stoxplus_vietnamcementsectorupdatereport-july2014-demo_20140812143543

TRANSCRIPT

‹#›

Vietnam Cement Sector Update Report 2014Issue date: July 30th, 2014

Part of StoxPlus’s Market Research Reports for Vietnam

@ 2014 StoxPlus Corporation.

All rights reserved. All information contained in this publication is copyrighted in the name of StoxPlus, and as such no part of this

publication may be reproduced, repackaged, redistributed, resold in whole or in any part, or used in any form or by any means graphic,

electronic or mechanical, including photocopying, recording, taping, or by information storage or retrieval, or by any other means, without

the express written consent of the publisher.

2

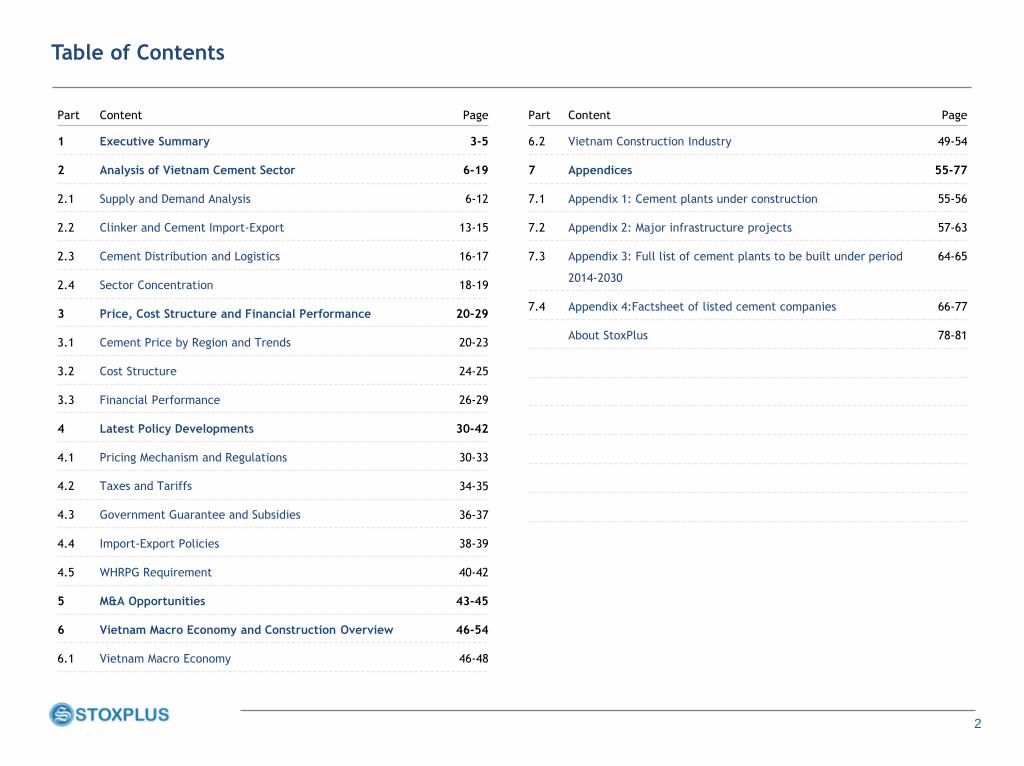

Table of Contents

Part Content Page

6.2 Vietnam Construction Industry 49-54

7 Appendices 55-77

7.1 Appendix 1: Cement plants under construction 55-56

7.2 Appendix 2: Major infrastructure projects 57-63

7.3 Appendix 3: Full list of cement plants to be built under period

2014-2030

64-65

7.4 Appendix 4:Factsheet of listed cement companies 66-77

About StoxPlus 78-81

Part Content Page

1 Executive Summary 3-5

2 Analysis of Vietnam Cement Sector 6-19

2.1 Supply and Demand Analysis 6-12

2.2 Clinker and Cement Import-Export 13-15

2.3 Cement Distribution and Logistics 16-17

2.4 Sector Concentration 18-19

3 Price, Cost Structure and Financial Performance 20-29

3.1 Cement Price by Region and Trends 20-23

3.2 Cost Structure 24-25

3.3 Financial Performance 26-29

4 Latest Policy Developments 30-42

4.1 Pricing Mechanism and Regulations 30-33

4.2 Taxes and Tariffs 34-35

4.3 Government Guarantee and Subsidies 36-37

4.4 Import-Export Policies 38-39

4.5 WHRPG Requirement 40-42

5 M&A Opportunities 43-45

6 Vietnam Macro Economy and Construction Overview 46-54

6.1 Vietnam Macro Economy 46-48

3

Section 1: Executive Summary

Contents

4

Executive Summary

Vietnam cement market would deviate from the

supply surplus, and reach an equilibrium by 2026 in

our base case forecasting.

Vietnam has experienced a surplus of cement since

2009, and the situation has become more serious

since 2011. Yet, the Master Plan developed in 2011

was meant to increase the number of cement plants

from now until 2020. We have carefully reviewed the

status of such expansion / new development of

cement plants to analyze the supply of Vietnam

cement.

Under our base case, which is a prudent scenario

based on analysis of macroeconomics and cement

demand factors such as the status of infrastructure

development and residential sector, we forecast a 5%

annual demand growth for cement until 2030. The

result is that Vietnam in general will continue the

surplus until 2026.

It is importantly to note that the scenario may be

different if the source of funding issue is resolved by

the Government and a number of mega construction

projects would be taken.

However, clinker capacity is still having a

significant shortage in the South

7.0 7.0 7.0 7.0 7.0 7.0 7.0

16.8 17.7 18.6 19.5 20.5 21.5 22.6

0

5

10

15

20

25

2013 2014E 2015E 2016E 2017E 2018E 2019E

Ton m

illion

Total Clinker Capacity Total consumption (5%)

Lack of cement in the South

The south does not have natural

resources necessary to produce

clinker. They will always have a

shortage of clinker

Overall, Vietnam will continue the supply surplus in

the coming years, but looking closer, the situation is

more complicated and varies by region.

In fact, the North and the Central will continue the

supply surplus. Demand in the North, at 3% annual

growth, will still be lower than the supply by 2030. In

the Central, even at the quickest demand growth of

7%, cement equilibrium would not be achieved until

2028.

Meanwhile, the South will continue to have a

shortage of clinker, which is supplied from the North

and Central. The clinker shortage in the South will

get worse and widen until 2020, as there are no

cement plant projects in the South until 2020.

Cement demand landscape can change

significantly based on the implementation of

infrastructure projects. However, the status of

those projects is very uncertain.

