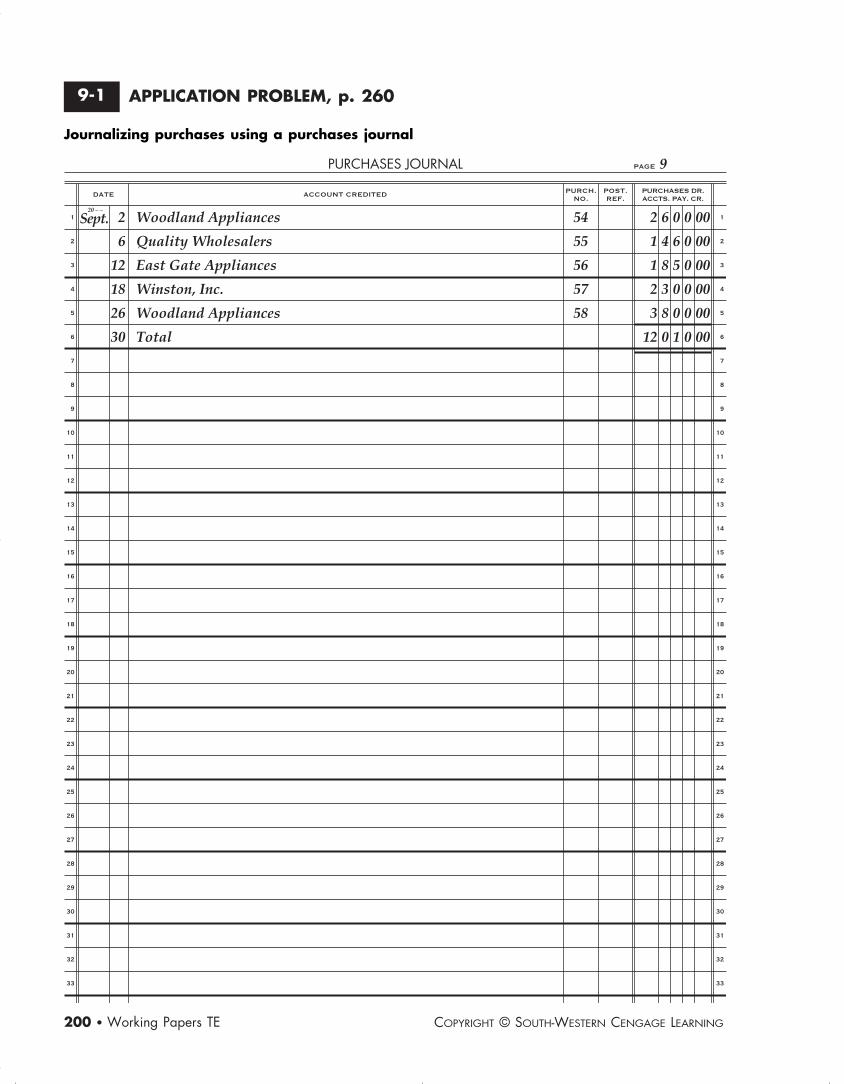

APPLICATION PROBLEM, p. 2609-1

Journalizing purchases using a purchases journal

PURCHASES JOURNAL PAGE 9

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

DATE ACCOUNT CREDITED PURCHASES DR.ACCTS. PAY. CR.

Sept.20 – –

2

6

12

18

26

30

Woodland Appliances

Quality Wholesalers

East Gate Appliances

Winston, Inc.

Woodland Appliances

Total

PURCH.NO.

POST.REF.

2 6 0 0 00

1 4 6 0 00

1 8 5 0 00

2 3 0 0 00

3 8 0 0 00

12 0 1 0 00

54

55

56

57

58

BTE_Ch09-193-220.qxd 10/29/07 7:02 PM Page 200 SECOND REVISED

Name Date Class

Chapter 9 Journalizing Purchases and Cash Payments • 201

Journ

aliz

ing c

ash

paym

ents

usi

ng a

cash

paym

ents

journ

al

CA

SH P

AYM

ENTS

JOU

RNA

LP

AG

E22

12

34

1 2 3 4 5 6 7 8 9 10 11 12 13 14

1 2 3 4 5 6 7 8 9 10 11 12 13 14

DA

TE

AC

CO

UN

T T

ITL

E

PU

RC

HA

SE

SD

ISC

OU

NT

CR

ED

IT

CA

SH

CR

ED

IT

Nov

.20

– –

1 4 6 9 11 13 18 21 23 25 27 30

Uti

liti

es E

xpen

se

The

Pro

Sho

p

Adv

erti

sing

Exp

ense

Ath

leti

c C

ente

r

Supp

lies

—O

ffic

e

Pur

chas

es

Supp

lies

—St

ore

Pur

chas

es

Pur

chas

es

Bes

t C

loth

ing

Tro

phy

Spor

ts

Car

ried

For

war

d

CK

.N

O.

PO

ST

.R

EF

.

