strategy utica 052808 - x-terra resources wellington... · energy strategy – the ... gastem inc....

TRANSCRIPT

Please see disclaimers on the last two pages of this report.

Domestic Energy

Energy Strategy – The Utica Shale Gas Play, Part II Kim Page, (416) 847-3400; [email protected] Dave Hammond, (416) 847-3406; [email protected]

May 28, 2008

S&P Energy Index vs. TSX Index

0

500

1000

1500

2000

2500

3000

3500

4000

4500

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 Feb-080

2000

4000

6000

8000

10000

12000

14000

16000

S&P Energy Index as % TSX Index

0%

5%

10%

15%

20%

25%

30%

35%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 Feb-08 Change in S&P Energy and TSX Indexes based on 12-month moving averages

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 Feb-08 Philadelphia Oil & Gas Services Index

0

50

100

150

200

250

300

350

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 Feb-08

Initiating Coverage on Three Juniors in the Heart of the Quebec Utica Play

• Improving completion technologies warrant a “fresh” look at the Utica

Barnett-like attributes of the Utica brings torrent of attention to Quebec amid improving frac technology, rendering shale plays economic.

• Resource potential is massive… even for Forest Oil and Talisman Estimated recoverable resource potential of +10 Bcf per section translates into ~ 25 Tcf over the entire Utica fairway, which covers ~1.5 million acres.

• Increased commitment from FST & TLM underscores potential While still in the early stages of proving commercially viable, investors are gaining confidence in the resource potential based on Majors’ CapX.

• We are initiating coverage on three junior players positioned in the… … most prospective acreage in the St. Lawrence Lowlands; Gastem Inc (GMR-V), Junex Inc. (JNX-V), and Questerre Energy Corp. (QEC-T).

Exhibit 1: Key Wells Drilled Along Utica Fairway Support More Testing

Source: Gastem Corporate Presentation

In any double-series graph above, the following legend applies: - - - S&P TSX S&P ENRS Source: WWCM, Bloomberg, PCQuote

Energy Strategy – The Utica Shale Gas Play

Kim Page, (416) 847-3400; [email protected] May 28, 2008 – 2 Dave Hammond, (416) 847-3406; [email protected]

Investment Thesis

Drilling Technology Warrants a Fresh Set of Glasses The evolution of drilling and completion technology is having a significant impact on the economics of tight sand and shale resource plays across North America. The resource potential of the Utica shale gas play in the St. Lawrence Lowlands of Quebec has long been known, but up until now not commercially viable. However, recent data from well testing, coring and petrophysical logs, combined with higher natural gas prices, has encouraged Utica shale players to move forward with expanded capital programs to further test and delineate the play’s potential. In particular, increased capital commitments by Forest Oil Corporation (FST-NYSE) and Talisman Energy Inc. (TLM-T) to further their understanding of the shale’s commercial potential has increased market confidence in the Utica play potential and warrants close attention.

We believe the Utica, if proven commercially viable, has the potential to be one of the largest resource plays in Canada. Other noteable shale trends in Western Canada, such as the Bakken trend in Saskatchewan and the Doig/Halfway/Montney trend in Northeast B.C. have proven highly economic using horizontal multi-stage frac completion techniques to develop these equally extensive plays.

In view of the enormous resource potential of the Utica, we are initiating coverage on what we believe to be three of the best positioned junior companies. First mover advantage has allowed these companies to retain massive acreage positions, with relatively low carrying costs, which now provides them with leverage over later entrants into the play, including the majors. The junior companies we are initiating coverage on are: Gastem Inc. (GMR-T) with a $4.25 target and Speculative Buy rating, Junex Inc. (JNX-T) with a $9.50 target and Speculative Buy rating, and Questerre Energy Corporation (QEC-T) with a $8.75 target and Speculative Buy rating.

Utica Shale Play Potential

So How Big is Big? The Utica shale trend has a very large aerial extent, with the most prospective portion of the play covering an area that spans over 5000 square kilometers. Several junior oil and gas companies have amassed large exploration permits within this prospective fairway over the past several years. Their conviction in the resource potential and determination to test the commercial viability of the play is likely to come to a head in the very near-term. Drilling programs planned this summer by both FST and TLM on their respective acreages with partners (details to follow) will focus on confirming commercial quantities of gas flow and reserves primarily by drilling horizontal wells completed with multi-stage fracs.

Initial estimates of the resource potential of the Quebec Utica shale play alone vary widely, however, based on most recent information could be ~25 Tcf of recoverable resource. This compares favorably with current proved reserves for all of Canada of 58 Tcf as estimated by the National Energy Board as at year-end 2007.

Some Areas More Prospective Than Others The most prospective portion of the Quebec Utica play lies within a corridor that parallels the St. Lawrence River, and covers an area of ~ 1.5 million acres. This area

Energy Strategy – The Utica Shale Gas Play

Kim Page, (416) 847-3400; [email protected] May 28, 2008 – 3 Dave Hammond, (416) 847-3406; [email protected]

runs from Southeast of Montreal right up through to Quebec City and overlies a relatively undisturbed (un-faulted) area with favorable topography given relatively flat farming land in the St. Lawrence Lowlands.

This area is most perspective in terms of the potential for commercial shale production for many reasons. Namely, ideal depth of burial is between 800 meters and 2,500 meters, pressure and rock porosity are ideal, seam thickness is over 100 meters (up to as high as 250-300 meters), there appears to be sufficient remaining total organic carbon of +1%, and thermal maturity of the shale measured in terms of Vitrinite Reflectance (Ro) is 1% to 3%.

Key area lies between Logan’s Line and the Appalachain Thrust Belt. The heart of the Utica play also appears to sit between Logan’s Line, a major thrust fault that demarks the separation between a relatively “un-disturbed” section of the basin to the Northwest and the Appalachain Thrust Belt Region to the Southeast (as seen in Exhibit 2). The thrust belt region is an area of high tectonic stresses that could render drilling operation difficult, and affect the impact of frac completions.

Exhibit 2: Questerre/Talisman Lands Ideally Situated in Heart of Play Along with the Forest/Gastem/Junex Acreages

Source: Questerre Energy Corporation Corporate Presentation, WWCM

Complex Geology Likely to Lead to Productive Variability The area of deposition of several shale sequences in this ancient St. Lawrence valley is huge, covering tens of thousands of square kilometers. Geologically, the Utica

Energy Strategy – The Utica Shale Gas Play

Kim Page, (416) 847-3400; [email protected] May 28, 2008 – 4 Dave Hammond, (416) 847-3406; [email protected]

shale was deposited in a deep water environment in the Appalachain Basin approximately 450 million years ago off the eastern flanks of the Canadian Shield within the St. Lawrence valley, a massive pre-depositional rift valley. The shale sequences of particular interest span the Upper to Middle Ordovician period, and include from shallower to deep the Lorraine, the Utica, and the Trenton-Black River formations (see Exhibit 3).

Exhibit 3: Stratigraphic Cross Section of Ordovician Shales & Well Log Identifying IP Rates of 4.6 mmcf/d

Source: Karlen, G. 2007. Resource Play Potential Utica Shales – Quebec Lowlands, EnCana Corp Poster Session – 2007 CSPG-CSEG Joint Convention, Calgary

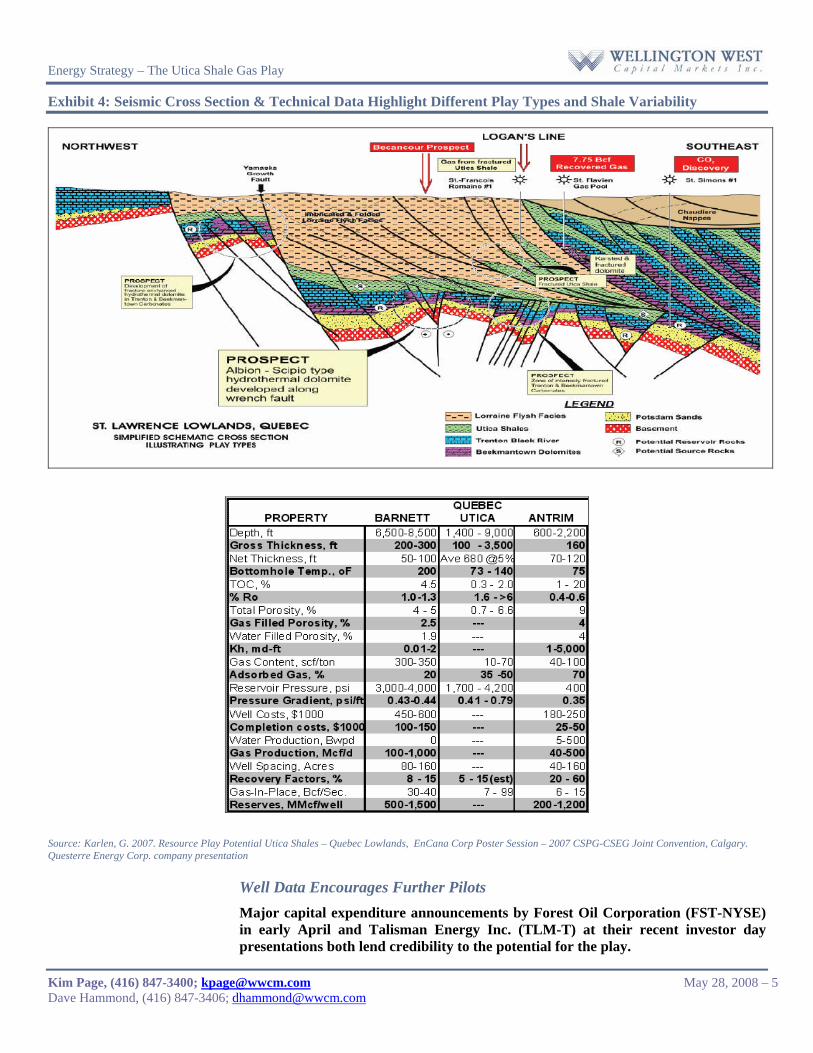

The geology of the Utica shale in the St. Lawrence Lowlands area is complex. We believe the rock character (formation thickness and orientation, mineralogy including clay, quartz and dolomite/carbonate content, original total organic content, thermal maturity, pressure gradient, etc.) vary widely across the region, and rock mechanics associated with the Appalachian Thrust Belt will likely have an impact on the results of each well. There may very well be two or three play styles in the area, including a primary fracture play within the Thrust Belt area. Exhibit 4 identifies the structural complexity of the area as evident in the seismic cross section running Northwest/Southeast across the St. Lawrence River, and demonstrates the properties of the Utica shale in comparison to the Barnett shale and Antrim shale, both which are commercially productive and undergoing extensive development.

Energy Strategy – The Utica Shale Gas Play

Kim Page, (416) 847-3400; [email protected] May 28, 2008 – 5 Dave Hammond, (416) 847-3406; [email protected]

Exhibit 4: Seismic Cross Section & Technical Data Highlight Different Play Types and Shale Variability

Source: Karlen, G. 2007. Resource Play Potential Utica Shales – Quebec Lowlands, EnCana Corp Poster Session – 2007 CSPG-CSEG Joint Convention, Calgary. Questerre Energy Corp. company presentation

Well Data Encourages Further Pilots Major capital expenditure announcements by Forest Oil Corporation (FST-NYSE) in early April and Talisman Energy Inc. (TLM-T) at their recent investor day presentations both lend credibility to the potential for the play.

