standards on regulation, supervision, documentation & financial reporting for iifs kazan summit...

TRANSCRIPT

STANDARDS ON REGULATION, SUPERVISION,

DOCUMENTATION & FINANCIAL REPORTING FOR IIFS

KAZAN SUMMIT 2015Kazan, May 15 th 2015

Prof.Dr.Necdet ŞensoyCentral Bank of the Republic of Turkey

1

2

Disclaimer

The opinions expressed in this presentation are my personal opinions

OUTLINE OF THE PRESENTATION

1. Comparative Overview of the Standard Setters & Standards

2. Some Examples of the Standards

3. Implementation of the Standards

4. Conclusion

5. Appendix – Islamic Standard Setters &Their Products

6. References3

PART 1

Comparative Overview of

the Standard Setters & Standards

4

Importance of Standards

Development, adoption, and

successful implementation of

international standards yields

both national and international benefits

Promote international financial stability

by facilitating better-informed

lending and investment decisions,

improving market integrity5

STANDARD SETTING ORGANIZATIONSFOR AUDITING & FINANCIAL REPORTING

CONVENTIONAL

• IASB International Accounting Standards Board

• IAASB International Auditing and Assurance Standards Board

ISLAMIC

• AAOIFI Accounting and Auditing Organization for Islamic Financial Institutions

6

STANDARD SETTING ORGANIZATIONSFOR REGULATION & SUPERVISION

CONVENTIONAL

BCBS Basel Committee on Banking Supervision

IAIS International Association of Insurance Supervisors

ISLAMIC

IFSB Islamic Financial Services board

7

STANDARD SETTING ORGANIZATIONSFOR REGULATION & UNIFICATION OF MARKETS

CONVENTIONAL

• ISDA International Swaps and Derivatives Association

• International Capital Market Association

• IOSCO The Global Standard Setter for securities markets regulation(IFSB also)

ISLAMIC

IIFM International Islamic Financial Market

8

Capital Adequacy & Liquidity Risk Management

Conventional vs Islamic

9

Capital Adequacy

BASEL III

• A global Regulatory Framework for more resilient Banks and Banking Systems

December 2010 & June 2011

IFSB

• IFSB-15 (2013)

Revised Capital Adequacy Standard for Institutions offering Islamic Financial Services

10

Liquidity Risk Management

BASEL III• International Framework for

Liquidity Risk Management, Standards and Monitoring

December 2010• The Liquidity Coverage

Ratio and liquidity risk monitoring tools January 2013

• The Net Stable Funding Ratio October 2014

IFSB

• Guidance Note -6

Guidance Note on Quantitative Measures for Liquidity Risk Management in Institutions offering Islamic Financial Services ( Excluding Takaful and Islamic Collective Investment Schemes )

April 201511

IFSB & IIFMThe Islamic Financial Services Board (IFSB)

• IFSB is an international standard-setting organisation that promotes and enhances the soundness and stability of the Islamic financial services industry by issuing global prudential standards and guiding principles for the industry, broadly defined to include banking, capital markets and insurance sectors.

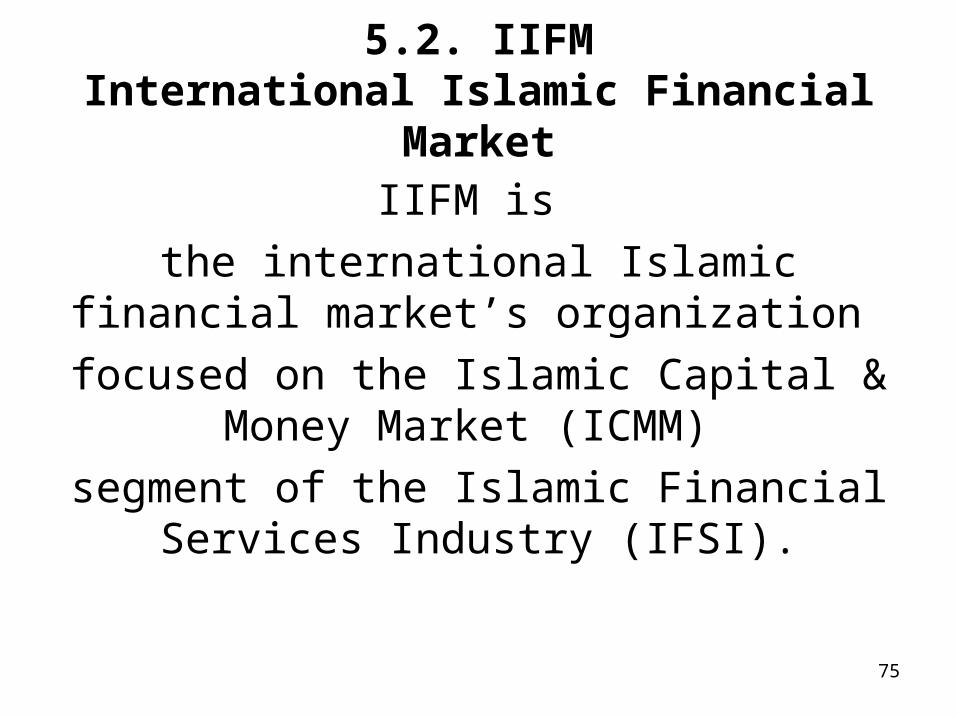

International Islamic Financial Market ( IIFM )

• IIFM is the international Islamic financial market’s organization focused on the Islamic Capital & Money Market (ICMM) & as per recent Board approval scope is extended to Corporate & Trade Finance segments of the Islamic Financial Services Industry (IFSI).

12

STANDARDS FORLIQUIDITY MANAGEMENT BY

ISLAMIC STANDARD SETTERS

IFSB

• IFSB-12 (March 2012)Guiding Principles on Liquidity Risk Management for Institutions offering Islamic Financial Services

IIFM

• IIFM -1 ( 2008 )

Master Agreement for Treasury Placement (MATP) is a global standard documentation published in Islamic Finance for liquidity Management purpose.

13

STANDARDS FORLIQUIDITY MANAGEMENT

IIFM – 5 ( 2013 )• Inter-Bank Unrestricted

Master Investment Wakalah

Agreement (UMWA) specifically designed to provide alternate liquidity management product to the Islamic finance industry in order to reduce over reliance on commodity murabaha based transactions.

