special issue suplemento especial august 2016 · ipho diseño y comunicación ... in 2015, the eu...

TRANSCRIPT

Industrias PesquerasRevista Marítima

Since 1927

S P E C I A L I S S U E S U P L E M E N T O E S P E C I A L AUGUST

2016

Introduction p.01 Interview: Ola Eriksen, Managing Director of the Nor-Fishing Foundation p.03 Per Sandberg, Minister of Fisheries of Norway p.18

Kathryn Stack, managing director of Europêche p.21 Opinion The LDAC, more than a chimera p.06 Companies Ibercisa Deck Machinery p.08 Asime p.14 Vanguard Marine p.26 Rabobank p.32 Statistics The situation of the european fishing areas at a glance p.12 A quick view to the main indicators p.28

16-19 AUGUST 2016

August 2016 - Special Issue Industrias Pesqueras 1

AUGUST 2016 · YEAR LXXXIX

Legal Deposit: PO 6/1958

EDITORAlfonso Paz-Andrade

DEPUTY EDITORNieves Garcí[email protected]

EDITORIAL ASSISTANTMar [email protected] [email protected]ús M. Benjamin

SALES MANAGERLuis de [email protected]

SUBSCRIPTIONSTere Pazó[email protected]

GRAPHIC DESIGNAND LAYOUTMiguel Á. Julián [email protected]

IPHO diseño y comunicaciónwww.ipho.es

MANAGING DIRECTORLuis de Miguel

PUBLISHED BYSIPSA Policarpo Sanz 22 - 3º dcha.36202 VIGO · SPAIN · Apartado de Correos nº 127Tel.: (986) 447075-437004-431389Fax: (986) 430625 · [email protected]

PRINTED BYGráficas Anduriña Industrias Pesqueras is a trade mark of SIPSA.All rights reserved.

SOCIAL MEDIA

https://www.facebook.com/industriaspesqueras

@IPesqueras · https://twitter.com/ipesqueras

Industrias Pesqueras would like to thank all our collaborators, companies, advertisers and everyone who has made this Nor-Fishing 2016 special edition.

You can download the pdf version on www.industriaspesqueras.com

Cover photo: Jens Kristian Vang

The date has arrived. Nor Fishing, the prestigious

event dedicated to the fisheries industry in

Norway, is ready for a new edition. This biennial

event boasts a history of more than 50 years,

hosting exhibitors and visitors in increasing

numbers in each of its editions. Held at cities

such as Bergen and Oslo in the past, this trade

fair is this year organized at Trondheim, from 16

to 19 august, with the city’s famous fair center,

the Trondheim Spektrum, acting as the venue.

Nor Fishing brings together leading exhibitors of

shipyards, fishing equipment, deck machinery and

maritime electronics, allowing them to showcase

their products to an international list of clients. The

exhibition is, also, a platform for serious business

transactions, providing over 460 exhibitors with the

opportunity to serve over 14,000 trade buyers from

more than 52 countries.

During Nor-Fishing there are numerous seminars,

mini-conferences, presentations, lectures and

debates being held. This all contributes to

keeping the visitors up to dated with the latest

professional information. The exhibition has

also become the most important place to meet

colleagues, customers, suppliers, scientists,

researchers and senior officials. In order to

facilitate networking a huge variety of social

events such as festive buffet dinners, receptions,

a Student Day, seafood evenings etc. take place.

This special issue of Industrias Pesqueras is

fully dedicated to the exhibition. The currents

affairs of the fisheries sector, its challenges

and opportunities, from the point of view of

the voices of the industry are included in its

pages. A significant number of companies have

collaborated with us in this issue. Turn the

pages and discover all that the new edition of

Nor-Fishing will offer you.

INNOVATION AWARD NOMINEES

One of the main attractions of the parallel

programme of the exhibition is the Innovation

Award. The Nor-Fishing Foundation received

nine applications for this year’s award. There

has been an impressive development in the

fisheries industry with regard to vessels, gear and

equipment for quality handling of fish for many

decades. Today, much of the focus is on sorting

the catch, limiting the catch, environment and

sustainable development of fisheries nationally

and internationally.

The Jury has nominated the following three finalists:

Institute of Marine Research (IMR), Bergen, is

implementing a project where catch control is

tested through different adaptions to the net of

the so-called “Danish seine”. The objective is to

catch only the amount of fish that the vessel is

licenced to catch and has the capacity to handle.

This is important to the fishermen as well as fish

buyers with regard to quality and price, as well as

health, environment and safety considerations.

Scantrol Deep Vision AS, Bergen. Deep Vision

is being developed as an alternative and

supplemental method in relation to today’s

method, based on acoustics and experience, for

monitoring the catch by the use of stereographic

pictures from the trawl. A 3D modelling of the

fish gives the possibility of determining the

species and length, which in turn allows species

sorting in the trawl and a more efficient catch

from the point of view of market price, quota

control and reduced by-catch.

Selfa Arctic AS, Sandtorg has developed «the

world’s first» electrically propelled fishing

vessel in cooperation with Siemens/Trondheim

and with Corvus in Canada as supplier of the

batteries. The Norwegian Maritime Authority

has participated in order to develop a new set

of regulations to authorize such vessels. The

energy use is reduced by 40 – 60 % compared

to diesel operations.

The Award will be presented to the winner at

the official opening of Nor-Fishing on Tuesday

16 August 2016.

THE MEETING POINT OF THE WORLWIDE FISHERIES SECTOR

Industrias PesquerasRevista Marítima

Since 1927

Welcome to Nor-Fishing 2016!

SPNOR-FISHING 2016

Interview

IN NORWAY, WE HAVE SEEN A STEADY REDUCTION OF VESSELS, BUT THE ONES THAT ARE IN OPERATION HAVE STEADILY BECOME MORE EFFICIENT”

“

What is the role of Nor-Fishing in the

industry? Could we say that it reflects the

current situation?

Nor-Fishing has been around since 1960,

when we held the first exhibition. Our task is

to promote Norwegian technology in fisheries

and aquaculture. But over the years, we

have become so much more. Today, Nor-

Fishing is an important meeting place for the

industry, not only the Norwegian industry,

but globally. Every year, large numbers of

foreign visitors come to our exhibitions, and

usually there are also official delegations

from foreign countries. If Nor-Fishing could

be said to reflect the situation in the industry,

it is perhaps this: the Norwegian fisheries

industry is truly international, and the

exhibition reflects this.

Fisheries relationships between Europe

and Norway are strategic, also for trading

in sea products? How do you see the

current moment?

The EU is the largest market for Norwegian

seafood, accounting for as much as two

thirds of all our exports. Norway is therefore

dependent on Europe, but Europe is also

dependent on Norway for supplies of

seafood. In 2015, the EU imported almost

twice as much seafood as it exported, and

much of this came from Norway. In fact,

about 12 – 13% of EU seafood imports

came from Norway. In the past, we have

had some problems with access to certain

markets. As a non-member of the EU,

we are in a delicate position in relation to

market access in Europe. But so far, we

have managed to have workable trade

agreements that are to our mutual benefit.

The efforts being made by Norway

regarding the renewal of the fleet are

widely recognized. How does it look from

inside the country?

Over the past decade, there has been

a dramatic change in the Norwegian

fisheries fleet. Since 2005, more than

2000 vessels have been withdrawn from

the fishing grounds, and the number

of fishermen has also been drastically

reduced. In place of these smaller,

older vessels, we have got newer, larger

and much more efficient vessels that

have contributed greatly to improved

profitability in Norwegian fisheries.

Technology plays a central role in this

development. But we must also point out

that there have been structural changes

in the composition of the Norwegian fleet.

One of the most important changes was

the introduction of multiple quotas for a

single vessel. Previously, the rule was “one

vessel, one quota”. This led to several

owners having several vessels to fish

several quotas with one crew. This was not

very efficient, and very capital intensive.

Now, one owner may have one vessel with

one crew but fishing on several quotas,

and he is therefore able to operate much

more efficiently and profitably.

Could Norway be seen as a reference for

fleet renewal in Europe?

Perhaps, but we have to remember that

conditions vary from country to country.

However, that said, we must confess

that we are not unhappy with fleet

modernization at the moment.