Energy Strategy – The Utica Shale Gas Play

Kim Page, (416) 847-3400; [email protected] May 28, 2008 – 6 Dave Hammond, (416) 847-3406; [email protected]

The Majors Come to the Table Forest Oil’s plans to drill three horizontal wells this summer with completion operations on all three wells expected in late September/early October, as highlighted by J.C. Ridens, Chief Operating Officer, at our recent Utica Shale Gas Players conference. This comes on the back of two vertical wells drilled in 2007, which tested at rates of up to 1 mmcf/d. Forest oil believes there is upwards of 4 Tcf of potential recoverable resources on their lands alone. These resource estimates of 93 Bcf of original gas in place (OGIP) per square mile are based on similar resource recovery expectations of the Utica with the Barnett shale play in Texas. An estimated recovery rate of 15% would yield gross recoverable reserves of ~2.2 Bcf per well, assuming six horizontal development wells per section.

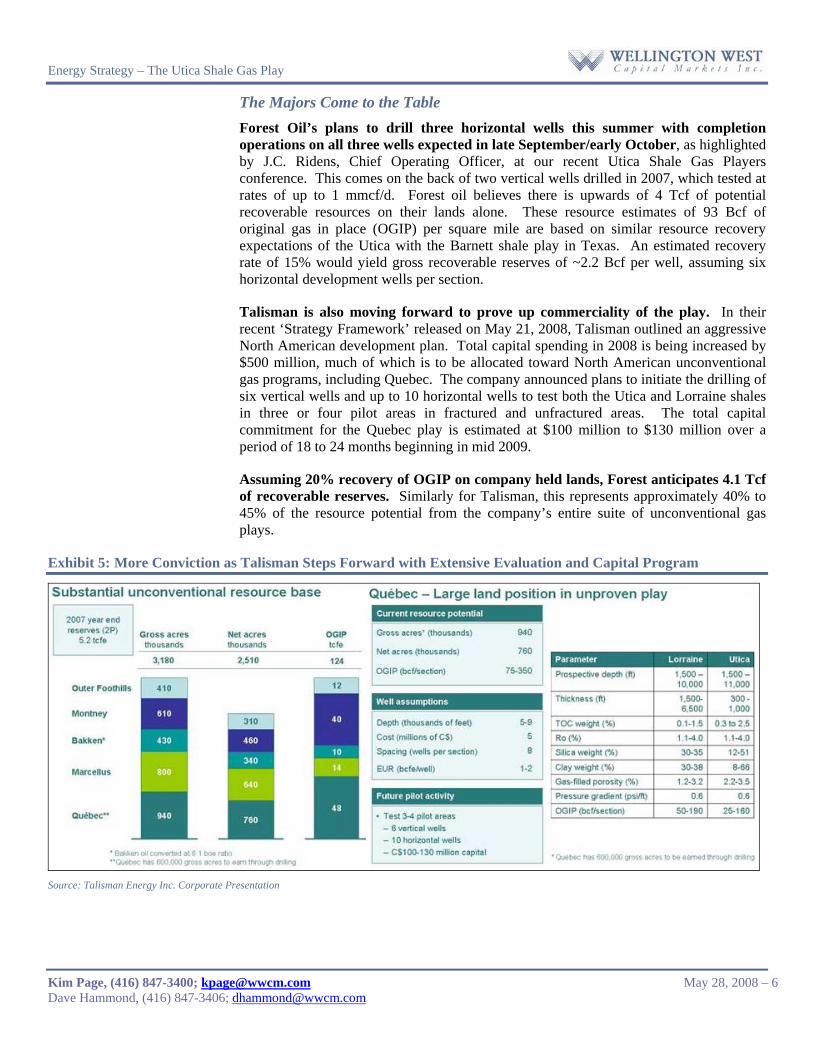

Talisman is also moving forward to prove up commerciality of the play. In their recent ‘Strategy Framework’ released on May 21, 2008, Talisman outlined an aggressive North American development plan. Total capital spending in 2008 is being increased by $500 million, much of which is to be allocated toward North American unconventional gas programs, including Quebec. The company announced plans to initiate the drilling of six vertical wells and up to 10 horizontal wells to test both the Utica and Lorraine shales in three or four pilot areas in fractured and unfractured areas. The total capital commitment for the Quebec play is estimated at $100 million to $130 million over a period of 18 to 24 months beginning in mid 2009.

Assuming 20% recovery of OGIP on company held lands, Forest anticipates 4.1 Tcf of recoverable reserves. Similarly for Talisman, this represents approximately 40% to 45% of the resource potential from the company’s entire suite of unconventional gas plays.

Exhibit 5: More Conviction as Talisman Steps Forward with Extensive Evaluation and Capital Program

Source: Talisman Energy Inc. Corporate Presentation

Energy Strategy – The Utica Shale Gas Play

Kim Page, (416) 847-3400; [email protected] May 28, 2008 – 7 Dave Hammond, (416) 847-3406; [email protected]

The recoverable resource potential from the Utica is massive for both Forest and Talisman, let alone for Gastem, Junex and Questerre. We anticipate that substantial capital programs by juniors on the play, will unfold.

Mounting Well Data Encourages Flurry of Activity Numerous wells have been drilled both historically and recently, which collectively have provided for an increasing data base of information helping to confirm OGIP estimates, rock parameters, flow rates, and ultimate recoverable resource estimates. Key wells completed to date include:

1. Becancour #8 - Arguably, one of the more significant wells to date was the #8 well drilled by Junex on the Becancour property in mid 2006. While drilling, Forest Oil agreed to cover the cost of cutting core, and based on analysis of 34 meters or core, log data, and well test information elected to exercise an option to enter into a US$8 million pilot project, including frac-ing the Becancour #8 well and drilling a horizontal development well, currently planned for this summer.

2. Gentilly #1 - A second significant well was the Gentilly #1 well drilled by Questerre Energy and Talisman Energy also in 2006, just a few kilometres away from the Becancour property. This well tested at IP rates of over 4.5 mmcf/d over a three day period then quickly declined to the ~300 mcf/d to 600 mcf/d range.

3. Villeroy - An older well drilled in 1973 at Villeroy just Northeast of the Gentilly well also tested at meaningful rates of between 0.2 to 1.2 mmcf/d over a 25 day period.

4. St. Francois-du-Lac #1 - And finally, a significant development was a frac well 50 miles to the Southwest of the Gentilly well drilled by Gastem in the summer of 2007, which also tested at rates of up to 1.0 mmcf/d.

Exhibit 6 outlines the land positions held and location of early wells that spawned the recent build-up of interest and capital commitments towards forwarding the play.

Energy Strategy – The Utica Shale Gas Play

Kim Page, (416) 847-3400; [email protected] May 28, 2008 – 8 Dave Hammond, (416) 847-3406; [email protected]

Exhibit 6: Recent Exponential Ramp-up is Just the Beginning

Source: Molopo Australia Limited Company Presentation & WWCM

Energy Strategy – The Utica Shale Gas Play

Kim Page, (416) 847-3400; [email protected] May 28, 2008 – 9 Dave Hammond, (416) 847-3406; [email protected]

Key Wells Planned for Near-term Key drilling operations planned this summer (see Exhibit 7) should help to quantify commerciality of play. Full scale development programs will follow presuming the initial horizontal well tests prove successful and commercial flow rates are evident.

Exhibit 7: Major Capital Expenditure Programs Will Help Quantify The Play

Summary of Major Capital Investment Plans - 2008/2009 Property Operator / Capital # of Wells Specific Plans

Partners ($mm)

Yamaska Forest Oil / ~$20 to $30 6 to 10 Complete earn-in with 2 horizontal wells

Gastem/Questerre/ Epsilon Drill total 3 horizontal wells summer 2008

Full scale development 2010

Gentilly Talisman / $100 to $131 15-20 Complete earn-in with 3 vertical wellsQuesterre Establish pilots in 3 to 4 areas

Drill up to 10 horizontal wellsFull scale development 2010

Becancour / Forest Oil / ~ $10 - $15 3-5 Forest to Frac Brecancour well this summerContrecoeur Junex Forest earn-in CapX is $8mm at

Becancour and $5mm at Contrecoeur

Others: Gastem to drill 6 well program on New York State Utica project Junex to drill 4 vertical wells with $6.5mm cpax incl. geophysical activity in SLL

Source: Questerre Energy Corporation Corporate Presentation

Energy Strategy – The Utica Shale Gas Play

Kim Page, (416) 847-3400; [email protected] May 28, 2008 – 10 Dave Hammond, (416) 847-3406; [email protected]

Infrastructure In-Place Help Support Economic Case Recent developments such as rising gas prices, improved technology, maturing shale gas expertise, and the presence of nearby infrastructure, all combine to make the Quebec Utica play compelling from an economic perspective, assuming flow rates meet our Utica “type well” profile. The St-Lawrence Lowlands is located near extensive infrastructure where an estimated 200 to 400 mmcf/d (seasonal variation) capacity is available on the TransCanada Pipe Line (see Exhibit 8). This capacity would suffice at least early on, as potential Utica production begins to ramp up. Another strong point for the Utica Shale - New York Border pricing typically averages US$1 above NYMEX Henry Hub, making the pricing environment attractive for producers.

Exhibit 8: In-place Infrastructure Shaves Years Off Development Time-line

Source: Questerre Energy Corporation Corporate Presentation

Under the assumption of Barnett shale-like production profiles, we model very attractive economic returns, evident with a calculated IRR of ~45% based on field gas prices of $9/mcf. Initial well drilling and completion costs are expected to drop from the $4 million to $5 million range (likely to vary widely based on well depths and completion techniques used) to the $3 million to $4 million range as services infrastructure is developed. In our “type well” scenario, we have assumed that average all-in costs (including tie-in, facilities, infrastructure, and pipeline), equate to $4 million per well.

Our ‘model well’ suggests strong IRR potential. Exhibit 9 summarizes the expected economic returns of our theoretical Utica “type well” based on the production profile shown assuming a base natural gas realized price of C$9/mcf, and on an un-leveraged basis. We assume an initial production rate of 2.5 mmcf/d, first year decline rate of 60%, and life of well recovery of 2.2 Bcf/well which is premised on 93 Bcf/section (as estimated by Forest Oil on their lands) and a more conservative 15% recovery rate.

Energy Strategy – The Utica Shale Gas Play

Kim Page, (416) 847-3400; [email protected] May 28, 2008 – 11 Dave Hammond, (416) 847-3406; [email protected]

Exhibit 9: Economic Assessment of “Type Well” Suggests Strong IRR Potential

Type Well ConversionWell Parameters: boe @ 6:1Well Cost - Drill, Complete & Tie-in/Facilities ($mm) $4.0Initial Production Rate (mmcf/d) 2.5 417Reserves (Bcf) 2.18 0.363Reserve Life Index (years) - Life of Project Average 7.7 7.7Average Success Rate 100%Financial Parameters:Wellhead Gas Price (CDN $/mcf) $9.00 $54.00Royalty Rate (%) 12.5%Operating & Transpo Expense ($/mcf) $1.50 $9.00G&A Expense ($/mcf) $0.75 $4.50Leverage ($/mcf) $0.00 $0.00Interest Rate (%) 6%Tax Rate (%) 36%PV Discount Rate 10%Result:F&D Costs ($/mcf) - Life of Project $1.84 $11.03Recycle Ratio 3.1xNet Present Value per mcf $1.84Internal Rate of Return (IRR) 45.7%

Decline Profile

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21

Years

Utic

a "T

ype

Wel

l" A

vera

ge

Ann

ual P

rodu

ctio

n (m

mcf

/d)

