spv and aif in europe: possible advantages for polish ...€¦ · spv and aif in europe: possible...

TRANSCRIPT

SPV and AIF in Europe:

Possible advantages for

Polish asset managers

Poland 2015

Agenda

WHAT ADVANTAGES CAN ARISE FOR POLISH ASSET MANAGERS/CLOSED-ENDED FUNDS FROM CREATING SPVS/PARTNERSHIPS IN FOREIGN JURISDICTIONS (E.G., LUXEMBOURG)

1. Possible ways/reasons for using Luxembourg SPVs/Partnerships

2. Legal and operational aspects

3. Main advantages for Polish asset managers

POSSIBLE IMPLEMENTATION OF AIFMD IN LUXEMBOURG

1. Introduction: preview of funds organisation pre AIFM

2. Few words on AIFMD

3. Reasons to have recourse to a third party AIFM

4. Advantages for managers to use a third party AIFM

WHAT ADVANTAGES CAN ARISE FOR POLISH ASSET MANAGERS/CLOSED-ENDED FUNDS FROM CREATING SPVS/PARTNERSHIPS IN FOREIGN JURISDICTIONS (E.G., LUXEMBOURG)

1. Possible ways/reasons for using Luxembourg SPVs/Partnerships

2. Legal and operational aspects

3. Main advantages for Polish asset managers

4

Before 1/1/2014 or before 10/2015 After 1/1/2014 or after 10/2015

(grandfathering rules) (grandfathering rules)

Closed-end fund

(Polish LP)

SKA

Commercial

business in

Poland

HoldCo

Tax Exempt

Tax Exempt

Closed-end fund

(Polish LP)Tax Exempt

SKA Tax Exempt

HoldCo

Commercial

business in

Poland

Possible ways/reasons for using Luxembourg

SPVs / Partnerships 1

5

Possible ways/reasons for using Luxembourg

SPVs / Partnerships 2Closed-end fund

(Polish LP) Tax Exempt

Luxembourg

SCS/SCSp

LuxGP

Polish partnership Tax Exempt

HoldCoCommercial

business in

Poland

Tax Exempt

Legal and operational aspects

7

Legal considerations

• Existence: as of the date of the LPA

• Domicile: located at the place of its central administration

• Share capital : no minimum share capital requirement

• Registration of the SCSp with the Luxembourg RCS

• LPA may be concluded as under private seal; no requirement of a notary

• Shareholding: one or more general partners and one or more limited partners

• Publication: identity of the partners and amounts contributed remain confidential and are

not subject to publication; only excerpts of the LPA are published

• Liability: general partners are indefinitely, jointly and severally liable; Limited partners are

liable up to the amount paid up and/or committed

• Contributions: in cash or in kind or in industry

• Can be regulated (with CSSF approval) or unregulated

• Securities: shares or interests

8

Accounting & Audit

• No obligation to keep annual accounts in accordance with the requirements of the commercial code

• No publication of the annual accounts

• No audit required

• For regulated SCSps: financial statements Lux GAAP or IFRS

• For unregulated SCSps: relative freedom to decide the accounting rules to be used

9

Taxation of SCSp : Tax transparency

Taxation of foreign investors :

• Capital duty upon contribution: not applicable

• Corporate income tax: not applicable

• Municipal business tax: not applicable if

• no commercial activity; and

• the Luxembourg general partner incorporated under the form of a commercial company

holds less than 5% of the SCSp interest

• Net wealth tax: not applicable

• Dividend withholding tax: not applicable

• Tax treaties: not applicable. However, tax treaties concluded between the country where

the assets are located and the investors might be applicable

Main advantages for Polish asset managers

11

Main advantages for Polish asset managers

• Suitable for structuring joint ventures, SPVs as well as open-ended funds and closed-ended funds

• Efficient for private equity/real estate transactions where tax transparency is required at the level of

the partnership

• Listing permitted

• Possibility to be concluded under private seal with limited information published on the LPA and the

identity of the limited partners

• Highly sophisticated and flexible contractual regime: possibility to govern admission of limited partners,

transfer of partnership interests, allocation of profit or losses, …

POSSIBLE IMPLEMENTATION OF AIFMD IN LUXEMBOURG

1. Introduction: preview of funds organisation pre AIFM

2. Few words on AIFMD

3. Reasons to have recourse to a third party AIFM

4. Advantages for managers to use a third party AIFM

13

Introduction: preview of funds organisation pre AIFM

INVESTORS

SIF

COMP 2COMP 1 COMP 4COMP 3

ASSETS

Investment Advisor(optional)

Investment Manager

(optional)

Central Administrator

Custodian

Auditor

Legal Advisor

14

Few words on AIFMD

The Alternative Investment Fund Managers Directive (AIFMD) is one of the major EU regulatory

initiatives to extend regulation and supervision to the alternative investment fund management industry.