GE

NE

RA

L

DE

BIT

CR

ED

IT

96

00

75

00

50

00

92

500

12

500

25

000

30

000

18

21

00

25

00

42

00

67

00

96

00

12

25

00

75

00

92

500

50

00

92

500

12

500

25

000

30

000

92

500

20

58

00

69

54

00

5

AC

CO

UN

TS

PA

YA

BL

ED

EB

IT

12

50

00

92

500

92

500

21

00

00

52

00

00

241

242

243

244

245

246

247

248

249

250

251

✔

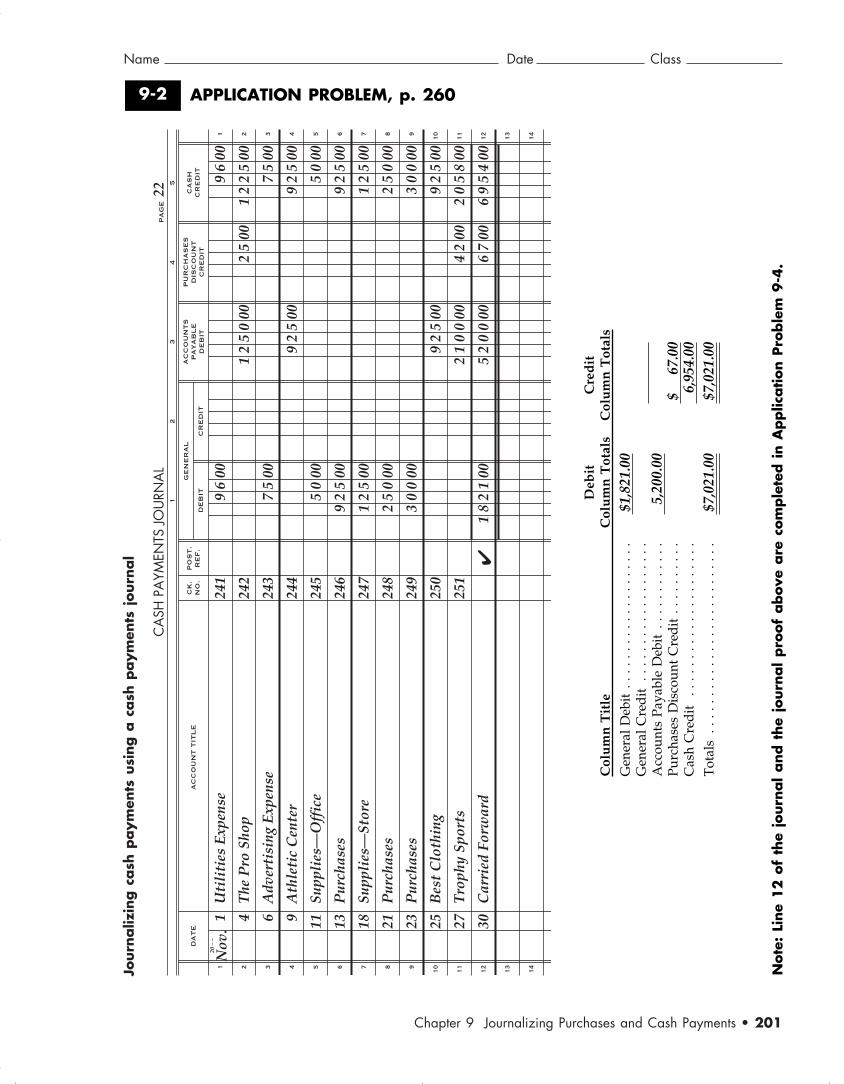

APPLICATION PROBLEM, p. 2609-2

Note

: Li

ne

12 o

f th

e jo

urn

al

and t

he

journ

al

pro

of

above

are

com

ple

ted i

n A

pplic

ation P

roble

m 9

-4.

Deb

itC

red

itC

olu

mn

Tit

leC

olu

mn

Tot

als

Col

um

n T

otal

s

Gen

eral

Deb

it .

. . .

. . .

. . .

. . .

. . .

. . .

.$1

,821

.00

Gen

eral

Cre

dit

. . .

. . .

. . .

. . .

. . .

. . .

.A

ccou

nts

Paya

ble

Deb

it .

. . .

. . .

. . .

. .5,

200.

00Pu

rcha

ses

Dis

coun

t C

red

it .

. . .

. . .

. . .

$

67.

00C

ash

Cre

dit

. . .

. . .

. . .

. . .

. . .

. . .

. . .

6,95

4.00

Tot

als

. . .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

. .

$7,0

21.0

0$7

,021

.00

BTE_Ch09-193-220.qxd 10/29/07 7:02 PM Page 201 SECOND REVISED

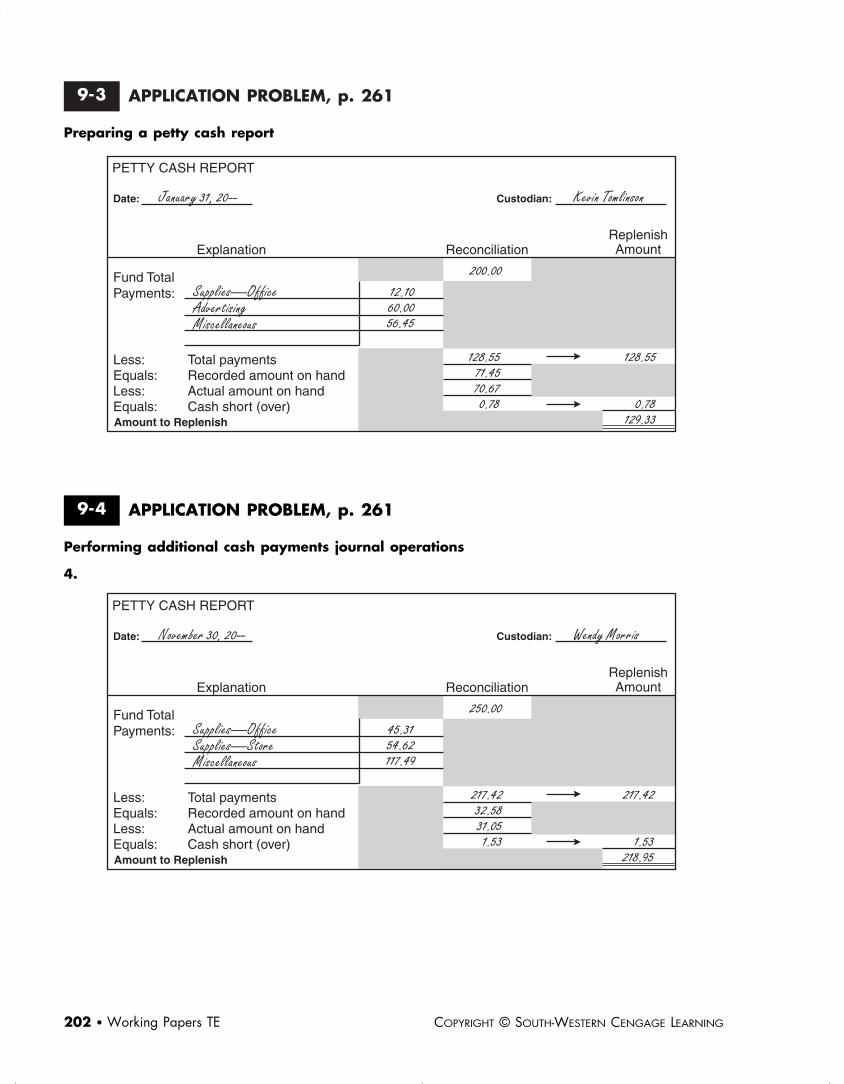

APPLICATION PROBLEM, p. 2619-3

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING202 • Working Papers TE

Preparing a petty cash report

APPLICATION PROBLEM, p. 2619-4

Performing additional cash payments journal operations

PETTY CASH REPORT

Fund TotalPayments:

