state of compliance 2013

TRANSCRIPT

State of Compliance 2013

18 October 2013

GLOBALIZATION:

THE REGULATORY

COMPLIANCE

TREND FOR TODAY

Agenda

oThe Story of Regulation

oGlobal Economy and Global Investment

oGlobal Regulation

oThe Joint Forum and their AIG Case Study

oAML

oConclusions

The Story of Regulation

Investment

Damage

Regulation

Global Investment

Real GDP Growth 2005-2010

Real GDP Growth 2011-2015 (Projected)

7

Regional GDP Trends 1990-2018

Global CDO Issuance 2000-2009

0.00

50,000.00

100,000.00

150,000.00

200,000.00

250,000.00

300,000.00

350,000.00

400,000.00

450,000.00

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

USD

Mill

ion

s

Year

AUD

EUR

GBP

JPY

Other

USD

http://www.sifma.org/uploadedFiles/Research/Statistics/SIFMA_GlobalCDOData.pdf

Global Regulation

G-20

ArgentinaAustraliaBrazilCanadaChinaFranceGermanyIndiaIndonesiaItalyJapanMexicoRussiaSaudi ArabiaSouth AfricaRepublic of KoreaTurkeyUnited KingdomUnited States of America

The Joint Forum

G20

BCBS IOSCO IAIS

Financial Stability Board

The Joint Forum: January 2010

Five Key Findings

1) Key Regulatory Differences within Sectors

• Banking

• Insurance

• Securities

2) Supervision and Regulation

3) Mortgage Origination

4) Hedge Funds

5) Credit Risk Transfer Products

AIG Case Study

Lessons from AIG Case Study

• Past may not be prologue when assessing risk of exotic investments

• Lack of liquidity weakened AIG

• AIG became too big to fail and required a bail out by the US government

• Global regulatory compliance standards will reduce the potential for regulatory arbitrage.

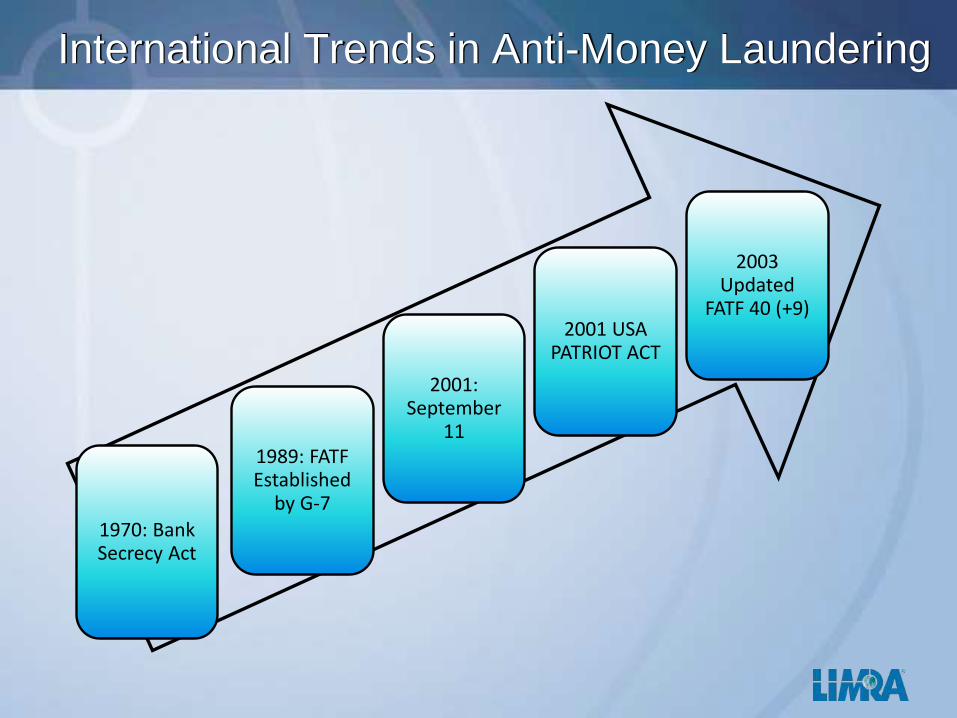

International Trends in Anti-Money Laundering

1970: Bank Secrecy Act

1989: FATF Established

by G-7

2001: September

11

2001 USA PATRIOT ACT

2003 Updated

FATF 40 (+9)

FATF Standards

A. Legal Systems

B. Measures to be taken by financial institutions and non-financial businesses and professions to prevent money laundering and terrorist financing.

