striving for success - rti · striving for success ... the protection of our environment, ......

TRANSCRIPT

Striving for Successin the Global Marketplace

RIDLEY TERMINALS INC.2016 ANNUAL REPORT

TABLE OF CONTENTS

01 Message from the Chairman 02 President’s Letter 04 Management’s Discussion and Analysis 11 Governance 12 Glossary of Terms 13 Statement of Management Responsibility 14 Independent Auditor’s Report 16 Statement of Financial Position 17 Statement of Comprehensive Income18 Statement of Changes in Equity 19 Statement of Cash Flows 20 Notes to the Financial Statements 36 Directory

Prince Rupert 44823685

Vancouver 4879

Seattle 4972

Los Angeles

5635

Lázaro Cárdenas

6925

Shanghai

TokyoBeijing

Hong Kong

Ridley Terminals Inc. (RTI) is uniquely positioned to play an important role in supporting exports from NorthAmerica to meet a growing global demand. RTI offers a highlevel of quality, reliable and uninterrupted services. Located on Ridley Island in Prince Rupert, British Columbia, RTI can offercustomers reduced sailing time to Asia by more than one day compared toVancouver, and nearly three days vis-à-vis Long Beach, California. Establishedin 1983, the Terminal has been operating for 34 years.

RTI historically serviced coal mines and refineries in northern British Columbia, Alberta and Saskatchewan. Commencing in 2010 theTerminal received product from the Southeast region of British Columbia and in 2011 received coal from the United States, both underlong term terminal service agreements. RTI’s customers produce high quality metallurgical coals used in steelmaking, as well as coal usedfor power generation, while the refineries produce petroleum coke as a byproduct. Coal accounts for 81% of RTI’s handling volume, withthe remaining volume coming from Petroleum Coke shipments. The majority of product shipped through RTI is destined for Asia, withproduct also being shipped to South America and Europe.

RTI’s vision is to provide value to the Crown while expanding on its role as a leading trade gateway between North American and worldmarkets. RTI’s mission is to provide its customers with premium, on-time services, while maintaining a safe and rewarding workenvironment.

In 2009 RTI and the Prince Rupert Port Authority came to terms on a 30 year land lease arrangement, with the option for a further 20 yearrenewal term. The 50 year term provides a working footprint for RTI and provides both parties with the peace of mind and security of along term working relationship. RTI also holds the rights to an adjacent area for a further 102 acres of additional stockyard capacity.

Newcastle 4148

NAUTICAL MILESBETWEEN PORTS

RTI 2016 ANNUAL REPORT | 01

Ridley Terminals Inc.

MESSAGE FROM THE CHAIRMAN

March 18, 2017

Honourable Marc GarneauMinister of TransportPlace de Ville, Tower C, 29th Floor,330 Sparks Street,Ottawa, ON, K1A 0N5

Minister,

On behalf of the Board of Directors, management and staff of Ridley Terminals Inc., I am pleased to provide to you our 2016 Annual Report.

The Board, management and staff continue to operate RTI in a commercial manner as mandated by the Government of Canada. Worldcoal prices experienced some recovery from the prior years’ decline and while shipment volumes have followed suit to an extent, theyhave yet to return to historical levels so the terminal continues to face challenges.

Significant steps continue to be taken to reduce costs and develop efficiencies until the shipping volumes

improve and diversification efforts come to fruition. In terms of the current diversification efforts, the terminal

has advanced its plan to facilitate the first propane export facility on Canada’s west coast, having now received

approval from federal regulators in respect of its project with AltaGas Ltd. In addition, diversification continues

to be explored beyond existing commodities.

As always, safety at RTI remains a primary focus. Continual efforts at improvement have helped to maintain low incident occurrencesrequiring medical attention. As noted previously, RTI believes zero lost time is the only acceptable objective and the Board, managementand staff will continue to work to that goal.

On behalf of the Board of Directors I would like to extend our continued thanks and appreciation to RTI’s management and staff.

Yours sincerely,

Signed Byng Giraud

Chair (Interim), Ridley Terminals Inc.

Ridley Terminals Inc.

02 | RTI 2016 ANNUAL REPORT

PRESIDENT’S LETTER

March 18, 2017

Our primary objective at RTI today is to develop and convert a terminal supporting only onecommodity, into one in support of a diversified set of Canadian commodities requiring access tooverseas markets. Our goal is to achieve this objective in a highly responsible manner, where thesafety and pride of our employees, the protection of our environment, and the support of ourcommunity and clients, serve as the guiding values in the process. In conducting our transformation,“respect” is the key word describing the approach to all facets of our path.

The year of 2016 was a turning point in our development. Coal markets reached

the bottom of their market cycle and we are now seeing signs of recovery with

increased volume handled in the last quarter of the year. We now have some

very interesting prospects under negotiation and if positively concluded, these

prospects will serve to stabilize our sources of revenue. In collaboration with our

main partner, CN Rail, we have already implemented some major improvements

to our respective operations, in a manner that will help both RTI and CN become

more efficient in serving our shared markets and making our clients truly

successful in the global marketplace.

In our effort to diversify our operation and reduce the risk for our shareholders, we have concluded asolid partnership with AltaGas, that will now result in the construction of the first LPG export terminalon Canada’s West Coast. We are currently working on new projects that will further improve anddiversify our sources of revenues, providing growth at the terminal for years to come.

Signed Marc DuludePresident and Chief Operating Officer

RTI 2016 ANNUAL REPORT | 03

04 | RTI 2016 ANNUAL REPORT

MANAGEMENT’S DISCUSSION & ANALYSIS

Ridley Terminals Inc.

SummaryAfter two and half years of declining shipment volumes handledby Ridley Terminals Inc. (RTI), a rally in coal and petroleum cokeshipments was experienced during the latter portion of 2016.During the fourth quarter of 2016, RTI’s customers benefittedgreatly from a rise in market prices that turned into a near recordsetting resurgence, where the premium hard coking coalbenchmark hit highs above the $300 per metric tonne mark. Thisrally, resulted in a nearly fourfold increase from the lows of 2015and early 2016. The driver for the resurgence was an undersupplyof product, resulting from production and labour interruptions invarious Australian mining operations, as well as changes indomestic mining policies issued by the Government of China.

In 2015 and early 2016, two of RTI’s customers filed forbankruptcy, while a few others during this same time periodrelinquished their deposits related to future capacity reservationsor made decisions to curtail or shutdown mining activities untilmarket conditions improve. Coal and petroleum coke producers

are now faced with the difficult decision of whether or not to wait for further signs of market stability before introducing higherlevels of production or restarting idle mines. During 2016, RTI wasable to execute a new contract with Conuma Coal Resources Ltd.,who had acquired the Canadian assets of Walter Energy Inc. in theTumbler Ridge region of British Columbia. Conuma restarted one of the three mines it acquired in September of 2016, with asecond mine recommencing operations in early 2017, and a third mine to recommence operations in the near future.

Even with the upswing in volumes to end the year, RTI’s railunloading volumes decreased in 2016 by 10.36% or 442,000tonnes when compared to 2015 for a total of 3,823,000 tonnesunloaded (2015: 4,265,000 tonnes). Ship-loading volumesdecreased by 9.93% or 440,000 tonnes during 2016 for a total of 3,992,000 tonnes loaded (2015: 4,432,000 tonnes).

Total comprehensive loss for 2016 was $1,291,000 (2015:$63,387,000). However, normalized income during the period,excluding revenue recognized on relinquished site capacityreservations of $0 (2015: $49,050,000), a non-recurring, non-cash

Forward-looking StatementsCertain statements in this report are forward-looking statements and are not historical facts. Inherent in these forward-lookingstatements are risks and uncertainties beyond the control or the ability of the Company to predict. Readers are cautioned thatfuture results may vary materially from any results stated or inferred by forward-looking statements contained herein.

RTI 2016 ANNUAL REPORT | 05

entry for impairment of coal assets of $0 (2015: $99,495,000) and anon-recurring legal settlement expense of $12,395,000 (2015: $0),was $11,104,000 (2015: loss of $12,942,000) for an increase of$24,046,000 or 185.80% since 2015.

Due to recent and past downturns in coal and petroleum cokemarkets, management initiated a diversification initiative to betterinsulate itself from exposure to the future troughs in the market.One such initiative has been met. RTI secured an agreement withAltaGas Ltd. to sublease a specific area of RTI’s footprint in orderfor AltaGas Ltd. to unload, store and load liquefied petroleum gas(LPG) for export. This project has received all necessary approvalsto proceed, a positive final investment decision has been reachedby AltaGas Ltd. and construction will begin in 2017, withshipments of LPG from RTI’s berth to commence in 2019.

