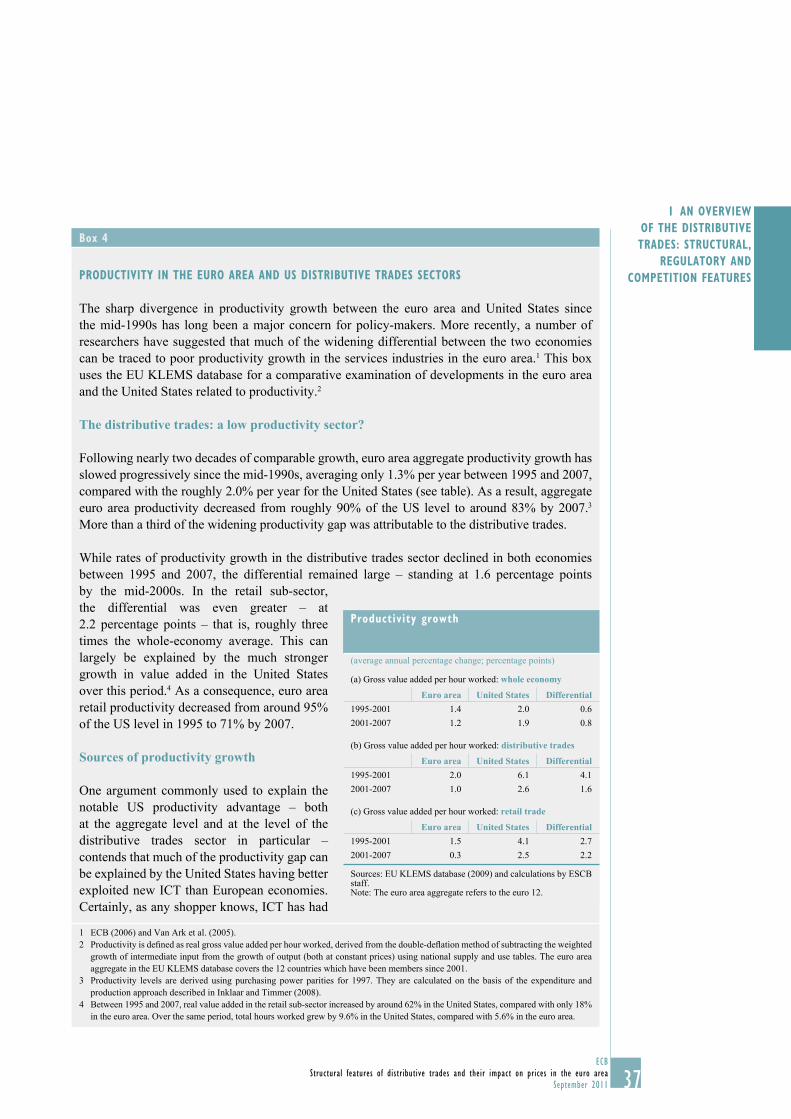

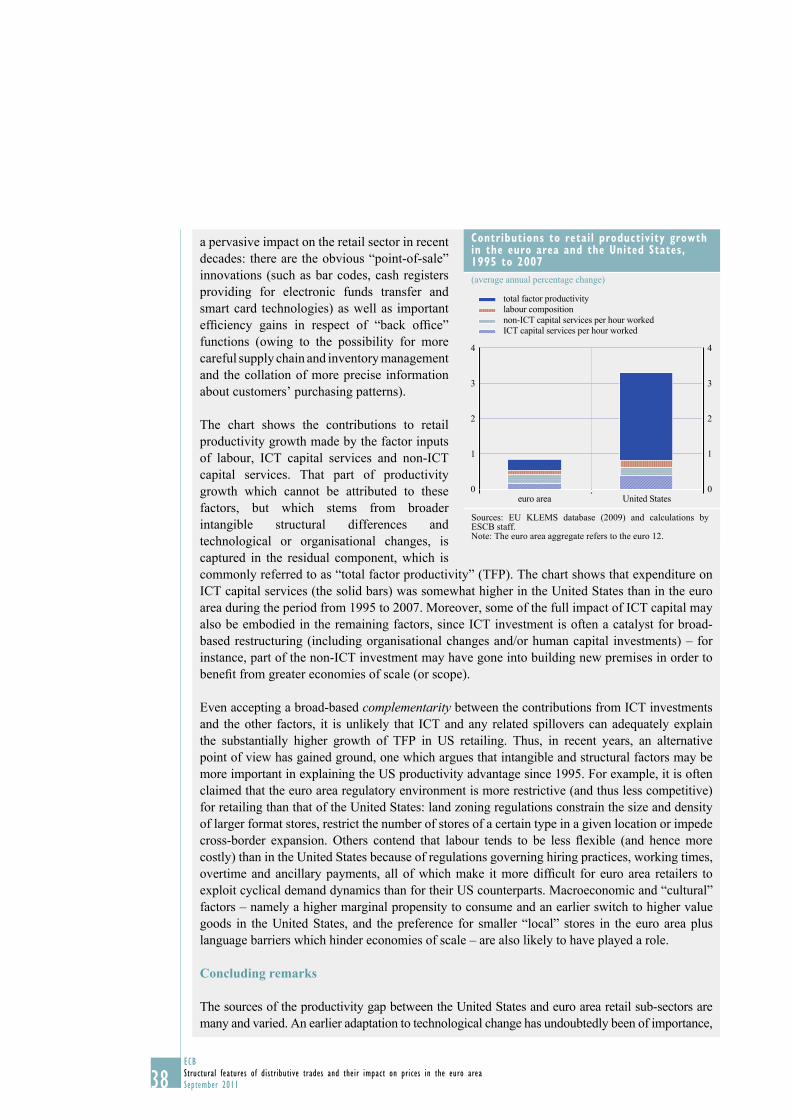

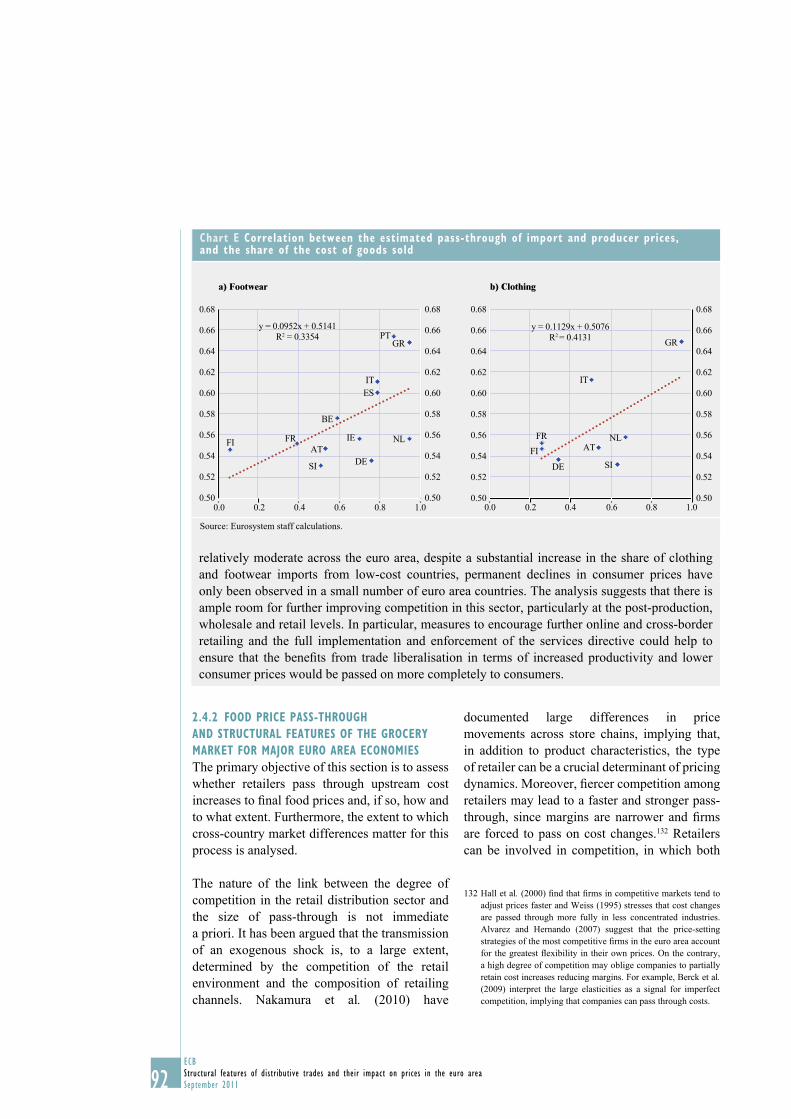

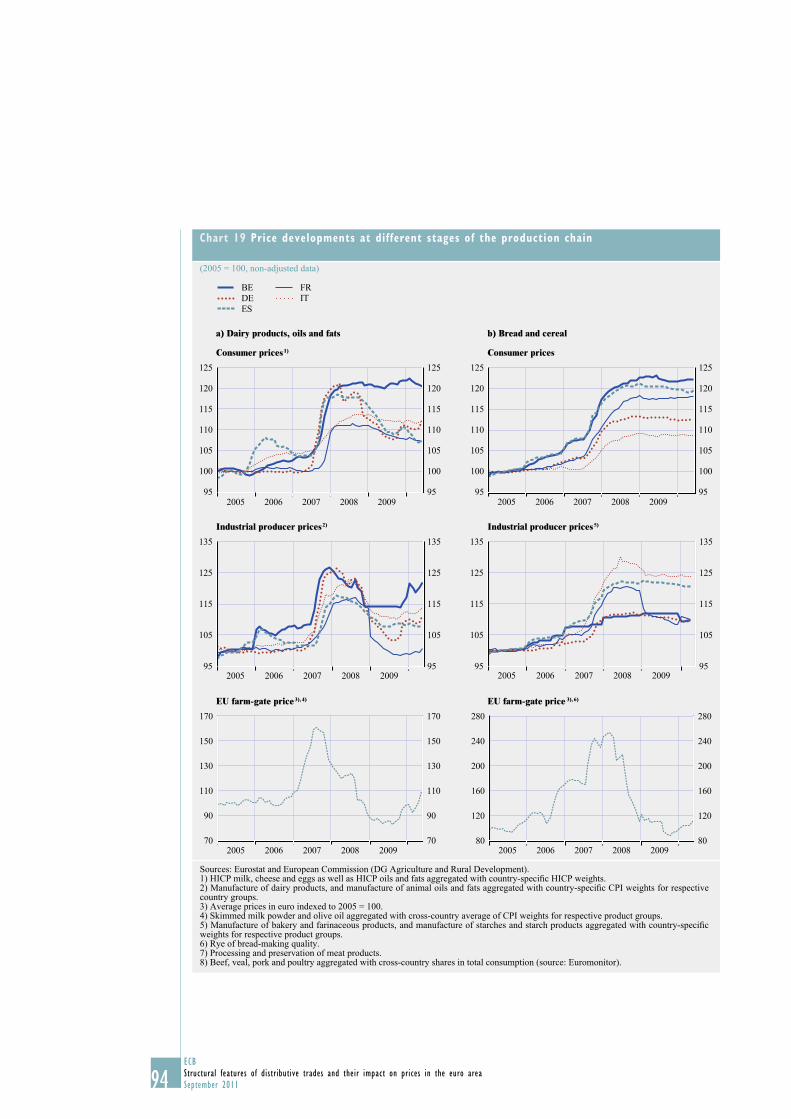

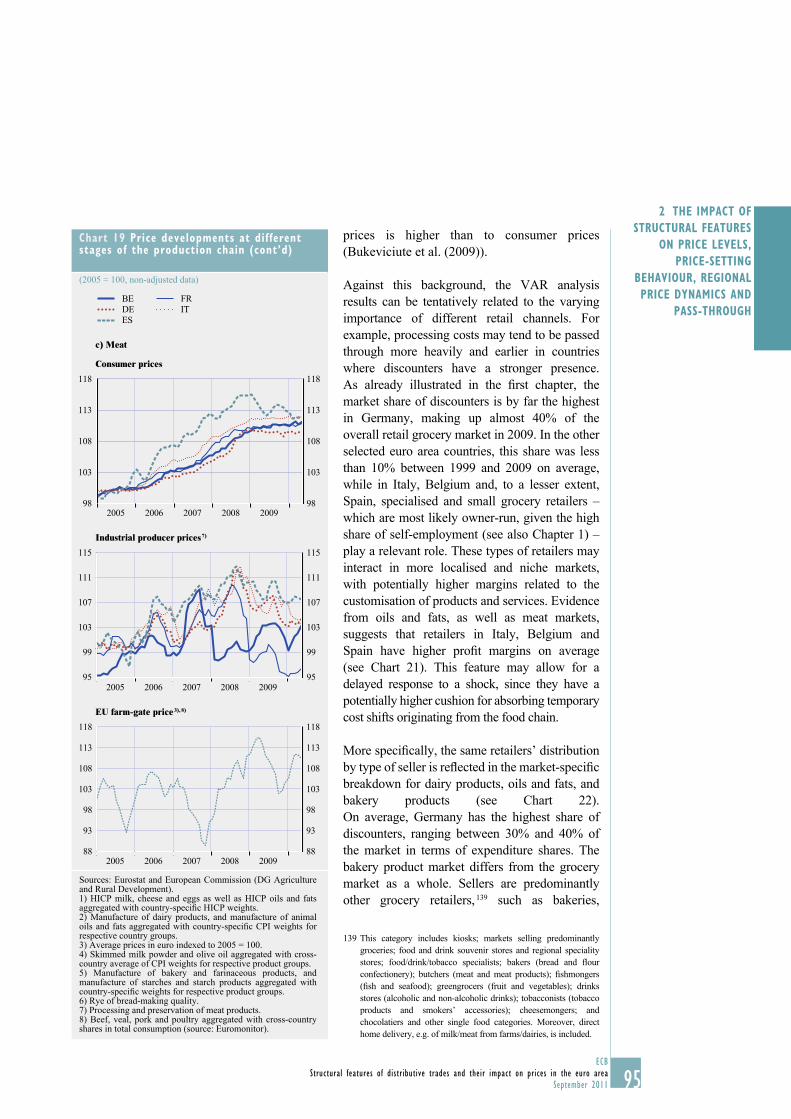

structural features of distributive trades and their impact on prices in

TRANSCRIPT

EURO

PEAN

CEN

TRAL

BAN

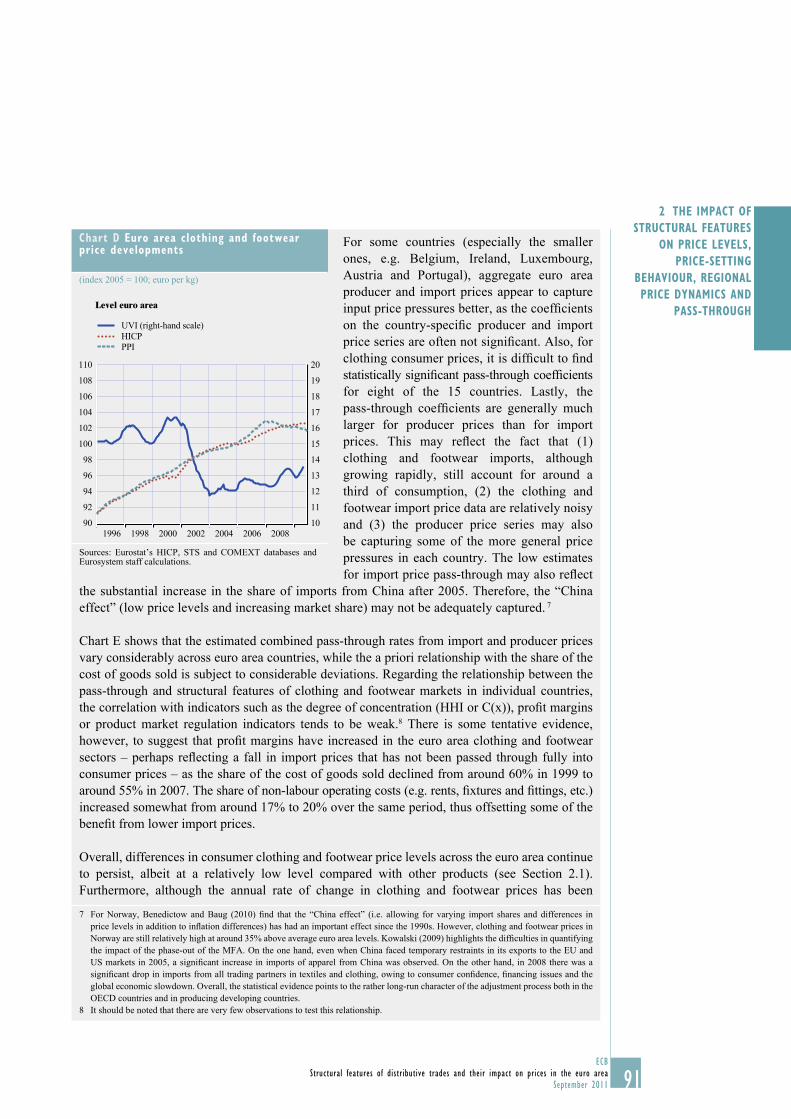

K

STRU

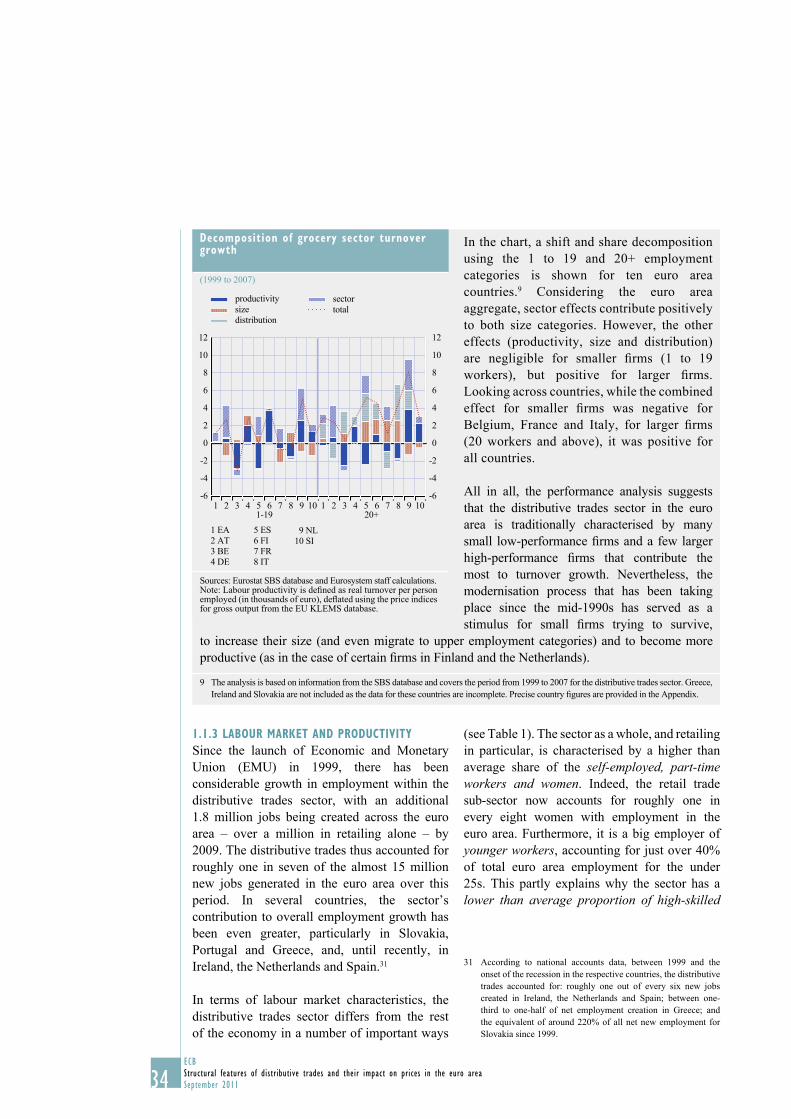

CTU

RAL

FEAT

URE

S O

F D

ISTR

IBU

TIVE

TRA

DES

SE

PTEM

BER

2011

STRUCTURAL FEATURES OF D I STR IBUT IVE TRADES AND THE IR IMPACT ON PR ICES IN THE EURO AREA

SEPTEMBER 2011

Structural Issues Report

STRUCTURAL FEATURES

OF DISTRIBUTIVE TRADES

AND THEIR IMPACT ON PRICES

IN THE EURO AREA

SEPTEMBER 2011

STRUCTURAL ISSUES REPORT

In 2011 all ECBpublications

feature a motiftaken from

the €100 banknote.

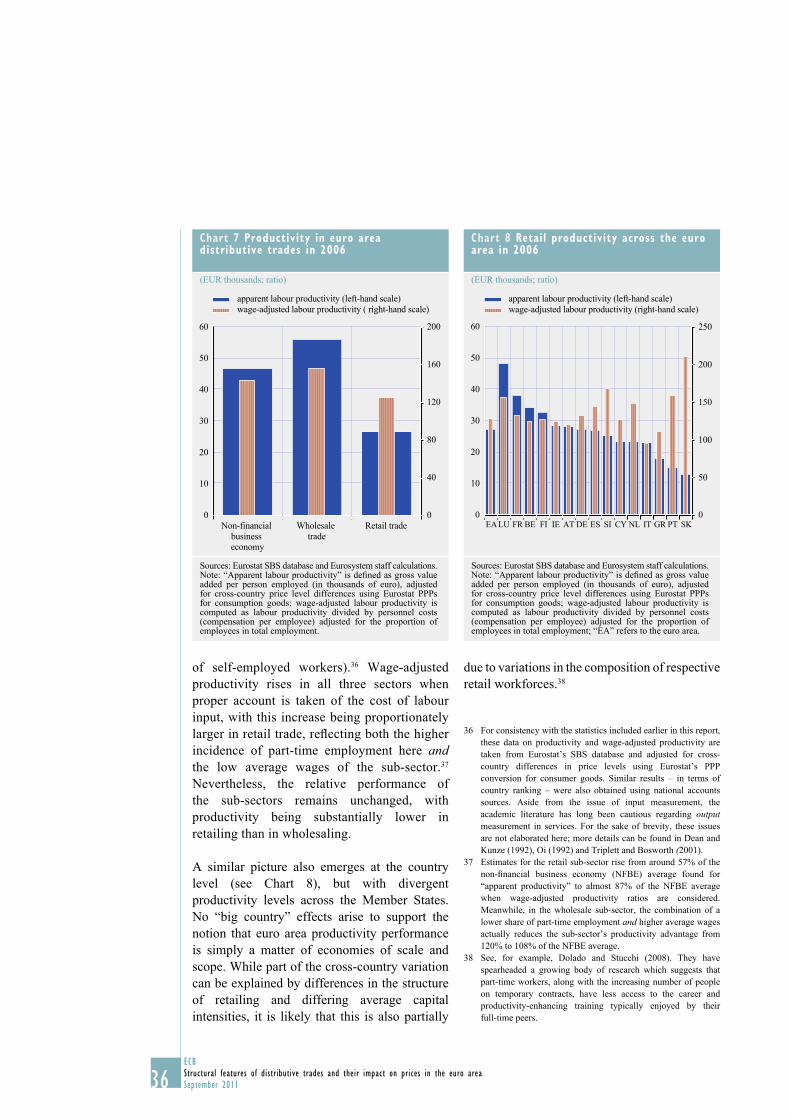

© European Central Bank, 2011

Address Kaiserstrasse 29

60311 Frankfurt am Main

Germany

Postal address Postfach 16 03 19

60066 Frankfurt am Main

Germany

Telephone +49 69 1344 0

Website http://www.ecb.europa.eu

Fax +49 69 1344 6000

All rights reserved. Any reproduction, publication or reprint in the form of a different publication, whether printed or produced electronically, in whole or in part, is permitted only with the explicit written authorisation of the ECB or the author(s).

ISBN 978-92-899-0820-7 (print)

ISBN 978-92-899-0821-4 (online)

3ECB

Structural features of distributive trades and their impact on prices in the euro area

