statutory accounting principles (e) working group ...€¦ · statutory accounting principles (e)...

TRANSCRIPT

Attachment A Ref #2016-39

© 2016 National Association of Insurance Commissioners 1

Statutory Accounting Principles (E) Working Group Maintenance Agenda Submission Form

Form A

Issue: Mortgage Loans With Multiple Lenders Check (applicable entity): P/C Life Health

Modification of existing SSAP New Issue or SSAP Interpretation

Description of Issue: The Investment Classification Project (detailed in agenda item #2013-36) supported a review of the investment SSAPs to address a variety of application questions, mostly focusing on definitions and scope limitations of each of the noted SSAPs. In response to an industry inquiry, SSAP No. 37—Mortgage Loans was included within the Investment Classification Project, with a specific focus to consider whether a partial interest in a mortgage loan (in which there is one borrower, with more than one lender identified in a single lending agreement, and all lenders are secured with the same real estate) should be in scope of SSAP No. 37, and reported in a similar manner as other mortgage loans on Schedule B. The mortgage loan structures intended to be the focus of this agenda item are investments when the reporting entity/ investor is a “participant in a mortgage loan.” This focus intends to consider standard mortgage loan agreements (with principal and interest payments) in which the mortgage loan agreement identifies more than one lender providing the funds to a sole borrower in a single loan agreement. These generally occur for larger commercial mortgage loans. The use of the term “participant” to identify these mortgage loan structures shall not be interpreted as encompassing “participating mortgages.” In a “participating mortgage” the lender is entitled to share in the rental or resale proceeds from the property by the borrower, generally as a certain percentage of the cash flows generated from the real estate acquired with the mortgage loan. Furthermore, this agenda item is not intended to encompass an interest in a “fund” with underlying real estate assets (such as a Real Estate Investment Trust—REIT). A scenario of the structure intended to be captured within this agenda item is listed below:

• Five reporting entities each provide a $400,000 commercial mortgage loan to a single borrower. • Mortgage loan is secured by a single $2,000,000 commercial real estate structure. • None of the lenders can foreclose on the borrower without all lenders agreeing to foreclose. • This is not a “securitization” in which the lenders are issued a security representing an interest in cash

flows, supported by the real estate collateral held in trust. Instead, the five lenders are all identified as lenders in the single loan agreement (“as participants in a mortgage loan”).

Pursuant to the guidance in SSAP No. 37, mortgage loans are defined as a debt obligation that is not a security, which is secured by a mortgage on real estate. Within the definition of a “security” in SSAP No. 37 (definition adopted from U.S. GAAP), a “participation” is specifically noted. As such, some have concluded that an insurer as a “participant” in a group mortgage loan agreement results with these mortgage loan structures being outside the scope of SSAP No. 37. Excerpt from SSAP No. 37:

2. A mortgage loan is defined as a debt obligation that is not a security, which is secured by a mortgage on real estate. (A security is a share, participation, or other interest in property or in an enterprise of the issuer or an obligation of the issuer that (a) either is represented by an instrument issued

Attachment A Ref #2016-39

© 2016 National Association of Insurance Commissioners 2

in bearer or registered form, or if not represented by an instrument, is registered in books maintained to record transfers by or on behalf of the issuer, (b) is of a type commonly dealt in on securities exchanges or markets or, when represented by an instrument, is commonly recognized in any area in which it is issued or dealt in as a medium for investment, and (c) either is one of a class or series or by its terms is divisible into a class or series of shares, participations, interests, or obligations).

From comments originally received, these transactions reflect “loan participation agreements” backed by real estate, in which a mortgage loan is made by multiple lenders to a single borrower. It has been communicated that the key difference between this “participant” agreement and a standard mortgage loan (one lender) is that the reporting entity is unable to unilaterally foreclose on the loan. Instead, all lenders identified as a “participant” in the group transaction must agree to foreclose on the mortgage loan. This structure appears to be similar to a bank loan acquired through a syndication, except that the loan is secured with real estate collateral. (Bank loans are captured within SSAP No. 26—Bonds; the Investment Classification Project revisions currently being considered for that SSAP would clarify that bank loans are not securities, but are fixed-income investments specifically noted for inclusion in SSAP No. 26. Definitions for bank loans acquired by assignment, participation or syndication are also proposed with the current exposures under the Investment Classification Project.) Although this “group mortgage loan” issue was requested to be considered by the Working Group as part of the Investment Classification Project, the Annual Statement Instructions already include guidance which implies that “loans subject to a participation agreement” would be captured in Schedule B – Part 1:

Column 14 – Value of Land and Buildings: Report the appraisal value of the property (for land and buildings). For loans subject to a participation agreement, include only the reporting entity’s pro rata share of the appraised value as it relates to the reporting entity’s interest in the mortgage loan.

The intent of this agenda item is to clarify the SSAP that should address these transactions, and clarify the appropriate reporting schedule for consistency purposes. Based on the substance of these items, as well as the current guidance in Schedule B-Part 1, initial proposed revisions (detailed in the staff recommendation) propose to clarify the inclusion of these agreements in SSAP No. 37—Mortgage Loans. However, the Working Group could consider other SSAPs / reporting structures. Regardless of the SSAP identified, it is anticipated that revisions would be needed to clarify the inclusion of these items within that SSAP. A summary of possible SSAPs that could be considered by the Working Group is listed below:

• SSAP No. 37—Mortgage Loan: This SSAP would reflect the investment as a mortgage loan (secured by real estate), and would allow the mortgage loan to be recorded at the principal amount of the loan made by a specific reporting entity. Revisions to the SSAP are recommended to clarify the inclusion of these structures within scope, as well as propose guidance for the assessment of impairment to ensure comparisons based on the full amount loaned by the group of lenders to the fair value of the real estate, rather than a comparison of the amount loaned by the reporting entity to the full fair value of the real estate. If included within this SSAP, the mortgage loan would be reported on Schedule B. Under current RBC factors, for health and p/c companies, the RBC would be .05, and for life companies, RBC would depend on the type of loan, status (good standing, 90-days past due, or in foreclosure) and loan-to-value and debt-service coverage.

o Staff Note: As identified above, staff recommends SSAP No. 37 for these agreements. This is also consistent with existing Annual Statement Instructions.

• SSAP No. 21—Other Admitted Assets: This SSAP would reflect that the transaction is a “collateral loan”

as an unconditional obligation for the payment of money secured by the pledge of an investment. This standard allows the loan balance to be admitted if the collateral qualifies as an investment to the extent

Attachment A Ref #2016-39

© 2016 National Association of Insurance Commissioners 3

that the collateral equals or exceeds the outstanding loan balance. If captured within SSAP No. 21, the investment would be reported on BA and the RBC for p/c and health companies would be 20%, and the RBC companies for life companies would be 30%.

o Staff Note: If the decision is made to not include these transactions within SSAP No. 37 (perhaps as a result of the group foreclosure restrictions), staff would recommend inclusion within SSAP No. 21 as a collateral loan. This would continue to reflect that a reporting entity acting as a “participant” in a mortgage loan agreement (as defined in this agenda item) does not result with the loan being considered a “security.” Classification within SSAP No. 21 (reported on Schedule BA) would result with a much higher RBC, particularly for mortgage loans that are in good standing. As the life RBC for mortgage loans (Schedule B) considers a variety of components (loan standing, loan-to-value ratio and debt service coverage), inclusion on BA may be perceived to result with an uncorrelated RBC as it does not consider elements specific to the mortgage loan.

• SSAP No. 26—Bonds: This SSAP would reflect the reporting entity’s “participant” structure as a “security” representing a creditor relationship whereby there is a fixed schedule for one or more future payments. If captured under this SSAP, the accounting and reporting of the loan would depend on an NAIC designation (requiring a credit assessment of the borrower), with either an amortized cost or fair value measurement method. (This SSAP would not consider the real estate collateral in valuation.) Although this approach could result with a more desirable RBC (on Schedule D-1), the original comments identified that obtaining an NRSRO rating for commercial mortgages is prohibitively expensive. If these items cannot be filed with the NAIC SVO, this could result with these structures being classified as 5* or 6*, with less desirable RBC.

o Staff Notes: It is staff’s initial interpretation that the “participant” lending structure is not intended to be captured within the “security” definition. Furthermore, the mortgage loan terms and real estate collateral is perceived to be a more relevant factor in determining valuation (e.g., impairment) and RBC then a credit assessment of the borrower (particularly if credit assessments are not feasible and the item is reported as a 5*).