Source: Forest Oil Corporation April 2008 Investors Presentation, WWCM

NB: Economic assumptions include maximum production royalty rate of 12.5%

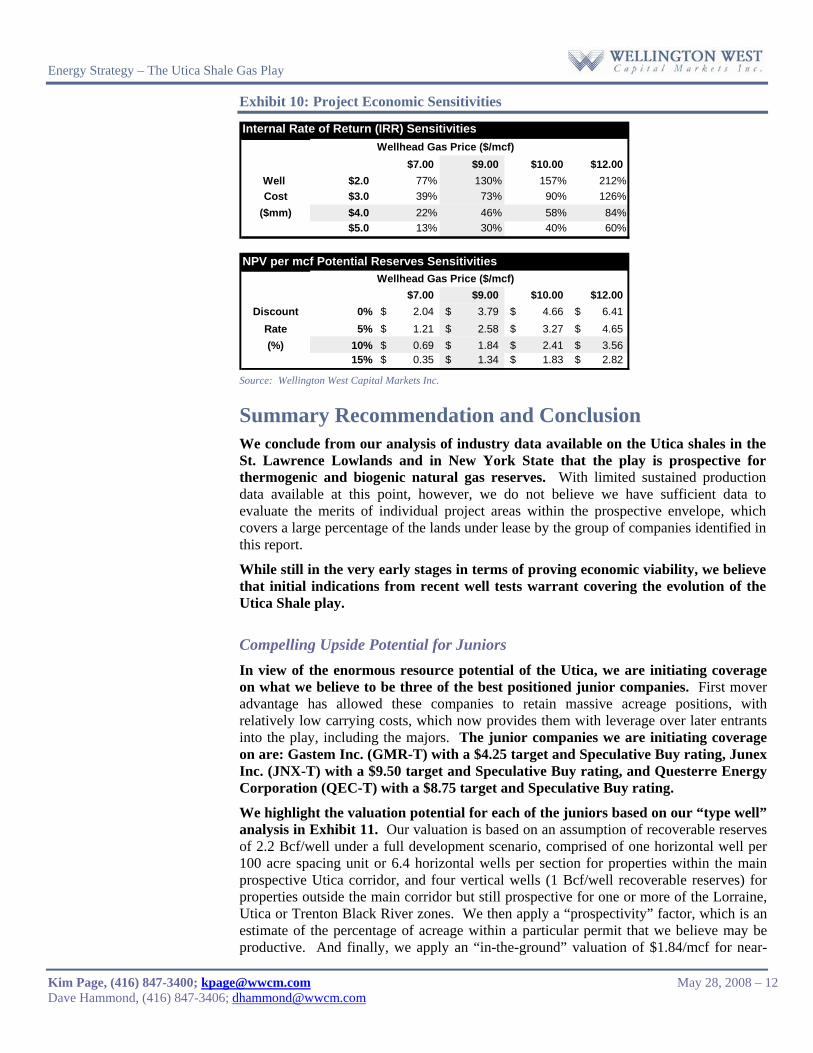

Our economic model drives a Net Present Value for reserves in the ground under our full development scenario of $1.84/mcf. In Exhibit 10 we provide a sensitivity analysis of calculated IRR and NPV per share based on varying gas prices, well costs and discount rates. We note that under current Eastern Canadian gas prices of over $10/mcf, economic returns under our “type well” scenario exceed 60% IRR and would compete with the Montney shale gas play currently under extensive development in Western Canada.

Energy Strategy – The Utica Shale Gas Play

Kim Page, (416) 847-3400; [email protected] May 28, 2008 – 12 Dave Hammond, (416) 847-3406; [email protected]

Exhibit 10: Project Economic Sensitivities

Internal Rate of Return (IRR) SensitivitiesWellhead Gas Price ($/mcf)

$0.46 $7.00 $9.00 $10.00 $12.00Well $2.0 77% 130% 157% 212%Cost $3.0 39% 73% 90% 126%

($mm) $4.0 22% 46% 58% 84%$5.0 13% 30% 40% 60%

NPV per mcf Potential Reserves SensitivitiesWellhead Gas Price ($/mcf)

$1.84 $7.00 $9.00 $10.00 $12.00Discount 0% 2.04$ 3.79$ 4.66$ 6.41$

Rate 5% 1.21$ 2.58$ 3.27$ 4.65$ (%) 10% 0.69$ 1.84$ 2.41$ 3.56$

15% 0.35$ 1.34$ 1.83$ 2.82$ Source: Wellington West Capital Markets Inc.

Summary Recommendation and Conclusion We conclude from our analysis of industry data available on the Utica shales in the St. Lawrence Lowlands and in New York State that the play is prospective for thermogenic and biogenic natural gas reserves. With limited sustained production data available at this point, however, we do not believe we have sufficient data to evaluate the merits of individual project areas within the prospective envelope, which covers a large percentage of the lands under lease by the group of companies identified in this report.

While still in the very early stages in terms of proving economic viability, we believe that initial indications from recent well tests warrant covering the evolution of the Utica Shale play.

Compelling Upside Potential for Juniors In view of the enormous resource potential of the Utica, we are initiating coverage on what we believe to be three of the best positioned junior companies. First mover advantage has allowed these companies to retain massive acreage positions, with relatively low carrying costs, which now provides them with leverage over later entrants into the play, including the majors. The junior companies we are initiating coverage on are: Gastem Inc. (GMR-T) with a $4.25 target and Speculative Buy rating, Junex Inc. (JNX-T) with a $9.50 target and Speculative Buy rating, and Questerre Energy Corporation (QEC-T) with a $8.75 target and Speculative Buy rating.

We highlight the valuation potential for each of the juniors based on our “type well” analysis in Exhibit 11. Our valuation is based on an assumption of recoverable reserves of 2.2 Bcf/well under a full development scenario, comprised of one horizontal well per 100 acre spacing unit or 6.4 horizontal wells per section for properties within the main prospective Utica corridor, and four vertical wells (1 Bcf/well recoverable reserves) for properties outside the main corridor but still prospective for one or more of the Lorraine, Utica or Trenton Black River zones. We then apply a “prospectivity” factor, which is an estimate of the percentage of acreage within a particular permit that we believe may be productive. And finally, we apply an “in-the-ground” valuation of $1.84/mcf for near-

Energy Strategy – The Utica Shale Gas Play

Kim Page, (416) 847-3400; [email protected] May 28, 2008 – 13 Dave Hammond, (416) 847-3406; [email protected]

term horizontal projects and $1.00/mcf for those projects not likely to be developed for several years, all risked at 50% to account for geological variability within the prospective acreage.

Even at this 50% risk factor, the implied valuations in the per share range of $8.51 to $19.33 for these assets alone suggest significant upside for shareholders should this play prove commercial. We note these valuation estimates are based on current share counts on an undiluted basis, and expect these companies will require significant additional capital to move forward with full development of these assets. We estimate capital requirements to develop core assets should be in the $350 million to +$1 billion range, with ultimate capital requirements dependent on sustained production levels and pace of development, which is certain to vary from project to project. We have therefore established our target price based on a further 50% reduction in this valuation to account for future dilution from required capital raises.

Energy Strategy – The Utica Shale Gas Play

Kim Page, (416) 847-3400; [email protected] May 28, 2008 – 14 Dave Hammond, (416) 847-3406; [email protected]

Exhibit 11: Core Shale Interests & Potential Resource Valuations – Risked at 50%

Unrisked Implied Valuation #Company/ Major Property Partner (s) Acreage Average Acreage Primary % Area Acreage Recoverable Potential Per Share

Symbol (gross) WI (%) (net) Zone (net) Resource Valuation # UndilutedPotential ($mm) Risked @ 50%

(Bcf) ($/shr)Gastem

GMR.V Yamaska Forest/Questerre 112000 15% 16800 Utica 70% 11760 256 471St. Jean Questerre 198000 50% 99000 Other 25% 24750 155 155St. Jean N. Questerre 54000 20% 10800 Other 25% 2700 59 59Joly Intragaz 35000 35% 12250 Utica 50% 6125 134 134New York Utica Energy 29000 65% 18850 Marcellus/ 70% 13195 82 152Total SLL Acreage: 157700 Utica 58530 686 970 $8.51* GMR owns WI in a total of over 1.1m acres gross in SLL & Gaspe* Amber Bank, W. Virginia - working interest in 24 producing wells

QuesterreQEC.T Yamaska Forest/GMR 112000 20% 22400 Utica 70% 15680 342 629

Gentilly Talisman 719788 24.4% 175572 Utica 70% 122900 2679 4927GORR 4.25% 30591 Utica 70% 21414 467 858

St. Jean N & S Gastem 253428 56% 143090 Other 25% 35773 224 224Total SLL Acreage: 371653 195767 3711 6637 $17.27* QEC also owns 50% WI in +20,000 acres in Antler, Sask. & EnCana farm-in lands in Greater Sierra, B.C.We have included $0.25/share in our target as rough estimate of value of Western Canadian assets

JunexJNX.V Becancour Forest 143141 15% 21471 Utica 35% 7515 164 301

Contrecoeur Forest 55000 40% 22000 Utica 70% 15400 336 617Nicolet Private 54363 50% 27182 Utica 70% 19027 415 763Richelieu 138606 100% 138606 Other 20% 27721 173 173St. Simon 57126 90% 51413 Other 20% 10283 64 64Lyster 108360 100% 108360 Other 10% 10836 68 68North Shore Properties 803211 100% 803211 Other 10% 80321 31 31Total SLL Acreage: 1172243 171103 1251 2018 $19.33* JNX owns a 1.5% ORRI in 1.8 mm acres held by Molopo Australia Limited and approx. 3mm gross acres in Gaspe region* JNX also owns 316,567 net acres of exploration lands in the Haldimand/Galt/Baie des Chaleurs region of the Gaspe Peninsula

# Valuation based on our "type well" model and assumptions which value potential recoverable resources at $1.84/mcf in-the-ground for near-term projects and $1.00/mcf for longer-term development areas * Other assets not included in valuation

ProspectivityUtica Shale Players - St. Lawrence Lowlands (SLL) Land Holdings

Source: Corporate Presentations, WWCM

Energy Strategy – The Utica Shale Gas Play

Kim Page, (416) 847-3400; [email protected] May 28, 2008 – 15 Dave Hammond, (416) 847-3406; [email protected]

Investment Risks

Our fundamental outlook for oil and gas producers and energy services companies remain favorable, however, several industry operating, political and currency risks could impact specific company’s ability to achieve our forecasts, including:

• Commodity price fluctuations could have a material impact on a company’s re-investment capacity, and hence ultimate growth potential. High netback gas reserves and low cost structure, along with a healthy balance sheet helps to mitigate commodity price exposure, coupled periodically with price protection through hedging strategies.

• Adverse well or reservoir performance in any one or a number of producing pools could result in abnormally high production decline rates impacting overall corporate volumes. Long life gas reserves, operated under prudent production practices, and more diversity in producing horizons helps mitigate exposure to high decline well/pool exposure.

• Field operational hazards such as well blowouts, explosions and fires within pipeline/gathering/facility infrastructure, mechanical equipment failures could lead to sour gas releases, spills, personal injuries and/or damage to the environment. Industry insurance policies, particularly those which include business disruption, help to mitigate financial exposure to such mishaps.

• Industry capacity constraints due to high levels of activities can result in shortages of services, products, equipment, or man power in many or all necessary components of the exploration and development drilling cycle. Increased competition leads to escalated land costs, along with other service costs during peak activity levels.

• Extraordinary hazards such as unusual swings in weather patterns, changes in regulatory operating or fiscal terms, or actions by certain groups such as industry organizations, local communities, or militant groups could impact the company’s ability to re-invest for future growth

Changing Political environments and currency exchange rate fluctuations could have a material impact on a company’s ability to operate, retain contractual rights to, and repatriate predictable cash flow from foreign assets. Concentrating on companies operating in more stable political and financial jurisdictions with favorable fiscal terms helps to mitigate some of these risks.

Energy Strategy – The Utica Shale Gas Play

Kim Page, (416) 847-3400; [email protected] May 28, 2008 – 16 Dave Hammond, (416) 847-3406; [email protected]

APPENDIX A - The Evolution of the Utica Shale Chronology of Key Events ~450mm Utica shale deposited years ago

1950’s Six of twelve wells on the St. Jean permit just 30 km southeast of Montreal were drilled in the 1950s, the most significant of which (the Eastern Canada No. 1 well), was assigned estimated potential gas reserves of two to three Bcf. In 1972, Shell drilled a deep well called the Saint-Armand No.1 just offsetting the St. Jean permit.

