special report section 7 - goinggoinggone? delaware hawaii (1/1/05) idaho ... cpa, flmi is president...

TRANSCRIPT

The Van Elsen Report©2003 Van Elsen Consulting, Inc.

All Rights ReservedPhone: 641-621-0057Toll Free: 888-GAZEBO-5Fax: 641-621-0058E-Mail Address:[email protected]

Website:www.VEConsulting.com

Mailing Address:Van Elsen Consulting, Inc.

2407 Drenthe LaanPella, Iowa 50219

CONTENTSAOMR Update . . . . . . . . . . . . . 1Identical Annual Statements . . . 22001 CSO Update . . . . . . . . . . 3Van Elsen Consulting, Inc. . . . . . 4

THE VAN ELSEN REPORTVol. VIII No. 5

September 10, 2003

Special Report

Section 7 - Going...Going...GONE?AOMR Updateby Mark RowleyIn September 2002, I wrote an articlefor the Van Elsen Report with about thesame title as this article. It describedwhy Section 7 Opinions were on theirway out. The reason given was that thenew Actuar ia l Opin ion andMemorandum Regulation (AOMR) hadbeen passed by the NAIC and that itwas expected to pass in many states in2003 and 2004. This turns out to be apoor forecast as on ly theFlorida Department of Financial Serviceshas passed the regulation. Much of thisis due to the AOMR receiving lowpriority by busy state insurancedepartments. However, some of it isalso due to state insurance departments(and the industry) being dissatisfied bythe alternate actuarial opinionsproposed. These alternate opinionswould have gone a long way to assistappointed actuaries in dealing with statevariations in valuation laws. At first glance it might appear that theonly thing to report along the lines ofSection 7 is that nothing much hashappened. Only one state has passedthe regulation, which can't possibly havemuch of an impact, right? On thecontrary, what it means is that everycompany licensed to do business in thestate of Florida must do a Section 8

opinion for year-end 2003 and annuallythereafter. Florida passed the laweffective for all valuation dates afterJanuary 23, 2003. Kerry Krantz,Valuation Actuary for Florida, confirmedmy understanding of this in a recente-mail. Also, Kerry recently made thefollowing information available on theSOA general interest web board foranyone wanting to read Florida'sregulation. Florida Administrative Code rule 4-138,part III, is available on the internet at:1. http://fac.dos.state.fl.us/2. Click Chapter 4 - Department of

Insurance -http://fac.dos.state.fl.us/faconline/chapter04.pdf

3. Click D4-138.040 to get to thebeginning of Part III ActuarialOpin ion & MemorandumRegulation.

According to Kerry, the "Scope" sectionof the regulation (4-138.041),paragraphs 1 and 2, makes it clear thatthe regulation is effective forDecember 31, 2003 valuations.For all practical purposes it appears thatSection 7 opinions are gone forcompanies licensed in Florida. While aSection 7 opinion could be filed in otherstates, it probably makes sense to file aSection 8 opinion everywhere, as longas the work is being done. There areRBC (C-3 factors) and potentially ratingagency advantages to filing a Section 8.Of course it also means that companiesneed to determine quickly whatresources are available to do the assetadequacy analysis (usually cash flowtesting) required as part of Section 8opinions. It is also important to keep inmind that efforts prior to year end

reduce the effort needed in January andFebruary. So are non-Florida small companies offthe hook? Perhaps they are, for now.But there are other ways regulators canrequire Section 8 opinions other thanthe new AOMR. For several yearscompanies using X-factors as part oftheir compliance with XXX have beenrequired to do a Section 8. Also, if youread the fine print of the 2001 CSOregulation you will find that Section 8opinions (asset adequacy analysis) arerequired for any company that valuesany of their business using the newmortality table. This will impact manycompanies for year-end 2004.For some companies, asset adequacyanalysis will be so expensive it may beworth doing all the things necessary (nobusiness in Florida, no X-factors, andno 2001 CSO) to avoid it. This may beworkable for a small number ofcompanies. 2001 CSO is just aminimum valuation standard, so if1980 CSO produces higher reserves, it

Pella, Iowa

2 The Van Elsen Report September 10, 2003

Vermeer Windmill, Pella, IA

can still be used. However, this will bedifficult, since products will becomeuncompetitive. In the long run theseproducts would need: 1980 CSOreserves & cash values, and 2001 CSOtax reserves and guideline premiums.Mark is a Consulting Actuary withVan Elsen Consulting, Inc. He can bereached at (515) 276-8565 [email protected].

