state responses to tax reform & coronavirus

TRANSCRIPT

State Responses to Tax Reform & CoronavirusAssociation for Computers and Taxation Annual ConferenceMay 18, 2020

Speakers

• Mike Dazé, Sr. Tax Law Analyst, State Direct Tax at Bloomberg Tax & Accounting• Matt Sontag, Software Product Lead at Bloomberg Tax & Accounting

2

2020: A Bit Unexpected

• Entered 2020 still considering continued impacts of 2017 tax act, but coronavirus brought additional changes to federal tax law to which states are responding

• Today's Roadmap:– First, we will give a high level refresher on the Tax Cut and Jobs Act (TCJA) then we will go over the

CARES Act to tee up our starting point for today's conversation.– Next, we will discuss the situation on the ground in the states, New York City, and Washington, D.C.– Then, we will dive in, focusing on IRC sections 172 (NOLs), 163(j) (limitations on business interest),

168 (regular depreciation), and 168(k) (bonus depreciation).– We will incorporate breaking news items along the way.– We will leave time for questions at the end.

3

Tax Cuts and Jobs Act

• Significant changes to the timing of ultimate corporate tax liability– Transition to territorial system with immediate taxation on "unreasonable" foreign profits– Net Operating Loss carryforwards only, limited to 80% of taxable income, but never expire– Interest expense can only offset 30% of EBITDA (EBIT from 2022 on), but excess carries forward

forever– Corporate AMT repealed with staged refunds for minimum tax credits– Regular and bonus depreciation modified for certain types of 15 year "qualified improvement property",

with immediate expensing for some types of property (reduced eligibility from 2022 on)

• Some changes to individual taxation– Cap on deduction of state and local taxes on personal federal income tax returns

4

Tax Cuts and Jobs Act

• We expected to see more of the same in 2020, as state and local tax has become an increasingly important national topic.

• What we were watching headed into January:– Would more states enact or consider entity-level taxes on pass-throughs as a workaround for

the SALT cap deduction?– Would we finally get additional Treasury regulations about section 163(j) and how would

states respond?– How would state budget forecasts impact legislative priorities in 2020?

5

Revenue Forecasts Were Positive

• New York City issued a report in mid-December 2019 estimating tax revenues to grow by 3.9 percent in FY 2020. This growth in revenue was expected to be driven primarily by property tax, but non-property tax revenue did account for almost 2 percent of the expected growth.– NYC report also identified a strong economic outlook for 2020, with fears of a

downturn receding, though an ongoing trade war with China remained one of the biggest risks to the economy. The report suggests that the trade war has caused weak business investment despite significant tax cuts provided by TCJA.

6

Revenue Forecasts: A Look at What Could Have Been?

• Maryland issued a paper for the 2020 legislative session showing the "[f]iscal 2019 general fund revenues exceeded the estimate by $217 million, or 1.2%. General fund revenues totaled $18.2 billion in fiscal 2019, an increase of 4.8% over fiscal 2018. The overattainment was mostly due to the personal income tax and the corporate income tax, both of which were impacted by the TCJA that took effect beginning in tax year 2018."

7

Coronavirus Changed Everything

• In response to global pandemic, Congress passed the "Coronavirus Aid, Relief, and Economic Security Act" or the "CARES Act" in March.

• The CARES Act amends key sections that were changed by TCJA.• Some states have issued guidance or enacted legislation in response to the CARES

Act.• In many cases, though, state legislatures are not in session, but states with rolling

conformity saw changes to their tax laws as a result of the CARES Act.

8

CARES Act

• Three key changes to assist businesses facing monumental business challenges– Taxpayers may carry back Net Operating Losses to five prior taxable years

• Includes 35% tax years but has complex interactions with AMT, BEAT, and FTCs– Taxpayers may use 50% instead of 30% limitation on interest, use 2019's "adjusted taxable

income" as the baseline for the calculation– Technical correction to fix the unintentional omission of Qualified Improvement Property

from 15-year property under TCJA (mistakenly characterized as 39 year property)• What we expect to see going forward

– As unemployment claims exceed 33 million and companies consider bankruptcy protection, additional federal legislation will be needed to help states face deteriorating financial conditions

9

States face dire financial situation

10

• Many states are facing breathtaking financial shortfalls due to Coronavirus– States facing immediate cash flow challenges as payment deadlines are delayed while outflows for

unemployment surge– States facing larger budget challenges as revenues from sales, payroll, and income taxes drop due to

mandatory social distancing rules, business closures, layoffs, wage reductions, etc.– Oklahoma State Treasurer news release May 6, 2020

• April gross receipts fell by more than $500 million, or 32%, year-over-year• Combined sales and use tax collections down $44.7 million, or 9.4%, compared to April 2019• Oil and natural gas production taxes down $19.1 million, or 24%.

