stock market in china - fdjpkc.fudan.edu.cn

TRANSCRIPT

Stock market in China

Jinfeng Ge

Fudan University

8 11th, 2017

Jinfeng Ge (Fudan University) Stock market in China 8 11th, 2017 1 / 38

Outline

Overview of China’s stock market.

Some special features of China’s stock market.

Jinfeng Ge (Fudan University) Stock market in China 8 11th, 2017 2 / 38

Number of firms

FE09CH10_Carpenter ARI 18 September 2017 12:24

ChiNext

SME board

Shenzhen main board

Shanghai main board

Other nontradable

Nontradable executiveor employee

Nontradable legal person

Nontradable state owned

Tradable mutual fund

Other tradable

a

b

500

0

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

1,000

1,500

2,000

2,500

3,000

3,500

Year

Year

0.5

0.0

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

0.0

10.0

20.0

30.0

40.0

50.0

60.0

Num

ber o

f lis

ted

firm

sM

arke

t cap

ital

izat

ion

(tri

llion

s of

RM

B)

Figure 1(a) Number of firms and (b) market capitalization of firms listed on China’s stock market, 1991–2016. (b) The time series of marketcapitalization is split at the year 2006 to accommodate a significant increase in scale. Figure adapted from Carpenter, Lu & Whitelaw(2017). Abbreviations: RMB, renminbi; SME, Small and Medium Enterprise.

The Split-Share Structure Reform of 2005 ushered in a second stage of privatization in China.As Li et al. (2011) and Liao, Liu & Wang (2014) explain, regulators and investors had becomeincreasingly aware of problems created by the split-share ownership structure, which weakenedminority shareholder protection and stifled the market for corporate control. After a number ofunsuccessful attempts to unlock nontradable shares, the CSRC devised a market mechanism tocompensate holders of tradable shares for potential adverse price impacts. Holders of nontradableshares in each firm would have to negotiate compensation to holders of tradable shares sufficientto secure their approval of the unlocking, which in turn would take place gradually over a periodof 1 year or longer. Most firms completed the reform by the end of 2007.

Liao, Liu & Wang (2014) use this reform as a natural experiment to measure the effect ofprivatization on firm performance. They find that the expectation of privatization boosted SOE

www.annualreviews.org • The Development of China’s Stock Market 237

Ann

u. R

ev. F

inan

c. E

con.

201

7.9:

233-

257.

Dow

nloa

ded

from

ww

w.a

nnua

lrev

iew

s.or

g A

cces

s pr

ovid

ed b

y St

ockh

olm

Uni

vers

ity -

Lib

rary

on

12/0

5/17

. For

per

sona

l use

onl

y.

Jinfeng Ge (Fudan University) Stock market in China 8 11th, 2017 3 / 38

The time series of market capitalization is split at the year2006 to accommodate a significant increase in scale

FE09CH10_Carpenter ARI 18 September 2017 12:24

ChiNext

SME board

Shenzhen main board

Shanghai main board

Other nontradable

Nontradable executiveor employee

Nontradable legal person

Nontradable state owned

Tradable mutual fund

Other tradable

a

b

500

019

9119

9219

9319

9419

9519

9619

9719

9819

9920

0020

0120

0220

0320

0420

0520

0620

0720

0820

0920

1020

1120

1220

1320

1420

1520

16

1,000

1,500

2,000

2,500

3,000

3,500

Year

Year

0.5

0.0

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

0.0

10.0

20.0

30.0

40.0

50.0

60.0

Num

ber o

f lis

ted

firm

sM

arke

t cap

ital

izat

ion

(tri

llion

s of

RM

B)

Figure 1(a) Number of firms and (b) market capitalization of firms listed on China’s stock market, 1991–2016. (b) The time series of marketcapitalization is split at the year 2006 to accommodate a significant increase in scale. Figure adapted from Carpenter, Lu & Whitelaw(2017). Abbreviations: RMB, renminbi; SME, Small and Medium Enterprise.

The Split-Share Structure Reform of 2005 ushered in a second stage of privatization in China.As Li et al. (2011) and Liao, Liu & Wang (2014) explain, regulators and investors had becomeincreasingly aware of problems created by the split-share ownership structure, which weakenedminority shareholder protection and stifled the market for corporate control. After a number ofunsuccessful attempts to unlock nontradable shares, the CSRC devised a market mechanism tocompensate holders of tradable shares for potential adverse price impacts. Holders of nontradableshares in each firm would have to negotiate compensation to holders of tradable shares sufficientto secure their approval of the unlocking, which in turn would take place gradually over a periodof 1 year or longer. Most firms completed the reform by the end of 2007.

Liao, Liu & Wang (2014) use this reform as a natural experiment to measure the effect ofprivatization on firm performance. They find that the expectation of privatization boosted SOE

www.annualreviews.org • The Development of China’s Stock Market 237

Ann

u. R

ev. F

inan

c. E

con.

201

7.9:

233-

257.

Dow

nloa

ded

from

ww

w.a

nnua

lrev

iew

s.or

g A

cces

s pr

ovid

ed b

y St

ockh

olm

Uni

vers

ity -

Lib

rary

on

12/0

5/17

. For

per

sona

l use

onl

y.

Jinfeng Ge (Fudan University) Stock market in China 8 11th, 2017 4 / 38

Normalized Real GDP for Large Countries 1991-2014

40

Figure 1. Normalized Real GDP in Large Countries by Year

This figure plots the normalized real GDP of China and other larger countries: United States, India, Brazil, and

Japan. The GDP data are in local currency and extracted from the World Bank database. The GDP values have been

adjusted for local inflation. The number is normalized to 1 in the starting year. Panel A and B plot the normalized

GDP of China and other larger countries for 1991-2014 and 2000-2014, respectively.

0

1

2

3

4

5

6

7

8

9

10

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

Panel A. Normalized Real GDP for Large Countries: 1991-2014

China United States India Brazil Japan

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Panel B. Normalized Real GDP of Large Countries: 2000-2014

China United States India Brazil Japan

Jinfeng Ge (Fudan University) Stock market in China 8 11th, 2017 5 / 38

Cumulative Annual Returns of Stock Indices in LargeCountries

41

Figure 2. Cumulative Annual Returns of Stock Indices in Large Countries

The figure plots the cumulative returns of the stock indices in large countries from 1992 to 2014. The indices are:

SSE Composite Index (China), S&P 500 (US), BSE Sensex (India), IBOV (Brazil) and Nikkei 225 (Japan). Annual

index return data are collected from Bloomberg. The nominal returns are in local currency and adjusted for local

inflation, measured by the year-end CPI. SSE and S&P 500 are value-weighted indices with total market

capitalization as the weight; SENSEX and IBOV are value-weighted indices with tradable shares’ market

capitalization as the weight. Nikkei is an equal-weighted index. SSE composite include all stocks listed in Shanghai

Stock Exchange. S&P 500, SENSEX, IBOV, and Nikkei include 500, 30, 50 and 225 stocks, respectively.

