spectra energy 2q_2007_spectraenergyearnings

TRANSCRIPT

August 6, 2007

Second Quarter 2007 Earnings ReviewFred Fowler

President and CEO

Greg EbelCFO

22

Safe Harbor StatementSafe Harbor StatementSome of the statements in this document concerning future company performance will be forward-looking within the meanings of the securities laws. Actual results may materially differ from those discussed in these forward-looking statements, and you should refer to the additional information contained in Spectra Energy’s Form 10-K and other filings made with the SEC concerning factors that could cause those results to be different than contemplated in today's discussion.

Reg G DisclosureIn addition, today’s discussion includes certain non-GAAP financial measures as defined under SEC Regulation G. A reconciliation of those measures to the most directly comparable GAAP measures is available on Spectra Energy’s Investor Relations website at www.spectraenergy.com.

33

Spectra Energy’s Second QuarterSpectra Energy’s Second Quarter• Ongoing EPS consistent with expectations• Solid results at Distribution and US Transmission; plant

turnarounds at Western Canada and weather challenges at Field Services affected earnings

• $650 million of expansion projects in-service by end of 2007 • Closed Spectra Energy Partners IPO on July 2nd – SE

received $345 million • Optimistic we will achieve 2007 financial goals

Committed to delivering results to shareholders with solid, steady growth and an attractive dividend to provide a total return of 8-10% in a relatively low risk environment

44

Earnings SummaryEarnings Summary

$ 264$ 192Ongoing Net Incomen/a$ 0.31Reported Diluted EPSn/a

(63)7

$ 3202Q06

$ 0.30

(11)7

$ 1962Q07

Ongoing Diluted EPS

Discontinued OperationsSpecial Items

Reported Net Income

• Special items:• 2Q07 – separation costs • 2Q06 – separation costs and costs to achieve Duke Energy/Cinergy

merger• Discontinued operations:

• 2Q07 - Sonatrach settlement proceeds, net of tax• 2Q06 - businesses retained by Duke Energy but reported as a part of

Spectra Energy Capital for 2006

55

U.S. TransmissionU.S. Transmission

• 2Q07 ongoing segment results were lower by $7 million compared with 2Q06 primarily a result of:• lower gas processing volumes from pipeline operations• increased earnings from M&NE and expansion projects• higher direct operating costs

• Significant advancements made on growth projects

$ 230$ 223Ongoing Segment EBIT---

$ 2302Q06

---$ 2232Q07

Special ItemsReported Segment EBIT

Reported & Ongoing Segment EBIT ($ millions)