Further diversification efforts continue to look towards a myriad ofCanadian commodities requiring an outlet to overseas markets.RTI’s primary advantage over other West Coast terminals in NorthAmerica is the existence of a deep-water berth capable ofhousing vessels up to 250,000 DWT. RTI has additional capacityoptions at its availability and continues to explore the potentialfor further terminal utilization and development. Diversificationefforts are not only being undertaken to better position RTI toweather fluctuating commodity cycles, but to also improve assetutilization by broadening the portfolio of products handled at RTI.

Operational Performance

OverviewThe following table depicts select measures of comparativeperformance for 2016:For the year ended December 31: 2016 2015 Var ($) Var (%)

Revenue (In thousands of $ CDN) 60,955 91,681 (30,726) -33.51%

Comprehensive (loss) profit (In thousands of $ CDN) (1,291) (63,387) 62,096 -97.96%

Cash flow from operations (In thousands of $ CDN) 15,240 18,273 (3,033) -16.60%

Vessel throughput (In thousands of tonnes) 3,992 4,432 (440) -9.93%

RevenuesFor the year ended December 31: 2016 2015 Var ($) Var (%)

(In thousands of Canadian dollars)

Throughput 39,547 39,885 (338) -0.85%

Shortfall penalties (Note 14) 18,588 - 18,588 100.00%

Berthage, lines and despatch 1,098 1,123 (25) -2.23%

Other 1,722 1,623 99 6.10%

Relinquished customer deposits and options (Note 14) - 49,050 (49,050) -100.00%

Total revenues 60,955 91,681 (30,726) -33.51%

Total revenues earned in 2016 were $60,955,000 (2015:$91,681,000) for a decrease of $30,726,000 or 33.51%.

Throughput revenue in 2016 was $39,547,000 (2015: $39,885,000)for a decrease of $338,000 or 0.85%. In 2016, the averagethroughput revenue per tonne of shipments increased by $0.91to $9.91, as opposed to $9.00 by the end of 2015. Lower overallvolumes handled resulted in a decreasing effect on throughputrevenue of $4,045,000, with a rise in average rates charged pertonne causing an opposing and increasing effect of $3,707,000 inthroughput revenue, netting to the overall change. Thus, the verysmall decrease in throughput revenue for the year is primarily aresult of lower volumes handled due to weak market conditionsin the first half of the year, offset by gains from annual terminalcontract rate increases.

Shortfall penalties of $18,588,000 were recognized in revenue in 2016 (2015: $0). Shortfall penalties are charged to customersthat do not achieve minimum annual contract volumes and arerecognized as revenue if the shortfall is not recoverable in futureperiods. Shortfall fees received, but where contractual recovery is possible in a future period, are booked as deferred revenue. See Note 14 within the Notes to the Financial Statements.

06 | RTI 2016 ANNUAL REPORT

Ridley Terminals Inc.

Berthage, lines and despatch revenue fell to $1,098,000 for adecrease of $25,000 or 2.23%, as a result of slightly less volumeand vessels handled in 2016.Other revenue rose to $1,722,000 (2015: $1,623,000) resulting inan increase of $99,000 or 6.10% over the same period in 2015. Thisincrease is primarily due to an increase in storage revenue earnedfrom coal stored on site at the terminal as slow moving inventorywas prevalent in the first half of the year.In 2016, $0 (2015: $49,050,000) of deposits and optionsrelinquished by customers, recorded as deferred, were recognizedin comprehensive income.Coal volumes accounted for 75.65% of total terminal shipments in2016, with petroleum coke covering the balance at 24.35%. Atotal of 57 vessels loaded product at RTI during 2016 comparedto 54 vessels in 2015. Average vessel cargo volumes fell to 70,000tonnes for a decrease of 12,000 tonnes over 2015.

Operating ExpensesFor the year ended December 31: 2016 2015 Var ($) Var (%)

(In thousands of Canadian dollars)

Salaries, wages and benefits 17,753 20,622 (2,869) -13.91%

Legal settlement (Note 21) 12,395 - 12,395 100.00%

Lease rental (Note 18) 12,200 10,465 1,735 16.58%

Depreciation (Note 11) 7,086 11,196 (4,110) -36.71%

Contract and professional services 5,269 4,938 331 6.70%

General and administration 3,273 3,345 (72) -2.15%

Loss on asset disposal (Note 11) 3,734 159 3,575 2248.43%

Equipment, operations and maintenance 2,518 3,390 (872) -25.72%

Site utilities 1,409 1,458 (49) -3.36%

Finance costs 705 907 (202) -22.27%

Other 339 349 (10) -2.87%

Management services (Note 19) 318 2,691 (2,373) -88.18%

Demurrage 39 11 28 254.55%

Bad debts 7 160 (153) -95.63%

Impairment of assets (Note 11) - 99,601 (99,601) -100.00%

Total operating expenses 67,045 159,292 (92,247) -57.91%

Expenses during 2016 totaled $67,045,000 (2015: $159,292,000)for a decrease of $92,247,000 or 57.91% over the prior year,primarily due to the non-recurring, non-cash entry forimpairment of the Company’s coal assets during 2015.

The following chart and summaries depict the proportion ofmanagement’s key operating expenditures, for 2016: ■ Salaries, wages and benefits = 26.48%■ Legal settlement (Note 21) = 18.49%■ Lease rental (Note 18) = 18.20%■Depreciation (Note 11) = 10.57%■ Contract and professional services = 7.86%

■ Loss on asset disposal (Note 11) = 5.57%

■General and administration = 4.88%

■ Equipment, operations and maintenance = 3.76%

■ Site utilities = 2.10%■ Finance costs = 1.05%■Other = 0.51%■Management services (Note 19) = 0.47%

■Demurrage = 0.06%■ Bad Debt = 0.01%

Salaries, wages and benefitsSalaries, wages and benefits fell to $17,753,000 from $20,622,000in 2015, for a decrease of $2,869,000 or 13.91%. This is due toincreased attrition at the terminal, as well as a reduction in shiftpremiums and overtime, which is consistent with 2016 levels ofthroughput at the terminal. In 2016, salaries, wages and benefitscomprised 26.48% of total expenses.

RTI 2016 ANNUAL REPORT | 07

Legal settlementLegal settlement rose to $12,395,000 from $0 in 2015. This is dueto a one-time, non-recurring legal settlement to that also resultedin the acquisition of wood-pellet terminal assets residing on theCompany’s leased land, previously owned by a past proponent of the Terminal. The legal settlement expense portion of the totaltransaction was $12,395,000 (Note 21). In 2016, legal settlementexpenditures comprised 18.49% of total expenses. Lease rentalLease rental expenses during 2016 were $12,200,000 comparedto $10,465,000 in 2015, for an increase of $1,735,000 or 16.58%.RTI’s lease agreement with the Prince Rupert Port Authority islinked to throughput volumes at the terminal. However,minimum volume guarantees require the Company to makeminimum payments at a higher threshold than the Terminal’s2016 throughput volumes (Note 18). In 2016, lease rentalexpenses comprised 18.20% of total recurring expenses.DepreciationDepreciation expenses fell to $7,086,000 from $11,196,000 in2015, for a decrease of $4,110,000 or 36.71%. This decrease was a result of a reduced depreciable net book value of coalassets resulting from 2015’s impairment of property, plant andequipment. In 2016, depreciation expense comprised 10.57% of total recurring expenses.

Contract and professional servicesContract and professional services rose to $5,269,000 from$4,938,000 in 2015, for an increase of $331,000 or 6.70%. Typically,a result of continued commercial and diversification initiatives,outlays in regards to professional services vary from year to year.In 2016, contract and professional service expenses comprised7.86% of total expenses.General and administrationGeneral and administration expenses for 2016 were $3,273,000compared to $3,345,000 in 2015, for a decrease of $72,000 or2.15%. The decreased general and administration expense during the period varied in tandem with the slight reduction inthroughput revenue experienced in 2016. In 2016, general andadministration comprised 4.88% of total recurring expenses.Loss on asset disposalLoss on asset disposal increased to $3,734,000 from $159,000 in2015, for an increase of $3,575,000 or 2,248.43%. this significantincrease was due to the derecognition of items of property, plantand equipment with limited use at the Terminal that occurredduring the year. In 2016, loss on asset disposal comprised 5.57%of total recurring expenses.

08 | RTI 2016 ANNUAL REPORT

Ridley Terminals Inc.

Equipment, operations and maintenanceEquipment, operations and maintenance expenses fell to$2,518,000 from $3,390,000 in 2015, for a decrease of $872,000 or25.72%. Decreases in equipment, operations and maintenanceexpenses were a result of the slight decrease in overallthroughput experienced in 2016 coupled with lower non-capitalmaintenance costs, in comparison with the prior year. In 2016,equipment, operations and maintenance expenses comprised3.76% of total recurring expenses.

