status of australian privatisations - october 2016

TRANSCRIPT

Status of Australian Privatisations

October 2016

2

1. Commonwealth privatisations

2. New South Wales – Transmission & Distribution

3. Victoria – Port of Melbourne

4. Western Australia – Mixed assets

5. Other States and Territories

6. Regulatory overlay

Overview

1. Commonwealth of Australia

3

Political context – ‘Asset Recycling Initiative’

4

• Liberal-National Coalition Government elected in Australia in September 2013 and

commissioned National Commission of Audit (NCA) report. NCA recommended further

privatisations, noting little had been privatised at Commonwealth level since 2006.

• In March 2014, Commonwealth Treasurer Joe Hockey announces 'Asset Recycling

Initiative' (API) where Commonwealth Government offers financial incentives to

State/Territory Governments to sell assets and recycle proceeds into new infrastructure.

• States/Territories entered May 2014 National Partnership Agreement on Asset Recycling:

– States/Territories receive a Commonwealth incentive payment of 15% of sale

proceeds from a privatised asset if they reinvest all proceeds into new infrastructure.

– Payments are allocated on a ‘first come first served’ basis from limited pool of funds.

– Sale of asset / construction of new infrastructure must commence by 30 June 2019.

• The 2014-15 federal budget allocated $5.9 billion to an Asset Recycling Fund. Legislation

was introduced into Federal Parliament to give effect to the API, but was blocked.

• The Government subsequently proceeded with the API under existing legislation.

Joe Hockey

NCA recommendations to the Commonwealth

5

Short term (2014-2016) Medium term (2016-2020) Long term (After 2020)

Medibank Australian Postal Corporation NBN Co Limited

Australian Hearing Services Moorebank Intermodal

Company Limited

Snowy Hydro Limited (minority

shareholding)

Australian Rail Track

Corporation Limited (ARTC)

Defence Housing Australia Royal Australian Mint

ASC Pty Ltd (Submarines) COMCAR

• National Commission of Audit recommended in favour of the privatisation of 10 entities, plus the

Medibank privatisation already underway at the time.

• NCA commented that other Commonwealth assets, including land & buildings, could be sold

• The Commonwealth Government adopted some, but not all, of these recommendations. If the

recommendations were adopted, Commonwealth Treasury commissioned a Scoping Study.

Status of Commonwealth privatisations

6

Asset Comment Status

Medibank Medibank listed on ASX in November 2014 Completed

Australian Hearing Services Consortium proposal under active consideration Underway

Snowy Hydro Limited Requires action by State Governments Did not proceed

Defence Housing Australia Scoping study completed, but did not proceed Did not proceed

Australian Submarines Ruled out given strategic importance to defence Did not proceed

ASIC Share Registry Competitive tender process is underway Underway

Australia Post Ruled out given period of disruption to post Did not proceed

Moorebank Intermodal Under development – privatisation premature Postponed

ARTC Delayed until after Inland Rail project completed Postponed

Royal Australian Mint Scoping study completed, but did not proceed Did not proceed

COMCAR No response by Government to NCA proposal Did not proceed

NBN Co Ltd Under development – privatisation premature Postponed

7

Competitive bidding process for privatised assets

EOI stage

• Interested parties invited to submit an EOI with

executed Confidentiality Deed Poll and

• EOIs contain information about the parties and

proposed ownership structure as well as interest,

experience, and capability.

• EOIs indicate financial capability, preparedness and

suitability.

Binding bid stage

• Shortlisted bidders given access to the full virtual

data room and vendor models (including due

diligence information for legal, accounting,

engineering, property, environmental).

• Bidders would also undertake site visits, receive

management presentations, and engage in a

question and answer process with the vendor.

• Bidders would each be issued with pro forma

contract documents. The contracts would be

negotiated independently with each bidder.

• The shortlisted bidders would be invited to submit

their final, legally binding, unconditional bids in

conjunction with the negotiated contracts.

• Bidders must have obtained informal clearance

from the ACCC and must have obtained Foreign

Investment Review Board (FIRB) clearances

• Final bidder selected and proceed to execution.

• Financial close.

Indicative bid stage

• Issue of an Information Memorandum and indicative

bid process letter

• Issue of vendor due diligence reports within

electronic data room (limited access)

• Bidders required to lodge indicative bid

• State will process indicative bids and shortlist

bidders for inclusion in binding bid stage.

8

Sale of shares in a privatisation vehicle

• Objective is to create a simple pre-packaged business,

inclusive of lease, that can be easily transferred by way

of a share sale

• Transfer of assets to State Holding Corporation (SHC).

• Implementation of long-term lease between Project

Company and SHC.

• Novation of third party contracts from Existing

Corporation to Project Company.

• Transfer of employees from Existing Corporation

into Project Company.

• Sale of shares in Project Company.

Investor Consortium State

Government

Existing Corporation

State Holding

Corporation (SHC)

Project Company to

be Privatised

Customers

Payment for shares

Transfer of shares

Novation of third party contracts

Transfer of

assets

State ownership

State

ownership

Transfer of some staff

Private

ownership

99 year lease

Third party

contracts

Ownership

Contracts

Transfers

2. State of New South Wales

9

10

Political context to NSW privatisations

• The Liberal/National Coalition government came to power in NSW

in March 2011 (under Premier Barry O’Farrell) and proceeded with

the following privatisations:

• The Coalition was re-elected 28 March 2015 (under Premier Mike

Baird) with a policy that included the privatisation of the NSW

electricity transmission and distribution (T&D) assets.

• Implementing legislation was enacted to authorise the T&D

privatisations in June 2015, following a political deal between the

Government and two independent senators. The Coalition holds

52 of 93 seats in Legislative Assembly (house of reps) but only 20

of 42 seats in Legislative Council (senate).

• Given political concerns, an outright sale of the networks was not

contemplated. Instead, the privatisation is via 99 year leases.

Premier Mike Baird

Privatised asset Price

Port of Newcastle – leased to Hastings consortium $1.75 billion

Port Botany – leased to IFM consortium $4.31 billion

Port Kembla – leased to IFM consortium $750 million

Mt Piper & Wallerawang generators – acquired by EA $160 million

Eraring & Shoalhaven generators – acquired by Origin $50 million

Macquarie Generation – acquired by AGL $1.505 billion

11

Transmission & distribution in NSW

• Transmission business for NSW

• 14,000km of transmission lines; 71GWh per annum

• The privatisation of TransGrid was completed in

December 2015 for a sale price of $10.26 billion to a

consortium lead by Hastings.

• Electricity distributor in western Sydney & Illawarra

• 883,000 retail electricity customers

• Endeavour Energy will be sold after Ausgrid. The

precise timing for the privatisation is currently

unknown.

