statement of accounts 2011/2012 -...

TRANSCRIPT

STATEMENT OF ACCOUNTS 2011/2012

Page 1 of 162

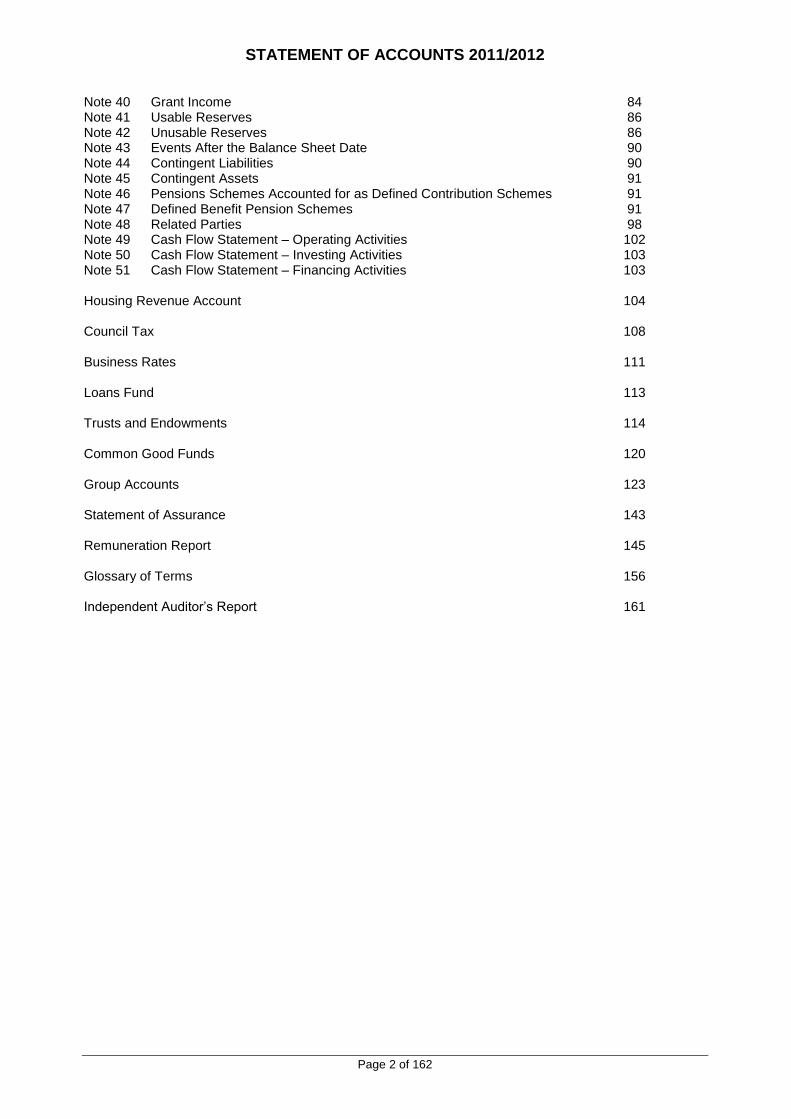

CONTENTS PAGE Explanatory Foreword by the Head of Finance 3 Statement of Responsibilities 13 Movement in Reserves Statement 14 Comprehensive Income and Expenditure Statement 16 Balance Sheet 17 Cash Flow Statement 18 Notes to the Financial Statements 19 Note 1 Accounting Policies 19 Note 2 Accounting Standards That Have Been Issued but Have Not Yet Been

Adopted

34 Note 3 Critical Judgements in Applying Accounting Policies 34 Note 4 Assumptions Made About the Future and Other Major Sources of

Estimation Uncertainty

34 Note 5 Adjustments between Accounting Basis and Funding Basis under

Regulations

36 Note 6 Transfers to/from Earmarked Reserves 41 Note 7 Amounts Reported for Resource Allocation Decisions 43 Note 8 Other Operating Expenditure 48 Note 9 Financing and Investment Income and Expenditure 48 Note 10 Taxation and Non Specific Grant Incomes 48 Note 11 Material Items of Income and Expense 48 Note 12 Exceptional Items and Prior Period Adjustments 48 Note 13 Trading Operations 50 Note 14 Agency Services 52 Note 15 Partnership Arrangements under the Community Care and Health

(Scotland) Act 2002

52 Note 16 External Audit Costs 52 Note 17 Councillors’ Remuneration 53 Note 18 Officers’ Remuneration 53 Note 19 Termination Benefits 53 Note 20 Construction Contracts 53 Note 21 Capital Expenditure and Capital Financing 53 Note 22 Property, Plant and Equipment 54 Note 23 Heritage Assets 61 Note 24 Heritage Assets – Five Year Summary of Transactions 61 Note 25 Heritage Assets – Further Information on Museums’ Collections 61 Note 26 Heritage Assets – Change in Accounting Policy 66 Note 27 Investment Properties 68 Note 28 Intangible Assets 68 Note 29 Assets Held for Sale 70 Note 30 Leases 70 Note 31 Private Finance Initiatives and Similar Contracts 73 Note 32 Impairment Losses 75 Note 33 Financial Instruments 75 Note 34 Nature and Extent of Risks Arising from Financial Instruments 77 Note 35 Inventories 80 Note 36 Debtors 81 Note 37 Cash and Cash Equivalents 82 Note 38 Creditors 82 Note 39 Provisions 82

STATEMENT OF ACCOUNTS 2011/2012

Page 2 of 162

Note 40 Grant Income 84 Note 41 Usable Reserves 86 Note 42 Unusable Reserves 86 Note 43 Events After the Balance Sheet Date 90 Note 44 Contingent Liabilities 90 Note 45 Contingent Assets 91 Note 46 Pensions Schemes Accounted for as Defined Contribution Schemes 91 Note 47 Defined Benefit Pension Schemes 91 Note 48 Related Parties 98 Note 49 Cash Flow Statement – Operating Activities 102 Note 50 Cash Flow Statement – Investing Activities 103 Note 51 Cash Flow Statement – Financing Activities 103 Housing Revenue Account 104 Council Tax 108 Business Rates 111 Loans Fund 113 Trusts and Endowments 114 Common Good Funds 120 Group Accounts 123 Statement of Assurance 143 Remuneration Report 145 Glossary of Terms 156 Independent Auditor’s Report 161

EXPLANATORY FOREWORD BY THE HEAD OF FINANCE

Page 3 of 162

INTRODUCTION

The purpose of the annual Statement of Accounts is to demonstrate proper stewardship of the Council’s financial affairs. The Statement has been prepared in accordance with the Code of Practice on Local Authority Accounting in the United Kingdom 2011/12 Based on International Financial Reporting Standards (the Code) and the 2011/12 Code Update, both of which were issued by the Chartered Institute of Public Finance and Accountancy (CIPFA) and the Local Authority (Scotland) Accounts Advisory Committee (LASAAC). This foreword provides an explanation of the Statement of Accounts and of the most significant matters reported in the Accounts, together with a summary of the financial outturn for the year ended 31 March 2012. 2011/12 sees the second year in which the Statement of Accounts has been produced using International Financial Reporting Standards (IFRS). The format is largely similar to the 2010/11 Statement of Accounts, although there have been some changes, mostly notably the introduction of a new category of fixed asset called Heritage Assets. The purpose of the Financial Statements is described in detail in the next section. Details of the significance of the changes with regard to Heritage Assets are included within the section on Significant Changes in Accounting Policies on page 9, in Note 12 on Exceptional Items and Prior Period Adjustments on pages 48 - 50 and in Note 26 on Heritage Assets - Change in Accounting Policy on Pages 66 - 68. FINANCIAL STATEMENTS During the year, the Council increased its Usable Reserves by £23,020,000 from £44,182,000 to £67,202,000, with the movements shown as follows:

31 March

2011 31 March

2012 (Increase)/ Decrease

£'000 £'000 £'000

General Fund Balance (17,404) (27,863) (10,459)

Earmarked General Fund Reserves (11,759) (19,595) (7,836)

Housing Revenue Account (HRA) (2,000) (2,000) -

Earmarked HRA Reserves (3,033) - 3,033

Capital Receipts Reserve (696) (692) 4

Capital Fund (5,956) (10,803) (4,847)

Repairs and Renewals Fund (980) (4,047) (3,067)

Insurance Fund (1,119) (1,250) (131)

Capital Grants Unapplied Account (1,235) (952) 283

Total Usable Reserves (44,182) (67,202) (23,020)

The largest movement is in the General Fund Balance, which has increased by £10,459,000. The Revenue Budget had been set to reduce this balance by £9,777,000. However, during the year, the measures that were put in place during 2010/11 to encourage proactive management of budgets across all services continued and this was supplemented by the early achievement of some savings, as reported to Policy and Resources Committee throughout the year. Significant transfers to the Invest to Save Fund (one of the Earmarked General Fund Reserves), the Capital Fund and the Winter Maintenance and Other Emergencies Fund (an element of the Repairs and Renewals Fund) were approved during the year. Policy and Resources Committee also approved a revised Usable Reserves Strategy.

The following statements are shown in the accounts. 1. Movement in Reserves Statement This statement shows the movement in the year on the different reserves held by the Council, analysed into “usable reserves” (i.e. those that can be applied to fund expenditure or reduce local taxation) and

EXPLANATORY FOREWORD BY THE HEAD OF FINANCE

Page 4 of 162

other reserves. The Surplus or (Deficit) on the Provision of Services line shows the true economic cost of providing the Council’s services, more details of which are shown in the Comprehensive Income and Expenditure Statement. These are different from the statutory amounts required to be charged to the General Fund Balance and the Housing Revenue Account for council tax setting and dwellings rent setting purposes. The Net Increase/Decrease before Transfers to Earmarked Reserves line shows the statutory General Fund Balance and Housing Revenue Account Balance before any discretionary transfers to or from earmarked reserves undertaken by the Council. 2. Comprehensive Income and Expenditure Statement This statement shows the accounting cost in the year of providing services in accordance with generally accepted accounting practices, rather than the amount to be funded from taxation. Authorities raise taxation to cover expenditure in accordance with regulations; this may be different from the accounting cost. The taxation position is shown in the Movement in Reserves Statement. 3. Balance Sheet The Balance Sheet shows the value as at the Balance Sheet date of the assets and liabilities recognised by the Council. The net assets of the Council (assets less liabilities) are matched by the reserves held by the Council. Reserves are reported in two categories. The first category of reserves are usable reserves, i.e. those reserves that the Council may use to provide services, subject to the need to maintain a prudent level of reserves and any statutory limitations on their use (for example the Capital Receipts Reserve that may only be used to fund capital expenditure or repay debt). The second category of reserves is those that the Council is not able to use to provide services. This category of reserves includes reserves that hold unrealised gains and losses (for example the Revaluation Reserve), where amounts would only become available to provide services if the assets are sold; and reserves that hold timing differences shown in the Movement in Reserves Statement line “Adjustments between accounting basis and funding basis under regulations”. 4. Cash Flow Statement The Cash Flow Statement shows the changes in cash and cash equivalents of the Council during the reporting period. The statement shows how the Council generates and uses cash and cash equivalents by classifying cash flows as operating, investing and financing activities. The amount of net cash flows arising from operating activities is a key indicator of the extent to which the operations of the Council are funded by way of taxation and grant income or from the recipients of services provided by the Council. Investing activities represent the extent to which cash outflows have been made for resources which are intended to contribute to the Council’s future service delivery. Cash flows arising from financing activities are useful in predicting claims on future cash flows by providers of capital (i.e. borrowing) to the Council. 5. Notes to the Financial Statements The Notes to the Financial Statements provide supplementary information on core financial transactions which are not detailed separately in the statements. 6. Housing Revenue Account Income and Expenditure Statement The Housing Revenue Account Income and Expenditure Statement shows the economic cost in the year of providing housing services in accordance with generally accepted accounting practices, rather than the amount to be funded from rents and other income. Authorities charge rents to cover expenditure in accordance with regulations; this may be different from the accounting cost. The increase or decrease in the year, on the basis of which rents are raised, is shown in the Movement on the Housing Revenue Account Statement. 7. Council Tax Income Account The Council Tax Income Account shows the gross income raised from council taxes levies and deductions made under Statute. The resultant net income is transferred to the Comprehensive Income and Expenditure Statement of the Council.