66

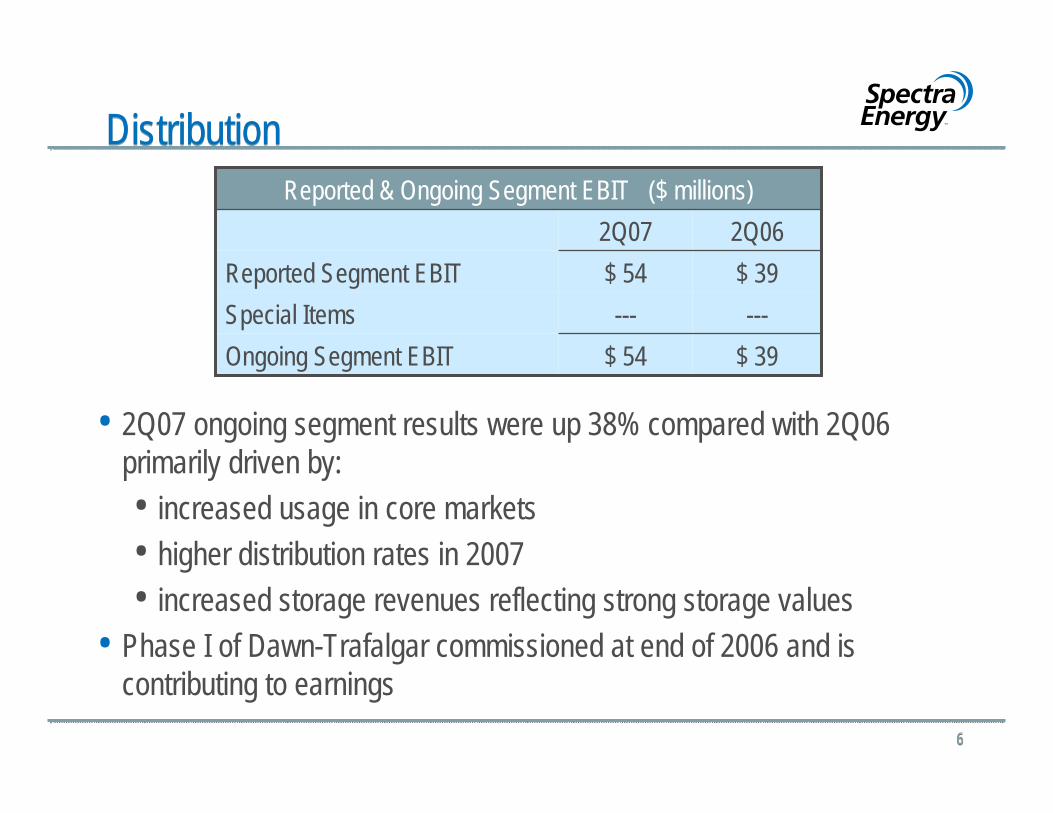

DistributionDistribution

• 2Q07 ongoing segment results were up 38% compared with 2Q06 primarily driven by:• increased usage in core markets • higher distribution rates in 2007 • increased storage revenues reflecting strong storage values

• Phase I of Dawn-Trafalgar commissioned at end of 2006 and is contributing to earnings

$ 39$ 54Ongoing Segment EBIT---

$ 392Q06

---$ 542Q07

Special ItemsReported Segment EBIT

Reported & Ongoing Segment EBIT ($ millions)

77

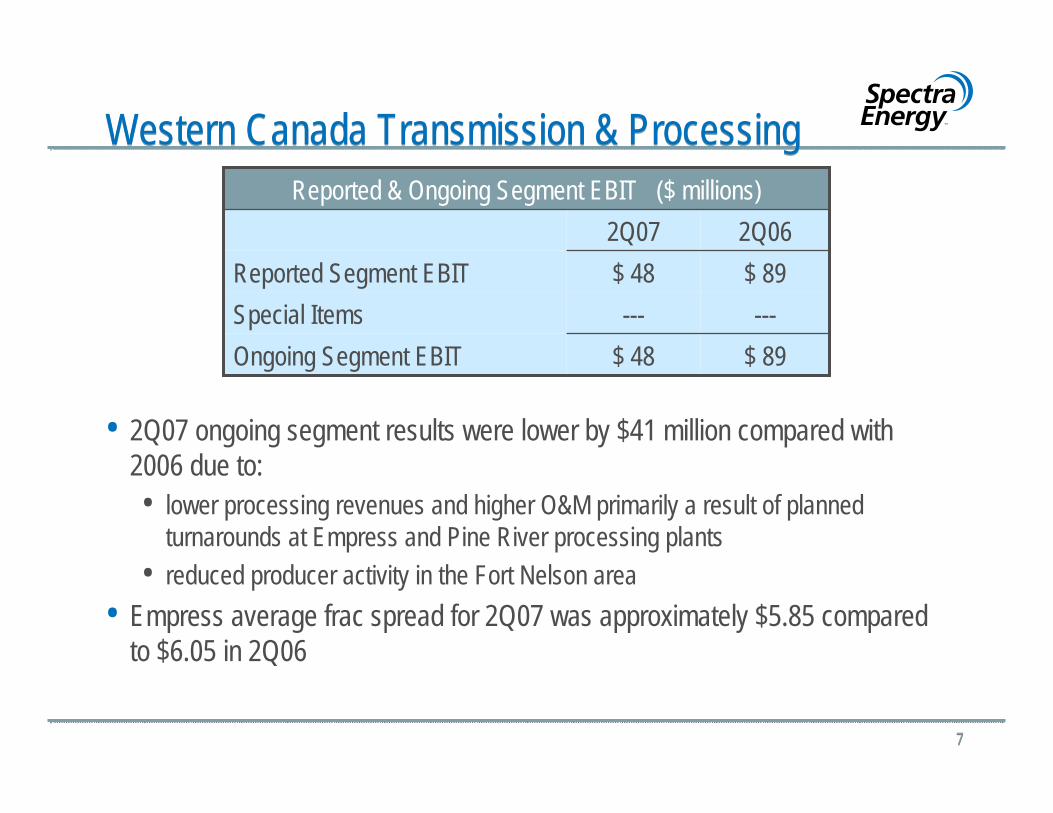

Western Canada Transmission & ProcessingWestern Canada Transmission & Processing

• 2Q07 ongoing segment results were lower by $41 million compared with 2006 due to: • lower processing revenues and higher O&M primarily a result of planned

turnarounds at Empress and Pine River processing plants • reduced producer activity in the Fort Nelson area

• Empress average frac spread for 2Q07 was approximately $5.85 compared to $6.05 in 2Q06

