state of vermont public utility commission case … · state of vermont public utility commission...

TRANSCRIPT

STATE OF VERMONT

PUBLIC UTILITY COMMISSION

Case No. 17-3112-INV

Investigation into the petition of Green Mountain Power Corporation's

tariff filing requesting an overall rate increase in the amount of 4.98%,

to take effect January 1, 2018.

PREFILED DIRECT TESTIMONY OF

DAVID P. VONDLE, CMC

SAGE MANAGEMENT CONSULTANTS, LLC

ON BEHALF OF THE

VERMONT DEPARTMENT OF PUBLIC SERVICE

August 14, 2017

Summary: Mr. Vondle provides an overview of the SAGE Management Consultants, LLC

testimony on the proposed Green Mountain Power capital expenditures and addresses

the enterprise-wide capital program.

List of Exhibits Sponsored by Mr. Vondle

Exhibit PSD-DPV-1 – Resume/CV

Exhibit PSD-DPV-2 – GMP Discovery Response GMP.DPS3.Q9

Exhibit PSD-DPV-3 – SAGE Reconciliation of GMP’s Reported Capital Expenditures

Exhibit PSD-DPV-4 – GMP Strategic Plan (November, 2015)

Exhibit PSD-DPV-5 – GMP Strategic Plan (November, 2016)

Exhibit PSD-DPV-6 – GMP Key Operating Objectives and Metrics (2015)

Exhibit PSD-DPV-7 – GMP Key Operating Objectives and Metrics (2016)

Exhibit PSD-DPV-8 – GMP Key Operating Objectives and Metrics (2017)

Exhibit PSD-DPV-9 – GMP Discovery Response DPS1.Q21

Exhibit PSD-DPV-10 – GMP Discovery Response – GMP.DPS3.Q29

Exhibit PSD-DPV-11 – GMP Discovery Response GMP.DPS3.Q28

Exhibit PSD-DPV-12 – GMP Discovery Response GMP.DPS1.Q17b

Exhibit PSD-DPV-13 – GMP Discovery Response GMP.DPS1.Q25

Exhibit PSD-DPV-14 – GMP Discovery Response – GMP.DPS3.Q8

Exhibit PSD-DPV-15 – GMP Discovery Response GMP.DPS1.Q42

Case No. 17-3112-INV

GMP Rate Case

PSD Direct Testimony of David P. Vondle, CMC

August 14, 2017

Page 1 of 14

Q1 Please state your name, occupation, and business address. 1

A1. My name is David P. Vondle. I am a Partner in SAGE Management Consultants, LLC 2

(“SAGE”), a regulatory and litigation support management consulting firm. My business 3

address is 4926 Calle de Tierra, NE, Albuquerque, New Mexico 87111. 4

5

Q2. Please describe your role, educational background, and experience. 6

A2. I am the Project Manager for the SAGE involvement in this case. I have over 25 years of 7

management consulting experience with special emphasis on providing regulatory and 8

litigation support services, including expert witness testimony for consumer advocates, 9

regulatory commissions, attorneys general, and law firms. In addition to conducting 10

many management audits for state regulatory commissions, I have appeared as an expert 11

witness in fifteen jurisdictions on topics that include capital program planning, storm cost 12

recovery, mergers, contract compliance, and affiliate relationships. 13

14

I, and various members of the SAGE team, have worked on recent engagements 15

involving Emera, a Canadian holding company and its subsidiaries Nova Scotia Power, 16

Inc., Bangor Hydro, and Maine Public Service Company; Eversource and its subsidiaries 17

Connecticut Light and Power and NSTAR Electric; PPL Corporation and its subsidiaries 18

PPL Electric Utilities, Louisville Gas & Electric, and Kentucky Power; and FirstEnergy 19

and its seven Pennsylvania, New Jersey, and Ohio utility operating company subsidiaries. 20

21

Case No. 17-3112-INV

GMP Rate Case

PSD Direct Testimony of David P. Vondle, CMC

August 14, 2017

Page 2 of 14

I have a Bachelor of Science degree in Industrial Management from University of Akron, 1

a Master of Business Administration degree from Southern Methodist University, and 2

have been designated a Certified Management Consultant (“CMC”) by the Institute of 3

