streaming video 2015 04 10 - svod - the battle begins

TRANSCRIPT

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

10 April 2015

Asia Pacific/Australia

Equity Research

Radio & TV Broadcasting (Media (AU)/Telecommunications (AU))

Streaming video THEME

SVOD: The battle begins

■ Proven demand for SVOD: Experience overseas demonstrates proven

demand for SVOD. Netflix is in almost 40% of US Internet homes (over 37mn

subs), with c. 60% total penetration including Hulu/Amazon. SVOD has grown

quickly in the UK (estimated c. 25% broadband household penetration).

■ Australian user base to grow rapidly; we forecast 1.5mn subs by

yearend: We anticipate strong demand for SVOD in Australia, driven by: (1)

low price points; (2) quality content; (3) adoption of connected devices, e.g.

Apple TV and Google Chromecast; and (4) distribution deals with Telcos.

■ $700mn industry revenue by 2023; room for three profitable players:

We expect SVOD penetration in Australia to grow to US levels of 60% of

broadband households over time and for industry revenue of over $700mn

by 2023. Netflix, Stan and Presto all have compelling content offerings, and

we do not expect a huge difference in market share among the three. We

provisionally model Netflix to take the highest share (40%) due to its global

reach and track record. We forecast 33% share for Stan and 27% for Presto

(due to its higher price point of A$14.99 for movies and TV).

■ Strong start for Stan: NEC and FXJ launched their SVOD JV Stan at the

end of January and signed over 100k subscribers within six weeks. We

forecast distribution deals to help Stan reach 500k subscribers by year-end

and 2mn by 2023. Our expectation that the market will be fragmented puts a

cap on SVOD valuations. We value Stan at A$312mn on a DCF basis.

Figure 1: Australian SVOD subscriber forecasts

Source: ABS, Credit Suisse estimates. Note: Penetration of Broadband Households.

0%

10%

20%

30%

40%

50%

60%

70%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2015 2016 2017 2018 2019 2020 2021 2022 2023

Stan Presto Netflix

Gross Penetration Net Penetration

Research Analysts

Fraser McLeish

61 2 8205 4069

Lucas Goode

61 2 8205 4431

10 April 2015

Streaming video 2

Table of contents Executive summary – expect rapid growth in SVOD 3

SVOD penetration in the United States at 60% 3 We forecast over 3mn SVOD subscribers in Australia by 2017 and 6mn by 2023 4 Market share – room for three players 4 Stan – we value at A$312mn on DCF basis 5

The SVOD model – quality content at low price 6 Content is king 6 Pricing – services priced at A$8.99 to A$14.99 7 Adoption of connected devices increasing 8 Bandwidth and data caps largely sufficient for HD streaming 9 Distribution deals to help drive adoption 9

The experience overseas 11 Netflix now in 40% of broadband-connected households in the US 11 US market worth over US$4bn in 2014 12 UK SVOD penetration has reached 25% 12 UK market projected to be worth almost £800m by 2018 13

Australian SVOD market forecasts 14 Penetration forecast to reach 60% of broadband households by 2023F 14 Australian SVOD market worth $700mn by 2023 15 Netflix to take largest share; room for three profitable players 16

Stan forecasts – breakeven in year 3 18 Stan revenue and market share forecasts 18 Stan breakeven by year 3 18 Stan financial forecasts 19 Base case valuation of A$312mn 20

SVOD valuation summary – valuation upside muted 21 Appendix - Impact of SVOD on linear TV 22

US and UK ad spend still growing despite audience declines 22 SVOD doesn't necessarily destroy live viewing 22 Pay TV 'cord cutting' not widespread in US 23

10 April 2015

Streaming video 3

Executive summary – expect rapid growth in SVOD

We expect uptake subscription video on demand (SVOD) in Australia to grow rapidly following

the launch of three major services in the past three months (Stan, Presto and Netflix).

The initial signs are positive with Stan having said that it is on track for over 100k

subscribers by mid-March (six weeks from launch).

The key attractions of SVOD are the low price point (c. A$10 per month), a wide range of

on demand content and the ability to access the service over multiple devices. All

operators have been signing distribution deals with Telcos and ISPs, and we expect this to

be a key take-up driver. We expect a high degree of overlap, with customers subscribing

to more than one service. Figure 2 contains a summary of the main SVOD services.

Figure 2: Summary of Australian SVOD services

Source: Company websites and press releases

SVOD penetration in the United States at 60%

The success of Netflix in the US demonstrates that there is proven demand for SVOD.

Netflix reported almost 38mn domestic streaming subscribers in 4Q14, equivalent to

almost 40% penetration of US broadband households (31% of total households). Our US

Internet team expects strong subscriber growth to continue, with Netflix projected to reach

56mn domestic subs by 2018.

Nielsen says total penetration of SVOD services (including Amazon Prime Instant Video

and Hulu Plus, was 55.5% of US TV households in December 2014, implying penetration

of broadband households of over 60%. This is in a market with multichannel pay-TV

Service Price Devices Key content (exclusive content in bold)

$10 p/mth

*HD available

• Android• Apple TV (via

AirPlay)• Chromecast• iOS• PC

• Better Call Saul (AMC)• Gallipoli (original)• Transparent (Amazon)• Mozart in the Jungle (Amazon)• Community (NBC)• Star Trek (CBS)• CSI (CBS)• Ray Donovan (Showtime)• Dexter (Showtime)

• Californication (Showtime)• Doctor Who (BBC)• Top Gear (BBC)• Viacom children’s and general

entertainment content (Nickelodeon, MTV, Comedy Central)

• Movies from MGM, Paramount and Sony

$9.99 p/mth(TV only)$14.99 p/mth(incl movies)

*SD only

• Android• Chromecast• iOS• PC

• Boardwalk Empire (HBO)• Entourage (HBO)• Rome (HBO)• True Blood (HBO)• The Sopranos (HBO)• The Wire (HBO)• Modern Family (Fox)• Ray Donovan (Showtime)

• Dexter (Showtime)• Sons of Anarchy (Fox)• Homeland (Fox)• Californication (Showtime)• Viacom children’s and general

entertainment content • Movies from MGM, Disney,

Universal and Sony

$8.99 p/mth(1 device, SD)$11.99 p/mth(2 devices, HD)$14.99(4 devices, 4K)

*HD and Ultra HD available

• Android• Apple TV• Chromecast• iOS• PC• Playstation• Smart TVs• XBox

• House of Cards (original)• Orange is the New Black

(original)• Bloodline (original)• Marco Polo (original)• Daredevil (original)

• Lost (Disney)• Heroes (Universal)• Suits (Universal)• Homeland (Fox)• Arrow (Warner)• Movies from Warner, Sony,

MGM and Universal

$9.99 p/mthfor streaming

• Most devices (no Apple TV)

• 117k subscribers at Dec 2014 (down from 123k in June)• c70% are streaming subs (also offer DVD and Blu Ray)

10 April 2015

Streaming video 4

penetration of c. 85%. Nielsen data shows that 31% of SVOD users in the United States

subscribe to more than one service.

The UK has also seen a rapid uptake of SVOD. Netflix UK launched in 2012, and we

estimate SVOD penetration is already at 25% of broadband households based on

research by MTM and Futuresource Consulting.

We forecast over 3mn SVOD subscribers in Australia by 2017 and 6mn by 2023

We forecast SVOD uptake in Australia to follow a similar path to the UK and ultimately

achieve similar levels of penetration as the US.

We forecast 1.5mn SVOD subscribers by the end of 2015, with uptake driven by Telco

distribution deals. We forecast 3.2mn total SVOD subscribers in Australia by 2017

(37% penetration of broadband households) and 6.2mn subscribers by 2023 (60%

gross penetration of broadband households). Assuming half of all subscribers take

more than one service, this implies net penetration of c. 40% of broadband households

(36% of total households).

Figure 3: SVOD penetration of broadband households Figure 4: Australian SVOD subscription forecasts

Source: Company data, Statistica, MTM, HIS, ONS. Source: Credit Suisse estimates.

Market share – room for three players

We believe that the Australian SVOD market will be large enough to support three strong

players. We forecast total SVOD industry revenues to grow to c. A$700mn by 2023,

equivalent to c. 12% of total home entertainment and pay-TV subscription revenues

(compared to the US where SVOD already accounts for 23% of home entertainment

industry revenue in 2014).

We expect all three players to have compelling content offerings and for a high proportion

of customers to subscribe to more than one service. Differences in price points and

distribution partnerships will be a key driver of market share, in our view.

It is very early to try to forecast market shares, but on the basis of what we know to date,

we have made some provisional forecasts. Given the strength of the offerings, we do not

expect a significant gap in market shares among the three services. We assume:

■ Netflix – we forecast Netflix to be the number-one provider (a 40% market share

longer term). This reflects its strong track record in other markets and its global reach

providing the ability to invest in own produced content.

■ Stan – Stan has got off to a good start and has signed up a strong slate of content

deals. Its owners are committed to the space, and it has the simplest offering in terms

of price. We forecast Stan to achieve c. a 33% market share in the longer term.