Less: Total paymentsEquals: Recorded amount on handLess: Actual amount on handEquals: Cash short (over)

Explanation ReconciliationReplenishAmount

Amount to Replenish

Date: Custodian:

Supplies—OfficeAdvertisingMiscellaneous

January 31, 20-- Kevin Tomlinson

12.10 60.0056.45

128.55 71.45 70.67 0.78

128.55

0.78 129.33

200.00

PETTY CASH REPORT

Fund TotalPayments:

Less: Total paymentsEquals: Recorded amount on handLess: Actual amount on handEquals: Cash short (over)

Explanation ReconciliationReplenishAmount

Amount to Replenish

Date: Custodian:

Supplies—OfficeSupplies—StoreMiscellaneous

November 30, 20-- Wendy Morris

45.3154.62117.49

217.42 32.58 31.05 1.53

217.42

1.53 218.95

250.00

4.

BTE_Ch09-193-220.qxd 10/29/07 7:02 PM Page 202 SECOND REVISED

Name Date Class

APPLICATION PROBLEM (concluded)9-4

Chapter 9 Journalizing Purchases and Cash Payments • 203

CA

SH P

AYM

ENTS

JOU

RNA

LP

AG

E23

12

34

1 2 3 4 5 6 7 8 9 10

1 2 3 4 5 6 7 8 9 10

DA

TE

AC

CO

UN

T T

ITL

E

PU

RC

HA

SE

SD

ISC

OU

NT

CR

ED

IT

CA

SH

CR

ED

IT

Nov

.20

– –

30 30 30

Bro

ught

For

war

d

Supp

lies

—O

ffic

e

Supp

lies

—St

ore

Mis

cell

aneo

us E

xpen

se

Cas

h Sh

ort

and

Ove

r

Tot

als

CK

.N

O.

PO

ST

.R

EF

.

GE

NE

RA

L

DE

BIT

CR

ED

IT

18

21

00

45

31

54

62

11

749

153

20

39

95

67

00

67

00

69

54

00

21

895

71

72

95

5

AC

CO

UN

TS

PA

YA

BL

ED

EB

IT

52

00

00

52

00

00

252

✔

Deb

itC

red

itC

olu

mn

Tit

leC

olu

mn

Tot

als

Col

um

n T

otal

s

Gen

eral

Deb

it .

. . .

. . .

. . .

. . .

. . .

. . .

.$2

,039

.95

Gen

eral

Cre

dit

. . .

. . .

. . .

. . .

. . .

. . .

.A

ccou

nts

Paya

ble

Deb

it .

. . .

. . .

. . .

. .5,

200.

00Pu

rcha

ses

Dis

coun

t C

red

it .

. . .

. . .

. . .

$

67.

00C

ash

Cre

dit

. . .

. . .

. . .

. . .

. . .

. . .

. . .

7,17

2.95

Tot

als

. . .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

. .

$7,2

39.9

5$7

,239

.95

3., 5

., 6

., 7

.

BTE_Ch09-193-220.qxd 10/29/07 7:02 PM Page 203 SECOND REVISED

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING204 • Working Papers TE

APPLICATION PROBLEM, p. 2629-5

Journalizing other transactions using a general journal

GENERAL JOURNAL PAGE 10

DATE ACCOUNT TITLE DEBIT CREDITDOC.NO.

POST.REF.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

Oct.20 – –

5

9

13

18

25

Supplies—Store

Accounts Payable/Displays Warehouse

Accounts Payable/Hendrix Products

Purchases Returns and Allow.

Supplies—Office

Accounts Payable/Office Express

Accounts Payable/T-J Designs

Purchases Returns and Allow.