0

1

2

3

4

5

6

SSE China S&P500 US BSE SENSEX India

IBOV Brazil Nikkei Japan

Figure 3. Consumer Price Index (CPI) of China for 1992-2014

This figure plots the monthly CPI of China from January 1992 to March 2014. Monthly CPI data is collected from

National Bureau of Statistics (NBS) of China.

-5%

0%

5%

10%

15%

20%

25%

30%

Jan

, 19

92

Au

g, 1

99

2

Ma

r, 1

99

3

Oct

, 19

93

Ma

y, 1

99

4

Dec

, 19

94

Jul,

19

95

Feb

, 19

96

Sep

, 19

96

Ap

r, 1

99

7

No

v, 1

99

7

Jun

, 19

98

Jan

, 19

99

Au

g, 1

99

9

Ma

r, 2

00

0

Oct

, 20

00

Ma

y, 2

00

1

Dec

, 20

01

Jul,

20

02

Feb

, 20

03

Sep

, 20

03

Ap

r, 2

00

4

No

v, 2

00

4

Jun

, 20

05

Jan

, 20

06

Au

g, 2

00

6

Ma

r, 2

00

7

Oct

, 20

07

Ma

y, 2

00

8

Dec

, 20

08

Jul,

20

09

Feb

, 20

10

Sep

, 20

10

Ap

r, 2

01

1

No

v, 2

01

1

Jun

, 20

12

Jan

, 20

13

Au

g, 2

01

3

Ma

r, 2

01

4

Oct

, 20

14

CPI

Jinfeng Ge (Fudan University) Stock market in China 8 11th, 2017 6 / 38

Value-Weighted Buy-and-Hold Returns of Stocks Listed inLarge Countries

42

Figure 4. Value-Weighted Buy-and-Hold Returns of Stocks Listed in Large Countries

This figure plots the value-weighted buy-and-hold returns (BHR) of the stocks listed in China (A-Share), US, India,

Brazil and Japan. The BHRs are calculated by accumulating value-weighted annual returns of all stocks listed in the

country with the lagged-one-year market capitalization as the weight. The returns are adjusted for stock split and

include cash dividends. Nominal returns are adjusted for inflation to be converted to real returns. Inflation is

measured by the year-end CPI rate of the listing country. We set the BHR to be 1 in year 2000. We appreciate the

CAFR-Chinese stock market research project for sharing with us the stock return data of A-share listed firms. Stock

returns of US listed firms are from CRSP. Stock return data for firms listed in other large countries are extracted

from Datastream. Annual stock returns are denominated in local currency. The number of unique firms to make the

plot for China, US, Brazil, India, Japan and Chinese firms listed overseas is 2872, 9369, 867, 3436, 6510 and 758,

respectively.

0

0.5

1

1.5

2

2.5

3

3.5

4

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

China United States

India Brazil

Japan Chinese Firms Listed Overseas

Jinfeng Ge (Fudan University) Stock market in China 8 11th, 2017 7 / 38

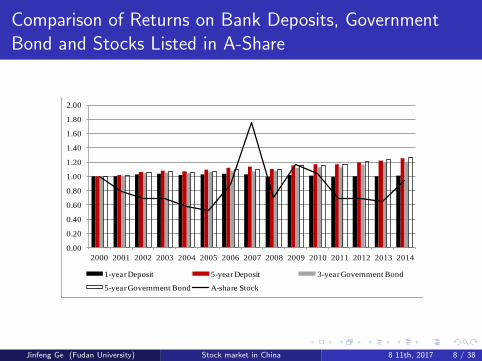

Comparison of Returns on Bank Deposits, GovernmentBond and Stocks Listed in A-Share

43

Figure 5. Comparison of Returns on Bank Deposits, Government Bond and Stocks Listed in A-Share

This figure plots the buy-and-hold returns on bank deposits, government bonds and stocks listed in China (A-Share).

The line represents the value-weighted buy-and-hold returns of stocks listed in Shanghai or Shenzhen stock

exchange, with the lagged-one-year market capitalization as the weight. The stock returns have been adjusted for

stock split and include cash dividends. The bars represent cumulative returns on 1-year and 5-year bank deposits,

and 3-year and 5-year government bonds in China. Nominal returns on bank deposits, government bonds and stocks

are adjusted for inflation (measured by the year-end inflation rate) to be converted to real returns. The deposit

interest rate and government bond yield data are extracted from the website of Peoples’ Bank of China (PBOC). If

the government bond is issued for multiple times in one year, we calculate the average yield of these issues and then

cumulate the mean return.

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

1-year Deposit 5-year Deposit 3-year Government Bond

5-year Government Bond A-share Stock

Jinfeng Ge (Fudan University) Stock market in China 8 11th, 2017 8 / 38

Operating Performance of Listed Firms and MatchedUnlisted Firms in China

44

Figure 6. Operating Performance of Listed Firms and Matched Unlisted Firms in China

This figure plots the value-weighted average ROA of listed firms and their one-to-one matched unlisted (private)

firms in China (A-Share), with year-end book assets as the weight. For each listed firm, we select from the sample of

unlisted firms the one with the closest book assets measured in the same year as the matching firm. Industry is

defined by the level-2 industry classification in Datastream. We require the book assets of the matching firm to be

within the [80%, 120%] range of the book assets of the listed firm. We exclude newly listed firms in each year. For

the period 1998-2013, 2767 distinct listed firms are matched with one unlisted firm each.

0.00

0.02

0.04

0.06

0.08

0.10

0.12

Listed Unlisted Matched

Jinfeng Ge (Fudan University) Stock market in China 8 11th, 2017 9 / 38

Comparison of Operating Performance of Listed Firmsbefore Special Treatment (/ST0) in China and ListedFirms before Delisting US

45

Figure 7. Comparison of Operating Performance of Listed Firms before Special Treatment (“ST”) in China

and Listed Firms before Delisting US

This figure plots the operating performance of firms listed in China (A-Share) in the [-5,0] year window before

receiving a “special treatment” (“ST”) and that of US listed firms before being delisted. Operating performance is

measured by ROA averaged across firms in the same window. Window 0 denotes the year when a firm becomes

special treated or delisted. “ST” firms in China include temporary ST and permanent ST. The former refers to firms

that ever received special treatment but later got their ST removed; the latter refers to firms that received special

treatment and never re-emerged from the special treatment later during the sample period. In total, there are 527

distinct “ST” firms in our sample, 82 of which are permanent “ST” firms. To make a sensible comparison, we allow

only permanent “ST” firms to enter the plot. For Chinese “ST” firms, window 0 refers to the year when the firm

becomes “ST”. For US delisted firm, window 0 refers to the delisting year, i.e., the year of last stock price available

or the year when the firm’s stock trading becomes inactive, depending on which date appeared later. We extract

delisting information for US listed firms from CRSP. CRSP document 6 major reasons for delisting: merger,

exchange, liquidation, being dropped, expire, and become foreign listed. We keep firms that are delisted for the

reason “liquidation” or “being dropped”. This leaves us 295 distinct firms that are delisted from US stock exchanges.