Vietnam is a developing country and still short of all

types of infrastructure, both the hard and the soft

infrastructure. There are 243 projects planned until

2030, which is value at a total of US$221bn.

However, the status of these infrastructure projects

is very uncertain, depending on the availability of

funding. Yet, State deficit continues to widen in

2013, to nearly 6% of GDP. Given the lack of funding,

the plan for infrastructure is more of a wish list with

low chance of being implemented as planned.

Sector Concentration: Vietnam cement is

characterized with three groups of players, i.e.

Vietnam Cement Industry Corporation (VICEM) with

32% in term of total sales volume from its 11

members companies; foreign players including

Holcim, Chinfon and LUKS Vietnam occupying 30% of

market share.

The remaining 48% is contributed by many local

private companies, of which notable players are The

Vissai (located in Ninh Binh province), Cong Thanh

Cement (located in Thanh Hoa province) and

Vietnam Cement Management Ltd (located in Quang

Binh province).

One of the new development in market share and

competition dynamics is the entrance of Viettel.

Viettel has acquired Cam Pha Cement, and recently

Ha Long Cement, making their total capacity of

clinker to be 3.6 MTPY, and cement to be 4.2 MTPY.

With the two acquisitions, Viettel has become the

largest State-owned player in terms of cement

capacity.

Price and Competition: Cement is no longer included

in the price basket for CPI index calculation but it is

subject to the so called “Price Declaration Program”

of the Government. Under this scheme, the price

notification must be sent to competent authorities by

manufacturing and business organizations and

individuals at least 5 days before the price

determination or adjustment.

Cement price is lowest in the North, and highest in

the South (due to freight and transportation cost of

clinker from the North to the South). Moreover,

domestic cement price has been on an upward trend

due to rising cost of raw materials and energy (coal

and electricity). The average price is US$57 in the

North, US$63 in the Central, and US$73 in the South.

Vietnam cement price is still lower than in

neighboring countries due to supply surplus and lack

of planning from the Government, leading to price

dumping.

5

Executive Summary

Major policy developments: Main regulation

document on this sector is the Cement Master Plan

issued under Decision 1488 by the Prime Minister in

Aug 2011. The Government imposed very strict

conditions for new cement license in terms of

capacity size, technical performance and financial

capability. To cope with soaring energy costs, the

policy also requires that by 2015 all plants must apply

the Waste Heat Recovery Power Generation

(“WHRPG”) to meet at least 20% of its electricity

consumption. By 2014 end, all cement projects with

a capacity of 2,500 tons of clinker per day must

have WHRPG system commissioned but only three

of them complied with the regulation until now.

Ministry of Finance is working with some donors such

as Asia Development Bank to provide soft financing to

help cement plants deal with this compliance and

environment matter.

The second policy development is the restructuring of

the Master Plan. By early 2014, the Government has

decided to delay 9 out of 16 cement factories

planned to be built by 2015 until after 2015. 24 other

projects planned for the period of 2016-2020 is also

under a very uncertain status.

The third regulatory development concerns the

Government loan guarantee scheme. The

Government recently decided not to provide

guarantee for cement loans. For example, Prime

Minister, in an official letter issued in early 2014,

rejected the request for foreign loan guarantee by

Tan Thang Cement Project.

Costing and Financial performance: We analyzed in

details cost of production of a cement player in the

Central. The cost structure is such that: coal 46%, raw

materials 15% electricity 8%, labor 6%, and other costs

24%. Given the cost of production, It is more cost-

efficient to transport clinker from the Central to grind

into cement in Ho Chi Minh, rather than transporting

cement from the Central to Ho Chi Minh.

Our data showed that historical EBITDA margin on

average for 20 public cement companies in Vietnam is

at 15.3% in 2013. In 2013, the EBITDA margin of most

cement companies reduced from their level in 2012.

The main reason is that due to weak demand, the

cement companies did not increased their sales price

while their input’s prices such as electricity, gas, oil

continue to rise.

Meanwhile, the average profit margin of listed cement

plants in 2013 is still negative, standing at -1.0%. This

is a slight decrease from the level of -0.4% in 2011,

indicating that many of the cement plants are still in

financial difficulty.

Sector Consolidation - Viettel is becoming a big

player: We are observing an active consolidation

tendency than ever in cement sector of Vietnam. In

this situation where many cement producers are

facing financial distressed, consolidation is just a

matter of timing to obtain the economy of scale for

this sector in both production and logistics.

Notable active acquirers are some local cement

companies with strong financial position, e.g. The

Vissai, Cong Thanh, Vietnam Cement Management Ltd

and foreign investors, e.g. Anhui (from China), Semen

Gresik (from Indonesia), to name a few.

Most recent active local buyer now is Viettel Group,

the largest military-run telecom provider. Viettel

Group just acquired Cam Phan Cement JSC from

Vinaconex JSC and most recently Ha Long Cement JSC

from Song Da Corporation. Viettel now holds 4.4MTPY

of cement from these two investees

6

Section 2: Analysis of Vietnam Cement Sector

2.1 Supply and Demand Analysis

2.2 Clinker and Cement Import-Export

2.3 Cement Distribution and Logistics

2.4 Sector concentration

Contents

7

Section 3: Analysis of Vietnam Cement Sector

Supply and Demand Analysis

According to our own analysis of supply and demand, the base case scenario of 5% demand growth,

Vietnam still has a supply surplus until 2026.

This page is intentionally left blank

8

Total cement consumption had a slight increase of 2% in 2013. However, cement consumption in the

North continued to decline, and the Central failed to keep up the same high growth as before.

Figure : Breakdown growth rate of consumption

Source: Cement Association and StoxPlus

-20%

-10%

0%

10%

20%

30%

40%

50%

2007 2008 2009 2010 2011 2012 2013

North Central South Whole country

Section 3: Analysis of Vietnam Cement Sector

Supply and Demand Analysis

Central’s cement

demand shot up in 2011

due to the construction

of Formosa

This page is intentionally left blank

9

Section 3: Analysis of Vietnam Cement Sector

Supply and Demand Analysis

Utilization rate

This page is intentionally left blank

10

The South continues to have a short supply of clinker. The South has to transport clinker from the

North and Central, but there are many logistics inefficiency in the process.

Section 3: Analysis of Vietnam Cement Sector

Supply and Demand Analysis

This page is intentionally left blank

11

While consumption decreased, cement capacity kept increasing from 2011-2013.

