study perfect your score score guide analyzing accounts ... · pdf filejournal entries...

TRANSCRIPT

Name Perfect YourScore Score

Identifying Accounting Terms 6 Pts.Analyzing Accounts Affected by Adjusting and Closing Entries 14 Pts.

Analyzing Adjusting and Closing Entries 9 Pts.Identifying the Accounting Cycle for a Service Business 8 Pts.

Total 37 Pts.

StudyGuide

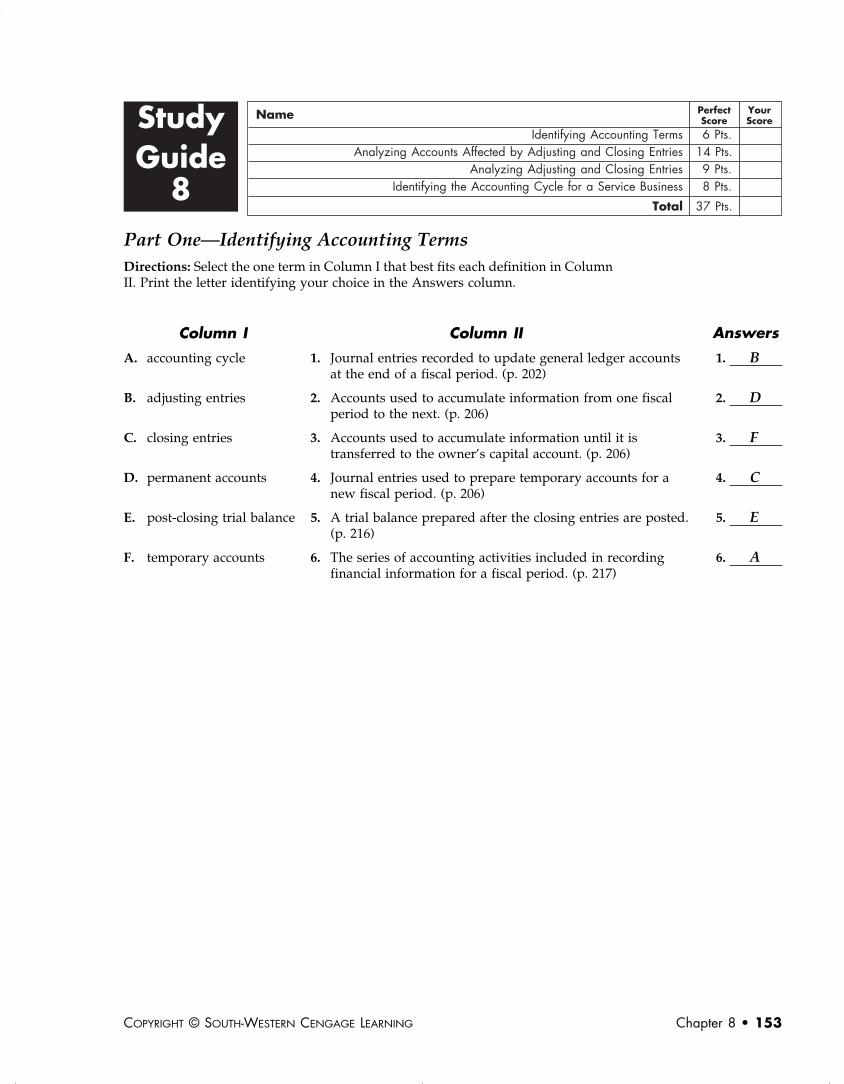

8Part One—Identifying Accounting TermsDirections: Select the one term in Column I that best fits each definition in ColumnII. Print the letter identifying your choice in the Answers column.

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING Chapter 8 • 153

Answers

1. B

2. D

3. F

4. C

5. E

6. A

Column I Column II

A. accounting cycle 1. Journal entries recorded to update general ledger accountsat the end of a fiscal period. (p. 202)

B. adjusting entries 2. Accounts used to accumulate information from one fiscalperiod to the next. (p. 206)

C. closing entries 3. Accounts used to accumulate information until it istransferred to the owner’s capital account. (p. 206)

D. permanent accounts 4. Journal entries used to prepare temporary accounts for anew fiscal period. (p. 206)

E. post-closing trial balance 5. A trial balance prepared after the closing entries are posted.(p. 216)

F. temporary accounts 6. The series of accounting activities included in recordingfinancial information for a fiscal period. (p. 217)

b-te_08-study-153-156.qxd 10/29/07 5:27 PM Page 153 SECOND REVISED

154 • Working Papers TE CENTURY 21 ACCOUNTING, 9TH EDITION

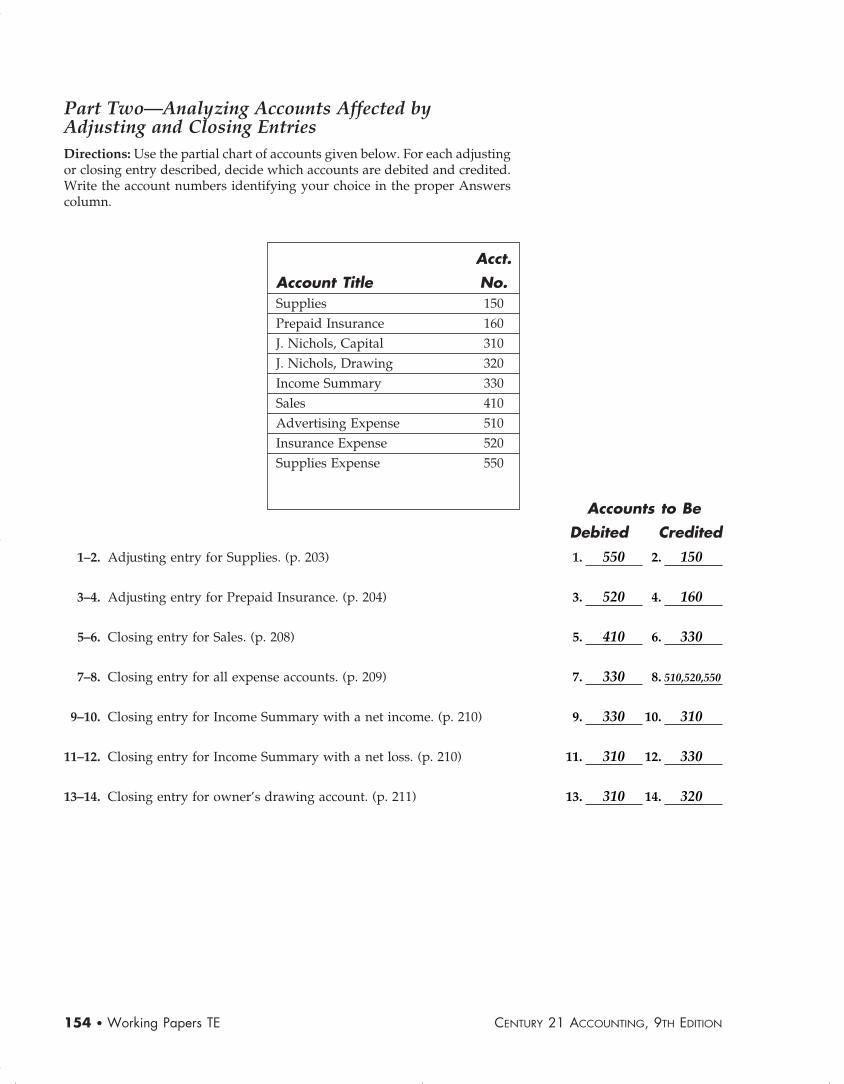

Part Two—Analyzing Accounts Affected byAdjusting and Closing EntriesDirections: Use the partial chart of accounts given below. For each adjustingor closing entry described, decide which accounts are debited and credited.Write the account numbers identifying your choice in the proper Answerscolumn.

Acct.

Account Title No.Supplies 150Prepaid Insurance 160J. Nichols, Capital 310J. Nichols, Drawing 320Income Summary 330Sales 410Advertising Expense 510Insurance Expense 520Supplies Expense 550

1–2. Adjusting entry for Supplies. (p. 203)

3–4. Adjusting entry for Prepaid Insurance. (p. 204)

5–6. Closing entry for Sales. (p. 208)

7–8. Closing entry for all expense accounts. (p. 209)

9–10. Closing entry for Income Summary with a net income. (p. 210)

11–12. Closing entry for Income Summary with a net loss. (p. 210)

13–14. Closing entry for owner’s drawing account. (p. 211)

Accounts to Be

Debited Credited

1. 550 2. 150

3. 520 4. 160

5. 410 6. 330

7. 330 8. 510,520,550

9. 330 10. 310

11. 310 12. 330

13. 310 14. 320

b-te_08-study-153-156.qxd 10/29/07 5:27 PM Page 154 SECOND REVISED

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING Chapter 8 • 155

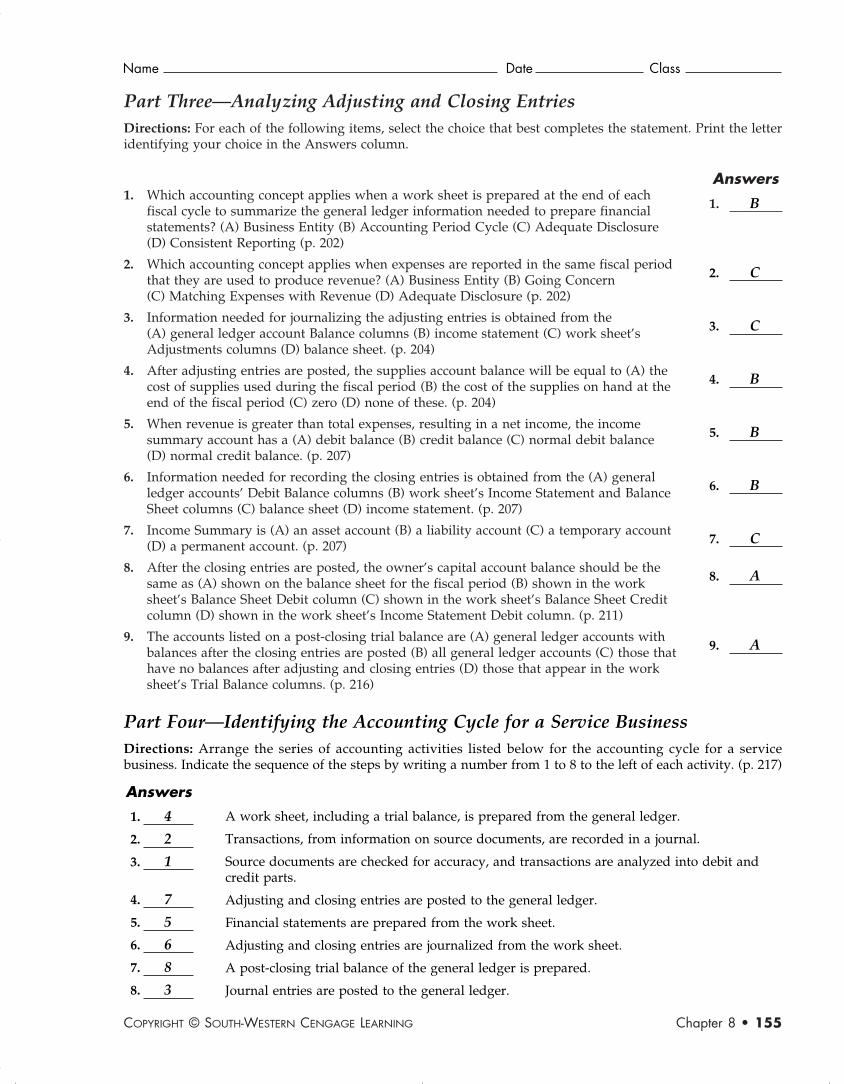

1. Which accounting concept applies when a work sheet is prepared at the end of eachfiscal cycle to summarize the general ledger information needed to prepare financialstatements? (A) Business Entity (B) Accounting Period Cycle (C) Adequate Disclosure(D) Consistent Reporting (p. 202)

2. Which accounting concept applies when expenses are reported in the same fiscal periodthat they are used to produce revenue? (A) Business Entity (B) Going Concern(C) Matching Expenses with Revenue (D) Adequate Disclosure (p. 202)

3. Information needed for journalizing the adjusting entries is obtained from the(A) general ledger account Balance columns (B) income statement (C) work sheet’sAdjustments columns (D) balance sheet. (p. 204)

4. After adjusting entries are posted, the supplies account balance will be equal to (A) thecost of supplies used during the fiscal period (B) the cost of the supplies on hand at theend of the fiscal period (C) zero (D) none of these. (p. 204)

5. When revenue is greater than total expenses, resulting in a net income, the incomesummary account has a (A) debit balance (B) credit balance (C) normal debit balance(D) normal credit balance. (p. 207)

6. Information needed for recording the closing entries is obtained from the (A) generalledger accounts’ Debit Balance columns (B) work sheet’s Income Statement and BalanceSheet columns (C) balance sheet (D) income statement. (p. 207)

7. Income Summary is (A) an asset account (B) a liability account (C) a temporary account(D) a permanent account. (p. 207)

8. After the closing entries are posted, the owner’s capital account balance should be thesame as (A) shown on the balance sheet for the fiscal period (B) shown in the worksheet’s Balance Sheet Debit column (C) shown in the work sheet’s Balance Sheet Creditcolumn (D) shown in the work sheet’s Income Statement Debit column. (p. 211)

9. The accounts listed on a post-closing trial balance are (A) general ledger accounts withbalances after the closing entries are posted (B) all general ledger accounts (C) those thathave no balances after adjusting and closing entries (D) those that appear in the worksheet’s Trial Balance columns. (p. 216)

Part Three—Analyzing Adjusting and Closing EntriesDirections: For each of the following items, select the choice that best completes the statement. Print the letteridentifying your choice in the Answers column.

Answers

1. B

2. C

3. C

4. B

5. B

6. B

7. C

8. A

9. A

Part Four—Identifying the Accounting Cycle for a Service BusinessDirections: Arrange the series of accounting activities listed below for the accounting cycle for a servicebusiness. Indicate the sequence of the steps by writing a number from 1 to 8 to the left of each activity. (p. 217)

Answers

1. 4

2. 2

3. 1

4. 7

5. 5

6. 6

7. 8

8. 3

A work sheet, including a trial balance, is prepared from the general ledger.

Transactions, from information on source documents, are recorded in a journal.

Source documents are checked for accuracy, and transactions are analyzed into debit andcredit parts.

Adjusting and closing entries are posted to the general ledger.

Financial statements are prepared from the work sheet.

Adjusting and closing entries are journalized from the work sheet.

A post-closing trial balance of the general ledger is prepared.

Journal entries are posted to the general ledger.

