study of containerized shipping of soybean meal exports · 1. overview of u.s. soybean and soybean...

TRANSCRIPT

prepared for the Illinois Soybean Association

April 29, 2011

Study of Containerized Shipping of Soybean Meal Exports

Page 0

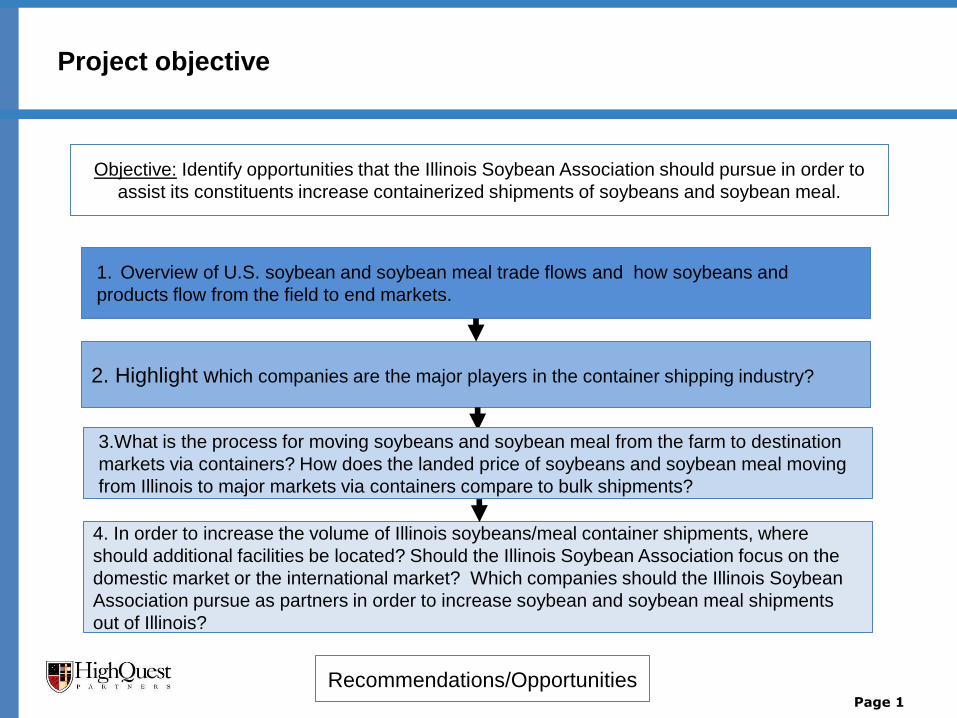

1. Overview of U.S. soybean and soybean meal trade flows and how soybeans and

products flow from the field to end markets.

2. Highlight which companies are the major players in the container shipping industry?

4. In order to increase the volume of Illinois soybeans/meal container shipments, where

should additional facilities be located? Should the Illinois Soybean Association focus on the

domestic market or the international market? Which companies should the Illinois Soybean

Association pursue as partners in order to increase soybean and soybean meal shipments

out of Illinois?

Project objective

Page 1

Objective: Identify opportunities that the Illinois Soybean Association should pursue in order to

assist its constituents increase containerized shipments of soybeans and soybean meal.

3.What is the process for moving soybeans and soybean meal from the farm to destination

markets via containers? How does the landed price of soybeans and soybean meal moving

from Illinois to major markets via containers compare to bulk shipments?

Recommendations/Opportunities

Table of contents

1. Executive Summary

2. Overview of U.S. and Illinois soybeans and soybean trade flows

3. Major players in the U.S. and Illinois container shipping industry

4. Landed price analysis of soybeans and soybean meal moving from

Illinois to major destination markets

4. Recommendations for increasing container movements of Illinois

soybeans and soybean meal

Page 2

Executive Summary - export outlook for containerized soybean and soybean meal shipments

• Asian demand for soybean and soybean meal is expected to increase substantially over the next

ten years as GDP per capita increases throughout the region resulting in consumers allocating a

greater portion of their incomes to consumption of animal protein and vegetable oil.

• At the same time, container shipping companies are expected to increase the number of containers

in production as well as their fleets in order to meet increased future demand for container

shipments.

• As the U.S. economy continues to improve, demand for containers in the Midwest is expected to

increase leading to improved availability of empty containers in the Chicago area that can be used

on the backhaul to Asia for shipping soybean and soybean meal.

• The completion of the Panama Canal project in 2014 is expected to result in an increase in

container shipments out of the Gulf, which shippers based in Illinois are ideally suited to take

advantage of given their access to the Mississippi, Illinois and Ohio Rivers.

• Illinois is well positioned to take advantage of these market dynamics due to its large soybean and

soybean meal production, the lack of local demand for protein meal which provides a strong

incentive to export to markets outside the state the proximity to Chicago, the largest container

market in the Midwest, to large soybean production areas.

Page 3

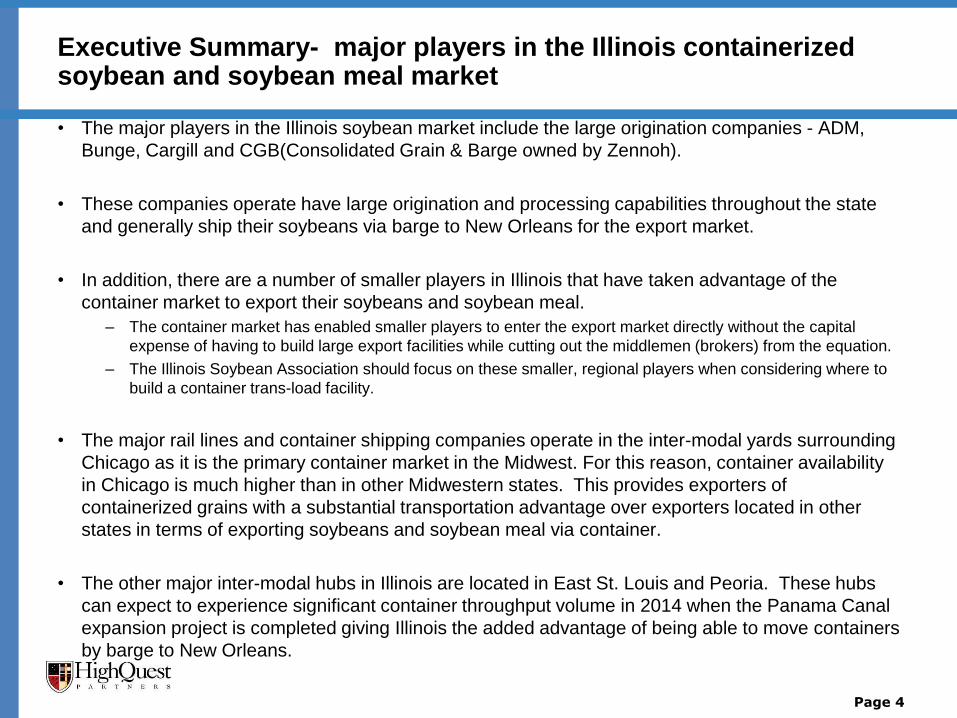

Executive Summary- major players in the Illinois containerized soybean and soybean meal market

• The major players in the Illinois soybean market include the large origination companies - ADM,

Bunge, Cargill and CGB(Consolidated Grain & Barge owned by Zennoh).

• These companies operate have large origination and processing capabilities throughout the state

and generally ship their soybeans via barge to New Orleans for the export market.

• In addition, there are a number of smaller players in Illinois that have taken advantage of the

container market to export their soybeans and soybean meal.

– The container market has enabled smaller players to enter the export market directly without the capital

expense of having to build large export facilities while cutting out the middlemen (brokers) from the equation.

– The Illinois Soybean Association should focus on these smaller, regional players when considering where to

build a container trans-load facility.

• The major rail lines and container shipping companies operate in the inter-modal yards surrounding

Chicago as it is the primary container market in the Midwest. For this reason, container availability

in Chicago is much higher than in other Midwestern states. This provides exporters of

containerized grains with a substantial transportation advantage over exporters located in other

states in terms of exporting soybeans and soybean meal via container.

• The other major inter-modal hubs in Illinois are located in East St. Louis and Peoria. These hubs

can expect to experience significant container throughput volume in 2014 when the Panama Canal

expansion project is completed giving Illinois the added advantage of being able to move containers

by barge to New Orleans.

Page 4

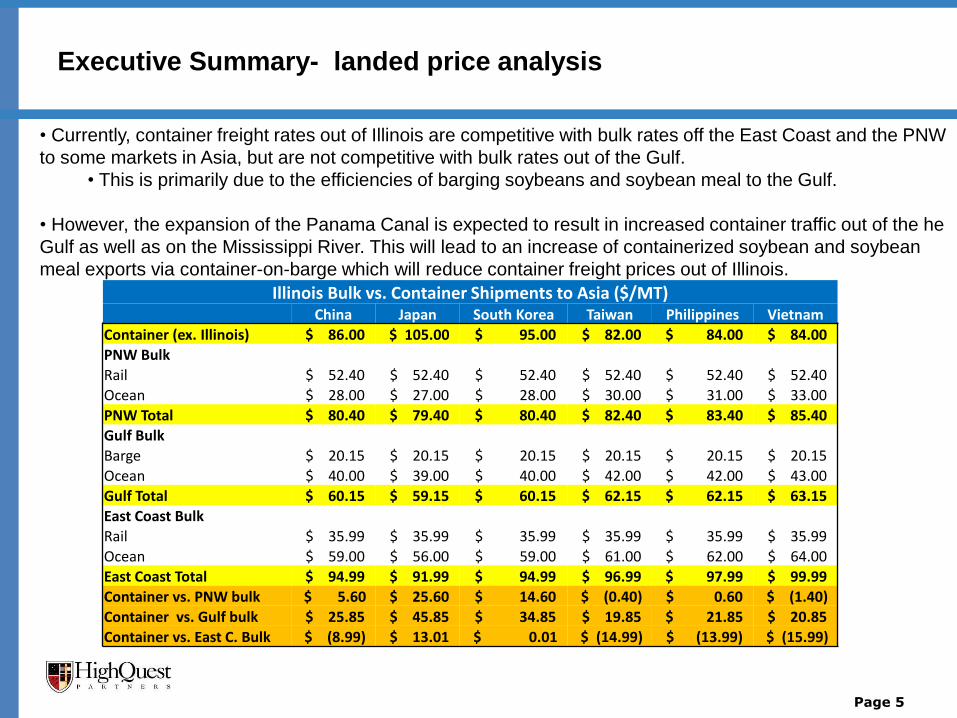

Executive Summary- landed price analysis

Page 5

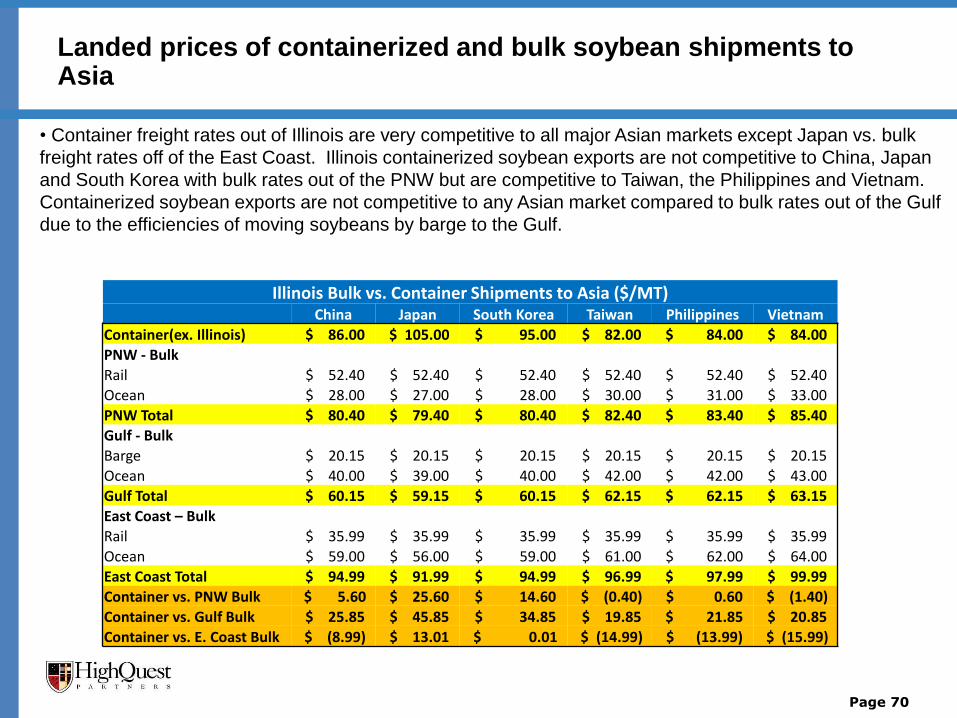

Illinois Bulk vs. Container Shipments to Asia ($/MT) China Japan South Korea Taiwan Philippines Vietnam

Container (ex. Illinois) $ 86.00 $ 105.00 $ 95.00 $ 82.00 $ 84.00 $ 84.00

PNW Bulk

Rail $ 52.40 $ 52.40 $ 52.40 $ 52.40 $ 52.40 $ 52.40

Ocean $ 28.00 $ 27.00 $ 28.00 $ 30.00 $ 31.00 $ 33.00

PNW Total $ 80.40 $ 79.40 $ 80.40 $ 82.40 $ 83.40 $ 85.40

Gulf Bulk

Barge $ 20.15 $ 20.15 $ 20.15 $ 20.15 $ 20.15 $ 20.15

Ocean $ 40.00 $ 39.00 $ 40.00 $ 42.00 $ 42.00 $ 43.00

Gulf Total $ 60.15 $ 59.15 $ 60.15 $ 62.15 $ 62.15 $ 63.15

East Coast Bulk

Rail $ 35.99 $ 35.99 $ 35.99 $ 35.99 $ 35.99 $ 35.99

Ocean $ 59.00 $ 56.00 $ 59.00 $ 61.00 $ 62.00 $ 64.00

East Coast Total $ 94.99 $ 91.99 $ 94.99 $ 96.99 $ 97.99 $ 99.99

Container vs. PNW bulk $ 5.60 $ 25.60 $ 14.60 $ (0.40) $ 0.60 $ (1.40)

Container vs. Gulf bulk $ 25.85 $ 45.85 $ 34.85 $ 19.85 $ 21.85 $ 20.85

Container vs. East C. Bulk $ (8.99) $ 13.01 $ 0.01 $ (14.99) $ (13.99) $ (15.99)

• Currently, container freight rates out of Illinois are competitive with bulk rates off the East Coast and the PNW

to some markets in Asia, but are not competitive with bulk rates out of the Gulf.