Section 3: Analysis of Vietnam Cement Sector

Supply and Demand Analysis

Source: StoxPlus

This page is intentionally left blank

12

Section 3: Analysis of Vietnam Cement Sector

Supply and Demand Analysis

Supply-demand forecasting by region

Source: StoxPlus’ estimates and analysis; Cement Association

This page is intentionally left blank

13

Section 3: Analysis of Vietnam Cement Sector

3.1 Supply and Demand Analysis

3.2 Clinker and Cement Import-Export

3.3 Cement Distribution and Logistics

3.4 Sector concentration

Contents

14

Section 3: Analysis of Vietnam Cement Sector

Clinker and Cement Import-Export

Although export do not bring profit, some cement plants have to push up the export volume to cover

variable costs and absorb part of fixed costs

This page is intentionally left blank

15

Section 3: Analysis of Vietnam Cement Sector

Clinker and Cement Import-Export

Trading and logistics companies are active in the export segment. Some players such as Thang Long,

Chinfon, and Cam Pha have an export advantage due to easy access to sea ports.

This page is intentionally left blank

16

Section 3: Analysis of Vietnam Cement Sector

3.1 Supply and Demand Analysis

3.2 Clinker and Cement Import-Export

3.3 Cement Distribution and Logistics

3.4 Sector concentration

Contents

17

Section 3: Analysis of Vietnam Cement Sector

Cement Distribution and Logistics

Clinker and cement are transported from the North and Central to the South. Ocean shipping is the

preferred means of transportation due to large volume and low cost.

• Due to the over-supply of clinker in the North and Central and the shortage in

the South, cement transportation route is mostly from the North and Central

to the South via ocean shipping.

• Ocean shipping is the preferred means of transportation for clinker and

cement due to the large volume and low-cost (do not have to pay for tolls). To

organize efficient water transport, the necessary and sufficient condition is to

have the port as well as appropriate means of handling and transportation

infrastructure.

• Trucks are only effective within the operational radius of 150-250 km

(backhauling).

• Railway transport can only apply to plants near the cargo terminal (as transit

and handling costs are very expensive to load the materials on board).

Maximum volume transported by rail is also limited (max. 30 tons / carriage)

and above all, cargo transport is in the lowest priority order of rail transport.

Major logistics challenges

• Major issue with logistics is that ports of grinding stations cannot handle big

vessels (20,000 DWT and above). Grinding stations in the South are mostly

built along rivers, with sea ports access. Hence, most of the ports in the South

can only receive vessels 2,000-5,000 DWT.

• Even if major ports in the North can receive bigger ships and vessels, it is

more economically efficient for cement plants to transport directly to the

ports of grinding stations in the South, rather than having to transfer clinker

and cement twice.

Clinker

Grinding &

PackagingWarehouse

Thanh Hoa

CanTho/Vinh

Long

Hiep Phuoc –

HCM

Quang Ninh

Hai Phong

Quang Binh

Figure : Clinker & cement transportation routes

Source: StoxPlus’ Analysis

18

Section 3: Analysis of Vietnam Cement Sector

3.1 Supply and Demand Analysis

3.2 Clinker and Cement Import-Export

3.3 Cement Distribution and Logistics

3.4 Sector concentration

Contents

19

Section 3: Analysis of Vietnam Cement Sector

Sales strategies of key players

This page is intentionally left blank

20

Section 3: Price, Cost Structure and Financial Performance

3.1 Cement Price by Region and Trends

3.2 Cost Structure

3.3 Financial performance

Contents

21

Section 3: Price, Cost Structure and Financial Performance

Cement Price by Region and Trends

Domestic cement price has been on an upward trend due to rising cost of raw materials and energy

(coal and electricity)

This page is intentionally left blank

22

Cement price is the highest in the South (around US$75-83), while is the lowest in the North (around

US$60-65)

• Cement price is the highest in the South, and the lowest in the North.

The reason is due to the concentration of limestone and other raw

materials, and cost of freight from the North to the South.

Availability of limestone and other materials

• Most of cement plants located in the North because of availability of

materials. Limestone and clay are highly available in the North,

especially Quang Ninh, Ninh Binh and Thanh Hoa provinces

• In the South, there is no limestone. Clays are only available at Kien

Giang province, which is about 150km far from Ho Chi Minh City.

Freight from the North to the South

• Domestic clinker has been transported from the North and the Central

to the South for many years with remarkably high transportation

freight.

• The South also used to import clinker (e.g. from Thailand) with higher

price than domestic clinker, which increased the Southern historical

cement price.

• More specifically, cement price is the highest in the Central Highlands,

followed by Southeast region (including Ho Chi Minh, Ba Ria – Vung Tau,

Binh Duong, Dong Nai). Cement price is the lowest in Ninh Binh and Ha

Nam, as they have the highest concentration of cement plants.

Section 3: Price, Cost Structure and Financial Performance

Cement Price by Region and Trends

This part is intentionally left blank

23

Vietnam cement price is still much lower than neighbouring countries due to supply surplus and lack

of planning from the Government, leading to price dumping.

Section 3: Price, Cost Structure and Financial Performance

Cement Price by Region and Trends

This page is intentionally left blank

24

Section 3: Price, Cost Structure and Financial Performance

3.1 Cement Price by Region and Trends

3.2 Cost Structure

3.3 Financial Performance

Contents

25

0

5

10

15

20

25

30

35

Material Coal Electricity Maintenance Labor SG&A Other fixed Originalprice

New price Other fixed SG&A Labor Maintenance Electricity Coal Material

US$m

n

Clinker Cost Analysis

Figure : Clinker cost of production of a leading cement player in the Central region

Source: StoxPlus’ Analysis

Original cost of production Our cost analysis

Section 3: Price, Cost Structure and Financial Performance

Cost Structure

This page is intentionally left blank

26

Section 3: Price, Cost Structure and Financial Performance

3.1 Cement Price by Region and Trends

3.2 Cost Structure

3.3 Financial Performance

Contents

27

The EBITDA margin of Vietnam cement companies has been much lower than their peers in region like

Thailand, Indonesia or China. The reasons lay on high fuel cost structure and low utilization rate

Source: StoxPlus, International Cement Review

Figure : Vietnamese Cement EBITDA vs. Regional Players

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

2008 2009 2010 2011 2012 2013

PT Semen Indonesia Anhui Conch (China)

Siam Cement Group (Thailand) Vietnam listed cement plants

Section 3: Price, Cost Structure and Financial Performance

Financial Performance

This part is intentionally left blank

28

In 2013, most of listed cement companies had lower EBITDA than that of 2012 due to high increase in

input price like coal and electricity. Most of high EBITDA margin companies belong to Vicem and

foreign-owned group.

Section 3: Price, Cost Structure and Financial Performance

Financial Performance

This page is intentionally left blank

29

The average D/E ratio of listed cement companies has improved, standing at 2.4 times. Big

borrowings put a burden to cement companies and some of them go to bankrupt.