• Electricity distributor in Sydney, Central Coast,

Newcastle and Hunter Valley regions of NSW

• 1.6 million retail electricity customers

• The first attempt at the privatisation of Ausgrid was

blocked by the Commonwealth Government. The

second attempt is now underway .

• Electricity distributor in regional NSW

• 803,000 retail electricity customers

• Essential Energy will not be sold. Politically, The

opposition to privatisation is stronger in regional

NSW than in metropolitan NSW.

100% now privatised 50.4% to be privatised

50.4% to be privatised Will not be privatised

• To appease political concerns, NSW Government has committed to maintain ownership of 100% of

Essential Energy and will also maintain an average ownership of 51% across all four electricity networks.

12

Successful privatisation of TransGrid

• Timetable: Transaction commenced 4 June 2015. RFQ was returned on 14 July 2015 and

shortlisting announced on 2 September 2015. Winning consortium was announced on 25

November 2015 with completion occurring on 16 December 2016.

• Financing of winning bid: NSW Electricity Networks (as the Hastings-led consortium) acquired

TransGrid for $10.258 billion, with a $5.5 billion limited recourse financing package provided by

the global syndicate of 12 local and global financiers.

• Outcome: See table below

Consortium Outcome

State Grid – MIRA (State Grid Corporation of China; Macquarie Infrastructure and Real Assets

Ltd)

Shortlisted

AusNet Services (AusNet Services) Did not bid

China Southern Power – CIC – GIP (China Investment Corp; China Southern Power Grid, Global

Infrastructure Partners)

Not

shortlisted

Hastings-led Group (Abu Dhabi Investment Authority (ADIA); Caisse de depot et placement du

Quebec (CDPQ); Hastings Funds Management; Kuwait Investment Authority (Wren House);

Spark Infrastructure), advised by JP Morgan and Royal Bank of Canada

Winner

QIC-IFM (Industry Funds Management (IFM), QIC Global Infrastructure), advised by Barclays Shortlisted

AustralianSuper-led Group (Australian Super; Borealis Infrastructure; Canada Pension Plan

Investment Board (CPPIB), advised by Credit Suisse

Shortlisted

Chung Kong Infrastructure (CKI) Did not bid

13

Problems privatising Ausgrid

• Timetable: Transaction commenced 24 November 2015, immediately TransGrid had concluded.

Indicative bids were due on 29 February 2016, but after one consortia withdrew, the two remaining

bidders were shortlisted. The transaction timetable clashed with the Australian federal election in

July, hence final bids were submitted on 25 July, after the election.

• Outcome: Press speculation was that the final bids received by the State for the 50.4% interest

were as high as $13 billion, valuing the 50.4% interest at a multiple of approximately 1.7 x RAB.

However, the Commonwealth Treasurer refused to provide foreign investment approval to both of the

final bidders, effectively eliminating them from the sale process. As a consequence, the initial

attempt to privatise Ausgrid was abandoned. The bidders were as follows:

• Limited bidders: Unlike the TransGrid privatisation, very few bidders were initially involved in the

Ausgrid privatisation. Industry comment is that everyone expected the Chinese to pay a high price

for the asset, so did not consider it worth participating.

• What next? New bid rules are due to be released by the NSW Government in October which are

likely to cap foreign control (probably in the 15-20% range). Meanwhile, domestic Australian funds

are being encouraged to bid for the asset. Industry comment is that many of the funds that did not

participate because of the Chinese participation, may now participate as they expect the asset to be

privatised at a cheaper price.

Bidder Outcome

State Grid Corporation, a Chinese SOE and the world’s largest electricity utility Blocked

Chung Kong Infrastructure (CKI) of Hong Kong Blocked

China Southern Power, Qatar Investment Authority, China Investment Corporation Withdrew

14

Foreign investment approvals

• Foreign Investment Review Board (FIRB) approval is required for acquisitions by foreign persons

into Australia that exceed various monetary thresholds. FIRM makes a recommendation to the

Commonwealth Treasurer, who makes a decision on the advice of his advisors. Decisions not to

grant approval are rare, but conditions are often imposed.

• Typically, a requirement of the privatisation process is that shortlisted bidders have obtained an

informal clearance from FIRB before submitting a final unconditional bid. Given FIRB timelines, this

has generally meant that an application is made to FIRB at a much earlier stage in the process.

• However, the FIRB process has been difficult in the context of the recent NSW privatisations,

suggesting a higher level of scrutiny by FIRB than has been the case historically.

• At a very late stage in the TransGrid privatisation process, FIRB announced to the bids for

TransGrid that it would impose various conditions on the bids, including:

1. Foreign ownership restrictions, reputed to be no more than 50% per foreign person

2. Requirement for local management and board representation

3. Control from Australia, given the critical role of TransGrid as the backbone for energy supply

for New South Wales and Canberra.

• In the Ausgrid privatisation process, FIRB reputed to have said initially that it was intending to

impose only minimal conditions on the acquisition. However, it seems apparent that national

security considerations were raised with FIRB. On 19 August 2016, the Treasurer made an order

under the Act prohibiting both State Grid and CKI from acquiring the 50.4% interest in the Ausgrid

business on the basis of national security considerations.

3. State of Victoria

15

Political context to VIC privatisations

16

• Victoria privatised its electricity generation and retail assets at any early stage:

– In October 1994 the Victorian industry was restructured.

– Five electricity distributors were created and Generation Victoria was disaggregated

down to four individual base load power stations (including Loy Yang B then under

construction), one portfolio of hydro plant and one of intermediate and peaking gas plant.

– During 1995-1997 all of these businesses, except the gas portfolio were privatised

• In 1996, Victoria also privatised two of its major ports, but abandoned plans to privatise

the Port of Melbourne following opposition by users.

• In recent years, Australia has experienced a series of port privatisations. The Port of

Brisbane was privatised in 2010, followed by Port Botany and Port Kembla in 2013,

Port Newcastle in 2014, and the Port of Darwin in 2015. Port of Melbourne remains one

of the few major ports on the east coast of Australia still owned by a State government.

• In the context of the Asset Recycling Initiative, the Victorian Government sought to

revisit plans to privatise the Port of Melbourne.

• The two different political parties in Victoria agreed that a privatisation of the Port of

Melbourne was appropriate. However, they differed in the particular privatisation model

that they each favoured.