C. Institutional and other measures necessary in systems for combating money laundering and terrorist financing.

D. International co-operation

http://www.fatf-gafi.org/dataoecd/7/40/34849567.PDF

+9 Special Recommendations (SR) on Terrorist Financing (TF)

I. Ratification and implementation of UN instruments

II. Criminalising the financing of terrorism and associated money laundering

III. Freezing and confiscating terrorist assets

IV. Reporting suspicious transactions related to terrorism

V. International co-operation

VI. Alternative remittance

VII.Wire transfers

VIII.Non-profit organisations

IX. Cash couriers

http://www.fatf-gafi.org/document/9/0,3343,en_32250379_32236920_34032073_1_1_1_1,00.html

A world of “no”?

Conclusions

oInterconnected economies create shared pain

oShared pain causes governments to seek shared solutions.

oThe global trend in regulation is Globalization

oGlobal standardization reduces the opportunities for regulatory arbitrage

oA world of “no?”

Day 1 Day 365

Risk

Compliance Technology

Independent Producer Clearinghouse (IPC)

Compliance Manuals

Audit Services

Anti-Money Laundering (AML)

3012

&

3130(b)

Adequacy

ReviewCompliance Consulting

Benchmarking, Research, Surveys

Compliance Status Improvement

Regulatory Services - The Continuity of Support

3012

&

3130(b)

Adequacy

Testing

www.limra.com/compliance : (877) 843-2641 : [email protected]

300 Day Hill Road Windsor, CT 06095

COMPLIANCE STRUCTURES

Compliance System: Regulatory Overview

Federal

States

SEC

FINRA

Corporation

Third Parties Field Offices

Producers

• Compliance Department

• Corporate oversight

• General direction

• Manuals

• Cleary state policies

• Cleary state procedures

• Specialized

• Supervisors

• Delegate authority

• Final decisions

• General oversight

• Administrative Support

• New Business

• Data entry

• Licensing /Registration

• Systems

• Order entry

• Communications

• Producers

• Good sales practices

• Active cooperation

Compliance System: Structural Example - Retail

Corporation

Law:

Gen Counsel

Business

Lines

Div. President

Compliance

Department:

CCO

Law

Department

Embedded

Compliance

Staff

Compliance

Department:

Staff

Compliance RAVPs

Regional VPs

Office Managers

Local Staff

Producers

Compliance AVPs

Teaching & Entrenching Compliance Principles

• Review regulatory requirements

• States

• FINRA

• Business Model

• Consider the Audience

• Home office staff may be licensed

• Local support staff may be licensed

• Does the firm have any special markets like international markets or options?

Teaching & Entrenching Compliance Principles

• Education Processes

• Formal Education Programs

• Insurance Agent required credit hours

• Regulatory Element

• Firm Element

• Annual Compliance Meetings

• Content

• Provided / mandated by government

• Firm created

• Third Parties

• Certification Processes

• Annual Attestation

Whistleblower System: Part 1

• Definition:

Most whistleblowers are internal whistleblowers, who report misconduct to a fellow employee or superior within their company. External whistleblowers, however, report misconduct to outside persons or entities. In these cases, depending on the information's severity and nature, whistleblowers may report the misconduct to lawyers, the media, law enforcement or watchdog agencies, or other local, state, or federal agencies. (http://en.wikipedia.org/wiki/Whistleblower)

• What are the primary functions of a “whistleblower?”

• Alert the public

• Alert law / regulatory enforcement

• Sarbanes-Oxley

• Applies to public companies

• Recognized the current “patchwork” protection for “whistleblowers”

Whistleblower System: Part 2

• FINRA Ombudsman Program

• Corporate Ombudsman Programs

• Anonymous

• Independent from business reporting lines

• Receive data from multiple sources

• Often referred to the Law Department (to preserve privilege)

• Because “whistleblowing” tends to be rare, reports are ad hoc, but will contain basic data about the source, nature of the issue, subject, (i.e. person) of reporting.