Section 3: Price, Cost Structure and Finance

Finance

This page is intentionally left blank

30

Nearly half of the listed cement companies got loss or broke even, only some companies had profit in

2013.

Section 3: Price, Cost Structure and Finance

Finance

This page is intentionally left blank

31

Reasons for high manufacturing costs and low profit of Vietnam cement plants

Low productivity rate

Due to the big surplus in cement supply, except some cement plants

in the South, most of Vietnam cement plants can not operate at full

capacity. The productivity rate for total cement plants in 2012 was

just around 77% in which cement plants in the North had productivity

rate of only around 63%. This caused high manufacturing costs and low

EBITDA margin for most Vietnam cement plants

This part is intentionally left blank

Late development

Vietnam cement sector developed later than Thailand by 10 years

and later than China by 20 years, so while cement plants of China

and Thailand nearly finished depreciation and paid back borrowings,

Vietnam cement plant has still been in the first stage with high

depreciation and loan interest costs.

Section 3: Price, Cost Structure and Finance

This part is intentionally left blank

This part is intentionally left blank

32

Section 4: Latest Policy Developments

4.1 Pricing Mechanism and Regulations

4.2 Taxes and Tariffs

4.3 Government Guarantee and Subsidies

4.4 Import-export Policies

4.5 WHRPG Requirement

Contents

33

Section 4: Latest Policy Developments

Pricing mechanism and regulations

The Government has eased its control of cement price in an attempt to develop a market-driven

pricing mechanism

Cement listed as goods subject to price declaration

• According to Law No. 11/2012/QH13, price declaration means

that the organizations and individuals shall send the price

notice of goods and services to competent governmental

agencies when determining and adjusting prices for goods and

services as required.

• Since 1 January 2014, cement is changed from products subject

to price stabilization to price declaration under Decree No.

177/2013/ND-CP. The price is allowed to follow the market

mechanism under the management of Government (the Price

Declaration mechanism).

How did the Price Stability Program work?

• VICEM had to propose an annual price adjustment timeline and

submit to the Government (Ministry of Finance) for approval.

• The Proposal needed to detail the price of each member of

VICEM. It consists of production cost and analysis on related

material inputs, existing cement price, planned cement price as

per the timeline, estimated revenue, contribution to State

budget, and Profit & Loss results.

• During the year, all price adjustments proposed by VICEM must

be agreed by the Price Management Department of Ministry of

Finance.

• In practice, the Price Management Department of Ministry of

Finance would work with the Government Office, the

Construction Material Department of Ministry of Construction

and the Vietnam National Cement Association (VNCA) to make

decision on any price adjustment proposed by cement

companies.

Cement price: regulatory roundup

• Under the Law on Price (Law No. 11/2012/QH13 dated 20 June 2012), the

Government shall manage the price under the market mechanism, respect

right of self-determination of price, the price competition of organizations

and individuals as prescribed by law.

• Decree No. 177/2013/ND-CP issued on 14 November 2013, cement is removed

from the list of goods and services subject to price stabilization, and moved

to list of goods and services subject to price declaration which include the

following:

− Cement and construction steel;

− Coal;

− Animal feed for cattle, poultry and fishery…;

− Printing paper and writing paper (roll), newsprint paper produced

domestically;

− Textbooks;

− Functional food for under-6-year-old children, etc.

How does the Price Declaration work?

• Starting in 2014, the Government has eased its control of cement price,

by replacing the Price Stability with Price Declaration program.

• Following the Decree No. 177/2013/ND-CP, the price notification must be

sent to competent authorities by manufacturing and business organizations

and individuals at least 5 days before the price determination or adjustment.

• Ministry of Finance (MOF), in collaboration with other related governmental

agencies and Prime Minister will consider to amend the list of goods and

services subject to price declaration, regarding the actual situation.

34

Section 4: Latest Policy Developments

4.1 Pricing mechanism and regulations

4.2 Taxes and Tariffs

4.3 Government Guarantee and Subsidies

4.4 Import-export Policies

4.5 WHRPG Requirement

Contents

35

Section 4: Latest Policy Developments

Taxes and Tariffs

The cement producers are obligated to pay different types of taxes and tariffs

Higher charge for the grant of mineral mining rights

• For the areas not subject to auction of mineral mining rights, containing coal,

limestone, and minerals being cement additives determined as the sources of

materials for cement plants project, cement producers shall have to pay the

fee for mineral mining licenses in accordance with Decree No. 203/2013/ND-

CP. Please refer to Appendix 3 for the calculation of charge.

Environmental Protection Tax (EPT)

• EPT is imposed on goods whose use is considered to have negative impact on

the environment. Please refer to Appendix 3 for the calculation of EPT.

• EPT rates of different types of coal are currently set at lower limit of the

standard reference range, implying that they are more likely to rise in the

future in line with growing interest in environmental issues.

Natural resources tax (NRT)

• NRT is imposed on the exploitation and use of natural resources including

metallic or non-metallic minerals, etc.

• NRT is calculated based on natural resource output used for royalty

calculation, royalty-liable price and royalty rate.

Increased transportation cost due to recent loading control policy

Figure : Environmental Protection Tax applied from Jan 2012

Figure : Natural resources tax rates applied since 1 Feb 2014

This part is intentionally left blank

This part is intentionally left blank

36

Section 4: Latest Policy Developments

4.1 Pricing mechanism and regulations

4.2 Taxes and Tariffs

4.3 Government Guarantee and Subsidies

4.4 Import-export Policies

4.5 WHRPG Requirement

Contents

37

Section 4: Latest Policy Developments

Government Guarantee and Subsidies

The Government no longer provides loan guarantee and material price subsidies to cement players

Foreign currency loan guarantee scheme

• Cement sector, as the core ingredient in construction sector, receives

many favors from the Government in borrowing capital especially from

foreign funds under guarantee of Government.

• From 1 Jan 2010 onwards, the Government guarantees for foreign loans

will be governed and construed in accordance with the Law No.

29/2009/QH12 and Decree No. 15/2011/ND-CP.

Government loan guarantee scheme for cement ceased already

• An alarming high level of public debts at 54.1% of GDP in 2013 (as

reported by MOF) in Vietnam has been debated at both National

Assembly’s sessions as well as local media. Among the public debt, loans

for cement sector guaranteed by the Government accounted for 8.96%.

• The Government recently decided not to provide guarantee for cement

loans. For example, Prime Minister, in an official letter issued in early

2014, rejected the request for foreign loan guarantee by Tan Thang

Cement Project.