EXPLANATORY FOREWORD BY THE HEAD OF FINANCE

Page 5 of 162

8. Business Rate Account The Business Rate Account is an agent’s statement that reflects the statutory obligation for billing authorities to maintain a separate Business Rate Account. The statement shows the gross income from rates and deductions made under Statute. The net income is paid to the Scottish Government as a contribution to the national non-domestic rate pool.

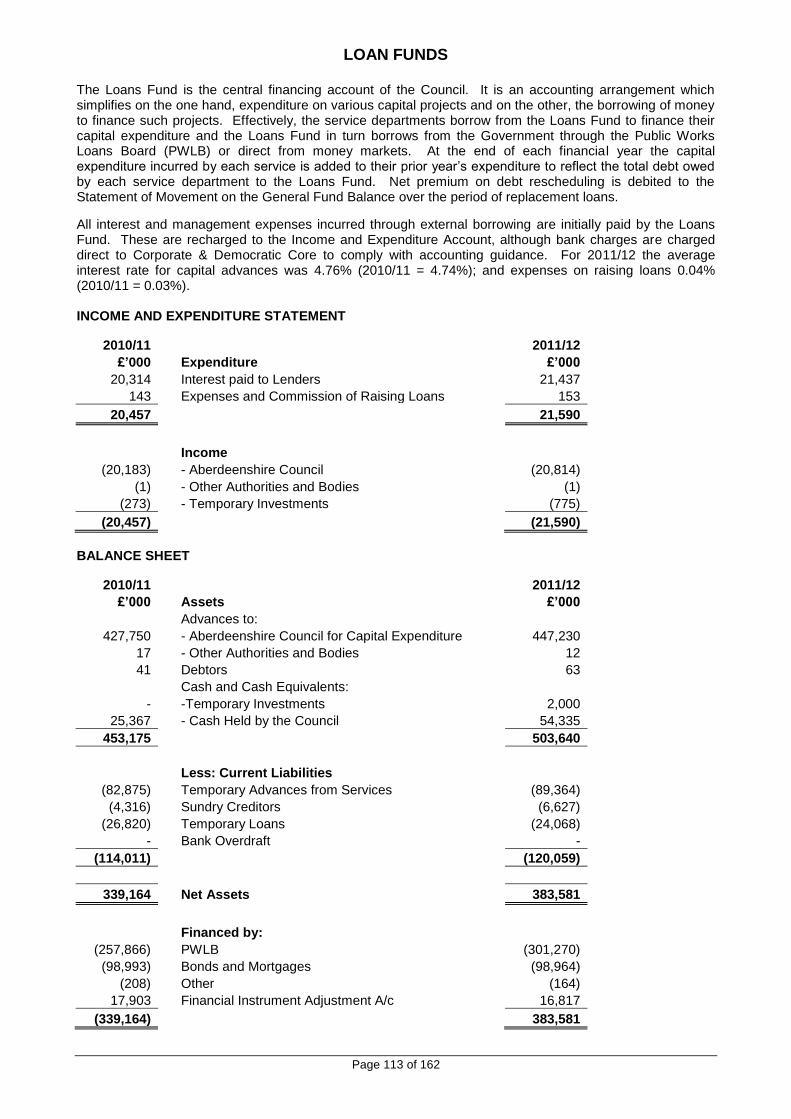

9. Loans Fund A Loans Fund is maintained under powers contained in the Local Government (Scotland) Act 1975 and is the central capital financing account of the Council. It is an accounting arrangement which simplifies the funding of capital projects, funded by borrowing to the actual borrowing undertaken. All advances to finance capital expenditure are made through the Loans Fund except for capital projects financed directly from revenue or from capital receipts. The Council uses the annuity method to calculate the repayment of loans fund advances. The maximum period for the repayment of those advances are set out in the Scottish Government’s Financial Circular 29/1975. All interest and management expenses incurred through external borrowing are initially paid by the Loans Fund. These are recharged to the Comprehensive Income and Expenditure Statement, although bank charges are charged direct to Corporate and Democratic Core. 10. Trust Funds and Common Good Funds

Trust Funds and Common Good Funds administered by the Council are shown separately within the Statement of Accounts, together with any relevant Notes that provide supplementary information. An Income and Expenditure Statement and Balance Sheet are shown for the total of all Trust Funds and similar statements are shown for the total of all Common Good Funds. 11. Group Accounts A Movement in Reserves Statement, a Comprehensive Income and Expenditure Statement, a Balance Sheet and a Cash Flow Statement, together with any relevant Notes are also shown for the Council and its Group entities. 12. Remuneration Report The Remuneration Report provides narrative details of the Council’s remuneration policy for its senior councillors, senior employees and subsidiary bodies where it has a role in determining the remuneration policy, and states how remuneration arrangements are managed, including the role and membership of any remuneration committee. It also discloses details of remuneration information for senior councillors, senior employees and subsidiary bodies, including pension benefits. Information is provided on the number of persons whose remuneration was £50,000 or more, disclosed in bands of £5,000. The Remuneration Report is produced in terms of the Scottish Government’s Local Government Finance Circular No 8/2011 (revised and re-issued). FINANCIAL OUTTURN 2011/12 1. General Fund Revenue Expenditure The Comprehensive Income and Expenditure Statement on page 16 shows a deficit on the provision of services of £26,131,000. When the figure is adjusted to take account of transactions that have been included on an accounting basis, expenditure and income that is required to be included on a funding basis under statute, and any transfers to or from Council reserves, the movement in the General Fund balance is an increase of £18,295,000. Of this movement, £7,836,000 has been transferred to Earmarked Reserves of the General Fund, giving an increase in the working balance of £10,459,000. This compares with a budgeted reduction of £9,777,000 in the working balance, giving a surplus of £20,236,000 on the working balance for the year.

EXPLANATORY FOREWORD BY THE HEAD OF FINANCE

Page 6 of 162

In 2011/12, the Council budgeted to spend £502,823,000 on the provision of Services. Actual expenditure was £485,681,000 or £17,142,000 lower than anticipated. Expenditure on other items such as Capital Financing Costs, Trading Accounts and transfers to and from various Council balances was budgeted at £38,484,000. Actual expenditure was £35,983,000 or £2,501,000 lower than anticipated. Income from Revenue Support Grant was budgeted at £344,291,000, income from Business Rates was budgeted at £68,500,000 and income from Council Tax was budgeted at £118,739,000. Actual income in total from these sources was £532,123,000 or £593,000 higher than anticipated. Taking all of the above into account gives net expenditure for the year which is £20,236,000 lower than anticipated. The actual working balance at the year end is £27,863,000. The surplus has been generated through proactive budget management across all services and the early achievement of some savings, as reported to Policy and Resources Committee throughout the year. This is a positive outturn that reflects sound financial management across all Council Services and will offer both protection against the uncertainty surrounding future years' financial pressures in the current climate, and, an opportunity to enhance service delivery through a managed programme of investment. Since these savings are largely one-off the surplus needs to be set aside to manage future financial risk and to create the capacity for refocusing service delivery. Reasons for the major underspends include:

management of vacant posts, particularly where services reviews are in progress;

a reduction in the number of teaching staff on conserved salaries, the non-filling of some vacancies and changes to the terms and conditions of service for Supply Teachers;

a reduction in the number of placements in residential care due to the use of more flexible local solutions;

a delay in negotiating the terms and conditions relating to the purchase of an Electronic Homecare Management System;

increased income from planning application fees and the rental of industrial and commercial properties;

increased income from the sale of recyclates, reduced levels of waste and a reduction in the costs associated with waste disposal including new contract prices being in place;

rephasing of schemes associated with the local economy, particularly those which rely on third parties;

lower leasing costs for vehicles as new vehicles have been purchased rather than leased and reductions in the purchase of small items of vehicles and plant as a result of delays in the tender process;

an underspend on Capital Financing Charges due to a combination of factors including delays in the capital programme, favourable borrowing conditions and lower than budgeted principal repayments;

delays in progressing a number of technologically based projects and savings in Hardware Maintenance Contracts, Software Infrastructure, Business Systems, the cost of Data Lines and the IT Development Strategy;

the return of a significant surplus from the Grampian Joint Police Board; and

a higher than forecast recovery of benefit subsidy. Partly offsetting these underspends are a number of overspends, including:

an increase in essential reactive maintenance of council properties;

a shortfall in achieving some cross service procurement savings as a result of a higher than anticipated inflation rate and policy implications associated with some of the originally planned savings; and

a significant increase in the provision for bad debts. The majority of the above items have been detailed in monitoring reports to the Council as issues arose throughout the financial year. The Council made some extremely difficult decisions in setting its budget for 2011/12 and the following three years. The underspend in 2011/12 includes savings brought forward from future years. Despite a significant increase in the provision for bad debts, increased income from a number of sources in the last few months of the year was experienced. There are still financial challenges ahead and the Council is well placed to face these challenges, starting from a strong base of sound financial performance. With the

EXPLANATORY FOREWORD BY THE HEAD OF FINANCE

Page 7 of 162

challenges comes opportunity, and the Council will continue to direct resources at areas of greatest need through a combination of further efficiency measures and realignment of budgets. 2. Housing Revenue Account (HRA) The HRA Income and Expenditure Statement on page 103 shows a deficit of £42,908,000. When the figure is adjusted to take account of transactions that have been included on an accounting basis, expenditure and income that is required to be included on a funding basis under statute, and any transfers to or from Council reserves, the movement in the HRA balance is a reduction of £3,033,000.

The revised HRA budget for 2011/12 had approved expenditure of £47,802,000 and income of £44,769,000, giving a net operating deficit of £3,033,000. Actual expenditure totalled £50,979,000 with income of £47,946,000, giving a net deficit of £3,033,000. This deficit was funded by a transfer from the HRA balance.

Although the net deficit was in line with the budget overall, there were a number of variances within the budget. Reasons for the underspends include:

lower salary costs due to vacant posts as a result of proactive vacancy management;

heating and lighting costs are lower than budget due to large credits received during the year relating to previous years;

planned maintenance costs are lower than budget due to tenders for the external painterwork contract being lower than anticipated;

cleaning costs are lower than budget due to delays in implementing the sheltered housing cleaning contract;

underspends in the capital programme and higher balances brought forward from previous years have resulted in reduced borrowing requirements. The cost of borrowing has also reduced due to lower interest rates;

rental income is higher than budget due to a net 35 properties being added to stock through the new build programme;

additional rental income in respect of housing support provided by staff in hostels;

additional income for the new build programme and the provision of equipment and adaptations to council house tenants; and

additional income from temporary accommodation units.

Partly offsetting these underspends are a number of overspends, including:

higher expenditure on response repairs due to higher levels of repairs to gas and oil heating systems and damage to buildings following the adverse weather over the winter months; and

a significant increase in the provision for bad debts.