1973 First notable Utica gas test – the Shell St. Francois No.1 well completed at a depth of 979 meters in the Utica shale delivered gas to surface on DST test at a rate of 265 mcf/d. Initial production rate was 4.6 mmcf/d at 3,543 psi – significantly over-pressured.

2000 Questerre began acquiring land prospective for the Utica shale

2002 Junex began acquiring land prospective for the Utica shale

2004 Gastem acquires the Yamaska permits

2005 Questerre executed farm-in agreement with Talisman on Gentilly permit. Same year Questerre farmed-in on Gastem’s interests in the St. Jean blocks.

2006 Junex executed a farm-in agreement with Forest Oil on the Becancour and Contrecoeur permits.

Dec 2006 Talisman spuds the Gentilly No.1 well – TVD 2,600 meters. Questerre pays 10.5% to earn a 17.5% WI plus has a 5% GORR (Gross Over-riding Royalty).

Jan/Feb 2007 Gastem and Questerre enter LOI re: Yamaska property and AMI for any projects wherein each must offer the other a 20% WI within the SLL region.

Forest Oil farms-in on Yamaska property – must spend $10 million to earn 60% WI. Questerre holds a 7.5% GORR convertible into 20% WI. Gastem farmed into Questerre’s interests on a 50/50 basis and is also subject to a 7.5% convertible GORR payable to Questerre.

Summer 2007 Gastem drilled two pilot vertical test wells, drilled to depth of ~1,800 meters; these are the St. Francois-du-Lac No.1 well and the St. Louis de Richelieu No.1 well, both on the Yamaska permit to test Utica and Trenton Black River zones.

Dec 2007 Gastem spuds the first Joly permit well and the Joly No. 4 well - under farm-in with Intragaz, must drill two wells to earn 50% interest in Joly property and 49% interest in two gas storage facilities.

Energy Strategy – The Utica Shale Gas Play

Kim Page, (416) 847-3400; [email protected] May 28, 2008 – 17 Dave Hammond, (416) 847-3406; [email protected]

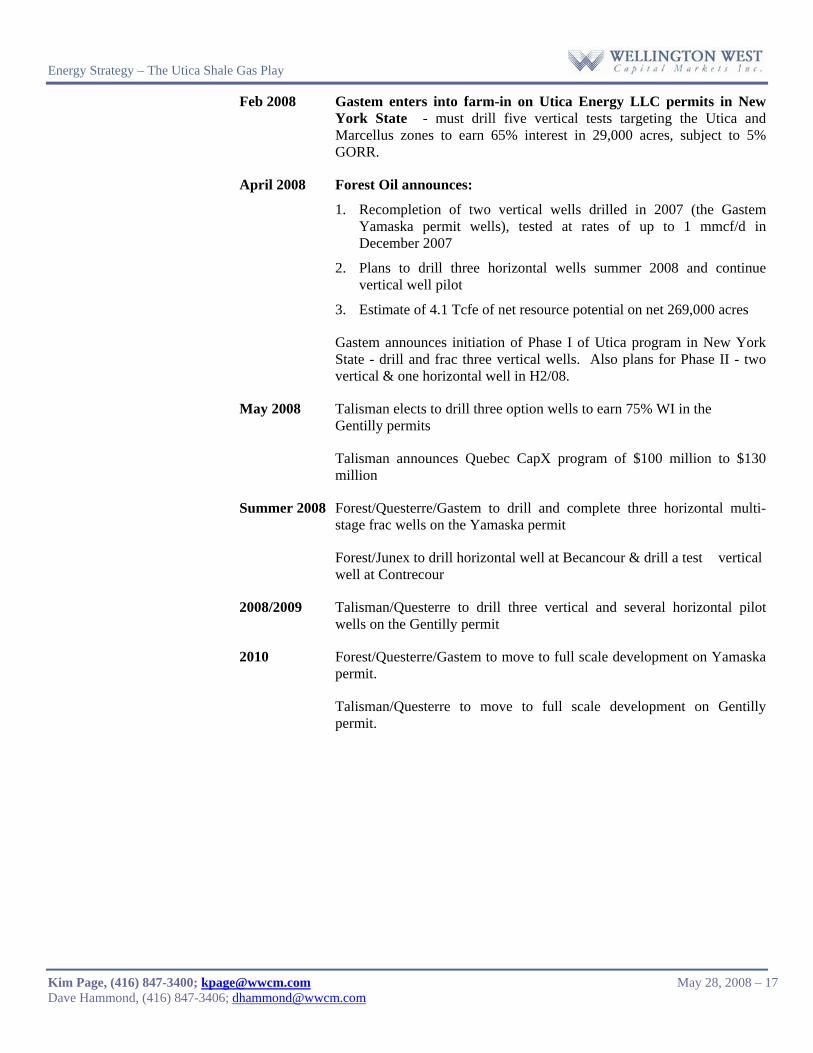

Feb 2008 Gastem enters into farm-in on Utica Energy LLC permits in New York State - must drill five vertical tests targeting the Utica and Marcellus zones to earn 65% interest in 29,000 acres, subject to 5% GORR.

April 2008 Forest Oil announces:

1. Recompletion of two vertical wells drilled in 2007 (the Gastem Yamaska permit wells), tested at rates of up to 1 mmcf/d in December 2007

2. Plans to drill three horizontal wells summer 2008 and continue vertical well pilot

3. Estimate of 4.1 Tcfe of net resource potential on net 269,000 acres

Gastem announces initiation of Phase I of Utica program in New York State - drill and frac three vertical wells. Also plans for Phase II - two vertical & one horizontal well in H2/08.

May 2008 Talisman elects to drill three option wells to earn 75% WI in the Gentilly permits

Talisman announces Quebec CapX program of $100 million to $130 million

Summer 2008 Forest/Questerre/Gastem to drill and complete three horizontal multi-stage frac wells on the Yamaska permit

Forest/Junex to drill horizontal well at Becancour & drill a test vertical well at Contrecour

2008/2009 Talisman/Questerre to drill three vertical and several horizontal pilot wells on the Gentilly permit

2010 Forest/Questerre/Gastem to move to full scale development on Yamaska permit.

Talisman/Questerre to move to full scale development on Gentilly permit.

Please see disclaimers on the last two pages of this report.

Energy

Gastem Inc. (GMR.V, $3.10) Recommendation: Speculative Buy Kim Page, (416) 847-3400; [email protected] Dave Hammond, (416) 847-3406; [email protected] May 26, 2008

All values in C$ unless otherwise noted.

Current Price $3.10 Target Price (12-Month) $4.25 Target Return 37% Changes Old New Net SLL Acreage Net Prospective Acres Potential Resource (Tcf) Estimated Value ($BN) Valuation/share (PPF*)

N/A N/A N/A N/A N/A

157,700 58,530

0.69 $0.97 $8.51

Recommendation N/A Spec Buy Target Price *Pre Project Financing

N/A $4.25

Company Profile Gastem Inc. (“Gastem”) is a Montreal, Canada based independent oil and gas exploration company, with exploration and storage rights to over one million acres of land in the St Lawrence Lowlands, Gaspe Peninsula in Quebec, and in New York State, USA. Gastem is partnered with Forest on the Yamaska permit, with potential full scale development in 2010.

In the Quebec Utica Sweet Spot: Initiating Coverage With $4.25 Target

• Key Yamaska asset located in heart of the Utica fairway Gastem holds a 15% WI in JV with Forest Oil on Yamaska propertywhere two horizontal wells are to be drilled and completed this summer.

• Gastem also moving forward on New York State Utica project Plans to drill five vertical & one horizontal well this summer should help substantiate GMR’s decision to acquire more lands in New York State.

• We estimate recoverable reserves of 686 Bcf valued at $970 million Our risked resource estimate drives an $8.51/share valuation even while being cautious on the prospectivity of the St. Jean and Joly acreage.

• Initiating coverage with a Speculative Buy rating and $4.25 target Gastem’s diversified base of assets in Quebec and operator position in New York State provide more avenues for success in the Utica play.

Financial Summary Shares O/S (M) 68.2 52-Week Trading RangeMarket Capitalization (M) $211 Average Weekly Volume 2,555,949 Net Debt - 2008E (M) -$3 Market Float (M) $195Enterprise Value (M) $208 Net BV/S - 2007 $0.06Key Properties: WI Acres (net) PartnerYamaska 15% 16,800

St.Jean 50% 99,000St.Jean N 20% 10,800

Joly 35% 12,250

New York 65% 18,850Key Management: Key Shareholders:Raymond Savoie Chairman, CEO, and Founder Officers/Directors ~8% of shrs o.s.Marc-Andre Lavoie President Michel Lemoine Secretary-TreasurerJean-Andre Guerin Head of Consulting CommitteeMurray Rodgers Executive Advisor Jon Kelafant Senior VPOrville Cole Operations/Project Manager - Yamaska

Forest to drill 3 pilot wells in July '08, test into 2009, and begin full scale development in 2010

Intragaz - GMR has option to drill 1 well by Dec '09 to earn 50% WI

$3.74-$0.40

Arrangement with QEC, wherein GMR to drill 1 well at St.Jean, and 1 at St.Jean N

GMR to drill 5 vertical wells and 1 horizontal well this year

Source: WWCM, Company report

Price Chart

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

May

-07

Jun-

07

Jul-0

7

Aug

-07

Sep-

07

Oct

-07

Nov

-07

Dec

-07

Jan-

08

Feb-

08

Mar

-08

Apr

-08

May

-08

Pric

e (C

$)

011223344556677889910101111121213131414151516161717

Mill

ions

Volu

me

Source: PC Quote

Energy Strategy – The Utica Shale Gas Play

Kim Page, (416) 847-3400; [email protected] May 28, 2008 – 19 Dave Hammond, (416) 847-3406; [email protected]

Investment Summary and Outlook Gastem Inc. (GMR-T) is an independent oil and gas exploration company based in Montreal, Quebec, with varying interests in seven permits, situated in the multi-TCF potential St. Lawrence Lowlands Basin, the Gaspe Peninsula, and in New York State. Gastem has amassed a substantial land position, prospective for the Utica shale formation, which runs through the Appalachian Basin in Quebec, down into New York State. The Utica shale has enormous potential for revoverable resource development, if planned drilling this summer confirms commerciality.

Based on our risked analysis, we estimate Gastem’s properties could have potential recoverable resources of 686 Bcf, which we value at $970M, or $8.51 per share on a pre financing basis. In view of Gastem’s substantial land holdings in the heart of the Yamaska fairway, strategic partnership with Forest Oil Corporation (FST-NYSE), and prospective Utica assets in New York State, we are initiating coverage on GMR with a $4.25 target price and Speculative Buy rating.

Investment Highlights A Long Way in a Short Period of Time Less than seven years in the making, Gastem has made major breakthroughs, commanding industry wide attention. The company was incorporated under the Canada Business Corporations Act in 2002, and listed on the TSX-Venture Exchange in January 2004. In what seemed overnight, Gastem quickly became a main-stream player following the April 1st, 2008 announcements pertaining to two Yamaska permit wells drilled by Gastem and completed by Forest in mid to late 2007. In light of the encouraging results from these Yamaska wells, Forest has elected to step-up capital commitments for the project. Plans are to drill more vertical pilot wells, in addition to two horizontal wells twinning the 2007 wells to establish commerciality of the Utica formation. With this, Gastem is getting geared up for increased exploration and development operations at Yamaska and on other properties, and to hone acquisition(s) of other Utica prospective lands within New York State.