Management Consultants. 4

5

My resume is attached as Exhibit PSD-DPV-1. 6

7

Q3. Have you ever testified before the Vermont Public Utilities Commission? 8

A3. No. 9

10

Q4. What is the purpose of the SAGE testimony? 11

A4. The SAGE team examined the current and planned Green Mountain Power (“GMP”) 12

capital expenditures and power supply portfolio and developed recommendations about 13

them. I address the total enterprise-wide capital program. Mr. Whitman addresses the 14

generation, transmission, and distribution capital programs. Mr. Rosenkoetter addresses 15

the support services capital programs. Mr. Evans addresses the power supply portfolio. I 16

summarize the SAGE team recommendations at the end of my testimony. 17

18

Q5. Why is examining a utility’s capital program important? 19

A4. Continued capital expenditures by an electric utility are required to accommodate growth 20

in the number of customers and the electric load, capture available operational savings, 21

comply with regulatory requirements, maintain or improve reliability and customer 22

Case No. 17-3112-INV

GMP Rate Case

PSD Direct Testimony of David P. Vondle, CMC

August 14, 2017

Page 3 of 14

service, and maintain or improve safety. A healthy utility will have a capital program that 1

addresses all of these needs. Ongoing capital expenditures are necessary to preserve or 2

improve reliability and customer service for the ratepayers and safety for employees and 3

the public. 4

5

Q6. Can you provide an overview of the proposed GMP capital program? 6

A6. Exhibit PSD-DPV-2 is the GMP response to DPS3.Q9 and shows the past and planned 7

capital expenditures for GMP (including CVPS). The table below shows the total GMP 8

capital expenditures, actual for years 2009 through 2016, and planned for years 2017 9

through 2021. The table also shows the depreciation expense for the years 2009 through 10

2016. 11

GMP Capital Expenditures and Depreciation Expense (in millions of dollars)1 12 13

Year Capital Expenditures Depreciation Expense

2009 71.4 33.1

2010 54.4 34.0

2011 62.3 36.8

2012 202.6 37.1

2013 144.1 46.3

2014 105.2 49.4

2015 108.9 49.0

2016 104.3 53.0

2017 129.1

2018 96.6

2019 98.6

2020 84.7

2021 87.8

Source: Exhibit PSD-DPV-2 – GMP.DPS3.Q9

1 The total capital expenditures reported in the discovery response to DPS3.Q.9 Attachment 2017 and 2018 is

$225.7 million, which is $13.7 million higher than the $212.0 million reported in the Otley, Fiske, Castonguay, and

Riley testimony exhibits, and the response to DPS1.Q.29. This information is documented in Exhibit PSD-DPV-3 –

SAGE Reconciliation of GMP’s Reported Capital Expenditures.

Case No. 17-3112-INV

GMP Rate Case

PSD Direct Testimony of David P. Vondle, CMC

August 14, 2017

Page 4 of 14

1

The capital expenditures exceed the depreciation expense for the years 2009 through 2

2016, meaning the rate base is increasing. Capital expenditures averaged $62.7 million 3

per year in 2009 through 2011, $174.4 million per year in 2012 and 2013, and $106.1 4

million per year in 2014 through 2016. Capital expenditures are forecast at $129.1 in 5

2017 and an average of $91.9 million per year in 2018 through 2021. The $212 million 6

capital expenditures proposed in this case for 2017 and 2018 average $106.0 million per 7

year, which is $43.3 million, or 69 %, higher than the average capital expenditures during 8

the 2009 through 2011 period. 9

10

Q7. What do you look for when examining utility capital programs? 11

A7. Each utility capital expenditure should be consistent with a well-founded overall strategic 12

plan and with the relevant well-developed subordinate plan like the transmission and 13

distribution (“T&D”) system plan or the information technology and systems (“IT”) plan. 14

Each capital expenditure should have a clear purpose or purposes and should be a logical 15

extension of the relevant company plan. That is, it should be easy to “connect the dots” 16

between a capital project and its purpose and justification. Further, the capital projects 17

chosen for implementation should produce the lowest present value revenue requirement 18

to achieve the objective. All reasonable alternatives should be considered before a capital 19

project is selected for implementation. 20

21

The strategic plan should guide the subordinate plans (like the T&D and IT plans) and 22

each subordinate plan should articulate the objectives it is trying to achieve. Each capital 23