■ Presto – Presto has the strongest distribution deals so we expect initial rapid uptake

as Telstra is providing 6m free to its new mobile and broadband customers. However,

Presto has the highest price point of the three operators (A$14.99 for movies and TV

39%

16%

60%

25%

0%

US UK Australia

Netflix Other

0%

10%

20%

30%

40%

50%

60%

70%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2015 2016 2017 2018 2019 2020 2021 2022 2023

Subscribers Net Penetration Gross Penetration

10 April 2015

Streaming video 5

bundled), so its content has to be meaningfully better in order to compete. We expect

Foxtel's cannibalisation dilemma to hold Presto back in terms of commitment to the

SVOD space. We forecast Presto to have 27% market share longer term.

Figure 5: SVOD subscribers by service Figure 6: Subscriber market share by service

Source: Credit Suisse estimates Source: Credit Suisse estimates

Stan – we value at A$312mn on DCF basis

Given our bullish outlook on SVOD subscriber growth, we believe that Stan can reach

500k subs by the end of 2015 and 750k subscribers by the end of 2016.

We forecast cash breakeven pre-marketing costs in 2016 and cash breakeven on a fully

allocated basis in 2017 (NEC has previously said that it expects breakeven on a pre-

marketing basis at 400-450k subs).

On a DCF basis, we value Stan at A$312mn (for 100%), equivalent to 9x FY20F EBITDA.

Whilst we expect the market to be large in terms of subscribers, the low price of the

product and our expectation that the market will be relatively fragmented would put a cap

on potential valuations for all players.

Figure 7: Stan summary financial forecasts

Source: Credit Suisse estimates. Note: Only includes cash marketing costs. Contra provided by partners not included.

0

500

1,000

1,500

2,000

2,500

3,000

2015 2016 2017 2018 2019 2020 2021 2022 2023

Netflix Stan Presto

20%

25%

30%

35%

40%

45%

2015 2016 2017 2018 2019 2020 2021 2022 2023

Stan Presto Netflix

2015 2016 2017 2018 2019 2020 2021 2022 2023

Year End Subs 500 750 1,050 1,260 1,449 1,630 1,793 1,937 2,072

Growth 50% 40% 20% 15% 13% 10% 8% 7%

Revenue ($m) 13 68 98 126 148 168 187 203 219

Expenses 43 65 78 96 109 120 129 136 142

EBITDA pre-marketing -30 4 20 30 38 48 58 68 77

Margin NM 5% 21% 23% 26% 29% 31% 33% 35%

Marketing Costs 18 10 13 12 13 14 15 15 16

EBITDA fully allocated -48 -6 7 17 26 34 43 52 60

Margin NM -9% 7% 14% 17% 20% 23% 26% 28%

10 April 2015

Streaming video 6

The SVOD model – quality content at low price

The rapid uptake of SVOD services around the world has been driven by a number of key

factors:

■ Content: Depth and quality of content is a necessity in attracting and retaining

customers and is the key differentiator between services.

■ Low price point: The low c. A$10 per month price point is key as it is a relatively small

commitment and means that consumers can generally afford more than one service.

We note that SVOD is particularly cheap relative to traditional pay-TV.

■ Availability of devices and fast broadband: Streaming requires connected devices

(e.g., Apple TV, connected smart TVs, Chromecast), fast Internet connections and

large data plans (Netflix is responsible for approximately one-third of US traffic).

■ Distribution: Partnerships with Telcos can provide a boost to subscriber acquisition

and retention. These arrangements also can include unmetered streaming.

We look at these issues in relation to the Australian market in more detail in this report.

Content is king

Managing the content mix is key to the SVOD model. The low-cost nature of the service

means that the content budget is relatively limited (when compared to pay-TV or

advertising funded FTA).

As a result, SVOD content tends to consist of a large library of older and typically non-

exclusive shows mixed with enough exclusive/proprietary and recent content to

differentiate itself from competitors and keep consumers coming back.

Content tends to be a mix of TV and movies, including full series that enable viewers to

'binge' on their favourite shows. Family and kids shows are a key part of the content mix.

SVOD is able to offer US cable content that is not shown on Australian FTA. It can also

cater to relatively niche audiences that can't be addressed by FTA (e.g., sci-fi, history, etc.).

Figure 8: Key Australian SVOD programming not available on FTA

Source: Company websites and press releases

The success of SVOD around the world is driving the creation of new content. There are

plenty of new shows becoming available in order to keep the content fresh enough so that

consumers continue to subscribe. SVOD providers are also increasingly generating their

own content (e.g., Netflix and Amazon).

10 April 2015

Streaming video 7

All three providers have announced a series of deals with major studios to date:

■ Stan: Key suppliers include AMC Networks, CBS/Showtime, NBCUniversal, MGM,

Village Roadshow, BBC Worldwide, Viacom and Sony Pictures. Exclusive shows

include Better Call Saul, Community and Amazon original Transparent.

■ Netflix: Major studio deals include Disney, Fox, NBCUniversal, Warner Bros and

Village Roadshow. Key exclusive content is Netflix original programming, such as

House of Cards, Orange is the New Black, Bloodline and Marco Polo.

■ Presto: Presto recently announced an output deal with 21st Century Fox, including

exclusive Australian SVOD rights to Modern Family. Presto also has exclusive

streaming rights to selected HBO content, including Boardwalk Empire, Entourage and

The Sopranos. Other studio agreements include CBS/Showtime, Disney, MGM, Sony

and Viacom. Presto also has access to original content from Foxtel and Seven.

Australian streaming search engine Gyde estimates that as at 24 March, Stan had the

largest library of the three major players, with c. 7,000 hours of content across 1,250 titles.

Netflix is estimated to have c5,000 hours and Presto c. 4,500 hours of content. We expect

these libraries to grow substantially over time (for example, Netflix Australia currently has

1,120 titles vs 7,110 titles on its US service, according to Gyde).

Content deals can take several forms, including:

■ Exclusive deals: Exclusive arrangements typically last for the life of the series. An

example is Stan's exclusive first-run Australian rights to Better Call Saul.

■ Life-of-series: Streaming rights to an ongoing series on a non-exclusive basis.

Depending on terms the content may be available immediately or subject to windowing.

■ Library content: Shorter-term agreements (typically two to three years) allowing a

service to select a certain number of hours from a studio's library subject to some

restrictions (e.g. windowing and tiering). The service may be able to update its library

during the life of the deal by removing older or unpopular items and replacing them with

other content.

Pricing – services priced at A$8.99 to A$14.99

The low monthly price of SVOD services is a key driver of adoption. The cost is a fraction

of full pay-TV and consumers can afford to subscribe to more than one service.

Netflix's standalone streaming plan in the US was priced from its launch in November

2010 through May 2014 at a single rate of US$7.99 per month, including streaming in HD

on up to two devices. In May 2014, Netflix moved to a new three-tiered pricing structure

(see Figure 9), with the cost of a basic subscription increasing by US$1 to US$8.99.

Existing subscribers were grandfathered in at the previous rate for two years.

Netflix made similar pricing changes to its international services at the time of the domestic

price increase, with the cost of the basic UK subscription raised from £5.99 to £6.99 per

month and "standard definition only" and "Family" plans added.

Netflix in Australia has the cheapest entry price for consumers at A$8.99, although this

only includes standard definition and access on a single device. Netflix benefits from not

having to charge GST as a foreign company (effectively a 10% cost benefit versus local

players). However, in order to watch high definition content and/or access via two devices

simultaneously, subscribers must pay A$11.99. A "Family" subscription that includes Ultra

HD (or 4K) streaming and access to four devices at once costs A$14.99 per month.

Stan has the simplest pricing model, with a single price of A$10 per month allowing access

to three screens at once in HD.

10 April 2015

Streaming video 8

Presto offers three separate subscriptions: A$9.99 for either Presto TV or Presto Movies,

or A$14.99 for both. Presto can be streamed on two devices simultaneously but does not

currently offer high definition.

Figure 9: SVOD pricing comparison

Australia USA UK

Netflix pricing per

month

A$8.99/mth (1 device, SD only)

A$11.99/mth (2 devices, HD)

A$14.99/mth (4 devices, 4K)

US$7.99/mth (1 device, SD only)

US$8.99/mth (2 devices, HD)

US$11.99/mth (4 devices, 4K)

£5.99/mth (1 device, SD only)

£6.99/mth (2 devices, HD)

£8.99/mth (4 devices, 4K)

Other SVOD pricing Stan A$10 per month

Presto A$9.99/mth for TV or

movies, A$14.99/mth for both

Hulu Plus US$8/mth

HBO Now US$15/mth

Lovefilm £5.99/mth

NOW TV Entertainment Pass

£6.99/mth

Pay TV ARPU (Cable

& Satellite only)

A$96/mth (Foxtel) US$117/mth (DirecTV)

US$84/mth (DISH)

£48/mth (Sky)

Source: Company data. ARPUs are for most recent reporting period.

Adoption of connected devices increasing

The ability to watch streaming content on multiple devices, particularly on the main screen,

is likely to be a key driver of adoption. Nielsen data shows that penetration of connected

devices is increasing (see Figure 10).

We estimate that 71% of Australian households now have a fixed broadband connection,

slightly below the US (78% in 2014 per Nielsen) and the UK (80% in 2014 per ONS). We

forecast broadband penetration to grow to 90% by 2022 (see Figure 11). Popular

connected devices and their compatibility with SVOD are summarised below.

