steel founders’ society of america salak - ask chemicals.pdf · steel founders’ society of...

TRANSCRIPT

Steel Founders’ Society of America“Spring Leadership Meeting”

May 17th 2017Pittsburgh, PA

Agenda

• Economic Overview- Global- Asia/Pacific (APAC)- Europe /Middle East/Africa (EMEA)- North America/South America

• Critical Economic Indicators

• Regional Foundry Projections

May 17 2017 SFSA Spring Meeting Global Overview

“Global Perspective of

Casting Markets”

Dan Salak

Management Consultant

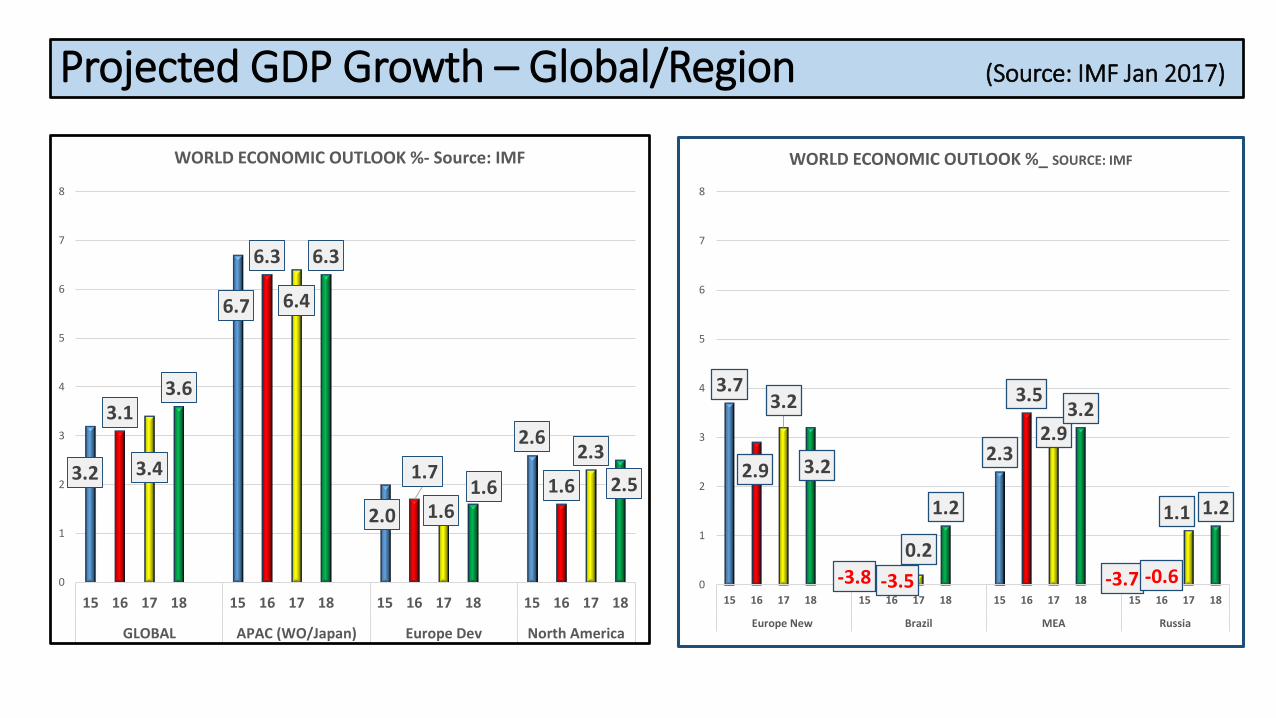

Projected GDP Growth – Global/Region (Source: IMF Jan 2017)

3.2

3.1

3.4

3.6

6.7

6.3

6.4

6.3

2.0

1.7

1.61.6

2.6

1.6

2.32.5

0

1

2

3

4

5

6

7

8

15 16 17 18 15 16 17 18 15 16 17 18 15 16 17 18

GLOBAL APAC (WO/Japan) Europe Dev North America

WORLD ECONOMIC OUTLOOK %- Source: IMF

3.7

2.9

3.2

3.2

-3.8 -3.50.2

1.2

2.3

3.5

2.93.2

-3.7 -0.6

1.1 1.2

0

1

2

3

4

5

6

7

8

15 16 17 18 15 16 17 18 15 16 17 18 15 16 17 18

Europe New Brazil MEA Russia

WORLD ECONOMIC OUTLOOK %_ SOURCE: IMF

Projected GDP Growth – Perspective (Source: IMF Jan 2017)

May 17 2017 SFSA Spring Meeting Global Overview

May 17 2017 SFSA Spring Meeting Global Overview

Economic activity slowed in 2016 but expected to increase 2017 – 2018

Increased expectations for developed nations (US, Germany, France, ..etc)

Large factors in this upward projection are expectations of fiscal stimulus within the United States, probable overflows outside the U.S. and policy stimulus within China.