The budget included £7,023,000 to meet capital expenditure. The variances detailed above produced a net underspend, which allowed expenditure of £13,872,000 to be used to meet capital expenditure whilst reducing the HRA balance by £3,033,000 as planned. This continues the strategy which had been in place over the previous two years to fund capital expenditure using the HRA balance as an alternative to borrowing. This strategy generated substantial savings on Capital Financing Costs. This strategy has reduced the HRA balance to £2,000,000 which is required to be retained as a working balance to meet any unexpected costs that occur. No further funding, other than any budgeted provision will be available to finance capital expenditure in 2012/13, and the balance of capital expenditure will be met from borrowing.

The HRA balance is in accordance with the 30 Year “Retention Plus” business plan agreed by the Council for the HRA. The business plan seeks to ensure that the future needs of the stock and of tenants can be met and are affordable.

EXPLANATORY FOREWORD BY THE HEAD OF FINANCE

Page 8 of 162

3. Trading Operations The Local Government in Scotland Act 2003 sets out a statutory duty for Councils to achieve Best Value. It provides a strong link between the duty of Best Value, the delivery of services and the reporting of financial performance. Councils are required to maintain statutory trading accounts for “significant trading operations”, and these operations should break even over a three year rolling period. Under the Act, the Council has established trading accounts for two services – Housing Repairs and Roads Operations. The trading operations returned a net surplus of £2,875,000 in 2011/12. Housing Repairs and Roads Operations both achieved their statutory break-even target over the three year period 2009/10 to 2011/12. Further details of the trading operations are set out in note 13 on pages 50 - 51. At its meeting on 10 November 2011, Policy and Resources Committee agreed that Housing Repairs would no longer be a statutory trading account, with effect from 1 April 2012. From that date, its costs will be consolidated into the Housing Revenue Account. 4. Capital Expenditure Under the Prudential Code for capital finance, Aberdeenshire Council is allowed to determine its own limits for borrowing and capital expenditure. Expenditure plans must be affordable, sustainable and prudent. Capital expenditure is aligned closely with the Council’s Corporate Asset Management Plan. The Council’s approach to asset management involves producing and continuing to update a wide range of relevant information on the performance of assets and the full investigation of capital and revenue spending decisions. Capital expenditure is reported in terms of the main themes that determine the strategic priorities of the Council. In 2011/12, total capital expenditure was £74,782,000, of which £8,442,000 was spent on Community Wellbeing, £19,087,000 was spent on Jobs and the Economy, £13,078,000 was spent on Lifelong Learning, £1,827,000 was spent on Sustainable Environment and £7,350,000 was spent on Corporate Improvement. In addition, £24,998,000 was spent on HRA Housing. Capital expenditure includes the purchase of intangible assets, such as software. MATERIAL ASSETS ACQUIRED OR LIABILITIES INCURRED An opportunity arose during the year to make an advance payment £20,963,000 to the North East Scotland Pension Fund in respect of deficit contributions for the period 2012-15. This capitalised payment attracted an advantageous discount over the payment of deficit contributions in year. The transaction has been recognised as a debtor on the balance sheet. PENSION LIABILITIES The Statement of Accounts includes the future pension liability of the Council resulting from the full implementation of IAS 19. Accounting Policy 1.6 on pages 21-22 sets out the Council’s policy on pension costs and note 42 on pages 86 - 90 and notes 46 - 47 on pages 91 - 98 give more details of the pension liabilities. The Council participates in the Local Government Pension Scheme which is administered by Aberdeen City Council, known as the North East Scotland Pension Fund. This Fund is in deficit due to a substantial fall in the value of world stock markets in previous years. The Council’s share of the net Fund deficit has increased during 2011/12 by £25,988,000. The deficit position on the Fund was considered as part of the triennial revaluation of the Pension Fund as at 31 March 2011. At each full revaluation of the Fund, the assets and liabilities of the Fund are recalculated in full. As a result of this recalculation, the value of both the assets and the liabilities has

EXPLANATORY FOREWORD BY THE HEAD OF FINANCE

Page 9 of 162

been reduced. However, the reduction in the value of the assets is greater than the reduction in the value of the liabilities, and this has resulted in an increase in the Council’s share of the net Fund deficit. A funding plan has been determined with the aim of recovering the deficit over a period of up to 22 years which requires additional contributions to correct the shortfall, and this is explained in Note 47 on page 96. The next triennial valuation will be as at 31 March 2014. MATERIAL AND UNUSUAL CHARGES OR CREDITS There are no material and unusual charges or credits that are required to be highlighted. SIGNIFICANT CHANGES IN ACCOUNTING POLICIES The Code of Practice on Local Authority Accounting in the United Kingdom 2011/12 introduced a change to the treatment in accounting for heritage assets held by the Council. Heritage assets are now required to be carried in the balance sheet at valuation. Various balances and transactions have been restated throughout the accounts. The change has necessitated the preparation of three Balance Sheets. These are as at 1 April 2010, 31 March 2011 and 31 March 2012. Other financial statements and disclosure notes have been restated for 2010/11. More details on the restatements are shown in Note 12 on Exceptional Items and Prior Period Adjustments and Note 26 on Heritage Assets – Change in Accounting Policy. MAJOR CHANGES IN STATUTORY FUNCTIONS There were no major changes in statutory functions during 2011/12, however on 7 August 2012, the Police and Fire Reform (Scotland) Act 2012 received royal assent. Responsibility for Police and Fire and Rescue Services will transfer from local government to new central government bodies on 1 April 2013. The full impact of the reform is being assessed currently CURRENT BORROWING FACILITIES

The Council’s Treasury Management Strategy sets out the following criteria to determine from whom the Council may borrow: any other UK local authority or government guaranteed institution and any bank, financial institution, insurance company or utility company which is governed by MiFID, the EU Markets in Financial Instruments Directive (2004/39/EC). The long term borrowing at 31 March 2012 was £400,398,000 (2010/11 £357,068,000) of which £301,270,000 (2010/11 £257,866,000) was from the Public Works Loan Board (PWLB) with the balance being market loans i.e. bonds and mortgages. During 2011/12 capital expenditure amounted to £74,782,000. This was funded by a combination of revenue funding, capital grant, capital receipts and long term borrowing. All new long term borrowing in 2011/12 was from the PWLB and no other financial instruments were used in 2011/12.

FUNDS AVAILABLE TO MEET CAPITAL EXPENDITURE

The total amount of capital expenditure incurred to 31 March 2012 (including the value of assets acquired under finance leases and PFI/PPP contracts) that has not yet been charged to the revenue account of the Council is £27,729,000. The reason it has not been charged to the revenue account is that the assets are to be financed in future years by charges to revenue as they are used by the Council. The resources used to finance this expenditure is a combination of PWLB and market borrowing.

SIGNIFICANT PROVISIONS AND WRITE OFFS There were no significant increases in provisions or write offs during the year.

EXPLANATORY FOREWORD BY THE HEAD OF FINANCE

Page 10 of 162

MATERIAL EVENTS AFTER THE REPORTING DATE No material events have occurred after the reporting date that require to be disclosed. FINANCIAL RATIOS For 2011/12 Councils in Scotland have introduced the use of ratios to support the interpretation of the Council’s financial statements, financial position and performance. 1. Reserves

1.1 Uncommitted General Fund Balance as a Percentage of Annual Budgeted Expenditure

Purpose: To reflect the percentage of reserves that are neither committed nor earmarked against the annual revenue budget.

Actual 2010/11

Actual 2011/12

3.16%

5.13%

1.2 Movement in the Uncommitted General Fund Balance

Purpose: To reflect the movement in reserves that are neither committed nor earmarked in accordance with the reserve strategy of the council. Actual

2010/11 Actual

2011/12 £’000 £’000 Opening Uncommitted General Fund Balance 9,519 17,404 Closing Uncommitted General Fund Balance 17,404 27,863 Movement Uncommitted General Fund Balance 7,885 10,459

The Working Balances provide a cushion against the impact of any unforeseen circumstances or emergencies. 2. Council Tax 2.1 In-year Collection Rate Purpose: To reflect the percentage of income received from Council Tax for year received by the year end.

Actual 2010/11

Actual 2011/12

95.83% 96.21% 2.2 Council Tax Income as a Percentage of Overall Funding Purpose: To reflect the percentage of funding for the Council that comes from Council Tax. Actual

2010/11 Actual

2011/12 £’000 £’000 Council Tax Income (117,970) (119,412) Overall Funding: CT/Business Rates/Non Ring Fenced Government Grants (538,887) (532,123) Movement General Fund Balance 21.89% 22.44%

EXPLANATORY FOREWORD BY THE HEAD OF FINANCE

Page 11 of 162

3. Financial Management 3.1 Actual Outturn as a Percentage of Net Expenditure Budget

Purpose: To reflect the percentage by which actual outturn differs from budgeted outturn. Actual

2010/11 Actual

2011/12 General Fund 1.9% 3.41% 4. Debt and Borrowing 4.1 Estimated Ratio of Financing Cost to Net Revenue Stream Purpose: This ratio indicates the percentage of the revenue budget that is required to meet the cost of external borrowing. A separate ratio is shown for the General Fund and Housing Revenue Account (HRA), and indicates the affordability of the Council’s capital expenditure proposals. Actual

2010/11 Actual

2011/12 General Fund 4.27% 5.84% Housing Revenue Account 15.99% 15.12% 4.2 Estimated Incremental Impact of Investment Decisions on Council Tax/Rents Purpose: This ratio links with the previous ratio and indicates the impact of capital expenditure plans on the revenue budget. Actual

2010/11 Actual

2011/12 General Fund zero zero Housing Revenue Account zero zero This indicates that, because there is no proposed change to the existing capital plans which impacts on the level of borrowing over the medium term there is no incremental effect on council tax or rents. 4.3 Net Borrowing and the Capital Financing Requirement Purpose: These indicators show the estimated total borrowing required to fund existing and additional capital expenditure proposals and the estimated level of actual borrowing. The indicators are only required for the Council’s overall position and are not divided between the General Fund and HRA. Actual

2010/11 Actual

2011/12 £m £m Net Borrowing 420 430 Capital Financing Requirement 485 499 Net borrowing is less than the capital financing requirement. This indicates that the Council is utilising internal revenue balances to meet the cash requirements of its capital investment plans. IMPACT OF ECONOMIC CLIMATE In 2011/12 the UK economy stagnated and entered back into recession in the final quarter. This together with the global economic climate and the fall out from the banking crisis in 2008, has impacted on the activities of the Council and is therefore reflected within the Statement of Accounts. The most material areas of impact are considered below. Impairment of Non Current Assets – Non current assets are valued on a five year rolling programme (see Note 22), although an impairment review is carried out at each balance sheet date. Asset values in

EXPLANATORY FOREWORD BY THE HEAD OF FINANCE

Page 12 of 162

Aberdeenshire have not been affected as significantly as in other parts of the country by the recession. Impairment losses totalling £14,730,000 have been recognised in the Revaluation Reserve or Surplus or Deficit on the Provision of Services, representing 0.72% of the net book value of non current assets. The main economic factors relate to changes in construction costs and market conditions. Impairment of Debtors - Bad Debt Provision - The credit risk the Council is exposed to has increased as a result of the economic downturn. This has been reflected when reviewing the bad debt provision in relation to the customers of the Council, which has increased by 2.06% as detailed below. The increase in provision is charged to the Comprehensive Income and Expenditure Statement.