September 2011

CONTENTS

EXECUTIVE SUMMARY 7

INTRODUCTION AND MOTIVATION 12

1 AN OVERVIEW OF THE DISTRIBUTIVE

TRADES: STRUCTURAL, REGULATORY

AND COMPETITION FEATURES 15

1.1 The importance, structure

and performance of the

distributive trades sector 15

1.1.1 Defi nitional issues 15

1.1.2 A closer look at the

grocery trade 17

1.1.3 Labour market

and productivity 34

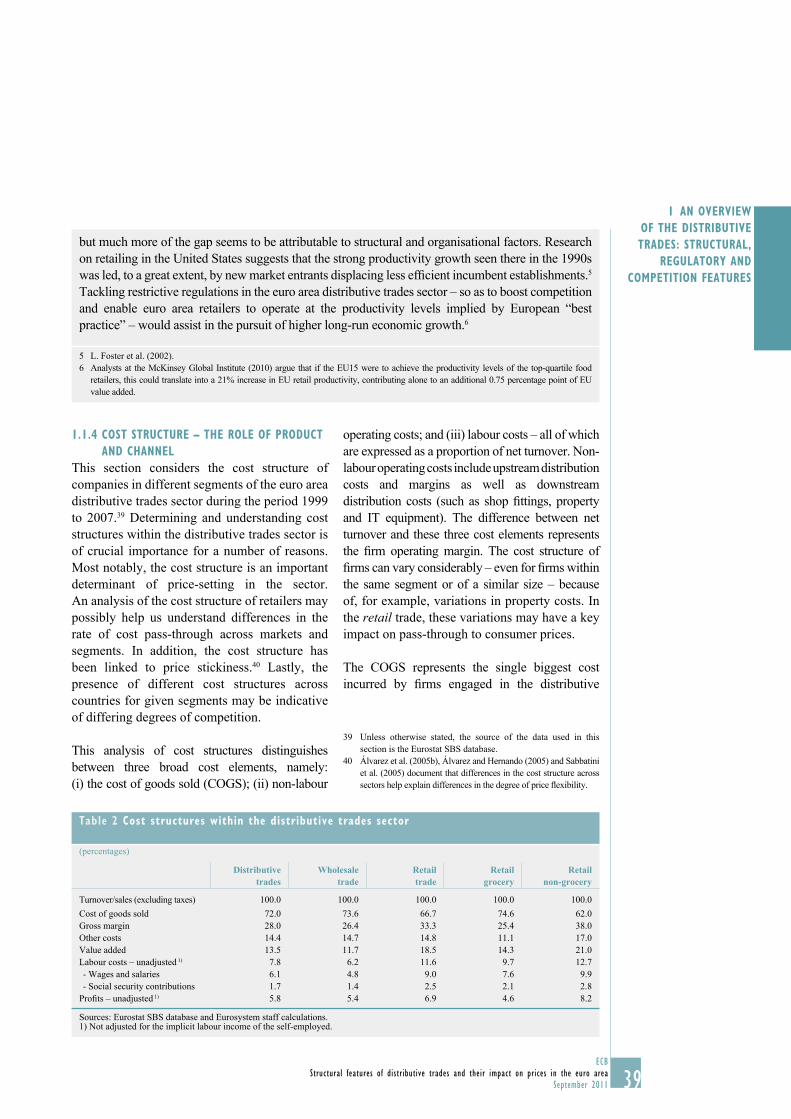

1.1.4 Cost structure – the role of

product and channel 39

1.2 Regulation in the distributive

trades sector 40

1.3 Competition in the distributive

trades 43

1.3.1 Conceptual overview 44

1.3.2 Empirical measures

of competition using

national data 47

1.3.3 Empirical measures

of competition using

store-level data 50

2 THE IMPACT OF STRUCTURAL FEATURES

ON PRICE LEVELS, PRICE-SETTING

BEHAVIOUR, REGIONAL PRICE DYNAMICS

AND PASS-THROUGH 60

2.1 The impact of structural features

on price level differences 60

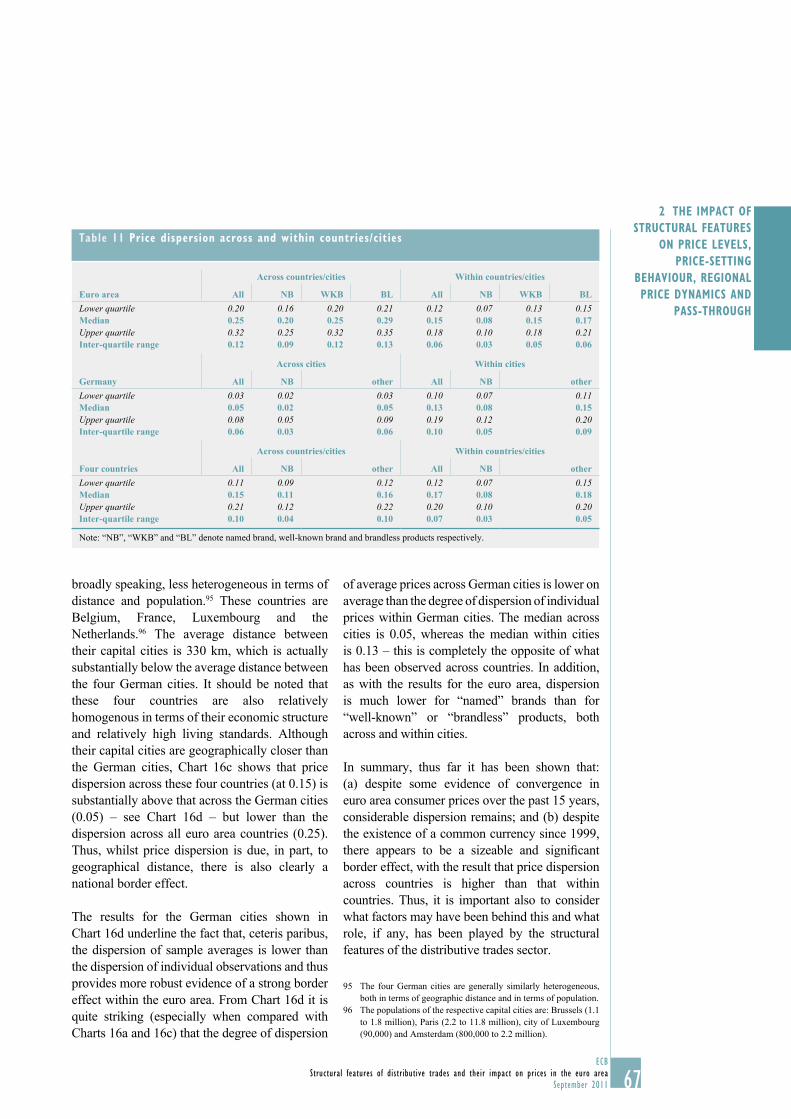

2.1.1 Introduction

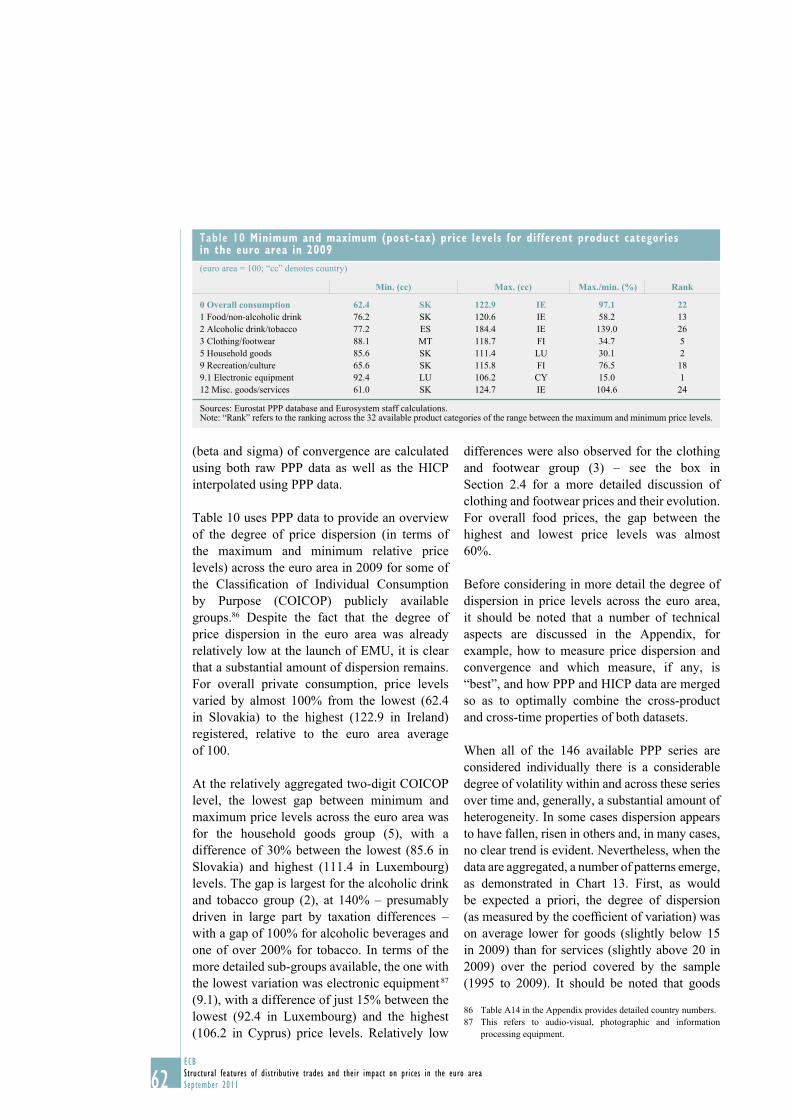

and motivation 60

2.1.2 The degree of price

dispersion and convergence 61

2.1.3 Is there a “border effect”

on prices? 65

2.1.4 The impact of the structural

features of the distributive

trades sector 68

2.2 Competition, outlet type and the

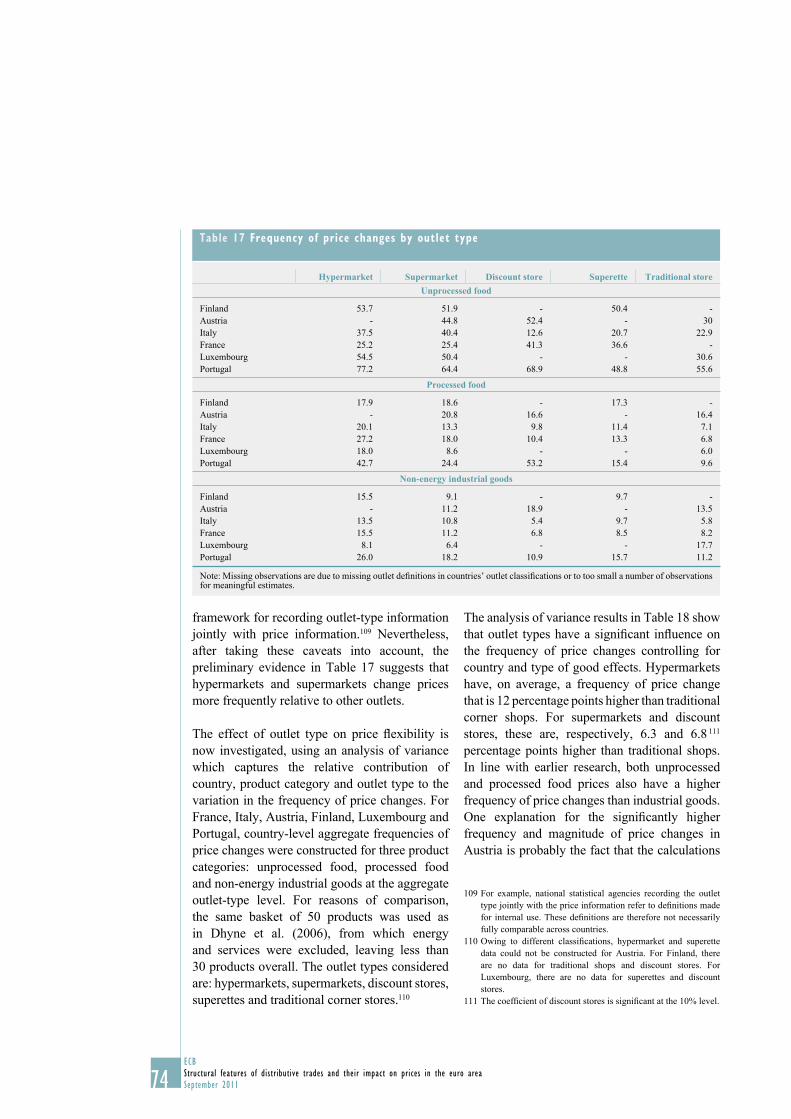

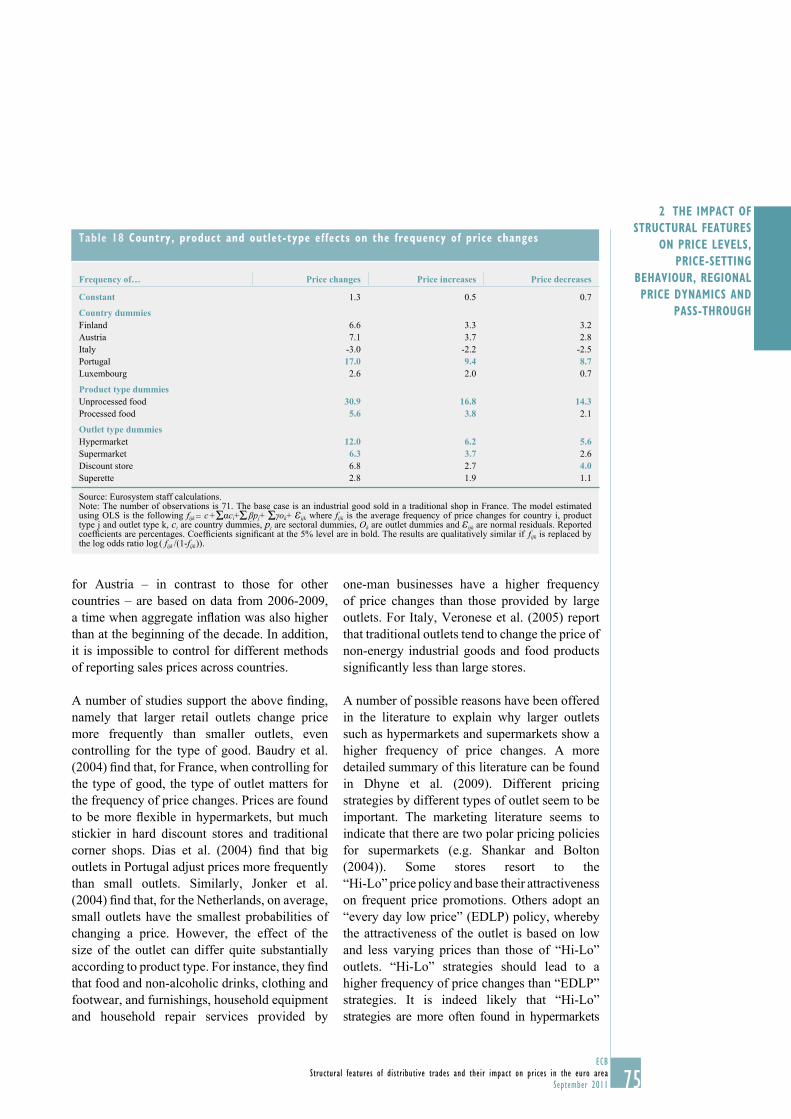

frequency of price changes 71

2.3 Retail sector concentration

and price dynamics: a regional

level analysis 76

2.4 The retail trades

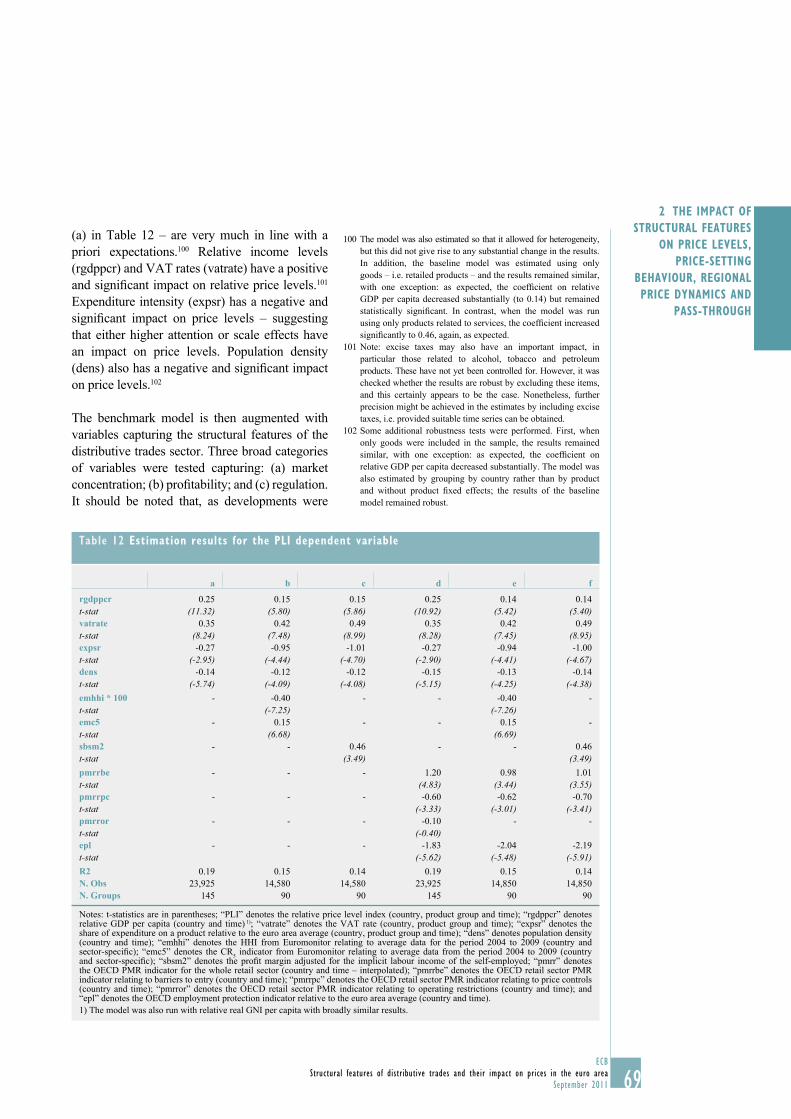

and pass-through 83

2.4.1 Pass-through into consumer

non-energy industrial

goods prices 84

2.4.2 Food price pass-through

and structural features

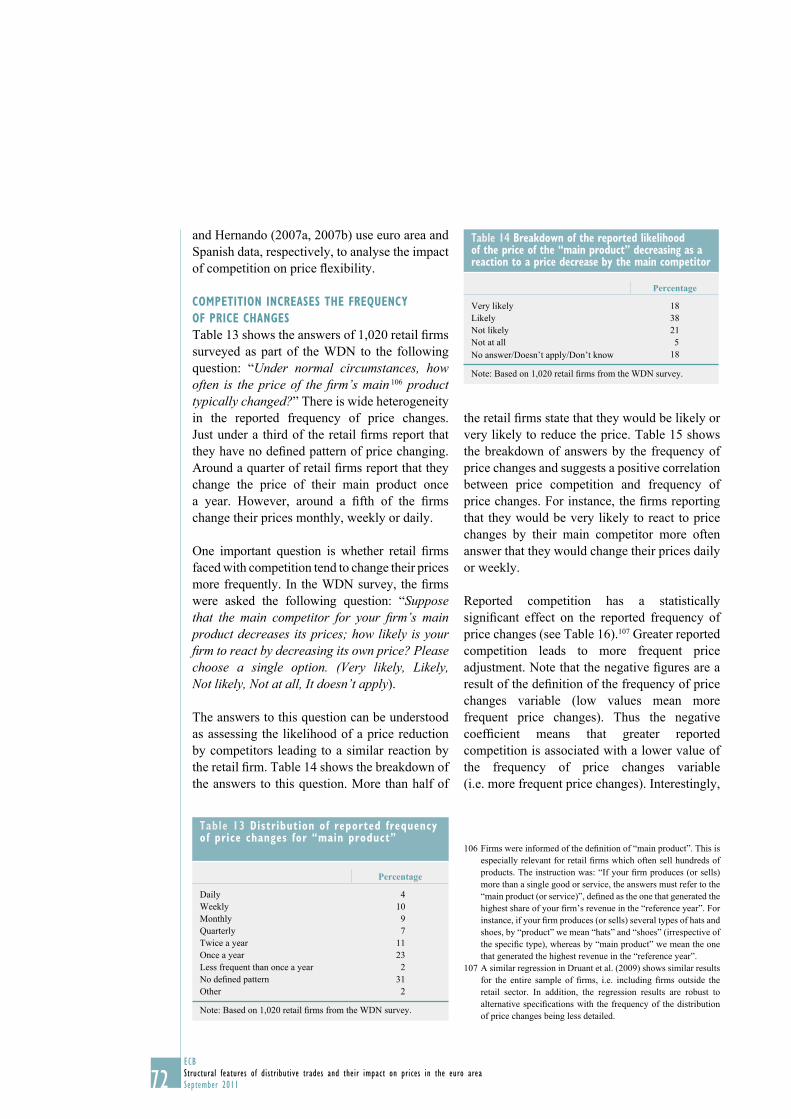

of the grocery market for

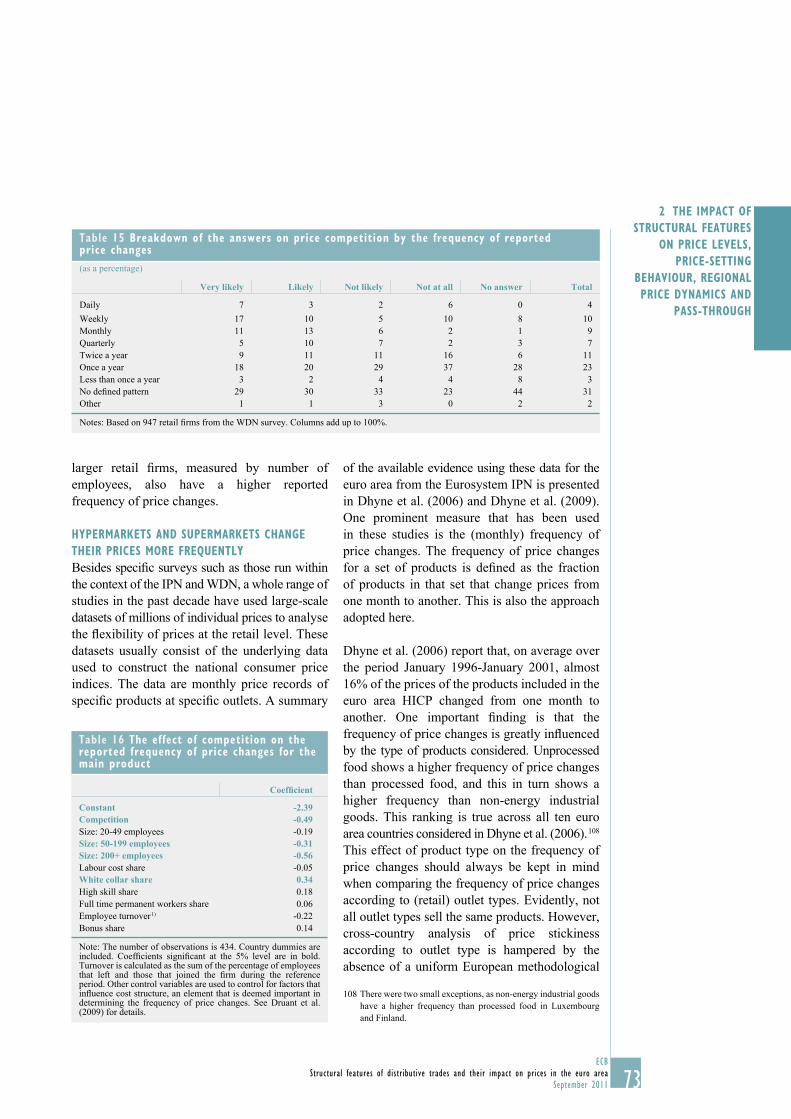

major euro area economies 92

ANNEXES 99

1 Additional country data

and background information 99

2 Additional technical

and background material 121

REFERENCES 131

LIST OF BOXES:

Online retail trade and the degree 1

of cross-border retail commerce 21

Implications of developments 2