14

Master Collateralized Murabaha Agreement (MCMA)

( Published on 16th November 2014 )

provides a mechanism for access to liquidity on a collateralized basis

(based on the Shari’ah principle of Ar’rahn) utilizing Sukuk and other Islamic securities portfolio

as collateral It is an important new tool for IFI’s

as they seek to address the increased global regulatory focus on liquidity and collateral

15

PART 2

Some Examples of the Standards

2.1. IFSB-17

2.2. IIFM interbank unrestricted Master investment wakalah agreement

2.3. AAOIFI Financial Accounting Standard No. 27

«Investment Accounts»

16

2.1. IFSB-17

Core Principles for Islamic Finance Regulation (Banking Segment)

17

Basel Core Principles vs. CPIFR (Banking)

18

9 BCBS Core Principles were transposed to the CPIFR unamended.

19 principles were transposed with some amendments.

The principle of interest rate risk was not transposed due to entire inapplicability.

4 new principles that are unique to Islamic finance institutions were added.

Unique CPIFR principles for IIFS

1. CPIFR 14 - Treatment of Investment Account Holders (IAH)

2. CPIFR 16 - Sharī`ah Governance Framework

3. CPIFR 24 - Equity Investment Risk4. CPIFR 26 - Rate of Return Risk5. CPIFR 32 - Islamic Windows

19

Unique CPIFR principles for IIFS -IAH

CPIFR 14 - Treatment of Investment Account Holders (IAH): “The supervisory

authority determines how IAH are treated in its jurisdiction. The supervisory authority

also determines the various implications (including the regulatory treatment,

governance and disclosures, and capital adequacy and associated risk-absorbency

features, etc.) relating to IAHs within its jurisdiction.”

In the current practice, the treatment of UIAH, under a Mudarabah contract, for

the calculation of CAR varies from jurisdiction to jurisdiction.

Besides, in some countries, IIFS maintain one or both of two types of prudential

reserves, as part of their strategy for mitigating displaced commercial risk: Profit

Equalisation Reserve (PER) and Investment Risk Reserve (IRR).

If the use of such reserves is not adequately controlled by the supervisory

authority, the consequence is an ‘intergenerational’ problem for IAH, since the

existing IAH are disadvantaged against future IAHs.

From the above, the Principle embraces the governance issue for PSIAs as well

as the capital adequacy issues.

20

Unique CPIFR principles for IIFS -UIAH

When Unrestricted Investment Account Holders are treated as Investors :

•Bear all the earning volatility

•Bear Risk of losses except misconduct & negligence in part of the IIFS

•So exclude ASSETS financed bu UIA from denominator of the Capital Adequacy formula

21

Unique CPIFR principles for IIFS -UIAH

When UIAs are treated as a LIABILITY of the IIFS

• IIFS bears the risks of assets funded by IAH

22

Unique CPIFR principles for IIFS

CPIFR 16 - Sharī`ah Governance Framework: “The supervisory authority determines

that IIFS have a robust Sharī`ah governance system in order to ensure an effective

independent oversight of Sharī`ah compliance over various structures and processes

within the organisational framework. The Sharī`ah governance structure adopted by an

IIFS is commensurate and proportionate with the size, complexity and nature of its

business. The supervisory authority also determines the general approach to Sharī`ah

governance in its jurisdiction, and lays down key elements of the process.”

IIFS have to ensure that their products and services comply with Shari`āh rules and principles. For this purpose, IIFS rely on the governance process and internal controls. In all aspects of IIFS operations including products and services, a governance structure, policies and procedures must exist to ensure that the Shari`āh rules and principles are adhered to at all times.

The IFSB’s guiding principles on Sharī`ah governance (IFSB-10) address the components of a sound Sharī`ah governance system, especially with regard to the competence, independence, confidentiality and consistency of Sharī`ah boards.

The supervisory authority should ensure that an IIFS have in place a comprehensive framework dealing with various issues such as hiring and dismissing Sharī`ah scholars, checking accountability and integrity (fit and proper test), and any potential for conflicts of interest.

23

Unique CPIFR principles for IIFS

CPIFR 24 - Equity Investment Risk: “The supervisory authority satisfies itself that adequate policies and procedures including appropriate strategies, risk management and reporting processes are in place for equity investment risk management, including Mudārabah and Mushārakah investments in the banking book (i.e. financing on a profit-and-loss sharing basis), taking into account the IIFS’s appetite and tolerance for risk. In addition, the supervisory authority ensures that the IIFS have in place appropriate and consistent valuation methodologies; define and establish the exit strategies in respect of their equity investment activities; and have sufficient capital when engaging in equity investment activities.”

This principle covers the issues pertaining to the management of risks inherent in the holding of equity instruments including Muḍārabah and Mushārakah investments in the banking book for investment purposes.

The supervisory authority may develop regulatory guidelines for measuring, managing and reporting the risk exposures when dealing with non-performance investments and providing provisions according to the Sharī`ah rules and regulations.