• SSAP No. 43R—Loan-backed and Structured Securities: This SSAP would reflect the cash-flow nature of

the transaction, as the reporting entity is entitled to a share of cash flows from the borrower’s repayment of mortgage loan. However, the security does not currently fit within the construct of SSAP No. 43R as the real asset collateral is not held in trust. If the investment was captured within this SSAP, the transactions would be reported on Schedule D-1, with RBC based on NAIC designation. (For SSAP No. 43R securities, the NAIC designation can be impacted if the security is financially modeled or not financially modeled, but with a CRP rating.)

o Staff Notes: Similar to the comments on SSAP No. 26, it is staff’s initial interpretation that the

“participant lending” structure is not intended to be captured within the “security” definition. Also consistent, the mortgage loan terms and real estate collateral is perceived to be a more relevant factor in determining valuation (e.g., impairment) and RBC then a credit assessment of the borrower. Lastly, as this investment does not place the real estate collateral in a trust, revisions to incorporate an exception to the current SSAP No. 43R provisions would be necessary for inclusion in this SSAP.

• SSAP No. 48—Joint Ventures, Partnership and LLC: This SSAP could reflect the investment as a joint

venture or partnership interest, but it does not seem that this mortgage loan structure would fit the intent of structures envisioned to be in scope, as this SSAP requires audited financial statements of the investee for admittance. If captured within this SSAP, the structure would be reported on Schedule BA as an other-than-invested asset with the underlying characteristic of a mortgage loan. If reported on BA, RBC for p/c

Attachment A Ref #2016-39

© 2016 National Association of Insurance Commissioners 4

and health companies would be 20%, and the RBC companies for life companies would be 30% unless the reporting entity filed the investment with the NAIC to receive a lower RBC.

o Staff Notes: As noted above, staff does not believe that this mortgage loan structure reflects the intent of what was to be captured within the scope of SSAP No. 48 as a joint venture or partnership. If captured within the scope of this SSAP, the reporting entity would need audited financial statements to be admitted.

Existing Authoritative Literature (underlining added for emphasis): SSAP No. 37—Mortgage Loans

2. A mortgage loan is defined as a debt obligation that is not a security, which is secured by a mortgage on real estate. (A security is a share, participation, or other interest in property or in an enterprise of the issuer or an obligation of the issuer that (a) either is represented by an instrument issued in bearer or registered form, or if not represented by an instrument, is registered in books maintained to record transfers by or on behalf of the issuer, (b) is of a type commonly dealt in on securities exchanges or markets or, when represented by an instrument, is commonly recognized in any area in which it is issued or dealt in as a medium for investment, and (c) either is one of a class or series or by its terms is divisible into a class or series of shares, participations, interests, or obligations).

Schedule B – Part 1: Mortgage Loans Owned December 31 of Current Year

Column 14 – Value of Land and Buildings: Report the appraisal value of the property (for land and buildings). For loans subject to a participation agreement, include only the reporting entity’s pro rata share of the appraised value as it relates to the reporting entity’s interest in the mortgage loan.

SSAP No. 26—Bonds: (Current Authoritative Guidance)

2. Bonds shall be defined as any securities representing a creditor relationship, whereby there is a fixed schedule for one or more future payments. This definition includes:

Note – Revisions to SSAP No. 26 are proposed under the Investment Classification Project:

3. Bonds shall be defined as any securities1 representing a creditor relationship, whereby there is a fixed schedule for one or more future payments. This definition includes:

Proposed Footnote to Define “Security”: This SSAP adopts the GAAP definition of a security as it is used in FASB Codification Topic 320 and 860: Security: A share, participation, or other interest in property or in an entity of the issuer or an obligation of the issuer that has all of the following characteristics:

a. It is either represented by an instrument issued in bearer or registered form or, if not represented by an instrument, is registered in books maintained to record transfers by or on behalf of the issuer.

b. It is of a type commonly dealt in on securities exchanges or markets or, when represented by an

instrument, is commonly recognized in any area in which it is issued or dealt in as a medium for investment.

c. It either is one of a class or series or by its terms is divisible into a class or series of shares,

participations, interests, or obligations.

Attachment A Ref #2016-39

© 2016 National Association of Insurance Commissioners 5

The following definitions are also proposed in SSAP No. 26 to define “bank loan”:

Bank Loan – Fixed-income instruments, representing indebtedness of a borrower, made by a financial institution and acquired by a reporting entity through an assignment, participation or syndication:

• Assignment – A bank loan assignment is defined as a fixed-income instrument in which there is

the sale and transfer of the rights and obligations of a lender (as assignor) under an existing loan agreement to a new lender (and as assignee) pursuant to an Assignment and Acceptance Agreement (or similar agreement) which effects a novation under contract law, so the new lender becomes the direct creditor of and is in contractual privity with the borrower having the sole right to enforce rights under the loan agreement.

• Participation – A bank loan participation is defined as a fixed-income investment in which a single

lender makes a large loan to a borrower and subsequently transfers (sells) undivided interests in the loan to other entities. Transfers by the originating lender may take the legal form of either assignments or participations. The transfers are usually on a nonrecourse basis, and the originating lender continues to service the loan. The participating entity may or may not have the right to sell or transfer its participation during the term of the loan, depending on the terms of the participation agreement. Reporting entities shall account for loan participations within the guidelines of this statement if the participation agreement provides the reporting entity with the right to sell or transfer its participation during the term of the loan. Loan Participations can be made on a parri-passu basis (where each participant shares equally) or a senior subordinated basis (senior lenders get paid first and the subordinated participant gets paid if there are sufficient funds left to make a payment).

• Syndication – A bank loan syndication is defined as a fixed-income investment in which several

lenders share in lending to a single borrower. Each lender loans a specific amount to the borrower and has the right to repayment from the borrower. Separate debt instruments exist between the debtor and the individual creditors participating in the syndication. Each lender in a syndication shall account for the amounts it is owed by the borrower. Repayments by the borrower may be made to a lead lender that then distributes the collections to the other lenders of the syndicate. In those circumstances, the lead lender is simply functioning as a servicer and shall not recognize the aggregate loan as an asset. A loan syndication arrangement may result in multiple loans to the same borrower by different lenders. Each of those loans is considered a separate instrument.

Activity to Date (issues previously addressed by the SAPWG, Emerging Accounting Issues WG, SEC, FASB, other State Departments of Insurance or other NAIC groups): The Investment Classification Project is addressed in agenda item 2013-36. However, per request of the Working Group, subsequent issues addressed pursuant to that project will have new agenda item references. These items will identify that they are captured within the direction of the “Investment Classification Project” originally detailed in agenda item 2013-36. Information or issues (included in Description of Issue) not previously contemplated by the SAPWG: None Convergence with International Financial Reporting Standards (IFRS): Not Applicable Staff Recommendation: Staff recommends that the Working Group move this item to the active listing, classified as nonsubstantive, and expose revisions to clarify that a reporting entity providing a mortgage loan as a “participant in a mortgage loan agreement” (as defined in this Form A - reflecting one borrower, with more-than-one lender in an agreement that does not reflect a “securitization of assets”) shall consider the mortgage loan in scope of SSAP No. 37. In addition to clarifying that these mortgage loans are not securities and in scope of SSAP No. 37, revisions are proposed to clarify the impairment assessment for these mortgage loans and incorporate disclosures for these structures.