Ola Eriksen, Managing Director of the Nor-Fishing Foundation

THE INTERNATIONAL FISHERIES TECHNOLOGY EXHIBITION NOR-FISHING

HAS BEEN HELD EVERY OTHER YEAR SINCE 1960, AND IT IS OPENING ITS

DOORS AGAIN. A RECORD NUMBER OF EXHIBITORS AND VISITORS ARE

EXPECTED THIS YEAR. “THIS YEAR’S EXHIBITION WILL BE THE LARGEST EVER”,

MANAGING DIRECTOR OF THE NOR-FISHING FOUNDATION, OLA ERIKSEN SAID

TO INDUSTRIAS PESQUERAS. 550 EXHIBITORS FROM 30 COUNTRIES HAVE

REGISTERED AND THE EXHIBITION AREA IS COMPLETED. IN FACT, THERE IS

A LONG WAITING LIST. WE TALKED WITH MR. ERIKSEN ABOUT THE CURRENT

EDITION OF THE EXHIBITION AND THE LEADING ROLE OF NORWAY IN THE

RENEWAL OF THE FLEET. THIS IS THE COMPLETE INTERVIEW.

August 2016 - Special Issue Industrias Pesqueras 3

4 Special Issue Industrias Pesqueras - August 2016

SPNOR-FISHING 2016Interview

What steps does Europe need to take in

this field?

I think it is commonly recognized that

one of the biggest problems in European

fisheries is the size and capacity of the

fleet, rather than the age. It has been

said that the EU fishing fleet should

be reduced by 50% in order to secure

sustainability in EU waters. At the same

time, fleet renewal would be necessary,

because the remaining 50% would have

to improve its performance considerably.

In Norway, we have seen a steady

reduction of the number of fishermen

and vessels over the years. But the

vessels that are in operation have

steadily become more efficient, both in

terms of catches and in terms of catch

utilization.

The industry has in sustainability one of

its main challenges. How is this point

reflected at the fair? What would be other

challenges?

Sustainability has been a major concern

for the Nor-Fishing Foundation for

many years, and in this we cooperate

with other institutions, for example the

Directorate of Fisheries. The Directorate

each year presents it Environment

Award to a company or institution that

has made significant contributions

to sustainability. We are also deeply

concerned with innovation, and the

Foundation has for many years now

presented its Innovation Award at the

“Norway is dependent on Europe, but Europe is also dependent on Norway for supplies of seafood”

August 2016 - Special Issue Industrias Pesqueras 5

SPNOR-FISHING 2016

Interview

exhibition. This award is also indirectly

linked to the issue of sustainability, as

much of the innovation presented is

concerned with the environment, better

use of raw material etc.

Regarding trends, What would you say is

the most important at the moment and for

the upcoming years?

There is no doubt that there will have

to be an even stronger emphasis

on sustainability and sustainable

management of world fisheries. We

just have to make sure that stocks are

properly managed. I think that the latest

developments in Norwegian fisheries

management may serve as a model in

this regard.

Secondly, I believe that we must

continue to make full use of technological

innovations also in fisheries. In a way, we

must make fisheries more scientific. Just

as we have done in modern aquaculture,

we must in the future base more of the

fisheries on science. Thus, research and

application of that research becomes

paramount to the global success of

fisheries.

And thirdly, we must recruit bright

young people to work in our industry.

Fortunately, many young people are

now beginning to see our industry as an

interesting sector with lots of potential

for their own career and intellectual

development.

“We must confess that we are not

unhappy with fleet modernization at the

moment”Photo: Nor-Fishing

6 Special Issue Industrias Pesqueras - August 2016

SPNOR-FISHING 2016Opinion

When the Advisory Councils of the

European Union where set up some 10

years ago, many thought them a futile

idea that would not bring any positive

outcomes. In earnest, I was one of the

sceptics, never thinking that a body

comprised of Industry, NGOs and other

Civil Society agents, sitting together to

jointly and unanimously decide on advice

to the EU institutions seemed as another

chimera.

If the task seemed difficult in the different

ACs with responsibility for parts of the

EU waters, with more homogeneity in the

composition of the participating fleets and

stakeholders, it seemed truly impossible

in the Long Distance AC, where the array

of fleets covered almost all variants,

pelagic, long liners, purse seiners,

trawlers… operating in all the oceans of

the world and with all EU fishing flags

present. The diversity also extended to

the other stakeholders, with presence of

NGOs very different in background and

objectives ranging from the social aspects

of agreements to the conservation or

preservation of the ecosystem.

Yet the ACs have proofed successful and

the Long Distance AC has also risen to

the task. The articulation of the work in

coherent working groups has allowed

to frame the debates and to move

forward the agendas, and by so doing

the initial wariness of the different actors

in composing the Council. As a result,

the LDAC has produced advice on many

thorny issues, and even established some

stable recommendations that have been

issued every year for particular meetings,

such as COFI or NAFO, an advice that

has gained influence as the basis for the

EU’s position at those annual meetings.

Another important aspect of the workings

of the LDAC is the continuous interaction

and collaboration with the officials of the

different institutions, especially the EU’s

Commission, although all the members

would like to see increased participation

form the Members States and the

Parliament, as well as being able to bring

more scientists and have them present

their advice openly in the sessions. More

importantly it would be even more interest

that they participate at the same time at

the meetings, allowing for an even richer

debate and more balanced and informed

decisions.

But the LDAC also has also been

active outside of its EU advisory role,

expanding it to countries partner of the

The LDAC must also use these vehicles to promote exiting EU legislation and practices that have proved to work well in favour of the environment, but also to promote other practices that are just landing on the international agenda and that cannot wait for the usual 10-year process to become standards

THE LDAC,

MORE THAN A CHIMERA

Ivan LopezPRESIDENT OF THE LDAC

Photo: Nor-Fishing

August 2016 - Special Issue Industrias Pesqueras 7

NOR-FISHING 2016Opinion SP

EU in fisheries agreements

such as those forming the

COMAFAT, a large body

including most of the Atlantic

African States. Through

an established and regular

meeting, this states have

been able to present in a less

formal but more effective

manner their problems and

views, while learning from our

experiences to improve their

fisheries legal frameworks

and practices. The success

of this venture will hopefully

soon be continued in the

East and in Asia and Oceania

where similar dialogues are

much needed.

The LDAC must also use

these vehicles to promote

exiting EU legislation and

practices that have proofed

to work well in favour of

the environment, but also

to promote other practices

that are just landing on the

international agenda and

that cannot wait for the usual

10-year process to become

standards. Rather we must

push to ensure that issues

such as labour conditions in

the Fishing industry become

an important paramount of

the industry, just like the

ecological aspects, and

without which access to the

EU markets cannot happen.

It is simply not tolerable to

hear the stories reported from

countries where the fishing

industry is fuelled by modern

slavery and child labour, the

EU must step up its game

and be prompt to forbid those

origins to enter our markets.

We no longer can hide behind

the WTO and its rulings,

neither behind the divisions

and Chinese walls inside the

EU institutions used as an

excuse or lame motive for

inaction. The EU must lead in

this as well, and the LDAC is

the best forum to discuss and

debate possible solutions and

actions as all parties involved

can find there a common

ground. The only certain thing

is that stern and committed

action is needed, because

we cannot preach our many

virtues on the protection of

the ecosystems and stocks to

these countries if we do not

address such a fundamental

breach of human decency

first, we simply would lose all

our legitimacy.