Management servicesManagement service expenses for 2016 were $318,000 comparedto $2,691,000 in 2015, for a decrease of $2,373,000 or 88.18%. The significant decrease in management service expenses duringthe period resulted from a change in management structure atthe Company for 2016 (Note 19). In 2016, management expensescomprised 0.47% of total recurring expenses.

Site utilitiesSite utilities fell to $1,409,000 from $1,458,000 in 2015, for adecrease of $49,000 or 3.36%. Decreases in site utilities were aresult of slightly decreased throughput during the year, causinglower consumption at the terminal. In 2016 site utilities expensescomprised 2.10% of total recurring expenses.

Cash FlowsCash flows from operating activities fell in 2016 to $15,240,000(2015: $18,273,000) for a decrease of $3,033,000 or 16.60% over 2015. This decrease is driven, by slightly lower terminalthroughput, but more notably, by increases of cash paid tosuppliers due to the legal settlement paid during the year (Note 21). However, this effect was counteracted by an $8 millionincrease in deposits from received from AltaGas during the year.

Cash flows from investing activities increased to $1,674,000 (2015:an outlay of $41,617,000) for an increase of $43,291,000 or104.02% over 2015. A significant portion of RTI’s fixed terminvestments, for which large cash outlays occurred in 2015,matured and were converted to cash during the year (Note 5).Management expects to reinvest these cash proceeds in 2017.Also included in this figure, is the $18 million in capital outlays for property, plant and equipment maintenance and upgradesduring the year.

Cash flows used in financing activities decreased slightly to$7,782,000 (2015: $7,799,000) for a decrease of $17,000 or 0.22%over 2015. No additional financing was drawn and regularrepayments were made with a slight reduction in interest onlower principal.

RTI 2016 ANNUAL REPORT | 09

CustomersRTI’s current customers have weathered a storm over the pastseveral years and have emerged into a profitable seaborn tradingmarket once again. Production from customers in the fourthquarter is up nearly 50% over the prior year’s fourth quarter, andRTI’s new customer, Conuma Coal Resources Limited, continuesto ramp up production from its mines in Tumbler Ridge. Inaddition to current customers, RTI is seeing a surge in interestfrom new customer looking to gain access to Asian markets for the sale of coal and petroleum coke from their respectiveoperations. New mine developments in Western Canada stillremain a possibility, but RTI itself remains conservativelyoptimistic on this front.

MarketsOversupply in the international coal markets continued into 2016 with a turnaround experienced in the latter half of the year.During 2016, China introduced production constraints on alldomestic mining operations to combat supply glut and complywith environmental sanctions. This effect, when combined withseveral supply issues with major Australian producers, pushed theprice of prime hard coking coal to near record highs.

Prices have since relaxed as a number of producers increasedproduction and restarted previously idled operations. In addition,

the Chinese relaxed supply constraints in response to thedemand through the winter season. Prices for prime hard coking coal have since stabilized above $160/MT.

Outlook on pricing remains positive as the Chinese plan totighten the restrictions on domestic production once again.However, it remains to be seen, whether or not new supplycoming online worldwide will outstrip demand once again.

PeopleRTI operates under a collective agreement with the InternationalLongshore and Warehouse Union (ILWU) local 523. The currentagreement, ratified in 2015, is for a term of six-years, expiring mid-2021. The safety record at RTI is commendable and this isachieved by a dedicated workforce who takes great pride inmaintaining a strong safety culture. The employees of RTI areapplauded for their ability to maintain and operate a Terminal inits 33rd year of operations, with once again very few interruptionsin service levels.

CommunityAs an industry leader, RTI recognizes that it not only has aresponsibility to its customers, but also to its community. RTIenjoys a strong relationship with the surrounding communitiesand strives to strengthen the relationships through activecommunity involvement and open communication aboutterminal developments.

RTI is situated within Tsimshian territory and strives to workcooperatively with the Coast Tsimshian First Nations of LaxKw’alaams and Metlakatla to develop and foster a good workingrelationship, and a commitment to work together towardcommon goals.

RTI takes pride in its ability to give back to Prince Rupert and thesurrounding communities through corporate social responsibility.The Company supports many community organizations byproviding funding in the areas of education, fine arts, team andevent sponsorships, and donations to many community events.Our level of involvement in the community has continued togrow over the years, and will continue to be a commitment of the company.

Ridley Terminals Inc. will continue to strive for excellence now and into the future for our customers, our communities, and ouremployees. Ridley Terminals will continue to initiate dialogue withthe public, liaise with the surrounding communities, and supportlocal education and other charitable initiatives in order to fulfillour obligation to be sound stewards of the surroundingcommunity and its environment.

10 | RTI 2016 ANNUAL REPORT

ResourcesThe completion of the stockyard conveyance expansion andsecond tandem rotary dumper will occur as market conditionsdictate and are being carefully observed as a potential option atpresent. Previous achievements included a major retrofit of theexisting rail unloading facility, the civil work required to providefor an additional 35 acres of stockyard, a significant increase in theterminal’s inbound and outbound rail lines, as well as the additionof a third stacker-reclaimer and its related conveyance, withretrofitting of the two original stacker-reclaimers on site to similarperformance capabilities to the third stacker-reclaimer.

As planned, the initiatives RTI has undertaken over the last severalyears has increased our terminal’s effectiveness and efficiency,improving both rail and vessel handling times. The ultimateindicator is that, once again, relatively no vessel demurrageexpense was experienced during 2016.

RegulatorySection 138(2) of the Financial Administration Act requires thateach crown corporation shall cause a special examination to becarried out at least once every ten years. The special examinationof RTI was due in December 2015 and was deferred pending theoutcome of the sale process. A special examination of RTI iscurrently underway. The Office of the Auditor General of Canadawill conduct the examination.

Environmental, Health and SafetyIn order to ensure environmental compliance, RTI is certified tothe ISO 14001 standard. RTI’s Health and Safety system is certifiedto the OHSAS 18001 standard. The Terminal puts at the forefrontof its operations and planning initiatives, compliance to strongenvironmental stewardship, as well as the resources necessary tosupport the Health and Safety programs.

RTI 2016 ANNUAL REPORT | 11

GOVERNANCE

The Articles of Incorporation state that Ridley Terminal Inc.’s(RTI’s) activities must be in compliance with therequirements of Part X of the Financial Administration Act(R.S.C. c. F-11). The by-laws provide for a Board of Directors(Board) consisting of from 3 to 7 members; and a minimum of 4 meetings of the Board each year. Byng Giraud was appointed as Chairman of RTI’s Board on October 4th, 2012. The Board has maintained theappointment of an Audit Committee and has also createdseveral vehicles to strengthen overall governance and toensure more effective oversight and accountability.

RTI’s management team, led by Marc Dulude, Presidentand COO, is responsible for the day to day activities at RTI, while working under the stewardship of the Board.

Emphasis has continued to be placed on avoidance of all unsafe practices, support of various community eventsand charities continue, and RTI stakeholders have shownincreased support for RTI’s financial self-sufficiency.

Ridley Terminals Inc.

OutlookAt December 31, 2016, RTI had working capital available of$97,552,000 (2015: $77,231,000) for an increase of $20,321,000 or26.31% and a current ratio of 4.98 (2015: 3.33). This increase inworking capital was due to decreased accounts payable andincreases in cash and accounts receivable. The strength of theseperformance measures across 2016 continues to exemplify thestrong cash management practices currently employed at RTI tomaintain sufficient cash to discharge all liabilities, despite thesustained downturn in coal markets. Forecasted shipments forcoal and petroleum coke are expected to outpace 2016, withexpectations for an increase of at least 25%.

Diversification efforts undertaken by RTI have led to the creationof an agreement between RTI and a Proponent to service bulkLPG for export through RTI’s existing dock facility. The Proponentis AltaGas Ltd., which has signed a sublease agreement allowingAltaGas Ltd. to construct an unloading and storage facilitysituated at RTI. A final investment decision was made by AltaGasLtd. on January 3, 2017, with actual construction activity to occurlater in the year.

Efforts beyond this commodity continue to be explored as RTIcontinues its agenda to become a multi-user and multi-commodity export terminal for bulk products produced in NorthAmerica.

As always, management continues to strive for greater efficiency,growth, and productivity. It is with continued confidence that wepresent RTI’s 2016 Annual Report.

Ridley Terminals Inc.

12 | RTI 2016 ANNUAL REPORT

GLOSSARY OF TERMS

DemurrageThe charterer of a ship is bound not to detain it, beyond thestipulated or usual time, to load or deliver the cargo, or to sail. Theextra time beyond the calculated laytime (being the days allowedto load and unload the cargo) are called the days of demurrage.The term is likewise applied to the payment for such delay.