Slightly lower expectations for Emerging Markets and Developing Nations due to stress of current financial conditions

A noted negative risk factor to global activity if “inward looking platforms”, “protectionism” and sharper than expected tightening of global financial conditions

A noted potential positive factor is mentioned if stimulus is larger than expected (US)

APAC - GDP GROWTH ~ 6.3% (Source: Trading Economics May 2017)

Auto

Ag

Mf

Mg

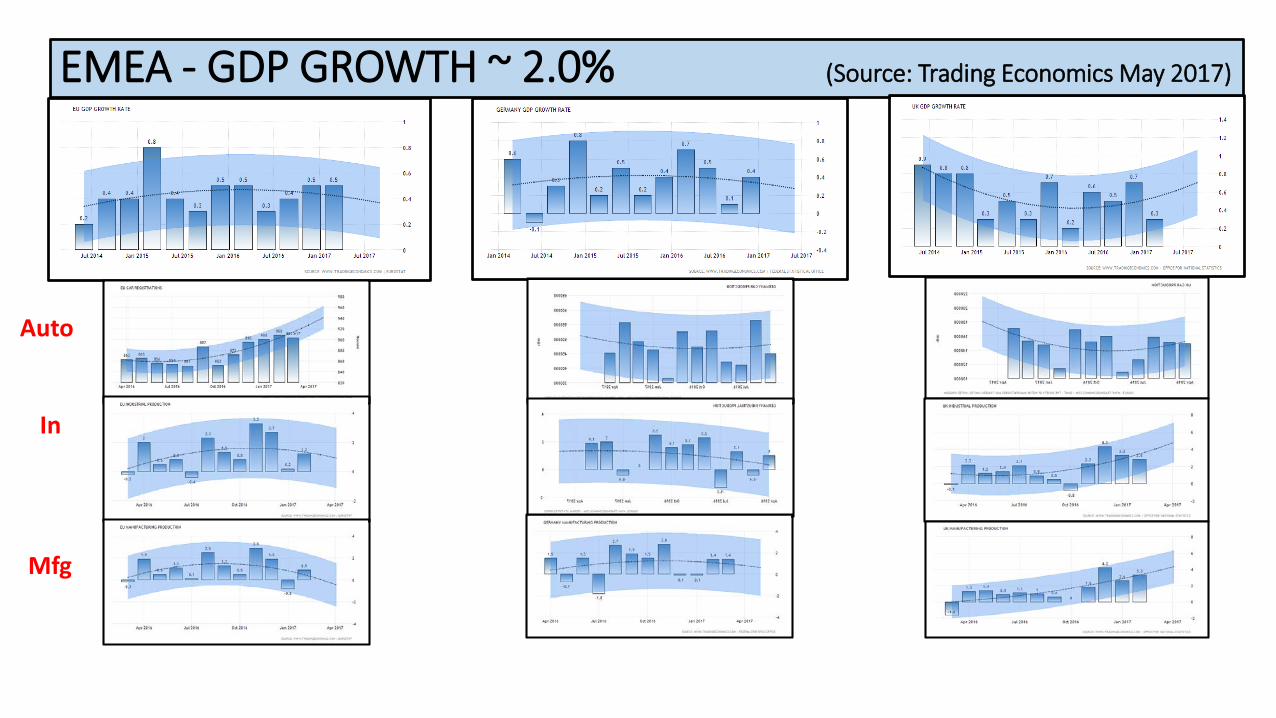

EMEA - GDP GROWTH ~ 2.0% (Source: Trading Economics May 2017)

Auto

In

Mfg

AMERICAS - GDP GROWTH ~ 2.5% (Source: Trading Economics May 2017)

Ag

Cs

Auto

Mg

• APAC continues to grow at a significant rate and primarily driven by China and India. However, growth in these 2 countries will have an impact on others in the APAC Region. Auto manufacture in particular will be increasing in China / India but volume reductions in S. Korea / Japan.

• EMEA the recovery of Automotive production is most significant as it is primary economic driver of EU . Initial boost from BREXIT move in UK is additive to the region. If NA economy over delivers on forecast there is hope of over flow into the EU.

• Americas is a “mixed bag” but overall positive. Brazil still facing significant challenges but have made significant progress in righting their economy. Reduced NAFTA implosion concerns but actual impact yet to be identified. Question remains of what level of economic success will be realized ‘17 –’18 ?