Identical AnnualStatementsby Mark RowleyThere has been discussionat the NAIC in recentweeks about whether theannual statement that aninsurance company files inthe various states should beidentical.Gloria Glover of the Blanks(E) Task Force wrote aletter (on August 27, 2003)to Randy Blumer of theFinancial Analysis WorkingGroup on this topic. Shewrites that there has beenconfusion among insurersrelated to Regulation XXXwhen the regulation hasbeen passed by somestates and not by others.She writes further: "Someinsurers have determinedtheir highest reserverequ i remen t s , havebooked, and reportedthose for all states. Some insurers havefiled the annual statement reflecting therequirements of the state of domicileand then have filed a qualified Statementof Actuarial Opinion in the otherstates…“In addition, states that have adoptedthe 2001 CSO table for life insurancewill likely require lower reserves than

states that have not adopted these newtables…“Although states expect that insurerswould file an identical annual statementin all states and disclose the domiciliarystate's prescribed practices in the Notesto Financial Statements, this does notappear to be happening in allcases…Upon review of the NAICAnnual Statement Instructions manuals,we were not able to locate any written

restrictions against insurers filingdifferent annual statements…We arenotifying the Financial Analysis WorkingGroup of this issue since financialanalysis is conducted on statements filedwith the NAIC… (which is)… the filingmade in the domestic state."There are many situations which haveled to this problem. Some of the more

common that we have encounteredinclude:1. Non-uniform adoption dates of

“XXX”.2. Non-uniform adoption dates of

valuation mortality tables.3. “Continuous CARVM” regulation in

Illinois.

Until such time as the states are able tosimultaneously adopt uniform valuation

regulations, this situationwill exist. Companiesalways will have the optionto use the “mostconservative” valuation lawas the basis of filing. This,however, is not alwayspractical.New valuation laws takeyears to be adopted by allstates. In many instances,this never occurs. Thenew regulation oftenresults in significantly lower(or in a few cases, higher)reserves. How long is acompany supposed to waitfor the last state to adoptthe new regulation?As a practical matter, thefiling of multiple annualstatements does not occurvery often. If the differencein reserves is not material,it is easier to hold the moreconservative reserves. If itis material, it may becomea problem in the state with

the more conservative reserves. Mostcompanies do not want to intentionallyfile statements, regardless of how fewstates would receive them, that showan impaired financial position.Mark is a Consulting Actuary withVan Elsen Consulting, Inc. He can bereached at (515) 276-8565 [email protected].

3 The Van Elsen Report September 10, 2003

2001 CSO Update - * Survey in Progress *by Terry HilkerTerry is a Actuarial Systems Analyst with Van Elsen Consulting, Inc. He can be reached at (515) 674-3174 [email protected]. The current survey may be found at http://www.VEConsulting.com/2001cso.html.

No Position Reported (8 States & DC)ConnecticutDistrict of ColumbiaGeorgia

MissouriMontana

New YorkRhode Island

South DakotaWest Virginia

States with No Current Plans to Adopt (2 States)Mississippi Wyoming

States Considering Adoption (10 States)AlabamaAlaskaDelaware

Hawaii (1/1/05)IdahoMichigan

Nevada (1/1/06)South Carolina (1/1/05)

Vermont Virginia

States Planning to Adopt - (Effective) - (24 States)Arizona (1/1/04)Arkansas (1/1/04)California (1/1/04)Colorado (1/1/04)Florida (?)Illinois (1/1/04)Indiana (1/1/04)

Iowa (1/1/04)Kansas (1/1/ 04)Kentucky (1/1/05 or 06)Louisiana (1/1/05)Maine (?)Massachusetts (1/1/04)Maryland (1/1/04)

Minnesota (1/1/04)Nebraska (1/1/04)New Hampshire (?)New Jersey (?/?/04)New Mexico (1/1/04)North Carolina (1/1/05)North Dakota (1/1/04)

Ohio (1/1/04)Oregon (1/1/04)Pennsylvania (1/1/04)Tennessee (1/1/04)Washington (1/1/04)Wisconsin (?)