■ Apple TV: Currently in over 1mn homes (source: SMH). Netflix has an app on Apple

TV. Stan can be watched via AirPlay. Presto currently doesn't support Apple TV.

■ Google Chromecast: Google has sold over 10mn units worldwide. Supported by all

three services.

■ Smart TVs: Nielsen data shows that 29% of Australians have Internet-ready TVs.

Parks Associates estimates that 70% of smart TV owners in the United States have

their sets connected. Netflix supports a number of smart TVs, the only service to do so.

■ IPTV: Presto is supported on c. 760k Telstra T-Boxes, Netflix on c. 200k Fetch TV

boxes.

■ Gaming consoles: Netflix is supported on Sony PlayStation and Microsoft Xbox One.

Stan and Presto are not currently compatible. Around 1.2mn PlayStations and Xboxes

were sold in Australia in 2014 alone according to data from NPD Group.

■ Smartphones and tablets: All three services support most newer iOS and Android

smartphones and tablets.

10 April 2015

Streaming video 9

Figure 10: Penetration of various devices Figure 11: Australian broadband penetration forecasts

Source: Nielsen. *Not necessarily connected Source: Company data, Credit Suisse estimates

Bandwidth and data caps largely sufficient for HD streaming

The average broadband download speed in Australia is 16.9Mbps (Source: Ookla), more

than sufficient to stream HD video. According to Netflix, SD streaming requires a download

speed of 1.5Mbps, while HD and Ultra HD streaming require speeds of 6.7Mbps and

15.5Mbps, respectively.

ABS data (see Figure 12) shows that 68% of Australian broadband connections have

advertised speeds above 8Mbps (sufficient for HD streaming), while 98% are able to

download at over 1.5Mbps (the minimum required for SD streaming).

All broadband plans under A$90 now include at least 200GB of data per month in their

bundled broadband/home phone plans (see Figure 13), while many are uncapped.

Standard definition streaming uses around 0.7GB of data per hour according to Netflix,

while HD and Ultra HD use 3GB/hr and 7GB/hr, respectively.

We also note that some of the services have agreed distribution deals that include

unmetering arrangements (e.g., iiNet/Netflix, Telstra/Presto).

Figure 12: Australian advertised download speeds (% of

total subscribers)

Figure 13: Data caps for plans under $90 per month

Source: Australian Bureau of Statistics, June 2014 Source: Company websites. *Includes 100GB bonus data **$80 p/mth

***$60 p/mth ^$70 p/mth

Distribution deals to help drive adoption

SVOD services have signed a number of distribution deals with Telcos. These agreements

include unmetering arrangements, longer free trials and bundling offers (with Telcos

paying a wholesale rate for the service). Distribution deals provide SVOD services with

significant exposure to large customer bases and help reduce marketing costs.

50%

22%18%

53%

37%

22%

55%

45%

29%

0%

10%

20%

30%

40%

50%

60%

PVR Households Tablet Penetration IPTV Capability*

2012 2013 20140%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2014 2015F 2016F 2017F 2018F 2019F 2020F 2021F 2022F 2023F

2%

31%

51%

17%

<1.5Mbps 1.5 - 8MBps 8 - 24MBps 24Mbps+

200GB

Unlimited

200GB

Unlimited Unlimited

Telstra* Optus iiNet** Dodo*** TPG^

10 April 2015

Streaming video 10

■ Presto currently has the best Australian distribution arrangements in place through its

relationship with Telstra (Telstra mobile, broadband and T-Box customers are eligible

for six months free Presto). These deals give it access to over 11mn mobile customers

(47% market share) and 3mn broadband customers (46% share).

■ Netflix's deals with Optus and iiNet provide exposure to c. 4.5mn mobile subscribers

and c2mn broadband customers.

■ Stan has announced a distribution deal with Vodafone covering both new and existing

customers on Vodafone Red plans, the only distribution deal with a mobile provider to

cover existing customers. We estimate that Vodafone has c. 2.5mn postpaid handheld

subscribers. Stan has also previously said that it is in discussions with Telstra.

10 April 2015

Streaming video 11

Figure 14: Australian SVOD distribution deals

Service Agreements

Netflix Unmetering arrangement with iiNet. We believe Netflix pays a small fee (c. A$1 per sub per month) to iiNet

Six months free Netflix to new Optus mobile or broadband customers on contracts of A$60 per month or more

(unmetered for fixed broadband customers)

Supported on Fetch TV service. Gives Netflix an extra installed base of c. 200,000 Fetch boxes

Presto Six months free Presto for new Telstra mobile and broadband customers (unmetered for fixed broadband

customers)

Six months free Presto for all T-Box owners (c760k T-Boxes in the market as of mid-2014)

Stan Three months free subscription to all existing Vodafone Red mobile subscribers

New and recontracting subscribers to Vodafone Red plans can choose to receive up to a year's free subscription to

Stan (six months for A$70 and A$80 plans, one year for A$100 plan)

Confirmed discussions with Telstra about "a promotional offer to Telstra customers"

Netflix has use of distribution deals globally, as it has expanded its geographic footprint. For

example, in the UK, Virgin Media last year added Netflix to its TiVo box, with new customers

receiving a six-month free subscription. Netflix signed a similar agreement with Orange in

France within two weeks of launch. Deutsche Telekom was Netflix's launch partner in

Germany, with the company's app being made available on the Telco's IPTV platform.

The experience overseas

Netflix now in 40% of broadband-connected households in the US

Netflix reported almost 38mn domestic streaming subscribers in 4Q14, equivalent to

c. 40% penetration of US broadband households and our US Internet team projects Netflix

to reach 56mn US subscribers by 2018 (equivalent to c. 52% penetration of broadband

households).

This high level of penetration has been achieved in a market where pay-TV penetration is

already high (86% of total TV households in 2014) and where there are a number of

competing SVOD services (e.g., Hulu and Amazon Instant Video).

Figure 15: Netflix domestic streaming subscribers Figure 16: Netflix domestic streaming penetration

Source: Company data, Credit Suisse estimates Source: Company data, IHS, Credit Suisse estimates

Including Amazon Prime Instant Video and Hulu Plus, Nielsen's Total Audience Report

(see Figure 17) estimates that total SVOD penetration of US TV households was 55.5% in

December 2014. We estimate that this equates to c. 60% penetration of broadband

households, or 58mn total subscriptions.

0%

10%

20%

30%

40%

50%

60%

0m

5m

10m

15m

20m

25m

30m

35m

40m

2008 2009 2010 2011 2012 2013 2014

Subscribers Growth

39%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

2008 2009 2010 2011 2012 2013 2014

All Households Broadband Households

10 April 2015

Streaming video 12

Nielsen data shows that around one-third of subscribers to Netflix, Amazon Prime and

Hulu Plus use more than one service (and 6% subscribe to all three). In total, Nielsen

estimates that 40.3% of US TV households (c. 44% penetration of broadband households)

subscribe to at least one SVOD service.

It is estimated that Netflix is now responsible for more than one-third of all downstream

Internet traffic in the US (see Figure 18).

Figure 17: Penetration of US TV households Figure 18: Share of US downstream Internet traffic

Source: Nielsen Total Audience Report Q4 2014 Source: Sandvine. Note: Fixed Internet only.

US market worth over US$4bn in 2014

The US SVOD market was worth US$4bn in 2014 and accounted for 23% of total home

entertainment revenue (source: Digital Home Entertainment Group). Netflix is projected to

earn US$5.8bn in domestic streaming revenue in 2018 according to our US team.

SVOD appears to be taking revenue share from other forms of home entertainment

(particularly DVD sales and rentals). Total US home entertainment revenue fell 2% in

2014, despite 27% growth in SVOD revenue, due to declines in physical sales and rentals

of 11% and 16%, respectively (see Figure 19).

Figure 19: US home entertainment revenue growth Figure 20: Share of US home entertainment revenue

(2014)

Source: Digital Home Entertainment Group Source: Digital Home Entertainment Group

UK SVOD penetration has reached 25%

Netflix entered the UK market in January 2012 and announced that it had reached 1mn

subscriptions by August 2012. Netflix was estimated to have reached 16% penetration of

Internet households in November 2014 (source: MTM Consulting), implying c. 3.5mn

subscribers.