The LDAC has produced advice on many thorny issues, and even established some stable recommendations that have been issued every year for particular meetings, such as COFI or NAFO

8 Special Issue Industrias Pesqueras - August 2016

SPNOR-FISHING 2016Companies

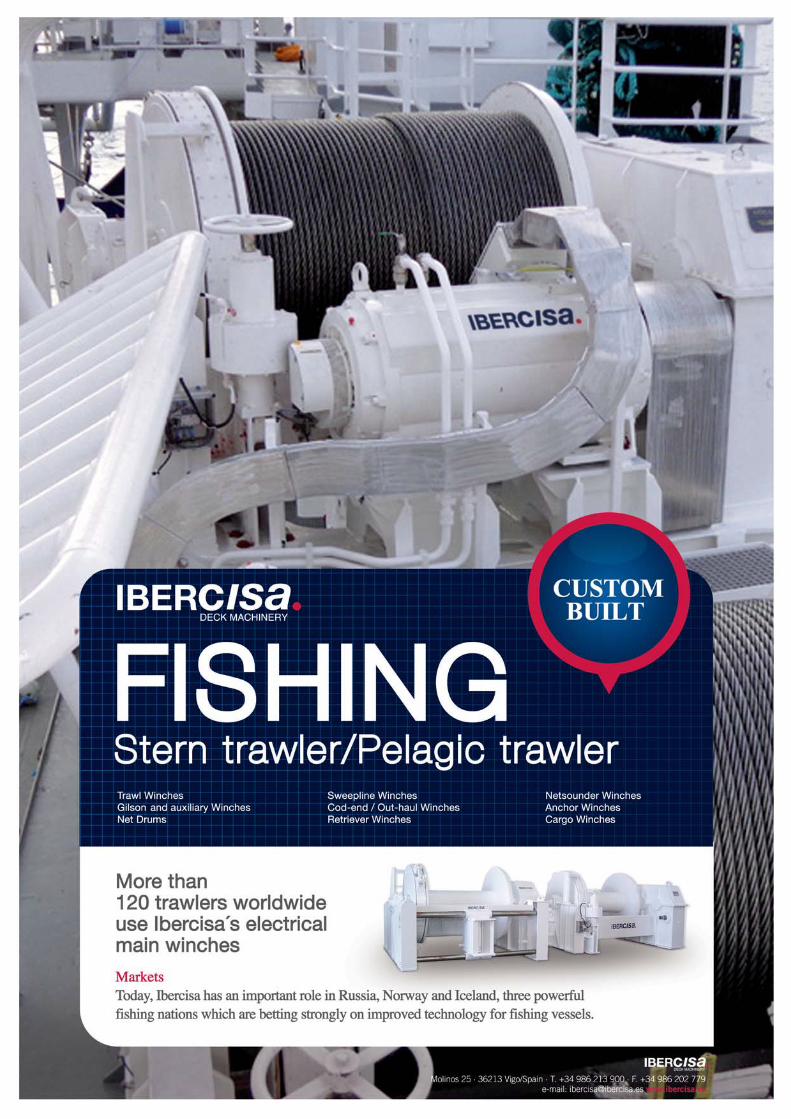

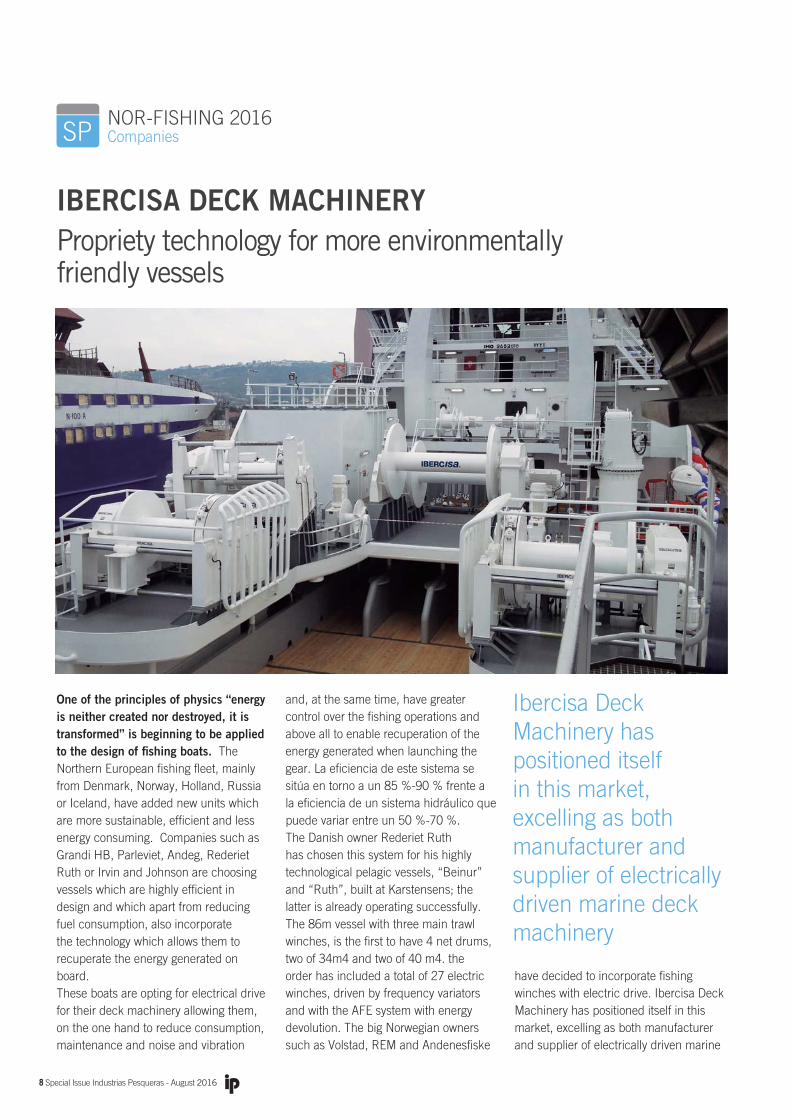

One of the principles of physics “energy

is neither created nor destroyed, it is

transformed” is beginning to be applied

to the design of fishing boats. The

Northern European fishing fleet, mainly

from Denmark, Norway, Holland, Russia

or Iceland, have added new units which

are more sustainable, efficient and less

energy consuming. Companies such as

Grandi HB, Parleviet, Andeg, Rederiet

Ruth or Irvin and Johnson are choosing

vessels which are highly efficient in

design and which apart from reducing

fuel consumption, also incorporate

the technology which allows them to

recuperate the energy generated on

board.

These boats are opting for electrical drive

for their deck machinery allowing them,

on the one hand to reduce consumption,

maintenance and noise and vibration

and, at the same time, have greater

control over the fishing operations and

above all to enable recuperation of the

energy generated when launching the

gear. La eficiencia de este sistema se

sitúa en torno a un 85 %-90 % frente a

la eficiencia de un sistema hidráulico que

puede variar entre un 50 %-70 %.

The Danish owner Rederiet Ruth

has chosen this system for his highly

technological pelagic vessels, “Beinur”

and “Ruth”, built at Karstensens; the

latter is already operating successfully.

The 86m vessel with three main trawl

winches, is the first to have 4 net drums,

two of 34m4 and two of 40 m4. the

order has included a total of 27 electric

winches, driven by frequency variators

and with the AFE system with energy

devolution. The big Norwegian owners

such as Volstad, REM and Andenesfiske

have decided to incorporate fishing

winches with electric drive. Ibercisa Deck

Machinery has positioned itself in this

market, excelling as both manufacturer

and supplier of electrically driven marine

IBERCISA DECK MACHINERY

Propriety technology for more environmentally friendly vessels

Ibercisa Deck Machinery has positioned itself in this market, excelling as both manufacturer and supplier of electrically driven marine deck machinery

August 2016 - Special Issue Industrias Pesqueras 9

10 Special Issue Industrias Pesqueras - August 2016

NOR-FISHING 2016CompaniesSP

company technical office and is

then manufactured in the Vigo

headquarters in conjunction

with the client, studying each

case as it arises and building

the machinery to customers

particular requirements.

The Dutch owner Parleviet, has

equipped two 86m length 16m

width trawlers with winches

driven by an electric motor

of 340 kW with a capacity for

3,300 metres of 32mm diam.

cable and a line pull of 44,9

tons at 39,4 m/min on the first

layer. In Russia the owners

Collective Farm After V.I. Lenina; and

vessel Pechora of Collective Farm Andez.

The efficiency of the equipment has

come from over the Atlantic. In the

United States of America, opting for

this type of technology came originally

from Fishermen`s Finest and in Canada

from Osprey which is building a boat in

Tersan, equipped for fishing shrimp in the

Northern seas but designed to operate

in other fisheries and in which

environmental issues have

been taken into consideration

having been conceived initially

as a “green” boat on which

the priority is waste reduction

and the recuperation and

recycling of excess energy. This

trawler will incorporate four

electric winches model MAI-

E/485/3000-34/IS for tripple

trwaler. The Fishermen's Finest

vessel includes, apart from

control systems, electric split

trawl winches, electric Gilson

winches, electric sweepline

winches, electric net sounder winches,

electric cod end winches, electric net

drums, electric auxiliary anchor winch,

electric mooring winch and electric

auxiliary winches.