Name Date Class

b-te_08-study-153-156.qxd 10/29/07 5:27 PM Page 155 SECOND REVISED

b-te_08-study-153-156.qxd 10/29/07 5:27 PM Page 156 SECOND REVISED

Name Date Class

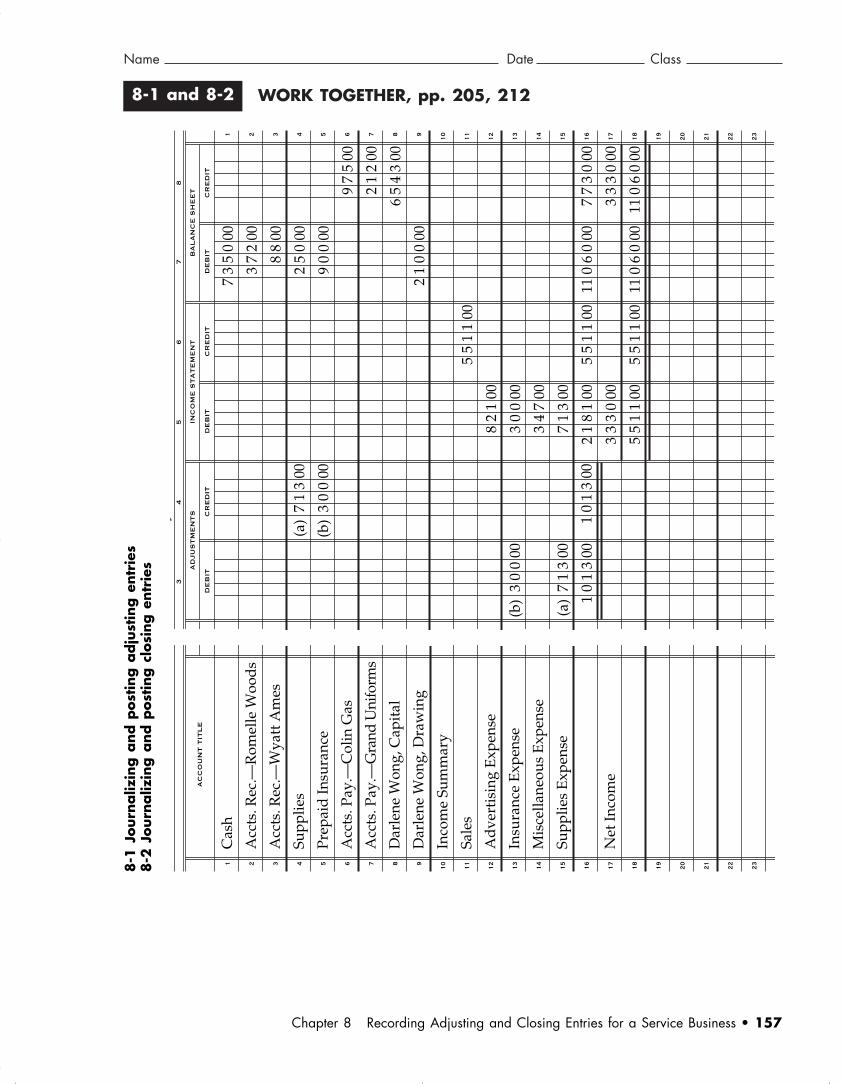

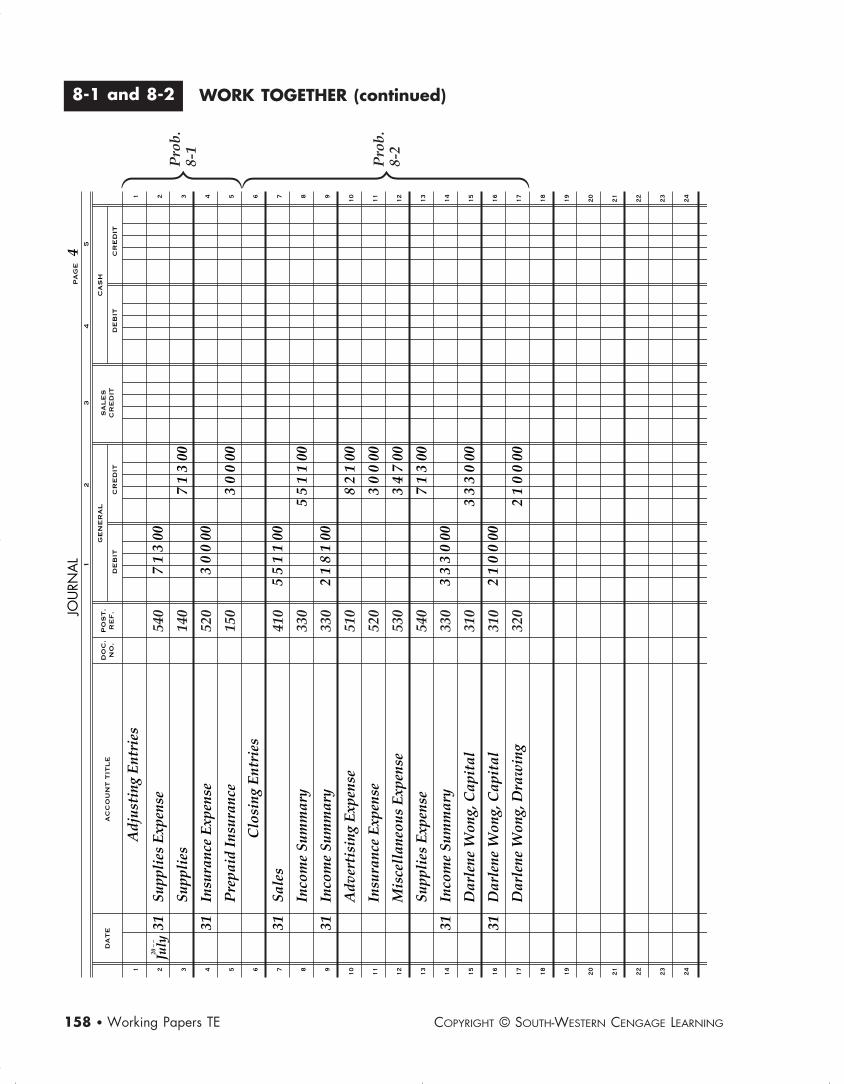

WORK TOGETHER, pp. 205, 2128-1 and 8-2

8-1

Journ

aliz

ing a

nd p

ost

ing a

dju

stin

g e

ntr

ies

8-2

Journ

aliz

ing a

nd p

ost

ing c

losi

ng e

ntr

ies

Chapter 8 Recording Adjusting and Closing Entries for a Service Business • 157

34

AD

JUS

TM

EN

TS

DE

BIT

CR

ED

IT

INC

OM

E S

TA

TE

ME

NT

DE

BIT

CR

ED

IT

BA

LA

NC

E S

HE

ET

DE

BIT

CR

ED

IT

56

78

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23

(b)

30

000

(a)

71

300

10

13

00

(a)

71

300

(b)

30

000

10

13

00

82

100

30

000

34

700

71

300

21

81

00

33

30

00

55

11

00

55

11

00

55

11

00

55

11

00

73

50

00

37

200

88

00

25

000

90

000

21

00

00

110

60

00

110

60

00

97

500

21

200

65

43

00

77

30

00

33

30

00

110

60

00

y

AC

CO

UN

T T

ITL

E

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23

Cas

h

Acc

ts. R

ec.—

Rom

elle

Woo

ds

Acc

ts. R

ec.—

Wya

tt A

mes

Supp

lies

Prep

aid

Insu

ranc

e

Acc

ts. P

ay.—

Col

in G

as

Acc

ts. P

ay.—

Gra

nd U

nifo

rms

Dar

lene

Won

g, C

apit

al

Dar

lene

Won

g, D

raw

ing

Inco

me

Sum

mar

y

Sale

s

Ad

vert

isin

g E

xpen

se

Insu

ranc

e E

xpen

se

Mis

cella

neou

s E

xpen

se

Supp

lies

Exp

ense

Net

Inco

me

BTE_Ch08-157-184.qxd 10/29/07 5:30 PM Page 157 SECOND REVISED

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING158 • Working Papers TE

WORK TOGETHER (continued)8-1 and 8-2

July

JOU

RNA

LP

AG

E

12

34

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

DA

TE

AC

CO

UN

T T

ITL

E

DO

C.

NO

.P

OS

T.

RE

F.