$ 89$ 48Ongoing Segment EBIT---

$ 892Q06

---$ 482Q07

Special ItemsReported Segment EBIT

Reported & Ongoing Segment EBIT ($ millions)

88

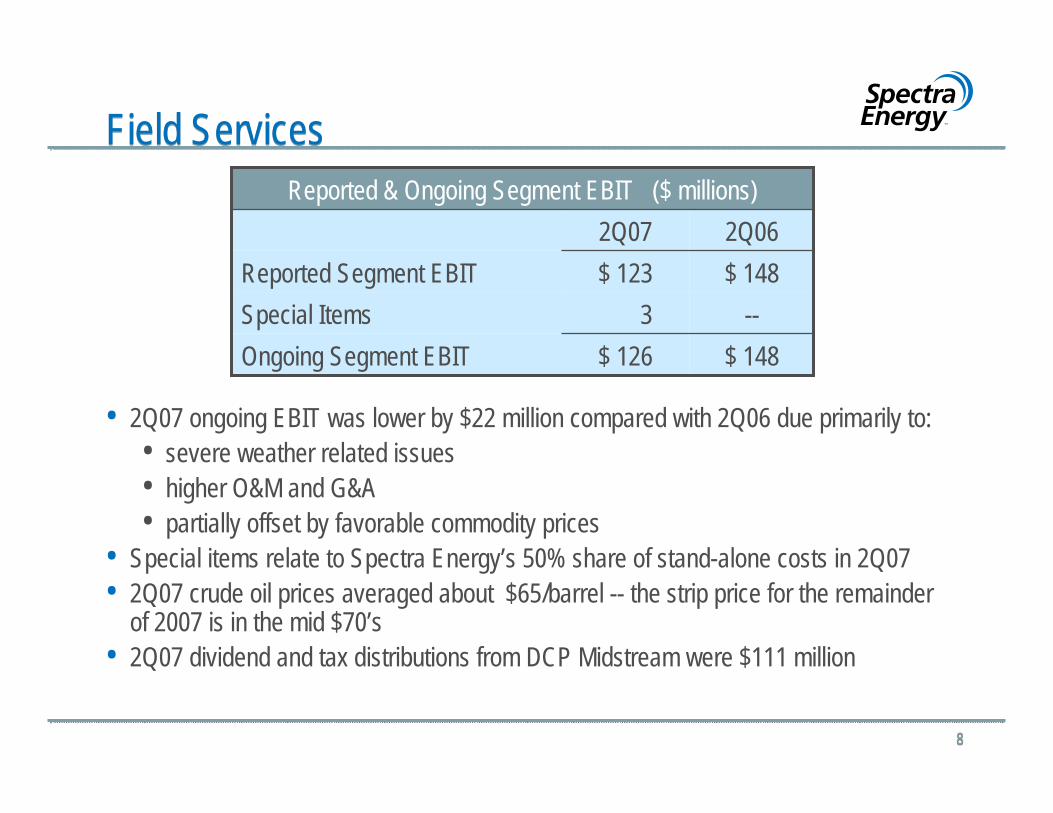

Field ServicesField Services

• 2Q07 ongoing EBIT was lower by $22 million compared with 2Q06 due primarily to:• severe weather related issues • higher O&M and G&A • partially offset by favorable commodity prices

• Special items relate to Spectra Energy’s 50% share of stand-alone costs in 2Q07 • 2Q07 crude oil prices averaged about $65/barrel -- the strip price for the remainder

of 2007 is in the mid $70’s• 2Q07 dividend and tax distributions from DCP Midstream were $111 million

$ 148$ 126Ongoing Segment EBIT--

$ 1482Q06

3$ 1232Q07

Special ItemsReported Segment EBIT

Reported & Ongoing Segment EBIT ($ millions)