• This is primarily due to the efficiencies of barging soybeans and soybean meal to the Gulf.

• However, the expansion of the Panama Canal is expected to result in increased container traffic out of the he

Gulf as well as on the Mississippi River. This will lead to an increase of containerized soybean and soybean

meal exports via container-on-barge which will reduce container freight prices out of Illinois.

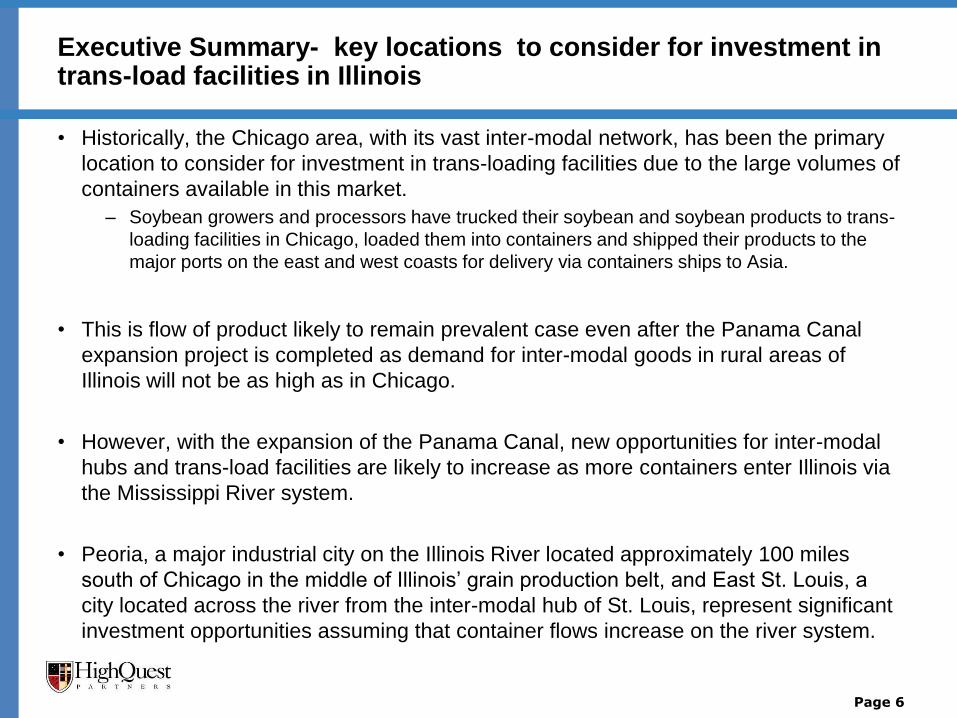

Executive Summary- key locations to consider for investment in trans-load facilities in Illinois

• Historically, the Chicago area, with its vast inter-modal network, has been the primary

location to consider for investment in trans-loading facilities due to the large volumes of

containers available in this market.

– Soybean growers and processors have trucked their soybean and soybean products to trans-

loading facilities in Chicago, loaded them into containers and shipped their products to the

major ports on the east and west coasts for delivery via containers ships to Asia.

• This is flow of product likely to remain prevalent case even after the Panama Canal

expansion project is completed as demand for inter-modal goods in rural areas of

Illinois will not be as high as in Chicago.

• However, with the expansion of the Panama Canal, new opportunities for inter-modal

hubs and trans-load facilities are likely to increase as more containers enter Illinois via

the Mississippi River system.

• Peoria, a major industrial city on the Illinois River located approximately 100 miles

south of Chicago in the middle of Illinois’ grain production belt, and East St. Louis, a

city located across the river from the inter-modal hub of St. Louis, represent significant

investment opportunities assuming that container flows increase on the river system.

Page 6

Executive Summary- SWOT analysis of investing in trans-loading facilities in Illinois

Page 7

Strengths Weaknesses

Easier access to smaller customers in foreign markets. Container prices dependent on availability, i.e. the level of trade activity in the U.S. and global economy.

Backhaul opportunities for containers returning to Asia leads to discounts, especially in markets located near major intermodal hubs such as Chicago and St. Louis.

Higher unit/ton cost and freight rates than bulk.

Lack of port infrastructure in Asia’s smaller markets makes it difficult to unload fully-loaded bulk vessels.

U.S. interior grain transportation infrastructure designed for bulk shipments.

Containers solve quality issues that some importers face with bulk vessels due to less water erosion and dust, etc.

U.S. grain export terminals intended for bulk shipments.

Allows smaller, more regional companies to enter export market without the capital cost of building export elevator.

Lack of major intermodal hubs in primary grain growing regions leads to higher cost to reposition containers in order to handle grain movements.

Major export markets (China, Taiwan, South Korea and Japan) are major container hubs in Asia.

Lack of drayage opportunities in major Midwest grain production markets.

Opportunities Threats

Panama Canal expansion leads to greater traffic of containers on the Mississippi River.

Further economic recession stunts demand for containerized imports of inter-modal goods from Asia to the U.S.

Possible trans-loader investment along the river system in industrial hubs such as Peoria and East St. Louis which are both located on major rail lines.

Continued boom in Intra-Asian trade leads to higher freight rates in Asia forcing container shippers to divert fleets from the Transpacific trade route.

Table of contents

1. Executive Summary

2. Overview of U.S. and Illinois soybeans and soybean trade flows

3. Major players in the U.S. and Illinois container shipping industry

4. Landed price analysis of soybeans and soybean meal moving from

Illinois to major destination markets

4. Recommendations for increasing container movements of Illinois

soybeans and soybean meal

Page 8

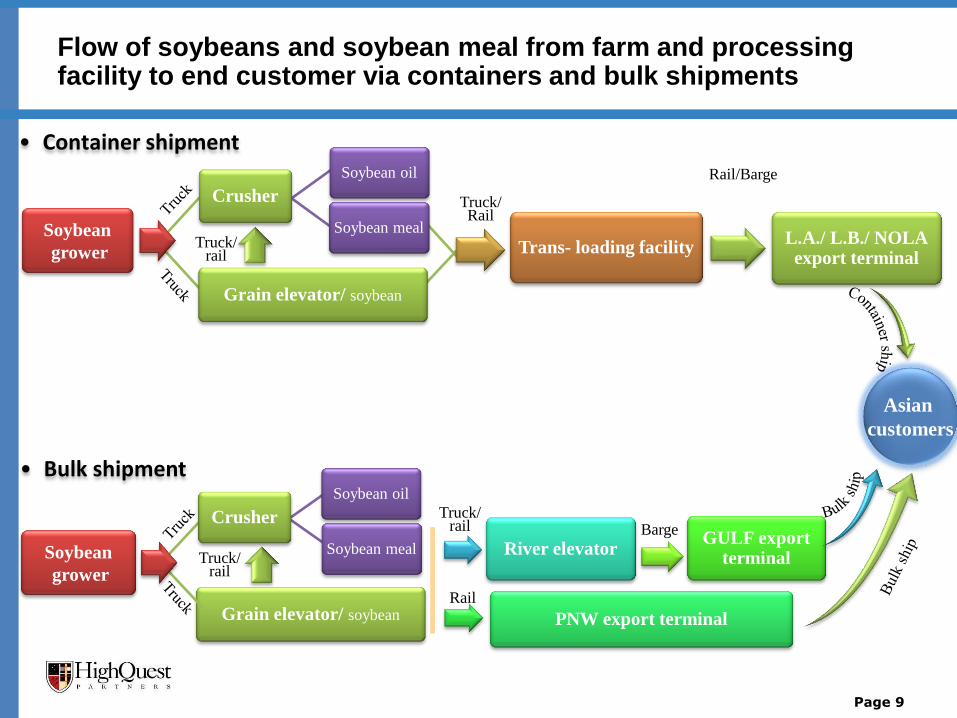

Flow of soybeans and soybean meal from farm and processing facility to end customer via containers and bulk shipments

Page 9

Soybean

grower

Soybean oil

Trans- loading facility Soybean meal

Grain elevator/ soybean

L.A./ L.B./ NOLA export terminal

• Container shipment

Asian

customers

Soybean

grower

Grain elevator/ soybean

Soybean oil

Soybean meal River elevator GULF export

terminal

PNW export terminal

Crusher

Truck/ rail

Truck/ Rail

Rail/Barge

Barge

Rail

Truck/ rail

Truck/ rail

Crusher

• Bulk shipment

U.S. soybean production and demand

Page 10

Source: USDA, HighQuest Partners analysis

• U.S. soybean production is expected to increase by 6.9% from 3.33 billion bushels in 2010/11 to 3.56

billion bushels in 2019/20, based on slightly increased harvested area and improved yields.

• Soybean exports are projected to grow to about 1.455 billion bushels due to continued strong import

demand (projected growth through 2019/20 is approximately 10%), particularly from China.

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

million b

ushels

U.S. soybean supply and demand

U.S. exports U.S. domestic use U.S. production

• Illinois’ soybean production is estimated to grow by approximately16% from 454 million bushels in 2010/11 to 540

million bushels in 2019/20 due to increased harvested area and improved yields.

• Illinois soybean production accounts for approximately 14-15% of total U.S. production and ranked 2nd nationwide (the

largest soybean production state is Iowa).

• Illinois soybean exports account for approximately 13-14% of total U.S. soybean exports and are projected to increase

through 2019 as global demand for soybeans continues to rise.

Page 11

Illinois soybean production and demand

0

100

200

300

400

500

600

700

million b

ushels

Illinois State soybean supply and demand

IL exports IL domestic use IL production

Source: PRX, HighQuest Partners analysis

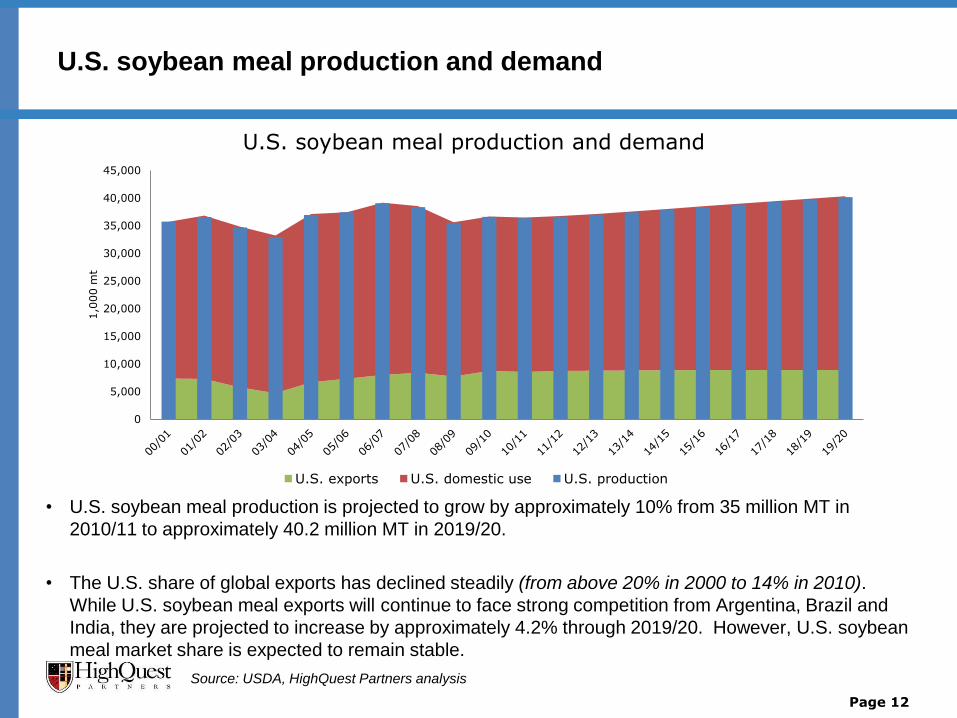

• U.S. soybean meal production is projected to grow by approximately 10% from 35 million MT in

2010/11 to approximately 40.2 million MT in 2019/20.