34.9%

14.0%

3.0% 2.6% 1.4%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Netflix YouTube Facebook AmazonVideo

Hulu

2H13 1H14 2H14

-20%

-10%

0%

10%

20%

30%

40%

50%

SubscriptionVOD

Digital Sales Physical Sales PhysicalRental*

TransactionVOD

2013 2014

Subscription VOD23%

Digital Sales9%

Physical Sales39%

Physical Rental*, 19%

Transaction VOD11%

10 April 2015

Streaming video 13

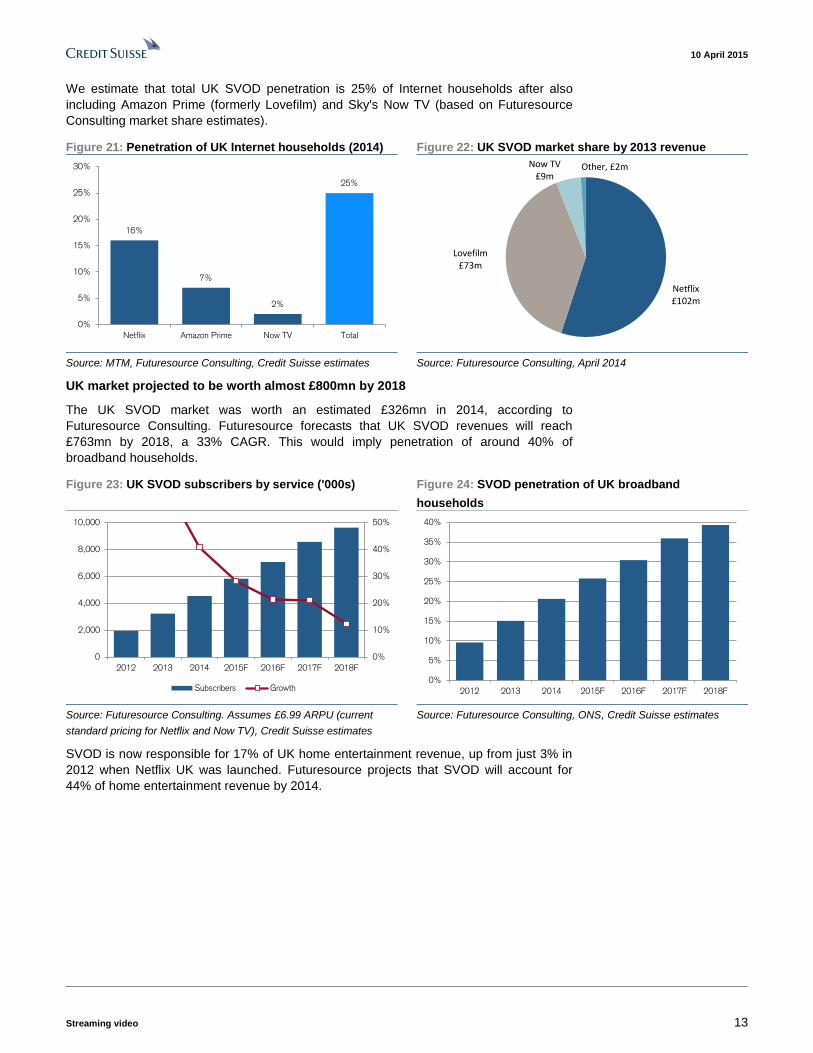

We estimate that total UK SVOD penetration is 25% of Internet households after also

including Amazon Prime (formerly Lovefilm) and Sky's Now TV (based on Futuresource

Consulting market share estimates).

Figure 21: Penetration of UK Internet households (2014) Figure 22: UK SVOD market share by 2013 revenue

Source: MTM, Futuresource Consulting, Credit Suisse estimates Source: Futuresource Consulting, April 2014

UK market projected to be worth almost £800mn by 2018

The UK SVOD market was worth an estimated £326mn in 2014, according to

Futuresource Consulting. Futuresource forecasts that UK SVOD revenues will reach

£763mn by 2018, a 33% CAGR. This would imply penetration of around 40% of

broadband households.

Figure 23: UK SVOD subscribers by service ('000s) Figure 24: SVOD penetration of UK broadband

households

Source: Futuresource Consulting. Assumes £6.99 ARPU (current

standard pricing for Netflix and Now TV), Credit Suisse estimates

Source: Futuresource Consulting, ONS, Credit Suisse estimates

SVOD is now responsible for 17% of UK home entertainment revenue, up from just 3% in

2012 when Netflix UK was launched. Futuresource projects that SVOD will account for

44% of home entertainment revenue by 2014.

16%

7%

2%

25%

0%

5%

10%

15%

20%

25%

30%

Netflix Amazon Prime Now TV Total

Netflix£102m

Lovefilm£73m

Now TV£9m

Other, £2m

0%

10%

20%

30%

40%

50%

0

2,000

4,000

6,000

8,000

10,000

2012 2013 2014 2015F 2016F 2017F 2018F

Subscribers Growth0%

5%

10%

15%

20%

25%

30%

35%

40%

2012 2013 2014 2015F 2016F 2017F 2018F

10 April 2015

Streaming video 14

Figure 25: UK home entertainment revenue growth Figure 26: UK SVOD % of home entertainment revenue

Source: Futuresource Consulting Source: Futuresource Consulting

Australian SVOD market forecasts

Penetration forecast to reach 60% of broadband households by 2023F

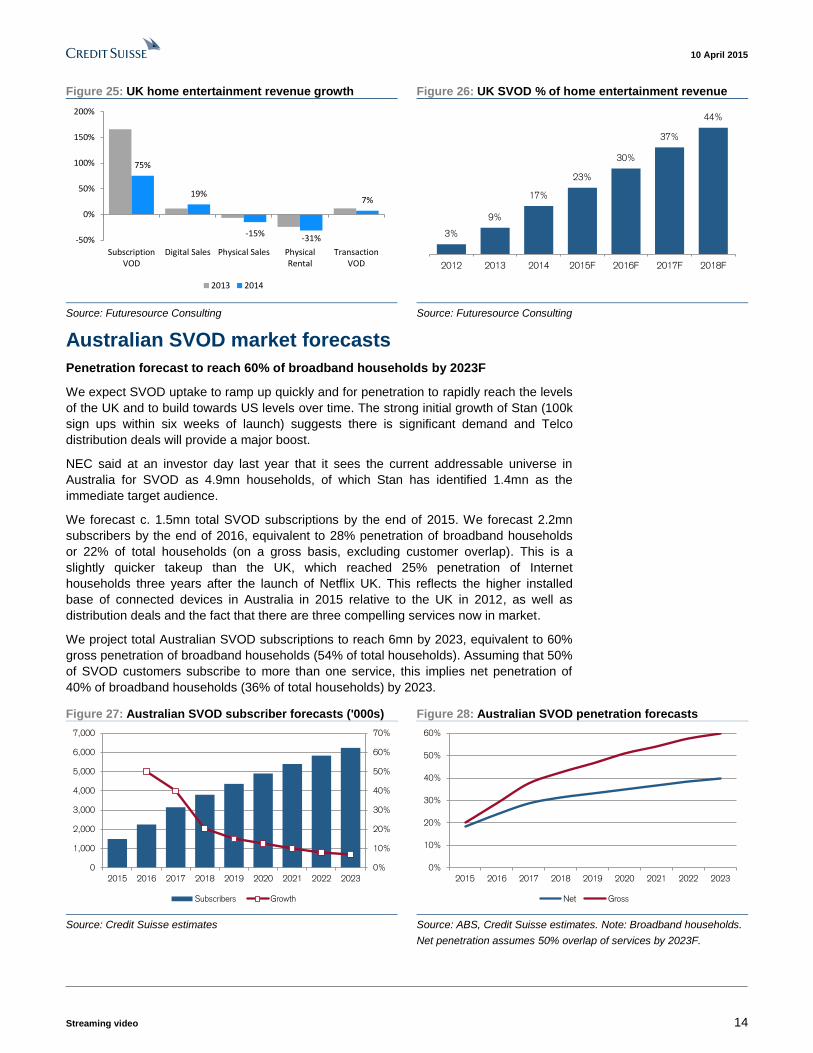

We expect SVOD uptake to ramp up quickly and for penetration to rapidly reach the levels

of the UK and to build towards US levels over time. The strong initial growth of Stan (100k

sign ups within six weeks of launch) suggests there is significant demand and Telco

distribution deals will provide a major boost.

NEC said at an investor day last year that it sees the current addressable universe in

Australia for SVOD as 4.9mn households, of which Stan has identified 1.4mn as the

immediate target audience.

We forecast c. 1.5mn total SVOD subscriptions by the end of 2015. We forecast 2.2mn

subscribers by the end of 2016, equivalent to 28% penetration of broadband households

or 22% of total households (on a gross basis, excluding customer overlap). This is a

slightly quicker takeup than the UK, which reached 25% penetration of Internet

households three years after the launch of Netflix UK. This reflects the higher installed

base of connected devices in Australia in 2015 relative to the UK in 2012, as well as

distribution deals and the fact that there are three compelling services now in market.

We project total Australian SVOD subscriptions to reach 6mn by 2023, equivalent to 60%

gross penetration of broadband households (54% of total households). Assuming that 50%

of SVOD customers subscribe to more than one service, this implies net penetration of

40% of broadband households (36% of total households) by 2023.

Figure 27: Australian SVOD subscriber forecasts ('000s) Figure 28: Australian SVOD penetration forecasts

Source: Credit Suisse estimates Source: ABS, Credit Suisse estimates. Note: Broadband households.

Net penetration assumes 50% overlap of services by 2023F.