Attachment A Ref #2016-39

© 2016 National Association of Insurance Commissioners 6

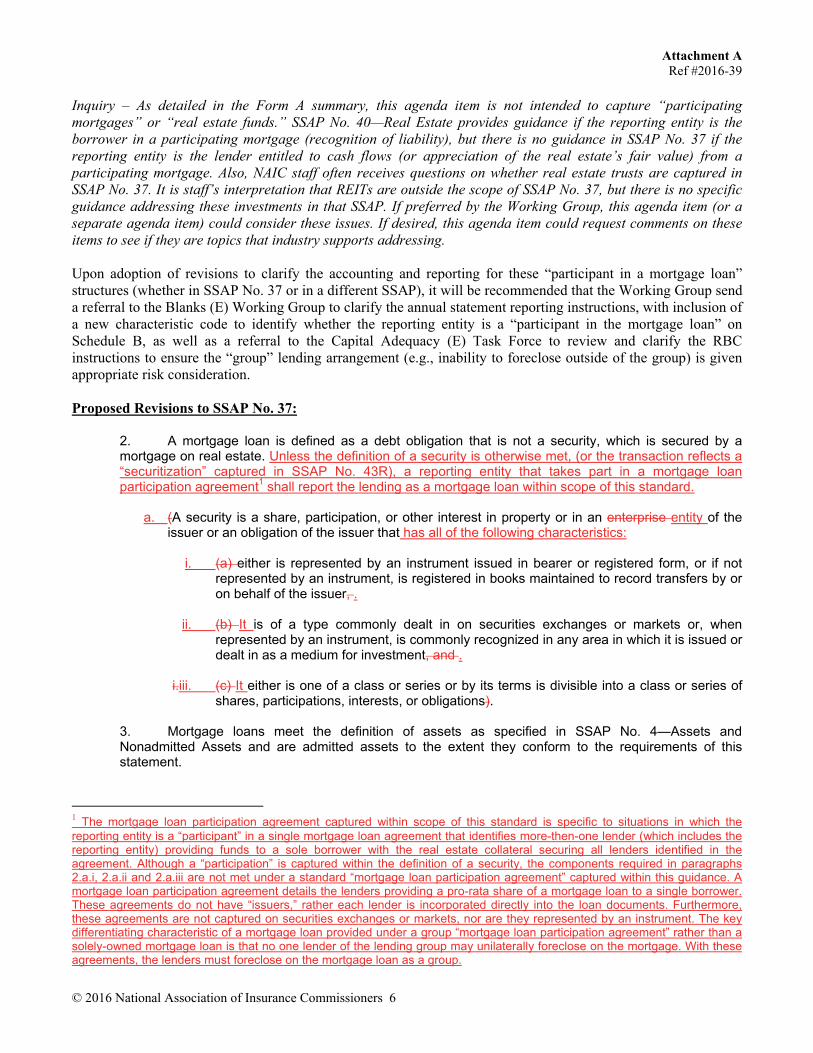

Inquiry – As detailed in the Form A summary, this agenda item is not intended to capture “participating mortgages” or “real estate funds.” SSAP No. 40—Real Estate provides guidance if the reporting entity is the borrower in a participating mortgage (recognition of liability), but there is no guidance in SSAP No. 37 if the reporting entity is the lender entitled to cash flows (or appreciation of the real estate’s fair value) from a participating mortgage. Also, NAIC staff often receives questions on whether real estate trusts are captured in SSAP No. 37. It is staff’s interpretation that REITs are outside the scope of SSAP No. 37, but there is no specific guidance addressing these investments in that SSAP. If preferred by the Working Group, this agenda item (or a separate agenda item) could consider these issues. If desired, this agenda item could request comments on these items to see if they are topics that industry supports addressing. Upon adoption of revisions to clarify the accounting and reporting for these “participant in a mortgage loan” structures (whether in SSAP No. 37 or in a different SSAP), it will be recommended that the Working Group send a referral to the Blanks (E) Working Group to clarify the annual statement reporting instructions, with inclusion of a new characteristic code to identify whether the reporting entity is a “participant in the mortgage loan” on Schedule B, as well as a referral to the Capital Adequacy (E) Task Force to review and clarify the RBC instructions to ensure the “group” lending arrangement (e.g., inability to foreclose outside of the group) is given appropriate risk consideration. Proposed Revisions to SSAP No. 37:

2. A mortgage loan is defined as a debt obligation that is not a security, which is secured by a mortgage on real estate. Unless the definition of a security is otherwise met, (or the transaction reflects a “securitization” captured in SSAP No. 43R), a reporting entity that takes part in a mortgage loan participation agreement1 shall report the lending as a mortgage loan within scope of this standard.

a. (A security is a share, participation, or other interest in property or in an enterprise entity of the

issuer or an obligation of the issuer that has all of the following characteristics:

i. (a) either is represented by an instrument issued in bearer or registered form, or if not represented by an instrument, is registered in books maintained to record transfers by or on behalf of the issuer, .

ii. (b) It is of a type commonly dealt in on securities exchanges or markets or, when represented by an instrument, is commonly recognized in any area in which it is issued or dealt in as a medium for investment, and .

i.iii. (c) It either is one of a class or series or by its terms is divisible into a class or series of shares, participations, interests, or obligations).

3. Mortgage loans meet the definition of assets as specified in SSAP No. 4—Assets and Nonadmitted Assets and are admitted assets to the extent they conform to the requirements of this statement.

1 The mortgage loan participation agreement captured within scope of this standard is specific to situations in which the reporting entity is a “participant” in a single mortgage loan agreement that identifies more-then-one lender (which includes the reporting entity) providing funds to a sole borrower with the real estate collateral securing all lenders identified in the agreement. Although a “participation” is captured within the definition of a security, the components required in paragraphs 2.a.i, 2.a.ii and 2.a.iii are not met under a standard “mortgage loan participation agreement” captured within this guidance. A mortgage loan participation agreement details the lenders providing a pro-rata share of a mortgage loan to a single borrower. These agreements do not have “issuers,” rather each lender is incorporated directly into the loan documents. Furthermore, these agreements are not captured on securities exchanges or markets, nor are they represented by an instrument. The key differentiating characteristic of a mortgage loan provided under a group “mortgage loan participation agreement” rather than a solely-owned mortgage loan is that no one lender of the lending group may unilaterally foreclose on the mortgage. With these agreements, the lenders must foreclose on the mortgage loan as a group.

Attachment A Ref #2016-39

© 2016 National Association of Insurance Commissioners 7

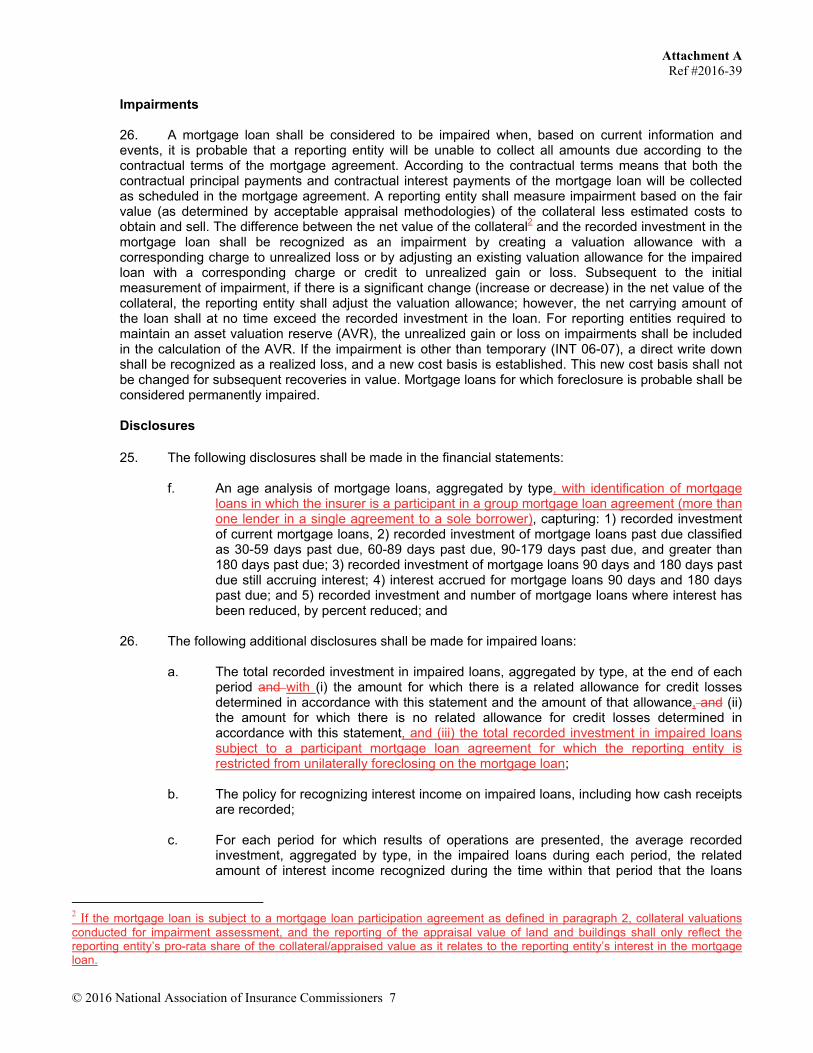

Impairments 26. A mortgage loan shall be considered to be impaired when, based on current information and events, it is probable that a reporting entity will be unable to collect all amounts due according to the contractual terms of the mortgage agreement. According to the contractual terms means that both the contractual principal payments and contractual interest payments of the mortgage loan will be collected as scheduled in the mortgage agreement. A reporting entity shall measure impairment based on the fair value (as determined by acceptable appraisal methodologies) of the collateral less estimated costs to obtain and sell. The difference between the net value of the collateral2 and the recorded investment in the mortgage loan shall be recognized as an impairment by creating a valuation allowance with a corresponding charge to unrealized loss or by adjusting an existing valuation allowance for the impaired loan with a corresponding charge or credit to unrealized gain or loss. Subsequent to the initial measurement of impairment, if there is a significant change (increase or decrease) in the net value of the collateral, the reporting entity shall adjust the valuation allowance; however, the net carrying amount of the loan shall at no time exceed the recorded investment in the loan. For reporting entities required to maintain an asset valuation reserve (AVR), the unrealized gain or loss on impairments shall be included in the calculation of the AVR. If the impairment is other than temporary (INT 06-07), a direct write down shall be recognized as a realized loss, and a new cost basis is established. This new cost basis shall not be changed for subsequent recoveries in value. Mortgage loans for which foreclosure is probable shall be considered permanently impaired.