in the retail trade structure

for infl ation measurement 27

Firm demographics, fi rm size and 3

performance analysis 32

Productivity in the euro area 4

and US distributive trades sectors 37

The distributive trades 5

in the new Member States 55

The impact of increased competition 6

in the distributive sector on employment

and output – a DSGE model analysis 81

Developments in clothing and footwear 7

prices 88

CONTENTS

4ECB

Structural features of distributive trades and their impact on prices in the euro area

September 2011

COUNTRIES

BE Belgium

DE Germany

EE Estonia

IE Ireland

GR Greece

ES Spain

FR France

IT Italy

CY Cyprus

LU Luxembourg

MT Malta

NL Netherlands

AT Austria

PT Portugal

SI Slovenia

SK Slovakia

FI Finland

ABBREVIATIONS AND GLOSSARY

OTHER

COGS cost of goods sold

COICOP Classifi cation of Individual Consumption According to Purpose

CPI Consumer Price Index

CRk k-fi rm concentration ratio

DSGE dynamic stochastic general equilibrium

ECB European Central Bank

EMU Economic and Monetary Union

EPL employment protection legislation

ESCB European System of Central Banks

EU European Union

FDI foreign direct investment

GDP gross domestic product

HHI Herfi ndahl-Hirschman Index

HICP Harmonised Index of Consumer Prices

ICT information and communication technology

IPN Infl ation Persistence Network

NACE statistical classifi cation of economic activities in the European Union

NCB national central bank

NUTS Nomenclature of Territorial Units for Statistics

OECD Organisation for Economic Co-operation and Development

PMR product market regulation

PPLD pseudo price level data

PPP purchasing power parity

RPLI relative price level index

SBS structural business statistics

TFP total factor productivity

VAT value added tax

WDN Wage Dynamics Network

5ECB

Structural features of distributive trades and their impact on prices in the euro area

September 2011

ABBREVIATIONS

AND

GLOSSARYGLOSSARY

Buying group: a group that uses the collective bargaining power of its members (fi rms and

entrepreneurs) to negotiate more competitive product prices.