GE

NE

RA

L

DE

BIT

CR

ED

IT

SA

LE

SC

RE

DIT

CA

SH

DE

BIT

CR

ED

IT

5

4

20 –

–31 31 31 31 31 31

Supp

lies

Exp

ense

Supp

lies

Insu

ranc

e E

xpen

se

Pre

paid

Ins

uran

ce

Sale

s

Inco

me

Sum

mar

y

Inco

me

Sum

mar

y

Adv

erti

sing

Exp

ense

Insu

ranc

e E

xpen

se

Mis

cell

aneo

us E

xpen

se

Supp

lies

Exp

ense

Inco

me

Sum

mar

y

Dar

lene

Won

g, C

apit

al

Dar

lene

Won

g, C

apit

al

Dar

lene

Won

g, D

raw

ing

71

300

30

000

55

11

00

82

100

30

000

34

700

71

300

33

30

00

21

00

00

71

300

30

000

55

11

00

21

81

00

33

30

00

21

00

00

Adj

usti

ng E

ntri

es

Clo

sing

Ent

ries

540

140

520

150

410

330

330

510

520

530

540

330

310

310

320

Pro

b.8-

1

Pro

b.8-

2

BTE_Ch08-157-184.qxd 10/29/07 5:30 PM Page 158 SECOND REVISED

Name Date Class

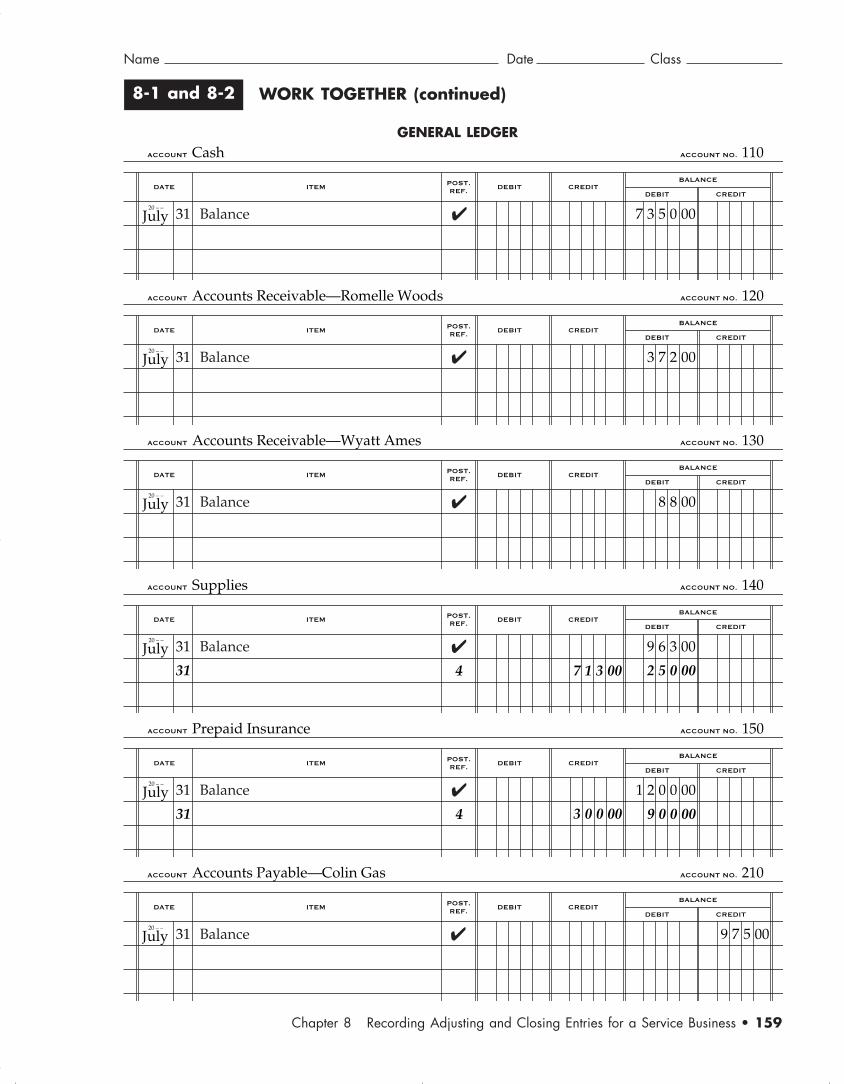

Chapter 8 Recording Adjusting and Closing Entries for a Service Business • 159

GENERAL LEDGER

WORK TOGETHER (continued)8-1 and 8-2

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

110Cash

July20 – –

31 7 3 5 0 00Balance ✔

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

120Accounts Receivable—Romelle Woods

July20 – –

31 3 7 2 00Balance ✔

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

130Accounts Receivable—Wyatt Ames

July20 – –

31 8 8 00Balance ✔

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

140Supplies

July20 – –

31

31 7 1 3 00

9 6 3 00

2 5 0 00

Balance ✔

4

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

150Prepaid Insurance

July20 – –

31

31 3 0 0 00

1 2 0 0 00

9 0 0 00

Balance ✔

4

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

210Accounts Payable—Colin Gas

July20 – –

31 Balance ✔ 9 7 5 00

BTE_Ch08-157-184.qxd 10/29/07 5:30 PM Page 159 SECOND REVISED

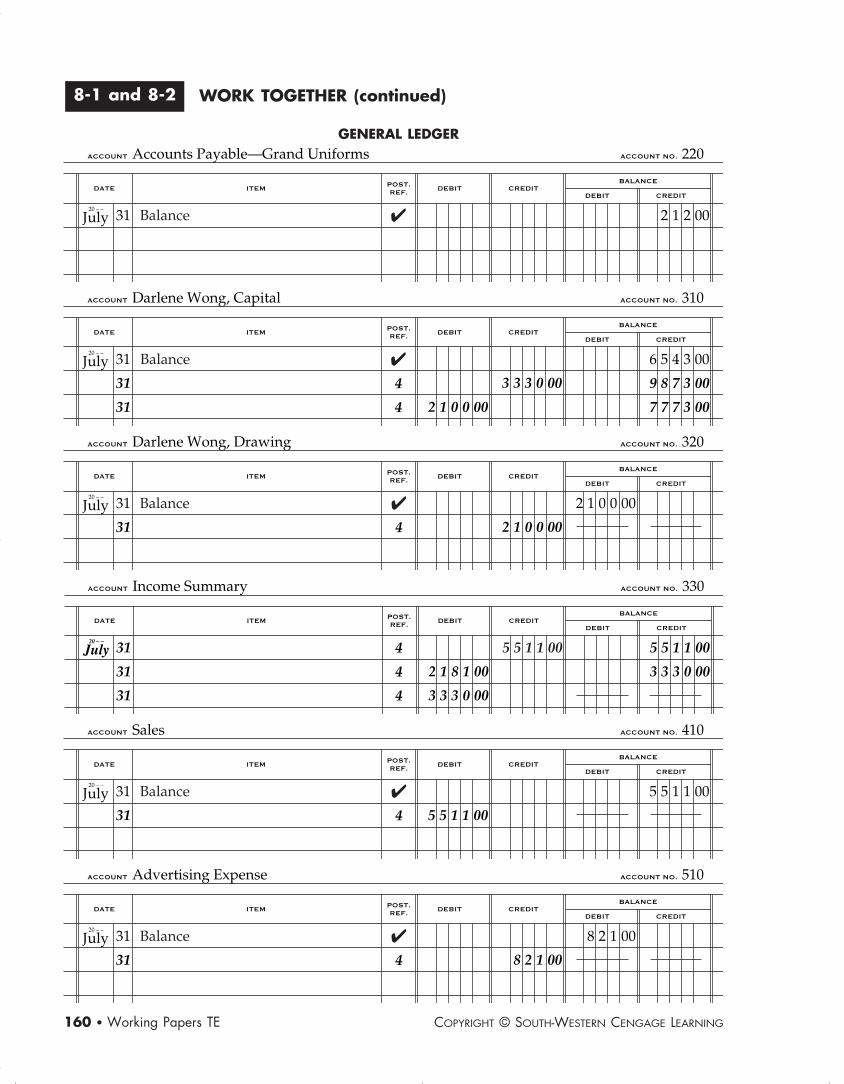

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING160 • Working Papers TE

GENERAL LEDGER

WORK TOGETHER (continued)8-1 and 8-2

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

220Accounts Payable—Grand Uniforms

July20 – –

31 Balance ✔ 2 1 2 00

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

310Darlene Wong, Capital

July20 – –

31

31

31 2 1 0 0 00

3 3 3 0 00

Balance ✔

4

4

6 5 4 3 00

9 8 7 3 00

7 7 7 3 00

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

320Darlene Wong, Drawing

July20 – –

31

31 2 1 0 0 00

2 1 0 0 00Balance ✔

4

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

330Income Summary

July20 – –

31

31

31

2 1 8 1 00

3 3 3 0 00

4

4

4

5 5 1 1 00

3 3 3 0 00

5 5 1 1 00

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

410Sales

July20 – –

31

31 5 5 1 1 00

Balance ✔

4

5 5 1 1 00

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

510Advertising Expense

July20 – –

31

31 8 2 1 00

8 2 1 00Balance ✔

4

BTE_Ch08-157-184.qxd 10/29/07 5:30 PM Page 160 SECOND REVISED

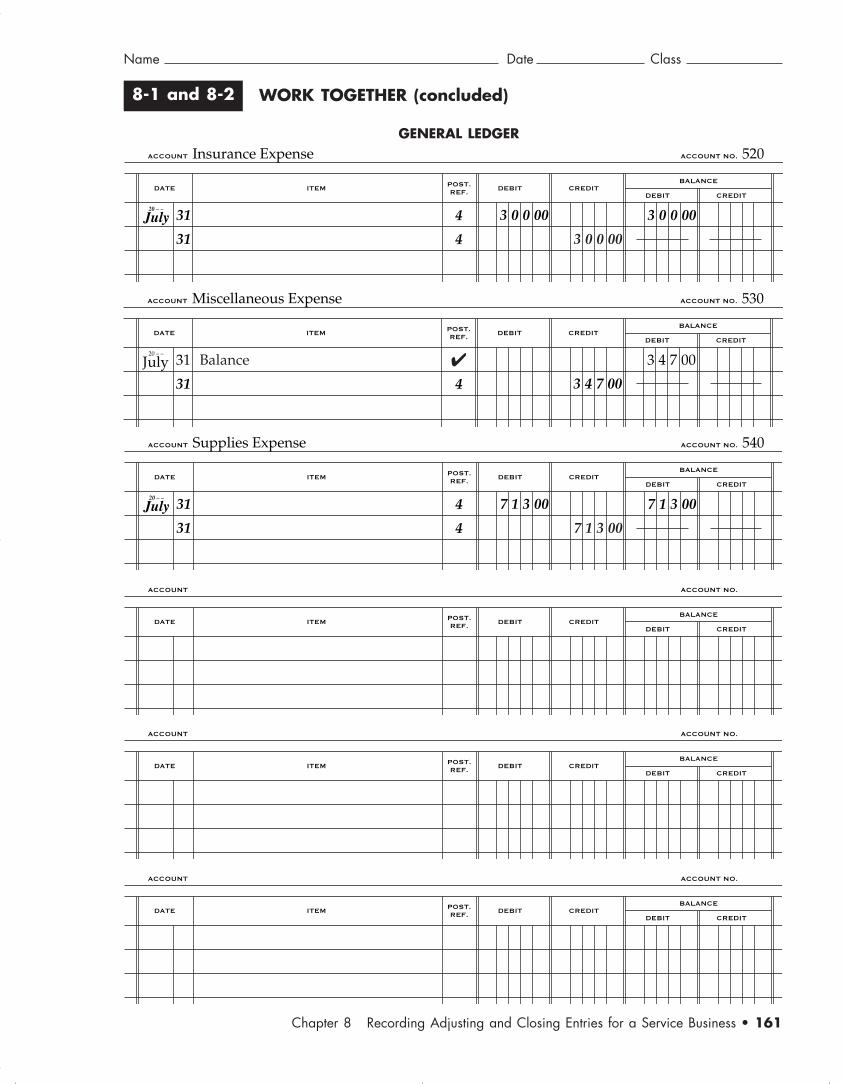

Name Date Class

Chapter 8 Recording Adjusting and Closing Entries for a Service Business • 161

GENERAL LEDGER

WORK TOGETHER (concluded)8-1 and 8-2

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

520Insurance Expense

July20 – –

31

31

3 0 0 00 3 0 0 004

4 3 0 0 00

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

530Miscellaneous Expense

July20 – –

31

31 3 4 7 00

3 4 7 00Balance ✔

4

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

540Supplies Expense

July20 – –

31

31

7 1 3 00 7 1 3 004

4 7 1 3 00

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

BTE_Ch08-157-184.qxd 10/29/07 5:30 PM Page 161 SECOND REVISED

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING162 • Working Papers TE

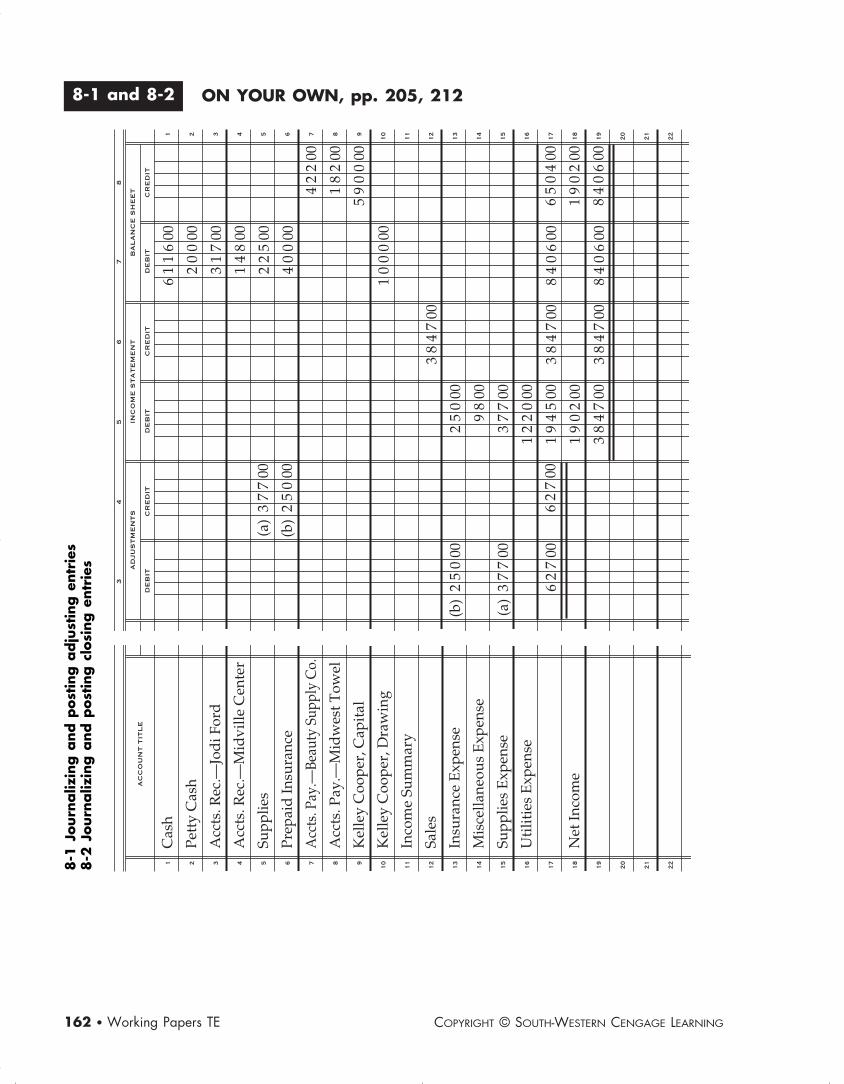

ON YOUR OWN, pp. 205, 2128-1 and 8-2

8-1

Journ

aliz

ing a

nd p

ost

ing a

dju

stin

g e

ntr

ies

8-2

Journ

aliz

ing a

nd p

ost

ing c

losi

ng e

ntr

ies

AC

CO

UN

T T

ITL

E

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22

Cas

h

Pett

y C

ash

Acc

ts. R

ec.—

Jod

i For

d

Acc

ts. R

ec.—

Mid

ville

Cen

ter

Supp

lies

Prep

aid

Insu

ranc

e

Acc

ts. P

ay.—

Beau

ty S

uppl

y C

o.

Acc

ts. P

ay.—

Mid

wes

t Tow

el

Kel

ley

Coo

per,

Cap

ital

Kel

ley

Coo

per,

Dra

win

g

Inco

me

Sum

mar

y

Sale

s

Insu

ranc

e E

xpen

se

Mis

cella

neou

s E

xpen

se

Supp

lies

Exp

ense

Uti

litie

s E

xpen

se

Net

Inco

me

34

AD

JUS

TM

EN

TS

DE

BIT

CR

ED

IT

INC

OM

E S

TA

TE

ME

NT

DE

BIT

CR

ED

IT

BA

LA

NC

E S

HE

ET

DE

BIT

CR

ED

IT

56

78

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22

(b)

25

000

(a)

37

700

62

700

(a)

37

700

(b)

25

000

62

700

25

000

98

00

37

700

12

20

00

19

45

00

19

02

00

38

47

00

38

47

00

38

47

00

38

47

00

61

16

00

20

000

31

700

14

800

22

500

40

000

10

00

00

84

06

00

84

06

00

42

200

18

200

59

00

00

65

04

00

19

02

00

84

06

00

BTE_Ch08-157-184.qxd 10/29/07 5:30 PM Page 162 SECOND REVISED

Name Date Class

Chapter 8 Recording Adjusting and Closing Entries for a Service Business • 163

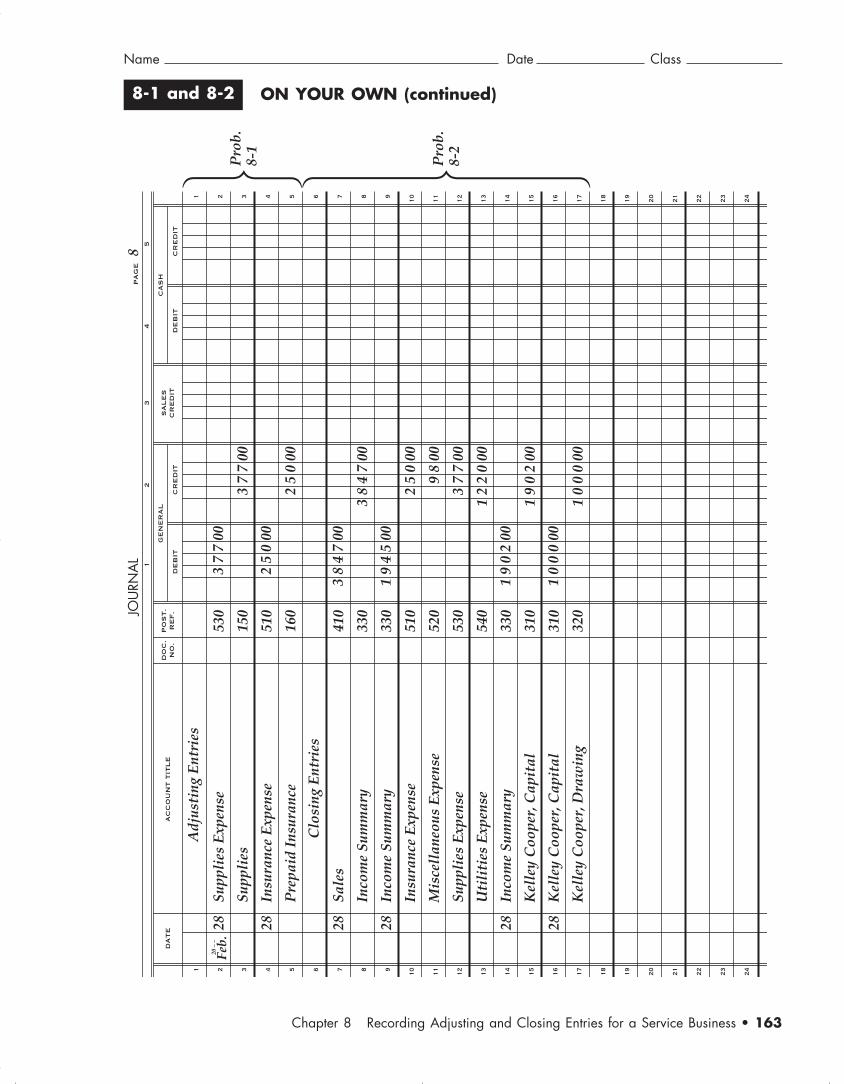

ON YOUR OWN (continued)8-1 and 8-2

Feb.

JOU

RNA

LP

AG

E

12

34

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

DA

TE

AC

CO

UN

T T

ITL

E

DO

C.

NO

.P

OS

T.

RE

F.