SPNOR-FISHING 2016Fisheries in Europe

NORTHEAST ATLANTIC REGION FLEET

Ten Member State fl eets operated in

the region in 2013; the most important

in terms of active vessel number was the

Spanish fl eet.

In terms of production, the UK, French,

Spanish and Irish fl eets were the most

important, collectively responsible for 80%

of the landed weight. In terms of value, the

same fl eets together accounted for 85% of

the value landed in 2013.

Overall, capacity of the NE Atlantic region

fl eet remained stable with reduced effort and

landed weight over the period 2010-2013,

while landed value increased steadily between

2009 and 2012, decreasing in 2013.

The main species landed included the small

pelagics Atlantic mackerel, jack and horse

mackerels, blue whiting and European

pilchard (sardine) and demersal species,

such as European hake and Norway lobster.

Revenue generated by the NE Atlantic

fl eet was Ð2.4 billion, 86% distributed

amongst four MS fl eets: France (Ð681

million), Spain (Ð641 million), UK (Ð438

million) and Portugal (Ð271 million).

GVA produced by the fl eet in 2013 was

estimated at Ð897.6 million and after

accounting for operating costs, the fl eet

made Ð314 million in gross profi t.

The small-scale fl eet generated Ð179 million

in GVA and Ð58 million in gross profi ts. The

large-scale fl eet generated Ð716 million in

GVA and Ð254 million in gross profi t.

Overall the NE Atlantic region fl eet

generated gross profi ts; only the Belgium

fl eet suffered net loss in 2013.

BALTIC SEA FLEET

Eight Member State fl eets operated in the

region in 2013; the most important in terms

of active vessel number was the Finnish

fl eet, followed by Estonia and Germany. The

Finnish fl eet also accounted for the most

effort deployed, followed by the Danish and

German fl eets.

In terms of production, the Finnish, Polish,

Swedish, Danish and Latvian fl eets were the

most important, collectively responsible for

about 85% of the value and weight landed in

2013.

Overall the Baltic Sea fl eet saw declines in

capacity, effort deployed and landings in

weight over the period 2009-2013 while

landed value increased steadily between

2009 and 2013. Herring, sprat and cod

remain the most important species landed.

Revenue generated by the Baltic Sea fl eet

was estimated at around Ð267.5 million,

with the Swedish and Polish fl eets together

contributing 43%. While overall the Baltic

fl eet was profi table (positive gross profi t), two

MSfl eets, Denmark and Germany, reported

gross losses in 2013.

GVA produced by the fl eet in 2013 was

estimatedat Ð121 million (+7%). After

accounting for operating costs, the fl eet made

a gross profi t of Ð40 million (+24%). The

highest GVA were generated by the Swedish

(Ð29 million) and Polish (Ð28 million) Baltic

fl eets followed by the Finnish (Ð17.9 million)

and Danish (Ð16.5 million) fl eets.

MEDITERRANEAN & BLACK SEA FLEET

Eleven Member State fl eets operated

in the region in 2013, with Bulgaria and

Romania fi shing exclusively in the Black

Sea. The analysis is restricted to the

available data by MSfl eets operating in

the region.

The EU fl eet fi shing in the Mediterranean

& Black Sea consisted of 35,497 vessels

(including Greece). Greece comprised the

largest fl eet in number (14,700 vessels)

while the Italian fl eet was the largest in

gross tonnage (143,000 GT).

By fi shing activity, and according to

the available data, the small-scale fl eet

possessed 68% of the fl eet in number

and accounted for 34% of the effort but

landed only 12% in weight ( 22% in

value) and generated 16% of gross profi t

Employment in 2013 was estimated

at 67,800 jobs (excluding Cyprus),

corresponding to 52,900 FTEs. The

small-scale fl eet represents almost

43% of the total employed in the

Mediterranean & Black Sea fl eet

In terms of production, landings

(excluding Greece) amounted to approx.

360,000 tonnes, corresponding to Ð1.3

billion. Italy, Spain, France and Croatia

were the leading countries, collectively.

Statistics

THE SITUATION OF THE EUROPEAN FISHING AREAS AT A GLANCE

12 Special Issue Industrias Pesqueras - August 2016

August 2016 - Special Issue Industrias Pesqueras 13

14 Special Issue Industrias Pesqueras - August 2016

NOR-FISHING 2016CompaniesSP

The Galician Association of Metal

Industries (ASIME) maintains its

commitment to diversification, especially in

the construction of fishing vessels, through

bigger investments in innovation in the

shipbuilding industry. Enrique M. Mallón,

General Secretary and spokesperson

ASIME, states: “We are confident that this

event will help us to promote the Galician

naval and maritime activity and also will

serve as a tool to attract investments

and contracts for shipyards and auxiliary

industry.”

According to the association, Nor-fishing is

an opportunity to expose the news of the

naval industry, which completes the entire

value chain related to shipbuilding and

ship repair industries and shows the most

important technological developments in

the industry.

New technologies 4.0 are creating added

value and increasing safety and efficiency,

so “we consider is essential apply them in

naval activity in order to achieve in this sector

the industry 4.0 standards”. ASIME always

considered essential the empowerment of

ASIME

Promoting diversification in the construction of fishing vessels

Enrique M. Mallón, secretario general y portavoz de Asime

16 Special Issue Industrias Pesqueras - August 2016

NOR-FISHING 2016CompaniesSP

Industry and we must show the Galician

capabilities and the strengths of our naval

and maritime supply chain.

Enrique M. Mallón, remarks: “We are

confident that in the next months the

volume of orders will be increased and we

remain committed, without any doubt, to

the renovation of the Galician and Spanish

fishing fleet in our shipyards.”

“We believe that the Galician shipbuilding

industry could build more than 20 fishing

vessels during the next four years and it

would be desirable that the government

articulate policies and measures

to foster acquisitions for the Galician ship-

owners.” “Our shipbuilding industry is

producing boats with the highest level of

technology and delivering them in countries

of northern Europe such as Norway or

Denmark.”

General Secretary of ASIME: “We are confident that in the next months the volume of orders will be increased and we remain committed, without any doubt, to the renovation of the Galician and Spanish fishing fleet in our shipyards.”

Photo: Nor-Fishing

18 Special Issue Industrias Pesqueras - August 2016

SP

“

How do you feel you were

received by the industry?

Fantastically.When I was

appointed Minister of Fisheries,

some people commented

that I “had to settle for” this

position, that I perhaps had

“higher aspirations”. But they

were completely wrong. As I

see it, this is the most exciting

position in Government. And

think of the potential of this

industry. This is the most

promising and exciting sector

in Norway. Norwegians have a

lot to be proud of in this fi eld.

I believe we have the world’s

best fi sheries management

system, and we are at the

forefront when it comes to

fi sheries and aquaculture

technology.

What do you think about the

Norwegian fi sheries industry

today?

Norway is the second largest

exporter of seafood, and we

are Europe’s largest fi sheries

and aquaculture nation. At

present, everything is growing,

and we could say that the

situation is a bit abnormal: we

have too much market and

too little fi sh. I was recently

in Poland, and down there

they were crying because they

could not get enough fi sh from

Norway for their processing

plants. Although we are on an

upward trend right now, we

should be aware that it might

not last. It is far from certain

that this positive development

will continue into the future.

We should also mention

the development of vessels

and gear technology. In a

way, Norwegian maritime

technology started with fi shing

vessels. The know-how and

technology in this fi eld was

later transferred to shipping,

and then to the offshore oil

sector. And now we see that

suppliers to the offshore

petroleum industry are turning

to fi sheries and aquaculture,

as offshore projects are getting

few and far between. In a way,

the circle is complete.

What special challenges do

you see in the coming years?

What we need to focus on

now is how we can achieve

a better utilization of the raw

material we take out of the

ocean. Globally, perhaps as

much as 30 million tonnes

are lost every year. Processing

waste, heads, intestines, offal

or what we now call “rest

raw material”. Much more of

this can be turned into food

for human consumption. In

addition, there are emerging

industries in chemicals and

cosmetics and other fi elds

Per Sandberg, Minister of Fisheries of Norway

PER SANDBERG IS RELATIVELY NEW IN HIS ROLE AS

MINISTER OF FISHERIES OF NORWAY. HE TOOK OVER ON

DECEMBER 2015, AND IS STILL LEARNING THE ROPES.

