state taxes and spatial misallocation - booth school of...

TRANSCRIPT

State Taxes and Spatial Misallocation

Pablo Fajgelbaum, Eduardo Morales, Juan Carlos Suarez Serrato, Owen Zidar

UCLA, Princeton, Duke, Chicago Booth

February 2016

Motivation

Regional fiscal autonomy varies considerably across countries, e.g.,

I France, Japan, United Kingdom: regional entities do not set tax policyI Canada, Spain, Italy: regions have large tax autonomyI U.S. state tax autonomy is similar to the later group

What are the aggregate consequences of regional di↵erences in taxes?

I Misallocation logic suggests potentially negative e↵ects

F Restuccia and Rogerson (2008); Hsieh and Klenow (2009)

I This paper: quantify the aggregate e↵ects of dispersion in tax rates

across U.S. states

Background on the U.S. State Tax System

3 Major Sources of Tax Revenue used by the States (4% of U.S. GDP)

I Sales tax (47% of total state tax revenue in 2012) more

I Personal income tax (35%) more

I Corporate income tax (5%) more

State tax rates are heterogeneous

I 90-10 percentiles of state tax-rate distributions: rates revenue

F 7%-1.4% (sales)F 9.2%-0% (personal income)F 4.6%-0% (corporate)

Changes in state tax revenue are strongly correlated with changes in directexpenditures

I E.g., education, public welfare, hospitals, highways, police, natural resources,parks and recreation.

This Paper

1 Quantitative Geography Model with U.S. State Tax System

I States with heterogeneous fundamentals

F productivity, amenities, trade costs, factor shares, fixed factors,ownership rates

I Workers and firms sort across states according to idiosyncratic draws

I Firms are monopolistically competitive

I 3 major state taxes and federal transfers

F finance state spending which may be valued by workers and firms

2 Estimation

I Elasticities of worker and firm location with respect to taxes

F data on economic activity and 350 state tax changes over 1980-2010

I Fundamentals

F match distribution of employment, wages, and trade in 2007

3 Main Counterfactual

I Movement to harmonized state tax system keeping government spendingconstant through inter-state transfers

Literature

Misallocation

I Across firms: Restuccia and Rogerson (2008), Hsieh and Klenow (2009)I Across cities: Brandt et al. (2013), Desmet and Rossi-Hansberg (2013), Moretti

and Hsieh (2015)I Rural-Urban gaps: Gollin et al. (2013), Lagakos and Waugh (2013), Bryan and

Morten (2015)

Trade/Economic Geography

I Spatial equilibrium models: Roback (1982), Krugman (1991), Krugman andVenables (1995), Helpman (1998), Tabuchi and Thisse (2002)

I Quantitative geography model: Allen and Arkolakis (2014), Caliendo et al. (2014),Ramondo et al. (2015), Redding (2015), Gaubert (2015)

Public Finance/Urban

I Fiscal competition: Flatters et al. (1973), Gordon (1983), Oates (1999), Keen andKonrad (2013), Ossa (2015)

I Factor Mobility and Policy Changes: Bartik (1991), Holmes (1998), Moretti andWilson (2014), Suarez Serrato and Zidar (2015)

I General Equilibrium: Shoven et al. (1972), Ballard et al. (1985), Altig et al.(2001), Albouy (2009)

Model

Worker Utility and Location

Fraction of workers who choose region n :

Ln =⇣vnv

⌘"W

State-specific “appeal”:

vn = un

✓

Gn

L�Wn

◆↵W ,n✓

(1� Tn)wn

Pn

◆1�↵W ,n

where

1� Tn ⌘ (1� tyn ) (1� tyfed)� twfed1 + tcn

Representative worker’s utility:

v ⌘

X

n

v"Wn

!1/"W

Firms Profits and Location

Fraction of firms who choose region n:

Mn =

⇡n

�

z1n�

⇡

!

"F��1

where z1n = z1�↵F,nn

⇣

Gn

M�Fn

⌘↵F,n

Profits of firm with productivity z located in i :

⇡i (z) = max (1� t i )

NX

n=1

xni �NX

n=1

⌧niciz

qni

!

where t i = tcorpfed + t li +PN

n=1 txn sni

I Dispersion in sales apportionment leads to price distortion more

Immobile capital owners in state n own a fraction bn of a portfolio that includes allfirms and fixed factors