17

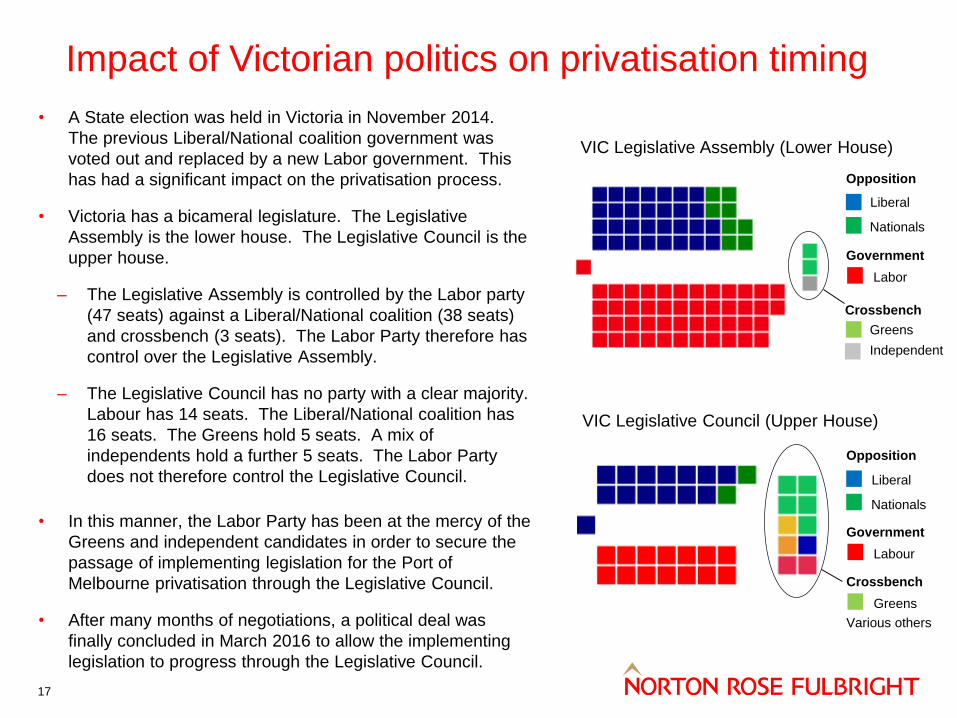

Impact of Victorian politics on privatisation timing

• A State election was held in Victoria in November 2014.

The previous Liberal/National coalition government was

voted out and replaced by a new Labor government. This

has had a significant impact on the privatisation process.

• Victoria has a bicameral legislature. The Legislative

Assembly is the lower house. The Legislative Council is the

upper house.

– The Legislative Assembly is controlled by the Labor party

(47 seats) against a Liberal/National coalition (38 seats)

and crossbench (3 seats). The Labor Party therefore has

control over the Legislative Assembly.

– The Legislative Council has no party with a clear majority.

Labour has 14 seats. The Liberal/National coalition has

16 seats. The Greens hold 5 seats. A mix of

independents hold a further 5 seats. The Labor Party

does not therefore control the Legislative Council.

• In this manner, the Labor Party has been at the mercy of the

Greens and independent candidates in order to secure the

passage of implementing legislation for the Port of

Melbourne privatisation through the Legislative Council.

• After many months of negotiations, a political deal was

finally concluded in March 2016 to allow the implementing

legislation to progress through the Legislative Council.

VIC Legislative Assembly (Lower House)

Opposition

Government

Liberal

Nationals

Labor

VIC Legislative Council (Upper House)

Opposition

Government

Labour

Liberal

Nationals

Crossbench

Greens

Various others

Crossbench

Greens

Independent

• The Port of Melbourne is approaching full capacity.

While a current expansion is addressing immediate

capacity constraints, all political parties recognised

that a second port is now required.

• The key point of difference between the political

parties involved the location of that second port and

the longer-term role of the Port of Melbourne

relative to that second port.

• The Labor Party (now the current government)

favoured selling a 99 year lease over the Port of

Melbourne. The Port of Melbourne would be

supplemented by the development of a second

container port at Bay West.

• The Coalition (previously in government and now

forming the opposition) favoured a 40 year lease

over the Port of Melbourne, following which it would

be decommissioned and the land sold for CBD

development. The Port of Hastings would be

developed as the port to replace the Port of

Melbourne during that 40 year period, gradually

being developed over time as the Port of Melbourne

reached capacity.

The political deal – a 15 year compensation clause

18

• The Labor Party initially proposed a 99 year lease

with a 50 year compensation clause if a second port

were built.

• However, the Labor Party’s proposal had the

practical effect of creating a deterrent to the Port of

Hastings while locking in its own proposal.

• The sticking point for negotiations in the upper

house therefore centred around the term of the

lease and the duration of this compensation clause.

• The Coalition initially wanted no compensation to

be paid, but later backed down and offered 15

years – the time in which Infrastructure Australia

estimates the Port of Melbourne will reach capacity.

• Ultimately, a political deal was reached involving a

involved a 50 year lease and a 15 year

compensation clause.

• In practice, this means that the option to develop

the Port of Hastings remains open if the Victorian

government were to change.

19

Top 20 Australian ports

Port HedlandPort DampierPort NewcastleHay PointPort GladstoneOther Ports

Port Export Focus Tonnage %National Privatised

Port Hedland WA 99% Specialist: iron ore 288,443,039 25.5% Imminent Utah Point Bulk Terminal only

Dampier WA 100% Specialist: iron ore 180,365,873 16.0% Possible

Newcastle NSW 98% Specialist: coal 148,861,567 13.2% Yes - 2014 98 year lease

Hay Point QLD 100% Specialist: coal 96,540,226 8.6% Yes - 2001 DBCT in 2001; other CT private

Gladstone QLD 76% Multi-commodity 85,293,760 7.6% No Privatisation abandoned 2015

Brisbane QLD 52% Large multi-cargo 37,563,421 3.3% Yes - 2010 99 year lease

Melbourne VIC 45% Large multi-cargo 35,059,320 3.1% Imminent Proposed 50 year lease

Fremantle WA 56% Large multi-cargo 31,980,238 2.8% On hold Privatisation proposed

Weipa QLD 100% Specialist: bauxite 29,041,572 2.6% On hold Associated with Rio Tinto mine

Kembla NSW 77% Specialist: coal 23,935,068 2.1% Yes - 2013 99 year lease

Botany NSW 34% Large multi-cargo 21,582,856 1.9% Yes - 2013 99 year lease

Abbot Point QLD 100% Specialist: coal 17,744,621 1.6% Partial - 2011 T0 & T1 CT privatised only

Geraldton WA 96% Specialist: iron ore 15,444,843 1.4% No

Bunbury WA 89% Specialist: alumina 15,331,906 1.4% No

Adelaide SA 57% Large multi-cargo 15,166,339 1.3% Yes – 2001 99 year lease of 6 ports

Esperance WA 94% Specialist: iron ore 13,875,044 1.2% No

Geelong VIC 38% Regional multi-cargo 12,836,648 1.1% Yes -1996 99 year lease

Townsville QLD 45% Regional multi-cargo 12,105,804 1.1% No Privatisation abandoned 2015