• The U.S. share of global exports has declined steadily (from above 20% in 2000 to 14% in 2010).

While U.S. soybean meal exports will continue to face strong competition from Argentina, Brazil and

India, they are projected to increase by approximately 4.2% through 2019/20. However, U.S. soybean

meal market share is expected to remain stable.

Page 12

U.S. soybean meal production and demand

Source: USDA, HighQuest Partners analysis

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

1,0

00 m

t

U.S. soybean meal production and demand

U.S. exports U.S. domestic use U.S. production

• Illinois’ soybean meal production is projected to increase by approximately17% from 5.2 million MT

in 2010/11 to 6.3 million MT in 2019/20 due to the expansion of the soybean processing in Illinois.

Illinois is the second largest state in terms of soybean meal production and exports.

• 88% of Illinois’ soybean meal production is exported out of the state, while 12% is used in local

animal feed production. This trend is likely to continue as soybean meal production increases at a

faster rate than in-state consumption.

Page 13

Illinois soybean meal production and demand

Source: PRX, HighQuest Partners analysis

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

1,0

00 m

t

Illinois soybean meal production and demand

IL exports IL domestic use IL production

• Processing accounts for the majority of total Illinois soybean utilization (past 5-year average is

approximately 60%).

• This share is expected to decrease gradually as Illinois’ soybean exports continue to grow at a

faster rate than local crushing due to increasing global demand for soybeans.

• However, the number of bushels of soybeans that will be processed is expected to grow by 1.6%

(CAGR) in the next ten years.

Page 14

Illinois soybean utilization

0

100

200

300

400

500

600

million b

ushels

Illinois soybean utilization

Seed Use

Residual Use

Crush

Exports

Source: PRX, HighQuest Partners analysis

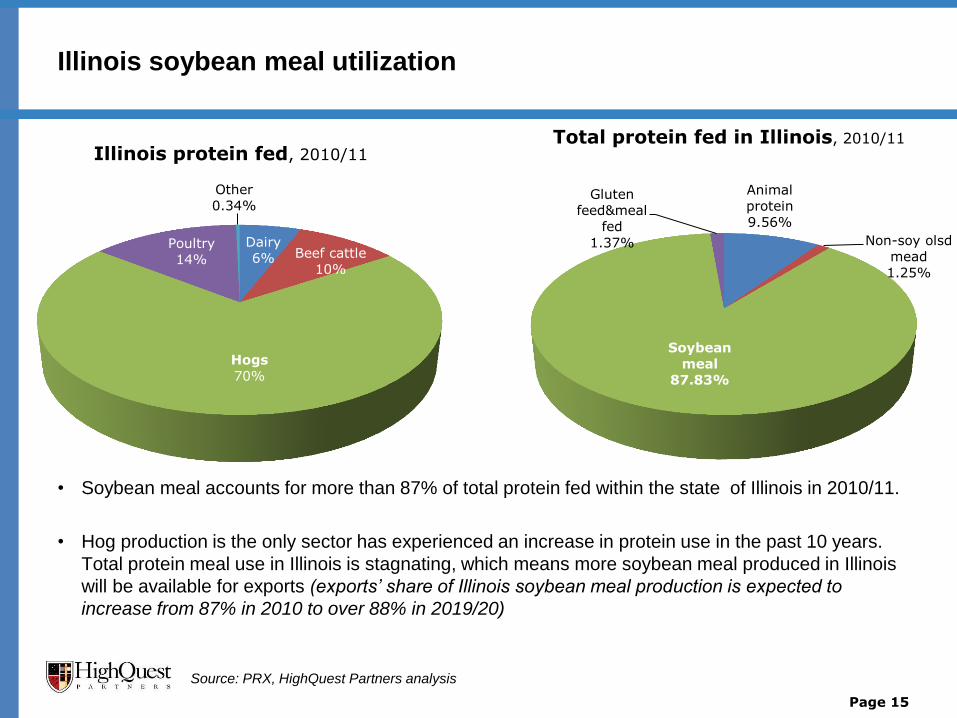

Illinois soybean meal utilization

• Soybean meal accounts for more than 87% of total protein fed within the state of Illinois in 2010/11.

• Hog production is the only sector has experienced an increase in protein use in the past 10 years.

Total protein meal use in Illinois is stagnating, which means more soybean meal produced in Illinois

will be available for exports (exports’ share of Illinois soybean meal production is expected to

increase from 87% in 2010 to over 88% in 2019/20)

Page 15

Dairy

6% Beef cattle

10%

Hogs

70%

Poultry

14%

Other

0.34%

Illinois protein fed, 2010/11

Animal

protein

9.56%

Non-soy olsd

mead

1.25%

Soybean

meal

87.83%

Gluten

feed&meal

fed

1.37%

Total protein fed in Illinois, 2010/11

Source: PRX, HighQuest Partners analysis

U.S. soybean export by port region

• Historically, the vast majority of soybeans have been exported via bulk shipments out of the Gulf

and PNW as these regions account for the majority of U.S. soybean export facilities and have

substantial ocean freight advantages to the primary destination markets for soybeans in Asia and

Latin America.

• So far, in the 2010/11 marketing year the Gulf has accounted for 61% of soybean exports while the

PNW accounts for 25%.

Page 16

Source: PRX, HighQuest Partners analysis

0

200

400

600

800

1000

1200

1400

1600

661 524 590 558

746 769 877

25

22

21 33

29

62 48

240

225

271 350

312

376 401

mill

ion

bu

she

ls

CA

PNW

Atlantic

Gulf- East

Gulf-TX

Gulf-Mis.

Mexico

Canada

Mexico 5%

Canada 3%

Gulf-TX 4%

Gulf-Mis. 55%

Gulf- East 2%

Atlantic 3% PNW

25%

CA 3%

Soybean export forecast by port, 2010/11

U.S. soybean and meal products’ major export markets with focus on Asia

• The top three major Asian importers (China, Japan and Taiwan) accounted for 65% of total U.S. soybean exports in 2010.

• It is estimated that China’s share of total U.S. soybean exports will exceed 55% in 2010/11.

Page 17

• Asian importers account for less than 30% of total U.S. soybean meal exports.

• Southeast Asia accounts for about 55% of total U.S. soybean meal exported to Asia.

• Japan, the Philippines and Vietnam are the top three Asian countries that import U.S. soybean meal.

Source: USDA, HighQuest Partners analysis

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

1,0

00 m

t

Major U.S soybean importers (Asian countries)

ROW

Taiwan

Japan

Indonesia

China

0

2,000

4,000

6,000

8,000

10,000

12,000

1,0

00 m

t

Major U.S. soybean meal importers (Asian countries)

ROW

Vietnam

Thailand

Philippines

Korea, South

Japan

• In 2009, U.S. waterborne agricultural exports totaled 145 million MT, down by 1.5 million MT from

2008.

• During the same period, containers were used to transport 6% (8.7 million MT) of U.S. grain exports

to Asia.

• The primary destination markets for U.S. containerized grain exports in 2009 were Taiwan,

Indonesia and China. These countries accounted for 65% (5.7 million MT) of the total volume.

Page 18

Taiwan

33%

China

14% Indonesia

18% Thailand

6%

Japan

6%

Philippines

5%

Vietnam

4%

Malaysia

3%

Korea

2% HK

1%

Others

8%

Top 10 Destination Markets for U.S. Containerized Grain Exports, 2009

U.S. containerized grain exports

Source: USDA, Census Bureau, PIERS, HighQuest Partners analysis

Page 19

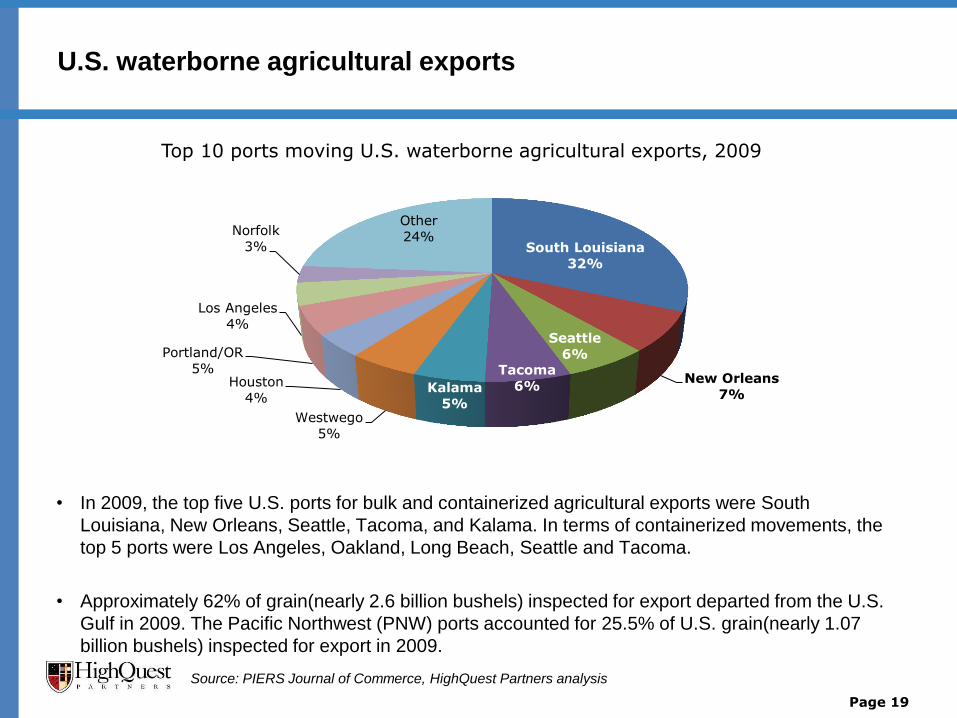

U.S. waterborne agricultural exports

Source: PIERS Journal of Commerce, HighQuest Partners analysis

• In 2009, the top five U.S. ports for bulk and containerized agricultural exports were South

Louisiana, New Orleans, Seattle, Tacoma, and Kalama. In terms of containerized movements, the

top 5 ports were Los Angeles, Oakland, Long Beach, Seattle and Tacoma.

• Approximately 62% of grain(nearly 2.6 billion bushels) inspected for export departed from the U.S.

Gulf in 2009. The Pacific Northwest (PNW) ports accounted for 25.5% of U.S. grain(nearly 1.07

billion bushels) inspected for export in 2009.

South Louisiana

32%

New Orleans

7%

Seattle

6% Tacoma

6% Kalama

5% Westwego

5%

Houston

4%

Portland/OR

5%

Los Angeles

4%

Norfolk

3%

Other

24%

Top 10 ports moving U.S. waterborne agricultural exports, 2009

• U.S. containerized grain exports to Asia exploded in 2007 and reached record highs in 2008 before

dropping sharply in the 2nd half of 2008 due to decreasing demand and tight equipment supply

caused by the global economic recession.

• Approximately 300,000 TEUs of grains were exported to Asia in 2009, down by 32% from the

previous year. However, the market showed recovery in latter half of 2009 and through 2010 as the

global economic situation improved.

Page 20

U.S. containerized grain exports

Source: estimated data collected by PIERS Journal of Commerce, HighQuest Partners analysis

0

100

200

300

400

500

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010Jan-Oc.

1,0

00 T

EU

s

Containerized grain exports to Asia

The CAGR between 2000 and 2008 was 22%

• Improving global and U.S. economic conditions, increased bulk ocean freight rates, a large and

early fall harvest and strong global demand for U.S. grain products contributed to a substantial

increase in volume of containerized grain shipments to Asia during October of 2010.

Page 21

U.S. containerized grain exports

Source: estimated data collected by PIERS Journal of Commerce, HighQuest Partners analysis, USDA

0

10

20

30

40

50

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

1,0

00 T

EU

s

U.S. containerized grain exports to Asia by month (2010)

2010 2007--09 ave.

October shipments reached nearly 40,000 TEUs, 15% over the 3-year average and 108% higher than September movements.

• Soybeans represent the top containerized grain export out of the U.S.(102,164 TEUs of soybean

and soybean meal), followed by DDGS and corn.

• DDGS exports to Asia are expected to continue increasing in the coming years as Asian feed

manufacturers seek less expensive alternatives to corn and soybean meal to formulate into animal

feed rations.

Page 22

U.S. containerized grain exports

Soybeans 32%

Distiller’s Grains

21%

Corn 15%

Animal Feed 14%

Soybean Meal

10%

Other Grain

Products

8%

U.S. containerized grain exports, first half year of 2010

Source: PIERS Journal of Commerce, HighQuest Partners analysis

Commodities TEU**

Soybeans 77,274

DDGS 49,702

Corn 35,526

Animal Feed 32,344

Soybean Meal 24,890

Other Grain Products 18,929

Total 238,666

U.S. soybean exports to Asia via container

• The top three importers of U.S. containerized soybeans are Indonesia, Taiwan and China. These

three markets account for approximately 75% of containerized soybean exports to Asia. The five

major Southeast Asian countries (Indonesia, Malaysia, Thailand, Vietnam and the Philippines)

account for about 60% of containerized soybean exports to Asia.