75%

19%

-15%-31%

7%

-50%

0%

50%

100%

150%

200%

SubscriptionVOD

Digital Sales Physical Sales PhysicalRental

TransactionVOD

2013 2014

3%

9%

17%

23%

30%

37%

44%

2012 2013 2014 2015F 2016F 2017F 2018F

0%

10%

20%

30%

40%

50%

60%

70%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2015 2016 2017 2018 2019 2020 2021 2022 2023

Subscribers Growth

0%

10%

20%

30%

40%

50%

60%

2015 2016 2017 2018 2019 2020 2021 2022 2023

Net Gross

10 April 2015

Streaming video 15

Australian SVOD market worth $700mn by 2023

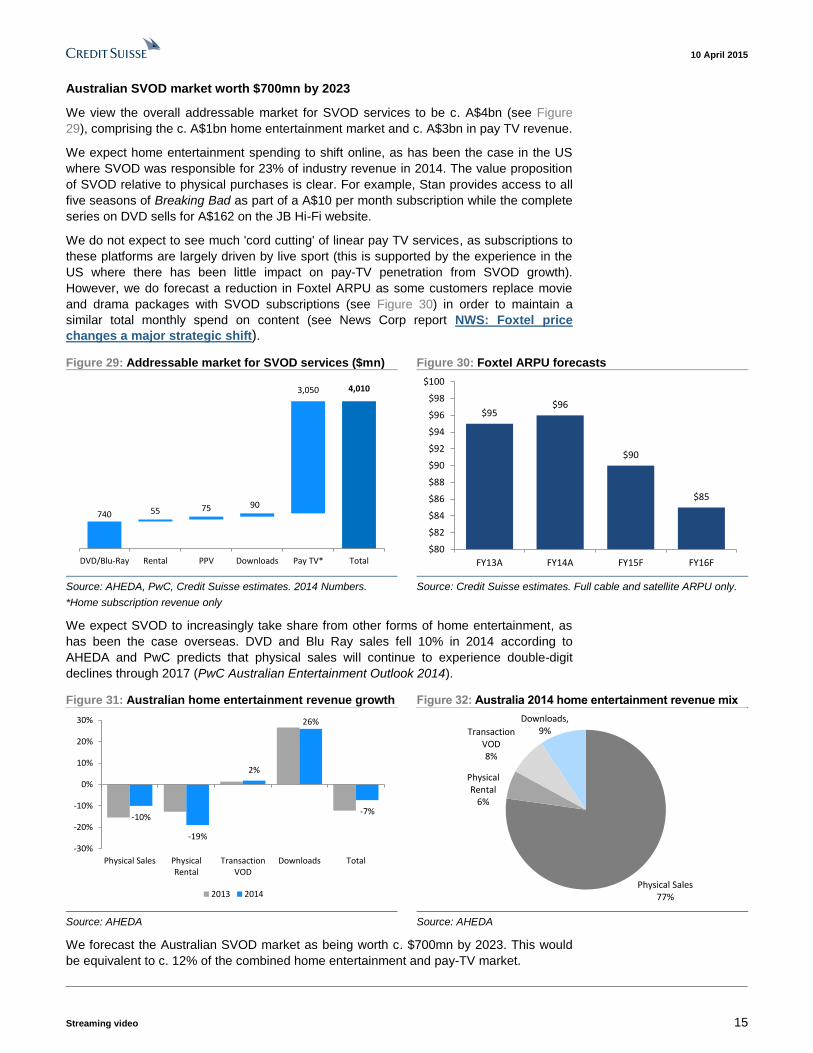

We view the overall addressable market for SVOD services to be c. A$4bn (see Figure

29), comprising the c. A$1bn home entertainment market and c. A$3bn in pay TV revenue.

We expect home entertainment spending to shift online, as has been the case in the US

where SVOD was responsible for 23% of industry revenue in 2014. The value proposition

of SVOD relative to physical purchases is clear. For example, Stan provides access to all

five seasons of Breaking Bad as part of a A$10 per month subscription while the complete

series on DVD sells for A$162 on the JB Hi-Fi website.

We do not expect to see much 'cord cutting' of linear pay TV services, as subscriptions to

these platforms are largely driven by live sport (this is supported by the experience in the

US where there has been little impact on pay-TV penetration from SVOD growth).

However, we do forecast a reduction in Foxtel ARPU as some customers replace movie

and drama packages with SVOD subscriptions (see Figure 30) in order to maintain a

similar total monthly spend on content (see News Corp report NWS: Foxtel price

changes a major strategic shift).

Figure 29: Addressable market for SVOD services ($mn) Figure 30: Foxtel ARPU forecasts

Source: AHEDA, PwC, Credit Suisse estimates. 2014 Numbers.

*Home subscription revenue only

Source: Credit Suisse estimates. Full cable and satellite ARPU only.

We expect SVOD to increasingly take share from other forms of home entertainment, as

has been the case overseas. DVD and Blu Ray sales fell 10% in 2014 according to

AHEDA and PwC predicts that physical sales will continue to experience double-digit

declines through 2017 (PwC Australian Entertainment Outlook 2014).

Figure 31: Australian home entertainment revenue growth Figure 32: Australia 2014 home entertainment revenue mix

Source: AHEDA Source: AHEDA

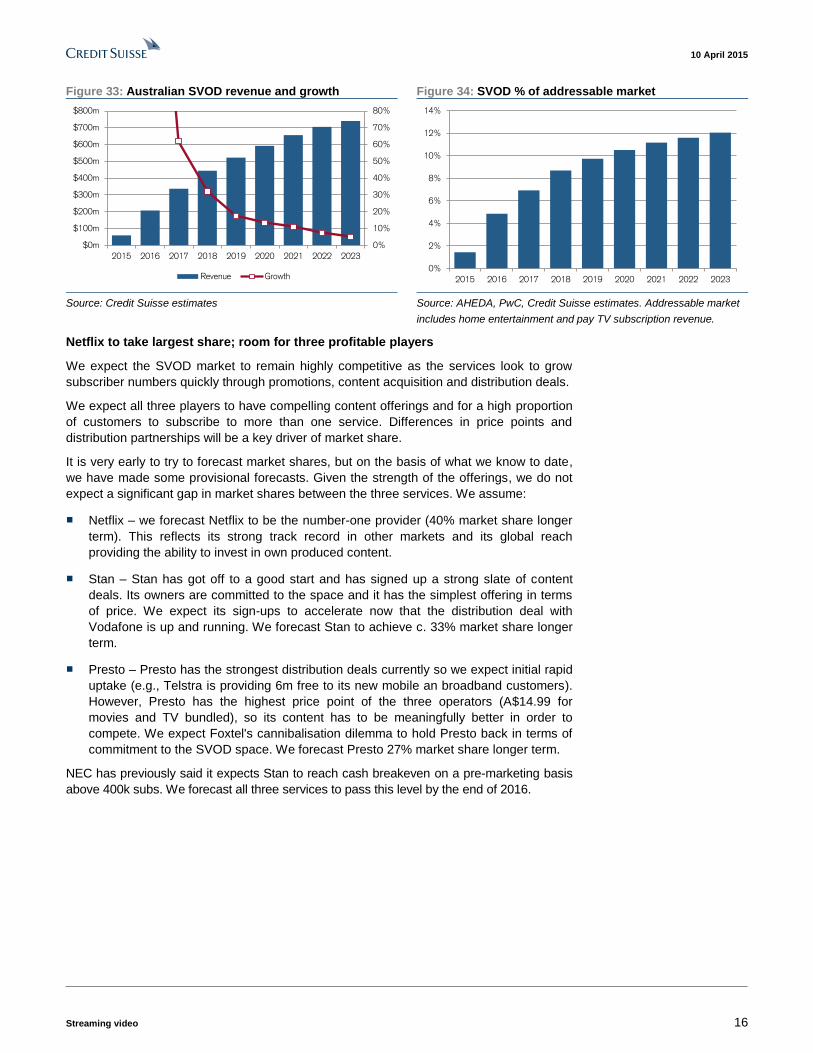

We forecast the Australian SVOD market as being worth c. $700mn by 2023. This would

be equivalent to c. 12% of the combined home entertainment and pay-TV market.

740

4,010

55 75 90

3,050

DVD/Blu-Ray Rental PPV Downloads Pay TV* Total

$95$96

$90

$85

$80

$82

$84

$86

$88

$90

$92

$94

$96

$98

$100

FY13A FY14A FY15F FY16F

-10%

-19%

2%

26%

-7%

-30%

-20%

-10%

0%

10%

20%

30%

Physical Sales PhysicalRental

TransactionVOD

Downloads Total

2013 2014Physical Sales

77%

Physical Rental

6%

Transaction VOD8%

Downloads, 9%

10 April 2015

Streaming video 16

Figure 33: Australian SVOD revenue and growth Figure 34: SVOD % of addressable market

Source: Credit Suisse estimates Source: AHEDA, PwC, Credit Suisse estimates. Addressable market

includes home entertainment and pay TV subscription revenue.

Netflix to take largest share; room for three profitable players

We expect the SVOD market to remain highly competitive as the services look to grow

subscriber numbers quickly through promotions, content acquisition and distribution deals.

We expect all three players to have compelling content offerings and for a high proportion

of customers to subscribe to more than one service. Differences in price points and

distribution partnerships will be a key driver of market share.

It is very early to try to forecast market shares, but on the basis of what we know to date,

we have made some provisional forecasts. Given the strength of the offerings, we do not

expect a significant gap in market shares between the three services. We assume:

■ Netflix – we forecast Netflix to be the number-one provider (40% market share longer

term). This reflects its strong track record in other markets and its global reach

providing the ability to invest in own produced content.

■ Stan – Stan has got off to a good start and has signed up a strong slate of content

deals. Its owners are committed to the space and it has the simplest offering in terms

of price. We expect its sign-ups to accelerate now that the distribution deal with

Vodafone is up and running. We forecast Stan to achieve c. 33% market share longer

term.