GE

NE

RA

L

DE

BIT

CR

ED

IT

SA

LE

SC

RE

DIT

CA

SH

DE

BIT

CR

ED

IT

5

8

20 –

–28 28 28 28 28 28

Supp

lies

Exp

ense

Supp

lies

Insu

ranc

e E

xpen

se

Pre

paid

Ins

uran

ce

Sale

s

Inco

me

Sum

mar

y

Inco

me

Sum

mar

y

Insu

ranc

e E

xpen

se

Mis

cell

aneo

us E

xpen

se

Supp

lies

Exp

ense

Uti

liti

es E

xpen

se

Inco

me

Sum

mar

y

Kel

ley

Coo

per,

Cap

ital

Kel

ley

Coo

per,

Cap

ital

Kel

ley

Coo

per,

Dra

win

g

37

700

25

000

38

47

00

25

000

98

00

37

700

12

20

00

19

02

00

10

00

00

37

700

25

000

38

47

00

19

45

00

19

02

00

10

00

00

Pro

b.8-

2

Adj

usti

ng E

ntri

es

Clo

sing

Ent

ries

530

150

510

160

410

330

330

510

520

530

540

330

310

310

320

Pro

b.8-

1

BTE_Ch08-157-184.qxd 10/29/07 5:30 PM Page 163 SECOND REVISED

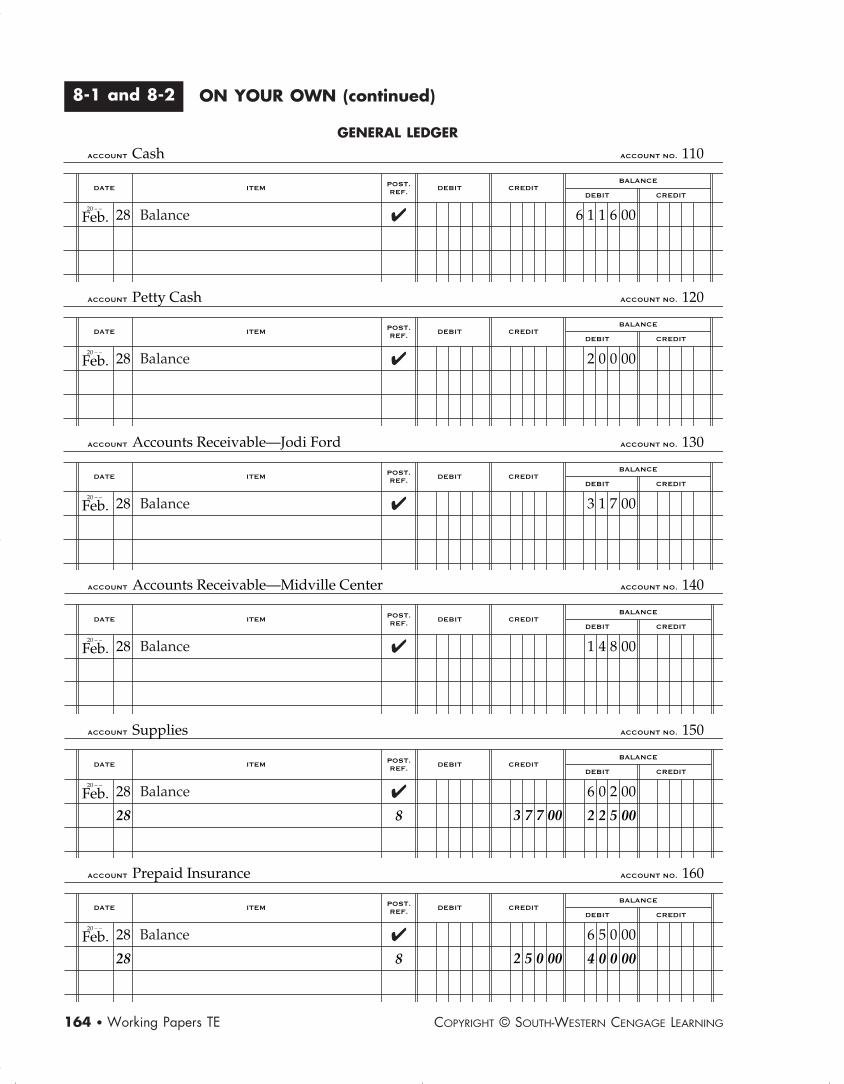

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING164 • Working Papers TE

GENERAL LEDGER

ON YOUR OWN (continued)8-1 and 8-2

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

110Cash

Feb.20 – –

28 6 1 1 6 00Balance ✔

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

120Petty Cash

Feb.20 – –

28 2 0 0 00Balance ✔

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

130Accounts Receivable—Jodi Ford

Feb.20 – –

28 3 1 7 00Balance ✔

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

140Accounts Receivable—Midville Center

Feb.20 – –

28 1 4 8 00Balance ✔

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

150Supplies

Feb.20 – –

28

28 3 7 7 00

6 0 2 00

2 2 5 00

Balance ✔

8

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

160Prepaid Insurance

Feb.20 – –

28

28 2 5 0 00

6 5 0 00

4 0 0 00

Balance ✔

8

BTE_Ch08-157-184.qxd 10/29/07 5:30 PM Page 164 SECOND REVISED

Name Date Class

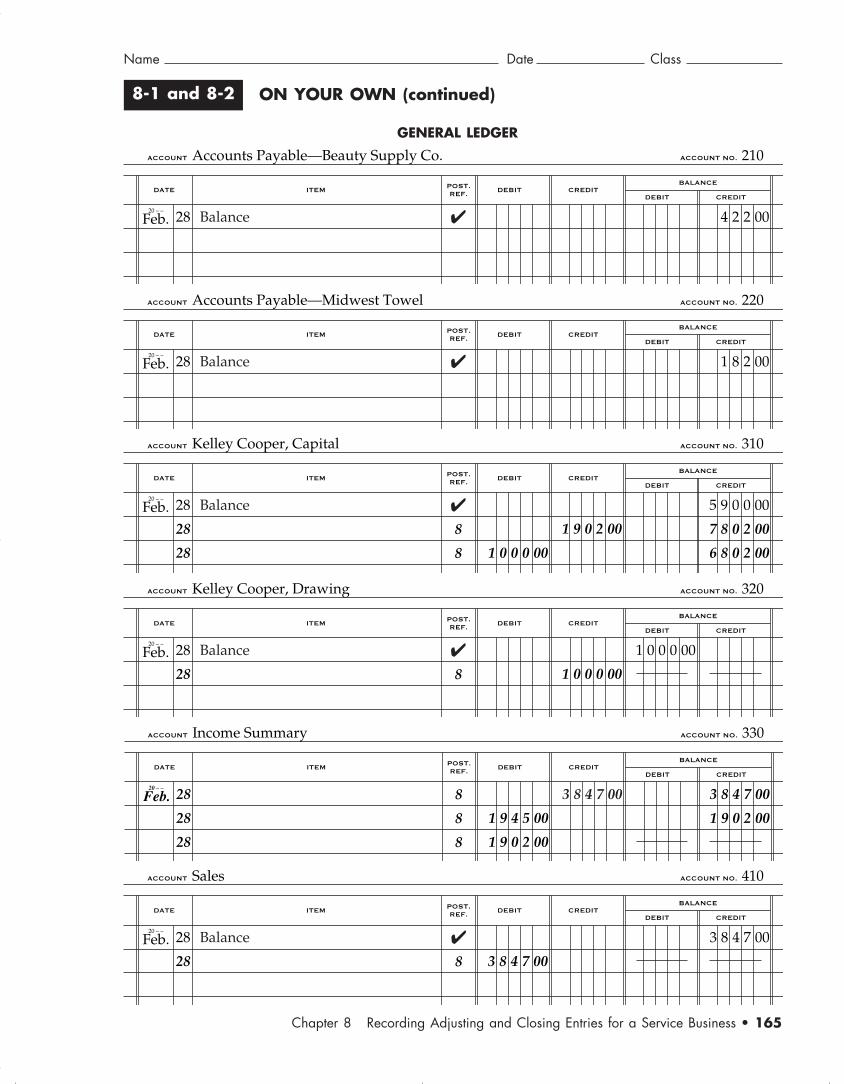

Chapter 8 Recording Adjusting and Closing Entries for a Service Business • 165

GENERAL LEDGER

ON YOUR OWN (continued)8-1 and 8-2

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

210Accounts Payable—Beauty Supply Co.

Feb.20 – –

28 Balance ✔ 4 2 2 00

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

220Accounts Payable—Midwest Towel

Feb.20 – –

28 Balance ✔ 1 8 2 00

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

310Kelley Cooper, Capital

Feb.20 – –

28

28

28 1 0 0 0 00

1 9 0 2 00

Balance ✔

8

8

5 9 0 0 00

7 8 0 2 00

6 8 0 2 00

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

320Kelley Cooper, Drawing

Feb.20 – –

28

28 1 0 0 0 00

1 0 0 0 00Balance ✔

8

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

330Income Summary

Feb.20 – –

28

28

28

1 9 4 5 00

1 9 0 2 00

8

8

8

3 8 4 7 00

1 9 0 2 00

3 8 4 7 00

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

410Sales

Feb.20 – –

28

28 3 8 4 7 00

Balance ✔

8

3 8 4 7 00

BTE_Ch08-157-184.qxd 10/29/07 5:30 PM Page 165 SECOND REVISED

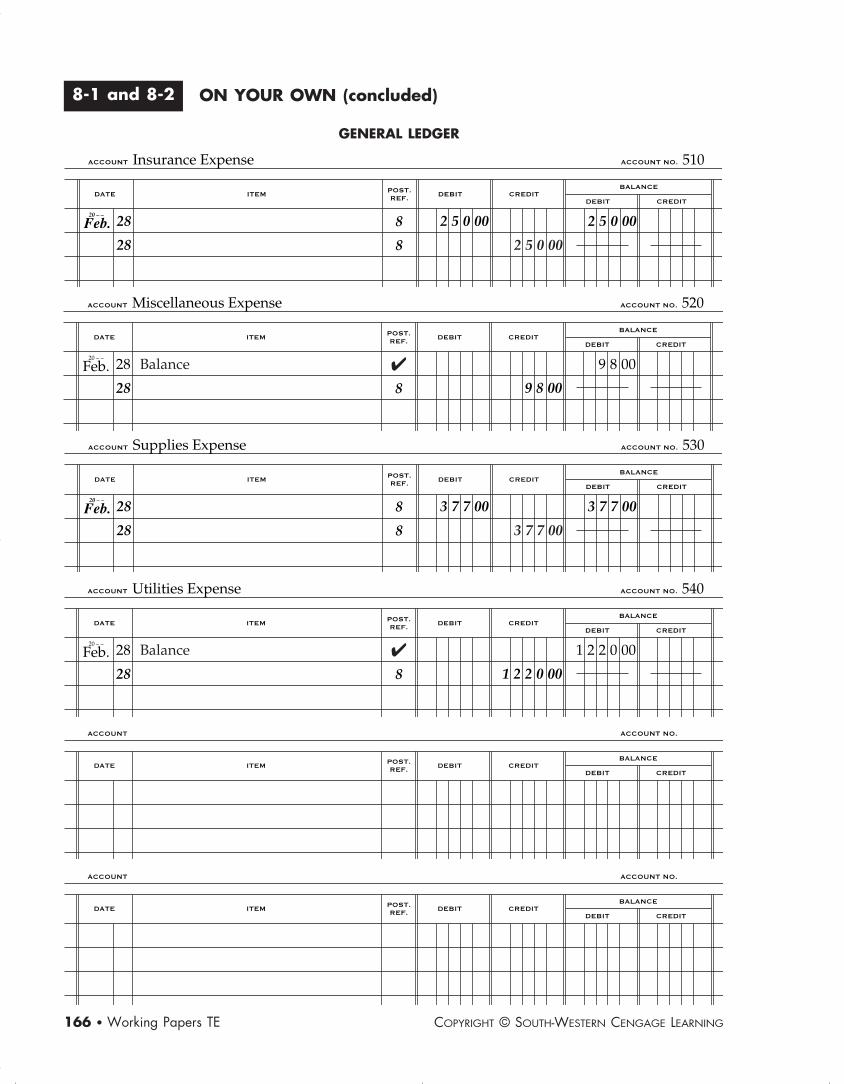

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING166 • Working Papers TE

GENERAL LEDGER

ON YOUR OWN (concluded)8-1 and 8-2

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

510Insurance Expense

Feb.20 – –

28

28

2 5 0 00 2 5 0 008

8 2 5 0 00

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

520Miscellaneous Expense

Feb.20 – –

28

28 9 8 00

9 8 00Balance ✔

8

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

530Supplies Expense

Feb.20 – –

28

28

3 7 7 00 3 7 7 008

8 3 7 7 00

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

540Utilities Expense

Feb.20 – –

28

28 1 2 2 0 00

1 2 2 0 00Balance ✔

8

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

BTE_Ch08-157-184.qxd 10/29/07 5:30 PM Page 166 SECOND REVISED

Name Date Class

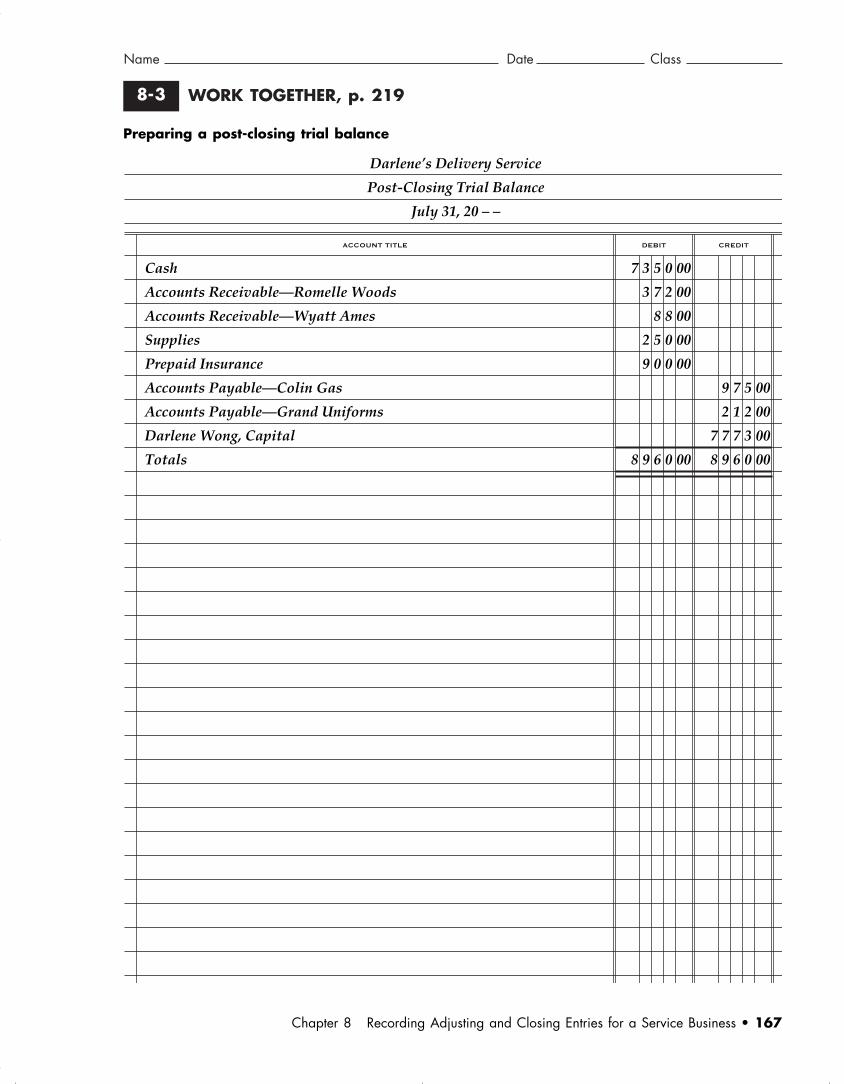

WORK TOGETHER, p. 2198-3

Preparing a post-closing trial balance

Chapter 8 Recording Adjusting and Closing Entries for a Service Business • 167

Cash

Accounts Receivable—Romelle Woods

Accounts Receivable—Wyatt Ames

Supplies

Prepaid Insurance

Accounts Payable—Colin Gas

Accounts Payable—Grand Uniforms

Darlene Wong, Capital

Totals

Darlene’s Delivery Service

Post-Closing Trial Balance

July 31, 20 – –

CREDITDEBITACCOUNT TITLE

7 3 5 0 00

3 7 2 00

8 8 00

2 5 0 00

9 0 0 00

8 9 6 0 00

9 7 5 00

2 1 2 00

7 7 7 3 00

8 9 6 0 00

BTE_Ch08-157-184.qxd 10/29/07 5:30 PM Page 167 SECOND REVISED

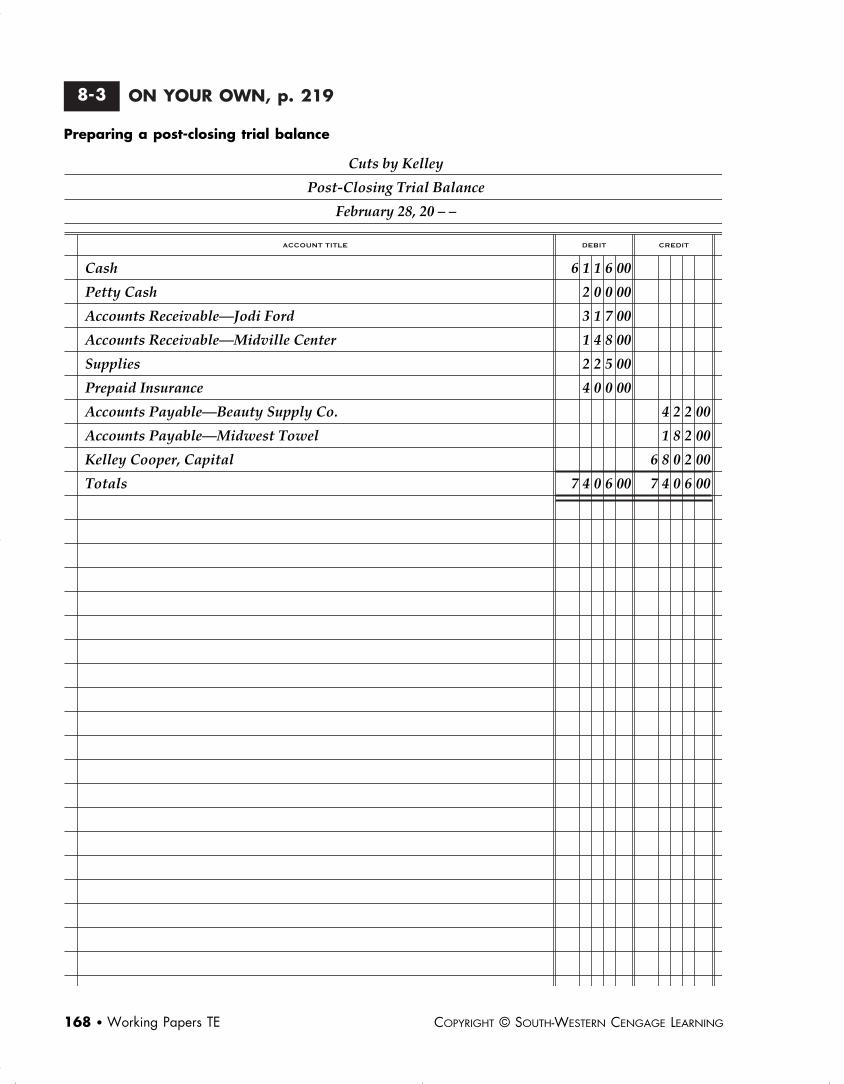

ON YOUR OWN, p. 2198-3

Preparing a post-closing trial balance

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING168 • Working Papers TE

Cash

Petty Cash

Accounts Receivable—Jodi Ford

Accounts Receivable—Midville Center

Supplies

Prepaid Insurance

Accounts Payable—Beauty Supply Co.