The AIFMD applies to the managers of AIFs. Therefore it is not the fund that is regulated by AIFMD,

only the manager of the AIF.

An AIF is defined as an undertaking that (1) raises capital (2) from a number of investors (3) with a view

to investing that capital for the benefit of those investors (4) in accordance with a defined investment

policy.

Exemptions examples: holding companies, joint ventures, SVs, supra national bodies,…

An AIFM will provide portfolio management and/or risk management services to AIFs. The AIFM can

either be an external manager appointed by or on behalf of the AIF, or the AIF itself.

Thresholds : EUR100M (leveraged) / EUR500M (unleveraged and closed ended for 5 years)

15

Reasons to have recourse to a third party AIFM

You may need a third party AIFM for various reasons such as:

- being above the thresholds (EUR100 M (leveraged) / EUR500 M (unleveraged and closed ended for 5 years))

- perform the investment management function, which is split in two: portfolio and risk management

- access the EU marketing passport and to manage and sell in Europe non EU AIFs

Further the AIFM:

- provides AIF governance (AIFM Board which will report on a regular basis to the AIF Board)

- provides AIF substance (AIFM has dedicated conducting officers)

- provides AIF operation control (AIFM holds the risk management and compliance functions and supervises

service providers)

- ensures investors to receive regular and comprehensive information on the AIF they invest in

- ensures regulators to receive detailed information on AIF and AIFM to enable them to identify any potential

systemic trends or events that may impact market stability

16

Advantages for managers to use a third party AIFM

• Takes away HR matters

• Specialized and skilled professionals who may provide better quality and faster results

• Tools and systems in place in order to reduce errors

• Field experience (most of the problems have been handled before)

• Legal, compliance and regulatory follow up/alerts

• Market knowledge

• Economies – it is less expensive as a whole dedicated team and infrastructure

• Centralized supervision of operations such as CA, TA, domiciliation, depositary services

17

INVESTORS

SIF

COMP 2COMP 1 COMP 4COMP 3

ASSETS

Investment Advisor(optional)

Investment Manager

(optional)

Central Administrator

Custodian

Auditor

Legal Advisor

18

Operational structure for a Luxembourg domiciled AIF using a third party AIFM

Investors / Initiators /

Shareholders

Investment Company / AIFBoard of Directors

MANAGEMENT COMPANY / AIFM

Risk Management

Marketing Passeport

Portfolio

Management

Compliance / Int. audit

Conflict & complaints

Valuation

Oversight of delegates

Custodian/

Depositary

Legal Advisor

Auditors

Other Advisors, Brokers …

Central Administrator

NAV calculation

Assets valuation

TA

KYC & AML

Monitor investment restrictions (optional)

Investment Manager /Investment Advisor

Manages the

portfolios in

accordance with the

investment

restrictions /

regulations

Pre- NAV eligibility

tests

Global Distributor /

Placement Agent

Appoints and oversees the

sub distributors

: appointed by

Investment

Advisor

: delegating scheme

AIFMD – third country AIFMs

Presented by Jane Pearce

MD Vistra Jersey

Warsaw - 3 November 2015

Agenda

1. Introduction – What is the industry facing?

2. Regulatory impact – key questions

3. Onshore vs Offshore

4. New operating conditions for AIFMs and their administrators

5. Three models for Jersey/other third country AIFMs

6. Private Placement into the EEA under NPPRS

7. Substances consequence

8. Parallel Fund Structures

9. ESMA Advice and Opinions issued on 30 July

What is the industry facing?

AIFMD

Impact on Operations for Managers

Separation of risk and portfolio management

Regulatory capital requirements

Raising Capital

Pre-sale disclosure

Registering for private placement

Annex IV reporting

PE specific restrictions

Tax…BEPS and carry taxation

Key questions – minimise regulatory impact?

Are you managing an AIF?

Where are you managing?

Where are you marketing?

Single asset structure (capital raising?)

The rise of the managed account

The offshore response

Passporting?