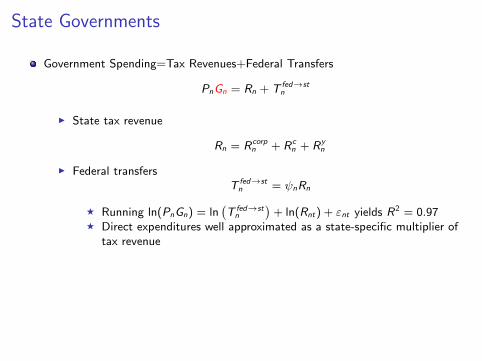

State Governments

Government Spending=Tax Revenues+Federal Transfers

PnGn = Rn + T fed!stn

I State tax revenue

Rn = Rcorpn + Rc

n + Ryn

I Federal transfersT fed!st

n = nRn

F Running ln(PnGn) = ln�

T fed!stn

�

+ ln(Rnt) + "nt yields R2 = 0.97F Direct expenditures well approximated as a state-specific multiplier of

tax revenue

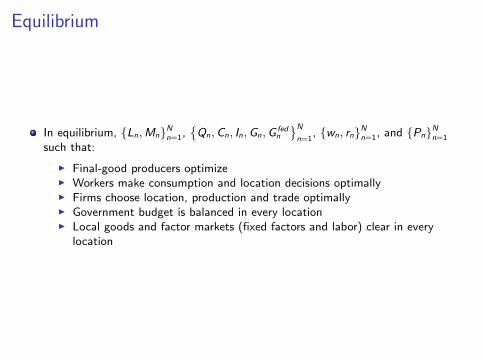

Equilibrium

In equilibrium, {Ln,Mn}Nn=1,�

Qn,Cn, In,Gn,G fedn

N

n=1, {wn, rn}Nn=1, and {Pn}Nn=1

such that:

I Final-good producers optimizeI Workers make consumption and location decisions optimallyI Firms choose location, production and trade optimallyI Government budget is balanced in every locationI Local goods and factor markets (fixed factors and labor) clear in every

location

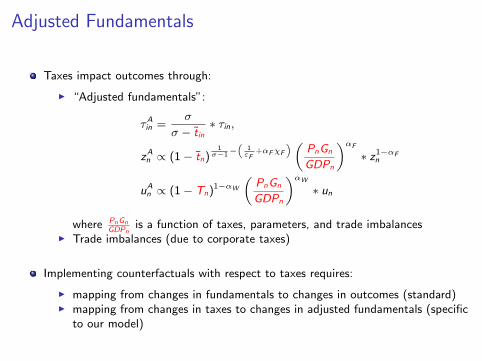

Adjusted Fundamentals

Taxes impact outcomes through:

I “Adjusted fundamentals”:

⌧Ain =�

� � tin⇤ ⌧in,

zAn / (1� tn)1

��1�⇣

1"F

+↵F�F

⌘ ✓PnGn

GDPn

◆↵F

⇤ z1�↵Fn

uAn / (1� Tn)

1�↵W

✓

PnGn

GDPn

◆↵W

⇤ un

where PnGnGDPn

is a function of taxes, parameters, and trade imbalancesI Trade imbalances (due to corporate taxes)

Implementing counterfactuals with respect to taxes requires:

I mapping from changes in fundamentals to changes in outcomes (standard)I mapping from changes in taxes to changes in adjusted fundamentals (specific

to our model)

Impact of Tax Dispersion on Worker Welfare

What is the e↵ect of eliminating dispersion in taxes {Tn} on worker welfare v keeping

{Gn} constant?

I Assume

F no trade frictions (⌧in = 1), perfect substitutes (� = 1), homogeneous firms("F= 1),

F no cross-state dispersion in income shares (�n = �) or in preferences forspending (↵W ,n = ↵W )

I Let Zn /�z0n/�n

�1/�n H�n�unG

↵Wn

�1/(1�↵W )and ⇣ ⌘ 1�↵W

1/"W+↵W�W+(1�↵W )�

Eliminating dispersion in{Tn} while keeping spending constant increases (decreases)

worker welfare if corr⇣Z⇣n , (1� Tn)

⇣⌘

is low (high) enough

Intuition

I Workers gain from dispersion in state-specific appeals, {vn}I State-specific appeal depends on both taxes and fundamentals (through prices)I High correlation between keep rates and fundamentals implies high dispersion

Consider corr⇣Z⇣n , (1� Tn)

⇣⌘= 0. Eliminating dispersion increases welfare if

(1� ↵W ) (1� �) > 1/"W + ↵W

I Holds for ↵W , �, �W large, "W small

Impact of Tax Dispersion on Real Income

Eliminating dispersion in {Tn} while keeping spending constant:

I may increase or decrease aggregate real income depending on the joint distributionof Tn, un, and Gn

I increases it under perfect mobility ("W ! 1), no public goods (↵W = 0), and nodispersion in amenities (un = 0)

F In this case, the model is the same as Hsieh and Klenow (2009)