Disclosures

25. The following disclosures shall be made in the financial statements:

f. An age analysis of mortgage loans, aggregated by type, with identification of mortgage loans in which the insurer is a participant in a group mortgage loan agreement (more than one lender in a single agreement to a sole borrower), capturing: 1) recorded investment of current mortgage loans, 2) recorded investment of mortgage loans past due classified as 30-59 days past due, 60-89 days past due, 90-179 days past due, and greater than 180 days past due; 3) recorded investment of mortgage loans 90 days and 180 days past due still accruing interest; 4) interest accrued for mortgage loans 90 days and 180 days past due; and 5) recorded investment and number of mortgage loans where interest has been reduced, by percent reduced; and

26. The following additional disclosures shall be made for impaired loans:

a. The total recorded investment in impaired loans, aggregated by type, at the end of each period and with (i) the amount for which there is a related allowance for credit losses determined in accordance with this statement and the amount of that allowance, and (ii) the amount for which there is no related allowance for credit losses determined in accordance with this statement, and (iii) the total recorded investment in impaired loans subject to a participant mortgage loan agreement for which the reporting entity is restricted from unilaterally foreclosing on the mortgage loan;

b. The policy for recognizing interest income on impaired loans, including how cash receipts

are recorded; c. For each period for which results of operations are presented, the average recorded

investment, aggregated by type, in the impaired loans during each period, the related amount of interest income recognized during the time within that period that the loans

2 If the mortgage loan is subject to a mortgage loan participation agreement as defined in paragraph 2, collateral valuations conducted for impairment assessment, and the reporting of the appraisal value of land and buildings shall only reflect the reporting entity’s pro-rata share of the collateral/appraised value as it relates to the reporting entity’s interest in the mortgage loan.

Attachment A Ref #2016-39

© 2016 National Association of Insurance Commissioners 8

were impaired, the recorded investments on nonaccrual status pursuant to SSAP No. 34, paragraph 6 and, unless not practicable, the amount of interest income recognized using a cash-basis method of accounting during the time within that period that the loans were impaired; and

d. For each period for which results of operations are presented, the activity in the

allowance for credit losses account, including the balance in the allowance for credit losses account at the beginning and end of each period, additions charged to operations, direct write-downs charged against the allowance, and recoveries of amounts previously charged off.

Staff Review Completed by: Julie Gann - NAIC Staff, October 2016 G:\DATA\Stat Acctg\3. National Meetings\A. National Meeting Materials\2016\Fall\Meeting\A - 16-39 - Mortgage Loan Multiple Lenders.docx

Attachment B Ref# 2016-40

© 2016 National Association of Insurance Commissioners 1

Statutory Accounting Principles (E) Working Group Maintenance Agenda Submission Form

Form A

Issue: Definition of LBSS Check (applicable entity): P/C Life Health

Modification of existing SSAP New Issue or SSAP Interpretation

Description of Issue: The Investment Classification Project (detailed in agenda item #2013-36) supported a review of the investment SSAPs to address a variety of application questions, mostly focusing on definitions and scope limitations of each of the noted SSAPs. SSAP No. 43R—Loan-backed and Structured Securities (SSAP No. 43R) was originally identified as a SSAP to review within the Investment Classification Project. Pursuant to the original project focus, the assessment of SSAP No. 43R is intended to include a review of definitions for the investments within scope, and to verify whether investments are being appropriately included (or excluded) from that standard. As the SAPWG initially focused on revisions to SSAP No. 26—Bonds under the Investment Classification Project in 2016, the Valuation of Securities (E) Task Force undertook a project to assist with reviewing the definitions for loan-backed and structured securities (LBSS) captured in SSAP No. 43R. In initiating this review, the Task Force identified that they have significant interest in SSAP No. 43R and would propose revised definitions, which may address industry concerns, pursuant to the SVO and Structured Securities Group (SSG) perspective. On June 10, 2016, the Task Force submitted a referral to the Working Group proposing definition changes for SSAP No. 43R investments. The proposed definitions focus on the collateral pool as the source of dynamic cash flow. As detailed in the referral, the Task Force recommends a change for SSAP No. 43R securities, broadly referred to as “structured finance securities,” to recognize that a dynamic cash flow pattern is the result of a specific structural construct, which includes all of the following:

• Legal isolation and pooling of a finite number of cash generating assets. • Each cash generating asset from a different obligor, • Cash generating assets are held in a trust, • Cash flows from the cash generating assets are used to pay the security holders.

In developing the recommended definition, the Task Force first exposed their proposed definition for comment in April 2016. The Task Force’s adopted definition, detailed in the June 2016 referral, reflects the exposed definition modified to incorporate comments received by the ACLI. Upon adoption of the definition, the Task Force agreed to recommend the proposed definition to the Statutory Accounting Principles (E) Working Group for consideration into SSAP No. 43R. VOSTF Proposed Definition (from May 17, 2016 memo) Modified to Reflect ACLI’s Comments: (Italics reflect changes incorporated from the ACLI comments.)

• Loan-backed securities and structured securities are more broadly characterized as structured finance securities.

• In a structured finance security, an issuer, typically an SPE): 1) sells loan-backed or structured securities

and uses the proceeds of the sale to purchase a pool of assets associated with multiple unrelated obligors, including derivatives, from one or more originators; and 2) places the such assets within a trust that serves as trustee for the benefit of the holders of the loan-backed or structured securities, with

Attachment B Ref# 2016-40

© 2016 National Association of Insurance Commissioners 2

instructions that the trustee use the cash flow generated by the assets to pay the holders of the SPE’s loan -backed or structured securities.

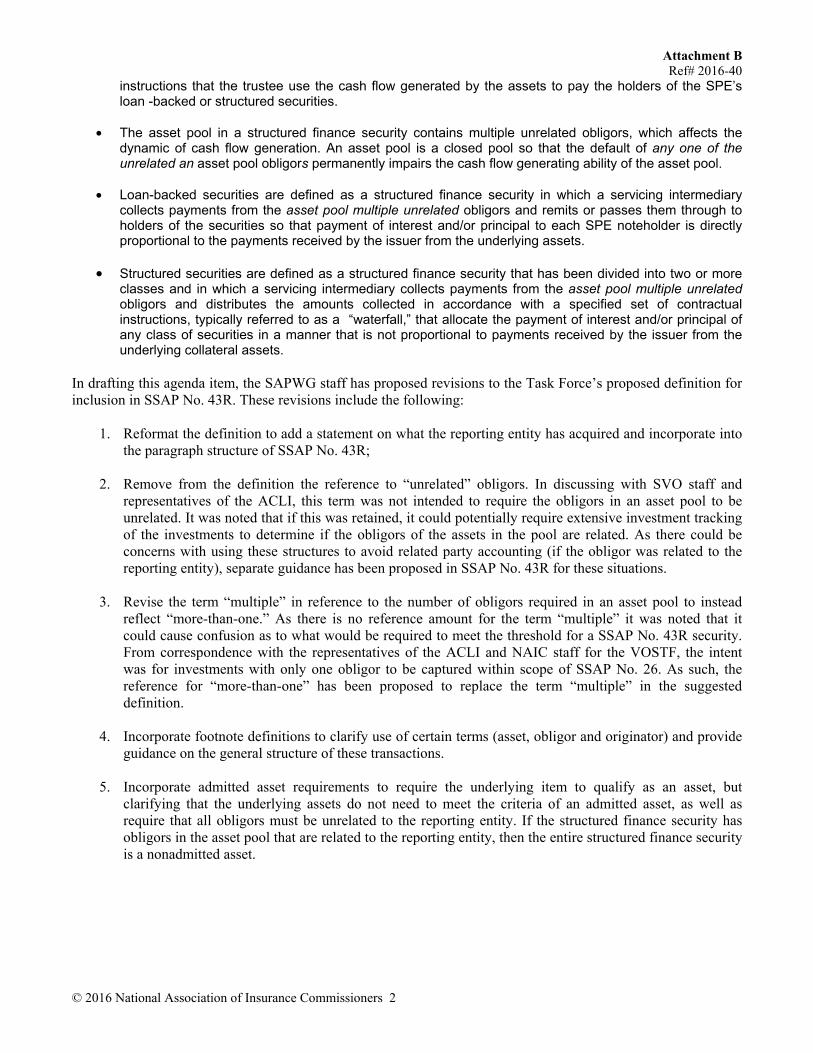

• The asset pool in a structured finance security contains multiple unrelated obligors, which affects the

dynamic of cash flow generation. An asset pool is a closed pool so that the default of any one of the unrelated an asset pool obligors permanently impairs the cash flow generating ability of the asset pool.