Unconventional Utica Shale Play - Higher Hanging Fruit Now Within Reach Drilling at Yamaska in the 1970’s by Shell and SOQUIP lead to the conclusion that abundant shale gas was present. At the time however, conventional oil was the priority, and ironically gas discoveries were typically considered an inconvenience. Well aware of improving economic potential in the face of rising North American gas prices, Gastem acquired the Yamaska property in 2004, while amassing an interest in over 400,000 gross acres of land in the St. Lawrence Lowlands. Through various joint venture arrangements, Gastem now holds a 15% WI in the Yamaska property, a core piece of the Utica story in view of Forest Oil’s indication that full scale commercial development is scheduled for 2010, should this summer’s two-well horizontal program prove commercial.

Talisman has been Active in the Area for Some Time, with Early A+ Indications Talisman had also been active in the area, drilling at St.Francoise just North of Gastem’s Yamaska property in late 2006/early 2007. In fact, Talisman’s Gentilly permits surround the Yamaska property, bounding it on three sides. When Talisman noticed that Gastem was gearing-up to drill their 1st well at Yamaska, they contacted Gastem’s engineering team to caution them of potential over-pressured horizons. Even

Energy Strategy – The Utica Shale Gas Play

Kim Page, (416) 847-3400; [email protected] May 28, 2008 – 20 Dave Hammond, (416) 847-3406; [email protected]

with this knowledge, Gastem’s well produced a huge gas-kick, heralding in a great deal of enthusiasm about the potential in the area.

Huge Resource Potential Gastem holds interests in over 1.1 million gross acres in the St. Lawrence Lowlands and Gaspe Peninsula regions. Ownership in the Yamaska permit in the heart of the Utica play fairway is a key driver in our valuation. Based on our risked analysis, we estimate the company’s properties could have potential recoverable resource of over 680 Bcf, which we value at $970mm or over $8.50 per share on a pre financing basis. This does not assign any incremental value to the additional Gaspe region acreage, nor the company’s Dundee permit near the Quebec/New York border.

Exhibit 12: Valuation Summary – Yamaska Permit is Key Driver in our Valuation Model

Unrisked Implied Valuation #Company/ Major Property Partner (s) Acreage Average Acreage Primary % Area Acreage Recoverable Potential Per ShareSymbol / (gross) WI (%) (net) Zone (net) Resource Valuation # Undiluted

Price Potential ($mm) Risked @ 50%(Bcf) ($/shr)

GastemGMR.V / Yamaska Forest/QEC 112000 15% 16800 Utica 70% 11760 256 471$3.10 St. Jean Questerre 198000 50% 99000 Other 25% 24750 155 155

St. Jean N. Questerre 54000 20% 10800 Other 25% 2700 59 59Joly Intragaz 35000 35% 12250 Utica 50% 6125 134 134New York Utica Energy 29000 65% 18850 Marcellus/ 70% 13195 82 152Total SLL Acreage: 157700 Utica 58530 686 970 $8.51* GMR owns WI in a total of over 1.1m acres gross in SLL & Gaspe* Amber Bank, W. Virginia - working interest in 24 producing wells

# Valuation based on our "type well" model and assumptions which value potential recoverable resources at $1.84/mcf in-the-ground for near-term projects and $1.00/mcf for longer-term development areas * Other assets not included in valuation

ProspectivityUtica Shale Players - St. Lawrence Lowlands (SLL) Land Holdings

Source: Gastem Company Reports, WWCM

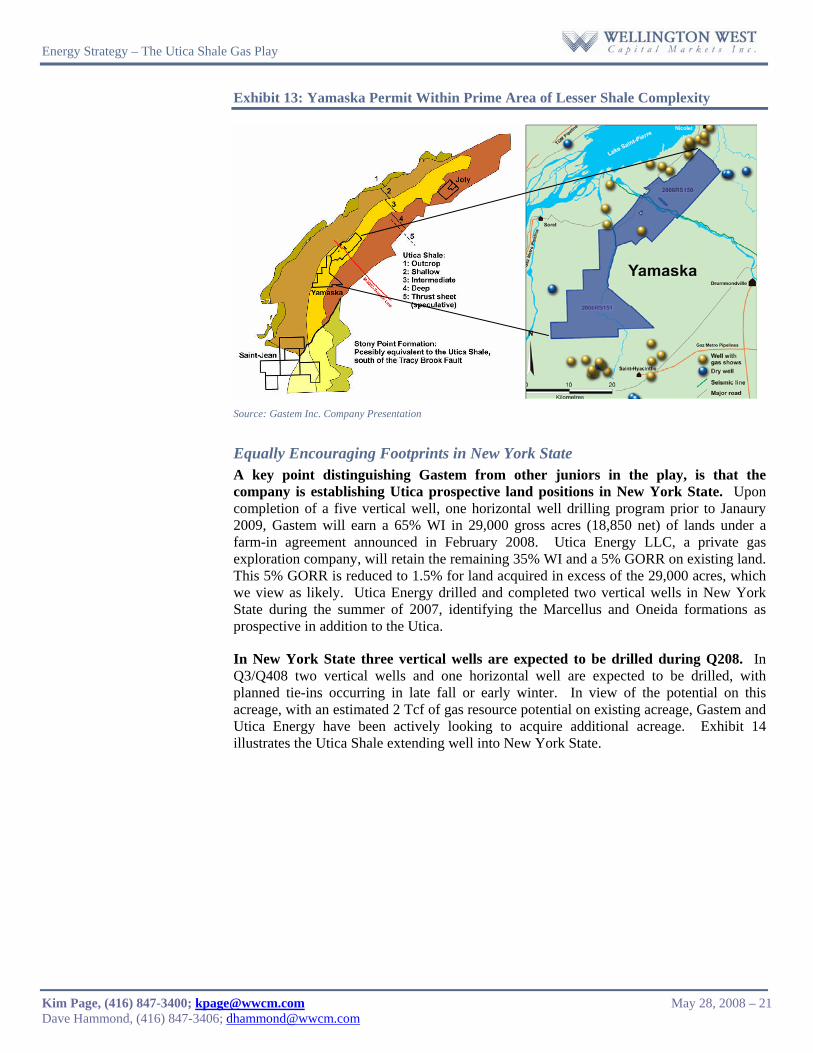

Shale Gas Project Profiles Early Indication Suggests Yamaska Permit is in Sweet-Spot of Utica Fairway Seismic data indicates a relatively flat and undisturbed series of shale horizons under the Yamaska property. In this property, Gastem holds a 15% WI in 112,000 (16,800 net) acres of land. Utica Shales range from 450 to 1,000 feet in thickness, at an average depth of ~1,400 metres on this property. The Yamaska property is almost entirely within zone 3, an area of intermediate depth most likely conducive to adequate reservoir pressure for commercial production rates, as indicated in Exhibit 13 below. As the Yamaska property sits within the main prospective Utica fairway, we assign a higher than average prospectivity measure of 70% compared with other properties given the higher predictive nature of the Shale and therefore expect a higher drilling success. Outside the main fairway, for comparison purposes, we assign a 10% to 50% prospectivity range. We note that Talisman has acquired an interest in land immediately offsetting three sides of Gastem’s Yamaska property, and we believe escalating interest by the majors provide even greater confidence in the economics of the play and this area specifically.

Energy Strategy – The Utica Shale Gas Play

Kim Page, (416) 847-3400; [email protected] May 28, 2008 – 21 Dave Hammond, (416) 847-3406; [email protected]

Exhibit 13: Yamaska Permit Within Prime Area of Lesser Shale Complexity

Source: Gastem Inc. Company Presentation

Equally Encouraging Footprints in New York State A key point distinguishing Gastem from other juniors in the play, is that the company is establishing Utica prospective land positions in New York State. Upon completion of a five vertical well, one horizontal well drilling program prior to Janaury 2009, Gastem will earn a 65% WI in 29,000 gross acres (18,850 net) of lands under a farm-in agreement announced in February 2008. Utica Energy LLC, a private gas exploration company, will retain the remaining 35% WI and a 5% GORR on existing land. This 5% GORR is reduced to 1.5% for land acquired in excess of the 29,000 acres, which we view as likely. Utica Energy drilled and completed two vertical wells in New York State during the summer of 2007, identifying the Marcellus and Oneida formations as prospective in addition to the Utica.

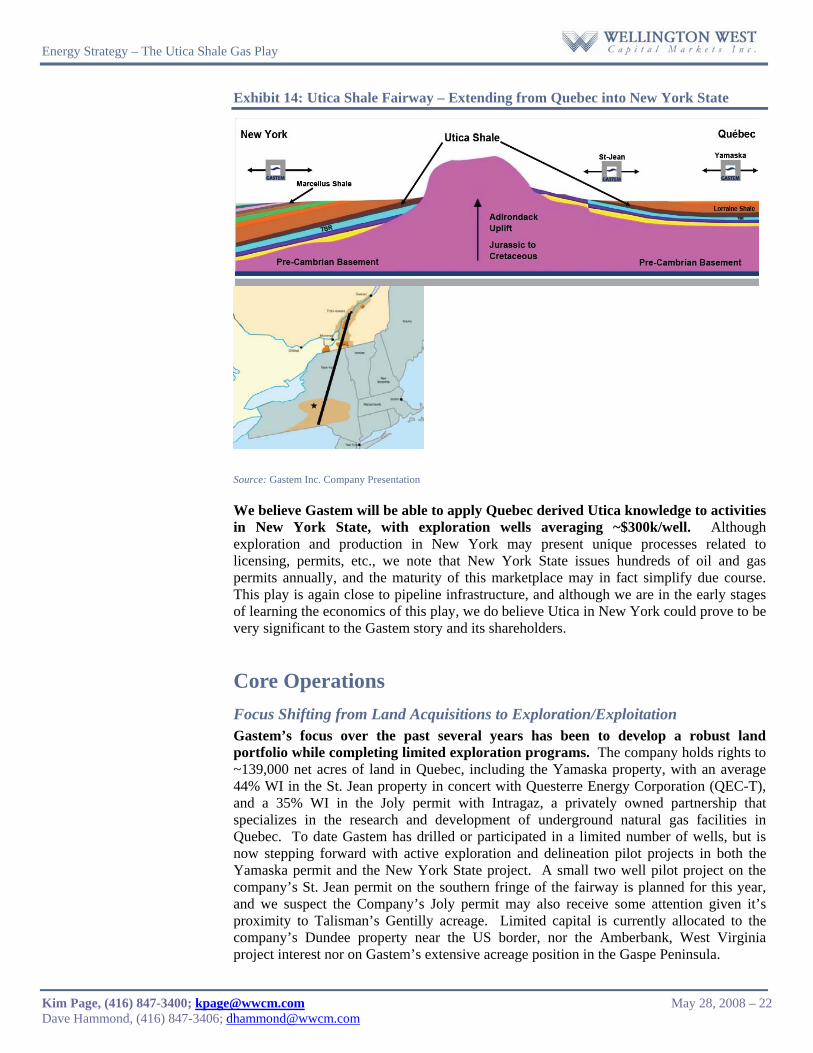

In New York State three vertical wells are expected to be drilled during Q208. In Q3/Q408 two vertical wells and one horizontal well are expected to be drilled, with planned tie-ins occurring in late fall or early winter. In view of the potential on this acreage, with an estimated 2 Tcf of gas resource potential on existing acreage, Gastem and Utica Energy have been actively looking to acquire additional acreage. Exhibit 14 illustrates the Utica Shale extending well into New York State.

Energy Strategy – The Utica Shale Gas Play

Kim Page, (416) 847-3400; [email protected] May 28, 2008 – 22 Dave Hammond, (416) 847-3406; [email protected]

Exhibit 14: Utica Shale Fairway – Extending from Quebec into New York State

Source: Gastem Inc. Company Presentation

We believe Gastem will be able to apply Quebec derived Utica knowledge to activities in New York State, with exploration wells averaging ~$300k/well. Although exploration and production in New York may present unique processes related to licensing, permits, etc., we note that New York State issues hundreds of oil and gas permits annually, and the maturity of this marketplace may in fact simplify due course. This play is again close to pipeline infrastructure, and although we are in the early stages of learning the economics of this play, we do believe Utica in New York could prove to be very significant to the Gastem story and its shareholders.