Page 23

Source: data from GIPSA

198,754

546,239

707,362

21,311 31,231

171,489

24,087

113,896 110,142

0

150,000

300,000

450,000

600,000

750,000

900,000

China M China T Indonesia Japan Korea Rep. Malaysia Philippines Thailand Vietnam

Met

ric

ton

s

US soybean exports to Asia in container

09/2010~01/2011 2009/10 2008/09 01/2008~08/20008

Note: data in the chart are 2009/10 containerized soybean export volumes

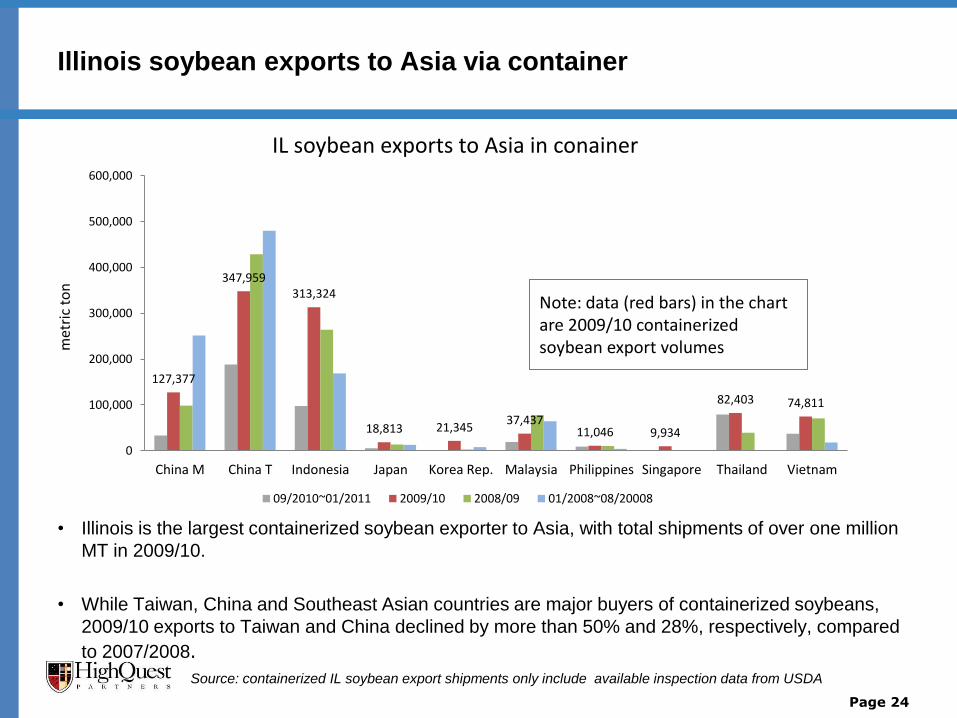

• Illinois is the largest containerized soybean exporter to Asia, with total shipments of over one million

MT in 2009/10.

• While Taiwan, China and Southeast Asian countries are major buyers of containerized soybeans,

2009/10 exports to Taiwan and China declined by more than 50% and 28%, respectively, compared

to 2007/2008.

Page 24

Illinois soybean exports to Asia via container

Source: containerized IL soybean export shipments only include available inspection data from USDA

127,377

347,959 313,324

18,813 21,345 37,437

11,046 9,934

82,403 74,811

0

100,000

200,000

300,000

400,000

500,000

600,000

China M China T Indonesia Japan Korea Rep. Malaysia Philippines Singapore Thailand Vietnam

met

ric

ton

IL soybean exports to Asia in conainer

09/2010~01/2011 2009/10 2008/09 01/2008~08/20008

Note: data (red bars) in the chart are 2009/10 containerized soybean export volumes

Total soybean exports by port (bulk and container)

Page 25

A majority of soybean exports from the U.S. are shipped in bulk out of the Gulf and

PNW. Buyers from Taiwan and Southeast Asia prefer containers due to port

capacity constraints in these countries.

Source: GIPSA/USDA, HighQuest Partners Analysis

2009/2010 China Taiwan Japan S. Korea Indonesia Malaysia Thailand Vietnam Philippines Total

GULF-bulk 57.0% 24.0% 97.4% 95.7% 29.8% 55.7% 70.7% 57.5%

Pacific-bulk 40.8% 36.6% 0.8% 24.7% 60.2% 34.4%

Container 0.9% 32.9% 1.0% 4.3% 45.0% 44.3% 24.6% 80.3% 39.8% 6.5%

Atlantic-bulk 0.4% 6.4% 0.6% 4.7% 19.6% 0.9%

Others 0.9% 0.9% 0.8%

1. Over 92% of total soybean exports out of the U.S. East Coast to East Asia and Southeast

Asia are shipped via containers. Approximately 70% of these shipments go to five major

Southeast Asian countries shown in the table above.

2. In 2009/2010, approximately 1.93 million MT of U.S. containerized soybean exports were

shipped to nine markets in Asia. Indonesia, Taiwan and China, the top three importers,

accounted for 707,362 MT, 546,239 MT, and 198,754 MT respectively.

Overview of container industry - current and projected availability of containers

• Most of the large Post-Panamax containerships delivered in 2010 were assigned to the more

lucrative Asia/Europe routes, while most of the remaining units have joined Far East/U.S. routes.

• A record number of Post-Panamax containerships with capacity of more than 7,500 TEUs will be

delivered in 2011.

• Collectively these new vessels will increase the capacity of the world containership fleet by 860,000

TEUs next year, accounting for approximately 63% of all new slots due for delivery in 2011.

• It is estimated that there will be 49 new Post-Panamax ships delivered in 2011 with capacity of

more than 10,000 TEUs (compared to 29 in 2010 and 15 in 2009), as well as delivery of 27 ships

with capacity of 7,500-9,999 TEUs in 2011 (compared to 32 in 2010 and 18 in 2009).

• The expected VLCS deliveries in 2011 are likely to enable carriers to mount four to five new high-

capacity Asia/Europe routes and five Asia/U.S. routes, with most of these expected to be launched

in the first half of the year.

Page 26

Source: Alphaliner, Journal of Commerce

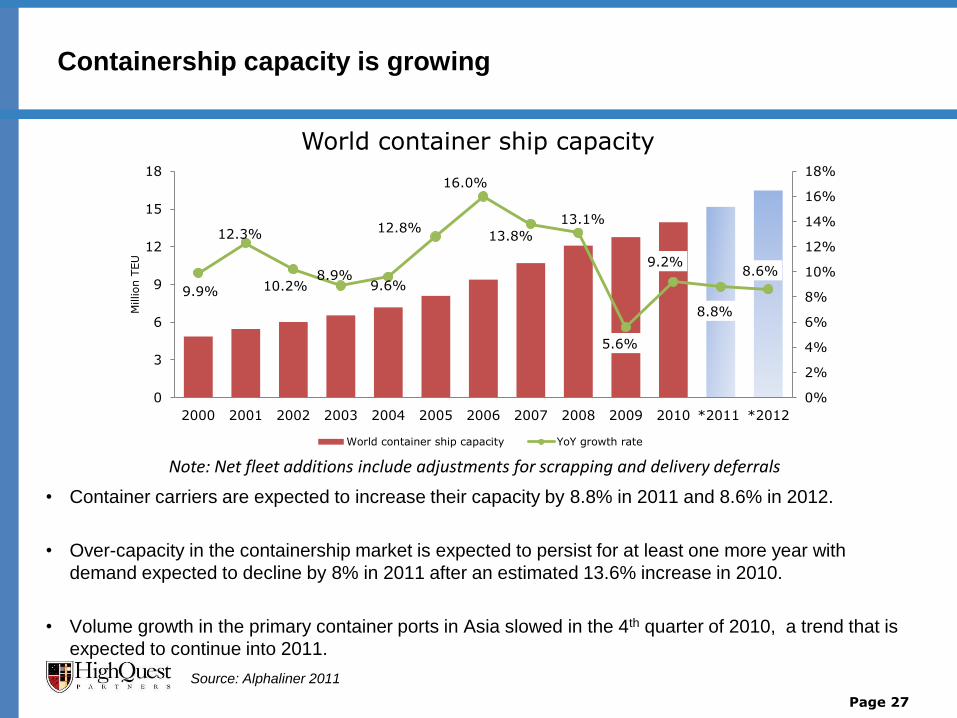

Containership capacity is growing

• Container carriers are expected to increase their capacity by 8.8% in 2011 and 8.6% in 2012.

• Over-capacity in the containership market is expected to persist for at least one more year with

demand expected to decline by 8% in 2011 after an estimated 13.6% increase in 2010.

• Volume growth in the primary container ports in Asia slowed in the 4th quarter of 2010, a trend that is

expected to continue into 2011.

Page 27

Source: Alphaliner 2011

Note: Net fleet additions include adjustments for scrapping and delivery deferrals

9.9%

12.3%

10.2% 8.9%

9.6%

12.8%

16.0%

13.8%

13.1%

5.6%

9.2%

8.8%

8.6%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0

3

6

9

12

15

18

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 *2011 *2012

Million T

EU

World container ship capacity

World container ship capacity YoY growth rate

Global shipping container shortage

• Many shipping container and leasing companies curtailed sourcing and producing

containers during the 2008-09 global recession. The 2010 rebound caught many of the

major container shipping lines by surprise. (It is estimated the industry needs up to 6

million shipping containers in order to regain the conventional 2.2 containers per

available slot. Put that into perspective, that equates to two years’ worth of production.)

Page 28

Inven

tory-to

-capacity ratio

It’s estimated that the

container box inventory-to-

fleet capacity ratio will drop

from 2.03 in 2010 to below

2, the lowest ratio on

record, by the end of 2011.

Source: Alphaliner, JOC, HighQuest Analysis

Shifting trend of global containerized trade

• Over the past decade, intra-Asian containerized trade has increased its share of global

containerized trade, whereas the share of transpacific and transatlantic containerized

shipping have declined.

• The explosion of intra-Asian trade has led to a global shipping container shortage

within the industry.

Page 29

32% 28% 31%

15% 18% 18%

21% 19% 17%

7% 5% 4%

26% 28% 30%

2000 2006 2009

Containerized trade composition

Intra Asia

Transatlantic

Transpacific

Asia-Europe

Others

Global shipping container shortage

Page 30

Source: Credit Suisse research report March 2011 JOC, HighQuest Analysis

• The bottleneck in container production could lead to a shortage of boxes later this year.

Most affected could be the backhaul shippers from the U.S. and Europe as carriers will

need to return empty containers back to demand locations in Asia quickly.

• Due to the financial crisis, container carriers and leasing companies disposed of a large

portion of their older stock as utilization levels fell. Manufacturing of new containers was

also halted in 2009 as demand fell. Carriers were largely unprepared for the surge in

demand that occurred in 2010, resulting in acute container shortages in the Far East. The

production of new containers began increasing in July 2010.

-1,500

-1,000

-500

0

500

1,000

1,500

2,000

2,500

3,000

3,500

-2,000

-1,000

0

1,000

2,000

3,000

4,000

5,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011E

1,0

00

TEU

s

Global container supply and demand

Total box sales Disposals Net growth

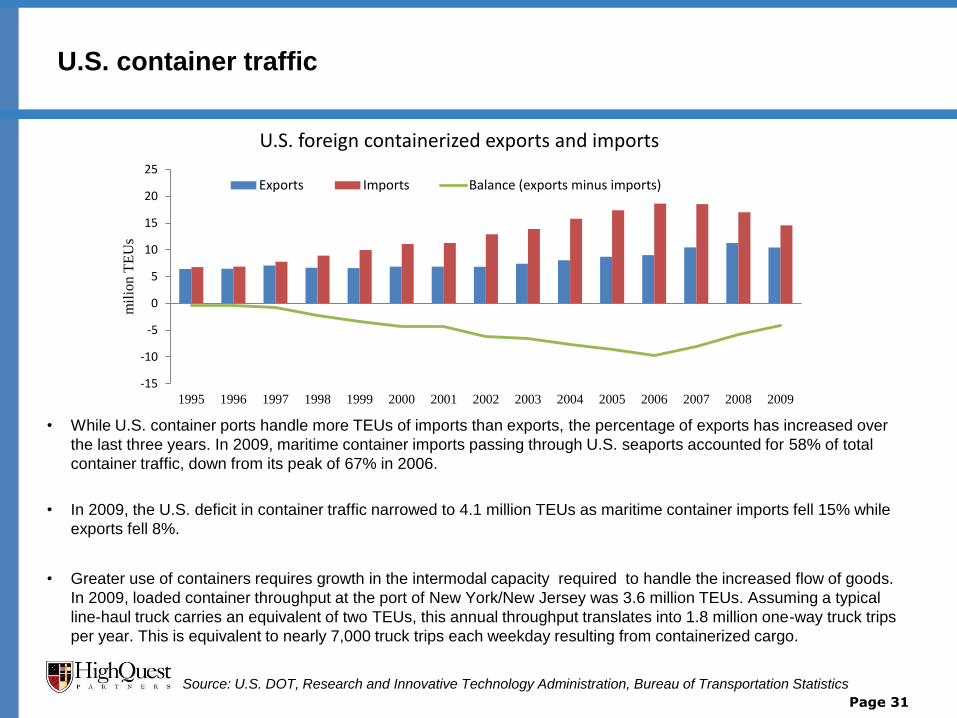

U.S. container traffic

• While U.S. container ports handle more TEUs of imports than exports, the percentage of exports has increased over

the last three years. In 2009, maritime container imports passing through U.S. seaports accounted for 58% of total

container traffic, down from its peak of 67% in 2006.