• Loan-backed securities are defined as a structured finance security in which a servicing intermediary

collects payments from the asset pool multiple unrelated obligors and remits or passes them through to holders of the securities so that payment of interest and/or principal to each SPE noteholder is directly proportional to the payments received by the issuer from the underlying assets.

• Structured securities are defined as a structured finance security that has been divided into two or more

classes and in which a servicing intermediary collects payments from the asset pool multiple unrelated obligors and distributes the amounts collected in accordance with a specified set of contractual instructions, typically referred to as a “waterfall,” that allocate the payment of interest and/or principal of any class of securities in a manner that is not proportional to payments received by the issuer from the underlying collateral assets.

In drafting this agenda item, the SAPWG staff has proposed revisions to the Task Force’s proposed definition for inclusion in SSAP No. 43R. These revisions include the following:

1. Reformat the definition to add a statement on what the reporting entity has acquired and incorporate into the paragraph structure of SSAP No. 43R;

2. Remove from the definition the reference to “unrelated” obligors. In discussing with SVO staff and representatives of the ACLI, this term was not intended to require the obligors in an asset pool to be unrelated. It was noted that if this was retained, it could potentially require extensive investment tracking of the investments to determine if the obligors of the assets in the pool are related. As there could be concerns with using these structures to avoid related party accounting (if the obligor was related to the reporting entity), separate guidance has been proposed in SSAP No. 43R for these situations.

3. Revise the term “multiple” in reference to the number of obligors required in an asset pool to instead reflect “more-than-one.” As there is no reference amount for the term “multiple” it was noted that it could cause confusion as to what would be required to meet the threshold for a SSAP No. 43R security. From correspondence with the representatives of the ACLI and NAIC staff for the VOSTF, the intent was for investments with only one obligor to be captured within scope of SSAP No. 26. As such, the reference for “more-than-one” has been proposed to replace the term “multiple” in the suggested definition.

4. Incorporate footnote definitions to clarify use of certain terms (asset, obligor and originator) and provide guidance on the general structure of these transactions.

5. Incorporate admitted asset requirements to require the underlying item to qualify as an asset, but clarifying that the underlying assets do not need to meet the criteria of an admitted asset, as well as require that all obligors must be unrelated to the reporting entity. If the structured finance security has obligors in the asset pool that are related to the reporting entity, then the entire structured finance security is a nonadmitted asset.

Attachment B Ref# 2016-40

© 2016 National Association of Insurance Commissioners 3

Excerpts from Agenda Item 2013-36: Investment Classification Project: (Identified SSAP No. 43R definitions and scope as key elements to consider.)

SSAP No. 43R—Loan-backed and Structured Securities Key Elements:

1. The cash flow assessments required within SSAP No. 43R have been misinterpreted for single-payer investments (e.g., equipment-trust certificates, credit tenant loans).

2. The definition of beneficial interests includes items that may be in the form of debt and equity. Items that resemble equity-interests do not fit in the definition of a loan-backed and structured security, but they are included in SSAP No. 43R.

3. Additional securities may be eligible to be financially modeled, but the determination of NAIC designation as a result of financial modeling is only addressed for loan-backed and structured securities.

Possible Options: A. Incorporate guidance to clarify the scope of SSAP No. 43R.

B. Consider accounting and reporting guidance in accordance with the review of other

investments conducted as part of this project.

Existing Authoritative Literature: SSAP No. 43R—Loan-backed and Structured Securities includes the following definitions:

2. Loan-backed securities are defined as securitized assets not included in structured securities, as

defined below, for which the payment of interest and/or principal is directly proportional to the payments received by the issuer from the underlying assets, including but not limited to pass-through securities, lease-backed securities, and equipment trust certificates.

3. Structured securities are defined as loan-backed securities which have been divided into two or more classes for which the payment of interest and/or principal of any class of securities has been allocated in a manner which is not proportional to payments received by the issuer from the underlying assets.

4. Loan-backed securities are issued by special-purpose corporations or trusts (issuer) established by a sponsoring organization. The assets securing the loan-backed obligation are acquired by the issuer and pledged to an independent trustee until the issuer’s obligation has been fully satisfied. The investor only has direct recourse to the issuer’s assets, but may have secondary recourse to third parties through insurance or guarantee for repayment of the obligation. As a result, the sponsor and its other affiliates may have no financial obligation under the instrument, although one of those entities may retain the responsibility for servicing the underlying assets. Some sponsors do guarantee the performance of the underlying assets.

U.S. GAAP – per the FASB Codification, Mortgage Backed Securities are defined as follows: (This definition is not adopted for SAP.)

Mortgage-Backed Securities (ASC Topic 948) – Securities issued by a governmental agency or corporation (for example, Government National Mortgage Association [GNMA] or Federal Home Loan Mortgage Corporation [FHLMC]) or by private issuers (for example, Federal National Mortgage Association [FNMA], banks, and mortgage banking entities). Mortgage-backed securities generally are referred to as mortgage participation certificates or pass-through certificates. A participation certificate represents an undivided interest in a pool of specific mortgage loans. Periodic payments on GNMA

Attachment B Ref# 2016-40

© 2016 National Association of Insurance Commissioners 4

participation certificates are backed by the U.S. government. Periodic payments on FHLMC and FNMA certificates are guaranteed by those corporations, but are not backed by the U.S. government.

(Definitions for asset-backed security, loan-backed security, or structured security were not found in the FASB Codification.)

SEC - Includes the following information for Asset-Backed Securities: (This information is not adopted in SAP.)

Asset-backed securities, or ABS, are securities that are backed by a discrete pool of self-liquidating financial assets. Asset-backed securitization is a financing technique in which financial assets, in many cases themselves less liquid, are pooled and converted into instruments that may be offered and sold more freely in the capital markets. In a basic securitization structure, an entity, often a financial institution and commonly known as a “sponsor,” originates or otherwise acquires a pool of financial assets, such as mortgage loans, directly or through an affiliate. It then sells the financial assets to a specially created investment vehicle that issues securities backed by those financial assets, which are “asset-backed securities.” Payment on the asset-backed securities depends primarily on the cash flows generated by the assets in the underlying pool and other rights designed to assure timely payment, such as guarantees or other features generally known as credit enhancements. The structure of asset-backed securities is intended, among other things, to insulate ABS investors from the corporate credit risk of the sponsor that originated or acquired the financial assets. Asset-backed securities are created by buying and bundling loans – such as residential mortgage loans, commercial mortgage loans or auto loans and leases – and creating securities backed by those assets that are then sold to investors. Often a bundle of loans is divided into separate securities with different levels of risk and returns. Payments on the loans are distributed to the holders of the lower-risk, lower-interest securities first, and then to the holders of the higher-risk securities. Most public offerings of ABS are conducted through expedited SEC procedures known as “shelf offerings.”

Activity to Date (issues previously addressed by the SAPWG, Emerging Accounting Issues WG, SEC, FASB, other State Departments of Insurance or other NAIC groups): The Investment Classification Project is addressed in agenda item 2013-36. However, per request of the Working Group, subsequent issues addressed pursuant to that project will have new agenda item references. These items will identify that they are captured within the direction of the “Investment Classification Project” originally detailed in agenda item 2013-36.

Information or issues (included in Description of Issue) not previously contemplated by the SAPWG: None

Convergence with International Financial Reporting Standards (IFRS): N/A

Staff Recommendation: Staff recommends that the Working Group receive the referral from the Valuation of Securities (E) Task Force, move this agenda item to the active listing, categorized as substantive, and expose revisions to SSAP No. 43R (with limited revisions to other SSAPs). As further detailed, this agenda item requests comments on the overall proposed change, and the securities that will be impacted if these revisions are adopted.

Key revisions reflected in the initial exposure include:

1. Revised definitions for investments within scope of SSAP No. 43R.

2. A title change of SSAP No. 43R as well as a broad change from LBSS to “structured finance security” throughout the SSAP.

3. Revisions to clarify admitted asset requirements.

4. Revisions to update the “effective” date guidance – removing explicit guidance on transition from the adoption of the 2009 SSAP No. 43R substantive revisions.

Attachment B Ref# 2016-40

© 2016 National Association of Insurance Commissioners 5

5. Update to the Q&A to remove outdated guidance, mostly pertaining to the 2009 transition, but also removing issues subsequently addressed or revised in the SSAP.