24

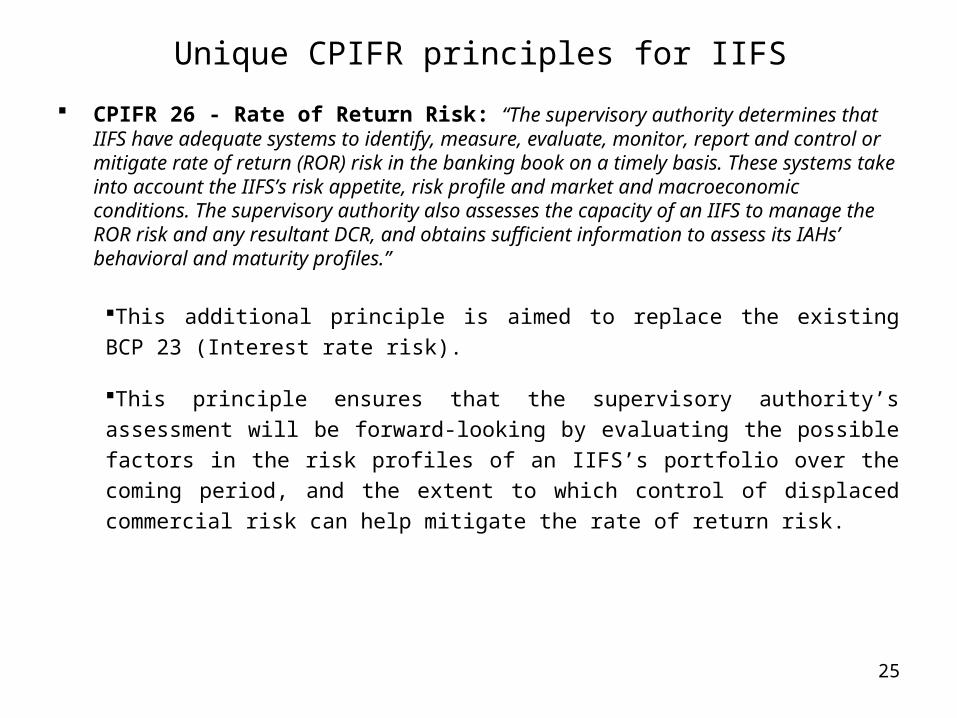

Unique CPIFR principles for IIFS

CPIFR 26 - Rate of Return Risk: “The supervisory authority determines that IIFS have adequate systems to identify, measure, evaluate, monitor, report and control or mitigate rate of return (ROR) risk in the banking book on a timely basis. These systems take into account the IIFS’s risk appetite, risk profile and market and macroeconomic conditions. The supervisory authority also assesses the capacity of an IIFS to manage the ROR risk and any resultant DCR, and obtains sufficient information to assess its IAHs’ behavioral and maturity profiles.”

This additional principle is aimed to replace the existing BCP 23 (Interest rate risk).

This principle ensures that the supervisory authority’s assessment will be forward-

looking by evaluating the possible factors in the risk profiles of an IIFS’s portfolio

over the coming period, and the extent to which control of displaced commercial risk

can help mitigate the rate of return risk.

25

Unique CPIFR principles for IIFS

CPIFR 32 - Islamic Windows: “Supervisory authorities define what forms of Islamic “windows” are permitted in their jurisdictions. The supervisory authorities review Islamic windows’ operations within their supervisory review process using the existing supervisory tools. The supervisory authorities in jurisdictions where windows are present satisfy themselves that the institutions offering such windows have the internal systems, procedures and controls to provide reasonable assurance that: (a) the transactions and dealings of the windows are in compliance with Sharī`ah rules and principles; (b) appropriate risk management policies and practices are followed; (c) Islamic and non-Islamic business are properly segregated; and (d) the institution provides adequate disclosures for its window operations.”

The issue of Islamic banking ‘windows’ is important. Islamic windows are present

in a majority of the IFSB member jurisdictions where Islamic finance is operating

Supervisory practices for regulating Islamic windows, in particular relating to

capital requirements, vary considerably across jurisdictions. This diversity of

windows’ operations raises a number of issues on supervision which are

substantially the same as those raised by fully-fledged IIFS.

This principle covers high level requirements such as governance, risk

management, internal controls, capital adequacy, etc.

26

2.2. IIFM- Interbank unrestricted Master investment wakalah agreement

( IIFM Inter-Bank Unrestricted Master Investment Wakalah Agreement is supplemented with an Operational Guidance Memorandum)

This global standard documentation is developed

to be used in the Islamic inter-bank market between financial institutions

in order to manage their liquidity requirements

The Operational Guidance Memorandum for the Wakalah agreement is one of the unique features of IIFM efforts

to enhance the development of Islamic finance industry.

This Memorandum is very useful whereby it explains how the standard to be used and in addition to that it provides very

comprehensive recommendations

27

IIFM Inter-Bank Unrestricted Master Investment Wakalah Agreement

The Investor, the Muwakkil

will appoint the Wakil as its Agent

to invest its funds in a Shari’ah compliant manner

in exchange for a fee,the Wakalah pool can be managed

on a segregated asset pool or

comingled asset pool basis at the Wakil’s discretion,

early termination which can be caused by the occurrence of default by either party, the calculation treatment of these events

are well defined in this documentation

the Wakil is obliged to notify the Muwakkil if the anticipated profit cannot be achieved etc.,

28

REPO vs. Collateralised murabaha

Conventional repos allow institutions

to lend out assets for short periods

to generate liquidity;

this is disallowed in Islamic finance

as it entails the charging of interest.

Collateral is often lent out by custodians,

a practice known as rehypothecation,

which also contravenes Islamic principles.Even the phrase "Islamic repo" is problematic among scholars who fear

the instruments will simply replicate conventional financial products without addressing a real economic need.

29

REPO vs. Collateralised murabaha

Collateralised murabaha

is a cost-plus profit arrangement which tries to avoid

such issues by having the financier buy the asset at market value and immediately sell the asset to the customer for a mark-up on a deferred payment

basis.

Because the mark-up price is agreed up front by both parties,

this addresses the element of ambiguity, or gharar, a key principle in Islamic finance.

Transactions can be secured by any sharia-compliant assets, including equities and sukuk (Islamic bonds).

The standard expressly forbids rehypothecation.

30

AAOIFI-Financial Accounting Standard No. 27«Investment Accounts» which replaces FAS 5&6

FAS No: 27 Investment Accounts

Updated and Replaced

FAS No: 6 Equity of Investment Account Holders and Their Equivalent

To be in effect for financial periods beginning

1 January 2016

31

Scope of the standard FAS 6

This standard addresses

the accounting rules relating to funds received by the Islamic bank for investment

in its capacity as a mudarib

at the Islamic bank’s discretion,

32

Either in whatever manner the Islamic bank deems appropriate

Equity of unrestricted investment account holders

or

Equity of restricted investment account holders

( subject to certain restrictions )

33

Scope of the standard FAS 27

This standard shall apply to on-balance sheet and off-balance sheet, unrestricted and restricted investment accounts

managed by Islamic Financial Institutions.