Portland VIC 80% Regional multi-cargo 5,333,712 0.5% Yes -1995 99 year lease

Darwin NT 65% Regional multi-cargo 4,299,008 0.4% 2015 99 year lease

DBCT = Dalrymple Bay Coal Terminal; CT = Coal Terminal

20

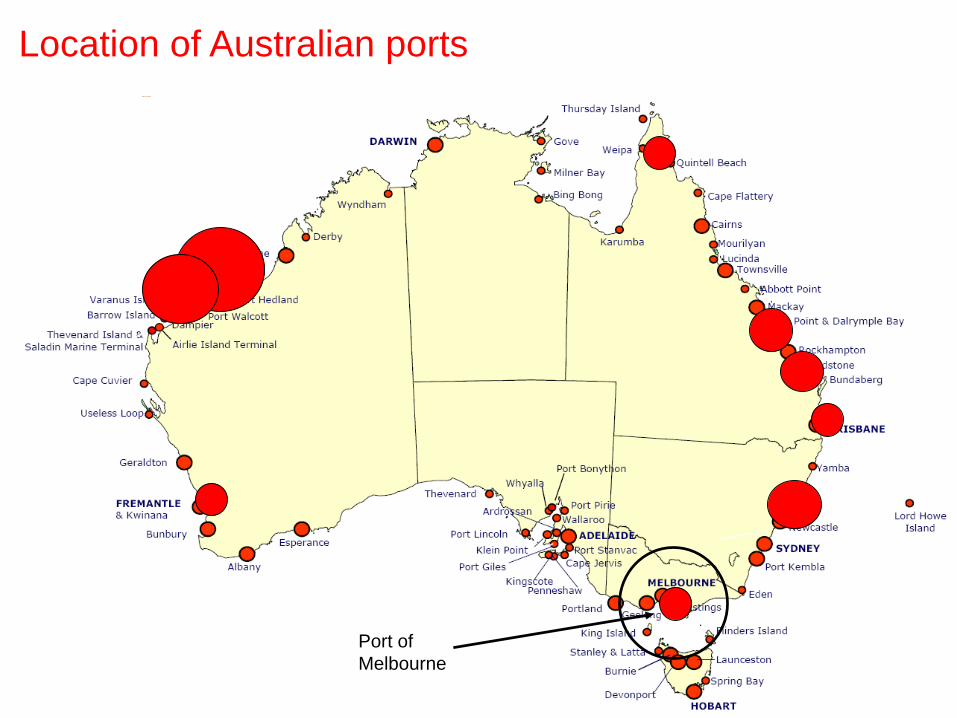

Location of Australian ports

Port of

Melbourne

• The Port of Melbourne is Australia’s largest

and most important maritime trade hub for

container, automotive and general cargo.

• The Port supports the State of Victoria and

south-eastern Australia. It is one of the top four

container ports in the Southern Hemisphere.

• The Port of Melbourne handles around 36% of

Australia’s container trade, amounting to some

2.579 million containers (TEU) per year in the

year to June 2014.

• During the 2013/14 financial year, the Port

experienced over 3,000 commercial ship visits,

throughput of over 85 million revenue tonnes

(35 million mass tonnes) and handling of over

350,000 automotive units.

• As well as containers, motor vehicles and

general cargo, the Port handles liquid bulk

products (such as crude oil imports and

petroleum product exports), and dry bulk

products (including cement, gypsum, sugar as

imports, and wheat, canola, barley as exports).

21

Port of Melbourne

Privatisation of port functions

• Three key port functions

– Regulatory:

– marine services (harbour control, pilotage);

– maritime safety, environmental response.

– Landowner:

– port planning & development, wharves,

berths;

– shipping channels, navigation, breakwaters.

– Operator:

– cargo-handling, warehousing, towage.

• Australian ports have in most cases already

outsourced stevedoring functions to private sector.

• Most common business model in ports globally is

public ownership with a private concession.

• Privatisation in Australia has focussed on transfer of

landowner functions to the private sector via long-

term leases, by market practice normally 99 years.

22

Port functions & cash flows

Revenue cash flows

• Land and property rentals:

– Note the recent media coverage of rental charges

• Wharfage / cargo charges:

– Typically a variable charge based on volume;

– Charged per unit loaded/unloaded.

• Berthage / tonnage / channel / ship charges:

– Typically a fixed capacity fee charged per vessel;

– Charged once per visit based on tonnage.

• Miscellaneous charges:

– Cargo handling/stevedoring (normally outsourced)

– Anchorage charges;

– Hire fees / Cargo storage fees;

– Security fees / Inspection fees;

– Pilotage charges (often outsourced);

– Infrastructure and dredging levies.

Focus of port

privatisations

23

Scope of the Port of Melbourne privatisation

Transfer of Landowner functions

• Successful bidder will:

– enter into 50-year lease over majority of current

landholdings and associated fixtures (including

buildings and wharf infrastructure), providing a

long-term leasehold interest in both occupied and

vacant land (including development rights);

– assume the interest in the leases with the existing

tenants, enabling collection of rent;

– lease an interest in the shipping channel seabed,

but with maintenance responsibilities;

– lease selected associated assets;

– have the right to charge port users for the

utilisation of port infrastructure, including

wharfage, channel fees, hire fees, security

charges and other utility charges

– obtain rights to the development of the new third

container terminal at the Port; and

– have the right to charge channel fees for

commercial vessels visiting Station Pier.

Retention of regulatory functions

• State will retain various functions within the

Victorian Ports Corporation (Melbourne) (VPC).

• VPC will:

– employ the Harbour Master;

– manage and own the Vessel Traffic Service;

– manage shipping anchorages and retain

related charging powers for anchorages;

– manage towage regulation;

– perform safety and environmental functions,

including for dangerous goods, waterside

emergency management and marine pollution.

• The State will retain the operation and associated

revenue streams of Station Pier and West Finger

Pier.

24

Competition restrictions

• Shortlisted bidders are typically required to have obtained an informal clearance from the Australian

Competition and Consumer Commission (ACCC) before submitting the final unconditional bid, or

otherwise identify why such clearance is not required:

– The key consideration for the ACCC is whether the proposed acquisition would have the effect,

or likely effect, of substantially lessening competition in any market in Australia.

– The informal clearance process is a clearly defined process and involves appropriate scrutiny

by the ACCC based on submissions, followed by potential public consultation.

• We also understand that additional restrictions have been applied to any entities that provide any of

the following services at the Port of Melbourne or any other Australian capital city port:

– stevedoring services

– container handling services

– services of an automotive terminal

• The restrictions will apply to owners and subsidiaries of the bidding entity, based on the standard

Corporations Act concept of ‘control’.

• The precise details of the restrictions are not yet publicly known, but the restrictions seem intended

to avoid any competition issues arising with the ACCC.

• The ACCC has no practical ability to block or

approve a particular privatisation structure, but its

view can be influential in some instances.