-0.30

-0.25

-0.20

-0.15

-0.10

-0.05

0.00

0.05

0.10

-5 -4 -3 -2 -1 0

China ST US Delisted due to Liquidation or Being Dropped

Jinfeng Ge (Fudan University) Stock market in China 8 11th, 2017 10 / 38

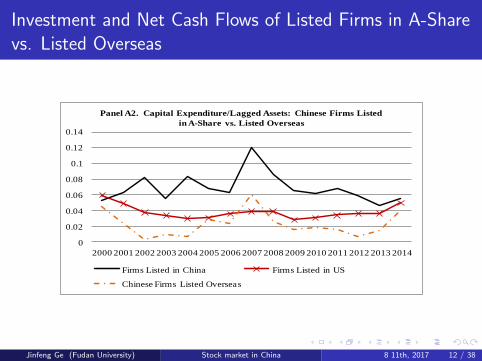

Investment and Net Cash Flows of Listed Firms in A-Sharevs. Listed in Other Large Countries

46

Figure 8. Investment and Net Cash Flows of Listed Firms in China and Other Large Countries

This figure plots the value-weighted average investment and net cash flows of listed firms in China (A-Share) and

other large countries by year. Panel A1 and A2 plot the average investment of listed firms. Investment is measured

by capital expenditure in year t scaled by the book assets in year t-1. Panel B1 and B2 plot the average net cash

flows of listed firms. Net cash flows are scaled by book assets. Net Cash Flow is calculated as EBITDA – Change in

Working Capital - Income Taxes – Capital Expenditure. Both the investment and cash flow measures are averaged

across firms with the year-end book assets as the weight. The sample is restricted to firms that have non-missing

data on EBITDA, capital expenditure, working capital, income taxes and book assets. In Panel A1 and B1, the

number of unique firms that enter the plot for China, US, India, Brazil and Japan is 2573, 7453, 3368, 799 and 6430,

respectively. In Panels A2 and B2, the number of unique Chinese firms listed overseas that enter the plot is 702.

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Panel A1. Capital Expenditure/Lagged Assets: Firms Listed in A-Share

vs. Listed in Other Large Countries

China United States India Brazil Japan

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Panel A2. Capital Expenditure/Lagged Assets: Chinese Firms Listed

in A-Share vs. Listed Overseas

Firms Listed in China Firms Listed in US

Chinese Firms Listed Overseas

Jinfeng Ge (Fudan University) Stock market in China 8 11th, 2017 11 / 38

Investment and Net Cash Flows of Listed Firms in A-Sharevs. Listed Overseas

46

Figure 8. Investment and Net Cash Flows of Listed Firms in China and Other Large Countries

This figure plots the value-weighted average investment and net cash flows of listed firms in China (A-Share) and

other large countries by year. Panel A1 and A2 plot the average investment of listed firms. Investment is measured

by capital expenditure in year t scaled by the book assets in year t-1. Panel B1 and B2 plot the average net cash

flows of listed firms. Net cash flows are scaled by book assets. Net Cash Flow is calculated as EBITDA – Change in

Working Capital - Income Taxes – Capital Expenditure. Both the investment and cash flow measures are averaged

across firms with the year-end book assets as the weight. The sample is restricted to firms that have non-missing

data on EBITDA, capital expenditure, working capital, income taxes and book assets. In Panel A1 and B1, the

number of unique firms that enter the plot for China, US, India, Brazil and Japan is 2573, 7453, 3368, 799 and 6430,

respectively. In Panels A2 and B2, the number of unique Chinese firms listed overseas that enter the plot is 702.

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Panel A1. Capital Expenditure/Lagged Assets: Firms Listed in A-Share

vs. Listed in Other Large Countries

China United States India Brazil Japan

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Panel A2. Capital Expenditure/Lagged Assets: Chinese Firms Listed

in A-Share vs. Listed Overseas

Firms Listed in China Firms Listed in US

Chinese Firms Listed Overseas

Jinfeng Ge (Fudan University) Stock market in China 8 11th, 2017 12 / 38

Net Cash Flow/Total Assets: Firms Listed in A-Sharevs.Listed in Other Large Countries

47

-0.02

-0.01

0

0.01

0.02

0.03

0.04

0.05

0.06

0.07

0.08

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Panel B1. Net Cash Flow/Total Assets: Firms Listed in A-Share vs.

Listed in Other Large Countries

China United States India Brazil Japan

-0.02

0.00

0.02

0.04

0.06

0.08

0.10

0.12

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Panel B2. Net Cash Flow/Total Assets: Chinese Firms Listed in A-Share

vs. Listed Overseas

Firms Listed in China Firms Listed in US Chinese Firms Listed Overseas

Jinfeng Ge (Fudan University) Stock market in China 8 11th, 2017 13 / 38

Net Cash Flow/Total Assets: Chinese Firms Listed inA-Share vs. Listed Overseas

47

-0.02

-0.01

0

0.01

0.02

0.03

0.04

0.05

0.06

0.07

0.08

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Panel B1. Net Cash Flow/Total Assets: Firms Listed in A-Share vs.

Listed in Other Large Countries

China United States India Brazil Japan

-0.02

0.00

0.02

0.04

0.06

0.08

0.10

0.12

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Panel B2. Net Cash Flow/Total Assets: Chinese Firms Listed in A-Share

vs. Listed Overseas

Firms Listed in China Firms Listed in US Chinese Firms Listed Overseas

Jinfeng Ge (Fudan University) Stock market in China 8 11th, 2017 14 / 38

Capital Expenditure/Lagged Assets around IPO

48

Figure 9. Investment and Net Cash Flows around IPO for Chinese vs. US Listed Firms

This figure plots the average investment and net cash flow of Chinese firms listed in mainland China (A-Share) and

Chinese firms listed overseas, and firms listed in the US around IPO. We require firms have non-missing capital

expenditure, net cash flows and total assets in the year prior to IPO. Investment is measured as capital expenditure

scaled by the lagged-one-year total assets. Net Cash Flow is calculated as EBITDA – Change in Working Capital -

Income Taxes – Capital Expenditure. Both the measures for investment and cash flows are averaged across firms

with year-end total assets as the weight. The number of firms listed in China, US and Chinese firms listed overseas

that enter the plot is 1599, 2749 and 483, respectively.

0

0.01

0.02

0.03

0.04

0.05

0.06

0.07

0.08

-1 0 1 2 3 4 5

Panel A. Capital Expenditure/Lagged Assets around IPO

Firms Listed in US Firms Listed in China

Chinese Firms Listed Overseas

0

0.01

0.02

0.03

0.04

0.05

0.06

0.07

0.08

0.09

-1 0 1 2 3 4 5

Panel B. Net Cash Flows/Total Assets around IPO

Firms Listed in US Firms Listed in China Chinese Firms Listed Overseas

Jinfeng Ge (Fudan University) Stock market in China 8 11th, 2017 15 / 38

Net Cash Flows/Total Assets around IPO

48

Figure 9. Investment and Net Cash Flows around IPO for Chinese vs. US Listed Firms

This figure plots the average investment and net cash flow of Chinese firms listed in mainland China (A-Share) and

Chinese firms listed overseas, and firms listed in the US around IPO. We require firms have non-missing capital

expenditure, net cash flows and total assets in the year prior to IPO. Investment is measured as capital expenditure

scaled by the lagged-one-year total assets. Net Cash Flow is calculated as EBITDA – Change in Working Capital -

Income Taxes – Capital Expenditure. Both the measures for investment and cash flows are averaged across firms

with year-end total assets as the weight. The number of firms listed in China, US and Chinese firms listed overseas

that enter the plot is 1599, 2749 and 483, respectively.