24

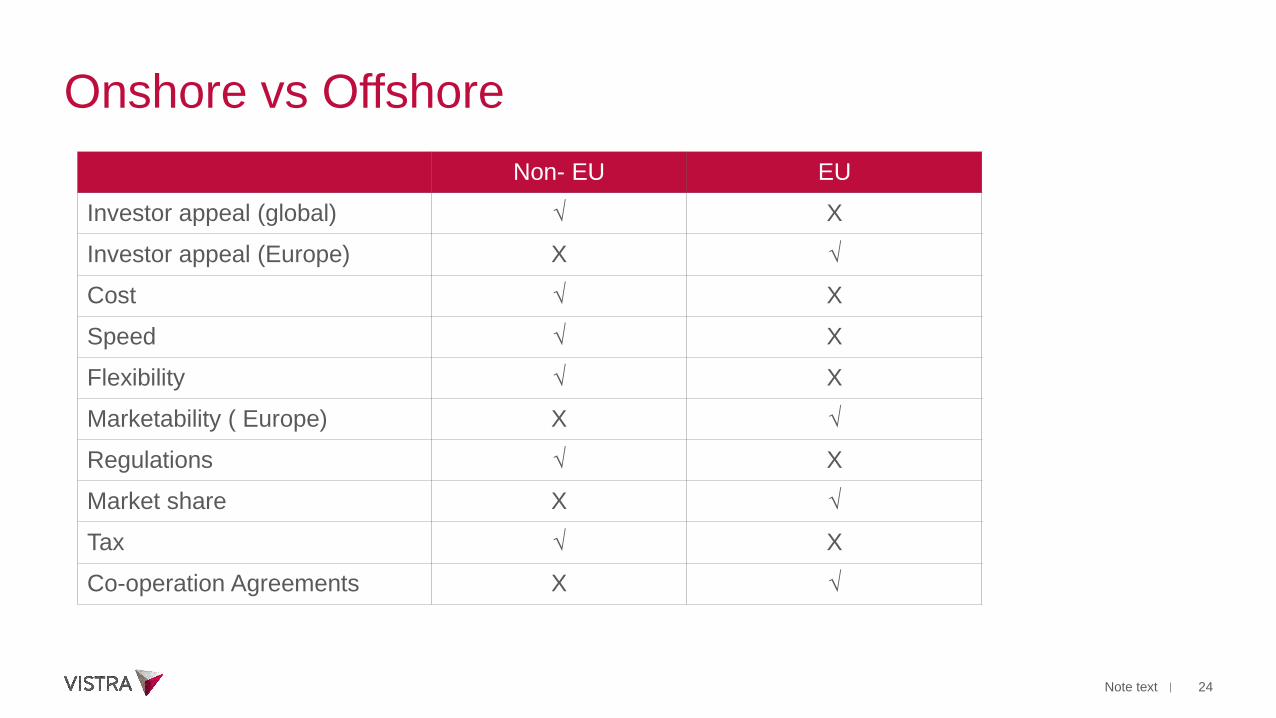

Onshore vs Offshore

Non- EU EU

Investor appeal (global) √ X

Investor appeal (Europe) X √

Cost √ X

Speed √ X

Flexibility √ X

Marketability ( Europe) X √

Regulations √ X

Market share X √

Tax √ X

Co-operation Agreements X √

Note text

New operating conditions for AIFMs and their administrators

Challenges from AIFMD

Reporting to the regulator

Authorisation process

Risk management

Marketing of funds

Remuneration

Depositary costs

Operational requirements

Depositary requirements

26

Three models for Jersey & other third country AIFMs

1. No impact - i.e. no EEA marketing – business

as usual in terms of Jersey regulation and

structuring

2. EEA Private Placement - currently available to

Jersey AIFMs marketing into EEA;

• 200 + AIMs using private placement,

• Many new GP/LP structures, and

• Significant number are sub-threshold

3.EEA Pass-porting

• currently only available to “fully complaint” EEA

AIFMs

Note text

Private Placement into the EEA under NPPRS

Private placement marketing in the EEA

- For those Jersey AIFMs currently marketing to professional investors into the

EEA;

- Using differing national private placement regimes (NPPRs) of individual EEA

states, subject to 3 new AIFMD conditions;

Co-operation agreements between JFSC and relevant EEA regulator(s)

FATF/AML compliance ( must be a co-operative jurisdiction)

Need to comply with AIFMD’s disclosure, reporting and transparency

provision.

Substances consequence

Letter box entity analysis is required

Increased scrutiny on management decision and board

qualifications/competence

Focus on “functions” - investor negotiations

- documenting of risk management

- documenting of decision making

BEPS agenda increases the scrutiny on substance and function

29

Parallel fund Structure

EU-AIFM/AIF with (Sub) Delegation to non-EU ( non AIFMD)

Portfolio manager

Note text

EU AIFM

Assets

EU AIF

(Lux)

Jersey LPGP

Portfolio risk

management

Delegation of

portfolio

management

OR Acting as

Investment

Advisor

EU Professional Investors Non-EU Professional Investors

Passporting and ESMA Advice/Opinions

Advice

To extend AIFMs in Jersey, Guernsey and Switzerland

(pending adjustments)

Difficulties in assessing US, Hong Kong and Singapore

Timing remains uncertain

Opinion

“insufficient evidence to indicate that the NPPRs have raised major issues

in terms of functioning and implementing AIFMD”

Divergent approaches with respect to marketing rules

Varying interpretations of “marketing” and “material changes”

Conclusion

Continued reliance on NPPR

Regulated structures will continue to provide optionality in the future

Questions ?