• Recent comments and submissions by the ACCC

regarding infrastructure privatisations:

– The ACCC is generally supportive of

privatisations on the basis that the private sector

can more efficiently operate assets.

– The ACCC’s primary concern is that the

privatisation structure needs to be set so as to

maximise competition and ensure any monopoly

assets are subject to effective regulation.

• The ACCC’s view has the potential to diverge from

the views of State Treasurers, who are seeking to

maximise the value of the privatised asset.

• The ACCC has raised concerns regarding some

historical privatisation structures:

– Privatisation of Telstra as a vertically-integrated

telecoms business.

– Privatisation of Sydney Airport inclusive of an

option for developing a second airport (rather than

having two competing airports).

Comments by the ACCC

• “There have been very high multiples paid for

some of these ports and the worry is that the

buyers may only recoup their outlays if they push

up prices quite a bit more than otherwise would

have happened,” Mr Sims told The Australian

Financial Review.

• “Governments should avoid the temptation to

attempt to maximise sale revenue by privatising

without appropriate price and access regulation in

place”: ACCC’s Container Stevedoring Monitoring

Report No. 16, October 2014

• “The regulator warns that “restrictions on

competition” inserted into sale conditions “may be

unlawful and could be unenforceable”. Its points of

reference were the sale of Port Botany and Port of

Newcastle, which included conditions that prevent

the world’s biggest coal port from building a

container terminal. The problem for the regulator is

that there is significant doubt over whether the

behaviours of government are contained by the

competition law”: The Australian Financial Review.

25

Views of the ACCC on privatisations

Views of ACCC on privatisations

4. State of Western Australia

26

Balancing the WA budget after the mining boom

27

• Mining and petroleum royalties are an important

source of the WA Government income. Those

sectors dominate the WA economy.

• Since 2013, royalties from these industries have

significantly decreased. Investment and production

in commodities has stalled following a fall in

commodity prices, particularly iron ore.

• As a result of these declining revenue streams, the

Government’s debt position has increased. Moody’s

downgraded the credit rating of the WA Government

from Aaa to Aa1 in August 2014.

• The WA Government is under significant political

pressure to restore the State’s credit rating and

bring the State’s debt back under control.

• As a part of the Federal Budget in May 2015, the

WA Government announced an asset investment

program totalling AUD 6.3 billion in 2015-16 and

AUD 24.1 billion over the subsequent four years.

Much of that investment will be funded by the sale

or privatisation of existing state-owned assets.

• In the 2015 State Budget, the WA Government

announced that: “The orderly disposal of State

assets has begun and will be significantly

expanded. Sales proceeds will be used to fund

existing infrastructure initiatives and reduce debt”.

Announcements by WA Government

28

• The WA Government announced the privatisation of a first tranche of (minor) asset sales in May 2014. The

first successful privatisation was the Perth Market Authority, but the other two have not yet occurred.

• In the 2015 WA Budget, the WA Government allocated funding to WA Treasury to progress the sale of the

first tranche of assets over the period to 30 June 2017.

• In addition, the WA Government has announced that its asset sales program will be “significantly

expanded”. The WA Government will investigate the potential privatisation of further assets.

First tranche (current) Second tranche (future) Not yet included

Kwinana Bulk Terminal* Fremantle Ports Western Power (remainder)

Utah Point Bulk Handling Facility WA TAB Synergy (remainder)

Perth Market Authority Forest Products Commission Horizon Power (remainder)

Portfolio of GRO housing stock Water Corporation (some assets)

Securitisation of KeyStart loans Dampier marine services facility

Vehicle feet sale and leaseback

Various Government buildings

Selected assets of Synergy,

Horizon Power, Western Power

We understand Kwinana may be

subsumed into Fremantle Ports

We understand Utah Point has

temporarily been placed on hold.

29

Delays to privatisations caused by WA politics

• WA has a bicameral legislature. The Legislative Assembly

is the lower house. The Legislative Council is the upper

house.

– Legislative Assembly is controlled by a Liberal/National

coalition (38 seats), against Labor (21 seats).

– The Legislative Council is controlled by a

Liberal/National coalition (22 seats), against Labor (11

seats), Greens (2 seats) and shooters & fishers (1 seat).

• In this manner, the Liberal/National coalition has a majority

in both houses of parliament in WA. Enactment of

legislation to implement the proposed privatisations should

therefore be provided.

• The last general election occurred in March 2013 and the

next general election is due in 2017.

• The Government will be a wary of potential electoral

concern regarding privatisations, hence the 2017 elections

could result in a pause in the privatisation programme to

avoid political backlash.

• The WA Government may also wish to avoid potentially

controversial privatisations, such as water and electricity.

WA Legislative Assembly

Government

Opposition

Liberal

Nationals

Labour

WA Legislative Council

Government

Opposition

Labour

Liberal

Nationals

Crossbench

Greens

S&F

Utah Point Bulk Handling Facility

30

• The Utah Point Bulk Handling Facility, located in Port Hedland, is

one of 4 berths at the Port owned by Pilbara Ports Authority.

• The Facility is new, commencing operation in September

2010. The Facility was designed specifically for small and

mid-tier miners and comprises:

– a single multi-user mini-cape berth and shiploader; and

– two stockyard product storage facilities and supporting

infrastructure, including a purpose built 10 km access

road and 13 independent stockpiles over 24 hectares.

• The Facility is used to export various bulk products, mostly

iron ore, manganese, and chromite. A total of 18.7 Mtpa

was exported through Utah Point during the FY 2013-14

financial year. The Facility had a design capacity of 20

Mtpa, but has operated at annualised rates of 22 Mtpa.

• The Facility earned AUD 86.5 million in revenue in FY 2012-

13 with expenditure of AUD 44.1 million on throughput of

12.4 Mtpa.

• Indicative DD issues: ‘Junior miners’ are the primary users

of the Facility and have been the hardest hit from the iron

ore price crash and hence are most exposed financially (eg

Atlas Iron).

31

Fremantle Ports

• Fremantle Ports is a WA Government trading enterprise that

strategically manages the Port of Fremantle. Fremantle Ports

was not part of any of the recent port amalgamations in WA.

• Fremantle Ports consists of two harbours: the Inner Harbour and

the Outer Harbour (see next slides). Fremantle Ports is the

State’s biggest general cargo port and Australia's fourth largest

container port.

• Fremantle Port’s Inner and Outer Harbours currently handle

around 91% of the WA’s sea imports and 30% of exports. The

value of this trade is estimated at AUD 12 billion annually.

• The port is a mix of facilities and services managed by

Fremantle Ports and private operators. Fremantle Ports provides

and maintains shipping channels, navigation aids, cargo

wharves at common user areas and leased terminals, the

Passenger Terminal, road and rail transport infrastructure in the

port area, moles and seawalls and other infrastructure such as

storage sheds, water, power and public amenities

• Services such as towage, pilotage (under contract to Fremantle

Ports), line boats and bunkering are provided by the private

sector. Fremantle Ports also cooperates with Commonwealth

Government agencies responsible for customs, quarantine and

maritime safety.