0

0.01

0.02

0.03

0.04

0.05

0.06

0.07

0.08

-1 0 1 2 3 4 5

Panel A. Capital Expenditure/Lagged Assets around IPO

Firms Listed in US Firms Listed in China

Chinese Firms Listed Overseas

0

0.01

0.02

0.03

0.04

0.05

0.06

0.07

0.08

0.09

-1 0 1 2 3 4 5

Panel B. Net Cash Flows/Total Assets around IPO

Firms Listed in US Firms Listed in China Chinese Firms Listed Overseas

Jinfeng Ge (Fudan University) Stock market in China 8 11th, 2017 16 / 38

Market-to-Book: Firms Listed in A-Share vs. Listed inOther Large Countries

49

Figure 10. Valuation of Firms Listed in China and Other Large Countries

This figure plots the aggregate market-to-book ratio of the firms listed in mainland China (A-Share) and firms listed

in other large countries. For each country, the aggregate market-to-book is calculated as the sum of market

capitalization of all stocks listed in this country divided by the sum of book equity of the same firms. To ensure

consistency of calculation of the numerator and denominator, we use stock-level book equity as the denominator for

firms that are listed in more than one market. Stock-level book equity as calculated as firm-level book equity

multiplied by the ratio of market capitalization of the stock listed in one country out of the total market capitalization

of the firm in all countries that the firm is listed in. In Panel A, the number of unique firms for China, US, India,

Brazil and Japan is 2662, 8467, 3333, 726 and 6432, respectively. In Panel B, the number of unique Chinese firms

listed overseas that enter the plot is 758.

0

1

2

3

4

5

6

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Panel A. Market-to-Book: Firms Listed in A-Share

vs. Listed in Other Large Countries

China United States India Brazil Japan

0

1

2

3

4

5

6

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Panel B. Market-to-Book: Chinese Listed in A-Share vs. Listed

Overseas

Firms Listed in China Chinese Firms Listed Overseas

Firms Listed in US

Jinfeng Ge (Fudan University) Stock market in China 8 11th, 2017 17 / 38

Market-to-Book: Chinese Listed in A-Share vs. ListedOverseas

49

Figure 10. Valuation of Firms Listed in China and Other Large Countries

This figure plots the aggregate market-to-book ratio of the firms listed in mainland China (A-Share) and firms listed

in other large countries. For each country, the aggregate market-to-book is calculated as the sum of market

capitalization of all stocks listed in this country divided by the sum of book equity of the same firms. To ensure

consistency of calculation of the numerator and denominator, we use stock-level book equity as the denominator for

firms that are listed in more than one market. Stock-level book equity as calculated as firm-level book equity

multiplied by the ratio of market capitalization of the stock listed in one country out of the total market capitalization

of the firm in all countries that the firm is listed in. In Panel A, the number of unique firms for China, US, India,

Brazil and Japan is 2662, 8467, 3333, 726 and 6432, respectively. In Panel B, the number of unique Chinese firms

listed overseas that enter the plot is 758.

0

1

2

3

4

5

6

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Panel A. Market-to-Book: Firms Listed in A-Share

vs. Listed in Other Large Countries

China United States India Brazil Japan

0

1

2

3

4

5

6

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Panel B. Market-to-Book: Chinese Listed in A-Share vs. Listed

Overseas

Firms Listed in China Chinese Firms Listed Overseas

Firms Listed in US

Jinfeng Ge (Fudan University) Stock market in China 8 11th, 2017 18 / 38

Chinese Stocks Listed in A-Share and in Overseas Markets

50

Table 1

Distribution of Firms Listed in China and Other Countries by Year

This table presents the summary statistics of firms listed in China and firms listed in other countries by year. Panel A

shows the distribution of Chinese listed firms in our sample by year. Columns 1 to 3 present the distribution for

Chinese firms listed in Shanghai or Shenzhen stock exchanges (“A-Share”). Columns 4 to 6 present the distribution

of firms headquartered in China and listed in overseas markets. Columns 2 and 5 report the number of state-owned

firms (SOE) listed in A-share and Chinese SOEs listed overseas. The state ownership information is extracted from

WIND under the data item “ultimate controller”. We define firms ultimately controlled by central SASAC (State-

owned Assets Supervision and Administration Commission of the State Council), local SASAC, Ministry of Finance,

and other government agency as state-owned firms. Columns 3 and 6 report the average book assets ($ billion) of

Chinese firms listed in A-Share and the average book assets of Chinese firms listed overseas, respectively. Panel B

presents the number of firms listed in other large countries by year, including US, India, Brazil and Japan.

Panel A. # of Chinese Stocks Listed in A-Share and in Overseas Markets

Firms Listed in A-Share Chinese Firms Listed Overseas

Year

# Listed

Firms

# of Listed

SOEs

Average Assets

($ Billion)

# Listed

Firms

# of Listed

SOEs

Average Assets

($ Billion)

(1) (2) (3)

(4) (5) (6)

2000 1041 779 0.25

51 46 1.32

2001 1123 844 0.31

65 47 2.68

2002 1192 900 0.37

80 47 2.42

2003 1255 796 0.43

97 53 2.63

2004 1343 820 0.46

128 62 3.02

2005 1340 813 0.51

167 70 3.32

2006 1418 823 0.69

203 80 8.48

2007 1522 841 0.98

268 102 17.03

2008 1577 858 1.07

337 111 17.47

2009 1723 873 1.20

384 123 19.04

2010 2071 910 1.25

431 131 21.28

2011 2300 902 1.31

490 133 27.40

2012 2464 943 1.35

534 141 31.40

2013 2465 1157 1.47

549 140 30.79

2014 2321 919 1.76 661 172 34.43

Panel B. # of Stocks Listed in Other Large Countries

Year United States India Brazil Japan

2000 6614 606 417 2909

2001 6369 688 379 3065

2002 6179 724 370 3103

2003 6109 877 390 3183

2004 5958 1109 432 3239

2005 5847 1303 431 3284

2006 5613 2517 432 3263

2007 5358 2644 436 3234

2008 5268 2725 424 3175

2009 5232 2758 413 3117

2010 5183 2730 408 3040

2011 5077 2715 386 2970

2012 4852 2652 351 2896

2013 4665 2999 535 2711

2014 4717 2876 506 2696

Total 9369 3436 867 6510

Jinfeng Ge (Fudan University) Stock market in China 8 11th, 2017 19 / 38

Correlation between 5-Year Stock Returns and Future GDPGrowth

51

Table 2

Correlation between 5-Year Stock Returns and Future GDP Growth

This table reports the Pearson correlation between 5-year stock returns and the future GDP growth in that country

for the top 20 countries according to the IMF GDP ranking in 2014. We include South Africa in addition to the top