PREVIOUSLY HE HAS NOT BEEN ENGAGED IN FISHERIES

MATTERS, BUT HE IS LEARNING FAST. HE IS ALSO KNOWN

AS ONE OF NORWAY’S MOST CONTROVERSIAL AND FREE-

SPOKEN POLITICIANS WITH STRONG OPINIONS ON MOST

MATTERS. WHEN MR. SANDBERG WAS APPOINTED, THERE

WERE MIXED REACTIONS. SOME EXPECTED HE WOULD

TOTALLY SCREW THINGS UP, WHILE OTHERS WERE HAPPY

TO GET A FISHERIES MINISTER WHO WOULD SURELY PUT

THE FISHERIES SECTOR ON THE POLITICAL AGENDA. NOR-

FISHING TEAM INTERVIEWED THE MINISTER BEFORE THE

EVENT. THIS IS A SUMMARY OF THE CONVERSATION.

THE FISHERIES AND AQUACULTURE INDUSTRY IS ONE OF THE SECTORS THAT NORWAY HAS TO DEVELOP FURTHER IN THE FUTURE”

“At present, everything is growing, and we could say that the situation is a bit abnormal: we have too much market and too little fi sh”

NOR-FISHING 2016Interview

Photos: Nor-Fishing

August 2016 - Special Issue Industrias Pesqueras 19

SP

that use fi sh raw material for

their production.

Norway is a small country, it

has to cooperate with other

countries on both resources

and markets. Do you have any

thoughts on that?

Although we are a small

country, in fi sheries and

aquaculture we are big.

It is worth noticing that

Norway participates in a

broad and very fruitful

cooperation within the

fi eld of fi sheries. I would

like to especially point

to our relationship with

Russia. In spite of sanctions

and the fact that

Norwegian

seafood

is now

barred

from

this

market, we have managed

to continue our cooperation

within the management of the

fi sheries in the Arctic. Yes,

there have been some smaller

incidents, but in general

this cooperation continues

sucessfully.

Market access is essential to the Norwegian seafood

industry. What is the current situation?

We are extremely dependent on the EU, because about

two thirds of our seafood is exported to that market. But

the EU is also dependent on us. The EU needs our fi sh for

their processing plants and they need our seafood for their

tables. The EU has a gigantic, - and increasing -, defi cit in

their fi sh trade, and has to import over 11 million tonnes

of seafood every year. While the EU is very important,

we have to develop other markets, too, and I have great

faith in the Norwegian seafood industry’s ability to do so.

Look at what happened when Russia banned Norwegian

seafood. Within a very short time our exporters had found

new markets, and our total exports continued to grow.

But Russia will be back. I have great faith in Russia.

Also, we should not forget countries like Japan and

China. On the Chinese market we have also had

some problems, but I believe these will be sorted

out shortly.

As Minister of Fisheries, how can you help the

industry internationally?

I am doing my best promoting Norwegian seafood

when I am travelling abroad. Some will probably

say that I am more active as an ambassador for

Norwegian seafood than as a Minister of Fisheries.

But I can live with that criticism. There is no reason

why I should not be able to promote Norwegigian

fi sheries technology also and I really look forward to

visiting Nor-Fishing this year.

At present, our country is going through a process

of change. The fi sheries and aquaculture industry

is one of the sectors that we have to develop further

in the future. We have enormous ambitions, also

internationally, and this is one of the reasons I am

looking forward to mingling with the elite of the

industry in Trondheim in August. I believe we have

a lot to offer to other countries in this fi eld. Many

could learn important lessons from Norwegian

fi sheries management, for example.

“We have to develop other markets, too, and I have great faith in the Norwegian seafood industry’s ability to do so”

NOR-FISHING 2016Interview

SPNOR-FISHING 2016

Interview

THE MAIN CHALLENGE OF THE SECTOR NOW IS TO TRY AND STAY VIABLE IN A COMPETITIVE MARKET”

“

From the point of view of the european

sector, Can you make an overview of the

opportunities and challenges of European

industry. What´s our current situation?

As a general overview, the European

fi shing sector has faced some tough

times over the last few years, in fact, it

seems we faced more challenges than

we had opportunities. The new changes

in the CFP have provided quite radical

legislation in the form of the deep-sea

ban, shark-fi nning ban, driftnet ban

and the discard ban and has brought a

lot of instability to the sector. The main

challenge of the sector now is to try and

stay viable in a competitive market. The

main challenge of Europêche is to try

and ensure that the rules are not only

workable for the sector but are justifi ed.

Rules for rules sake help no one. In this

way, a huge opportunity for us to change

the way the rules apply is the Technical

Measures Regulation which is currently

being debated in the EU institutions.

Since the current Technical Measures

Regulation has been in place, there

have been two unsuccessful attempts to

revise it. Now we have a real chance to

devolve a lot of the decision-making to a

regional level, more tailor-made to each

sea basin.

Regarding individual countries, which

fl eets are emerging and which would

need a greater boost. Is traditional north-

south imbalance remain?

The North East Atlantic is a real success

story; we now have 36 stocks being fi shed at

MSY compared to 27 two years ago and

just two in 2003. In fact, the number of

stocks within safe biological limits has

almost doubled in the last decade.

But it is also important that we

prioritise the Mediterranean which

represents about 1.6% of global

catches. It is important that the

sector are also more proactive in this

development since it would serve as

an example to neighbouring non-

EU countries. One major obstacle

however is that very little data exists

on the Mediterranean leading to gaps

in knowledge. Member States and the

Commission need to invest more in

research and support

scientists to better

identify the

problem

areas and

produce

tailor-

made

solutions. Yet, the Mediterranean has also

had its share of success with the spectacular

recovery of bluefi n tuna, whose quota has

been increased by 20% every year. This

goes to show that the right measures,

coupled with a strong commitment from

the industry, will certainly lead to abundant

waters and sustainable fi shing communities.

Within Europêche, I don’t believe there is a

real north-south divide, since we represent a

united industry, affected by the same rules

and regulations; we have been defending

the interests of the sector as a whole since

1969.

Kathryn Stack, managing director of Europêche

KATHRYN STACK, A FORMER SENIOR POLICY ADVISER ON FISHERIES POLICY IN

THE EUROPEAN PARLIAMENT, IS THE MANAGING DIRECTOR OF EUROPÊCHE

SINCE LAST YEAR. THE MAIN FISHING BODY IN EUROPE REPRESENTS 80,000

FISHERMEN AND 45,000 VESSELS WITHIN THE EU FLEET. EUROPÊCHE HAS

12 MEMBER ORGANISATIONS ACROSS NINE COUNTRIES, INJECTING Ð41.3BN

INTO THE EUROPEAN ECONOMY. STACK HAS A MASTER’S DEGREE, ON

INTERNATIONAL POLITICS AT UNIVERSITÉ LIBRE DE BRUXELLES. LOOKING

FORWARD TO KNOW THE OPINION OF THE FISHERIES SECTOR IN EUROPE, DUE

THE CELEBRATION OF NOR-FISHING, WE TALKED WITH HER ABOUT THE FUTURE

OF THE FLEET; THE IMPLEMENTATION OF THE CPF; THE DISCARD BAN AND THE

REST OF CHALLENGES FACING THE INDUSTRY NOWADAYS.

August 2016 - Special Issue Industrias Pesqueras 21

22 Special Issue Industrias Pesqueras - August 2016

SPNOR-FISHING 2016Interview

One of the main challenges of the industry

is the renewal if the fleet, the search

for efficiency,etc. Would you say that

Europe is moving in this direction or it is

necessary to increase efforts?

Fishermen are the first to want to develop

the fleet and invest in technology and new

gears to adapt to the new CFP but this

often requires a heavy financial investment

considering that 50% of EU fleet is over 25

years old. European funding for fleet renewal

focuses on safety and health equipment on

board, selectivity, energy efficiency, catch

quality and the discard ban. However, the

actual modernisation of the vessel is subject

to too strong conditionality (for example,

engine replacement). We believe that this

should be allowed if it does not increase the

fishing capacity of the vessel and aims at

reducing energy consumption.