Sources of revenue (2013)

$135.6m

$19.0m

$17.5m

$12.3m

$11.1m $6.6m

Charges on cargo

Rentals and leases

Charges on ships

Shipping services

Miscellaneous revenue

Port utilities and services

Regulatory overlay

32

Legal and regulatory context for ports in WA

• There is no formal State-based direct regulation of ‘third

party access’ to port infrastructure in WA or of pricing for the

use of port infrastructure.

• A threat of regulation exists. The WA government may

request the Economic Regulation Authority of WA (ERA) to

inquire into matters relating to both regulated and non-

regulated industries, including pricing, quality, business

practices and compliance costs.

• To date, to prevent excessive extraction of economic rent by

port authorities (in public ownership), relevant provisions

have existed in statutory governance arrangements for the

port authorities.

• The PAA requires port authorities to “act in accordance with

prudent commercial principles [and] endeavour to make a

profit”. The PAA’s focus on efficient resource allocation and

accountability has arguably limited scope for port authorities

to extract excessive rent.

• The PAA will not apply to privatised entities, so the threat of

regulation by the ERA will be the primary form of regulation.

Not yet clear if this will be enhanced.

Port Authorities Act 1999 (WA)

• The Port Authorities Act 1999 (WA) (PAA) governs

WA port authorities, covering their functions,

responsibilities, concept of operations and related

matters.

• Under the Act, the port authorities may operate as

Government Trading Enterprises.

• Prior to the passage of the Act, each port authority

was established under its own individual legislation.

• The State Government announced on 2 February

2012 that seven of the State's eight port authorities

would be consolidated into four regional port

authorities.

• The resulting consolidation involved the creation of

the new Pilbara Ports Authority, for example.

However, Fremantle Ports was not subject to the

consolidation.

• It is not yet clear how the PAA will be modified to

address the privatisation, although it is possible that

the privatisations may follow the NSW model.

Electricity sector privatisations in WA

33

• In 2006, the WA electricity sector was reformed by

disaggregating WA’s vertically-integrated electricity

utility, Western Power Corporation into four

separate state-owned entities:

– Verve Energy, originally responsible for power

generation in the SWIS, later merged with

Synergy;

– Western Power, responsible for transmission and

distribution of electricity in the SWIS;

– Synergy, now responsible for the retailing of

electricity and power generation in the SWIS;

– Horizon Energy, responsible for generation,

distribution and sale of electricity outside the

SWIS.

• WA operates an energy market known as the

South West Interconnected System (SWIS),

governed by the Wholesale Electricity Rules (which

are a bespoke variant to the National Electricity

Market Rules on the east coast of Australia).

• As yet, little electricity sector privatisations have

occurred in WA.

• In March 2014, the WA Government launched a

review of the WA electricity market. An options

paper was released on 24 March 2015, including a

report and conclusions.

• In the WA Government’s response to the review, the

WA Government indicated:

– Synergy would not be privatised or restructured as a

gentailer, rather the WA Government will consider

sales of specific generation assets;

– the WA will implement full retail contestability (hence

choice of electricity suppliers) once the Government

subsidy for the electricity market is reduced to zero –

this is expected to occur within the next four years;

– Retail tariff and other regulatory functiosn currently

undertaken by the Economic Regulatory Authority

(ERA) will be transitioned to the Australian Energy

Regulator;

– some wholesale electricity market reform will occur,

including reforms to the current capacity charge,

potential introduction of facility bidding, transfer of

system management to the independent market

operator, and reforms to regulation of Western Power

Synergy – energy retail & generation

34

• Following the re-merger of Synergy with Verve

Energy on 1 January 2014, Synergy is WA’s

largest integrated generation-retailer.

• Synergy over 1 million industrial, commercial

and residential customers, generating total

annual revenue of around AUD 1.5 billion.

• The WA Government determines Synergy's

generation capacity, which is currently capped at

3,000 megawatts (MW). Synergy produces

about 10,000 gigawatt hours (GWh) of electricity

each year, or 60% of the electricity sold to

households and business customers in the

SWIS and about 45 per cent of the contestable

gas load in the industrial and commercial market

• The Government has indicated it has no current

plans to privatise or restructure Synergy.

• However, in its recent Energy Market Review

Report, the WA Office of Public Utilities

concluded that it would be desirable for the

State-owned generation assets to be privatised.

Western Power - lines

35

• Western Power is the WA State Government

owned corporation that builds, maintains and

operates the transmission and distribution

network in the SWIS.

• Recommendations have been made by key

stakeholders to establish a clear pathway for

the privatisation of Western Power.

• In December 2014, the WA Office of Public

Utilities released its Energy Market Review

Report. This report suggested a full or partial

privatisation of the network in order to reduce

the State’s net debt exposure.

• However, the WA Government response

indicates that selected sale of generation

assets from Synergy is instead favoured.

• If privatisation occurred, it is estimated that

the business could be restructured and split:

– the transmission business is estimated to have a

value in the order of AUD 6.5 billion;

– the distribution network is estimated to have a

value in the order of AUD 2.5 billion. Source: Energy

Market Review

Options Paper

36

• Horizon Power is a fully vertically-integrated electricity

generator, distributor and retailer owned and operated by

the WA Government.

• Horizon Power services the remainder of WA not

included in the SWIS, this includes:

– the entire North West Interconnected System (NWIS); and

– non-interconnected systems in regional towns and remote

communities.

• Horizon Power manages 38 separate systems: the NWIS

in the Pilbara and the connected network between

Kununurra, Wyndham and Lake Argyle, and 34 stand-

alone systems in regional towns and remote

communities.

• Horizon Power supplies around 100,000 residents and

10,000 businesses.

• Although no firm statement has been released at this

time, reports suggest the WA Government has been

considering a privatisation of Horizon Power.

• The asset sales announced by the WA Government

include the sale of certain generation assets.

Horizon Power – regional WA

Selected generation assets in second tranche

37

• In its May 2015 Budget announcements, the WA

Government indicated it would be selling certain individual

electricity generation assets owned by the State-owned

electricity generators, Synergy and Horizon Power.

• The generation assets sale are expected to include:

– the 55MW Mumbida wind farm, owned by Synergy;

– the 10MW Greenough solar farm, owned by Synergy;

– possibly Synergy’s 240MW Muja AB coal-fired power

station;

– Horizon Power’s 86MW Karratha simple-cycle gas

turbine power station.

• However, the WA Government has not yet released a

definitive list of the various generation assets that it is

intending to sell.