2010/11

2011/12 Increase/

(Decrease)

£’000 £’000 %

General Debtors 3,458 4,239 22.58

Revenues 20,928 22,649 (8.22)

Housing Rents 1,203 1,239 2.99

Total Bad Debt Provision 25,589 28,127 9.92

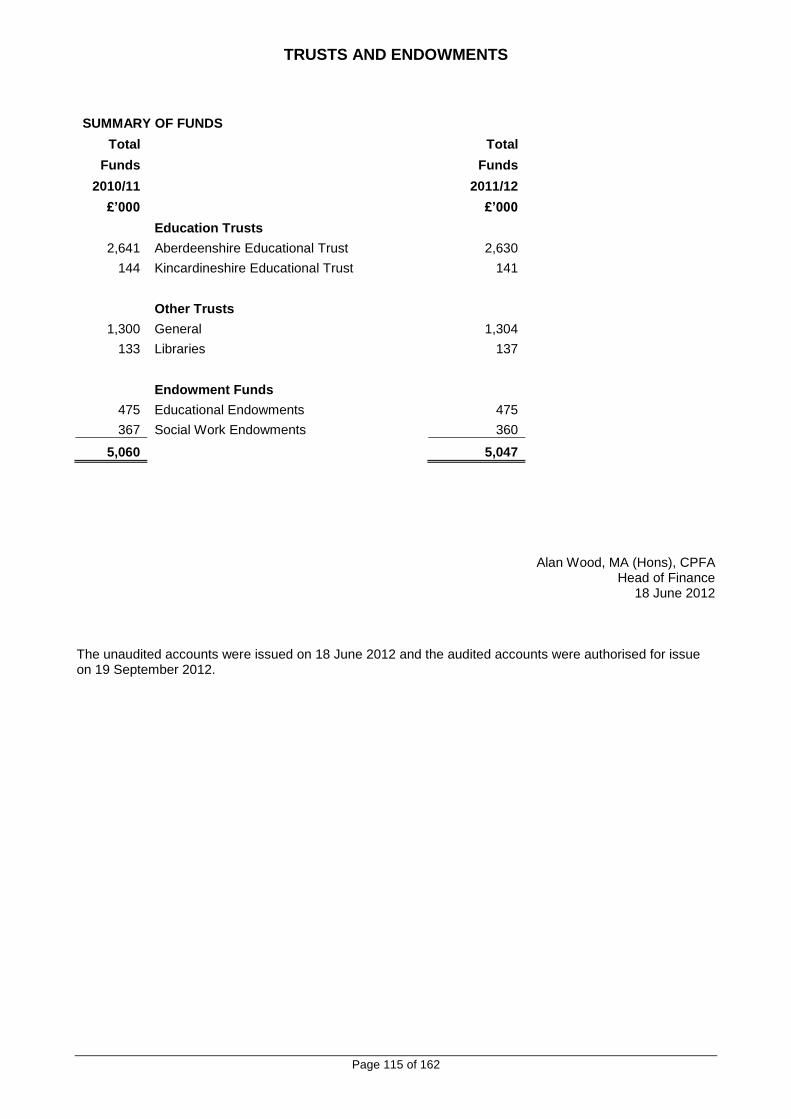

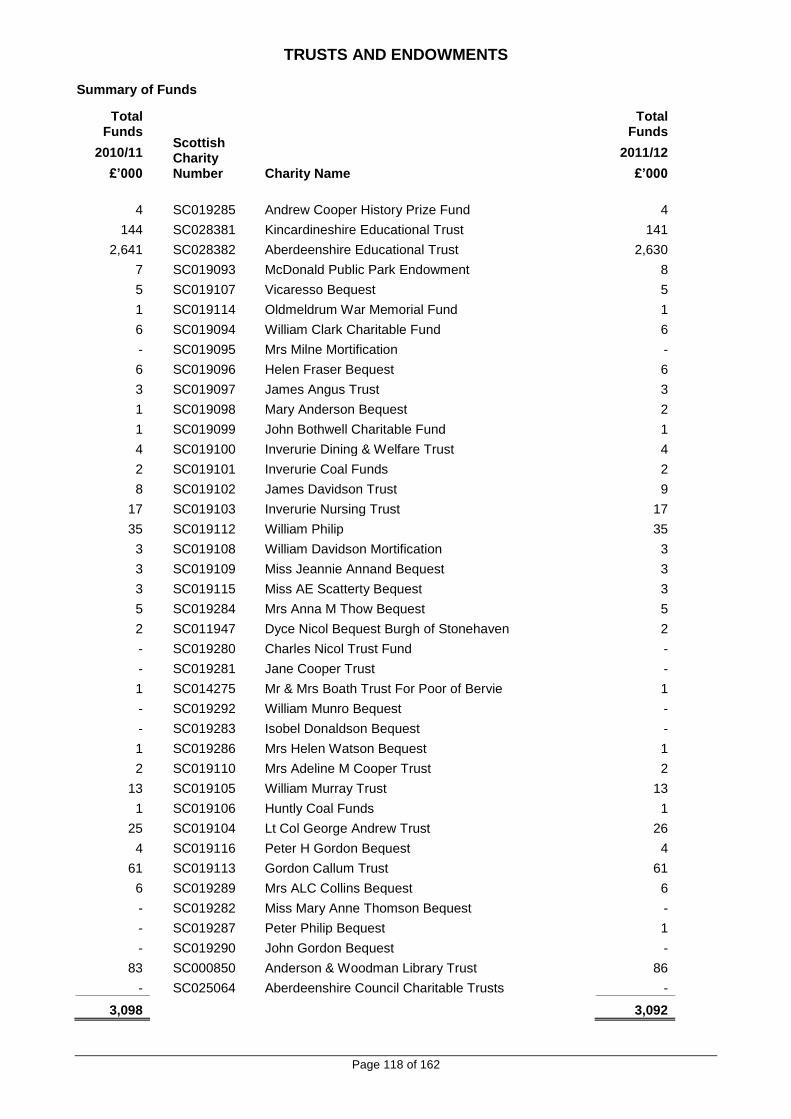

Shareholding Values - associated with the economic downturn is a reduction in share prices. The Council administers 423 Trusts and Endowments with a total value of £5,047,000, details of which can be found on pages 113 - 118. Of the funds invested, £2,850,000 is invested in stocks and shares. These consist of unit trusts and stocks and shares some of which are managed by fund managers. The change in value of investments is a decrease of £12,000 from 2010/11 to 2011/12. Treasury Management Activities - The Council has been pro-active in its approach to Treasury Management and has not suffered any adverse effects from the economic situation in 2011/12. As a result of the banking crisis, the credit ratings of many of the financial institutions used by the Council previously to invest its cash balances, now fall outwith the criteria of the Council’s Investment Policy and low levels of bank interest rates have led to relatively low levels of investment returns. However long term borrowing rates during the year were at historic lows and borrowing requirements were secured significantly lower than anticipated. RELATIONSHIP WITH OTHER PUBLISHED DOCUMENTS A summarised version of the financial statements will be published on the Council’s website. ACKNOWLEDGEMENTS The production of the Statement of Accounts is very much a team effort involving many staff from both my own and other services of the Council. I would like to take this opportunity to thank all those involved for their help and co-operation.

Alan Wood, MA (Hons), CPFA Head of Finance

18 June 2012

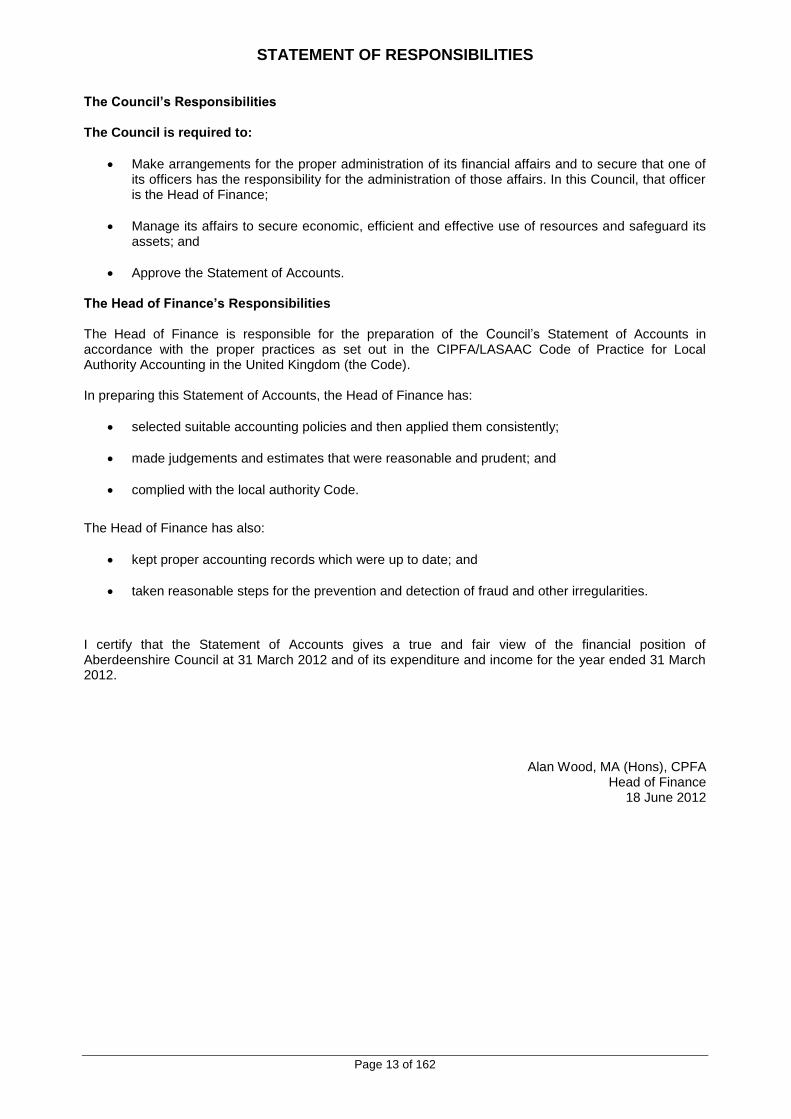

STATEMENT OF RESPONSIBILITIES

Page 13 of 162

The Council’s Responsibilities The Council is required to:

Make arrangements for the proper administration of its financial affairs and to secure that one of its officers has the responsibility for the administration of those affairs. In this Council, that officer is the Head of Finance;

Manage its affairs to secure economic, efficient and effective use of resources and safeguard its assets; and

Approve the Statement of Accounts. The Head of Finance’s Responsibilities The Head of Finance is responsible for the preparation of the Council’s Statement of Accounts in accordance with the proper practices as set out in the CIPFA/LASAAC Code of Practice for Local Authority Accounting in the United Kingdom (the Code). In preparing this Statement of Accounts, the Head of Finance has:

selected suitable accounting policies and then applied them consistently;

made judgements and estimates that were reasonable and prudent; and

complied with the local authority Code.

The Head of Finance has also:

kept proper accounting records which were up to date; and

taken reasonable steps for the prevention and detection of fraud and other irregularities.

I certify that the Statement of Accounts gives a true and fair view of the financial position of Aberdeenshire Council at 31 March 2012 and of its expenditure and income for the year ended 31 March 2012.