99

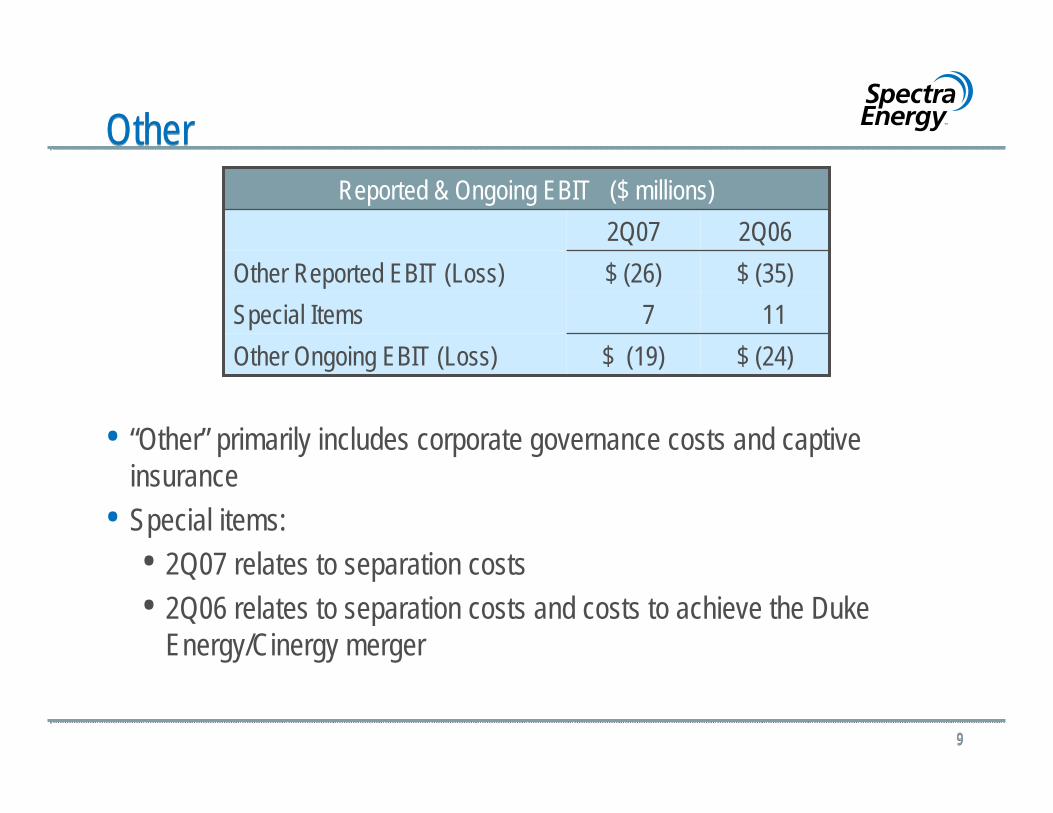

OtherOther

• “Other” primarily includes corporate governance costs and captive insurance

• Special items:• 2Q07 relates to separation costs • 2Q06 relates to separation costs and costs to achieve the Duke

Energy/Cinergy merger

$ (24)$ (19)Other Ongoing EBIT (Loss)11

$ (35)2Q06

7$ (26)2Q07

Special ItemsOther Reported EBIT (Loss)

Reported & Ongoing EBIT ($ millions)