Intuition

I Real income maximized under no dispersion of MPL.I But labor mobility is a↵ected by compensating di↵erentials,

v = unG↵Wn ((1� Tn)(MPLn))1�↵W

Key Forces

Agglomeration

I Home market e↵ects due to trade costs (final consumption andintermediates): {"W , "F ,�, {�n}}

I Returns to public spending: {↵F ,n,↵W ,n,�F ,�W }

Congestion

I Fixed factor used in production (land and structures): {�n}I Dispersed ownership of fixed factors: {bn}

Heterogeneity in productivity, endowments, amenities, trade costs: {zn,Hn, un, ⌧in}

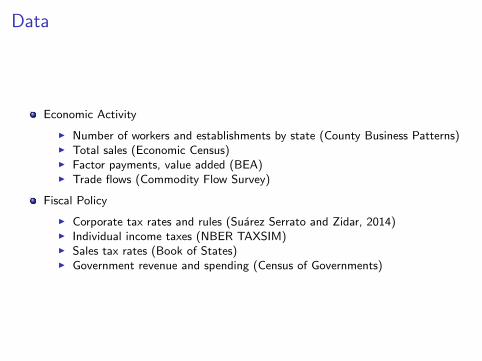

Data and Estimation

Data

Economic Activity

I Number of workers and establishments by state (County Business Patterns)I Total sales (Economic Census)I Factor payments, value added (BEA)I Trade flows (Commodity Flow Survey)

Fiscal Policy

I Corporate tax rates and rules (Suarez Serrato and Zidar, 2014)I Individual income taxes (NBER TAXSIM)I Sales tax rates (Book of States)I Government revenue and spending (Census of Governments)

Estimation Strategy

Elasticities of firm and worker location estimated from data on economic activityand taxes from 1980-2010

I {"W ,↵W ,n} estimated from labor-supply equationI {"F ,↵F} estimated using firm-mobility equation

Fundamentals, technologies, and ownership rates calibrated to (exactly) matchdata in 2007

I {zn,Hn, un, ⌧in} chosen to match spending shares, sales shares, employment,and wages details

I {�n,�n} match input and labor shares details

I {bn} match trade deficits details

Other parameters:

I Demand elasticity: � = 4 (Head et al., 2013)I {�W ,�F} 2 {{0, 0} , {1, 1}} (re-estimate in each case)

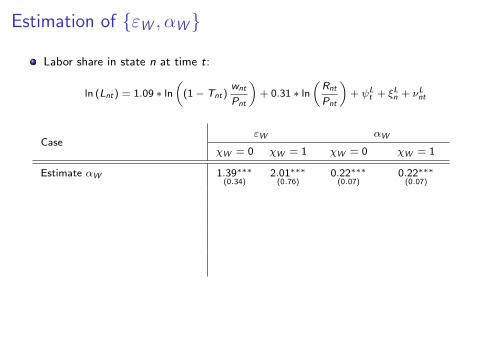

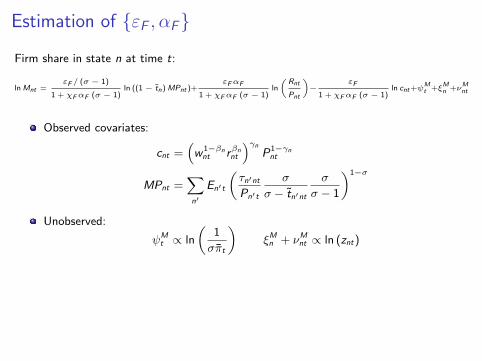

Estimation of {"W ,↵W}

Labor share in state n at time t:

ln (Lnt) ="W

�1� ↵W ,n

�

1 + �W "W↵W ,nln

✓(1� Tnt)

wnt

Pnt

◆+

"W↵W ,n

1 + �W "W↵W ,nln

✓Rnt

Pnt

◆+ L

t +⇠Ln+⌫

Lnt

I Identification assumption:

E[⌫Lnt | L, ⇠L,ZLnt ] = 0

I We use other-state taxes as instruments: ZLnt = (t⇤cnt , t

⇤xnt , t

⇤ynt )

Estimation of {"W ,↵W}

Labor share in state n at time t:

ln (Lnt) = 1.09 ⇤ ln

✓(1� Tnt)

wnt

Pnt

◆+ 0.31 ⇤ ln

✓Rnt

Pnt

◆+ L

t + ⇠Ln + ⌫Lnt

Case"W ↵W

�W = 0 �W = 1 �W = 0 �W = 1

Estimate ↵W 1.39⇤⇤⇤(0.34)

2.01⇤⇤⇤(0.76)

0.22⇤⇤⇤(0.07)

0.22⇤⇤⇤(0.07)