Significant Points

Critical Foundry Market Segments

AUTO / Light Truck AGR / Construction Mining/Hvy. Const Aerospace

Heavy Truck (C5-8) Energy Railroad Military

Automotive Light Vehicle - Americas Source: OICA

29109373192998 3387522 3457204 3600000 3750000

10815629 11371386 11784050 11930041 11727230 11727230

4316320 3605042 2911966 2608755 2728150 2806920

20412847 20551644 20352534 20353846 20415380 20644150

0

5000000

10000000

15000000

20000000

25000000

2013 2014 2015 2016 2017P 2018P

America's LV Production - Source HIS Automotive

Can Mex US SA TOTAL

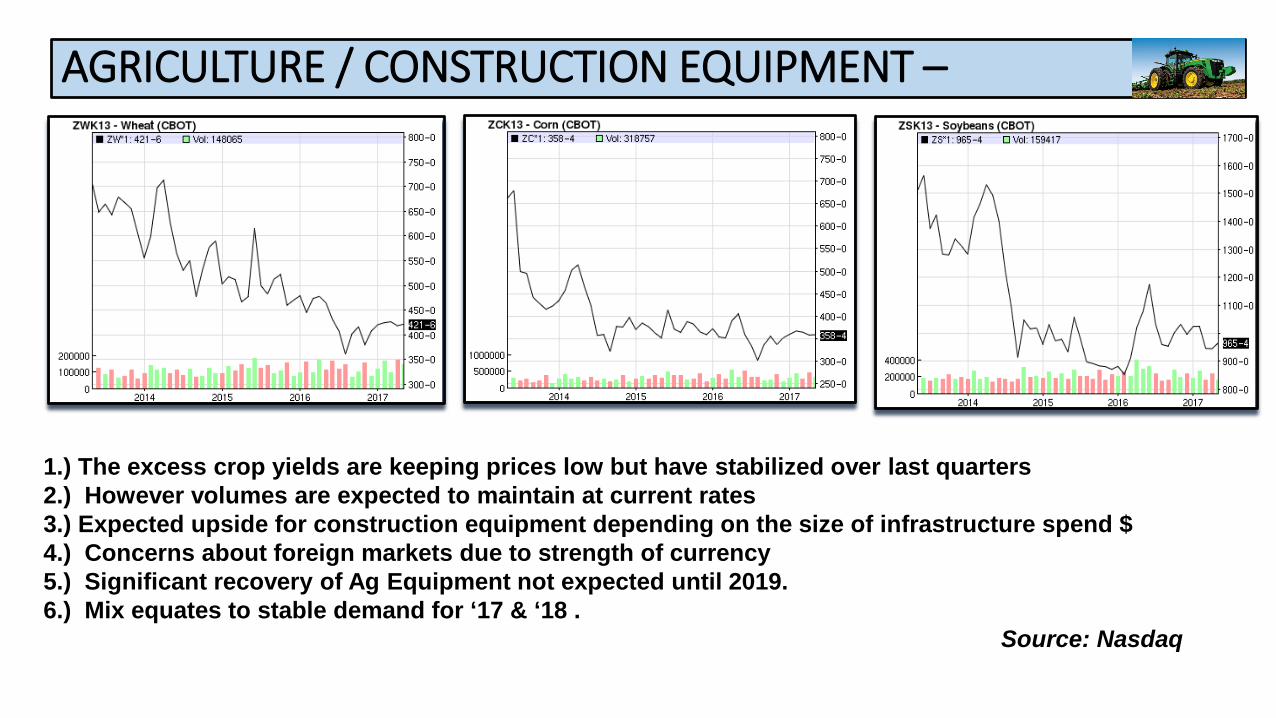

AGRICULTURE / CONSTRUCTION EQUIPMENT –

1.) The excess crop yields are keeping prices low but have stabilized over last quarters 2.) However volumes are expected to maintain at current rates3.) Expected upside for construction equipment depending on the size of infrastructure spend $4.) Concerns about foreign markets due to strength of currency5.) Significant recovery of Ag Equipment not expected until 2019.6.) Mix equates to stable demand for ‘17 & ‘18 .