1010

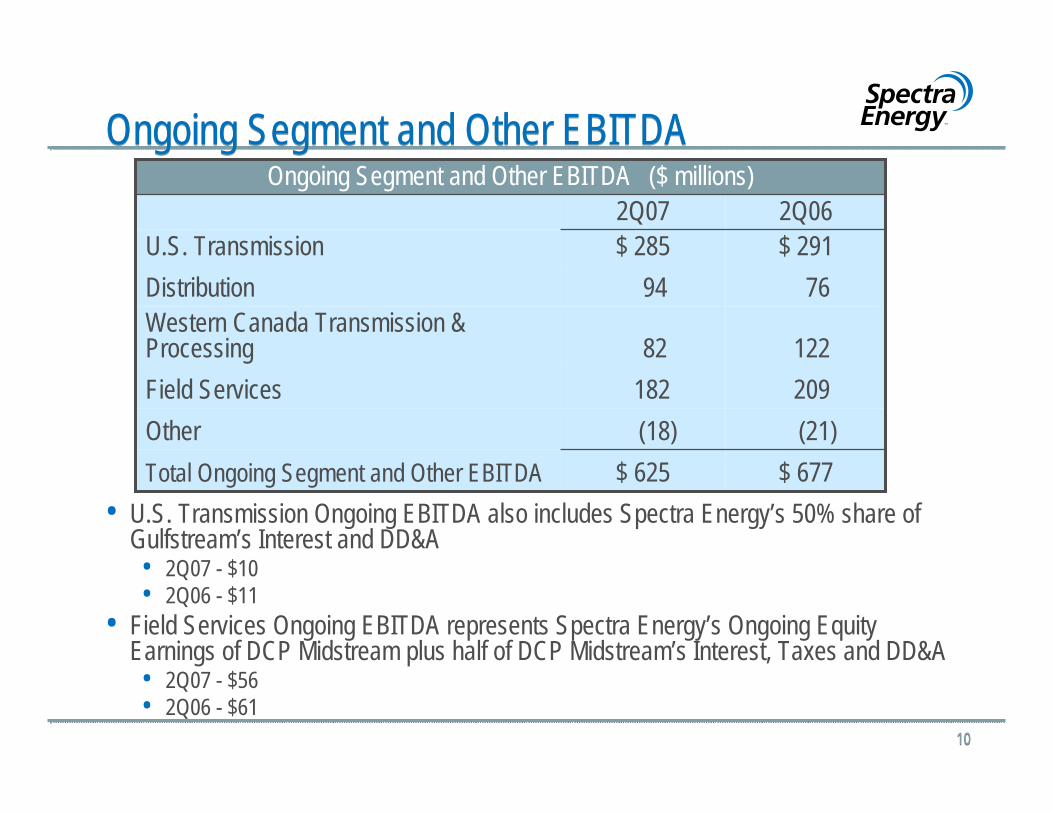

Ongoing Segment and Other EBITDAOngoing Segment and Other EBITDA

• U.S. Transmission Ongoing EBITDA also includes Spectra Energy’s 50% share of Gulfstream’s Interest and DD&A• 2Q07 - $10 • 2Q06 - $11

• Field Services Ongoing EBITDA represents Spectra Energy’s Ongoing Equity Earnings of DCP Midstream plus half of DCP Midstream’s Interest, Taxes and DD&A• 2Q07 - $56• 2Q06 - $61

(21)(18)Other$ 677$ 625Total Ongoing Segment and Other EBITDA

209182Field Services12282

Western Canada Transmission & Processing

7694Distribution$ 291$ 285U.S. Transmission2Q062Q07

Ongoing Segment and Other EBITDA ($ millions)

1111

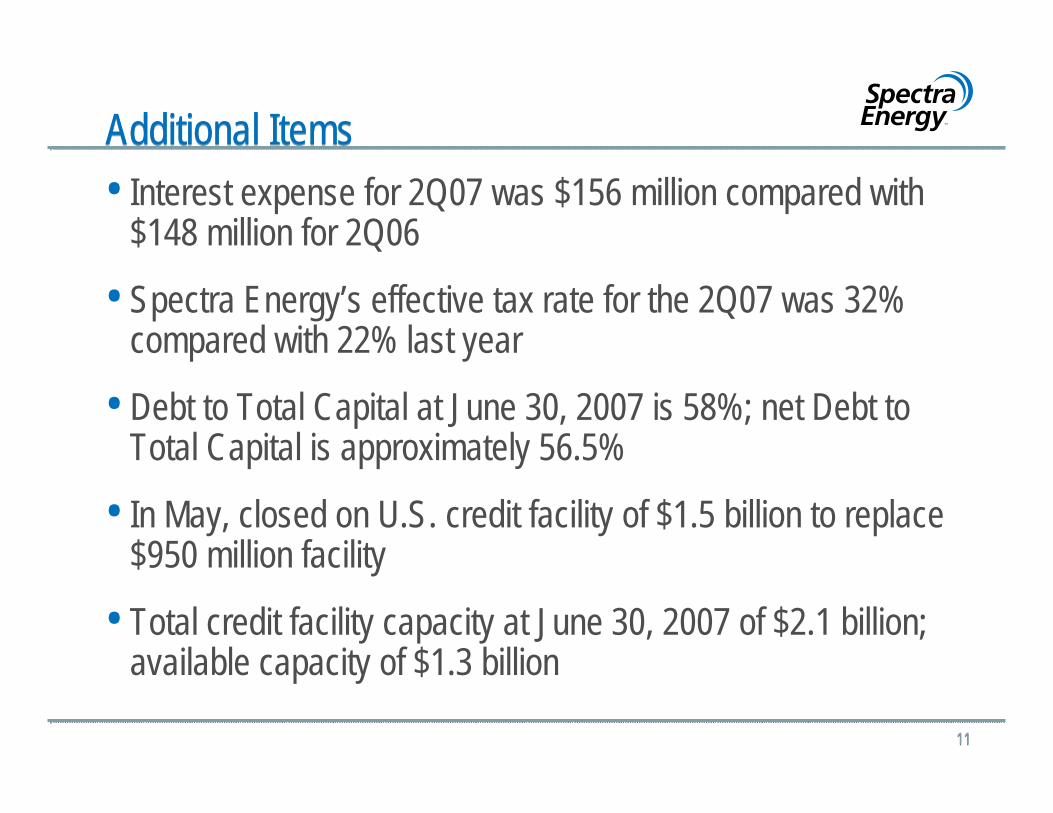

Additional ItemsAdditional Items• Interest expense for 2Q07 was $156 million compared with

$148 million for 2Q06

• Spectra Energy’s effective tax rate for the 2Q07 was 32% compared with 22% last year

• Debt to Total Capital at June 30, 2007 is 58%; net Debt to Total Capital is approximately 56.5%

• In May, closed on U.S. credit facility of $1.5 billion to replace $950 million facility