20 countries. We calculate the correlation for 1991-2014, or for a period starting from the year when the stock return

data become available in our dataset and ending at 2014, if the first stock return data are available after 1991. The

correlation is estimated using cumulative stock returns of a 5-year interval and the cumulative GDP growth in the

next 5-year interval (so we get stock returns for year t, t+5, ….and GDP growth for year t+1, t+6, …), back from

2014 on a rolling basis. Country-level stock returns are calculated as value-weighted stock returns of individual

stocks listed in a country, with the lagged one year market capitalization as the weight. The last row tests the

difference in the correlation coefficients of China and developed countries as a group, and the difference of China

and other emerging countries as a group. We use the OECD Classification to define developed and emerging

countries. Emerging countries include China, Brazil, Russian Federation, India, Mexico, Indonesia, Turkey and

Saudi Arabia. We do not have individual stock return data for South Korea so we calculate the correlation using the

stock market index (KOSPI Korea). For Saudi Arabia, the stock market index data are available for a longer period

than individual stock return data in our sample, so we report the correlation calculated from the stock market index

(the DFMGI Index). ***, ** and * denote the statistical significance at 1%, 5% and 10% levels.

IMF GDP

Ranking Country

Individual Stock

or Index Returns

Sample

Period Correlation

p-

value

1 United States Stock Return 1991-2014 0.565*** 0.004

2 China Stock Return 1991-2014 0.012 0.958

3 Japan Stock Return 1991-2014 0.418** 0.046

4 Germany Stock Return 1991-2014 0.697*** <0.001

5 United Kingdom Stock Return 1991-2014 0.322 0.133

6 France Stock Return 1991-2014 0.602*** 0.003

7 Brazil Stock Return 1995-2014 0.560** 0.012

8 Italy Stock Return 1991-2014 0.286 0.195

9 India Stock Return 1991-2014 0.573*** 0.006

10 Russian Federation Stock Return 1996-2014 0.547** 0.032

11 Canada Stock Return 1991-2014 0.524** 0.014

12 Australia Stock Return 1991-2014 0.469** 0.023

13 South Korea Index Return 1991-2014 -0.156 0.793

14 Spain Stock Return 1991-2014 0.593*** 0.002

15 Mexico Stock Return 1991-2014 0.322 0.143

16 Indonesia Stock Return 1991-2014 0.349 0.121

17 Netherlands Stock Return 1991-2014 0.735*** <0.001

18 Turkey Stock Return 1991-2014 0.414* 0.054

19 Saudi Arabia Index Return 1995-2014 0.196 0.524

20 Switzerland Stock Return 1991-2014 0.288 0.182

1 South Africa Stock Return 1991-2014 0.619*** 0.002

Chinese Stocks Listed

Overseas Stock Return 1991-2014 0.414* 0.069

Difference Group

Mean of

Correlation China

Difference

(Other

p-

Value

Countries-

China)

Developed 0.568 0.012 0.556*** <0.001

Emerging 0.567 0.012 0.555*** <0.001

Jinfeng Ge (Fudan University) Stock market in China 8 11th, 2017 20 / 38

Level and Growth of Net Income of Chinese Firms bySector

52

Table 3

Level and Growth of Net Income of Chinese Firms by Sector

This table reports the level and growth of net income generated by industrial sector in China. We group all industrial

firms into state-owned enterprises (SOEs) and non-state-owned enterprises (non-SOEs). Within the SOE group and

the non-SOE group, we further distinguish firms to Listed SOE, Unlisted SOE, Listed Non-SOE and Unlisted Non-

SOE. Panel A reports the proportions of the aggregate net income of each group out of the aggregated net income of

all industrial firms, listed or unlisted industrial firms in China. Panel B reports the aggregate net income growth rate

of each group. We calculate aggregate net income growth for each group as the increase in net income aggregated

across firms of this group from year t-1 to year t, scaled by the total net income generated by the same group of

firms in year t-1. The bottom row of Panel B reports the Pearson correlations between the net income growth rate of

each group of firms and the contemporaneous GDP growth rate in China. We extract net income data for all

industrial firms and those for SOEs from the statistical yearbook of National Bureau of Statistics (NBS). ***, ** and

* denote statistical significance at 1%, 5% and 10% level, respectively.

Panel A. Net Income Percentage of Chinese Firms Listed in A-Share

Year SOE/All Listed/All Listed SOE/Listed All

Unlisted Non-

SOE/Unlisted All

(1) (2) (3) (4)

2000 53.74% 35.10% 89.94% 65.84%

2001 49.03% 24.96% 94.50% 66.09%

2002 44.10% 24.23% 90.71% 70.81%

2003 43.66% 25.42% 88.31% 71.55%

2004 41.41% 25.85% 89.85% 75.47%

2005 39.58% 23.72% 92.46% 76.87%

2006 39.92% 22.15% 90.26% 74.40%

2007 36.63% 21.20% 86.68% 76.84%

2008 27.98% 17.45% 85.02% 84.07%

2009 26.02% 15.73% 80.97% 84.24%

2010 27.34% 15.14% 79.88% 82.04%

2011 25.65% 14.42% 77.43% 83.08%

2012 23.48% 13.70% 78.17% 85.20%

2013 21.25% 17.62% 79.20% 91.14%

2014 20.01% 19.32% 75.55% 82.31%

Panel B. Net Income Growth of Chinese Firms by Sector

Year All Listed Unlisted Listed SOE

Listed Non-

SOE

Unlisted

Non-SOE

(1) (2) (3) (4) (5) (6)

2001 0.060 -0.246 0.225 -0.208 -0.588 0.23

2002 0.217 0.182 0.229 0.134 0.998 0.317

2003 0.474 0.546 0.451 0.505 0.944 0.466

2004 0.424 0.448 0.415 0.473 0.257 0.493

2005 0.243 0.141 0.279 0.174 -0.152 0.302

2006 0.336 0.247 0.363 0.217 0.611 0.319

2007 0.408 0.349 0.426 0.295 0.843 0.472

2008 0.128 -0.071 0.182 -0.089 0.044 0.294

2009 0.145 0.031 0.168 -0.018 0.311 0.171

2010 0.552 0.494 0.563 0.474 0.579 0.522

2011 0.15 0.095 0.159 0.061 0.229 0.174

2012 0.005 -0.045 0.014 -0.036 -0.077 0.04

2013 0.104 0.42 0.054 0.439 0.353 0.128

2014 0.019 0.064 -0.063 -0.01 0.22 0.034

Average 0.233 0.188 0.247 0.172 0.327 0.283

Correlation Coefficient 0.687*** 0.390 0.713*** 0.361 0.411 0.627**

P-Value 0.007 0.168 0.004 0.204 0.144 0.022

Jinfeng Ge (Fudan University) Stock market in China 8 11th, 2017 21 / 38

Net Income Growth of Chinese Firms by Sector

52

Table 3

Level and Growth of Net Income of Chinese Firms by Sector

This table reports the level and growth of net income generated by industrial sector in China. We group all industrial

firms into state-owned enterprises (SOEs) and non-state-owned enterprises (non-SOEs). Within the SOE group and

the non-SOE group, we further distinguish firms to Listed SOE, Unlisted SOE, Listed Non-SOE and Unlisted Non-