Electricity Subsidies are no longer available and even a premium charge

is being proposed

• Previously in 2010, the cement and steel companies only had to pay

US$0.04/KWh, which equals to 57%-63% of export price, but costs

US$0.06/kWh, according to Ministry of Industry and Trade (“MoIT”),

meaning that Vietnam Electricity Group (EVN) inevitably incurred losses.

In fact, cement and steel industry, the two power-intensive sectors, were

said to enjoy total subsidy of US$120mn in 2010 only according to a

statement by the Minister of Finance, Mr. Vuong Dinh Hue.

• From 2012, it was proposed to reduce the level of subsidy and then

gradually cut off. Electricity selling price should be allowed to change in

accordance with market mechanism as stipulated in Decision No.

24/2011/QD-TTg & Circular No. 31/2011/TT-BCT.

• Since June 2013, MoIT has drafted a new retail electricity price schedule

in which cement and steel industries are discriminated from other

manufacturing sectors to be charged at higher price. Steel and cement

firms shall pay 2-16% higher than the current average retail price. Please

refer to Appendix 3 for the details.

Similarly, Coal Price Subsidies were stopped recently

• Players in four industries including thermal electricity, cement, paper,

and fertilizer used to enjoy a preferential coal price as its input material.

Specifically, it was equal to 70-80% of domestic market price and 50% of

export price in 2008.

• From early 2013, the coal price that cement companies were charged was

still lower than its production cost and that loss was covered by export

turnover. Therefore, the Government continued to discuss the roadmap

for further price hikes so that the coal price would be market-driven as

stipulated in Decree No. 177/2013/ND-CP.

Government loan guarantees for cement sector

• As of 31 Oct 2013, Vietnamese government guaranteed foreign loans

worth US$1.378bn for 17 cement projects, accounting for 8.96% of total

government-backed debts, according to Agency for Debt Management and

External Finance, MOF.

• There were four SOE projects including Dong Banh, Thai Nguyen, Tam

Diep and Hoang Mai which were in huge loss-making situations and on the

edge of bankruptcy. Their total debt was US$229mn and the MOF has

actually repaid the loans, assuming guarantor’s role.

• In a press release in 2012, MOF has announced that US$30-40 mn each

year will be spent on settling foreign debts for local cement producers

until 2018.

38

Section 4: Latest Policy Developments

4.1 Pricing mechanism and regulations

4.2 Taxes and Tariffs

4.3 Government Guarantee and Subsidies

4.4 Import-export Policies

4.5 WHRPG Requirement

Contents

39

Section 4: Latest Policy Developments

Import-export Policies

Cement industry looks to limit imports of clinker and cement to protect domestic producers

Legal basis

• The export tariff and preferential import tariff schedule changes annually. For the

year 2014, the MOF promulgated Circular No. 164/2013/TT-BTC on 15 Nov 2013.

Raw materials

• Main raw materials for cement production consist of Coal, Limestone, Clay, Iron

ore, and Gymsum. The export and import tariffs of these items have little changes

in some recent years.

Clinker and Cement

Table 42: Export-Import tax rate, 2014

This part is intentionally left blank

40

Section 4: Latest Policy Developments

4.1 Pricing mechanism and regulations

4.2 Taxes and Tariffs

4.3 Government Guarantee and Subsidies

4.4 Import-export Policies

4.5 WHRPG Requirement

Contents

41

Decision 1488/QD-TT approved The Master Plan in cement sector period 2011-2020

More stringent conditions for a new license:

• Decision 1488/QD-TT puts more strictly controls on new entrance by

setting various technical requirements:

- Capacity: minimum 2,500 tons of clinker per day

- Thermal energy consumption: Less than or equal to 730 Kcal/kg

clinker

- Electricity consumption: Less than or equal to 90kWh/ cement ton

- Emission dust concentration: Less than or equal to 30mg/Nm3

- Applying Waste Heat Gas Generator to meet at least 20% electricity

consumption.

• Investors are also required to have strong financial positions, with

minimum chartered capital of at least 20% of the project’s total

investment.

However, the Master Plan has not been strictly implemented

• The Master Plan also approved 27 new projects until 2015 with total

additional capacity of 31.68mn tons and will make total country capacity

increased to 94.24mn tons by 2015.

• However, most of those 27 projects were suspended or delayed due to

the economic downturn and financial shortage by the owner. We expect

those projects will be stopped or implemented after 2015. In 9month

2013, total country capacity was 75.9mn tons and we expect the total

country capacity in 2014 and 2015 to be 80.6mn tons instead of 94mn

tons as the Master Plan. (In 2014, Xuan Thanh 2 with capacity of 2.3mn

tons and Vissai Ha Nam with capacity of 2.4mn tons will finish its

construction and go in to operation)

Government indirectly control cement price through Vicem

• The Government still indirectly exercise the control over cement

price via VICEM. In general, all price increases proposed by VICEM

and other cement companies must be agreed by the Price

Management Department of Ministry of Finance.

• VICEM has raised its price by 6% in September 2013. However, the

sales price increase still not enough to cover the increase of coal

and electricity price.

Section 4: Latest Policy Developments

Decision 1488/QD-TT

42

Section 4: Latest Policy Developments

WHRPG Requirement

By 2014 end, all cement projects with a capacity of 2,500 tonnes of clinker per day must have

WHRPG system commissioned but only three of them complied with the regulation until now

About Waste Heat Recovery Power Generation (“WHRPG”) system

Regulation on WHRPG (under Decision No. 1488/QD-TTg)

• Projects already in operation or under construction with a capacity of

2,500 tons of clinker per day will be forced to complete the investment

in WHRPG systems by 31 Dec 2014 at the latest; and

• All new cement projects with a capacity of 2,500 tons of clinker per

day and above must be equipped with WHRPG, except for cement

production lines using industrial waste and other waste as fuel.

This part is intentionally left blank

WHRPG

43

Section 5: M&A Opportunities

Contents

44

Section 5: M&A Opportunities

Cement sector has been experiencing an active consolidation than ever in Vietnam by both among

domestic players and inbound transactions from giant regional players

Rationales for Consolidation

• The sector is very fragmented with many small scale plants for many

players along the country. Many of them run a cement plant for the

first time.

• Many State-owned enterprises such as the construction players

including Song Da Corporation and Vinaconex JSC under pressure by the

Government to divest their cement businesses as “non-core”. The

Government now allows a “loss-making sale” of a State-owned cement

plant i.e. below the par value.

• The Government has already allowed foreign investors to own cement

factories along with material mines (clay, limestone) in Vietnam such

as Gresik.