Source: Nasdaq

CONSTRUCTION EQUIPMENT –

CONSTRUCTION EQUIPMENT DEMAND GLOBAL

$72 B

$89 B

Source: Off Highway Research 8/25/16

Mining Equipment Deliveries

Source: Mining . Com 03/16

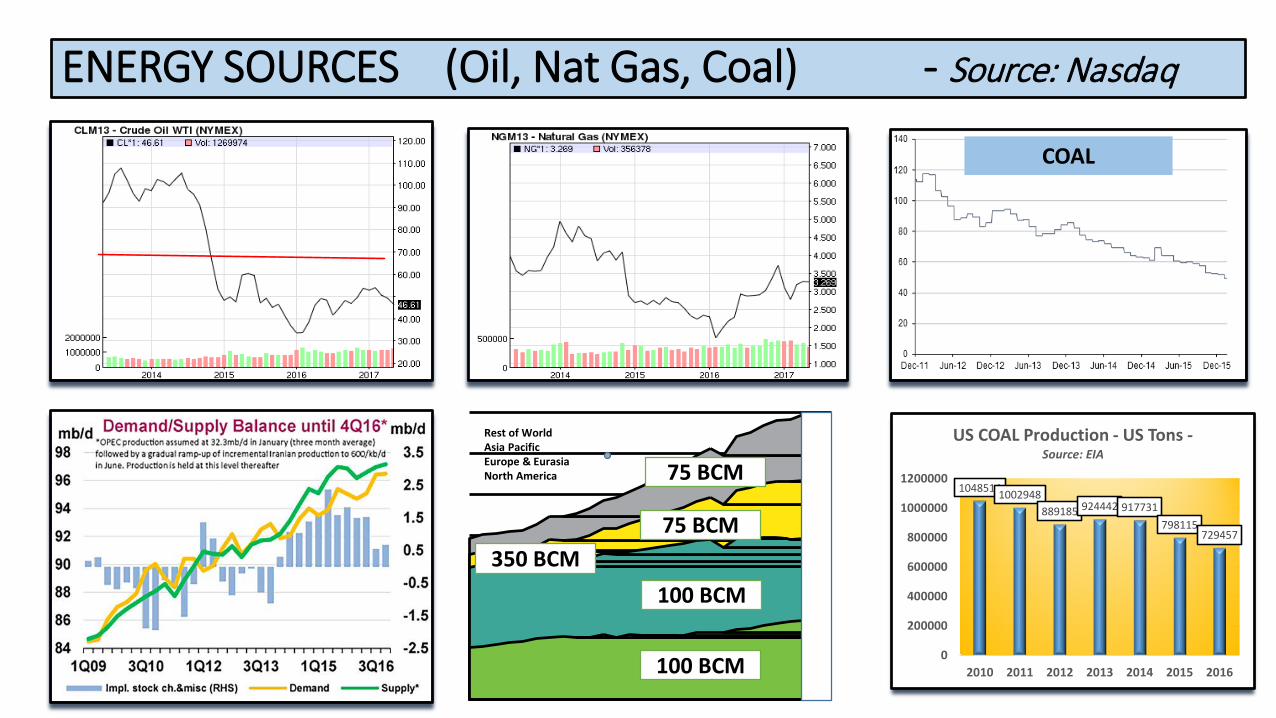

ENERGY SOURCES (Oil, Nat Gas, Coal) - Source: Nasdaq

COAL

10485141002948889185 924442 917731

798115729457

0

200000

400000

600000

800000

1000000

1200000

2010 2011 2012 2013 2014 2015 2016

US COAL Production - US Tons -Source: EIA

Rest of WorldAsia PacificEurope & EurasiaNorth America

350 BCM

100 BCM

100 BCM

75 BCM

75 BCM

ENERGY SOURCES (Oil, Nat Gas, Coal) - Source: Nasdaq

COAL

1.) Global Oil capacity exceeds Global demand. $100 Oil will not return barring a cataclysmic event 2.) North American ‘frack” producers continue to innovate to lower costs and improve efficiency3.) OPEC nations utilizing the “valve” as their form of innovation.4.) Longer term threats from electric vehicles fuel efficient vehicles5.) Shorter term looks positive for Americas production

