stainless steel a bright future in a changing world ppg may 2012

DESCRIPTION

ISSF_2011_Sustainability_Case_StudieTRANSCRIPT

1

Stainless steel a bright future

in a changing world?BIR World Annual Conference

RomeMay 30 , 2012

Pascal PAYET-GASPARDSecretary General ISSF

2

Agenda

Stainless steel: short term perspectives An industry facing many challenges … but a bright long term future Conclusions

3

Agenda

Stainless steel: short term perspectives An industry facing many challenges … but a bright long term future Conclusions

4

Since 1980 stainless steel has grownfaster than most metallic materials

0

100

200

300

400

500

600

1980 1985 1990 1995 2000 2005 2010

Galvanized Steel

Stainless Steel

Aluminium

Carbon Steel

Long term evolution of the world consumption of stainless steel and substitutes CAGR 80 - 10

6,0 %

4,6 %

4,0 %

2,3 %

Historically, stainless steel growthwas much stronger than carbon steel growth, a fact that led to the perceptionthat stainless steel was « different » andimmune to the woes of « ordinary » steel

Source, ISSF, Laplace Conseil

5

However, since 2006, stainless steelhas under-performed its competition

80

100

120

140

160

180

200

2000 2002 2004 2006 2008 2010

Galvanized steel

Stainless Steel

Aluminium

Carbon Steel

Recent evolution of the world consumption of stainless steel and substitutesCAGR 00 - 10

5,6 %5,6 %5,3 %5,0 %

Recession started two yearsearlier for stainless steeland was much deeper; 2010recovery is much stronger

Source, ISSF, Laplace Conseil

6

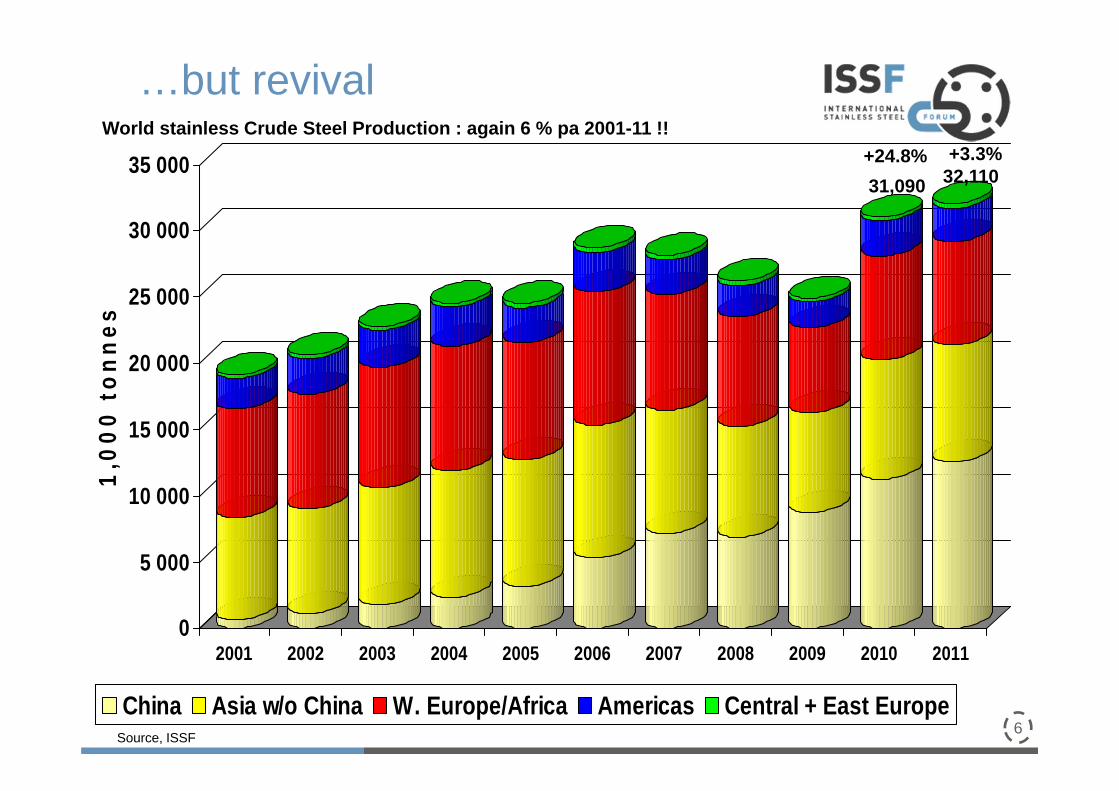

0

5 000

10 000

15 000

20 000

25 000

30 000

35 000

1,0

00

to

nn

es

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

China Asia w/o China W. Europe/Africa Americas Central + East Europe

+24.8%31,090

+3.3%32,110

World stainless Crude Steel Production : again 6 % pa 2001-11 !!