DespatchRevenue earned when a vessel is loaded and or discharged morerapidly than the allowed laytime. Despatch is the opposite ofdemurrage and generally amounts to half of the demurrage rate.

Consumer Price Index (CPI) An indicator of changes in consumer prices experienced byCanadians. It is obtained by comparing, over time, the cost of afixed basket of goods and services purchased by consumers. The CPI is widely used as an indicator of the change in thegeneral level of consumer prices or the rate of inflation.

ImpairmentA reduction in the carrying value of property, plant andequipment to reflect a lower value in use of the property, plantand equipment, to the end of its useful life. This change bookvalue is calculated with careful analysis of expected future cashflows and fair market value, and is triggered by changing externalfactors such as demand from markets for the company’s services.

International Organization for Standardization (ISO)A global federation of over a hundred national standards bodieswith central secretariat in Geneva, Switzerland. An ISO standard isan international standard published by the ISO. For example:The ISO 14000 environmental management standards exist toensure products and services have the lowest possibleenvironmental impact.

Liquified Petroleum Gas (LPG)Also referred to as simply propane or butane, is a mixture ofhydrocarbon gases used as fuel in heating appliances, cookingequipment, and vehicles.

Metallurgical CoalBituminous coal from which the volatile constituents are drivenoff by baking in an oven at temperatures as high as 2,000 degreesFahrenheit so that the fixed carbon and residual ash are fusedtogether forming coke, which along with pulverized coal isconsumed in making steel.

Petroleum cokeA carbonaceous solid derived from oil refinery cracking processes.Crude oil must be refined to produce gasoline and otherproducts. A residue is left over from this process that can befurther refined by coking it at high temperatures and under greatpressure. The resulting product is pet coke, a hard substance thatis similar to thermal coal.

Stacker-ReclaimerA large machine that has the capability of both stacking bulkmaterials into storage piles and recovering (reclaiming) thematerial, using a bucket wheel, from the storage piles. Stacker-Reclaimers are rated in tonnes per hour for capacity and travel ona rail between stockpiles in the stockyard. It can typically move inthree directions: horizontally along the rail, vertically by luffing itsboom, and rotationally by slewing its boom.

Thermal CoalCoal used for steam/power generation or for space heatingpurposes, including all anthracite coals and bituminous coals not included under coking coal.

RTI 2016 ANNUAL REPORT | 13

Ridley Terminals Inc.

STATEMENT OF MANAGEMENT RESPONSIBILITY

The accompanying financial statements of Ridley Terminals Inc. (the Company), and all information in the annual report pertaining to the Company, are the responsibility of management, and have been approved by the Board of Directors.

These financial statements have been prepared by management in accordance with International Financial Reporting Standards (IFRS).Financial statements are not precise, because they include some amounts that are based on estimates and judgments. Management hasdetermined such amounts on a reasonable basis. Financial information used in the annual report is consistent with that in the financialstatements.

Management maintains a system of internal control designed to provide reasonable assurance that assets are safeguarded and controlled, transactions comply with relevant authorities and accounting systems provide relevant and reliable financial information.

The Board of Directors of the Company is responsible for ensuring that management fulfills its responsibilities for financial reporting andinternal controls. The Board exercises this responsibility through an Audit Committee consisting of three non-management members. The Audit Committee meets regularly with management and with the external and internal auditors to review the scope and result of theannual audit, and to review the financial statements and related financial reporting matters prior to submitting the financial statements tothe Board of Directors for approval.

These financial statements have been independently audited in accordance with Canadian generally accepted auditing standards by the Company's external auditor, the Auditor General of Canada, and his report is included with these financial statements.

Signed Signed M. Dulude C. DixonPresident & COO Controller

March 23, 2017

14 | RTI 2016 ANNUAL REPORT

Ridley Terminals Inc.

RTI 2016 ANNUAL REPORT | 15

December 31 December 312016 2015

$ $

ASSETSCurrent assets

Cash and cash equivalents (Note 5) 76,080 67,552 Short-term investments (Note 6) 20,475 20,087 Accounts receivable (Note 7) 18,171 15,174 Inventory (Note 8) 7,045 7,220 Prepaid expenses (Note 9) 311 291

122,082 110,324

Non-current assetsLong-term investments (Note 6) - 20,122 Pension benefit asset (Note 10) 3,250 - Property, plant and equipment (Note 11) 169,797 174,668

173,047 194,790

295,129 305,114

LIABILITIESCurrent liabilities

Accounts payable and other liabilities (Note 12) 10,813 21,516 Current portion of long-term debt (Note 13) 7,291 7,077 Current portion of deferred revenue (Note 14) 6,426 4,500

24,530 33,093

Non-current liabilities Other liabilities 317 637 Long-term debt (Note 13) 13,287 20,578 Asset retirement obligation (Note 15) 7,199 6,989 Deferred revenue (Note 14) 48,117 39,717 Pension benefit liability (Note 10) - 1,130

68,920 69,051

93,450 102,144

SHAREHOLDER'S EQUITYCapital stock (Note 16) 136,042 136,042 Contributed surplus (Note 16) 64,000 64,000 Accumulated retained earnings 1,637 2,928

201,679 202,970

295,129 305,114

Commitments (Note 18), Contingencies (Note 21)

The accompanying notes are an integral part of these financial statements.

STATEMENT OF FINANCIAL POSITIONFor the year ended December 31 (in thousands of Canadian dollars)

16 | RTI 2016 ANNUAL REPORT14

Ridley Terminals Inc.

2016 2015

$ $

REVENUESThroughput 39,547 39,885 Shortfall penalties (Note 14) 18,588 - Other 1,722 1,623 Berthage, lines and despatch 1,098 1,123 Relinquished customer deposits and options (Note 14) - 49,050

60,955 91,681

EXPENSESSalaries, wages and benefits 17,753 20,622 Legal settlement (Note 21) 12,395 - Lease rental (Note 18) 12,200 10,465 Depreciation (Note 11) 7,086 11,196 Contract and professional services 5,269 4,938 Loss on asset disposal (Note 11) 3,734 159 General and administration 3,273 3,345 Equipment, operations and maintenance 2,518 3,390 Site utilities 1,409 1,458 Finance costs 705 907 Other 339 349 Management services (Note 19) 318 2,691 Demurrage 39 11 Bad debts 7 160 Impairment of assets (Note 11) - 99,601

67,045 159,292

NET OPERATING LOSS (6,090) (67,611)

Net foreign exchange (loss) gain (600) 1,718 Interest income 1,073 906

NET LOSS BEFORE OTHER COMPREHENSIVE INCOME (5,617) (64,987)

OTHER COMPREHENSIVE INCOME(Not to be reclassified to comprehensive income in subsequent periods)

Defined benefit plan actuarial gains (Note 10) 4,326 1,600

TOTAL COMPREHENSIVE LOSS (1,291) (63,387)

The accompanying notes are an integral part of these financial statements.

STATEMENT OF COMPREHENSIVE INCOMEFor the year ended December 31 (in thousands of Canadian dollars)

RTI 2016 ANNUAL REPORT | 17

Ridley Terminals Inc.

AccumulatedCapital Contributed Retained Stock Surplus Earnings Total

$ $ $ $

Balance at January 1, 2015 136,042 64,000 66,315 266,357

Total comprehensive lossLoss for the year - - (64,987) (64,987)Defined benefit plan actuarial gains - - 1,600 1,600

Total comprehensive loss for the year - - (63,387) (63,387)

Balance at December 31, 2015 136,042 64,000 2,928 202,970

Total comprehensive lossLoss for the year - - (5,617) (5,617)Defined benefit plan actuarial gains - - 4,326 4,326

Total comprehensive loss for the year - - (1,291) (1,291)

Balance at December 31, 2016 136,042 64,000 1,637 201,679

The accompanying notes are an integral part of these financial statements.

STATEMENT OF CHANGES IN EQUITYFor the year ended December 31 (in thousands of Canadian dollars)

18 | RTI 2016 ANNUAL REPORT

Ridley Terminals Inc.