Estimate ↵W ,n = ↵0 + ↵1POLn 1.24 3.08 [0.14, 0.18] [0.16, 0.17]

Assume ↵W = 0 1.04⇤⇤⇤(0.31)

1.04⇤⇤⇤(0.31)

Assume ↵F = 0.05 = 1N

Pn

RnGDPn

1.15⇤⇤⇤(0.32)

1.22⇤⇤⇤(0.36)

Assume ↵W ,n = RnGDPn

1.25⇤⇤⇤(0.36)

1.4⇤⇤⇤(0.49)

Estimation of {"W ,↵W}

Labor share in state n at time t:

ln (Lnt) = 1.09 ⇤ ln

✓(1� Tnt)

wnt

Pnt

◆+ 0.31 ⇤ ln

✓Rnt

Pnt

◆+ L

t + ⇠Ln + ⌫Lnt

Case"W ↵W

�W = 0 �W = 1 �W = 0 �W = 1

Estimate ↵W 1.39⇤⇤⇤(0.34)

2.01⇤⇤⇤(0.76)

0.22⇤⇤⇤(0.07)

0.22⇤⇤⇤(0.07)

Estimate ↵W ,n = ↵0 + ↵1POLn 1.24 1.57 [0.21, 0.22] [0.21, 0.23]

Assume ↵W = 0 0.93⇤⇤⇤(0.28)

0.93⇤⇤⇤(0.28)

Assume ↵F = 0.05 = 1N

Pn

RnGDPn

1.09⇤⇤⇤(0.31)

1.15⇤⇤⇤(0.35)

Assume ↵W ,n = RnGDPn

1.19⇤⇤⇤(0.35)

1.33⇤⇤⇤(0.45)

Estimation of {"F ,↵F}

Firm share in state n at time t:

lnMnt = 0.89 ⇤ ln ((1� tn)MPnt) + 0.14 ⇤ ln

✓Rnt

Pnt

◆� 2.69 ⇤ ln cnt + M

t + ⇠Mn + ⌫Mnt

Case"F ↵F

�F = 0 �F = 1 �F = 0 �F = 1

Estimate ↵F 2.70⇤⇤⇤(0.33)

3.15⇤⇤⇤(0.77)

0.05(0.06)

0.05(0.06)

Assume ↵F = 0 2.70⇤⇤⇤(0.61)

3.12⇤⇤⇤(0.45)

Assume ↵F = 0.05 2.67⇤⇤⇤(0.32)

2.67⇤⇤⇤(0.32)

details

Counterfactuals

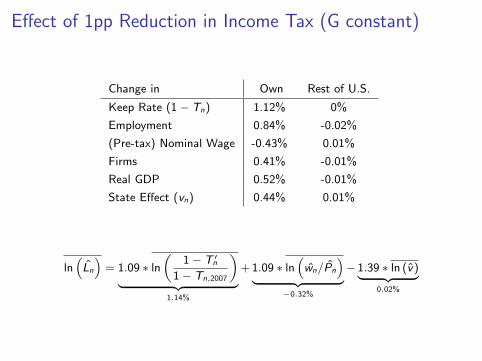

E↵ect of 1pp Reduction in Income Tax (G constant)

Change in Own Rest of U.S.

Keep Rate (1� Tn) 1.12% 0%

Employment 0.84% -0.02%

(Pre-tax) Nominal Wage -0.43% 0.01%

Firms 0.41% -0.01%

Real GDP 0.52% -0.01%

State E↵ect (vn) 0.44% 0.01%

ln⇣

Ln

⌘

= 1.09 ⇤ ln✓

1� T 0n

1� Tn,2007

◆

| {z }

1.14%

+1.09 ⇤ ln⇣

wn/Pn

⌘

| {z }

�0.32%

� 1.39 ⇤ ln (v)| {z }

0.02%

1pp Reduction in California’s Income Tax (G constant)

Figure : Employment Change (% points)

�������−��������������−��������������−��������������−��������������−��������������−�������&$� �����

Implementing Spending-Constant Counterfactuals

Goal: assess the impact of tax dispersion keeping government spending constant

I Replace�

tyn,2007, tcn,2007, t

ln,2007, t

xn,2007

withn

(ty )0 , (tc)0 ,�

t l�0, (0tx)

o

s.t.

⇣

t jn⌘0

= aj + b ⇤ t jn,2007

for n = 1, ..,N, j = y , c, l , x and aj , b � 0. fig.

I Keep government spending {Gn} constant through an inter-state transfersystem. I.e., for each b, find

�

aj

such that

NX

n=1

P 0nGn,2007 =

NX

n=1

R 0n +

⇣

T fed!stn

⌘0

Compute the change in aggregate real income and worker welfare,

bv =

X

n

Ln,2007bv"Wn0

!