Source, ISSF

…but revival

7

Agenda

Stainless steel: short term perspectives An industry facing many challenges … but a bright long term future Conclusions

8

China accounts for all the growthsince 2000

World Stainless Steel production (Million tonnes of crude steel)

0

5

10

15

20

25

30

35

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Europe

North America

Other Asia

China

Other Countries

CAGR 00-10Total +5%

+34 %

0 %

0 %

+0 %

+2 %

Source, ISSF, Laplace Conseil

9

Since 2000 most of the stainless growthis attributable to S200 & S400

Stainless steel production by grade (Million tonnes of crude steel)

0

5

10

15

20

25

30

35

2000 2002 2004 2006 2008 2010

S300

S400

+5,0 %

2,5 %

6,2 %

28,4 %

S200

CAGR 00 - 10

S300 has declined in all regionof the world outside China

Source, ISSF, Laplace Conseil

10

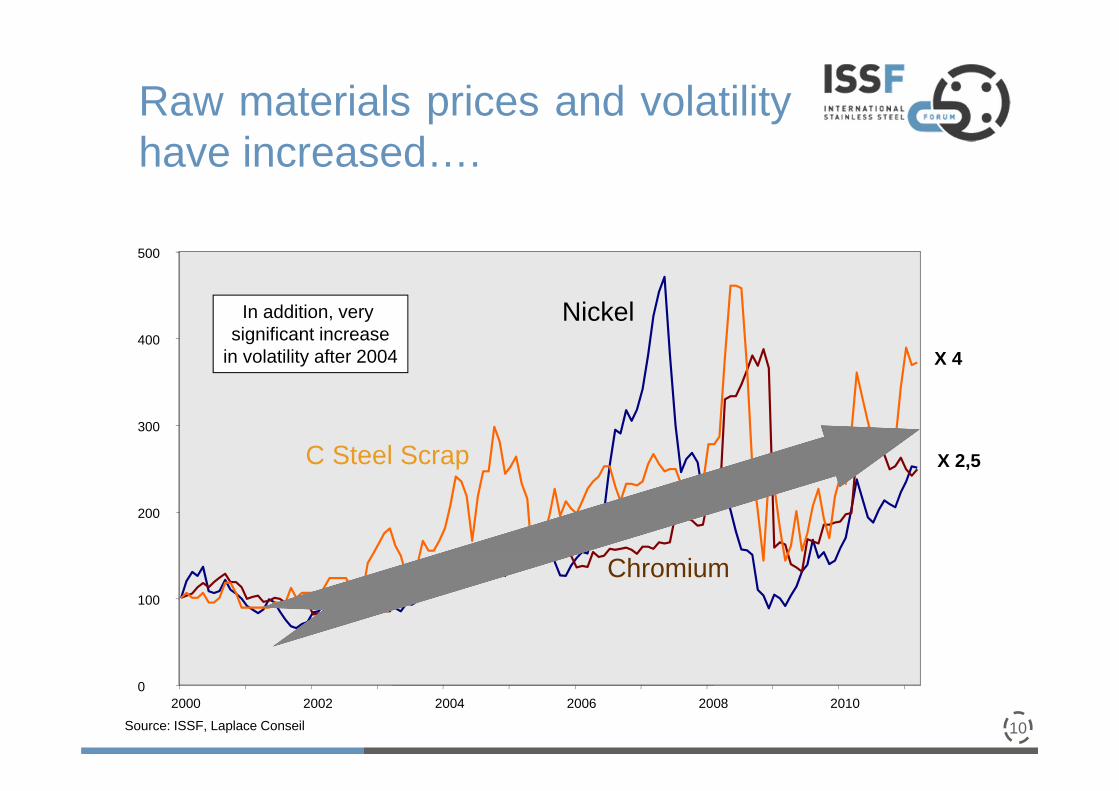

Raw materials prices and volatilityhave increased….

X 4

X 2,5

0

100

200

300

400

500

2000 2002 2004 2006 2008 2010

In addition, very significant increase

in volatility after 2004

C Steel Scrap

Nickel

Chromium

Source: ISSF, Laplace Conseil

11

… combined with margins squeeze …

190

-310-340

-400

-300

-200

-100

0

100

200

300

2000 2010

230

-140-170

2000 2010

50 €/yr2,1%/yrof average price

37 €/yr2,8%/yrof averge price

Factor costincrease

Transformation margin decrease(net of scrap)

Price cost squeeze for 304 SS (€/t) Price cost squeeze for 430 SS (€/t)

Factor costincrease

Transformation margin decrease(net of scrap)