Under the proposed definition, it is intended that securities with a single-obligor will no longer be in scope of SSAP No. 43R, but will instead be captured within SSAP No. 26 (proposed revisions also clarify this change in SSAP No. 26.) Comments are requested on this proposed change, whether the proposed definition adds or removes other securities from the scope of SSAP No. 43R, and if there are any unintended consequences from incorporating the revised definition into SSAP No. 43R. Comments are also requested on other aspects of SSAP No. 43R that should be reviewed under the Investment Classification Project, with a specific inquiry on the continued inclusion of past effective date / transition guidance as well as the Q&A Implementation Guide.

• Commenters providing information on the impact to securities from the proposed definition are requested

to provide detailed information on the security, including where it was previously reported (if not previously in scope) or where it would subsequently be captured (if no longer in scope) if the proposed definition for SSAP No. 43R is adopted.

• Commenters are requested to provide information regarding the need to retain effective date and transition guidance from initial application of the 2009 substantive revisions, and whether there are concerns with the proposed deletion of transition-related questions from Appendix A - Question and Answer Implementation Guide in SSAP No. 43R.

With exposure of the proposed revisions to SSAP No. 43R, staff recommends a referral to the Structured Securities Group (SSG) to verify that the inclusion of the proposed definition will not impact the scope of securities captured within the financial modeling process. If the revised definition is adopted, referrals to the Blanks (E) Working Group and the Valuation of Securities (E) Task Force would be recommended so that the terminology is updated in all NAIC publications.

As the proposed revisions will result with some securities being classified to a different SSAP, staff has proposed for the revisions to be considered substantive. To facilitate initial discussion, proposed revisions are shown in the agenda item for initial exposure. However staff recommends that the Working Group proceed with directing NAIC staff to draft an issue paper for historical purposes.

Staff Note: It is anticipated that a request may be subsequently received to reconsider the “modified filing exempt” guidance currently included in SSAP No. 43R from the Structured Securities Group (SSG). Revisions to that guidance are not proposed to be included in this agenda item, and if requested, will be considered in a separate agenda item.

Staff Review Completed by: Julie Gann - NAIC Staff, September 2016

Proposed Revisions to SSAP No. 43R

SCOPE OF STATEMENT

1. This statement establishes statutory accounting principles for investments in loan-backed securities and structured securitiesstructured finance securities. In accordance with SSAP No. 103R—Transfers and Servicing of Financial Assets and Extinguishments of Liabilities (SSAP No. 103R), retained beneficial interests from the sale of loan-backed securities and structured securitiesstructured finance securities are accounted for in accordance with this statement. In this statement loan-backed securities and structured securities are collectively referred to as loan-backed securitiesstructured finance securities.

SUMMARY CONCLUSION

Attachment B Ref# 2016-40

© 2016 National Association of Insurance Commissioners 6

2. A reporting entity’s investment in a structured finance security reflects the acquisition of a loan-backed or structured security, often issued by an special purpose entity (SPE), that reflects the right for the reporting entity to receive future cash flows generated from a pool of assets1, associated with multiple more-than-one obligor2, held in trust:

a. Issuer acquires a pool of assets, including derivatives, associated with multiple more-than-one obligor from one or more originators3.

b. Issuer places the pool of assets within a trust for the benefit of the holders of the structured finance security, with instructions that the trustee use the cash flow generated by the assets to pay the holders of the structured finance security.

3. The asset pool in a structured finance security contains multiple unrelated more-than-one obligor, which affects the dynamic of cash flow generation. An asset pool is a closed pool so that the default of any one of the unrelatedasset pool obligors permanently impairs the cash flow generating ability of the asset pool.

4. Loan-backed securities are defined as a structured finance security in which a servicing intermediary collects payments from the multiple unrelated obligors (more-than-one) and remits or passes them through to holders of the securities so that payment of interest and/or principal to each SPE noteholder is directly proportional to the payments received by the issuer from the underlying assets.

5. Structured securities are defined as a structured finance security that has been divided into two or more classes and in which a servicing intermediary collects payments from the multiple unrelated obligors (more-than-one) and distributes the amounts collected in accordance with a specified set of contractual instructions, typically referred to as a “waterfall,” that allocate the payment of interest and/or principal of any class of securities in a manner that is not proportional to payments received by the issuer from the underlying collateral assets.

2. Loan-backed securities are defined as securitized assets not included in structured securities, as defined below, for which the payment of interest and/or principal is directly proportional to the payments received by the issuer from the underlying assets, including but not limited to pass-through securities, lease-backed securities, and equipment trust certificates.

3. Structured securities are defined as loan-backed securities which have been divided into two or more classes for which the payment of interest and/or principal of any class of securities has been allocated in a manner which is not proportional to payments received by the issuer from the underlying assets.

4. Loan-backed securities are issued by special-purpose corporations or trusts (issuer) established by a sponsoring organization. The assets securing the loan-backed obligation are acquired by the issuer and pledged to an independent trustee until the issuer’s obligation has been fully satisfied. The investor only has direct recourse to the issuer’s assets, but may have secondary recourse to

1 The term “assets” refers to items meeting the asset definition in SSAP No. 4, paragraph 2. It is not permissible to securitize or establish a structured finance security for underlying items that do not qualify as assets. For example, it is not permissible to securitize future cash flows from a “management service contract” for services that will be provided in the future. The management service contract does not qualify as a recognizable asset.

2 The “obligor” is the underlying borrower. For a mortgage-backed security, the obligor obtains the mortgage from the originator and is responsible for principle and interest payments under the terms of the mortgage. With a securitization of cash flows, the obligor has sold the right to collect a specific set of future cash flows (e.g., rent from commercial office building).

3 The “originator” (often a bank) provides the initial loan or funds to the obligor. For a mortgage-backed security, the originator provides the mortgage. With a securitization of cash flows, the originator has purchased the right to collect future cash flows. The originator sells these loans/rights to cash flows to the issuer (SPE). The issuer then pools the acquired assets and issues loan-backed or structured securities representing rights to the expected cash flows (repayment of loan or cash receipts) from the obligors.

Attachment B Ref# 2016-40

© 2016 National Association of Insurance Commissioners 7

third parties through insurance or guarantee for repayment of the obligation. As a result, the sponsor and its other affiliates may have no financial obligation under the instrument, although one of those entities may retain the responsibility for servicing the underlying assets. Some sponsors do guarantee the performance of the underlying assets.

6. Loan-backed and structuredStructured finance securities meet the definition of assets as defined in SSAP No. 4—Assets and Nonadmitted Assets and are admitted assets to the extent they conform to the requirements of this statement.

a. In a structured finance security, the underlying assets in the asset pool generating the cash flows must meet the definition of an asset in SSAP No. 4, but do not need to qualify as admitted assets in order for the structured finance security to be an admitted asset. For example, a structured finance security representing expected cash flows from lease payments generated from an underlying asset pool of aircraft may be an admitted asset even though aircraft held directly by the reporting entity would be considered a nonadmitted asset.

b. A reporting entity shall not admit any structured finance securities involving assets related to insurance products or premiums (such as life settlements).

b.c. It is the intent to prohibit use of structured finance securities as a means to engage in related party transactions. Transactions involving related parties shall follow the guidance in SSAP No. 25. In the event a structure finance security is identified as a mechanism to engage in related-party transactions, the structured finance security shall be nonadmitted4.

5.7. The scope of this statement encompasses all types of loan-backed and structured finance securities, including, but not limited to, the following:

a. Loan-backed and sStructured finance securities acquired at origination,

b. Loan-backed and sStructured finance securities acquired subsequent to origination for which it is probable, at acquisition, that the reporting entity will be able to collect all contractually required payments receivable, and are accounted for at acquisition under SSAP No. 103R,

c. Loan-backed and sStructured finance securities for which it is probable, either known at acquisition or identified during the holding period5, that the reporting entity will be unable to collect all contractually required payments receivable, and

d. Transferor’s beneficial interests in securitization transactions that are accounted for as sales under SSAP No. 103R and purchased beneficial interests in securitized financial assets6.

6.8. At acquisition, loan-backed and structured finance securities, except for loan-backed or structured finance securities that are beneficial interests that are not of high credit quality or can contractually be prepaid or otherwise settled in such a way that the reporting entity would not recover substantially all of its recorded amount7 (see paragraphs 19-2322-25), shall be reported at cost, including brokerage and related fees. Acquisitions and dispositions shall be recorded

4 Nonadmittance is required to prevent structured finance securities from being used as a way to circumvent statutory accounting provisions for related party transactions.