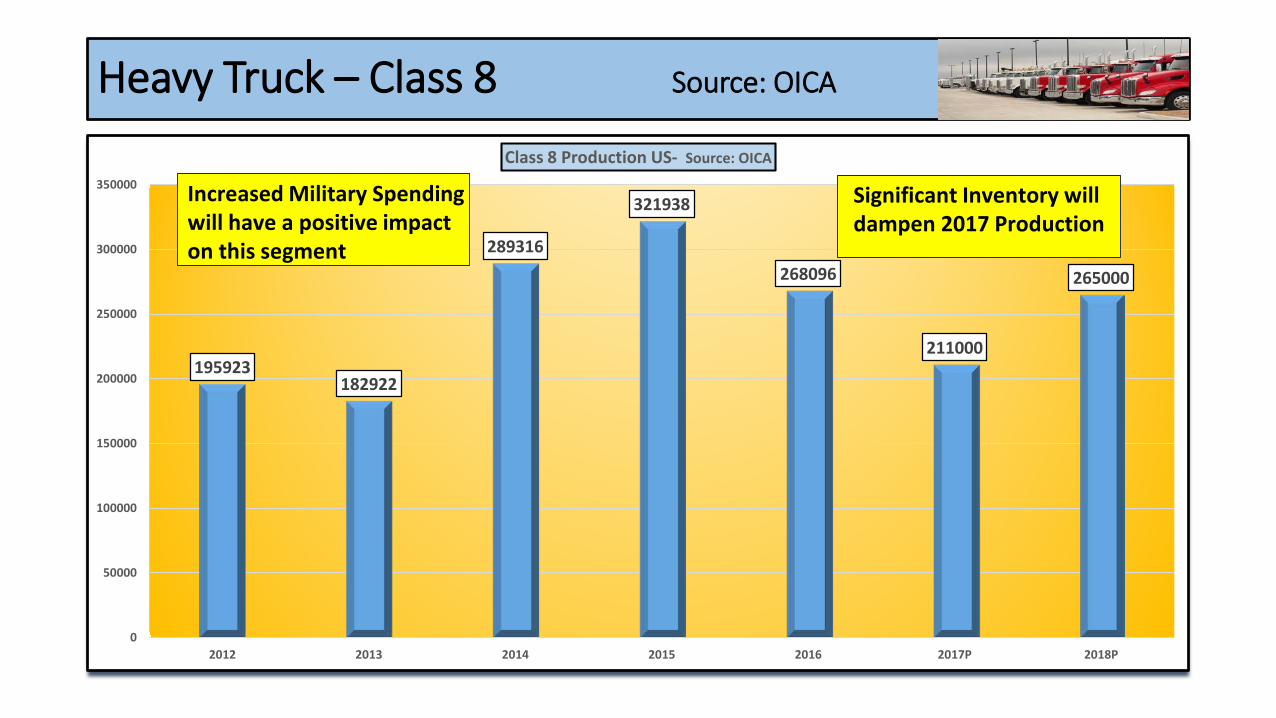

Heavy Truck – Class 8 Source: OICA

195923182922

289316

321938

268096

211000

265000

0

50000

100000

150000

200000

250000

300000

350000

2012 2013 2014 2015 2016 2017P 2018P

Class 8 Production US- Source: OICA

Significant Inventory will dampen 2017 Production

Increased Military Spendingwill have a positive impacton this segment

Rail Car Deliveries Source: Progressive Railroading 12/16

85000

56669

45200 4200047800

54600

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

2015 2016 2017 2018 2019 2020

Rail Car Deliveries

~ 350,000 Cars in Storage

Aerospace products & partsElectronic computer equipment

AcceleratingGrowth

DeceleratingGrowth

AcceleratingDecline

DeceleratingDecline

+

-

Metalworking machineryFabricated metal productsConstruction machinerySemiconductorsElectric lighting equipment

Communications equipment

Motor vehicles and partsIndustrial machineryNavigational, measuring, electromedical, &control instruments

Household appliancesMedical equipment & supplies

Electrical equipmentBasic chemicalsPublic works constructionMaterial handling equipment

Ventilation, heating, air conditioning, & commercial refrigeration equipment

Pharmaceuticals & medicinesAlumina & aluminum

Oil & gas well drillingMining and oil and gas field machinery

Iron & steel productsEngine, turbine, & power transmission equipment

Paper

Private nonresidential constructionHousing starts

Figure 1 – Industrial Sector by Phase of Cycle, February 2016

Industrial Phase Cycle – Source: MAPI Foundation

Source(s): MAPI Foundation

May 17 2017 SFSA Spring Meeting Global Overview

• Market Segments that have “bottomed out” and could be additive to NA volume: Mining Equipment – Agriculture Equipment - Energy Generation

• Market Segments that project continued downward volume and could be negative to NA volume: Class 5 -8 Trucks – Railroad Car Builds

• Market Segment that expect to stay near recent production levels and be neutral to NA volume: Automotive & Light Vehicles

Significant Points For 2017

May 17 2017 SFSA Spring Meeting Global Overview

Casting Production Actual/Projection - Global/Region – MT

May 17 2017 SFSA Spring Meeting Global OverviewMay 17 2017 SFSA Spring Meeting Global Overview

46,739

25,576

16,053

10,888

3,988

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

GI DI AL STEEL NF

METAL EVOLUTION 2005 - 2015

2005 Global 2010 Global 2015 Global

SIGNIFICANT CHANGE

AUTOMOTIVE ENGINES

5,817

4,310 2,728

2,158 1,118

9,610

5,047 4,427

2,314 681

31,311

16,219

8,898

6,416

2,187

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

GI DI ALUM STEEL NF

2015 MT METAL BY REGION

AMERICAS EMEA APAC

Global Tonnage /Region – Metric Tons

May 17 2017 SFSA Spring Meeting Global OverviewMay 17 2017 SFSA Spring Meeting Global Overview

90.198.5 100.8 103.2 104.4 104.1 105.4 109.0 112.0 117.0 121.1

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

2010 2011 2012 2013 2014 2015 2016P 2017P 2018P 2019P 2020P

Global Tonnage - 2015 Census Modern Castings

AMERICAS EMEA APAC TOTAL

APAC Market Segment Expectations 2016 thru 2018

End Markets Current TrendsCyclicality

Heavy Truck Class 3 thru 8

Mining Heavy Equipment

CarsLight Trucks

Energy GenerationOil – NG - ALT

Agriculture&

Construction

High

High

High

Medium

Low

Medium

• China Auto production running strong• India Auto increase could be 10%• Significant energy being invested in electric vehicle technology• Increased production in C/I will result in lower production J/K

+2 %

+3%

+3%

+2%

• Mining industry has been the epi-center of over build* Mining cycle is similar around the world. Point of difference is China continues to use significant amounts of coal for power generation

• Growth in 2017 to be close to 5% but 2017 -2018 to be -8%. • Changes to the Chinese economic focus more related to

construction and driving demand for large trucks

• The impetus of environmental programmes has accelerated the Chinese Wind Energy business both domestially and for expot.

• Coal production important part of power grid.

• Steady production and increase in railway track• Over $200 Bn investment in HSR• Smaller but substancial HSR in Japan and India

• Agriculture sector is producing crops at a high rate for domestic consumption and export.

• Construction Equipment segment is surging due to focus in China for population housing and Inidai for industrial development

Growth Trend

+3%

RailroadCars

May 17 2017 SFSA Spring Meeting Global Overview

Aerospace&

Other +2% Medium• China striving to build passenger airliners through COMAC .• To date projects have been in extended delays to deadlines .• Currently engaged in possible JV with Russia to build Regional jets.