Discounter: a retail entity that typically uses a relatively small sales area to offer a limited range of

products at a discounted price.

Hypermarket: a retail facility that combines a supermarket and a department store and usually has

a sales area of above 2,500m².

Non-fi nancial business sector: comprises the total economy, excluding the agriculture and fi shing,

fi nancial intermediation services and public services sectors.

Private label: the own company brand of a retailer (usually produced by an outside fi rm).

Quaranta table: a diagnostic tool for the checking and approval of purchasing power parity survey

results.

7ECB

Structural features of distributive trades and their impact on prices in the euro area

September 2011

EXECUTIVE

SUMMARYEXECUTIVE SUMMARY

The distributive trades sector, which is primarily

accounted for by wholesale and retail trade,

is not only economically important in its own

right, but also relevant to monetary policy.

Ultimately, it is retailers who set the actual

prices of most consumer goods. They are the

main interface between producers of consumer

goods and consumers, with around half of

private consumption accounted for by retail

trade. The “value added” of this intermediation

service can be substantial, as this accounts for,

on average, about 25% of consumer prices.

The purpose of this report is to analyse the

structural features of the distributive trades

sector and the developments within it, as well

as how these may infl uence prices and price

dynamics.

Several aspects are relevant. From a monetary

policy point of view, increasing the degree of

competition in the distributive trades sector

may have effects not only on price levels,

but also on price dynamics, via a reduction in

mark-ups, an increase in price fl exibility and a

greater and more rapid pass-through of changes

in costs to prices. Structural developments,

such as the increasing market penetration of

hard discounters, online trade and private label

brands, the role of buying groups and the relative

bargaining power between producers and

retailers are of great importance to consumers

and price determination. In addition, these

may have implications for the measurement of

consumer prices and infl ation. More generally,

the distributive trades sector plays an important

role in determining cross-country differentials

in productivity growth, both within and outside

Europe: the sector has accounted for over

one-third of the widening gap in aggregate

productivity between the euro area and the

United States since the mid-1990s.

A specifi c contribution of this report is the use

of a wide range of data sources,1 including a

unique dataset on the location of over 100,000

individual grocery stores across most of the euro

area, to investigate how to better measure the

degree of competition and concentration in this

sector, and to compare sector developments

from a national, regional and local perspective.

AN OVERVIEW OF THE DISTRIBUTIVE

TRADES SECTOR

The distributive trades sector covers three broad

sub-sectors: motor, wholesale and retail trade.

This report primarily focuses on wholesale and

retail trade. In general, wholesalers intermediate

between fi rms, whereas retailers intermediate

between fi rms and consumers. Depending on

which measure is considered, the distributive

trades account for a varying proportion of the

non-fi nancial business sector: around one-third

in terms of total turnover, number of fi rms and

self-employment and around 15% to 25% in

terms of other measures, such as value added

and overall employment. Although by some

measures (most notably value added) the

wholesale trade sub-sector is larger than the retail

trade sub-sector, this report focuses on the latter

owing to the fact that it is closer to consumers

and consumer prices; retail trade is also more

important with regard to direct employment.

The distributive trades in general, and retail trade

in particular, have a number of distinguishing

features in relation to the rest of the non-fi nancial

business sector. They are generally more labour-

intensive and have more lower-skilled workers

on average. Profi t margins in both retail and

wholesale trade are below average, but this

may simply refl ect a high degree of turnover

(per unit of capital employed) rather than strong

competitive pressures.

The retail trade sub-sector also displays

signifi cant diversity across both euro area

In particular, it utilises: (i) time series provided by national 1

statistical institutes on regional consumer price indices broken

down across a number of product groups, as well as information

from private databases (such as store location data from Nielsen

and retailing and consumer goods-related modules from

Euromonitor Passport); (ii) detailed data and the “Quaranta

tables” from Eurostat’s PPP database; (iii) individual price

and survey data collected under both the Infl ation Persistence

Network and Wage Dynamics Network of the Eurosystem; and

(iv) country-specifi c information provided by ESCB staff, which

is used to construct a new indicator of the degree of regulation on

shop opening times.

8ECB

Structural features of distributive trades and their impact on prices in the euro area

September 2011

countries and segments. Substantial price

differences exist between branded and private

label goods and also across store types. The

rapid growth of discounters, of private label

brands and of online trade, clearly visible to

consumers, has had a noteworthy impact, but this

has been of varying importance across countries.

Buying groups affecting the bargaining power

between producers and retailers, although less

well-known to consumers, are also important in

price-setting.

The acquisition cost of goods sold represents the

single biggest cost incurred by the distributive

trades sector, albeit with some notable variation

in magnitude across sectors. In terms of

importance, this is generally followed by labour

costs. The cost structure, as a whole, plays a

signifi cant role in explaining price-setting, and

analysing this can help explain differences in

the rate of pass-through of costs across sectors.

More generally, differences in cost structures

and the resulting profi t margins across countries

for given segments may be indicative of

differing degrees of competition.

As regards the labour market, the distributive

trades sector accounts for a high percentage of

self-employed and part-time workers, as well as

young and female workers. On average, these

account for a high proportion of low-skilled,

low-productivity and, consequently, low-paid

labour. They also account for a signifi cant

proportion of the new jobs created over the

last 15 years. Much of the growth in turnover

and employment within the sector has come

from larger fi rms, refl ecting the fact that this

historically fragmented sector is gradually

consolidating.

Although the report focuses on the distributive

trades sector in euro area countries, it also

considers developments in this sector in some of

the EU’s newer Member States. Many large euro

area retailers have invested substantially in the new

Member States and have undoubtedly contributed

strongly to the modernisation, expansion and

productivity of the distributive trades here.

Nonetheless, notwithstanding the substantial

changes and convergence that have already

occurred, there remains some heterogeneity, both

with regard to the euro area countries and within

the new Member States themselves.

MEASURING REGULATION AND COMPETITION

IN THE DISTRIBUTIVE TRADES SECTOR

Regulation and competition in the distributive

trades sector are key issues and are discussed

in some detail within this report. As regards

regulatory issues, there are a large number

of areas of activity that are subject to specifi c

regulations in the sector, covering issues as

diverse as the setting-up of establishments,

contractual relationships with suppliers, opening

hours, price controls, promotions and sale

conditions, and waste and recycling. These

vary substantially across countries and regions,

as well as in terms of products and store

type/size. An appropriate degree of regulation

is a necessary feature of a market economy;

however, excessive or badly designed regulation

can hinder competition and favour incumbents.

In addition, general planning regulations have

often been cited by competition authorities as

playing an important role in creating barriers

to entry or expansion in the distributive

trades. Fragmented national, regional and

local commercial planning frameworks, in

conjunction with different rules on property

and land ownership, are factors likely to

dissuade entrepreneurs and fi rms from entering

certain markets. These regulations may also

have unintended consequences. Indeed, some

commentators partly attribute the growth

of discounters to planning restrictions,

as discounters frequently fall below specifi ed

size thresholds subject to additional restrictions.

While they may facilitate cross-country

comparisons, summary measures of product

market regulation need to be interpreted with

caution and should not be taken at face value.

In this report, a new indicator of shop opening

time restrictions is developed using detailed

country-level information, which allows for

a more nuanced and differentiated view on

9ECB

Structural features of distributive trades and their impact on prices in the euro area

September 2011

EXECUTIVE

SUMMARYthis issue. More generally, while there is clear

evidence of an easing in the degree of product

market regulation in the distributive trades

sector across almost all countries, there remains

considerable scope for further progress.

Regulatory differences across countries may

also impede online commerce in general and

cross-border e-commerce in particular. The

strong growth, but relatively low market share,

of domestic online commerce and the importance

of physical cross-border retail shopping in many

parts of the euro area illustrate the potential for

cross-border e-commerce. This is all the more

so in view of the evidence that online prices

can differ signifi cantly across countries and

that consumer choice is often restricted because

domestic online suppliers only offer a limited

range of products.

Measuring effective competition in the

distributive trades sector is particularly diffi cult.

This report tries to improve our understanding

in this area. It considers a number of

different indicators (concentration, profi tability,

pass-through) at different levels of spatial (local,

regional and national) and organisational (store,

parent company and buying group) aggregation,

as well as both upstream (producer-related)

and downstream (consumer-related) aspects.

These can provide differing messages. At the

national level, a number of key results are

found. A general fi nding is that concentration is

relatively low at the national level in southern

European countries owing to the persistence of

a more traditional retail structure. The degree

of concentration also varies substantially

across the retail sub-sector, being highest for

electronics and appliances and grocery retailing.

Over time, a slight upward drift in concentration

has been observed for most retail segments,

refl ecting the ongoing consolidation in

European retail trade. Lastly, there tends to be a

positive correlation between concentration and

profi tability measures, possibly partly related to

effi ciency gains.

Regional and local measures of competition are

also constructed by using a unique dataset on

the location of over 100,000 individual grocery

stores spread across the euro area. As regards

which level is “best”, this may depend on the

perspective involved. For example, for large

producers, competition might be best considered

at the national or supranational level. For food

and grocery producers, competition might be

primarily regional, whereas, for consumers,

it might be local. Considering fi rst the results for

the downstream (consumer) market, while there

are some similarities with the results obtained

when using national data, there are also some

noteworthy differences: some markets that

appeared to be relatively fragmented at the

national level actually turned out to be quite

concentrated at the local level and vice versa.

As for the upstream market, concentration

measures using buying group information

generally provide a relatively similar picture

to store-level measures, albeit with certain

differences. Overall, the key message is that

measuring the degree of competition in retail

trade is not a straightforward matter; this is an

issue that should be carefully considered along a

number of different dimensions.

THE ROLE OF THE STRUCTURAL FEATURES OF THE

DISTRIBUTIVE TRADES SECTOR IN EXPLAINING

DIFFERENCES IN PRICE LEVELS AND DYNAMICS

Given that the intermediation services provided

by the distributive trades sector account

for a large part of consumer prices and that

distributive services are not generally traded

internationally, this report considers to what

extent the structural aspects of the retail sub-

sector, combined with other indicators, help

to explain differences in price levels, price

dynamics and convergence. The main fi ndings

are as follows.

There remains a 1) considerable degree of price dispersion across the euro area; this is

lower on average for goods than for services,

but it is still sizeable in most cases – tending

to be lower for electronics and for clothing

and footwear and higher for food products.

The evidence points to a limited degree of

price convergence that appears to come to a

halt around the period 2004 to 2006. There is

10ECB

Structural features of distributive trades and their impact on prices in the euro area

September 2011

also compelling evidence of a strong “border

effect” on price differentials across euro

area countries, which suggests ample scope

for further improving the Single Market.

The structural and regulatory features of

the distributive trades sector appear to help

explain differences in price levels across

countries.

Using information drawn from the Infl ation 2)

Persistence Network and the Wage Dynamics

Network of the Eurosystem, the report

considers price-setting behaviour. It fi nds that

higher competition is associated with more frequent price changes in the retail sub-sector.

Another fi nding is that price changes are more

frequent in supermarkets and hypermarkets,

though not larger in average magnitude.

These results hold across countries and

product types.

Using a combination of two unique datasets, 3)

the report examines the relationship between

price dynamics at the regional level and

competition (measured at different levels of

organisational and spatial aggregation and

across a number of product groups). It fi nds

that higher market concentration has, in recent times, been associated with higher price growth for food and drink products.

The interpretation of this correlation calls

for further research, but it does appear to

be robust and to hold across individual

countries.

This report also considers the magnitude and 4)

speed of cost pass-through. As a stylised

fact, producer prices show a stronger and faster reaction to cost shocks than consumer prices. However, there is large dispersion in

respect of the transmission of costs to prices

across countries and sectors. The degree of

competition appears to be positively related

to the long-run pass-through of import

prices to consumer prices. As regards food

prices, a more pronounced presence of

discounters seems to be associated with

a higher pass-through. In the clothing

segment, changes in import prices are not

fully transmitted to consumer prices.

CONCLUSIONS AND POLICY IMPLICATIONS

This report contributes to a better 1)

understanding of the impact of the structural

features of the distributive trades sector on

prices and price-setting behaviour, thereby

improving on previous research in this area.

From a policy perspective, it highlights the

importance of structural reforms that help

enhance competition in this sector.

The fi ndings regarding the impact of 2)

structural features on price-setting behaviour

and on price level differences across euro

area countries suggest that further progress

in improving effective competition in the

distributive trades sector could help reduce

border effects, narrow price differentials,

strengthen the Single Market and enhance

the effectiveness of monetary policy.

As concerns product market regulation, 3)

although there is evidence of an easing in the

degree of regulation impacting the distributive

trades sector across almost all euro area

countries, there remains considerable scope

for further progress. However, the indicators

available for this analysis may only capture

some aspects of regulation.

With regard to labour markets, the 4)

distributive trades sector has the potential

to be a major contributor to job growth,

particularly for specifi c groups of the labour

force, such as the low-skilled. Given the

“Europe 2020” growth strategy of the EU,

and in view of the high unemployment

rates arising from the crisis, this would be

an important point to consider. However,

sector-specifi c product market and more

general labour market structural rigidities

may impede productivity growth and job

creation in this sector.

11ECB

Structural features of distributive trades and their impact on prices in the euro area

September 2011

EXECUTIVE

SUMMARYAll in all, a crucial step towards further 5)

progress would be the full implementation of

the Services Directive. The benefi ts arising

from further liberalisation and harmonisation

of market conditions may be seen, in part,

from the report’s fi nding that higher product

market regulation is associated with higher

price levels. Moreover, structural reforms

in the distributive trades sector could

reduce mark-ups and give rise to substantial

increases in both output and real wages.

In order to unleash the full potential and

benefi ts of online and cross-border trade,

remaining regulatory and legislative barriers

(such as consumer law and VAT-related

issues) need to be addressed. This could also

contribute signifi cantly to improving the

functioning of the Single Market.

The implications of ongoing developments 6)

in the distributive trades sector for the

measurement of price levels and price

changes should also be considered by the

relevant bodies to avoid the emergence

of biases in measures of consumer price

infl ation. Relevant issues here would be the

analysis of alternative methods to consider

new outlets and new product characteristics

and prices, as well as how, and when, to

introduce them into the HICP basket (e.g. via

hedonic regressions or consumer surveys),

and the need to ensure that samples are

regularly updated and remain representative.

This report uses a wide range of data sources – 7)

some of which are unique – to study an area

that has been under-investigated, especially at

the European level. There is, however, ample

room for further research in this direction.

In particular, it is important to gain further

insight into how competition impacts retail

price levels at a more disaggregated level

(i.e. at the local or regional level rather than

at just the national level). In this regard, the

collection of more price level data at a highly

disaggregated level (e.g. across store types,

regions, etc.) would be particularly useful.

12ECB

Structural features of distributive trades and their impact on prices in the euro area

September 2011

INTRODUCTION AND MOTIVATION

The distributive trades, consisting of

wholesaling and retailing, are a key sector of

the economy. As the main interface between

producers and consumers, the sector is

particularly important from a monetary policy

point of view: this is where most consumer

goods prices are ultimately set. Despite almost

20 years of the Single Market, mark-ups in the

distributive trades sector can still be substantial

and differ considerably across countries,

while cross-border trade remains limited. This

report examines the structural features of the

distributive trades sector which are likely to

play an important role in determining price level

and infl ation differences across countries.

Given its key role in the economy, the

distributive trades sector has been studied

extensively by policy-makers, though generally

from a different perspective. The European

Commission recently published the results of its

market monitoring exercise, which covers a

wide range of issues affecting the retail trades,

such as consumer accessibility, relationships

with upstream producers, labour markets,

logistics and information and communication

technology (ICT), as well as energy use.2

Many national competition authorities have also

conducted comprehensive reviews of the

distributive trades sector in their countries –

for example, those of Ireland and the

United Kingdom.3 These reports illustrate the

challenging issues involved and the complex

interaction between upstream agents (producers

and wholesalers) and downstream agents

(retailers), as well as the importance of the

regulatory environment in supporting

competition in this sector.4 However, there is

relatively little research investigating the impact

of the structural features of the distributive

trades on prices and price-setting behaviour.