Case No. 17-3112-INV

GMP Rate Case

PSD Direct Testimony of David P. Vondle, CMC

August 14, 2017

Page 5 of 14

expenditure should be made in furtherance of the utility’s goals and objectives, ideally to 1

provide good reliability and customer service at the lowest present value revenue 2

requirement. Selected capital expenditures should flow from the plans and each capital 3

project should be tied to achieving one or more specific objective. 4

5

Because utilities have a financial incentive to maintain and build their rate bases, it is 6

important for regulators to be able to scrutinize the capital programs to assure that each 7

expenditure is necessary and justified with adequate documentation and financial 8

analyses. In their testimonies, Messrs. Whitman and Rosenkoetter look at the 9

documentation for individual capital projects and groups of related capital projects 10

(capital programs). They identify capital programs or projects that do not appear to be 11

fully justified based on the documentation produced by GMP through its discovery 12

responses. 13

14

Q8. Does the GMP strategic plan provide adequate guidance to subordinate plans and 15

capital program planning? 16

A8. GMP produced copies of strategic plan documents for 2015 and 2016 in response to 17

discovery requests. The mission in the 2015 strategic plan is, “To be the Best Small 18

Company in America.” The 2016 strategic plan added, “Vermont’s Energy 19

Transformation Company.” These documents are attached as Exhibits PSD-DPV-4 and 20

PSD-PDV-5. These mission statements, however, do not give much specific guidance to 21

T&D, IT, and Facilities capital plans. 22

23

Case No. 17-3112-INV

GMP Rate Case

PSD Direct Testimony of David P. Vondle, CMC

August 14, 2017

Page 6 of 14

The strategic plan strategy section does include, “Build incredible connection with customers 1

and communities through superior service & innovative programs” and “target investments 2

that produce value for customers and communities.” These messages provide some capital 3

program guidance. 4

5

The GMP strategic plan does not have a capital program section, so specific capital program 6

planning guidance is not included. 7

8

Q9. Does GMP have other guidance for the capital program? 9

A9. To an extent. GMP has Key Operating Objectives and Metrics. These objectives and 10

metrics have Customer, Financial, Net Power Cost, Technology and Innovation, and 11

Employee sections. The document is a mix of initiatives, targets, and performance 12

reporting including the Vermont Service Quality Performance Index. However, the Key 13

Operating Objectives and Metrics do not address the capital program and capital 14

expenditures directly. The “Key Operating Objectives and Metrics” documents produced 15

by GMP in discovery are attached as Exhibits PSD-DPV-6, PSD-DPV-7, and PSD-DPV-16

8. Only inferences can be drawn regarding capital spending guidance from the Key 17

Operating Objectives and Metrics. 18

19

Q10. Does GMP provide adequate guidance for developing capital programs? 20

A10. No. The strategic plan should include specific guidance for the approximate total capital 21

expenditures each year and the Company’s priorities for capital expenditures. GMP 22

should also require each department to have a rigorous, objective, and documented 23

Case No. 17-3112-INV

GMP Rate Case

PSD Direct Testimony of David P. Vondle, CMC

August 14, 2017

Page 7 of 14

process for analyzing and prioritizing the candidate capital projects each year tied to 1

achieving performance objectives for reliability, customer service, safety, and other 2

factors relevant to each department. The prioritization scheme in each department should 3

allow the GMP executive team good visibility into the proposed projects and the 4

alternatives. The sum of projects designed to achieve each objective, such as reliability, 5

should be the least cost set of alternatives that can be reasonably expected to achieve the 6

objective. Departmental capital project proposals should be presented as sets of projects 7

each designed to achieve a stated objective. 8

9

Q11. How does GMP categorize its capital projects? 10

A11. GMP categorizes its projects in two ways. In one version, GMP lists each project as 11