-4 %

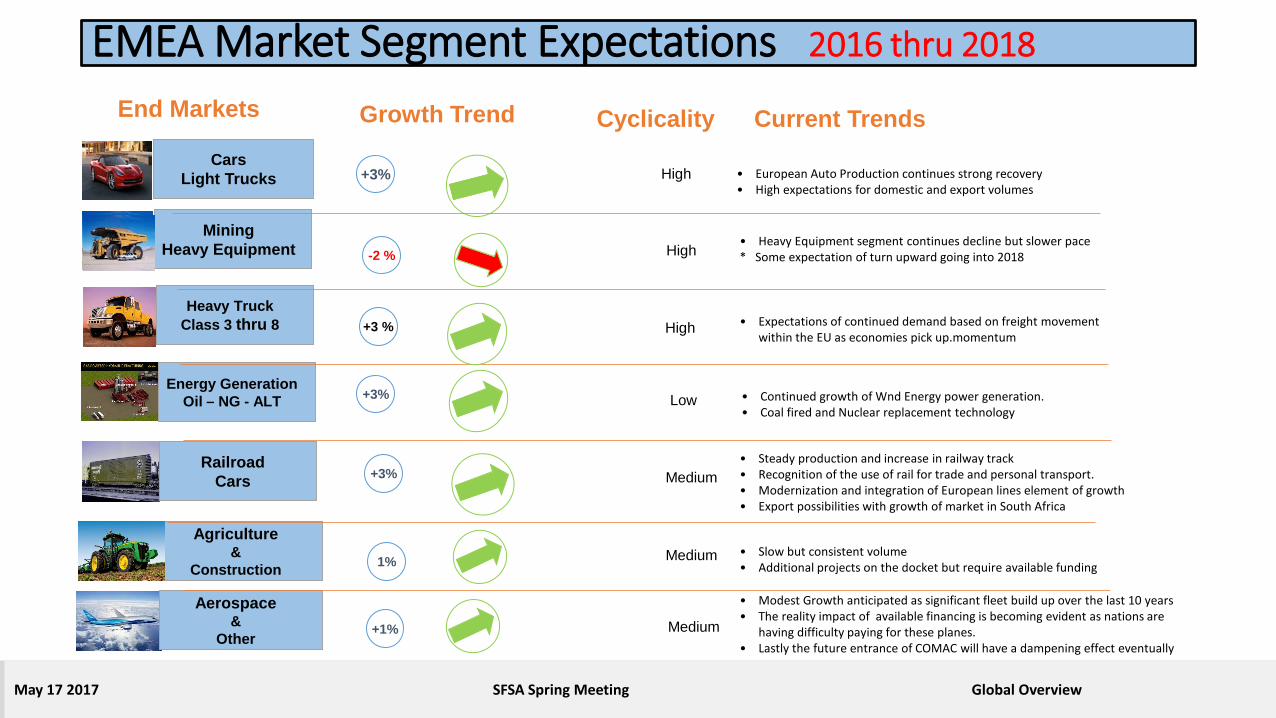

EMEA Market Segment Expectations 2016 thru 2018

End Markets Current TrendsCyclicality

Heavy Truck Class 3 thru 8

Mining Heavy Equipment

CarsLight Trucks

Energy GenerationOil – NG - ALT

Agriculture&

Construction

High

High

High

Medium

Low

Medium

• European Auto Production continues strong recovery • High expectations for domestic and export volumes

+3 %

+3%

+3%

+3%

• Heavy Equipment segment continues decline but slower pace* Some expectation of turn upward going into 2018

• Expectations of continued demand based on freight movement within the EU as economies pick up.momentum

• Continued growth of Wnd Energy power generation. • Coal fired and Nuclear replacement technology

• Steady production and increase in railway track• Recognition of the use of rail for trade and personal transport.• Modernization and integration of European lines element of growth• Export possibilities with growth of market in South Africa

• Slow but consistent volume • Additional projects on the docket but require available funding

Growth Trend

1%

RailroadCars

May 17 2017 SFSA Spring Meeting Global Overview

Aerospace&

Other +1% Medium

• Modest Growth anticipated as significant fleet build up over the last 10 years• The reality impact of available financing is becoming evident as nations are

having difficulty paying for these planes.• Lastly the future entrance of COMAC will have a dampening effect eventually

-2 %

S America Market Segment Expectations 2016 thru 2018

End Markets Current TrendsCyclicality

Heavy Truck Class 3 thru 8

Mining Heavy Equipment

CarsLight Trucks

Energy GenerationOil – NG - ALT

Agriculture&

Construction

High

High

High

Medium

Low

Medium

• Brazil has been working hard to come back from devastating economic situation• The situation has stabilized and production is reurning to a more normal state• The increase is important but also based off lower than normal numbers

+29 %

+7%

+8%

+5%

• As global demand increases so does Mining in Brazil• Stability of the currency and import/export policies are having a positive impact

• During the worst of the economic difficulties production of vehicles was sharply curtailed• Materials previously difficult to afford or obtain are now available

• Backlog of Wind Energy components demand is now being produced

• Current Rail Car fleet is an average of 30 yrs old• Considerable investment is focused onincreasing the railroad footprint in Brazil

• Investments in both sectors has been miniscule over the last 4 years• Expectations that the economic recovery will drive need for additional Construction /