• The WA Treasurer commented in his budget speech that

the privatisation would include:

“individual generation assets of Synergy and Horizon

Power, and Wester Power’s non-core assets”.

Muja AB 240MW coal-fired power station

• Muja Power Station is situated 225 kilometres south

east of Perth and 22 kilometres east of Collie. It is

Synergy's largest power station. Muja Power Station

is coal-fired and is comprised of Stages A, B, C and

D, dating from 1966.

• Muja Stages C and D produce 854 megawatts (MW)

of electricity.

• Stages A and B have been undergoing refurbishment

and have recently been recommissioned. This

refurbishment has been controversial. Corrosion

problems and a problematic joint venture resulted in

a $308 million cost overrun.

Water Corporation

Wastewater assets

38

• Water Corporation operates 106 wastewater

treatment plants across Western Australia,

including three large, metropolitan plants –

Woodman Point, Beenyup and Subiaco – which

collect and treat about 80% of the state’s

wastewater.

• In August 2014, a confidential report revealing

that the plants are the “most notable examples”

of Water Corp assets being examined for

privatisation was mistakenly tabled in the WA

Parliament.

• If privatisation occurs, it will most likely involve

packages of wastewater plants that are

progressively sold over a period of time.

• However, Water Corporation has not specifically

been mentioned in the context of the

privatisation tranches identified to date. It is

likely that any announcements will be delated

until after the sale of the C&E business.

Construction and Engineering

• In January 2015, Water Corporation announced

that it would pursue a private buyer for its

engineering and construction services team in

order to shift its focus to building new infrastructure

to support Perth’s rapid growth and meet the

demands of the drying climate.

• The team comprises 152 permanent employees

who provide in-house civil construction and

mechanical, and electrical fabrication and

construction services.

• Water Corporation expects to determine the new

owner by mid-2015.

• The sale of the construction and engineering

business was not specifically mentioned in the WA

budget in the context of the WA privatisation

programme, presumably to de-politicise the sale.

• Concerns have been raised, for example, by the

relevant union (United Voice WA) regarding job

losses.

5. Other States and Territories

39

Queensland abandoned its privatisations

40

• Queensland has experienced a range of privatisations, including Queensland TAB (1999), Sun

Retail (2006), PowerDirect (2007), parts of Queensland Rail (2010, 2013), Port of Brisbane

(2010), Forestry Plantations Queensland (2013), and Queensland Motorways (2014)

• The previous government, lead by Premier Campbell Newman, was pursuing a range of further

privatisations. The government was formed by the Liberal National Party (LNP) and had the

largest majority in QLD history, holding 73 seats compared to Labor’s 9 seats.. Assets

contemplated for privatisation included:

– Port of Gladstone coal terminal;

– Port of Townsville and associated rail;

– SunWater’s industrial pipelines, being the key water business in Queensland;

– Powerllnk, the key transmission business in QLD;

– Energex, the electricity distributor for Queensland, except south-east Queensland

– Ergon Energy, the electricity distributor for south-east Queensland

• However, asset privatisation became a key election issue in the February 2015 elections in

QLD. Contrary to expectations, the Labour Party clawed back the seats it had lost and was

elected into power under Premier Annastacia Palaszczuk.

• A key election promise of the Labour Party was that it would no proceed with any privatisations.

As a consequence, all QLD privatisations have been abandoned.

South Australia, Tasmania and the Territories

41

State of South Australia

• SA has already privatised its electricity and port infrastructure assets, so has not been a major

participant in the current wave of privatisations.

• Historic privatisations undertaken in SA have included: Pipelines Authority of South Australia

(1995), State Government Insurance Commission (1995), Bank SA (1996), Forwood Products

(1996), Adelaide Airport (1998), ETSA transmission (1999), Torrens Island power station

(2000), and Electranet (2000)

State of Tasmania

• Tasmania unsuccessfully attempted to privatise its Aurora electricity business in 2013, but the

business was withdrawn from sale as the bids received were not considered sufficiently high.

This Aurora business is still a candidate for future privatisation.

• Otherwise, the Premier of Tasmania, Will Hodgman, has stated “Let me be clear: we will not

be selling any government or public owned assets” and has maintained this position since

2014.

Northern Territory and Australian Capital Territory

• Port of Darwin was successfully privatised in October 2015 to Landbridge Group for $506

million by way of lease. The privatisation was controversial given concerns raised by the US.

• The NT and ACT have been considering privatisation of smaller assets.

6. Regulatory overlay

42

43

Managing the federal balance of power

States defer to Commonwealth

• Under the Constitution of Australia, certain

infrastructure services (namely post and telecoms)

are the subject of Commonwealth regulation rather

than State-based regulation.

• The Commonwealth also has power to regulate

certain significant national infrastructure on the basis

of its importance to inter-state trade or commerce or

to the national economy. The national access

regime has been enacted on this basis.

Commonwealth defers to States

• Otherwise, the power to regulate infrastructure lies

primarily with the States. The States have then

agreed with the Commonwealth and between

themselves to adopt various consistent regulatory

approaches (as mentioned in the previous slide).

• In relation to nationally significant infrastructure, the

States and the Commonwealth have agreed a

certification regime in which the State-based regime

has primacy if certain minimum criteria are met.

44

Hilmer Reforms and National Competition Policy

• The relationship between the Commonwealth and States in

relation to infrastructure regulation has been heavily influenced

by the National Competition Policy, dating from 1992.

• The ‘Hilmer Review’ of 1993 recommended a series of reforms to

harmonise infrastructure regulation across Australia, leading to

three key agreements between the Commonwealth and States in

1995.

• Competition payments were made by the Commonwealth to the

States in consideration for the implementation of various

competition policy reforms. The result has been the adoption of a

broadly consistent approach to infrastructure regulation

throughout Australia.

• Pursuant to these agreements, a co-operative approach between

the States lead to the adoption of the National Electricity Law and

the National Gas Law by most States based on the simultaneous

enactment of identical State-based legislation.

• WA is an exception and has tended to follow its own path,

although it is broadly similar to other states.

• Infrastructure regulation harmonisation issues are currently

pursued through the Council of Australian Governments (COAG).

45

Australia’s regulation of infrastructure types

• INSERT TABLE • [ ].

Infrastructure Exclusionary conduct

(ensuring non-discriminatory access)

Exploitative conduct

(preventing monopoly pricing)

Gas National Gas Law – negotiate / arbitrate

model for natural gas pipeline access (a

variant applies in WA)

Distribution businesses must submit

reference tariffs for approval that are derived

using the BBM/RAB approach.

Water A range of state-based access regimes

exist, typically involving the use of a

negotiate-arbitrate model

A range of state-based regimes exist, but

they typically use either the BBM/RAB

approach or a retail minus methodology.