• In 2009, the U.S. deficit in container traffic narrowed to 4.1 million TEUs as maritime container imports fell 15% while

exports fell 8%.

• Greater use of containers requires growth in the intermodal capacity required to handle the increased flow of goods.

In 2009, loaded container throughput at the port of New York/New Jersey was 3.6 million TEUs. Assuming a typical

line-haul truck carries an equivalent of two TEUs, this annual throughput translates into 1.8 million one-way truck trips

per year. This is equivalent to nearly 7,000 truck trips each weekday resulting from containerized cargo.

Page 31

Source: U.S. DOT, Research and Innovative Technology Administration, Bureau of Transportation Statistics

-15

-10

-5

0

5

10

15

20

25

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

mil

ion T

EU

s U.S. foreign containerized exports and imports

Exports Imports Balance (exports minus imports)

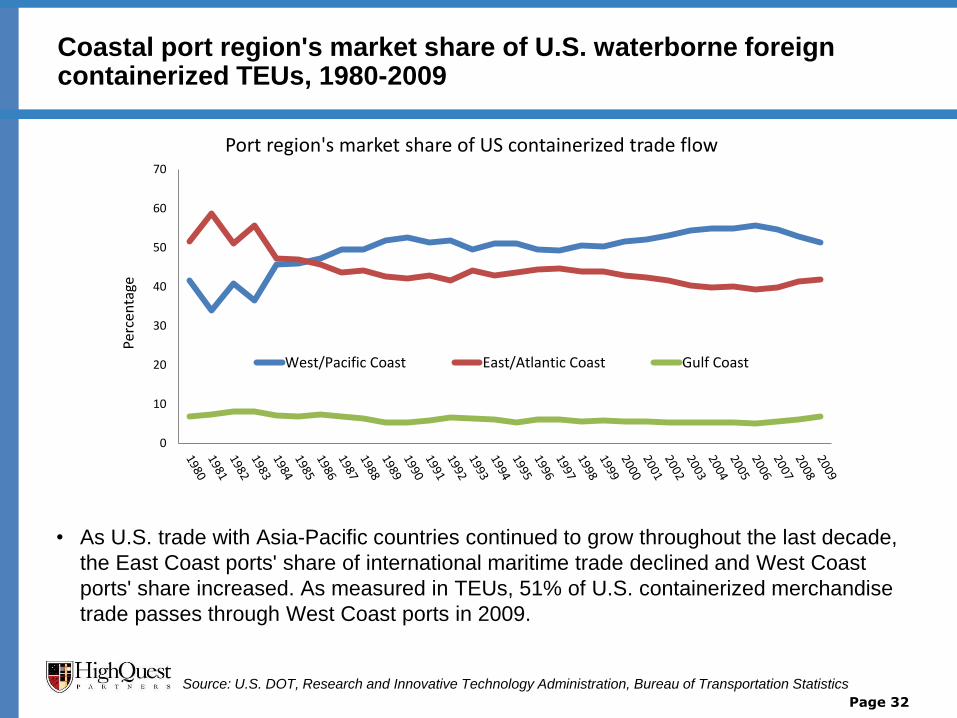

Coastal port region's market share of U.S. waterborne foreign containerized TEUs, 1980-2009

• As U.S. trade with Asia-Pacific countries continued to grow throughout the last decade,

the East Coast ports' share of international maritime trade declined and West Coast

ports' share increased. As measured in TEUs, 51% of U.S. containerized merchandise

trade passes through West Coast ports in 2009.

Page 32

Source: U.S. DOT, Research and Innovative Technology Administration, Bureau of Transportation Statistics

0

10

20

30

40

50

60

70

Perc

enta

ge

Port region's market share of US containerized trade flow

West/Pacific Coast East/Atlantic Coast Gulf Coast

U.S. containerized trade with Asia, 1999-2010

• U.S. containerized trade with several Asian countries is chronically imbalanced, especially with

China, Japan and South Korea. What is notable is the rapidity at which these imbalances have

emerged over the last decade. The imports/exports ratio has increased from close to 1:1 in 1996 to

2.7:1 in 2006 before declining to approximately 2:1 in 2010. This trend is expected to continue for

as long as China continues to peg the yuan to the U.S. dollar and has substantial implications on

the movements of containers as well as on transport costs.

Page 33

Source: PIERS, Japan Maritime Center

Million T

EU

s

Ratio

0.0

0.5

1.0

1.5

2.0

2.5

3.0

0

5

10

15

20

25

2010 2009 2008 2007 2006 2005 2004 2003 2002 2001 2000 1999

U.S. containerized trade with Asia

Imports Exports Ratio Imp/Exp

Top 10 trading partners for U.S. waterborne foreign containerized imports

• In 2009, the U.S.’ top ten trading partners accounted for nearly three-quarters (71%) of inbound

container TEUs, while more than half (56%) of the outbound container TEUs were to these countries.

• China was the leading containerized merchandise trading partner, accounting for nearly one-half

(48%) of U.S. maritime imported TEUs, almost double the 25% share of such trade in 2000. China

accounted for 22% of U.S. exported TEUs in 2009, more than double the 9% it accounted for in 2000.

Page 34

Source: U.S. DOT, Research and Innovative Technology Administration

0

5

10

15

20

25

30

35

40

45

50

Chin

a

(excl

udin

g

Hong K

ong)

Japan

South

Kore

a

Hong K

ong

Tai

wan

Vie

tnam

Ger

man

y

Thai

land

India

Ital

y

Oth

ers

Pe

rce

nta

ge

Share of total TEUs, 2000 Share of total TEUs, 2005

Share of total TEUs, 2009

Far East- US monthly supply-demand in TEU, 2009-2011

• Transpacific trade volumes are expected to grow by 7- 8% in 2011, according to the latest TSA

(Transpacific Stabilization Agreement) forecasts.

• Vessel utilization levels have fallen below 90% (88% to West Coast, 95% to East Coast) since

October last year, and have remained relatively weak in January this year due to the 25% year-on-

year increase in capacity deployed on these routes.

• The weaker than expected utilization levels could have a negative impact on the TransPacific

carriers’ attempt to raise freight rates for 2011/12 season.

Page 35

Source: Alphaliner, HighQuest Partners Analysis

Dem

and

/su

pp

ly in

TEU

th

ou

san

ds Est. utilization level %

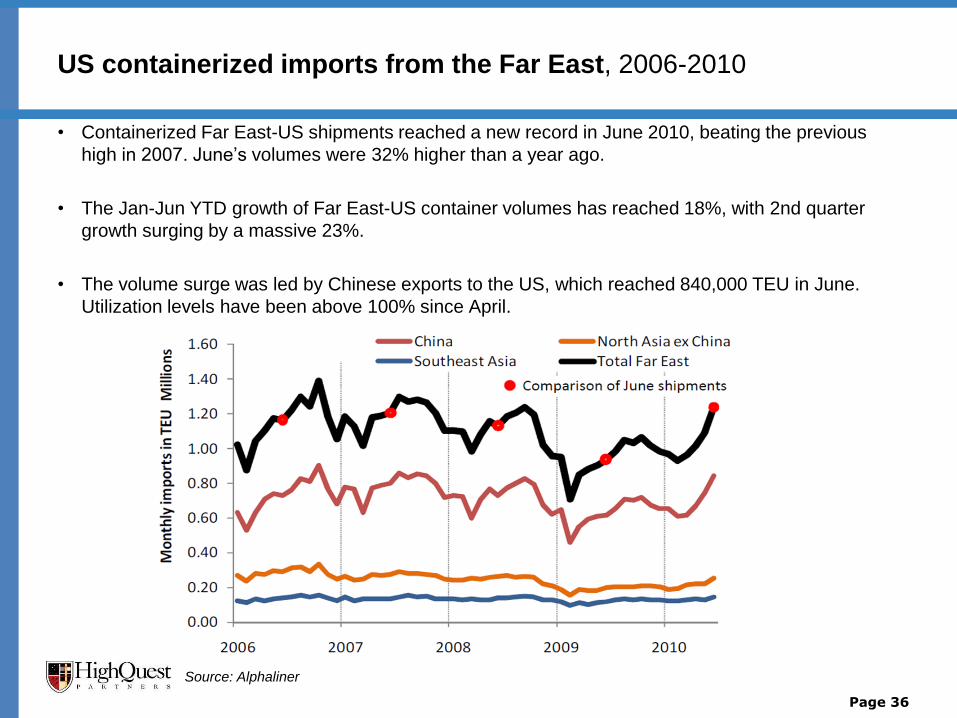

US containerized imports from the Far East, 2006-2010

• Containerized Far East-US shipments reached a new record in June 2010, beating the previous

high in 2007. June’s volumes were 32% higher than a year ago.

• The Jan-Jun YTD growth of Far East-US container volumes has reached 18%, with 2nd quarter

growth surging by a massive 23%.

• The volume surge was led by Chinese exports to the US, which reached 840,000 TEU in June.

Utilization levels have been above 100% since April.

Source: Alphaliner

Page 36

Top 25 container ports for U.S. international maritime freight (2009 - thousands of TEUs)

Source: U.S. DOT, Research and Innovative Technology Administration, Bureau of Transportation Statistics

Major US container ports

Source: Intermodal Association Statistics

Page 38

0 1,000,000 2,000,000 3,000,000 4,000,000 5,000,000 6,000,000

Los Angeles

Long Beach

New York

Savannah

Oakland

Norfolk

Houston

Seattle

Charleston, SC

Tacoma

Miami

Port Everglades

Baltimore

New Orleans

San Juan

Jacksonville

Willmington, NC

Philadelphia

Wilmington, DE

Gulfport

US Ports' Container Traffic, 2005- 2009 Average (TEUs)

• Top 10 ports handled 75% of total US container traffic in 2009.

• Los Angeles and Long Beach account for 35% of total US container traffic from 2005 to 2009.

Major U.S. seaports’ foreign containerized trade (exports - imports)

• In 2010, the volume of inbound container shipments through the ports of Los Angeles, Long Beach

and New York/New Jersey reached 3.97 million TEUs, 3.13 million TEUs and 2.58 million TEUs,

respectively, while the outbound container shipments out of the three ports were 1.84 million TEUs,

1.56 million TEUs and 1.52 million TEUs, respectively.

Page 39

2,133

1,567

1,061

(152)

(152)

(115)

(325)

339

60

139

(500) 0 500 1,000 1,500 2,000 2,500

Port of Los Angeles

Port of Long Beach

Port of New York/New Jersey

Port of Savannah

Port of Oakland

Port of Norfolk

Port of Houston

Port of Seattle

Port of Charleston

Port of Tacoma

000 TEUs

Major ports' container deficit (red)/surplus (blue)

The volume of inbound

containers at the ports of Los

Angeles and Long Beach was

3.7 million TEUs more than

the outbound volume in 2010.

Container freight in US agriculture

• U.S. agricultural exporters began viewing container freight as a viable option for

shipping goods to Asia in 2007 when bulk freight prices rose substantially.

• The primary reason that agricultural exporters started using container freight was due

to the economy in the U.S. at that time.

– As the U.S. economy was in a significant boom period, U.S. consumers were importing large

volumes of Asian electronic and inter-modal goods into the U.S. via containers.

– The challenge for container shipping companies was that there was not the same demand for

U.S. goods in Asia, so containers were returning empty.

– The container companies realized that they needed to pursue new markets in order to secure

backhaul to Asia in their containers and they began to pursue agricultural products by offering

very cheap rates that were competitive with bulk shipments.

• Historically, the primary driver of container freight prices has been availability, not

distance, so it is better to locate a trans-loader near an inter-modal hub where

containers are readily available.

• In the Midwest, Chicago represents the low price container market (despite its distance

from the major West Coast ports) due to its high availability of containers.

Page 40

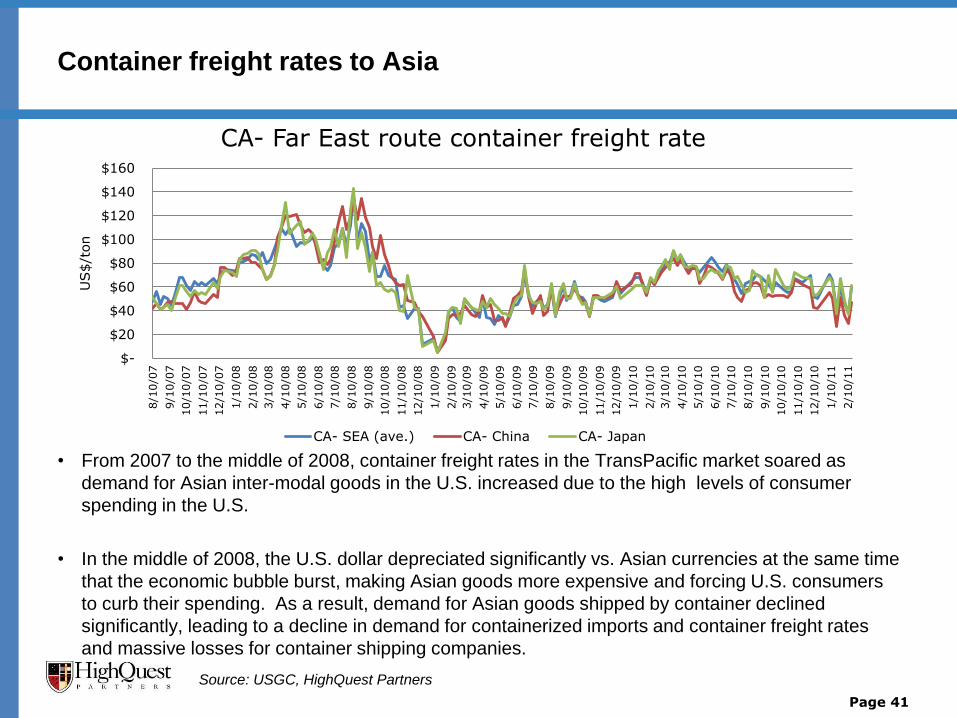

Container freight rates to Asia

• From 2007 to the middle of 2008, container freight rates in the TransPacific market soared as

demand for Asian inter-modal goods in the U.S. increased due to the high levels of consumer

spending in the U.S.