Farm equipment

Growth Trend

+5%

RailroadCars

May 17 2017 SFSA Spring Meeting Global Overview

Aerospace&

Other +4% Medium• Embraer is a global supplier of aircraft and continues to participate in the small /

private jest marlket. .• Orders have been steady and competitive with Bombardier of Canada

+8%

NA Market Segment Expectations 2016 thru 2018

End Markets Current TrendsCyclicality

Heavy Truck Class 3 thru 8

Mining Heavy Equipment

CarsLight Trucks

Energy GenerationOil – NG - ALT

Agriculture&

Construction

High

High

High

Medium

Low

Medium

• Only 1 year removed from a production record sales continue to relatively stable• Existing fleet remains just below record high for age of vehicles• Demand for Light vehicles remains strong

0%

• Mining industry oks as though it has bottomed out• Increased industrial production would have impact on commodity pricing and demand• Still do not significant upward movement until 2019

• Significant drop in expected orders for 2017 but improvement in 2018 • Plus side is that Oil tanker new regulations are helping to side step inventory issue• 350k cars on the sidelines due to lreduced freight activity.

• The decline oif the industry has appeared to hit bottom.• Efforts to compete at lower oil pricing is bearing fruit• If increased economic activity develops isegment could become a positive vs 2016.

• New customer segments helping to mute decline (Chemicals Ind – Plastic pellets)• Needs improvemnt from the energy sector to change dynamic• Plus side is that Oil tanker new regulations are helping to side step inventory issue• 350k cars on the sidelines due to lreduced freight activity.

• Agriculture sector has appeared to bottom out and pricing stable• Construction Equipment has upside with current environment• Additional stimulus would accelerate the demand for the CE segment.

Growth Trend

+3%

RailroadCars

May 17 2017 SFSA Spring Meeting Global Overview

Aerospace&

Other +2% Medium• Significant orders on the books for Boeing and Bombardier• Increased Military spending will be additive to the mix• Storm clouds on the near horizon is financial challenges of many of the customers

-2 %

-5 %

0%

-10%

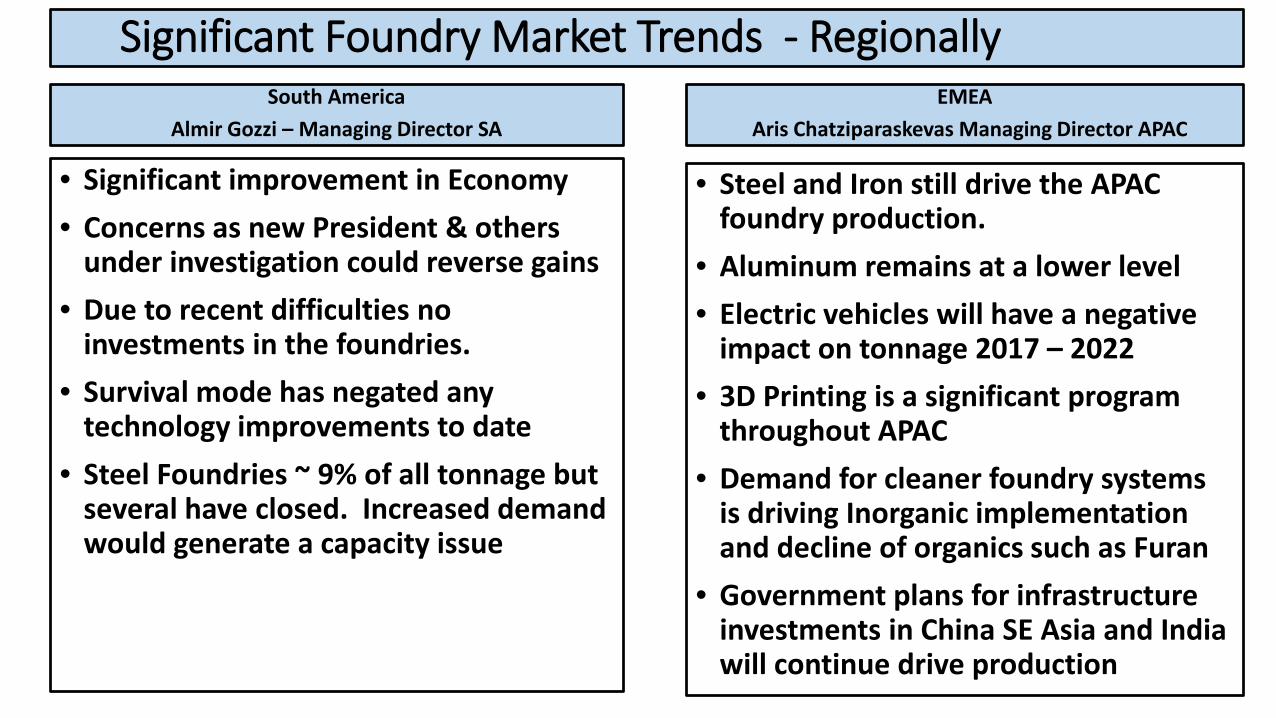

South America Almir Gozzi – Managing Director SA

• Significant improvement in Economy• Concerns as new President & others

under investigation could reverse gains• Due to recent difficulties no

investments in the foundries.• Survival mode has negated any

technology improvements to date• Steel Foundries ~ 9% of all tonnage but

several have closed. Increased demand would generate a capacity issue

EMEAAris Chatziparaskevas Managing Director APAC

• Steel and Iron still drive the APAC foundry production.