How are european states responding to

the implementation of the CFP?

The CFP has brought some radical

changes to the way the sector operate

their fisheries. All stocks must reach

MSY levels in the next four years. A

serious problem facing some of our

members now is the Western Baltic

cod quota which ICES recommend

applying the MSY approach and cutting

the quota by a whopping -93%. There

is also a 6 week closure in this area

during the optimum fishing time which

only serves to displace effort from a

good period with abundant stocks

to vulnerable areas. These kind of

measures will annihilate the local fishing

communities in this area. Not only are

the fishermen dependent on fishing

for their livelihoods but also for the

“The new changes in the CFP have provided quite radical legislation in the form of the deep-sea ban, shark-finning ban, driftnet ban and the discard ban and has brought a lot of instability to the sector”

August 2016 - Special Issue Industrias Pesqueras 23

other services (processors,

handlers, ice suppliers etc)

who depend on the catch.

Once these industries go

bankrupt, they won’t come

back again. The socio-

economic impact of fisheries

must always be borne in

mind when allocating fishing

opportunities.

The transparency policy is

currently one of the strategies

of the sector. There is

unanimity? What is being

done? How can we bring this

message to consumers?

The European fishing fleet is one

of the most strictly monitored

and controlled in the world.

We have strict labelling and

IUU rules and are committed

to more transparency in the

global supply chain. As a result,

transparency in EU products is

of the highest level. Problems

arise with illegal products from

third countries which may enter

the EU which compete at a

lower cost with our EU products.

This creates an unfair systems

since our operators have stuck

to the rules and have much

higher working costs. Our

industry has made great efforts

and has committed significant

investment to equip itself with

the systems and tools necessary

to ensure compliance with

both European legislation and

standards agreed internationally.

It is essential that the same

requirements apply to fleets of

third countries who may not

follow the stringent measures

applicable to the EU fleet.

And, to finish, EU recently

published a report on the

need to harmonize the

European market for eco-

labels. Any thoughts on that?

It is difficult to answer fully

since we are a European

umbrella organisation and

some of our members are

certified and some aren’t so

we cannot speak for everyone.

Regarding the drivers of eco-

labels; it is difficult to pin-point

one driver. NGOs pressure

retailers to make sure their

seafood is sustainably sourced

and consumers demand this

from the retailers. From our

perspective, a price premium

and improved reputation is of

great benefit from these sorts

of schemes but some in the

industry feel resentful for having

to pay a private third party to

confirm that they are indeed

complying with the rules of

the Common Fisheries Policy.

In this way, there should be

standard measures laid down

by the Commission to ensure

that ecolabels do not mislead

consumers and that there are

no rogue labels (i.e. ‘dolphin

friendly’ may not mean ‘turtle

friendly’ etc).

“Transparency in EU products is of the highest level”

NOR-FISHING 2016Interview SP

24 Special Issue Industrias Pesqueras - August 2016

SPNOR-FISHING 2016Interview

Next year the last phase of the

implementation of the rule of

discard will come into force.

How is the sector facing this

new standard?

The discard ban has been

more of a trial and error

exercise with many in the

industry nervous about the

economic impact of choke

species. Choke species are

species for which the quota

has been reached thus preventing the

vessel from returning to sea, effectively

‘choking’ the fishery. The expected

outcome of a choke situation is the

bankruptcy of the fishing operations

concerned. Europêche organised a

hearing on this issue in the European

Parliament recently inviting scientists and

economists from across Europe to analyse

the economic impact of the landing

obligation. One expert stated that if all

assumptions come true, by 2019 the UK

whitefish fleet would be receiving just 28%

of the revenue they achieved in 2013.

The situation is even worse for the UK

nephrops fleet, which, in the worst-case

scenario, would receive just

5% of 2013 revenue. We have

a situation where the quota

allocation fails to deal with the

complexity of mixed fisheries.

Fish will remain uncaught,

reducing food supply and

vessels will either be tied up or

have already gone bankrupt.

This is a serious situation;

the flexibilities can of course

alleviate in the short term and

the fleet can try to moderate the effects

with selectivity trials but inevitably some of

the effects will always remain. Something

has to change to allow these fleets to

continue fishing. A good starting point

would be realistic uplifts in quota coupled

with close monitoring and frequent choke

analyses.

August 2016 - Special Issue Industrias Pesqueras 25

26 Special Issue Industrias Pesqueras - August 2016

NOR-FISHING 2016CompaniesSP

Vanguard Marine has developed the

design of the SOLAS 420 RB (Rescue

Boat) focusing on safety and performance

standards, combining them with the needs

of a compact size boat. The result is a strong

RIB with a low fuel consumption, lightweight

and maximized space. Rescue Boat

purposes can be combined with a wide range

of everyday tasks such as transferring crew

and equipment, carrying out inspections, and

many other auxiliary tasks.

The safety equipment fulfi lls the SOLAS

requirements including among other items a

manual searchlight 12V 30W, battery 12V 19

Ah, battery charger and

a 45 liter anti-spill tank that allows a 25 Hp or

40 Hp overboard engine providing responsive

handling and easy steering.

The V-hull, has been manufactured from

four-millimeter thick marine grade aluminum

which is easy to repair and 100% recyclable,

once

built it

is fi lled with

closed cell foam making

it unsinkable. The hull features a tube with

fi ve independent air compartments with

safety release valves to automatically release

excess pressure as well as all other safety

equipment required by SOLAS regulations.

The infl atable tube is constructed from high

abrasion and weather protection resistance

Polyurethane, manufactured using

VANGUARD MARINE

Safety and effi ciency in compact size rescue boats

August 2016 - Special Issue Industrias Pesqueras 27

NOR-FISHING 2016Companies SP

mechanical and robotic systems, together

with Thermosealing® technology, that

creates a double seal that is stronger than

the original material.

The SOLAS 420 RB has been designed,

built and tested following strict criteria,

backed with a rigorous quality control, it

is MED certified, modules B and D, by

LR according to the Marine Equipment

Directive MED 96/98/EC and International

Convention for Safety of Life at Sea SOLAS

74 amendments and IMO LSA code

resolution MSC 48(66) chapter V MSC/

Circ.980 amendments.

The result is a strong RIB with a low fuel consumption, lightweight and maximized space

28 Special Issue Industrias Pesqueras - August 2016

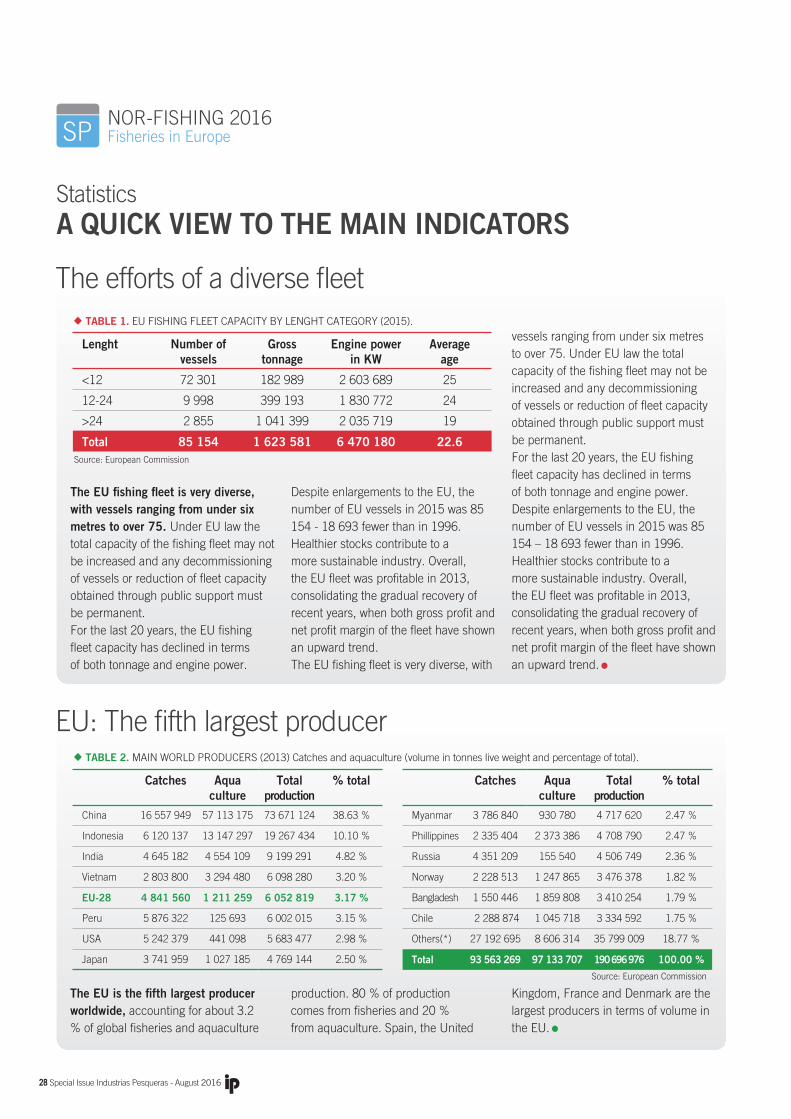

SPNOR-FISHING 2016Fisheries in Europe

The EU fi shing fl eet is very diverse,

with vessels ranging from under six

metres to over 75. Under EU law the

total capacity of the fi shing fl eet may not

be increased and any decommissioning

of vessels or reduction of fl eet capacity

obtained through public support must

be permanent.