Supplies—Store

Accounts Payable/Classic Fixtures

2 7 5 00

6 4 0 00

2 1 5 00

3 9 0 00

1 8 0 00

2 7 5 00

6 4 0 00

2 1 5 00

3 9 0 00

1 8 0 00

M39

DM25

M40

DM26

M41

BTE_Ch09-193-220.qxd 10/29/07 7:02 PM Page 204 SECOND REVISED

Name Date Class

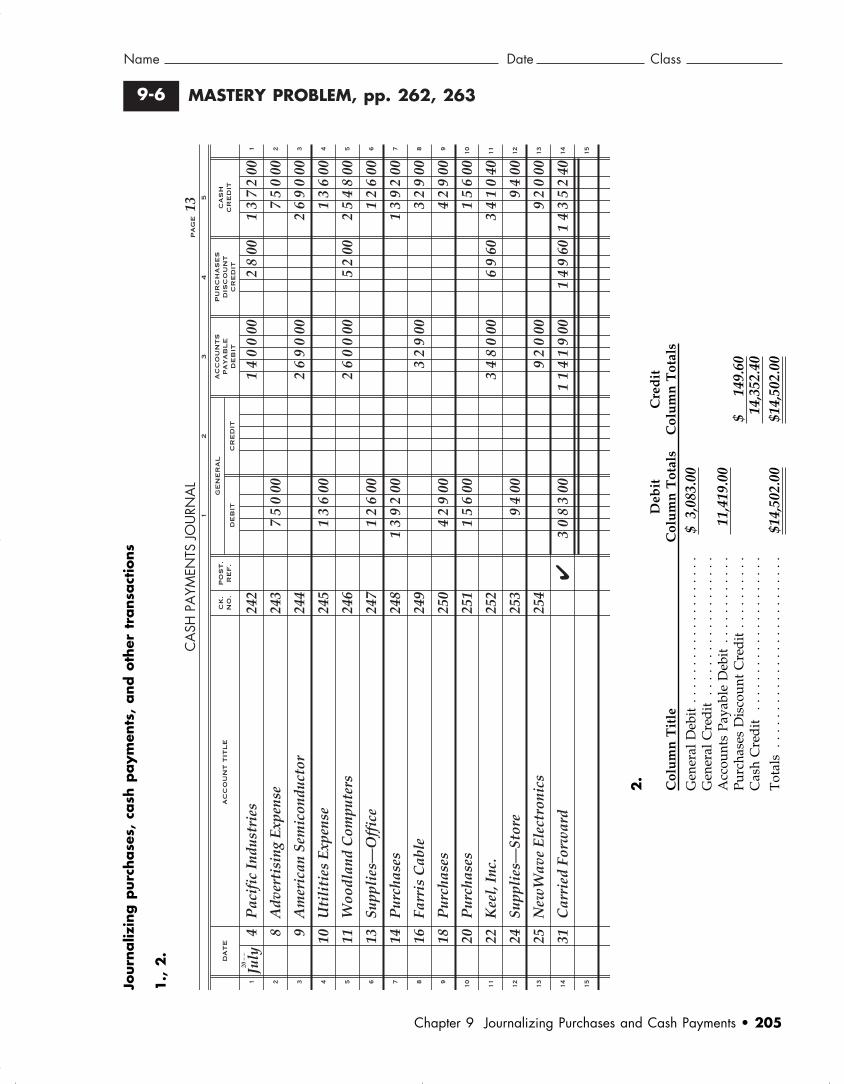

MASTERY PROBLEM, pp. 262, 2639-6

Chapter 9 Journalizing Purchases and Cash Payments • 205

CA

SH P

AYM

ENTS

JOU

RNA

LP

AG

E13

12

34

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

DA

TE

AC

CO

UN

T T

ITL

E

PU

RC

HA

SE

SD

ISC

OU

NT

CR

ED

IT

CA

SH

CR

ED

IT

July

20 –

–

4 8 9 10 11 13 14 16 18 20 22 24 25 31

Pac

ific

Ind

ustr

ies

Adv

erti

sing

Exp

ense

Am

eric

an S

emic

ondu

ctor

Uti

liti

es E

xpen

se

Woo

dlan

d C

ompu

ters

Supp

lies

—O

ffic

e

Pur

chas

es

Farr

is C

able

Pur

chas

es

Pur

chas

es

Kee

l, In

c.

Supp

lies

—St

ore

New

Wav

e E

lect

roni

cs

Car

ried

For

war

d

CK

.N

O.

PO

ST

.R

EF

.

GE

NE

RA

L

DE

BIT

CR

ED

IT

75

000

13

600

12

600

13

92

00

42

900

15

600

94

00

30

83

00

28

00

52

00

69

60

14

960

13

72

00

75

000

26

90

00

13

600

25

48

00

12

600

13

92

00

32

900

42

900

15

600

34

10

40

94

00

92

000

14

35

240

5

AC

CO

UN

TS

PA

YA

BL

ED

EB

IT

14

00

00

26

90

00

26

00

00

32

900

34

80

00

92

000

11

41

900

242

243

244

245

246

247

248

249

250

251

252

253

254

✔

Journ

aliz

ing p

urc

hase

s, c

ash

paym

ents

, and o

ther

tra

nsa

ctio

ns

1., 2

.

Deb

itC

red

itC

olu

mn

Tit

leC

olu

mn

Tot

als

Col

um

n T

otal

s

Gen

eral

Deb

it .

. . .

. . .

. . .

. . .

. . .

. . .

.$

3,08

3.00

Gen

eral

Cre

dit

. . .

. . .

. . .

. . .

. . .

. . .

.A

ccou

nts

Paya

ble

Deb

it .

. . .

. . .

. . .

. .11

,419

.00

Purc

hase

s D

isco

unt

Cre

dit

. . .

. . .

. . .

.$

1

49.6

0C

ash

Cre

dit

. . .

. . .

. . .

. . .

. . .

. . .

. . .

14,3

52.4

0T

otal

s .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

.$1

4,50

2.00

$14,

502.

00

2.

BTE_Ch09-193-220.qxd 10/29/07 7:02 PM Page 205 SECOND REVISED

MASTERY PROBLEM (continued)9-6

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING206 • Working Papers TE

PURCHASES JOURNAL PAGE 7

1

2

3

4

5

6

7

8

9

10

11

12

13

14

1

2

3

4

5

6

7

8

9

10

11

12

13

14

DATE ACCOUNT CREDITED PURCHASES DR.ACCTS. PAY. CR.

July20 – –

2

6

12

15

27

31

Woodland Computers

NewWave Electronics

Helms Supply

Keel, Inc.

Woodland Computers

Total

PURCH.NO.

POST.REF.

2 6 0 0 00

2 5 6 0 00

5 5 0 00

3 4 8 0 00

3 2 0 0 00

1 2 3 9 0 00

354

355

356

357

358

1., 5.

GENERAL JOURNAL PAGE 11

DATE ACCOUNT TITLE DEBIT CREDITDOC.NO.

POST.REF.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

1

2

3

4

5

6

7

8

9

10

11

12

13

14

July20 – –

8

12

15

30

Supplies—Store

Accounts Payable/Willcut & Bishop

Accounts Payable/NewWave Electronics

Purchases Returns and Allow.

Supplies—Office

Accounts Payable/Office Express

Accounts Payable/Woodland Computers

Purchases Returns and Allow.

1 2 5 00

1 6 4 0 00

1 0 6 00

1 2 0 00

1 2 5 00

1 6 4 0 00

1 0 6 00

1 2 0 00

M39

DM25

M40

DM26

1.

BTE_Ch09-193-220.qxd 10/29/07 7:02 PM Page 206 SECOND REVISED

Name Date Class

MASTERY PROBLEM (concluded)9-6

3., 4

., 6

., 7

.

Chapter 9 Journalizing Purchases and Cash Payments • 207

CA

SH P

AYM

ENTS

JOU

RNA

LP

AG

E14

12

34

1 2 3 4 5 6 7 8

1 2 3 4 5 6 7 8

DA

TE

AC

CO

UN

T T

ITL

E

PU

RC

HA

SE

SD

ISC

OU

NT

CR

ED

IT

CA

SH

CR

ED

IT

July

20 –

–

31 31 31 31

Bro

ught

For

war

d

Hel

ms

Supp

ly

Supp

lies

—O

ffic

e

Supp

lies

—St

ore

Mis

cell

aneo

us E

xpen

se

Cas

h Sh

ort

and

Ove

r

Tot

als

CK

.N

O.