SOE. Panel A reports the proportions of the aggregate net income of each group out of the aggregated net income of

all industrial firms, listed or unlisted industrial firms in China. Panel B reports the aggregate net income growth rate

of each group. We calculate aggregate net income growth for each group as the increase in net income aggregated

across firms of this group from year t-1 to year t, scaled by the total net income generated by the same group of

firms in year t-1. The bottom row of Panel B reports the Pearson correlations between the net income growth rate of

each group of firms and the contemporaneous GDP growth rate in China. We extract net income data for all

industrial firms and those for SOEs from the statistical yearbook of National Bureau of Statistics (NBS). ***, ** and

* denote statistical significance at 1%, 5% and 10% level, respectively.

Panel A. Net Income Percentage of Chinese Firms Listed in A-Share

Year SOE/All Listed/All Listed SOE/Listed All

Unlisted Non-

SOE/Unlisted All

(1) (2) (3) (4)

2000 53.74% 35.10% 89.94% 65.84%

2001 49.03% 24.96% 94.50% 66.09%

2002 44.10% 24.23% 90.71% 70.81%

2003 43.66% 25.42% 88.31% 71.55%

2004 41.41% 25.85% 89.85% 75.47%

2005 39.58% 23.72% 92.46% 76.87%

2006 39.92% 22.15% 90.26% 74.40%

2007 36.63% 21.20% 86.68% 76.84%

2008 27.98% 17.45% 85.02% 84.07%

2009 26.02% 15.73% 80.97% 84.24%

2010 27.34% 15.14% 79.88% 82.04%

2011 25.65% 14.42% 77.43% 83.08%

2012 23.48% 13.70% 78.17% 85.20%

2013 21.25% 17.62% 79.20% 91.14%

2014 20.01% 19.32% 75.55% 82.31%

Panel B. Net Income Growth of Chinese Firms by Sector

Year All Listed Unlisted Listed SOE

Listed Non-

SOE

Unlisted

Non-SOE

(1) (2) (3) (4) (5) (6)

2001 0.060 -0.246 0.225 -0.208 -0.588 0.23

2002 0.217 0.182 0.229 0.134 0.998 0.317

2003 0.474 0.546 0.451 0.505 0.944 0.466

2004 0.424 0.448 0.415 0.473 0.257 0.493

2005 0.243 0.141 0.279 0.174 -0.152 0.302

2006 0.336 0.247 0.363 0.217 0.611 0.319

2007 0.408 0.349 0.426 0.295 0.843 0.472

2008 0.128 -0.071 0.182 -0.089 0.044 0.294

2009 0.145 0.031 0.168 -0.018 0.311 0.171

2010 0.552 0.494 0.563 0.474 0.579 0.522

2011 0.15 0.095 0.159 0.061 0.229 0.174

2012 0.005 -0.045 0.014 -0.036 -0.077 0.04

2013 0.104 0.42 0.054 0.439 0.353 0.128

2014 0.019 0.064 -0.063 -0.01 0.22 0.034

Average 0.233 0.188 0.247 0.172 0.327 0.283

Correlation Coefficient 0.687*** 0.390 0.713*** 0.361 0.411 0.627**

P-Value 0.007 0.168 0.004 0.204 0.144 0.022

Jinfeng Ge (Fudan University) Stock market in China 8 11th, 2017 22 / 38

Potential listing venues for Chinese firmsFE09CH10_Carpenter ARI 18 September 2017 12:24

Table 1 Potential listing venues for Chinese firms

SSE SZSE SEHK NYSE NASDAQ

Legal costs Low Low Medium High High

Dual class permitted No No No Yes Yes

Earnings/sizerequirement

Strict positiveearningsthreshold for3 consecutiveyears

Strict positive earningsthreshold for3 consecutive years formain board, softerthresholds for SMEand ChiNext boards

Softer 3-yearearningsthreshold

Softer 3-yearearnings or sizethreshold

Even softerearnings or sizethreshold

Selectionmechanism

IB sponsorshipand CSRCapproval

IB sponsorship andCSRC approval

IB sponsorship Registrationbased

Registrationbased

Average processingtime

10 months 10 months 6 months 4 months 4 months

Total marketcapitalization,August 2016(trillions ofdollars)

4.0 3.2 3.2 19.3 9.1

Parent company CSRC CSRC HK Exchangesand ClearingLimited

IntercontinentalExchange

The NasdaqOMX Group

Year founded 1990 1990 1891 1792 1971

Number of listedcompanies, August2016

1,114 1,796 1,925 3,176 3,170

Abbreviations: CSRC, China Securities Regulatory Commission; IB, investment bank; NYSE, New York Stock Exchange; SEHK, Stock Exchange ofHong Kong; SME, Small and Medium Enterprise; SSE, Shanghai Stock Exchange; SZSE, Shenzhen Stock Exchange.

Table 1 summarizes the listing requirements, legal costs, processing time, and number andsize of Chinese firms for mainland, Hong Kong, and US exchanges. Whereas listing in Chinais least expensive, incorporating overseas is generally most expensive because it requires foreignlegal counsel, particularly when the firm uses a complex variable interest entity structure to by-pass Chinese restrictions on foreign direct investment in strategic industries. Therefore, foreignincorporation is generally an option only for larger firms. Requirements on prelisting net incomealso vary across exchanges. The SSE is strictest, requiring 3-year cumulative net profits in excessof RMB 30 million, whereas the NASDAQ is the most tolerant, allowing negative earnings forfirms that meet other criteria. Finally, governance requirements also vary across exchanges. TheUS exchanges allow dual-class structures with differential voting rights, whereas the Hong Kongand Chinese exchanges do not.

In addition to differential listing requirements, Chinese firms may also consider longer-termeffects of listing choice. Evidence from the literature on cross-listing on US exchanges providessome insights: Compared to firms that do not cross-list, firms that cross-list exhibit lower votingpremia and thus better minority shareholder protection; are more likely to terminate poorlyperforming CEOs; and have higher Tobin’s Q, lower cost of capital, and larger stock return and

www.annualreviews.org • The Development of China’s Stock Market 241

Ann

u. R

ev. F

inan

c. E

con.

201

7.9:

233-

257.

Dow

nloa

ded

from

ww

w.a

nnua

lrev

iew

s.or

g A

cces

s pr

ovid

ed b

y St

ockh

olm

Uni

vers

ity -

Lib

rary

on

12/0

5/17

. For

per

sona

l use

onl

y.