2016 2015

$ $

OPERATING ACTIVITIESCash receipts from customers 53,239 54,379 Cash receipts from sub-lessee (Note 17) 15,000 8,006 Interest received 1,073 906 Cash paid for salaries, wages and benefits (15,327) (17,635)Defined benefit and defined contribution plan (Note 10) (2,766) (3,254)Cash paid to suppliers (24,450) (17,400)Cash paid for lease rental (11,529) (6,729)

Cash flows from operating activities 15,240 18,273

INVESTING ACTIVITIES Cash paid to purchase property, plant and equipment (Note 21) (18,063) (1,408)Cash from disposition of investments 19,737 - Cash paid to purchase investments - (40,209)

Cash flows from (used in) investing activities 1,674 (41,617)

FINANCING ACTIVITIESRepayment of long-term debt (7,077) (6,874)Financing costs paid (705) (925)

Cash flows used in financing activities (7,782) (7,799)

Net increase (decrease) in cash and cash equivalents 9,132 (31,143)Cash and cash equivalents, beginning of the year 67,552 96,967 Effect of exchange rate fluctuations on cash held (604) 1,728

Cash and cash equivalents, end of the year (Note 5) 76,080 67,552

The accompanying notes are an integral part of these financial statements.

STATEMENT OF CASH FLOWSFor the year ended December 31 (in thousands of Canadian dollars)

RTI 2016 ANNUAL REPORT | 19

Ridley Terminals Inc.

20 | RTI 2016 ANNUAL REPORT

Ridley Terminals Inc.

1 – GOVERNING STATUTES AND NATURE OF OPERATIONSRidley Terminals Inc. (the Company), incorporated under the Canada Business Corporations Act on December 18, 1981, operates a bulk commodityfacility on Ridley Island in Prince Rupert, British Columbia. The facility provides bulk commodity rail unloading, storage, and vessel loading services toa variety of North American coal producers. On June 11, 1998, the Canada Marine Act received Royal Assent. This Act came into force on November1, 2000, at which time the Canada Ports Corporation Act was repealed and the Canada Ports Corporation was dissolved. Under the Canada MarineAct, the Company became a parent Crown corporation named in Part I of Schedule III of the Financial Administration Act. The Company is a federalCrown corporation exempt from income tax.The Company is domiciled in Canada. The address of the Company’s principal place of business is 2110 Ridley Road, Prince Rupert, British ColumbiaV8J 4H3.In July 2015, the Company was issued a directive (P.C. 2015-1114) pursuant to section 89 of the Financial Administration Act to align its travel,hospitality, conference and event expenditure policies, guidelines and practices with Treasury Board policies, directives and related instruments ontravel, hospitality, conference and event expenditures in a manner that is consistent with its legal obligations, and to report on the implementationof this directive in the Company’s next corporate plan. The Company is in the process of updating its policies and will be providing guidelines andpractices to ensure compliance with the directive. The Company expects to complete the process during 2017.

2 – GOING CONCERNIn December 2012, the Company’s shareholder announced its intention to sell the business. These financial statements have been prepared without making any assumptions as to the outcomes of the potential sale, and, as such, they do not contemplate any significant changes to theCompany’s existing activities.

3 – BASIS OF PRESENTATION

Statement of ComplianceThe annual financial statements have been prepared in accordance with International Financial Reporting Standards (IFRS). The financial statements were authorized for issue by the Board of Directors on March 23, 2017.

Functional CurrencyThe financial statements are presented in Canadian dollars, which is the Company’s functional currency. All tabular financial information presentedin Canadian dollars has been rounded to the nearest thousand.

Use of Estimates and JudgmentsThe preparation of the annual financial statements in conformity with IFRS requires management to make judgments, estimates and assumptionsthat affect the application of accounting policies and the reported amounts of assets, liabilities, income and expenses. Actual results may differ fromthese estimates.Estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognized in the year in which the estimates are revised and in any future years affected.Information about assumptions and estimation uncertainties that have a significant risk of resulting in a material adjustment within the nextfinancial year are included in the following notes:Notes 4 and 11: Estimated useful lives of property, plant and equipment – assumption and estimation uncertainty exists within the useful lives used as actual useful lives of property, plant, and equipment could vary significantly from these assumptions and estimates. Note 11: Determination of recoverable amount of property, plant and equipment – assumptions and estimation uncertainty exists in the discount rate,inflation rate and cash flows used.Note 15: Asset retirement obligation – assumption and estimation uncertainty exists with the future undiscounted reclamation costs and the rates and timing used to discount the cost of reclamation, as actual costs of reclamation could vary significantly from these assumptions and estimates.Note 10: Pension benefits – assumption and estimation uncertainty exists within the discount rate, estimate of life expectancy, future salary increasesand overtime as a percentage of base salary assumptions used, as actual rates could vary significantly from these assumptions and estimates.Note 21: Contingencies – assumption and estimation uncertainty exists within contingencies described as actual results could vary significantly fromthese assumptions and estimates.

NOTES TO THE FINANCIAL STATEMENTS(amounts in tables are in thousands of Canadian dollars)

RTI 2016 ANNUAL REPORT | 21

Ridley Terminals Inc. | Notes to the Financial Statements(amounts in tables are in thousands of Canadian dollars)

The significant judgments made in applying the Company’s accounting policies include:Note 8: Classification of critical spares in inventory – significant judgements have been made to re-classify items from property, plant and equipment to inventory, based on the purpose of these items, and in determining the amount at which to transfer the items into inventory.Note 11: Determination of components and the method to be used to depreciate property, plant and equipment – significant judgments have been made to partition components and select a most representative depreciation method to accurately reflect the value in use of each componentacross the life of the component in service.Note 11: Determination of whether there were significant indicators that an impairment loss recognized in prior periods may no longer exist or may havedecreased – significant judgments have been made in assessing whether external and internal sources of information are significant and supportestimating the recoverable amount of assets for which an impairment loss was recognized in prior periods.Note 11: Recognition and measurement of property, plant and equipment – significant judgments have been made in determining whether futureeconomic benefits are expected to flow to the entity in recognizing property, plant and equipment and the amount to recognize as cost, in relation to the enclosed dry bulk storage assets acquired (Note 21).Note 14: Recognition of shortfall revenue – significant judgments have been made in determining the timing and ability of a customer to apply itsdeferred shortfall penalty to future throughput revenue.Note 14: Recognition of deferred sub-lease revenue – significant judgments have been made in determining whether transactions are linked, thecomponents of revenue, the allocation of consideration received, and the nature and timing of revenue recognition related to certain agreements.Note 14: Classification of deferred revenue between current and non-current liabilities – significant judgments have been made in determining theexpected timing of customers’ application of deposits and shortfall penalties to revenue.

4 – SIGNIFICANT ACCOUNTING POLICIESThe accounting policies set out below have been applied consistently to all years presented in these financial statements.

Foreign CurrencyTransactions in foreign currencies are translated to the functional currency of the Company at exchange rates on the dates of the transactions.Monetary assets and liabilities denominated in foreign currencies at the reporting date are translated to the functional currency at the exchange rate at that date. Foreign currency differences arising on translation are recognized in net profit or loss before other comprehensive income.

Cash and Cash EquivalentsCash and cash equivalents comprise cash balances and cash equivalents having a term to maturity of three months or less when acquired orconvertible to cash at any time at the option of the Company and subject to an insignificant risk of changes in value.

InvestmentsInvestments are comprised of fixed term guaranteed investments. These investments provide guaranteed principal and a higher rate of return for surplus cash balances not required for operational or other investment purposes for periods of up to two years.

Fair Value MeasurementFair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. The fair value measurement is based on the presumption that the transaction to sell the asset or transfer the liability takes place either:• In the principal market for the asset or liability, or• In the absence of a principal market, in the most advantageous market for the asset or liability

The principal or the most advantageous market must be accessible to the Company.The fair value of an asset or a liability is measured using the assumptions that market participants would use when pricing the asset or liability,assuming that market participants act in their economic best interest.The Company uses valuation techniques that are appropriate in the circumstances and for which sufficient data are available to measure fair value,maximizing the use of relevant observable inputs and minimizing the use of unobservable inputs.All assets and liabilities for which fair value is measured or disclosed in the financial statements are categorized within the fair value hierarchy,described as follows, based on the lowest level input that is significant to the fair value measurement as a whole:• Level 1 — Quoted (unadjusted) market prices in active markets for identical assets or liabilities• Level 2 — Valuation techniques for which the lowest level input that is significant to the fair value measurement is directly or indirectly observable• Level 3 — Valuation techniques for which the lowest level input that is significant to the fair value measurement is unobservable

22 | RTI 2016 ANNUAL REPORT

Ridley Terminals Inc. | Notes to the Financial Statements(amounts in tables are in thousands of Canadian dollars)

For the purpose of fair value disclosures, the Company has determined classes of assets and liabilities on the basis of the nature, characteristics and risks of the asset or liability and the level of the fair value hierarchy as explained above.

Financial InstrumentsA financial instrument is any contract that gives rise to a financial asset of one entity and a financial liability or equity instrument of another entity.

Financial AssetsInitial recognition and measurementThe Company’s financial assets are classified, at initial recognition, as financial assets at fair value through profit or loss or loans and receivables. All financial assets are recognized initially at fair value plus, in the case of financial assets not recorded at fair value through profit or loss, transactioncosts that are attributable to the acquisition of the financial asset.