5 Securities classified within the type of paragraph 67.a. or 67.b. may be required to change classification to type 67.c. when it becomes probable that the reporting entity will be unable to collect all contractually required payments receivable. 6 The accounting requirements related to these type of securities included in paragraphs 21-2422-25 shall be determined at acquisition or initial transfer. 7 As referenced in the Relevant Literature section, this statement adopts EITF 99-20, including the scope requirements of that guidance.

Attachment B Ref# 2016-40

© 2016 National Association of Insurance Commissioners 8

on the trade date, not the settlement date, except for the acquisition of private placement loan-backed and structured finance securities which shall be recorded on the funding date. For securities where all information is not known as of the trade date (e.g., actual payment factors and specific pools), a reporting entity shall make its best estimate based on known facts.

7.9. Amortization of premium or discount shall be calculated using the scientific (constant yield) interest method and shall be recorded as an adjustment to investment income.(INT 07-01) The interest method results in a constant effective yield equal to the prevailing rate at the time of purchase or at the time of subsequent adjustments to book value. The amortization period shall reflect estimates of the period over which repayment of principal of the loan-backed and structured finance securities is expected to occur, not the stated maturity period.

8.10. Interest shall be accrued using the effective-yield method using the redemption prices and redemption dates used for amortizing premiums and discounts. Interest income consists of interest collected during the period, the change in the due and accrued interest between the beginning and end of the period as well as reductions for premium amortization and interest paid on acquisition of loan-backed and structured finance securities, and the addition of discount accrual. Contingent interest may be accrued if the applicable provisions of the underlying contract and the prerequisite conditions have been met.

9.11. For reporting entities required to maintain an IMR, the accounting for realized capital gains and

losses on sales of loan-backed and structured securities shall be in accordance with SSAP No. 7—Asset Valuation Reserve and Interest Maintenance Reserveparagraph 38 of this statement. For reporting entities not required to maintain an IMR, realized gains and losses on sales of loan-backed and structured securities shall be recorded on the trade date and shall be reported as net realized capital gains or losses in the Statement of Income. (Drafting Note: Revised to be consistent with paragraph 29 and 38.)

10.12. A loan-backed or structured finance security may provide for a prepayment penalty or

acceleration fee in the event the investment is liquidated prior to its scheduled termination date. These fees shall be reported as investment income when received.

11.13. The amount of prepayment penalty and/or acceleration fees to be reported as investment income shall be calculated as follows:

a. The amount of investment income reported is equal to the total proceeds (consideration) received less the Par value of the investment; and

a. Any difference between the book adjusted carrying value (BACV) and the Par Value at the time of disposal shall be reported as realized capital gains and losses subject to the authoritative literature in SSAP No. 7.

Collection of All Contractual Cashflows is Probable

12.14. The following guidance applies to loan-backed and structured finance securities for which it is probable that the investor will be able to collect all contractually required payments receivable. (Paragraphs 18-2019-21 provide guidance for structured finance securities in which collection of all contractual cash flows is not probable and paragraphs 21-2422-25 provide guidance for beneficial interests.) Prepayments are a significant variable element in the cash flow of loan-backed and structured finance securities because they affect the yield and determine the expected maturity against which the yield is evaluated. Falling interest rates generate faster prepayment of the mortgagesassets (e.g., mortgages) underlying the security, shortening its duration. This causes the reporting entity to reinvest assets sooner than expected at potentially less advantageous rates. This is called prepayment risk. Extension risk is created by rising interest rates which slow repayment and can significantly lengthen the duration of the security. Differences in cash flows can also result from other changes in the cash flows from the underlying assets. If assets are delinquent or otherwise not generating cash flow, which this should be reflected in the cash flow analysis through diminishing security cash flows, even if assets have not been liquidated and gain/losses have not been booked.

Attachment B Ref# 2016-40

© 2016 National Association of Insurance Commissioners 9

13.15. Changes in currently estimated cash flows, including the effect of prepayment assumptions, on

loan-backed and structured finance securities shall be reviewed periodically, at least quarterly. The prepayment rates of the underlying loans shall be used to determine prepayment assumptions. Prepayment assumptions shall be applied consistently across portfolios to all securities backed by similar collateral (similar with respect to coupon, issuer, and age of collateral). Reporting entities shall use consistent assumptions across portfolios for similar collateral within controlled affiliated groups. Since each reporting entity may have a unique method for determining the prepayment assumptions, it is impractical to set standard assumptions for the industry. Relevant sources and rationale used to determine each prepayment assumption shall be documented by the reporting entity.

14.16. Loan-backed and sStructured finance securities shall be revalued using the currently estimated cash flows, including new prepayment assumptions, using either the prospective or retrospective adjustment methodologies, consistently applied by type of securities. However, if at any time during the holding period, the reporting entity determines it is no longer probable that they will collect all contractual cashflows, the reporting entity shall apply the accounting requirements in paragraphs 18-2019-21.

15.17. The prospective approach recognizes, through the recalculation of the effective yield to be applied to future periods, the effects of all cash flows whose amounts differ from those estimated earlier and the effects and changes in projected cash flows. Under the prospective method, the recalculated effective yield will equate the carrying amount of the investment to the present value of the anticipated future cash flows. The recalculated yield is then used to accrue income on the investment balance for subsequent accounting periods. There are no accounting changes in the current period unless the security is determined to be other than temporarily impaired.

16.18. The retrospective methodology changes both the yield and the asset balance so that expected future cash flows produce a return on the investment equal to the return now expected over the life of the investment as measured from the date of acquisition. Under the retrospective method, the recalculated effective yield will equate the present value of the actual and anticipated cash flows with the original cost of the investment. The current balance is then increased or decreased to the amount that would have resulted had the revised yield been applied since inception, and investment income is correspondingly decreased or increased.

Collection of All Contractual Cashflows is Not Probable

17.19. The following guidance applies to loan-backed and structured finance securities with evidence of deterioration of credit quality since origination for which it is probable, either known at acquisition or identified during the holding period, that the investor will be unable to collect all contractually required payments receivable, except for those beneficial interests that are not of high credit quality or can contractually be prepaid or otherwise settled in such a way that the reporting entity would not recover substantially all of its recorded amount determined at acquisition (see paragraphs 21-2422-25).

18.20. The reporting entity shall recognize the excess of all cash flows expected at acquisition over the investor’s initial investment in the loan-backed or structured finance security as interest income on an effective-yield basis over the life of the loan-backed or structured finance security (accretable yield).8 Any excess of contractually required cash flows over the cash flows expected to be collected is the nonaccretable difference. Expected prepayments shall be

8 A loan-backed or structured finance security may be acquired at a discount because of a change in credit quality or rate or both. When a loan-backed or structured finance security is acquired at a discount that relates, at least in part, to the security’s credit quality, the effective interest rate is the discount rate that equates the present value of the investor’s estimate of the security’s future cash flows with the purchase price of the loan-backed or structured finance security.

Attachment B Ref# 2016-40

© 2016 National Association of Insurance Commissioners 10

treated consistently for determining cash flows expected to be collected and projections of contractual cash flows such that the nonaccretable difference is not affected. Similarly, the difference between actual prepayments and expected prepayments shall not affect the nonaccretable difference.

19.21. An investor shall continue to estimate cash flows expected to be collected over the life of the loan-backed or structured finance security. If, upon subsequent evaluation:

a. The fair value of the loan-backed or structured finance security has declined below its

amortized cost basis, an entity shall determine whether the decline is other than temporary (INT 06-07). For example, if, based on current information and events, there is a decrease in cash flows expected to be collected (that is, the investor is unable to collect all cash flows expected at acquisition plus any additional cash flows expected to be collected arising from changes in estimate after acquisition (in accordance with paragraph 2021.b.), an other-than-temporary impairment shall be considered to have occurred. The investor shall consider both the timing and amount of cash flows expected to be collected in making a determination about whether there has been a decrease in cash flows expected to be collected.

b. Based on current information and events, if there is a significant increase in cash flows

previously expected to be collected or if actual cash flows are significantly greater than cash flows previously expected, the investor shall recalculate the amount of accretable yield for the loan-backed or structured finance security as the excess of the revised cash flows expected to be collected over the sum of (1) the initial investment less (2) cash collected less (3) other-than-temporary impairments plus (4) amount of yield accreted to date. The investor shall adjust the amount of accretable yield by reclassification from nonaccretable difference. The adjustment shall be accounted for as a change in estimate in conformity with SSAP No. 3—Accounting Changes and Corrections of Errors (SSAP No. 3), with the amount of periodic accretion adjusted over the remaining life of the loan-backed or structured finance security (prospective method).