Accounts Payable—Midwest Towel

Kelley Cooper, Capital

Totals

Cuts by Kelley

Post-Closing Trial Balance

February 28, 20 – –

CREDITDEBITACCOUNT TITLE

6 1 1 6 00

2 0 0 00

3 1 7 00

1 4 8 00

2 2 5 00

4 0 0 00

7 4 0 6 00

4 2 2 00

1 8 2 00

6 8 0 2 00

7 4 0 6 00

BTE_Ch08-157-184.qxd 10/29/07 5:30 PM Page 168 SECOND REVISED

Name Date Class

Chapter 8 Recording Adjusting and Closing Entries for a Service Business • 169

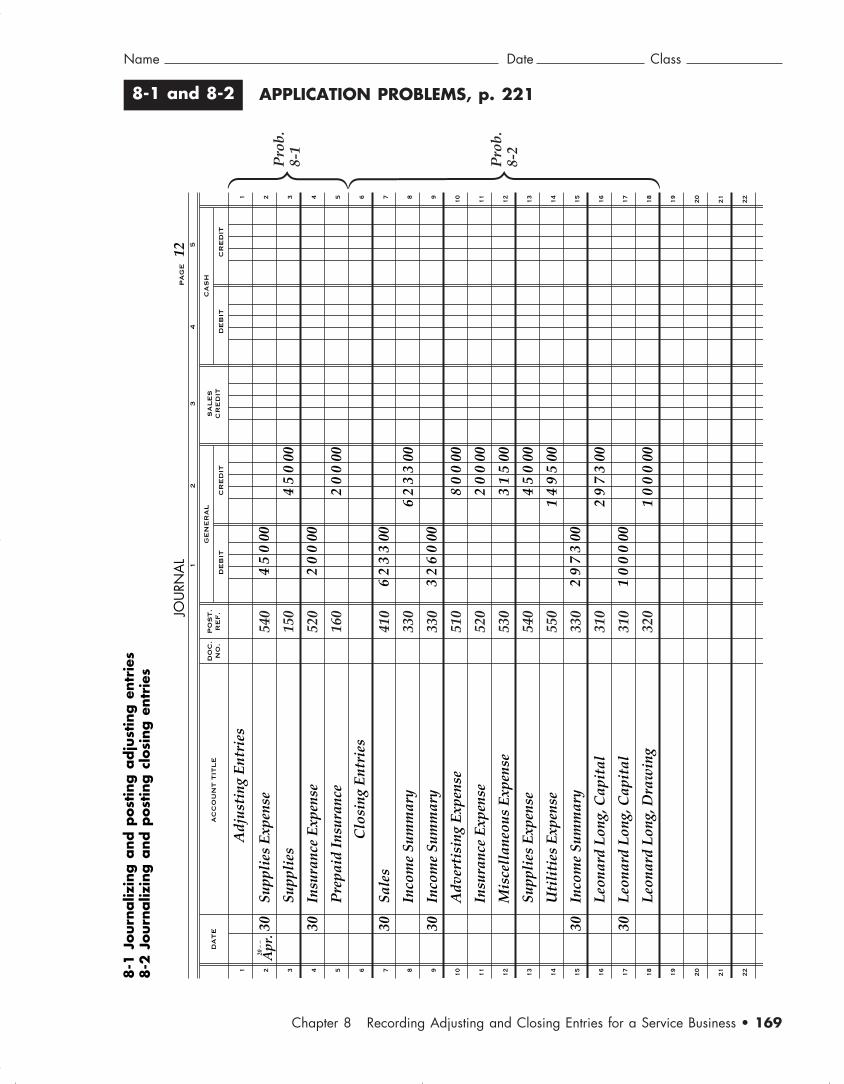

APPLICATION PROBLEMS, p. 2218-1 and 8-2

8-1

Journ

aliz

ing a

nd p

ost

ing a

dju

stin

g e

ntr

ies

8-2

Journ

aliz

ing a

nd p

ost

ing c

losi

ng e

ntr

ies

Apr

.

JOU

RNA

LP

AG

E

12

34

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22

DA

TE

AC

CO

UN

T T

ITL

E

DO

C.

NO

.P

OS

T.

RE

F.

GE

NE

RA

L

DE

BIT

CR

ED

IT

SA

LE

SC

RE

DIT

CA

SH

DE

BIT

CR

ED

IT

5

12

20 –

–30 30 30 30 30 30

Supp

lies

Exp

ense

Supp

lies

Insu

ranc

e E

xpen

se

Pre

paid

Ins

uran

ce

Sale

s

Inco

me

Sum

mar

y

Inco

me

Sum

mar

y

Adv

erti

sing

Exp

ense

Insu

ranc

e E

xpen

se

Mis

cell

aneo

us E

xpen

se

Supp

lies

Exp

ense

Uti

liti

es E

xpen

se

Inco

me

Sum

mar

y

Leo

nard

Lon

g, C

apit

al

Leo

nard

Lon

g, C

apit

al

Leo

nard

Lon

g, D

raw

ing

45

000

20

000

62

33

00

80

000

20

000

31

500

45

000

14

95

00

29

73

00

10

00

00

45

000

20

000

62

33

00

32

60

00

29

73

00

10

00

00

Adj

usti

ng E

ntri

es

Clo

sing

Ent

ries

540

150

520

160

410

330

330

510

520

530

540

550

330

310

310

320

Pro

b.8-

1

Pro

b.8-

2

BTE_Ch08-157-184.qxd 10/29/07 5:30 PM Page 169 SECOND REVISED

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING170 • Working Papers TE

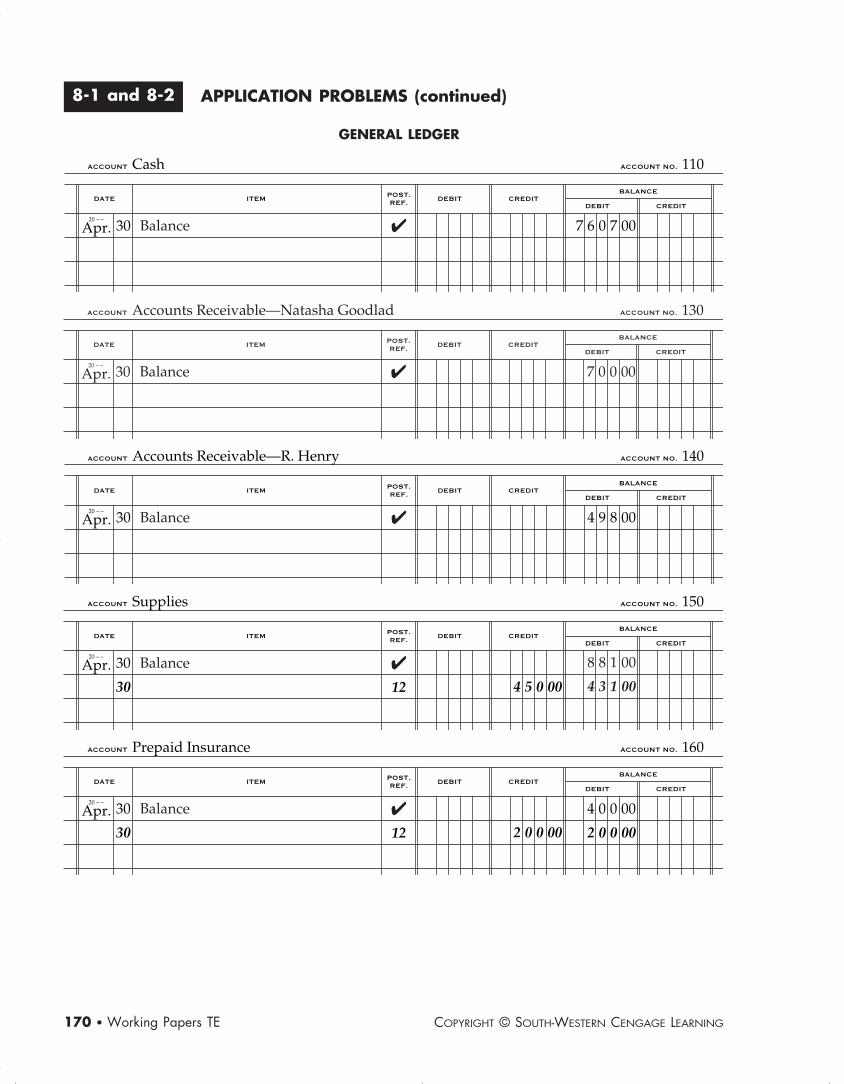

GENERAL LEDGER

APPLICATION PROBLEMS (continued)8-1 and 8-2

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

110Cash

Apr.20 – –

30 7 6 0 7 00Balance ✔

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

130Accounts Receivable—Natasha Goodlad

Apr.20 – –

30 7 0 0 00Balance ✔

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

140Accounts Receivable—R. Henry

Apr.20 – –

30 4 9 8 00Balance ✔

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

150Supplies

Apr.20 – –

30

30 4 5 0 00

Balance ✔

12

8 8 1 00

4 3 1 00

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

160Prepaid Insurance

Apr.20 – –

30

30 2 0 0 00

4 0 0 00

2 0 0 00

Balance ✔

12

BTE_Ch08-157-184.qxd 10/29/07 5:30 PM Page 170 SECOND REVISED

Name Date Class

Chapter 8 Recording Adjusting and Closing Entries for a Service Business • 171

GENERAL LEDGER

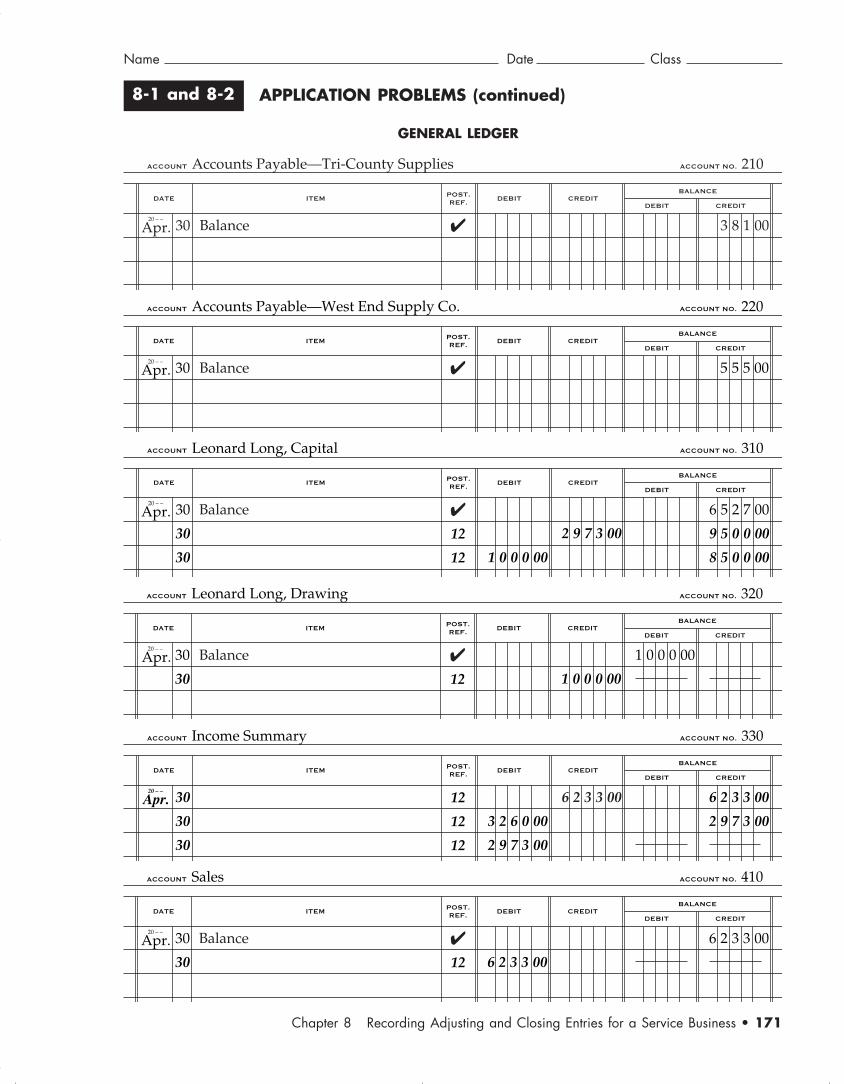

APPLICATION PROBLEMS (continued)8-1 and 8-2

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

210Accounts Payable—Tri-County Supplies

Apr.20 – –

30 Balance ✔ 3 8 1 00

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

220Accounts Payable—West End Supply Co.