Subsequent measurementa. Financial assets at fair value through profit or lossFinancial assets at fair value through profit or loss include financial assets held for trading and financial assets designated upon initial recognition atfair value through profit or loss. Financial assets are classified as held for trading if they are acquired for the purpose of selling or repurchasing in thenear term. Financial assets at fair value through profit or loss are carried in the statement of financial position at fair value with net changes in fairvalue presented as a loss or a gain in net operating profit or loss in the statement of comprehensive income. The Company has not designated anyfinancial assets at fair value through profit or loss.The Company’s cash and cash equivalents are classified as held for trading.

b. Loans and receivablesLoans and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. After initialmeasurement, such financial assets are subsequently measured at amortized cost using the effective interest rate (EIR) method, less impairment.Amortized cost is calculated by taking into account any discount or premium on acquisition and fees or costs that are an integral part of the EIR. The EIR amortization is included in interest income in the statement of comprehensive income. The losses arising from impairment are recognizedin net operating profit or loss in the statement of comprehensive income.The Company’s investments and accounts receivable are classified as loans and receivables.

DerecognitionA financial asset is primarily derecognized when the rights to receive cash flows from the asset have expired, or the Company has transferred its rights to receive cash flows from the asset and has transferred substantially all the risks and rewards of the asset.

Impairment of Financial AssetsThe Company assesses, at each reporting date, whether there is objective evidence that a financial asset or a group of financial assets is impaired. An impairment exists if one or more events that has occurred since the initial recognition of the asset, has an impact on the estimated future cashflows of the financial asset or the group of financial assets that can be reliably estimated. Evidence of impairment may include indications that thedebtors or a group of debtors is experiencing significant financial difficulty, default or delinquency in interest or principal payments, the probabilitythat they will enter bankruptcy or other financial reorganization and observable data indicating that there is a measurable decrease in the estimatedfuture cash flows, such as changes in arrears or economic conditions that correlate with defaults.

Financial assets carried at amortized costFor financial assets carried at amortized cost, the Company first assesses whether impairment exists individually for financial assets that areindividually significant, or collectively for financial assets that are not individually significant. If the Company determines that no objective evidenceof impairment exists for an individually assessed financial asset, whether significant or not, it includes the asset in a group of financial assets withsimilar credit risk characteristics and collectively assesses them for impairment. Assets that are individually assessed for impairment and for which an impairment loss is, or continues to be, recognized are not included in a collective assessment of impairment.The amount of any impairment loss identified is measured as the difference between the asset’s carrying amount and the present value ofestimated future cash flows (excluding future expected credit losses that have not yet been incurred). The present value of the estimated future cash flows is discounted at the financial asset’s original effective interest rate.The carrying amount of the asset is reduced through the use of an allowance account and the loss is recognized in net operating profit or loss in the statement of comprehensive income.

Financial LiabilitiesInitial recognition and measurementFinancial liabilities are recognized initially at fair value and, in the case of loans and borrowings and payables, net of directly attributable transactioncosts.The Company’s financial liabilities include accounts payable and other liabilities, and long-term debt.

Subsequent measurementAfter initial recognition, interest-bearing loans and borrowings are subsequently measured at amortized cost using the EIR method. Gains and lossesare recognized in net operating profit or loss in the statement of comprehensive income when liabilities are derecognized as well as through the EIR amortization process. Amortized cost is calculated by taking into account any discount or premium on acquisition and fees or costs that are anintegral part of the EIR. The EIR amortization is included as finance costs in the statement of comprehensive income.

RTI 2016 ANNUAL REPORT | 23

Ridley Terminals Inc. | Notes to the Financial Statements(amounts in tables are in thousands of Canadian dollars)

DerecognitionA financial liability is derecognized when the obligation under the liability is discharged or cancelled, or expires.

Offsetting of Financial InstrumentsFinancial assets and financial liabilities are offset and the net amount is reported in the statement of financial position if there is a currentlyenforceable legal right to offset the recognized amounts and there is an intention to settle on a net basis, to realize the assets and settle the liabilities simultaneously.

Share CapitalCommon shares are classified as equity. Incremental costs directly attributable to the issue of common shares are recognized as a deduction from equity.Preference share capital is classified as equity as it is non-redeemable, or redeemable only at the Company’s option, and any dividends arediscretionary. Dividends thereon are recognized as distributions within equity.

Property, Plant and EquipmentRecognition and measurementItems of property, plant and equipment are measured at cost less accumulated depreciation and accumulated impairment losses. Cost includes expenditures that are directly attributable to the acquisition of the asset. The cost of self-constructed assets includes the cost ofmaterials and direct labour, any other costs directly attributable to bringing the assets to a working condition for their intended use, the costs of dismantling and removing the items and restoring the site on which they are located, and borrowing costs on qualifying assets for which thecommencement date for capitalization is on or after January 1, 2010.When parts of an item of property, plant and equipment have different useful lives, they are accounted for as separate items of property, plant and equipment.Gains and losses on disposal of an item of property, plant and equipment are determined by comparing the proceeds from disposal with the carrying amount of property, plant and equipment, and are recognized net within gain or loss on asset disposal on the statement ofcomprehensive income.

Subsequent costsThe cost of replacing a part of an item of property, plant and equipment is recognized in the carrying amount of the item if it is probable that thefuture economic benefits embodied within the part will flow to the Company, and its cost can be measured reliably. The carrying amount of thereplaced part is derecognized. The costs of the day-to-day servicing of property, plant and equipment are recognized in net operating profit or loss as incurred.

DepreciationDepreciation is calculated on the depreciable amount, which is the cost of an asset less its residual value. Depreciation of an asset commenceswhen it is available for use.Depreciation is recognized in net operating profit or loss on a straight-line basis over the estimated useful lives of each part of an item of property,plant and equipment, since this most closely reflects the expected pattern of consumption of the future economic benefits embodied in the asset.Assets recognized under finance leases are depreciated over the shorter of the lease term and their useful lives unless it is reasonably certain that the Company will obtain ownership by the end of the lease term, in which case they are depreciated over the useful lives of the assets. The terminal facility assets are depreciated on a straight-line basis up to 2039.The estimated useful lives for all other asset classes are as follows:• Machinery and equipment 5-10 years• Office equipment and furniture 3-5 yearsDepreciation methods, useful lives and residual values are reviewed at each financial year end and adjusted if appropriate.

InventoryWarehouse inventory consists of supplies, consumables and repair parts. Inventory is initially recognized at the cost incurred to acquire it, and is subsequently measured at the lower of weighted average cost and net realizable value.

Impairment of Non-Financial AssetsThe carrying amounts of the Company’s non-financial assets, other than inventories, are reviewed at each reporting date to determine whetherthere is any indication of impairment. If any such indication exists, then the asset’s recoverable amount is estimated. The recoverable amount of an asset or cash-generating unit (CGU) is the greater of its value in use and its fair value less costs to sell. In assessingvalue in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current marketassessments of the time value of money and the risks specific to the asset. For the purpose of impairment testing, assets that cannot be testedindividually are grouped together into CGUs, the smallest group of assets that generates cash inflows from continuing use that are largelyindependent of the cash inflows of other assets or groups of assets.An impairment loss is recognized if the carrying amount of an asset or its CGU exceeds its estimated recoverable amount. Impairment losses arerecognized in net operating profit or loss. Impairment losses recognized in respect of CGUs are allocated to reduce the carrying amounts of theother assets in the unit on a pro rata basis.

24 | RTI 2016 ANNUAL REPORT

Ridley Terminals Inc. | Notes to the Financial Statements(amounts in tables are in thousands of Canadian dollars)

Impairment losses recognized in prior years are assessed at each reporting date for any indications that the loss has decreased or no longer exists.An impairment loss is reversed if there has been a change in the estimates used to determine the recoverable amount. An impairment loss isreversed only to the extent that the asset’s carrying amount does not exceed the carrying amount that would have been determined, net ofdepreciation or amortization, if no impairment loss had been recognized.