“must do,” “should do,” or “would like to do.” The response to GMP.DPS1.Q21, which 12

is attached as Exhibit DSP-DPV-9 explains: 13

GMP makes decisions for capital projects in upcoming years based on 14

what is needed to provide safe, reliable, cost-effective service to customers and 15

then all financial metrics flow from that. As described by Mr. Otley in his 16

testimony, every year, capital budget owners forecast projects needed to 17

continue to provide safe, reliable, cost-effective service to customers in the 18

coming year. Every project then goes through a screen of must do, should do, 19

and would like to do and is reviewed by a subset of leadership team members. 20

This final capital budget is then approved by GMP for the coming year. 21

22

Mr. Otley’s testimony defines the three categories as: 23

Case No. 17-3112-INV

GMP Rate Case

PSD Direct Testimony of David P. Vondle, CMC

August 14, 2017

Page 8 of 14

“Must Do” projects are viewed as compulsory in the year proposed. The “Should 1

Do” category “represents work that GMP does to keep advancing the cost 2

effectiveness, performance, reliability, and safety of their operations. The “Like 3

to Do” category of projects are those that focus on advancements that can 4

provide customers and operations with a “leapfrog in performance” (Testimony 5

of Brian Otley, April 14, 2017, page 6, 1-17). 6

7

Most of these GMP proposed capital projects fall into the first two categories. Projects 8

justified by safety, technical/regulatory compliance, or reliability are considered “must 9

do” projects (Exhibit PSD-DPV-10 – DPS3.Q29), and are considered “non-negotiable.” 10

(Exhibit PSD-DPV-11 – GMP.DPS.3.Q28). 11

12

This categorization and prioritization scheme seems to be based on management 13

judgement of “must do, should do, or would like to do” and each project is not tied to 14

accomplishing a specific purpose or formal project analysis other than the “must dos” for 15

safety, compliance, or reliability. This first categorization method is not useful in 16

evaluating the value of capital projects. 17

18

The second capital project categorization version is more helpful. GMP classified the projects 19

included in its tariff filing as: Safety, Reliability, Operational Efficiency, Compliance, State 20

Energy Policy, Customer Service, Generation Operation, Generation, or a combination of two 21

or more purposes. A few projects were classified as “various.” See Exhibit PSD-DAW-6 22

Case No. 17-3112-INV

GMP Rate Case

PSD Direct Testimony of David P. Vondle, CMC

August 14, 2017

Page 9 of 14

(GMP discovery response GMP.DPS1.Q29) (attached to the testimony of Mr. Whitman). 1

This classification scheme is more helpful in evaluating each proposed project. 2

3

Q12. How does the second GMP capital project categorization scheme assist in the 4

evaluation of the various departmental capital programs? 5

A.12 Tying the project to the purpose(s) of the project provides context to link each project to a 6

goal or objective and to consider the effect of the project on achieving the goal or 7

objective. For example, the sum of the projects addressing safety should be adequate to 8

achieve a safety goal with the lowest present value of revenue requirement. Likewise, the 9

sum of the projects addressing reliability should achieve a reliability goal with the lowest 10

present value of revenue requirement. A project with an operational efficiency goal must 11

be shown to have a reasonable chance of generating sufficient O&M savings to justify the 12

capital expenditure. A good practice for large capital expenditure projects is to develop a 13

formal business case for the project. The documentation for each set of capital projects 14

(capital programs) addressing each objective should be sufficient to show how they will 15

meet the objective, how they fit with each other, and how they provide the lowest present 16

value revenue requirement alternative to meet the objective. 17

18

Q13. Does GMP’s past performance and future goals indicate the need for a large capital 19

program? 20

A.13 No. GMP’s reported performance is good. In 2016, GMP met or exceeded the stretch 21

goal for all seventeen Service Quality metrics. See Exhibit PSD-DPV-12 (GMP 22

Case No. 17-3112-INV

GMP Rate Case

PSD Direct Testimony of David P. Vondle, CMC

August 14, 2017

Page 10 of 14

discovery response GMP.DPS1.Q17.b). These 17 goals cover customer service, safety, 1

and reliability, the key areas of utility performance. In addition to having good reliability, 2

customer service, and safety, GMP also reports having the second lowest rates in New 3