The objective of this report is to shed light on

these aspects by examining: (a) the main features

of, and issues relating to, the euro area

distributive trades sector from a monetary policy

perspective; and (b) the impact of these features

on price levels and infl ation behaviour.

The distributive trades sector has been

undergoing substantial changes, in terms

of, for example, growing consolidation and

internationalisation and changing retail

formats (e.g. the increasing market shares of

supermarkets and hypermarkets, the growth of

the discount sector and the expansion of private

label brands). These developments infl uence

competition and cost structure and play an

important role in determining mark-ups and,

thus, affect fi nal consumer prices in the euro

area. As regards labour market issues, this sector

has contributed signifi cantly to the improvement

in employment growth experienced by the

euro area during the past decade. However,

productivity is comparatively low and the sector

accounts for more than one-third of the widening

The European Commission’s Directorate-General for Health 2

and Consumer Policy also regularly studies the retail markets

in its Consumer Markets Scoreboard (CMS), focusing on the

integration of the retail internal market, particularly from the

consumer perspective. To date, fi ve editions of the CMS have

been published (European Commission, (2011b), (2010c),

(2010b), (2009) and (2008)). Each of these considers the general

progress made in the integration of the retail internal market as

well as specifi c topics. For example, the third and fi fth editions of

the CMS consider cross-border and online consumer purchases.

Both of these issues are discussed in Box 1 of this report.

In 2006, the UK Competition Commission (UKCC) initiated, 3

at the request of the country’s Offi ce of Fair Trading (OFT),

a comprehensive two-year study into the supply of groceries by

retailers in the United Kingdom. This is because the OFT believed

there were “reasonable grounds for suspecting that a feature…of the market…prevents, restricts or distorts competition”. The fi nal

report (UKCC, (2008)) concluded as follows: “…in many important respects, competition in the UK groceries industry is effective and delivers good outcomes for consumers, but not all is well. We have concerns in two principal areas. First, we found that several grocery retailers have strong positions in a number of local markets. Second, we found that the transfer of excessive risk and unexpected costs by grocery retailers to their suppliers through various supply chain practices…”. The Competition

Authority of Ireland has, in recent years, undertaken two studies

related to the distributive trades sector: the fi rst study – the

“Grocery Monitor Project” – was initiated following the abolition

of the Groceries Order in March 2006 to assess how the grocery

retail and wholesale trade in Ireland had responded to the new

legislative environment; the second – “Retail-related Import and

Distribution Study” – was published in 2009.

One key fi nding from the Irish study was that the retail planning 4

system made it diffi cult for new retailers to enter the Irish grocery

market and for existing retailers to expand their operations. A

similar conclusion was drawn by the French competition authority

(Autorité de la concurrence) in 2007, prompting a reform of the

authorisation procedure for large outlets in France a year later. In

February 2011 Germany’s federal cartel offi ce (Bundeskartellamt)

announced an investigation into the relationship between leading

grocery retailers and their suppliers.

13ECB

Structural features of distributive trades and their impact on prices in the euro area

September 2011

INTRODUCTION AND

MOTIVATIONin the aggregate productivity gap between the

United States and the euro area that has occurred

since the mid-1990s. These issues are presented

in more detail in Section 1.1 of the report.

As described in Section 1.2, regulation plays

a fundamental role in the distributive trades

sector, particularly in terms of barriers to

entry, operating restrictions and price controls.

Although regulation varies primarily at the

national level, in some countries, there is also

an important regional element, which may help

disentangle the effects of regulation from other

economy-wide factors. Section 1.3 considers

the empirical measurement of competition,

which is often assessed in terms of the degree

of concentration within a sector. However, the

relationship between concentration and price

levels and sector dynamics is ambiguous.

Regarding price levels, the presence of

economies of scale or scope can have a potential

downward impact on prices stemming from

large, effi cient players. But this effect has to be

assessed against the potential upward impact

from reduced competition. Other things being

equal, increased competition should improve

effi ciency and reduce mark-ups, and thereby

lead to lower prices. However, increased

competition may also give rise to ongoing

dynamic effects via higher productivity levels

and growth, which can result in lower infl ation

as well as lower price levels.

Having set the scene, the second part of the

report considers the impact of the structural

features of the distributive trades sector on

price level differences, price-setting behaviour,

regional price change dynamics and the

pass-through of costs. These are discussed in

Sections 2.1, 2.2, 2.3 and 2.4 respectively. The

signifi cance of the regulatory and structural

features of the distributive trades for price level

differences is underlined in Section 2.1, which

also investigates the “border effect” on price

differentials. Section 2.2 considers the impact

of store formats on price-setting and examines

the extent to which structural differences

and competition infl uence the frequency of

price changes. However, competition in the

distributive trades sector must also be considered

from a number of different perspectives – most

importantly, spatially (in terms of local, regional,

national or supranational markets) and from the

position of upstream and downstream agents

(although consumers interact with retailers at

the individual store level, producers usually

interact with retailers at the parent company or

even buying group level). Hence, Section 2.3

considers regional price dynamics and the extent

to which these are infl uenced by the measures

of concentration calculated at the regional and

local level in Section 1.3.

The link between competition and the degree of

cost pass-through is, to some extent, ambiguous.

In the (theoretical) case of perfect competition,

retailers have no option but to fully pass through

increases in upstream producer prices, as they

have no excess profi ts that can be used as a

buffer. In the case of imperfect competition,

where many competing producers sell products

that are differentiated from one another,

the degree of pass-through will depend on many

factors and the link between competition and

the extent of pass-through may be less clear.

The relationship between the structural aspects

of the distributive trades sector and the degree

of pass-through is considered in more detail in

Section 2.4. An empirical analysis is undertaken

for consumer goods in general, and for prices of

food and clothing and footwear in particular.

This report uses a wide range of data sources

and some unique datasets. More specifi cally, it

utilises: (i) detailed data and the “Quaranta

tables” from Eurostat’s purchasing power parity

(PPP) database to study the impact of

competition and regulation in the distributive

trades sector on price level differences across

countries; (ii) individual price and survey data

collected under the Eurosystem’s Infl ation

Persistence Network (IPN) and Wage Dynamics

Network (WDN) to consider the impact of

competition and the structural features of the

distributive trades sector on price-setting

behaviour; (iii) country-specifi c information

14ECB

Structural features of distributive trades and their impact on prices in the euro area

September 2011

provided by ESCB staff 5 to construct a new and

more refi ned indicator of the extent of regulation

on shop opening times; (iv) time series provided

by national statistical institutes on regional

consumer price dynamics (broken down across

a number of product groups), which are

combined with a unique “census-type” database

on grocery store locations. For a complete

overview of the main data sources used in this

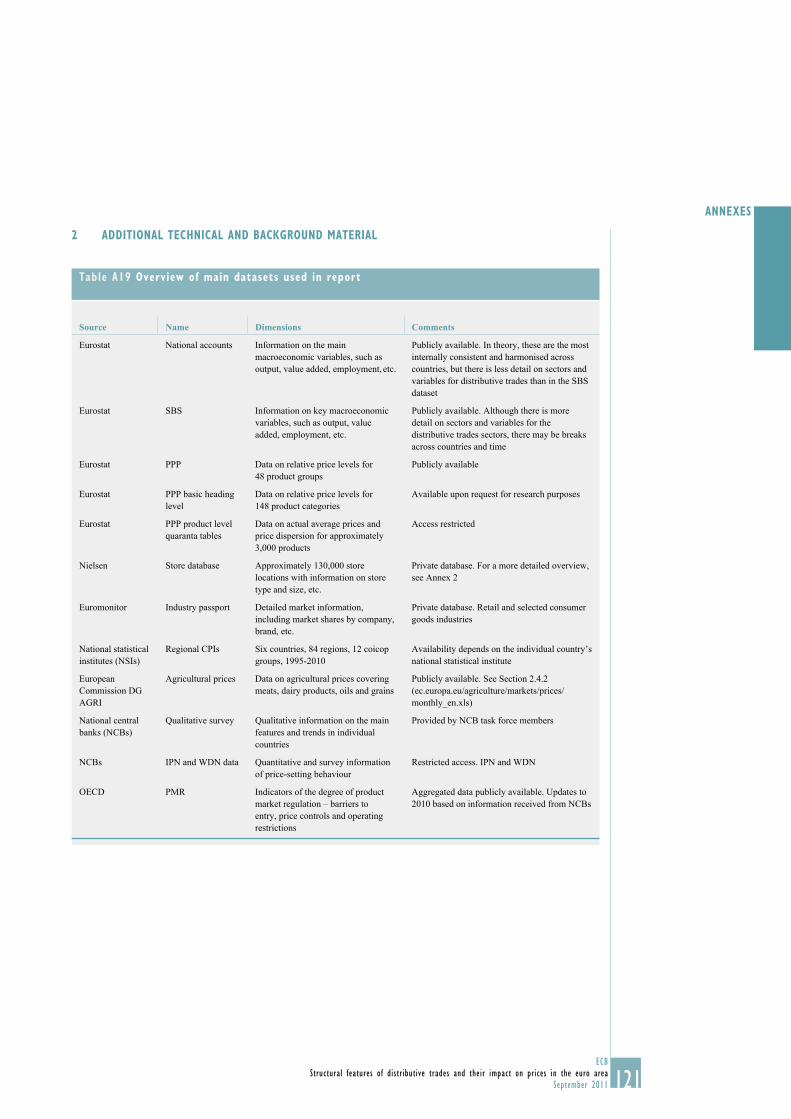

report, see Table A19 in the Appendix.

Given the original and challenging nature of

much of the analysis contained in this report,

the fi ndings and conclusions in some areas must

be considered as preliminary. Nonetheless,

the research highlights the fact that the structural

features of the distributive trades sector, as well

as the degree of competition within it, are of

importance to monetary policy-makers whose

primary aim is to maintain price stability.

These staff are members of the Monetary Policy Committee task 5

force that was responsible for drafting this report.

15ECB

Structural features of distributive trades and their impact on prices in the euro area

September 2011

I AN OVERVIEW

OF THE DISTRIBUTIVE

TRADES: STRUCTURAL,

REGULATORY AND

COMPETITION FEATURES

1 AN OVERVIEW OF THE DISTRIBUTIVE

TRADES: STRUCTURAL, REGULATORY

AND COMPETITION FEATURES

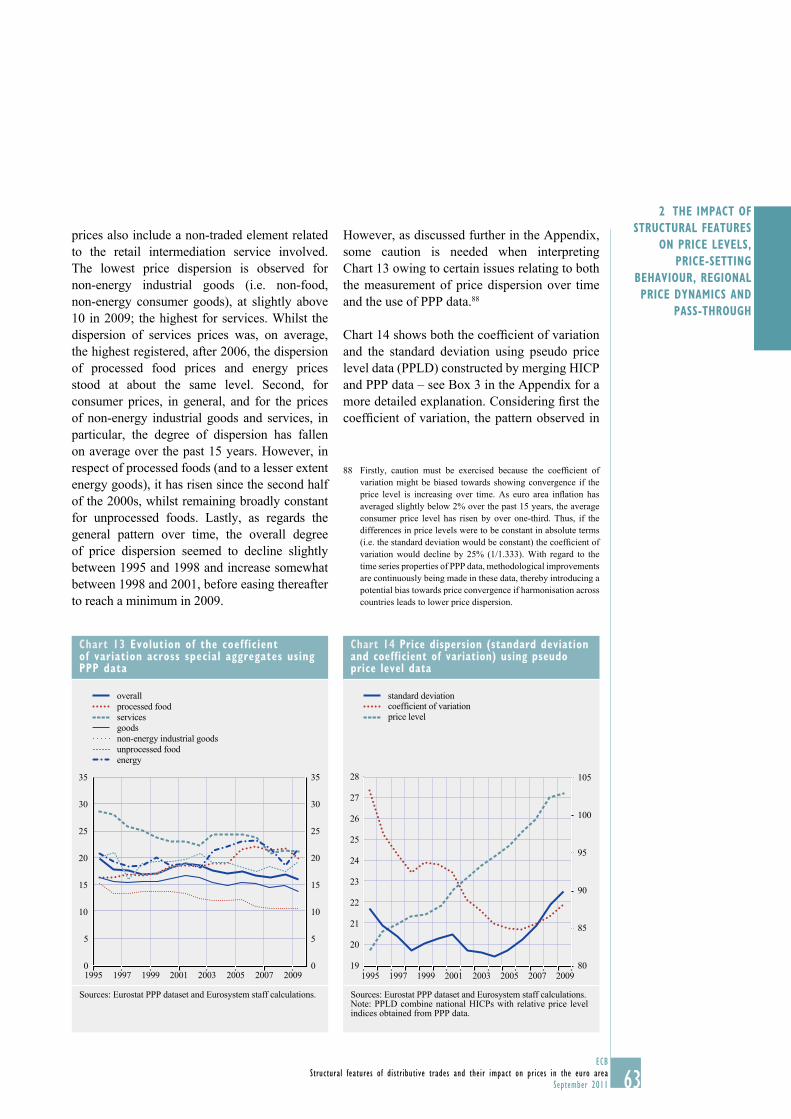

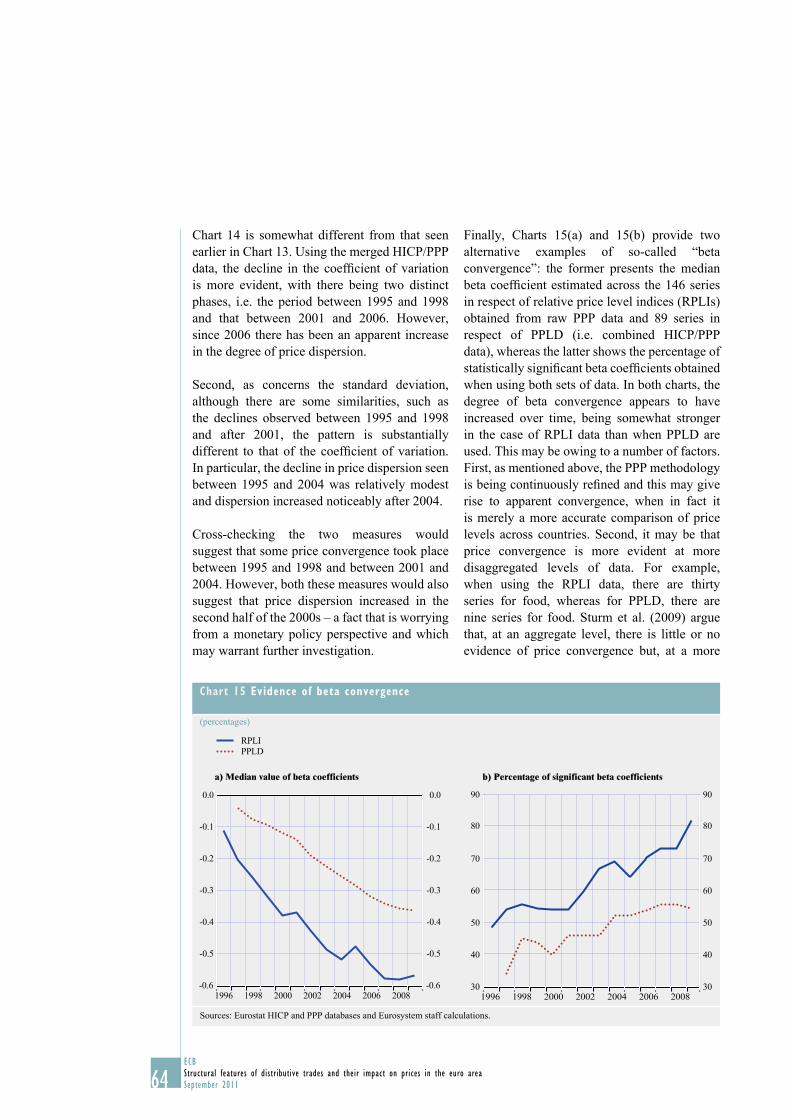

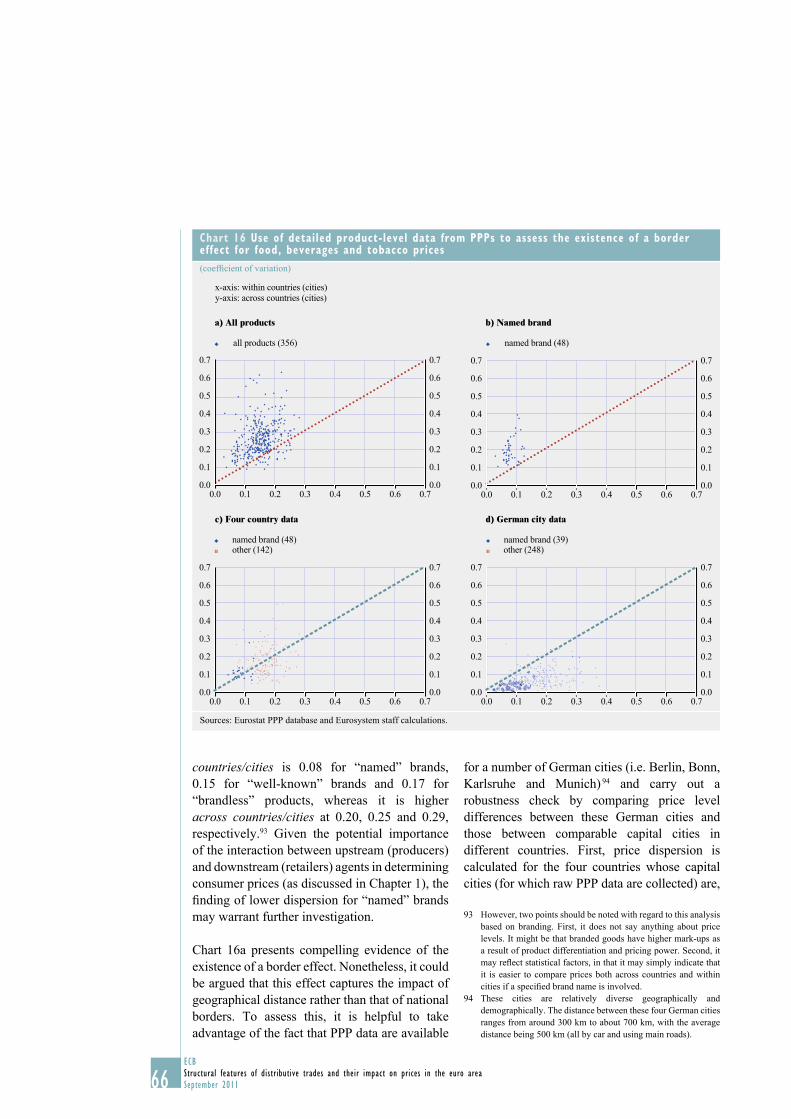

This chapter provides an overview of the distributive trades sector in the euro area in order to give an insight into the key features of the sector that will underpin the analysis in Chapter 2.