PO

ST

.R

EF

.

GE

NE

RA

L

DE

BIT

CR

ED

IT

30

83

00

23

45

84

32

74

34

32

65

11

036

036

14

960

14

960

143

52

40

55

000

18

175

150

84

15

5

AC

CO

UN

TS

PA

YA

BL

ED

EB

IT

114

19

00

55

000

119

69

00

255

256

✔

Deb

itC

red

itC

olu

mn

Tit

leC

olu

mn

Tot

als

Col

um

n T

otal

s

Gen

eral

Deb

it .

. . .

. . .

. . .

. . .

. . .

. . .

.$

3,26

5.11

Gen

eral

Cre

dit

. . .

. . .

. . .

. . .

. . .

. . .

.$

0.36

Acc

ount

s Pa

yabl

e D

ebit

. . .

. . .

. . .

. . .

11,9

69.0

0Pu

rcha

ses

Dis

coun

t C

red

it .

. . .

. . .

. . .

149.

60C

ash

Cre

dit

. . .

. . .

. . .

. . .

. . .

. . .

. . .

15,0

84.1

5T

otal

s .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

.$1

5,23

4.11

$15,

234.

11

6.

BTE_Ch09-193-220.qxd 10/29/07 7:02 PM Page 207 SECOND REVISED

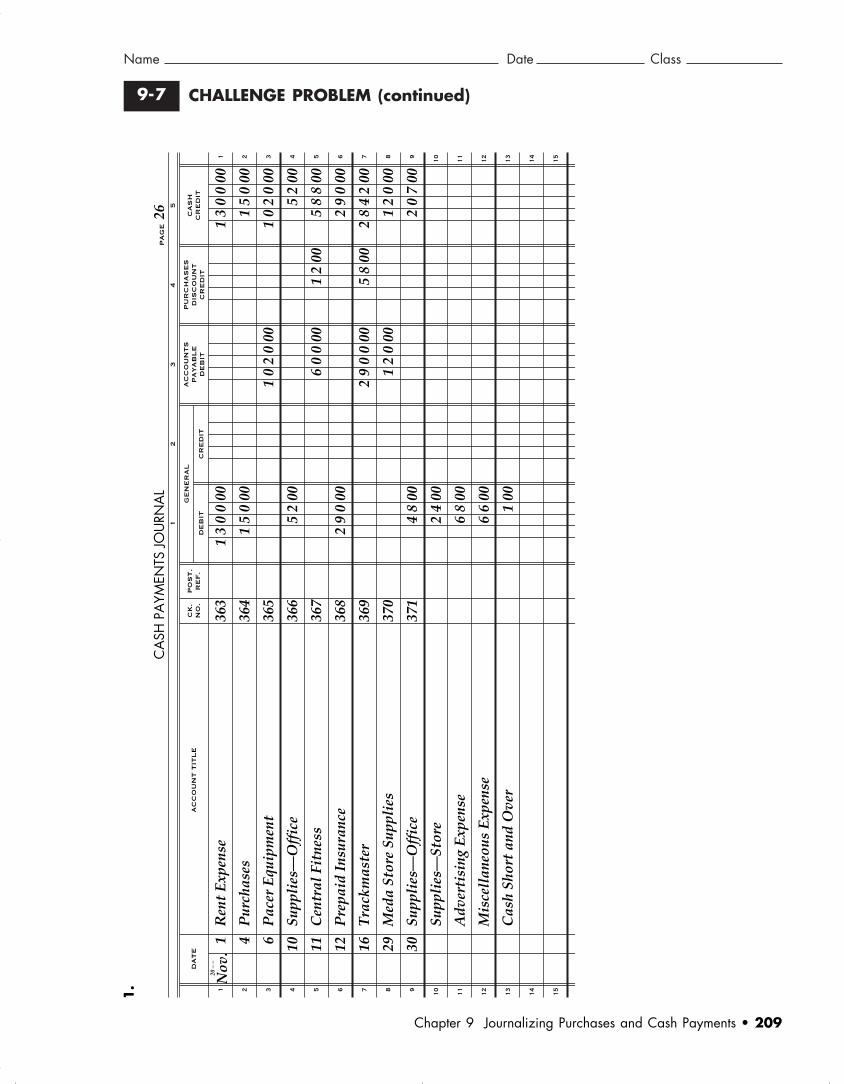

CHALLENGE PROBLEM, p. 2639-7

Journalizing purchases, cash payments, and other transactions

1.

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING208 • Working Papers TE

PURCHASES JOURNAL PAGE 12

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

DATE ACCOUNT CREDITED PURCHASES DR.ACCTS. PAY. CR.

Nov.20 – –

3

9

Central Fitness

Trackmaster

PURCH.NO.

POST.REF.

8 6 0 00

2 9 0 0 00

84

85

BTE_Ch09-193-220.qxd 10/29/07 7:02 PM Page 208 SECOND REVISED

Name Date Class

CHALLENGE PROBLEM (continued)9-7

Chapter 9 Journalizing Purchases and Cash Payments • 209

1.

CA

SH P

AYM

ENTS

JOU

RNA

LP

AG

E26

12

34

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

DA

TE

AC

CO

UN

T T

ITL

E

PU

RC

HA

SE

SD

ISC

OU

NT

CR

ED

IT

CA

SH

CR

ED

IT

Nov

.20

– –

1 4 6 10 11 12 16 29 30

Ren

t E

xpen

se

Pur

chas

es

Pac

er E

quip

men

t

Supp

lies

—O

ffic

e

Cen

tral

Fit

ness

Pre

paid

Ins

uran

ce

Tra

ckm

aste

r

Med

a St

ore

Supp

lies

Supp

lies

—O

ffic

e

Supp

lies

—St

ore

Adv

erti

sing

Exp

ense

Mis

cell

aneo

us E

xpen

se

Cas

h Sh

ort

and

Ove

r

CK

.N

O.

PO

ST

.R

EF

.