■ Presto – Presto has the strongest distribution deals currently so we expect initial rapid

uptake (e.g., Telstra is providing 6m free to its new mobile an broadband customers).

However, Presto has the highest price point of the three operators (A$14.99 for

movies and TV bundled), so its content has to be meaningfully better in order to

compete. We expect Foxtel's cannibalisation dilemma to hold Presto back in terms of

commitment to the SVOD space. We forecast Presto 27% market share longer term.

NEC has previously said it expects Stan to reach cash breakeven on a pre-marketing basis

above 400k subs. We forecast all three services to pass this level by the end of 2016.

0%

10%

20%

30%

40%

50%

60%

70%

80%

$0m

$100m

$200m

$300m

$400m

$500m

$600m

$700m

$800m

2015 2016 2017 2018 2019 2020 2021 2022 2023

Revenue Growth0%

2%

4%

6%

8%

10%

12%

14%

2015 2016 2017 2018 2019 2020 2021 2022 2023

10 April 2015

Streaming video 17

Figure 35: SVOD subscribers by service Figure 36: Subscriber market share by service

Source: Credit Suisse estimates Source: Credit Suisse estimates

0

500

1,000

1,500

2,000

2,500

2015 2016 2017 2018 2019 2020 2021 2022 2023

Netflix Stan Presto

20%

25%

30%

35%

40%

45%

2015 2016 2017 2018 2019 2020 2021 2022 2023

Stan Presto Netflix

10 April 2015

Streaming video 18

Stan forecasts – breakeven in year 3

Stan revenue and market share forecasts

Stan has started strongly with the company saying it was on track for 100k sign ups only

six weeks from launch. We expect increased awareness and distribution deals to drive

ongoing uptake.

We assume Stan is able to take about a 33% share of subscribers in the medium to long

term. On this basis, we forecast Stan to achieve 500k subscribers by the end of 2015 and

750k by the end of 2016. We forecast Stan to grow to just over 2mn subscribers by 2023.

Figure 37: Australian market subscriber forecasts Figure 38: Stan net adds and subscriber growth

Source: Credit Suisse estimates Source: Credit Suisse estimates

Stan breakeven by year 3

We forecast Stan to reach cash breakeven on a pre-marketing basis by the end of its

second year. We expect overall profitability (including marketing costs) to follow in year 3.

While NEC has previously said that it believes it expects breakeven before marketing

costs at around 400-450k subscribers.

We assume a net cash investment of A$74mn to break even (slightly above NEC estimate

at its 2014 investor day of A$50mn–$65mn to break even, which was made before the

announcement of Fairfax as a JV partner). This compares to the A$100mn that NEC and

FXJ says that it has committed to the JV (including non-cash marketing inventory).

Longer term we forecast EBITDA margins to grow to 28% (by 2023). This is in line with

Netflix in the US, which reported EBITDA margins of 28% in 4Q14 and our US team

forecasts this to expand to 36% by 2018.

Figure 39: Netflix US costs per sub per month Figure 40: Netflix US quarterly EBITDA and margin

Source: Company data. Domestic streaming only. Source: Company data. Domestic streaming only.

0%

10%

20%

30%

40%

50%

60%

70%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2015 2016 2017 2018 2019 2020 2021 2022 2023

Stan Presto Netflix

Gross Penetration Net Penetration

0%

10%

20%

30%

40%

50%

60%

0

100

200

300

400

500

600

2015 2016 2017 2018 2019 2020 2021 2022 2023

Net Adds Sub Growth

$5.20

$5.40

$5.60

$5.80

$6.00

$6.20

$6.40

$6.60

$6.80

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

1Q12

2Q12

3Q12

4Q12

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

3Q14

4Q14

Domestic Subs Cost per Sub

0%

5%

10%

15%

20%

25%

30%

0

50

100

150

200

250

300

1Q12

2Q12

3Q12

4Q12

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

3Q14

4Q14

EBITDA ($m) Margin

10 April 2015

Streaming video 19

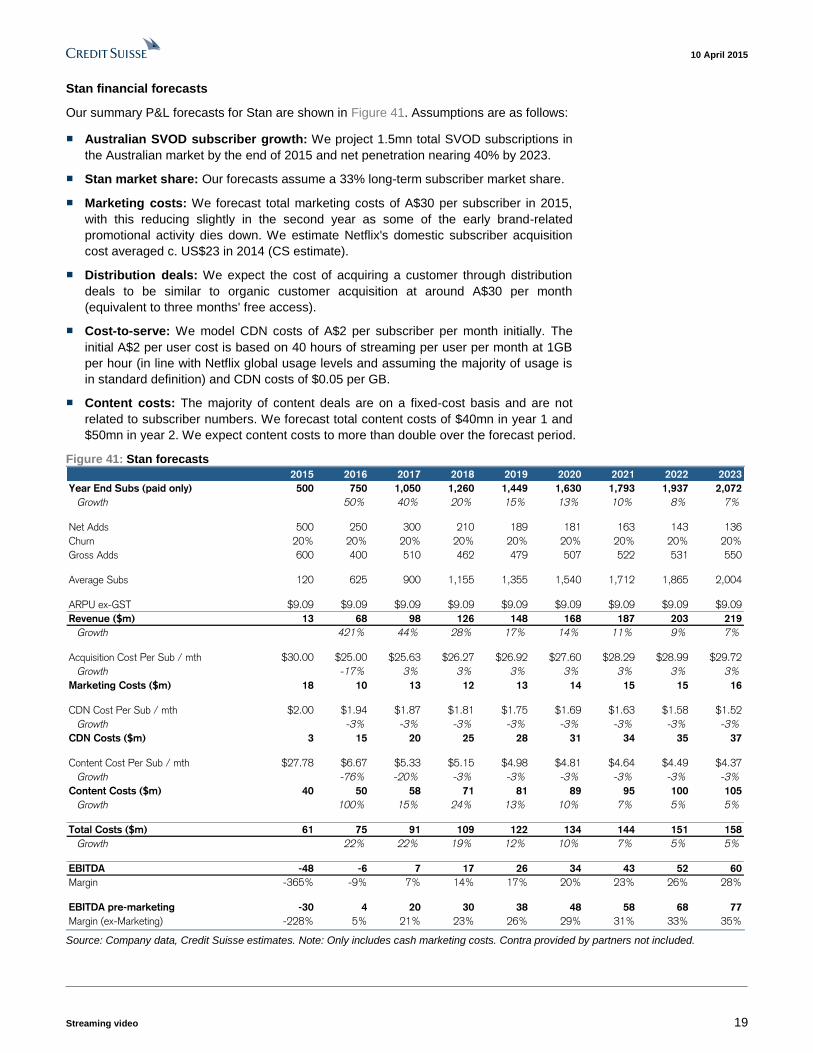

Stan financial forecasts

Our summary P&L forecasts for Stan are shown in Figure 41. Assumptions are as follows:

■ Australian SVOD subscriber growth: We project 1.5mn total SVOD subscriptions in

the Australian market by the end of 2015 and net penetration nearing 40% by 2023.

■ Stan market share: Our forecasts assume a 33% long-term subscriber market share.

■ Marketing costs: We forecast total marketing costs of A$30 per subscriber in 2015,

with this reducing slightly in the second year as some of the early brand-related

promotional activity dies down. We estimate Netflix's domestic subscriber acquisition

cost averaged c. US$23 in 2014 (CS estimate).

■ Distribution deals: We expect the cost of acquiring a customer through distribution

deals to be similar to organic customer acquisition at around A$30 per month

(equivalent to three months' free access).

■ Cost-to-serve: We model CDN costs of A$2 per subscriber per month initially. The

initial A$2 per user cost is based on 40 hours of streaming per user per month at 1GB

per hour (in line with Netflix global usage levels and assuming the majority of usage is

in standard definition) and CDN costs of $0.05 per GB.

■ Content costs: The majority of content deals are on a fixed-cost basis and are not

related to subscriber numbers. We forecast total content costs of $40mn in year 1 and

$50mn in year 2. We expect content costs to more than double over the forecast period.

Figure 41: Stan forecasts

Source: Company data, Credit Suisse estimates. Note: Only includes cash marketing costs. Contra provided by partners not included.