34

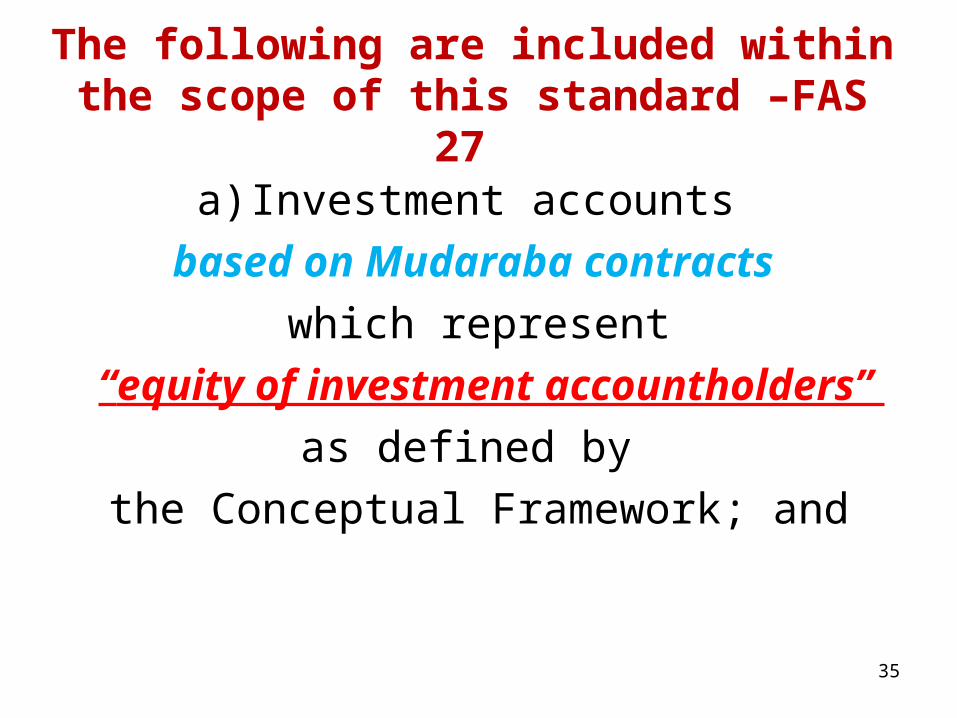

The following are included within the scope of this standard –FAS 27

a) Investment accounts

based on Mudaraba contracts

which represent

“equity of investment accountholders”

as defined by

the Conceptual Framework; and

35

The following are included within the scope of this standard –FAS 27

b) Investment accounts that are

based on Mudaraba contracts

that are placed on

“short term basis”

(overnight, seven days, one month basis)

by other financial institutions

as “interbank-bank deposits”

for the purpose of liquidity management36

An Investment Accountdefined by FAS 27

An account

for the holder of an instrument

under a Mudaraba or its equivalent

representing funds

received by the Islamic Financial Institution for investment

on behalf of the other party (rab al maal)

with or without conditions as regards how the funds may be invested. (Para 3)

37

Profit sharing Mudaraba based investment accounts defined by FAS 27

provides authority over decisions

with regards to the use of and deployment of the funds

received by the Islamic Financial Institution

are treated as

equity of investment accountholders and presented as an on-balance sheet item in the financial statement of Islamic Financial Institution

(Para 4)

38

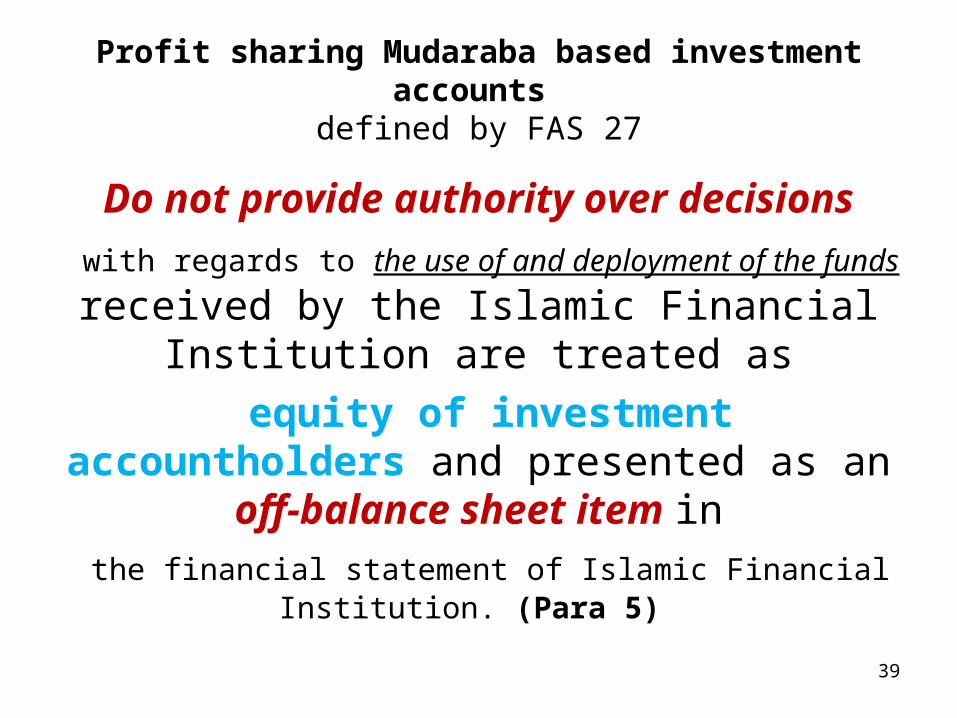

Profit sharing Mudaraba based investment accounts defined by FAS 27

Do not provide authority over decisions

with regards to the use of and deployment of the funds

received by the Islamic Financial Institution are treated as

equity of investment accountholders and presented as an off-balance sheet item in the financial statement of Islamic Financial Institution.

(Para 5)

39

Presentation and disclosure requirements by FAS 6

Disclosure should be made,

in the notes on significant accounts,

of the percentage of the funds of unrestricted investment account holders

which the Islamic bank has agreed with them to invest in order to produce returns for them. (para 15)

40

Presentation and disclosure requirements by FAS 6

Equity of unrestricted investment account holders

shall be presented as

an independent category in the statement of financial position of the Islamic bank

between

liabilities and owners’ equity. (para 16)

41

Information on

equity of restricted investment account holders

shall be presented

in the statement of changes in restricted investments and their equivalent or at the foot of the statement of financial position.

(para 17)

42

Presentation and disclosure requirements by FAS 6

Presentation and disclosure requirementsby FAS 27

Investment Accounts

Equity of on-balance sheet investment accountholders

shall be presented as an independent category

in the statement of financial position

of the Islamic Financial Institution

between liabilities and owners’ equity

(Para 21)

43

Presentation and disclosure requirements by FAS 27

Investment Accounts

Information on equity of

off-balance sheet investment accountholdersshall be presented in

the statement of changes in off-balance sheet investment account and their equivalent

or

at the foot notes of the statement of financial position. (Para 22)

44

PART 3

Implementation of the Standards

3.1. IFSB

3.2. IIFM

3.3. AAOIFI

45

3.1. implementation of IFSB standards

IFSB makes important surveys covering Regulatory and Supervisory Authorities (RSAs) and market players.