GE

NE

RA

L

DE

BIT

CR

ED

IT

13

00

00

15

000

52

00

29

000

48

00

24

00

68

00

66

00

100

12

00

58

00

13

00

00

15

000

10

20

00

52

00

58

800

29

000

28

42

00

12

000

20

700

5

AC

CO

UN

TS

PA

YA

BL

ED

EB

IT

10

20

00

60

000

29

00

00

12

000

363

364

365

366

367

368

369

370

371

BTE_Ch09-193-220.qxd 10/29/07 7:02 PM Page 209 SECOND REVISED

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING210 • Working Papers TE

CHALLENGE PROBLEM (continued)9-7

GENERAL JOURNAL PAGE 11

DATE ACCOUNT TITLE DEBIT CREDITDOC.NO.

POST.REF.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

Nov.20 – –

2

8

Supplies—Store

Accounts Payable/Meda Store Supplies

Accounts Payable/Central Fitness

Purchases Returns and Allow.

1 2 0 00

2 6 0 00

1 2 0 00

2 6 0 00

M43

DM54

1.

BTE_Ch09-193-220.qxd 10/29/07 7:02 PM Page 210 SECOND REVISED

Name Date Class

CHALLENGE PROBLEM (concluded)9-7

2.

Chapter 9 Journalizing Purchases and Cash Payments • 211

a. For any other transactions that occur frequently. For example, if a business

frequently purchases merchandise for cash, a Purchases Debit amount column

could be added.

b. There are circumstances where either entry could be correct. Insurance premiums

paid in advance technically are assets until the insurance is “used up.’’ If

premiums are paid in advance for a long period of time, such as one or two

years, a business probably would record the premium as an asset, Prepaid

Insurance. Then each period financial statements are prepared, record the

portion used up as an expense; thus, the asset would be reduced gradually.

However, if the premium paid is for only a month, the insurance would be

“used up’’ before financial statements are prepared. Therefore, it would be

simpler to record the premium payment as an expense, Insurance Expense.

BTE_Ch09-193-220.qxd 10/29/07 7:02 PM Page 211 SECOND REVISED

USING SOURCE DOCUMENTS, p. 265

Journalizing purchases, cash payments, and other transactions fromsource documents

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING212 • Working Papers TE

TO: Messler Sailing 142 River Street Naperville, IL 60540-3172

INVOICE

DATE:

INV. NO.

TERMS:

ACCT. NO.

1Form

DESCRIPTIONQUANTITY CAT. NO.

Suddard Industries1423 Commercial RoadBell City, LA 70630-6213

UNIT PRICE TOTAL

REC'D 10/03/- - P324

jib sheetjib halyard

TOTAL

43234233

2520

$ 1,125.00$ 1,100.00

$ 2,225.00

$ 45.00$ 55.00

9/30/- -6234

30 days2450

BAL. BRO‘T. FOR‘D. . . 12,485 25

SUBTOTAL . . . . . . . . . . . . . . . . . . . 12,485 25AMT. THIS CHECK . . . . . . . . . . . . . 1,520 00BAL. CAR‘D. FOR‘D. . . . . . . . . . . . 10,965 25

OTHER:

AMT. DEPOSITED . . . .

SUBTOTAL . . . . . . . . . . . . . . . . . . . 12,485 25Date

NO. 458 $

Date: October 4 20 - -

To: Seaside Manufacturing

For: On account

1,520.00 Form 2

BTE_Ch09-193-220.qxd 10/29/07 7:02 PM Page 212 SECOND REVISED

Name Date Class

USING SOURCE DOCUMENTS (continued)

Chapter 9 Journalizing Purchases and Cash Payments • 213

3Form

Attached invoice from SullivanSupply Co. is for store supplies,bought on account, $105.00

MEMORANDUM

NO. 39

DATE October 4, 20--

Messler Sailing

Messler Sailing

142 River Street

Naperville, IL 60540-3172

DEBIT MEMORANDUM NO. 25 4Form

DESCRIPTIONQUANTITY CAT. NO. UNIT PRICE TOTAL

Life preserversdamaged in transit

JS-34211 $ 275.00$ 25.00

DATEOctober 8, 20--

TO

ACCOUNT NO.2040

Seaside Manufacturing1430 Industrial RoadOcean City, WA 98569-2198

BAL. BRO‘T. FOR‘D. . . 10,965 25

SUBTOTAL . . . . . . . . . . . . . . . . . . . 12,229 25AMT. THIS CHECK . . . . . . . . . . . . . 625 00BAL. CAR‘D. FOR‘D. . . . . . . . . . . . 11,604 25

OTHER:

AMT. DEPOSITED . . . . 10 09 20 -SUBTOTAL . . . . . . . . . . . . . . . . . . . 12,229 25

Date

NO. 459 $

Date: October 10 20 - -

To: Willcutt & Bishop

For: Office Supplies

1,264 00

625.00 Form 5

BTE_Ch09-193-220.qxd 10/29/07 7:02 PM Page 213 SECOND REVISED

USING SOURCE DOCUMENTS (continued)

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING214 • Working Papers TE

TO: Messler Sailing 142 River Street Naperville, IL 60540-3172

INVOICE

DATE:

INV. NO.

TERMS:

ACCT. NO.

6Form

DESCRIPTIONQUANTITY CAT. NO.

Aquatic Manufacturing42 Industrial RoadStratford, CA 93266-4762

UNIT PRICE TOTAL

REC'D 10/11/-- P325

Fiberglass repair kitU-bolts, 1”U-bolts, 2”TOTAL

53263466347

51020

$ 300.00$ 160.00$ 460.00$ 920.00

$ 60.00$ 16.00$ 23.00

10/8/--15484

2/10, n/301420

7Form

Attached invoice from OfficeZone is for office supplies,bought on account, $95.00

MEMORANDUM

NO. 40

DATE October 12, 20--

Messler Sailing

BAL. BRO‘T. FOR‘D. . . 11,604 25

SUBTOTAL . . . . . . . . . . . . . . . . . . . 11,604 25AMT. THIS CHECK . . . . . . . . . . . . . 425 00BAL. CAR‘D. FOR‘D. . . . . . . . . . . . 11,179 25

OTHER:

AMT. DEPOSITED . . . .