– California budget surplus to disappear• $54 billion budget deficit projected through June 2021• 18% unemployment expected

States face dire financial situation

11

• Cost to all states related to the pandemic could reach $500 billion– Study by Univ. of Penn. Wharton School economist highlights:

• State and local revenue losses• Unemployment claims• Demand for health services

– Pennsylvania Treasurer emphasizes that fiscal crisis is more than states can handle without federal support

How will states respond longer term?

12

• Looking to Great Recession for a model:– Temporary limits or bans on use of NOL carryovers to offset current liability– Accelerated evaluation of apportionment methodologies to increase taxable income– Raised rates or imposed surcharges (some temporary or focused on larger corporations)– Changed to combined reporting

• What immediate steps have states taken?– A look at key provisions impacted by both TCJA and the CARES Act.

Net Operating Losses (I.R.C. § 172)

NOLs

• TCJA: For tax years beginning after Dec. 31, 2017, the 2017 tax act amends I.R.C. § 172(b)(1)(A) to eliminate NOL carrybacks, except for farming NOLs under I.R.C. § 172(c), and to allow unused NOLs to be carried forward indefinitely. The act also limits the deduction of NOL carryovers to 80 percent of taxable income.

• CARES Act: For tax years beginning before Jan. 1, 2021, the CARES Act repeals the 80 percent limitation and further amends I.R.C. § 172(b)(1) to provide that NOLs arising in a tax year beginning after Dec. 31, 2017, and before Jan. 1, 2021, may be carried back to each of the five tax years preceding the loss year, and the special rules for farming losses arising in the same years do not apply.

14

CARES Act NOL Changes: Modeling Federal

• Critical to model the actual impact of NOL carrybacks given various attributes, such as:– Federal tax rates applicable to the carryback period:

• 35% pre-2018• Reduced rate (below current 21% statutory rate) possible due to GILTI/BEAT post-2017

– Foreign Tax Credit carryover balances during the carryback period– Impact on AMT (note that minimum tax credit generally refundable in full by 2019 tax year)– Calculation complexity / effort required

• Consider corollary consequences:– Impact on audit status for the carryback year (“reopening” closed years to the extent of the NOL)– Potential additional attention on uncertain tax positions– Contractual obligations