Jinfeng Ge (Fudan University) Stock market in China 8 11th, 2017 23 / 38

EQUITY PRICING

The A-Share Premium Puzzle

Information Asymmetry and Behavioral Effects

Stock Price Informativeness

Cross-Sectional Patterns in Returns

Jinfeng Ge (Fudan University) Stock market in China 8 11th, 2017 24 / 38

The A-Share Premium Puzzle

FE09CH10_Carpenter ARI 18 September 2017 12:24

are negatively correlated with the relative supply of A shares and positively correlated with thesupply of B shares. Chan, Menkveld & Yang (2008) provide an explanation based on informationasymmetry within the A-share market and find that traditional measures of information asymmetryhelp to explain the cross section of A-share premia.

Mei, Scheinkman & Xiong (2009) use the dual-class structure to test the theory that speculativetrading in the presence of short-sales constraints can lead to overvaluation (Miller 1977; Harrison& Kreps 1978; Chen, Hong & Stein 2002; Scheinkman & Xiong 2003). They view B-share pricesas controls for stock fundamentals and find that A-share premia are cross-sectionally correlatedwith turnover rates and idiosyncratic return volatility, proxies for speculative motives in trading.In 2001, the CSRC allowed domestic Chinese investors to hold B shares, which brought B-sharediscounts down to 40%, according to Karolyi, Li & Liao (2009). They find that the firms with thegreatest declines in B-share discounts were those with the lowest state ownership and concludethat political risk is an important determinant of the price differential.

With the introduction of the QFII program in 2002, which allows qualified foreign institutionalinvestors to directly hold A shares, B-share issuance and trading has largely died out. However,A-share premia over corresponding H shares with identical cash flow and voting rights are stillprevalent for firms that are dual-listed in mainland China and Hong Kong. Figure 2 shows thetime series of the median A-H premium, i.e., A-share price divided by H-share price, for the fullsample of dual-listed firms, as well as for firms in the lower half of this sample as ranked by marketcapitalization (i.e., smaller firms) and for firms in the financial and manufacturing sectors, since2006. The full-sample median has been about 1.5 or 2 in recent years, but was over 3 in 2009and peaked in the 10–15 range in the late 1990s and early 2000s. The median A-H premium forsmaller firms is consistently higher than for larger firms, possibly reflecting the shell value of alisting on the domestic Chinese stock market that could potentially be acquired by a firm seekingto circumvent the usual listing process for A shares. A-H premia are consistently higher for firms

0.0

1.0

0.5

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0Ja

n 20

06

May

200

6

Sep

2006

Jan

2007

May

200

7

Sep

2007

Jan

2008

May

200

8

Sep

2008

Jan

2009

May

200

9

Sep

2009

Jan

2010

May

201

0

Sep

2010

Jan

2011

May

201

1

Sep

2011

Jan

2012

May

201

2

Sep

2012

Jan

2013

May

201

3

Sep

2013

Jan

2014

May

201

4

Sep

2014

Jan

2015

May

201

5

Sep

2015

Jan

2016

All firms

Small firms

Financial and insurance sectors

Manufacturing sector

Date

A-s

hare

pre

miu

m(A

-sha

re p

rice

/H-s

hare

pri

ce)

Figure 2Median A-share premium, i.e., A-share price divided by H-share price, 2006–2016. Shown are the full sample of firms with dual listingsof A shares in Shanghai or Shenzhen and H shares in Hong Kong (blue); the half of this sample containing smaller firms (orange); firmsin the financial and insurance sectors ( green); and firms in the manufacturing sector ( purple).

www.annualreviews.org • The Development of China’s Stock Market 243

Ann

u. R

ev. F

inan

c. E

con.

201

7.9:

233-

257.

Dow

nloa

ded

from

ww

w.a

nnua

lrev

iew

s.or

g A

cces

s pr

ovid

ed b

y St

ockh

olm

Uni

vers

ity -

Lib

rary

on

12/0

5/17

. For

per

sona

l use

onl

y.

Jinfeng Ge (Fudan University) Stock market in China 8 11th, 2017 25 / 38

Information Asymmetry and Behavioral Effects I

Brennan and Cao (1997) show nearby investors are better informedthan those farther away, and will thus react less to information andwill execute trades of opposite sign, they find that trades of investorsacross branches within a given region are positively correlated andthat trades across regions are negatively correlated

Jia, Wang and Xiong (2015) study the reactions of A- and H-shareprices of dual-listed stocks to analysts.revisions of earnings forecastsand find that A-share prices react more strongly to revisions fromlocal, mainland-based analysts, whereas H-share prices react morestrongly to revisions from foreign analysts. They attribute this resultto investors.greater trust in analysts from their home region,associated with social and cultural factors such as those studied byGuiso, Sapienza and Zingales (2008, 2009)

Jinfeng Ge (Fudan University) Stock market in China 8 11th, 2017 26 / 38

Information Asymmetry and Behavioral Effects II

Andrade, Bian and Burch (2013) identify China.s stock market as anatural setting for the study of asset price bubbles generated bydispersion in investor beliefs because of its short-sale constraints andthe dominance of retail investors. Focusing on the 2007 stock pricebubble, they find that stocks with greater analyst coverage hadsmaller bubbles, attributing this to analysts.coordinating beliefs.

Hong et al. (2014) exploit the uneven rise in household wealth andthe growth of the middle class across Chinese regions over the period1998õ2012 to test for evidence of keeping-up-with-the-Jonesespreferences and trading for status concerns. They use a province orcity.s GDP per capita as a proxy for status concerns and use thedifference between small and large stock turnover as a proxy for localstock turnover. They show that investors in regions that becamericher faster traded more actively in small local stocks

Jinfeng Ge (Fudan University) Stock market in China 8 11th, 2017 27 / 38

Stock Price Informativeness I

The framework by Roll (1988): R-squared and the Economy.

Capital Asset Pricing Model (CAPM), represents the expected returnof stock j as

rj ,t = rf + βj (rm,t − rf )

where rm,t is the return on a fully diversified portfolio of assets and rfis the risk-free return. The coefficient βj relates the stock’s return tothe sole pricing factor, the equity risk premium

Using Market Model regressions of the form

rj ,t = αj + βj rm,t + ej ,t

where ej ,t is the residual component of stock j ’s return not explainedby the equity risk premium and and αj = βj (1 − rf ) is non-stochastic

Jinfeng Ge (Fudan University) Stock market in China 8 11th, 2017 28 / 38

Stock Price Informativeness II

Variance decomposition

Variance (rj ,t) = Variance (βj rm,t) + Variance (ej ,t)

where Variance (βj rm,t) is the market-wide variation in the stock’sreturn and Variance (ej ,t) is the firm-specific variation in its return

Roll (1988) notes that the regression R-square measures both thegoodness of fit of the Market Model for stock j.s returns data andthe fraction of the variation in stock j.s return related tomarket-wide fluctuations. A lower R-square merely means that moreof the variation in stock j.s price is firm-specific õthe stock.sreturns are less synchronous with the overall market.