Electricity National Electricity Law – negotiate /

arbitrate model with some standard terms

(a variant applies in WA)

Distribution businesses are subject to

revenue caps and retail price caps derived

using the BBM/RAB approach.

Telecoms Telecoms Access Regime – ex ante access

determinations

Telstra has been subject to CPI-X retail price

caps, but deregulation is occurring.

Wholesale pricing is determined by a number

of means, including BBM/RAB.

Airports Airports are potentially subject to access

regulation under the national access

regime.

ACCC undertakes price monitoring of the top

four leased federal airports against various

benchmark financial metrics

Ports Generally lightly regulated – reliant on

threat of regulation

Generally lightly regulated – reliant on threat

of regulation

Rail State-based access regimes – negotiate /

arbitrate model with some undertakings

Below-rail access pricing has generally been

based on the BBM/RAB approach.

Overview of State-based regulation

• Ports are not heavily regulated in Australia.

• If regulation exists, it is generally directed at:

– channel access;

– vertically-integrated facilities (eg

wharves/berths);

– non-contestable services.

• Most regulation of Australian ports involves price

monitoring. In some cases access regimes apply.

• Some port access regimes have been certified as

effective under the national access regime:

– Dalrymple Bay Coal Terminal, QLD;

– South Australian Ports.

• Regulation may also apply to specific

infrastructure associated with ports, including:

– grain silos (a new Code is under review);

– railway systems (eg Aurizon QLD undertaking);

– gas pipelines (National Gas Law).

Approach of different States

• NSW – NSW removed Ministerial approval of port pricing in

the NSW port privatisations and implemented a price

monitoring regime by the Minister. If the Minister is

dissatisfied, an IPART investigation can be requested.

• VIC - The VIC regime is adjusted every 5 years on review

by ESC. The ESC review for 2014 favours continued

reference tariffs, price monitoring, increased transparency

and a credible threat of greater regulation.

• SA – SA currently has a price monitoring regime, although

ESCOSA has the power to make pricing determinations. SA

also has a port access regime that has been certified under

the national access regime.

• QLD – QLD has applied access regulation to DBCT. Other

ports are not currently subject to access regulation or

monitoring, although declaration by QCA could occur (or an

undertaking ‘voluntarily’ sought). Open access is a condition

of the WICET lease. Port Brisbane has given a voluntary

access undertaking.

• WA – Relies on Government ownership and policy to control

pricing, so will need to reform their regulatory regimes when

privatising ports. In WA, certain port services could become

regulated services subject to ERAWA oversight.

46

Example – ports, primarily subject to State regulation

• CIRA was agreed by the Council of Australian

Governments (COAG) to achieve a simpler and

more consistent approach to the economic

regulation of significant ports.

• The States agreed to review the regulation of ports

to ensure they were consistent with the CIRA

agreed principles (see right).

• The various reviews resulted in a range of

conclusions. Generally, the conclusions of the

various reviews favoured:

– Commercial negotiations;

– Light-handed regulation and price monitoring;

– Threat of greater regulation if a light-handed

regulatory approach failed.

• KMPG undertook an audit for COAG in 2009 of the

various State-based ports reviews and confirmed

the veracity of the reviews – although WA failed to

make the deadline.

Agreed principles set out in CIRA

• Where possible, commercial negotiations and

outcomes should be promoted.

• States should create the structures and settings for

competitive markets, rather than regulating ad hoc.

• Regulation should only be applied only where

evidence of a market failure, such as:

– monopoly pricing / substantial market power;

– risk of upstream or downstream discrimination.

• Price monitoring to improve transparency is a first

step where price regulation is required.

• Any regulation should occur via an independent

State regulator acting within binding time limits.

• Third party access regimes should include

consistent regulatory principles (as listed in CIRA).

• Access regimes must be capable of national

certification under the national access regime.

47

Ports - consistency between State-based regimes

Competition and Infrastructure Reform

Agreement 2006 (CIRA)

• The national access regime is set out in Part IIIA of

the Competition and Consumer Act 2010 (Cth).

• Any person can apply to the National Competition

Council (NCC) for the access regime to be applied

to any port service.

• The NCC will undertake public consultation and

make a recommendation to the relevant State

Treasurer whether statutory criteria are met.

• Once regulated, a port service would be subject to

a negotiate/arbitrate regime before the ACCC.

• To date, this regime has been applied to rail but

not yet to ports. Possible it could be applied.

• Ability to offer access undertakings.

• A State can seek a declaration that its existing

ports regulatory regime is “effective”. By doing so,

it can formally displace the Commonwealth Part

IIIA regime so that only the State’s access regime

will apply. South Australia has achieved this for its

State-based Ports regime.

Price surveillance (Part VIIA)

• Price surveillance can apply to supply of goods or

services in any industry, including ports.

• Price inquiries: Commonwealth Treasurer can

require ACCC to hold price inquiries. ACCC has

ability to prevent price increases during the inquiry.

• Price notifications: Commonwealth Treasurer or

ACCC (with approval) may notify goods or services

and hence restrict price increases.

• Price monitoring: Commonwealth Treasurer may

direct ACCC to monitor prices, costs and profits in

relation to the supply of goods or services.

• At present, no Australian port infrastructure is

subject to either Part IIIA or Part VIIA. However,

either regime could potentially be applied if

concerns arose from the public or port users.

• The Part VIIA regime has been applied to

stevedoring operations at various key ports. The

ACCC currently monitors prices, costs and profits

of stevedores at those ports.

48

Ports - Commonwealth regulatory overlay

National Access Regime (Part IIIA)

49

About Norton Rose Fulbright

Norton Rose Fulbright "…continue to be market leaders" and “their knowledge

of industry is first rate”. Infrastructure & Projects – Asia-Pacific Region Chambers

0

Dr Martyn Taylor

Partner

Norton Rose Fulbright Australia

+61 2 9330 8056

Contact us

nortonrosefulbright.com

2185357250

Norton Rose Fulbright Australia is a law firm as defined in the Legal Profession Acts of the Australian states and territory in which it practises.

Norton Rose Fulbright LLP, Norton Rose Fulbright Australia, Norton Rose Fulbright Canada LLP, Norton Rose Fulbright South Africa (incorporated as Deneys Reitz Inc) and Fulbright & Jaworski LLP, each of which is a separate legal entity,

are members (‘the Norton Rose Fulbright members’) of Norton Rose Fulbright Verein, a Swiss Verein. Norton Rose Fulbright Vere in helps coordinate the activities of the Norton Rose Fulbright members but does not itself provide legal

services to clients.

The purpose of this communication is to provide general information of a legal nature. It does not contain a full analysis of the law nor does it constitute an opinion of any Norton Rose Fulbright entity on the points of law discussed. You must

take specific legal advice on any particular matter which concerns you. If you require any advice or further information, please speak to your usual contact at Norton Rose Fulbright.