1"W

Eliminating Tax Dispersion

Parametrization Constant Spending Variable Spending

↵W ,n ↵F Welfare GDP Welfare GDP

0.22 0.04 0.15% 0.12% 0.98% 0.92%

↵0 + ↵1POLn 0.04 0.15% 0.12% 0.96% 0.93%Rn

GDPn0.04 0.17% 0.12% 0.39% 0.94%

Rn0GDPn0

of random n0 6= n 0.04 0.17% 0.11% 0.38% 0.95%

0.00 0.00 0.20% 0.10% 0.16% 0.10%

0.22 0.00 0.16% 0.10% 0.48% -0.05%

0.00 0.04 0.19% 0.11% 0.44% 0.93%

Eliminating Tax Dispersion

Parametrization Constant Spending Variable Spending

↵W ,n ↵F Welfare GDP Welfare GDP

0.22 0.04 0.15% 0.12% 0.98% 0.92%

↵0 + ↵1POLn 0.04 0.15% 0.12% 0.96% 0.93%Rn

GDPn0.04 0.17% 0.12% 0.39% 0.94%

Rn0GDPn0

of random n0 6= n 0.04 0.17% 0.11% 0.38% 0.95%

0.00 0.00 0.20% 0.10% 0.16% 0.10%

0.22 0.00 0.16% 0.10% 0.48% -0.05%

0.00 0.04 0.19% 0.11% 0.44% 0.93%

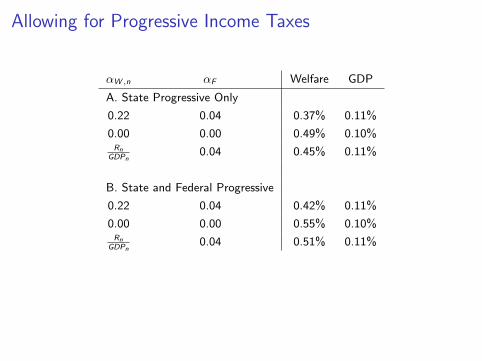

Allowing for Progressive Income Taxes

↵W ,n ↵F Welfare GDP

A. State Progressive Only

0.22 0.04 0.37% 0.11%

0.00 0.00 0.49% 0.10%Rn

GDPn0.04 0.45% 0.11%

B. State and Federal Progressive

0.22 0.04 0.42% 0.11%

0.00 0.00 0.55% 0.10%Rn

GDPn0.04 0.51% 0.11%

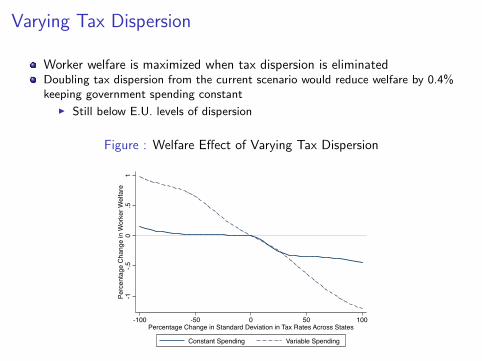

Varying Tax Dispersion

Worker welfare is maximized when tax dispersion is eliminated

Doubling tax dispersion from the current scenario would reduce welfare by 0.4%keeping government spending constant

I Still below E.U. levels of dispersion

Figure : Welfare E↵ect of Varying Tax Dispersion

-1-.5

0.5

1Pe

rcen

tage

Cha

nge

in W

orke

r Wel

fare

-100 -50 0 50 100Percentage Change in Standard Deviation in Tax Rates Across States

Constant Spending Variable Spending

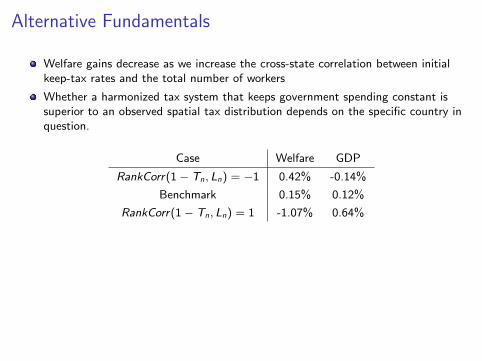

Alternative Fundamentals

Welfare gains decrease as we increase the cross-state correlation between initialkeep-tax rates and the total number of workers

Whether a harmonized tax system that keeps government spending constant issuperior to an observed spatial tax distribution depends on the specific country inquestion.

Case Welfare GDP

RankCorr(1� Tn, Ln) = �1 0.42% -0.14%

Benchmark 0.15% 0.12%

RankCorr(1� Tn, Ln) = 1 -1.07% 0.64%

Conclusion

We study the e↵ects of the state tax distribution on welfare and the distribution ofeconomic activity in the U.S.