The findings of these surveys, which provided a detailed picture of the requirements, intentions and plans of its

members over the medium to long term,

gave a clear indication of the direction of

regulatory reforms in Islamic finance.

In particular, the findings highlighted those areas that the IFSB members feel must be addressed as a priority –

jointly by them and the IFSB – to assist in the all-important objective of standards implementation

46

Implementation of the IFSB Standards

The IFSB members

implement the IFSB’s standards and guidelines

on a voluntary basis.

Each member of the IFSB is entitled to determine its own timeline for implementation based on the market and industry

dynamics in its territory/jurisdiction.

The IFSB undertook its third IFSB Standards Implementation Survey in 2014 (2014 Survey)

to assess the implementation status of

the IFSB standards, with a view to formulating policy recommendations for the implementation process over the

medium to longer term.47

2014 Survey

The number of respondent RSAs was

30 from 22 countries,

which consisted of 21 IFSB full members,

seven associate members, and

two observer members from

Asia, GCC, North Africa and West Africa.

As of end-December 2014,

a total of 16 IFSB standards covering the three sectors of the IFSI – namely, Islamic banking, Takāful and the Islamic capital market – were assessed in the survey

questions.48

The key findings of the 2014 Survey

(a) Banking SectorAll the IFSB standards in the banking sector,

including those issued recently, have been implemented by one or more RSAs

Based on the assessment on 22 RSAs which are supervising the banking sector,

a total of 12 RSAs (55% of respondents) have implemented one or more standards,

2 RSAs (9%) were in the process of implementing them (“in

progress”), and

6 RSAs (27%) were planning to implement the IFSB standards.

49

IFSB-1: Capital Adequacy, IFSB-3:Corporate Governance and

IFSB-4: Disclosure to PromoteTransparency and Market Discipline.

About one-third of respondent bankingRSAs

implemented

Another 15–20% of RSAs were

in the process of implementing them, and

about one third of RSAs were

planning to implement those standards.

50

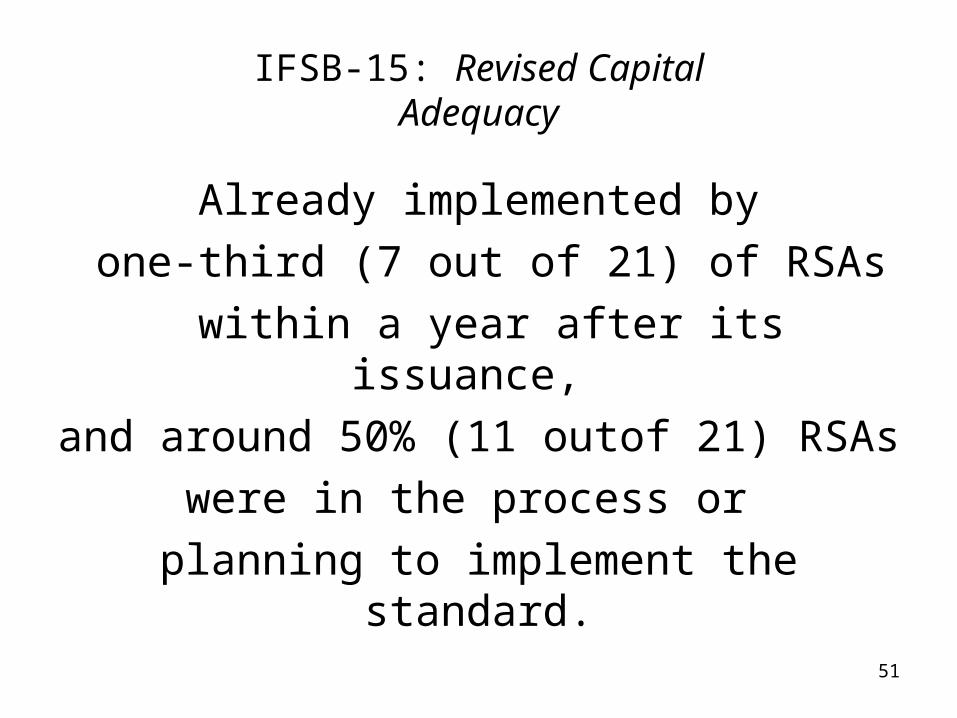

IFSB-15: Revised CapitalAdequacy

Already implemented by

one-third (7 out of 21) of RSAs

within a year after its issuance,

and around 50% (11 outof 21) RSAs

were in the process or

planning to implement the standard.

51

IFSB-13: Stress Testing and IFSB-16: Revised Supervisory Review Process

More than one-fifth of RSAs had implemented

and most of the RSAs indicated that they were

planning to implement those standards.

52

IFSB-12: Liquidity Risk Management

Only IFSB-12: Liquidity Risk Management has a low implementation rate

(9%, or 2 out of 22 RSAs)

however,

another 41% RSAs (9 out of 22)

were in the process of implementing the standard

53

IFSB-2and IFSB-7,

The two IFSB Capital Adequacy Standards for IIFS,

were completely implemented by

70% (7 out of 10 respondent RSAs) and

57% (4 out of 7 respondent RSAs) respectively.

However, the results are not conclusive because

of the low number of responses for these two standards. Since IFSB-2 and IFSB-7 are mainly based on Pillar 1 of

Basel II, only banking RSAs that are adopting Basel II responded to these standards.