Core Operations Focus Shifting from Land Acquisitions to Exploration/Exploitation Gastem’s focus over the past several years has been to develop a robust land portfolio while completing limited exploration programs. The company holds rights to ~139,000 net acres of land in Quebec, including the Yamaska property, with an average 44% WI in the St. Jean property in concert with Questerre Energy Corporation (QEC-T), and a 35% WI in the Joly permit with Intragaz, a privately owned partnership that specializes in the research and development of underground natural gas facilities in Quebec. To date Gastem has drilled or participated in a limited number of wells, but is now stepping forward with active exploration and delineation pilot projects in both the Yamaska permit and the New York State project. A small two well pilot project on the company’s St. Jean permit on the southern fringe of the fairway is planned for this year, and we suspect the Company’s Joly permit may also receive some attention given it’s proximity to Talisman’s Gentilly acreage. Limited capital is currently allocated to the company’s Dundee property near the US border, nor the Amberbank, West Virginia project interest nor on Gastem’s extensive acreage position in the Gaspe Peninsula.

Energy Strategy – The Utica Shale Gas Play

Kim Page, (416) 847-3400; [email protected] May 28, 2008 – 23 Dave Hammond, (416) 847-3406; [email protected]

Exhibit 15: Geographically Tight Focus Area – Simplifying Operations

Source: Gastem Inc. Company Website

Forest Whips Yamaska Operations into High-Gear At Yamaska, Forest plans to drill three horizontal wells in 2008, two of which would be twins to two vertical wells drilled by Gastem on the Yamaska permit in 2007. These vertical wells were: the Saint-Francois-du-Lac No.1, which was spud on May 25th 2007 and drilled to total depth of 1,700 metres; and the St.Louis-de-Richelieu No. 1 which was spud on June 23rd, 2007 and drilled to total depth of 1,760 metres. Both were drilled on time and through the Utica Shale. Both tested non-commercial quantities of gas, but at initial rates of up to 1 mmcf/d, providing encouragement for horizontal well pilot now being undertaken by Forest.

Following encouraging results from these two wells, Forest agreed to reimburse half the cost of those wells (~$2.5 million), and exercise its option to complete the Yamaska production trials. Forest Oil has the option to earn up to 60% WI in the property by spending at least $10 million for exploration and development by the end of 2008. Completion of the two horizontal wells to be spud this summer is expected in late September/early October with long-term production testing planned thereafter. This could provide a foundation for full scale development in 2009-2010. In light of increased activity in the area generally, we anticipate droves of information regarding adjacent acreage that will assist in determining the commerciality of the Utica in the region. Gastem retains a 15% WI in the permit while partners including Questerre and Epsilon Energy Ltd. (EPS-T) hold the balance.

Joly Permit - Another Piece of the Puzzle Gastem holds 35% WI in 35,000 gross acres (12,250 net) at Joly, roughly 50 kms south of Quebec City. Gastem has the option to drill one well by Dec ’09 in order to earn a 50% WI in gas production, along with 49% of storage and 50% of exploration permits. Storage refers to a working arrangement with Intragaz, a private company that was recently acquired by Junex. We are not aware of any immediate plans for this property, but expect results from Talisman’s drilling activity this summer may bring this permit to the forefront going into next winter.

Energy Strategy – The Utica Shale Gas Play

Kim Page, (416) 847-3400; [email protected] May 28, 2008 – 24 Dave Hammond, (416) 847-3406; [email protected]

Two Wells Planned on St. Jean Permit, Nothing at Amber Bank, West Virginia Gastem holds a 50% WI in 198,000 gross acres (99,000 net) at St-Jean, and a 20% WI on another 54,000 gross acres (10,800 net) at St-Jean Nord. Average WI in both projects is 44%. Gastem has an arrangement with Questerre, wherein Gastem will drill one well on the St. Jean permit and one on the St. Jean Nord permit by end of this year in order to maintain their working interests.

In late 2006 Gastem entered into a 25% WI farm-in agreement with Epsilon Energy and participated in the drilling of 24 wells in the Amber Bank, West Virginia project. Gastem is considering additional low risk production ventures at Amber Bank, but nothing is imminent as yet.

History and Management First Mover in Quebec, Management Shows Tact Gastem’s current team has achieved meaningful results for shareholders, showing a keen sense and business tact. In discussions with Gastem, we believe they will also be working to add to their leadership team, and potentially place an Executive with Shale Gas experience. Along this vein, Mr. Murray Rodgers has recently joined the company as a Board of Director and Strategic Advisor. Gastem’s key management team is listed below.

Raymond Savoie LL.L, Chairman, CEO and founder of Gastem: Formerly Quebec Minister of Mines, Mr. Savoie has been involved with various aspects of mining exploration for the past 20 years and is currently president and director of several public and private companies. From 1985 to 1991, Mr. Savoie was Quebec's Minister of Mines and from 1991-1994, Minister of Revenue and held several other portfolios.

Marc-Andre Lavoie M.Phil, M.Sc, Senior Vice President: Mr. Lavoie is former Director at BNP Paribas in London and New York, and has 14 years of capital markets experience. Since July 2006, Mr. Lavoie is the principal of an investment fund active in commercial property and private equity in North America and Europe. Mr Lavoie a graduate of the St Francis Xavier University and holds masters degrees in Finance and Economics from London School of Economics and Cambridge University.

Jon Kelafant, M.SC., Senior Vice President, and Board Member: Mr. Kelafant is also Senior Vice President of Advanced Resources International and President of Utica Energy. He has 22 years of experience in developing oil and gas projects, notably shale projects, in the US as well as overseas.

W.Murray Rodgers, P.Geol., Executive Advisor, and Member of the Board: Ex-president and CEO of Trident Exploration, Mr. Rogers is a Professional petroleum geologist with 28 years of exploration and production experience in both Canada and Internationally.

Michel Lemoine LL.L, Secretary-Treasurer, Engineer and Lawyer: Michel is founder of Pellemon, V-P and CEO of the industrial division of SNC-Lavalin, and now specializing in arbitration. Mr. Lemoine serves on the Board of several public and private companies, and is involved as arbitrator in formal arbitration procedures.

Jean-Andre Guerin, M.A, Head of the Consulting Committee. Mr. Guérin has been consulting for Gastem since early 2007 providing assistance in the planning and execution of the exploration program, landholdings development, partnership agreements and

Energy Strategy – The Utica Shale Gas Play

Kim Page, (416) 847-3400; [email protected] May 28, 2008 – 25 Dave Hammond, (416) 847-3406; [email protected]

contract management. Mr. Guérin has over 30 years of experience in the oil and gas sector. He was Vice-president / Director Hydro-Québec Oil & Gas from 2002 to 2006 and Chairman of the Québec Energy Board from 1997 to 2002.

Orville Cole, Director of Operations and President of Gastem USA: Mr. Cole has over 20 years of extensive field and project management experience, gained most recently as the CEO of Strike Petroleum. Mr. Cole is an expert in well fracturing and completions, and has worked in a field management capacity for Halliburton in Alberta. Mr. Cole is specialised in the management of Oil & Gas drilling operations with a particular expertise in well completions.

Capital Structure Management Stake Gastem management and insiders hold approximately 8% of 57 million shares outstanding (68.2 million FD).

Exhibit 16: Share Capital Common Shares # of Shares (mm) Amount ($mm) Per Share ($)

Issued in 2004 8.9 $3 $0.34Issued in 2005 12.0 $3 $0.27Issued in 2006 18.3 $3.70 $0.20Issued for cash in 2007 8.4 $6.50 $0.77Issued flow-through shares in 2007 1.7 $1.20 $0.70April 2008 private placement 4.8 $10.16 $2.14

Current Outstanding 56.7

Common Stock OptionsWeighted A verage

Exercise PriceOptions Outstanding as at Dec 31, 2007 3.7 $0.52

WarrantsTotal Warrants Outs tanding as at Dec 31, 2007 7.8 $0.56

Total Shares Outstanding (FD) 68.2 Source: Gastem Company Reports

Valuation and Summary Recommendation First Mover Advantage, Sweet-Spot Landholder, Building USA Asset Base Gastem has amassed a substantial land position that we believe has enormous potential for near-term commercial production of natural gas. Based on our risked analysis, we estimate Gastem’s properties could have potential recoverable resource of 686 Bcf, which we value at $970M, or over $8 per share on a pre financing basis (Exhibit 12).

In view of Gastem’s substantial land holdings in the heart of the Yamaska fairway, strategic partnership with Forest Oil Corporation (FST-NYSE), and prospective Utica assets in New York State, we are initiating coverage on GMR with a $4.25 target price and Speculative Buy rating.

Energy Strategy – The Utica Shale Gas Play

Kim Page, (416) 847-3400; [email protected] May 28, 2008 – 26 Dave Hammond, (416) 847-3406; [email protected]

Our valuation is based on an assumption of recoverable reserves of 2.2 Bcf/well under a full development scenario, comprised of one horizontal well per 100 acre spacing unit or 6.4 horizontal wells per section for properties within the main prospective Utica corridor, and four vertical wells (1 Bcf/well recoverable reserves) for properties outside the main corridor but still prospective for one or more of the Lorraine, Utica or Trenton Black River zones. We then apply a “prospectivity” factor, which is an estimate of the percentage of acreage within a particular permit that we believe may be productive. And finally, we apply an “in-the-ground” valuation of $1.84/mcf for near-term horizontal projects and $1.00/mcf for those projects not likely to be developed for several years, all risked at 50% to account for geological variability within the prospective acreage.

Even at this 50% risk factor, the implied valuations suggest significant upside for shareholders should this play prove commercial. We note this valuation is based on current share counts on an undiluted basis, and expect the company will require significant additional capital to move forward with full development of these assets. We estimate capital requirements to develop core assets should be in the $350 million to +$1 billion range, with ultimate capital requirements dependent on sustained production levels and pace of development, which is certain to vary from project to project. We have therefore established our target price based on a further 50% reduction in this valuation to account for future dilution from required capital raises.

Please see disclaimers on the last two pages of this report.

Energy

Junex Inc. (JNX-V, $3.65) Recommendation: Speculative Buy Kim Page, (416) 847-3400; [email protected] Dave Hammond, (416) 847-3406; [email protected] May 26, 2008

All values in C$ unless otherwise noted.

Current Price $3.65 Target Price (12-Month) $9.50 Target Return 260% Changes Old New Net SLL Acreage (mm) Net Prospective Acres Potential Resource (Tcf) Estimated Value ($BN) Valuation/share (PPF*)

N/A N/A N/A N/A N/A

1.17 152,101

1.1 $1.9

$18.19 Recommendation N/A Spec Buy Target Price * Pre Project Financing

N/A $9.50

Company Profile Junex Inc. (“JNX”) is a Quebec based Oil and Gas exploration company with rights on over six million acres of land in the Quebec Appalachian geological basin. One million acres are located within the St-Lawrence Lowlands. JNX owns three drilling rigs, is pursuing complimentary activities such as natural brine production, and is partnered with Gastem Inc., and Pétrolia Inc., in the Saint-Simon well located in the Lowlands.

Massive SLL and Gaspe Peninsula Acreage: Initiating Coverage with a $9.50 Target

• Largest landholders in the Appalachain Basin JNX is by far the largest landholder with 1.2mm net acres of land in the St. Lawrence Lowlands and a further ~ 5mm acres in the Gaspe Peninsula

• Solid partnership with Forest Oil in two properties and sharing rigs JNX has a 15% WI in 143mm acres at Becancour & a 40% WI in 55mmacres at Contrecoeur, both to be operated by FST; and owns three rigs.