12

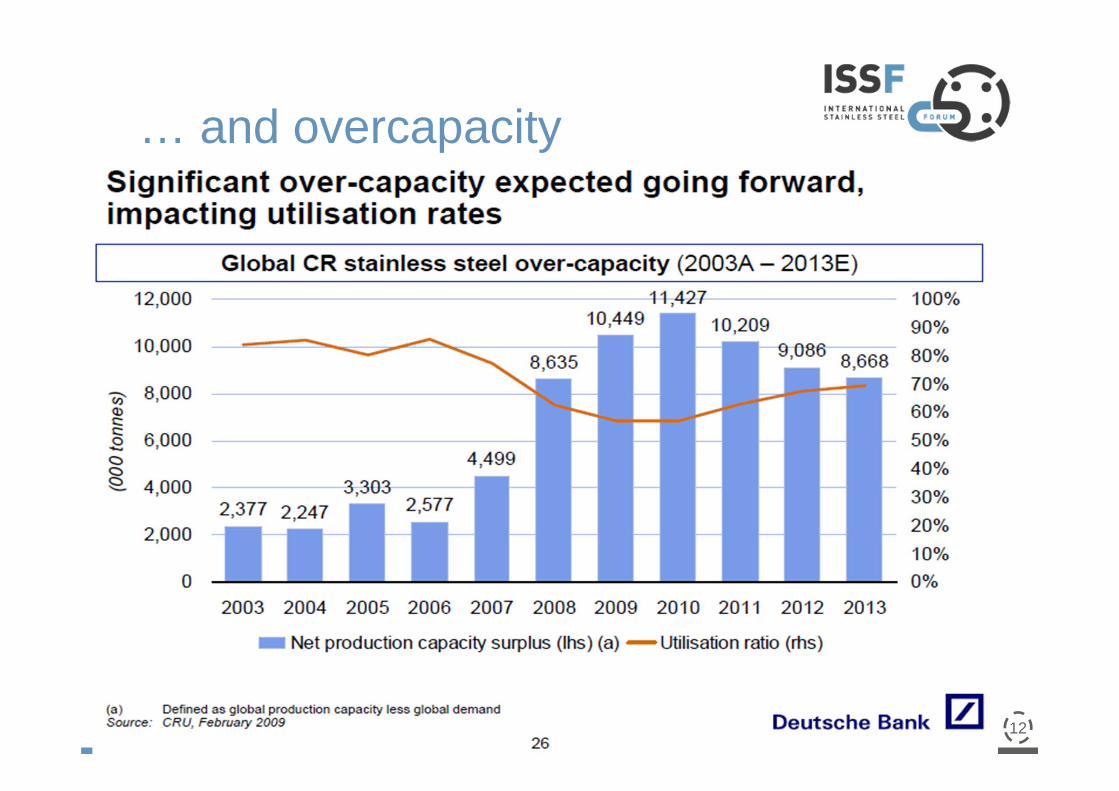

… and overcapacity

CRU World Stainless Steel Conference, 6-7 February 2012

13

Source : SMR, 2010

Top 20 stainless steel companies

14

Profit

15

What have been the reactionsof the producers? Cut costs, improve productivity by using latest

technologies Close inefficient mills (Europe-Americas) Look for cheaper raw materials :

– Nickel Pig Iron (China)– Backward integration (Asia)

Integrate into distribution to better control downwards supply chain (Europe, Asia, Americas)

Move to higher, value added products or margins: 400 series, duplex, 316 etc…

For integrated mills, split the stainless business: Aperam, Inoxum

16

Agenda

Stainless steel: short term perspectives An industry facing many challenges … but a bright long term future Conclusions

17

India: the next after China?

Source: SMR 2010

18

Price of competing materials2000-2010: stainless doing well !!

steel

Al

Source, ISSF

St st

19

An industry constantly growingin size and efficiencyConsidering the 4 largest world companies in stainless steel melting production

with fully integrated stainless steel shops , hot rolling mills and a clear shift to Asia

2000: Over 1 Mt 34% of the market2005: Over 1.5 Mt 32% of the market2012 (e): Over 3 Mt 38% of the market

20

The raw material challenge

Nickel Pig Iron: more an opportunity than a threat? – a ceiling to the price of nickel– a regulation to the S/D balance

Chrome– an available resource with high productivity and low

cost producers coming up LME: a tool to be positively used !!