• Total credit facility capacity at June 30, 2007 of $2.1 billion;available capacity of $1.3 billion

1212

M&NE Phase IV (CanaportTM)

Dawn Storage Deliverability

Dawn-TrafalgarPhase II, III

Processing Plant Expansion

Ramapo

Islander East

TEMAX/Lebanon East

Time II

Gulfstream Phase III & IV

Copiah Storage

SE Supply Header

Cape CodDawn Area Storage

St. Clair Power

Moss Bluff Expansion

Egan Expansion

Gas Gathering Pipelines

Lebanon Connector

Rockaway Beach

AGT East/West

NE Gateway

Steckman Ridge

AccidentGlade Spring

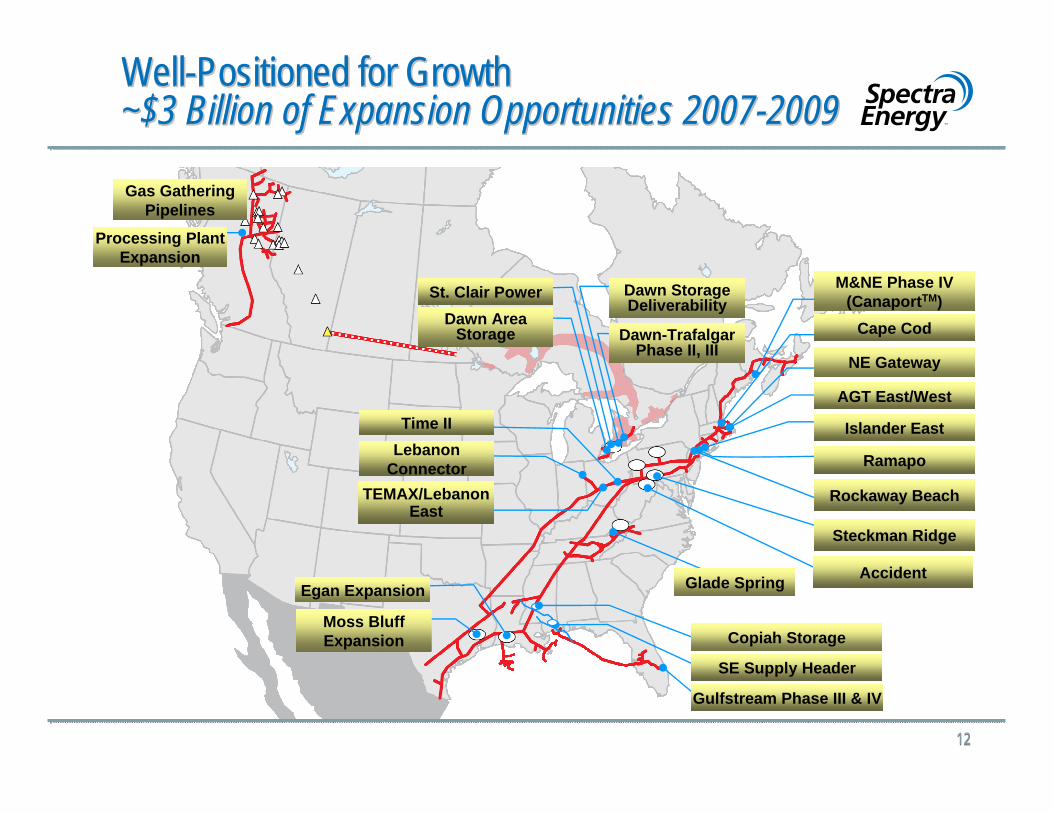

Well-Positioned for Growth~$3 Billion of Expansion Opportunities 2007-2009WellWell--Positioned for GrowthPositioned for Growth~$3 Billion of Expansion Opportunities 2007~$3 Billion of Expansion Opportunities 2007--20092009

1313

Well-Positioned for GrowthNortheast GatewayWell-Positioned for GrowthNortheast GatewayNortheast Gateway

• 16 mile, 24” offshore pipeline in Massachusetts Bay to connect Excelerate’s Deepwater LNG port to Algonquin’s Hubline Pipeline