SUBTOTAL . . . . . . . . . . . . . . . . . . . 11,604 25Date

NO. 460 $

Date: October 15 20 - -

To: Northern Electric

For: Utilities

425.00 Form 8

BTE_Ch09-193-220.qxd 10/29/07 7:02 PM Page 214 SECOND REVISED

Name Date Class

USING SOURCE DOCUMENTS (continued)

Chapter 9 Journalizing Purchases and Cash Payments • 215

BAL. BRO‘T. FOR‘D. . . 11,179 25

SUBTOTAL . . . . . . . . . . . . . . . . . . . 11,725 75AMT. THIS CHECK . . . . . . . . . . . . . 901 60BAL. CAR‘D. FOR‘D. . . . . . . . . . . . 10,824 15

OTHER:

AMT. DEPOSITED . . . . 10 18 20 -SUBTOTAL . . . . . . . . . . . . . . . . . . . 11,725 75

Date

NO. 461 $

Date: October 19 20 - -

To: Aquatic Manufacturing

For: On account: $920.00 less 2 % cash discount

546 50

901.60 Form 9

TO: Messler Sailing 142 River Street Naperville, IL 60540-3172

INVOICE

DATE:

INV. NO.

TERMS:

ACCT. NO.

10Form

DESCRIPTIONQUANTITY CAT. NO.

NORTHERN SAIL COMPANY253 Beach Blvd.Boston, MA 02169-5029

UNIT PRICE TOTAL

REC'D 10/20/-- P326

Viking-16 mainsailSunset-13 mainsail

TOTAL

B-23B-44

23

$ 3,198.00$ 1,377.00

$ 4,575.00

$ 1,599.00$ 459.00

10/18/--895

30 days1820

BTE_Ch09-193-220.qxd 10/29/07 7:02 PM Page 215 SECOND REVISED

USING SOURCE DOCUMENTS (continued)

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING216 • Working Papers TE

BAL. BRO‘T. FOR‘D. . . 10,824 15

SUBTOTAL . . . . . . . . . . . . . . . . . . . 10,824 15AMT. THIS CHECK . . . . . . . . . . . . . 2,560 00BAL. CAR‘D. FOR‘D. . . . . . . . . . . . 8,264 15

OTHER:

AMT. DEPOSITED . . . .

SUBTOTAL . . . . . . . . . . . . . . . . . . . 10,824 15Date

NO. 462 $

Date: October 20 20 - -

To: WRRX Radio

For: Advertising

2,560.00 Form 11

Messler Sailing

142 River Street

Naperville, IL 60540-3172

DEBIT MEMORANDUM NO. 26 12Form

DESCRIPTIONQUANTITY CAT. NO. UNIT PRICE TOTAL

Fiberglass repair kitmissing components

5322 $ 120.00$ 60.00

DATEOctober 22, 20--

TO

ACCOUNT NO.1420

Aquatic Manufacturing42 Industrial RoadStratford, CA 93266-4762

BTE_Ch09-193-220.qxd 10/29/07 7:02 PM Page 216 SECOND REVISED

Name Date Class

USING SOURCE DOCUMENTS (continued)

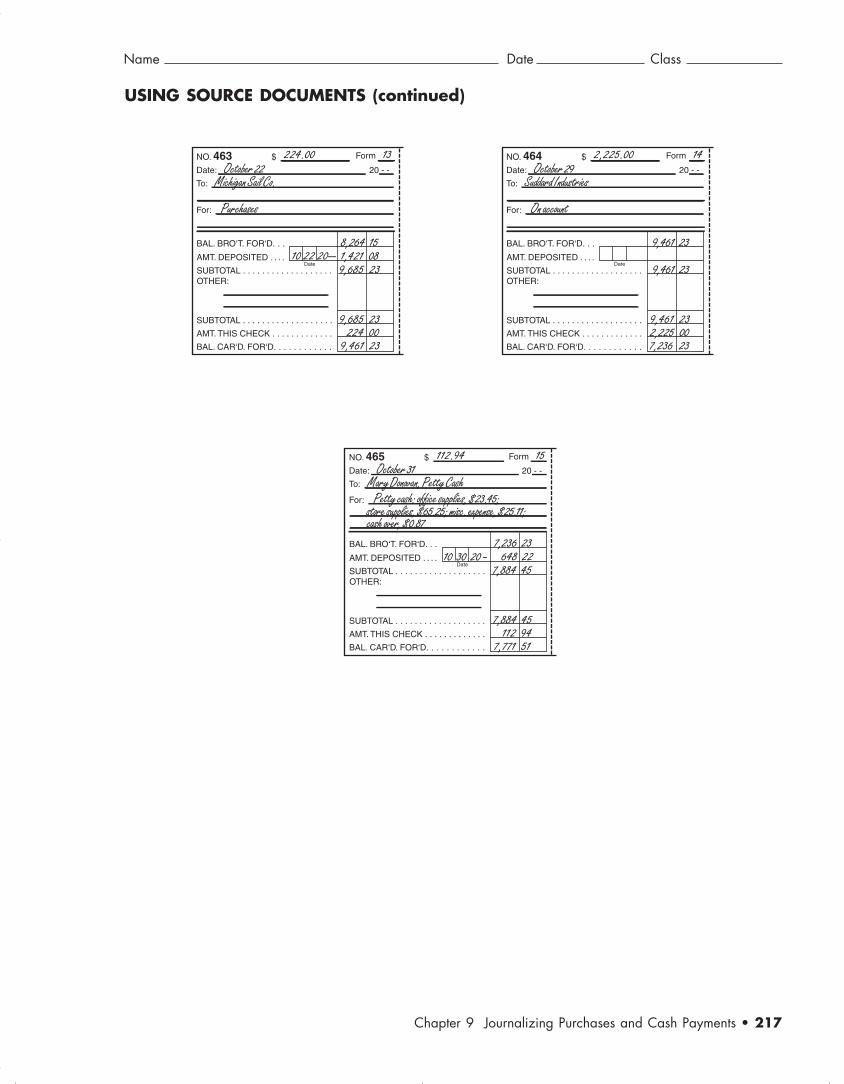

Chapter 9 Journalizing Purchases and Cash Payments • 217

BAL. BRO‘T. FOR‘D. . . 8,264 15

SUBTOTAL . . . . . . . . . . . . . . . . . . . 9,685 23AMT. THIS CHECK . . . . . . . . . . . . . 224 00BAL. CAR‘D. FOR‘D. . . . . . . . . . . . 9,461 23

OTHER:

AMT. DEPOSITED . . . .