– an opportunity to better pilot the raw material volalility … but a market still to be better regulated and more transparent

21

7.0%

17.1%9.4%

0.6%38.9%

27.0%

NiCrMoothersElectricityDirect emissions

0.65ton CO2/ton SS

0.36ton CO2/ton SS

Raw materials total 2.80ton CO2/ton SS

A sustainable material

The stainless steel industry itself contributes directly for less than 10 % of total emissions

Most of the emissions are coming from upstream: raw materials and electricity generation

Stainless steels compare favorably to competing materials Al,Cu,Mg

Total 3,81 ton CO2/ ton SS

Source: ISSF, SCM

CO2 emission from cradle to grave without the recycling credit which is around 1ton CO2/ton

22

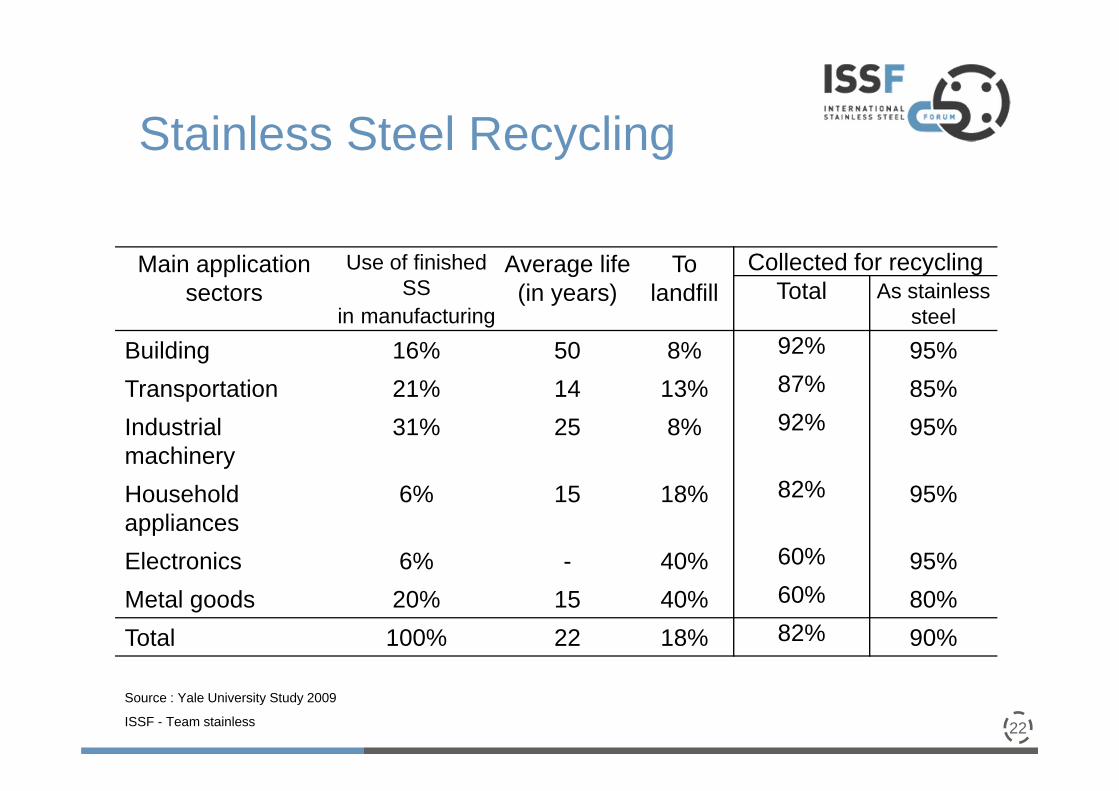

Stainless Steel Recycling

Main applicationsectors

Use of finished SS

in manufacturing

Average life(in years)

To landfill

Collected for recyclingTotal As stainless

steelBuilding 16% 50 8% 92% 95%Transportation 21% 14 13% 87% 85%Industrial machinery

31% 25 8% 92% 95%

Household appliances

6% 15 18% 82% 95%

Electronics 6% - 40% 60% 95%Metal goods 20% 15 40% 60% 80%Total 100% 22 18% 82% 90%

Source : Yale University Study 2009

ISSF - Team stainless

23

Stainless Steel Recycling:over 80 %!

2005Source : Yale University Study 2009

ISSF - Team stainless

24

Chrysler Building, 1930

Catherine Houska for Nickel Institute

Stainless steel has been used as an architectural material since about 1930.

25

Sustainable applications: Bio-Gas

• Bio Gas plant

• Severe corrosion conditions

• Low maintenanceSource :Kosa/ISSF Book of New Applications316Ti grade

26

High strength, corrosion resistance – Long lifeSource: Outokumpu Oyj/ ISSF Book of New Applications (grade SAF2205(Duplex)

Stainless Steel BridgeStockholm

27

Agenda

Stainless steel: short term perspectives An industry facing many challenges … but a bright long term future Conclusions

28

A bright future

Despite current difficulties shared by many heavy industries, the stainless steel industry has a bright future: – Potential growth in emerging countries is enormous– In sustainability, stainless steels are unmatched compared to

other materials– The industry is now catching up with overcapacity and

restructuring measures Public authorities should recognise these intrisinsic

properties and help the industry :– to restructure itself – to adopt free and fair trade practices – to improve the raw materials markets transparency and avoid

excess volatility which damages its long term growth and profitability

29

Thank you for your attention!