Detailed M&A Activity Review

• In 2012 only, we recorded 4 M&A transactions in the cement industry. A

highlight is that first inbound M&A deal (Indonesia's PT Semen Gresik

acquired Thang Long Cement Co. from Geleximco in a deal worth

US$230mn). Gresik is the largest State-owned cement group in

Indonesia. The main purpose of this acquisition is to gain access to

material mines in Vietnam and to export clinker back to Indonesia

(where demand for cement is in greater demand).

• Most active local buyer now is Viettel Group, the largest military-run

telecom provider. Viettel Group just acquired Cam Phan Cement JSC

from Vinaconex JSC and most recently Ha Long Cement JSC from Song

Da Corporation.

• The Vissai, a construction business, also appears as an active buyer.

They recently got approval of the Government to purchase entire stake

in Dong Banh Cement JS C, from the Construction Machinery

Corporation (COMA).

Key drivers

Key drivers for cement sector consolidation are:

• A number of foreign regional players are either eying or penetrating

into Cement sector including Siam Cement Group and WACEM (Africa).

• Not only cement but related businesses such as building materials and

infrastructure players are also getting exposure to Vietnam. Most

noticeable transactions are SCG Building Materials and Prime Group,

and Japan Pile Corp and Phan Vu Pile Corp.

• The Government policies with regard to foreign ownership have been

now eased not only in ownership in a cement business but also related

licensing matters for clays and limestone.

45

Opportunities for M&A in cement sector are obvious, however, successful M&A deal between

domestic cement plant and foreign investor requires not only efforts from both sides but also

supports from government.

Section 5: M&A Opportunities

This page is intentionally left blank

46

Section 6: Vietnam Macro Economy and Construction Overview

6.1 Vietnam Macro Economy

6.2 Vietnam Construction Industry

Contents

47

Section 6: Vietnam Macroeconomic and Construction Overview

Vietnam Economy

Vietnam economy has some initial recovery signals recently but how has the distressed economic

situation developed?

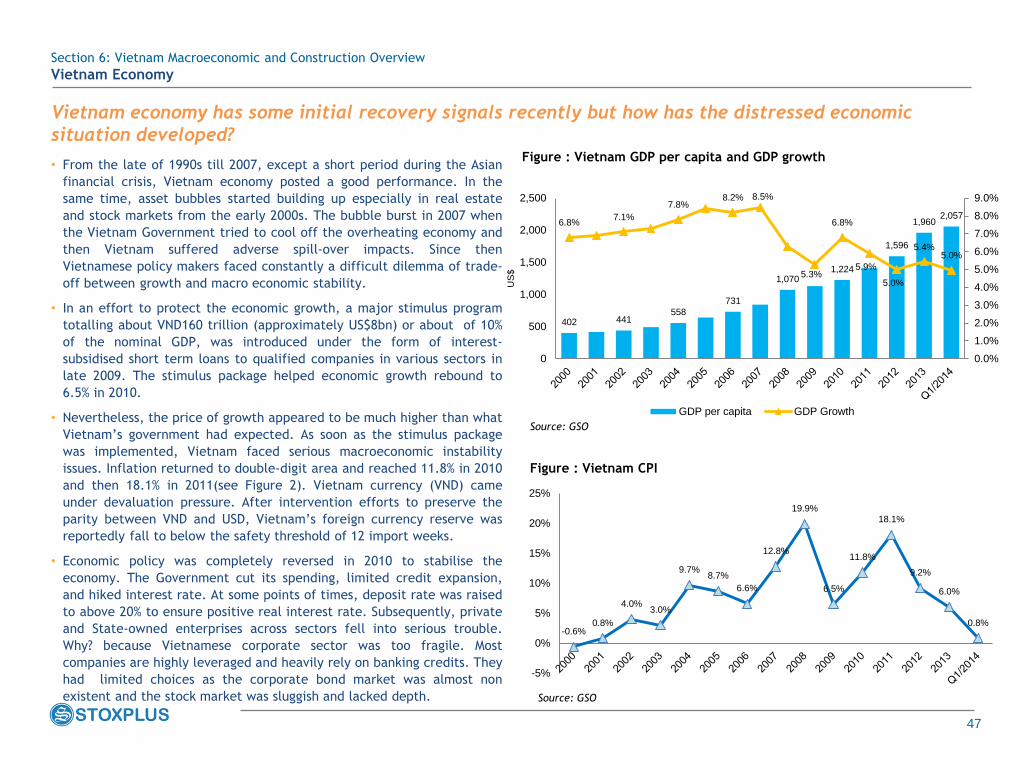

• From the late of 1990s till 2007, except a short period during the Asian

financial crisis, Vietnam economy posted a good performance. In the

same time, asset bubbles started building up especially in real estate

and stock markets from the early 2000s. The bubble burst in 2007 when

the Vietnam Government tried to cool off the overheating economy and

then Vietnam suffered adverse spill-over impacts. Since then

Vietnamese policy makers faced constantly a difficult dilemma of trade-

off between growth and macro economic stability.

• In an effort to protect the economic growth, a major stimulus program

totalling about VND160 trillion (approximately US$8bn) or about of 10%

of the nominal GDP, was introduced under the form of interest-

subsidised short term loans to qualified companies in various sectors in

late 2009. The stimulus package helped economic growth rebound to

6.5% in 2010.

• Nevertheless, the price of growth appeared to be much higher than what

Vietnam’s government had expected. As soon as the stimulus package

was implemented, Vietnam faced serious macroeconomic instability

issues. Inflation returned to double-digit area and reached 11.8% in 2010

and then 18.1% in 2011(see Figure 2). Vietnam currency (VND) came

under devaluation pressure. After intervention efforts to preserve the

parity between VND and USD, Vietnam’s foreign currency reserve was

reportedly fall to below the safety threshold of 12 import weeks.

• Economic policy was completely reversed in 2010 to stabilise the

economy. The Government cut its spending, limited credit expansion,

and hiked interest rate. At some points of times, deposit rate was raised

to above 20% to ensure positive real interest rate. Subsequently, private

and State-owned enterprises across sectors fell into serious trouble.

Why? because Vietnamese corporate sector was too fragile. Most

companies are highly leveraged and heavily rely on banking credits. They

had limited choices as the corporate bond market was almost non

existent and the stock market was sluggish and lacked depth.

Figure : Vietnam GDP per capita and GDP growth

Figure : Vietnam CPI

402 441558

731

1,0701,224

1,596

1,9602,057

6.8%7.1%

7.8%8.2% 8.5%

5.3%

6.8%

5.9%

5.0%

5.4%5.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

0

500

1,000

1,500

2,000

2,500

US

$

GDP per capita GDP Growth

-0.6%0.8%

4.0%3.0%

9.7%8.7%

6.6%

12.8%

19.9%

6.5%

11.8%

18.1%

9.2%

6.0%

0.8%

-5%

0%

5%

10%

15%

20%

25%

Source: GSO

Source: GSO

48

Section 6: Vietnam Macroeconomic and Construction Overview

Vietnam Economy

State Deficit has been increasing steadily since 2010. Meanwhile, State capital investment

expenditure decreases sharply, with a slight bounce back in 2013.