Designing a Supervisory System: Part 1

• Conduct an inventory of the businesses in which the firm engages

• Determine the requirements of the applicable securities laws or regulations

• Determine who is responsible for supervising the conduct

• Determine if internal firm policies further curtail conduct beyond regulatory requirements.

• Analyze the data, determine whether any gaps, deficiencies or inaccuracies in the existing supervisory procedures.

Designing a Supervisory System: Part 2

• In conducting this analysis, firms should review whether:

• Has the firm has launched new business lines or products

• Have there been changes in the securities laws and regulations

require revisions to WSPs

• Review customer complaints, litigation, branch office exams, other

internal audits or regulatory issues reported in the media

• The information gleaned from this analysis should be developed into new

or amended supervisory procedures that resolve any identified gaps,

deficiencies or inaccuracies.

* http://www.finra.org/Industry/Issues/SupervisoryControl/P038007

SOCIAL MEDIA FOR FINANCIAL

SERVICES: COMPLIANCE AND RISK

MANAGEMENT

Agenda

•Introduction to Social Media Risk

•Compliance Considerations for your Strategy

•Current regulations apply to social media.

•Business use defines the compliance issues.

•Learn “best practices” from regulators’ use of social media.

INTRODUCTION TO

SOCIAL MEDIA RISK

Risk Environment

Clouds

DevicesCrowds

Propagation and “Going Viral”

• Intra network propagation

• “Like”

• Re-Tweet

• Inter network propagation

• LinkedIn to Twitter

• Twitter to Facebook

• Facebook to the world

• Viral communications

• Advertising

• Sales Material

Single Sign-on for the social net…

Part 1:

Current regulations applyto social media.

FINRA Regulatory Notice 10-06

The old rules apply!

Static Content

Adoption

Entanglement

State Insurance Advertising Regulations

§8513. Disclosure Requirements

A. In connection with any advertising, solicitation, negotiation, or procurement of a universal life insurance policy:

1. any statement of policy cost factors or benefits shall contain:a. the corresponding guaranteed policy cost factors or benefits, clearly identified;b. a statement explaining the nonguaranteed nature of any current interest rates, charges, or other fees applied to the policy, including the insurer's rights to alter any of these factors;c. any limitations on the crediting of interest, including identification of those portions of the policy to which a specified interest rate shall be credited.2. Any illustration of the policy value shall be accompanied by the corresponding net cash surrender value.3. Any statement regarding the crediting of a specific current interest rate shall also contain the frequency and timing by which such rate is determined.4. If any statement refers to the policy being interest indexed, the index shall be described. In addition, a description shall be given of the frequency and timing of determining the interest rate and of any adjustments made to the index in arriving at the interest rate credited under the policy.5. Any illustrated benefits based upon nonguaranteed interest, mortality, or expense factors shall be accompanied by a statement indicating that these benefits are not guaranteed.6. If the guaranteed cost factors or initial policy cost factor assumptions would result in policy values becoming exhausted prior to the policy's maturity date, such fact shall be disclosed, including notice that coverage will terminate under such circumstances.

AUTHORITY NOTE: Promulgated in accordance with Title 22, Section 2 and Title 36, Section 682 of the Insurance Laws of the State of Louisiana.HISTORICAL NOTE: Promulgated by the Department of Insurance, Commissioner of Insurance, LR 11 :690 (July 1985).

SEC: Registered Investment Advisers

§ 275.206(4)-1 Advertisements by investment advisers.

(a) It shall constitute a fraudulent, deceptive, or manipulative act, practice, or course of business within the meaning of section 206(4) of the Act (15 U.S.C. 80b–6(4)) for any investment adviser registered or required to be registered under section 203 of the Act (15 U.S.C. 80b–3), directly or indirectly, to publish, circulate, or distribute any advertisement:

(1) Which refers, directly or indirectly, to any testimonial of any kind concerning the investment adviser or concerning any advice, analysis, report or other service rendered by such investment adviser; or