I Quantitative economic geography model with U.S. state tax systemI Estimate key parameters using observed variation in taxesI Simulate counterfactual state tax distributions keeping government spending

constant

In the U.S., tax dispersion leads to aggregate worker welfare losses across manyspecifications

I 0.2% worker welfare and 0.1% GDP gain from eliminating spatial dispersionin taxes accounting for 4% of GDP

F Gains increase to 0.45% under progressive income taxes

I Doubling tax dispersion leads to welfare loss of 0.4%

F eliminating tax dispersion maximizes worker welfareF the answers depend on the country in question

Distribution of Tax Rates Across States

0.1

.2.3

.4D

ensi

ty

0 5 10State Tax Rates in 2010

Sales Individual IncomeCorporate Sales Apportioned Corporate

back

Tax Revenue as Share of GDP Across States

90-10 percentiles of the distribution of sales, personal income, and corporate tax revenueshares: 76%-30%, 49%-0%, 8%-0%

0.0

2.0

4.0

6.0

8S

tate

Tax

Rev

enue

as

Sha

re o

f GD

P in

201

0

AK

DE

NH

WY TX SD

CO LA NV

OR

GA

TN VA

OK

MT IL

MO

WA

ND FL AZ

NE

UT

SC AL

OH IA NM

MD

NC PA

KS IN ID NJ

MA RI

CA

KY MI

CT

NY WI

VT

MN

AR

MS

ME

WV HI

Income Sales

Corporate

back

Dispersion in Sales Tax Rates Across States

Sales tax rates:

5 Highest Rates Rate 5 Lowest Rates Rate

California 8.25% Delaware 0%

New Jersey 7% Montana 0%

Mississippi 7% New Hampshire 0%

Tennessee 7% Alaska 0%

Indiana 7% Oregon 0%

Only final consumption is subject to sales taxes

I Firms do not pay sales taxes when buying intermediates

back

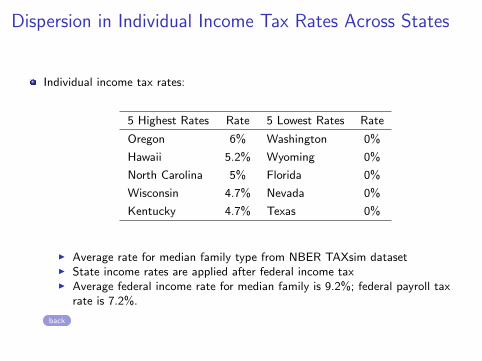

Dispersion in Individual Income Tax Rates Across States

Individual income tax rates:

5 Highest Rates Rate 5 Lowest Rates Rate

Oregon 6% Washington 0%

Hawaii 5.2% Wyoming 0%

North Carolina 5% Florida 0%

Wisconsin 4.7% Nevada 0%

Kentucky 4.7% Texas 0%

I Average rate for median family type from NBER TAXsim datasetI State income rates are applied after federal income taxI Average federal income rate for median family is 9.2%; federal payroll tax

rate is 7.2%.

back

Dispersion in Corporate Tax Rates Across States

Corporate tax rates:

5 Highest Rates Rate 5 Lowest Rates Rate

Iowa 12% Washington 0%

Pennsylvania 10% Wyoming 0%

Minnesota 10% Florida 0%

New Jersey 9% Nevada 0%

Rhode Island 9% Texas 0%

Applied on profits and apportioned through sales, payroll, and capital

I A single-plant firm j from i with export share s jni to state n pays:

F t li ⇡ji to state i , where t li = tcorpi ⇥ ✓li

F s jni txn⇡

ji to state n, where txn = tcorpn ⇥ ✓xn

F t j⇡ji in total, where t j = tcorpfed + t li +

P

n sjni t

xn

Internal trade matters for determining the corporate tax rate.

Federal corporate tax rate is 18%.

back

Estimation of {"F ,↵F}

Firm share in state n at time t:

lnMnt ="F / (� � 1)

1 + �F↵F (� � 1)ln ((1 � tn)MPnt )+

"F↵F

1 + �F↵F (� � 1)ln

✓Rnt

Pnt

◆�

"F

1 + �F↵F (� � 1)ln cnt+

Mt +⇠Mn +⌫Mnt

Observed covariates:

cnt =⇣

w 1��nnt r�nnt

⌘�nP1��nnt

MPnt =X

n0

En0t

✓

⌧n0ntPn0t

�

� � tn0nt

�� � 1

◆1��

Unobserved:

Mt / ln

✓

1�⇡t

◆

⇠Mn + ⌫Mnt / ln (znt)

