strategic outlook of global hybridization trends in select off highway commercial vehicle markets

TRANSCRIPT

1 NB77-18

Strategic Outlook of Global Hybridization Trends in Select

Off-highway Commercial Vehicle Markets Growth in Demand is Set to Drive Production to Around 90,258 Units by 2018

NB77-18

February 2013

2 NB77-18

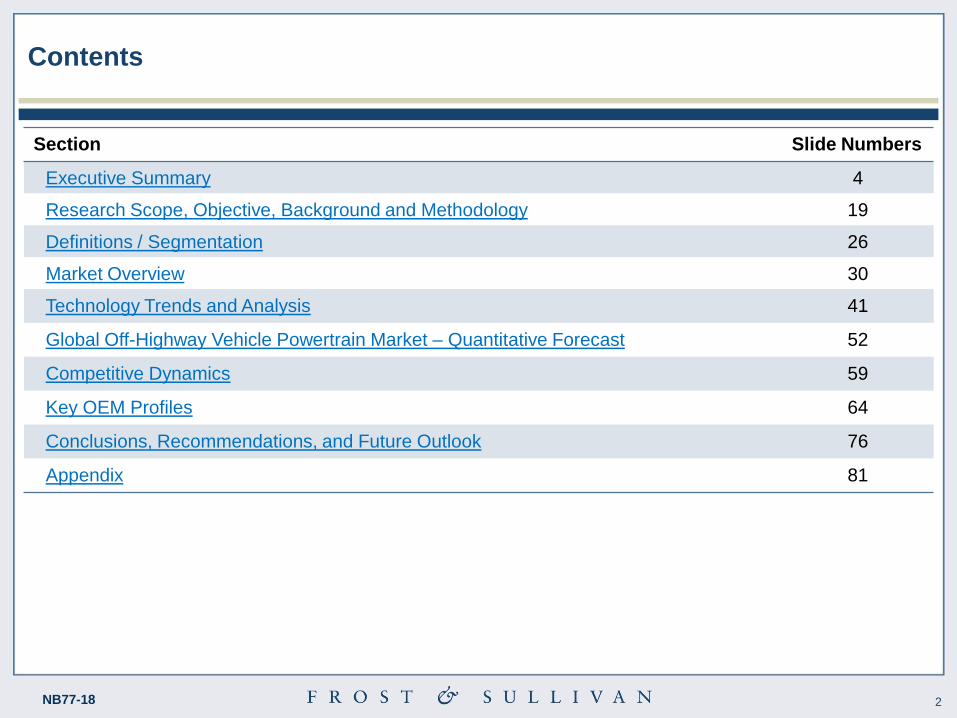

Contents

Section Slide Numbers

Executive Summary 4

Research Scope, Objective, Background and Methodology 19

Definitions / Segmentation 26

Market Overview 30

Technology Trends and Analysis 41

Global Off-Highway Vehicle Powertrain Market – Quantitative Forecast 52

Competitive Dynamics 59

Key OEM Profiles 64

Conclusions, Recommendations, and Future Outlook 76

Appendix 81

3 NB77-18 3 NB77-18

Executive Summary

4 NB77-18

Impact of Mega Trends on Off-highway Construction and Agricultural Vehicles

Markets

Expansion of Industrial

Agriculture to ROW

• More global large-scale farms as governments address food security concerns

• Large harvesters and combines see sales growth in developing nations for mono-culture farming.

• Engines with more horsepower (100−400 hp) to see increasing demand.

Growth Industries of the Future

• Government infrastructure investment expected to resurface roads and rebuild bridges

• Agriculture: Population growth expected to result in increased food production especially from land sources, because fish and seafood stock are projected to decline.

Waste Diversion Programs

• Waste streams increasingly seen as potential new source of supply for metals, plastics, compost, and natural gas.

• This trend is expected to result in lower than projected demand for newly mined resources.

Smart and Eco Cities, Mass

Transit Infrastructure

• Mass transit infrastructure expected to see high demand in the future. Specifically, high speed, light, and monorail, along with bus rapid transit systems, to see increased market adoption.

• Increased demand seen for specialised equipment.

Alternative Fuels

• With emissions regulations for diesel engines becoming more stringent, a few OEMs are seeing a resurgence in demand for gasoline, LPG, and CNG engines in smaller equipment.

• Demand for bio-diesel and ethanol expected to remain strong.

Source: Frost & Sullivan analysis. Image source: zenlifesolutions.com,

5 NB77-18

Impact of Mega Trends on Off-highway Construction and Agricultural Vehicles

Markets (continued)

Decreased demand for construction

equipment in developed markets

• The construction market is mature, and has relatively fewer activities in progress.

• A transition to rebuilding and maintenance rather than infrastructure expansion is occurring, indicating a demand for smaller vehicles and equipment.

