state budget update elizabeth grovenstein adam brueggemann office of state budget and management

TRANSCRIPT

State Budget Update

Elizabeth GrovensteinAdam BrueggemannOffice of State Budget and Management

2

Session Etiquette

• Please turn off all cell phones.

• Please keep side conversations to a minimum.

• If you must leave during the presentation, please do so as quietly as possible.

• Thank you for your cooperation!

3

About OSBM: Constitutional & Statutory

State Budget Act & Article III of NC Constitution:• Director of the Budget

– The Governor is required to prepare a recommended budget per NC Constitution (Article III, Section 5(3))

• Budget Development– Required to clearly distinguish program continuation, reductions,

eliminations, expansions, and new programs– Must also contain capital improvements in context of the Six-Year

Capital Improvements Plan required by G.S. 143C-8-6– The Governor must provide a budget message

4

About OSBM: Constitutional & Statutory

State Budget Act & Article III of NC Constitution: • Budget Requirements

– The Governor must present a balanced budget– Budget recommendations must be included for all Governmental and Proprietary Funds

• Administration of the Budget– The Governor administers the budget once it is enacted by the

General Assembly – Administered in accordance with the NC Constitution (Article III,

Section 5(3)) and the State Budget Act– The constitution requires the Governor to take steps necessary to

maintain a balanced budget at all times

5

About OSBM: Organizational Chart

6

About OSBM: Major Functions

Provide fiscal advice to the Governor Prepare Governor’s recommended budget Apply State law and policy in the administration of the budget Publish the State Budget Manual – includes State Budget Act

and policies on budget preparation, administration, travel, and other matters

Forecast and monitor state revenues Conduct management analysis requested by legislature or

agencies Produce official population estimates for state, counties,

municipalities Staff to Council of Internal Audit

7

Budget Development: UNC System

BOG Unified Budget Request GS 143C-3-3(b)

Continuation

- Building Reserves- Enrollment Growth- Annualizations- Remove NR Items

Expansion

- Salary Increases- New Programs- Expand Existing Programs

Capital

- New Construction- R&R- Land Acquisitions

IT

- Acquiring or Maintaining IT Infrastructure

8

Budget Development: BD 307 Certification

9

Budget Development: Post Legislative Summary

10

Budget Administration: Budget Revisions

G.S. 143C-6-4(g) “Transfers or changes within the budget of The University of North Carolina may be provided as in Article 1 of Chapter 116 of the General Statutes.”

11

Budget Administration

11• Certified & Auth.

• Yes

• Change Requirements and Receipts

12• Authorized Only

• Yes

• Change Requirements & Receipts

14

• Authorized Only

• No

• Realign Requirements Only

Revision Type

Impacts

OSBM Approval

Action

12

Budget Administration

When to Use Type 11

•Distribution of Statewide Reserves•Allocation of Agency Reserves •Enrollment Growth•Building Reserves•Reserves in Individual Campus Budgets•Carry Forward – if Statutory or in Session Law•Organizational Budget Changes Mandated by General Assembly – if Statutory or in Session Law•Tuition and Fees Approved by BOG G.S. 116-40.22(c)•Transfers between SRCIs G.S. 116-30.2