Alan Wood, MA (Hons), CPFA Head of Finance

18 June 2012

MOVEMENT IN RESERVES STATEMENT FOR THE YEAR ENDED 31 MARCH 2012

Page 14 of 162

General Fund

Balance

Earmarked General

Fund Reserves

Housing Revenue Account

Earmarked HRA

Reserves

Capital Receipts Reserve

Capital Fund

Repairs and

Renewals Fund

Insurance Fund

Capital Grants

Unapplied Account

Total Usable

Reserves

Restated Total

Unusable Reserves

Restated Total

Council Reserves

Notes Ref

£’000 £'000 £'000 £'000 £'000 £'000 £'000 £'000 £'000 £'000 £'000 £'000

Balance at 31 March 2010 (9,519) (6,772) (2,000) (17,772) (699) (5,919) (3,173) (1,219) (490) (47,563) (1,066,052) (1,113,615)

Movement in Reserves During 2010/11

(Surplus) or Deficit on the Provision of Services (22,900) - (1,551) - - - - - - (24,451) - (24,451)

Other Comprehensive Income and Expenditure - - - - - - - - - - (31,587) (31,587)

Total Comprehensive Income and Expenditure (22,900) - (1,551) - - - - - - (24,451) (31,587) (56,038)

Adjustments Between Accounting Basis & Funding Basis Under Regulations 10,373 - 18,204 - - - - - (745) 27,832 (27,832) - 5

Net(Increase)/ Decrease before Transfers to Earmarked Reserves (12,527) - 16,653 - - - - - (745) 3,381 (59,419) (56,038)

Transfers to/from Earmarked Reserves 4,642 (4,987) (16,653) 14,739 3 (37) 2,193 100 - - - -

(Increase)/ Decrease in 2010/11

(7,885)

(4,987)

-

14,739

3

(37)

2,193

100

(745)

3,381 (59,419) (56,038)

Balance at 31 March 2011 Carried Forward (17,404) (11,759) (2,000) (3,033) (696) (5,956) (980) (1,119) (1,235) (44,182) (1,125,471) (1,169,653)

Notes Ref 6 6 Refer to Note 12 for restatements

MOVEMENT IN RESERVES STATEMENT FOR THE YEAR ENDED 31 MARCH 2012

Page 15 of 162

General Fund

Balance

Earmarked General

Fund Reserves

Housing Revenue Account

Earmarked HRA

Reserves

Capital Receipts Reserve

Capital Fund

Repairs and

Renewals Fund

Insurance Fund

Capital Grants

Unapplied Account

Total Usable

Reserves

Total Unusable Reserves

Total Council

Reserves Notes Ref

£'000 £'000 £'000 £'000 £'000 £'000 £'000 £'000 £'000 £'000 £'000 £'000

Balance at 31 March 2011

(17,404)

(11,759)

(2,000) (3,033)

(696) (5,956) (980) (1,119)

(1,235) (44,182) (1,125,471)

(1,169,653)

Movement in Reserves During 2011/12

(Surplus) or Deficit on the Provision of Services (16,777) - 42,908 - - - - - - 26,131 - 26,131

Other Comprehensive Income and Expenditure - - - - - - - - - - (115,773) (115,773)

Total Comprehensive Income and Expenditure (16,777) - 42,908 - - - - - - 26,131 (115,773) (89,642)

Adjustments Between Accounting Basis & Funding Basis Under Regulations (11,392) - (38,042) - - - - - 283 (49,151) 49,151 - 5

Net (Increase) Decrease before Transfers to Earmarked Reserves (28,169) - 4,866 - - - - - 283 (23,020) (66,622) (89,642

Transfers to/from Earmarked Reserves 17,710 (7,836) (4,866) 3,033 4 (4,847) (3,067) (131) - - - -

(Increase) Decrease in 2011/12 (10,459) (7,836) - 3,033 4 (4,847) (3,067) (131) 283 (23,020) (66,622) (89,642)

Balance at 31 March 2012 Carried Forward (27,863) (19,595) (2,000) - (692) (10,803) (4,047) (1,250) (952) (67,202) (1,192,093) (1,259,295)

Notes Ref 6 6

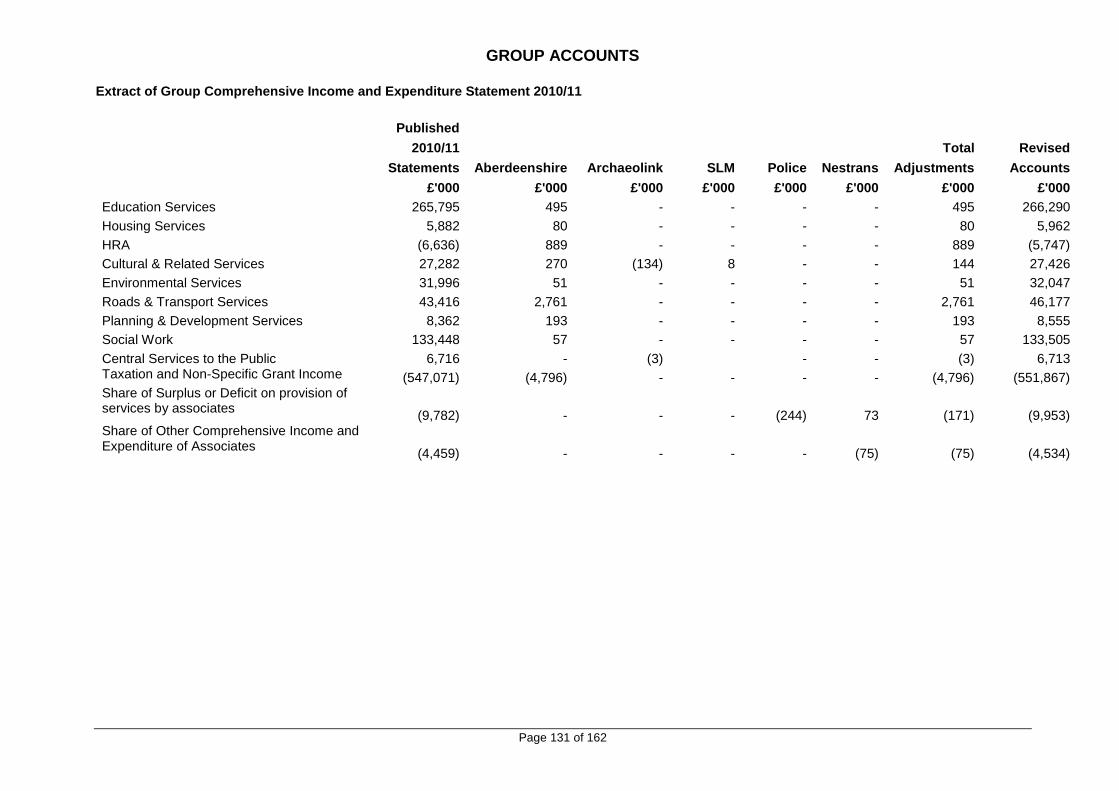

COMPREHENSIVE INCOME AND EXPENDITURE STATEMENT FOR THE YEAR ENDED 31 MARCH 2012

Page 16 of 162

Restated Restated

Gross Restated Net Gross Net

Expenditure Income Expenditure Expenditure Income Expenditure Notes

2010/11 2010/11 2010/11 Aberdeenshire Services 2011/12 2011/12 2011/12 Ref

£'000 £'000 £'000 £'000 £'000 £'000

293,312 (26,995) 266,317 Education Services 256,605 (3,730) 252,875

45,651 (39,689) 5,962 Housing Services 47,113 (40,802) 6,311

37,214 (42,953) (5,739) HRA 86,309 (46,061) 40,248

42,235 (14,848) 27,387 Cultural & Related Services 32,777 (10,331) 22,446

38,661 (6,614) 32,047 Environmental Services 35,447 (7,243) 28,204

70,704 (24,527) 46,177 Roads & Transport Services 37,088 (1,118) 35,970

18,779 (10,224) 8,555 Planning & Development Services 18,901 (11,155) 7,746

159,480 (25,970) 133,510 Social Work 151,471 (26,335) 125,136

27,589 (20,876) 6,713 Central Services 30,020 (24,737) 5,283

8,827 - 8,827 Fire Services 7,969 - 7,969

17,814 (1,042) 16,772 Police Services 16,111 - 16,111

2,860 - 2,860 Exceptional Items - (48) (48) 12

9,958 (46) 9,912 Corporate & Democratic Core 9,103 (61) 9,042

1,613 (62,332) (60,719) Non Distributed Costs 3,340 - 3,340

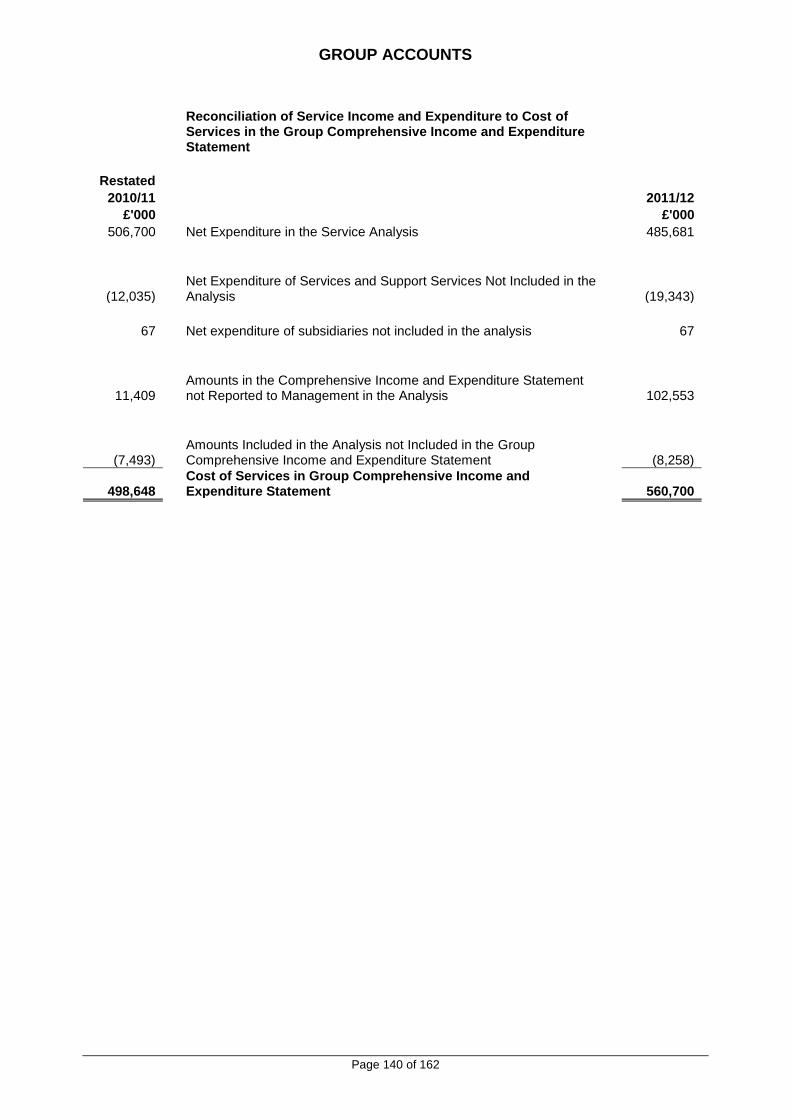

774,697 (276,116) 498,581 COST OF SERVICES 732,254 (171,621) 560,633 7

41,492 (42,031) (539) Other Operating Expenditure 39,487 (39,799) (312) 8

31,166 (1,792) 29,374 Financing and Investment Income and Expenditure 26,970 (809) 26,161 9

- (551,867) (551,867) Taxation and Non-Specific Grant Income - (560,351) (560,351) 10

(24,451) (Surplus) or Deficit on Provision of Services 26,131

(43,372) Surplus on revaluation of non current assets (134,903)

11,785 Actuarial losses on pension assets/liabilities 19,130

(31,587) Other Comprehensive Income and Expenditure (115,773)

(56,038) Total Comprehensive Income and Expenditure (89,642)