54

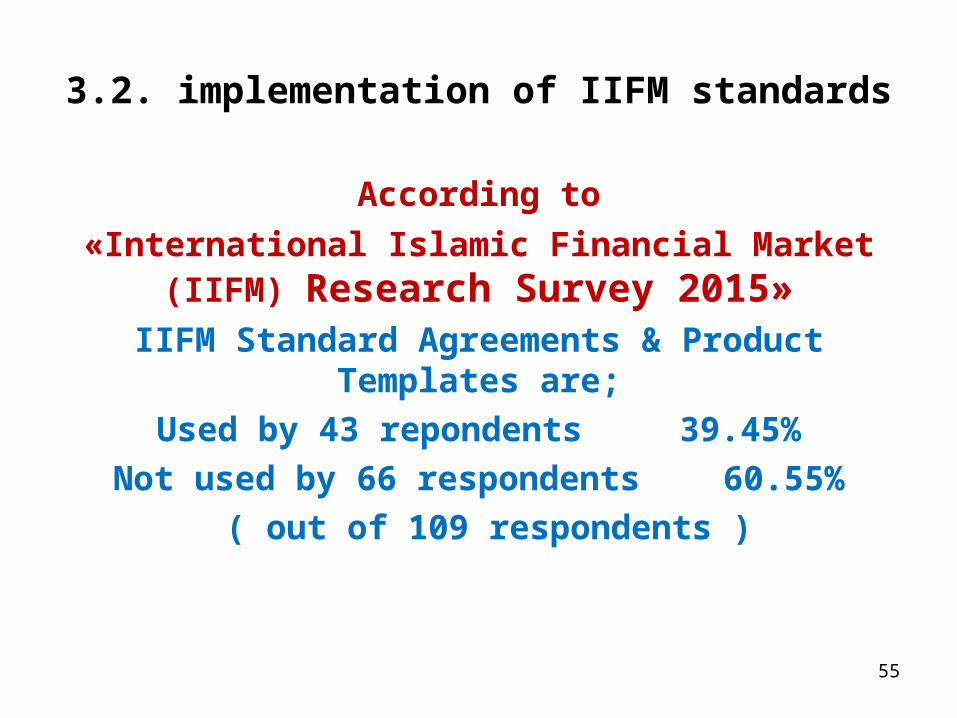

3.2. implementation of IIFM standards

According to

«International Islamic Financial Market (IIFM) Research Survey 2015»

IIFM Standard Agreements & Product Templates are;

Used by 43 repondents 39.45%

Not used by 66 respondents 60.55%

( out of 109 respondents )

55

implementation of IIFM standards

The MCMA Agreement used by 21 respondents 45.65%

The Master Wakalah Agreement used by 22 47.83%

PRS Two Sales Structure used by 08 17.39 %

PRS Single Sale Structure used by 08 21.74%

The TMA Agreement used by 26 56.52%

The MATP Agreement used by 26 56.52%

( Total Respondents 46 )

56

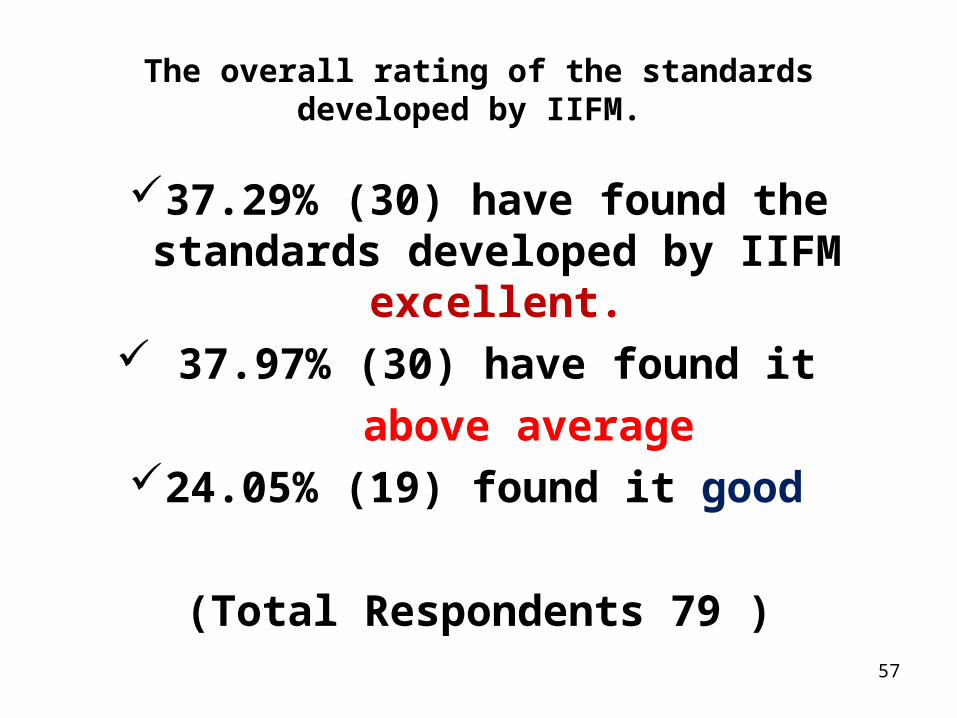

The overall rating of the standards developed by IIFM.

37.29% (30) have found the standards developed by IIFM excellent. 37.97% (30) have found it

above average 24.05% (19) found it good

(Total Respondents 79 )

57

3.3. implementation of AAOIFI standards

AAOIFI has gained assuring support for the implementation of its standards, which are now adopted in the Kingdom of Bahrain, Dubai International Financial Centre, Jordan, Lebanon, Qatar, Sudan and Syria. The relevant authorities in Australia, Indonesia, Malaysia, Pakistan, Kingdom of Saudi Arabia, and South Africa have issued guidelines that are based on AAOIFI’s standards and pronouncements.

58

4. CONCLUSION

Regulation, supervision, documentation and financial reporting are very critical issues

regarding the confidence on Institutions offering Islamic Financial Services

because of the fiduciary relation as well as all other Institutions offering Financial Services

It is a must for Financial Stability to have standards in such issues

Globalization of Islamic Finance by cross border transactions and multinational investments requires high quality standards for having international confidence and

trust on islamic financial instruments and institutions

59

CONCLUSION (cont.)

Parallel to the development of Islamic Finance Industry and its international recognition,

international standard setters on Islamic Finance Industry

are having cooperation with conventional standard setters

Because of the dynamic and inductive nature

of such standards

there is a continuous change depending on the needs of the industry best practices

60

PART 5

Appendix : Islamic Standard Setters & their Products

5.1. IFSB

5.2. IIFM

5.3. AAOIFI

61

5.1. IFSB

Started operations in 2003 The Islamic Financial Services Board (IFSB) is

an international standard-setting organisation

that promotes and enhances the soundness and stability of the Islamic financial services industry

by issuing global prudential standards and

guiding principles for the industry,

broadly defined to include banking, capital markets and insurance sectors.

62

IFSB

• The IFSB also conducts research and coordinates initiatives on industry related issues, as well as organises roundtables, seminars and conferences for regulators and industry stakeholders.

63

IFSB

To this end,

the work of the IFSB complements that of

the Basel Committee on Banking Supervision International Organisation of Securities Commissions and the International Association of Insurance Supervisors.

64

IFSB

As at April 2015,

the 188 members of the IFSB comprise61 regulatory and supervisory authorities, 08 international inter-governmental organisations, and

119 market players (financial institutions, professional firms and industry

associations) operating in 45 jurisdictions.