• In the middle of 2008, the U.S. dollar depreciated significantly vs. Asian currencies at the same time

that the economic bubble burst, making Asian goods more expensive and forcing U.S. consumers

to curb their spending. As a result, demand for Asian goods shipped by container declined

significantly, leading to a decline in demand for containerized imports and container freight rates

and massive losses for container shipping companies.

Page 41

$-

$20

$40

$60

$80

$100

$120

$140

$160

8/1

0/0

7

9/1

0/0

7

10/1

0/0

7

11/1

0/0

7

12/1

0/0

7

1/1

0/0

8

2/1

0/0

8

3/1

0/0

8

4/1

0/0

8

5/1

0/0

8

6/1

0/0

8

7/1

0/0

8

8/1

0/0

8

9/1

0/0

8

10/1

0/0

8

11/1

0/0

8

12/1

0/0

8

1/1

0/0

9

2/1

0/0

9

3/1

0/0

9

4/1

0/0

9

5/1

0/0

9

6/1

0/0

9

7/1

0/0

9

8/1

0/0

9

9/1

0/0

9

10/1

0/0

9

11/1

0/0

9

12/1

0/0

9

1/1

0/1

0

2/1

0/1

0

3/1

0/1

0

4/1

0/1

0

5/1

0/1

0

6/1

0/1

0

7/1

0/1

0

8/1

0/1

0

9/1

0/1

0

10/1

0/1

0

11/1

0/1

0

12/1

0/1

0

1/1

0/1

1

2/1

0/1

1

US$/t

on

CA- Far East route container freight rate

CA- SEA (ave.) CA- China CA- Japan

Source: USGC, HighQuest Partners

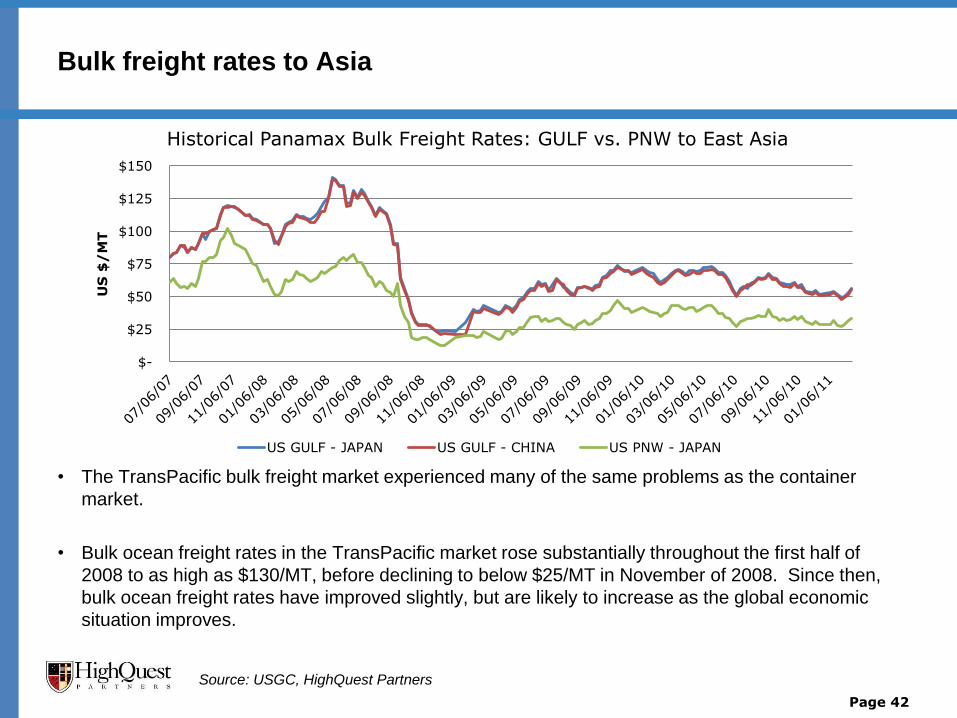

• The TransPacific bulk freight market experienced many of the same problems as the container

market.

• Bulk ocean freight rates in the TransPacific market rose substantially throughout the first half of

2008 to as high as $130/MT, before declining to below $25/MT in November of 2008. Since then,

bulk ocean freight rates have improved slightly, but are likely to increase as the global economic

situation improves.

Page 42

Bulk freight rates to Asia

Source: USGC, HighQuest Partners

$-

$25

$50

$75

$100

$125

$150

US

$/

MT

Historical Panamax Bulk Freight Rates: GULF vs. PNW to East Asia

US GULF - JAPAN US GULF - CHINA US PNW - JAPAN

Seasonal patterns of U.S. soybean exports to major Asian markets

• China is by far the largest import market for U.S. soybeans in Asia, followed by Japan, Taiwan and

South Korea. China is likely to represent 55% of total U.S. soybean exports in 2010/11. Argentina

and Brazil are the U.S.’ major competitors in these markets.

Page 43

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

Sep-0

7

Nov-0

7

Jan-0

8

Mar-

08

May-0

8

Jul-

08

Sep-0

8

Nov-0

8

Jan-0

9

Mar-

09

May-0

9

Jul-

09

Sep-0

9

Nov-0

9

Jan-1

0

Mar-

10

May-1

0

Jul-

10

Sep-1

0

Nov-1

0

metr

ic t

on

China soybean imports

0

75,000

150,000

225,000

300,000

375,000

450,000

Sep-0

7

Nov-0

7

Jan-0

8

Mar-

08

May-0

8

Jul-

08

Sep-0

8

Nov-0

8

Jan-0

9

Mar-

09

May-0

9

Jul-

09

Sep-0

9

Nov-0

9

Jan-1

0

Mar-

10

May-1

0

Jul-

10

Sep-1

0

Nov-1

0

metr

ic t

on

Japan soybean imports

0

75,000

150,000

225,000

300,000

375,000

450,000

Sep-0

7

Nov-0

7

Jan-0

8

Mar-

08

May-0

8

Jul-

08

Sep-0

8

Nov-0

8

Jan-0

9

Mar-

09

May-0

9

Jul-

09

Sep-0

9

Nov-0

9

Jan-1

0

Mar-

10

May-1

0

Jul-

10

Sep-1

0

Nov-1

0

metr

ic t

on

Taiwan soybean imports

0

50,000

100,000

150,000

200,000

250,000

Sep-0

7

Nov-0

7

Jan-0

8

Mar-

08

May-0

8

Jul-

08

Sep-0

8

Nov-0

8

Jan-0

9

Mar-

09

May-0

9

Jul-

09

Sep-0

9

Nov-0

9

Jan-1

0

Mar-

10

May-1

0

Jul-

10

Sep-1

0

Nov-1

0

metr

ic t

on

S. Korea soybean imports

• While Indonesia is the largest export market for U.S. soybeans in Southeast Asia, soybean volumes

into Vietnam have increased substantially due to the rise in container shipments to this country.

Page 44

Seasonal patterns of U.S. soybean exports to major Asian markets

0

75,000

150,000

225,000

300,000

375,000

Sep

-07

No

v-0

7

Jan

-08

Mar

-08

May

-08

Jul-

08

Sep

-08

No

v-0

8

Jan

-09

Mar

-09

May

-09

Jul-

09

Sep

-09

No

v-0

9

Jan

-10

Mar

-10

May

-10

Jul-

10

Sep

-10

No

v-1

0

met

ric

ton

Indonesia soybean imports

0

30,000

60,000

90,000

120,000

150,000

180,000

Sep

-07

No

v-0

7

Jan

-08

Mar

-08

May

-08

Jul-

08

Sep

-08

No

v-0

8

Jan

-09

Mar

-09

May

-09

Jul-

09

Sep

-09

No

v-0

9

Jan

-10

Mar

-10

May

-10

Jul-

10

Sep

-10

No

v-1

0

met

ic t

on

Thailand soybean imports

0

30,000

60,000

90,000

120,000

met

ric

ton

Malaysia, Vietnam and Philippines soybean imports

Major Chinese container ports

Source: China Customs, Port of Hamburg Statistics

Page 45

0

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

140,000,000

2009 2008 2007 2006 2005

Major Chinese Ports' Container Traffic, TEUs

Dalian

Xiamen

Tianjin

Qingdao

Ningbo

Guangzhou

Shenzhen

Hong Kong

Shanghai

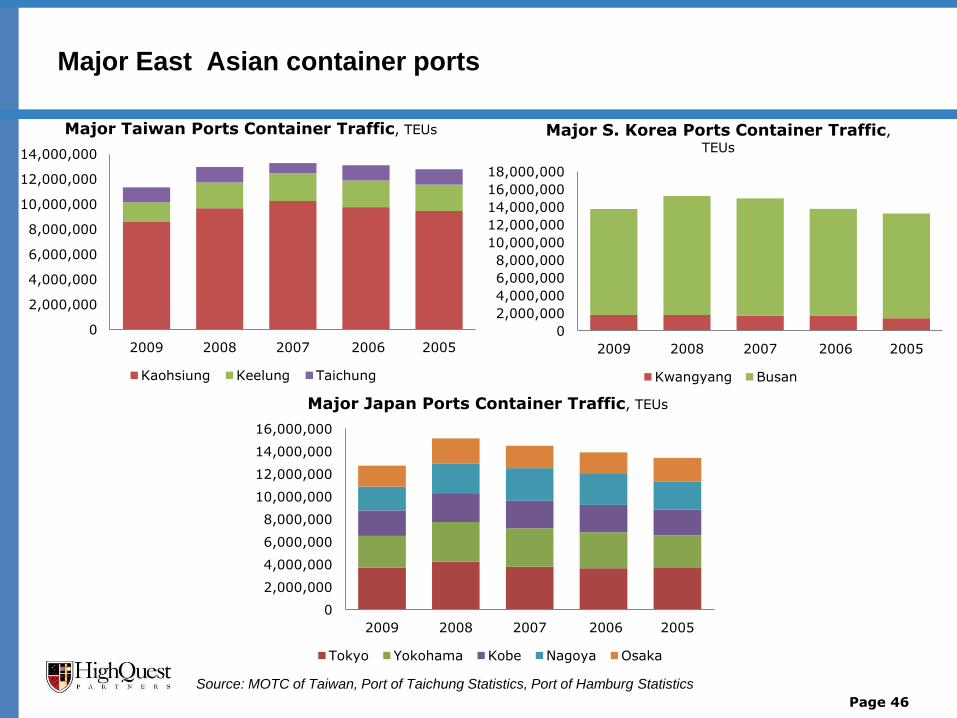

Major East Asian container ports

Page 46

Source: MOTC of Taiwan, Port of Taichung Statistics, Port of Hamburg Statistics

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

2009 2008 2007 2006 2005

Major Taiwan Ports Container Traffic, TEUs

Kaohsiung Keelung Taichung

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

18,000,000

2009 2008 2007 2006 2005

Major S. Korea Ports Container Traffic,

TEUs

Kwangyang Busan

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

2009 2008 2007 2006 2005

Major Japan Ports Container Traffic, TEUs

Tokyo Yokohama Kobe Nagoya Osaka

Major Southeast Asian container ports

Source: Port of Hamburg Statistics, Port of Bangkok Authority, Report of "Thailand Shipping Report Q4 2010"

Page 47

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

18,000,000

2009 2008 2007 2006 2005

Major SEA Ports Container Traffic (TEUs)

Laem Chabang (Thailand) Bangkok (Thailand) Ho Chi Minh City (Vietnam)

Jakarta (Indonesia) Manila (Philippines)

Container vs. Bulk Shipping- Strengths and Weaknesses

• Historically, the vast majority of grains exported out of the U.S. have been transported via ocean-

going bulk vessels due to:

– sheer volumes that can be moved in bulk vs. containers

– unit/ton cost advantages of loading grain in bulk;

– interior transportation flows of U.S. grain movements;

– ability of U.S. grain elevators to load in bulk vs. container;

– ability of U.S. export grain terminals to load bulk vessels more easily than container vessels

and

– lack of major intermodal hubs located near major U.S. grain production centers.

• However, in 2006, the economics of loading U.S. grains in containers changed substantially as

significant volumes of containers entered the U.S. Midwest and returned to Asia without a backhaul,

substantially reducing container shipper margins.