SUBTOTAL . . . . . . . . . . . . . . . . . . . 9,685 23Date

NO. 463 $

Date: October 22 20 - -

To: Michigan Sail Co.

For: Purchases

224.00 Form 13

1,421 0810 22 20--BAL. BRO‘T. FOR‘D. . . 9,461 23

SUBTOTAL . . . . . . . . . . . . . . . . . . . 9,461 23AMT. THIS CHECK . . . . . . . . . . . . . 2,225 00BAL. CAR‘D. FOR‘D. . . . . . . . . . . . 7,236 23

OTHER:

AMT. DEPOSITED . . . .

SUBTOTAL . . . . . . . . . . . . . . . . . . . 9,461 23Date

NO. 464 $

Date: October 29 20 - -

To: Suddard Industries

For: On account

2,225.00 Form 14

BAL. BRO‘T. FOR‘D. . . 7,236 23

SUBTOTAL . . . . . . . . . . . . . . . . . . . 7,884 45AMT. THIS CHECK . . . . . . . . . . . . . 112 94BAL. CAR‘D. FOR‘D. . . . . . . . . . . . 7,771 51

OTHER:

AMT. DEPOSITED . . . . 10 30 20 -SUBTOTAL . . . . . . . . . . . . . . . . . . . 7,884 45

Date

NO. 465 $

Date: October 31 20 - -

To: Mary Donovan, Petty CashFor: Petty cash: office supplies, $23.45; store supplies, $65.25; misc. expense, $25.11; cash over, $0.87

648 22

112.94 Form 15

BTE_Ch09-193-220.qxd 10/29/07 7:02 PM Page 217 SECOND REVISED

USING SOURCE DOCUMENTS (continued)

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING218 • Working Papers TE

CA

SH P

AYM

ENTS

JOU

RNA

LP

AG

E15

12

34

1 2 3 4 5 6 7 8 9 10 11 12 13

1 2 3 4 5 6 7 8 9 10 11 12 13

DA

TE

AC

CO

UN

T T

ITL

E

PU

RC

HA

SE

SD

ISC

OU

NT

CR

ED

IT

CA

SH

CR

ED

IT

Oct

.20

– –

4 10 15 19 20 22 29 31 31

Seas

ide

Man

ufac

turi

ng

(2

)

Supp

lies

—O

ffic

e

(5

)

Uti

liti

es E

xpen

se

(8)

Aqu

atic

Man

ufac

turi

ng

(9

)

Adv

erti

sing

Exp

ense

(1

1)

Pur

chas

es

(1

3)

Sudd

ard

Indu

stri

es

(14)

Supp

lies

—O

ffic

e

(1

5)

Supp

lies

—St

ore

Mis

cell

aneo

us E

xpen

se

Cas

h Sh

ort

and

Ove

r

Tot

als

CK

.N

O.

PO

ST

.R

EF

.

GE

NE

RA

L

DE

BIT

CR

ED

IT

62

500

42

500

25

60

00

22

400

23

45

65

25

25

11

39

47

81

087

087

18

40

18

40

15

20

00

62

500

42

500

90

160

25

60

00

22

400

22

25

00

11

294

85

93

54

5

AC

CO

UN

TS

PA

YA

BL

ED

EB

IT

15

20

00

92

000

22

25

00

46

65

00

458

459

460

461

462

463

464

465

Deb

itC

red

itC

olu

mn

Tit

leC

olu

mn

Tot

als

Col

um

n T

otal

s

Gen

eral

Deb

it .

. . .

. . .

. . .

. . .

. . .

. . .

.$

3947

.81

Gen

eral

Cre

dit

. . .

. . .

. . .

. . .

. . .

. . .

.$

0.87

Acc

ount

s Pa

yabl

e D

ebit

. . .

. . .

. . .

. . .

4665

.00

Purc

hase

s D

isco

unt

Cre

dit

. . .

. . .

. . .

.18

.40

Cas

h C

red

it .

. . .

. . .

. . .

. . .

. . .

. . .

. .85

93.5

4T

otal

s .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

. . .

.$

8612

.81

$86

12.8

1

BTE_Ch09-193-220.qxd 10/29/07 7:02 PM Page 218 SECOND REVISED

Name Date Class

USING SOURCE DOCUMENTS (concluded)

Chapter 9 Journalizing Purchases and Cash Payments • 219

PURCHASES JOURNAL PAGE 10

1

2

3

4

5

6

7

8

9

1

2

3

4

5

6

7

8

9

DATE ACCOUNT CREDITED PURCHASES DR.ACCTS. PAY. CR.

Oct.20 – –

3

11

20

31

Suddard Industries (1)

Aquatic Manufacturing (6)

Northern Sail Company (10)

Total

PURCH.NO.

POST.REF.

2 2 2 5 00

9 2 0 00

4 5 7 5 00

7 7 2 0 00

324

325

326

GENERAL JOURNAL PAGE 14

DATE ACCOUNT TITLE DEBIT CREDITDOC.NO.

POST.REF.

1

2

3

4

5

6

7

8

9

10

11

12

1

2

3

4

5

6

7

8

9

10

11

12

Oct.20 – –

4

8

12

22

Supplies—Store (3)

Accounts Payable/Sullivan Supply Co.

Accounts Payable/Seaside Manufacturing (4)

Purchases Returns and Allow.

Supplies—Office (7)

Accounts Payable/Office Zone

Accounts Payable/Aquatic Manufacturing (12)

Purchases Returns and Allow.

1 0 5 00

2 7 5 00

9 5 00

1 2 0 00

1 0 5 00

2 7 5 00

9 5 00

1 2 0 00

M39

DM25

M40

DM26

BTE_Ch09-193-220.qxd 10/29/07 7:02 PM Page 219 SECOND REVISED

BTE_Ch09-193-220.qxd 10/29/07 7:02 PM Page 220 SECOND REVISED