England. See Exhibit PSD-DPV-13 (GMP Discovery response GMP.DPS1.Q25). 4

5

In general, the 2017 Key Operating Objectives and Metrics recognizes this with modest 6

goals like, “Achieve continued improvement over 5-year average in SAIFI and CAIDI 7

reliability statistics,” and “Continued focus on 100% execution of safety regimen 8

resulting in reduced accidents and lost time while implementing new strategies to 9

influence safety culture.” See Exhibit PSD-PDV-12. Most of the 2017 targeted 10

improvements are continuations of current initiatives and improvement trends. 11

12

However, even modest improvements over good performance must be carefully 13

considered. This is because incremental investment for further improvement usually 14

produces diminishing returns. If improvement programs are well-crafted, the “low 15

hanging fruit” of high returns for small investments are taken first. Necessarily, future 16

efforts then require higher investment for lower returns. That is, ever more dollars are 17

required to achieve the next unit of improvement. Once good performance is achieved, 18

utilities are wise to limit capital spending to maintain the good performance with only 19

targeted, modest efforts to improve performance. Capital programs should be the least 20

cost set of alternatives to achieve the Company objectives and the documentation of the 21

capital programs should demonstrate this fact. 22

23

Case No. 17-3112-INV

GMP Rate Case

PSD Direct Testimony of David P. Vondle, CMC

August 14, 2017

Page 11 of 14

Q14. Are there other indicators that a large capital program at GMP is not needed? 1

A14. Yes. Some of the largest drivers of electric utility capital programs have been completed 2

by GMP. Current typical large electric utility capital programs are Advanced Metering 3

Infrastructure (AMI), Smart Grid (Grid Automation), and the Customer Information 4

System (CIS). GMP has largely completed all of these large capital investment programs 5

and is enjoying the fruits of the investments. See Exhibit PSD-DPS-14 (GMP Discovery 6

response GMP.DPS3.Q8). These three programs are particularly attractive to utilities 7

because the large capital investments required are offset by decreases in O&M costs. 8

Thus, the rate base is increased but the impact on rates is moderated. For example, 9

capital expenditures for automation can reduce O&M expenditures for things like meter 10

readers, turn-ons and turn-offs, fault locations, and resetting breakers. 11

12

GMP reports that it has, “essentially completed the AMI and CIS programs” and “capital 13

spending for CIS is now specific to upgrades to the software systems and hardware 14

infrastructure every several years that operate CIS.” See Exhibit PSD-DPV-14. Further, 15

“smart grid investments have leveraged millions of dollars of both direct and indirect savings 16

for customers. This includes O&M savings due to decreased meter readers and decreased 17

mileage from meter reader vehicles as well as savings from faster outage response times and 18

better automation of substations and related equipment.” See Exhibit PSD-DPV-14. 19

20

Regarding the Smart Grid program, GMP reports that, “The primary expenses and capital 21

spending associated with the Smart Grid project were expended several years ago. 22