– This development led to an increase in containerized grain backhaul volumes to Asia and

forced many grain companies to reconsider how they were shipping grains back to Asia.

– As the container shipping companies began offering discounts to exporters for shipping their

grains to Asia, the cost of shipping containerized grain declined significantly and made it more

affordable for buyers in Asia to consider containerized shipments over bulk.

– Containers enabled U.S. local elevators and regional grain companies to enter the export

market directly without the capital expense of building an export elevator and cut out the

middlemen, thus increasing these companies margins.

Page 48

Strengths and weaknesses of shipping soybeans via container vs. bulk

Page 49

Strengths Weaknesses

1. Identity preservation for non-GMO and organic soybeans.

1. Container prices dependent on availability, i.e. U.S. and global economy.

2. Easier access to smaller customers in foreign markets. These customers prefer containers as it cuts out cost of middle man.

2. Higher unit/ton cost and freight rates than bulk.

3. Lack of backhaul opportunities for containers returning to Asia leads to discounts from some container shippers, especially in markets located near major intermodal hubs, i.e. Chicago and St. Louis.

3. U.S. interior grain transportation infrastructure set up for bulk.

4. Lack of port infrastructure (storage, inland transportation, etc.) in Asia’s smaller markets makes it difficult to unload fully-loaded bulk vessels.

4. U.S. grain export terminals set up for bulk.

5. Containers help to solve quality issues that some importers face with bulk vessels due to less water erosion, dust, etc.

5. Lack of major intermodal hubs in primary grain growing regions leads to higher cost to reposition containers for grain movements.

6. Enables smaller, more regional companies to enter export market without capital cost of building export elevator.

6. Lack of drayage opportunities in major Midwest grain production markets.

7. Major export markets (China, Taiwan, South Korea and Japan) are major container hubs in Asia.

8. Increased transload and container infrastructure in U.S. Midwest.

Table of contents

1. Executive Summary

2. Overview of U.S. and Illinois soybeans and soybean trade flows

3. Major players in the U.S. and Illinois container shipping industry

4. Landed price analysis of soybeans and soybean meal moving from

Illinois to major destination markets

4. Recommendations for increasing container movements of Illinois

soybeans and soybean meal

Page 50

Major players in the U.S. and Illinois container shipping industry

• Container shipping companies and the major rail lines dominate the U.S. containerized

shipping industry.

• The majority of containers enter the U.S. at major port facilities on the East, Gulf and

West coasts and are then moved on to rail cars for shipments to inter-modal yards in

the U.S. Midwest. The containers are then returned to the port via rail empty or with

agricultural goods from the Midwest.

• The top 20 container shipping companies (seen slide 47) accounted for approximately

87% of global TEUs moved in 2010 and 68% of the total container fleet moved in

2010.

• The major rail lines accounted for the vast majority of containers shipped internally in

the U.S.

• All of these companies have major operations in Illinois as Chicago and St. Louis are

two of the major container destination markets in the U.S.

Page 51

Containerized grain flows in Illinois

• Illinois has a decided advantage over the other major production states on

containerized exports of soybeans due to its proximity to the major inter-modal yards in

Chicago and St. Louis.

• Chicago represents the largest container market in the Midwest due to its high demand

for inter-modal goods. Container availability is generally higher here than in other

Midwest states.

– The high container availability in Chicago allows grain shippers in Illinois greater access to

containers and provides these exporters cheaper freight rates to the ports than other

Midwestern states.

– St. Louis is another major inter-modal hub in close proximity to growers and processors

located in southern Illinois.

• Soybean growers and processors in Illinois can deliver their soybeans and soybean

meal by truck to trans-loaders located near the inter-modal hubs, load their products

into containers and then rail the containers to the East, West and Gulf Coast ports for

export to Asia at a lower cost than their competitors as containers do not need to be

repositioned and growers and processors do not have to travel the same distance as

growers and processors in neighboring soybean producing states.

Page 52

Container shipping companies, 2010

Page 53

Ranking Operator TEU TEU % Ships Ship %

1 APM-Maersk 2,176,416 15.17% 586 12.06%

2 Mediterranean Shipping Co 1,923,803 13.41% 461 9.49%

3 CMA CGM Group 1,231,245 8.58% 399 8.21%

4 Evergreen Line 606,814 4.23% 161 3.31%

5 Hapag-Lloyd 593,798 4.14% 132 2.72%

6 CSAV Group 585,177 4.08% 158 3.25%

7 APL 580,700 4.05% 145 2.98%

8 COSCO Container L. 544,804 3.80% 138 2.84%

9 Hanjin Shipping 483,073 3.37% 106 2.18%

10 CSCL 462,203 3.22% 139 2.86%

11 MOL 399,681 2.79% 96 1.98%

12 NYK Line 392,085 2.73% 99 2.04%

13 Hamburg Süd Group 378,744 2.64% 117 2.41%

14 OOCL 352,477 2.46% 78 1.61%

15 K Line 334,705 2.33% 80 1.65%

16 Yang Ming Marine Transport Corp. 322,091 2.25% 79 1.63%

17 Hyundai M.M. 320,735 2.24% 61 1.26%

18 Zim 318,815 2.22% 94 1.93%

19 PIL (Pacific Int. Line) 261,103 1.82% 140 2.88%

20 UASC 217,872 1.52% 56 1.15%

Subtotal 12,486,341 87.04% 3,325 68.43%

World total * 14,344,943 4,859

* Including top 100 container lines, as of March, 2011

• The top 20 global container shipping companies accounted for approximately 87% of total TEU’s shipped and 68% of all

container ships in 2010.

• Each of these companies have operations in the inter-modal yards in Chicago which leads to increased container availability

in the state of Illinois and lower prices.

Major container shipping companies and market share

Page 54

Maersk, 15%

MSC, 12%

CMA CGM , 8%

Evergreen

5%

APL

Hapag-Lloyd COSCO

CSAV Hanjin

CSCL

NYK

Mitsui O.S.K.

OOCL

Hamburg Süd

Zim

K Line

YMMTC

Hyundai

PIL UASC

Other

TEU capacity Market Share

Maersk

9%

MSC, 7%

CMA CGM ,

7%

Evergreen,

2.8%

APL, 2.4%

Hapag-Lloyd

COSCO

Other

47%

Number of Ships Market Share

Maersk and Mediterranean Shipping Company (MSC) are the largest container

shippers with a collective 27% TEU market share.

Source: Alphaliner

Major shipping companies for the Far East to N. America route

Page 55

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

CSAV

MSC

Maersk

CMA CGM

MOL

Zim

CSCL

OOCL

Hapag-Lloyd

COSCON

K Line

NYK

YMMTC

Evergreen

Hyundai MM

Hanjin

APL

TEU Capacity Deployed by Trade Route: August, 2010

FE - N. Am Eur- N. Am Eur- FE ME/ISC related Africa related LatAm related

ANZ/Oceania related Intra-FE Intra-Eur Unassigned Idle

Source: Alphaliner

National intermodal system

• Chicago has more inter-modal hubs than any other market in the Midwest and thus the highest

container availability in the region.

• All of the major rail lines operating in the U.S. and Canada have inter-modal hubs in the vicinity of

Chicago.

Page 56

Illinois grain production, elevators and transportation systems

• Many grain elevators in Illinois are located within close proximity to inter-modal rail hubs.

• This enables these elevators the option to truck their soybeans and soybean meal to trans-loaders

near the inter-modal yards at low trucking costs and affords them access to the export market at

competitive prices.

Page 57

Chicago area railroad intermodal map

Page 58

Railway companies’ intermodal ramps in Illinois

UPRR

Intermodal ramp Port

Chicago (Global I- 14th St.), IL

Chicago (Global II- Northlake), IL

Chicago (Global III- Rochelle), IL

Chicago (Global IV- Joliet), IL

Yard Center, IL

Dupo/St. Louis, IL

Los Angeles

Long Beach

Oakland

Portland

Seattle

Page 59

BNSF

Intermodal ramp Port

Chicago (Cicero), IL

Chicago (Corwith), IL

Chicago (Willow Springs), IL

Logistics Park (Elwood), IL

St. Louis

Seattle

Tacoma

Portland

Los Angeles

Long Beach

Oakland

CNRR

Intermodal ramp Port

Chicago, IL (16800, S. Center

St., Harvey, IL)

Belledune, NB

Halifax, NS

Mobile, AL

Montreal, QC

New Orleans, LA

Prince Rupert, BC

Saint John, NB

Vancouver, BC

CPR

Intermodal ramp Port

Chicago (Schiller Park), IL

Chicago (Bensenville), IL

Montreal, QC

Vancouver, BC

• The UP and BNSF rail lines have access to major ports

on the West Coast, while the CN and CP (the major

Canadian rail lines) have access to ports in the Lakes,

Gulf and West Coast regions.

Page 60

Railway companies’ intermodal ramps in Illinois

CSX

Intermodal ramp Port

E. St. Louis, IL

Chicago (59th St.), IL

Chicago (Bedford Park), IL

Boston

New York/New Jersey

(EMT/NYCT/PNCT)

Philadelphia

Baltimore

Norfolk

Charleston

Savannah

Jacksonville

Ft. Lauderdale

Miami

Tampa

Norfolk Southern

Intermodal ramp Port

Chicago, IL-47th Street

Chicago, IL-63rd

Chicago, IL-Calumet (2040 East

106th Street)

Chicago, IL-Landers (7540 S.

Western Avenue)

Decatur, IL

New York/New Jersey

Baltimore

Norfolk

Charleston

Savannah

Jacksonville

Miami

• The CSX and Norfolk Southern operate almost exclusively on the East Coast.

UP system map

Page 61

UP Intermodal facilities in Illinois

• Global I, Illinois 14th St., Chicago

• Global II, Illinois Northlake, IL

• Global III, Illinois Rochelle, IL

• Global IV, Illinois Joliet, IL

• Yard Center, Illinois Dolton, IL

Page 62

• Dupo, Illinois (St. Louis)

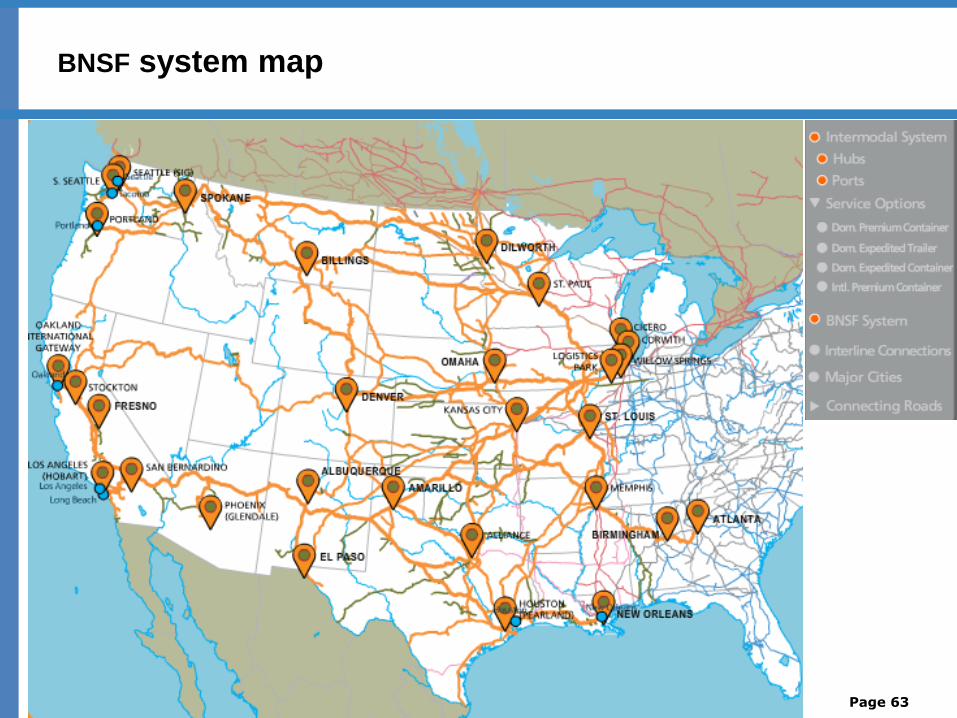

BNSF system map

Page 63

CSX system map

Page 64

Norfolk Southern system map

Page 65

CNRR system map

Page 66

CNRR ships grains to Asia

Page 67

CPR system map

Page 68

Table of contents

1. Executive Summary

2. Overview of U.S. and Illinois soybeans and soybean trade flows

3. Major players in the U.S. and Illinois container shipping industry

4. Landed price analysis of soybeans and soybean meal moving from

Illinois to major destination markets

4. Recommendations for increasing container movements of Illinois

soybeans and soybean meal

Page 69

Landed prices of containerized and bulk soybean shipments to Asia

Page 70

Illinois Bulk vs. Container Shipments to Asia ($/MT) China Japan South Korea Taiwan Philippines Vietnam

Container(ex. Illinois) $ 86.00 $ 105.00 $ 95.00 $ 82.00 $ 84.00 $ 84.00

PNW - Bulk

Rail $ 52.40 $ 52.40 $ 52.40 $ 52.40 $ 52.40 $ 52.40

Ocean $ 28.00 $ 27.00 $ 28.00 $ 30.00 $ 31.00 $ 33.00

PNW Total $ 80.40 $ 79.40 $ 80.40 $ 82.40 $ 83.40 $ 85.40

Gulf - Bulk

Barge $ 20.15 $ 20.15 $ 20.15 $ 20.15 $ 20.15 $ 20.15

Ocean $ 40.00 $ 39.00 $ 40.00 $ 42.00 $ 42.00 $ 43.00

Gulf Total $ 60.15 $ 59.15 $ 60.15 $ 62.15 $ 62.15 $ 63.15

East Coast – Bulk

Rail $ 35.99 $ 35.99 $ 35.99 $ 35.99 $ 35.99 $ 35.99

Ocean $ 59.00 $ 56.00 $ 59.00 $ 61.00 $ 62.00 $ 64.00

East Coast Total $ 94.99 $ 91.99 $ 94.99 $ 96.99 $ 97.99 $ 99.99

Container vs. PNW Bulk $ 5.60 $ 25.60 $ 14.60 $ (0.40) $ 0.60 $ (1.40)

Container vs. Gulf Bulk $ 25.85 $ 45.85 $ 34.85 $ 19.85 $ 21.85 $ 20.85

Container vs. E. Coast Bulk $ (8.99) $ 13.01 $ 0.01 $ (14.99) $ (13.99) $ (15.99)

• Container freight rates out of Illinois are very competitive to all major Asian markets except Japan vs. bulk

freight rates off of the East Coast. Illinois containerized soybean exports are not competitive to China, Japan

and South Korea with bulk rates out of the PNW but are competitive to Taiwan, the Philippines and Vietnam.