Beneficial Interests

20.22. Paragraphs 22-25 The following paragraphs provide statutory accounting guidance for interest income and impairment for a reporting entity that continues to hold an interest in securitized financial assets accounted for as sales under SSAP No. 103R, or that purchases a beneficial interest in securitized financial assets that are not of high credit quality or can contractually be prepaid or otherwise settled in such a way that the reporting entity would not recover substantially all of its recorded amount, determined at acquisition or the date of transfer9. Beneficial interests that are of high credit quality and cannot contractually be prepaid or otherwise settled in such a way that the reporting entity would not recover substantially all of its recorded investment, shall be accounted for in accordance with paragraphs 13-1714-18.

21.23. The reporting entity shall recognize the excess of all cash flows attributable to the beneficial

interest estimated at the acquisition/transaction date (referred to herein as the transaction date) over the initial investment (the accretable yield) as interest income over the life of the beneficial interest using the effective yield method. If the holder of the beneficial interest is the reporting entity that transferred the financial assets for securitization, the initial investment would be the fair value of the beneficial interest as of the date of transfer, as required by SSAP No. 103R. The amount of accretable yield shall not be displayed in the balance sheet.

22.24. The reporting entity that holds a beneficial interest shall continue to update the estimate of cash

flows over the life of the beneficial interest. If upon evaluation:

9 The accounting requirements related to these types of securities included in paragraphs 21-2422-25 shall be determined at acquisition or initial transfer. As referenced in the Relevant Literature section, this statement adopts EITF 99-20 (as amended by FAS 166), including the scope requirements of that guidance.

Attachment B Ref# 2016-40

© 2016 National Association of Insurance Commissioners 11

a. Based on current information and events it is probable that there is a favorable (or an

adverse) change in estimated cash flows from the cash flows previously projected, then the investor shall recalculate the amount of accretable yield for the beneficial interest on the date of evaluation as the excess of estimated cash flows over the beneficial interest’s reference amount (the reference amount is equal to (1) the initial investment less (2) cash received to date less (3) other-than-temporary impairments recognized to date [as described in paragraph 2324.b.] plus (4) the yield accreted to date. The adjustment shall be accounted for prospectively as a change in estimate in conformity with SSAP No. 3, with the amount of periodic accretion adjusted over the remaining life of the beneficial interest. Based on estimated cash flows, interest income may be recognized on a beneficial interest even if the net investment in the beneficial interest is accreted to an amount greater than the amount at which the beneficial interest could be settled if prepaid immediately in its entirety.

b. The fair value of the beneficial interest has declined below its reference amount; a

reporting entity shall determine whether the decline is other-than-temporary. If, based on current information and events it is probable that there has been an adverse change in estimated cash flows (in accordance with paragraph 2324.a.), then (1) an other-than-temporary impairment shall be considered to have occurred and (2) the beneficial interest shall be written down to the current estimate of cash flows at the financial reporting date discounted at a rate equal to the current yield used to accrete the beneficial interest with the resulting change being recognized as a realized loss. Determining whether there has been a favorable (or an adverse) change in estimated cash flows from the cash flows previously projected (taking into consideration both the timing and amount of the estimated cash flows) involves comparing the present value of the remaining cash flows as estimated at the initial transaction date (or at the last date previously revised) against the present value of the cash flows estimated at the current financial reporting date. The cash flows shall be discounted at a rate equal to the current yield used to accrete the beneficial interest. If the present value of the original cash flows estimated at the initial transaction date (or the last date previously revised) is less than the present value of the current estimate of cash flows expected to be collected, the change is considered favorable (that is, an other-than-temporary impairment shall be considered to have not occurred). If the present value of the original cash flows estimated at the initial transaction date (or the last date previously revised) is greater than the present value of the current estimated cash flows, the change is considered adverse (that is, an other-than-temporary impairment shall be considered to have occurred). However, absent any other factors that indicate an other-than-temporary impairment has occurred, changes in the interest rate of a “plain-vanilla,” variable-rate beneficial interest generally shall not result in the recognition of an other-than-temporary impairment10 (a plain-vanilla, variable-rate beneficial interest does not include those variable-rate beneficial interests with interest rate reset formulas that involve either leverage or an inverse floater).

23.25. All cash flows estimated at the transaction date are defined as the holder’s estimate of the

amount and timing of estimated future principal and interest cash flows used in determining the purchase price or the holder’s fair value determination for purposes of determining a gain or loss under SSAP No. 103R. Subsequent to the transaction date, estimated cash flows are defined as the holder’s estimate of the amount and timing of estimated principal and interest cash flows based on the holder’s best estimate of current information and events. A change in

10 Changes in the interest rate of a “plain-vanilla,” variable-rate beneficial interest (a plain-vanilla, variable-rate beneficial interest does not include those variable-rate beneficial interests with interest rate reset formulas that involve either leverage or an inverse floater) generally should not result in the recognition of an other-than-temporary impairment. For plain-vanilla, variable-rate beneficial interests, the yield is changed to reflect the revised interest rate based on the contractual interest rate reset formula. For example, if a beneficial interest pays interest quarterly at a rate equal to LIBOR plus 2 percent, the yield of that beneficial interest is changed prospectively to reflect changes in LIBOR. However, changes in the fair value of a plain-vanilla, variable-rate beneficial interest due to credit events should be considered when evaluating whether there has been an other-than-temporary impairment.

Attachment B Ref# 2016-40

© 2016 National Association of Insurance Commissioners 12

estimated cash flows is considered in the context of both timing and amount of the estimated cash flows.

Reporting Guidance for All Loan-Backed and Structured Finance Securities

24.26. Loan-backed and sStructured finance securities shall be valued and reported in accordance with this statement, the Purposes and Procedures Manual of the NAIC Investment Analysis Office, and the designation assigned in the NAIC Valuations of Securities product prepared by the NAIC Securities Valuation Office or equivalent specified procedure. The carrying value method shall be determined as follows:

a. For reporting entities that maintain an Asset Valuation Reserve (AVR), loan-backed and structured finance securities shall be reported at amortized cost, except for those with an NAIC designation of 6, which shall be reported at the lower of amortized cost or fair value.

b. For reporting entities that do not maintain an AVR, loan-backed and structured finance securities designated highest-quality and high-quality (NAIC designations 1 and 2, respectively) shall be reported at amortized cost; loan-backed and structured finance securities that are designated medium quality, low quality, lowest quality and in or near default (NAIC designations 3 to 6, respectively) shall be reported at the lower of amortized cost or fair value.

Designation Guidance

25.27. For securities within the scope of this statement, the initial NAIC designation used to determine the carrying value method and the final NAIC designation for reporting purposes is determined using a multi-step process. The Purposes and Procedures Manual of the NAIC Investment Analysis Office provides detailed guidance. A general description of the processes is as follows:

a. Financial Modeling: The NAIC identifies securities where financial modeling must be used to determine the NAIC designation. NAIC designation based on financial modeling incorporates the insurers’ carrying value for the security. For those securities that are financially modeled, the insurer must use NAIC CUSIP specific modeled breakpoints provided by the modelers in determining initial and final designation for these identified securities. Securities where modeling results in zero expected loss in all scenarios are automatically considered to have a final NAIC designation of NAIC 1, regardless of the carrying value. The three-step process for modeled securities is as follows:

i. Step 1: Determine Initial Designation – The current amortized cost (divided by

remaining par amount) of a loan-backed or structured finance security is compared to the modeled breakpoint values assigned to the six (6) NAIC designations for each CUSIP to establish the initial NAIC designation.

ii. Step 2: Determine Carrying Value Method – The carrying value method, either

the amortized cost method or the lower of amortized cost or fair value method, is then determined as described in paragraph 25 26 based upon the initial NAIC designation from Step 1.

iii. Step 3: Determine Final Designation – The final NAIC designation that shall be

used for investment schedule reporting is determined by comparing the carrying value (divided by remaining par amount) of a security (based on paragraph 2627.a.ii.) to the NAIC CUSIP specific modeled breakpoint values assigned to the six (6) NAIC designations for each CUSIP. This final NAIC designation shall be applicable for statutory accounting and reporting purposes (including establishing the AVR charges). The final designation is not used for establishing the appropriate carrying value method in Step 2 (paragraph 276.a.ii.).

Attachment B Ref# 2016-40

© 2016 National Association of Insurance Commissioners 13

b. Modified Filing Exempt Securities: The modified filing exempt method is for securities that are not subject to modeling under paragraph 2627.a., and is further defined in the Purposes and Procedures Manual of the NAIC Investment Analysis Office and have a NAIC Credit Rating Provider (CRP) rating. The four-step process for these securities is similar to the three-step process described in paragraphs 2627.a.i. through 2627.a.iii.