New product opportunity—hybrid heavy construction

equipment

• Heavy-use, high duty-cycle heavy equipment demonstrating business case for hybrid power trains allows for smaller internal combustion engines than are normally associated with this equipment.

Rightsizing and downsizing

• Shift toward smaller engines expected, which provide the added benefit of offering greater visibility around equipment.

• Users are hobby farmers, small orchards, and vineyards using smaller tractors.

Growing regulations

• Trends toward stricter and greater regulations for noise and emissions from urban construction vehicles; in turn, this trend is expected to drive demand for low hp equipment. e.g. Tier IVi/Stage III

Source: Frost & Sullivan analysis. Image source: zenlifesolutions.com,

6 NB77-18

Key Findings Rising fuel prices and increasingly stringent emissions legislation expected to propel hybrid powertrain

production to 90,258 units by 2018.

• Strengthening emission regulations globally and continued volatility in fuel prices are the

key drivers for hybridization of off-highway equipment powertrains.

• Hybrid powertrains are expected to account for 3.0% (90,258 units) of global off-highway

powertrain production in 2018.

• Hybrid technology development is gaining focus in the regions of Europe, Asia and North

America in that order.

• Asia is expected to emerge as the key market among these three regions with an

estimated production of 43,000 units in 2018.

• Every major OEM in key markets is researching and developing hybrid powertrains.

Frost & Sullivan expects key product launches in the short- to medium-term.

• An estimated potential to reduce fuel consumption by up to 50.0%, these hybrid

powertrains are expected to command a price premium of 30.0% over equivalent

conventional powertrain equipment.

• Developments in power electronics, in particular in the field of insulated gate bipolar

transistors (IGBTs), are expected to drive cost reduction of hybridization in the medium

to long-term.

• Hybridization is an effective engine downsizing strategy; and hence Frost & Sullivan

expects market opportunity in the below 56kW (76hp) power bandwidth. The emission

requirements become less stringent below this point.

• Significant potential for application in urban environments since hybridization results in

smaller and quieter engines.

Global

level

Region

level

OEM

and

techno

-logy

level

Source: Frost & Sullivan analysis.

7 NB77-18

Drivers and Restraints Hybrid powertrain technology will enable emissions compliance and reduce total cost of ownership. Further

technical developments will reduce cost and drive growth, and technology and cost restraints.

Driv

ers

R

estra

ints

Driv

ers

R

es

train

ts

Technology

transfer from

the transport

sector

Significant fuel

economy improvement

benefits over

equivalent IC-only

powertrain

Strengthening

emission legislation

necessitating adoption

of hybrid powertrain Corporate social

responsibility

improving OEM

brand image

Technological

advancement and

maturity

accelerating OEM

adoption of

technology

Government

incentives driving

unit shipment

growth

High upfront

cost of hybrid

technology

High cost

of battery

technology

Suitability for

different

applications

Challenges in battery

technology raising

application concerns

Priorities for

rental market

customers

Customer

perception of

durability

8 NB77-18

0.0

200.0

400.0

600.0

800.0

2011 2018

Re

ve

nu

e (

$ M

illio

n)

Motor Generator Control Electronics Power Electronics

Ultracapacitor Battery

Strategic Fact Sheet The hybrid powertrain market is expected to account for 3.0% of the global off-highway powertrain market by

2018. Revenue from components market is expected to reach $644.4 million by 2018.

Off-highway Hybrid Commercial Vehicle Market: Powertrain Penetration, Global, 2011 and 2018

Off-highway Hybrid Commercial Vehicle Market: Hybrid Vehicle Component Revenue Forecast, Global, 2011 and 2018

$ 20.8 million

$ 644.4 million

0

50

100

150

200

250

300

350

Asia Europe NA RoW

Re

ve

nu

e (

$ M

illio

n)

Motor/Generators Control Electronics

Power Electronics Ultracapacitors

Batteries

$33.4 mil.

$99.3 mil.

$194.6 mil.

$317.1 mil.

Off-highway Hybrid Commercial Vehicle Market: Hybrid Vehicle Component Revenue Forecast by Region, Global,

2018

Off-highway Hybrid Commercial Vehicle Market: Key Takeaways, 2011–2018

• By 2018, hybrid powertrain is expected to reach

3.0% of suitable applications or 90,258 units.

• Certain segments of the off-highway industry are

particularly suitable for hybrid powertrain. Ex:

excavators, wheel loaders, and forklifts.

• To drive widespread adoption of hybrid technology

mild hybridization needs to be adopted, enabling

machinery to be converted quickly and at a lower

cost. Economies of scale are also possible with

integrators developing flexible hybrid modules.