• 25 year firm contract with ExcelerateEnergy for entire 800 mmcf/day

• Construction began in May• Pipe lay is complete; plowing/jetting in

progress• Estimated capital expenditures: $240

million• In-service December ‘07

1414

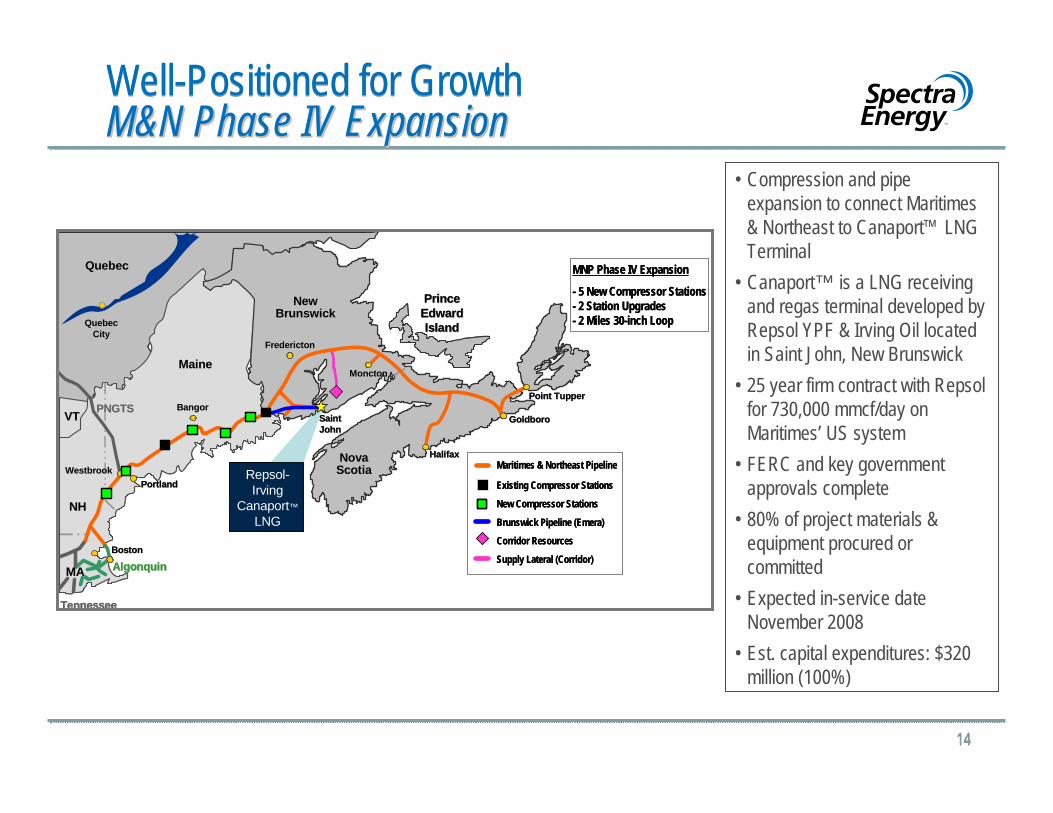

Well-Positioned for GrowthM&N Phase IV ExpansionWell-Positioned for GrowthM&N Phase IV ExpansionM&N Phase IV Expansion

• Compression and pipe expansion to connect Maritimes & Northeast to Canaport™ LNG Terminal

• Canaport™ is a LNG receiving and regas terminal developed by Repsol YPF & Irving Oil located in Saint John, New Brunswick

• 25 year firm contract with Repsol for 730,000 mmcf/day on Maritimes’ US system

• FERC and key government approvals complete

• 80% of project materials & equipment procured or committed

• Expected in-service date November 2008

• Est. capital expenditures: $320 million (100%)

MNP Phase IV Expansion

- 5 New Compressor Stations- 2 Station Upgrades- 2 Miles 30-inch Loop

MNP Phase IV Expansion

- 5 New Compressor Stations- 2 Station Upgrades- 2 Miles 30-inch Loop

Maritimes & Northeast Pipeline

Existing Compressor Stations

New Compressor Stations

Brunswick Pipeline (Emera)

Corridor Resources

Supply Lateral (Corridor)

Maritimes & Northeast Pipeline

Existing Compressor Stations

New Compressor Stations

Brunswick Pipeline (Emera)

Corridor Resources

Supply Lateral (Corridor)