2015 2016 2017 2018 2019 2020 2021 2022 2023

Year End Subs (paid only) 500 750 1,050 1,260 1,449 1,630 1,793 1,937 2,072

Growth 50% 40% 20% 15% 13% 10% 8% 7%

Net Adds 500 250 300 210 189 181 163 143 136

Churn 20% 20% 20% 20% 20% 20% 20% 20% 20%

Gross Adds 600 400 510 462 479 507 522 531 550

Average Subs 120 625 900 1,155 1,355 1,540 1,712 1,865 2,004

ARPU ex-GST $9.09 $9.09 $9.09 $9.09 $9.09 $9.09 $9.09 $9.09 $9.09

Revenue ($m) 13 68 98 126 148 168 187 203 219

Growth 421% 44% 28% 17% 14% 11% 9% 7%

Acquisition Cost Per Sub / mth $30.00 $25.00 $25.63 $26.27 $26.92 $27.60 $28.29 $28.99 $29.72

Growth -17% 3% 3% 3% 3% 3% 3% 3%

Marketing Costs ($m) 18 10 13 12 13 14 15 15 16

CDN Cost Per Sub / mth $2.00 $1.94 $1.87 $1.81 $1.75 $1.69 $1.63 $1.58 $1.52

Growth -3% -3% -3% -3% -3% -3% -3% -3%

CDN Costs ($m) 3 15 20 25 28 31 34 35 37

Content Cost Per Sub / mth $27.78 $6.67 $5.33 $5.15 $4.98 $4.81 $4.64 $4.49 $4.37

Growth -76% -20% -3% -3% -3% -3% -3% -3%

Content Costs ($m) 40 50 58 71 81 89 95 100 105

Growth 100% 15% 24% 13% 10% 7% 5% 5%

Total Costs ($m) 61 75 91 109 122 134 144 151 158

Growth 22% 22% 19% 12% 10% 7% 5% 5%

EBITDA -48 -6 7 17 26 34 43 52 60

Margin -365% -9% 7% 14% 17% 20% 23% 26% 28%

EBITDA pre-marketing -30 4 20 30 38 48 58 68 77

Margin (ex-Marketing) -228% 5% 21% 23% 26% 29% 31% 33% 35%

10 April 2015

Streaming video 20

We expect costs per subscriber to decline over time as the subscriber base grows,

ultimately falling below A$6 per sub ex-marketing by 2023.

Figure 42: Stan costs per sub per month (pre marketing) Figure 43: Stan revenue and EBITDA margin

Source: Company data. Domestic streaming only. Source: Company data. Domestic streaming only.

Base case valuation of A$312mn

Based on the assumptions outlined in the previous section, we value Stan on a DCF basis

at A$312mn (for 100%). This equates to a value of A$190 per subscriber based on the

2020F subscriber base of 1.63mn.

We note that Netflix currently has a market capitalisation of US$26bn or US$520 per sub.

Figure 44: Stan DCF

Source: Company data, Credit Suisse estimates

The economics of a streaming service are highly dependent on the size of the subscriber

base given the largely fixed nature of content costs.

NEC has previously indicated that Stan will reach breakeven pre-marketing costs at

around 400-450k subscribers and we estimate that a customer base of c. 750k is

necessary to reach cash breakeven post-marketing. Given the start-up costs involved,

Stan likely needs a customer base of 800k–900k to be NPV positive.

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

0

500

1,000

1,500

2,000

2,500

2015 2016 2017 2018 2019 2020 2021 2022 2023

Subs Cost per Sub

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

$0m

$50m

$100m

$150m

$200m

$250m

2015 2016 2017 2018 2019 2020 2021 2022 2023

Revenue Margin

DCF 2015 2016 2017 2018 2019 2020 2021 2022 2023

EBITDA -48 -6 10 20 29 37 46 56 62

D&A -5 5 5 5 5 5 5 5 5

EBIT -53 -1 15 25 34 42 51 61 67

Tax 0 0 -5 -8 -10 -13 -15 -18 -20

Capex -15 -5 -5 -5 -5 -5 -5 -5 -5

FCF -63 -11 1 8 14 19 26 33 37

Present Value -60 -9 1 6 9 12 14 16 16

Valuation 332

WACC 10%

TGR 5%

10 April 2015

Streaming video 21

Figure 45: Stan EBITDA margin at various subscriber

base levels (2020F)

Figure 46: Stan EV at various 2020F subscriber base

levels

Source: Company data, Credit Suisse estimates Source: Company data. Domestic streaming only.

SVOD valuation summary – valuation upside muted

We expect SVOD penetration to grow rapidly and do see room for three profitable players.

However, we expect the low price point and fragmented market share to mean that profits

for the individual players will be capped at relatively low levels.

Given the early stage nature of the segment, we do not include any value for SVOD in our

NEC/FXJ or TLS/NWS forecasts at the current time.

Current trading multiples for Australian TV broadcasters and Netflix are shown below.

Figure 47: Relevant trading multiples

Source: Company data, IBES, Credit Suisse estimates. *Covered by Credit Suisse Emerging Companies

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

300 400 500 750 1,000 1,500 2,000 2,500 3,000

Margin (pre-marketing) Margin (post-marketing) -$200m

-$100m

$0m

$100m

$200m

$300m

$400m

$500m

$600m

$700m

$800m

300 400 500 750 1,000 1,500 2,000 2,500 3,000

Share Mkt Cap P/E EV/EBITDA

June Y/E Price A$mn Rating TP FY15F FY16F FY17F FY15F FY16F FY17F

Australian Television

Nine Entertainment $2.15 2,022 OUTPERFORM $2.46 12.7x 10.7x 10.1x 8.1x 7.2x 7.0x

Prime Media* $0.88 322 OUTPERFORM $1.05 9.6x 9.1x 8.4x 6.5x 6.4x 6.3x

Seven West Media* $1.41 1,409 NEUTRAL $1.50 8.3x 8.0x 8.1x 6.6x 6.5x 6.6x

Southern Cross Media* $1.11 813 UNDERPERFORM $0.90 12.1x 10.9x 10.3x 8.2x 7.9x 7.6x

Ten Network Holdings* $0.20 526 NEUTRAL $0.22 NM NM NM NM NM 14.8x

SVOD

Netflix, Inc. $441.35 34,731 NEUTRAL $417.00 104.6x 83.3x 47.0x 46.7x 37.4x 20.4x

Credit Suisse Coverage

10 April 2015

Streaming video 22

Appendix – Impact of SVOD on linear TV

In this section, we briefly consider the impact of SVOD uptake on linear TV viewing and

advertising. We look at the key trends from the US and the UK, where SVOD penetration

is already at relatively high levels.

US and UK ad spend still growing despite audience declines

In the US, the 18-49 audience has declined in each of the past eight years across the Big

4 broadcast networks in the US (ABC, CBS, FOX and NBC), although the rate of decline

was substantially less in the 2013-14 ratings season after the previous year was impacted

by particularly poor ratings at FOX.

Overall, 18-49 audiences have declined at a 4.6% CAGR over the past five years across

the Big 4 networks. Despite the audience decline, broadcast TV advertising saw a 3.5%

CAGR over the same period.

Likewise, UK TV ad spend has grown 5% in each of the past two years despite viewing

declines of 4%–5% per person as higher CPMs have offset audience declines.

Figure 48: US Big 4 broadcast audience (18-49) vs FTA ad

spend

Figure 49: UK TV viewing vs TV ad spend

Source: Nielsen, MagnaGlobal Source: BARB, ZenithOptimedia. Note: Average weekly time spent

viewing TV per person. Includes FTA and pay TV.

SVOD doesn't necessarily destroy live viewing

While live TV viewing in the US fell slightly in 2014, we note that due to increases in time

shifted viewing and digital video, overall video consumption grew 2%. Additionally, Nielsen

data shows that the top quintile of streamers also watch more live TV than both non-

streamers and the overall population.

Figure 50: 2014 US viewing growth Figure 51: Consumption of video content per month

Source: Nielsen. Note: All People 18+ Source: Nielsen

-15%

-10%

-5%

0%

5%

10%

15%

18-49 Audience FTA Ad Spend

-6%

-4%

-2%

0%

2%

4%

6%

2011 2012 2013 2014

Weekly Time Spent TV ad spend

-3%

10%

63%

2%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

Live TV Time Shifted Digital Total

23.80.0 2.8

251.0223.1 233.7

0

50

100

150

200

250

300

Top Quintile Non Streamers All

Streaming TV

10 April 2015

Streaming video 23

Interestingly, evidence is also inconclusive that the availability of content on demand

negatively impacts live viewing. In the case of some programs, greater accessibility leads

to greater overall popularity.

Figure 52: 18-49 ratings pre-and-post SVOD availability

Source: Nielsen. Note: Blue line is 18-49 Nielsen ratings, purple line is total audience across all platforms

Pay-TV 'cord cutting' not widespread in US

Traditional pay-TV penetration in the US peaked in 2010 at 88% of households, according

to Digital TV Research, with a 5% CAGR in IPTV services offset by flat satellite

subscriptions and a slight decline in overall cable services. However, 'cord-cutting' does

not appear to be widespread with penetration still at 86% in 2014 per Digital TV Research

and penetration forecast to remain at c85% through the end of the decade.

Figure 53: US linear pay TV households (mn) Figure 54: US linear pay TV penetration

Source: Digital TV Research Source: Digital TV Research, IHS.