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

2011 2018

Total Production Hybrid powertrain

1,775 90,258

Un

its P

rod

uce

d

Note: All figures are rounded; the base year is 2011. Source: Frost & Sullivan analysis.

9 NB77-18

Regional Perspectives The Asian market is expected to produce 43,000 hybrid powertrain systems by 2018, thus accounting for

nearly half of total global production.

0.4

28

0

10

20

30

40

50

2011

2018

Un

its

pro

du

ce

d

(‘000)

Europe

0.2

14

0

10

20

30

40

50

2011

2018 U

nit

s p

rod

uce

d

(‘000)

North America

0.1 5

0

10

20

30

40

50

2011

2018 U

nit

s p

rod

uce

d

(‘000)

ROW

Off–highway Hybrid Commercial Vehicle Market: Global Production and Customer Perception by Region, 2011 and 2018

Leading Hybrid

OEMs in N.

America

Caterpillar

John Deere

Leading Hybrid

OEMs in Europe

Deutz

Heinzmann Leading Hybrid

OEMs in Asia

Komatsu

Toyota

North America

• Corporate social

responsibility is an

important driver.

• Comparatively lower

fuel costs affect the

business case for

adoption.

Europe

Fuel savings and corporate

social responsibility are

important drivers here,

leading to high penetration in

certain applications.

South America

Natural resource development will

require the development of

infrastructure.

Asia

• Sales are driven by fuel

economy and corporate

social responsibility.

• Reduced noise is an

important factor,

particularly when operating

in built-up urban areas.

Note: All figures are rounded; the base year is 2011. Source: Frost & Sullivan analysis.

1.1

43

0

10

20

30

40

50

20

11

20

18 U

nit

s p

rod

uce

d

(‘000)

Asia

10 NB77-18

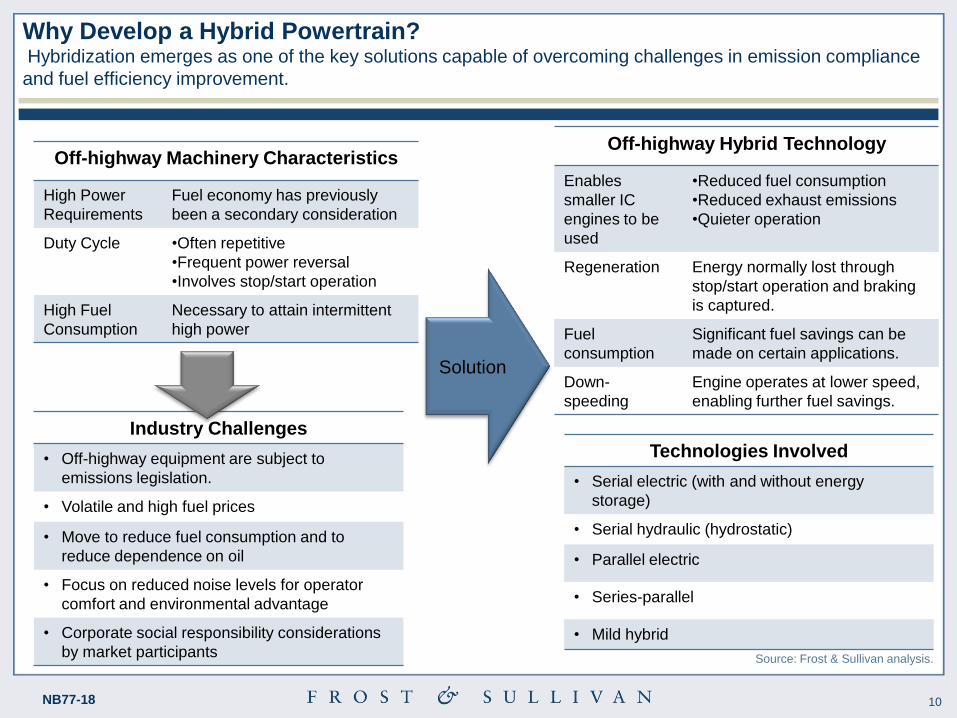

Why Develop a Hybrid Powertrain? Hybridization emerges as one of the key solutions capable of overcoming challenges in emission compliance

and fuel efficiency improvement.

Off-highway Machinery Characteristics

High Power

Requirements

Fuel economy has previously

been a secondary consideration

Duty Cycle •Often repetitive

•Frequent power reversal

•Involves stop/start operation

High Fuel

Consumption

Necessary to attain intermittent

high power

Industry Challenges

• Off-highway equipment are subject to

emissions legislation.

• Volatile and high fuel prices

• Move to reduce fuel consumption and to

reduce dependence on oil

• Focus on reduced noise levels for operator

comfort and environmental advantage

• Corporate social responsibility considerations

by market participants

Off-highway Hybrid Technology

Enables

smaller IC

engines to be

used

•Reduced fuel consumption

•Reduced exhaust emissions

•Quieter operation

Regeneration Energy normally lost through

stop/start operation and braking

is captured.