Case No. 17-3112-INV

GMP Rate Case

PSD Direct Testimony of David P. Vondle, CMC

August 14, 2017

Page 12 of 14

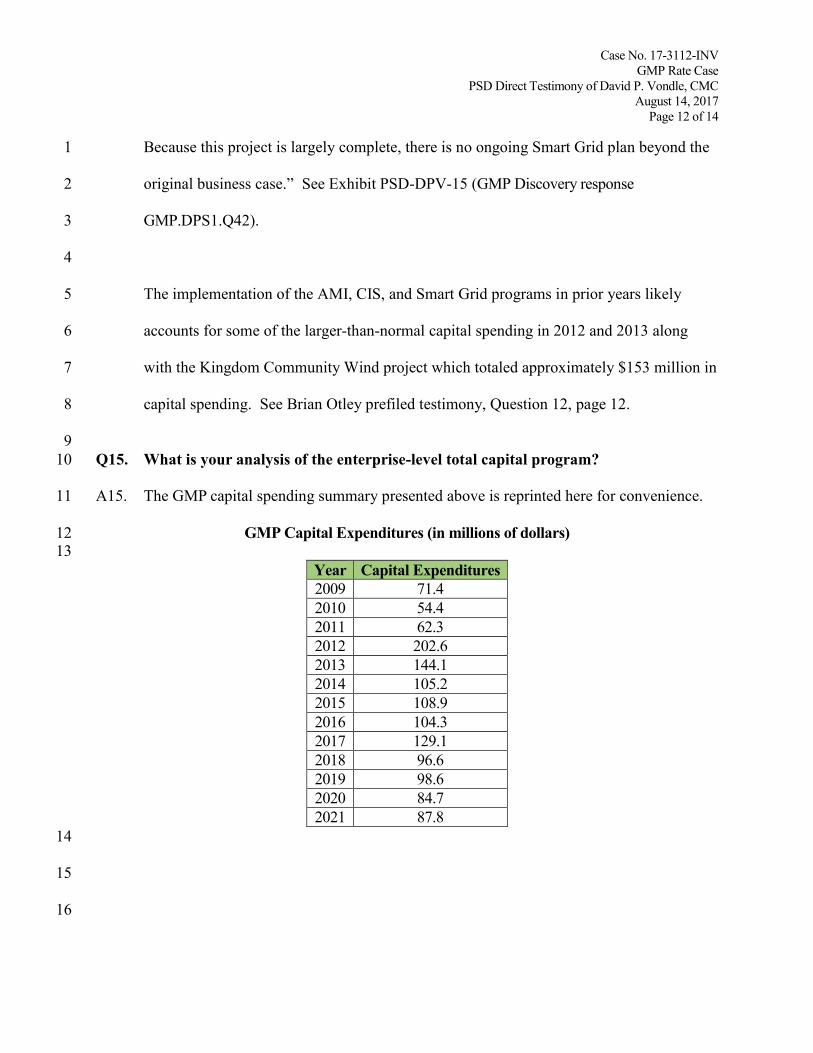

Because this project is largely complete, there is no ongoing Smart Grid plan beyond the 1

original business case.” See Exhibit PSD-DPV-15 (GMP Discovery response 2

GMP.DPS1.Q42). 3

4

The implementation of the AMI, CIS, and Smart Grid programs in prior years likely 5

accounts for some of the larger-than-normal capital spending in 2012 and 2013 along 6

with the Kingdom Community Wind project which totaled approximately $153 million in 7

capital spending. See Brian Otley prefiled testimony, Question 12, page 12. 8

9

Q15. What is your analysis of the enterprise-level total capital program? 10

A15. The GMP capital spending summary presented above is reprinted here for convenience. 11

GMP Capital Expenditures (in millions of dollars) 12 13

Year Capital Expenditures

2009 71.4

2010 54.4

2011 62.3

2012 202.6

2013 144.1

2014 105.2

2015 108.9

2016 104.3

2017 129.1

2018 96.6

2019 98.6

2020 84.7

2021 87.8

14

15

16

Case No. 17-3112-INV

GMP Rate Case

PSD Direct Testimony of David P. Vondle, CMC

August 14, 2017

Page 13 of 14

Q16. Do the GMP planning and operational performance improvement targets justify the 1

magnitude of the planned capital program in 2017? 2

A.16 No. The overall capital program trend shows decreased spending beginning in 2014 and 3

continuing through 2021. However, the downward trend does not reach the level of GMP 4

capital spending before the large projects in 2012 and 2013. I would expect the overall 5

level of GMP capital spending to return to the prior level after the major capital programs 6

of AMI, Smart Grid, and CIS. The average for 2009 through 2012 is $62.7 million per 7

year. Compounding the 2009–2011 average of $62.7 million by a 3% annual inflation 8

rate would put GMP capital expenditures for 2017 at $74.9 million and for 2018 at $77.1 9

million. This would be a total of $151.0 million for 2017 and 2018. 10

11

There is no enterprise-level evidence of why the capital program in 2017 and 2018 should 12

not be more consistent with the 2009–2011 levels. With little customer or load growth, 13

no major improvement programs under way, and adequate reliability, customer service, 14

and safety, there is no clear reason why the much higher level of capital spending in 2017 15

and 2018 is needed. A more realistic capital program for 2017 and 2018 might be on the 16

order of $151.0 million. Please refer to Mr. Winn’s testimony for the recommendation 17

related to this analysis. 18

19

Of course, GMP should continue to make the capital expenditures required to support 20

growth in the number of customers and load; maintain reliability, customer service, and 21

safety; capture cost justified operational efficiencies; and comply with all legislative, 22

regulatory, and policy requirements. However, the documentation for these capital 23