Estimation of {"F ,↵F}

Firm share in state n at time t:

lnMnt ="F / (� � 1)

1 + �F↵F (� � 1)ln ((1 � tn)MPnt )+

"F↵F

1 + �F↵F (� � 1)ln

✓Rnt

Pnt

◆�

"F

1 + �F↵F (� � 1)ln cnt+

Mt +⇠Mn +⌫Mnt

Identification assumption:

E[⌫Mnt ⇤ (ZLnt ,MP⇤

nt , ⇠M , M)0] = 0

where

MP⇤nt =

X

n0 6=n

E⇤n0t

✓

⌧n0ntP⇤n0t

�

� � t⇤n0nt

�� � 1

◆1��

,

back

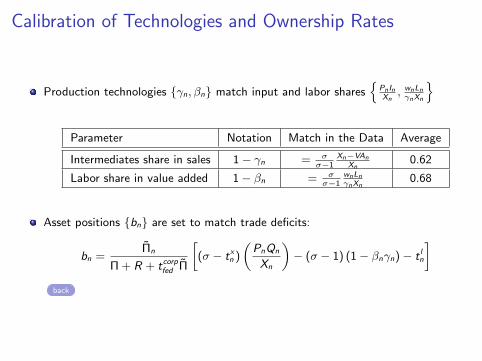

Calibration of Technologies and Ownership Rates

Production technologies {�n,�n} match input and labor sharesn

PnInXn

, wnLn�nXn

o

Parameter Notation Match in the Data Average

Intermediates share in sales 1� �n = ���1

Xn�VAnXn

0.62

Labor share in value added 1� �n = ���1

wnLn�nXn

0.68

Asset positions {bn} are set to match trade deficits:

bn =⇧n

⇧+ R + tcorpfed ⇧

(� � txn )

✓

PnQn

Xn

◆

� (� � 1) (1� �n�n)� t ln

�

back

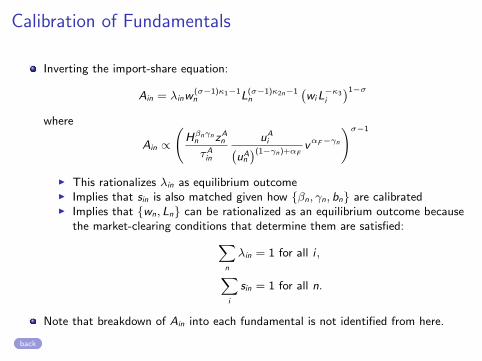

Calibration of Fundamentals

Inverting the import-share equation:

Ain = �inw(��1)1�1n L(��1)2n�1

n

�

wiL�3i

�1��

where

Ain /

H�n�nn zAn⌧Ain

uAi

�

uAn

�(1��n)+↵Fv↵F��n

!��1

I This rationalizes �in as equilibrium outcomeI Implies that sin is also matched given how {�n, �n, bn} are calibratedI Implies that {wn, Ln} can be rationalized as an equilibrium outcome because

the market-clearing conditions that determine them are satisfied:X

n

�in = 1 for all i ,

X

i

sin = 1 for all n.

Note that breakdown of Ain into each fundamental is not identified from here.

back

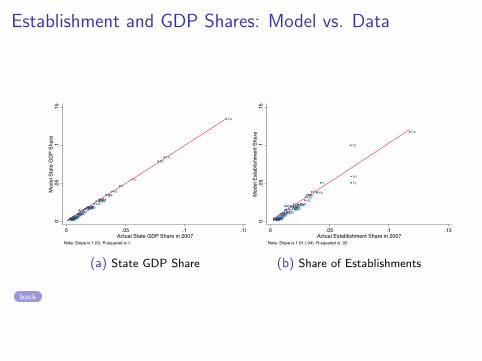

Establishment and GDP Shares: Model vs. Data

ALAZ

AR

CA

COCT

DE

FL

GA

HIID

IL

IN

IAKSKY LA

ME

MD

MAMI

MN

MS

MO

MTNE

NVNH

NJ

NM

NY

NC

ND

OH

OKOR

PA

RISC

SD

TN

TX

UTVT

VAWA

WV

WI

WY0.0

5.1

.15

Mod

el S

tate

GDP

Sha

re

0 .05 .1 .15Actual State GDP Share in 2007

Note: Slope is 1 (0). R-squared is 1.

(a) State GDP Share

AL AZAR

CA

COCT

DE

FL

GA

HIID

IL

IN

IAKS

KYLA

ME

MDMA

MI

MN

MS

MO

MTNENV

NH

NJ

NM

NY

NC

ND

OH

OKOR

PA

RI

SC

SD

TN

TX

UTVT

VAWA

WV

WI

WY0.0

5.1

.15

Mod

el E

stab

lishm

ent S

hare

0 .05 .1 .15Actual Establishment Share in 2007

Note: Slope is 1.01 (.04). R-squared is .92.