2010 2013 2014 2020

IPTV 7.3 12.4 13.9 18.2

Satellite 36.2 37.1 37.0 38.0

Digital Cable 49.8 54.9 57.3 60.4

Analog Cable 18.4 7.6 3.7 0.0

0

20

40

60

80

100

120

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2013 2014 2020

10 April 2015

Streaming video 24

Companies Mentioned (Price as of 09-Apr-2015)

21st Century Fox Inc. (FOXA.OQ, $34.36) Amazon com Inc. (AMZN.OQ, $383.54) Apple Inc (AAPL.OQ, $126.56) British Sky Broadcasting (SKYB.L, 1045.0p) CBS Corporation (CBS.N, $61.2) Comcast Corporation Inc. (CMCSA.OQ, $59.59) Deutsche Telekom (DTEGn.F, €17.37) DirecTV (DTV.OQ, $87.36) Fairfax Media (FXJ.AX, A$0.985) Google, Inc. (GOOGL.OQ, $548.02) Hutch Telcom (HTA.AX, A$0.084) JB Hi-Fi (JBH.AX, A$19.0) Liberty Global (LBTYA.OQ, $52.02) Microsoft Corporation (MSFT.OQ, $41.48) Netflix, Inc. (NFLX.OQ, $439.5) News Corporation (NWS.AX, A$20.62) Nine Entertainment (NEC.AX, A$2.15) Orange (ORAN.PA, €15.5) Prime Media Group (PRT.AX, A$0.88) * Quickflix (QFX.AX, A$0.001) Seven West Media Ltd (SWM.AX, A$1.41) * Singapore Telecom (STEL.SI, S$4.37) Sony (6758.T, ¥3,620) Southern Cross Media Group (SXL.AX, A$1.11) * Telstra Corporation (TLS.AX, A$6.27) Ten Network Holdings (TEN.AX, A$0.2) * The Walt Disney Company (DIS.N, $106.77) Viacom Inc. (VIAB.OQ, $69.32) Vodafone Group (VOD.L, 225.7p) iiNet (IIN.AX, A$8.89) * * CSEC Coverage

Disclosure Appendix

Important Global Disclosures

Lucas Goode and Fraser McLeish, each certify, with respect to the companies or securities that the individual analyzes, that (1) the views expressed in this report accurately reflect his or her personal views about all of the subject companies and securities and (2) no part of his or her compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this report.

The analyst(s) responsible for preparing this research report received Compensation that is based upon various factors including Credit Suisse's total revenues, a portion of which are generated by Credit Suisse's investment banking activities

As of December 10, 2012 Analysts’ stock rating are defined as follows:

Outperform (O) : The stock’s total return is expected to outperform the relevant benchmark*over the next 12 months.

Neutral (N) : The stock’s total return is expected to be in line with the relevant benchmark* over the next 12 months.

Underperform (U) : The stock’s total return is expected to underperform the relevant benchmark* over the next 12 months.

*Relevant benchmark by region: As of 10th December 2012, Japanese ratings are based on a stock’s total return relative to the analyst's coverage uni verse which consists of all companies covered by the analyst within the relevant sector, with Outperforms representing the most att ractive, Neutrals the less attractive, and Underperforms the least attractive investment opportunities. As of 2nd October 2012, U.S. and Canadian as well as European ra tings are based on a stock’s total return relative to the analyst's coverage universe which consists of all companies covered by the analyst within the relevant sector, with Outperforms representing the most attractive, Neutrals the less attractive, and Underperforms the least attractive investment opportunities. For Latin Ame rican and non-Japan Asia stocks, ratings are based on a stock’s total return relative to the average total return of the relevant country or regional benchmark; prior to 2nd October 2012 U.S. and Canadian ratings were based on (1) a stock’s absolute total return potential to its current share price and (2) the relative attractiveness of a stock’s total return potential within an analyst’s coverage universe. For Australian and New Zealand stocks, 12 -month rolling yield is incorporated in the absolute total return calculation and a 15% and a 7.5% threshold replace the 10-15% level in the Outperform and Underperform stock rating definitions, respectively. The 15% and 7.5% thresholds replace the +10-15% and -10-15% levels in the Neutral stock rating definition, respectively. Pr ior to 10th December 2012, Japanese ratings were based on a stock’s total return relative to the average total return of the relevant country or regional benchmark.

Restricted (R) : In certain circumstances, Credit Suisse policy and/or applicable law and regulations preclude certain types of communications, including an investment recommendation, during the course of Credit Suisse's engagement in an investment banking transaction and in certain other circumstances.

Volatility Indicator [V] : A stock is defined as volatile if the stock price has moved up or down by 20% or more in a month in at least 8 of the past 24 months or the analyst expects significant volatility going forward.

Analysts’ sector weightings are distinct from analysts’ stock ratings and are based on the analyst’s expectations for the fundamentals and/or valuation of the sector* relative to the group’s historic fundamentals and/or valuation:

Overweight : The analyst’s expectation for the sector’s fundamentals and/or valuation is favorable over the next 12 months.

10 April 2015

Streaming video 25

Market Weight : The analyst’s expectation for the sector’s fundamentals and/or valuation is neutral over the next 12 months.

Underweight : The analyst’s expectation for the sector’s fundamentals and/or valuation is cautious over the next 12 months.

*An analyst’s coverage sector consists of all companies covered by the analyst within the relevant sector. An analyst may cover multiple sectors.

Credit Suisse's distribution of stock ratings (and banking clients) is:

Global Ratings Distribution

Rating Versus universe (%) Of which banking clients (%)

Outperform/Buy* 44% (53% banking clients)

Neutral/Hold* 38% (51% banking clients)

Underperform/Sell* 16% (43% banking clients)

Restricted 3%

*For purposes of the NYSE and NASD ratings distribution disclosure requirements, our stock ratings of Outperform, Neutral, and Underperform most closely correspond to Buy, Hold, and Sell, respectively; however, the meanings are not the same, as our stock ratings are determined on a relative basis. (Please refer to definitions above.) An investor's decision to buy or sell a security should be based on investment objectives, current holdin gs, and other individual factors.

Credit Suisse’s policy is to update research reports as it deems appropriate, based on developments with the subject company, the sector or the market that may have a material impact on the research views or opinions stated herein.

Credit Suisse's policy is only to publish investment research that is impartial, independent, clear, fair and not misleading. For more detail please refer to Credit Suisse's Policies for Managing Conflicts of Interest in connection with Investment Research: http://www.csfb.com/research-and-analytics/disclaimer/managing_conflicts_disclaimer.html

Credit Suisse does not provide any tax advice. Any statement herein regarding any US federal tax is not intended or written to be used, and cannot be used, by any taxpayer for the purposes of avoiding any penalties.

See the Companies Mentioned section for full company names

The subject company (NEC.AX, SWM.AX, NFLX.OQ) currently is, or was during the 12-month period preceding the date of distribution of this report, a client of Credit Suisse.

Credit Suisse expects to receive or intends to seek investment banking related compensation from the subject company (NEC.AX, SWM.AX, TEN.AX, NFLX.OQ) within the next 3 months.

As of the date of this report, Credit Suisse makes a market in the following subject companies (NFLX.OQ).

For other important disclosures concerning companies featured in this report, including price charts, please visit the website at https://rave.credit-suisse.com/disclosures or call +1 (877) 291-2683.

Important Regional Disclosures

Singapore recipients should contact Credit Suisse AG, Singapore Branch for any matters arising from this research report.

The analyst(s) involved in the preparation of this report have not visited the material operations of the subject company (NEC.AX, PRT.AX, SWM.AX, SXL.AX, TEN.AX, NFLX.OQ) within the past 12 months

Restrictions on certain Canadian securities are indicated by the following abbreviations: NVS--Non-Voting shares; RVS--Restricted Voting Shares; SVS--Subordinate Voting Shares.

Individuals receiving this report from a Canadian investment dealer that is not affiliated with Credit Suisse should be advised that this report may not contain regulatory disclosures the non-affiliated Canadian investment dealer would be required to make if this were its own report.

For Credit Suisse Securities (Canada), Inc.'s policies and procedures regarding the dissemination of equity research, please visit http://www.csfb.com/legal_terms/canada_research_policy.shtml.

As of the date of this report, Credit Suisse acts as a market maker or liquidity provider in the equities securities that are the subject of this report.

Principal is not guaranteed in the case of equities because equity prices are variable.

Commission is the commission rate or the amount agreed with a customer when setting up an account or at any time after that.

To the extent this is a report authored in whole or in part by a non-U.S. analyst and is made available in the U.S., the following are important disclosures regarding any non-U.S. analyst contributors: The non-U.S. research analysts listed below (if any) are not registered/qualified as research analysts with FINRA. The non-U.S. research analysts listed below may not be associated persons of CSSU and therefore may not be subject to the NASD Rule 2711 and NYSE Rule 472 restrictions on communications with a subject company, public appearances and trading securities held by a research analyst account.

Credit Suisse Equities (Australia) Limited ............................................................................................................... Lucas Goode ; Fraser McLeish

Credit Suisse Emerging Companies (Australia) Pty Limited ("CSEC") is the research report provider in relation to this report. Credit Suisse has disclosed its conflicts of interest also in this report as Credit Suisse is a material shareholder in CSEC; the distributor of this research; and has re-branded this document. Despite the foregoing, Credit Suisse is not liable or responsible for the content of this research report and provides it as distributor for informational purposes only

10 April 2015

Streaming video 26

Credit Suisse Emerging Companies (Australia) Pty Limited ("CSEC") is an incorporated joint venture entered into between Credit Suisse and First NZ Capital. Pursuant to this arrangement, Credit Suisse makes available to its clients certain research produced by CSEC. CSEC is not an affiliate or related body corporate of Credit Suisse. Credit Suisse is not liable or responsible for the content of such research and provides such research as its distributor for informational purposes only

CSEAL Analysts involved in the preparation of this report may be co-located with Credit Suisse Emerging Companies (CSEC) analysts.

For Credit Suisse disclosure information on other companies mentioned in this report, please visit the website at https://rave.credit-suisse.com/disclosures or call +1 (877) 291-2683.

10 April 2015

Streaming video 27