Other Notes to the Comprehensive Income and Expenditure Statement 11, 13 - 20

BALANCE SHEET AS AT 31 MARCH 2012

Page 17 of 162

Restated 1 April

2010

Restated 31 March

2011

31 March

2012

Notes

Ref

£’000 £’000 £’000

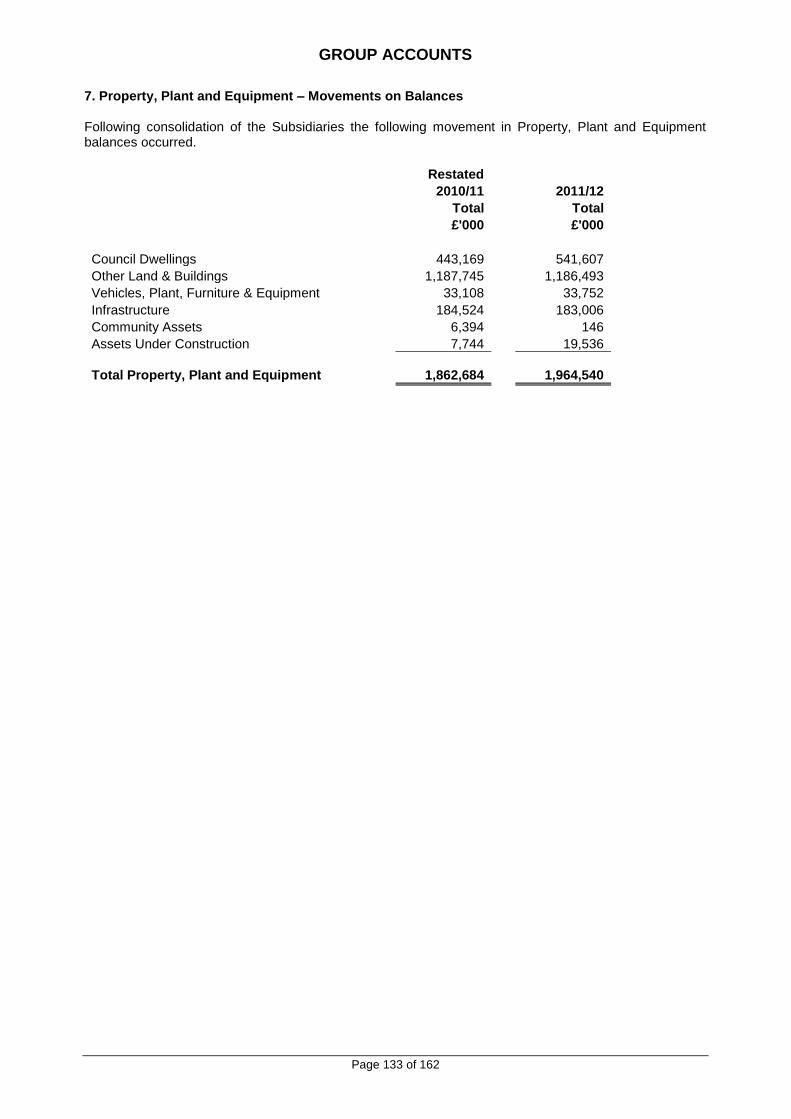

1,832,702 1,861,878 Property, Plant & Equipment 1,963,347 22

1,220 1,320 Heritage Assets 1,320 23-26

1,062 1,669 Investment Property 1,490 27

2,690 2,031 Intangible Assets 1,656 28

6,630 2,782 Long Term Debtors 16,163 36

1,844,304 1,869,680 Long Term Assets 1,983,976

- - Short Term Investments 2,000 33

1,256 3,086 Assets Held for Sale 2,011 29

3,766 3,921 Inventories 4,118 35

29,316 31,900 Short Term Debtors 36,009 36

14,765 25,367 Cash and Cash Equivalents 54,335 37

49,103 64,274 Current Assets 98,473

(5,610) (26,820) Short Term Borrowing (24,068) 33

(77,399) (78,699) Short Term Creditors (72,303) 38

(319) (5,128) Provisions (3,906) 39

(83,328) (110,647) Current Liabilities (100,277)

(3,540) (3,134) Provisions (5,254) 39

(351,522) (357,068) Long Term Borrowing (400,398) 33

(329,082) (281,401) Other Long Term Liabilities (304,391) 38

(12,320) (12,051) Capital Grants Receipts in Advance (12,834) 40

(696,464) (653,654) Long Term Liabilities (722,877)

1,113,615 1,169,653 Net Assets 1,259,295

(47,563) (44,182) Usable Reserves (67,202) 41

(1,066,052) (1,125,471) Unusable Reserves (1,192,093) 42

(1,113,615) (1,169,653) Total Reserves (1,259,295)

Other Notes to the Balance Sheet 1 - 4, 21, 30 - 34, 43 - 48

Alan Wood, MA (Hons) CPFA Head of Finance

18 June 2012

The unaudited accounts were issued on 18 June 2012 and the audited accounts were authorised for issue on 19 September 2012.

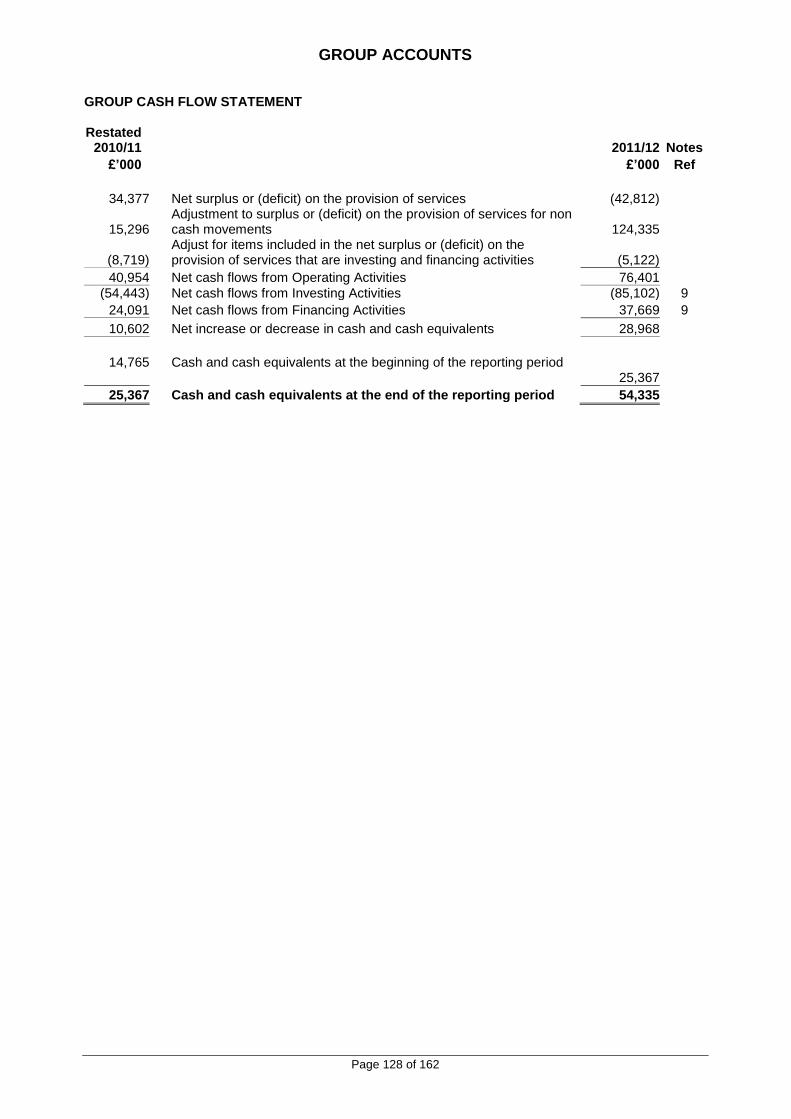

CASH FLOW STATEMENT FOR THE YEAR ENDED 31 MARCH 2012

Page 18 of 162

Restated 2010/11 2011/12

Notes Ref

£’000 £’000

24,451 Net surplus or (deficit) on the provision of services (26,131)

25,225 Adjust net surplus or deficit on the provision of services for non cash movements 107,668

(8,697) Adjust for items included in the net surplus or deficit on the provision of services that are investing and financing activities (5,122)

40,979 Net cash flows from Operating Activities 76,415 49 (54,465) Investing Activities (85,102) 50

24,088 Financing Activities 37,655 51

10,602 Net increase or decrease in cash and cash equivalents 28,968

14,765 Cash and cash equivalents at the beginning of the reporting period 25,367

25,367 Cash and cash equivalents at the end of the reporting period 54,335 37

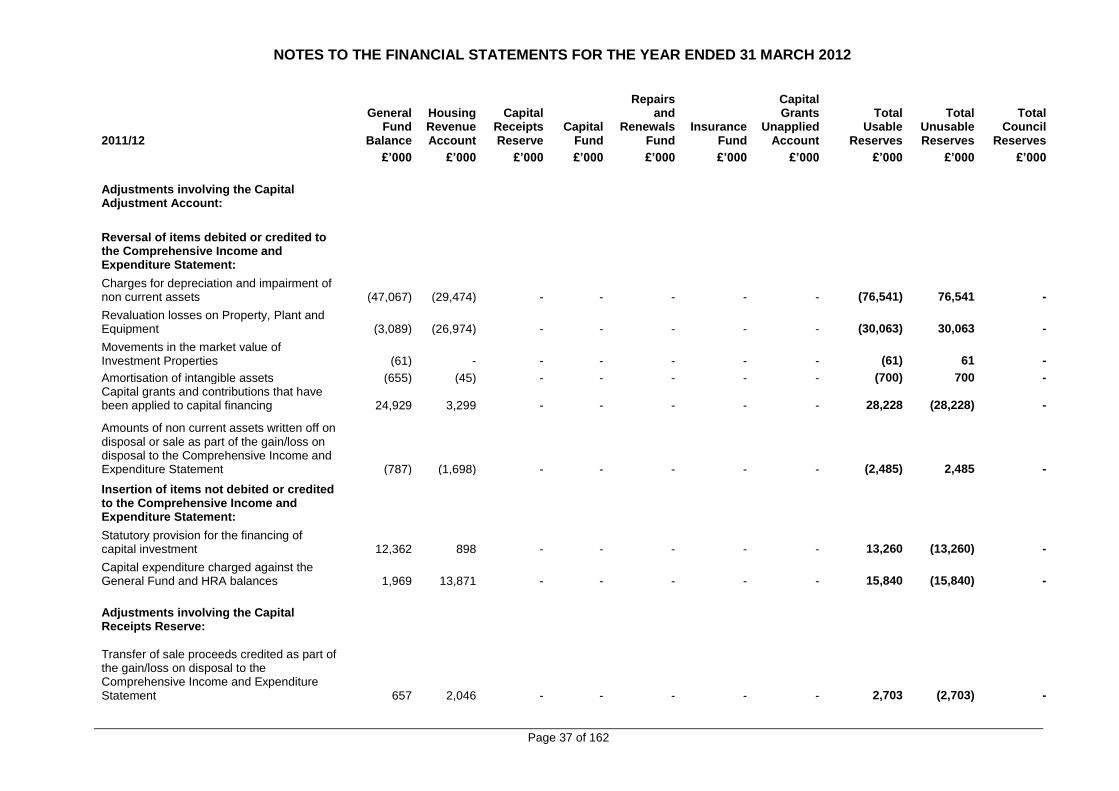

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 MARCH 2012

Page 19 of 162

1. Accounting Policies 1.1 General Principles The Statement of Accounts summarises the Council’s transactions for the 2011/12 financial year and its position at the year end of 31 March 2012. The Council is required to prepare an annual Statement of Accounts by the Local Authority Accounts (Scotland) Regulations 1985, which section 12 of the Local Government in Scotland Act 2003 requires to be prepared in accordance with proper accounting practices. These practices primarily comprise the Code of Practice on Local Authority Accounting in the United Kingdom 2011/12 and the 2011/12 Code Update and the Service Reporting Code of Practice 2011/12, supported by International Financial Reporting Standards (IFRS) and statutory guidance issued under section 12 of the 2003 Act. The accounting convention adopted in the Statement of Accounts is principally historical cost, modified by the revaluation of certain categories of non-current assets and financial instruments. 1.2 Accruals of Income and Expenditure Activity is accounted for in the year that it takes place, not simply when cash payments are made or received. In particular:

revenue from the sale of goods is recognised when the Council transfers the significant risks and rewards of ownership to the purchaser and it is probable that economic benefits or service potential associated with the transaction will flow to the Council;

revenue from the provision of services is recognised when the Council can measure reliably the percentage of completion of the transaction and it is probable that economic benefits or service potential associated with the transaction will flow to the Council;

supplies are recorded as expenditure when they are consumed – where there is a gap between the date supplies are received and their consumption, they are carried as inventories on the Balance Sheet;

expenses in relation to services received (including services provided by employees) are recorded as expenditure when the services are received rather than when payments are made;

interest payable on borrowings and receivable on investments is accounted for on the basis of the effective interest rate for the relevant financial instrument rather than the cash flows fixed or determined by the contract; and

where revenue and expenditure have been recognised but cash has not been received or paid, a debtor or creditor for the relevant amount is recorded in the Balance Sheet. Where there is evidence that debts are unlikely to be settled, the balance of debtors is written down and a charge made to revenue for the income that might not be collected.

1.3 Cash and Cash Equivalents Cash is represented by cash in hand and deposits with financial institutions repayable without penalty on notice of not more than 24 hours. Cash equivalents are investments that mature in three months or less and that are readily convertible to known amounts of cash with insignificant risk of change in value. In the Balance Sheet and Cash Flow Statement, cash and cash equivalents are shown net of bank overdrafts that are repayable on demand and form an integral part of the Council’s cash management. 1.4 Charges to Revenue for Non-Current Assets Services, support services and trading accounts are debited with the following amounts to record the cost of holding non-current assets during the year:

depreciation attributable to the assets used by the relevant service;

revaluation and impairment losses on assets used by the service where there are no accumulated gains in the Revaluation Reserve against which the losses can be written off; and

amortisation of intangible assets attributable to the service. The Council is not required to raise council tax to cover depreciation, impairment losses, revaluation losses or amortisation. However, it is required to make an annual contribution from revenue towards the reduction in its overall borrowing requirement equal to loans fund principal repayments. Depreciation,

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 MARCH 2012

Page 20 of 162

impairment losses, revaluation losses and amortisations are therefore substituted by a funding contribution in the General Fund Balance, by way of an adjusting transaction with the Capital Adjustment Account in the Movement in Reserves Statement for the difference between the two. 1.5 Employee Benefits (i) Benefits Payable During Employment Short-term employee benefits are those due to be settled within twelve months of the year end. They include such benefits as wages and salaries, paid annual leave and paid sick leave, bonuses and non-monetary benefits for current employees, and are recognised as an expense in the year in which employees render service to the Council. An accrual is made for the cost of holiday entitlements and flexi time earned by employees but not taken before the year end and which employees can carry forward into the next financial year. The accrual is made at the wage and salary rates applicable in the following accounting year, being the period in which the employee takes the benefit. The accrual is charged to the Surplus or Deficit on the Provision of Services, but then reversed out through the Movement in Reserves Statement so that holiday benefits are charges to revenue in the financial year in which the holiday absence occurs. (ii) Termination Benefits Termination benefits are amounts payable as a result of a decision by the Council to terminate an officer’s employment before the normal retirement date or an officer’s decision to accept voluntary redundancy and are charged on an accruals basis to the relevant service line in the Comprehensive Income and Expenditure Statement when the Council is demonstrably committed to either terminating the employment of an officer or group of officers or making an offer to encourage voluntary redundancy. Where termination benefits involve the enhancement of pensions, statutory provisions require the General Fund balance to be charged with the amount payable by the Council to the pension fund or pensioner in the year, not the amount calculated according to the relevant accounting standards. In the Movement in Reserves Statement, appropriations are required to and from the Pensions Reserve to remove the notional debits and credits for pension enhancement termination benefits and replace them with debits for the cash paid to the pension fund and pensioners and any such amounts payable but unpaid at the year end. (iii) Post Employment Benefits Employees of the Council are members of one of two separate pension schemes:

The Scottish Teachers’ Pension Scheme, administered by the Scottish Government; and

The Local Government Pension Scheme The North East Scotland Pension Fund, administered by Aberdeen City Council.

Both schemes provide defined benefits to members (retirement lump sums and pensions), earned as employees worked for the Council. However, the arrangements for the teachers’ scheme mean that liabilities for these benefits cannot be identified specifically to the Council. The scheme is therefore accounted for as if it were a defined contributions scheme – no liability for future payments of benefits is recognised in the Balance Sheet and the Education Service line in the Comprehensive Income and Expenditure Statement is charged with the employer’s contributions payable to Teachers’ Pensions in the year. (iv) The Local Government Pension Scheme The Local Government Scheme is accounted for as a defined benefits scheme:

the liabilities of the North East Scotland Pension Fund attributable to the Council are included in the Balance Sheet on an actuarial basis using the projected unit method i.e. an assessment of the future payments that will be made in relation to retirement benefits earned to date by employees, based on assumptions about mortality rates, employee turnover rates, etc, and projections of projected earnings for current employees;

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 MARCH 2012

Page 21 of 162

liabilities are discounted to their value at current prices, using a discount rate of 4.9% (based on a weighted average of “spot yields” on AA rated corporate bonds);

the assets of the North East Scotland Pension Fund attributable to the Council are included in the Balance Sheet at their fair value: - quoted securities – current bid price; - unquoted securities – professional estimate; - unitised securities – current bid price; and - property – market value; and

The change in the net pensions liability is analysed into seven components: - current service cost – the increase in liabilities as a result of years of service earned this year

– allocated in the Comprehensive Income and Expenditure Statement to the services for which the employees worked;

- past service cost – the increase in liabilities arising from current year decisions whose effect relates to years of service earned in earlier years – debited to the Surplus/Deficit on the Provision of Services in the Comprehensive Income and Expenditure Statement as part of Non Distributed Costs;

- interest cost – the expected increase in the present value of liabilities during the year as they move one year closer to being paid – debited to the Finance and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement;

- expected return on assets – the annual investment return on the fund assets attributable to the Council, based on an average of the expected long term return – credited to the Finance and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement;

- gains/losses on settlements and curtailments – the result of actions to relieve the Council of liabilities or events that reduce the expected future service or accrual of benefits of employees – debited/credited to the Surplus/Deficit on the Provision of Services in the Comprehensive Income and Expenditure Statement as part of Non Distributed Costs;

- actuarial gains and losses – changes in the net pensions liability that arise because events have not coincided with assumptions made at the last actuarial valuation or because the actuaries have updated their assumptions – debited to the Pensions Reserve; and

- contributions paid to the North East Scotland Pension Fund – cash paid as employer’s contributions to the pension fund in settlement of liabilities; not accounted for as an expense.

In relation to retirement benefits, statutory provisions require the General Fund balance to be charged with the amount payable by the Council to the Pension Fund or directly to pensioners in the year, not the amount calculated according to the relevant accounting standards. In the Movement in Reserves Statement, this means that there are appropriations to and from the Pensions Reserve to remove the notional debits and credits for retirement benefits and replace them with debits for the cash paid to the pension fund and pensioners and any such amounts payable but unpaid at the year end. The negative balance that arises on the Pensions Reserve thereby measures the beneficial impact to the General Fund of being required to account for retirement benefits on the basis of cash flows rather than as benefits are earned by employees. (v) Discretionary Benefits The Council also has restricted powers to make discretionary awards of retirement benefits in the event of early retirements. Any liabilities estimated to arise as a result of an award to any member of staff (including teachers) are accrued in the year of the decision to make the award and accounted for using the same policies as are applied to the Local Government Pension Scheme. 1.6 Events after the Balance Sheet Date Events after the Balance Sheet date are those events, both favourable and unfavourable, that occur between the end of the reporting period and the date when the Statement of Accounts is authorised for issue. Two types of events can be identified:

those that provide evidence of conditions that existed at the end of the reporting period – the Statement of Accounts is adjusted to reflect such events; and

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 MARCH 2012

Page 22 of 162

those that are indicative of conditions that arose after the reporting period – the Statement of Accounts is not adjusted to reflect such events, but where a category of events would have a material effect disclosure is made in the notes of the nature of the events and their estimated financial effect.

Events taking place after the date of authorisation for issue are not reflected in the Statement of Accounts. 1.7 Exceptional Items When items of income and expense are material, their nature and amount is disclosed separately, either on the face of the Comprehensive Income and Expenditure Statement or in the notes to the accounts, depending on how significant the items are to an understanding of the Council’s financial performance. 1.8 Financial Liabilities Financial liabilities are recognised on the Balance Sheet when the Council becomes a party to the contractual provisions of a financial instrument and initially measured at fair value and carried at their amortised cost subsequently. Annual charges to the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement for interest payable are based on the carrying amount of the liability, multiplied by the effective rate of interest for the instrument. The effective interest rate is the rate that exactly discounts estimated future cash payments over the life of the instrument to the amount at which it was originally recognised. For most of the borrowings that the Council has, this means that the amount presented in the Balance Sheet is the outstanding principal repayable (plus accrued interest reflected in Creditors) and interest charged to the Comprehensive Income and Expenditure Statement is the amount payable for the year according to the loan agreement. Gains and losses on the repurchase or early settlement of borrowing are credited and debited to the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement in the year of repurchase/settlement. However, where repurchase has taken place as part of a restructuring of the loan portfolio that involves the modification or exchange of existing instruments, the premium or discount is respectively deducted from or added to the amortised cost of the new or modified loan and the write-down to the Comprehensive Income and Expenditure Statement is spread over the life of the loan by an adjustment to the effective interest rate. Where premiums and discounts have been charged to the Comprehensive Income and Expenditure Statement, regulations allow the impact on the General Fund Balance to be spread over future years. The Council has a policy of spreading the gain/loss over the term that was remaining on the loan against which the premium was payable or discount receivable when it was repaid. The reconciliation of amounts charged to the Comprehensive Income and Expenditure Statement to the net charge required against the General Fund Balance is managed by a transfer to or from the Financial Instruments Adjustment Account in the Movement in Reserves Statement. 1.9 Financial Assets Financial assets are classified into two types:

loans and receivables – assets that have fixed or determinable payments but are not quoted in an active market; and

available-for-sale assets – assets that have a quoted market price and/or do not have fixed or determinable payments.