For the last 20 years, the EU fi shing

fl eet capacity has declined in terms

of both tonnage and engine power.

Despite enlargements to the EU, the

number of EU vessels in 2015 was 85

154 - 18 693 fewer than in 1996.

Healthier stocks contribute to a

more sustainable industry. Overall,

the EU fl eet was profi table in 2013,

consolidating the gradual recovery of

recent years, when both gross profi t and

net profi t margin of the fl eet have shown

an upward trend.

The EU fi shing fl eet is very diverse, with

vessels ranging from under six metres

to over 75. Under EU law the total

capacity of the fi shing fl eet may not be

increased and any decommissioning

of vessels or reduction of fl eet capacity

obtained through public support must

be permanent.

For the last 20 years, the EU fi shing

fl eet capacity has declined in terms

of both tonnage and engine power.

Despite enlargements to the EU, the

number of EU vessels in 2015 was 85

154 – 18 693 fewer than in 1996.

Healthier stocks contribute to a

more sustainable industry. Overall,

the EU fl eet was profi table in 2013,

consolidating the gradual recovery of

recent years, when both gross profi t and

net profi t margin of the fl eet have shown

an upward trend.

The EU is the fi fth largest producer

worldwide, accounting for about 3.2

% of global fi sheries and aquaculture

production. 80 % of production

comes from fi sheries and 20 %

from aquaculture. Spain, the United

Kingdom, France and Denmark are the

largest producers in terms of volume in

the EU.

Statistics

A QUICK VIEW TO THE MAIN INDICATORS

The efforts of a diverse fl eet

EU: The fi fth largest producer

TABLE 1. EU FISHING FLEET CAPACITY BY LENGHT CATEGORY (2015).

TABLE 2. MAIN WORLD PRODUCERS (2013) Catches and aquaculture (volume in tonnes live weight and percentage of total).

Lenght Number of vessels

Gross tonnage

Engine power in KW

Averageage

<12 72 301 182 989 2 603 689 25

12-24 9 998 399 193 1 830 772 24

>24 2 855 1 041 399 2 035 719 19

Total 85 154 1 623 581 6 470 180 22.6

Catches Aquaculture

Total production

% total

China 16 557 949 57 113 175 73 671 124 38.63 %

Indonesia 6 120 137 13 147 297 19 267 434 10.10 %

India 4 645 182 4 554 109 9 199 291 4.82 %

Vietnam 2 803 800 3 294 480 6 098 280 3.20 %

EU-28 4 841 560 1 211 259 6 052 819 3.17 %

Peru 5 876 322 125 693 6 002 015 3.15 %

USA 5 242 379 441 098 5 683 477 2.98 %

Japan 3 741 959 1 027 185 4 769 144 2.50 %

Catches Aquaculture

Total production

% total

Myanmar 3 786 840 930 780 4 717 620 2.47 %

Phillippines 2 335 404 2 373 386 4 708 790 2.47 %

Russia 4 351 209 155 540 4 506 749 2.36 %

Norway 2 228 513 1 247 865 3 476 378 1.82 %

Bangladesh 1 550 446 1 859 808 3 410 254 1.79 %

Chile 2 288 874 1 045 718 3 334 592 1.75 %

Others(*) 27 192 695 8 606 314 35 799 009 18.77 %

Total 93 563 269 97 133 707 190 696 976 100.00 %

Source: European Commission

Source: European Commission

August 2016 - Special Issue Industrias Pesqueras 29

NOR-FISHING 2016Companies SP

30 Special Issue Industrias Pesqueras - August 2016

SPNOR-FISHING 2016Fisheries in Europe

Herring and mackerel The market

Atlantic, North-East 3 600 950 74.4 %

Mediterranean 413 841 8.5 %

Atlantic, Eastern Central 379 677 7.8 %

Indian Ocean, West 187 815 3.9 %

Atlantic, South-West 125 491 2.6 %

Atlantic, North-West 65 196 1.3 %

Atlantic, South-East 44 869 0.9 %

Inland waters 12 569 0.3 %

Black Sea 11 152 0.2 %

Total 4 841 560 100.00 %

Herring 716 043 14.8 %

Mackerel 450 246 9.3 %

Sprat 337 676 7.0 %

Sardine 243 376 5.0 %

Horse mackerel 190 193 3.9 %

Skipjack tuna 163 134 3.4 %

Hake 154 703 3.2 %

Cod 142 229 2.9 %

Small pelagics 132 144 2.7 %

Yellowfi n tuna 128 127 2.6 %

Blue whiting 122 378 2.5 %

Sharks 112 350 2.3 %

Plaice 95 231 2.0 %

Anchovy 90 567 1.9 %

Scallop 80 458 1.7 %

TABLE 3A. TOTAL EU CATCHES IN FISHING AREAS (2013)(volume in tonnes live weight and percentage of total).

TABLE 3B. TOP 15 SPECIES CAUGHT BY THE EU (2013)(volume in tonnes live weight and percentage of total).

The leading fi shing countries

in terms of volume are

Spain, Denmark, the United

Kingdom and France, which

combined, account for more

than half of EU catches.

Catches add up to around

80 % of the total volume

of the EU production.

Although the European fl eet

operates worldwide, EU

catches are taken primarily

in the North-East Atlantic,

in the Mediterranean and in

the Eastern Central Atlantic,

and the species most fi shed

are herring and mackerel.

TABLE 4. TRADE OF FISHERIES AND AQUACULTURE PRODUCTSBETWEEN THE EU AND THIRD COUNTRIES (2014)(volume in tonnes and value in thousands of EUR).

TABLE 4A. IMPORT OF FISHERIES AND AQUACULTURE PRODUCTS BY MAIN PRESERVATION CATEGORIES- EXTRA EU-TRADE (2014)(Percentage of total).

TABLE 4B. EXPORT OF FISHERIES AND AQUACULTURE PRODUCTS BY MAIN PRESERVATION CATEGORIES- EXTRA EU-TRADE (2014)(Percentage of total).

Imports Exports

tonnes value tonnes value

Pelagic fi sh 1 057 615 3 226 300 1 118 369 1 372 097

Salmonids 837 320 4 429 927 117 676 702 642

Other fi sh 1 881 271 5 917 574 405 804 1 191 656

Crustaceans 621 184 4 474 711 66 816 311 198

Mollusc 614 215 1 997 959 46 291 225 477

Non-foods use products

936 103 914 014 390 213 518 314

Total EU-28 5 947 708 20 960 485 2 145 169 4 321 384

The EU is the leading trader

of fi sheries and aquaculture

products in the world in terms

of value. EU trade (imports and

exports) has increased over the

past few years, reaching EUR

45.9 billion in 2014. Norway,

China, Ecuador and Morocco

are the EU’s main suppliers,

while the United States,

Norway, Switzerland and China

are the EU’s main customers.