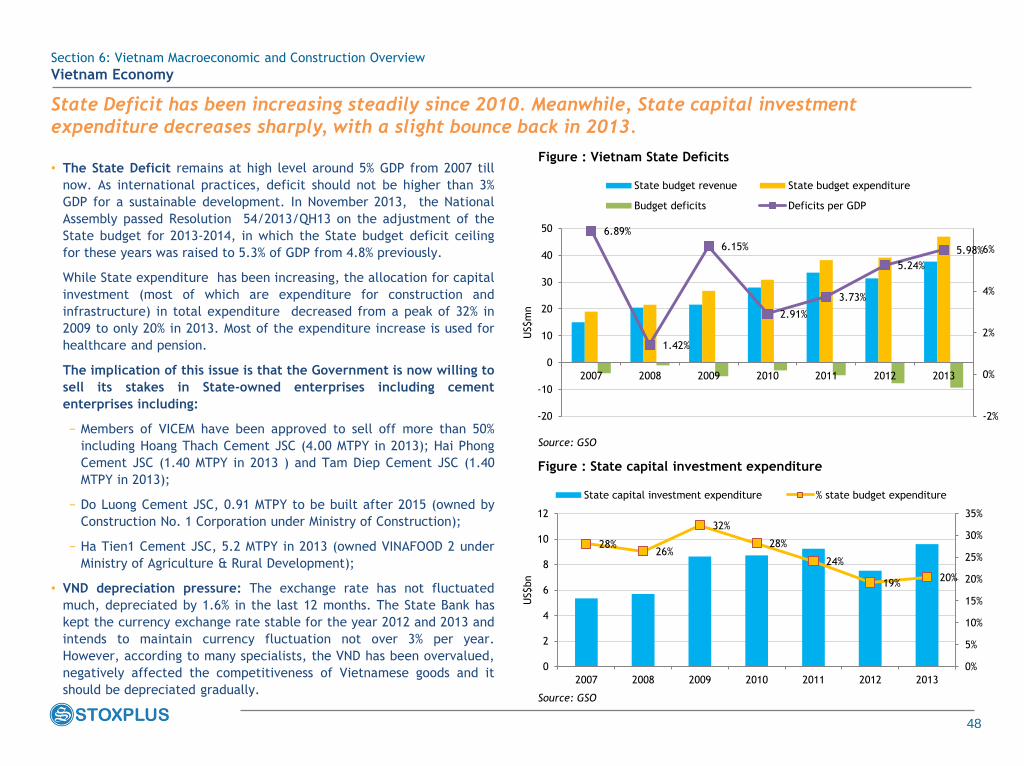

• The State Deficit remains at high level around 5% GDP from 2007 till

now. As international practices, deficit should not be higher than 3%

GDP for a sustainable development. In November 2013, the National

Assembly passed Resolution 54/2013/QH13 on the adjustment of the

State budget for 2013-2014, in which the State budget deficit ceiling

for these years was raised to 5.3% of GDP from 4.8% previously.

While State expenditure has been increasing, the allocation for capital

investment (most of which are expenditure for construction and

infrastructure) in total expenditure decreased from a peak of 32% in

2009 to only 20% in 2013. Most of the expenditure increase is used for

healthcare and pension.

The implication of this issue is that the Government is now willing to

sell its stakes in State-owned enterprises including cement

enterprises including:

− Members of VICEM have been approved to sell off more than 50%

including Hoang Thach Cement JSC (4.00 MTPY in 2013); Hai Phong

Cement JSC (1.40 MTPY in 2013 ) and Tam Diep Cement JSC (1.40

MTPY in 2013);

− Do Luong Cement JSC, 0.91 MTPY to be built after 2015 (owned by

Construction No. 1 Corporation under Ministry of Construction);

− Ha Tien1 Cement JSC, 5.2 MTPY in 2013 (owned VINAFOOD 2 under

Ministry of Agriculture & Rural Development);

• VND depreciation pressure: The exchange rate has not fluctuated

much, depreciated by 1.6% in the last 12 months. The State Bank has

kept the currency exchange rate stable for the year 2012 and 2013 and

intends to maintain currency fluctuation not over 3% per year.

However, according to many specialists, the VND has been overvalued,

negatively affected the competitiveness of Vietnamese goods and it

should be depreciated gradually.

6.89%

1.42%

6.15%

2.91%

3.73%

5.24%

5.98%

-2%

0%

2%

4%

6%

-20

-10

0

10

20

30

40

50

2007 2008 2009 2010 2011 2012 2013

US$m

n

State budget revenue State budget expenditure

Budget deficits Deficits per GDP

Figure : Vietnam State Deficits

28%26%

32%

28%

24%

19%20%

0%

5%

10%

15%

20%

25%

30%

35%

0

2

4

6

8

10

12

2007 2008 2009 2010 2011 2012 2013

US$bn

State capital investment expenditure % state budget expenditure

Figure : State capital investment expenditure

Source: GSO

Source: GSO

49

Section 6: Vietnam Macro Economy and Construction Overview

6.1 Vietnam Macro Economy

6.2 Vietnam Construction Industry

Contents

50

Section 6: Vietnam Macroeconomic and Construction Overview

Vietnam Construction Industry

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

2009 2010 2011 2012 2013

Total construction output Specialized construction services

Civil engineering works Non-residential buildings

Residential buildings

Figure : Growth rate of construction gross output by types of work

Source: GSO

Market sizing and growth potentials

This part is intentionally left blank

51

Thank to the golden age population with the urbanization rate up to 3% per year and high demand

for infrastructure development, the construction and infrastructure development sector has been

potential in long term.