• Even tempered estimates yield +1 Tcf potential recoverable resource Our risked analysis estimates potential recoverable resources of 1.25 Tcf valued at +$19/shr compared with JNX’s estimate of over 3 Tcf.

• Initiating coverage with a Speculative Buy rating and $9.50 target JNX’s massive SLL acreage with several core properties in the heart of the Utica play drives TGT, with no value attributed to the Gaspe acreage.

Financial Summary Shares O/S (M) 52.2 52-Week Trading RangeMarket Capitalization (M) $196 Average Weekly Volume 1,013,540 Net Debt - 2008E (M) -$10 Market Float (M) $108Enterprise Value (M) $186 Net BV/S - 2007 $0.52Key Properties: WI Acres (net) PartnerBecancour 15% 21,471Contrecoeur 40% 22,000Nicolet 50 27,182Richelieu 100% 138,606St.Simon 90% 51,413Lyster 100% 108,360North Shore Properties 100% 803,211Other Properties 1.5% 72,000

Other Key Assets Junex holds 3.2M shares of Petrolia & 0.55M shares of GastemKey Management: Key Shareholders:Jean-Yves Lavoie President and CEO Officers/Directors ~35%Jacques Aubert Chairman Institutional ~25%Andre Caille Strategic Advisor Lemaire Family ~10%Dr. Roberto AguileraDaniel Courteau

$4.34-$0.52

ORRI in 1.8 mm acres held by Molopo Australia Limited, and ~3 mm acres in Gaspe

Forest to frac a well in July 08, and has committed to spend $8mm

Source: Company reports, WWCM

Price Chart

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

May

-07

Jun-

07

Jul-0

7

Aug

-07

Sep-

07

Oct

-07

Nov

-07

Dec

-07

Jan-

08

Feb-

08

Mar

-08

Apr

-08

May

-08

Pric

e (C

$)

0

1

1

2

2

3

3

4

4

5

Mill

ions

Volu

me

Source: PC Quote

Energy Strategy – The Utica Shale Gas Play

Kim Page, (416) 847-3400; [email protected] May 28, 2008 – 28 Dave Hammond, (416) 847-3406; [email protected]

Investment Summary and Outlook Junex Inc. (JNX-V) is a Quebec based company with oil and gas exploration rights on over six million acres of land in the St. Lawrence Lowlands and Gaspésie (Gaspe Peninsula) areas within the Appalachain Basin. Over one million of these acres are located in the St. Lawrence Lowlands (SLL) area, with three key properties in the heart of the play. In addition to large resource potential within the shales, which Junex has identified to be over 3 Tcf net to interests, the company also owns three drilling rigs, offers drilling services, and owns the rights to natural brine production and a gas storage facility. Based on our risked analysis, we estimate the company’s properties could have potential recoverable resource of over 1 Tcf, which we value at $2.1BN or over $19 per share on a pre financing basis. In view of Junex’s large land holdings, strategic partnership with Forest Oil Corporation (FST-NYSE), and huge resource potential, we are initiating coverage on JNX with a $9.50 target price and Speculative Buy rating.

Investment Highlights Early Mover Advantage - For Years Junex has been Acquiring Highly Prospective Shale Properties As far back as 2002, Junex began building a large land position in St. Lawrence Lowlands to capture exposure in what the company’s founder, Jean-Yves Lavoie, President & CEO, knew was a highly prospective shale gas area. He believed this region had long-since demonstrated proven natural gas production from numerous wells drilled across a large regional shale basin. Junex now holds over 1.1 million net acres of land rights in this area, and has become the largest Canadian based landholder in the region. These lands cover a Barnett style shale play in heart of the Utica play fairway at Becancour, Contrecoeur, and Nicolet in which Junex holds working interests ranging from 15% to 100%, and an Antrim style shale play prospective in many of Junex’s properties located along the North Shore of the St. Lawrence River.

Several Joint-Venture Arrangements Diversify Exposure Junex has a number of joint-venture partnerships, providing a diversified portfolio of assets in which the company is now actively planning development pilot projects:

1. Becancour - In 2006 Junex signed its first agreement with Forest Oil related to Junex’s interest in the 143,141 gross acres Becancour/Champlain permit. Under this agreement, Forest Oil had the ability to earn 100% working interest in the permit by:

a. Coring the previously drilled Becancour #8 well, b. Committing to spend US $8mm over an 18-month period following

exercise of election, and c. Providing Junex with the option to retain a 5% over-riding royalty interest

(ORRI) in the Utica convertible to a direct 15% WI, plus Junex retained a 100% WI in the overburden, Trenton/Black River and deeper horizons, and 100% interest in both the brine production operations and the Becancour underground natural gas storage facility.

In May 2007 following the coring and analysis of a 34 meter core section and of data from the Becancour #8 well, Forest exercised its option to earn-in on the permit and committed to an $8mm pilot-project. Subsequent operations include a

Energy Strategy – The Utica Shale Gas Play

Kim Page, (416) 847-3400; [email protected] May 28, 2008 – 29 Dave Hammond, (416) 847-3406; [email protected]

frac completion on the Becancour #8 well, and the planned drilling of at least one horizontal test well to be completed with multi-stage fracs, and if proven commercially viable, move towards full scale development in 2010.

2. Contrecoeur - In April 2008 a 2nd agreement with Forest Oil for was established related to Junex’s interest in the 55,000 gross acre Contrecoeur property located just 50 kilometers Northeast of Montreal whereby Forest would acquire an option to earn a 60% interest in the permit subject to:

a. Paying Junex an up-front fee of US$1mm b. Committing to spend a further US$4mm over an 18-month period

following exercise of election, c. Junex retaining a 100% WI in the overburden, Trenton/Black River and

deeper horizons, and d. Junex will, as operator, begin drilling an exploration well on the permit

prior to July 2008.

3. Haldimand/Galt/Chaleurs Bay – Announced earlier this month, Junex, Pétrolia (PEA-V), and Gastem Inc. (GMR-V) formed a three-way partnership to develop the Haldimand project in the Gaspee peninsula. Under the terms of the agreement, over the next 12 months, $5mm is expected to be allocated for further development of the Haldimand #1 well previously identified by Pétrolia. A nine square km area has been identified with Junex, as the operator for a minimum of 2 years, having a 45% WI, Pétrolia having a 45% WI, and Gastem the remaining 10% WI. A 5% ORRI will be payable to Terrenex Ventures Ltd (acquired by Questerre Energy Corporation in April 2008); two-thirds of the royalty being paid by Junex and the remaining third, by Pétrolia. Junex also holds 50% to 100% interests in Galt and Chaluers Bay permits, for a total of approximately 1.1 million acres.

4. Additional Interests – In addition to all this, Junex holds ~ 0.55mm shares in Gastem (GMR-V) and 3.2mm shares in Pétrolia (PEA-V), with an aggregate current market value of ~$7mm. Also, Junex has a 1.5% ORRI in the 1.85 million acres in the SLL held by Australia based Molopo Australia Limited.

Huge Resource Potential Junex now holds over 1.1 million net acres of land rights in this area, and has become the largest Canadian based landholder in the region. These lands cover a Barnett style shale play in heart of the Utica play fairway. Based on our risked analysis, we estimate the company’s properties could have potential recoverable resource of over 1.2 Tcf, which we value at $2.1B or over $19 per share on a pre-financing basis (Exhibit 17). This does not assign any incremental value to the additional 5 million acres of lands the company has access to in the Gaspe Peninsula, which is prospective for light oil and gas bearing Devonian aged Hydrothermal Dolomites.

Energy Strategy – The Utica Shale Gas Play

Kim Page, (416) 847-3400; [email protected] May 28, 2008 – 30 Dave Hammond, (416) 847-3406; [email protected]

Exhibit 17: Valuation Summary – Three Key Permits In Heart of Utica Fairway Drive Valuation

Unrisked Implied Valuation #Company/ Major Property Partner (s) Acreage Average Acreage Primary % Area Acreage Recoverable Potential Per Share

Symbol (gross) WI (%) (net) Zone (net) Resource Valuation # UndilutedJunex

JNX.V Becancour Forest 143141 15% 21471 Utica 35% 7515 164 301Contrecoeur Forest 55000 40% 22000 Utica 70% 15400 336 617Nicolet Private 54363 50% 27182 Utica 70% 19027 415 763Richelieu 138606 100% 138606 Other 20% 27721 173 173St. Simon 57126 90% 51413 Other 20% 10283 64 64Lyster 108360 100% 108360 Other 10% 10836 68 68North Shore Properties 803211 100% 803211 Other 10% 80321 31 31Total SLL Acreage: 1172243 171103 1251 2018 $19.33* JNX owns a 1.5% ORRI in 1.8 mm acres held by Molopo Australia Limited and approx. 3mm gross acres in Gaspe region* JNX also owns 316,567 net acres of explorat ion lands in the Haldimand/Galt/Baie des Chaleurs region of the Gaspe Peninsula

# Valuation based on our "type well" model and assumptions which value potential recoverable resources at $1.84/mcf in-the-ground for near-term projects and $1.00/mcf for longer-term development areas * Other assets not included in valuation

ProspectivityUtica Shale Players - St. Lawrence Lowlands (SLL) Land Holdings

Source: Junex Company Reports, WWCM

Energy Strategy – The Utica Shale Gas Play

Kim Page, (416) 847-3400; [email protected] May 28, 2008 – 31 Dave Hammond, (416) 847-3406; [email protected]

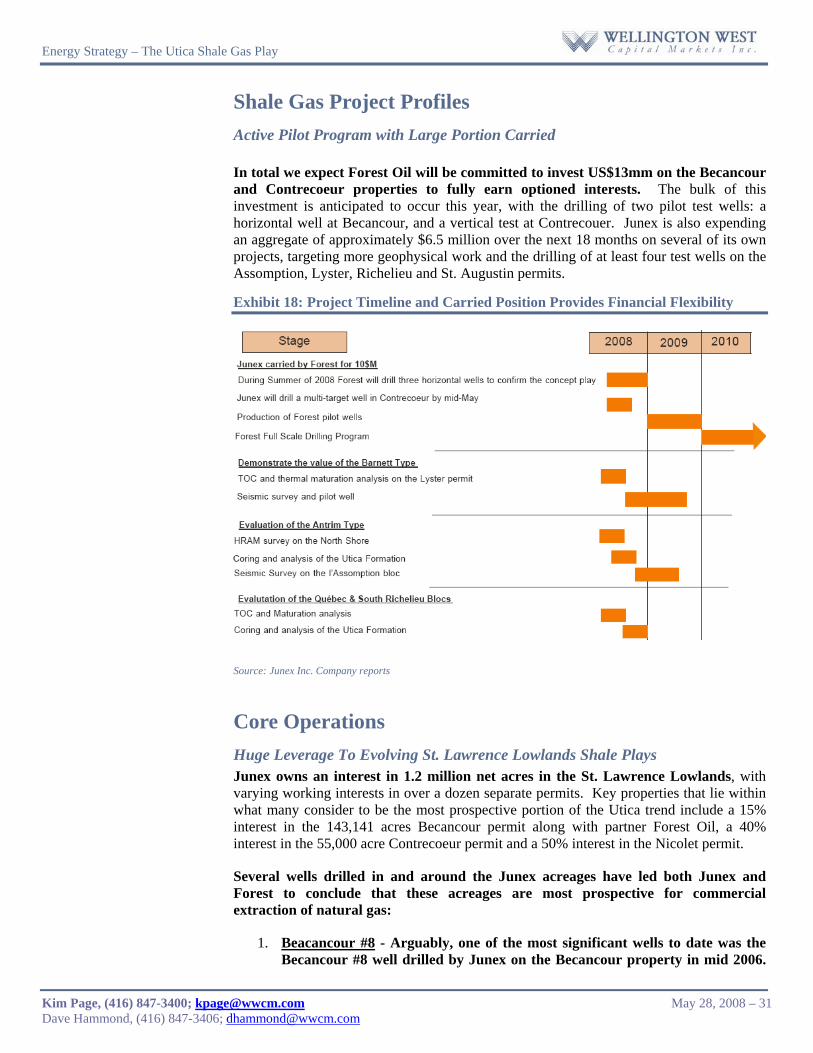

Shale Gas Project Profiles Active Pilot Program with Large Portion Carried

In total we expect Forest Oil will be committed to invest US$13mm on the Becancour and Contrecoeur properties to fully earn optioned interests. The bulk of this investment is anticipated to occur this year, with the drilling of two pilot test wells: a horizontal well at Becancour, and a vertical test at Contrecouer. Junex is also expending an aggregate of approximately $6.5 million over the next 18 months on several of its own projects, targeting more geophysical work and the drilling of at least four test wells on the Assomption, Lyster, Richelieu and St. Augustin permits.