1.1 THE IMPORTANCE, STRUCTURE

AND PERFORMANCE OF THE DISTRIBUTIVE

TRADES SECTOR

This section considers the macroeconomic importance and structure of the distributive trades, including their economic evolution, cost structures and labour market features.

The main fi ndings are that the distributive trades are of key importance in the macroeconomy, both directly and – functioning as intermediaries between producers and consumers – indirectly. They have a number of distinguishing features, generally being more labour-intensive and employing more lower-skilled workers. While profi t margins are below average, this may refl ect a high degree of turnover (per unit of capital employed) rather than strong competitive pressures. The retail trade sub-sector displays signifi cant diversity across both euro area countries and segments. Key issues are the growing internationalisation of retail trade along with the growth of discounters, of private label brands and of online trade.

1.1.1 DEFINITIONAL ISSUES

The distributive trades function as

“intermediaries” between economic agents that

are upstream (e.g. producers) and those that

are downstream (e.g. consumers). While they

generally do not produce goods themselves

(although that is changing 6), they clearly provide

a necessary economic service.

The distributive trades sector covers three

broad areas: motor, wholesale and retail trade.7

The motor trade is considered to be a separate

sub-sector with quite different characteristics,

partly because of the close link between the

companies in this fi eld and the automotive

industry.8 Wholesale trade companies generally

do not sell directly to consumers, but rather to

businesses and retailers. Retailers generally

sell directly to consumers, but not necessarily

exclusively so. As will be highlighted below,

wholesale and retail trade are by far the largest

sub-sectors within the distributive trades sector.

As a result, and given the specifi c nature of

the motor trade sub-sector, this report focuses

primarily on wholesale and retail trade.9

ECONOMIC IMPORTANCE OF THE DISTRIBUTIVE

TRADES

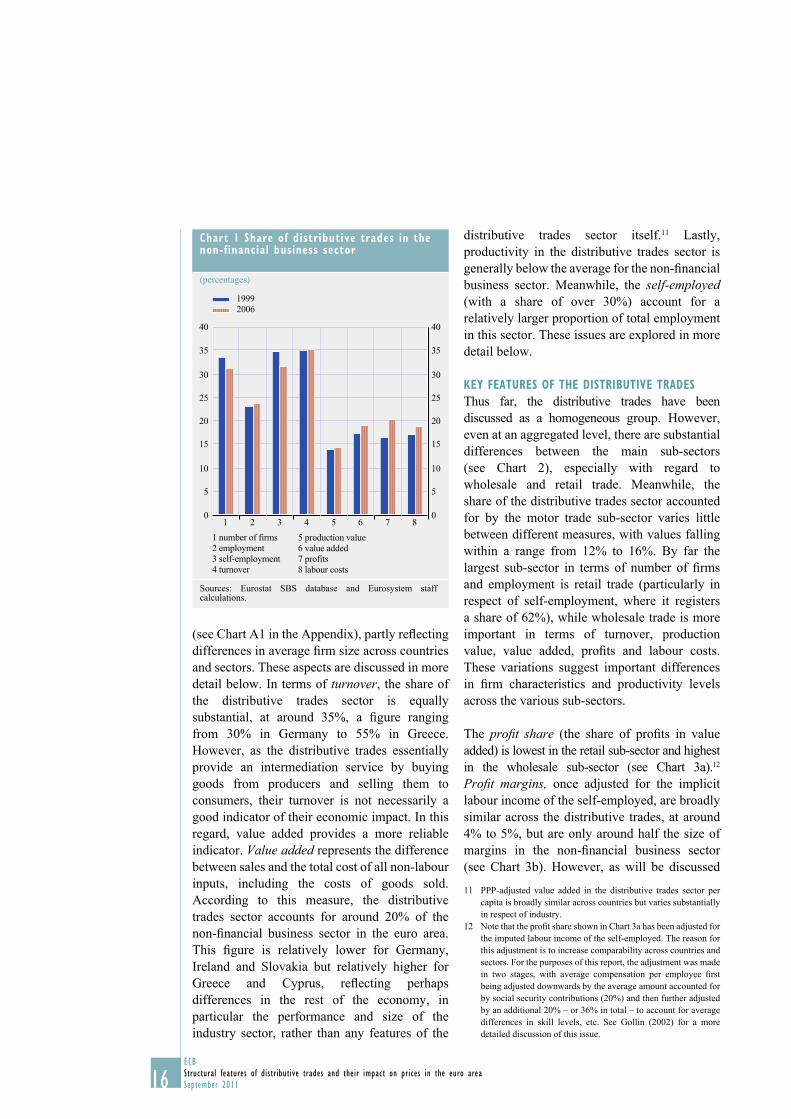

In the euro area as a whole, the distributive

trades sector accounts for approximately 33% of

fi rms in the non-fi nancial business sector

(see Chart 1).10 This is a fi gure that ranges from

around 25% in Germany to 40% in Slovakia

For example, with the increasing importance of private or own-6

label brands and with companies in the clothing and footwear

segment both producing and selling clothing.

Table A20 in the Appendix shows the breakdown and 7

composition of the distributive trades sector according

to the NACE Rev. 2 system used by EU institutions for

classifying economic activities, which was adopted in 2006

for implementation from 2008 onwards. For reasons of data

availability, the previous classifi cation system, NACE Rev. 1.1,

is largely used in this report. This is broadly similar to NACE

Rev. 2, but there are certain differences.

For a more detailed overview of the automotive sector, see the 8

website of the European Commission’s Directorate-General for

Competition (http://ec.europa.eu/competition/sectors/motor_

vehicles/overview_en.html).

This section primarily uses data from Eurostat’s Structural 9

Business Statistics (SBS) dataset; for an overview of the main

datasets used in this report, see Table A19. SBS data are used

owing to the rich level of disaggregation at which these data

are available, plus the fact that there is a separate module with

specifi c information on the features of the distributive trades.

However, it may also be the case that for some countries, owing

to changes in methodology, comparisons over long periods of

time should be made with caution. For example, as regards the

SBS data for Portugal, a gap exists for the period prior to 2004,

as the national statistical authority only had access to

administrative data from that year onwards. Hence, any

comparisons related to the pre-2004 period should be made with

care.

The non-fi nancial business sector is comprised of the total economy, 10

excluding the agriculture and fi shing, fi nancial intermediation

services and public services sectors. It includes the mining and

quarrying, manufacturing, utilities, construction, distributive trades,

hotels and restaurants, transport, storage and communication,

and real estate, renting and business activities sectors.

16ECB

Structural features of distributive trades and their impact on prices in the euro area

September 2011

(see Chart A1 in the Appendix), partly refl ecting

differences in average fi rm size across countries

and sectors. These aspects are discussed in more

detail below. In terms of turnover, the share of

the distributive trades sector is equally

substantial, at around 35%, a fi gure ranging

from 30% in Germany to 55% in Greece.

However, as the distributive trades essentially

provide an intermediation service by buying

goods from producers and selling them to

consumers, their turnover is not necessarily a

good indicator of their economic impact. In this

regard, value added provides a more reliable

indicator. Value added represents the difference

between sales and the total cost of all non-labour

inputs, including the costs of goods sold.

According to this measure, the distributive

trades sector accounts for around 20% of the

non-fi nancial business sector in the euro area.

This fi gure is relatively lower for Germany,

Ireland and Slovakia but relatively higher for

Greece and Cyprus, refl ecting perhaps

differences in the rest of the economy, in

particular the performance and size of the

industry sector, rather than any features of the

distributive trades sector itself.11 Lastly,

productivity in the distributive trades sector is

generally below the average for the non-fi nancial

business sector. Meanwhile, the self-employed (with a share of over 30%) account for a

relatively larger proportion of total employment

in this sector. These issues are explored in more

detail below.

KEY FEATURES OF THE DISTRIBUTIVE TRADES

Thus far, the distributive trades have been

discussed as a homogeneous group. However,

even at an aggregated level, there are substantial

differences between the main sub-sectors

(see Chart 2), especially with regard to

wholesale and retail trade. Meanwhile, the

share of the distributive trades sector accounted

for by the motor trade sub-sector varies little

between different measures, with values falling

within a range from 12% to 16%. By far the

largest sub-sector in terms of number of fi rms

and employment is retail trade (particularly in

respect of self-employment, where it registers

a share of 62%), while wholesale trade is more

important in terms of turnover, production

value, value added, profi ts and labour costs.

These variations suggest important differences

in fi rm characteristics and productivity levels

across the various sub-sectors.

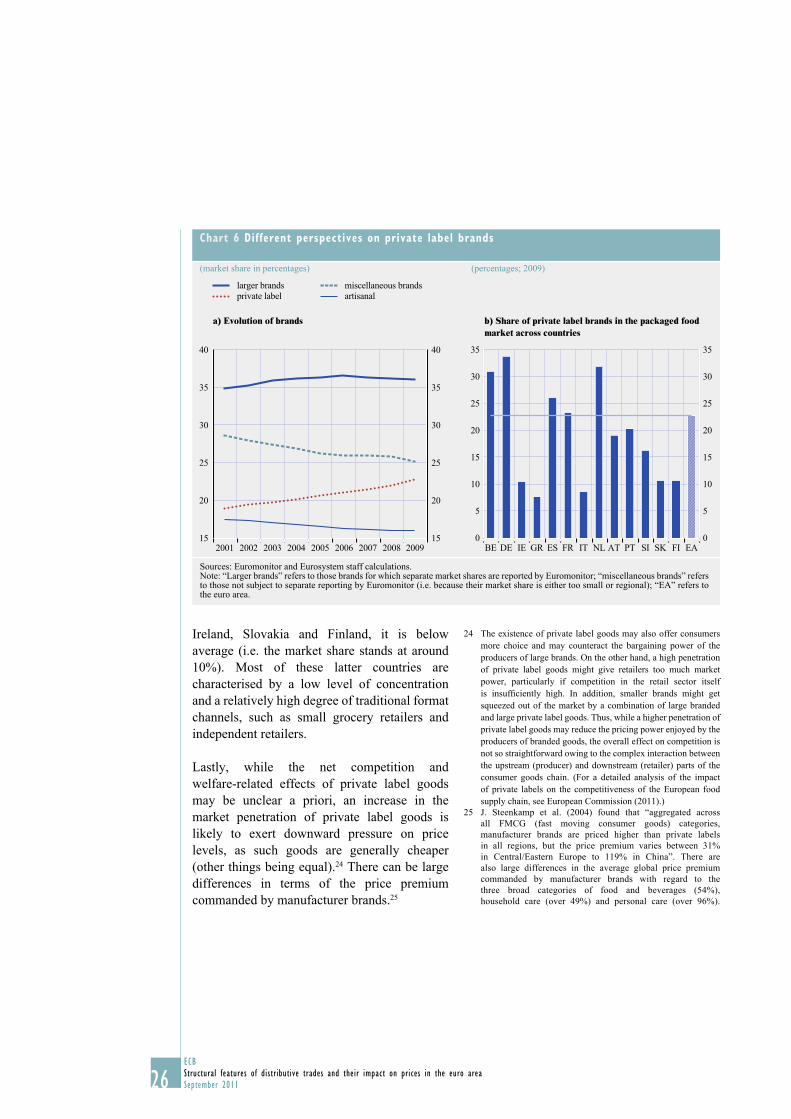

The profi t share (the share of profi ts in value

added) is lowest in the retail sub-sector and highest

in the wholesale sub-sector (see Chart 3a).12

Profi t margins, once adjusted for the implicit

labour income of the self-employed, are broadly

similar across the distributive trades, at around

4% to 5%, but are only around half the size of

margins in the non-fi nancial business sector

(see Chart 3b). However, as will be discussed

PPP-adjusted value added in the distributive trades sector per 11

capita is broadly similar across countries but varies substantially

in respect of industry.

Note that the profi t share shown in Chart 3a has been adjusted for 12

the imputed labour income of the self-employed. The reason for

this adjustment is to increase comparability across countries and

sectors. For the purposes of this report, the adjustment was made

in two stages, with average compensation per employee fi rst

being adjusted downwards by the average amount accounted for

by social security contributions (20%) and then further adjusted

by an additional 20% – or 36% in total – to account for average

differences in skill levels, etc. See Gollin (2002) for a more

detailed discussion of this issue.

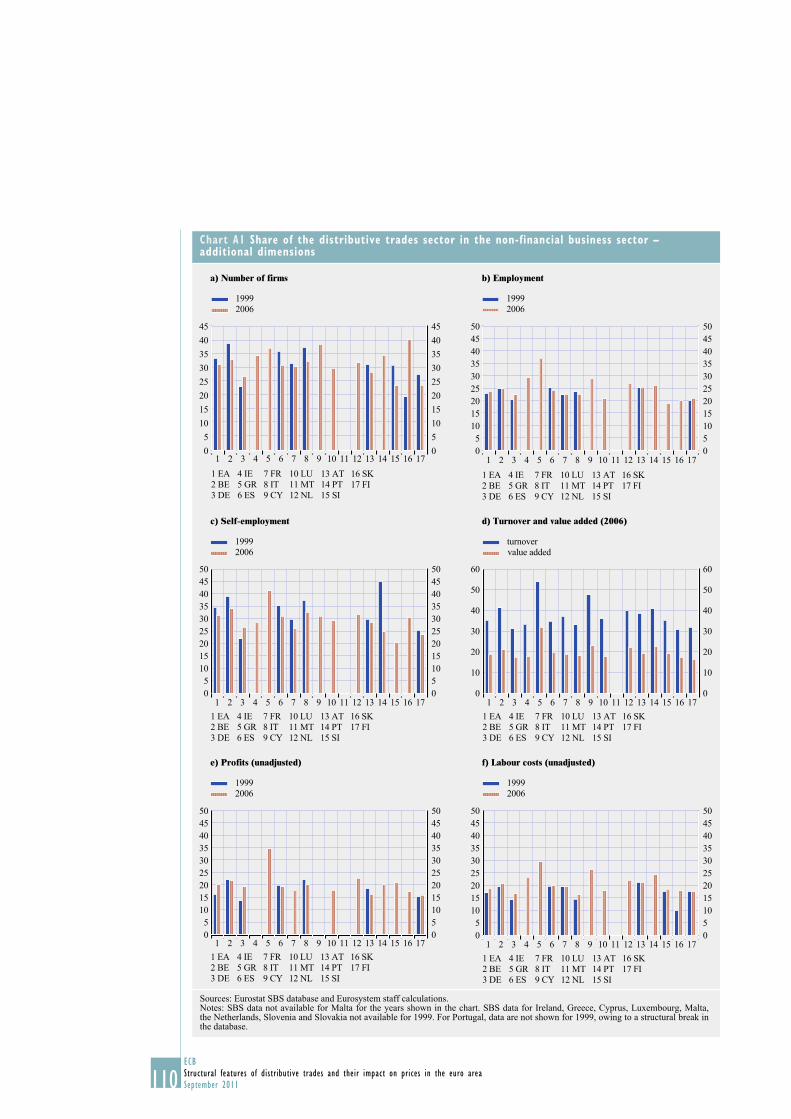

Chart 1 Share of distributive trades in the non-financial business sector

(percentages)

0

5

10

15

20

25

30

35

40

0

5

10

15

20

25

30

35

40

1999

2006

2 employment

3 self-employment

4 turnover

1 number of firms

1 2 3 4 5 6 7 8

5 production value

6 value added

7 profits

8 labour costs

Sources: Eurostat SBS database and Eurosystem staff calculations.