TennesseeTennessee

PortlandPortland

MonctonMoncton

Quebec Quebec CityCity

Nova Nova ScotiaScotia

New New BrunswickBrunswick

QuebecQuebec

MaineMaine

VTVT

NHNH

Prince Prince Edward Edward IslandIsland

HalifaxHalifax

BostonBoston

FrederictonFredericton

GoldboroGoldboroBangorBangor

Saint Saint JohnJohn

Point TupperPoint TupperPNGTSPNGTS

AlgonquinAlgonquinMAMA

WestbrookWestbrook Repsol-Irving

Canaport™LNG

TennesseeTennessee

PortlandPortland

MonctonMoncton

Quebec Quebec CityCity

Nova Nova ScotiaScotia

New New BrunswickBrunswick

QuebecQuebec

MaineMaine

VTVT

NHNH

Prince Prince Edward Edward IslandIsland

HalifaxHalifax

BostonBoston

FrederictonFredericton

GoldboroGoldboroBangorBangor

Saint Saint JohnJohn

Point TupperPoint TupperPNGTSPNGTS

AlgonquinAlgonquinMAMA

WestbrookWestbrook Repsol-Irving

Canaport™LNG

1515

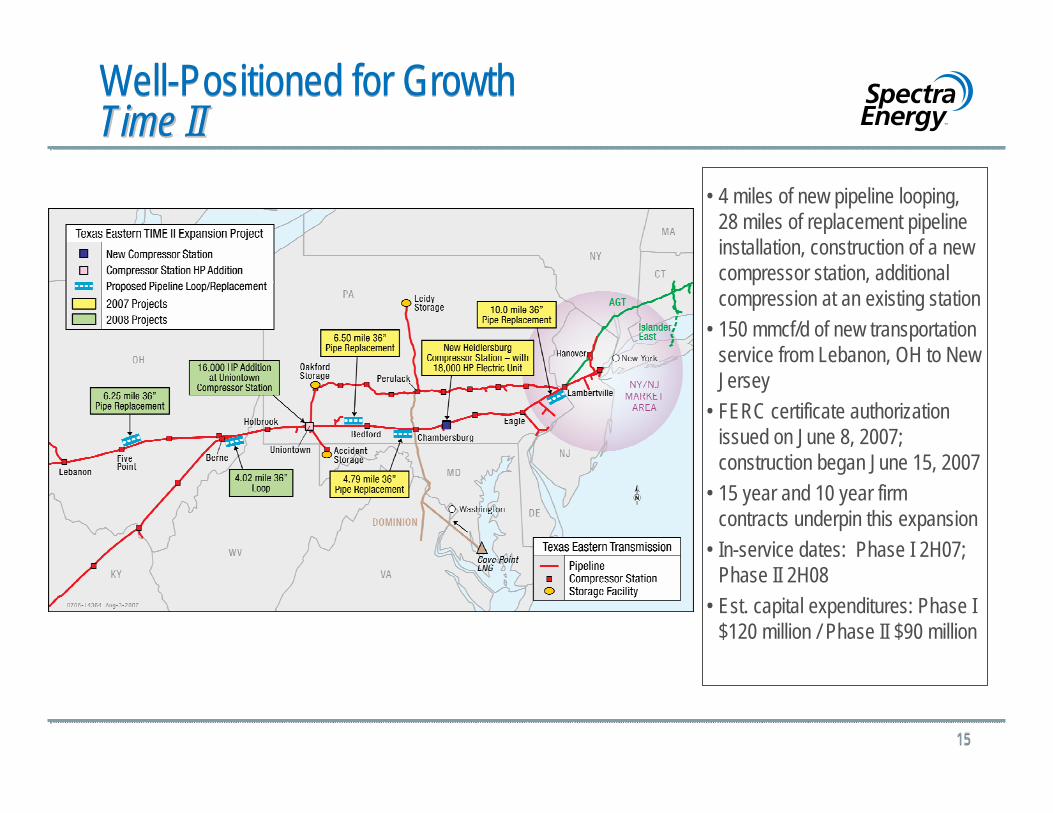

Well-Positioned for GrowthTime IIWell-Positioned for GrowthTime IITime II

• 4 miles of new pipeline looping, 28 miles of replacement pipeline installation, construction of a new compressor station, additional compression at an existing station

• 150 mmcf/d of new transportation service from Lebanon, OH to New Jersey

• FERC certificate authorization issued on June 8, 2007; construction began June 15, 2007

• 15 year and 10 year firm contracts underpin this expansion

• In-service dates: Phase I 2H07; Phase II 2H08

• Est. capital expenditures: Phase I $120 million / Phase II $90 million

1616

Well-Positioned for GrowthSoutheast Supply HeaderWell-Positioned for GrowthSoutheast Supply HeaderSoutheast Supply Header

• 270 miles of pipe from Perryville Hub in NE La. to Mobile, Al

• Provides alternative to offshore supply

• 95% of capacity is subscribed under firm, long-term agreements

• Pipe is currently being delivered• Prime contractors retained• Expect FERC certification later this

year• Est. capital expenditures: $400 million• In-service in summer ‘08

1717

Value PropositionValue Proposition• A premier pure-play midstream natural gas company

in North America• Attractive industry dynamics• Positioned in fastest growing markets• Diverse supply base• Seasoned management team• Strong balance sheet and stable cash flows• Financial flexibility• Solid steady growth and attractive dividend yield