• Aluminum remains at a lower level • Electric vehicles will have a negative

impact on tonnage 2017 – 2022• 3D Printing is a significant program

throughout APAC• Demand for cleaner foundry systems

is driving Inorganic implementation and decline of organics such as Furan

• Government plans for infrastructure investments in China SE Asia and India will continue drive production

Significant Foundry Market Trends - Regionally

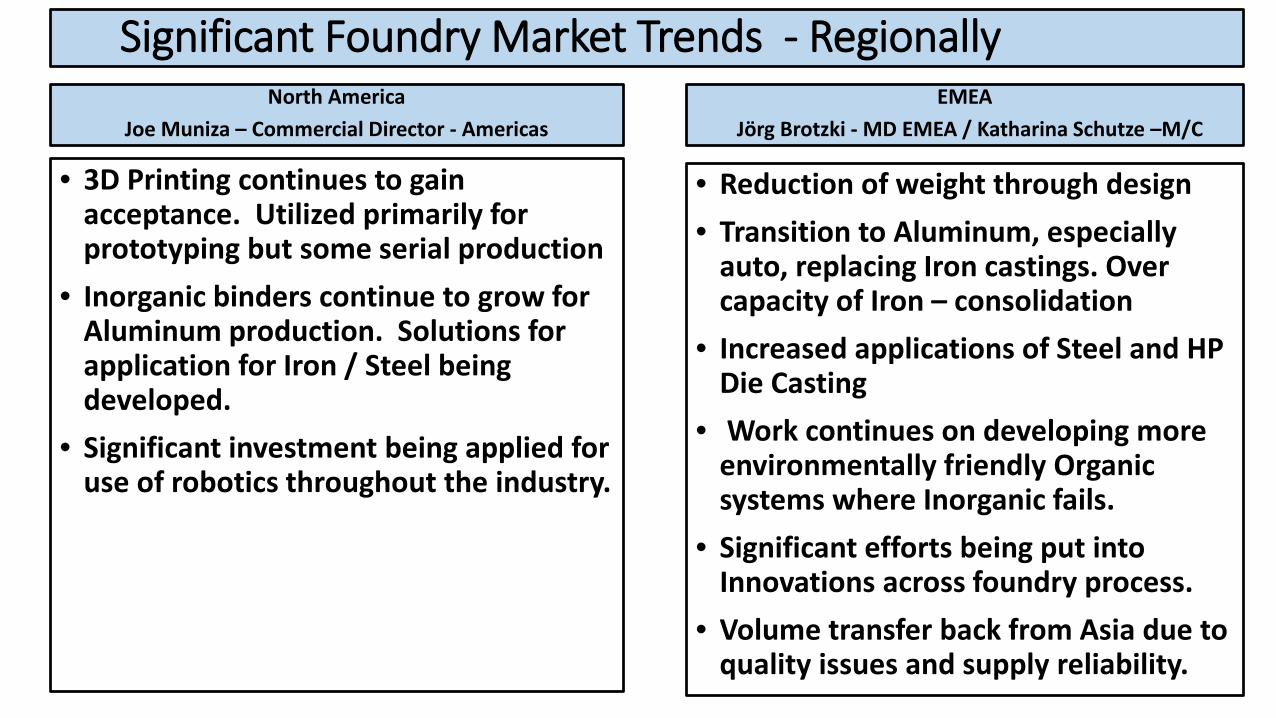

North America Joe Muniza – Commercial Director - Americas

• 3D Printing continues to gain acceptance. Utilized primarily for prototyping but some serial production

• Inorganic binders continue to grow for Aluminum production. Solutions for application for Iron / Steel being developed.

• Significant investment being applied for use of robotics throughout the industry.

EMEAJörg Brotzki - MD EMEA / Katharina Schutze –M/C

• Reduction of weight through design • Transition to Aluminum, especially

auto, replacing Iron castings. Over capacity of Iron – consolidation

• Increased applications of Steel and HP Die Casting

• Work continues on developing more environmentally friendly Organic systems where Inorganic fails.

• Significant efforts being put into Innovations across foundry process.

• Volume transfer back from Asia due to quality issues and supply reliability.

Significant Foundry Market Trends - Regionally

Thank You !

• Ryan Moore – Steel Founders’ Society of America• Katharina Schütze – ASK Chemicals Hilden GmbH• Charlie Hoertz – ASK Chemicals Dublin OH• Joe Muniza – ASK Chemicals - Americas• Almir Gozzi – ASK Chemicals - South America• Aris Chatziparaskevas – ASK Chemicals APAC• Jörg Brotzki – ASK Chemicals – EMEA• Luiz Totti – ASK Chemicals - Americas

May 17 2017 SFSA Spring Meeting Global Overview

May 17 2017 SFSA Spring Meeting Global Overview

Steel Founders’ Society of America“Spring Leadership Meeting”

May 17th 2017Pittsburgh, PA