15

Modeling Using Software

16

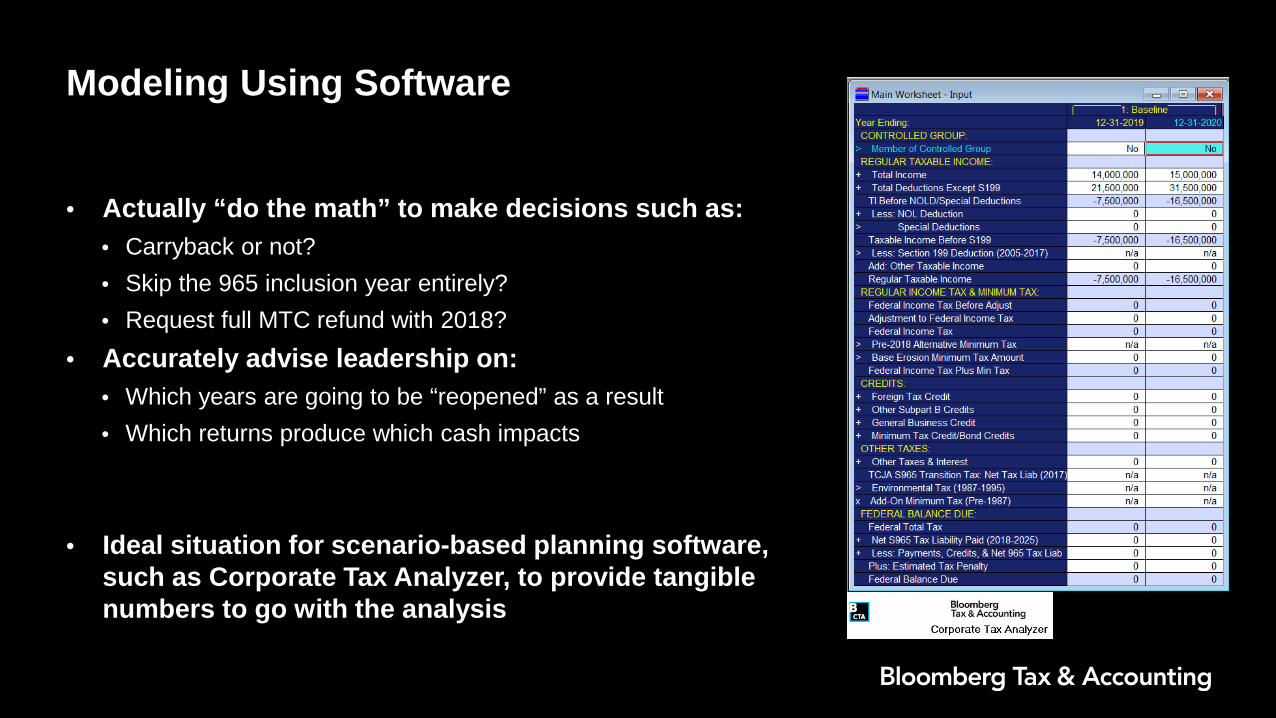

• Actually “do the math” to make decisions such as:• Carryback or not?• Skip the 965 inclusion year entirely?• Request full MTC refund with 2018?

• Accurately advise leadership on:• Which years are going to be “reopened” as a result• Which returns produce which cash impacts

• Ideal situation for scenario-based planning software, such as Corporate Tax Analyzer, to provide tangible numbers to go with the analysis

Example of Modeling using CTA

17

• Electing 5-year carryback – impacts:• AMT• FTCs• GBCs

• Consider:• Expirations• Actual cash flows• Uncertain tax positions

Example of Modeling using CTA

18

• Note the 2018 full refund of the minimum tax liability• At this time, AMT represents a

timing issue within amended returns / expedited claims for refund

• May represent a judgment call related to effort triage

State Response to TCJA and CARES Act NOL Changes

For some states, rolling conformity nominally adopts TCJA's indefinite life as well as the CARES Act 5 year carryback: Alaska, Delaware (carryback limited to $30,000), Maryland, Missouri, Oklahoma

For other states, which have disallowed NOL carrybacks entirely, partial rolling conformity nominally adopts TCJA's indefinite life, but does not permit CARES Act carrybacks: Colorado, DC, Florida, Georgia, Hawaii, Kentucky, Maine, New Mexico, North Dakota, South Carolina, Utah, Virginia, West Virginia

The remaining states have all adopted their own specific NOL rules

19

CARES Act NOL Changes: Modeling State

• "As things are" - As with Federal, model your actual impact of NOLs:– For states thus far conformed to the 5-year carryback, model the impact on carryback years– For States disallowing carrybacks, the now-indefinite lives under TCJA will have affected your

valuation allowance calculations for existing carryovers, but there is still value to modeling the impacts of Coronavirus on your business, including any prospective changes in geographic footprint or taxable presence risks in newly-aggressive States

• "As things could be“– What do you think are the potential impacts?

20

CARES Act NOL Changes: Modeling State

21

Limitations on Business Interest (I.R.C. § 163(j))

Limitations on Business Interest

• TCJA: For tax years beginning after Dec. 31, 2017, the act amends I.R.C. § 163(j) to limit the deduction for net interest expense incurred by a business to the sum of business interest income, 30 percent of adjusted taxable income, and floor plan financing interest. Businesses with average annual gross receipts of $25 million or less are exempt from the limit. Disallowed interest may be carried forward indefinitely.

• CARES Act: For tax years beginning in 2019 and 2020, the CARES Act increases the adjusted taxable income limitation from 30 percent to 50 percent for tax years beginning in 2019 and 2020, and allows taxpayers to use 2019 adjusted taxable income as adjusted taxable income in 2020.

23

CARES Act Limitations on Business Interest Changes: Modeling Federal

• While these changes seem to be an unmitigated blessing, there is potential complex interactions, for example:– The increased expense deduction a taxpayer may claim in 2019 and, in particular, in 2020 will impact

the net operating loss carrybacks (if elected) from those tax years, which will change the impact those carrybacks have on the overall tax posture

24

Limitations on Business Interest Calculations: Modeling Federal

25

• Taxpayer may choose:– 2019: (100K) or 900K?– 2020: (5M), (7.1M), or

(8.1M)?