States Adopted - (Effective) - (3 States)Oklahoma (7/14/03) Texas (5/1/03) Utah (6/13/03)

4 The Van Elsen Report September 10, 2003

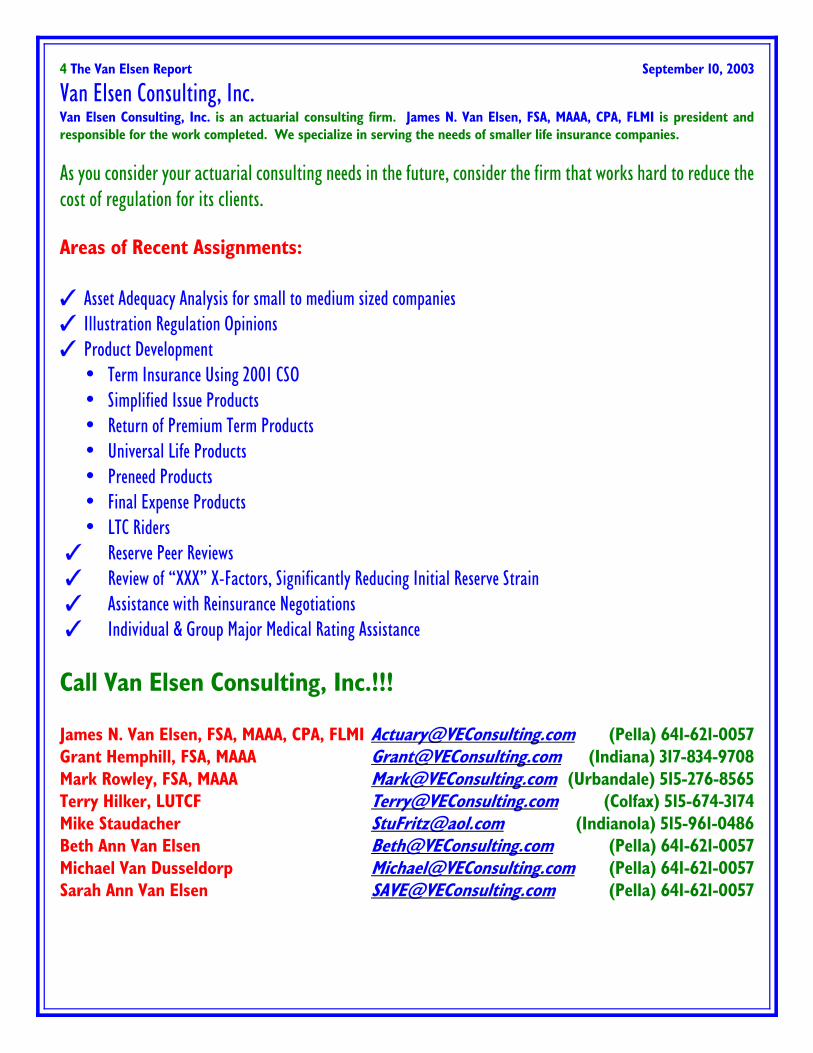

Van Elsen Consulting, Inc.Van Elsen Consulting, Inc. is an actuarial consulting firm. James N. Van Elsen, FSA, MAAA, CPA, FLMI is president andresponsible for the work completed. We specialize in serving the needs of smaller life insurance companies.

As you consider your actuarial consulting needs in the future, consider the firm that works hard to reduce thecost of regulation for its clients.

Areas of Recent Assignments:

T Asset Adequacy Analysis for small to medium sized companiesT Illustration Regulation OpinionsT Product Development

• Term Insurance Using 2001 CSO• Simplified Issue Products• Return of Premium Term Products• Universal Life Products• Preneed Products• Final Expense Products• LTC Riders

T Reserve Peer Reviews T Review of “XXX” X-Factors, Significantly Reducing Initial Reserve Strain T Assistance with Reinsurance Negotiations T Individual & Group Major Medical Rating Assistance

Call Van Elsen Consulting, Inc.!!! James N. Van Elsen, FSA, MAAA, CPA, FLMI [email protected] (Pella) 641-621-0057Grant Hemphill, FSA, MAAA [email protected] (Indiana) 317-834-9708Mark Rowley, FSA, MAAA [email protected] (Urbandale) 515-276-8565Terry Hilker, LUTCF [email protected] (Colfax) 515-674-3174Mike Staudacher [email protected] (Indianola) 515-961-0486Beth Ann Van Elsen [email protected] (Pella) 641-621-0057Michael Van Dusseldorp [email protected] (Pella) 641-621-0057Sarah Ann Van Elsen [email protected] (Pella) 641-621-0057