13

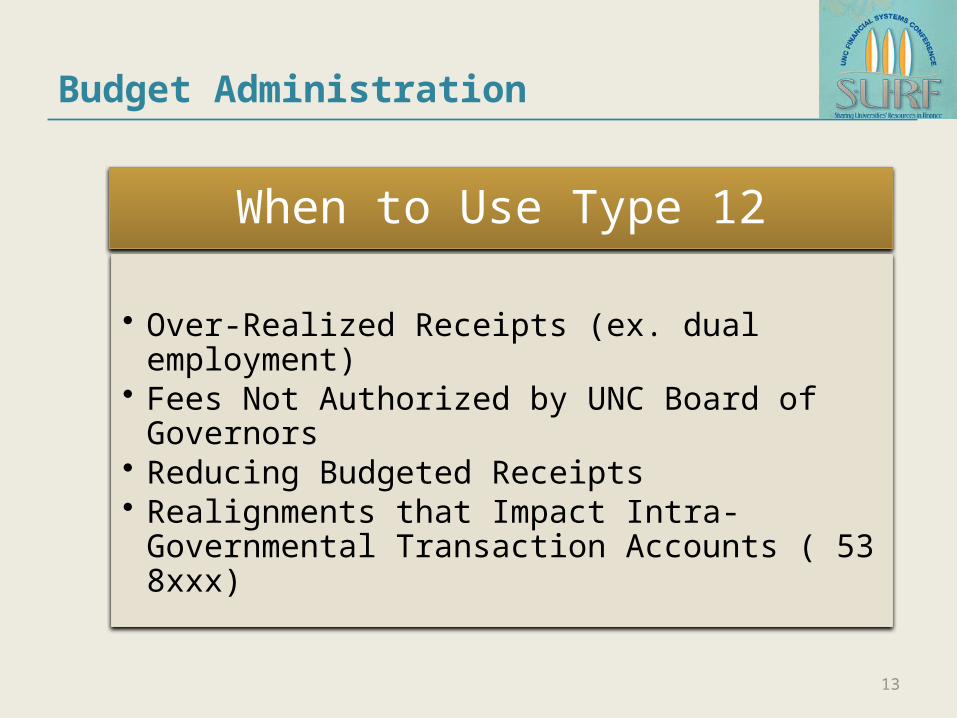

Budget Administration

When to Use Type 12

• Over-Realized Receipts (ex. dual employment)• Fees Not Authorized by UNC Board of Governors• Reducing Budgeted Receipts• Realignments that Impact Intra-Governmental

Transaction Accounts ( 53 8xxx)

14

Budget Administration

When to Use Type 14

• Realignments within or between purpose codes of a budget code

• Excludes Reserves and Intra-Governmental Transactions which must be a Type 12

• Excludes realignments between budget codes which must be a Type 11.

15

Budget Administration

Receipts within UNC System are restricted per G.S. 116-30.3A to a maximum of 10% above certified levels.

OSBM uses IBIS reports and budget/expenditure reports generated by OSC (BD701) to review budget and actuals.

16

Budget Administration: Allotments

G.S. 143C-6-3 “To receive operating funds appropriated to it, a State agency shall submit . . . a request for an allotment of the amount estimated to be required for the ensuing fiscal period.”

G.S. 116-30.2 explains that G.S. 143C-6-3 does apply to appropriations to SRCI’s.

Currently operating allotment requests are made on a monthly basis including payroll and operating funds.

OSBM uses IBIS and also expenditure/allotment reports generated by OSC (BD702).

17

End of Year Procedures: Carry Forward

18

End of Year Procedures: BD 701 Reports

What does OSBM review on the June BD 701?

Cert/Auth Requirements, Receipts, and Appropriation match IBIS (RK 317, 325, 325 reports).

No Negative Budgets at Account Level (Certified & Authorized).

No Over-Expended Line Items (or approved budget pool – see handout).

No Appropriation in Purpose 102 or 103. No Expenditures in Reserve Accounts (71xx NCAS or

83xx FRS)

19

End of Year Procedures: BD 701 Reports

What does OSBM review on the June BD 701?

No Untitled Accounts Carry Forward Transactions Reflected Correctly At least One Dollar Left Unexpended

20

Other OSBM Responsibilities

OSBM promulgates state travel policies and regulations consistent with G.S. 138-5, 138-6, and 138-7, which are applicable to all funds on deposit with the State Treasurer.

OSBM promulgates state moving expenses policies and regulations consistent with G.S. 138-8.

Director of the Budget is authorized to determine when to pay severance wages or discontinued service retirement consistent with G.S. 126-8-5.

21

Other OSBM Responsibilities

G.S. 115C-457.1 establishes the Civil Penalty and Forfeiture Fund to be administered by OSBM.

UNC parking fines are required to be remitted, less the cost of collection as determined annually by OSBM (up to maximum of 20%).

Annual mailing list certification required to be submitted to OSBM per G.S. 143-169.1.

Biennial fee report is required per G.S. 143C-9-4 to be submitted to the General Assembly.

22

NC GEAR

• Review and analysis of efficiency and effectiveness of executive branch

• Staff of 4 time limited/2 permanent employees and outside consulting firm TBD

• Reviewing statutory authority, organizational structure, performance, and funding sources of programs

• Major statewide areas for review include HR, purchasing, IT, parking, motor fleet

• Final report due February 15, 2015• Email suggestions to: [email protected]

23

FY 2014-15 Budget: Next Steps

• February 10, 2014 Budget requests submitted• February 21, 2014 meeting with UNC System• February 11 – April, 2014 OSBM staff review budget

requests, meetings with State Budget Director and Governor’s Office staff, updated revenue estimates

• May 2014 finalize budget recommendations• May 14, 2014 General Assembly convenes

26

Integrated Budget Information System (IBIS)

• Replace mainframe legacy systems by creating an integrated, web-based statewide budget system

• Incorporate program information and performance measurement into the State’s budgeting process

• Improve reporting and analytical capabilities

• Reduce dependency on manual processes for data collection, manipulation and analysis

http://ibis.nc.gov/

27

IBIS Scope

Budget Execution

Budget Development

Program Information

Administrative Features

Budget Revisions Worksheet I Strategic Planning Work Queue

Allotments Worksheet II Program Data My MessagesSalary Control Worksheet III Program

CrosswalkHistory

Certification Reports Program Structure

Journal Entry Reports

Budget CodeFund CodeReports

28

IBIS Work Queue

• Filter and Sort instead of search.• Filter/Sort any field.• Must use 11-0001 format for

budget revisions (not 11-1).• Refine search by applying

multiple filters.• Clear filters by hitting refresh on

browser.• In work queue, right click form

to print.