17ECB

Structural features of distributive trades and their impact on prices in the euro area

September 2011

I AN OVERVIEW

OF THE DISTRIBUTIVE

TRADES: STRUCTURAL,

REGULATORY AND

COMPETITION FEATURES

later in Section 1.3, comparisons of profi t

margins across sectors should be made and

interpreted with caution.13 The fact that the

distributive trades sector provides intermediation

services, often involving a very high turnover

rate for goods, means that low profi t margins do

not necessarily imply low profi tability, for

example if measured in terms of return on capital.

Overall, and notwithstanding the differences

highlighted above, the breakdown and features

of the main sub-sectors are broadly similar

across euro area countries. Wholesale trade

is most important in terms of value added and

turnover, but retail trade is more signifi cant in

terms of employment, number of fi rms and,

above all, interaction with consumers. The next

section examines the retail trade sub-sector in

more detail.

1.1.2 A CLOSER LOOK AT THE GROCERY TRADE

Retail trade is divided roughly evenly into

grocery trade (primarily food and certain

household items) and non-grocery trade

(clothing and footwear, household furnishings

and electronic goods). These two parts of the

Aside from the issue of imputing the labour income of the self-13

employed, the calculation and interpretation of profi tability

measures is quite complex. See ECB (2004) for a more detailed

discussion.

Chart 2 Share of sub-sectors in the distributive trades sector in 2006

(percentages)

0

10

20

30

40

50

60

70

0

10

20

30

40

50

60

70

Motor vehicles

and auto fuel

Wholesale and

commission trade

Retail trade

number of firms

self-employment

production value

profits

employment

turnover

value added

labour costs

Sources: Eurostat SBS database and Eurosystem staff calculations.

Chart 3 Comparison across distributive trades sub-sectors

(average profi t share (adjusted) in euro area distributive trades sectors; percentages)

(average profi t margin (turnover; adjusted) in euro area distributive trades sectors; percentages)

distributive trades wholesale trade

retail trade non-financial business

a) Profit share b) Profit margins

25

30

35

40

45

25

30

35

40

45

1997 1999 2001 2003 20050

2

4

6

8

10

12

14

0

2

4

6

8

10

12

14

1997 1999 2001 2003 2005

Sources: Eurostat SBS database and Eurosystem staff calculations.

18ECB

Structural features of distributive trades and their impact on prices in the euro area

September 2011

sub-sector differ substantially in terms of their

main economic characteristics, with grocery

trade being somewhat more homogeneous than

non-grocery trade. This section considers the

grocery trade in more detail.

Most consumers obtain the basic necessities

required for daily living, such as food and

household goods, in the grocery market.

However, although the goods sold here may

be broadly similar across countries, there are

notable differences across countries in terms

of, for example, store format, the degree of

internationalisation, market penetration by hard

discounters and private label brands, and the

role of buying groups.

These differences are clearly visible in the

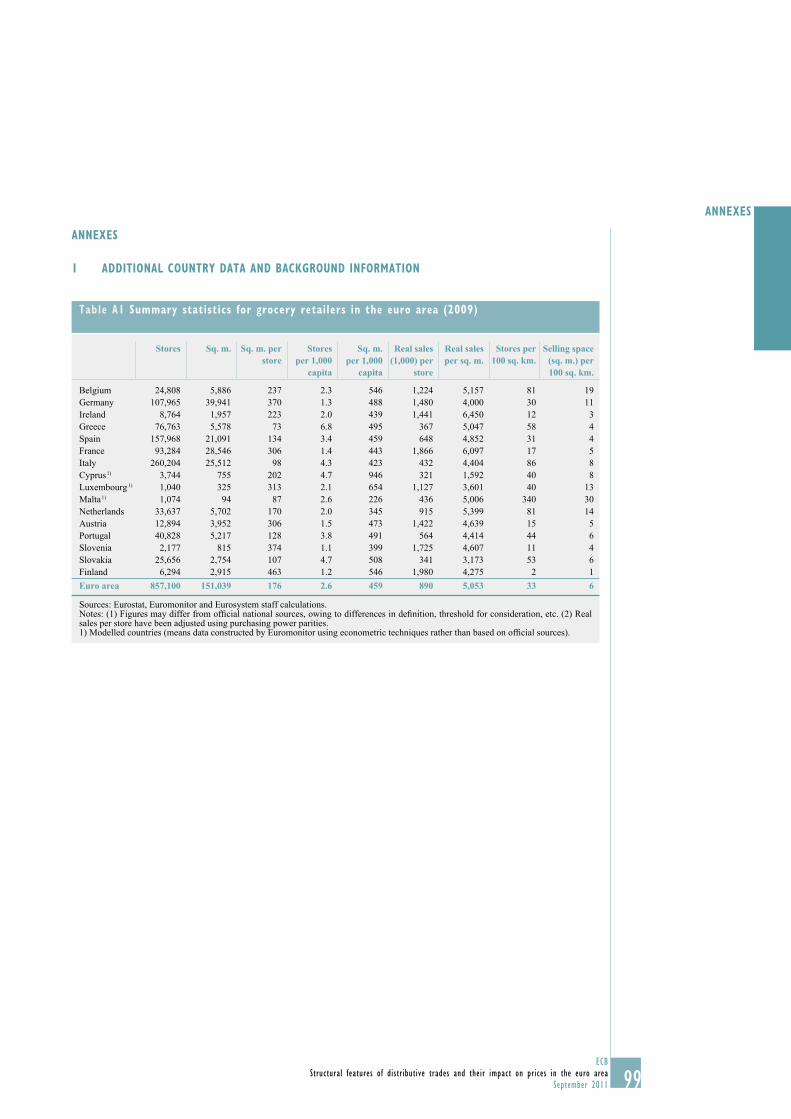

summary statistics presented in Table A1.

The total number of grocery stores in the euro

area is approximately 850,000, the majority of

which, unsurprisingly, are located in the larger

economies. However, it is striking that both Italy

and Spain feature more stores than Germany

and France, despite having smaller populations.

This may be due, in part, to differing defi nitions

and thresholds for classifying stores. When

it comes to selling space, measured in square

metres – which is perhaps a more meaningful

indicator – Germany (with almost 40 million m²)

and France (with almost 30 million m²) account

for the largest proportion of the total euro area

grocery selling space of 150 million m². This

inverse correlation between number of stores and

selling space captures an important distinction

in the European grocery trade. Southern

European countries, such as Greece, Cyprus,

Italy, Portugal, Spain and Malta, tend to have

more traditional and smaller grocery retailers

than certain northern European countries, for

example Finland, Germany, France and Austria.

In terms of real sales per store, Finland and

France have the highest on average, but in

the case of Finland this is mainly because the

stores are generally of a large size – a feature

of the grocery trade in both these countries.

On a square metre basis, the countries with the

highest real sales per store are Ireland, France,

the Netherlands and Belgium.

It should be borne in mind that these statistics

are somewhat crude, being country averages

only; they do not account for heterogeneity

across stores or regions. Furthermore, when

trying to interpret the different indicators, it is

also necessary to consider geographical and

economic differences between countries (such

as population density and distribution and

income levels), as well as socio-cultural and

regulatory factors.

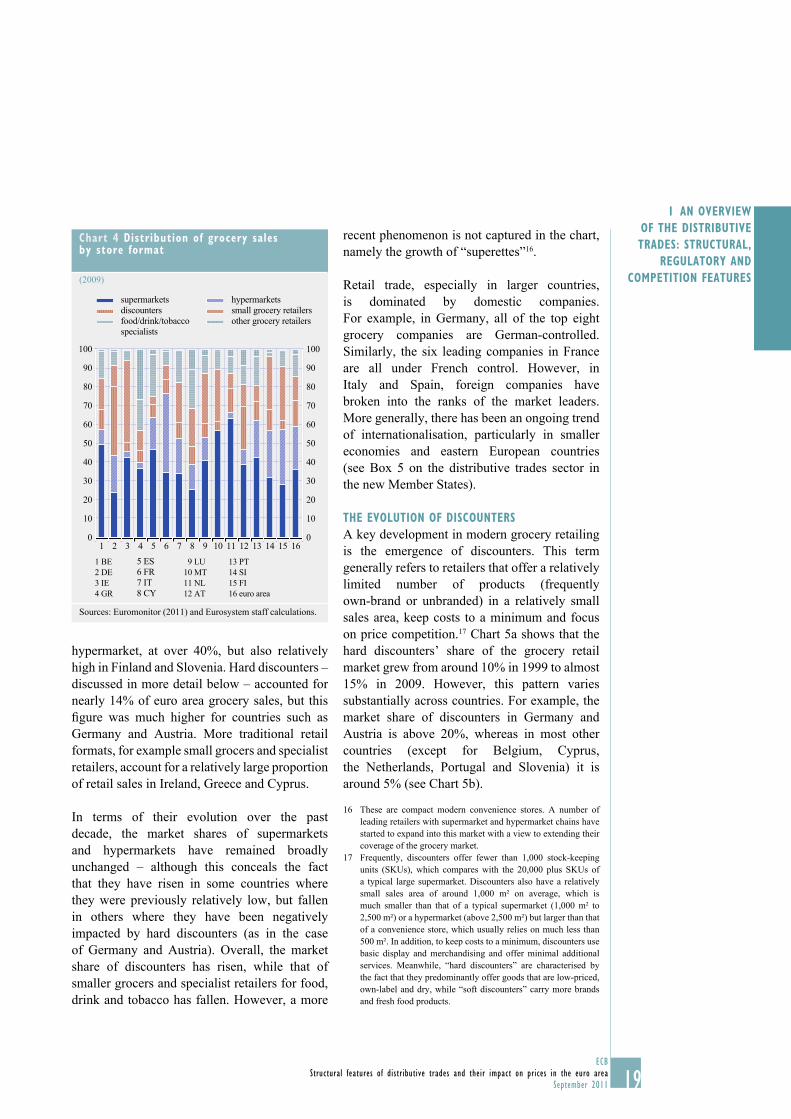

Chart 4 presents the distribution of grocery

sales by store format across countries;

this varies considerably, refl ecting a combination

of factors, such as historical legacies, societal

preferences, socio-geographical factors and

regulatory conditions.14

On average, supermarkets accounted for just

over 33% of grocery sales in the euro area in

2009. However, at the country level, their

market share was lowest in Germany (at around

25%), where hard discounters dominate grocery

sales, and in Cyprus, where smaller, traditional

retailers account for a relatively large proportion

of sales. The market share of supermarkets was

relatively high in the Netherlands and Malta,

where hypermarkets account for a relatively

small proportion of grocery sales. While a small

market size may explain this in the case of

Malta, this is clearly not so for the Netherlands,

where planning restrictions are behind the

absence of hypermarkets.15 On average,

hypermarkets accounted for approximately 25%

of grocery sales in the euro area. Their market

share was highest in France, the “home” of the

The defi nition of store formats is to some extent arbitrary. 14

In general, the store size (in terms of square metres) and range

(in terms of the number and breadth of goods stocked) are the

criteria used. Hypermarkets tend to have a sales area above

2,500 m²; supermarkets one between 1,000 m² and 2,500 m²;

and discounters a sales area of between 400 m² and 1,000 m²,

with a relatively limited range of goods.

In its Economic Surveys of the Netherlands, the OECD has 15

noted that “planning restrictions in the Netherlands have

inhibited the entry and expansion of large-format operators,

which has impeded productivity growth in the sector. While

Dutch planning and zoning restrictions have been successful

in protecting small and specialist retailers located in town

centres, they also may distort competition and offer considerable

incumbency advantages to established retailers, thus creating

and maintaining rents”.

19ECB

Structural features of distributive trades and their impact on prices in the euro area

September 2011

I AN OVERVIEW

OF THE DISTRIBUTIVE

TRADES: STRUCTURAL,

REGULATORY AND

COMPETITION FEATURES

hypermarket, at over 40%, but also relatively

high in Finland and Slovenia. Hard discounters –

discussed in more detail below – accounted for

nearly 14% of euro area grocery sales, but this

fi gure was much higher for countries such as

Germany and Austria. More traditional retail

formats, for example small grocers and specialist

retailers, account for a relatively large proportion

of retail sales in Ireland, Greece and Cyprus.

In terms of their evolution over the past

decade, the market shares of supermarkets

and hypermarkets have remained broadly

unchanged – although this conceals the fact

that they have risen in some countries where

they were previously relatively low, but fallen

in others where they have been negatively

impacted by hard discounters (as in the case

of Germany and Austria). Overall, the market

share of discounters has risen, while that of

smaller grocers and specialist retailers for food,

drink and tobacco has fallen. However, a more

recent phenomenon is not captured in the chart,

namely the growth of “superettes”16.

Retail trade, especially in larger countries,

is dominated by domestic companies.

For example, in Germany, all of the top eight

grocery companies are German-controlled.

Similarly, the six leading companies in France

are all under French control. However, in

Italy and Spain, foreign companies have

broken into the ranks of the market leaders.

More generally, there has been an ongoing trend

of internationalisation, particularly in smaller

economies and eastern European countries

(see Box 5 on the distributive trades sector in

the new Member States).

THE EVOLUTION OF DISCOUNTERS

A key development in modern grocery retailing

is the emergence of discounters. This term

generally refers to retailers that offer a relatively

limited number of products (frequently

own-brand or unbranded) in a relatively small

sales area, keep costs to a minimum and focus

on price competition.17 Chart 5a shows that the

hard discounters’ share of the grocery retail

market grew from around 10% in 1999 to almost

15% in 2009. However, this pattern varies

substantially across countries. For example, the

market share of discounters in Germany and

Austria is above 20%, whereas in most other

countries (except for Belgium, Cyprus,

the Netherlands, Portugal and Slovenia) it is

around 5% (see Chart 5b).

These are compact modern convenience stores. A number of 16

leading retailers with supermarket and hypermarket chains have

started to expand into this market with a view to extending their

coverage of the grocery market.

Frequently, discounters offer fewer than 1,000 stock-keeping 17

units (SKUs), which compares with the 20,000 plus SKUs of

a typical large supermarket. Discounters also have a relatively

small sales area of around 1,000 m² on average, which is

much smaller than that of a typical supermarket (1,000 m² to

2,500 m²) or a hypermarket (above 2,500 m²) but larger than that

of a convenience store, which usually relies on much less than

500 m². In addition, to keep costs to a minimum, discounters use

basic display and merchandising and offer minimal additional

services. Meanwhile, “hard discounters” are characterised by

the fact that they predominantly offer goods that are low-priced,

own-label and dry, while “soft discounters” carry more brands

and fresh food products.

Chart 4 Distribution of grocery sales by store format

(2009)

0

10

20

30

40

50

60

70

80

90

100

0

10

20

30

40

50

60

70

80

90

100

supermarkets

discounters

food/drink/tobacco

specialists

hypermarkets

small grocery retailers

other grocery retailers

1 BE

2 DE

3 IE

4 GR

5 ES

6 FR

7 IT

8 CY

9 LU

10 MT

11 NL

12 AT

13 PT

14 SI

15 FI

16 euro area

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

Sources: Euromonitor (2011) and Eurosystem staff calculations.

20ECB

Structural features of distributive trades and their impact on prices in the euro area

September 2011

Given that discounters tend to have lower

prices (although any comparison of prices

is made diffi cult by the lack of comparable

brands), this increase in market share over time

and heterogeneity across countries may have

implications for price levels and infl ation, both

in terms of measurement issues (see the box

entitled “Implications of developments in the

retail trade structure for infl ation measurement”)

and in terms of explaining country differences.