Containerized soybean exports are not competitive to any Asian market compared to bulk rates out of the Gulf

due to the efficiencies of moving soybeans by barge to the Gulf.

Domestic: bulk rail rates from origins to PNW and east coast

• Rail costs from different locations in the

Midwest to east coast ports (Brunswick,

GA/ Norfolk, VA) fall in the range of $33

/MT to $36.7/MT. The most economical

route is Columbus, OH – Norfolk and the

route from Gibson City, IL to Brunswick is

the most expensive. This is due to the

fact that Illinois is further from the major

East Coast ports than most other

locations in the Eastern Corn Belt.

Page 71

$34.5

$35.0

$35.5

$36.0

$36.5

$37.0$

/ m

etri

c to

n

Rail rates from origins to east coast (Brunswick)

Source: rates quoted by Transportation Consultants Co. in April, 2011

• Illinois has a significant disadvantage in

shipping soybeans and soybean meal to PNW

compared with North Dakota, Nebraska, and

Minnesota in terms of rail cost. This is largely

due to the increased distance from Illinois to

the PNW in comparison with the other

markets. It costs 12% more to move

soybeans from Ruff, IL to PNW ports than from

Jamestown, ND to PNW ports. Union Pacific

does not publish rates from Illinois to the PNW.

.

$44

$46

$48

$50

$52

$54

$/m

etri

c to

n

Rail rates from origins to PNW

• Illinois has a substantial barge freight advantage over Iowa and Minnesota for moving

soybeans and soybean meal to the Gulf. In addition, the Illinois, Ohio and Mississippi

Rivers are open year round except in the far north of Illinois..

Page 72

Domestic: bulk barge rates from origins to NOLA

Source: rates quoted by Transportation Consultants Co. in April, 2011

$5

$10

$15

$20

$25

$30

$35

$40

$45

$/

met

ric

ton

Barge rates from origins to Asia PEKIN ST. PAUL IOWA ST. LOUIS CINCINNATI MT. VERNON/ HENDERSON

Bulk Ocean freight rates from U.S. to Asia

• The PNW is most competitive in terms of bulk ocean freight cost to Asia. On average,

it costs twice as much to ship soybeans from the East Coast to Asia than from PNW to

Asia.

Page 73

Source: rates quoted by Transportation Consultants Co. in April, 2011

$25

$30

$35

$40

$45

$50

$55

$60

$65

$70

China Yokohama Inchon/Pusan Taiwan Manila Ho Chi Minh

City

Kuala

Lumpur

Jakarta Singapore

$/

sho

rt t

on

Bulk ocean freight rates (from US to Asia) comparison

Long Beach Portland NOLA Brunswick, GA

• Southern California offers the most competitive container freight rates to Asia and also

has the most available containers. On average, container freight rates to Asia are over

10% higher in PNW, 20% higher in east coast, and 30% higher in Gulf than in

Southern California.

Page 74

Container ocean freight rates from U.S. to Asia

$75

$85

$95

$105

$115

$125

$135

China Yokohama S. Korea Kaohsiung Manila Ho Chi Minh City

$/m

etri

c to

n

Container freight rates (from US to Asia) comparison

Long Beach, CA. Portland, OR. NOLA Brunswick, GA

Source: rates quoted by Transportation Consultants Co. in April, 2011

Freight rate comparison from origins to Asia via container

Note: When container rates are quoted, they are not quoted with a specific route. The 3rd party logistics company decides the most

economical route, but it is not up to the shipper.

Page 75

Source: rates quoted by Transportation Consultants Co. in April, 2011

$80

$100

$120

$140

$160

$180

China Yokohama S. Korea Kaohsiung Manila Ho Chi Minh City

$/

met

ric

ton

Container rates from origins to Asia BNSF ramp at Chicago Central IL Central IA Central MN Central KS

• Chicago is the largest container hub in Midwest and the largest rail hub across the nation.

• As a result, there are more containers available in Chicago in particular and in Illinois in general

than in Iowa or Minnesota resulting in lower container shipping costs in Illinois. Illinois has a 8.6%

container freight rate advantage over Iowa and a 14% advantage over Illinois due to container

availability, which is the driver of price.

• The cost of exporting soybeans in bulk from Illinois through the PNW to Asia is nearly 7% higher

than that of exporting soybeans from Nebraska and North Dakota on average. However, the bulk

freight rate for shipping soybeans from Illinois to Asia is still lower than shipping from the East

Coast.

Page 76

Freight rate comparison from origins to Asia via bulk (1)

Source: rates quoted by Transportation Consultants Co. in April, 2011

$75

$79

$83

$87

$91

China Yokohama S. Korea Taiwan Manila Ho Chi Minh

City

Kuala Lumpur Jakarta Singapore

$/

met

ric

ton

Freight rates to Asia (through PNW) Fremont, NE Ruff, IL Hinton, IA Templeton, IA Murdock, MN Lamberton, MN Alton, ND Jameston, ND

• The differences of shipping costs to Asia through ports on the Atlantic coast among

different locations in Illinois, Indiana and Ohio are negligible but highest in Illinois.

Page 77

Freight rate comparison from origins to Asia via bulk (2)

Source: rates quoted by Transportation Consultants Co. in April, 2011

$95

$99

$103

$107

$111

China Yokohama S. Korea Taiwan Manila Ho Chi Minh

City

Kuala Lumpur Jakarta Singapore

$/

met

ric

ton

Freight rates to Asia (through Atlantic coast)

Gibson City, IL Sidney, IL Clymers, IN Montpelier, IN Columbus, OH Lima, OH

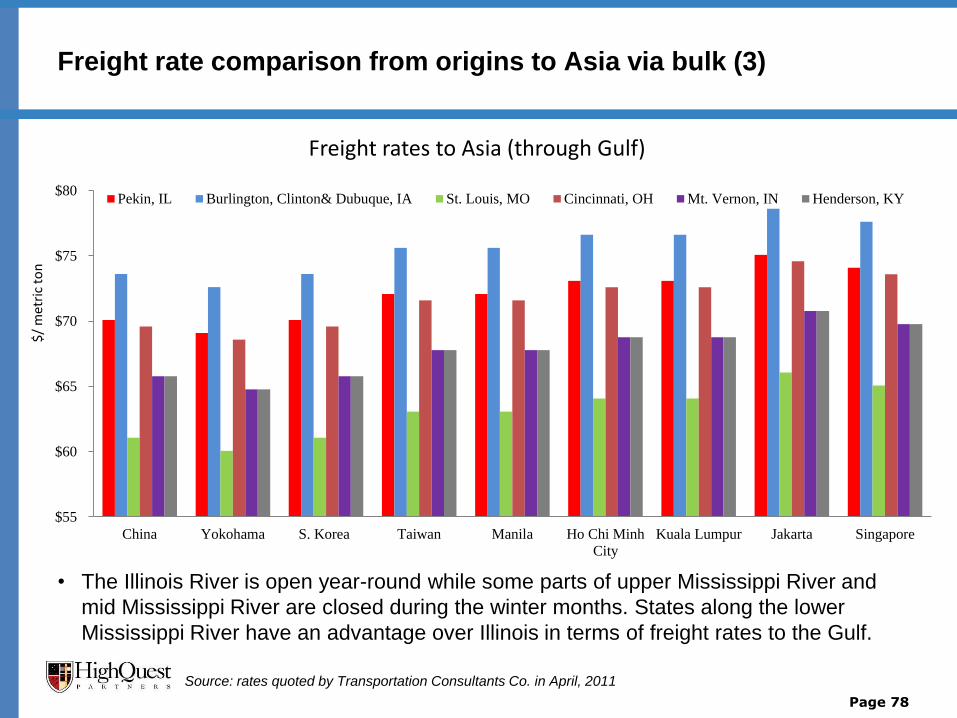

• The Illinois River is open year-round while some parts of upper Mississippi River and

mid Mississippi River are closed during the winter months. States along the lower

Mississippi River have an advantage over Illinois in terms of freight rates to the Gulf.

Page 78

Freight rate comparison from origins to Asia via bulk (3)

$55

$60

$65

$70

$75

$80

China Yokohama S. Korea Taiwan Manila Ho Chi Minh

City

Kuala Lumpur Jakarta Singapore

$/

met

ric

ton

Freight rates to Asia (through Gulf)

Pekin, IL Burlington, Clinton& Dubuque, IA St. Louis, MO Cincinnati, OH Mt. Vernon, IN Henderson, KY

Source: rates quoted by Transportation Consultants Co. in April, 2011

Table of contents

1. Executive Summary

2. Overview of U.S. and Illinois soybeans and soybean trade flows

3. Major players in the U.S. and Illinois container shipping industry

4. Landed price analysis of soybeans and soybean meal moving from

Illinois to major destination markets

4. Recommendations for increasing container movements of Illinois

soybeans and soybean meal

Page 79

Conclusions –grain exporting market outlook

• The significant growth in containers moving from Asian manufacturing plants to U.S.

consumer markets has generated a tremendous opportunity to use backhaul flow of

containers to Asia to ship grains to the region. U.S. containerized soybean exports

have increased about 160% since 2000 to over 91,000 TEUs in 2010, accounting for

4.7% of total soybean exports.

• South East Asia is the region importing the largest volume of containerized soybeans

and soybean meal from the U.S., accounting for 62% of total U.S. grain exports via

container. As new sources for low cost production of manufactured goods continue to

develop in Southeast Asia, demand for filling backhaul containers returning to this

region will increase. This presents a growing opportunity for U.S. soybean exporters.

• The prospects for containerized U.S. soybean and soybean meal exports to Asia are

promising because of:

– increasing grain and protein demand in Asia, particularly in China and Southeast Asia;

– rising imbalance of US- Asia containerized trade (2.6:1) leaving more opportunities for

container backhauls and

– the expansion of the Panama Canal which will bring larger container vessels to the Gulf coast

providing opportunities to barge containers from the Midwest to Gulf ports.

Page 80

Conclusions – container market outlook

• Global containership capacity has increased to nearly 14 million TEUs, representing

approximately a 286% increase in the last decade. Over-capacity in the containership

market is expected to last for at least one more year, which should put downward

pressure on container freight rates.

• The rising demand for containers in Asia due to the explosion in intra-Asian trade has

led to a global shipping container shortage. It is estimated that the industry needs up to

6 million containers (2 years’ worth of production) to restore the imbalance to

conventional levels.

• However, there are a large volume of containers available in the southern California

and south Atlantic port regions due to the imbalance of container traffic between the

U.S. and Asia. Westbound containerized soybean and soybean meal exports

represent good business for ocean carriers because they help to minimize costs to

reposition containers to Asia.

• Union Pacific Railroad Co., is building a transloading facility transferring grains from

covered hopper cars directly to containers in Barstow/Yermo area, just outside of the

L.A. Basin and before the congested rail corridors.

Page 81

Recommendation – new transloading facility

• We recommend that the Illinois Soybean Association consider making an

investment to build a transloading facility in Peoria, IL to drive the future

growth of containerized Illinois soybean and soybean meal exports to Asia.

– Peoria, which is one of hubs of the grain marketing network in Illinois, is

located about 180 miles southwest of Chicago, the largest container hub

in Midwest and the nation’s largest rail hub and is also a major industrial

center.

– Because of competitiveness of bulk shipping, soybeans and soybean

meal must be located adjacent to intermodal facilities to avoid costly

drayage costs. Peoria is located about 78 miles northwest of Decatur

which is a Norfolk Southern inter-modal terminal, about 117 miles

southwest of UP’s intermodal ramp in Joliet and 113 miles southwest of

the BNSF Logistics Park inter-modal ramp.

– Peoria is the largest city on the Illinois River. The expansion of Panama

Canal will create more opportunities to ship containerized soybeans and

soybean meal via barge from the Illinois River to Gulf ports.

Page 82