Strongly Agree

14%

Agree59%

Disagree25%

Strongly Dis-agree

2%

Work Queue Meets Expectations

29

IBIS Work Queue

• Status Field – If left blank, only filters your queue.• Approved = Approved by OSBM• Submitted to OSBM = Approved by Campus, Pending OSBM• Approved Internally = Approved by Campus (ex. Type 14)• All = Any Status (Approved, Returned, Deleted, etc.) • All Active = All Items Pending Action (Excl. approved/deleted)• Validated = Checked for Errors (Does Not Mean Approved) • BRU = Campus (Budget Reporting Unit)• AGENCY = UNC General Administration

30

IBIS Work Queue

31

IBIS Budget Revisions

• Positions Tab – Only the Fund, Account, and FTE

are required.– If Salary is entered, it must be

annual salary.• Budget Detail Tab– Excel Processing feature makes

data entry of numerous accounts easier.

• Attachments Tab– Allows multiple formats (PDF,

Word, Excel)

Strongly Agree17%

Agree73%

Disagree8%

Strongly Disagree

2%

Budget Revision Form Meets Ex-pectations

32

IBIS Budget Revisions

• Using the Excel Processing Feature

33

IBIS Reports

• Frequently Used Reports Available in IBIS – BD 307 Certification– RK 325 Budget Reports– RK 15 Multi-Purpose Report

(Used for Custom Searches)– Under Development: WK1

Strongly Agree10%

Agree52%

Disagree38%

I can find the information I need in IBIS Reports

34

IBIS Reports

• Link to current reports available on IBIS website

35

IBIS Reports

36

IBIS Reports

• RK 15 Multi-Purpose Report – Budget Revision Search Tool– Find All Budget Revisions for a Budget Code, Fund,

or Account– Search Across Multiple Budget Codes, Funds, or

Accounts– Search Across Type 11, 12, and 14– Access from Reports

37

IBIS Reports

• How to Find the RK 15 Multi-Purpose Report

38

IBIS Reports

39

IBIS Reports

• Example of RK 15 Report Output

40

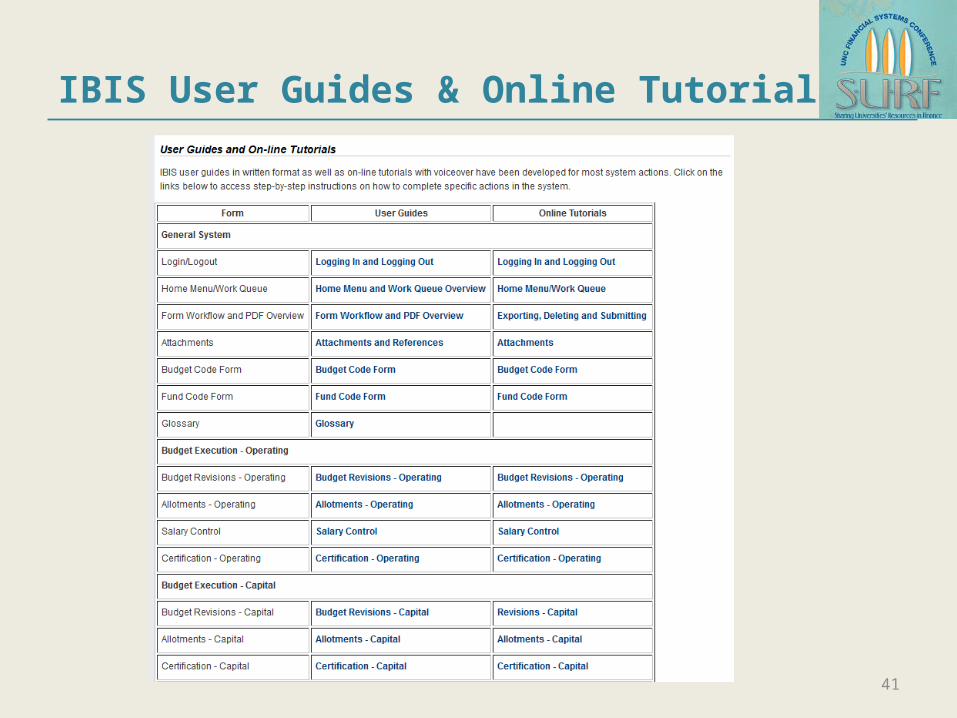

IBIS User Guides & Online Tutorials

41

IBIS User Guides & Online Tutorials

42

IBIS Future Functionality

• Worksheet I – Continuation Budget Prep.• Type 14 Revision Rules– No realignments impacting reserves and intra-

transfer accounts.– No realignment of receipts.

43

Questions & Answers

Thank You!

Elizabeth GrovensteinAdam Brueggemann