• Model actual impact on carryback years to determine optimum outcome for your specific situation.

State Limitations on Business Interest Deduction

• Rolling conformity states follow both the TCJA and CARES Act amendments to I.R.C. §163(j)

– Alabama, Alaska, Colorado, Delaware, D.C., Illinois, Louisiana, Maryland, Massachusetts, Missouri, Montana, Nebraska, North Dakota, Oklahoma, Rhode Island, Utah

• Some states with static conformity dates may apply only the TCJA limitations– Arizona (Jan. 1, 2020), Hawaii (Dec. 31, 2018), Idaho (Jan. 1, 2020), Kentucky (Dec. 31, 2018),

Maine (Dec. 31, 2019), Minnesota (Dec. 31, 2018), Vermont (Dec. 31, 2018)• Other states have their own rules

– Indiana decouples from the federal limitations and requires adjustments in federal carryover years– Mississippi does not have general conformity; allows deductions for business interest– South Carolina specifically does not adopt I.R.C. § 163(j) limitations

26

CARES Act Limitations on Business Interest Changes: Modeling State

• Calculate the actual impacts of the various state implementations

27

Depreciation (I.R.C. §168)

Depreciation

• TCJA: For property placed in service after Dec. 31, 2017, act amends I.R.C. § 168 by providing a 15-year recovery period for qualified improvement property, with the term “15-year property” defined fairly narrowly. The act also repeals I.R.C. § 168(b) requirement that farming business property is subject to the 150 percent declining balance method and in its place creates a 5-year recovery period for machinery or equipment used in a farming business and placed in service after Dec. 31, 2017.

• CARES Act: For property placed in service after Dec. 31, 2017, the CARES Act makes a technical correction to the 2017 tax act by amending I.R.C. § 168 and providing a 15-year recovery period for “any qualified improvement property,” which is added to the definition of “15-year property” in I.R.C. § 168(e)(3)(E).

29

Regular Depreciation

• Amended return opportunity– Taxpayers not electing to claim 100 percent bonus depreciation, could amend 2018 returns to

depreciate qualified improvement property over 15 years, instead of 39 years– Conforming states could see an impact from amended returns requesting refunds

• The shorter recovery period might provide an incentive for investment in improvements to nonresidential real property.

30

CARES Act Regular Depreciation Changes: Modeling

31

• Depreciation software such as Advantage Fixed Assets can easily update assets for the QIP changes and then compare the impact– Important to understand how the

change impacts the modeling you are doing both at the federal and state levels

Bonus Depreciation (I.R.C. § 168(k))

Bonus Depreciation

• TCJA: With respect to I.R.C. § 168(k), changes made by the 2017 tax act include expanding the definition of qualified property and allowing full expensing for property placed in service after Sept. 27, 2017, and reducing the percentage that may be expensed after Dec. 31, 2022.

• CARES Act: As a technical correction to the amendments made by the 2017 tax act, the CARES Act treats qualified improvement property as 15-year property; thus making it eligible for 100 percent bonus depreciation.

33

Bonus Depreciation in the States

• Rolling conformity– Alabama, Alaska (except oil and gas industry), Colorado, Delaware, Kansas, Louisiana, Missouri,

Montana, Nebraska, New Mexico, North Dakota, Oklahoma, Utah• Decoupling states

– Many states, those with rolling conformity and those with static conformity, have not adopted the federal bonus depreciation deduction.

– Depreciation is determined under I.R.C. § 168, without the § 168(k) election; either the current version or I.R.C. § 168 as of the static conformity date applies

• Rolling examples: Connecticut, Illinois, Iowa, Maryland, New York, Rhode Island• Static examples: Arizona, California, Florida, Georgia, Hawaii, Idaho, Maine, Minnesota

– The few states without general conformity (e.g., Arkansas, Mississippi, New Jersey) also do not adopt bonus depreciation

• Amended return opportunity for qualified improvement property

34

CARES Act Bonus Depreciation Changes: Modeling

• Adjusting asset type settings for Bonus Depreciation changes, both in Federal and State books, should be straightforward

– Easily model the actual impacts of these changes on your company

35

Conclusion

Q&A

37