Apr.20 – –

30 Balance ✔ 5 5 5 00

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

310Leonard Long, Capital

Apr.20 – –

30

30

30 1 0 0 0 00

2 9 7 3 00

Balance ✔

12

12

6 5 2 7 00

9 5 0 0 00

8 5 0 0 00

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

320Leonard Long, Drawing

Apr.20 – –

30

30 1 0 0 0 00

1 0 0 0 00Balance ✔

12

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

330Income Summary

Apr.20 – –

30

30

30

3 2 6 0 00

2 9 7 3 00

12

12

12

6 2 3 3 00

2 9 7 3 00

6 2 3 3 00

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

410Sales

Apr.20 – –

30

30 6 2 3 3 00

Balance ✔

12

6 2 3 3 00

BTE_Ch08-157-184.qxd 10/29/07 5:30 PM Page 171 SECOND REVISED

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING172 • Working Papers TE

GENERAL LEDGER

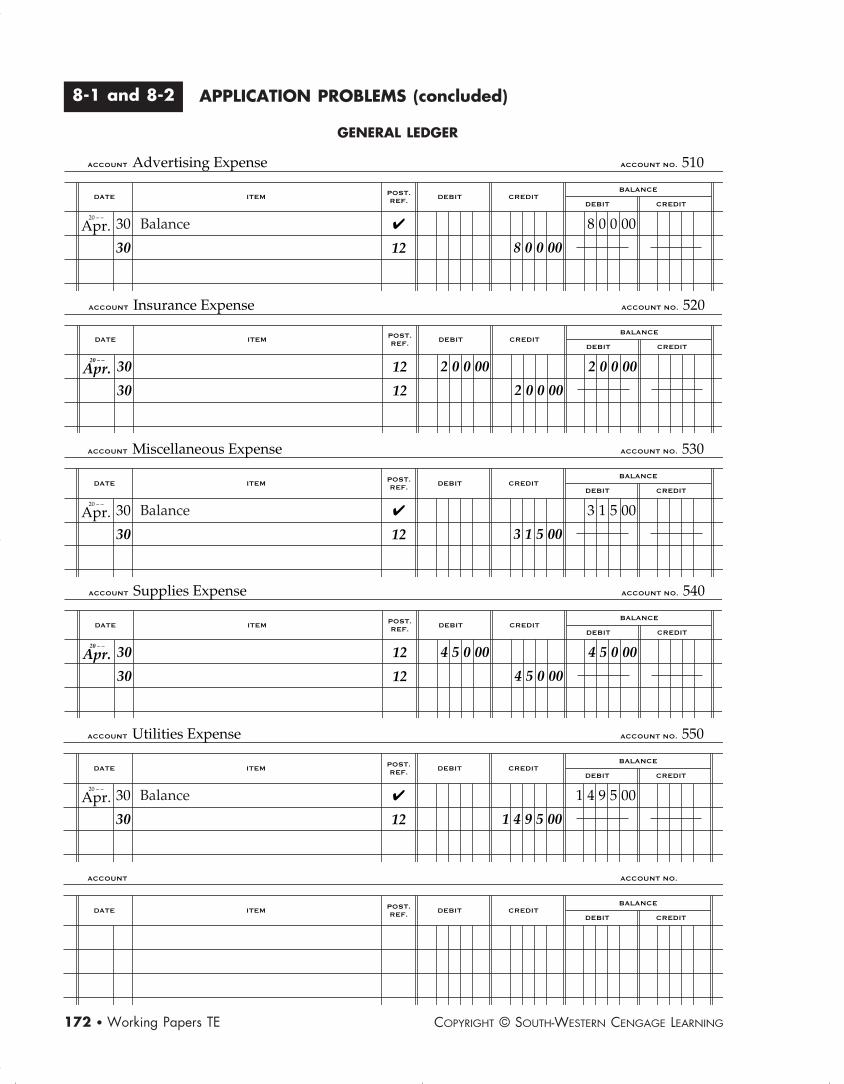

APPLICATION PROBLEMS (concluded)8-1 and 8-2

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

510Advertising Expense

Apr.20 – –

30

30 8 0 0 00

8 0 0 00✔

12

Balance

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

520Insurance Expense

Apr.20 – –

30

30

2 0 0 00

2 0 0 00

2 0 0 0012

12

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

530Miscellaneous Expense

Apr.20 – –

30

30 3 1 5 00

3 1 5 00✔

12

Balance

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

540Supplies Expense

Apr.20 – –

30

30

4 5 0 00

4 5 0 00

4 5 0 0012

12

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

550Utilities Expense

Apr.20 – –

30

30 1 4 9 5 00

1 4 9 5 00✔

12

Balance

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

BTE_Ch08-157-184.qxd 10/29/07 5:30 PM Page 172 SECOND REVISED

Name Date Class

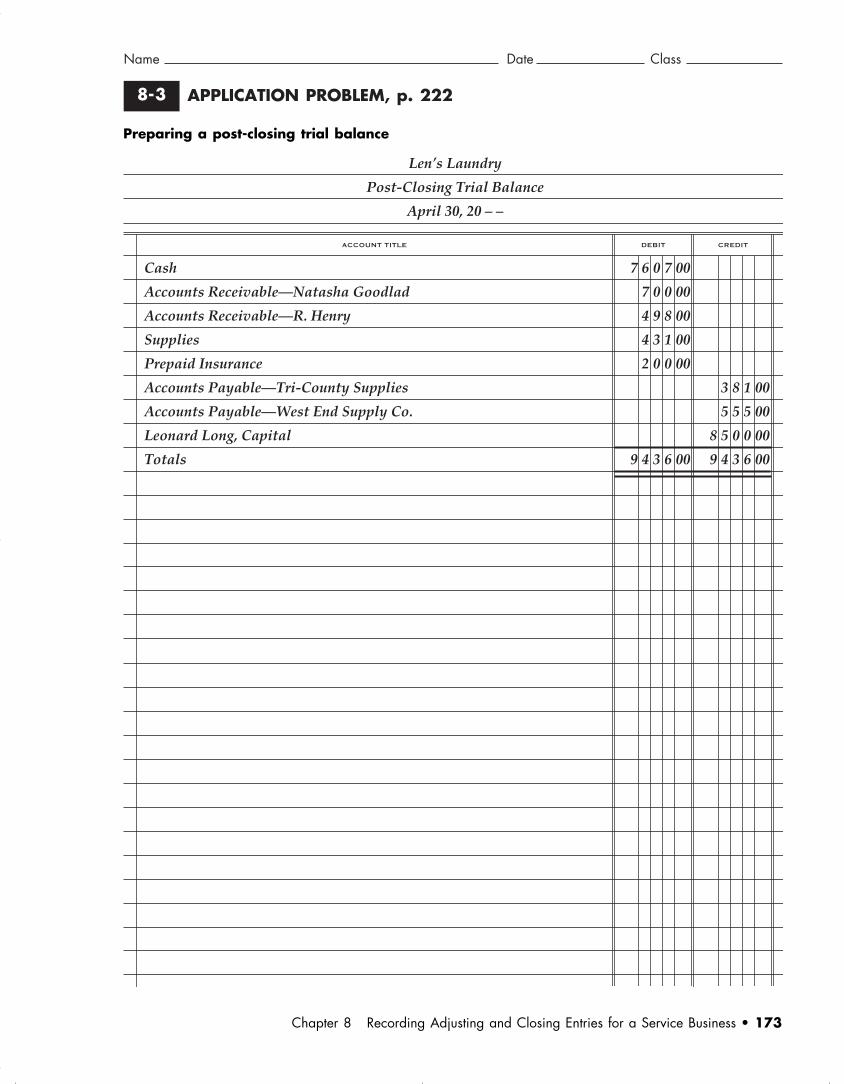

APPLICATION PROBLEM, p. 2228-3

Preparing a post-closing trial balance

Chapter 8 Recording Adjusting and Closing Entries for a Service Business • 173

Cash

Accounts Receivable—Natasha Goodlad

Accounts Receivable—R. Henry

Supplies

Prepaid Insurance

Accounts Payable—Tri-County Supplies

Accounts Payable—West End Supply Co.

Leonard Long, Capital

Totals

Len’s Laundry

Post-Closing Trial Balance

April 30, 20 – –

CREDITDEBITACCOUNT TITLE

7 6 0 7 00

7 0 0 00

4 9 8 00

4 3 1 00

2 0 0 00

9 4 3 6 00

3 8 1 00

5 5 5 00

8 5 0 0 00

9 4 3 6 00

BTE_Ch08-157-184.qxd 10/29/07 5:30 PM Page 173 SECOND REVISED

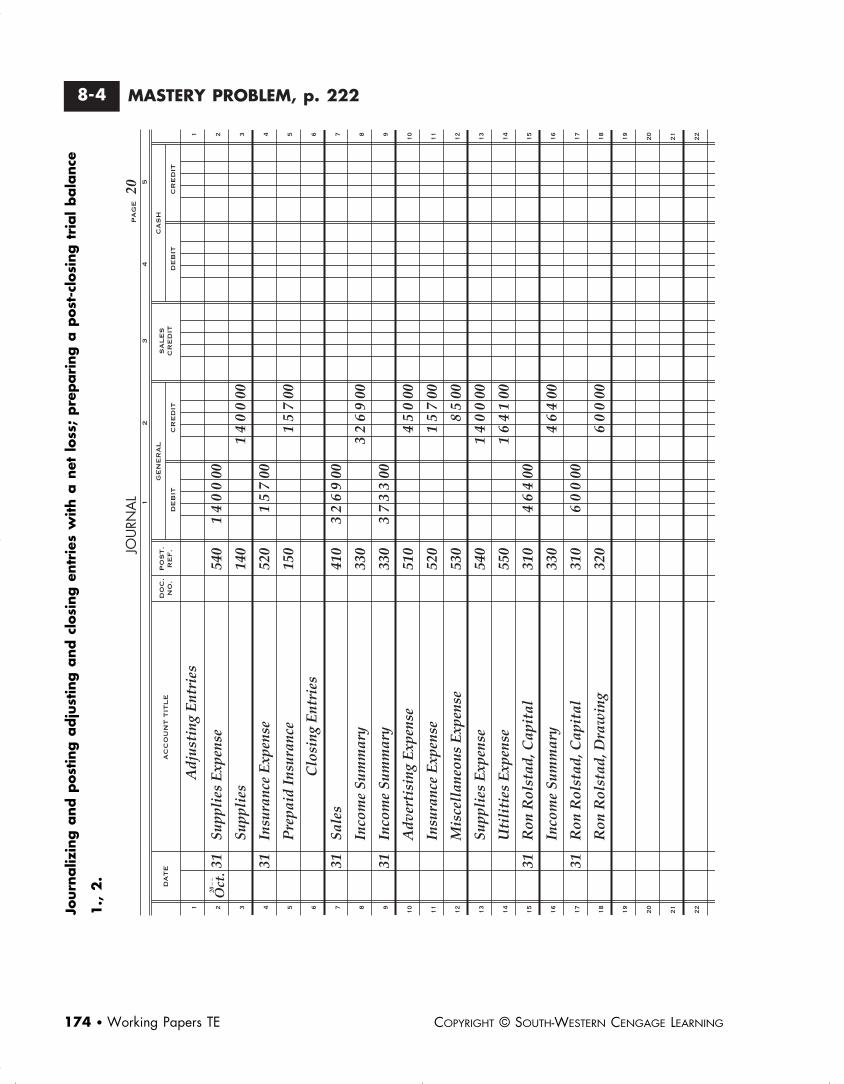

MASTERY PROBLEM, p. 2228-4

Journ

aliz

ing a

nd p

ost

ing a

dju

stin

g a

nd c

losi

ng e

ntr

ies

with

a n

et l

oss

; pre

pari

ng a

post

-clo

sing t

rial

bala

nce

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING174 • Working Papers TE

1., 2

.

JOU

RNA

LP

AG

E

12

34

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22

DA

TE

AC

CO

UN

T T

ITL

E

DO

C.

NO

.P

OS

T.

RE

F.