(i) Loans and Receivables Loans and receivables are recognised on the Balance Sheet when the Council becomes a party to the contractual provisions of a financial instrument and are initially measured at fair value. They are measured subsequently at their amortised cost. Annual credits to the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement for interest receivable are

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 MARCH 2012

Page 23 of 162

based on the carrying amount of the asset multiplied by the effective rate of interest for the instrument. For most of the loans that the Council has made, this means that the amount presented in the Balance Sheet is the outstanding principal receivable (plus accrued interest reflected in Debtors) and interest credited to the Comprehensive Income and Expenditure Statement is the amount receivable for the year in the loan agreement. However, the Council has made a number of loans to small businesses and other organisations at less than market rates (soft loans). When soft loans are made, a loss is recorded in the Comprehensive Income and Expenditure Statement (debited to the appropriate service) for the present value of the interest that will be foregone over the life of the instrument, resulting in a lower amortised cost than the outstanding principal. Interest is credited to the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement at a marginally higher effective rate of interest than the rate receivable from the small businesses and other organisations, with the difference serving to increase the amortised cost of the loan in the Balance Sheet. Statutory provisions require that the impact of soft loans on the General Fund Balance is the interest receivable for the financial year – the reconciliation of amounts debited and credited to the Comprehensive Income and Expenditure Statement to the net gain required against the General Fund Balance is managed by a transfer to or from the Financial Instruments Adjustment Account in the Movement in Reserves Statement. Where assets are identified as impaired because of a likelihood arising from a past event that payments due under the contract will not be made, the asset is written down and a charge made to the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement. The impairment loss is measured as the difference between the carrying amount and the present value of the revised future cash flows discounted at the asset’s original effective interest rate. Any gains and losses that arise on the derecognition of an asset are credited/debited to the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement. (ii) Available-for-Sale Assets Available-for-sale assets are recognised on the Balance Sheet when the Council becomes a party to the contractual provisions of a financial instrument and are initially measured and carried at fair value. Where the asset has fixed or determinable payments, annual credits to the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement for interest receivable are based on the amortised cost of the asset multiplied by the effective rate of interest for the instrument. Where there are no fixed or determinable payments, income (e.g. dividends) is credited to the Comprehensive Income and Expenditure Statement when it becomes receivable by the Council. Assets are maintained in the Balance Sheet at fair value. Values are based on the following principles:

instruments with quoted market prices – the market price;

other instruments with fixed and determinable payments – discounted cash flow analysis; and

equity shares with no quoted market prices – independent appraisal of company valuations. Changes in fair value are balanced by an entry in the Available-for-Sale Reserve and the gain/loss is recognised in the Surplus/Deficit on Revaluation of Available-for-Sale Financial Assets. The exception is where impairment losses have been incurred – these are debited to the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement, along with any net gain/loss for the asset accumulated in the Reserve. Where financial assets are identified as impaired because of a likelihood arising from a past event that payments due under the contract will not be made (fixed or determinable payments) or fair value falls below cost, the asset is written down and a charge made to the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement. If the asset has fixed or determinable payments, the impairment loss is measured as the difference between the carrying amount and the present value of the revised future cash flows discounted at the asset’s original effective interest rate. Otherwise, the impairment loss is measured as any shortfall of fair value against the acquisition cost of the instrument (net of any principal repayment and amortisation).

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 MARCH 2012

Page 24 of 162

Any gains and losses that arise on the derecognition of the asset are credited/debited to the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement, along with any accumulated gains/losses previously recognised in the Available-for Sale Reserve. Where fair value cannot be measured reliably, the instrument is carried at cost (less any impairment losses). (iii) Instruments Entered Into Before 1 April 2006 The Council entered into a number of financial guarantees that are not required to be accounted for as financial instruments. These guarantees are reflected in the Statement of Accounts to the extent that provisions might be required or a contingent liability note is needed under the policies set out in the section on Provisions, Contingent Liabilities and Contingent Assets. 1.10 Foreign Currency Translation Where the Council has entered into a transaction denominated in a foreign currency, the transaction is converted into sterling at the exchange rate applicable on the date on which the transaction was effective. Where amounts in foreign currency are outstanding at the year end, they are reconverted at the spot exchange rate at 31 March. Resulting gains or losses are recognised in the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement. 1.11 Government Grants and Contributions Whether paid on account, by instalments or in arrears, government grants and third party contributions and donations are recognised as due to the Council when there is reasonable assurance that:

the Council will comply with the conditions attached to the payments, and;

the grants or contributions will be received. Amounts recognised as due to the Council are not credited to the Comprehensive Income and Expenditure Account until conditions attaching to the grant or contribution have been satisfied. Conditions are stipulations that specify that the future economic benefits or service potential embodied in the asset acquired using the grant or contribution are required to be consumed by the recipient as specified or future economic benefits or service potential must be returned to the transferor. Monies advanced as grants and contributions for which conditions have not been satisfied are carried in the Balance Sheet as creditors. When conditions are satisfied, the grant or contribution is credited to the relevant service line (attributable revenue grants/contributions) or Taxation and Non-Specific Grant Income (non-ring-fenced revenue grants and all capital grants) in the Comprehensive Income and Expenditure Statement. Where capital grants are credited to the Comprehensive Income and Expenditure Statement, they are reversed out of the General Fund Balance in the Movement in Reserves Statement. Where the grant has yet to be used to finance capital expenditure, it is posted to the Capital Grants Unapplied Account. Where it has been applied, it is posted to the Capital Adjustment Account. Amounts in the Capital Grants Unapplied Account are transferred to the Capital Adjustment Account once they have been applied to fund capital expenditure. 1.12 Heritage Assets Tangible and Intangible Heritage Assets (described in this summary of significant accounting policies as heritage assets) Aberdeenshire Council’s Museum Service’s collections relate to the natural and man-made history of Aberdeenshire. There are three distinct collections: Fine & Applied Art, Natural Sciences, and Human History. These are held in support of the Museum Service’s primary objective which is “To collect, research, conserve, interpret and make accessible to all people living in Aberdeenshire the museum collection belonging to Aberdeenshire Council”. The vast majority of the objects held were acquired in the 19th century and the first half of the 20th century.

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 MARCH 2012

Page 25 of 162

Aberdeenshire Council’s Archaeology Service’s collections and heritage assets either relate directly to the everyday activities of protecting and managing all known elements of the historic environment within Aberdeenshire Council (it also provides a similar service to Moray and Angus Councils) or are physical items that have been allocated to it under the Council’s Asset Management Plan. There are four distinct collections: the Aikey Brae Stone Circle at Mintlaw, the Rhynie Man, Vertical Aerial Photograph Collection and a Photograph and Slide collection. In the opinion of the Council, reliable information on cost or valuation is not available for the majority of these collections. This is owing to the lack of information on purchase cost, the lack of comparable market values, the diverse nature of the objects and the volume of items held. The Council has applied a de minimus of £100,000 for reporting Heritage Assets on the Balance Sheet. These collections are therefore not reported as assets in the Balance Sheet, with the exception of the Vertical Aerial Photograph Collection, for which a replacement cost is available. The Council has a historic valuation (1978) for part of the Fine Art collection, and three further paintings were valued in 2011. Five archaeological items, including the Deskford Carnyx regarded as of national importance, on loan to National Museums Scotland were valued by them in 2011 at current sale room prices. The Council’s collections are accounted for as follows: Fine & Applied Art That part of the Fine Art collection which was valued in 1978 is valued at the 1978 historical value (£9,000); the three paintings valued in 2011 by National Galleries of Scotland were deemed to have a total value of £20,000. These item are not reported on the Balance Sheet as they are below the Council’s de minimus threshold. Acquisitions are made by purchase or donation. Purchases are recorded at cost. Natural Sciences, Human History, Aikey Brae Stone Circle and Rhynie Man The Council does not consider that reliable cost or valuation information can be obtained for the vast majority of items held in the collections of Natural Sciences, Human History, the Aikey Brae Stone Circle or the Rhynie Man. This is because of the diverse nature of the items held, the number of items held and the lack of comparable market values. Therefore, the Council does not recognise these assets on its Balance Sheet. A small number of archaeological items on loan to National Museums Scotland have been valued by them in 2011. One item, the Deskford Carnyx, has been valued at £750,000 in view of its national importance, and is shown on the Balance Sheet. The other four items have been valued at a total of £100,000, and are not shown on the Balance Sheet. In addition, Hareshowe Farm, Aden Country Park is valued at £250,000 and is shown on the Balance Sheet. The valuation basis is fair value. Vertical Aerial Photograph Collection and Photograph and Slide Collection The Vertical Aerial Photograph Collection has been valued at £320,000, which is the estimated cost of replacing the collection, and is shown in the Balance Sheet. The Photograph and Slide Collection is valued at £14,000 and is not shown on the Balance Sheet. Preservation costs Expenditure which, in the Council’s view, is required to preserve or clearly prevent further deterioration of individual collection items is recognised in the Comprehensive Income and Expenditure Statement when it is incurred. Further information on the collections is given in Notes 23 to 26 to the accounts.

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 MARCH 2012

Page 26 of 162

General Heritage assets are deemed to have indeterminate lives and a high residual value; hence the Council does not consider it appropriate to charge depreciation. The carrying amounts of heritage assets are reviewed where there is evidence of impairment for heritage assets, e.g. where an item has suffered physical deterioration or breakage or where doubts arise as to its authenticity. Any impairment is recognised and measured in accordance with the Council’s general policies on impairment – see note 1.21 (iii) on page 31. The Council will occasionally dispose of heritage assets where an item which is too badly damaged or deteriorated to be of any further use for the purposes of Council, to improve the curatorial care of the collections by the disposal of duplicate or unprovenanced material of low intrinsic relevance to the Acquisition Policy, or to transfer to the ownership of another Accredited museum any item which, by reasons of changes in public, social or educational need, administrative responsibility, development priorities, or the establishment of a new Accredited museum, the Principal Museums & Heritage Officer advises the Council would be more appropriately placed elsewhere. Any money received by the Council as the result of the sale of a museum item must be used for the benefit of the collection. Normally this will mean it is placed in the Aberdeenshire Heritage Artefact Acquisition Fund or Aberdeenshire Farming Museum Purchase Fund, as appropriate, and used for the acquisition of further items but in exceptional cases improvements relating to the care of collections may be justifiable. 1.13 Intangible Assets Expenditure on non-monetary assets that do not have physical substance but are controlled by the Council as a result of past events (e.g. software licences) is capitalised when it is expected that future economic benefits or service potential will flow from the intangible asset to the Council. Internally generated assets are capitalised where it is demonstrable that the project is technically feasible and is intended to be completed (with adequate resources being available) and the Council will be able to generate future economic benefits or deliver service potential by being able to sell or use the asset. Expenditure is capitalised where it can be measured reliably as attributable to the asset and restricted to that incurred during the development phase (research expenditure is not capitalised). Expenditure on the development of websites is not capitalised if the website is solely or primarily intended to promote or advertise the Council’s goods or services. Intangible assets are measured initially at cost. Amounts are not revalued, as the fair value of the assets held by the Council cannot be determined by reference to an active market. The amortisable amount of an intangible asset is amortised over its useful life to the relevant service line(s) in the Comprehensive Income and Expenditure Statement. No amortisation charge is made for an intangible asset in the year of acquisition. Thereafter, the straight line method is applied, based on the opening balance. A full year’s amortisation charge is made in the year of disposal. An asset is tested for impairment whenever there is an indication that the asset might be impaired – any losses recognised are posted to the relevant service line(s) in the Comprehensive Income and Expenditure Statement. Any gain or loss arising on the disposal or abandonment of an intangible asset is posted to the Other Operating Expenditure line in the Comprehensive Income and Expenditure Statement. Where expenditure on intangible assets qualifies as capital expenditure for statutory purposes, amortisation, impairment losses and disposal gains and losses are not permitted to have an impact on the General Fund Balance. The gains and losses are therefore reversed out of the General Fund Balance in the Movement in Reserves Statement and posted to the Capital Adjustment Account and (for sale proceeds) the Capital Receipts Reserve.

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 MARCH 2012

Page 27 of 162