Exhibit 18: Project Timeline and Carried Position Provides Financial Flexibility

Source: Junex Inc. Company reports

Core Operations Huge Leverage To Evolving St. Lawrence Lowlands Shale Plays Junex owns an interest in 1.2 million net acres in the St. Lawrence Lowlands, with varying working interests in over a dozen separate permits. Key properties that lie within what many consider to be the most prospective portion of the Utica trend include a 15% interest in the 143,141 acres Becancour permit along with partner Forest Oil, a 40% interest in the 55,000 acre Contrecoeur permit and a 50% interest in the Nicolet permit.

Several wells drilled in and around the Junex acreages have led both Junex and Forest to conclude that these acreages are most prospective for commercial extraction of natural gas:

1. Beacancour #8 - Arguably, one of the most significant wells to date was the Becancour #8 well drilled by Junex on the Becancour property in mid 2006.

Energy Strategy – The Utica Shale Gas Play

Kim Page, (416) 847-3400; [email protected] May 28, 2008 – 32 Dave Hammond, (416) 847-3406; [email protected]

While drilling, Forest Oil agreed to cover the cost of cutting core, and based on analysis of 34 meters or core, log data, and well test information elected to exercise an option to enter into a US$8mm pilot project, including fracing the Becancour #8 well and drilling a horizontal development well, currently planned for this summer.

2. Gentilly #1 - A second significant well was the Gentilly #1 well drilled by Questerre Energy and Talisman Energy also in 2006, just a few kilometres away from the Becancour property. This well tested at IP rates of over 4.5 mmcf/d over a three day period then quickly declined to the ~300 mvf/d to 600 mcf/d range.

3. Villeroy - An older well drilled in 1973 at Villeroy just Northeast of the Gentilly well (an asset Mr. Jean-Yves Lavoie knew going back 30+ years) also tested at meaningful rates of between 0.2 million to 1.2 million mmcf/d over a 25 day period.

4. St. Francois-du-Lac #1 - And finally, a well some 50 miles to the Southwest of the Gentilly well drilled by Gastem in the summer of 2007 also tested at rates of up to 1.0 mmcf/d.

The results from all these wells encouraged Junex to complete further seismic studies on their property in 2007. And the mounting data from the growing number of wells with positive shows, combined with core analysis, and independent studies on the resource potential of the Lorraine, Trenton Black-River and Utica shales, all encouraged Forest oil to accumulate more interests in the play.

In June of this year Junex plans to spend ~$1.1mm to complete an HRAM survey on the N.Shore, as well as a 30 sq. kilometers seismic survey. By the end of Q2/08 Junex is expected to commence their pilot program at Contrecoeur, and has plans for at least one additional pilot well in 2009. Natural gas in the Trenton Black-River is Junex’s primary target, and their secondary objective is natural brine production. Next winter, Junex plans to spend an additional $2mm for a well at Lyster. At St-Augustin, Junex plans to drill one well this summer, and has allocated $700k for the project. At Richelieu South, Junex plans to drill one well in 2009, following results of geochemical analysis later this year.

Energy Strategy – The Utica Shale Gas Play

Kim Page, (416) 847-3400; [email protected] May 28, 2008 – 33 Dave Hammond, (416) 847-3406; [email protected]

Exhibit 19: Junex Holds Largest Land Position of the Canadian Players in the Appalachian Basin

Source: Junex Inc. Corporate Website

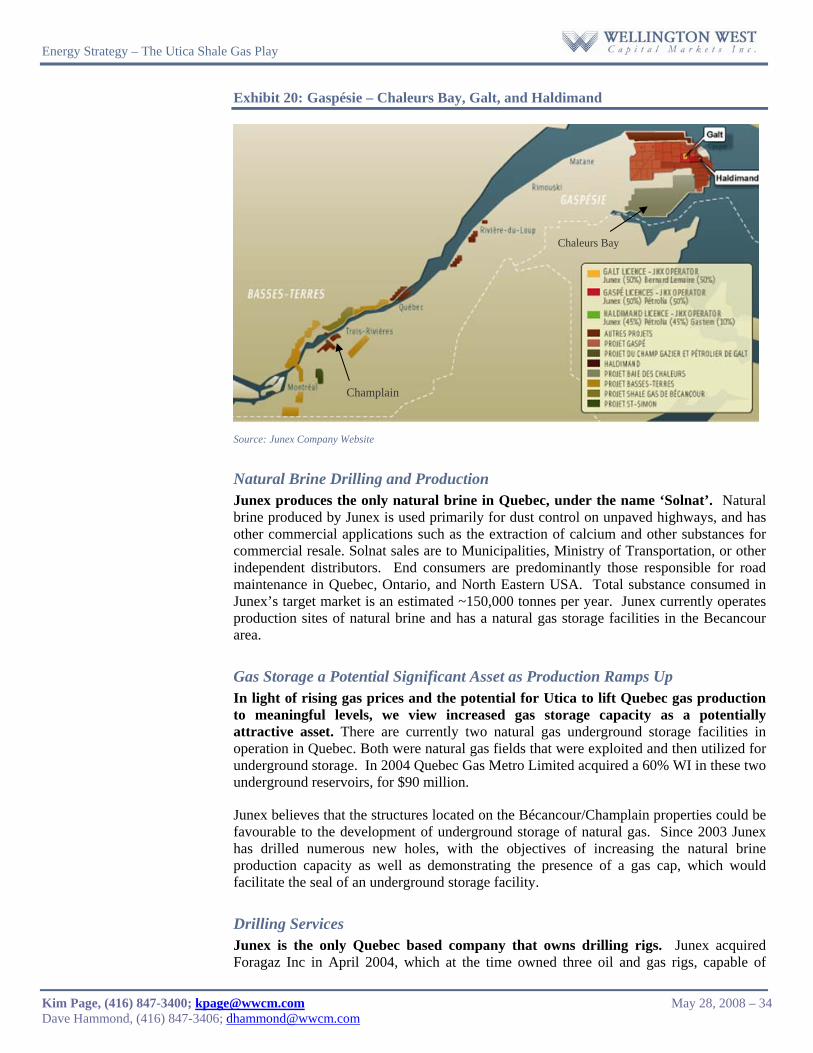

Gaspésie Exploration Projects: Chaleurs Bay, Galt, and Haldimand Junex is also active in the region of Gaspésie, under a joint-venture arrangement with Pétrolia. Under the arrangement, Junex and Petrolia each have a 50 percent stake on licenses covering about 291 square km’s between the Galt property and the Pétrolia -Haldimand discovery well. Junex will be the operator in this area, and Pétrolia has granted Junex a 0.5% to 2.5% royalty on any production from their Gastonguay and Gaspe properties. This year Junex plans to drill one oil development well at Haldimand, stimulate a low productivity gas well in the Galt concession, and further redefine an exploration target in the Chaleurs Bay prospect area.

Chaleurs Bay is an onshore sedimentary basin with highly prospective reservoir rocks. Junex has >1 million acres at Chaleurs with 100% WI, and using seismic, aeromagnetic, and surface data, have compiled numerous prospects. This year and in 2009 Junex plans to complete additional surveys, potentially re-enter the Paspebiac well, and complete new exploratory wells later this year or in 2009. At Galt Junex has a joint-venture with a private company ‘Gestion Bernard Lemaire’. The 1st well drilled at Galt showed small quantities of oil and gas, and the 3rd well produced 1,300 boe in 2007.

Energy Strategy – The Utica Shale Gas Play

Kim Page, (416) 847-3400; [email protected] May 28, 2008 – 34 Dave Hammond, (416) 847-3406; [email protected]

Exhibit 20: Gaspésie – Chaleurs Bay, Galt, and Haldimand

Source: Junex Company Website

Natural Brine Drilling and Production Junex produces the only natural brine in Quebec, under the name ‘Solnat’. Natural brine produced by Junex is used primarily for dust control on unpaved highways, and has other commercial applications such as the extraction of calcium and other substances for commercial resale. Solnat sales are to Municipalities, Ministry of Transportation, or other independent distributors. End consumers are predominantly those responsible for road maintenance in Quebec, Ontario, and North Eastern USA. Total substance consumed in Junex’s target market is an estimated ~150,000 tonnes per year. Junex currently operates production sites of natural brine and has a natural gas storage facilities in the Becancour area.

Gas Storage a Potential Significant Asset as Production Ramps Up In light of rising gas prices and the potential for Utica to lift Quebec gas production to meaningful levels, we view increased gas storage capacity as a potentially attractive asset. There are currently two natural gas underground storage facilities in operation in Quebec. Both were natural gas fields that were exploited and then utilized for underground storage. In 2004 Quebec Gas Metro Limited acquired a 60% WI in these two underground reservoirs, for $90 million.

Junex believes that the structures located on the Bécancour/Champlain properties could be favourable to the development of underground storage of natural gas. Since 2003 Junex has drilled numerous new holes, with the objectives of increasing the natural brine production capacity as well as demonstrating the presence of a gas cap, which would facilitate the seal of an underground storage facility.

Drilling Services Junex is the only Quebec based company that owns drilling rigs. Junex acquired Foragaz Inc in April 2004, which at the time owned three oil and gas rigs, capable of

Chaleurs Bay

Champlain

Energy Strategy – The Utica Shale Gas Play

Kim Page, (416) 847-3400; [email protected] May 28, 2008 – 35 Dave Hammond, (416) 847-3406; [email protected]

drilling 400 to 2,000 metres deep. This acquisition added drilling services to Junex line of expertise, and drilling service revenues.

History and Management A History of Diversified Interests Junex was founded in March 1999 by Mr. Jacques Aubert, former president of SOQUIP (Société Québécoise d’initiatives pétrolières), and Mr. Jean Yves, a petroleum engineer with over 20 years of hydrocarbon exploration experience. Junex completed an initial public offering in 2001 with a listing on the TSX Venture Exchange (JNX.V), and in 2002 became the first Quebec company to develop and produce a natural brine field. Over the following few years, Junex completed various exploration exercises to developed its properties, and positive cash flow was achieved in 2006. Since 2006, Junex has preceded with multiple partnership arrangements, aggressively targeting the Utica Shales, the Trenton/Black-River along the St-Lawrence Lowlands, and the oil discovery in Gaspésie.

Management and Board of Directors Jean-Yves Lavoie is President, Co-Founder and CEO of Junex which was created in 1999 and was first listed on the stock market in June 2001. He was employed by SOQUIP as a petroleum engineer from 1974 to 1980 after which he remained active as a technical consultant and drilling engineer on several oil and gas projects in Quebec and overseas. All these different experiences either prior of following the production process have permitted him to refine his entrepreneurship qualities. As president of Les Ressources Naturelles Jaltin Inc. he has, among other things, initiated the realization of the natural gas underground storage of Pointe-du-Lac. This was a first in Quebec and also a first worldwide to ever be perform in non-consolidated sediments. Mister Lavoie is a member of l’Ordre des Ingénieurs du Québec as well as the Association of Engineers, Geologists and Geophysicists of Alberta.