In addition to their possible impact on average

price levels, given the relatively small store

size, in some countries discounters have

found it easier to open new stores than

supermarkets – a fact which may have

implications for the evolution of competition

over time and across countries.18

However, gauging the implications of this

growth in discounters for the overall level of

competition in the grocery market is somewhat

complicated. Although discounters and other

grocery retailers undoubtedly compete in the

same overall market (grocery retailing),

they may not always compete in the same

market segment or for the same customer group.

McKinsey and Company (2005) argue that

discounters only serve 20% of the consumer

market (i.e. “shoppers who care about price

above all else”).19 The more recent development

that many “conventional” retail chains are now

starting their own discount banner further

supports the argument that discounters and

conventional supermarkets may not always be

competing directly in the very same market.

McKinsey and Company (2005) argue that “discounters are 18

growing largely because regulation allows them to open more

quickly and easily than their non-discount rivals” (i.e. owing

to their limited product range and smaller average store size).

However, this has not been the case in Spain, where, up until

2010, a special licence was required in most regions for discount

stores and large retail outlets.

In this regard, Cleeren et al. (2010) use an empirical entry model 19

to study competition between grocery discounters and traditional

supermarkets in Germany. They fi nd evidence for competition

both within and between the supermarket and discount formats.

However, these effects may be complex and require careful

interpretation. For instance, they fi nd that the entry of the fi rst

two discounters has no signifi cant effect on the performance of

supermarkets in a given area.

Chart 5 Discount retailers

(discounters’ share in percentages)

a) Evolution of discounters’ market share in the euro area b) Market share of discounters across countries (2009)

0

2

4

6

8

10

12

14

16

0

2

4

6

8

10

12

14

16

1999 2005 20090

5

10

15

20

25

30

35

40

0

5

10

15

20

25

30

35

40

BE DE IE GR ES FR IT CY LU MT NL AT PT SI FI EA

Sources: Euromonitor and Eurosystem staff calculations.Note: “EA” refers to the euro area.

21ECB

Structural features of distributive trades and their impact on prices in the euro area

September 2011

I AN OVERVIEW

OF THE DISTRIBUTIVE

TRADES: STRUCTURAL,

REGULATORY AND

COMPETITION FEATURES

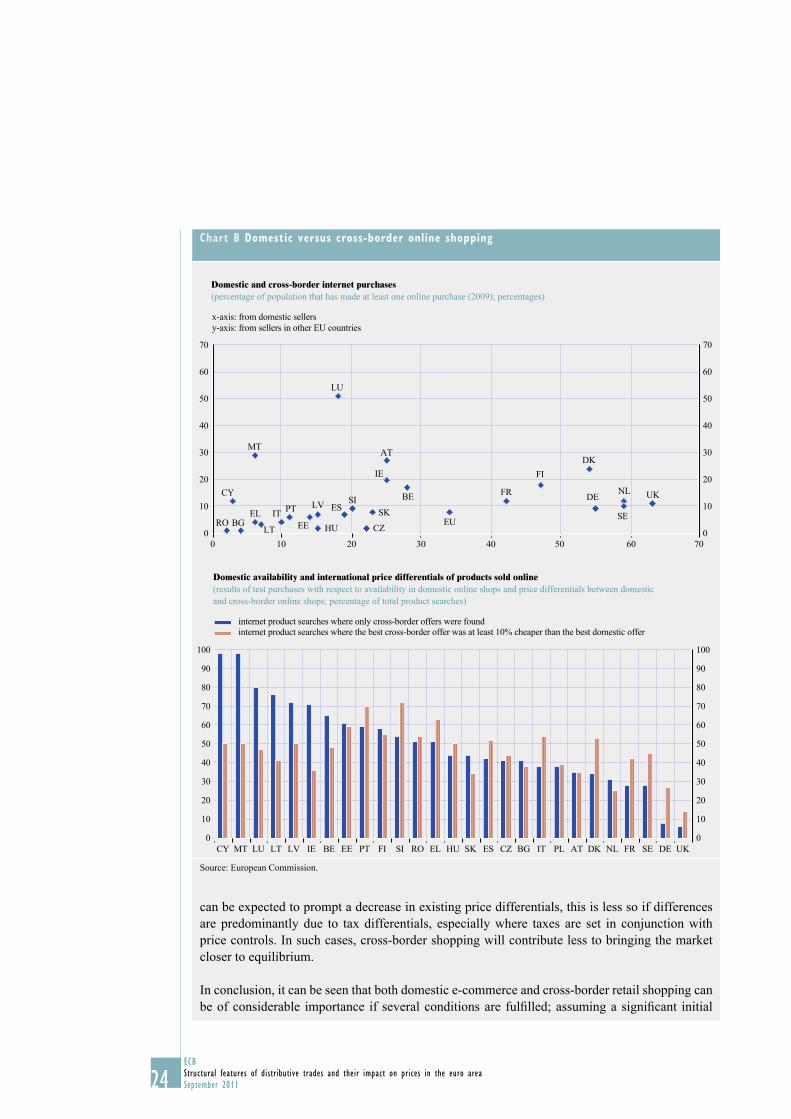

Box 1

ONLINE RETAIL TRADE AND THE DEGREE OF CROSS-BORDER RETAIL COMMERCE

Online retail trade is often regarded as the epitome of a “perfect” market and associated with

improved possibilities for market participants to compare prices 1 (increased transparency) and with

a dramatic decrease in the importance of geographical proximity for consumption expenditure.

The evolution of online retail trade should contribute to lower prices, less (local) pricing power

on the part of individual market participants and increased competition. In addition, sellers would

have a better chance of reaching more customers, which would allow for economies of scale.

Consumers would have access to a wider range of products, as their product choice would not be

limited to the supply of goods available in local sellers’ stores. From a monetary policy perspective,

the evolution of online retail trade is interesting for two main reasons: the potential for lower and

regionally (but also internationally) less divergent prices for equal or comparable products and

the possibility of more fl exible prices (i.e. more frequent price changes).2

The e-commerce market of the EU has grown considerably compared with that of other

economies. In 2006, it was estimated to have reached a value of €106 billion, which was roughly

comparable to its US counterpart. Around 60% of internet users in the EU shopped online

in 2010, though fi gures vary strongly across countries.3 In particular markets, such as airline

travel, the emergence of online trade has completely altered the traditional operating models,

for example airline companies selling their services via travel agents. Today, some EU low-cost

carriers basically only sell their services online. The internet is also the fastest growing retail

channel. In 2008, only direct retail sales (used by 79% of retailers) were more common than sales

via e-commerce (used by 51% of retailers), and e-commerce was signifi cantly more popular than

mail order trade (30%). Although online trade is growing rapidly, it still accounts for just a small

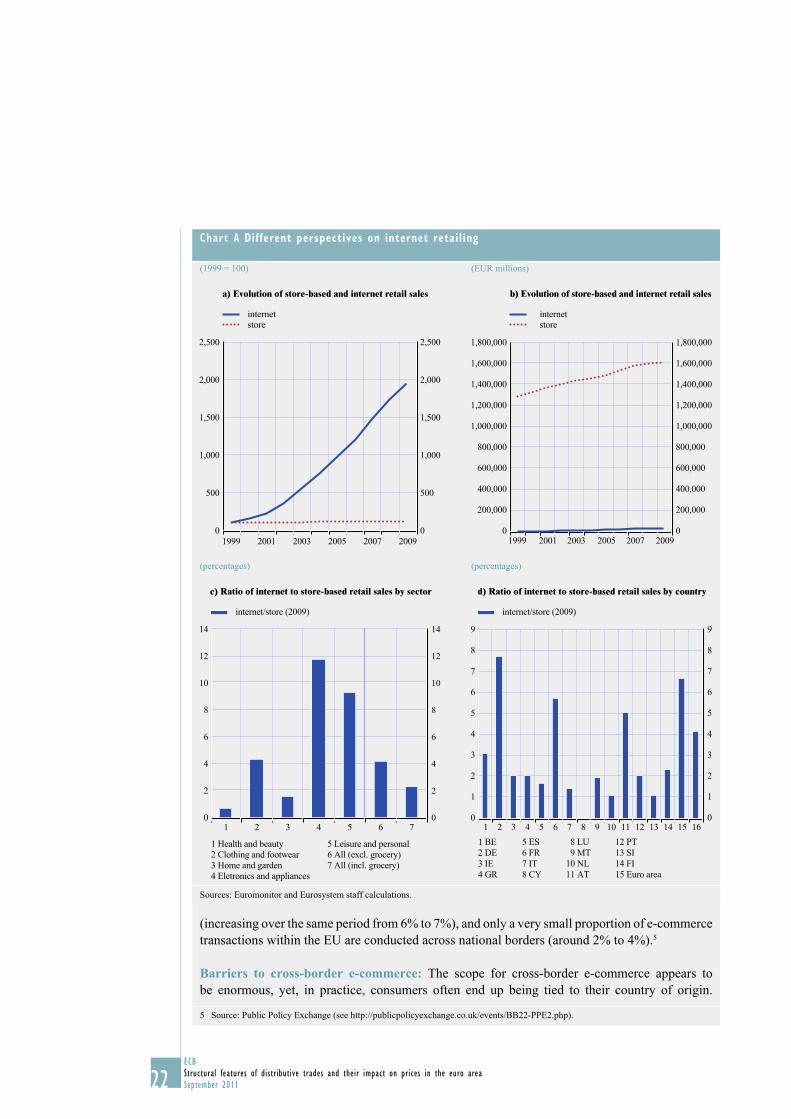

proportion of overall retail trade (see Chart A(a) and Chart A(b)), with some notable exceptions

across markets and countries (see Chart A(c) and Chart A(d)). The markets with the highest

penetration of online trade are electronics and appliances (12%), leisure and personal goods

(10%) and clothing and footwear.4 Penetration remains relatively low in the health and beauty,

house and garden and grocery markets. Meanwhile, the ratio of online to store-based retail sales

is highest in Germany, Finland, France and the Netherlands, but relatively low in Spain, Italy,

Cyprus, Malta and Portugal.

One noticeable fact is the widening discrepancy between domestic and cross-border e-commerce. From 2006 to 2008, the share of all EU consumers purchasing at least one item over the internet

rose from 27% to 33%. Meanwhile, cross-border e-commerce remains much less important

1 According to the European Commission, the internet has become a convenient alternative to “window shopping” and is shaping the

way that consumers approach their purchasing activity: three out of fi ve Europeans with internet access at home compare prices online

before making a purchase, either online or in a physical store.

2 However, Lünnemann and Wintr (2011) have found that internet prices are not necessarily more fl exible than those of traditional

“brick and mortar” stores. Instead, there is substantial heterogeneity in the frequency of price changes across shop types and product

categories.

3 In Romania, for example, only 9% of internet users were found to shop online, while the corresponding fi gure for the United Kingdom

was much higher, at 79%. Meanwhile, 69% of the EU population is comprised of “internet users”, with 60% being “regular internet users”

(see Eurostat (2010)).

4 According to Nielsen (2010), internet sales are particularly popular in specifi c product categories, such as books, clothing and footwear,

electronics and music.

22ECB

Structural features of distributive trades and their impact on prices in the euro area

September 2011

(increasing over the same period from 6% to 7%), and only a very small proportion of e-commerce

transactions within the EU are conducted across national borders (around 2% to 4%).5

Barriers to cross-border e-commerce: The scope for cross-border e-commerce appears to

be enormous, yet, in practice, consumers often end up being tied to their country of origin.

5 Source: Public Policy Exchange (see http://publicpolicyexchange.co.uk/events/BB22-PPE2.php).

Chart A Different perspectives on internet retailing

(1999 = 100) (EUR millions)

a) Evolution of store-based and internet retail sales b) Evolution of store-based and internet retail sales

0

500

1,000

1,500

2,000

2,500

0

500

1,000

1,500

2,000

2,500

1999 2001 2003 2005 2007 2009

internet

store

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

1999 2001 2003 2005 2007 2009

internet

store

(percentages) (percentages)

c) Ratio of internet to store-based retail sales by sector d) Ratio of internet to store-based retail sales by country

0

2

4

6

8

10

12

14

0

2

4

6

8

10

12

14

internet/store (2009)

1 Health and beauty

2 Clothing and footwear

3 Home and garden

4 Eletronics and appliances

5 Leisure and personal

6 All (excl. grocery)

7 All (incl. grocery)

1 2 3 4 5 6 70

1

2

3

4

5

6

7

8

9

0

1

2

3

4

5

6

7

8

9

internet/store (2009)

1 BE

2 DE

3 IE

4 GR

5 ES

6 FR

7 IT

8 CY

8 LU

9 MT

10 NL

11 AT

12 PT

13 SI

14 FI

15 Euro area

1 2 3 4 5 6 7 8 9 1110 12 13 14 15 16

Sources: Euromonitor and Eurosystem staff calculations.

23ECB

Structural features of distributive trades and their impact on prices in the euro area

September 2011

I AN OVERVIEW

OF THE DISTRIBUTIVE

TRADES: STRUCTURAL,

REGULATORY AND

COMPETITION FEATURES

Frequently, they are either redirected to national sites or refused a sale. In an EU-wide test of

online shops, it was possible in only 39% of cases to place an order with an online shop that

was not located in the same country as the buyer. The remaining 61% of orders failed either

because traders refused to serve the consumer’s country or for other reasons (technical problems

or because a particular payment option was not available). Language barriers may also have been

an issue here, but their importance is not easy to quantify.

Regulatory barriers contribute to signifi cant market fragmentation at the EU level. Consumer

law, electronic waste regulations and postal systems are affected by regulatory fragmentation.

Complex value added tax (VAT) requirements for traders selling across borders make it diffi cult

for smaller brands and retailers to do business across the EU. These restrictions are directly

hindering the growth and competitiveness of small and medium-sized enterprises now active in

this sector or aspiring to be so in the future.

Thus, barriers to cross-border trading appear to be the biggest obstacle to the growth of

e-commerce in the EU. Nevertheless, the potential for more cross-border online shopping and,

hence, for increased competition, lower prices and greater price fl exibility seems to be there.

In 2008, one-third of EU citizens indicated that they would consider buying goods or services

from another Member State online if these were cheaper or better. In addition, in more than half

of all Member States, at least 50% of the products tested were found to be at least 10% cheaper

in a foreign internet shop (shipping costs included). Furthermore, it was generally the case that

half of the tested products could not be found in any domestic internet shop.

Cross-border shopping could play a signifi cant role in the development of the Single Market.

The potential effect of an improved regulatory environment – with suffi cient trust between market

participants – on cross-border online trade can also be seen from examples of particularly intense

“traditional” cross-border retail shopping, e.g. between the Republic of Ireland and Northern

Ireland and within the “Grande Région” encompassing Luxembourg and the surrounding regions

of Belgium, Germany and France.6

There are several drivers of cross-border retail shopping. Of course, price differentials (owing

to matters of taxation (e.g. VAT), exchange rates, and perhaps also factors such as differences

in labour costs, living standards, and in the rent levels or pricing practices of wholesalers) play

a role. Differences in the range of available products or simply (additional) transport costs close

to zero (e.g. if people cross the border anyway as they work in the neighbouring country or in

the case of particular geographical proximity) are further drivers.7 Cross-border retail trade can

increase competition and thus contribute to reducing price level differences across countries and

regions (Section 2.1 discusses the fact that prices appear to vary more across borders/countries

than within borders/countries). The potential impact on price levels and divergence between

prices obviously depends on the determinants of this divergence. While cross-border shopping

6 In Luxembourg, 9.5% of consumption expenditure by resident households took place outside national borders in 2009 (rising

from 5.4% in 2002). Consumption by non-resident households reached 22% of total private consumption in the country.

Thus, cross-border shopping can clearly be a bi-directional phenomenon. Some goods are cheaper in Luxembourg, while others can

be purchased for less abroad. For instance, at its normal rate of 15%, VAT is lower in Luxembourg than in the surrounding countries,

but some sellers complain about not having the possibility of importing goods from the most competitive foreign supplier and about

being forced to make imports via Belgium – some of the producers here have assigned a certain “territorial exclusivity” regarding

Luxembourg to Belgian intermediaries, which leads to additional costs. In addition, some goods produced for the German market,

for example, cannot be offered by domestic fi rms, as these goods are not traded by the Belgian intermediary and are only offered by

German intermediaries.

7 See European Commission (2003), p. 8.

24ECB

Structural features of distributive trades and their impact on prices in the euro area

September 2011

can be expected to prompt a decrease in existing price differentials, this is less so if differences

are predominantly due to tax differentials, especially where taxes are set in conjunction with

price controls. In such cases, cross-border shopping will contribute less to bringing the market

closer to equilibrium.

In conclusion, it can be seen that both domestic e-commerce and cross-border retail shopping can

be of considerable importance if several conditions are fulfi lled; assuming a signifi cant initial