Employee BenefitsThe Company operates a defined benefit pension plan, which requires contributions to be made to a separately administered fund.The cost of providing benefits under the defined benefit plan is determined using the projected unit credit method.Re-measurements, comprising of actuarial gains and losses, the effect of the asset ceiling (excluding net interest) and the return on plan assets(excluding net interest) are recognized immediately in the statement of financial position with a corresponding debit or credit to othercomprehensive income in the period in which they occur. Re-measurements are not reclassified to comprehensive income in subsequent periods.Net interest is calculated by applying the discount rate used to discount the defined benefit obligation to the net defined benefit liability or asset.The Company recognizes the following changes in the net defined benefit obligation under salaries, wages and benefits in the statement ofcomprehensive income:• Service costs comprising current service costs, past-service costs, gains and losses on curtailments and non-routine settlements• Net interest expense or income• Administrative costs paid from plan assets

Defined contribution planA defined contribution plan is a post-employment benefit plan under which an entity pays fixed contributions into a separate entity and will haveno legal or constructive obligation to pay further amounts. Obligations for contributions to defined contribution pension plans are recognized as anemployee benefit expense in net operating profit or loss in the years during which services are rendered by employees. Prepaid contributions arerecognized as an asset to the extent that a cash refund or a reduction in future payments is available. Contributions to a defined contribution planthat are due more than 12 months after the end of the year in which the employees render the service are discounted to their present value.

Revenue and Deferred RevenueThroughput revenueThroughput revenue is earned for unloading customers’ bulk materials from rail cars and loading those materials on ships. Throughput revenue is determined by multiplying a customer’s contracted throughput rate by the number of tonnes handled. Fifty percent of throughput revenue isrecognized when bulk materials are unloaded from rail cars, and the remaining fifty percent is recognized when the materials are loaded on a ship.

Berthage, lines and despatchLines revenue is earned for securing ships to the Company’s berth during vessel loading. Berthage is earned for docking and undocking ships at the Company’s berth and despatch revenue is an incentive payment earned by loading ships faster than the stipulated standard timeframe. Lines,berthage and despatch revenue for each ship is recognized when the ship leaves the Company’s berth.

Sub-leaseCustomer sub-lease payments received in advance of access rights to property are initially recognized as deferred revenue and recognized asrevenue on a straight-line basis over the term of sub-lease agreement. Costs incurred in earning sub-lease revenue are recognized as an expense in the period incurred.

Shortfall penaltiesCertain contracts require customers to process a minimum volume of bulk materials each year and incur a shortfall penalty should this minimumnot be attained. If a contract allows a customer to apply the penalty to throughput charges in future years where the minimum volumerequirement is exceeded, the penalty amount is recognized in deferred revenue. Deferred amounts received are recognized as revenue when theyare applied to reduce throughput charges or when they cease to be recoverable by the customer. Where a contract does not allow a customer toapply the penalty in future years, penalty amounts are recognized in revenue in the year they are incurred.

OtherOther revenue includes revenue related to storage fees and other miscellaneous revenue earned by the Company. This revenue is recognized when related services are performed.

DepositsCustomer deposits are payments made by customers in consideration for a contractual obligation of the Company to supply throughput capacityin future periods. These payments are classified as deferred revenue and recognized as revenue when the customer is provided with the capacity it has reserved or when the customer relinquishes its contractual rights.

OptionsCustomer options are payments made by customers in consideration for the right to make a deposit and reserve throughput capacity in futureperiods. These payments are classified as deferred revenue. If an option lapses, it is recognized as revenue. If an option is exercised, the optionpayment is deemed to be part of the total consideration received for the reserved throughput capacity, and the option payment is recognized as revenue when the customer is provided with the capacity it has reserved.

RTI 2016 ANNUAL REPORT | 25

Ridley Terminals Inc. | Notes to the Financial Statements(amounts in tables are in thousands of Canadian dollars)

Net Gain on Recycled Site MaterialRecycled site material is excess bulk material made available in site cleanup and stockyard management activities. The material consists of a mixtureof different types of coal, gravel, wood pellets and other detritus. Judgment was applied in determining the accounting policy for recognizing,measuring, presenting and disclosing net gains on recycled site material. The Company recognizes an asset and a gain related to the recycled sitematerial when it is probable an economic benefit will flow to the Company from it, and when its value can be measured reliably. The asset ismeasured at net recoverable value with unrealized remeasurement gains or losses recognized in net gain or loss on recycled site material on thestatement of comprehensive income. Gross proceeds from the ultimate sale of recycled site material are netted with directly attributable costs,including the cost from derecognizing any related recycled site material asset already recorded as well as the cost from derecognizing any relatedprepaid freight and other selling expenses recorded as assets. The resulting net gain or loss on the ultimate sale of the recycled site material isrecognized in the net gain or loss on recycled site material line on the statement of comprehensive income.

Asset Retirement ObligationThe liability for an asset retirement obligation is recognized in the year incurred, for example, upon acquisition of an asset for which there is a related asset retirement obligation. This value is subsequently adjusted for any changes resulting from age, changes in regulatory requirements and any changes to the timing or the amount of the original estimate of undiscounted cash flows. The associated retirement costs are capitalized as part of the carrying amount of the capital asset and amortized over the life of the asset. The liability is increased over time through periodiccharges to income and it is reduced by actual costs of decommissioning and reclamation.

Government AssistanceAs the Government of Canada is the sole shareholder of the Company, government assistance received for the repayment of debt is recorded ascontributed surplus. Government assistance for the Company's capital assets is deferred and amortized to income on the same basis as the relatedcapital asset.

Lease PaymentsPayments made under operating leases are recognized in profit or loss on a straight-line basis over the term of the lease. Lease incentives received, if any, are recognized as an integral part of the total lease expense over the term of the lease.

Accounting Standards Issued But Not Yet EffectiveThe Company is currently assessing the impact that the following standards will have on the financial statements. The impacts of the changes are not known at this time.

IFRS 9: Financial instruments In July 2014, the IASB issued IFRS 9 - Financial Instruments, which replaces the earlier versions of IFRS 9 (2009, 2010, and 2013) and completes the IASB’s project to replace IAS 39 - Financial Instruments: Recognition and Measurement. IFRS 9 includes a logical model for classification andmeasurement of financial assets; a single, forward-looking ‘expected credit loss’ impairment model and a substantially-reformed approach to hedgeaccounting to better link the economics of risk management with its accounting treatment. IFRS 9 is effective for annual periods beginning on orafter January 1, 2018 and must be applied retrospectively with some exemptions. Earlier adoption is permitted. The Company has commenced apreliminary assessment of the potential impact of IFRS 9 on its financial statements and does not intend to early adopt the standard. The Companydoes not expect a significant impact from the adoption of IFRS 9.

IFRS 15: Revenue from Contracts with Customers In May 2014, the IASB issued IFRS 15 - Revenue from Contracts with Customers, which supersedes IAS 18 - Revenue, IAS 11 - Construction Contractsand other interpretive guidance associated with revenue recognition. IFRS 15 provides a single, principles-based five-step model to be applied to all contracts with customers to determine how and when an entity should recognize revenue. The standard also provides guidance on whetherrevenue should be recognized at a point in time or over time as well as requirements for more informative, relevant disclosures. IFRS 15 is effectivefor annual periods beginning on or after January 1, 2018 with earlier adoption permitted. The Company has established an implementation planand has commenced a preliminary assessment of the transition method and alternatives and the potential impacts of IFRS 15 on its financialstatements. The Company anticipates the adoption of IFRS 15 to have an impact on the financial statements, however the extent of the anticipatedimpact is not known at this time. The Company does not intend to early adopt the standard.

IFRS 16: LeasesIn January 2016, the IASB issued IFRS 16 - Leases, which supersedes IAS 17 - Leases. IFRS 16 establishes principles for the recognition, measurement,presentation and disclosure of leases. The standard establishes a single model for lessees to bring leases on-balance sheet while lessor accountingremains largely unchanged and retains the finance and operating lease distinctions. The standard requires lessees to recognize assets and liabilitiesfor all leases unless the lease term is 12 months or less or the underlying asset has a low value. IFRS 16 is effective for annual periods beginning on or after January 1, 2019 with earlier adoption permitted, but only if also applying IFRS 15 - Revenue from Contracts with Customers. The Company is currently evaluating the impact of IFRS 16 on its financial statements and does not intend to early adopt the standard. The Company anticipatesthe adoption of IFRS 16 to have an impact on the financial statements, however the extent of the anticipated impact is not known at this time.

Amendments to IAS 7 – Statement of Cash FlowsIn January 2016, the IASB issued amendments to IAS 7 - Statement of Cash Flows. The amendments require disclosures that enable users of thefinancial statements to evaluate changes in liabilities arising from financing activities, including both changes arising from cash flow and non-cashchanges. The amendments to IAS 7 are effective prospectively for annual periods beginning on or after January 1, 2017 with earlier adoptionpermitted. The Company intends to adopt the amendments to IAS 7 in its financial statements for the annual period beginning on January 1, 2017.The Company does not expect the amendments to IAS 7 to have a material impact on its financial statements.