GE

NE

RA

L

DE

BIT

CR

ED

IT

SA

LE

SC

RE

DIT

CA

SH

DE

BIT

CR

ED

IT

5

20

Oct

.20

– –

31 31 31 31 31 31

Supp

lies

Exp

ense

Supp

lies

Insu

ranc

e E

xpen

se

Pre

paid

Ins

uran

ce

Sale

s

Inco

me

Sum

mar

y

Inco

me

Sum

mar

y

Adv

erti

sing

Exp

ense

Insu

ranc

e E

xpen

se

Mis

cell

aneo

us E

xpen

se

Supp

lies

Exp

ense

Uti

liti

es E

xpen

se

Ron

Rol

stad

, Cap

ital

Inco

me

Sum

mar

y

Ron

Rol

stad

, Cap

ital

Ron

Rol

stad

, Dra

win

g

14

00

00

15

700

32

69

00

45

000

15

700

85

00

14

00

00

16

41

00

46

400

60

000

14

00

00

15

700

32

69

00

37

33

00

46

400

60

000

Adj

usti

ng E

ntri

es

Clo

sing

Ent

ries

540

140

520

150

410

330

330

510

520

530

540

550

310

330

310

320

BTE_Ch08-157-184.qxd 10/29/07 5:30 PM Page 174 SECOND REVISED

Name Date Class

Chapter 8 Recording Adjusting and Closing Entries for a Service Business • 175

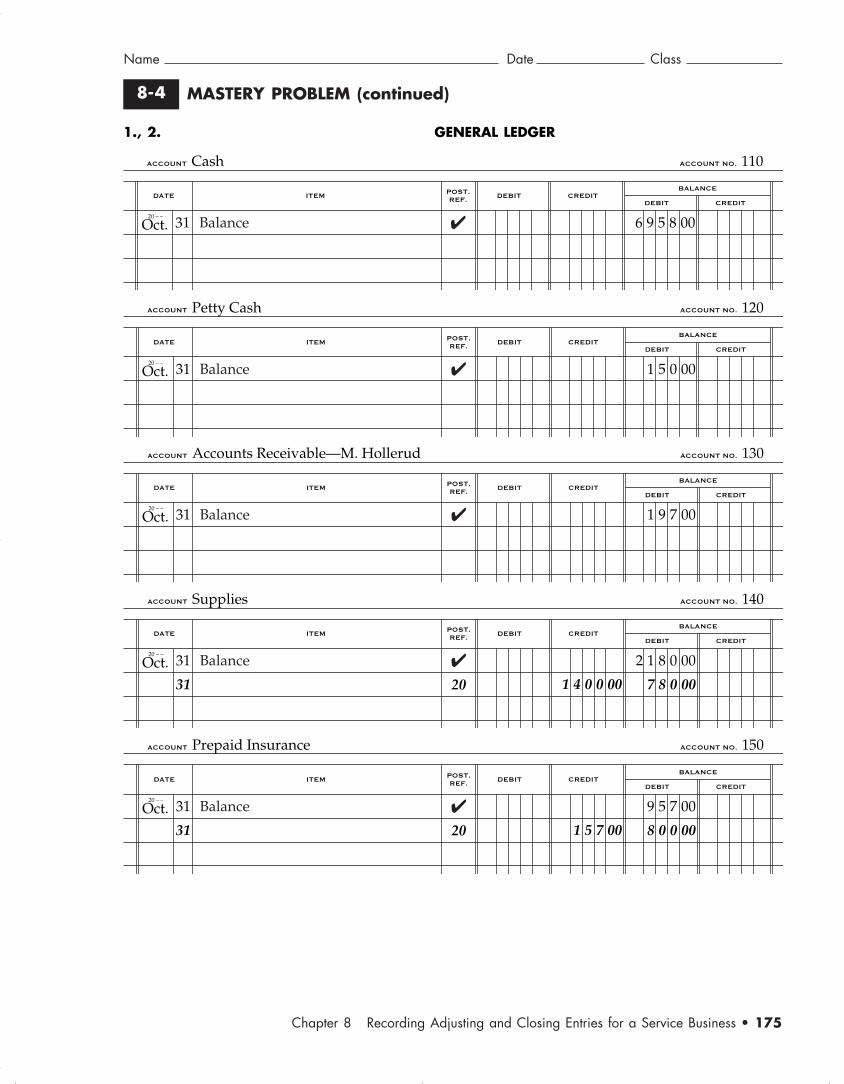

MASTERY PROBLEM (continued)8-4

1., 2. GENERAL LEDGER

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

110Cash

Oct.20 – –

31 6 9 5 8 00Balance ✔

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

120Petty Cash

Oct.20 – –

31 1 5 0 00Balance ✔

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

130Accounts Receivable—M. Hollerud

Oct.20 – –

31 1 9 7 00Balance ✔

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

140Supplies

Oct.20 – –

31

31 1 4 0 0 00

2 1 8 0 00

7 8 0 00

Balance ✔

20

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

150Prepaid Insurance

Oct.20 – –

31

31 1 5 7 00

9 5 7 00

8 0 0 00

Balance ✔

20

BTE_Ch08-157-184.qxd 10/29/07 5:30 PM Page 175 SECOND REVISED

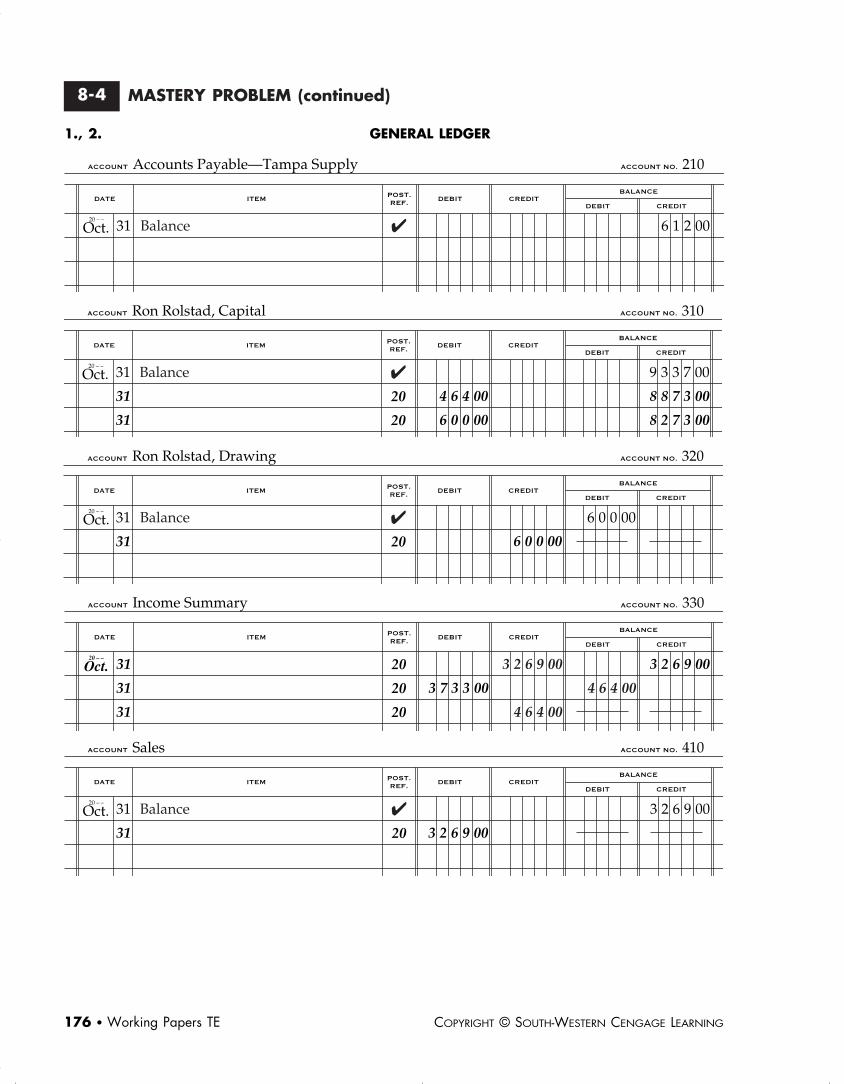

MASTERY PROBLEM (continued)8-4

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING176 • Working Papers TE

1., 2. GENERAL LEDGER

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

210Accounts Payable—Tampa Supply

Oct.20 – –

31 Balance ✔ 6 1 2 00

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

310Ron Rolstad, Capital

Oct.20 – –

31

31

31

4 6 4 00

6 0 0 00

Balance ✔

20

20

9 3 3 7 00

8 8 7 3 00

8 2 7 3 00

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

320Ron Rolstad, Drawing

Oct.20 – –

31

31 6 0 0 00

6 0 0 00Balance ✔

20

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

330Income Summary

Oct.20 – –

31

31

31

3 7 3 3 00 4 6 4 00

20

20

20

3 2 6 9 003 2 6 9 00

4 6 4 00

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

410Sales

Oct.20 – –

31

31 3 2 6 9 00

Balance ✔

20

3 2 6 9 00

BTE_Ch08-157-184.qxd 10/29/07 5:30 PM Page 176 SECOND REVISED

Name Date Class

Chapter 8 Recording Adjusting and Closing Entries for a Service Business • 177

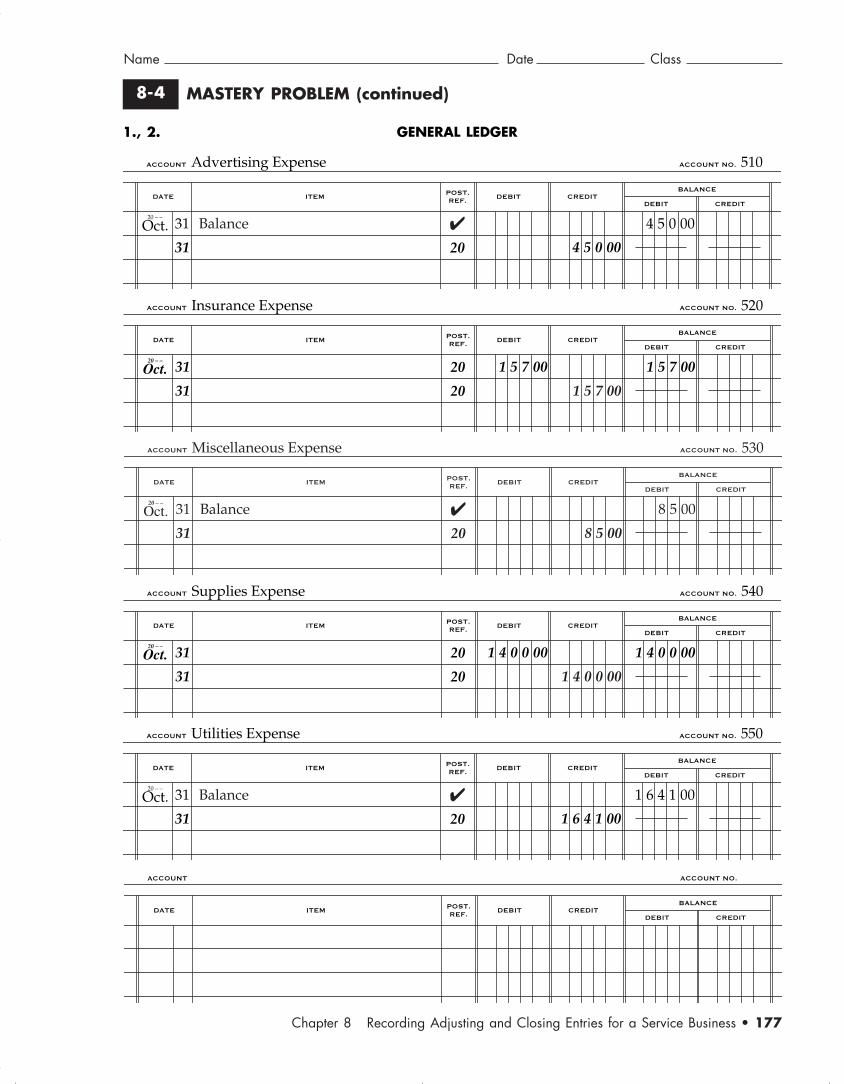

MASTERY PROBLEM (continued)8-4

1., 2. GENERAL LEDGER

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

510Advertising Expense

Oct.20 – –

31

31 4 5 0 00

4 5 0 00Balance ✔

20

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

520Insurance Expense

Oct.20 – –

31

31

1 5 7 00 1 5 7 0020

20 1 5 7 00

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

530Miscellaneous Expense

Oct.20 – –

31

31

8 5 00Balance ✔

20 8 5 00

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

540Supplies Expense

Oct.20 – –

31

31

1 4 0 0 00 1 4 0 0 0020

20 1 4 0 0 00

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

550Utilities Expense

Oct.20 – –

31

31 1 6 4 1 00

1 6 4 1 00Balance ✔

20

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

BTE_Ch08-157-184.qxd 10/29/07 5:30 PM Page 177 SECOND REVISED

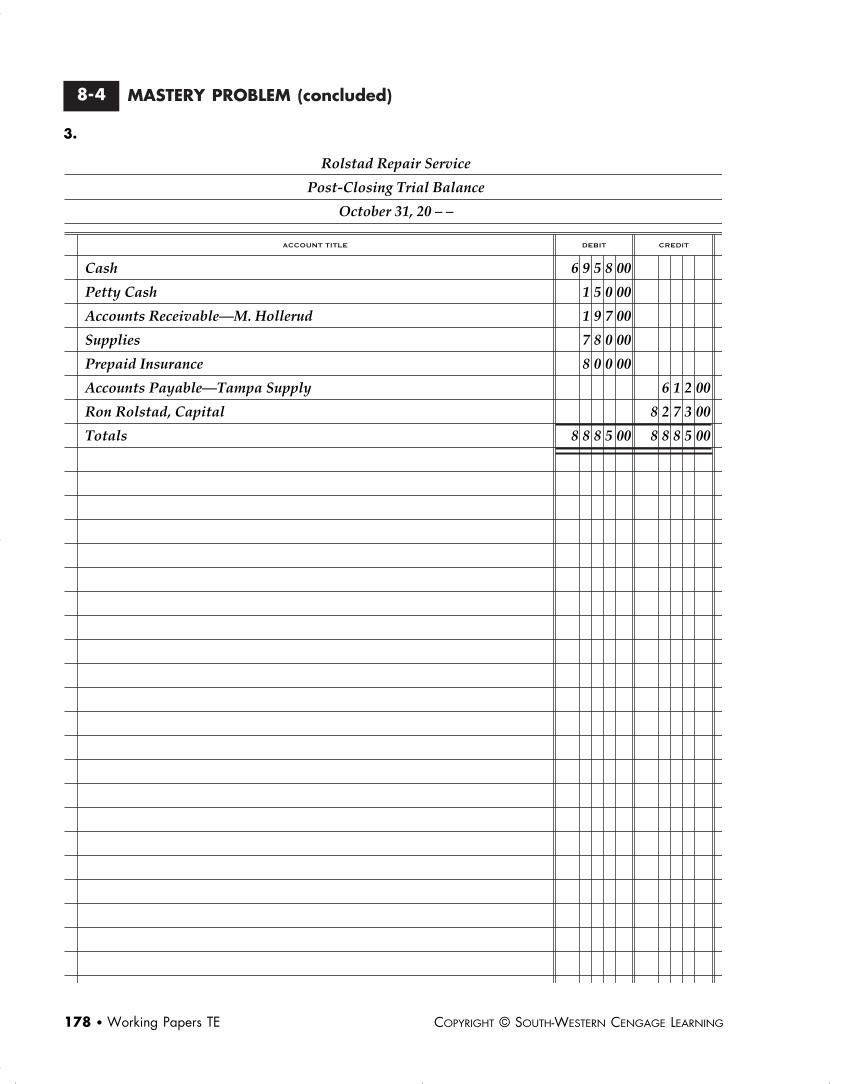

MASTERY PROBLEM (concluded)8-4

3.

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING178 • Working Papers TE

Cash

Petty Cash

Accounts Receivable—M. Hollerud

Supplies

Prepaid Insurance

Accounts Payable—Tampa Supply

Ron Rolstad, Capital

Totals

Rolstad Repair Service

Post-Closing Trial Balance

October 31, 20 – –

CREDITDEBITACCOUNT TITLE

6 9 5 8 00

1 5 0 00

1 9 7 00

7 8 0 00

8 0 0 00

8 8 8 5 00

6 1 2 00

8 2 7 3 00

8 8 8 5 00

BTE_Ch08-157-184.qxd 10/29/07 5:30 PM Page 178 SECOND REVISED

Name Date Class

Chapter 8 Recording Adjusting and Closing Entries for a Service Business • 179

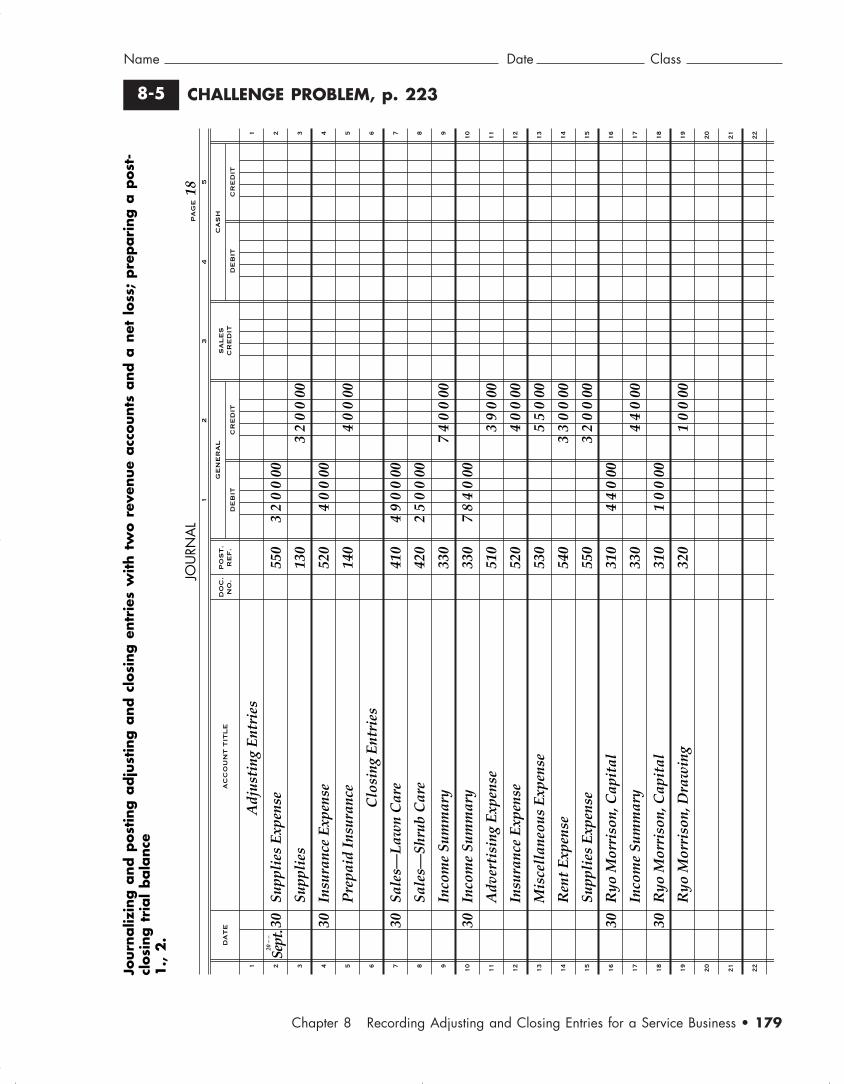

CHALLENGE PROBLEM, p. 2238-5

Journ

aliz

ing a

nd p

ost

ing a

dju

stin

g a

nd c

losi

ng e

ntr

ies

with t

wo r

even

ue

acc

ounts

and a

net

loss

; pre

pari

ng a

post

-cl

osi

ng t

rial

bala

nce

1., 2

.

JOU

RNA

LP

AG

E18

12

34

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22

DA

TE

AC

CO

UN

T T

ITL

E

DO

C.

NO

.P

OS

T.

RE

F.