Figure : Rural and Urban population growth rate

0.3% 0.3%0.0% 0.0% 0.0% -0.5%

0.5% 0.3%0.0%

3.2%3.0%

3.9%3.7% 3.7%

4.5%

2.1%2.5%

3.1%

1.1% 1.1% 1.1% 1.1% 1.1% 1.0% 1.0% 1.0% 1.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

2006 2007 2008 2009 2010 2011 2012 2013e 2014f

Rural growth rate Urban growth rate Population growth rate

Source: GSO and StoxPlus

Section 6: Vietnam Macroeconomic and Construction Overview

Vietnam Construction Industry

This part is intentionally left blank

52

Section 6: Vietnam Macroeconomic and Construction Overview

Vietnam Construction Industry

Infrastructure development: Vietnam would need to invest US$220bn until 2030

This page is intentionally left blank

53

There are 130 infrastructure projects in 2015-2020, compared with 71 remaining projects for 2010-

2015. Central region will have an increase in infrastructure in 2015-2020.

0 5 10 15 20 25 30 35 40 45

Airports

Oil & Gas Popelines

Ports

Power Plants and T&D

Railways

Roads & Bridges

Water

2015-2020 2010-2015

Figure : No. of major infrastructure projects, by timeframe (US$mn)

Source: StoxPlus

Figure : Distribution of infrastructure project during 2010-2015

Figure : Distribution of infrastructure project during 2015-2020

Source: StoxPlus

Source: StoxPlus

Central25%

North33%

South42%

Central31%

North20%

South49%

Section 6: Vietnam Macroeconomic and Construction Overview

Vietnam Construction Industry

54

The majority of projects within 2010-2015 are already under construction. Meanwhile, the status of

projects within 2015-2020 are still under planning stage and source of funding is a critical

Section 6: Vietnam Macroeconomic and Construction Overview

Vietnam Construction Industry

This page is intentionally left blank

55

Section 7: Appendices

7.1 Appendix 1: Cement plants under construction

7.2 Appendix 2: Major infrastructure projects

7.3 Appendix 3: Full list of cement plants to be built under period

2014-2030

7.4 Appendix 4: Factsheet of listed cement companies

Contents

56

Appendix 1: Cement plants under construction

Figure 27: Cement Plants under construction

Cement Plants Location Capacity (million

ton/year)

Situation

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

For full list of all cement plants to be built in the period 2013-2020, please see the Appendix 4

57

Section 7: Appendices

7.1 Appendix 1: Cement plants under construction

7.2 Appendix 2: Major infrastructure projects

7.3 Appendix 3: Full list of cement plants to be built under period

2014-2030

7.4 Appendix 4: Factsheet of listed cement companies

Contents

58

Appendix 2: Major infrastructure projects

This page is intentionally left blank

59

Appendix 2: Major infrastructure projects

This page is intentionally left blank

60

Appendix 2: Major infrastructure projects

This page is intentionally left blank

61

Appendix 2: Major infrastructure projects

This page is intentionally left blank

62

Appendix 2: Major infrastructure projects

This page is intentionally left blank

63

Appendix 2: Major infrastructure projects

This page is intentionally left blank

64

Section 7: Appendices

7.1 Appendix 1: Cement plants under construction

7.2 Appendix 2: Major infrastructure projects

7.3 Appendix 3: Full list of cement plants to be built under period

2014-2030

7.4 Appendix 4: Factsheet of listed cement companies

Contents

65

Appendix 3: Full list of cement plants to be built under period 2014-2030

This page is intentionally left blank

66

Section 7: Appendices

Contents

7.1 Appendix 1: Cement plants under construction

7.2 Appendix 2: Major infrastructure projects

7.3 Appendix 3: Full list of cement plants to be built under period

2014-2030

7.4 Appendix 4: Factsheet of listed cement companies

This section has been generated and automatically by StoxPlus using our database of more than 2000+ public companies in Vietnam. However, the

data has been reviewed thoughtfully by our data clerks and analysts.

67

Appendix 4: Fact sheet of listed cement companies

This page is intentionally left blank

68

Appendix 4: Fact sheet of listed cement companies

This page is intentionally left blank

69

Appendix 4: Fact sheet of listed cement companies

This page is intentionally left blank

70

Appendix 4: Fact sheet of listed cement companies

This page is intentionally left blank

71

Appendix 4: Fact sheet of listed cement companies

This page is intentionally left blank

72

Appendix 4: Fact sheet of listed cement companies

This page is intentionally left blank

73

Appendix 4: Fact sheet of listed cement companies

This page is intentionally left blank

74

Appendix 4: Fact sheet of listed cement companies

This page is intentionally left blank

75

Appendix 4: Fact sheet of listed cement companies

This page is intentionally left blank

76

Appendix 4: Fact sheet of listed cement companies

This page is intentionally left blank

77

Appendix 4: Fact sheet of listed cement companies

This page is intentionally left blank

Introduction about StoxPlus Corporation

and Research Capability

79

Overview about StoxPlus Research Services

Our Research division has been established as an

independent research house in Vietnam to provide local

insights to our clients at quality standards of the

World’s prestige advisory firms.

Our research team with a team of 5 experienced

analysts and researchers with CFA Charterholders,

ACCA Chartered Accountants and MBAs with extensive

experience in investment, banking, corporate finance

and technology with well respected firms in the United

Kingdom, Australia and Vietnam.

Our research services consists of

Standard research reports (ready for sales via our

website www.stoxresearch.com ); and

Customisable services based on specific

requirements

Our team covers all key sectors of Vietnam including

Financials, Logistics, Healthcare, Homebuilding, etc

Our research clients are mostly foreign institutional

investors and industry players who are penetrating into

Vietnam.

Selection of our Regular Research Clients:

80

Market Research Service

• Market understandings

• Market sizing & segmentation

• Market dynamics

• Industry analysis

• Customer segmentation

• Value chain analysis

• Regulatory and policy framework

• Key player profiles

Business Intelligence

• Key account profiling

• Competition analysis

• Commercial partner seeking

• Management background check

• Financial and operational due diligence

Market Entry Advisory

• Market assessment

• Market entry strategy defining

• Site location analysis

• Product and pricing strategy

• PPP/Joint ventures/M&A/licensing

• Vendors, outsourcers and distributors

search

Industries we regularly cover:

Financial Sector

• Vietnamese banking

• Retail banking and home

credit

• Insurance

• Brokerage

• Asset management

Healthcare Sector

• Hospital operation

• Drugs

• Medical devices

• Laboratory/medical testing

• Diagnostic imaging

Construction & others

• Home builders

• Cement and concrete

• Construction materials

• Infrastructure i.e. ports

• Real estates

• Natural rubbers

Consumerism

• Beers

• Soft drinks

• Alcoholic

• Pharmaceutical

• Education

About StoxPlus

We provide sector research reports for all key industries as well as comprehensive

analysis and local insights customized for your Vietnam market entry solutions. Our

research services include:

‹#›

If you have any question with regard to this Report, please

contact us:

Thuan Nguyen

CEO+84 (0) 35626962 (ext. 111)

+84 (0) 98398 0000

Hanoi Office

5th Floor, Indovina Bank Building

36 Hoang Cau Street

Hanoi, Vietnam

+ 84 (4) 3562 6962

Lan Nguyen

Research Associate+84 (0) 35626962 (ext. 108)