(2) Which refers, directly or indirectly, to past specific recommendations of such investment adviser which were or would have been profitable to any person: Provided, however, That this shall not prohibit an advertisement which sets out or offers to furnish a list of all recommendations made by such investment adviser within the immediately preceding period of not less than one year if such advertisement, and such list if it is furnished separately: (i) State the name of each such security recommended, the date and nature of each such recommendation (e.g., whether to buy, sell or hold), the market price at that time, the price at which the recommendation was to be acted upon, and the market price of each such security as of the most recent practicable date, and (ii) contain the following cautionary legend on the first page thereof in print or type as large as the largest print or type used in the body or text thereof: “it should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities in this list”; or

(3) Which represents, directly or indirectly, that any graph, chart, formula or other device being offered can in and of itself be used to determine which securities to buy or sell, or when to buy or sell them; or which represents directly or indirectly, that any graph, chart, formula or other device being offered will assist any person in making his own decisions as to which securities to buy, sell, or when to buy or sell them, without prominently disclosing in such advertisement the limitations thereof and the difficulties with respect to its use; or

(4) Which contains any statement to the effect that any report, analysis, or other service will be furnished free or without charge, unless such report, analysis or other service actually is or will be furnished entirely free and without any condition or obligation, directly or indirectly; or

(5) Which contains any untrue statement of a material fact, or which is otherwise false or misleading.(b) For the purposes of this section the term advertisement shall include any notice, circular, letter or other written communication addressed to

more than one person, or any notice or other announcement in any publication or by radio or television, which offers (1) any analysis, report, or publication concerning securities, or which is to be used in making any determination as to when to buy or sell any security, or which security to buy or sell, or (2) any graph, chart, formula, or other device to be used in making any determination as to when to buy or sell any security, or which security to buy or sell, or (3) any other investment advisory service with regard to securities.

(Sec. 206, 54 Stat. 852, as amended; 15 U.S.C. 80b–6)[26 FR 10549, Nov. 9, 1961, as amended at 62 FR 28135, May 22, 1997]

Not Just Advertising…

• Not Just Advertising / Sales Literature

• CAN- SPAM

• State Registration Disclosure / Solicitation

• Fraud

• Pump and Dump

• … all the old issues on a new platform…

… and that’s the good news!

The problem is NOT what rules

apply, but HOW they apply.

Part 2:

Business use defines the compliance issues.

Look who’s talking now!

How do you want to engage?

Brand Awareness / ManagementEducation / Edutainment

ResearchSurveys

Social GoodOperationsRecruiting

Fraud Early WarningIdentify and Respond to Complaints

Virtual Business CardWhite Papers

Build CommunityE-Mail Replacement

Warm LeadsEngage with Gen Y

Collaborate with Clients and Centers of Influence

Part 3:

Learn “best practices” from regulators’ use of social media.

Lessons from the Regulators

Conclusion

•Current regulations apply to social media.

•Business use defines the compliance issues.

•Learn “best practices” from regulators’ use of

social media.

Q&A

LIMRA AND COMPLIANCE 2012Past, Present and Future

Compliance and Regulatory Services

We provide a wide range of products and services to help companies run an effective compliance program and meet today's regulatory scrutiny. We strive to be the trusted source for compliance knowledge and serve the industry through our unique solutions and meetings.

KEY ISSUES AND NEW

DIRECTIONS

Focus

Anti-Money Laundering

• AML Training

• AML Independent Testing

• AML Roundtable

Fiduciary Standards

• Training requirements

• Buy, Sell and Hold Recommendations

NAIC Annuity Regulation

AnnuityXT

LIMRA's AnnuityXT is today's ready solution for meeting your annuity training needs. It gives you the power and control to choose the CE training program you want to use, and the on-demand reporting system allows you and your distributors to monitor and report training status in real time.

Social Media

• NAIC White Paper Comments:

• Draft 1

• LIMRA Member Comments on the First Draft

• Draft 2

• LIMRA Member Comments on the Second Draft

60

New Directions

• Anti-Money Laundering

• Fiduciary Standards

• NAIC Suitability Standards

• Social Media

• …What’s next?

• Industry driven

• Research Supported

• Thought Leaders

61

Q&A

Thank you for your membership!

Thomas Caraher860-285-7873

Stephen Selby 860-285-7858

@limra_crs