(b) Share of Establishments

back

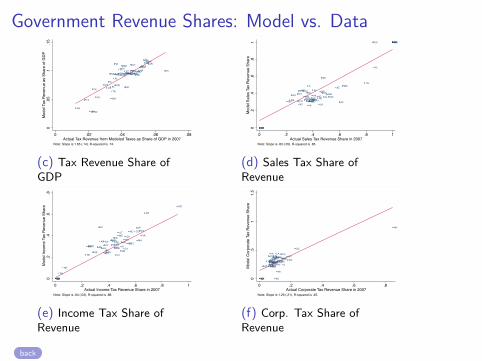

Government Revenue Shares: Model vs. Data

AL

AZ

ARCA

CO

CT

DEFL

GA

HI

ID

IL

IN

IA

KS

KY

LA

MEMD

MA

MI

MN

MS

MO

MT

NE

NV

NH

NJNMNYNCND OHOK

OR

PARI

SC

SD

TN

TX

UTVT

VA

WA

WV

WI

WY

0.0

5.1

.15

Mod

el T

ax R

even

ue a

s Sh

are

of G

DP

0 .02 .04 .06 .08Actual Tax Revenue from Modeled Taxes as Share of GDP in 2007

Note: Slope is 1.65 (.14). R-squared is .74.

(c) Tax Revenue Share ofGDP

AL

AZ

AR

CA

CO

CT

DE

FL

GA HI

ID

IL

IN

IA

KSKY

LAME

MD

MA

MI

MN

MS

MO

MT

NE

NV

NH

NJ NM

NYNC

ND

OHOK

OR

PA

RISC

SD

TN

TX

UT

VTVA

WA

WVWI

WY

0.2

.4.6

.81

Mod

el S

ales

Tax

Rev

enue

Sha

re

0 .2 .4 .6 .8 1Actual Sales Tax Revenue Share in 2007

Note: Slope is .83 (.05). R-squared is .85.

(d) Sales Tax Share ofRevenue

AL

AZ

AR

CA

CO

CT

DE

FL

GA

HI

ID

ILIN

IAKSKY

LA

ME

MDMA

MIMN

MS

MO

MT

NE

NV

NH

NJ

NM

NYNC

ND

OH

OK

OR

PA

RI

SC

SD

TN

TX

UT

VT

VA

WA

WV WI

WY0.2

.4.6

.8M

odel

Inco

me

Tax

Reve

nue

Shar

e

0 .2 .4 .6 .8 1Actual Income Tax Revenue Share in 2007

Note: Slope is .64 (.03). R-squared is .88.

(e) Income Tax Share ofRevenue

AL

AZAR CACOCT

DE

FLGA

HIID IL

INIA

KS KY

LA

MEMD

MA

MI

MN

MS

MO

MTNE

NV

NH

NJNM

NYNC

NDOH

OKORPA

RISC

SD

TN

TX

UT

VT

VA

WA

WVWI

WY0.5

11.

5M

odel

Cor

pora

te T

ax R

even

ue S

hare

0 .2 .4 .6 .8Actual Corporate Tax Revenue Share in 2007

Note: Slope is 1.29 (.21). R-squared is .45.

(f) Corp. Tax Share ofRevenue

back

Price Distortion

Sales apportionment leads to price distortion:

pni (z) = ⌧ni�

� � tni

�� � 1

ciz, where

where

tni =txn �

P

n0 txn0sn0 i

1� ti

I tni = 0 under no dispersion in sales apportionment across states (txn = tx forall n) back

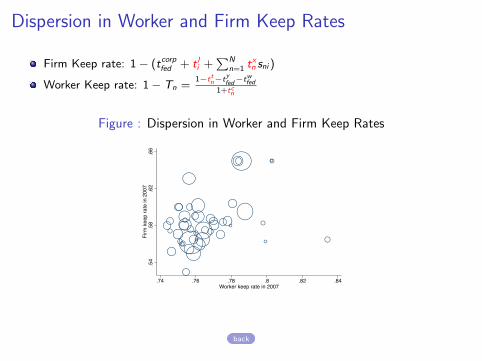

Dispersion in Worker and Firm Keep Rates

Firm Keep rate: 1� (tcorpfed + t li +PN

n=1 txn sni )

Worker Keep rate: 1� Tn =1�ttn�tyfed�twfed

1+tcn

Figure : Dispersion in Worker and Firm Keep Rates

.54

.58

.62

.66

Firm

kee

p ra

te in

200

7

.74 .76 .78 .8 .82 .84Worker keep rate in 2007

back