GE

NE

RA

L

DE

BIT

CR

ED

IT

SA

LE

SC

RE

DIT

20 –

–

CA

SH

DE

BIT

CR

ED

IT

5

Sept

.30 30 30 30 30 30

Adj

usti

ng E

ntri

es

Supp

lies

Exp

ense

Supp

lies

Insu

ranc

e E

xpen

se

Pre

paid

Ins

uran

ce

Clo

sing

Ent

ries

Sale

s—L

awn

Car

e

Sale

s—Sh

rub

Car

e

Inco

me

Sum

mar

y

Inco

me

Sum

mar

y

Adv

erti

sing

Exp

ense

Insu

ranc

e E

xpen

se

Mis

cell

aneo

us E

xpen

se

Ren

t E

xpen

se

Supp

lies

Exp

ense

Ryo

Mor

riso

n, C

apit

al

Inco

me

Sum

mar

y

Ryo

Mor

riso

n, C

apit

al

Ryo

Mor

riso

n, D

raw

ing

32

00

00

40

000

49

00

00

25

00

00

78

40

00

44

000

10

000

32

00

00

40

000

74

00

00

39

000

40

000

55

000

33

00

00

32

00

00

44

000

10

000

550

130

520

140

410

420

330

330

510

520

530

540

550

310

330

310

320

BTE_Ch08-157-184.qxd 10/29/07 5:30 PM Page 179 SECOND REVISED

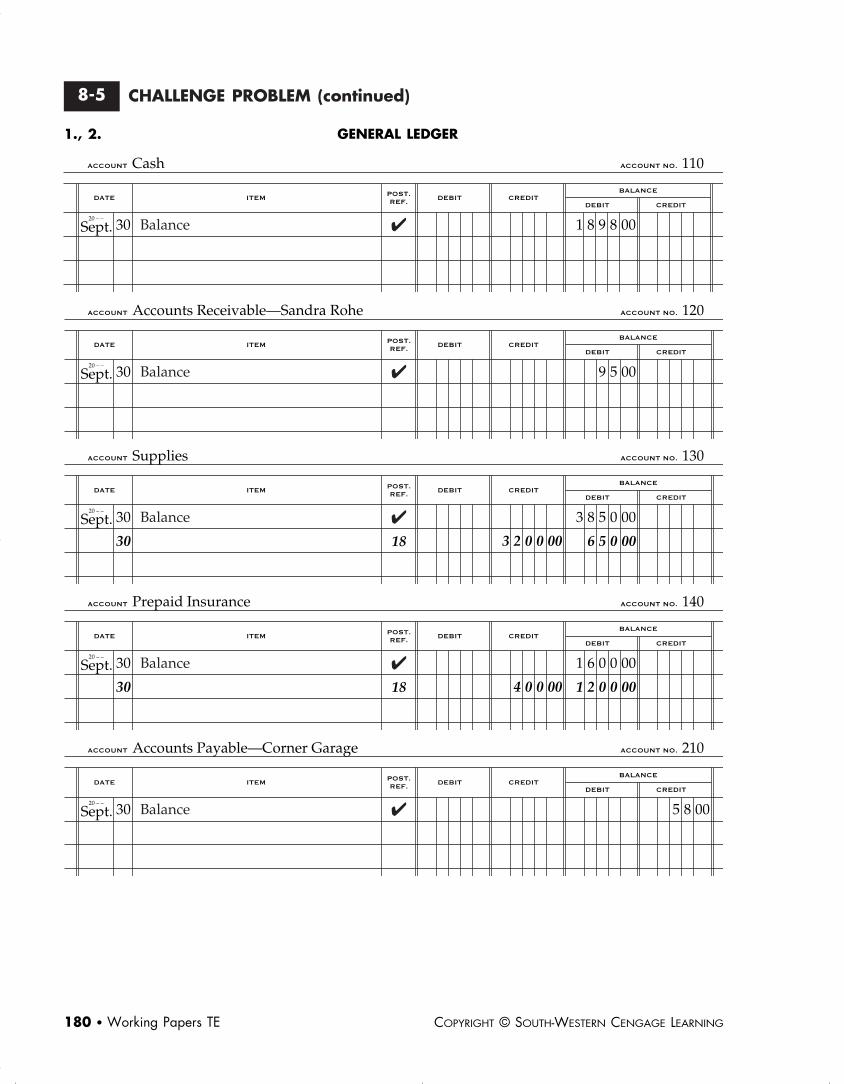

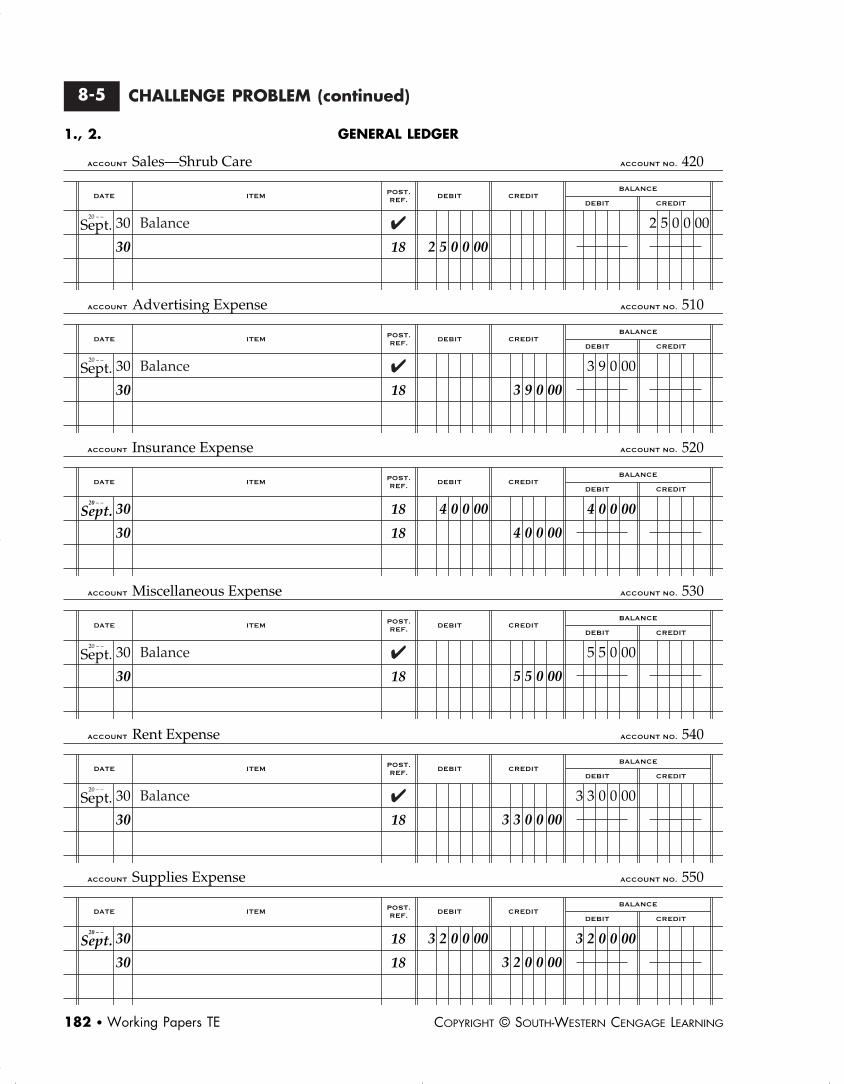

CHALLENGE PROBLEM (continued)8-5

1., 2.

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING180 • Working Papers TE

GENERAL LEDGER

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

110Cash

Sept.20 – –

30 1 8 9 8 00Balance ✔

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

120Accounts Receivable—Sandra Rohe

Sept.20 – –

30 9 5 00Balance ✔

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

130Supplies

Sept.20 – –

30

30 3 2 0 0 00

3 8 5 0 00

6 5 0 00

Balance ✔

18

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

140Prepaid Insurance

Sept.20 – –

30

30 4 0 0 00

1 6 0 0 00

1 2 0 0 00

Balance ✔

18

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

210Accounts Payable—Corner Garage

Sept.20 – –

30 5 8 00Balance ✔

BTE_Ch08-157-184.qxd 10/29/07 5:30 PM Page 180 SECOND REVISED

Name Date Class

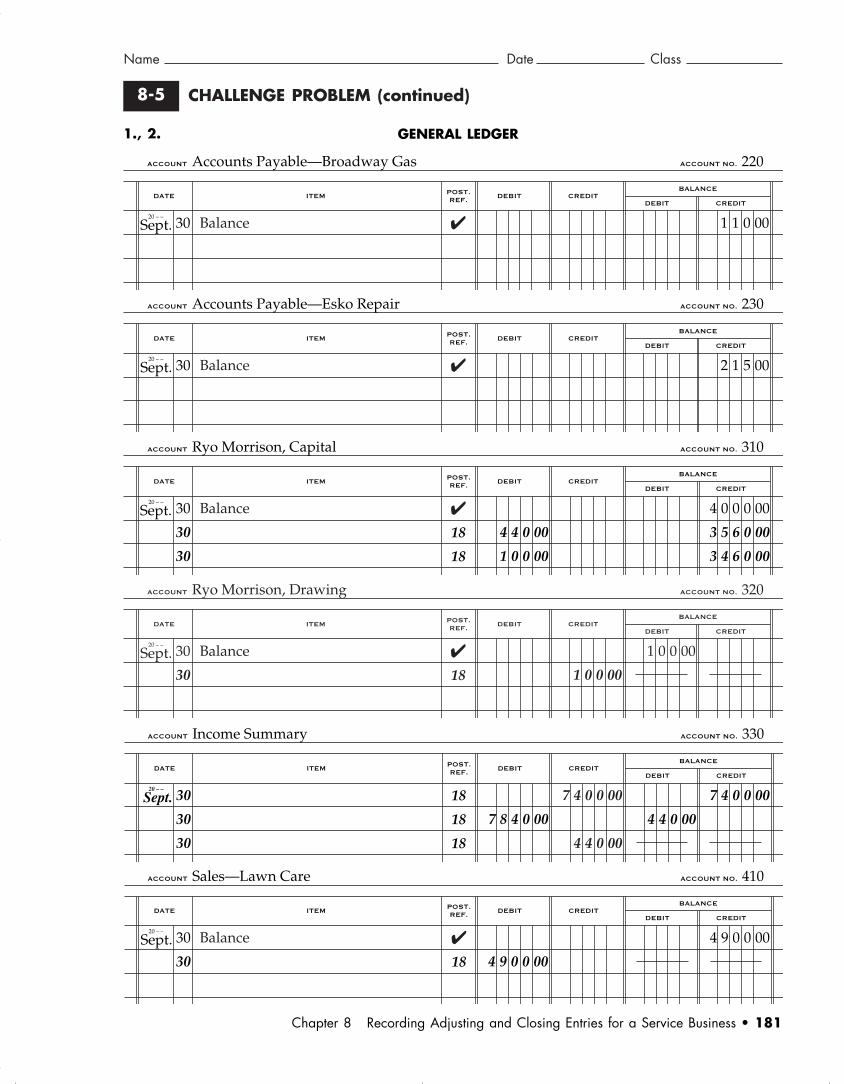

CHALLENGE PROBLEM (continued)8-5

1., 2.

Chapter 8 Recording Adjusting and Closing Entries for a Service Business • 181

GENERAL LEDGER

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

220Accounts Payable—Broadway Gas

Sept.20 – –

30 Balance ✔ 1 1 0 00

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

230Accounts Payable—Esko Repair

Sept.20 – –

30 Balance ✔ 2 1 5 00

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

310Ryo Morrison, Capital

Sept.20 – –

30

30

30

4 4 0 00

1 0 0 00

Balance ✔

18

18

4 0 0 0 00

3 5 6 0 00

3 4 6 0 00

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

320Ryo Morrison, Drawing

Sept.20 – –

30

30 1 0 0 00

1 0 0 00Balance ✔

18

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

330Income Summary

Sept.20 – –

30

30

30

7 8 4 0 00 4 4 0 00

18

18

18

7 4 0 0 007 4 0 0 00

4 4 0 00

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

410Sales—Lawn Care

Sept.20 – –

30

30 4 9 0 0 00

Balance ✔

18

4 9 0 0 00

BTE_Ch08-157-184.qxd 10/29/07 5:30 PM Page 181 SECOND REVISED

CHALLENGE PROBLEM (continued)8-5

1., 2.

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING182 • Working Papers TE

GENERAL LEDGER

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

420Sales—Shrub Care

Sept.20 – –

30

30 2 5 0 0 00

Balance ✔

18

2 5 0 0 00

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

510Advertising Expense

Sept.20 – –

30

30 3 9 0 00

3 9 0 00Balance ✔

18

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

520Insurance Expense

Sept.20 – –

30

30

4 0 0 00

4 0 0 00

4 0 0 0018

18

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

530Miscellaneous Expense

Sept.20 – –

30

30 5 5 0 00

5 5 0 00Balance ✔

18

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

540Rent Expense

Sept.20 – –

30

30 3 3 0 0 00

3 3 0 0 00Balance ✔

18

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

550Supplies Expense

Sept.20 – –

30

30

3 2 0 0 00

3 2 0 0 00

3 2 0 0 0018

18

BTE_Ch08-157-184.qxd 10/29/07 5:30 PM Page 182 SECOND REVISED

Name Date Class

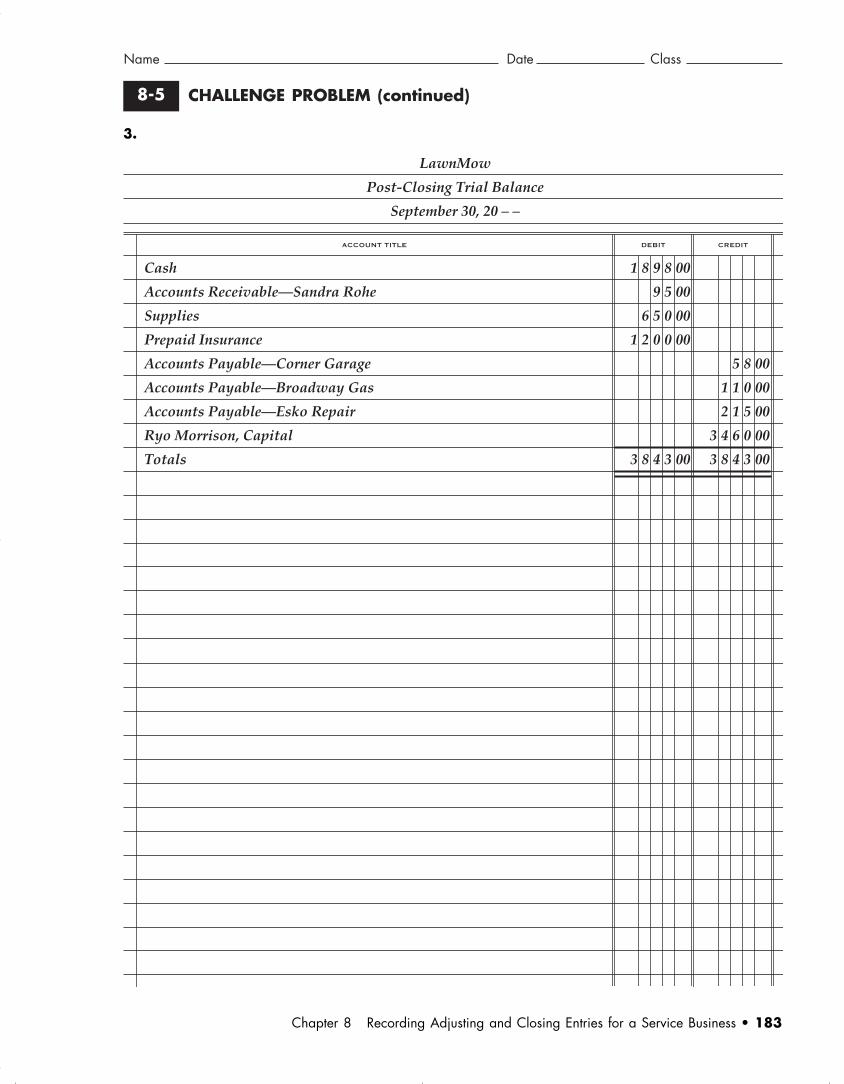

CHALLENGE PROBLEM (continued)8-5

3.

Chapter 8 Recording Adjusting and Closing Entries for a Service Business • 183

Cash

Accounts Receivable—Sandra Rohe

Supplies

Prepaid Insurance

Accounts Payable—Corner Garage

Accounts Payable—Broadway Gas

Accounts Payable—Esko Repair

Ryo Morrison, Capital

Totals

LawnMow

Post-Closing Trial Balance

September 30, 20 – –

CREDITDEBITACCOUNT TITLE

1 8 9 8 00

9 5 00

6 5 0 00

1 2 0 0 00

3 8 4 3 00

5 8 00

1 1 0 00

2 1 5 00

3 4 6 0 00

3 8 4 3 00

BTE_Ch08-157-184.qxd 10/29/07 5:30 PM Page 183 SECOND REVISED

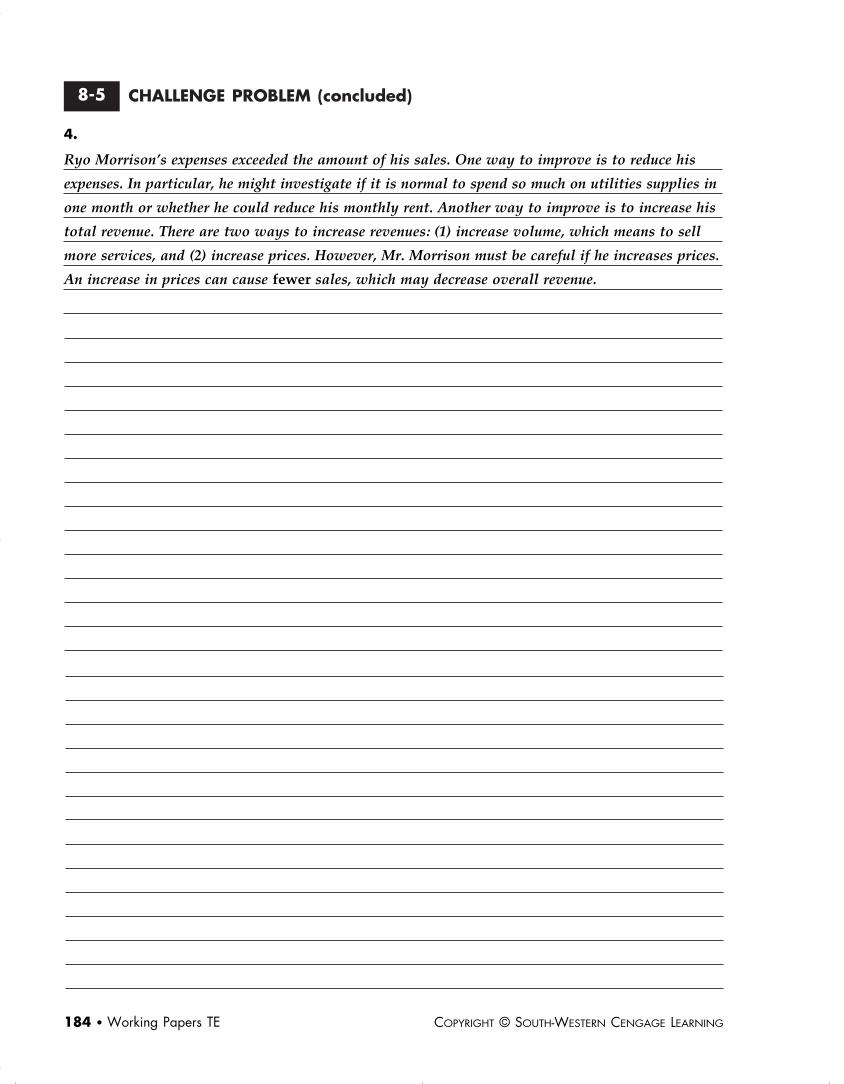

CHALLENGE PROBLEM (concluded)8-5

4.

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING184 • Working Papers TE

Ryo Morrison’s expenses exceeded the amount of his sales. One way to improve is to reduce his

expenses. In particular, he might investigate if it is normal to spend so much on utilities supplies in

one month or whether he could reduce his monthly rent. Another way to improve is to increase his

total revenue. There are two ways to increase revenues: (1) increase volume, which means to sell

more services, and (2) increase prices. However, Mr. Morrison must be careful if he increases prices.

An increase in prices can cause fewer sales, which may decrease overall revenue.

BTE_Ch08-157-184.qxd 10/29/07 5:30 PM Page 184 SECOND REVISED