26 | RTI 2016 ANNUAL REPORT

Ridley Terminals Inc. | Notes to the Financial Statements(amounts in tables are in thousands of Canadian dollars)

5 – CASH AND CASH EQUIVALENTS2016 2015

(In thousands of Canadian dollars) $ $

Cash 42,994 46,745 Term deposits 33,086 20,807

76,080 67,552

The Company’s exposure to market risk and a sensitivity analysis for financial assets and liabilities is disclosed in Note 20. Term deposits consist of a multi-term GIC with no penalty for withdrawal and a 3.65% rate of return, maturing in 2017, and a 30-day demand deposit account requiring 30-day notice before withdrawal but providing a higher yield than fully liquid savings accounts.

6 – INVESTMENTS2016 2015

(In thousands of Canadian dollars) $ $

Short-term investments 20,475 20,087 Long-term investments - 20,122

20,475 40,209

The Company’s exposure to market risk and a sensitivity analysis for financial assets and liabilities is disclosed in Note 20. Short-term investmentsconsist of a 2-year GIC with a 1.75% rate of return, maturing in August of 2017.

7 – ACCOUNTS RECEIVABLE2016 2015

(In thousands of Canadian dollars) $ $

Trade 17,641 15,146 Allowance for doubtful accounts (167) (160)Net trade receivable 17,474 14,986 Other 697 188

Total accounts receivable 18,171 15,174

The allowance for doubtful accounts is related to a receivable that is over a year past due and relates to one customer. Other accounts receivableconsists of net recoverable GST and miscellaneous receivables.

8 – INVENTORYThe amount expensed as a result of write-downs of inventory to net realizable value during the year was $98,000 (2015: $233,000). The amount ofinventory expensed during the year was $1,470,000 (2015: $841,000). During the year, the Company transferred items totaling $528,000 (2015; $0)from property, plant and equipment to inventory (Note 11). The Company has pledged its inventory as security for its long-term debt (Note 13).

9 – PREPAID EXPENSES2016 2015

(In thousands of Canadian dollars) $ $

Insurance 292 236 Other 19 55

311 291

Ridley Terminals Inc. | Notes to the Financial Statements(amounts in tables are in thousands of Canadian dollars)

RTI 2016 ANNUAL REPORT | 27

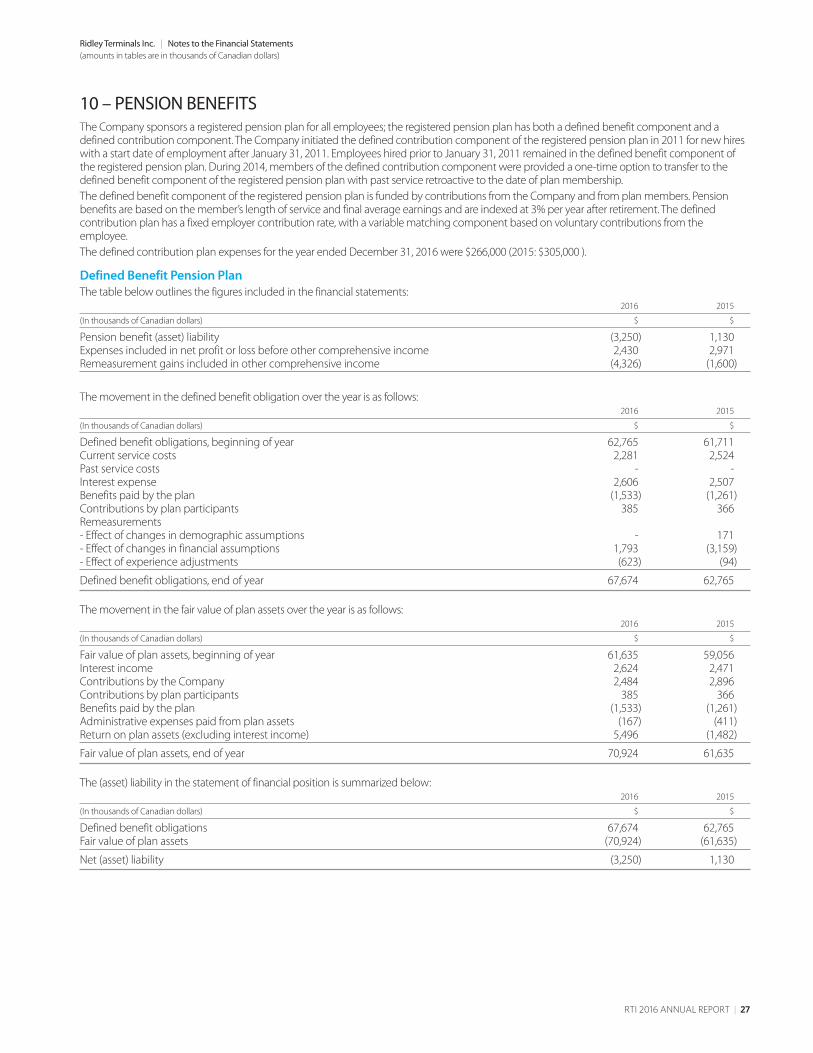

10 – PENSION BENEFITS The Company sponsors a registered pension plan for all employees; the registered pension plan has both a defined benefit component and adefined contribution component. The Company initiated the defined contribution component of the registered pension plan in 2011 for new hireswith a start date of employment after January 31, 2011. Employees hired prior to January 31, 2011 remained in the defined benefit component ofthe registered pension plan. During 2014, members of the defined contribution component were provided a one-time option to transfer to thedefined benefit component of the registered pension plan with past service retroactive to the date of plan membership.The defined benefit component of the registered pension plan is funded by contributions from the Company and from plan members. Pensionbenefits are based on the member’s length of service and final average earnings and are indexed at 3% per year after retirement. The definedcontribution plan has a fixed employer contribution rate, with a variable matching component based on voluntary contributions from theemployee.The defined contribution plan expenses for the year ended December 31, 2016 were $266,000 (2015: $305,000 ).

Defined Benefit Pension PlanThe table below outlines the figures included in the financial statements:

2016 2015

(In thousands of Canadian dollars) $ $

Pension benefit (asset) liability (3,250) 1,130 Expenses included in net profit or loss before other comprehensive income 2,430 2,971 Remeasurement gains included in other comprehensive income (4,326) (1,600)

The movement in the defined benefit obligation over the year is as follows:2016 2015

(In thousands of Canadian dollars) $ $

Defined benefit obligations, beginning of year 62,765 61,711 Current service costs 2,281 2,524 Past service costs - - Interest expense 2,606 2,507 Benefits paid by the plan (1,533) (1,261)Contributions by plan participants 385 366 Remeasurements - Effect of changes in demographic assumptions - 171 - Effect of changes in financial assumptions 1,793 (3,159)- Effect of experience adjustments (623) (94)

Defined benefit obligations, end of year 67,674 62,765

The movement in the fair value of plan assets over the year is as follows:2016 2015

(In thousands of Canadian dollars) $ $

Fair value of plan assets, beginning of year 61,635 59,056 Interest income 2,624 2,471 Contributions by the Company 2,484 2,896 Contributions by plan participants 385 366 Benefits paid by the plan (1,533) (1,261)Administrative expenses paid from plan assets (167) (411)Return on plan assets (excluding interest income) 5,496 (1,482)

Fair value of plan assets, end of year 70,924 61,635

The (asset) liability in the statement of financial position is summarized below:2016 2015

(In thousands of Canadian dollars) $ $

Defined benefit obligations 67,674 62,765 Fair value of plan assets (70,924) (61,635)

Net (asset) liability (3,250) 1,130

Ridley Terminals Inc. | Notes to the Financial Statements(amounts in tables are in thousands of Canadian dollars)

28 | RTI 2016 ANNUAL REPORT

The components of the defined benefit cost included in net operating profit or loss (NP) and other comprehensive income (OCI) are summarizedbelow:

2016 2015

(In thousands of Canadian dollars) $ $

Current service cost 2,281 2,524 Past service cost - - Net interest (income) expense (18) 36 Administrative expenses paid from plan assets 167 411

Defined benefit cost included in NP 2,430 2,971

Remeasurements - Effect of changes in demographic assumptions - 171 - Effect of changes in financial assumptions 1,793 (3,159)- Effect of experience adjustments (623) (94)- (Return) on plan assets (excluding interest income) (5,496) 1,482

Defined benefit gain included in OCI (4,326) (1,600)

The net (asset) liability is reconciled as follows:2016 2015

(In thousands of Canadian dollars) $ $

Net liability, beginning of year 1,130 2,655 Defined benefit cost included in NP 2,430 2,971 Defined benefit (gain) included in OCI (4,326) (1,600)Contributions by the Company (2,484) (2,896)

Net (asset) liability, end of year (3,250) 1,130

Assumed mortality rates are in accordance with the private Canadian pensioners’ mortality table issued by the Canadian Institute of Actuaries with mortality improvements under scale CPM-B.