65

Standards Published by IFSB

• December 2005: IFSB-1: Guiding Principles of Risk Management for Institutions (other than Insurance Institutions) offering only Islamic Financial Services (IIFS)

• December 2005: IFSB-2: Capital Adequacy Standard for Institutions (other than Insurance Institutions) offering only Islamic Financial Services (IIFS)

66

67

December 2006: IFSB-3: Guiding Principles on Corporate Governance for Institutions offering only Islamic Financial Services (Excluding Islamic Insurance (Takâful) Institutions and Islamic Mutual Funds

December 2007: IFSB-4: Disclosures to Promote Transparency and Market Discipline for Institutions offering Islamic Financial Services (excluding Islamic Insurance (Takâful) Institutions and Islamic Mutual Funds)

68

December 2007: IFSB-5: Guidance on Key Elements in the Supervisory Review Process of Institutions offering Islamic Financial Services (excluding Islamic Insurance (Takâful) Institutions and Islamic Mutual Funds)

December 2008: IFSB-6: Guiding Principles on Governance for Islamic Collective Investment SchemesJanuary 2009: IFSB-7: Capital Adequacy Requirements for Sukûk, Securitisations and Real Estate investment

December 2009: IFSB-8: Guiding Principles on Governance for Takâful (Islamic Insurance) Undertakings

December 2009: IFSB-9: Guiding Principles on Conduct of Business for Institutions offering Islamic Financial Services

69

December 2009: IFSB-10: Guiding Principles on Sharîah Governance Systems for Institutions offering Islamic Financial Services

December 2010: IFSB-11: Standard on Solvency Requirements for Takâful (Islamic Insurance) Undertakings

March 2012: IFSB-12: Guiding Principles on Liquidity Risk Management for Institutions offering Islamic Financial Services

March 2012: IFSB-13: Guiding Principles on Stress Testing for Institutions offering Islamic Financial Services

December 2013: IFSB-14: Standard On Risk Management for Takāful (Islamic Insurance) Undertakings

70

December 2013: IFSB-15: Revised Capital Adequacy Standard for Institutions Offering Islamic Financial Services [Excluding Islamic Insurance (Takāful) Institutions and Islamic Collective Investment Schemes]

March 2014: IFSB-16: Revised Guidance on Key Elements In The Supervisory Review Process of Institutions Offering Islamic Financial Services (Excluding Islamic Insurance (Takāful) Institutions and Islamic Collective Investment Schemes)

April 2015 IFSB-17

Core Principles for Islamic Finance Regulation (Banking

Segment)

71

Guidance Notes by IFSB • March 2008: GN-1: Guidance Note in Connection

with the Capital Adequacy Standard: Recognition of Ratings by External Credit Assessment Institutions (ECAIs) on Sharî'ah-Compliant Financial Instruments

• December 2010: GN-2: Guidance Note in Connection with the Risk Management and Capital Adequacy Standards: Commodity Murâbahah Transactions

72

73

March 2011: GN-4: Guidance Note in Connection with the IFSB Capital Adequacy Standard: The Determination of Alpha in the Capital Adequacy Ratio for Institutions (other than Insurance Institutions) offering only Islamic Financial Services March 2011: GN-5: Guidance Note on the Recognition of Ratings by external Credit Assessment Institutions (ECAIS) on Takâful and ReTakâful Undertakings

December 2010: GN-3: Guidance Note on the Practice of Smoothing the Profits Payout to Investment Account Holders

74

Technical Notes by IFSB

TN-1: Technical Note on Issues in Strengthening Liquidity Management of Institutions Offering Islamic Financial Services: The Development of Islamic Money Markets

5.2. IIFMInternational Islamic Financial Market

IIFM is

the international Islamic financial market’s organization

focused on the Islamic Capital & Money Market (ICMM)

segment of the Islamic Financial Services Industry (IFSI).

75

IIFM

Founded in 2002 by

Islamic Development Bank,

Autoriti Monetari Brunei Darussalam,

Bank Indonesia,

Central Bank of Bahrain,

Central Bank of Sudan and

the Bank Negara Malaysia (delegated to Labuan Financial Services Authority)

as a neutral and non-profit organization.

76

IIFM

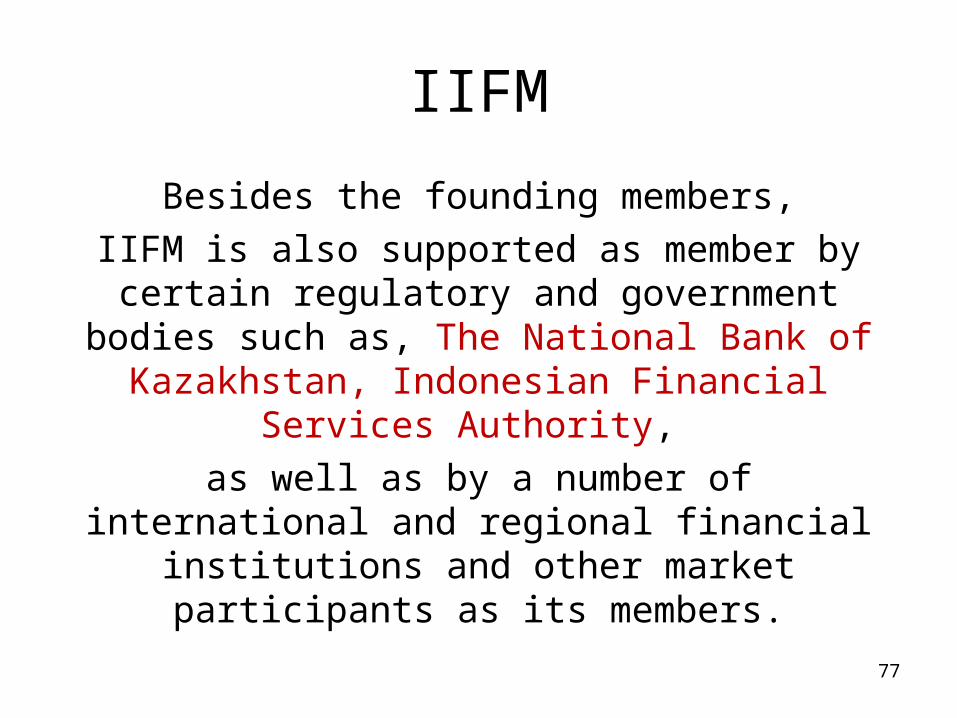

Besides the founding members,

IIFM is also supported as member by certain regulatory and government bodies such as,

The National Bank of Kazakhstan, Indonesian Financial Services Authority,

as well as by a number of international and regional financial institutions and other

market participants as its members.