Fuel

consumption

Significant fuel savings can be

made on certain applications.

Down-

speeding

Engine operates at lower speed,

enabling further fuel savings.

Technologies Involved

• Serial electric (with and without energy

storage)

• Serial hydraulic (hydrostatic)

• Parallel electric

• Series-parallel

• Mild hybrid

Source: Frost & Sullivan analysis.

Solution

11 NB77-18

Key Industry Participants The majority of key off-highway vehicle manufacturers focusing on development of hybrid technology and

equipment.

Key Component and

System Suppliers Atlas Weyhausen

Mecalac

Caterpillar

Shantui

Komatsu , Doosan,

Hitachi, Kobelco

Case, Sany,

Sunward, Yuchai (P)

TICO

Still

Mitsubishi

Doosan (P)

Volvo

John Deere

Hitachi

P = Planned Source: Frost & Sullivan analysis.

BAE, Henizmann, ZF, Dana,

Maxwell, Deutz, Eaton

The following are examples of OEM involvement

towards hybrid powertrain:

Bulldo

-zer

Fork

-lift

Wheel

Loaders

Compact

Equipment

Excav

-ators

12 NB77-18

Regional Perspectives (Machinery) The perspectives on hybrid powertrain for off-highway equipment are distinct and varied with a different

emphasis in every region.

Source: Frost & Sullivan analysis.

Market Machinery Powertrain Hybridization Factors

Europe • Wheel Loader

• Excavator

• Hybrid diesel-electric with energy

storage usually in the form of battery for

wheel loaders and capacitors for

excavators.

• Engine manufacturers are beginning to

ensure that future diesel engines are

‘hybrid-compatible’.

• Recent launch. Sales will initially be made for

Corporate Social Responsibility (CSR)

reasons. Later in the cycle fuel economy and

emissions will become more important.

• City centre operation and driver comfort will

drive sales of some machines

• First excavators are in the 20-tonne class.

Technology will penetrate other machine

capacities

APAC • Excavator

• Fork Lift

• Diesel-electric with capacitors

• Fork lift uses both serial and parallel

technology in the same platform.

Batteries are used for energy storage

• Key drivers are fuel economy and operator

comfort. Intensive work cycles and high fuel

costs create a good business case.

• Operator comfort is also recognized as a key

benefit (reduced noise).

North America • Bulldozers

• Hybrid Wheel

Loader

• Bulldozer uses diesel –electric currently

without energy storage. Possible use of

batteries as technology matures.

• Wheel loaders moving toward full series

hybrid

• Greater use of batteries will be considered

when cost reduces and technology improves.

• Rental firms (major customer group) are

beginning to enquire about fuel economy.

Technology premium will be key however.

13 <0000-00> NB77-18 13

Geographic Regions

The regional markets covered in this research service are:

• North America consists of United States, Mexico and Canada

• Europe consists of Western Europe, Eastern Europe and Russia

• Asia consists of China, Japan, India, South Korea, Indonesia and Pakistan

• Rest of World consists of key markets in South America, Africa, Middle East, Rest of Asia, and Oceania

(Australia and New Zealand).

Geographic Definitions and Research Timeline Research Scope

Source: Frost & Sullivan research.

Off-highway vehicles Vehicle Type

2012 to 2018 Forecast Period

2009 to 2018 Study Period

2011 Base Year

14 <0000-00> NB77-18 14

Key Contacts

Ananth Srinivasan

Team Leader – Off highway Vehicle Research

Linkedin:

http://www.linkedin.com/in/ananthapadmanabh

ansrinivasan

Sandeep Kar

Global Director- Commercial Vehicle Research

Jeannette Garcia

Corporate Communications – North America

Direct: +1.210.477.8427

Email: [email protected]

15 <0000-00> NB77-18 15

Legal Disclaimer

Frost & Sullivan takes no responsibility for any incorrect information supplied to us by

manufacturers or users. Quantitative market information is based primarily on interviews

and therefore is subject to fluctuation. Frost & Sullivan research services are limited

publications containing valuable market information provided to a select group of

customers. Our customers acknowledge, when ordering or downloading, that Frost &

Sullivan research services are for customers’ internal use and not for general publication or

disclosure to third parties. No part of this research service may be given, lent, resold or

disclosed to noncustomers without written permission. Furthermore, no part may be

reproduced, stored in a retrieval system, or transmitted in any form or by any means,

electronic, mechanical, photocopying, recording or otherwise, without the permission of the

publisher.

For information regarding permission, write to:

Frost & Sullivan

331 E. Evelyn Ave. Suite 100

Mountain View, CA 94041