Case No. 17-3112-INV

GMP Rate Case

PSD Direct Testimony of David P. Vondle, CMC

August 14, 2017

Page 14 of 14

expenditures should clearly show how they are achieving the GMP objectives at the 1

lowest present value revenue requirement. 2

3

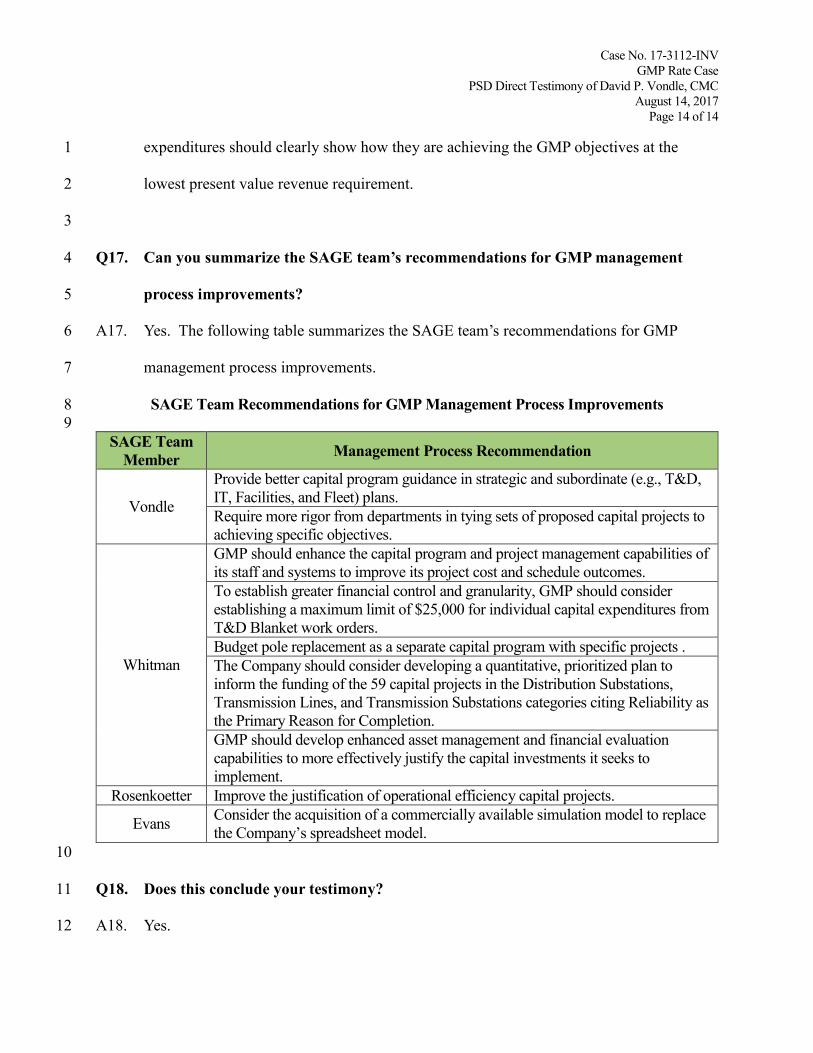

Q17. Can you summarize the SAGE team’s recommendations for GMP management 4

process improvements? 5

A17. Yes. The following table summarizes the SAGE team’s recommendations for GMP 6

management process improvements. 7

SAGE Team Recommendations for GMP Management Process Improvements 8

9

SAGE Team

Member Management Process Recommendation

Vondle

Provide better capital program guidance in strategic and subordinate (e.g., T&D,

IT, Facilities, and Fleet) plans.

Require more rigor from departments in tying sets of proposed capital projects to

achieving specific objectives.

Whitman

GMP should enhance the capital program and project management capabilities of

its staff and systems to improve its project cost and schedule outcomes.

To establish greater financial control and granularity, GMP should consider

establishing a maximum limit of $25,000 for individual capital expenditures from

T&D Blanket work orders.

Budget pole replacement as a separate capital program with specific projects .

The Company should consider developing a quantitative, prioritized plan to

inform the funding of the 59 capital projects in the Distribution Substations,

Transmission Lines, and Transmission Substations categories citing Reliability as

the Primary Reason for Completion.

GMP should develop enhanced asset management and financial evaluation

capabilities to more effectively justify the capital investments it seeks to

implement.

Rosenkoetter Improve the justification of operational efficiency capital projects.

Evans Consider the acquisition of a commercially available simulation model to replace

the Company’s spreadsheet model.

10

Q18. Does this conclude your testimony? 11

A18. Yes.12