77

Expanded IIFM scope of work (only standard setting organization which develop standardized Islamic

financial contracts and product templates )

In addition to existing focus of

Capital & Money Market standard agreements and products templates.

Included

Corporate Finance & Trade Finance segment

This to further enhance the development of Islamic financial industry globally through its documentation and Islamic

products unification efforts which are much needed for a robust, transparent and vibrant industry.

78

Producing standard documentation by IIFM

IIFM has taken a pioneering role

in producing standard documentation

in specific areas for the Islamic finance industry

in order to provide Shari’ah harmonization,

best practices, transparency and clarity for sound business activities

79

Published Standards by IIFM

1. IIFM Master Collateralized Murabahah Agreement

2. IIFM Reference Paper on I’aadat Al Shira’a (Repo Alternative) and Collateralization

3. IIFM Standard Agreements Adaptation Procedures & Policies for Institutions

4. IIFM Standard on Interbank Unrestricted Master Investment Wakalah Agreement

5. ISDA/IIFM Mubadalatul Arbaah (MA) (Profit Rate Swap)

6. ISDA/IIFM Tahawwut (Hedging) Master Agreement (TMA)

7. Master Agreement for Treasury Placement (MATP)

80

IIFM Guidances

Operational Guidance Memorandum For International Islamic Financial Market (IIFM) Interbank Unrestricted Master Investment Wakalah Agreement

Master Collateralized Murabahah Agreement Opretatıonal Guidance Memorandum

81

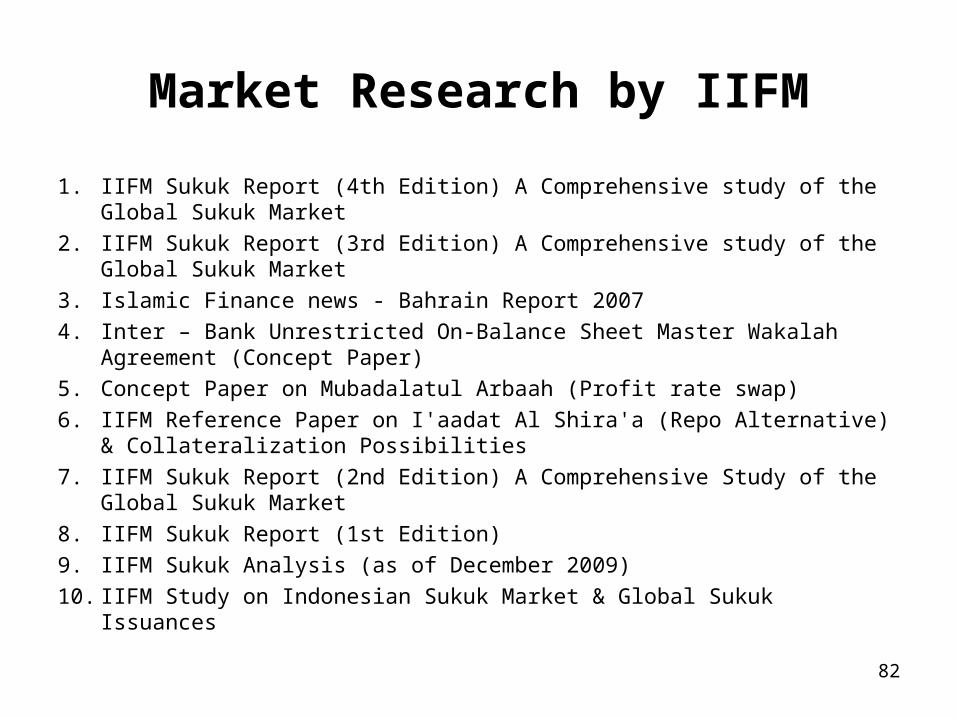

Market Research by IIFM

1. IIFM Sukuk Report (4th Edition) A Comprehensive study of the Global Sukuk Market

2. IIFM Sukuk Report (3rd Edition) A Comprehensive study of the Global Sukuk Market

3. Islamic Finance news - Bahrain Report 2007

4. Inter – Bank Unrestricted On-Balance Sheet Master Wakalah Agreement (Concept Paper)

5. Concept Paper on Mubadalatul Arbaah (Profit rate swap)

6. IIFM Reference Paper on I'aadat Al Shira'a (Repo Alternative) & Collateralization Possibilities

7. IIFM Sukuk Report (2nd Edition) A Comprehensive Study of the Global Sukuk Market

8. IIFM Sukuk Report (1st Edition)

9. IIFM Sukuk Analysis (as of December 2009)

10. IIFM Study on Indonesian Sukuk Market & Global Sukuk Issuances

82

83

84

5.3. AAOIFI

The Accounting and Auditing Organization for Islamic Financial Institutions(AAOIFI) is

an Islamic international autonomous non-for-profit corporate body that prepares accounting, auditing,

governance, ethics and Shari'a standards for Islamic financial institutions and the industry.

Professional qualification programs (notably CIPA, the Shari’a Adviser and Auditor "CSAA", and the corporate

compliance program) are presented now by AAOIFI in its efforts to enhance the industry’s human resources base

and governance structures.

85

AAOIFI

As an independent international organization,

AAOIFI is supported by institutional members (200 members from 40 countries, so far)

including

central banks,

Islamic financial institutions, and

other participants from the international Islamic banking and finance industry, worldwide.

86

STANDARDS BY AAOIFI «Accounting and Auditing Organization for Islamic Financial Institutions» promulgated 5 group of Standards :

1.Sharia Standards

2.Accounting Standards

3.Auditing Standards

4.Governance Standards

5.Ethics Standards

87

88

89

90

91

92

6.REFERENCES

• Web site of Islamic Financial Services Board ( IFSB) , www.ifsb.org• Islamic Financial Services Industry Stability Report by IFSB, 2015• Web site of AAOIFI, www.aaoifi.com • Web site of IIFM, www.iifm.net • Adel Mohammed Sarea, The Level of Compliance with AAOIFI

Accounting Standards: Evidence from Bahrain• International Islamic Financial Market (IIFM) Research Survey

Questionnaire, Results & Analysis (the Report), April 2015

93