Jinfeng Ge (Fudan University) Stock market in China 8 11th, 2017 29 / 38

US Stock Comovement, 1926 õ2010

6

Figure 1. US Stock Comovement, 1926 – 2010 Panel A. R-squared is the mean of the R2s of Market Model regressions of each US stock’s weekly (Weds.-to-Weds.) total return of the CRSP value-weighted market return. Means are weighted by either total return variation or market capitalization.

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

55%

60%

65%

70%

75%

19

26

19

28

19

30

19

32

19

34

19

36

19

38

19

40

19

42

19

44

19

46

19

48

19

50

19

52

19

54

19

56

19

58

19

60

19

62

19

64

19

66

19

68

19

70

19

72

19

74

19

76

19

78

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

R s

qu

are

d

Total Variance Weighted R2

Market Capitalization Weighted R2

Jinfeng Ge (Fudan University) Stock market in China 8 11th, 2017 30 / 38

Firm-specific variation in US Stock Market

7

Panel B. Market-wide variation is the mean across all US stocks of the sum-of-squared variation explained by the Market Model. Firm-specific variation is the corresponding residual variation.

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.50

0.55

0.60

0.65

0.70

0.75

0.80

0.85

0.90

19

26

19

28

19

30

19

32

19

34

19

36

19

38

19

40

19

42

19

44

19

46

19

48

19

50

19

52

19

54

19

56

19

58

19

60

19

62

19

64

19

66

19

68

19

70

19

72

19

74

19

76

19

78

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

Sto

ck r

etu

rn v

aria

nce

Firm-specific variation

Market-wide variation

Jinfeng Ge (Fudan University) Stock market in China 8 11th, 2017 31 / 38

Less Synchronous Stock Returns in Higher IncomeEconomies I

9

Figure 2. Less Synchronous Stock Returns in Higher Income Economies Panel A. Mean stock-level market model R2, by year from 1995 to 2010 for each country, estimated using weekly (Weds.-to-Weds.) DataStream total returns and country total return indexes. Countries are sorted by their mean R2 over all years.

0% 10% 20% 30% 40% 50% 60% 70% 80%

ChinaRussiaTurkey

ColombiaArgentina

TaiwanPakistanMalaysia

SpainMexicoGreece

HungaryCzech Republic

IndiaItaly

JapanPeru

SingaporeChile

NetherlandsBrazil

ThailandFinland

SwitzerlandPortugal

IsraelNorway

IndonesiaSouth Korea

PolandPhilippines

BelgiumAustria

DenmarkHong Kong

United StatesSweden

FranceIreland

GermanyCanada

New ZealandSouth Africa

United KingdomAustralia

2010

2009

2008

2007

2006

2005

2004

2003

2002

2001

2000

1999

1998

1997

1996

1995

Jinfeng Ge (Fudan University) Stock market in China 8 11th, 2017 32 / 38

Less Synchronous Stock Returns in Higher IncomeEconomies II

10

Panel B. Country means of the stock-level Market Model R2s from Panel A plotted against log of per capita GDP (constant 2000 US dollars). Both are means for 1995 to 2010.

Argentina

Australia

Austria Belgium

Brazil

Canada

Chile

China

Colombia

Czech Rep.

Denmark

Finland

France

Germany

Greece

HK

Hungary

India

Indonesia

Ireland

Israel

Italy Japan

Malaysia

Mexico

Netherlands

New Zealand

Norway

Pakistan

Peru

Philippines

Poland Portugal

Russia

Singapore

S. Africa

S. Korea

Spain

Sweden

Switzerland Thailand

Turkey

UK

US

0%

5%

10%

15%

20%

25%

30%

35%

40%

2.50 2.75 3.00 3.25 3.50 3.75 4.00 4.25 4.50 4.75

Gra

nd

me

an R

sq

uar

ed

(1

99

5 -

20

10

)

Mean from 1995 to 2010 of log of per capita GDP (Constant 2000 US dollars)

Jinfeng Ge (Fudan University) Stock market in China 8 11th, 2017 33 / 38

Market Efficiency

Informational efficiency can reflect private arbitrageurs gathering newinformation, reassessing firms.fundamental values, and trading toprofit from those reassessments (Grossman 1976); or more meaningfulpublic announcements (Fama et al. 1969); or more energetic insidertrading (Manne 1966)

Each can push stock prices towards fundamental values, all else equal,raising informational efficiency where informed arbitrage is less costly,disclosure fuller and timelier, or insider trades more informative

Jinfeng Ge (Fudan University) Stock market in China 8 11th, 2017 34 / 38

Functional Efficiency I

Informational efficiency is a means to an end, not necessarily an endper se

The social purpose of financial markets is arguably to allocate theeconomy.s savings to their highest value uses (Schumpeter 1911).Tobin (1984) defines the stock market as functionally efficient if stockprice changes push the economy towards a microeconomically efficientallocation of capital, and notes that functional and informationalefficiency need not coincide. Indeed, Grossman and Stiglitz (1980)and Black (1985) argue they cannot if information is costly. Thus,tests of how closely share prices obey a martingale (Griffin, Kelly andNardari 2013) need not gauge functional efficiency

Jinfeng Ge (Fudan University) Stock market in China 8 11th, 2017 35 / 38

Functional Efficiency II

Such considerations shift our focus from informational efficiency tofunctional efficiency: Do stock prices that move about moreasynchronously better direct capital to its highest value uses

Wurgler (2000) gauges the functional efficiency of a country.sfinancial system by the correlation of capital spending with valueadded across industries. If a country.s capital spending concentratesin its higher value-added industries, capital flows to where it createsmore new wealth. Wurgler finds more functional efficiency in thefinancial systems of economies with higher mean incomes, largerfinancial sectors, and stronger shareholder rights.

Jinfeng Ge (Fudan University) Stock market in China 8 11th, 2017 36 / 38

Functional Efficiency and R-square

21

Figure 3. Functional Efficiency and R2 Higher levels of Wurgler’s (20000) measure of functional efficiency indicate a greater concentration of capital spending in industries with higher value-added. R-squared is from Morck et al. (2000). Both variables use mid 1990s data.

Indonesia

India

Colombia

Turkey

Chile

Philippines

Mexico

Netherlands

Singapore

Portugal

Ireland

Australia

Finland

Canada

Greece

Norway

Korea

Malaysia

Italy

US

Japan

Peru

Sweden

France

Belgium

Spain

NZ

UK

Austria

HK

Denmark

Germany

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

0.4 0.5 0.6 0.7 0.8 0.9 1 1.1 1.2

Mar

ket

Mo

de

l R-s

qu

are

d

Functional efficiency

Jinfeng Ge (Fudan University) Stock market in China 8 11th, 2017 37 / 38

Investment in Innovation and Firm-specific Event Intensity

27

Figure 4. Investment in Innovation and Firm-specific Event Intensity

The stocks of firms in US industries with histories of heavier investment in Information

technology-related capital assets exhibit higher firms-specific return volatility in the 1990s

century. Circle sizes reflect relative industry total assets.

Source: Chun et al. (2008, p. 117)

Jinfeng Ge (Fudan University) Stock market in China 8 11th, 2017 38 / 38