24%

47%

3%

20%

5%

21%

45%

4%

17%

13%

Source: European Commission Source: European Commission

Source: European Commission

Source: European Commission

Source: European Commission

NOR-FISHING 2016CompaniesSP

RE-BRANDING OF WILD SEAFOOD IS WHERE THE FUTURE GROWTH POTENTIAL OF THE INDUSTRY IS THE STRONGEST”

“

Rabobank is a European fi nancial

institution geared to primary industry. But

lower production, higher demand, more

and more imports characterizes our

markets. Is food production in Europe

still feasible?

Rabobank is a fi nancial institution

that focuses on the Food and Agri

sector in the broad context, not

just primary production, but the

entire value chain from seed to

dinner table, or as we say in seafood

from net to plate. This incorporates

technology companies such as

suppliers of vaccines and genetics up

to retailers and food service companies.

Indeed there is more imports, but there

are also more exports as the global

economy becomes increasingly

connected. Food production is

most defi nitely possible in

Europe. In fact while in

Europe there may not be

a considerable upside in the volume of

food we consume but people in Europe

are increasingly focused on heathier and

more convenient food which drives value

of food consumption. Other value drivers

are the growing demand for biological/

organic foods, demand for artisanal/local

products and growth of certain premium

categories.

What are the major funding needs in

the fi sheries sector? Where is the growth

potential for our industry and where

should efforts be directed?

Speaking about the funding needs of

the industrial fi shing sector, these are

two fold: fl eet renewal, replacing old

vessels with new more modern vessels

and acquisitions for the consolidation of

the sector. The global fi shing industry is

consolidating and most leading players

are actively looking to acquire smaller

players, vessels or quotas to achieve

a number of strategic goals. Both of

these two drivers can create effi ciencies

and synergies. And create growth for

the industry. Although not specially a

funding requirement as the other two,

marketing and market development is an

ongoing effort of all fi shing and seafood

companies. In our view, re-branding

of wild seafood and creating premium

products that justify the uniqueness and

healthiness of this protein is where the

future growth potential of the industry is

the strongest.

Regarding the renewal of the fl eet? Is

Rabobank acting in this fi eld?

Rabobank is a fi nancier of a number of

leading fi shing companies globally and

naturally some of the capital has been

Gorjan Nikolik, Associate Director Animal Protein of the Rabobank International

RABOBANK IS A NETHERLANDS BASED, INTERNATIONAL FINANCIAL SERVICES

PROVIDER OPERATING ON THE BASIS OF COOPERATIVE PRINCIPLES. IT OFFERS

RETAIL BANKING, WHOLESALE BANKING, PRIVATE BANKING, LEASING AND REAL

ESTATE SERVICES FOCUSING ON THE FOOD FIELD, INCLUDING THE FISHERIES

SECTOR. “RABOBANK IS COMMITTED TO BEING A LEADING CUSTOMER-FOCUSED

COOPERATIVE BANK IN THE NETHERLANDS AND A LEADING FOOD AND AGRI

BANK WORLDWIDE WITH ASSETS TOTALING AT 670 BILLION EURO”, SAID. THE

ORGANIZATION HAS APPROXIMATELY 52,000 EMPLOYEES WORLDWIDE AND

OPERATES IN 40 COUNTRIES. ITS INTERNATIONAL ACTIVITIES ARE AIMED AT

INCREASING THE AVAILABILITY OF FOOD, IMPROVING THE ACCESS TO FOOD,

PROMOTING HEALTHY NUTRITION AND ENHANCING THE STABILITY OF THE

FOOD INDUSTRY THROUGH ITS INTERNATIONAL ACTIVITIES. WE TALKED WITH

GORJAN NIKOLIK, ASSOCIATE DIRECTOR ANIMAL PROTEIN OF THE RABOBANK

INTERNATIONAL FOOD & AGRIBUSINESS RESEARCH AND ADVISORY, ABOUT THE

FUTURE OF THE PRIMERY INDUSTRY EN EUROPE AND THE ACTIVITY OF THE

BANK IN FISHERIES SECTOR.

32 Special Issue Industrias Pesqueras - August 2016

August 2016 - Special Issue Industrias Pesqueras 33

SPNOR-FISHING 2016Companies

34 Special Issue Industrias Pesqueras - August 2016

used for fleet renewal. We do not have

any specific financial products targeting

fleet renewal.

All analysts agree that aquaculture will

be key in the future, but when will the

aquaculture industry finally take off?

Aquaculture is taking off globally but in

not equally in all regions. Some countries

due to a combination of natural resources,

human resources, supportive legislation/

government and capital availability

have created successful aquaculture

hubs which have become major global

exporters. Globally China, India, Thailand,

Indonesia, Ecuador and Chile are good

examples. In Europe, Norway is the

leading aquaculture hub with a world

leading salmon industry. Scotland, Greece

and Faroe Islands, although on a smaller

scale also have successful aquaculture

industries which are major exporters

and contributors to the local economy.

Although Spain has a very significant

and growing aquaculture industry, in fact

largest in volume terms in the EU, it is not

concentrated on one species and not as

export focused on the others. It is also not

as important relatively speaking to the local

economy as the others, also in part due to

the much larger Spanish economy.

What are the criteria of Rabobank to

support a project?

Depending on the region Rabobank could

provide financing and financial services

to companies of different sizes. In all EU

countries we operate at the wholesale/

corporate banking level, this means that

the minimum company size is EUR 100

million sales or EUR 10 million EBITDA,

but this is rough estimate. There are also

other considerations including leverage and

sustainability considerations. In some select

regions Rabobank operates with a “Rural

banking model”. In these regions, such

as Brazil, Chile, parts of the US, Australia

and New Zeeland, Rabobank also provides

financial services also to small rural

enterprises, such as famers and small food

producers, above a certain size.

How are sustainability issues integrated

into Rabobank decisions? Do these

aspects inevitably affect corporate

profitability?

Sustainability is a very important aspect

of every commercial engagement.

Rabobank does not provide services to

companies engaged in unsustainable

practices. In the seafood industry we

have a separate policy on this for both

wild catch and aquaculture, both can be

found on our web site.

Let’s talk about supply channels. How are

the supply channels changing due to the

evolution of the logistics industry and the

Internet?

Logistics are a key enabling factor

for growthseafood consumption and

demand. This is especially relevant in

developing countries. The huge increase

in seafood consumption in Asia is at

least in part due to the advances in cool

chain logistics. This trend is continuing

and enabling a large increase in the

value of seafood consumption as well

as global trade (which in turn increases

diversity and availability). Especially the

development of pre-packaged fresh

seafood at retail level has been a major

value driver globally, as well as Spain.

“Rabobank does not provide services to companies engaged in unsustainable practices. In the seafood industry we have a separate policy on this for both wild catch and aquaculture”

Photos: Nor-Fishing

36 Industrias Pesqueras - June 2015

JANUARY Special issue on: Fishing Gears

FEBRUARY Special issue on: Electronic Equipments

MARCH Special issue on: Safety and Rescue Operations

APRIL “The fishing industry on the international stage”

MAY Preview: Navalia 2016

JUNE Special issue on: Fisheries Technology

JULY Special issue on: Engines and Propulsion/ Fuels and Lubricants

AUGUST Special issue on: Transport and Logistics

SEPTEMBER Special issue on: Longline Fleet

OCTOBER Preview: Conxemar 2016

NOVEMBER Special issue on: Tropical Tuna Fleet

DECEMBER Special issue on: Cold Storage Facilities and Industrial Cold

SPECIALS ISSUES AND PREVIEWS 2016

AISTER 10

ASIME 26

ARMON SHIPYARD Contraportada

BAITRA 25

CARDAMA SHIPYARD 13

EGALSA 20

EURORED 29

FAUSTINO CARCELLER 7

FOLCH ROPES 24

FREIRE SHIPYARD 17

IBERCISA DECK MACHINERY Portada Interior

INDUSTRIAS FERRI 33

MARINE INSTRUMENTS 11

METALSHIPS & DOCKS 27

MORENOT 9

MORGERE 29

MURUETA SHIPYARD 31

NEUWALME 14

NODOSA SHIPYARD 22

OBEKI 33

OLEX 5

PANELFA 35

PIPEWORKS 25

PROGENER 13

REGENASA 35

ROTOGAL Contraportada Interior

SANTYMAR 9

SCHOTTEL 2

VANGUARD MARINE 15

VICUS 16

VOLVO PENTA 23

VULKAN COUPLINGS 4

SUMMARY OF PUBLICITY